UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number (811-22335)

Evermore Funds Trust

(Exact name of registrant as specified in charter)

89 Summit Avenue

Summit, New Jersey 07901

(Address of principal executive offices) (Zip code)

Eric LeGoff

89 Summit Ave, 3rd Floor

Summit, New Jersey 07901

(Name and address of agent for service)

(866) 383-7667

Registrant’s telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2011

Item 1. Reports to Stockholders.

Elements of Our Active Value Investment Approach

At Evermore Global Advisors, LLC, we employ an active value approach to investing. We seek to leverage our deep operating and investing experience and extensive global relationships to identify and invest in great companies around the world that have compelling valuations and are undergoing strategic changes which we believe will unlock value.

|

|

Seeking to Generate Value . . . | |

|

|

• | Catalyst-Driven Investing. We do more than pick cheap stocks and hope for their prices to rise. We invest in companies where a series of catalysts exist to unlock value. The catalysts we look for reflect strategic changes in the company’s management, operations or financial structure that are already underway. They are not broadly recognized, but we believe they are likely to have a significant impact on a stock’s performance over time. |

|

|

Supporting Our Active Value Orientation . . . | |

|

|

• | Original Fact-Based Research. We conduct our own, original fact-based research to validate management’s stated objectives and identify catalysts to unlock value. We also perform detailed business segment analysis on each company we research. |

|

|

• | Business Operating Experience. Our senior team has hands-on business operating experience; including starting and managing businesses, sitting on company boards, and assisting management of multi-national corporations restructure their businesses. We rely on this experience to better evaluate investment opportunities. |

|

|

• | A Global Network of Strategic Relationships. Over the past 20 years, members of our investment team have developed an extensive global network of strategic relationships, including individuals and families that control businesses, corporate board members, corporate management, regional brokerage firms, press contacts, etc. We leverage these relationships to help generate and better evaluate investment opportunities. |

|

|

• | Taking a Private Equity Approach to Public Equity Investing. When we are interested in an investment opportunity, we get to know the management team of the company, study the company’s business model, evaluate the competitive and regulatory environment, and test and crosscheck what the management team tells us against our own experience. |

|

|

• | Always Active, Sometimes Activist. We are always engaged with the companies in which we invest to ensure management teams follow through on their commitments to change. On limited occasions, when we are not satisfied with |

|

|

| 1 |

|

|

| the efforts of management, we may play an activist role working with other shareholders to facilitate change. |

|

|

Executing Our Approach . . . | |

|

|

• | Targeting Complex Investment Opportunities. We love looking at holding companies and conglomerates that are often under-researched and/or misunderstood. |

|

|

• | Investing Across the Capital Structure. We evaluate all parts of a company’s capital structure to determine where the best risk-adjusted return potential exists. At times, we may invest in multiple parts of a company’s capital structure (e.g., investing in both a company’s debt and equity). |

|

|

• | Investing in Merger Arbitrage and Distressed Situations. We look to take advantage of announced merger and acquisition deals where an attractive spread exists between the market price and the announced deal price for the target company. We also look for opportunities in distressed companies that have filed or may file for bankruptcy, or are involved in reorganizations or financial restructurings. |

|

|

• | Exploiting Short Selling Opportunities. We will seek to take advantage of short selling opportunities to address currency, security, sector and market risk. |

|

|

• | Tactically Managing Cash Levels. We are not afraid to hold significant cash positions when it makes sense for the portfolios. |

|

|

2 |

|

A Letter from the CEO

Dear Shareholder:

Last year proved to be quite challenging for global and European investors, as the tragic events in Japan, Middle East unrest, the European Debt Crisis, and the U.S. debt ceiling debate coupled with an S&P downgrade collectively caused unprecedented volatility in global markets in the second and third quarters. The Evermore Funds were adversely impacted by these events from a short-term investment performance standpoint, especially as a result of our high concentration of European (and Euro Crisis Zone) special situation investments. Throughout this turbulent period, our investment team continued to maintain its conviction in our portfolio holdings and took advantage of depressed valuations to add to existing positions and start new ones. The fourth quarter brought some semblance of normalcy back to the global markets, as European leaders began focusing more seriously to come up with solutions for the European debt crisis. During the quarter, we saw a series of catalysts begin to unfold across our portfolio, which validated our continued conviction in our holdings, and brought positive investment performance results.

Market events in 2011 led us to the difficult decision to close the Evermore European Value Fund and focus our mutual fund efforts on the flagship Evermore Global Value Fund. The European Value Fund liquidated as of January 31, 2012. As such, the discussion in David Marcus’ Portfolio Manager Letter will focus on the Evermore Global Value Fund, which in 2011 also happened to own every position that was held in the Evermore European Value Fund.

Despite the market turmoil in 2011, as I look back at our second year in business, I see an organization with a stronger team and great partners. We are very pleased to have Nathan Gantcher join us as Chairman of our Fund Board of Trustees. Mr. Gantcher has tremendous Board and corporate governance experience having served as vice chairman of CIBC Oppenheimer and as a member of many public and private company boards. On the investment team front, we brought in a new research analyst, Thomas O, who has both private equity and deep value investing experience primarily in the U.S. and Asia. On the sales and distribution front, Adam Ermanis joined us as Institutional Sales Director. Adam has spent 10 years in a variety of senior sales roles at two large deep value, special situations focused asset management firms.

We continue to be extremely appreciative of the efforts of our employees, Board of Trustees and advisors. As I stated in last year’s letter, having the right partners is also key to the success of our business. I would like to thank the following service

|

|

| 3 |

providers for their support over the past year: U.S. Bank Fund Services, LLC (Fund administrator, accountant, transfer agent), U.S. Bank N.A. (Fund custodian), Quasar Distributors LLC (Fund distributor), Drinker Biddle & Reath LLP (Fund counsel), Cipperman & Company (counsel to the Fund’s independent Trustees), Ernst & Young LLP (Fund auditor), Alaric Compliance Services, LLC, Tiller, LLC (marketing communications), JCPR, Inc. (public relations and marketing), Eze Castle Software (order management system provider), Advent Software (portfolio management software provider), and all of our executing brokers.

Eric LeGoff

CEO, Evermore Funds Trust

|

|

4 |

|

A Letter from the Portfolio Manager

|

A pessimist sees the difficulty in every opportunity; an optimist sees the opportunity in every difficulty. |

-Winston Churchill |

Dear Shareholder:

Fund performance in 2011 was disappointing. The Evermore Global Value Fund’s Institutional Shares ended down 19.82% for the one year period ended December 31, 2011. The year started off well for the Fund with significant gains across the portfolio during the first quarter. However, panic across the world, and especially in Europe, during the second and third quarters significantly impacted our largest holdings. This was the case even though there was little company specific news on our names. Unfortunately, fear and panic was not contained to Europe alone—there was much concern and uncertainty concerning U.S. economic growth, the slowing of the Chinese economy, the crisis in the Mid-East, etc. We continue to stay laser focused and sift through all the news, the noise, and the stress to find those opportunities that are below the radar, misunderstood, mispriced and offer the potential for substantial rewards relative to the risk inherent in these investments.

Last year was a year where real value was actually created in a variety of the Funds’ holdings. Because of the market turmoil, this value was not reflected in those holdings respective stock prices. Sevan Drilling’s first deepwater rig started production and the construction of their second rig progressed according to plan. Retail Holdings continued its ongoing liquidation with a significant cash distribution. Old Mutual plc and Orkla both accelerated their transformations and are refocusing on core operations. Our largest holding, Grupo Prisa spent the bulk of the year rightsizing operations and working to restructure its levered balance sheet. This is just a sampling of what was taking place within our portfolio. We firmly believe these transformative moves are value accretive to the intrinsic value of these securities, yet regardless of catalysts at work, most of them were down significantly in the second and third quarters. Investors were in sheer panic mode and it seemed that any news in our names was perceived as bad news.

However, after two quarters that were marked by fear and panic in the global markets, the fourth quarter began to show some signs of relief. Investors started taking their heads out of the sand and catalysts began to be recognized by the market.

We continue to own many of the securities in the portfolio that we originally bought during 2010, our first year in business. As I have said in the past, we are long term investors and our investments often take time to come to fruition. While we are not happy having to report being down as much as we were during the year, we are very

|

|

| 5 |

happy that we took advantage of the carnage and panic to average down our cost in certain existing positions and initiate new positions where the indiscriminate selling created compelling buying opportunities. Can a 50 cent dollar go to 40 or even 30 cents on the dollar? Of course it can, and in 2011 it did in many cases. But, our strategy focuses on buying cheap stocks with catalysts and, in the long run, we are true believers that these catalysts should cause these securities to trade closer to their intrinsic values.

European leaders inched closer to getting their acts together to address the European debt crisis, and although things remain far from resolved, the market has gotten somewhat more comfortable that Europe is on a path towards an acceptable resolution.

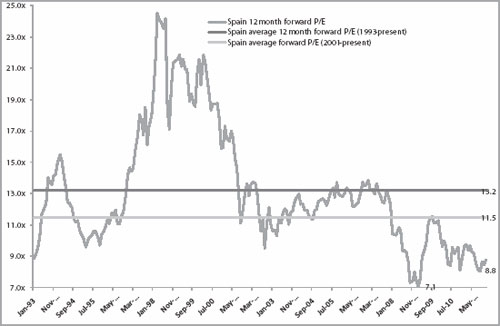

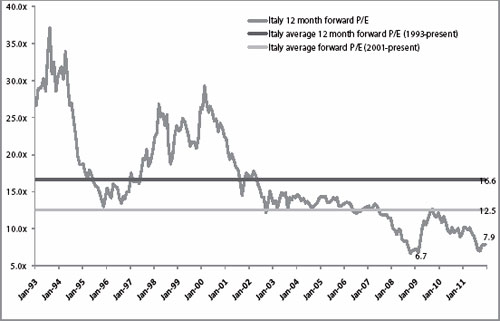

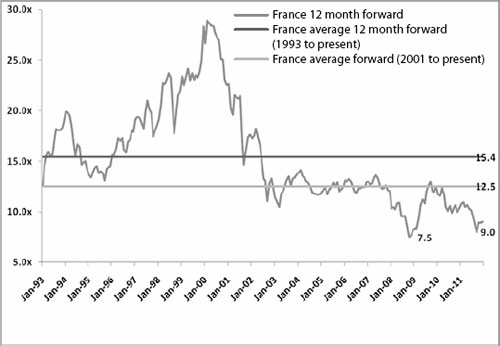

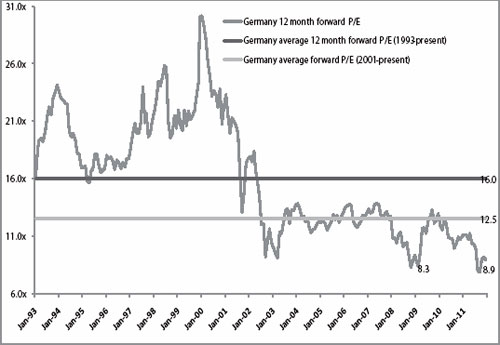

In our Q3 update, we discussed how cheap the European markets had gotten. Below we have updated data points for 4 European markets through 12/31/11 to show that Europe remains extremely cheap in a historical context. We remind you that we do not buy markets, we buy companies. However, when entire markets sell off and trade at depressed levels we find more of our type of mispriced securities.

Spain

|

|

6 |

|

Italy

France

|

|

| 7 |

Germany

Source: MSCI, IBES, Datastream, Morgan Stanley Research

Let’s now review several of our key positions where catalysts were at work during 2011:

Grupo Prisa (Bloomberg Symbols: PRIS/B and J0003 SM). Prisa is a Spanish media conglomerate with pay TV, newspaper, radio stations, and education businesses in Spanish speaking countries around the world. We continue to own Prisa B Preferred shares, which trade on the NYSE, and Prisa warrants, which trade on the Madrid Stock Exchange. The Prisa B shares are scheduled to pay an annual dividend of between $0.90 and $1.00 for the next three years. At its year-end share price, that represented almost a 20% annual yield. In June of 2014, these shares mandatorily convert to an ordinary share. The Prisa warrants give us the option to buy Prisa ordinary shares at 2 Euros per share until June of 2014.

The equity is trading between 4 and 5 times depressed cash flows, mostly because of the company’s exposure to Spain, its focus on media businesses, and its debt load. At the end of 2011, the company pushed out the maturity of most of its bank debt from 2012 to 2014/2015. This provides an important first step to lowering the debt load via noncore asset sales and organic cash flows, and replacing bank debt with public debt.

The Polanco family, which owns 20% of the company, and two other investors/ board members collectively, recently injected €150 million of equity in the company at €2 per share, which is 150% higher than the current stock price. Practically, this action helped close the refinancing, but it also signaled long term confidence in the business from Prisa’s most vested, informed, long term investors. Finally, a professional CFO (who is the CEO in waiting) was hired in 2011 and he is focusing on

|

|

8 |

|

aggressively managing the existing businesses and optimizing their portfolio of assets. In 2011, the company laid off 18% of its workforce, which were the first layoffs in the company’s history.

Sevan Drilling ASA (Bloomberg Symbol: SEVDR NO). Sevan Drilling is a Nor-we gian oil drilling company. This special situation was created because of a botched IPO of Sevan Drilling by its former parent company, Sevan Marine. At its current trading level, the market is implying a value for the company’s existing rig fleet, which is brand new and includes two additional rigs that are being built, at $500 million per rig. As a point of reference, in 2011, Transocean (RIG) bought very similar assets from Aker Drilling at close to $700 million per rig. New building rig prices are in the mid $600 million per rig range.

In December 2011, Seadrill (Bloomberg Symbol: SDRL), a company controlled by John Fredrikson, the richest man in Norway who controls a vast empire of oil & gas transport and drilling businesses, bought a 28% stake in Sevan Drilling. New board members and a management team heavily incentivized by a robust options package have been put in place, making the sale of the company to Seadrill or another bidder in the next eighteen months likely.

EI Towers S.p.A. (Bloomberg Symbol: EIT IM). EI Towers is an Italian company that owns and operates broadcast and telecommunications towers in Italy. Our original position, Digital Multimedia Technologies (Bloomberg Symbol: DMT IM), merged in December with the tower infrastructure business of MediaSet, forming the largest tower infrastructure company in Italy. The merger ratio was determined by pricing the DMT equity at €28 per share. Assuming minimal synergies from the merger (which could end up being substantial), the current price of EI Towers values the combined company at a very attractive valuation. Additional catalysts that we believe should unlock value in the coming years include stripping out overlapping costs from the legacy companies and the entrance of new competitors to the Italian television market, which should meaningfully increase the size of the customer base.

Orkla ASA (Bloomberg Symbol: ORK NO). Orkla is a Norwegian conglomerate with consumer goods, energy, aluminum and financial businesses. Based on our conservative sum of the parts valuation, Orkla trades at a 35% discount to its intrinsic value. The company is undertaking an initiative to divest noncore assets and focus their business as a branded consumer company. Currently, they are the incumbent market leader for consumer goods in the Nordic region and other select markets including Russia, Austria, and India. In November, the company announced the sale of its Bakers business to another Norwegian company. Orkla has been paying shareholders special dividends as assets are sold. In addition, investors have been paid to wait for this transformation to take place in the form of a 5% annual dividend that has been funded from ongoing operations.

ModusLink Global Solutions (Bloomberg Symbol: MLNK). ModusLink is an undermanaged, overcapitalized logistics company that is the subject of an activist

|

|

| 9 |

campaign that is aimed at replacing management and pursuing strategic alternatives for the company. The company currently has a market cap of $250 million, about $120 million in excess cash, over $2 billion of net operating loss carry forwards, and trades at an EV/EBITDA multiple of about 6 times. We believe that this company will likely be sold, or broken up in parts, within 18 months. There are a group of activists vying for control of this company so the status quo remaining is very unlikely. Last year, the company was approached with a bid in the $9 range (stock currently trades at about $5.65). While we don’t think we will see a bid in that range, we think a transaction between $7 and $8 per share could be possible.

Frontline 4.5% 2014 Convertible Bond. Our position in the 2014 Frontline convertible bond provides a 9% current yield and a 30% yield to maturity while being covered by a fairly robust, liquid asset base. In late 2011, Frontline restructured itself by selling certain vessels and new building commitments and reworking leases on existing tankers. The result was a substantially lower fixed cost base for the convertible bond holders. In our estimation, there is ample asset coverage in terms of tanker values, even in weaker than current markets, to help hedge our investment. The most likely catalyst that will cause this bond to trade to par is the accretion toward maturity. Beyond that, we hold a free option that the operating environment for tankers improves, in which case the bond should trade higher before 2014. In the meantime, we will collect our yield and grind up to par.

SeaCo Ltd. (Bloomberg Symbol: SEAOF). SeaCo owned a large container fleet. In December 2011, the company announced that it closed the sale of its container leasing business to China’s HNA Group Company Ltd. and Hong Kong’s Bravia Capital for approximately $528 million. That equated to approximately $0.64 per share. SeaCo announced that it would pay out $0.65 per share in early 2012 and additional amounts in eighteen months as the company completes it liquidation. We decided to exit the position in December when the stock traded above the first payout level. There may be further opportunities to participate in the final wind down of SeaCo over the next eighteen months.

|

|

|

| And it comes from saying no to 1,000 things to make sure we don’t get on the wrong track or try to do too much. We’re always thinking about new markets we could enter, but it’s only by saying no that you can concentrate on the things that are really important. |

|

| -Steve Jobs |

|

A Look Ahead

We do not take the crisis in Europe lightly – it is real and the outcome is yet to be determined. That said, we strongly believe that some of the best opportunities globally can be found in Europe and here in the U.S. This is why European and U.S. securities represent the largest regional concentrations in our portfolio. We live a nomadic lifestyle as investors. Our investment style allows us to go anywhere, but we

|

|

10 |

|

don’t have to. We move to where we see value and opportunity and when that plays out we move to new areas.

We believe it is important to say “NO” often. As Steve Jobs said in the quote above, we believe it is important to be focused. This comes not by looking at everything in the global stock universe. Rather, it comes by looking for the attributes that must be present for an investment to be considered for the Fund. “NO” is the first thought. Investments must prove that “YES” is the right answer. Something that is just “OK” is never good enough. We must be convinced that real value and the ability to unlock it are inherent in the opportunity. Period. No excuses. No falling in love with positions.

As we head into 2012, we remain excited about our portfolio, but also very mindful of the Eurozone crisis and its potential impact on global markets. So, how do we prepare ourselves for troubled times yet seek to prosper if things are not so bad? By continuing to strictly adhere to our investment approach, which includes:

|

|

– | Buying stocks and other securities with what we feel is a significant “margin of safety” |

|

|

– | Focusing on special situations where there are catalysts present, so we are not relying on the broader market moves for value creation |

|

|

– | Maintaining reasonable cash levels to try to take advantage of opportunistic situations where positions we own (or are evaluating) sell off for reasons that we believe are short term or market driven but, do not cut the intrinsic value of the underlying investment |

|

|

– | Maintaining currency, market and/or security hedges |

Our commitment to you is that we will continue to be true to our approach through good and bad times. We believe this approach should translate to superior long-term investment returns for our shareholders. We once again thank you for your continued confidence and support.

Sincerely,

David Marcus

Portfolio Manager

|

|

| 11 |

Management’s Discussion of Fund Performance

As was discussed in the CEO and Portfolio Manager letters to shareholders, 2011 was a difficult year for the Evermore Global Value Fund and Evermore European Value Fund (the “Evermore Funds” or “Funds”). The year started strong for both Funds, but as crisis after crisis arose across the globe in the second and third quarters, many of the Fund’s portfolio holdings got battered. The fourth quarter brought a significant reduction in market volatility as European leaders got more serious about providing long term solutions to the European debt crisis. The Funds’ investment performance also moved in a positive direction in the fourth quarter, as a number of catalysts began to unfold across the portfolios.

Disappointing investment performance in 2011 can be largely attributed to the fact that both of the Funds had a high level of concentration in European securities, and especially in Spain and Italy, which were at the heart of the Eurozone crisis. We continue to maintain a high level of conviction in these European holdings, as well as our holdings in other regions.

Evermore Global Value Fund

For the year ended December 31, 2011, the Evermore Global Value Fund’s Class I shares were down 19.82%. The MSCI All-Country World Index was down 7.35% during the same period. The biggest detractors to performance in 2011 were Prisa Warrants, Prisa Class B Convertible Preferred ADR, Sino Forest, Balda AG, and Eniro AB. The biggest contributors to performance for the year were: SeaCo Ltd., Retail Holdings NV, Prisa Class A ADR, Charter Communications Inc., and Swedish Match AB.

As a result of the volatility in the markets in the second and third quarters of 2011, we added to our market and security hedges by shorting and buying put options on a number of European banks and industrial companies in the third quarter, which contributed to performance during this extremely volatile period.

As of December 31, 2011, our largest five positions were Prisa Class B Convertible Preferred ADR, Justice Holdings Ltd., American International Group 5/22/2038, 8.625% Bond, ModusLink Global Solutions Inc., and EI Towers S.p.A. The Fund’s cash position stood at 9.2%, which included other assets in excess of liabilities.

Evermore European Value Fund

The Evermore Funds’ Board of Trustees approved a plan of liquidation for the Evermore European Value Fund on December 16, 2011. As a result, the Fund began an orderly disposition of its holdings during the following week and the Fund was left with just a few positions as of year-end. For the year ended December 31, 2011, the Evermore European Value Fund’s Class I shares were down 24.45%. The MSCI Daily Total Return Net Europe Local Index was down 11.06% during the same period.

|

|

12 |

|

The biggest detractors to performance in 2011 were Prisa Class B Convertible Preferred ADR, Eniro AB, Balda AG, RHJ International, and Prisa Warrants. The biggest contributors to performance for the year were: Prisa Class A ADR, Siemens AG, Swedish Match AB, Sevan Drilling ASA, and Schibsted ASA.

As a result of the volatility in the markets in the second and third quarters of 2011, we added to our market and security hedges by shorting and buying put options on a number of European banks and industrial companies in the third quarter, which contributed to performance during this extremely volatile period.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

Past performance does not guarantee future results. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

Mutual fund investing involves risk. Principal loss is possible. The Funds invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. Investing in smaller companies involves additional risks such as limited liquidity and greater volatility. The Funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually grater for longer-term debt securities. Investment in lower-rated, non-rated and distressed securities presents a greater risk of loss to principal and interest than higher-rated securities. Additional special risks relevant to our Funds involve derivatives and hedging. Please refer to the prospectus for further details.

The Evermore European Value Fund concentrates its investments in a single region, which may subject it to greater risk and volatility than a broadly diversified fund.

Please refer to the Schedules of Investments for complete holdings information. Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

The MSCI All-Country World Index is an unmanaged index comprised of 48 country indices, including 23 developed and 25 emerging market country indices, and is calculated with dividends reinvested after deduction of holding tax. The index is a trademark of Morgan Stanley Capital International and is not available for direct investment. The MSCI Daily Total Return Net Europe Local Index is a free float adjusted market capitalization weighted index comprised of 16 European developed market indices and reinvests dividends after deduction of withholding tax on the days securities are quoted ex-dividend. The index is a trademark of Morgan Stanley Capital International and is not available for direct investment.

|

|

| 13 |

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income. Free cash flow is revenue less operating expenses including interest expense and maintenance capital spending. It is the discretionary cash that a company has after all expenses and is available for purposes such as dividend payments, investing back into the business or share repurchases.

Forward P/E is a measure of price-to earnings ratio (P/E) using forecasted earnings for the P/E calculation. While the earnings used are just an estimate and are not as reliable as current earnings data, there is still benefit in estimated P/E analysis. The forecasted earnings used in the formula can either be for the next 12 months or for the next full-year fiscal period.

EV/EBITDA (Enterprise Value/EBITDA) is a valuation multiple used in finance and investment to measure the value of a company. This important multiple is often used in conjunction with, or as an alternative to, the P/E ratio (Price/Earnings ratio) to determine the fair market value of a company.

Must be preceded or accompanied by a prospectus.

The Evermore Funds are distributed by Quasar Distributors, LLC.

|

|

14 |

|

|

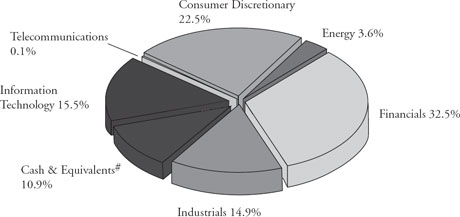

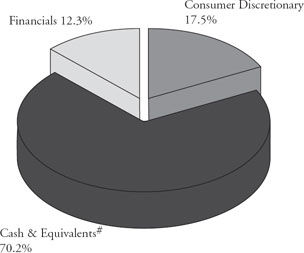

SECTOR ALLOCATION* at December 31, 2011 (Unaudited) |

Evermore Global Value Fund

(Allocations based on total net assets)

Evermore European Value Fund

(Allocations based on total net assets)

|

|

* | Includes long common stocks and options. |

# | Cash equivalents and other assets less liabilities. |

|

|

| 15 |

Evermore Funds

|

EXPENSE EXAMPLE for the Six Months Ended December 31, 2011 (Unaudited) |

As a shareholder of the Evermore European Value Fund or the Evermore Global Value Fund (each a “Fund” and collectively the “Funds”), you incur two types of costs: (1) transaction costs, including sales charges or loads; and (2) ongoing costs, including investment advisory fees, distribution fees, and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (7/1/11 - 12/31/11).

Actual Expenses

The first line of the table on the next page provides information about actual account values based on actual returns and actual expenses. You will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds’ transfer agent. If you request a redemption be made by wire transfer, currently a $15.00 fee is charged by the Funds’ transfer agent. You will be charged a redemption fee equal to 2% of the net amount of the redemption if you redeem shares less than 30 calendar days after you purchase them. An Individual Retirement Account (“IRA”) will be charged a $15.00 annual maintenance fee. To the extent the Funds invest in shares of other investment companies as part of its investment strategy, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Funds invest in addition to the expenses of the Funds. Actual expenses of the underlying funds may vary. These expenses are not included in the example below. The example below includes, but is not limited to, investment advisory fees, shareholder servicing fees, fund accounting fees, custody fees and transfer agent fees. However, the example below does not include portfolio trading commissions and related expenses, and other extraordinary expenses as determined under generally accepted accounting principles. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds’ actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

|

|

16 |

|

Evermore Funds

|

EXPENSE EXAMPLE for the Six Months Ended December 31, 2011 (Unaudited), continued |

Evermore Global Value Fund

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Beginning |

| Ending |

| Expenses Paid |

| ||||||

|

|

|

|

| |||||||||

Class A Actual^ |

| $ | 1,000 |

|

| $ | 808 |

|

| $ | 8.20 |

|

|

Class A Hypothetical (5% annual return before expenses)+ |

| $ | 1,000 |

|

| $ | 1,016 |

|

| $ | 9.15 |

|

|

Class C Actual^ |

| $ | 1,000 |

|

| $ | 804 |

|

| $ | 11.59 |

|

|

Class C Hypothetical (5% annual return before expenses)+ |

| $ | 1,000 |

|

| $ | 1,012 |

|

| $ | 12.93 |

|

|

Class I Actual^ |

| $ | 1,000 |

|

| $ | 807 |

|

| $ | 7.06 |

|

|

Class I Hypothetical (5% annual return before expenses)+ |

| $ | 1,000 |

|

| $ | 1,017 |

|

| $ | 7.88 |

|

|

|

|

^ | Excluding interest expense and dividend expense on securities sold short, your actual cost of investments in the Fund would be $7.29 for Class A shares, $10.68 for Class C shares and $6.15 for Class I shares. |

+ | Excluding interest expense and dividend expense on securities sold short, your hypothetical cost of investment in a fund would be $8.13 for Class A shares, $11.93 for Class C shares and $6.87 for Class I shares. |

* | Expenses are equal to the Fund’s expense ratios for the most recent six-month period, including interest expense and dividend expense on securities sold short, of 1.80% for Class A shares, 2.55% for Class C shares and 1.55% for Class I shares multiplied by the average account value over the period multiplied by 184/365 (to reflect the one-half year period). If interest expense and dividends on securities sold short was excluded, the annualized ratio would have been 1.60% for Class A shares, 2.35% for Class C shares and 1.35% for Class I shares. Expense ratios reflect fee waivers currently in effect. |

Evermore European Value Fund

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Beginning |

| Ending |

| Expenses Paid |

| ||||||

|

|

|

|

| |||||||||

Class A Actual^ |

| $ | 1,000 |

|

| $ | 764 |

|

| $ | 7.96 |

|

|

Class A Hypothetical (5% annual return before expenses)+ |

| $ | 1,000 |

|

| $ | 1,016 |

|

| $ | 9.10 |

|

|

Class I Actual^ |

| $ | 1,000 |

|

| $ | 764 |

|

| $ | 6.85 |

|

|

Class I Hypothetical (5% annual return before expenses)+ |

| $ | 1,000 |

|

| $ | 1,017 |

|

| $ | 7.83 |

|

|

|

|

^ | Excluding interest expense and dividend expense on securities sold short, your actual cost of investments in the Fund would be $7.11 for Class A shares and $6.00 for Class I shares. |

+ | Excluding interest expense and dividend expense on securities sold short, your hypothetical cost of investment in the Fund would be $8.13 for Class A shares and $6.87 for Class I shares. |

* | Expenses are equal to the Fund’s expense ratios for the most recent six-month period, including interest expense and dividend expense on securities sold short, of 1.79% for Class A shares and 1.54% for Class I shares multiplied by the average account value over the period multiplied by 184/365 (to reflect the one-half year period). If interest expense and dividends on securities sold short was excluded, the annualized ratio would have been 1.60% for Class A shares and 1.35% for Class I shares. Expense ratios reflect fee waivers currently in effect. |

|

|

| 17 |

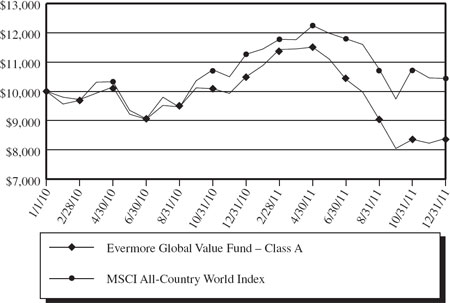

Evermore Global Value Fund

Value of $10,000 vs. MSCI All-Country World Index

|

|

|

|

|

|

|

|

|

| |

Total Returns |

|

| One Year |

| Since Inception |

| Value of |

| ||

|

|

|

|

| ||||||

Class A |

| (20.04)% |

| (8.37)% |

| $8,396 |

|

| ||

Class A (with sales charge) |

| (24.02)% |

| (10.71)% |

| $7,973 |

|

| ||

Clsss C |

| (20.56)% |

| (9.11)% |

| $8,262 |

|

| ||

Class C (with sales charge) |

| (21.35)% |

| (9.11)%* |

| $8,262 |

|

| ||

Class I |

| (19.82)% |

| (8.16)% |

| $8,435 |

|

| ||

MSCI All-Country World Index |

| (7.35)% |

| 2.17% |

| $10,439 |

|

| ||

|

|

* | Sales charges for Class C are not applicable if shares not sold within one year. |

The above graph and table illustrates the performance of a hypothetical $10,000 investment made on January 1, 2010, and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns reflect fee waivers in effect. In the absence of such waivers, total return would be reduced. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for an index.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 866-EVERMORE or (866) 383-7667.

The Fund imposes a 2.00% redemption fee on shares redeemed within 30 days. Performance does not reflect the redemption fee. If reflected, total returns would be reduced.

|

|

18 |

|

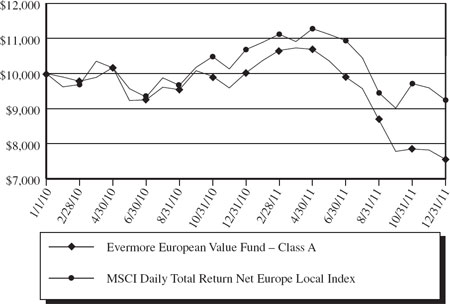

Evermore European Value Fund

Value of $10,000 vs. MSCI Daily Total Return Net Europe Local Index

|

|

|

|

|

|

|

|

|

| |

Total Returns |

|

| One Year |

| Since Inception |

| Value of |

| ||

|

|

|

|

| ||||||

Class A |

| (24.65)% |

| (13.11)% |

| $7,550 |

|

| ||

Class A (with sales charge) |

| (28.44)% |

| (15.31)% |

| $7,170 |

|

| ||

Class I |

| (24.63)% |

| (12.88)% |

| $7,590 |

|

| ||

MSCI Daily Total Return Net Europe Local Index |

| (11.06)% |

| (3.88)% |

| $9,239 |

|

| ||

The above graph and table illustrates the performance of a hypothetical $10,000 investment made on January 1, 2010, and is not intended to imply any future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns reflect fee waivers in effect. In the absence of such waivers, total return would be reduced. The chart assumes reinvestment of capital gains and dividends for a fund and dividends for an index.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 866-EVERMORE or (866) 383-7667.

The Fund imposes a 2.00% redemption fee on shares redeemed within 30 days. Performance does not reflect the redemption fee. If reflected, total returns would be reduced.

|

|

| 19 |

|

Evermore Global Value Fund |

|

SCHEDULE OF INVESTMENTS at December 31, 2011 |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

|

|

|

| ||

COMMON STOCKS – 61.6% |

|

|

| ||||

|

|

|

|

|

| ||

Aerospace & Defense – 0.2% |

|

|

|

| |||

| 8,600 |

| Exelis, Inc. |

|

|

|

|

|

|

| (United States) |

| $ | 77,830 |

|

|

|

|

|

|

| ||

Communications Equipment – 8.4% |

|

|

|

| |||

| 105,547 |

| Balda AG (Germany)* |

|

| 592,001 |

|

| 39,500 |

| Cisco Systems, Inc. |

|

|

|

|

|

|

| (United States) |

|

| 714,160 |

|

| 60,352 |

| Ei Towers SPA |

|

|

|

|

|

|

| (Italy)*1 |

|

| 1,466,199 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 2,772,360 |

|

|

|

|

|

|

| ||

Diversified Telecommunication |

|

|

|

| |||

| 43,800 |

| Sistema JSFC – ADR |

|

|

|

|

|

|

| (Russia)* |

|

| 736,278 |

|

|

|

|

|

|

| ||

Energy Equipment & Services – 3.6% |

|

|

|

| |||

| 1,391,419 |

| Sevan Drilling AS |

|

|

|

|

|

|

| (Norway)* |

|

| 1,178,908 |

|

|

|

|

|

|

| ||

Exploration & Production – 3.0% |

|

|

|

| |||

| 588,200 |

| Pulse Seismic, Inc. |

|

|

|

|

|

|

| (Canada)* |

|

| 1,010,405 |

|

|

|

|

|

|

| ||

Household Durables – 3.9% |

|

|

|

| |||

| 78,455 |

| Retail Holdings NV |

|

|

|

|

|

|

| (Netherlands)* |

|

| 1,278,817 |

|

|

|

|

|

|

| ||

Industrial Conglomerates – 9.8% |

|

|

|

| |||

| 35,800 |

| EXOR SPA (Italy) |

|

| 717,733 |

|

| 133,500 |

| Justice Holdings Ltd. |

|

|

|

|

|

|

| (United Kingdom)*1 |

|

| 1,782,985 |

|

| 99,520 |

| Orkla ASA (Norway) |

|

| 741,082 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 3,241,800 |

|

|

|

|

|

|

| ||

Insurance – 5.6% |

|

|

|

| |||

| 143,000 |

| Genworth Financial, |

|

|

|

|

|

|

| Inc. (United States)* |

|

| 936,650 |

|

| 428,202 |

| Old Mutual PLC |

|

|

|

|

|

|

| (United Kingdom) |

|

| 900,644 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 1,837,294 |

|

|

|

|

|

|

| ||

Internet Software & Services – 4.9% |

|

|

|

| |||

| 299,252 |

| ModusLink Global |

|

|

|

|

|

|

| Solutions, Inc. |

|

|

|

|

|

|

| (United States) |

|

| 1,615,961 |

|

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

|

|

|

| ||

Machinery – 3.1% |

|

|

|

|

| ||

| 86,320 |

| Fiat Industrial SPA |

|

|

|

|

|

|

| (Italy)*1 |

| $ | 735,395 |

|

| 4,300 |

| ITT Corp. |

|

|

|

|

|

|

| (United States) |

|

| 83,119 |

|

| 8,600 |

| Xylem, Inc. |

|

|

|

|

|

|

| (United States) |

|

| 220,934 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 1,039,448 |

|

|

|

|

|

|

| ||

Media – 12.0% |

|

|

|

|

| ||

| 468,213 |

| Constantin Medien |

|

|

|

|

|

|

| AG (Germany)* |

|

| 775,051 |

|

| 297,328 |

| Eniro AB (Sweden)* |

|

| 492,679 |

|

| 41,136 |

| Promotora de |

|

|

|

|

|

|

| Informaciones SA |

|

|

|

|

|

|

| (Spain)* |

|

| 46,126 |

|

| 549,904 |

| Promotora de |

|

|

|

|

|

|

| Informaciones SA – |

|

|

|

|

|

|

| Class B – ADR |

|

|

|

|

|

|

| (Spain)* |

|

| 2,661,536 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 3,975,392 |

|

|

|

|

|

|

| ||

Movies & Entertainment – 1.1% |

|

|

|

| |||

| 81,303 |

| Highlight |

|

|

|

|

|

|

| Communications AG |

|

|

|

|

|

|

| (Switzerland)* |

|

| 362,060 |

|

|

|

|

|

|

| ||

Shipping & Logistics – 3.4% |

|

|

|

| |||

| 5,757 |

| Bollore SA (France) |

|

| 1,128,521 |

|

|

|

|

|

|

| ||

Textiles, Apparel & Luxury |

|

|

|

| |||

Goods – 0.4% |

|

|

|

| |||

| 200 |

| J.G. Boswell Co. |

|

|

|

|

|

|

| (United States)* |

|

| 139,000 |

|

|

|

|

|

|

| ||

TOTAL COMMON STOCKS |

|

|

|

| |||

(Cost $25,445,007) |

|

| 20,394,074 |

| |||

|

|

|

|

|

| ||

|

|

|

|

| |||

PARTNERSHIPS & TRUSTS – 7.9% |

|

|

|

| |||

|

|

|

|

| |||

Real Estate Investment Trusts – 7.9% |

|

|

|

| |||

| 32,000 |

| American Capital |

|

|

|

|

|

|

| Agency Corp. |

|

|

|

|

|

|

| (United States)1 |

|

| 898,560 |

|

| 61,843 |

| General Growth |

|

|

|

|

|

|

| Properties, Inc. |

|

|

|

|

|

|

| (United States)1 |

|

| 928,883 |

|

The accompanying notes are an integral part of these financial statements.

|

|

20 |

|

|

Evermore Global Value Fund |

|

SCHEDULE OF INVESTMENTS at December 31, 2011 Continued |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

| |||||||

| 151,600 |

| iStar Financial, Inc. – |

|

|

|

|

|

|

| REIT (United |

|

|

|

|

|

|

| States)*1 |

| $ | 801,964 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 2,629,407 |

|

|

|

|

|

|

| ||

TOTAL PARTNERSHIPS & TRUSTS |

|

|

|

| |||

(Cost $2,414,414) |

|

| 2,629,407 |

| |||

|

|

|

|

|

| ||

|

|

|

|

|

| ||

WARRANTS – 6.0% |

|

|

|

| |||

|

|

|

|

|

|

|

|

Consumer Finance – 1.2% |

|

|

|

| |||

| 27,783 |

| Capital One Financial |

|

|

|

|

|

|

| Corp., Expiration: |

|

|

|

|

|

|

| November, 2018, |

|

|

|

|

|

|

| Exercise Price: $42.13 |

|

|

|

|

|

|

| (United States)* |

| 405,632 |

| |

|

|

|

|

|

| ||

Diversified Financial Services – 1.4% |

|

|

|

| |||

| 101,240 |

| Bank of America Corp., |

|

|

|

|

|

|

| Expiration: January, 2019, |

|

|

|

|

|

|

| Exercise Price: $13.30 |

|

|

|

|

|

|

| (United States)* |

|

| 204,505 |

|

| 31,620 |

| JPMorgan Chase & |

|

|

|

|

|

|

| Co., Expiration: |

|

|

|

|

|

|

| October, 2018, |

|

|

|

|

|

|

| Excercise Price: $42.42 |

|

|

|

|

|

|

| (United States)* |

|

| 268,769 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 473,274 |

|

|

|

|

|

|

| ||

Insurance – 0.6% |

|

|

|

| |||

| 19,800 |

| Hartford Financial |

|

|

|

|

|

|

| Services Group, Inc., |

|

|

|

|

|

|

| Expiration: June, 2019, |

|

|

|

|

|

|

| Excercise Price: $9.70 |

|

|

|

|

|

|

| (United States)* |

|

| 180,972 |

|

|

|

|

|

|

| ||

Media – 2.8% |

|

|

|

| |||

| 8,059,777 |

| Promotora de |

|

|

|

|

|

|

| Informaciones |

|

|

|

|

|

|

| SA – Class A, |

|

|

|

|

|

|

| Expiration: June, 2014, |

|

|

|

|

|

|

| Excercise Price: $2.00 |

|

|

|

|

|

|

| (Spain)* |

|

| 938,821 |

|

|

|

|

|

|

| ||

TOTAL WARRANTS |

|

|

|

| |||

(Cost $6,107,602) |

|

| 1,998,699 |

| |||

|

|

| |||||

|

|

|

|

|

|

|

|

Principal |

|

|

| Value |

| ||

|

|

|

|

| |||

CORPORATE BONDS – 9.6% |

|

|

|

| |||

|

|

|

|

| |||

Commercial Banking – 1.7% |

|

|

|

| |||

$ | 500,000 |

| Hapag-Lloyd AG, |

|

|

|

|

|

|

| 9.000%, 10/15/2015 |

|

|

|

|

|

|

| (United Kingdom) |

| $ | 566,233 |

|

|

|

|

|

|

| ||

Insurance – 5.0% |

|

|

|

| |||

| 1,300,000 |

| American International |

|

|

|

|

|

|

| Group, Inc., |

|

|

|

|

|

|

| 8.625%, 5/22/2038 |

|

|

|

|

|

|

| (United States)2 |

|

| 1,635,296 |

|

|

|

|

|

|

| ||

Real Estate Investment |

|

|

|

| |||

Trusts – 2.9% |

|

|

|

| |||

| 1,110,000 |

| iStar Financial, Inc., |

|

|

|

|

|

|

| 5.950%, 10/15/2013 |

|

|

|

|

|

|

| (United States) |

|

| 962,925 |

|

|

|

| |||||

TOTAL CORPORATE BONDS |

|

|

|

| |||

(Cost $3,253,049) |

|

| 3,164,454 |

| |||

|

|

| |||||

|

|

|

|

| |||

CONVERTIBLE BOND – 2.8% |

|

|

|

| |||

|

|

|

|

| |||

Shipping & Logistics – 2.8% |

|

|

|

| |||

| 2,000,000 |

| Frontline Ltd., |

|

|

|

|

|

|

| 4.500%, 4/14/2015 |

|

|

|

|

|

|

| (United States) |

|

| 930,000 |

|

|

|

|

|

|

| ||

TOTAL CONVERTIBLE BOND |

|

|

|

| |||

(Cost $1,145,554) |

|

| 930,000 |

| |||

|

|

|

|

|

| ||

|

|

|

|

| |||

MUNICIPAL BONDS – 2.2% |

|

|

|

| |||

|

|

|

|

| |||

Tobacco – 2.2% |

|

|

|

| |||

| 10,840 |

| Northern Tobacco |

|

|

|

|

|

|

| Securitization Co., |

|

|

|

|

|

|

| 5.670%, 6/1/2046 |

|

|

|

|

|

|

| (United States) |

|

| 303,195 |

|

| 22,895 |

| Tobacco Settlement |

|

|

|

|

|

|

| Financing Corp., |

|

|

|

|

|

|

| 6.125%, 6/1/2047 |

|

|

|

|

|

|

| (United States) |

|

| 432,486 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 735,681 |

|

|

|

|

|

|

| ||

TOTAL MUNICIPAL BONDS |

|

|

|

| |||

(Cost $1,134,360) |

|

| 735,681 |

| |||

|

|

| |||||

The accompanying notes are an integral part of these financial statements.

|

|

| 21 |

|

Evermore Global Value Fund |

|

SCHEDULE OF INVESTMENTS at December 31, 2011 Continued |

|

|

|

|

|

|

|

|

Contracts |

| Value |

| ||||

|

|

|

|

| |||

PUT OPTIONS PURCHASED – 0.7% |

|

|

|

| |||

|

|

|

|

| |||

Auto Manufacturers – 0.1% |

|

|

|

| |||

| 610 |

| Daimler AG-Registered |

|

|

|

|

|

|

| Shares, Expiration: |

|

|

|

|

|

|

| March, 2012, |

|

|

|

|

|

|

| Strike Price: $24.00 |

|

|

|

|

|

|

| (Germany) |

| $ | 20,527 |

|

|

|

|

|

|

| ||

Capital Markets – 0.1% |

|

|

|

| |||

| 454 |

| Deutsche Bank AG, |

|

|

|

|

|

|

| Expiration: April, 2012, |

|

|

|

|

|

|

| Strike Price: $22.50 |

|

|

|

|

|

|

| (Germany) |

|

| 41,995 |

|

|

|

|

|

|

| ||

Commerical Banks – 0.3% |

|

|

|

| |||

| 1,716 |

| Banco Bilbao Vizcaya |

|

|

|

|

|

|

| Argentaria, Expiration: |

|

|

|

|

|

|

| March, 2012, |

|

|

|

|

|

|

| Strike Price: $5.25 |

|

|

|

|

|

|

| (Spain) |

|

| 35,535 |

|

| 1,837 |

| Banoco Santander SA, |

|

|

|

|

|

|

| Expiration: March, |

|

|

|

|

|

|

| 2012, Strike Price: |

|

|

|

|

|

|

| $5.25 (Spain) |

|

| 76,080 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 111,615 |

|

|

|

|

|

|

| ||

Diversified Telecommunication |

|

|

|

| |||

Services – 0.1% |

|

|

|

| |||

| 1,507 |

| Telefonica SA, |

|

|

|

|

|

|

| Expiration: March, |

|

|

|

|

|

|

| 2012, Strike Price: |

|

|

|

|

|

|

| $12.00 (Spain) |

|

| 37,058 |

|

|

|

|

|

|

| ||

Energy Equipment & Services – 0.1% |

|

|

|

| |||

| 423 |

| Alstom, Expiration: |

|

|

|

|

|

|

| March, 2012, |

|

|

|

|

|

|

| Strike Price: $18.00 |

|

|

|

|

|

|

| (France) |

|

| 22,994 |

|

|

|

|

|

|

| ||

Real Estate Investment Trusts – 0.0% |

|

|

|

| |||

| 843 |

| American Capital |

|

|

|

|

|

|

| Agency Corp., |

|

|

|

|

|

|

| Expiration: March, |

|

|

|

|

|

|

| 2012, Strike Price: |

|

|

|

|

|

|

| $18.00 (United States) |

|

| 4,215 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

Contracts |

| Value |

| ||||

| |||||||

| 315 |

| American Capital |

|

|

|

|

|

|

| Agency Corp., |

|

|

|

|

|

|

| Expiration: |

|

|

|

|

|

|

| March, 2012, |

|

|

|

|

|

|

| Strike Price: $20.00 |

|

|

|

|

|

|

| (United States) |

| $ | 1,575 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 5,790 |

|

|

|

|

|

|

| ||

Trading Companies & |

|

|

|

| |||

Distributors – 0.0% |

|

|

|

| |||

| 166 |

| TAL International |

|

|

|

|

|

|

| Group, Inc., |

|

|

|

|

|

|

| Expiration: |

|

|

|

|

|

|

| January, 2012, |

|

|

|

|

|

|

| Strike Price: $20.00 |

|

|

|

|

|

|

| (United States) |

|

| 415 |

|

|

|

|

|

|

| ||

TOTAL PURCHASED OPTIONS |

|

|

|

| |||

(Cost $963,472) |

|

| 240,394 |

| |||

|

|

|

|

|

| ||

|

|

|

|

| |||

TOTAL INVESTMENTS IN |

|

|

|

| |||

SECURITIES – 90.8% |

|

|

|

| |||

(Cost $40,463,458) |

|

|

| 30,092,709 |

| ||

Other Assets in Excess |

|

|

|

| |||

of Liabilities – 9.2% |

|

| 3,058,880 |

| |||

|

|

|

|

|

| ||

|

|

|

|

|

| ||

TOTAL NET |

|

|

|

| |||

ASSETS – 100.0% |

| $ | 33,151,589 |

| |||

|

|

| |||||

|

|

|

ADR |

| American Depository Receipt |

* |

| Non-income producing security. |

1 |

| All or a portion of this security was segregated as collateral for forward currency contracts. |

2 |

| Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration, which are normally those transactions with qualified institutional buyers. |

The accompanying notes are an integral part of these financial statements.

|

|

22 |

|

|

Evermore Global Value Fund |

|

SCHEDULE OF SECURITIES SOLD SHORT at December 31, 2011 |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

| |||||||

SECURITIES SOLD SHORT – 2.5% |

|

|

|

| |||

|

|

|

|

| |||

Capital Markets – 0.8% |

|

|

|

| |||

| 7,100 |

| Deutsche Bank AG |

| $ | 268,806 |

|

|

|

|

|

|

| ||

Commercial Banks – 1.6% |

|

|

|

| |||

| 50,300 |

| Barclays PLC |

|

| 137,755 |

|

| 17,790 |

| Barclays PLC – ADR |

|

| 195,512 |

|

| 165,109 |

| Lloyds Banking |

|

| 66,320 |

|

| 22,096 |

| Royal Bank of |

|

| 140,752 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 540,339 |

|

|

|

|

|

|

| ||

Media – 0.1% |

|

|

|

| |||

| 41,135 |

| Promotora de |

|

| 46,125 |

|

|

|

|

|

|

| ||

TOTAL SECURITIES SOLD SHORT |

|

|

|

| |||

(Proceeds $731,303) |

| $ | 855,270 |

| |||

|

|

|

| ||||

|

|

|

ADR |

| American Depository Receipt |

* |

| Non-income producing security. |

| ||

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS® is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Fund’s Administrator, U.S. Bancorp Fund Services, LLC. | ||

|

|

|

|

|

|

|

Country |

| Percent of |

| Net of | ||

United States |

|

| 35.2 | % |

| – |

Spain# |

|

| 11.5 | % |

| 11.7% |

Italy |

|

| 8.8 | % |

| – |

United Kingdom# |

|

| 6.4 | % |

| 8.0% |

Norway |

|

| 6.3 | % |

| – |

Netherlands |

|

| 3.8 | % |

| – |

Germany# |

|

| 3.5 | % |

| 4.3% |

France |

|

| 3.4 | % |

| – |

Canada |

|

| 3.0 | % |

| – |

Russia |

|

| 2.2 | % |

| – |

Sweden |

|

| 1.5 | % |

| – |

Switzerland |

|

| 1.1 | % |

| – |

Cash & |

|

| 13.3 | % |

| – |

|

|

|

|

|

| |

Total |

|

| 100.0 | % |

|

|

|

|

|

|

|

| |

|

|

^ | Includes money market fund and other assets in excess of liabilities. |

# | Includes securities sold short. |

The accompanying notes are an integral part of these financial statements.

|

|

| 23 |

|

Evermore European Value Fund |

|

SCHEDULE OF INVESTMENTS at December 31, 2011 |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

|

|

|

| ||

COMMON STOCKS – 25.9% |

|

|

|

| |||

|

|

|

|

|

|

|

|

Industrial Conglomerates – 12.3% |

|

|

|

| |||

| 15,850 |

| Justice Holdings Ltd. |

| $ | 211,688 |

|

|

|

|

|

|

| ||

Media – 13.6% |

|

|

|

|

| ||

| 58,200 |

| Constantin Medien |

|

| 96,341 |

|

|

|

|

|

|

|

|

|

| 7,236 |

| Promotora de |

|

| 8,114 |

|

|

|

|

|

|

|

|

|

| 26,736 |

| Promotora de |

|

| 129,402 |

|

|

|

|

|

|

| ||

|

|

|

|

|

| 233,857 |

|

|

|

|

|

|

| ||

TOTAL COMMON STOCKS |

|

|

|

| |||

(Cost $647,175) |

|

| 445,545 |

| |||

|

|

|

|

|

| ||

|

|

|

|

|

| ||

WARRANT – 3.9% |

|

|

|

| |||

|

|

|

|

|

| ||

Media – 3.9% |

|

|

|

| |||

| 570,387 |

| Promotora de |

|

| 66,436 |

|

|

|

|

|

|

| ||

TOTAL WARRANT |

|

|

|

| |||

(Cost $163,271) |

|

| 66,436 |

| |||

|

|

|

| ||||

|

|

|

|

|

|

|

|

Contracts |

|

|

|

|

|

| |

(100 shares per contract) |

|

|

|

| |||

PUT OPTION PURCHASED – 0.0% |

|

|

|

| |||

|

|

|

|

|

|

|

|

Trading Companies & Distributors – 0.0% |

|

|

|

| |||

| 27 |

| TAL International |

|

| 67 |

|

|

|

|

|

|

| ||

TOTAL PURCHASED OPTION |

|

|

|

| |||

(Cost $1,512) |

|

| 67 |

| |||

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

|

|

|

| ||

SHORT-TERM INVESTMENT – 55.5% |

|

|

|

| |||

|

|

|

|

|

| ||

Money Market Fund – 55.5% |

|

|

|

| |||

| 957,308 |

| Invesco Liquid Assets |

| $ | 957,308 |

|

|

|

|

|

|

| ||

TOTAL SHORT-TERM INVESTMENT |

|

|

|

| |||

(Cost $957,308) |

|

| 957,308 |

| |||

|

|

|

|

|

| ||

TOTAL INVESTMENTS IN SECURITIES – 85.3% |

|

|

|

| |||

(Cost $1,769,266) |

|

| 1,469,356 |

| |||

Other Assets in Excess |

|

| 251,886 |

| |||

|

|

|

|

|

| ||

TOTAL NET |

| $ | 1,721,242 |

| |||

|

|

|

| ||||

|

|

|

ADR |

| American Depository Receipt |

* |

| Non-income producing security. |

1 |

| All or a portion of this security was segregated as collateral for forward currency contracts. |

2 |

| 7-day yield as of December 31, 2011. |

The accompanying notes are an integral part of these financial statements.

|

|

24 |

|

|

Evermore European Value Fund |

|

SCHEDULE OF SECURITIES SOLD SHORT at December 31, 2011 |

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

|

|

|

| ||

SECURITIES SOLD SHORT – 0.5% |

|

|

|

| |||

|

|

|

|

|

|

|

|

Media – 0.5% |

|

|

|

|

| ||

| 7,234 |

| Promotora de |

| $ | 8,112 |

|

|

|

|

|

|

| ||

TOTAL SECURITIES SOLD SHORT |

|

|

|

| |||

(Proceeds $7,866) |

| $ | 8,112 |

| |||

|

|

| |||||

|

|

* | Non-income producing security. |

|

|

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS® is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Fund’s Administrator, U.S. Bancorp Fund Services, LLC. | |

|

|

|

|

|

|

|

Country |

| Percent of |

| Net of | ||

United Kingdom |

|

| 12.3 | % |

| – |

Spain# |

|

| 11.4 | % |

| 11.9% |

Germany |

|

| 5.6 | % |

| – |

United States |

|

| – |

|

| – |

Cash & |

|

| 70.7 | % |

| – |

|

|

|

|

|

| |

Total |

|

| 100.0 | % |

|

|

|

|

|

|

|

| |

|

|

^ | Includes money market fund and other assets in excess of liabilities. |

# | Includes securities sold short. |

The accompanying notes are an integral part of these financial statements.

|

|

| 25 |

(This Page Intentionally Left Blank.)

|

|

26 |

|

Evermore Funds

|

|

|

|

|

|

|

|

STATEMENTS OF ASSETS AND LIABILITIES at December 31, 2011 | |||||||

|

| Evermore |

| Evermore |

| ||

ASSETS |

|

|

|

|

|

|

|

Investments in securities, at value^ (Note 2) |

| $ | 30,092,709 |

| $ | 1,469,356 |

|

Unrealized gain on forward currency contracts |

|

| 414,747 |

|

| 106,014 |

|

Foreign Cash (cost of $12,324 and |

|

| 12,272 |

|

| 23,651 |

|

Receivables: |

|

| �� |

|

|

|

|

Investment securities sold |

|

| 4,234,236 |

|

| 132,640 |

|

Fund shares sold |

|

| 3,600 |

|

| — |

|

Dividends and interest, net |

|

| 120,882 |

|

| 1,197 |

|

Due from adviser, net |

|

| — |

|

| 72,171 |

|

Due from broker, net |

|

| — |

|

| 7,836 |

|

Prepaid expenses |

|

| 39,550 |

|

| — |

|

|

|

|

| ||||

Total assets |

|

| 34,917,996 |

|

| 1,812,865 |

|

|

|

|

| ||||

LIABILITIES |

|

|

|

|

|

|

|

Unrealized loss on forward currency contracts |

|

| 5,870 |

|

| 19,146 |

|

Securities sold short, at value (proceeds $731,303 and |

|

| 855,270 |

|

| 8,112 |

|

Due to broker, net |

|

| 129,570 |

|

| — |

|

Due to custodian |

|

| 506,507 |

|

| — |

|

Payables: |

|

|

|

|

|

|

|

Currency payable |

|

| 7,936 |

|

| 577 |

|

Fund shares redeemed |

|

| 198,885 |

|

| — |

|

Investment advisory fees, net |

|

| 7,657 |

|

| — |

|

Administration fees |

|

| 7,894 |

|

| 11,539 |

|

Custody fees |

|

| 7,268 |

|

| 6,731 |

|

Distribution fees |

|

| 9,266 |

|

| 408 |

|

Fund accounting fees |

|

| 6,312 |

|

| 9,724 |

|

Transfer agent fees |

|

| 9,983 |

|

| 9,663 |

|

Other accrued expenses |

|

| 13,989 |

|

| 25,723 |

|

|

|

|

| ||||

Total liabilities |

|

| 1,766,407 |

|

| 91,623 |

|

|

|

|

| ||||

NET ASSETS |

| $ | 33,151,589 |

| $ | 1,721,242 |

|

|

|

|

| ||||

COMPONENTS OF NET ASSETS |

|

|

|

|

|

|

|

Paid-in capital |

| $ | 43,801,037 |

| $ | 3,611,919 |

|

Undistributed net investment income (loss) |

|

| 229,557 |

|

| (86,868 | ) |

Accumulated net realized loss on investments, foreign |

|

| (788,774 | ) |

| (1,590,349 | ) |

Net unrealized depreciation on investments |

|

| (10,370,749 | ) |

| (299,910 | ) |

Net unrealized appreciation on foreign currency |

|

| 404,485 |

|

| 86,696 |

|

Net unrealized depreciation on securities sold short |

|

| (123,967 | ) |

| (246 | ) |

|

|

|

| ||||

Net assets |

| $ | 33,151,589 |

| $ | 1,721,242 |

|

|

|

|

| ||||

^Cost of Investments |

| $ | 40,463,458 |

| $ | 1,769,266 |

|

|

|

|

| ||||

# Financial statements are presented on a liquidation basis. (Note 1)

The accompanying notes are an integral part of these financial statements.

|

|

| 27 |

Evermore Funds

|

|

|

|

|

|

|

|

STATEMENTS OF ASSETS AND LIABILITIES at December 31, 2011 | |||||||

|

| Evermore |

| Evermore |

| ||

Class A: |

|

|

|

|

|

|

|

Net assets |

| $ | 5,330,870 |

| $ | 174,260 |

|

Shares issued and outstanding (unlimited number |

|

| 641,137 |

|

| 23,075 |

|

Net asset value, and redemption price per share |

| $ | 8.31 |

| $ | 7.55 |

|

|

|

|

| ||||

Maximum offering price per share* |

|

|

|

|

|