UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number (811-22335)

Evermore Funds Trust

(Exact name of registrant as specified in charter)

89 Summit Avenue

Summit, New Jersey 07901

(Address of principal executive offices) (Zip code)

Eric LeGoff

89 Summit Ave, 3rd Floor

Summit, New Jersey 07901

(Name and address of agent for service)

(866) 383-7667

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2014

Item 1. Reports to Stockholders.

| Annual Report | |||||

| December 31, 2014 | |||||

| Evermore Global Value Fund |

Table of Contents

| Shareholder Letter & Management Discussion | |||

| of Fund Performance | 1 | ||

| Sector Allocation | 14 | ||

| Expense Example | 15 | ||

| Performance Information | 17 | ||

| Schedule of Investments | 18 | ||

| Statement of Assets and Liabilities | 22 | ||

| Statement of Operations | 25 | ||

| Statement of Changes in Net Assets | 26 | ||

| Financial Highlights | 28 | ||

| Notes to Financial Statements | 32 | ||

| Report of Independent Registered Public Accounting Firm | 47 | ||

| Approval of Investment Advisory Agreement | 48 | ||

| Trustees and Officers | 50 | ||

| Additional Information | 53 | ||

| Privacy Notice | 55 | ||

Evermore Global Value Fund

Elements of Our Investment Approach

At Evermore Global Advisors, we seek to leverage our deep operating and investing experience and extensive global relationships to identify and invest in special situations – companies around the world that have compelling valuations and are undergoing strategic changes which we believe will unlock value.

Seeking to Generate Value . . .

| • | Catalyst-Driven Investing. We do more than pick undervalued stocks and hope for their prices to rise. We invest in companies where we’ve determined a series of catalysts exist to unlock value. The catalysts we look for are not broadly recognized, but they are likely to have a significant impact on a stock’s performance over time. Examples of catalysts include management changes, financial and operational restructurings, spin-offs, breakups, mergers, acquisitions, etc. |

Supporting Our Active Value Orientation . . .

| • | Original Fact-Based Research. We do not rely on brokerage reports to research companies. We conduct our own, original fact-based research to validate management’s stated objectives and identify catalysts to unlock value. We also perform detailed business segment analysis on each company we research. |

| • | Business Operating Experience. Our senior team has hands-on business operating experience; including starting and managing businesses, sitting on company boards, and assisting management of multi-national corporations restructure their businesses. We rely on this experience to better evaluate investment opportunities. |

| • | A Global Network of Strategic Relationships. Over the past 20 years, our investment team has developed an extensive global network of strategic relationships, including individuals and families that control businesses, corporate board members, corporate management, regional brokerage firms, press contacts, etc. We leverage these relationships to help generate and better evaluate investment opportunities. |

| • | Taking a Private Equity Approach to Public Equity Investing. When we are interested in an investment opportunity, we get to know the management team of the company, study the company’s business model, evaluate the competitive and regulatory environment, and test and crosscheck everything the management team tells us against our own experience. |

| • | Always Active, Sometimes Activist. We are always engaged with the companies in which we invest to ensure management teams follow through on their commitments to change. On limited occasions, when we are not satisfied with the efforts of management, we may play an activist role working with other shareholders to facilitate change. |

1

Evermore Global Value Fund

Executing Our Approach . . .

| • | Targeting Complex Investment Opportunities. We love looking at holding companies and conglomerates that are often under-researched and/or misunderstood. |

| • | Investing Across the Capital Structure. We evaluate all parts of a company’s capital structure to determine where the best risk-adjusted return potential exists. At times, we may invest in multiple parts of a company’s capital structure (e.g., investing in both a company’s debt and equity). |

| • | Merger Arbitrage and Distressed Companies. We look to take advantage of announced merger and acquisition deals where an attractive spread exists between the market price and the announced deal price for the target company. We also look for opportunities in distressed companies that have filed or may file for bankruptcy, or are involved in reorganizations or financial restructurings. |

| • | Exploiting Short Selling Opportunities. We will seek to take advantage of short selling opportunities to address currency, security, sector and market risk. |

| • | Tactically Managing Cash Levels. We are not afraid to hold significant cash positions when it makes sense for the portfolios. |

2

Evermore Global Value Fund

A Letter from the CEO

Eric LeGoff

CEO, Evermore Funds Trust

Dear Shareholder,

The Evermore Global Value Fund (the “Fund”) had a difficult year from an investment performance standpoint, as geopolitical, macroeconomic and pandemic events, including the Ukrainian-Russia crisis, slowing European Gross Domestic Product (“GDP”) growth, EBOLA fears, and declining oil prices, adversely impacted a number of our special situations investments. On a positive note, Fund assets again grew substantially last year, increasing by about 52% to $235.5 million, and bringing assets of Evermore Global Advisors, the Fund’s investment adviser, to about $358 million at year-end 2014. This growth is a testament to the hard work of our entire organization.

We approach 2015 with measured optimism, as we see a market environment that offers its own set of catalysts that we believe will help create value across our holdings. For example, low oil prices will help our industrial companies lower their operating expenses; a declining Euro will help our European companies that are major exporters compete more effectively in the global marketplace; and we believe the European Central Bank’s (“ECB’s”) recent announcement of a gargantuan $1.3 trillion quantitative easing program could have the same positive dramatic effects on European companies and their stock prices as it had in the U.S. Beyond the macroeconomic environment in Europe, we see continued growth in merger and acquisition, spin-off and activist activity across the region, which should provide us with many interesting opportunities on which to focus.

In the spring of 2014, Evermore welcomed Matthew Epstein to its investment team as a senior research analyst. Matt previously worked for a large, New Jersey based asset management firm where he gained many years of special situations and private equity investing experience. Matt has quickly become a contributing member of the team.

David Marcus and I continue to be extremely appreciative of the efforts of our employees, Board of Trustees, advisors, and service providers. I would like to thank the following service providers for their support over the past year: U.S. Bancorp Fund Services, LLC (Fund administrator, accountant, transfer agent); U.S. Bank N.A. (Fund custodian); Quasar Distributors LLC (Fund distributor); Drinker Biddle & Reath LLP (Fund counsel); John Canning of Cipperman Compliance Services, LLC (Chief Compliance Officer and compliance services provider); Gary M. Gardner (counsel to the Fund’s independent trustees); Ernst & Young (Fund auditor); Olmec Systems, Inc. (technology support provider); Tiller, LLC (marketing communications provider); JCPR, Inc. (public relations and marketing provider); Eze Castle Software

3

(order management system provider); Advent Software (portfolio management software provider); and Bloomberg (market data provider).

And finally, the entire Evermore team would like to thank you, our shareholders, for the continued support and confidence you have shown us. We wish you all the best for a happy, healthy and prosperous 2015.

Sincerely,

Eric LeGoff

CEO, Evermore Funds Trust

4

Evermore Global Value Fund

A Letter from the Portfolio Manager

David Marcus

Portfolio Manager

“Long ago, Ben Graham taught me that ‘Price is what you pay; value is what you get.’ Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.” – Warren Buffett

Dear Shareholder,

For the year ended December 31, 2014, Class I shares of the Evermore Global Value Fund (the “Fund”) were down 6.58% while the MSCI All Country World Index (“MSCI ACWI”) was up 4.16%, and the HFRX Event Driven Index (“HFRX ED”) was down 4.06%.

Year-end 2014 marked the five year anniversary of the Fund and a period over which international, and especially European, markets were marked by varying levels of crisis and significant volatility. European value and event driven special situations have struggled to gain a strong footing. U.S. markets, conversely, showed reasonably steady gains over the period. The fact that the Fund’s portfolio has been heavily concentrated in European investments over this time has certainly had an adverse impact on the Fund’s investment performance. Here is a review of the Fund’s performance versus our benchmarks:

Average Annual Total Returns as of December 31, 2014

| Since | ||||

| Inception | ||||

| 1 Year | 3 Year | 5 Year | 1/1/10 | |

| Fund (EVGIX) | -6.58% | 11.57% | 3.21% | 3.21% |

| MSCI ACWI | 4.16% | 14.10% | 9.20% | 9.20% |

| HFRX ED | -4.06% | 5.00% | 2.30% | 2.30% |

The performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance data current to the most recent month end may be obtained by calling 866-EVERMORE or (866-383-7667). The Fund imposes a 2% redemption fee on shares held for 30 days or less. Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced. The Fund’s gross expense ratio is 1.59%.

5

2014 was a disappointing follow-up to what was a very good 2013. The year started off fine with a continuation of the same positive situations that we had seen in 2013 – an acceleration in restructurings, refocusing by companies, breakups, spinoffs, management changes, and an increase in merger and acquisition (“M&A”) activity. There was optimism and a cautious sense of recovery. The view was that Europe, having come out of recession in 2013, would see a major pick-up in GDP growth and that, along with other positive developments, would result in meaningful releases of value in select European companies.

So, what happened?

Russia invaded Crimea/Ukraine. Panic set in quickly. Consumer sentiment fell off a cliff. Sanctions were levied and the economic impact of reduced trade with Russia/Ukraine began to show. People questioned whether Russia might not stop with the invasion of Ukraine. The long expected quantitative easing (“QE”) program from the European Central Bank (“ECB”) did not materialize as expected. Ebola fears that started in Africa began to spread around the world. The positive sentiment we had coming into 2014 quickly vaporized and became fearful and negative. Overall, the perception shifted to a perspective that the long talked about recovery in Europe would now be pushed out and it would continue to be a tomorrow story, not a today story.

We fundamentally disagree with this perspective on both the macro and micro level. We believe that 2014 was a period marked by investor stress and uncertainty, but that today there are many European companies which are less expensive than they have been in years with better prospects that investors have not fully focused on. Our recent trips to Europe and conversations with European business operators and owners have corroborated our thoughts.

It is important to note that we have not made a decision to “allocate” a large percent of the Fund’s assets to Europe – we are agnostic to geography. Rather, we make allocations to those investment opportunities that are most compelling from a valuation and catalyst standpoint on a company specific basis. We happen to have a large exposure to European special situations because, in our opinion, that is where the best opportunities exist today.

Some of the special situations we own have been reporting year over year top line growth in excess of 15% in their best segments. These increases are off of already meaningfully reduced baselines of revenues, so they are telling us that they believe (1) they have seen a bottom, and (2) there is surely a long way to go back up.

We are compelled to own select companies that are restructuring and making the right strategic moves in a time of low growth and cyclical downturns. These companies have been streamlining operations to focus on the businesses that have the ability to generate the strongest cash flows, making the necessary cuts to improve operational inefficiencies, and selling non-essential/losing businesses. What is left behind are more pure play companies that sell at sizable discounts to cash flow and/or book value.

6

So, while widespread consistent top-line growth is unsteady and has generally fallen the last five years, these smartly run businesses have remained profitable on their bottom lines due to the cuts they have, and are continuing, to make. When incremental top line growth begins to come back more broadly, we expect our companies will show increased cash flows coming through that exceed investors’ current expectations. This potential upside in profitability and earnings power will be a much deserved positive outcome of their savvy and focused cost cutting efforts.

Considering the macro environment, we ask ourselves, what could stimulate top line growth and a return of investor and consumer confidence? We believe the answer lies in a mix of a weakening Euro, sharply falling oil and energy prices, near zero interest rates, and the recently announced €1.1 trillion ($1.33 trillion) ECB quantitative easing (QE) program.

Armed with a long-term perspective, these are just a few reasons to suggest that now is an excellent time to be sifting through the muck of European uncertainty. We remain highly confident in the quality of our portfolio holdings, the value in their underlying assets, and believe that going into the New Year our portfolio is positioned with the potential to deliver real value creation.

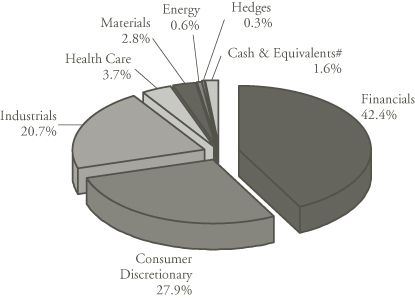

Portfolio Construction and Activity

The Fund ended the year with 32 equity (issuer) positions, the top 10 of which represented 46.5% of the Fund’s total net assets. Below please find year-end market cap, geographic region, and strategy breakdowns of the Fund’s portfolio as of December 31, 2014.1

|  |

_______________

1 Market cap, geographic region and strategy breakdown are show as a percentage of invested capital in equity positions only.

7

Portfolio Review

Spin-off activity was again on the rise in 2014, growing globally from 37 in 2013 to 60 in 20142. We continue to focus on spin-offs, which often are extremely attractive situations, as they are generally not well understood parts of larger companies that can come to the market extremely mispriced.

The Fund participated in a number of spin-offs in 2013, including ING U.S. (now VOYA Financial), which was spun-off from ING Groep NV (also a Fund holding since 2013). In June 2014, ING Groep spun-off another one of its business segments – NN Group NV – via an initial public offering. NN Group is the largest insurance provider in the Netherlands. We participated in the IPO, which was priced at what we believed was an extremely low valuation – under 0.6 times book value. In a very short time, book value has grown to about €45 ($54.45) per share. The company expects to pay between 40 and 50 percent of operating cash flow to shareholders. The underlying insurance businesses are strong. The biggest risk to the stock continues to be litigation from legacy annuity products. We believe the stock is cheap even after factoring in a significant settlement.

The Fund also invested in an interesting arbitrage situation during the year. Alliant Techsystems Inc., primarily a U.S. based defense company, is also the parent of an outdoor and leisure business called Vista Outdoor (“Vista”). The long position the Fund has in Alliant is part of an arbitrage trade to create a Vista spinoff very cheaply, as Alliant and another U.S. based defense business, Orbital Sciences Corp., are scheduled to merge in 2015 and simultaneously spinoff Vista. We have no interest in the defense businesses, but believe Vista is extremely compelling. Today, we can “create” the new Vista by buying Alliant and shorting Orbital and get to “own” it now before it trades on a stand-alone basis. At the time of purchase, Vista was being valued at barely 6 times EBITDA and 9 times earnings. My experience is that investors will generally start focusing on these types of spin-offs once they are on their own and we would expect to see Vista valued closer to where its peers trade, which is about 50% higher. We believe this is one of those unique situations where the opportunity is not in the new merged company, but is actually in the lesser known and misunderstood division that is getting spun-off as a new standalone public company.

The Fund also invested in several interesting restructuring special situations, including Fomento de Construcionnes y Contratas SA (“FCC”) (one of the leading detractors to Fund performance for the year) and Green Brick Partners, Inc. (“Green Brick”) (the leading contributor to Fund performance for the year).

We initiated our position in FCC, a Spain based construction and concession conglomerate, in early 2014. The company is in the midst of a transformative financial and operational restructuring. An acquisition spree in the mid-2000s left the company in an over-leveraged, under-earning state by the end of the decade. In addition to its core businesses of water services, waste collection, and construction, FCC accumulated a portfolio of non-core businesses including cement production, real estate ownership and development, and furniture rental, to name a few. In 2013,

_______________

2 Spinoff Research, January 2015 issue.

8

the controlling shareholder, Esther Koplowitz, brought in Juan Béjar as CEO to sell assets, pay down debt, and refocus the company. We have met Mr. Béjar on several occasions and believe he is one of the best CEOs in Europe with the skills to successfully restructure both financially and operationally. In 2014, Mr. Béjar began selling non-core assets, and consummated a €1 billion ($1.21 billion) rights issue, €765 million ($925.7 million) of which was used to pay down €900 million ($1.09 billion) of debt. As part of the financial restructuring, Carlos Slim, the Mexican billionaire, became a 25.6% owner of the company and Esther Koplowitz went from being a majority investor to a minority investor – a very positive result.

Using a sum of the parts analysis where we look at comparable business transactions and other publicly traded companies’ valuations, we estimate that FCC is worth around €24.00 ($29.04) per share versus €11.75 ($14.22) per share as of year-end. Today, FCC is trading at less than 5 times the depressed cash flows of their best businesses, water and waste treatment, where peers typically trade between 8 and 11 times cash flow. Green Brick is a very interesting situation. The predecessor company was called BioFuels Energy, which was a defunct alternative energy business. David Einhorn from Greenlight Capital took control and recapitalized the business into a large home builder in Atlanta and parts of Texas. We were able to buy this company in the third quarter pre-conversion after documents were filed with the SEC, but still little understood by the market. At the time we initiated our position in the stock, we were creating the new business at less than 7 times earnings with excellent management, and main shareholders that include Greenlight and Dan Loeb’s Third Point, which collectively own 67%. We took advantage of the inherent mispricing by the market of the warrants that were issued to shareholders to create our position extremely cheap.

The Fund’s largest detractor to performance for the year was Sevan Drilling AS. Sevan, a deep water drilling company, suffered a fate similar to most oil exploration companies and sold off meaningfully. Severe downward pressure on the price of oil, along with problems on one of their rigs during the year, caused the stock to decline over 78% in the year. At year end, the stock was trading at less than 2 times earnings and less than 25% of replacement value for its assets. The company has restructured its credit facilities and is running at a higher level of efficiency than at any time in the history of the company. As a result, the Fund continues to hold this position. Unfortunately, due to the volatility of the commodity price, today, investors have little interest in Sevan or other oil related businesses.

Another of the Fund’s top detractors to performance in 2014 was Genworth Financial Inc., the U.S. based multiline insurance company. We decided to exit this position in the fourth quarter at a loss after owning the position for several years. The original thesis centered on the reorganization of their Mortgage Insurance business. Our view was that the stock was trading at a substantial discount to book value and that they would be able to ring fence the mortgage insurance problem, which they were in fact able to do. The stock performed well until late in 2014 when it emerged that the Long Term Care business was having significant issues and might require the company to do a capital raise. This was not part of our original thesis and, as a result, we determined that it was time to move on in spite of the significant discount to book value.

9

Closing Thoughts

In this environment, there are a lot of cheap stocks to be had outside the United States, but you cannot own them all and expect to generate an outsized return. I firmly believe that the key to creating value is found in identifying those certain catalysts that are likely to accrete shareholder value in the years to come. Understanding the nature, potential impact and time frame of such catalysts is the road map to successful special situations investing.

We spend a great deal of time trying to understand management’s appraisal of their business and proposed path. Ultimately, we believe that management is the most important catalyst to value creation and we strive to place our investment capital alongside some of the best operators the world, and especially Europe, have to offer.

In 2014, we made several trips to Europe. Based on these visits, in my opinion, the news headlines have not accurately reflected the underlying improvements in businesses across a variety of sectors that have been years in the making. Beyond improving business fundamentals, we enter 2015 with some significant tailwinds behind European companies – low oil prices, low interest rates, low valuations, increasing M&A and spin-off activity, and a huge ECB mandated quantitative easing program. In our view, these developments represent an inflection point for the prospects of many European companies.

We are nomadic and roam to where we believe the best investment opportunities exist. When we believe they have played out, we move on. We continue to believe that out of crisis comes opportunity. In our opinion, the situation that has evolved out of the crisis in Europe has set the stage for a multiyear opportunity for special situations in the region. The key is to be extremely selective.

And, while many investors are nervous about the U.S. markets, we continue to find selective cases where there are compelling breakup, spinoff, and activist situations in which to invest.

As such, I believe that the special situations in which we have invested, and the opportunities we continue to find, have the potential to provide our Fund shareholders with attractive long term investment returns.

Thank you once again for your ongoing partnership, confidence and support.

Sincerely,

David E. Marcus

Portfolio Manager

10

Management’s Discussion of Fund Performance

For the year ended December 31, 2014, Class I shares of the Evermore Global Value Fund (the “Fund”) were down 6.58% while the MSCI All Country World Index (“MSCI ACWI”) was up 4.16%, and the HFRX Event Driven Index (“HFRX ED”) was down 4.06%.

2014 was a disappointing follow-up to what was a very good 2013. The year started off fine with a continuation of the same positive situations that we had seen in 2013 – an acceleration in restructurings, refocusing by companies, breakups, spinoffs, management changes, and an increase in M&A activity. There was optimism and a cautious sense of recovery. The view was that Europe, having come out of recession in 2013, would see a major pick-up in GDP growth and that, along with other positive developments, would result in meaningful releases of value in select European companies. However, we believe a series of events had a major negative impact on our performance, especially in the second and third quarters of the year.

Russia invaded Crimea/Ukraine. Panic set in quickly. Consumer sentiment fell off a cliff. Sanctions were levied and the economic impact of reduced trade with Russia/Ukraine began to show. People questioned whether Russia might not stop with the invasion of Ukraine. The long expected quantitative easing (“QE”) program from the European Central Bank (“ECB”) did not materialize as expected. Ebola fears that started in Africa began to spread around the world. The positive sentiment we had coming into 2014 quickly vaporized and became fearful and negative, and investor perception shifted to a perspective that the long talked about recovery in Europe would now be pushed out and it would continue to be a tomorrow story, not a today story.

Three of the top five contributors to Fund performance were U.S. positions; two were European positions. Four of the top five detractors to Fund performance were European positions; one was a U.S. position. The largest contributors and detractors to the Fund performance for the year were:

For the Year Ended 12/31/14

| Top 5 Contributors to Performance | Top 5 Detractors to Performance |

| Green Brick Partners, Inc. | Sevan Drilling ASA |

| Compagnie d’Enterprises CFE SA | Genworth Financial Inc. |

| Voya Financial, Inc. | Fomento de Construcionnes y Contratas SA |

| Gramercy Property Trust Inc. | Sky Deutschland AG |

| Ei Towers S.p.A. | Bolloré SA |

A short discussion on several of the contributors and detractors listed above can be found in the Portfolio Manager’s letter to shareholders located at the beginning of this annual report.

11

As of December 31, 2014, the Fund’s ten largest issuer positions were as follows:

Evermore Global Value Fund

Top 10 Positions

| Issuer Position | % of Net Assets |

| Ambac Financial Group, Inc. | 6.6% |

| Vivendi SA | 6.2% |

Alliant Techsystems, Inc.3 | 6.0% |

| NN Group NV | 5.0% |

| Green Brick Partners, Inc. | 5.0% |

| Sky Deutschland AG | 4.8% |

| Fomento de Construcionnes y Contratas SA | 4.5% |

| ING Groep NV | 4.4% |

| Voya Financial, Inc. | 3.9% |

| American International Group, Inc. | 3.7% |

At year-end 2014, the Fund’s cash position stood at 0.6%.

_______________

3 Alliant Techsystems plans to merge with Orbital Sciences (a short position in the Fund as of 12/31/14) and simultaneously will spin-off Vista Outdoor, a leisure equipment and products company, in the first quarter of 2015.

12

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

Past performance does not guarantee future results. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. Investing in smaller companies involves additional risks such as limited liquidity and greater volatility than larger companies. The Fund may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment in lower-rated, non-rated and distressed securities presents a greater risk of loss to principal and interest than higher-rated securities. Investments in special situations may involve greater risks when compared to other investments if expected developments do not occur. Additional special risks relevant to our Fund involve derivatives and hedging. Please refer to the prospectus for further details.

Please refer to the Schedules of Investments for complete holdings information. Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

The MSCI All-Country World Index is an unmanaged index comprised of 48 country indices, including 23 developed and 25 emerging market country indices, and is calculated with dividends reinvested after deduction of holding tax. The index is a trademark of Morgan Stanley Capital International and is not available for direct investment.

Hedge Fund Research, Inc. (HFR) utilizes a UCITSIII compliant methodology to construct the HFRX Hedge Fund Indices. The methodology is based on defined and predetermined rules and objective criteria to select and rebalance components to maximize representation of the Hedge Fund Universe. The HFRX Event Driven Index is being used under license from Hedge Fund Research, Inc. which does not approve or endorse the Evermore Global Value Fund.

It is not possible to invest directly in an index.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income. “EBIT” is the acronym for earnings before taxes and interest. “EBITDA” is the acronym for earnings before interest, taxes, depreciation and amortization. “Book Value” is calculated by subtracting a company’s liabilities from its assets. “Price to Book Value” is a ratio used to compare a stock’s market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value per share.

Must be preceded or accompanied by a prospectus.

The Evermore Global Value Fund is distributed by Quasar Distributors, LLC. Quasar Distributors, LLC is affiliated with U.S. Bancorp Fund Services, LLC and U.S. Bank N.A.

13

Evermore Global Value Fund

| SECTOR ALLOCATION* as a Percentage of Net Assets at December 31, 2014 (Unaudited) |

*Does not include security sold short.

#Cash equivalents and other assets less liabilities.

14

Evermore Global Value Fund

| EXPENSE EXAMPLE for the Six Months Ended December 31, 2014 (Unaudited) |

As a shareholder of the Evermore Global Value Fund (the “Fund”), you incur two types of costs: (1) transaction costs, including sales charges or loads; and (2) ongoing costs, including investment advisory fees, distribution fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (7/1/14 – 12/31/14).

Actual Expenses

The first line of the table below provides information about actual account values based on actual returns and actual expenses. You will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Fund’s transfer agent. If you request a redemption be made by wire transfer, currently a $15.00 fee is charged by the Fund’s transfer agent. You will be charged a redemption fee equal to 2% of the net amount of the redemption if you redeem shares less than 30 calendar days after you purchase them. An Individual Retirement Account (“IRA”) will be charged a $15.00 annual maintenance fee. To the extent the Fund invests in shares of other investment companies as part of its investment strategy, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Fund invests in addition to the expenses of the Fund. Actual expenses of the underlying funds may vary. These expenses are not included in the example below. The example below includes, but is not limited to, investment advisory fees, shareholder servicing fees, fund accounting fees, custody fees and transfer agent fees. However, the example below does not include portfolio trading commissions and related expenses, and other extraordinary expenses as determined under generally accepted accounting principles. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account value and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples

15

Evermore Global Value Fund

| EXPENSE EXAMPLE for the Six Months Ended December 31, 2014 (Unaudited), Continued |

that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending | Expenses Paid | |

| Account Value | Account Value | During the Period | |

| 7/1/14 | 12/31/14 | 7/1/14 – 12/31/14* | |

| Class A Actual | $1,000 | $ 930 | $7.78 |

| Class A Hypothetical (5% annual | |||

| return before expenses) | $1,000 | $1,017 | $8.13 |

| Class I Actual | $1,000 | $ 931 | $6.57 |

| Class I Hypothetical (5% annual | |||

| return before expenses) | $1,000 | $1,018 | $6.87 |

| * | Expenses are equal to the Fund’s expense ratios for the most recent six-month period, including interest expense and dividend expense on securities sold short, of 1.61% for Class A shares and 1.36% forClass I shares multiplied by the average account value over the period multiplied by 184/365 (to reflect the one-half year period). |

16

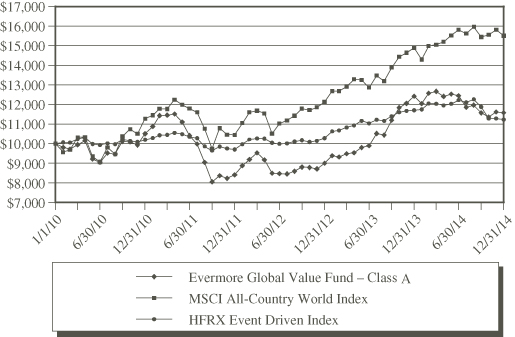

Evermore Global Value Fund

Value of $10,000 vs. MSCI All-Country World Index &

HFRX Event Driven Index (Unaudited)

| Total Annualized | Since | Value of | |||

| Returns Year Ended | Inception | $10,000 | |||

| December 31, 2014 | 1 Year | 3 Year | 5 Year | (1/1/2010) | (12/31/14) |

| Class A | (6.83)% | 11.25% | 2.97% | 2.97% | $11,573 |

| Class A | |||||

| (with sales charge*) | (11.46)% | 9.35% | 1.91% | 1.91% | $10,444 |

| Class I | (6.58)% | 11.57% | 3.21% | 3.21% | $11,713 |

| MSCI All-Country | |||||

| World Index | 4.16% | 14.10% | 9.17% | 9.17% | $15,506 |

| HFRX Event | |||||

| Driven Index | (4.06)% | 5.00% | 2.30% | 2.30% | $11,226 |

| * | The maximum sales charge (load) imposed on a purchase is 5.00%. |

This chart illustrates the performance of a hypothetical $10,000 investment made on January 1, 2010, and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns reflect fee waivers/recoupments in effect. In the absence of such waivers/recoupments, total return would be reduced. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for an index.

17

Evermore Global Value Fund

| SCHEDULE OF INVESTMENTS at December 31, 2014 |

| Market | |||||||

| Shares | Value# | ||||||

| COMMON STOCKS – 92.8% | |||||||

| Aerospace & Defense – 6.0% | |||||||

| 121,006 | Alliant | ||||||

| Techsystems, Inc. | |||||||

| (United States) | $ | 14,066,948 | |||||

| Asset Management & | |||||||

| Custody Banks – 5.3% | |||||||

| 13,524,484 | SC Fondul | ||||||

| Proprietatea SA | |||||||

| (Romania) | 3,259,972 | ||||||

| 213,600 | Voya Financial, Inc. | ||||||

| (United States) | 9,052,368 | ||||||

| 12,312,340 | |||||||

| Cable & Satellite – 4.8% | |||||||

| 1,386,427 | Sky Deutschland | ||||||

AG (Germany)*1 | 11,199,750 | ||||||

| Casinos & Gaming – 5.2% | |||||||

| 800,898 | OPAP SA (Greece) | 8,582,685 | |||||

| 231,900 | Universal | ||||||

| Entertainment | |||||||

| Corp. (Japan) | 3,466,147 | ||||||

| 12,048,832 | |||||||

| Construction & Engineering – 10.9% | |||||||

| 76,814 | Compagnie | ||||||

| d’Enterprises | |||||||

| (Belgium) | 7,870,579 | ||||||

| 738,886 | Fomento de | ||||||

| Contrucciones | |||||||

| (Spain)* | 10,433,708 | ||||||

| 3,276,920 | Maire Tecnimont | ||||||

| SpA (Italy)* | 7,064,520 | ||||||

| 25,368,807 | |||||||

| Diversified Financial Services – 4.4% | |||||||

| 784,700 | ING Groep NV | ||||||

(Netherlands)*1 | 10,138,086 | ||||||

| General Merchandise Stores – 2.6% | |||||||

| 278,157 | Retail Holdings | ||||||

NV (Hong Kong)2 | 6,119,454 | ||||||

| Health Care Providers | |||||||

| & Services – 3.7% | |||||||

| 497,327 | Lifco AB (Sweden)* | 8,580,598 | |||||

| Home Building – 5.0% | |||||||

| 1,415,353 | Green Brick | ||||||

| Partners, Inc. | |||||||

| (United States)* | 11,605,895 | ||||||

| Industrial Conglomerates – 3.7% | |||||||

| 7,800 | Bollore Protection | ||||||

| SA (France)* | 35,522 | ||||||

| 1,044,300 | Bollore SA | ||||||

(France)1 | 4,755,852 | ||||||

| 27,711,000 | K1 Ventures Ltd. | ||||||

| (Singapore) | 3,894,623 | ||||||

| 8,685,997 | |||||||

| Insurance – 13.5% | |||||||

| 527,731 | Ambac Financial | ||||||

| Group, Inc. | |||||||

(United States)*1 | 12,929,409 | ||||||

| 394,100 | NN Group NV | ||||||

(Netherlands)*1 | 11,765,291 | ||||||

| 706,440 | UNIQA Insurance | ||||||

| Group AG | |||||||

| (Austria) | 6,629,964 | ||||||

| 31,324,664 | |||||||

| Media – 10.3% | |||||||

| 376,190 | Havas SA (France) | 3,071,844 | |||||

| 7,128,484 | Promotora de | ||||||

| Informaciones SA | |||||||

| (Spain)* | 2,211,891 | ||||||

| 3,683,197 | Promotora de | ||||||

| Informaciones SA – | |||||||

| Class A – | |||||||

| (Spain) ADR* | 4,309,340 | ||||||

| 581,666 | Vivendi SA | ||||||

| (France) | 14,478,012 | ||||||

| 24,071,087 | |||||||

| Metals & Mining – 2.8% | |||||||

| 257,400 | ThyssenKrupp | ||||||

| AG (Germany) | 6,556,983 | ||||||

The accompanying notes are an integral part of these financial statements.

18

Evermore Global Value Fund

| SCHEDULE OF INVESTMENTS at December 31, 2014, Continued |

| Market | |||||||

| Shares | Value# | ||||||

| Multi-line Insurance – 3.7% | |||||||

| 155,300 | American | ||||||

| International | |||||||

| Group, Inc. | |||||||

| (United States) | $ | 8,698,353 | |||||

| Oil & Gas Drilling – 0.6% | |||||||

| 10,392,243 | Sevan Drilling AS | ||||||

| (Norway)* | 1,490,245 | ||||||

| Other Diversified Financial | |||||||

| Services – 5.3% | |||||||

| 45,183 | Ackermans & | ||||||

| van Haaren NV | |||||||

| (Belgium) | 5,571,346 | ||||||

| 465,900 | American | ||||||

| Capital Ltd. | |||||||

(United States)*1 | 6,806,799 | ||||||

| 12,378,145 | |||||||

| Real Estate Management | |||||||

| & Development – 5.0% | |||||||

| 2,109,035 | Deutsche Office | ||||||

| AG (Germany)* | 7,451,742 | ||||||

| 1,520,000 | Selvaag Bolig AS | ||||||

| (Norway) | 4,099,289 | ||||||

| 11,551,031 | |||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $211,055,534) | 216,197,215 | ||||||

| PARTNERSHIPS & TRUSTS – 4.2% | |||||||

| Real Estate Investment Trusts – 4.2% | |||||||

| 1,045,172 | Gramercy Property | ||||||

| Trust, Inc. | |||||||

| (United States) | 7,211,687 | ||||||

| 199,000 | Saltangen Property | ||||||

(Sweden)*2 | 2,552,738 | ||||||

| TOTAL PARTNERSHIPS | |||||||

| & TRUSTS | |||||||

| (Cost $7,449,401) | 9,764,425 | ||||||

| WARRANTS – 1.1% | |||||||

| Insurance – 1.1% | |||||||

| 174,371 | Ambac Financial | ||||||

| Group, Inc., | |||||||

| Expiration: | |||||||

| April, 2023, | |||||||

| Exercise Price: | |||||||

| $16.67 | |||||||

| (United States)* | 2,484,787 | ||||||

| TOTAL WARRANTS | |||||||

| (Cost $2,729,833) | 2,484,787 | ||||||

| Contracts | |||||||

| CALL OPTIONS PURCHASED – 0.2% | |||||||

| Hedges – 0.1% | |||||||

| 3,000 | CurrencyShare | ||||||

| Swiss Franc, | |||||||

| Expiration: | |||||||

| March, 2015, | |||||||

| Strike Price: | |||||||

| 107 CHF | |||||||

(Switzerland)3 | 22,500 | ||||||

| 900 | iShares 20+ Year | ||||||

| Treasury Bond | |||||||

| Fund, Expiration: | |||||||

| March, 2015, | |||||||

| Strike Price: | |||||||

| $124 | |||||||

(United States)3 | 339,750 | ||||||

| 362,250 | |||||||

| Multi-line Insurance – 0.1% | |||||||

| 4,450 | Genworth | ||||||

| Financial, Inc., | |||||||

| Expiration: | |||||||

| January, 2016, | |||||||

| Strike Price: | |||||||

| $15 | |||||||

(United States)3 | 122,375 | ||||||

| TOTAL CALL OPTIONS | |||||||

| PURCHASED | |||||||

| (Cost $1,158,773) | 484,625 | ||||||

The accompanying notes are an integral part of these financial statements.

19

Evermore Global Value Fund

| SCHEDULE OF INVESTMENTS at December 31, 2014, Continued |

| Market | |||||||

| Contracts | Value# | ||||||

| PUT OPTIONS PURCHASED – 0.1% | |||||||

| Hedges – 0.1% | |||||||

| 440 | DAX 03/20/15 | ||||||

| P8600, | |||||||

| Expiration: | |||||||

| March, 2015, | |||||||

| Strike Price: | |||||||

| 8600 EUR | |||||||

(Germany)4 | $ | 230,007 | |||||

| TOTAL PUT OPTIONS | |||||||

| PURCHASED | |||||||

| (Cost $788,041) | 230,007 | ||||||

| SHORT-TERM INVESTMENT – 0.6% | |||||||

| Money Market Fund – 0.6% | |||||||

| 1,439,556 | Invesco Liquid | ||||||

| Assets Portfolio – | |||||||

| Institutional | |||||||

Class, 0.07%5 | $ | 1,439,556 | |||||

| TOTAL SHORT-TERM | |||||||

| INVESTMENT | |||||||

| (Cost $1,439,556) | 1,439,556 | ||||||

| TOTAL INVESTMENTS | |||||||

| IN SECURITIES – 99.0% | |||||||

| (Cost $224,621,138) | 230,600,615 | ||||||

| Other Assets in Excess | |||||||

| of Liabilities – 1.0% | 2,443,740 | ||||||

| TOTAL NET | |||||||

| ASSETS – 100.0% | $ | 233,044,355 | |||||

| # | See Significant Accounting Policies of accompanying Notes to Financial Statements regarding valuation of securities. |

| * | Non-income producing security. |

| ADR | American Depositary Receipt |

| CHF | Swiss Franc |

| EUR | Euro |

| 1 | All or a portion of this security was segregated as collateral for forward foreign currency contract. |

| 2 | Affiliated company as defined by the Investment Company Act of 1940. |

| 3 | 100 shares per contract. |

| 4 | 5 shares per contract. |

| 5 | Seven-day yield as of December 31, 2014. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS® is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Fund’s Administrator, U.S. Bancorp Fund Services, LLC.

| SCHEDULE OF SECURITY SOLD BUT NOT YET PURCHASED at December 31, 2014 |

| Shares | Value | ||||||

| SECURITY SOLD BUT NOT | |||||||

| YET PURCHASED – 3.1% | |||||||

| Aerospace & Defense – 3.1% | |||||||

| 269,499 | Orbital Sciences Corp. | ||||||

| (United States)* | $ | 7,246,828 | |||||

| TOTAL SECURITY SOLD | |||||||

| BUT NOT YET PURCHASED | |||||||

| (Proceeds $6,854,372) | $ | 7,246,828 | |||||

| * | Non-income producing security. |

The accompanying notes are an integral part of these financial statements.

20

Evermore Global Value Fund

| COUNTRY ALLOCATION at December 31, 2014 |

| Country | Long Exposure | Short Exposure^ | Net Exposure | ||||||||||

| United States | 33.0 | % | 3.3 | % | 29.7 | % | |||||||

| Germany | 11.5 | % | — | 11.5 | % | ||||||||

| France | 10.1 | % | — | 10.1 | % | ||||||||

| Netherlands | 9.9 | % | — | 9.9 | % | ||||||||

| Spain | 7.6 | % | — | 7.6 | % | ||||||||

| Belgium | 6.1 | % | — | 6.1 | % | ||||||||

| Sweden | 5.0 | % | — | 5.0 | % | ||||||||

| Greece | 3.9 | % | — | 3.9 | % | ||||||||

| Italy | 3.2 | % | — | 3.2 | % | ||||||||

| Austria | 3.0 | % | — | 3.0 | % | ||||||||

| Hong Kong | 2.8 | % | — | 2.8 | % | ||||||||

| Norway | 2.5 | % | — | 2.5 | % | ||||||||

| Singapore | 1.7 | % | — | 1.7 | % | ||||||||

| Japan | 1.5 | % | — | 1.5 | % | ||||||||

| Romania | 1.5 | % | — | 1.5 | % | ||||||||

| Switzerland# | 0.0 | % | — | 0.0 | % | ||||||||

| Total | 103.3 | % | 3.3 | % | 100.0 | % | |||||||

| ^ | Securities sold but not yet purchased. |

| # | Less than 0.1%. |

| FORWARD FOREIGN CURRENCY CONTRACTS at December 31, 2014 |

As of December 31, 2014, the Fund had the following forward currency contracts outstanding with Morgan Stanley:

| Amount | Amount | ||||||||||||||||||

| of | of | Net | |||||||||||||||||

| Currency | Currency | Settle- | Currency | Currency | Unrealized | ||||||||||||||

| to be | to be | ment | to be | to be | Fair | Appreciation | |||||||||||||

| Received | Received | Date | Delivered | Delivered | Value | (Depreciation) | |||||||||||||

| EUR | 7,000,000 | 3/11/15 | USD | 8,712,900 | $ | 8,475,807 | $ | (237,093 | ) | ||||||||||

| USD | 131,879,516 | 3/11/15 | EUR | 105,667,600 | 127,945,464 | 3,934,052 | |||||||||||||

| USD | 3,772,571 | 3/11/15 | JPY | 431,200,000 | 3,602,170 | 170,401 | |||||||||||||

| NOK | 11,600,000 | 3/11/15 | USD | 1,632,178 | 1,553,315 | (78,863 | ) | ||||||||||||

| USD | 7,289,405 | 3/11/15 | NOK | 50,004,000 | 6,695,857 | 593,548 | |||||||||||||

| RON | 1,500,000 | 3/11/15 | USD | 416,782 | 404,234 | (12,548 | ) | ||||||||||||

| USD | 3,861,840 | 3/11/15 | RON | 13,730,000 | 3,700,094 | 161,746 | |||||||||||||

| USD | 11,148,315 | 3/11/15 | SEK | 83,809,600 | 10,753,651 | 394,664 | |||||||||||||

| SGD | 635,000 | 3/11/15 | USD | 489,625 | 478,781 | (10,844 | ) | ||||||||||||

| USD | 4,393,880 | 3/11/15 | SGD | 5,678,400 | 4,281,438 | 112,442 | |||||||||||||

| Net Value of Outstanding Forward Currency Contracts | $ | 167,890,811 | $ | 5,027,505 | |||||||||||||||

| EUR | Euro |

| JPY | Japanese Yen |

| NOK | Norwegian Krone |

| RON | Romanian New Leu |

| SGD | Singapore Dollar |

| SEK | Sweedish Krona |

| USD | U.S. Dollars |

The accompanying notes are an integral part of these financial statements.

21

Evermore Global Value Fund

| STATEMENT OF ASSETS AND LIABILITIES at December 31, 2014 |

| ASSETS | ||||

| Investments in unaffiliated securities, at value^ (Note 2) | $ | 221,928,423 | ||

| Investments in affiliated securities, at value * | 8,672,192 | |||

| Total investments, at value | 230,600,615 | |||

| Unrealized gain on forward foreign currency contracts | 5,366,853 | |||

| Receivables: | ||||

| Investment securities sold | 30,928 | |||

| Fund shares sold | 180,891 | |||

| Dividends and interest, net | 124,563 | |||

| Due from broker, net | 7,496,979 | |||

| Prepaid expenses | 67,883 | |||

| Total assets | 243,868,712 | |||

| LIABILITIES | ||||

| Unrealized loss on forward foreign currency contracts | 339,348 | |||

| Securities sold but not yet purchased, at market value# | 7,246,828 | |||

| Payables: | ||||

| Investment securities purchased | 386,624 | |||

| Foreign currency payable | 1,985 | |||

| Fund shares redeemed | 2,536,951 | |||

| Investment advisory fees, net | 156,279 | |||

| Administration fees | 20,751 | |||

| Custody fees | 19,244 | |||

| Distribution fees | 7,098 | |||

| Fund accounting fees | 10,434 | |||

| Transfer agent fees | 12,793 | |||

| Other accrued expenses | 86,022 | |||

| Total liabilities | 10,824,357 | |||

| NET ASSETS | $ | 233,044,355 | ||

| COMPONENTS OF NET ASSETS | ||||

| Paid-in capital | $ | 236,333,588 | ||

| Accumulated net investment income | 2,113,119 | |||

| Accumulated net realized loss on investments, foreign | ||||

| currency transactions & forward foreign currency contracts | (16,008,004 | ) | ||

| Net unrealized appreciation on investments, foreign | ||||

| currency translations & forward foreign currency contracts | 10,605,652 | |||

| Net assets | $ | 233,044,355 | ||

| ^ Cost of unaffiliated investments | $ | 217,741,980 | ||

| * Cost of affiliated investments | $ | 6,879,158 | ||

| # Proceeds received | $ | 6,854,372 | ||

The accompanying notes are an integral part of these financial statements.

22

Evermore Global Value Fund

| STATEMENT OF ASSETS AND LIABILITIES at December 31, 2014, Continued |

| Class A: | ||||

| Net assets | $ | 33,076,601 | ||

| Shares issued and outstanding (unlimited number | ||||

| of shares authorized without par value) | 3,145,539 | |||

| Net asset value, and redemption price per share | $ | 10.52 | ||

| Maximum offering price per share* | $ | 11.07 | ||

| Class I: | ||||

| Net assets | $ | 199,967,754 | ||

| Shares issued and outstanding (unlimited number | ||||

| of shares authorized without par value) | 18,926,058 | |||

| Net asset value, offering price, and redemption price per share | $ | 10.57 | ||

| * | The maximum offering price per share is calculated as the net asset value per share as of December 31, 2014 divided by (1-front-end sales charge (5%)): $10.52/95.00%. In addition, Class A share investments of $1 million or more, which are purchased at Net Asset Value, are subject to a 0.75% contingent deferred sales charge (“CDSC”) if redeemed within 12 months. |

The accompanying notes are an integral part of these financial statements.

23

(This Page Intentionally Left Blank.)

24

Evermore Global Value Fund

| STATEMENT OF OPERATIONS for the Year Ended December 31, 2014 |

| INVESTMENT INCOME* | ||||

| Income | ||||

| Dividends (net of $169,320 foreign withholding tax) | $ | 2,313,330 | ||

| Interest | 60,186 | |||

| Other income | 699 | |||

| Total investment income | 2,374,215 | |||

| EXPENSES (Note 3) | ||||

| Investment advisory fees | 2,299,230 | |||

| Administration fees | 124,182 | |||

| Transfer agent fees | 119,747 | |||

| Custody fees | 156,205 | |||

| Legal fees | 108,121 | |||

| Distribution fees – Class A | 84,987 | |||

| Registration fees | 81,252 | |||

| Fund accounting fees | 67,550 | |||

| Audit fees | 41,393 | |||

| Chief Compliance Officer fees | 47,953 | |||

| Reports to shareholders | 23,711 | |||

| Trustee fees | 32,022 | |||

| Insurance expense | 28,100 | |||

| Miscellaneous expenses | 4,822 | |||

| Interest expense to broker | 12 | |||

| Total expenses | 3,219,287 | |||

| Plus expenses recouped | 32,229 | |||

| Net expenses | 3,251,516 | |||

| Net investment loss | (877,301 | ) | ||

| REALIZED AND UNREALIZED GAIN (LOSS) ON | ||||

| INVESTMENTS, FOREIGN CURRENCY TRANSACTIONS, | ||||

| FORWARD FOREIGN CURRENCY CONTRACTS | ||||

| & SECURITIES SOLD BUT NOT YET PURCHASED | ||||

| Net realized gain on investments, foreign currency | ||||

| transactions & forward foreign currency contracts* | 4,851,515 | |||

| Net realized loss on securities sold but not yet purchased | (207,022 | ) | ||

| Change in net unrealized depreciation on investments, foreign | ||||

| currency translations & forward foreign currency contracts | (20,246,546 | ) | ||

| Net realized and unrealized loss on investments, foreign | ||||

| currency transactions, forward foreign currency contracts & securities | ||||

| sold but not yet purchased | (15,602,053 | ) | ||

| Net decrease in net assets resulting from operations | $ | (16,479,354 | ) | |

| * No affiliated transactions recorded. | ||||

The accompanying notes are an integral part of these financial statements.

25

Evermore Global Value Fund

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended | Year Ended | |||||||

| December 31, | December 31, | |||||||

| 2014 | 2013 | |||||||

| INCREASE (DECREASE) IN NET ASSETS FROM: | ||||||||

| OPERATIONS | ||||||||

| Net investment income (loss) | $ | (877,301 | ) | $ | 491,277 | |||

| Net realized gain on investments, foreign currency | ||||||||

| transactions, forward foreign currency contracts & | ||||||||

| securities sold but not yet purchased | 4,644,493 | (1,234,992 | ) | |||||

| Change in net unrealized depreciation on investments, foreign | ||||||||

| currency translations & forward foreign currency contracts | (20,246,546 | ) | 34,910,034 | |||||

| Net decrease in net assets resulting from operations | (16,479,354 | ) | 34,166,319 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| From net investment income: | ||||||||

| Class A | (1,590,274 | ) | — | |||||

| Class I | (10,411,345 | ) | — | |||||

| Total distributions from net investment income | (12,001,619 | ) | — | |||||

| Total distributions to shareholders | (12,001,619 | ) | — | |||||

| CAPITAL SHARE TRANSACTIONS (Note 3) | ||||||||

| Net increase in net assets derived from net change in | ||||||||

| outstanding shares – Class A (a) | 8,809,495 | 7,678,409 | ||||||

| Net decrease in net assets derived from net change in | ||||||||

| outstanding shares – Class C (a) | — | (229,111 | ) | |||||

| Net increase in net assets derived from net change in | ||||||||

| outstanding shares – Class I (a) | 97,100,731 | 33,641,063 | ||||||

| Total increase in net assets | ||||||||

| from capital share transactions | 105,910,226 | 41,090,361 | ||||||

| Total increase in net assets | 77,429,253 | 75,256,680 | ||||||

| NET ASSETS | ||||||||

| Beginning of year | 155,615,102 | 80,358,422 | ||||||

| End of year | $ | 233,044,355 | $ | 155,615,102 | ||||

| Undistributed net investment income | $ | 2,113,119 | $ | 579,392 | ||||

The accompanying notes are an integral part of these financial statements.

26

Evermore Global Value Fund

| STATEMENTS OF CHANGES IN NET ASSETS, Continued |

| (a) | Summary of capital share transactions is as follows: |

| Year Ended | Year Ended | |||||||||||||||

| December 31, 2014 | December 31, 2013 | |||||||||||||||

| Class A | Shares | Value | Shares | Value | ||||||||||||

| Shares sold | 1,764,178 | $ | 20,264,915 | 1,187,490 | $ | 11,536,000 | ||||||||||

| Shares issued in reinvestment | ||||||||||||||||

| of distributions | 147,537 | 1,518,160 | — | — | ||||||||||||

Shares redeemed1 | (1,151,424 | ) | (12,973,580 | ) | (396,657 | ) | (4,078,308 | ) | ||||||||

| Transfer in from Class C* | — | — | 24,606 | 220,717 | ||||||||||||

| Net increase | 760,291 | $ | 8,809,495 | 815,439 | $ | 7,678,409 | ||||||||||

| Year Ended | Year Ended | |||||||||||||||

| December 31, 2014 | December 31, 2013 | |||||||||||||||

| Class C | Shares | Value | Shares | Value | ||||||||||||

| Shares sold | — | $ | — | 3,396 | $ | 30,000 | ||||||||||

| Shares issued in reinvestment | ||||||||||||||||

| of distributions | — | — | — | — | ||||||||||||

| Shares redeemed | — | — | (4,251 | ) | (38,394 | ) | ||||||||||

| Transfer out to Class A* | — | — | (24,912 | ) | (220,717 | ) | ||||||||||

| Net increase | — | $ | — | (25,767 | ) | $ | (229,111 | ) | ||||||||

| Year Ended | Year Ended | |||||||||||||||

| December 31, 2014 | December 31, 2013 | |||||||||||||||

| Class I | Shares | Value | Shares | Value | ||||||||||||

| Shares sold | 11,451,084 | $ | 133,511,275 | 6,109,680 | $ | 63,872,436 | ||||||||||

| Shares issued in reinvestment | ||||||||||||||||

| of distributions | 985,879 | 10,193,991 | — | — | ||||||||||||

Shares redeemed2 | (4,212,987 | ) | (46,604,535 | ) | (3,147,139 | ) | (30,231,373 | ) | ||||||||

| Net increase | 8,223,976 | $ | 97,100,731 | 2,962,541 | $ | 33,641,063 | ||||||||||

| 1 | Net of redemption fees of $143 and $72, respectively. |

| 2 | Net of redemption fees of $2,150 and $830, respectively. |

| * | Effective April 2, 2013, the Evermore Global Value Fund converted the Class C shares into theClass A shares. |

The accompanying notes are an integral part of these financial statements.

27

Evermore Global Value Fund

| FINANCIAL HIGHLIGHTS For a capital share outstanding throughout the year |

CLASS A

| Year Ended December 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | * | |||||||||||||||

| Net asset value, | ||||||||||||||||||||

| beginning of year | $ | 11.85 | $ | 8.59 | $ | 8.31 | $ | 10.50 | $ | 10.00 | ||||||||||

| INCOME FROM INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (loss)** | (0.07 | ) | 0.03 | 0.31 | 0.14 | 0.02 | ||||||||||||||

| Net realized and unrealized | �� | |||||||||||||||||||

| gain (loss) on investments | (0.73 | ) | 3.23 | 0.29 | (2.25 | ) | 0.48 | |||||||||||||

| Total from | ||||||||||||||||||||

| investment operations | (0.80 | ) | 3.26 | 0.60 | (2.11 | ) | 0.50 | |||||||||||||

| LESS DISTRIBUTIONS | ||||||||||||||||||||

| From net investment income | (0.53 | ) | — | (0.28 | ) | (0.08 | ) | — | ||||||||||||

| Return of capital | — | — | (0.04 | ) | — | — | ||||||||||||||

| Total distributions | (0.53 | ) | — | (0.32 | ) | (0.08 | ) | — | ||||||||||||

| Paid-in capital from | ||||||||||||||||||||

| redemption fees (Note 2) | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | ||||||||||

| Net asset value, end of year | $ | 10.52 | $ | 11.85 | $ | 8.59 | $ | 8.31 | $ | 10.50 | ||||||||||

| Total return without sales load | (6.83 | )% | 37.95 | % | 7.24 | % | (20.04 | )% | 5.00 | % | ||||||||||

| Total return with sales load | (11.46 | )% | 31.08 | % | 1.85 | % | (24.02 | )% | (0.28 | )% | ||||||||||

| SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, | ||||||||||||||||||||

| end of year (thousands) | $ | 33,077 | $ | 28,258 | $ | 13,491 | $ | 5,331 | $ | 3,651 | ||||||||||

| Portfolio turnover rate | 42 | % | 54 | % | 45 | % | 94 | % | 77 | % | ||||||||||

The accompanying notes are an integral part of these financial statements.

28

Evermore Global Value Fund

| FINANCIAL HIGHLIGHTS For a capital share outstanding throughout the year, Continued |

CLASS A

| Year Ended December 31, | ||||||||||||||||||||

2014 | 2013 | 2012 | 2011 | 2010* | ||||||||||||||||

| RATIO OF EXPENSES TO AVERAGE NET ASSETS | ||||||||||||||||||||

Before expenses absorbed2,6 | 1.60 | % | 1.81 | % | 2.13 | % | 2.24 | % | 3.60 | % | ||||||||||

After expenses absorbed3,6 | — | 1.62 | % | 1.61 | % | 1.70 | % | 1.62 | % | |||||||||||

After expenses recouped3,6 | 1.61 | % | — | — | — | — | ||||||||||||||

| RATIO OF NET INVESTMENT INCOME (LOSS) TO AVERAGE NET ASSETS | ||||||||||||||||||||

Before expenses absorbed4,6 | (0.59 | )% | 0.09 | % | 3.07 | %7 | 0.94 | % | (1.59 | )% | ||||||||||

After expenses absorbed5,6 | — | 0.28 | % | 3.59 | %7 | 1.48 | % | 0.39 | % | |||||||||||

After expenses recouped5,6 | (0.60 | )% | — | — | — | — | ||||||||||||||

| * | Fund commenced operations on January 1, 2010. |

| ** | Calculated using the average shares outstanding method. |

| 1 | Amount less than $0.01. |

| 2 | The ratio of expenses to average net assets before expenses absorbed includes interest expense. The ratio excluding interest expense was 1.59% for the year ended December 31, 2014; and 1.79%, 2.12%, 2.14% and 3.58% for the years ended December 31, 2013, 2012, 2011 and 2010, respectively. |

| 3 | The ratio of expenses to average net assets after expenses absorbed/recouped includes interest expense. The ratio excluding interest expense was 1.60% for the year ended December 31, 2014; and 1.60%, 1.60%, 1.60% and 1.60% for the years ended December 31, 2013, 2012, 2011 and 2010, respectively. |

| 4 | The ratio of net investment income (loss) to average net assets before expenses absorbed includes interest expense. The ratio excluding interest expense was (0.57)% for the year ended December 31, 2014; and 0.11%, 3.08%, 1.04% and (1.57)% for the years ending December 31, 2013, 2012, 2011 and 2010, respectively. |

| 5 | The ratio of net investment income to average net assets after expenses absorbed/recouped includes interest expense. The ratio excluding interest expense was (0.58)% for the year ended December 31, 2014; and 0.30%, 3.60%, 1.58% and 0.41% for the years ending December 31, 2013, 2012, 2011 and 2010, respectively. |

| 6 | Does not include expenses of the investment companies in which the Fund invests. |

| 7 | Certain prior period ratios have been corrected. |

The accompanying notes are an integral part of these financial statements.

29

Evermore Global Value Fund

| FINANCIAL HIGHLIGHTS For a capital share outstanding throughout the year |

CLASS I

| Year Ended December 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010* | ||||||||||||||||

| Net asset value, | ||||||||||||||||||||

| beginning of year | $ | 11.90 | $ | 8.61 | $ | 8.32 | $ | 10.52 | $ | 10.00 | ||||||||||

| INCOME FROM INVESTMENT OPERATIONS | ||||||||||||||||||||

| Net investment income (loss)** | (0.04 | ) | 0.05 | 0.34 | 0.17 | 0.03 | ||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||

| gain (loss) on investments | (0.69 | ) | 3.24 | 0.28 | (2.26 | ) | 0.49 | |||||||||||||

| Total from | ||||||||||||||||||||

| investment operations | (0.73 | ) | 3.29 | 0.62 | (2.09 | ) | 0.52 | |||||||||||||

| LESS DISTRIBUTIONS | ||||||||||||||||||||

| From net investment income | (0.60 | ) | — | (0.29 | ) | (0.11 | ) | — | ||||||||||||

| Return of capital | — | — | (0.04 | ) | — | — | ||||||||||||||

| Total distributions | (0.60 | ) | — | (0.33 | ) | (0.11 | ) | — | ||||||||||||

| Paid-in capital from | ||||||||||||||||||||

| redemption fees (Note 2) | 0.00 | 1 | 0.00 | 1 | 0.00 | 1 | — | — | ||||||||||||

| Net asset value, end of year | $ | 10.57 | $ | 11.90 | $ | 8.61 | $ | 8.32 | $ | 10.52 | ||||||||||

| Total return | (6.58 | )% | 38.21 | % | 7.55 | % | (19.82 | )% | 5.20 | % | ||||||||||

| SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, | ||||||||||||||||||||

| end of year (thousands) | $ | 199,968 | $ | 127,357 | $ | 66,648 | $ | 27,595 | $ | 32,058 | ||||||||||

| Portfolio turnover rate | 42 | % | 54 | % | 45 | % | 94 | % | 77 | % | ||||||||||

The accompanying notes are an integral part of these financial statements.

30

Evermore Global Value Fund

| FINANCIAL HIGHLIGHTS For a capital share outstanding throughout the year, Continued |

CLASS I

| Year Ended December 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010* | ||||||||||||||||

| RATIO OF EXPENSES TO AVERAGE NET ASSETS | ||||||||||||||||||||

Before expenses absorbed2,6 | 1.35 | % | 1.56 | % | 1.88 | % | 2.01 | % | 3.23 | % | ||||||||||

After expenses absorbed3,6 | — | 1.37 | % | 1.36 | % | 1.46 | % | 1.37 | % | |||||||||||

After expenses recouped3,6 | 1.36 | % | — | — | — | — | ||||||||||||||

| RATIO OF NET INVESTMENT INCOME (LOSS) TO AVERAGE NET ASSETS | ||||||||||||||||||||

Before expenses absorbed4,6 | (0.33 | )% | 0.34 | % | 3.32 | %7 | 1.14 | % | (1.30 | )% | ||||||||||

After expenses absorbed5,6 | — | 0.53 | % | 3.84 | %7 | 1.69 | % | 0.56 | % | |||||||||||

After expenses recouped5,6 | (0.34 | )% | — | — | — | — | ||||||||||||||

| * | Fund commenced operations on January 1, 2010. |

| ** | Calculated using the average shares outstanding method. |

| 1 | Amount less than $0.01. |

| 2 | The ratio of expenses to average net assets before expenses absorbed includes interest expense. The ratio excluding interest expense was 1.34% for the year ended December 31, 2014; and 1.54%, 1.87%, 1.90% and 3.21% for the years ended December 31, 2013, 2012, 2011 and 2010, respectively. |

| 3 | The ratio of expenses to average net assets after expenses absorbed/recouped includes interest expense. The ratio excluding interest expense was 1.35% for the year ended December 31, 2014; and 1.35%, 1.35%, 1.35% and 1.35% for the years ended December 31, 2013, 2012, 2011 and 2010, respectively. |

| 4 | The ratio of net investment income (loss) to average net assets before expenses absorbed includes interest expense. The ratio excluding interest expense was (0.32)% for the year ended December 31, 2014; and 0.36%, 3.33%, 1.25% and (1.28)% for the years ending December 31, 2013, 2012, 2011 and 2010, respectively. |

| 5 | The ratio of net investment income to average net assets after expenses absorbed/recouped includes interest expense. The ratio excluding interest expense was (0.33)% for the year ended December 31, 2014; and 0.55%, 3.85%, 1.80% and 0.58% for the years ending December 31, 2013, 2012, 2011 and 2010, respectively. |

| 6 | Does not include expenses of the investment companies in which the Fund invests. |

| 7 | Certain prior period ratios have been corrected. |

The accompanying notes are an integral part of these financial statements.

31

Evermore Global Value Fund

| NOTES TO FINANCIAL STATEMENTS December 31, 2014 |

| NOTE 1 – ORGANIZATION |

The Evermore Global Value Fund (the “Fund”) is a series of shares of Evermore Fund Trust (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “1940 Act”) as an open-end management investment company. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies.” The Fund commenced operations on January 1, 2010.

The investment objective of the Fund is to seek capital appreciation by investing in securities from markets around the world, including U.S. markets.

The Fund offers Class A and Class I shares. Class A shares are sold with a front-end sales charge. Each class of shares has equal rights as to earnings and assets except that each class bears different distribution expenses. Each class of shares has exclusive voting rights with respect to matters that affect just that class. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets. Class A shares are sold with a front-end sales charge of 5.00%. Purchases greater than $1 million into the Fund are offered at net asset value and subject to a 0.75% contingent deferred sales charge (“CDSC”) if redeemed within 12 months. Class I shares have no sales charge and are offered primarily for direct investment by investors such as pension and profit sharing plans, employee benefit trusts, certain financial intermediaries, endowments, foundations and corporations. For Class I shares, the offering and redemption price per share for the Fund is equal to the Fund’s net asset value per share. The Fund charges a 2.00% redemption fee on shares (both Class A and I) held less than 30 days.

| NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies consistently followed by the Fund. These policies are in conformity with accounting principles generally accepted in the United States of America.

| A. | Investment Valuation and Fair Value Measurement. All domestic equity securities that are traded on a national securities exchange, except those listed on the NASDAQ Global Market® (“NASDAQ”) are valued at the last reported sale price on the exchange on which the security is principally traded. Securities traded on NASDAQ will be valued at the NASDAQ Official Closing Price. If, on a particular day, an exchange-traded or NASDAQ security does not trade, then the mean between the most recent quoted bid and |

32

Evermore Global Value Fund

| NOTES TO FINANCIAL STATEMENTS December 31, 2014, Continued |

asked prices will be used. All equity securities that are not traded on a listed exchange are valued at the last sale price in the over-the-counter market. If a non-exchange traded security does not trade on a particular day, then the mean between the last quoted closing bid and asked price will be used.

Debt securities exceeding 60 days to maturity are valued by using the mean between the closing bid and asked prices provided by an independent pricing service. If the closing bid and ask prices are not readily available, the pricing service provides a price determined utilizing independent quotations from bond dealers and bond market activity or by a matrix pricing method, which is a formula driven valuation technique. The formula driven techniques generally consider such factors as yields or prices of bonds of comparable quality, type of issue, coupon, ratings, and general market conditions. Securities for which prices are not available from an independent pricing service, but where an active market exists, are valued using market quotations obtained from one or more dealers that make markets in the securities. Debt securities having a maturity of less than 60 days are valued at amortized cost with any discount or premium being accreted or amortized on a straight-line basis until maturity.

The Fund invests substantially in securities traded on foreign exchanges (see “Foreign Currency Translation” below). Investments that are primarily traded on foreign exchanges are generally valued in their local currencies as of the close of their primary exchange or market, or if there were no transactions on such day, at the mean between the bid and asked prices. The local prices are converted to U.S. dollars using the applicable currency exchange rates as of the close of the New York Stock Exchange. Exchange rates are provided daily by recognized independent pricing agents. Foreign currency forward contracts are valued at the current day’s interpolated foreign exchange rate, as calculated using the current day’s exchange rate, and the relevant forward rates provided by an independent pricing service.

There may be less publicly available information about a foreign company than about a U.S. company. Foreign issuers may not be subject to accounting, auditing and financial reporting standards and requirements comparable to, or as uniform as, those of U.S. issuers. The number of securities traded, and the frequency of such trading, in non-U.S. securities markets, while growing in volume, is for the most part, substantially less in U.S. markets. As a result, securities of many foreign issuers may be less liquid and their prices more volatile than securities of comparable U.S. issues. Transaction costs, the costs associated with buying and selling securities, in non-U.S. securities markets may be higher than in the U.S. securities markets. There is generally less

33

Evermore Global Value Fund

| NOTES TO FINANCIAL STATEMENTS December 31, 2014, Continued |

government supervision and regulation of exchanges, brokers and issuers than there is in the U.S. The Fund’s foreign investments may include both voting and non-voting securities, sovereign debt and participations in foreign government deals. The Fund may have greater difficulty taking appropriate legal action with respect to foreign issuers in U.S. courts.

For foreign securities traded on foreign exchanges, the Trust has selected Interactive Data’s Fair Value Information Services (“FVIS”) to provide pricing data with respect to foreign security holdings held by the Fund. The use of this third-party pricing service is designed to capture events occurring after a foreign exchange closes that may affect the value of certain holdings of the Fund’s securities traded on those foreign exchanges. The Fund utilizes a confidence level when determining the use of the FVIS prices. The confidence level is a measure of the historical relationship that each foreign exchange traded security has to movements in various indices and the price of the security’s corresponding American Depositary Receipt, if one exists. FVIS provides the confidence level for each security for which it provides a price. If the FVIS provided price falls within the confidence interval the Fund will value the particular security at that price. If the FVIS provided price does not fall within the confidence level the particular security will be valued at the preceding closing price on its respective foreign exchange, or if there were no transactions on such day, at the mean between the bid and asked prices.

Securities for which quotations are not readily available are valued at their respective fair values as determined in good faith by the Board of Trustees. When a security is “fair valued,” consideration is given to the facts and circumstances relevant to the particular situation, including a review of various factors set forth in the pricing procedures adopted by the Fund’s Board of Trustees. Fair value pricing is an inherently subjective process, and no single standard exists for determining fair value. Different funds could reasonably arrive at different values for the same security. The use of fair value pricing by a fund may cause the net asset value of its shares to differ from the net asset value that would be calculated without regard to such considerations.

As described above, the Fund utilizes various methods to measure the fair value of its investments on a recurring basis. U.S. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

| Level 1 – | Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. These types of assets generally included in this category are equities listed in active markets. | |

| Level 2 – | Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. |

34

Evermore Global Value Fund

| NOTES TO FINANCIAL STATEMENTS December 31, 2014, Continued |

| These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. The types of assets generally included in this category are bonds and financial instruments classified as derivatives. | ||