Ally Auto Assets LLC

Corporation Trust Center

1209 Orange Street

Wilmington, Delaware 19801

September 24, 2015

VIA EDGAR

Securities and Exchange Commission

450 Fifth Street, N.W.

Washington, D.C. 20549

| Attention: | Katherine Hsu |

| Folake Ayoola |

| Re: | Ally Auto Assets LLC |

| Amendment No. 1 to Registration Statement on Form SF-3 |

| Filed August 14, 2015 |

| File No. 333-204844 |

Dear Ladies and Gentlemen:

This letter is provided on behalf of Ally Auto Assets LLC (the “Company”) in response to your letter dated August 26, 2015 (the “Letter”) relating to comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) in connection with the above-referenced submission. For your reference, we have listed your questions and our corresponding answers.

Registration Statement on Form SF-3

General

| 1. | Please confirm that, if you or an underwriter obtain a due diligence report from a third-party provider, for any offering occurring on or after June 15, 2015, you, or the underwriter, as applicable, will furnish a Form ABS-15G with the Commission at least five business days before the first sale in the offering making publicly available the findings and conclusions of any third-party due diligence report you or the underwriter have obtained. See Section II.H.1 of the Nationally Recognized Statistical Rating Organizations Adopting Release (Release No. 34-72936). |

Response: We confirm that if we or an underwriter obtain a due diligence report from a third-party provider, for any offering occurring on or after June 15, 2015, we will, or we will require the underwriter to, as applicable, furnish a Form ABS-15G with the Commission at least five business days before the first sale in the offering making publicly available the findings and conclusions of any third-party due diligence report we or any underwriter have obtained.

Securities and Exchange Commission

September 24, 2015

Page 2

Asset Representations Review, page 44

| 2. | We note your disclosure that noteholders holding at least 5% of the outstanding aggregate principal balance of the notes may initiate a vote for an asset representations review. We further note your disclosure on page 80 that, because the notes are in book-entry form, “[a]ll references in this prospectus to actions by noteholders refer to actions taken by DTC…” Please revise your disclosure to make clear that investors (i.e., beneficial owners) will be able to initiate a vote for an asset representations review. Please make conforming changes throughout the document, including in the voting section on page 46. |

Response: We have revised our disclosure in“The Receivables Pool—Asset Representations Review” on page 44 to clarify that investors or beneficial owners will be able to initiate a vote for an asset representations review.

Voting, page 46

| 3. | Please confirm that notes held by the sponsor or servicer, or any affiliates thereof, are not included in the calculation of determining whether 5% of investors have elected to initiate a vote. See Section V.B.3(a)(2)(c)(i)(b) of the 2014 Regulation AB II Adopting Release (stating “the maximum percentage of investors’ interest in the pool required to initiate a vote may not be greater than 5% of the total investors’ interest in the pool (i.e., interests that are not held by affiliates of the sponsor or servicer)”). |

Response: We have revised our disclosure on page 46 to make clear that notes held by the sponsor or servicer, or any affiliates thereof, are not included in the calculation of determining whether 5% of investors have elected to initiate a vote.

| 4. | We note your disclosure that “[w]ithin [45] days of publication that the delinquency trigger has been met… the noteholders may determine whether or review of 60 day or more delinquent receivables should be initiated by the asset representations reviewer” and “[t]he indenture trustee will allow noteholders to vote for at least [45] days.” Depending upon the dates selected, a narrow time window could make it difficult for investors to use the shelf investor communication mechanism in connection with the asset review vote. Please revise, as appropriate, to ensure that investors will be able to use the investor communication mechanism or advise. |

Response: We have revised the disclosure on page 46 to extend the time period to 90 days for demanding a vote. We believe that 90 days will provide sufficient time for investors to use the investor communication mechanism and demand a vote. We have also revised our disclosure to provide that the vote will remain open for 150 days after publication that the delinquency trigger has been met or exceeded. We believe such time periods will give investors sufficient time to communicate at each stage.

Securities and Exchange Commission

September 24, 2015

Page 3

The Asset Representations Review, page 46

| 5. | We note your response to comment 6. We further note your disclosure on page 47 that, “[t]he transaction documents require that any breach of the representations and warranties mustmaterially and adversely affect the interest of the noteholders [or the certificateholders] before the sponsor or the depositor would be required to repurchase such receivables.” (emphasis added) Please revise your disclosure to confirm that an investor, through the appropriate medium, can make a repurchase request whether or not the sponsor or depositor make a determination that the breach materially and adversely affects the interest of the noteholders. |

Response: We have revised our disclosure on page 47 to confirm that the investors can make a repurchase request regardless of whether the sponsor or depositor make a determination that the breach materially and adversely affects the interest of the noteholders.

Dispute Resolution, page 47

| 6. | We note your response to comment 14 and your revised disclosure including “noteholders” as part of the group that may utilize the dispute resolution provision. As indicated in our comment 2 above, please revise your disclosure to describe how investors (i.e., beneficial owners) may utilize the dispute resolution provision. Also explain the process they will use to notify the transaction parties of a repurchase request and a referral to dispute resolution, if such process is different from the process used by noteholders through DTC. |

Response: We have revised our disclosure in“The Receivables Pool—Dispute Resolution” on page 47 to clarify that investors or beneficial owners will be able to use the dispute resolution procedures. We included the following address placeholder on page 47 of our prior amendment, which investors can use to initiate a dispute resolution proceeding: “Within [30] days of the filing of the first monthly statement to securityholders following the end of the 180-day period, the requesting party must initiate the proceedings and provide notice (as defined by the [AAA][FINRA][JAMS][ADR] Rules) to the sponsor and the depositor of its intent to pursue resolution through mediation or arbitration at [insert email address or other address].” In connection with each transaction, we will insert the email or other address that can be used by an investor to provide notice of its intent to commence a dispute resolution proceeding.

| 7. | We note your disclosure that limits the use of the dispute resolution provision to “breach of a representation or warranty related to a receivable made by the depositor or the sponsor in the transaction documents, whichmaterially and adversely affects the interest of the noteholders [or the certificateholders] in the related receivable…” (emphasis added). Please provide us with an analysis of how the “materially and adversely” limitation is consistent with the shelf eligibility dispute resolution provision. Please refer to General Instruction I.B.1(c) of Form SF-3 and Section V.B.3(a)(3) of the 2014 ABS Adopting Release (“…investors should be able to utilize the dispute resolution … for those requests in which investors believe that the resolution offered by the sponsor does not make them whole). |

Securities and Exchange Commission

September 24, 2015

Page 4

Response: We have revised our disclosure on page 47 to provide that a breach which results in an investor not being made whole will be sufficient grounds to commence a dispute resolution proceeding related to a receivable if, upon the 180th day after a demand is received, the sponsor or the depositor has failed to resolve such investor’s demand.

| 8. | We note your disclosure that, “[i]n the event that the asset representations reviewer determines that the representations and warranties related to a receivable have not failed, any repurchase request related to that receivable will be deemed to be resolved and that receivable may not be subject to a dispute resolution proceeding.” This part of your dispute resolution provision appears inconsistent with the shelf eligibility requirement. Please refer to General Instruction I.B.1(c) of Form SF-3 and Section V.B.3(a)(3) of the 2014 ABS Adopting Release (“…while we believed that our asset review shelf requirement would help investors evaluate whether a repurchase request should be made, we structured the dispute resolution provision so that investors could utilize the dispute resolution provision for any repurchase request, regardless of whether investors direct a review of the assets. We believe that organizing the dispute resolution requirement as a separate subsection in the shelf eligibility requirements will help to clarify the scope of the dispute resolution provision.). |

Response: We note that the disclosure quoted above was included on page 55 of Amendment No. 2 to Form SF-3 filed by Ford Credit Auto Receivables Two LLC (File No. 333-205596) on September 4, 2015 (the “Ford Filing”). Additionally, the sale and servicing agreement filed as Exhibit 10.3 to the Ford Filing states in Section 2.6(a) that “if the Receivable subject to a Repurchase Request was part of a Review and the Review Report states no Test Fails for the Receivable, the Repurchase Request for the Receivable will be deemed to have been resolved.” In the Commission’s October 6, 2014 announcement, it stated that the draft filing review program was designed “[t]o assist ABS issuers in preparing for the new disclosure requirements, [and that] the Division intends to make draft registration statements and related staff comment letters available to the public in advance of the compliance date.” Upon the initial disclosure of those draft registration statements and the related staff comment letters, we included the above referenced language in our amendment as well. Since the Commission did not object to the inclusion of this standard prior to declaring the Ford Filing effective, we and other issuers who have included this language will be at a competitive disadvantage compared to other market participants if we and other issuers are required to remove the above quoted disclosure.

Whether an investor voted affirmatively, negatively or abstained in the vote to cause a review will not affect whether that investor can use the dispute resolution proceeding. An investor will also be entitled to refer a dispute related to any receivables that the asset representations reviewer did not review to a dispute resolution proceeding as well as any receivable that the asset representations reviewer reviewed and found to have failed a test.

Additionally, the asset representations reviewer is an independent third party reviewer and should be capable of resolving any dispute related to the representations and warranties given with respect to a receivable. Therefore, a decision by the asset representations reviewer with respect to the representations and warranties related to a delinquent receivable should be a sufficient resolution of any related dispute.

Securities and Exchange Commission

September 24, 2015

Page 5

Credit Risk Retention, page 79

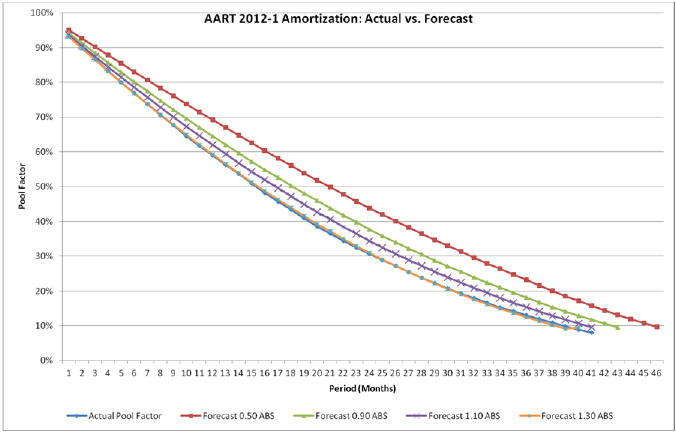

| 9. | We note that, in calculating the fair value of the residual interest, you have assumed that receivables prepay at a constant rate. In Section III.B.1.b. of the Credit Risk Retention Adopting Release (Release No. 34-73407) (Oct. 22, 2014), the agencies stated that we expect the key inputs and assumptions would not assume straight lines. Please revise or tell us why you believe an assumption of a constant prepayment rate is appropriate here. |

Response: The prepayment model described in our disclosure measures prepayments as a percentage of the initial pool balance for each month. As a result, the rate of prepayments increases over time and results in a curve instead of a constant rate. The attachedExhibit A shows the actual pool balance amortization for one of our recent securitization transactions versus some of the prepayment rates presented in the prospectus supplement for that transaction. We will adjust the projection based on the nature of the collateral for each transaction as well as our historical experience with prepayments of other similar receivables.

| 10. | Please revise to disclose material terms of the eligible horizontal cash reserve account or include a cross-reference to where that disclosure can be found. Please refer to Rule 4(b) and Rule 4(c)(1)(iii) of Regulation RR. |

Response: We have added a cross-reference to our disclosure on page 80 to reference the material terms of the eligible horizontal cash reserve account.

We hope that the foregoing has been responsive to the Staff’s comments. If you have any questions related to this letter, please contact my counsel, Janette McMahan of Kirkland & Ellis LLP, at (212) 446-4754.

| Sincerely, |

| /s/ Ryan C. Farris |

| Ryan C. Farris |

| President, Ally Auto Assets LLC |

| cc: | Richard V. Kent, Ally Auto Assets LLC |

| Janette McMahan, Kirkland & Ellis LLP |

EXHIBIT A