Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22376

PIMCO Equity Series VIT

(Exact name of registrant as specified in charter)

650 Newport Center Drive, Newport Beach, CA 92660

(Address of principal executive office)

Trent W. Walker

Treasurer (Principal Financial & Accounting Officer)

PIMCO Equity Series VIT

650 Newport Center Drive, Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Brendan C. Fox

Dechert LLP

1900 K Street, N.W.

Washington, D.C. 20006

Registrant’s telephone number, including area code: (888) 877-4626

Date of fiscal year end: December 31

Date of reporting period: December 31, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507

Table of Contents

| Item 1. | Reports to Shareholders. |

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1).

• PIMCO Equity Series VIT—Institutional and Advisor Classes

Table of Contents

PIMCO Equity Series VIT®

Annual Report

December 31, 2015

PIMCO Global Dividend Portfolio

Share Classes

| n | Institutional |

| n | Advisor |

Table of Contents

| Page | ||||

| 2 | ||||

| 4 | ||||

| 6 | ||||

| 8 | ||||

| 10 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 15 | ||||

| 20 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| | 38 | | ||

| 39 | ||||

Approval of Investment Advisory Contract and Other Agreements | 40 | |||

Prior to July 13, 2015 the Portfolio’s name was PIMCO EqS Pathfinder PorfolioTM

This material is authorized for use only when preceded or accompanied by the current PIMCO Equity Series VIT (the “Trust”) prospectus for the Portfolio. The variable product prospectus may be obtained by contacting your Investment Consultant.

Table of Contents

Dear Shareholder,

Please find enclosed the Annual Report for the PIMCO Equity Series VIT covering the twelve-month reporting period ended December 31, 2015. The following pages contain specific details about the investment performance of the Portfolio and a discussion of the factors that most affected performance during the reporting period.

Highlights of the financial markets during the twelve-month reporting period include:

| n | Heightened market volatility throughout the reporting period was sparked by a mix of investor concerns including geopolitical developments, monetary policy and the potential for slowing global economic growth, which generally contributed to dampened investor sentiment. In particular, increasing concern over the outlook for Chinese growth sent commodity prices and inflation expectations lower, while also negatively impacting prices of emerging market (“EM”) debt and equities. In addition, the Chinese equity market began a strong decline in June 2015, which prompted the Chinese government to prop-up equity share prices and devalue the Chinese yuan. Volatility in Chinese equity markets continued into January 2016 on renewed concern over slowing Chinese economic growth. Furthermore, rising tension in the Middle East and the continued debt crisis in Greece also contributed to investor unease throughout the reporting period. |

| n | Economic data in the U.S. continued to confirm a healthy economy, particularly labor market indicators such as employment and wages. Still, signs of caution remained, particularly as U.S. consumers appeared to be more selective in their spending and chose to save rather than spend their windfall from lower gas prices. Additionally, consumer sentiment and certain housing indicators softened towards the end of the reporting period, and December 2015 U.S. manufacturing data indicated the fastest contraction in six years. Within the Eurozone, volatility increased despite gradual improvement in the underlying economies. Eurozone economic data also showed generally positive signs of an early recovery but were tempered slightly by sluggish inflation. |

| n | The theme of divergent global central bank monetary policy continued throughout the reporting period. The European Central Bank (“ECB”) expressed its commitment to increase quantitative easing (or large-scale asset purchases), along with the Bank of Japan and the People’s Bank of China who also indicated their intent to accelerate such measures. The Federal Reserve (“Fed”), on the other hand, moved on December 16 to raise the Federal Funds Rate by 0.25% to a new range of 0.25% - 0.50%, marking its first rate hike in nine years. However, the Fed noted that future increases in its target rate would be “gradual” and in-line with their previous projections, which helped to ease investor concerns. Outside of the reporting period on January 27, the Fed opted to leave the Federal Funds Rate unchanged, noting their intent to closely monitor how the global economy and markets influence the U.S. economic outlook. |

| n | Equity markets showed mixed performance globally amid a period marked by economic uncertainty, increased volatility and divergent central bank monetary policy. U.S. equities, as represented by the S&P 500 Index, returned 1.38% (on a total return basis) and developed market equities outside the U.S., as represented by the MSCI EAFE Net Dividend Index (USD Unhedged), declined 0.81% over the reporting period. However, ultra-easy monetary policy in Europe and Japan benefited European and Japanese equity markets, which generally posted positive returns. |

| n | EM equities, as represented by the MSCI Emerging Markets Index (Net Dividends in USD), declined 14.92% over the same period, due to headwinds from a stronger U.S. dollar, falling commodity prices, concerns over slower Chinese economic growth, and declining Chinese equities. Chinese stocks reached all-time highs midway through the reporting period before declining over the second half of the reporting period as several attempts to support the Chinese equity market by the People’s Bank of China, along with persistently weak economic data, highlighted the country’s decelerating growth. In addition, Brazil’s economic and political woes continued throughout the year as the Brazilian real fell 33% against the U.S. dollar and the country’s credit rating was downgraded by S&P and Fitch to sub-investment grade. These events, along with general anticipation of the |

| 2 | PIMCO EQUITY SERIES VIT |

Table of Contents

Fed’s first rate hike in nearly a decade, were contributing factors to EM equity underperformance relative to most developed market equities. |

| n | Style-wise, growth equities outperformed value globally as the MSCI All Country World Growth Index (Net Dividends in USD) returned 1.55% and the MSCI All Country World Value Index (Net Dividends in USD) declined 6.26% over the reporting period. The healthcare and consumer staples sectors were the top performing equity sectors, while the energy and materials sectors were the worst performing equity sectors over the reporting period. |

| n | U.S. Treasuries, as represented by the Barclays U.S. Treasury Index, returned 0.84% for the reporting period as yields generally rose slightly across the Treasury yield curve. The benchmark ten-year U.S. Treasury note yielded 2.27% at the end of the reporting period, up from 2.17% on December 31, 2014. The Barclays U.S. Aggregate Index, a widely used index of U.S. investment-grade bonds, returned 0.55% for the reporting period. |

Thank you again for the trust you have placed in us. We value your commitment and will continue to work diligently to meet your broad investment needs.

| Sincerely,

Brent R. Harris Chairman of the Board, PIMCO Equity Series VIT

February 18, 2016 |

| ANNUAL REPORT | DECEMBER 31, 2015 | 3 |

Table of Contents

Important Information About the Portfolio

PIMCO Equity Series VIT (the “Trust”) is an open-end management investment company currently consisting of one investment portfolio, the PIMCO Global Dividend Portfolio (formerly known as the PIMCO EqS Pathfinder Portfolio®) (the “Portfolio”). The Portfolio is only available as a funding vehicle under variable life insurance policies or variable annuity contracts issued by insurance companies (“Variable Contracts”). Individuals may not purchase shares of the Portfolio directly. Shares of the Portfolio also may be sold to qualified pension and retirement plans outside of the separate account context.

The Portfolio seeks to provide current income that exceeds the average yield on global stocks by investing under normal circumstances at least 75% of its assets in equity and equity-related securities, including common and preferred stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock), as well as securities issued by real estate investment trusts, master limited partnerships and other equity trusts and depositary receipts. When making equity investments, PIMCO may use bottom-up, fundamental analysis to seek to identify attractively valued issuers that currently pay dividends and have the potential for earnings and dividend growth over time. In pursuing its objective to provide current income, the Portfolio may employ a so-called “dividend capture” strategy. As described in greater detail in the Portfolio’s prospectus, this strategy is designed to opportunistically increase the Portfolio’s income through a short-term holding.

The values of equity securities, such as common stocks and preferred stocks, have historically risen and fallen in periodic cycles and may decline due to general market conditions, which are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. Equity securities may also decline due to factors that affect a particular industry or industries, such as labor shortages, increased production costs and competitive conditions within an industry. In addition, the value of an equity security may decline for a number of reasons that directly relate to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services, as well as the historical and prospective earnings of the issuer and the value of its assets. Different types of equity securities may react differently to these developments and a change in the financial condition of a single issuer may affect securities markets as a whole.

During a general downturn in the securities markets, multiple asset classes, including equity securities, may decline in value simultaneously. The market price of equity securities owned by a Portfolio may go up or down, sometimes rapidly or unpredictably. Equity securities generally have greater price volatility than fixed income securities and common

stocks generally have the greatest appreciation and depreciation potential of all corporate securities. As of the date of this report, Europe is one of the worst performing regions for equity markets, as deflationary concerns weighed on the values of equity securities.

The Portfolio may be subject to various risks as described in the Portfolio’s prospectus. Some of these risks may include, but are not limited to, the following: equity risk, dividend-oriented stocks risk, value investing risk, foreign (non-U.S.) investment risk, emerging markets risk, sovereign debt risk, market risk, issuer risk, interest rate risk, call risk, credit risk, high yield and distressed company risk, currency risk, real estate risk, liquidity risk, leveraging risk, management risk, small-cap and mid-cap company risk, derivatives risk, short sale risk and convertible securities risk. A complete description of these and other risks is contained in the Portfolio’s prospectus.

The Portfolio may use derivative instruments for hedging purposes or as part of an investment strategy. Use of these instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, leverage risk, management risk and the risk that the Portfolio may not be able to close out a position when it would be most advantageous to do so. Certain derivative transactions may have a leveraging effect on the Portfolio. For example, a small investment in a derivative instrument may have a significant impact on the Portfolio’s exposure to interest rates, currency exchange rates or other investments. As a result, a relatively small price movement in an asset, investment or component of the index underlying a derivative instrument may cause an immediate and substantial loss or gain, which translates into heightened volatility for the Portfolio. The Portfolio may engage in such transactions regardless of whether the Portfolio owns the asset, instrument or components of the index underlying the derivative instrument. The Portfolio may invest a significant portion of its assets in these types of instruments. If it does, the Portfolio’s investment exposure could far exceed the value of its portfolio securities and its investment performance could be primarily dependent upon securities it does not own. The Portfolio’s investment in foreign (non-U.S.) securities may entail risk due to foreign (non-U.S.) economic and political developments; this risk may be increased when investing in emerging markets.

The value of an equity security of an issuer that has paid dividends in the past may decrease if the issuer reduces or eliminates future payments to its shareholders. If the dividends or distributions received by a Portfolio decrease, the Portfolio may have less income to distribute to the Portfolio’s shareholders. In addition, during certain market conditions, the equity securities of issuers that have paid regular dividends or distributions may not be widely available or may be highly concentrated in particular sectors of the market. A Portfolio may invest a significant portion of its assets in value stocks. Value stocks may

| 4 | PIMCO EQUITY SERIES VIT |

Table of Contents

perform differently from other types of stocks and the market as a whole. A value stock may decrease in price or may not increase in price as anticipated by PIMCO if it continues to be undervalued by the market or the factors that the portfolio manager believes will cause the stock price to increase do not occur.

The geographical classification of foreign (non-U.S.) securities in this report are classified by the country of incorporation of a holding. In certain instances, a security’s country of incorporation may be different from its country of economic exposure.

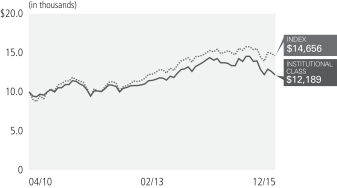

On the Portfolio Summary page in this Shareholder Report, the Average Annual Total Return table and Cumulative Returns chart measure

performance assuming that any dividend and capital gain distributions were reinvested. The Cumulative Returns chart reflects only Institutional Class performance. Performance for the Class M, Administrative Class and Advisor Class shares, if applicable, may be higher or lower based on each class’s expense ratios. The Portfolio’s total annual operating expense ratios on the Portfolio Summary page are as of the currently effective prospectus, as supplemented to date. The Portfolio measures its performance against a broad-based securities market index (benchmark index). The benchmark index does not take into account fees, expenses, or taxes. The Portfolio’s past performance, before and after taxes, is not necessarily an indication of how the Portfolio will perform in the future.

The following table discloses the inception dates of the Portfolio and its respective share classes along with the Portfolio’s diversification status as of period end:

| Portfolio Name | Portfolio Inception | Institutional Class | Class M | Administrative Class | Advisor Class | Diversification Status | ||||||||||||||||||||

PIMCO Global Dividend Portfolio | 04/14/10 | 04/14/10 | — | — | 04/14/10 | Diversified | ||||||||||||||||||||

An investment in the Portfolio is not a deposit of a bank and is not guaranteed or insured by the Federal Deposit Insurance Corporation or any other government agency. It is possible to lose money on investments in the Portfolio.

The Trustees are responsible generally for overseeing the management of the Trust. The Trustees authorize the Trust to enter into service agreements with the Adviser, the Distributor, the Administrator and other service providers in order to provide, and in some cases authorize service providers to procure through other parties, necessary or desirable services on behalf of the Trust and the Portfolio. Shareholders are not parties to or third-party beneficiaries of such service agreements. Neither this Portfolio’s prospectus nor summary prospectus, the Trust’s Statement of Additional Information (“SAI”), any contracts filed as exhibits to the Trust’s registration statement, nor any other communications, disclosure documents or regulatory filings (including this report) from or on behalf of the Trust or the Portfolio creates a contract between or among any shareholder of the Portfolio, on the one hand, and the Trust, the Portfolio, a service provider to the Trust or the Portfolio, and/or the Trustees or officers of the Trust, on the other hand. The Trustees (or the Trust and its officers, service providers or other delegates acting under authority of the Trustees) may amend the most recent prospectus or use a new prospectus, summary prospectus or SAI with respect to the Portfolio or the Trust, and/or amend, file and/or issue any other communications, disclosure documents or regulatory filings, and may amend or enter into any contracts to which the Trust or the Portfolio is a party, and interpret the investment objectives, policies, restrictions and contractual provisions applicable to the Portfolio, without shareholder input or approval,

except in circumstances in which shareholder approval is specifically required by law (such as changes to fundamental investment policies) or where a shareholder approval requirement is specifically disclosed in the Trust’s then-current prospectus or SAI.

PIMCO has adopted written proxy voting policies and procedures (“Proxy Policy”) as required by Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted by the Trust as the policies and procedures that PIMCO will use when voting proxies on behalf of the Portfolio. A description of the policies and procedures that PIMCO uses to vote proxies relating to portfolio securities of the Portfolio, and information about how the Portfolio voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30, are available without charge, upon request, by calling the Trust at (888) 87-PIMCO, on the Portfolio’s website at pvit.pimco-funds.com, and on the Securities and Exchange Commission’s (“SEC”) website at www.sec.gov.

The Portfolio files a complete schedule of the Portfolio’s holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. A copy of the Portfolio’s Form N-Q is available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. The Portfolio’s Form N-Q will also be available without charge, upon request, by calling the Trust at (888) 87-PIMCO and on the Portfolio’s website at pvit.pimco-funds.com. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

PIMCO Equity Series VIT is distributed by PIMCO Investments LLC, 1633 Broadway, New York, New York 10019.

| ANNUAL REPORT | DECEMBER 31, 2015 | 5 |

Table of Contents

PIMCO Global Dividend Portfolio (Consolidated)

Cumulative Returns Through December 31, 2015

Investment Objective and Strategy Overview

| » | The PIMCO Global Dividend Portfolio seeks to provide current income that exceeds the average yield on global stocks. The Portfolio’s secondary objective is to seek to provide long-term capital appreciation. The Portfolio seeks to achieve its investment objective by investing under normal circumstances at least 75% of its assets in equity and equity-related securities, including common and preferred stock (and securities convertible into, or that Pacific Investment Management Company LLC (“PIMCO”) expects to be exchanged for, common or preferred stock), as well as securities issued by real estate investment trusts, master limited partnerships and other equity trusts and depositary receipts. The Portfolio may invest in securities issued by large-capitalization, mid-capitalization and small-capitalization companies. In pursuing its investment objective to provide current income, the Portfolio may use a so-called “dividend capture” strategy, which is designed to opportunistically increase the Portfolio’s income though a short-term holding. |

| Average Annual Total Return for the period ended December 31, 2015 | ||||||||||||||

| 1 Year | 5 Year | Fund Inception (04/14/2010) | ||||||||||||

| PIMCO Global Dividend Portfolio Institutional Class | (8.75)% | 2.97% | 3.18% | ||||||||||

| PIMCO Global Dividend Portfolio Advisor Class | (8.98)% | 2.74% | 2.94% | |||||||||||

| MSCI All Country World Index± | (2.36)% | 6.09% | 6.34% | ||||||||||

All Portfolio returns are net of fees and expenses.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. The Portfolio’s performance does not reflect the deduction of additional charges and expenses imposed in connection with investing in Variable Contracts, which will reduce returns. For performance current to the most recent month-end, visit pvit.pimco-funds.com. The Portfolio’s total annual operating expense ratio as stated in the Portfolio’s current prospectus, as supplemented to date, is 1.07% for Institutional Class shares, and 1.32% for Advisor Class shares.

± The MSCI All Country World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The Index consists of 46 country indices comprising 23 developed and 23 emerging market country indices.

It is not possible to invest in an unmanaged index.

| 6 | PIMCO EQUITY SERIES VIT |

Table of Contents

Top 10 Holdings1

Vodafone Group PLC | 3.7% | |||||

Aegon NV | 3.1% | |||||

QUALCOMM, Inc. | 3.0% | |||||

AT&T, Inc. | 3.0% | |||||

PG&E Corp. | 3.0% | |||||

Lloyds Banking Group PLC | 2.9% | |||||

Western Digital Corp. | 2.9% | |||||

China Mobile Ltd. | 2.8% | |||||

Pfizer, Inc. | 2.7% | |||||

HSBC Holdings PLC | 2.7% |

Geographic Breakdown1

United States | 52.2% | |||||

United Kingdom | 12.9% | |||||

Netherlands | 4.1% | |||||

Italy | 3.9% | |||||

Japan | 3.8% | |||||

France | 3.5% | |||||

Australia | 3.3% | |||||

Hong Kong | 2.8% | |||||

Switzerland | 2.2% | |||||

Spain | 1.6% | |||||

Taiwan | 1.5% | |||||

Canada | 1.4% | |||||

Greece | 1.2% | |||||

Germany | 1.1% | |||||

Brazil | 1.1% | |||||

Other | 0.9% |

1 % of Investments, at value as of 12/31/2015. Top 10 Holdings and Geographic Breakdown solely reflect long positions. Securities sold short, financial derivative instruments and short-term instruments are not taken into consideration.

Portfolio Insights

| » | Stock selection in the software and technology hardware storage & peripherals industries detracted from relative returns, as the Portfolio’s holdings within these industries significantly underperformed the MSCI All Country World Index over the reporting period. |

| » | Stock selection in the oil gas & consumable fuels industry also detracted from relative returns as the Portfolio’s holdings, notably Golar LNG Partners LP and Targa Resources Corp., underperformed the MSCI All Country World Index over the reporting period. |

| » | Overweight exposure to the tobacco and chemicals industries positively contributed to relative returns, as the Portfolio’s holdings within these industries outperformed the MSCI All Country World Index over the reporting period. |

| » | Over the reporting period, the top three contributors to performance were Aena SA, Imperial Tobacco Group PLC and NN Group NV, while the top three detractors from performance were Targa Resources Corp., Tronox Ltd. and Golar LNG Partners LP. |

| ANNUAL REPORT | DECEMBER 31, 2015 | 7 |

Table of Contents

Expense Example PIMCO Global Dividend Portfolio (Consolidated)

Example

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees (if applicable), and other Portfolio expenses. The Example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The Expense Example does not reflect any fees or other expenses imposed by the Variable Contracts. If it did, the expenses reflected in the Expense Example would be higher. The Example is based on an investment of $1,000 invested at the beginning of the period and held from July 1, 2015 to December 31, 2015 unless noted otherwise in the table and footnotes below.

Actual Expenses

The information in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = $8.60), then multiply the result by the number in the appropriate column for your share class, in the column titled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other portfolios.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the information under the heading “Hypothetical (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different portfolios. In addition, if these transactional costs were included, your costs would have been higher.

Expense ratios may vary period to period because of various factors, such as an increase in expenses that are not covered by the management fees such as fees and expenses of the independent trustees and their counsel, extraordinary expenses and interest expense.

| Actual | Hypothetical (5% return before expenses) | |||||||||||||||||||||||||||||||||

| Beginning Account Value (07/01/15) | Ending Account Value (12/31/15) | Expenses Paid During Period* | Beginning Account Value (07/01/15) | Ending Account Value (12/31/15) | Expenses Paid During Period* | Net Annualized Expense Ratio** | ||||||||||||||||||||||||||||

| Institutional Class | $ | 1,000.00 | $ | 876.60 | $ | 4.28 | $ | 1,000.00 | $ | 1,021.06 | $ | 4.61 | 0.89 | % | ||||||||||||||||||||

| Advisor Class | 1,000.00 | 875.60 | 5.48 | 1,000.00 | 1,019.78 | 5.90 | 1.14 | |||||||||||||||||||||||||||

* Expenses Paid During Period are equal to the net annualized expense ratio for the class, multiplied by the average account value over the period, multiplied by 187/365 (to reflect the one-half year period). Overall fees and expenses of investing in the Portfolio will be higher because the example does not reflect variable contract fees and expenses.

** Net Annualized Expense Ratio is reflective of any applicable contractual fee waivers and/or expense reimbursements or voluntary fee waivers. Details regarding fee waivers can be found in Note 9 in the Notes to Financial Statements.

| 8 | PIMCO EQUITY SERIES VIT |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| ANNUAL REPORT | DECEMBER 31, 2015 | 9 |

Table of Contents

Financial Highlights PIMCO Global Dividend Portfolio (Consolidated)

| Selected Per Share Data for the Year Ended: | Net Asset Value Beginning of Year | Net Investment Income (a) | Net Realized/ Unrealized Gain (Loss) | Total from Investment Operations | Dividends from Net Investment Income (b) | Distributions from Net Realized Capital Gains (b) | Total Distributions | |||||||||||||||||||||

| Institutional Class | ||||||||||||||||||||||||||||

12/31/2015 | $ | 12.46 | $ | 0.34 | $ | (1.43 | ) | $ | (1.09 | ) | $ | (0.63 | ) | $ | (1.22 | ) | $ | (1.85 | ) | |||||||||

12/31/2014 | 12.53 | 0.29 | (0.16 | ) | 0.13 | 0.00 | (0.20 | ) | (0.20 | ) | ||||||||||||||||||

12/31/2013 | 10.72 | 0.27 | 1.83 | 2.10 | (0.29 | ) | 0.00 | (0.29 | ) | |||||||||||||||||||

12/31/2012 | 9.85 | 0.21 | 0.77 | 0.98 | (0.11 | ) | 0.00 | (0.11 | ) | |||||||||||||||||||

12/31/2011 | 10.33 | 0.11 | (0.58 | ) | (0.47 | ) | (0.01 | ) | 0.00 | (0.01 | ) | |||||||||||||||||

| Advisor Class | ||||||||||||||||||||||||||||

12/31/2015 | 12.39 | 0.30 | (1.42 | ) | (1.12 | ) | (0.61 | ) | (1.22 | ) | (1.83 | ) | ||||||||||||||||

12/31/2014 | 12.48 | 0.25 | (0.14 | ) | 0.11 | 0.00 | (0.20 | ) | (0.20 | ) | ||||||||||||||||||

12/31/2013 | 10.69 | 0.24 | 1.81 | 2.05 | (0.26 | ) | 0.00 | (0.26 | ) | |||||||||||||||||||

12/31/2012 | 9.82 | 0.18 | 0.78 | 0.96 | (0.09 | ) | 0.00 | (0.09 | ) | |||||||||||||||||||

12/31/2011 | 10.31 | 0.08 | (0.57 | ) | (0.49 | ) | 0.00 | 0.00 | 0.00 | |||||||||||||||||||

| (a) | Per share amounts based on average number of shares outstanding during the year. |

| (b) | Determined in accordance with federal income tax regulations, see Note 2(d) in the Notes to Financial Statements for more information. |

| (c) | Effective July 13, 2015, the Portfolio’s advisory fee was decreased by 0.06% to an annual rate of 0.69%. |

| 10 | PIMCO EQUITY SERIES VIT | See Accompanying Notes |

Table of Contents

| Net Asset Value End of Year | Total Return | Net Assets End of Year (000s) | Ratio of Expenses to Average Net Assets | Ratio of Expenses to Average Net Assets Excluding Waivers | Ratio of Expenses to Average Net Assets Excluding Interest Expense | Ratio of Expenses to Average Net Assets Excluding Interest Expense and Waivers | Ratio of Net Investment Income to Average Net Assets | Portfolio Turnover Rate | ||||||||||||||||||||||||||

| $ | 9.52 | (8.75 | )% | $ | 40,582 | 0.95 | %(c) | 1.10 | %(c) | 0.93 | %(c) | 1.08 | %(c) | 2.68 | % | 152 | % | |||||||||||||||||

| 12.46 | 1.06 | 52,234 | 0.98 | 1.12 | 0.97 | 1.11 | 2.22 | 31 | ||||||||||||||||||||||||||

| 12.53 | 19.60 | 57,768 | 0.98 | 1.15 | 0.97 | 1.14 | 2.29 | 29 | ||||||||||||||||||||||||||

| 10.72 | 9.98 | 58,740 | 0.99 | 1.15 | 0.97 | 1.13 | 2.02 | 26 | ||||||||||||||||||||||||||

| 9.85 | (4.54 | ) | 66,439 | 0.98 | 1.18 | 0.97 | 1.17 | 1.14 | 238 | |||||||||||||||||||||||||

| 9.44 | (8.98 | ) | 284,406 | 1.20 | (c) | 1.35 | (c) | 1.18 | (c) | 1.33 | (c) | 2.43 | 152 | |||||||||||||||||||||

| 12.39 | 0.90 | 380,293 | 1.23 | 1.37 | 1.22 | 1.36 | 1.98 | 31 | ||||||||||||||||||||||||||

| 12.48 | 19.19 | 449,196 | 1.23 | 1.40 | 1.22 | 1.39 | 2.05 | 29 | ||||||||||||||||||||||||||

| 10.69 | 9.77 | 413,524 | 1.24 | 1.40 | 1.22 | 1.38 | 1.77 | 26 | ||||||||||||||||||||||||||

| 9.82 | (4.72 | ) | 387,651 | 1.23 | 1.43 | 1.22 | 1.42 | 0.83 | 238 | |||||||||||||||||||||||||

| See Accompanying Notes | ANNUAL REPORT | DECEMBER 31, 2015 | 11 |

Table of Contents

Consolidated Statement of Assets and Liabilities PIMCO Global Dividend Portfolio

| (Amounts in thousands, except per share amounts) | December 31, 2015 | |||

Assets: | ||||

Investments, at value | ||||

Investments in securities* | $ | 321,783 | ||

Investments in Affiliates | 5,659 | |||

Financial Derivative Instruments | ||||

Over the counter | 854 | |||

Foreign currency, at value | 76 | |||

Receivable for investments sold | 2,978 | |||

Interest and dividends receivable | 1,039 | |||

Dividends receivable from Affiliates | 3 | |||

Reimbursement receivable from PIMCO | 11 | |||

Total Assets | 332,403 | |||

Liabilities: | ||||

Financial Derivative Instruments | ||||

Over the counter | $ | 1,166 | ||

Payable for investments purchased | 5,229 | |||

Payable for investments in Affiliates purchased | 3 | |||

Deposits from counterparty | 450 | |||

Payable for Portfolio shares redeemed | 135 | |||

Accrued investment advisory fees | 160 | |||

Accrued supervisory and administrative fees | 106 | |||

Accrued distribution fees | 66 | |||

Other liabilities | 100 | |||

Total Liabilities | 7,415 | |||

Net Assets | $ | 324,988 | ||

Net Assets Consist of: | ||||

Paid in capital | $ | 292,521 | ||

Undistributed net investment income | 14,673 | |||

Accumulated undistributed net realized gain | 52,343 | |||

Net unrealized (depreciation) | (34,549 | ) | ||

| $ | 324,988 | |||

Net Assets: | ||||

Institutional Class | $ | 40,582 | ||

Advisor Class | 284,406 | |||

Shares Issued and Outstanding: | ||||

Institutional Class | 4,261 | |||

Advisor Class | 30,136 | |||

Net Asset Value and Redemption Price Per Share Outstanding: | ||||

Institutional Class | $ | 9.52 | ||

Advisor Class | 9.44 | |||

Cost of investments in securities | $ | 356,005 | ||

Cost of investments in Affiliates | $ | 5,659 | ||

Cost of foreign currency held | $ | 76 | ||

* Includes repurchase agreements of: | $ | 1,716 | ||

| 12 | PIMCO EQUITY SERIES VIT | See Accompanying Notes |

Table of Contents

Consolidated Statement of Operations PIMCO Global Dividend Portfolio

| (Amounts in thousands) | Year Ended December 31, 2015 | |||

Investment Income: | ||||

Interest | $ | 2 | ||

Dividends, net of foreign taxes* | 14,440 | |||

Dividends from Investments in Affiliates | 67 | |||

Total Income | 14,509 | |||

Expenses: | ||||

Investment advisory fees | 2,886 | |||

Supervisory and administrative fees | 1,395 | |||

Distribution and/or servicing fees - Advisor Class | 873 | |||

Dividends on short sales | 74 | |||

Trustee fees | 47 | |||

Interest expense | 9 | |||

Miscellaneous expense | 20 | |||

Total Expenses | 5,304 | |||

Waiver and/or Reimbursement by PIMCO | (616 | ) | ||

Net Expenses | 4,688 | |||

Net Investment Income | 9,821 | |||

Net Realized Gain (Loss): | ||||

Investments in securities | 51,958 | |||

Investments in Affiliates | (109 | ) | ||

Exchange-traded or centrally cleared financial derivative instruments | (362 | ) | ||

Over the counter financial derivative instruments | 8,933 | |||

Short sales | 771 | |||

Foreign currency | (295 | ) | ||

Net Realized Gain | 60,896 | |||

Net Change in Unrealized Appreciation (Depreciation): | ||||

Investments in securities | (98,116 | ) | ||

Investments in Affiliates | 72 | |||

Over the counter financial derivative instruments | (4,186 | ) | ||

Short sales | 489 | |||

Foreign currency assets and liabilities | 38 | |||

Net Change in Unrealized (Depreciation) | (101,703 | ) | ||

Net (Decrease) in Net Assets Resulting from Operations | $ | (30,986 | ) | |

* Foreign tax withholdings - Dividends | $ | 504 | ||

| See Accompanying Notes | ANNUAL REPORT | DECEMBER 31, 2015 | 13 |

Table of Contents

Consolidated Statements of Changes in Net Assets PIMCO Global Dividend Portfolio

| (Amounts in thousands†) | Year Ended December 31, 2015 | Year Ended December 31, 2014 | ||||||

(Decrease) in Net Assets from: | ||||||||

Operations: | ||||||||

Net investment income | $ | 9,821 | $ | 9,672 | ||||

Net realized gain | 60,896 | 39,750 | ||||||

Net change in unrealized (depreciation) | (101,703 | ) | (43,148 | ) | ||||

Net Increase (Decrease) in Net Assets Resulting from Operations | (30,986 | ) | 6,274 | |||||

Distributions to Shareholders: | ||||||||

From net investment income (a) | ||||||||

Institutional Class | (2,489 | ) | 0 | |||||

Advisor Class | (17,274 | ) | 0 | |||||

From net realized capital gains (a) | ||||||||

Institutional Class | (4,384 | ) | (841 | ) | ||||

Advisor Class | (30,972 | ) | (6,209 | ) | ||||

Total Distributions | (55,119 | ) | (7,050 | ) | ||||

Portfolio Share Transactions: | ||||||||

Net (decrease) resulting from Portfolio share transactions** | (21,434 | ) | (73,661 | ) | ||||

Total (Decrease) in Net Assets | (107,539 | ) | (74,437 | ) | ||||

Net Assets: | ||||||||

Beginning of year | 432,527 | 506,964 | ||||||

End of year* | $ | 324,988 | $ | 432,527 | ||||

* Including undistributed net investment income of: | $ | 14,673 | $ | 16,322 | ||||

| † | A zero balance may reflect actual amounts rounding to less than one thousand. |

| ** | See Note 13 in the Notes to Financial Statements. |

| (a) | Determined in accordance with federal income tax regulations, see Note 2(d) in the Notes to Financial Statements for more information. |

| 14 | PIMCO EQUITY SERIES VIT | See Accompanying Notes |

Table of Contents

Consolidated Schedule of Investments PIMCO Global Dividend Portfolio

December 31, 2015

| SHARES | MARKET VALUE (000S) | |||||||||||

| INVESTMENTS IN SECURITIES 99.1% | ||||||||||||

| COMMON STOCKS 95.2% | ||||||||||||

| AUSTRALIA 3.4% | ||||||||||||

| CONSUMER DISCRETIONARY 1.2% | ||||||||||||

G8 Education Ltd. | 1,486,026 | $ | 3,843 | |||||||||

|

| |||||||||||

| HEALTH CARE 1.0% | ||||||||||||

Sonic Healthcare Ltd. | 253,434 | 3,281 | ||||||||||

|

| |||||||||||

| INDUSTRIALS 1.2% | ||||||||||||

Spotless Group Holdings Ltd. | 4,911,980 | 3,849 | ||||||||||

|

| |||||||||||

Total Australia | 10,973 | |||||||||||

|

| |||||||||||

| BRAZIL 1.1% | ||||||||||||

| HEALTH CARE 0.5% | ||||||||||||

Qualicorp S.A. | 424,006 | 1,508 | ||||||||||

|

| |||||||||||

| UTILITIES 0.6% | ||||||||||||

Light S.A. | 790,900 | 1,974 | ||||||||||

|

| |||||||||||

Total Brazil | 3,482 | |||||||||||

|

| |||||||||||

| CANADA 1.4% | ||||||||||||

| UTILITIES 1.4% | ||||||||||||

Capital Power Corp. | 362,476 | 4,655 | ||||||||||

|

| |||||||||||

Total Canada | 4,655 | |||||||||||

|

| |||||||||||

| FRANCE 3.5% | ||||||||||||

| CONSUMER STAPLES 1.2% | ||||||||||||

Carrefour S.A. | 138,095 | 3,985 | ||||||||||

|

| |||||||||||

| UTILITIES 2.3% | ||||||||||||

Engie S.A. | 419,384 | 7,429 | ||||||||||

|

| |||||||||||

Total France | 11,414 | |||||||||||

|

| |||||||||||

| GERMANY 1.1% | ||||||||||||

| MATERIALS 1.1% | ||||||||||||

Covestro AG (a) | 95,849 | 3,503 | ||||||||||

|

| |||||||||||

Total Germany | 3,503 | |||||||||||

|

| |||||||||||

| GREECE 1.2% | ||||||||||||

| CONSUMER DISCRETIONARY 1.2% | ||||||||||||

OPAP S.A. | 436,492 | 3,830 | ||||||||||

|

| |||||||||||

Total Greece | 3,830 | |||||||||||

|

| |||||||||||

| HONG KONG 2.8% | ||||||||||||

| TELECOMMUNICATION SERVICES 2.8% | ||||||||||||

China Mobile Ltd. | 801,000 | 9,016 | ||||||||||

|

| |||||||||||

Total Hong Kong | 9,016 | |||||||||||

|

| |||||||||||

| ITALY 3.9% | ||||||||||||

| FINANCIALS 2.7% | ||||||||||||

Intesa Sanpaolo SpA | 2,606,475 | 8,656 | ||||||||||

|

| |||||||||||

| SHARES | MARKET VALUE (000S) | |||||||||||

| INDUSTRIALS 1.2% | ||||||||||||

Societa Iniziative Autostradali e Servizi SpA | 380,886 | $ | 4,047 | |||||||||

|

| |||||||||||

Total Italy | 12,703 | |||||||||||

|

| |||||||||||

| JAPAN 3.8% | ||||||||||||

| CONSUMER DISCRETIONARY 1.5% | ||||||||||||

Bridgestone Corp. | 144,385 | 4,952 | ||||||||||

|

| |||||||||||

| TELECOMMUNICATION SERVICES 2.3% | ||||||||||||

Nippon Telegraph & Telephone Corp. | 188,925 | 7,519 | ||||||||||

|

| |||||||||||

Total Japan | 12,471 | |||||||||||

|

| |||||||||||

| MEXICO 0.5% | ||||||||||||

| CONSUMER STAPLES 0.5% | ||||||||||||

Coca-Cola Femsa S.A.B. de C.V. ‘L’ | 225,800 | 1,615 | ||||||||||

|

| |||||||||||

Total Mexico | 1,615 | |||||||||||

|

| |||||||||||

| NETHERLANDS 4.1% | ||||||||||||

| FINANCIALS 4.1% | ||||||||||||

Aegon NV | 1,775,701 | 10,043 | ||||||||||

NN Group NV | 92,542 | 3,265 | ||||||||||

|

| |||||||||||

Total Netherlands | 13,308 | |||||||||||

|

| |||||||||||

| RUSSIA 0.5% | ||||||||||||

| CONSUMER STAPLES 0.5% | ||||||||||||

Magnit PJSC SP - GDR | 35,479 | 1,427 | ||||||||||

|

| |||||||||||

Total Russia | 1,427 | |||||||||||

|

| |||||||||||

| SPAIN 1.6% | ||||||||||||

| CONSUMER STAPLES 1.6% | ||||||||||||

Ebro Foods S.A. | 270,685 | 5,325 | ||||||||||

|

| |||||||||||

Total Spain | 5,325 | |||||||||||

|

| |||||||||||

| SWITZERLAND 2.3% | ||||||||||||

| HEALTH CARE 2.3% | ||||||||||||

Roche Holding AG | 26,491 | 7,341 | ||||||||||

|

| |||||||||||

Total Switzerland | 7,341 | |||||||||||

|

| |||||||||||

| TAIWAN 1.5% | ||||||||||||

| INFORMATION TECHNOLOGY 1.5% | ||||||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. | 1,149,652 | 4,960 | ||||||||||

|

| |||||||||||

Total Taiwan | 4,960 | |||||||||||

|

| |||||||||||

| UNITED KINGDOM 13.0% | ||||||||||||

| CONSUMER STAPLES 1.1% | ||||||||||||

Imperial Tobacco Group PLC | 64,789 | 3,422 | ||||||||||

|

| |||||||||||

| ENERGY 1.0% | ||||||||||||

Golar LNG Partners LP | 255,140 | 3,414 | ||||||||||

|

| |||||||||||

| SHARES | MARKET VALUE (000S) | |||||||||||

| FINANCIALS 7.2% | ||||||||||||

HSBC Holdings PLC | 1,116,392 | $ | 8,813 | |||||||||

ICAP PLC | 645,828 | 4,848 | ||||||||||

Lloyds Banking Group PLC | 8,969,857 | 9,651 | ||||||||||

|

| |||||||||||

| 23,312 | ||||||||||||

|

| |||||||||||

| TELECOMMUNICATION SERVICES 3.7% | ||||||||||||

Vodafone Group PLC | 3,730,644 | 12,098 | ||||||||||

|

| |||||||||||

Total United Kingdom | 42,246 | |||||||||||

|

| |||||||||||

| UNITED STATES 49.5% | ||||||||||||

| CONSUMER DISCRETIONARY 8.8% | ||||||||||||

Comcast Corp. ‘A’ | 128,740 | 7,265 | ||||||||||

General Motors Co. | 236,850 | 8,055 | ||||||||||

Kohl’s Corp. | 69,565 | 3,313 | ||||||||||

Macy’s, Inc. | 92,407 | 3,233 | ||||||||||

SeaWorld Entertainment, Inc. | 179,073 | 3,526 | ||||||||||

Time Warner, Inc. | 50,908 | 3,292 | ||||||||||

|

| |||||||||||

| 28,684 | ||||||||||||

|

| |||||||||||

| ENERGY 1.9% | ||||||||||||

Schlumberger Ltd. | 88,822 | 6,195 | ||||||||||

|

| |||||||||||

| FINANCIALS 6.7% | ||||||||||||

Blackstone Group LP | 253,121 | 7,401 | ||||||||||

Navient Corp. | 260,095 | 2,978 | ||||||||||

Prudential Financial, Inc. | 79,418 | 6,466 | ||||||||||

Regions Financial Corp. | 506,387 | 4,861 | ||||||||||

|

| |||||||||||

| 21,706 | ||||||||||||

|

| |||||||||||

| HEALTH CARE 7.5% | ||||||||||||

AbbVie, Inc. | 140,181 | 8,304 | ||||||||||

Merck & Co., Inc. | 135,051 | 7,134 | ||||||||||

Pfizer, Inc. | 276,397 | 8,922 | ||||||||||

|

| |||||||||||

| 24,360 | ||||||||||||

|

| |||||||||||

| INDUSTRIALS 2.0% | ||||||||||||

Neilsen Holdings PLC | 141,080 | 6,574 | ||||||||||

|

| |||||||||||

| INFORMATION TECHNOLOGY 12.3% | ||||||||||||

Apple, Inc. | 68,285 | 7,188 | ||||||||||

Cisco Systems, Inc. | 292,650 | 7,947 | ||||||||||

QUALCOMM, Inc. | 198,466 | 9,920 | ||||||||||

Symantec Corp. | 261,597 | 5,494 | ||||||||||

Western Digital Corp. | 157,135 | 9,436 | ||||||||||

|

| |||||||||||

| 39,985 | ||||||||||||

|

| |||||||||||

| MATERIALS 3.3% | ||||||||||||

International Paper Co. | 191,472 | 7,219 | ||||||||||

Steel Dynamics, Inc. | 193,787 | 3,463 | ||||||||||

|

| |||||||||||

| 10,682 | ||||||||||||

|

| |||||||||||

| TELECOMMUNICATION SERVICES 4.0% | ||||||||||||

AT&T, Inc. | 286,684 | 9,865 | ||||||||||

CenturyLink, Inc. | 127,347 | 3,204 | ||||||||||

|

| |||||||||||

| 13,069 | ||||||||||||

|

| |||||||||||

| See Accompanying Notes | ANNUAL REPORT | DECEMBER 31, 2015 | 15 |

Table of Contents

Consolidated Schedule of Investments PIMCO Global Dividend Portfolio (Cont.)

| SHARES | MARKET VALUE (000S) | |||||||||||

| UTILITIES 3.0% | ||||||||||||

PG&E Corp. | 182,315 | $ | 9,697 | |||||||||

|

| |||||||||||

| Total United States | 160,952 | |||||||||||

|

| |||||||||||

| Total Common Stocks (Cost $341,573) | 309,221 | |||||||||||

|

| |||||||||||

| REAL ESTATE INVESTMENT TRUSTS 3.1% | ||||||||||||

| UNITED STATES 3.1% | ||||||||||||

| FINANCIALS 3.1% | ||||||||||||

Colony Capital, Inc. ‘A’ | 322,957 | 6,291 | ||||||||||

Outfront Media, Inc. | 165,873 | 3,621 | ||||||||||

|

| |||||||||||

| 9,912 | ||||||||||||

|

| |||||||||||

Total Real Estate Investment Trusts |

| 9,912 | ||||||||||

|

| |||||||||||

| MARKET VALUE (000S) | ||||||||||||

| SHORT-TERM INSTRUMENTS 0.8% | ||||||||||||

| REPURCHASE AGREEMENTS (c) 0.5% | ||||||||||||

| $ | 1,716 | |||||||||||

|

| |||||||||||

| PRINCIPAL AMOUNT (000S) | ||||||||||||

| U.S. TREASURY BILLS 0.3% | ||||||||||||

0.195% due 01/14/2016 - 01/21/2016 (b)(e) | $ | 934 | 934 | |||||||||

|

| |||||||||||

| Total Short-Term Instruments (Cost $2,650) | 2,650 | |||||||||||

|

| |||||||||||

| Total Investments in Securities (Cost $356,005) | 321,783 | |||||||||||

|

| |||||||||||

| SHARES | MARKET VALUE (000S) | |||||||||||

| INVESTMENTS IN AFFILIATES 1.7% | ||||||||||||

| SHORT-TERM INSTRUMENTS 1.7% | ||||||||||||

| CENTRAL FUNDS USED FOR CASH MANAGEMENT PURPOSES 1.7% | ||||||||||||

PIMCO Short-Term | 573,086 | $ | 5,659 | |||||||||

|

| |||||||||||

| Total Short-Term Instruments (Cost $5,659) | 5,659 | |||||||||||

|

| |||||||||||

| Total Investments in Affiliates (Cost $5,659) | 5,659 | |||||||||||

| Total Investments 100.8% (Cost $361,664) | $ | 327,442 | ||||||||||

Financial Derivative (Cost or Premiums, net $0) |

| (312 | ) | |||||||||

| Other Assets and Liabilities, net (0.7%) | (2,142 | ) | ||||||||||

|

| |||||||||||

| Net Assets 100.0% | $ | 324,988 | ||||||||||

|

| |||||||||||

NOTES TO CONSOLIDATED SCHEDULE OF INVESTMENTS (AMOUNTS IN THOUSANDS*):

| * | A zero balance may reflect actual amounts rounding to less than one thousand. |

| (a) | Security did not produce income within the last twelve months. |

| (b) | Coupon represents a weighted average yield to maturity. |

BORROWINGS AND OTHER FINANCING TRANSACTIONS

(c) REPURCHASE AGREEMENTS:

| Counterparty | Lending Rate | Settlement Date | Maturity Date | Principal Amount | Collateralized By | Collateral (Received) | Repurchase Agreements, at Value | Repurchase Agreement Proceeds to be Received (1) | ||||||||||||||||||||

SSB | 0.010% | 12/31/2015 | 01/04/2016 | $ | 1,716 | Fannie Mae 2.140% due 11/7/2022 | $ | (1,751 | ) | $ | 1,716 | $ | 1,719 | |||||||||||||||

|

|

|

|

|

| |||||||||||||||||||||||

Total Repurchase Agreements |

| $ | (1,751 | ) | $ | 1,716 | $ | 1,719 | ||||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||||||

| (1) | Includes accrued interest. |

BORROWINGS AND OTHER FINANCING TRANSACTIONS SUMMARY

The following is a summary by counterparty of the market value of Borrowings and Other Financing Transactions and collateral (received) as of December 31, 2015:

| Counterparty | Repurchase Agreement Proceeds to be Received | Payable for Reverse Repurchase Agreements | Payable for Sale-Buyback Transactions | Total Borrowings and Other Financing Transactions | Collateral (Received) | Net Exposure (2) | ||||||||||||||||||

Global/Master Repurchase Agreement | ||||||||||||||||||||||||

SSB | $ | 1,719 | $ | 0 | $ | 0 | $ | 1,719 | $ | (1,751 | ) | $ | (32 | ) | ||||||||||

|

|

|

|

|

| |||||||||||||||||||

Total Borrowings and Other Financing Transactions | $ | 1,719 | $ | 0 | $ | 0 | ||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

| (2) | Net Exposure represents the net receivable/(payable) that would be due from/to the counterparty in the event of default. Exposure from borrowings and other financing transactions can only be netted across transactions governed under the same master agreement with the same legal entity. The Portfolio and Subsidiary are recognized as two separate legal entities. As such, exposure cannot be netted. See Note 7, Principal Risks, in the Notes to Financial Statements for more information regarding master netting arrangements. |

| 16 | PIMCO EQUITY SERIES VIT | See Accompanying Notes |

Table of Contents

December 31, 2015

(d) FINANCIAL DERIVATIVE INSTRUMENTS: OVER THE COUNTER

FORWARD FOREIGN CURRENCY CONTRACTS:

| Counterparty | Settlement Month | Currency to be Delivered | Currency to be Received | Unrealized Appreciation/ (Depreciation) | ||||||||||||||||||||||||

| Asset | Liability | |||||||||||||||||||||||||||

BOA | 01/2016 | EUR | 12,482 | $ | 13,715 | $ | 150 | $ | 0 | |||||||||||||||||||

| 02/2016 | $ | 13,725 | EUR | 12,482 | 0 | (151 | ) | |||||||||||||||||||||

CBK | 01/2016 | 13,639 | 12,482 | 0 | (74 | ) | ||||||||||||||||||||||

| 01/2016 | 18,054 | GBP | 12,165 | 0 | (120 | ) | ||||||||||||||||||||||

| 02/2016 | GBP | 12,165 | $ | 18,054 | 119 | 0 | ||||||||||||||||||||||

DUB | 01/2016 | TRY | 4,391 | 1,503 | 5 | 0 | ||||||||||||||||||||||

HUS | 01/2016 | EUR | 30,866 | 32,894 | 0 | (650 | ) | |||||||||||||||||||||

| 02/2016 | HKD | 36,100 | 4,660 | 0 | 0 | |||||||||||||||||||||||

| 02/2016 | SGD | 232 | 164 | 1 | 0 | |||||||||||||||||||||||

MSB | 01/2016 | GBP | 12,165 | 18,341 | 407 | 0 | ||||||||||||||||||||||

UAG | 01/2016 | $ | 33,715 | EUR | 30,866 | 0 | (171 | ) | ||||||||||||||||||||

| 02/2016 | EUR | 30,866 | $ | 33,739 | 172 | 0 | ||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||||||

Total Forward Foreign Currency Contracts |

| $ | 854 | $ | (1,166 | ) | ||||||||||||||||||||||

|

|

|

| |||||||||||||||||||||||||

WRITTEN OPTIONS:

AS OF DECEMBER 31, 2015, THERE WERE NO OPEN WRITTEN OPTIONS. TRANSACTIONS IN WRITTEN CALL AND PUT OPTIONS FOR PERIOD ENDED DECEMBER 31, 2015:

| # of Contracts | Notional Amount | Premiums | ||||||||||

Balance at Beginning of Period | 0 | $ | 3,082 | $ | (338 | ) | ||||||

Sales | 7,573 | 0 | (1,364 | ) | ||||||||

Closing Buys | (7,356 | ) | (3,082 | ) | 1,655 | |||||||

Expirations | (217 | ) | 0 | 47 | ||||||||

Exercised | 0 | 0 | 0 | |||||||||

|

|

|

|

|

| |||||||

Balance at End of Period | 0 | $ | 0 | $ | 0 | |||||||

|

|

|

|

|

| |||||||

FINANCIAL DERIVATIVE INSTRUMENTS: OVER THE COUNTER SUMMARY

The following is a summary by counterparty of the market value of OTC financial derivative instruments and collateral (received)/pledged as of December 31, 2015:

| (e) | Securities with an aggregate market value of $934 have been pledged as collateral for financial derivative instruments as governed by International Swaps and Derivatives Association, Inc. master agreements as of December 31, 2015. |

| Financial Derivative Assets | Financial Derivative Liabilities | |||||||||||||||||||||||||||||||||||||||||||||

| Counterparty | Forward Foreign Currency Contracts | Purchased Options | Swap Agreements | Total Over the Counter | Forward Foreign Currency Contracts | Written Options | Swap Agreements | Total Over the Counter | Net Market Value of OTC Derivatives | Collateral (Received)/ Pledged | Net Exposure (1) | |||||||||||||||||||||||||||||||||||

BOA | $ | 150 | $ | 0 | $ | 0 | $ | 150 | $ | (151 | ) | $ | 0 | $ | 0 | $ | (151 | ) | $ | (1 | ) | $ | 0 | $ | (1 | ) | ||||||||||||||||||||

CBK | 119 | 0 | 0 | 119 | (194 | ) | 0 | 0 | (194 | ) | (75 | ) | 0 | (75 | ) | |||||||||||||||||||||||||||||||

DUB | 5 | 0 | 0 | 5 | 0 | 0 | 0 | 0 | 5 | (160 | ) | (155 | ) | |||||||||||||||||||||||||||||||||

HUS | 1 | 0 | 0 | 1 | (650 | ) | 0 | 0 | (650 | ) | (649 | ) | 934 | 285 | ||||||||||||||||||||||||||||||||

MSB | 407 | 0 | 0 | 407 | 0 | 0 | 0 | 0 | 407 | (290 | ) | 117 | ||||||||||||||||||||||||||||||||||

UAG | 172 | 0 | 0 | 172 | (171 | ) | 0 | 0 | (171 | ) | 1 | 0 | 1 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

Total Over the Counter | $ | 854 | $ | 0 | $ | 0 | $ | 854 | $ | (1,166 | ) | $ | 0 | $ | 0 | $ | (1,166 | ) | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||

| (1) | Net Exposure represents the net receivable/(payable) that would be due from/to the counterparty in the event of default. Exposure from OTC derivatives can only be netted across transactions governed under the same master agreement with the same legal entity. The Portfolio and Subsidiary are recognized as two separate legal entities. As such, exposure cannot be netted. See Note 7, Principal Risks, in the Notes to Financial Statements for more information regarding master netting agreements. |

| See Accompanying Notes | ANNUAL REPORT | DECEMBER 31, 2015 | 17 |

Table of Contents

Consolidated Schedule of Investments PIMCO Global Dividend Portfolio (Cont.)

FAIR VALUE OF FINANCIAL DERIVATIVE INSTRUMENTS

The following is a summary of the fair valuation of the Portfolio’s derivative instruments categorized by risk exposure. See Note 7, Principal Risks, in the Notes to Financial Statements on risks of the Portfolio.

Fair Values of Financial Derivative Instruments on the Consolidated Statement of Assets and Liabilities as of December 31, 2015:

| Derivatives not accounted for as hedging instruments | ||||||||||||||||||||||||

| Commodity Contracts | Credit Contracts | Equity Contracts | Foreign Exchange Contracts | Interest Rate Contracts | Total | |||||||||||||||||||

Financial Derivative Instruments - Assets | ||||||||||||||||||||||||

Over the counter | ||||||||||||||||||||||||

Forward Foreign Currency Contracts | $ | 0 | $ | 0 | $ | 0 | $ | 854 | $ | 0 | $ | 854 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Financial Derivative Instruments - Liabilities | ||||||||||||||||||||||||

Over the counter | ||||||||||||||||||||||||

Forward Foreign Currency Contracts | $ | 0 | $ | 0 | $ | 0 | $ | 1,166 | $ | 0 | $ | 1,166 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

The Effect of Financial Derivative Instruments on the Consolidated Statement of Operations for the period ended December 31, 2015:

| Derivatives not accounted for as hedging instruments | ||||||||||||||||||||||||

| Commodity Contracts | Credit Contracts | Equity Contracts | Foreign Exchange Contracts | Interest Rate Contracts | Total | |||||||||||||||||||

Net Realized Gain (Loss) on Financial Derivative Instruments | ||||||||||||||||||||||||

Exchange-traded or centrally cleared | ||||||||||||||||||||||||

Purchased Options | $ | 0 | $ | 0 | $ | (81 | ) | $ | 0 | $ | 0 | $ | (81 | ) | ||||||||||

Written Options | 0 | 0 | (281 | ) | 0 | 0 | (281 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| $ | 0 | $ | 0 | $ | (362 | ) | $ | 0 | $ | 0 | $ | (362 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Over the counter | ||||||||||||||||||||||||

Forward Foreign Currency Contracts | $ | 0 | $ | 0 | $ | 0 | $ | 8,932 | $ | 0 | $ | 8,932 | ||||||||||||

Written Options | 0 | 0 | (29 | ) | 0 | 0 | (29 | ) | ||||||||||||||||

Swap Agreements | 0 | 0 | 30 | 0 | 0 | 30 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| $ | 0 | $ | 0 | $ | 1 | $ | 8,932 | $ | 0 | $ | 8,933 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| $ | 0 | $ | 0 | $ | (361 | ) | $ | 8,932 | $ | 0 | $ | 8,571 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net Change in Unrealized Appreciation (Depreciation) on Financial Derivative Instruments |

| |||||||||||||||||||||||

Over the counter | ||||||||||||||||||||||||

Forward Foreign Currency Contracts | $ | 0 | $ | 0 | $ | 0 | $ | (4,093 | ) | $ | 0 | $ | (4,093 | ) | ||||||||||

Written Options | 0 | 0 | 53 | 0 | 0 | 53 | ||||||||||||||||||

Swap Agreements | 0 | 0 | (146 | ) | 0 | 0 | (146 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| $ | 0 | $ | 0 | $ | (93 | ) | $ | (4,093 | ) | $ | 0 | $ | (4,186 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

FAIR VALUE MEASUREMENTS

The following is a summary of the fair valuations according to the inputs used as of December 31, 2015 in valuing the Portfolio’s assets and liabilities:

| Category and Subcategory | Level 1 | Level 2 | Level 3 | Fair Value at 12/31/2015 | ||||||||||||

Investments in Securities, at Value | ||||||||||||||||

Common Stocks | ||||||||||||||||

Australia | ||||||||||||||||

Consumer Discretionary | $ | 0 | $ | 3,843 | $ | 0 | $ | 3,843 | ||||||||

Health Care | 0 | 3,281 | 0 | 3,281 | ||||||||||||

Industrials | 0 | 3,849 | 0 | 3,849 | ||||||||||||

Brazil | ||||||||||||||||

Health Care | 0 | 1,508 | 0 | 1,508 | ||||||||||||

Utilities | 0 | 1,974 | 0 | 1,974 | ||||||||||||

Canada | ||||||||||||||||

Utilities | 4,655 | 0 | 0 | 4,655 | ||||||||||||

France | ||||||||||||||||

Consumer Staples | 0 | 3,985 | 0 | 3,985 | ||||||||||||

Utilities | 0 | 7,429 | 0 | 7,429 | ||||||||||||

Germany | ||||||||||||||||

Materials | 3,503 | 0 | 0 | 3,503 | ||||||||||||

Greece | ||||||||||||||||

Consumer Discretionary | 0 | 3,830 | 0 | 3,830 | ||||||||||||

| Category and Subcategory | Level 1 | Level 2 | Level 3 | Fair Value at 12/31/2015 | ||||||||||||

Hong Kong | ||||||||||||||||

Telecommunication Services | $ | 0 | $ | 9,016 | $ | 0 | $ | 9,016 | ||||||||

Italy | ||||||||||||||||

Financials | 0 | 8,656 | 0 | 8,656 | ||||||||||||

Industrials | 0 | 4,047 | 0 | 4,047 | ||||||||||||

Japan | ||||||||||||||||

Consumer Discretionary | 0 | 4,952 | 0 | 4,952 | ||||||||||||

Telecommunication Services | 0 | 7,519 | 0 | 7,519 | ||||||||||||

Mexico | ||||||||||||||||

Consumer Staples | 1,615 | 0 | 0 | 1,615 | ||||||||||||

Netherlands | ||||||||||||||||

Financials | 0 | 13,308 | 0 | 13,308 | ||||||||||||

Russia | ||||||||||||||||

Consumer Staples | 1,427 | 0 | 0 | 1,427 | ||||||||||||

Spain | ||||||||||||||||

Consumer Staples | 0 | 5,325 | 0 | 5,325 | ||||||||||||

Switzerland | ||||||||||||||||

Health Care | 0 | 7,341 | 0 | 7,341 | ||||||||||||

| 18 | PIMCO EQUITY SERIES VIT | See Accompanying Notes |

Table of Contents

December 31, 2015

| Category and Subcategory | Level 1 | Level 2 | Level 3 | Fair Value at 12/31/2015 | ||||||||||||

Taiwan | ||||||||||||||||

Information Technology | $ | 0 | $ | 4,960 | $ | 0 | $ | 4,960 | ||||||||

United Kingdom | ||||||||||||||||

Consumer Staples | 0 | 3,422 | 0 | 3,422 | ||||||||||||

Energy | 3,414 | 0 | 0 | 3,414 | ||||||||||||

Financials | 0 | 23,312 | 0 | 23,312 | ||||||||||||

Telecommunication Services | 0 | 12,098 | 0 | 12,098 | ||||||||||||

United States | ||||||||||||||||

Consumer Discretionary | 28,684 | 0 | 0 | 28,684 | ||||||||||||

Energy | 6,195 | 0 | 0 | 6,195 | ||||||||||||

Financials | 21,706 | 0 | 0 | 21,706 | ||||||||||||

Health Care | 24,360 | 0 | 0 | 24,360 | ||||||||||||

Industrials | 6,574 | 0 | 0 | 6,574 | ||||||||||||

Information Technology | 39,985 | 0 | 0 | 39,985 | ||||||||||||

Materials | 10,682 | 0 | 0 | 10,682 | ||||||||||||

Telecommunication Services | 13,069 | 0 | 0 | 13,069 | ||||||||||||

Utilities | 9,697 | 0 | 0 | 9,697 | ||||||||||||

Real Estate Investment Trusts | ||||||||||||||||

United States | ||||||||||||||||

Financials | 9,912 | 0 | 0 | 9,912 | ||||||||||||

Short-Term Instruments | ||||||||||||||||

Repurchase Agreements | 0 | 1,716 | 0 | 1,716 | ||||||||||||

U.S. Treasury Bills | 0 | 934 | 0 | 934 | ||||||||||||

| $ | 185,478 | $ | 136,305 | $ | 0 | $ | 321,783 | |||||||||

| Category and Subcategory | Level 1 | Level 2 | Level 3 | Fair Value at 12/31/2015 | ||||||||||||

Investments in Affiliates, at Value | ||||||||||||||||

Short-Term Instruments | ||||||||||||||||

Central Funds Used for Cash Management Purposes | $ | 5,659 | $ | 0 | $ | 0 | $ | 5,659 | ||||||||

Total Investments | $ | 191,137 | $ | 136,305 | $ | 0 | $ | 327,442 | ||||||||

Financial Derivative Instruments - Assets |

| |||||||||||||||

Over the counter | $ | 0 | $ | 854 | $ | 0 | $ | 854 | ||||||||

Financial Derivative Instruments - Liabilities |

| |||||||||||||||

Over the counter | $ | 0 | $ | (1,166 | ) | $ | 0 | $ | (1,166 | ) | ||||||

Totals | $ | 191,137 | $ | 135,993 | $ | 0 | $ | 327,130 | ||||||||

There were no significant transfers between Levels 1, 2, or 3 during the period ended December 31, 2015.

| See Accompanying Notes | ANNUAL REPORT | DECEMBER 31, 2015 | 19 |

Table of Contents

1. ORGANIZATION

The PIMCO Global Dividend Portfolio (the “Portfolio”) is a series of the PIMCO Equity Series VIT (the “Trust”). The Trust is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company organized as a Delaware statutory trust on December 28, 2009. The Portfolio offers two classes of shares: Institutional and Advisor. The Trust is designed to be used as an investment vehicle by separate accounts of insurance companies that fund variable annuity contracts and variable life insurance policies and by qualified pension and retirement plans. Pacific Investment Management Company LLC (“PIMCO”) serves as the investment adviser (the “Adviser”) for the Portfolio.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Portfolio in the preparation of its financial statements in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The Portfolio is treated as an investment company under the reporting requirements of U.S. GAAP. The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

(a) Securities Transactions and Investment Income Securities transactions are recorded as of the trade date for financial reporting purposes. Realized gains and losses from securities sold are recorded on the identified cost basis. Dividend income is recorded on the ex-dividend date, except certain dividends from foreign securities where the ex-dividend date may have passed, which are recorded as soon as the Portfolio is informed of the ex-dividend date. Interest income, adjusted for the accretion of discounts and amortization of premiums, is recorded on the accrual basis from settlement date, with the exception of securities with a forward starting effective date, where interest income is recorded on the accrual basis from effective date. For convertible securities, premiums attributable to the conversion feature are not amortized. Estimated tax liabilities on certain foreign securities are recorded on an accrual basis and are reflected as components of interest income or net change in unrealized appreciation (depreciation) on investments on the Consolidated Statement of Operations, as appropriate. Tax liabilities realized as a result of such security sales are reflected as a component of net realized gain (loss) on investments on the Consolidated Statement of Operations. Paydown gains and losses on mortgage-related and other asset-backed securities are recorded as components of interest income on the Consolidated Statement of

Operations. Income or short-term capital gain distributions received from registered investment companies are recorded as dividend income. Long-term capital gain distributions received from registered investment companies are recorded as realized gains.

Distributions received from investments such as real estate investment trust securities, may include a return of capital invested. Such distributions reduce the cost basis of the respective securities. Return of capital distributions, if any, in excess of the cost basis of the security are recognized as capital gain.

(b) Cash and Foreign Currency The functional and reporting currency for the Portfolio is the U.S. dollar. The market values of foreign securities, currency holdings and other assets and liabilities are translated into U.S. dollars based on the current exchange rates each business day. Purchases and sales of securities and income and expense items denominated in foreign currencies, if any, are translated into U.S. dollars at the exchange rate in effect on the transaction date. The Portfolio does not separately report the effects of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized gain (loss) and net change in unrealized appreciation (depreciation) from investments on the Consolidated Statement of Operations. The Portfolio may invest in foreign currency-denominated securities and may engage in foreign currency transactions either on a spot (cash) basis at the rate prevailing in the currency exchange market at the time or through a forward foreign currency contract (see Financial Derivative Instruments, if any). Realized foreign exchange gains or losses arising from sales of spot foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and the U.S. dollar equivalent of the amounts actually received or paid are included in net realized gain (loss) on foreign currency transactions on the Consolidated Statement of Operations. Net unrealized foreign exchange gains and losses arising from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period are included in net change in unrealized appreciation (depreciation) on foreign currency assets and liabilities on the Consolidated Statement of Operations.

(c) Multiclass Operations Each class offered by the Portfolio has equal rights as to assets and voting privileges (except that shareholders of a class have exclusive voting rights regarding any matter relating solely to that class of shares). Income and non-class specific expenses are allocated daily to each class on the basis of the relative net assets. Realized and unrealized capital gains and losses are allocated daily based on the relative net assets of each class of the Portfolio. Class specific expenses, where applicable, currently include supervisory and

| 20 | PIMCO EQUITY SERIES VIT |

Table of Contents

December 31, 2015

administrative and distribution and servicing fees. Under certain circumstances, the per share net asset value (“NAV”) of a class of the Portfolio’s shares may be different from the per share NAV of another class of shares as a result of the different daily expense accruals applicable to each class of shares.

(d) Dividends and Distributions to Shareholders Dividends from net investment income, if any, are declared daily and distributed to shareholders quarterly. Net realized capital gains earned by the Portfolio, if any, will be distributed no less frequently than once each year.

Income dividends and capital gain distributions are determined in accordance with income tax regulations which may differ from U.S. GAAP. Differences between tax regulations and U.S. GAAP may cause timing differences between income and capital gain recognition. Examples of events that give rise to timing differences include wash sales, straddles and capital loss carryforwards. Further, the character of investment income and capital gains may be different for certain transactions under the two methods of accounting. Examples of transactions that may cause character differences include the treatment of paydowns on mortgage-backed securities, swaps, foreign currency transactions and contingent debt instruments. As a result, income dividends and capital gain distributions declared during a fiscal period may differ significantly from the net investment income (loss) and realized gains (losses) reported on the Portfolio’s annual financial statements presented under U.S. GAAP.

Distributions classified as a tax basis return of capital, if any, are reflected on the Consolidated Statements of Changes in Net Assets and have been recorded to paid in capital. In addition, other amounts have been reclassified between undistributed (overdistributed) net investment income (loss), accumulated undistributed (overdistributed) net realized gains (losses) and/or paid in capital to more appropriately conform financial accounting to tax characterizations of dividend distributions.

(e) New Accounting Pronouncements In June 2014, the Financial Accounting Standards Board (“FASB”) issued an Accounting Standards Update (“ASU”), ASU 2014-11, that expanded secured borrowing accounting for certain repurchase agreements. The ASU also sets forth additional disclosure requirements for certain transactions accounted for as sales in order to provide financial statement users with information to compare to similar transactions accounted for as secured borrowings. The ASU became effective prospectively for annual periods beginning after December 15, 2014, and interim periods beginning after March 15, 2015. The Portfolio has adopted the ASU. The financial statements have been modified to provide enhanced disclosures surrounding secured borrowing transactions, if any. See the Notes to Consolidated Schedule of Investments for additional details.

In August 2014, the FASB issued ASU 2014-15 requiring management to evaluate whether there are conditions or events, considered in the aggregate, that raise substantial doubt about the entity’s ability to continue as a going concern. The ASU is effective prospectively for annual periods ending after December 15, 2016, and interim periods thereafter. At this time, management is evaluating the implications of these changes on the financial statements.

In May 2015, the FASB issued ASU 2015-07 which removes the requirement to categorize within the fair value hierarchy all investments for which fair value is measured using the NAV per share practical expedient. The ASU also removes the requirement to make certain disclosures for all investments that are eligible to be measured at fair value using the NAV per share practical expedient. The ASU is effective for annual periods beginning after December 15, 2015 and interim periods within those annual periods. At this time, management is evaluating the implications of these changes on the financial statements.

3. INVESTMENT VALUATION AND FAIR VALUE MEASUREMENTS

(a) Investment Valuation Policies The price of the Portfolio’s shares is based on the Portfolio’s NAV. The NAV of the Portfolio, or each of its share classes, as applicable, is determined by dividing the total value of portfolio investments and other assets attributable to the Portfolio or class, less any liabilities, by the total number of shares outstanding of the Portfolio or class.

On each day that the New York Stock Exchange (“NYSE”) is open, Portfolio shares are ordinarily valued as of the close of regular trading (“NYSE Close”). Information that becomes known to the Portfolio or its agents after the time as of which NAV has been calculated on a particular day will not generally be used to retroactively adjust the price of a security or the NAV determined earlier that day. The Portfolio reserves the right to change the time its NAV is calculated if the Portfolio closes earlier, or as permitted by the SEC.

For purposes of calculating NAV, portfolio securities and other assets for which market quotes are readily available are valued at market value. Market value is generally determined on the basis of official closing prices or the last reported sales prices, or if no sales are reported, based on quotes obtained from established market makers or prices (including evaluated prices) supplied by the Portfolio’s approved pricing services, quotation reporting systems and other third-party sources (together, “Pricing Services”). The Portfolio will normally use pricing data for domestic equity securities received shortly after the NYSE Close and does not normally take into account trading, clearances or settlements that take place after the NYSE Close. A foreign (non-U.S.) equity security traded on a foreign exchange or on more than one exchange is typically valued using pricing information

| ANNUAL REPORT | DECEMBER 31, 2015 | 21 |

Table of Contents

Notes to Financial Statements (Cont.)