Ally Auto Assets LLC

Corporation Trust Center

1209 Orange Street

Wilmington, Delaware 19801

March 31, 2016

VIA EDGAR

Securities and Exchange Commission

450 Fifth Street, N.W.

Washington, D.C. 20549

| Attention: | Katherine Hsu | |

| Benjamin Meeks | ||

| Re: | Ally Auto Assets LLC / Ally Bank Lease Trust | |

| Registration Statement on Form SF-3 | ||

| Filed February 8, 2016 | ||

| File No. 333-209435 | ||

Dear Ladies and Gentlemen:

This letter is provided on behalf of Ally Auto Assets LLC (the “Company”) in response to your letter dated March 7, 2016 (the “Letter”) relating to comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) in connection with the above-referenced submission. For your reference, we have listed your questions and our corresponding answers.

Registration Statement on Form SF-3

General

| 1. | Please confirm that the depositor or any issuing entity previously established, directly or indirectly, by the depositor or any affiliate of the depositor have been current with Exchange Act reporting during the last twelve months with respect to asset-backed securities involving the same asset class. Please refer to General Instruction I.A.2. of Form SF-3. |

Response: The depositor has been current and timely with Exchange Act reporting during the last twelve months with respect to asset-backed securities involving the same asset class as this offering. The CIK number for Ally Central Originating Lease Trust, an affiliate of the depositor that has offered a class of asset-backed securities involving the same asset class as this offering, is 0001546491.

Securities and Exchange Commission

March 31, 2016

Page 2

The CIK numbers for issuing entities established by the depositor that have issued asset-backed securities involving the same asset class as this offering and have been required to make Exchange Act reports during the last twelve months are as follows:

Name | CIK | |

| Ally Auto Receivables Trust 2012-SN1 | 0001557473 | |

| Ally Auto Receivables Trust 2013-SN1 | 0001577943 | |

| Ally Auto Receivables Trust 2014-SN1 | 0001600571 | |

| Ally Auto Receivables Trust 2014-SN2 | 0001621990 | |

| Ally Auto Receivables Trust 2015-SN1 | 0001637287 | |

| 2. | Please file your outstanding exhibits, including the forms of agreements, with your next amendment. |

Response: We confirm that we have filed our outstanding exhibits, including the forms of agreements, with Amendment No. 1 to the Registration Statement, filed March 31, 2016.

| 3. | Please confirm that all material terms to be included in the finalized agreements will also be disclosed in the final Rule 424(b) prospectus and that finalized agreements will be filed and made part of the registration statement no later than the date of the final prospectus, including unqualified legal and tax opinions. Refer to Item 1100(f) of Regulation AB and Instruction 1 to Item 601 of Regulation S-K. |

Response: We confirm that all material terms to be included in the finalized agreements will be disclosed in the final Rule 424(b) prospectus and that, consistent with our existing practices, finalized agreements will be filed and made part of the registration statement no later than the date of the final prospectus, including unqualified legal and tax opinions.

| 4. | Please confirm that the portion of the securitized pool balance attributable to the residual value of the physical property underlying the leases, as determined in accordance with the transaction agreements for the securities, will not constitute 65% or more, as measured by dollar volume, of the securitized pool balance as of the measurement date. Refer to Item 1101(c)(2)(v)(A) of Regulation AB. |

Response: We confirm that the portion of the securitized pool balance attributable to the residual value of the physical property underlying the leases, as determined in accordance with the transaction agreements for the securities, will not constitute 65% or more, as measured by dollar volume, of the securitized pool balance as of the measurement date.

| 5. | Please describe the relationship between Ally Bank Lease Trust and Ally Central Originating Lease LLC so that it is clear why Ally Central Originating Lease LLC is signing the registration statement on behalf Ally Bank Lease Trust. Please refer to Section III.A.6.c of Release No. 33-8518 (Dec. 22, 2004). |

Securities and Exchange Commission

March 31, 2016

Page 3

Response: As described in the cited reference (Section III.A.6.c of Release No. 33-8518), Ally Bank Lease Trust (“ABLT”), the issuer of the underlying financial asset, must sign the registration statement. The power of attorney filed as Exhibit 24.2 to the registration statement on February 6, 2016 granted to Ally Central Originating Lease LLC (“ACOL LLC”), as attorney-in-fact, the power to sign the registration statement on behalf of ABLT. We have revised the signature page to the registration statement to indicate that ACOL LLC is signing as attorney-in-fact on behalf of ABLT. Because ABLT is a trust and does not have any officers or directors, either the trustee or another entity or person would need to sign the registration statement on behalf of ABLT.

Registration Statement Cover Page

| 6. | The registration statement includes principal executive office addresses for Ally Auto Assets LLC and Ally Central Originating Lease Trust, the latter of which is not one of the two registrants listed on the cover page of the registration statement. Please confirm that the correct entity names are shown and that the registration statement includes the principal executive office address for each of the registrants. |

Response: The principal executive office address for Ally Bank Lease Trust was correctly included; however, the name “Ally Central Originating Lease Trust” was inadvertently listed on the cover page. We have corrected the name on the cover in Amendment No. 1 to the Registration Statement, filed March 31, 2016.

| 7. | We note your footnote to the Calculation of Registration Fee table indicating that you intend to rely on Rule 457(p). Please revise to state whether the offerings registered on the prior registration statements have been completed or terminated or the prior registration statements have been withdrawn. |

Response: We have revised the footnote to the Calculation of Registration Fee table to clarify that the offerings registered on the prior registration statements will be terminated and will be withdrawn upon the effectiveness of this registration statement.

Summary, page 2

| 8. | We note that you indicate that Ally Servicing LLC will act as a sub-servicer in this transaction. Please include bracketed language to indicate that you will provide the information required by Item 1108(b) and (c) of Regulation AB for this affiliate as well as for any other affiliates that will participate in the servicing for the pool assets. |

Response: We have added cross-references in the“Summary” to reference“The Servicer and the Administrator” and“Servicing and Administration Procedures” in the prospectus. Those sections describe the information required to be included in the prospectus by Item 1108(b) and (c) of Regulation AB with respect to Ally Servicing LLC (“Ally Servicing”). These sections include a discussion of Ally Servicing’s name and form of organization, how long Ally Servicing has been servicing lease assets and a discussion of Ally Servicing’s experience servicing assets. We have added an additional description of Ally Servicing’s responsibilities with respect to the overall servicing function. Any limitations on the Ally Servicing’s liability

Securities and Exchange Commission

March 31, 2016

Page 4

are discussed in“The Transfer Agreements and Servicing Agreements.” We have added bracketed language to indicate that we will provide any additional information required by Item 1108(b) and (c) of Regulation AB should any other affiliates participate in the servicing of the pool assets.

Description of Auto Lease Business—Acquisition and Underwriting of Motor Vehicle Leases, page 35

| 9. | We note your disclosure that “[a]pplications are first evaluated through an automated process” and “are approved or declined and credit decisions are made either entirely through the automated process or through the automated process followed by manual review by a credit underwriter.” However, the adopting release for Item 1111(a)(8) notes that “where originators may approve loans at a variety of levels, the loans underwritten at an incrementally higher level of approval are evaluated based on judgmental underwriting decisions, the criteria for the first level of underwriting should be disclosed, and loans that are included in the pool despite not meeting the criteria for this first level of underwriting criteria should be disclosed under Item 1111(a)(8).” See Issuer Review of Assets in Offerings of Asset-Backed Securities, Release No. 33-9176 (Jan. 20, 2011). Please revise your disclosure to make it clear that applications approved following manual review by a credit underwriter are disclosed as exception applications under Item 1111(a)(8) or advise. |

Response: With respect to the initial review of an application, certain applications are approved through an automated process because the application may contain characteristics that can be processed automatically while some applications contain characteristics that are not amenable to an automatic process and need to be manually reviewed to complete the process. In the initial review, we consider both the automated process and the initial manual process to be the first level of review. If the application does not satisfy the underwriting criteria established at the first level, the application is only approved at an incrementally higher level of approval. If an application is approved despite not having satisfied all of the underwriting criteria at the first level, the related lease asset will be disclosed as an exception under“The Lease Assets and Secured Notes—Exceptions to Underwriting Guidelines” in the prospectus. The disclosure related to the exception will also include the nature of the exception and the number of lease assets in the pool that are exceptions and the percentage of the pool that constitutes that type of exception.

Voting, page 59

| 10. | We note that the cross-reference in the third paragraph does not match the heading of the section to which it appears you intend to refer (“—The Asset Representations Review Process”). Please revise or advise. |

Response: We have revised the above referenced cross-reference.

Securities and Exchange Commission

March 31, 2016

Page 5

Dispute Resolution, page 61

| 11. | We note your statement that “… any noteholder may, upon discovery of a breach of a representation or warranty related to a lease asset made by ABLT or the sponsor in the transaction documents, which … in the case of a noteholder (including a beneficial owner of the notes) … results in that noteholder not being made whole, demand that ACOL LLC, on behalf of ABLT, or Ally Bank purchase the related lease asset from the 20 -SN pool.” We note also your disclosure in the section beginning on page 104 titled “Book-Entry Registration” indicating that “[n]oteholders will not be recognized by the AART indenture trustee as noteholders as that term is used in the AART indenture, and noteholders will be permitted to exercise the rights of noteholders only, indirectly through DTC and its DTC participants.” Please revise one or both of these statements as necessary to explain how a beneficial owner of a note may exercise its rights to demand repurchase of a lease asset and to make it clear that the second statement noted above does not prevent beneficial owners of notes from exercising their rights as otherwise described in the prospectus. |

Response: We have added language on page 104 under the heading“Book Entry Registration” clarifying that the general rule does not apply if the prospectus otherwise includes beneficial owners of the notes in the usage of the term “noteholders.”

| 12. | We note your disclosure that “[t]he review period may be extended by up to an additional [30] days if the asset representations reviewer requests missing review materials that are subsequently provided within the [60-day] period ….” Please revise your disclosure to describe how the asset representations review will proceed if such missing review materials are not provided. |

Response: We have revised our disclosure to clarify that if any materials requested by the asset representations reviewer are not provided, the result of the affected test will be a failure as a result of missing or insufficient documentation, as described on page 60 of the Prospectus under“The Lease Assets and the Secured Notes—Asset Representations Review—The Asset Representations Review Process.”

| 13. | We note your disclosure that in the event that the asset representations reviewer determines that the representations and warranties related to a lease asset have not failed, any purchase request related to that lease asset will be deemed to be resolved. Please revise this provision to provide, or confirm supplementally, that an investor will be permitted to refer a dispute related to any lease asset to dispute resolution. Refer to General Instruction I.B.1(c) of Form SF-3 and Section V.B.3(a)(3) of the 2014 ABS Adopting Release. |

Response: We confirm that an investor will be entitled to refer a dispute related to any lease asset to dispute resolution, including a lease asset that the asset representations reviewer reviewed and found to have not failed a test.

Securities and Exchange Commission

March 31, 2016

Page 6

The AART Indenture, page 84

| 14. | We note your disclosure regarding availability of copies of the AART indenture. Please revise to clarify that it is the “final” AART indenture that will be filed with the SEC no later than the date of the filing of the final prospectus for the notes. Refer to Item 1100(f) of Regulation AB and Instruction 1 to Item 601 of Regulation S-K. |

Response: We have revised the disclosure to clarify that “[a] copy of the final AART indenture under which the notes are issued will be available to noteholders from the depositor upon request and will be filed with the SEC no later than the date of the filing of the final prospectus for the notes” on page 84 under the heading“The Notes—The AART Indenture” and have also made a similar revision on page 96 under the heading“The Notes—The ABLT Indenture” with respect to the ABLT indenture.

Credit Risk Retention—Retained Eligible Horizontal Residual Interest, page 102

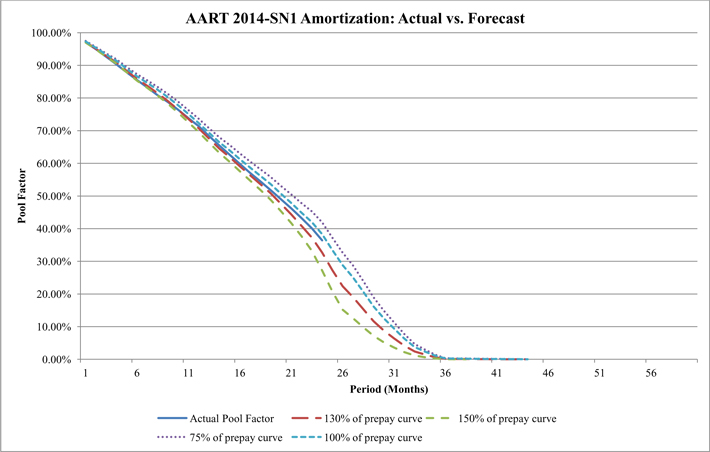

| 15. | We note that, in calculating the fair value of the residual interest, you have assumed that lease assets prepay at a constant rate. In Section III.B.1.b. of the Credit Risk Retention Adopting Release (Release No. 34-73407) (Oct. 22, 2014), the agencies stated that we expect the key inputs and assumptions would not assume straight lines. Please explain why you believe that assuming a constant prepayment rate is appropriate. |

Response: As we noted in our response letter to the Commission dated September 24, 2015, with respect to the Ally Auto Assets LLC SF-3 Registration Statement, file no. 333-204844, and as noted in the response letter of our affiliate, Capital Auto Receivables LLC, to the Commission dated December 23, 2015, with respect to its Registration Statement, file no. 333-208079, the prepayment model described in our disclosure measures prepayments as a percentage of the a projected pool balance for each month. As a result, the rate of prepayments results in a curve instead of a constant rate because the projection is based on a forecast of the actual payments due under the related leases and the proceeds from the sale of the vehicle at the end of the lease term. The attachedExhibit A shows the actual pool balance amortization for one of our prior securitization transactions versus some of the prepayment rates presented in the prospectus supplement for that transaction. We will adjust the projection based on the nature of the lease assets for each transaction as well as our historical experience with prepayments of other similar lease assets.

Asset Representations Reviewer, page 146

| 16. | Your disclosure suggests that a third party may perform pre-closing due diligence services for the transaction. Please confirm that, if you or an underwriter obtains a due diligence report from a third-party provider, you or the underwriter, as applicable, will furnish a Form ABS-15G to the Commission at least five business days before the first sale in the offering making publicly available the findings and conclusions of any third-party due diligence report you or the underwriter has obtained. See Section II.H.1 of the Nationally Recognized Statistical Rating Organizations Adopting Release (Release No. 34-72936) (Aug. 27, 2014). |

Securities and Exchange Commission

March 31, 2016

Page 7

Response: We confirm that if we or an underwriter obtain a due diligence report from a third-party provider, we will, or we will require the underwriter to, as applicable, furnish a Form ABS-15G with the Commission at least five business days before the first sale in the offering making publicly available the findings and conclusions of any third-party due diligence report we or any underwriter have obtained.

We hope that the foregoing has been responsive to the Staff’s comments. If you have any questions related to this letter, please contact my counsel, Janette McMahan of Kirkland & Ellis LLP, at (212) 446-4754.

| Sincerely, |

/s/ Ryan C. Farris |

| Ryan C. Farris |

| President, Ally Auto Assets LLC |

| cc: | Richard V. Kent, Ally Auto Assets LLC |

Janette McMahan, Kirkland & Ellis LLP

EXHIBIT A