As filed with the Securities and Exchange Commission on June 6, 2011

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22378

(Exact name of registrant as specified in charter)

|

| 333 South Grand Avenue, Suite 1800 |

| Los Angeles, CA 90071 |

(Address of principal executive offices) (Zip code)

|

| Ronald R. Redell |

| President |

| DoubleLine Funds Trust |

| 333 South Grand Avenue, Suite 1800 |

| Los Angeles, CA 90071 |

(Name and address of agent for service)

Registrant’s telephone number, including area code: (213) 633-8200

Date of fiscal year end: March 31

Date of reporting period: March 31, 2011

Item 1. Reports to Stockholders.

Annual Report

March 31, 2011

DoubleLine Total Return Bond Fund

DBLTX (I-share)

DLTNX (N-share)

DoubleLine Core Fixed Income Fund

DBLFX (I-share)

DLFNX (N-share)

DoubleLine Emerging Markets Fixed Income Fund

DBLEX (I-share)

DLENX (N-share)

DoubleLine Multi-Asset Growth Fund

DMLIX (I-share)

DMLAX (A-share)

| | |

DoubleLine Capital LP | | 333 S. Grand Avenue 18th Floor Los Angeles, California 90071 doubleline.com |

Table of Contents

| | | | | | |

| | Annual Report | | March 31, 2011 | | 3 |

President’s Letter

May 6, 2011

Dear DoubleLine Funds Shareholder:

The DoubleLine Funds Trust was organized on January 11, 2010. We launched two Funds on April 6, 2010: the DoubleLine Total Return Bond Fund and the DoubleLine Emerging Markets Fixed Income Fund. On June 1, 2010, we launched our third Fund, the DoubleLine Core Fixed Income Fund. On December 20, 2010 we launched our fourth Fund, the DoubleLine Multi-Asset Growth Fund. In the first fiscal year of operations, investors have allocated over $6 billion to the Funds. We strive to deliver superior risk-adjusted returns while working to avoid crossing the double line of risk on the road to successful investing. This motto was inspired by Piet Mondrian (1872-1944), a leading abstract painter of the 20th century, known for his simplicity in balancing brilliant colors and bold black lines. DoubleLine Capital, advisor to the Funds, strives for similar balance by providing investment solutions that integrate risk management with the pursuit of excess returns.

Highlights of Financial Markets through our annual reporting period (April 6, 2010-March 31, 2011)

| | · | | Treasuries: The day before the reporting period began, the 10-year Treasury reached a 4.00% yield, a point that ironically coincided with the conclusion of the Federal Reserve’s Large Scale Asset Program (LSAP), more widely known as quantitative easing. With the start of the first round of quantitative easing, QE1, and amid disappointing reports of economic growth, deflation concerns and flight-to-quality flows from the brewing debt and currency crises in the eurozone, Treasuries rallied to a yield of 2.39% on the 10-year by early October. As a second round of money printing appeared to be in the offing, yields began to rise sharply, anticipating the QE2 program unveiled by the Fed on November 3. The rally in Treasury prices through February alternately was explained by expectations of improved economic growth (according to the Fed), concern over the potential of inflation and currency debasement (according to QE detractors), or both. The 10-year Treasury raced to 3.54% in mid-December and moved sideways thereafter, ending the first quarter of 2011 at 3.47%. |

Markets now are focused on the implications of the approaching end of QE2 in June. DoubleLine does not believe any market disruption or sustained rise in yield is likely at this time. To the contrary, we see a drop in yields as more likely. The case of QE1 is instructive. Foreign central banks easily absorbed the bonds not purchased by the Fed after QE1 ended in March 2010. We believe that central banks, as well as commercial banks and households, have room to add Treasury holdings. Foreign central banks especially appear to have incentive to buy Treasuries as they seek to limit the appreciation of their currencies versus the dollar. Dealers and hedge funds appear to have larger short positions than is normally the case and will likely be forced into the market if yields fail to rise. Finally, as of the date of this letter, the yield curve is very steep, suggesting the Fed’s purchases to date have not pushed Treasury prices above fair value.

| | | | | | | | | | | | | | | | |

| | | | | | U.S. Treasury Yield Curve | |

| Term | | | | | 4/6/2010 | | | 3/31/2011 | | | Change | |

3 MONTH | | | | | | | 0.163 | | | | 0.091 | | | | -0.072 | |

6 MONTH | | | | | | | 0.249 | | | | 0.169 | | | | -0.080 | |

1 YEAR | | | | | | | 0.432 | | | | 0.273 | | | | -0.159 | |

2 YEAR | | | | | | | 1.136 | | | | 0.821 | | | | -0.315 | |

3 YEAR | | | | | | | 1.703 | | | | 1.299 | | | | -0.405 | |

5 YEAR | | | | | | | 2.696 | | | | 2.277 | | | | -0.419 | |

7 YEAR | | | | | | | 3.402 | | | | 2.920 | | | | -0.482 | |

10 YEAR | | | | | | | 3.951 | | | | 3.470 | | | | -0.480 | |

30 YEAR | | | | | | | 4.832 | | | | 4.508 | | | | -0.325 | |

Table by DoubleLine from Bloomberg data | |

| | · | | Agency Mortgage-Backed Securities (Agency MBS): Agency MBS, as represented by the Barclays Capital U.S. MBS Index, returned 4.98% over the period (April 6, 2010-March 31, 2011), underperforming the Treasury market by 25 bps and the Barclays Capital U.S. Aggregate Bond Index return of 5.70%. This underperformance resulted from the shorter duration of the MBS index and the drop in U.S. Treasury yields. Prepayment speeds on lower coupon pass-throughs increased slightly while speeds on higher coupons remained muted relative to these borrowers’ current rate incentive. Prepayment speeds are expected to remain muted going forward given the increase in 10-year U.S. Treasury yields since the beginning of October along with the decreased capability of borrowers to refinance due to a weakening housing market. |

| | · | | Non-Agency MBS: The private label MBS universe delivered outsized returns, with the PrimeX FRM 1 and the PrimeX FRM 2, both baskets of MBS backed by prime fixed-rated residential mortgages, returning 19.2% and 20.7%, respectively. Market prices benefited from the “cheapness” of non-Agency MBS relative to their ultimate expected returns at maturity and shrinking supply, thanks to the lack of new issuance since 2007. |

| | · | | Corporate Bonds: Despite European sovereign debt concerns, a volcanic eruption in Iceland and the Deepwater Horizon oil rig explosion, both investment grade and high yield corporate bonds performed well during the period April 6, 2010 through March 31, 2011. The Barclays Capital US Credit Index returned 7.59% and the Barclays Capital U.S. High Yield Cash Pay Index returned 13.94% versus a return of 5.70% for the Barclays Capital U.S. Aggregate Bond Index. Key drivers of performance in the corporate bond space included: |

| | 1. | Reported corporate earnings, which beat consensus expectations; |

| | 2. | Continued corporate deleveraging and refinancing, which increased corporate cash flows; |

| | 3. | Investor demand for corporate debt, fueled by the low level of absolute Treasury yields due to quantitative easing; and |

| | 4. | Low default rates on non-investment grade issues. |

| | · | | Emerging Markets Fixed Income: All three EM debt sectors—sovereign, corporate and local currency—posted solid returns for the period. |

| | | | | | |

| | Annual Report | | March 31, 2011 | | 5 |

April 6, 2010 through March 31, 2011

| | | | | | | | | | | | | | | | | | |

| | | | | Return | | | Volatility | | | Sharpe | | | YTM | |

US$ Indices | | | | | | | | | | | | | | | | | | |

JP Morgan EMBI GD—Sovereign | | | | | 8.40% | | | | 4.50% | | | | 1.8 | | | | 6.10% | |

JP Morgan CEMBI BD—Corporate | | | | | 9.10% | | | | 2.60% | | | | 3.4 | | | | 6.00% | |

Non US$ Index | | | | | | | | | | | | | | | | | | |

JP Morgan GBI EM—Local Currency | | | | | 9.90% | | | | 10.70% | | | | 0.9 | | | | 6.60% | |

Table by DoubleLine from JP Morgan data | | | | | | | | | | | | | | | | | | |

Government local currency bonds were the best performer: the JP Morgan Global Bond Index Emerging Markets-Local Currency returned 9.9% over the period, with the bulk of returns coming from currency appreciation. Positive returns were broad-based across all regions, led by Brazil and South Africa which saw their currencies appreciate 7.4% and 6.9%, respectively. Both external sovereign and corporate EM debt benefited from a decline in the 10-year U.S. Treasury yield of 48 bps. EM corporate debt outperformed EM sovereign debt as the JP Morgan Corporate Emerging Markets Bond Index-Broad Diversified (CEMBI BD) spread tightened by 36 bps over the period versus the JP Morgan Emerging Markets Bond Index-Global Diversified (EMBI GD), which saw its spread widen by 37 bps. The high yield credits in both the EMBI GD and the CEMBI BD outperformed their investment grade counterparts over the period by 2.5% and 5.0%, respectively. The EMBI GD saw the strongest performance out of lower rated countries with Argentina, Belize, Iraq and Jamaica posting the strongest returns. The CEMBI BD saw similar strong performance out of Argentina, Barbados, Indonesia and Jamaica.

| | · | | Global Equities: Global equity markets posted strong returns for the first quarter of 2011. Favorable economic indicators and corporate earnings provided strong support for equities. Aside from relatively strong quarterly performance, there continue to be concerns regarding the Federal Reserve’s plans for quantitative easing, geopolitical risk surrounding the Middle East/North Africa (MENA) and the ramifications of the Japan earthquake. |

| | · | | Commodities: The broad-based commodities market returned 32.61% over the period April 6, 2010 through March 31, 2011, as measured by the S&P Goldman Sachs Commodity Total Return Index (GSCI). The period began with a sell-off in May 2010 after growing fears that over-indebtedness in Europe would lead to a global economic contraction. However, geopolitical instability in the MENA region led crude oil prices higher. Light, sweet crude futures opened the reporting period at $86.84 per barrel on April 6, 2010, during the May sell-off fell to a low of $68.01 on May 20, then rallied to end March 31, 2011 at $106.72. Reports indicate $15 to $30 of the barrel price reflects a geopolitical risk premium. Food and metals price inflation were further fueled by QE2. |

Fund Highlights

DoubleLine Total Return Bond Fund

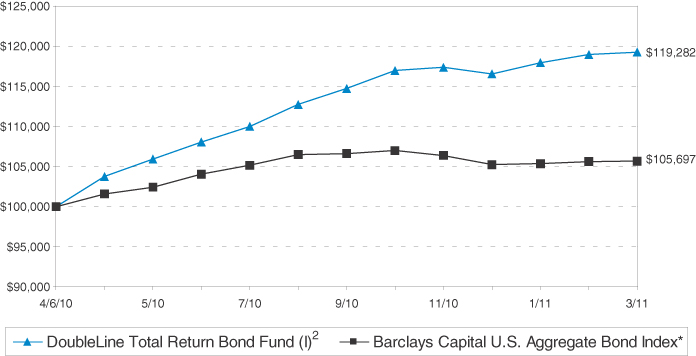

Since inception on April 6, 2010 through March 31, 2011 the DoubleLine Total Return Bond Fund (Class I) has outperformed the Barclays Capital U.S. Aggregate Bond Index by 13.58% (19.28% versus 5.70%). This outperformance was primarily driven by investment positions in two subsectors of the MBS market: (1) non-Agency residential mortgage backed securities (RMBS), which have generated higher loss-adjusted yields than other credit sectors, and (2) high cash flowing Agency collateralized mortgage obligations (CMOs).

| | | | | | | | | | | | | | | | |

| | | | | | March 2011 | | | 1Q2011 | | | Since Inception

(4-6-10 to 3-31-11) | |

I-Share | | | | | | | 0.25% | | | | 2.33% | | | | 19.28% | |

N-Share | | | | | | | 0.32% | | | | 2.27% | | | | 19.04% | |

Barclays Capital US Aggregate Index | | | | | | | 0.06% | | | | 0.42% | | | | 5.70% | |

DoubleLine Emerging Markets Fixed Income Fund

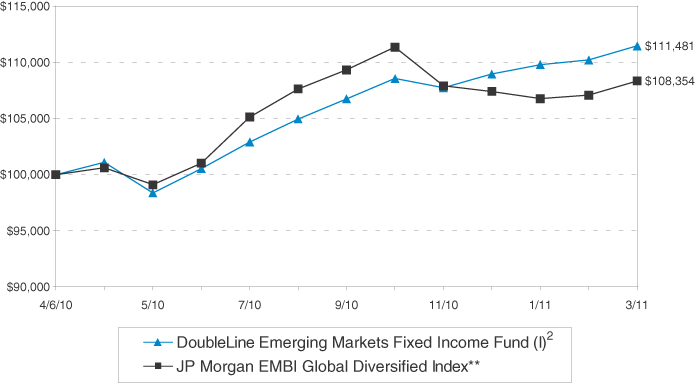

From its inception on April 6, 2010 through March 31, 2011, the DoubleLine Emerging Markets Fixed Income Fund (I shares) returned 11.48%, an outperformance of 313 bps over the JP Morgan Emerging Markets Bond Index-Global Diversified, which returned 8.35%. The Fund’s outperformance was driven predominantly by investing in EM corporate debt, which outperformed EM sovereign and quasi-sovereign debt over the period. EM corporate debt spreads tightened by 36 bps over the period on improving credit fundamentals and a positive rating outlook. This compares favorably to EM sovereign and quasi-sovereign debt where the index saw spreads widen by 37 bps during that timeframe. Additionally, the Fund benefited from a slight overweight position to non-investment grade credits relative to its benchmark.

| | | | | | | | | | | | | | | | |

| | | | | | March 2011 | | | 1Q2011 | | | Since Inception

(4-6-10 to 3-31-11) | |

I-Share | | | | | | | 1.14% | | | | 2.30% | | | | 11.48% | |

N-Share | | | | | | | 1.12% | | | | 2.24% | | | | 11.25% | |

JP Morgan Emerging Markets Bond Global Diversified Index | | | | | | | 1.19% | | | | 0.87% | | | | 8.35% | |

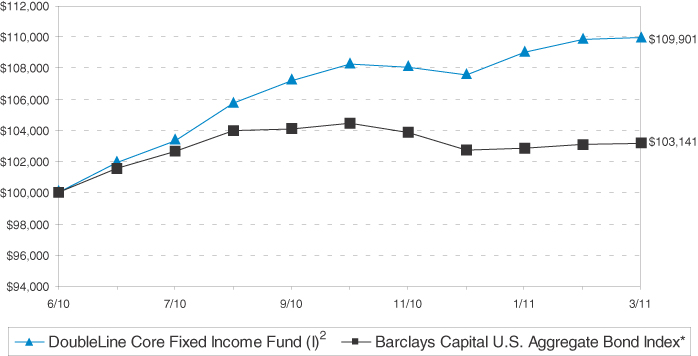

DoubleLine Core Fixed Income Fund

From its June 1, 2010 inception through March 31, 2011, the DoubleLine Core Fixed Income Fund (I shares) returned 9.90%, an outperformance of 676 bps over the Barclays Capital U.S. Aggregate Bond Index, which returned 3.14%. The Fund’s outperformance can be attributed mainly to management’s active sector allocation, which included overweighting Treasuries from inception through August 2010, then underweighting Treasuries thereafter; and investments in emerging markets and mortgage-backed securities.

| | | | | | | | | | | | | | | | |

| | | | | | March 2011 | | | 1Q2011 | | | Since Inception

(6-1-10 to 3-31-11) | |

I-Share | | | | | | | 0.10% | | | | 2.23% | | | | 9.90% | |

N-Share | | | | | | | 0.09% | | | | 2.18% | | | | 9.71% | |

Barclays Capital US Aggregate Index | | | | | | | 0.06% | | | | 0.42% | | | | 3.14% | |

DoubleLine Multi-Asset Growth Fund

Since inception on December 20, 2010 through March 31, 2011, the DoubleLine Multi-Asset Growth Fund (I shares) returned 1.24%. The Fund’s positive performance during the first quarter of 2011 was due to allocations to both the global fixed income sectors and real asset sectors. The equity exposure detracted from performance but provided diversification benefits in an attempt to lower overall volatility.

| | | | | | |

| | Annual Report | | March 31, 2011 | | 7 |

| | | | | | | | | | | | | | | | |

| | | | | | March 2011 | | | 1Q2011 | | | Since Inception

(12-20-10 to 3-31-11) | |

I-Share | | | | | | | 0.24 | % | | | 1.04 | % | | | 1.24 | % |

A-Share | | | | | | | | | | | | | | | | |

No Load | | | | | | | 0.12 | % | | | 0.82 | % | | | 1.02 | % |

With Load | | | | | | | -4.13 | % | | | -3.46 | % | | | -3.27 | % |

Blended 60% Barclays Capital US Aggregate Index/25% S&P 500/15% S&P GSCI | | | | | | | 0.69 | % | | | 3.42 | % | | | 4.29 | % |

On behalf of the team at DoubleLine, I thank you for your support of the Funds. On the following pages of this Annual Report, you will find specific information regarding each Fund’s operation and holdings. DoubleLine was founded with the prevailing objective that clients come first, and that our success will be predicated upon being relevant to clients. With that in mind, we will continue to strive to provide investment solutions that integrate risk management with the pursuit of excess return. We value the trust you have placed in us and if you have any questions please do not hesitate to call 877-DLINE11 (354-6311) or visit our website at www.doublelinefunds.com.

Sincerely,

Ronald R. Redell

Past performance is not a guarantee of future results.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Please refer to the Schedule of Investments for a complete list of fund holdings.

This report is for the information of shareholders of the Funds. It may also be used as sales literature when preceded or accompanied by the current prospectus.

Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset-Backed and Mortgage-Backed securities include additional risks that investors should be aware of including credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Investments in lower rated and non-rated securities present a greater risk of loss to principal and interest than higher rated securities. The Emerging Markets Fixed Income Fund and the Multi-Asset Growth Fund are non-diversified meaning each may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, these Funds may be more susceptible to any single economic, political or regulatory event than a more diversified fund, and a decline in the market value of one of the Fund’s investments may affect that Fund’s value more than if the Fund were a diversified fund. The Core Fixed Income Fund, Emerging Markets Fixed Income Fund and Multi-Asset Growth Fund may invest in foreign securities, which involve political, economic, and currency risks, greater volatility, and differences in accounting methods. These risks are greater for investments in emerging markets. The Multi-Asset Growth Fund may invest in securities related to real estate, which may decline in value as a result of factors affecting the real estate industry. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Commodity-linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Investing in derivatives could lose more than the amount invested. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. For more details regarding the risks of the Funds, please consult the current prospectus.

JP Morgan EMBI Global Diversified Index—This index is an uniquely-weighted version of the EMBI Global. It limits the weights of those index countries with larger debt stocks by only including specified portions of these countries’ eligible current face amounts of debt outstanding. The countries covered in the EMBI Global Diversified are identical to those covered by EMBI Global.

Barclay’s Capital U.S. Aggregate Bond Index—This index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the US investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis.

Barclay’s Capital U.S. Treasury Index—This index includes public obligations of the U.S. Treasury. Treasury bills are excluded by the maturity constraint but are part of a separate Short Treasury Index. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS are excluded.

Barclays Capital U.S. MBS Index—This index measures the performance of investment grade fixed-rate mortgage-backed pass-through securities of the Government-Sponsored Enterprises (GSEs): Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC).

PrimeX—This index is a synthetic credit default swap (CDS) index which references non-Agency Prime residential mortgage-backed securities (RMBS). There are 20 prime RMBS deals referenced in each sub-index from 2005, 2006, and 2007.

Barclays Capital U.S. Credit Index—This index is the U.S. Credit component of the U.S. Government/Credit Index and consists of publicly issued US corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. The U.S. Credit Index is the same as the former U.S. Corporate Investment Grade Index.

Barclays Capital U.S. High Yield Cash Pay Index—This index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issuer from countries designated as emerging markets (e.g. Argentina, Brazil, Venezuela, etc.) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. Original issue zeros, step-up coupon structures, 144As and pay-in-kind (PIK, as of October 1, 2009) are also included.

JP Morgan Corporate Emerging Markets Bond Index—Broad Diversified (CEMBI GD)—This index is a market capitalization weighted index consisting of US-denominated Emerging Market corporate bonds. It is a liquid global corporate benchmark representing Asia, Latin America, Europe and the Middle East/Africa.

JP Morgan Emerging Markets Bond Index—Global Diversified (EMBI GD)—This index tracks total returns for US dollar denominated debt instruments issued by emerging market sovereign entities, including Brady bonds, loans and Eurobonds, and quasi-sovereign entities.

JP Morgan GBI EM—Local Currency—Comprehensive emerging market debt benchmarks that track local currency bonds issued by Emerging Market governments.

Standard & Poor’s/Goldman Sachs Commodity Total Return Index (GSCI)—This is a composite index of commodity sector returns which represents a broadly diversified, unleveraged, long-only position in commodity futures. This index’s components qualify for inclusion in the index based on liquidity measures and are weighted in relation to their global production levels, making the index a valuable economic indicator and commodities market benchmark.

S&P 500 Index—This Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks.

A direct investment cannot be made in an index. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses applicable to mutual fund investments.

A basis point (bps) equals 0.01%.

Duration is a commonly used measure of the potential volatility of the price of a debt security, or the aggregate market value of a portfolio of debt securities, prior to maturity. Securities with a longer duration generally have more volatile prices than securities of comparable quality with a shorter duration.

Volatility—The standard deviation of the index.

Sharpe—A ratio to measure risk-adjusted performance calculated by subtracting the risk-free rate from the rate of return for a portfolio/index and dividing the result by the standard deviation of the portfolio returns.

YTM—Yield to Maturity—The rate of return anticipated on a bond if it is held until the maturity date.

The DoubleLine Funds are distributed by Quasar Distributors, LLC.

This commentary may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to a Fund and market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein.

DoubleLine has no obligation to provide revised assessments in the event of changed circumstances. While we have gathered this information from sources believed to be reliable, DoubleLine cannot guarantee the accuracy of the information provided. Securities discussed are not recommendations and are presented as examples of issue selection or portfolio management processes. They have been picked for comparison or illustration purposes only. The views expressed above (including any forward-looking statements) may not be relied upon as investment advice or as an indication of the Funds’ trading intent. Information about the Funds’ holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary. No security presented within is either offered for sale or purchase. DoubleLine reserves the right to change its investment perspective and outlook without notice as market conditions dictate or as additional information becomes available.

Investment strategies may not achieve the desired results due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors. The views and forecasts expressed in this material are as of the date indicated, are subject to change without notice, may not come to pass and do not represent a recommendation or offer of any particular security, strategy, or investment.

| | | | | | |

| | Annual Report | | March 31, 2011 | | 9 |

| | |

| |

| Schedule of Investments DoubleLine Total Return Bond Fund | | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| | COLLATERALIZED MORTGAGE OBLIGATIONS 50.4% | |

| |

| | | | Adjustable Rate Mortgage Trust, | |

| $ | 6,200,000 | | | Series 2005-2 | | | 0.73% | # | | | 06/25/2035 | | | | 3,105,797 | |

| | 7,825,841 | | | Series 2007-3 | | | 3.73% | #^ | | | 11/25/2037 | | | | 4,402,755 | |

| |

| | | | Aegis Asset Backed Securities Trust, | |

| | 738,019 | | | Series 2003-2 | | | 2.80% | # | | | 11/25/2033 | | | | 576,999 | |

| | 8,683,689 | | | Series 2004-1 | | | 2.28% | # | | | 04/25/2034 | | | | 6,251,670 | |

| | 1,512,104 | | | Series 2004-2 | | | 1.55% | # | | | 06/25/2034 | | | | 996,696 | |

| |

| | | | American Home Mortgage Investment Trust, | |

| | 9,270,840 | | | Series 2005-1 | | | 2.46% | # | | | 06/25/2045 | | | | 8,014,571 | |

| | 3,344,389 | | | Series 2006-2 | | | 6.60% | # | | | 06/25/2036 | | | | 2,187,357 | |

| | 15,586,667 | | | Series 2007-A | | | 6.10% | #^ | | | 01/25/2037 | | | | 10,680,639 | |

| |

| | | | Argent Securities, Inc., | |

| | 850,957 | | | Series 2004-W6 | | | 0.80% | # | | | 04/25/2034 | | | | 708,260 | |

| |

| | | | Asset Backed Securities Corporation, | |

| | 9,239,571 | | | Series 2003-HE6-M1 | | | 1.22% | # | | | 11/25/2033 | | | | 7,666,049 | |

| | 2,745,019 | | | Series 2004-HE3-M2 | | | 1.37% | # | | | 06/25/2034 | | | | 1,966,408 | |

| |

| | | | Banc of America Alternative Loan Trust, | |

| | 15,842,779 | | | Series 2005-6-2CB2 | | | 6.00% | | | | 07/25/2035 | | | | 13,901,397 | |

| | 6,187,944 | | | Series 2005-6-4CB1 | | | 6.50% | | | | 07/25/2035 | | | | 5,276,587 | |

| | 5,976,705 | | | Series 2005-8-2CB1 | | | 6.00% | | | | 09/25/2035 | | | | 4,804,294 | |

| | 5,000,000 | | | Series 2006-5-CB14 | | | 6.00% | # | | | 06/25/2046 | | | | 3,497,288 | |

| | 8,203,000 | | | Series 2006-6-CB3 | | | 6.00% | | | | 07/25/2046 | | | | 6,744,831 | |

| | 14,669,286 | | | Series 2006-8-1A1 | | | 6.25% | # I/F I/O | | | 11/25/2036 | | | | 2,476,897 | |

| | 4,987,557 | | | Series 2006-8-1A2 | | | 0.70% | # | | | 11/25/2036 | | | | 3,327,893 | |

| | 3,849,846 | | | Series 2007-2-2A1 | | | 6.00% | | | | 06/25/2037 | | | | 2,708,351 | |

| |

| | | | Banc of America Commercial Mortgage, Inc., | |

| | 5,303,000 | | | Series 2002-2-G | | | 5.85% | ^ | | | 07/11/2043 | | | | 5,417,351 | |

| | 208,613,168 | | | Series 2004-6-XP | | | 0.67% | # I/O | | | 12/10/2042 | | | | 551,782 | |

| | 305,033,137 | | | Series 2005-4-XP | | | 0.35% | # I/O | | | 07/10/2045 | | | | 1,018,079 | |

| | 280,871,687 | | | Series 2006-1-XP | | | 0.34% | # I/O | | | 09/10/2045 | | | | 1,159,747 | |

| |

| | | | Banc of America Funding Corporation, | |

| | 6,107,936 | | | Series 2009-R15A-4A2 | | | 5.75% | #^ | | | 12/26/2036 | | | | 4,572,401 | |

| |

| | | | Banc of America Funding Trust, | |

| | 722,059 | | | Series 2005-6 | | | 5.50% | | | | 10/25/2035 | | | | 725,336 | |

| | 31,364,693 | | | Series 2006-2 | | | 6.00% | | | | 03/25/2036 | | | | 31,984,851 | |

| | 1,088,242 | | | Series 2006-2 | | | 22.10% | # I/F | | | 03/25/2036 | | | | 1,256,494 | |

| | 13,491,804 | | | Series 2006-3 | | | 6.33% | # | | | 03/25/2036 | | | | 13,894,635 | |

| | 5,879,061 | | | Series 2006-7 | | | 6.04% | # | | | 10/25/2036 | | | | 3,889,393 | |

| | 6,020,431 | | | Series 2006-7 | | | 5.91% | # | | | 10/25/2036 | | | | 3,813,810 | |

| | 5,444,750 | | | Series 2006-8T2 | | | 6.10% | # | | | 10/25/2036 | | | | 3,917,574 | |

| | 2,897,696 | | | Series 2006-B | | | 5.63% | # | | | 03/20/2036 | | | | 2,378,883 | |

| | 3,227,161 | | | Series 2006-G | | | 0.47% | # | | | 07/20/2036 | | | | 2,756,990 | |

| | 2,003,296 | | | Series 2006-H | | | 6.02% | # | | | 09/20/2046 | | | | 1,793,294 | |

| | 3,587,642 | | | Series 2007-1 | | | 5.84% | # | | | 01/25/2037 | | | | 2,408,833 | |

| | 5,285,495 | | | Series 2007-3 | | | 5.83% | # | | | 04/25/2037 | | | | 3,763,994 | |

| | 6,383,135 | | | Series 2007-5 | | | 5.50% | | | | 07/25/2037 | | | | 5,229,738 | |

| | 6,658,251 | | | Series 2009-R14 | | | 16.0% | #^ I/F | | | 06/26/2035 | | | | 6,742,335 | |

| | 5,742,588 | | | Series 2010-R1 | | | 13.9% | #^ I/F | | | 07/28/2036 | | | | 4,950,685 | |

| |

| | | | Banc of America Large Loan, | |

| | 3,726,654 | | | Series 2006-BIX1-C | | | 0.44% | #^ | | | 10/15/2019 | | | | 3,558,587 | |

| |

| | | | Banc of America Mortgage Securities, Inc., | |

| | 5,367,079 | | | Series 2004-K-4A1 | | | 5.24% | # | | | 12/25/2034 | | | | 5,010,193 | |

| |

| | | | BCAP LLC Trust, | |

| | 9,679,787 | | | Series 2007-AA2-2A7 | | | 6.00% | | | | 04/25/2037 | | | | 7,189,899 | |

| | 10,660,819 | | | Series 2007-AA2-2A8 | | | 5.75% | | | | 04/25/2037 | | | | 7,660,396 | |

| | 18,000,000 | | | Series 2008-RR3-A1B | | | 6.65% | # | | | 10/25/2036 | | | | 16,376,301 | |

| |

| | | | BCRR Trust, | |

| | 10,500,000 | | | Series 2010-LEAF-32A | | | 4.23% | #^ | | | 12/22/2032 | | | | 10,492,084 | |

| |

| | | | Bear Stearns Adjustable Rate Mortgage Trust, | |

| | 25,890,868 | | | Series 2006-4-4A1 | | | 5.82% | # | | | 10/25/2036 | | | | 22,154,920 | |

| |

| | | | Bear Stearns Asset Backed Securities Trust, | |

| | 17,688,539 | | | Series 2005-AC2-2A1 | | | 5.25% | | | | 04/25/2035 | | | | 16,660,030 | |

| | 54,507,800 | | | Series 2005-AC2-IA | | | 5.25% | | | | 04/25/2035 | | | | 49,741,937 | |

| | 6,869,203 | | | Series 2006-AC1-IA1 | | | 5.75% | # | | | 02/25/2036 | | | | 5,301,561 | |

| | 3,864,712 | | | Series 2007-SD1-IA2A | | | 6.00% | | | | 10/25/2036 | | | | 3,002,624 | |

| | 1,958,912 | | | Series 2007-SD1-IA3A | | | 6.50% | | | | 10/25/2036 | | | | 1,328,476 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Bear Stearns Commercial Mortgage Securities, Inc., | |

| $ | 3,441,000 | | | Series 2000-WF1-F | | | 8.18% | # | | | 02/15/2032 | | | | 3,436,738 | |

| | 110,064,196 | | | Series 2004-16-X2 | | | 0.88% | # I/O | | | 02/13/2046 | | | | 1,214,426 | |

| | 42,492,952 | | | Series 2004-PWR5-X2 | | | 0.99% | # I/O | | | 07/11/2042 | | | | 540,455 | |

| | 110,784,572 | | | Series 2004-PWR6 | | | 0.80% | # I/O | | | 11/11/2041 | | | | 1,249,705 | |

| | 750,000 | | | Series 2005-PWR10-AM | | | 5.45% | # | | | 12/15/2015 | | | | 773,390 | |

| | 21,647,397 | | | Series 2005-PWR7-X2 | | | 0.20% | # I/O | | | 02/11/2041 | | | | 105,806 | |

| |

| | | | Capital Trust, | |

| | 11,424,000 | | | Series 2005-3A-A2 | | | 5.16% | ^ | | | 06/25/2035 | | | | 11,445,477 | |

| |

| | | | CD Mortgage Trust, | |

| | 8,983,129 | | | Series 2006-CD2-AAB | | | 5.55% | # | | | 01/15/2046 | | | | 9,412,588 | |

| |

| | | | Centex Home Equity Loan Trust, | |

| | 2,750,000 | | | Series 2004-A | | | 4.93% | # | | | 01/25/2034 | | | | 2,767,846 | |

| |

| | | | Chase Mortgage Financial Trust, | |

| | 12,149,564 | | | Series 2007-S5-1A18 | | | 6.00% | | | | 07/25/2037 | | | | 9,903,924 | |

| |

| | | | Chase Mortgage Loan, | |

| | 4,088,871 | | | Series 2003-4-2M1 | | | 1.15% | # | | | 03/25/2033 | | | | 2,543,413 | |

| |

| | | | Chaseflex Trust, | |

| | 3,037,788 | | | Series 2006-1-2A2 | | | 5.94% | # | | | 06/25/2036 | | | | 3,012,854 | |

| | 17,021,312 | | | Series 2006-2-A2B | | | 0.45% | # | | | 09/25/2036 | | | | 13,101,210 | |

| | 12,267,515 | | | Series 2007-1-1A1 | | | 6.50% | | | | 02/25/2037 | | | | 8,255,069 | |

| |

| | | | Citi Mortgage Alternative Loan Trust, | |

| | 15,655,017 | | | Series 2006-A2-A2 | | | 6.00% | | | | 05/25/2036 | | | | 13,210,815 | |

| | 10,000,000 | | | Series 2006-A5-A3 | | | 6.00% | | | | 10/25/2036 | | | | 8,698,290 | |

| | 7,619,730 | | | Series 2007-A1-1A7 | | | 6.00% | | | | 01/25/2037 | | | | 5,750,523 | |

| | 15,467,589 | | | Series 2007-A1-IA5 | | | 6.00% | | | | 01/25/2037 | | | | 11,791,569 | |

| | 19,619,910 | | | Series 2007-A1-IA9 | | | 5.15% | # I/F I/O | | | 01/25/2037 | | | | 2,620,520 | |

| | 17,845,331 | | | Series 2007-A3-IA1 | | | 6.00% | # | | | 03/25/2037 | | | | 13,335,183 | |

| | 39,039,185 | | | Series 2007-A3-IA3 | | | 5.15% | # I/F I/O | | | 03/25/2037 | | | | 4,763,893 | |

| | 4,200,165 | | | Series 2007-A5-1A11 | | | 6.00% | | | | 05/25/2037 | | | | 3,093,619 | |

| | 2,200,635 | | | Series 2007-A8-A1 | | | 6.00% | | | | 10/25/2037 | | | | 1,728,862 | |

| |

| | | | Citicorp Mortgage Securities, Inc., | |

| | 37,058,120 | | | Series 2005-1-1A4 | | | 5.50% | | | | 02/25/2035 | | | | 37,326,549 | |

| |

| | | | Citicorp Residential Mortgage Securities, Inc., | |

| | 6,594,000 | | | Series 2006-2-A5 | | | 6.04% | # | | | 09/25/2036 | | | | 5,733,312 | |

| |

| | | | Citigroup Commercial Mortgage Securities, Inc., | |

| | 144,013,510 | | | Series 2004-C2 | | | 1.10% | #^ I/O | | | 10/15/2041 | | | | 907,472 | |

| | 5,326,781 | | | Series 2006-C5 | | | 5.68% | #^ | | | 10/15/2049 | | | | 4,688,423 | |

| | 7,000,000 | | | Series 2009-RR1 | | | 5.32% | ^ | | | 12/21/2049 | | | | 6,853,421 | |

| |

| | | | Citigroup Mortgage Loan Trust, Inc., | |

| | 6,841,646 | | | Series 2005-5-2A2 | | | 5.75% | | | | 08/25/2035 | | | | 5,773,597 | |

| | 2,961,316 | | | Series 2005-9-21A1 | | | 5.50% | | | | 10/25/2035 | | | | 2,426,680 | |

| | 7,903,982 | | | Series 2006-FX1-A6 | | | 5.85% | # | | | 10/25/2036 | | | | 5,271,727 | |

| | 3,375,000 | | | Series 2006-WF1-A2D | | | 5.92% | # | | | 03/25/2036 | | | | 2,363,212 | |

| | 21,282,978 | | | Series 2006-WF2-A2D | | | 6.16% | # | | | 05/25/2036 | | | | 13,465,602 | |

| | 2,303,418 | | | Series 2007-12-2A1 | | | 6.50% | ^ | | | 04/25/2037 | | | | 1,607,323 | |

| | 4,495,817 | | | Series 2007-2-2A | | | 6.00% | | | | 11/25/2036 | | | | 4,364,768 | |

| | 3,302,133 | | | Series 2007-9-2A2 | | | 6.50% | ^ | | | 05/25/2037 | | | | 1,774,897 | |

| | 5,185,041 | | | Series 2010-2-5A1 | | | 5.50% | #^ | | | 12/25/2035 | | | | 5,313,789 | |

| | 36,000,000 | | | Series 2010-8-6A4 | | | 10.78% | #^ | | | 12/26/2036 | | | | 27,720,000 | |

| |

| | | | Commercial Mortgage Pass-Through Certificates, | |

| | 3,750,000 | | | Series 2001-J1A-G | | | 6.83% | #^ | | | 02/16/2034 | | | | 3,762,279 | |

| | 1,540,000 | | | Series 2007-C9-A2 | | | 5.81% | # | | | 12/10/2049 | | | | 1,573,361 | |

| |

| | | | Countrywide Alternative Loan Trust, | |

| | 5,814,470 | | | Series 2005-20CB-4A1 | | | 5.25% | | | | 07/25/2020 | | | | 5,373,245 | |

| | 10,687,216 | | | Series 2005-26CB-A11 | | | 12.60% | # I/F | | | 07/25/2035 | | | | 9,901,918 | |

| | 15,739,335 | | | Series 2005-28CB-1A2 | | | 1.00% | # | | | 08/25/2035 | | | | 11,304,714 | |

| | 3,456,662 | | | Series 2005-28CB-3A6 | | | 6.00% | | | | 08/25/2035 | | | | 2,478,378 | |

| | 1,997,666 | | | Series 2005-60T1-1A | | | 34.10% | # I/F | | | 12/25/2035 | | | | 2,813,333 | |

| | 2,828,323 | | | Series 2005-64CB-1A14 | | | 5.50% | | | | 12/25/2035 | | | | 2,345,906 | |

| | 7,528,307 | | | Series 2005-73CB-1A5 | | | 1.05% | # | | | 01/25/2036 | | | | 5,514,511 | |

| | 18,939,662 | | | Series 2005-73CB-1A6 | | | 4.45% | # I/F I/O | | | 01/25/2036 | | | | 2,620,361 | |

| | 4,350,296 | | | Series 2005-79CB-A5 | | | 5.50% | | | | 01/25/2036 | | | | 3,227,837 | |

| | 8,872,235 | | | Series 2005-85CB-2A6 | | | 20.70% | # I/F | | | 02/25/2036 | | | | 8,614,559 | |

| | 5,897,225 | | | Series 2005-86CB-A5 | | | 5.50% | | | | 02/25/2036 | | | | 4,228,995 | |

| | 12,753,872 | | | Series 2005-J10-1A11 | | | 5.50% | | | | 10/25/2035 | | | | 10,702,941 | |

| | 3,211,502 | | | Series 2005-J10-1A13 | | | 0.95% | # | | | 10/25/2035 | | | | 2,420,841 | |

| | 2,264,073 | | | Series 2005-J10-1A15 | | | 5.50% | | | | 10/25/2035 | | | | 2,024,143 | |

| | 6,556,497 | | | Series 2005-J11-1A3 | | | 5.50% | | | | 11/25/2035 | | | | 6,127,026 | |

| | | | | | | | |

| 10 | | DoubleLine Funds | | | | | The accompanying notes are an integral part of these financial statements | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Countrywide Alternative Loan Trust, (Cont.) | |

| $ | 4,269,929 | | | Series 2005-J11-6A1 | | | 6.50% | | | | 09/25/2032 | | | | 4,117,907 | |

| | 5,735,623 | | | Series 2005-J13-2A5 | | | 0.73% | # | | | 11/25/2035 | | | | 4,245,322 | |

| | 11,471,246 | | | Series 2005-J13-2A6 | | | 4.77% | # I/F I/O | | | 11/25/2035 | | | | 1,233,022 | |

| | 4,907,889 | | | Series 2005-J2-1A5 | | | 0.75% | # | | | 04/25/2035 | | | | 4,067,001 | |

| | 15,101,198 | | | Series 2005-J2-1A6 | | | 4.75% | # I/F I/O | | | 04/25/2035 | | | | 1,648,587 | |

| | 11,853,711 | | | Series 2006-12CB-A3 | | | 5.75% | | | | 05/25/2036 | | | | 7,274,338 | |

| | 5,629,011 | | | Series 2006-15CB-A1 | | | 6.50% | | | | 06/25/2036 | | | | 3,461,355 | |

| | 4,578,253 | | | Series 2006-18CB-A12 | | | 0.85% | # | | | 07/25/2036 | | | | 2,658,910 | |

| | 4,578,253 | | | Series 2006-18CB-A13 | | | 5.25% | # I/F I/O | | | 07/25/2036 | | | | 597,986 | |

| | 4,420,758 | | | Series 2006-19CB-A15 | | | 6.00% | | | | 08/25/2036 | | | | 3,787,601 | |

| | 19,085,837 | | | Series 2006-24CB-A14 | | | 6.90% | # I/F I/O | | | 08/25/2036 | | | | 3,437,958 | |

| | 17,796,700 | | | Series 2006-24CB-A5 | | | 0.85% | # | | | 08/25/2036 | | | | 11,532,226 | |

| | 6,681,009 | | | Series 2006-26CB-A17 | | | 6.25% | | | | 09/25/2036 | | | | 4,597,529 | |

| | 18,926,249 | | | Series 2006-29T1-1A2 | | | 6.25% | | | | 10/25/2036 | | | | 14,301,147 | |

| | 2,493,976 | | | Series 2006-29T1-2A12 | | | 44.50% | # I/F | | | 10/25/2036 | | | | 4,475,785 | |

| | 1,527,613 | | | Series 2006-29T1-2A23 | | | 32.30% | # I/F | | | 10/25/2036 | | | | 1,984,017 | |

| | 6,796,153 | | | Series 2006-36T2-2A1 | | | 6.25% | | | | 12/25/2036 | | | | 4,672,501 | |

| | 6,079,661 | | | Series 2006-39CB-1A10 | | | 6.00% | | | | 01/25/2037 | | | | 4,580,232 | |

| | 29,015,969 | | | Series 2006-39CB-2A2 | | | 6.30% | # I/F I/O | | | 01/25/2037 | | | | 5,733,602 | |

| | 9,731,411 | | | Series 2006-39CB-2A4 | | | 0.70% | # | | | 01/25/2037 | | | | 3,551,279 | |

| | 5,000,000 | | | Series 2006-6CB-1A4 | | | 5.50% | | | | 05/25/2036 | | | | 3,784,623 | |

| | 3,006,974 | | | Series 2007-11T1-A24 | | | 38.40% | # I/F | | | 05/25/2037 | | | | 4,004,625 | |

| | 31,055,194 | | | Series 2007-17CB-1A10 | | | 28.80% | # I/F | | | 08/25/2037 | | | | 40,105,236 | |

| | 5,152,184 | | | Series 2007-18CB-2A25 | | | 6.00% | | | | 08/25/2037 | | | | 3,953,590 | |

| | 2,865,379 | | | Series 2007-19-1A10 | | | 37.50% | # I/F | | | 08/25/2037 | | | | 4,210,921 | |

| | 14,945,136 | | | Series 2007-21CB-2A2 | | | 27.40% | # I/F | | | 09/25/2037 | | | | 20,508,712 | |

| | 25,974,697 | | | Series 2007-4CB-2A1 | | | 7.00% | | | | 03/25/2037 | | | | 12,291,928 | |

| | 1,295,056 | | | Series 2007-8CB-A12 | | | 38.70% | # I/F | | | 05/25/2037 | | | | 1,965,258 | |

| | 1,382,452 | | | Series 2007-8CB-A8 | | | 38.60% | # I/F | | | 05/25/2037 | | | | 2,097,235 | |

| | 1,932,418 | | | Series 2007-9T1-1A4 | | | 0.75% | # | | | 05/25/2037 | | | | 1,118,298 | |

| | 1,932,418 | | | Series 2007-9T1-1A5 | | | 5.25% | # I/F I/O | | | 05/25/2037 | | | | 248,389 | |

| | 5,490,435 | | | Series 2007-9T1-2A1 | | | 6.00% | | | | 05/25/2037 | | | | 3,621,615 | |

| |

| | | | Countrywide Asset-Backed Certificates, | |

| | 4,239,637 | | | Series 2005-13-AF3 | | | 5.43% | | | | 02/25/2033 | | | | 3,445,888 | |

| |

| | | | Countrywide Home Loans Mortgage Pass Through Trust, | |

| | 14,269,771 | | | Series 2002-32-2A6 | | | 5.00% | | | | 01/25/2018 | | | | 14,628,827 | |

| | 4,518,647 | | | Series 2005-27-2A1 | | | 5.50% | | | | 12/25/2035 | | | | 4,132,445 | |

| | 7,713,367 | | | Series 2005-28-A7 | | | 5.25% | | | | 01/25/2019 | | | | 6,652,597 | |

| | 5,730,782 | | | Series 2005-HYB8-1A1 | | | 2.68% | # | | | 12/20/2035 | | | | 4,522,363 | |

| | 9,700,000 | | | Series 2005-J4-A5 | | | 5.50% | | | | 11/25/2035 | | | | 8,211,244 | |

| | 3,000,000 | | | Series 2007-15-1A16 | | | 6.25% | | | | 09/25/2037 | | | | 2,715,681 | |

| | 18,167,073 | | | Series 2007-7-A2 | | | 5.75% | | | | 06/25/2037 | | | | 16,993,779 | |

| | 7,000,000 | | | Series 2007-9-A11 | | | 5.75% | | | | 07/25/2037 | | | | 6,202,298 | |

| | 3,817,011 | | | Series 2007-J3-A1 | | | 0.75% | # | | | 07/25/2037 | | | | 3,163,588 | |

| | 19,085,055 | | | Series 2007-J3-A2 | | | 5.25% | # I/F I/O | | | 07/25/2037 | | | | 2,222,907 | |

| |

| | | | Countrywide Reperforming Trust, | |

| | 3,512,208 | | | Series 2005-R1-1AF1 | | | 0.61% | #^ | | | 03/25/2035 | | | | 3,023,734 | |

| | 3,566,663 | | | Series 2005-R1-1AS | | | 5.68% | #^ I/O | | | 03/25/2035 | | | | 440,111 | |

| |

| | | | Credit Suisse First Boston Commercial Mortgage Pass-Through Certificates, | |

| | 1,235,000 | | | Series 2001-CF2 | | | 6.93% | ^ | | | 02/15/2034 | | | | 1,232,717 | |

| | 7,887,000 | | | Series 2001-CF2 | | | 6.56% | ^ | | | 02/15/2034 | | | | 7,874,025 | |

| | 4,088,000 | | | Series 2001-CK3 | | | 7.29% | ^ | | | 06/15/2034 | | | | 4,081,271 | |

| | 419,546,622 | | | Series 2004-C3 | | | 0.82% | #^ I/O | | | 07/15/2036 | | | | 1,006,954 | |

| | 1,902,892 | | | Series 2004-C3 | | | 4.30% | | | | 07/15/2036 | | | | 1,901,953 | |

| | 336,816,143 | | | Series 2005-C1 | | | 0.49% | #^ I/O | | | 02/15/2038 | | | | 1,215,940 | |

| | 229,026,168 | | | Series 2005-C2 | | | 0.70% | #^ I/O | | | 04/15/2037 | | | | 1,279,363 | |

| | 67,631,820 | | | Series 2005-C4 | | | 0.41% | #^ I/O | | | 08/15/2038 | | | | 239,160 | |

| | 5,963,456 | | | Series 2006-TFL2 | | | 0.49% | #^ | | | 10/15/2021 | | | | 5,838,060 | |

| |

| | | | Credit Suisse First Boston Mortgage Backed Trust, | |

| | 17,774,955 | | | Series 2005-12 | | | 7.00% | | | | 01/25/2036 | | | | 7,289,696 | |

| | 8,083,273 | | | Series 2006-3 | | | 6.11% | # | | | 11/25/2036 | | | | 4,585,451 | |

| | 6,095,595 | | | Series 2006-4 | | | 5.68% | # | | | 12/25/2036 | | | | 3,874,308 | |

| | 18,845,764 | | | Series 2007-1 | | | 5.90% | # | | | 05/25/2037 | | | | 11,511,209 | |

| |

| | | | Credit Suisse First Boston Mortgage Securities Corporation, | |

| | 844,199 | | | Series 2002-34-CB2 | | | 5.87% | # | | | 01/25/2033 | | | | 770,655 | |

| | 650,807 | | | Series 2004-AR8-2A1 | | | 2.84% | # | | | 09/25/2034 | | | | 626,324 | |

| | 2,227,513 | | | Series 2005-10-5A5 | | | 5.50% | | | | 11/25/2035 | | | | 1,905,619 | |

| |

| | | | Credit Suisse Mortgage Capital Certificates, | |

| | 3,055,355 | | | Series 2005-1R | | | 5.75% | ^ | | | 12/26/2035 | | | | 2,513,029 | |

| | 46,607,886 | | | Series 2006-2 | | | 5.05% | # I/F I/O | | | 03/25/2036 | | | | 5,933,561 | |

| | 8,338,411 | | | Series 2006-2 | | | 0.95% | # | | | 03/25/2036 | | | | 4,847,360 | |

| | 7,317,095 | | | Series 2006-2 | | | 6.50% | | | | 03/25/2036 | | | | 5,241,678 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| $ | 18,840,082 | | | Series 2006-6 | | | 7.00% | | | | 07/25/2036 | | | | 8,276,966 | |

| | 31,593,264 | | | Series 2006-6 | | | 6.00% | | | | 07/25/2036 | | | | 20,292,811 | |

| | 1,395,000 | | | Series 2006-7 | | | 6.00% | | | | 08/25/2036 | | | | 1,185,111 | |

| | 5,969,620 | | | Series 2006-9 | | | 38.40% | # I/F | | | 11/25/2036 | | | | 8,317,569 | |

| | 12,327,207 | | | Series 2006-9 | | | 6.00% | | | | 11/25/2036 | | | | 11,214,615 | |

| | 45,802,635 | | | Series 2007-1-3A1 | | | 6.00% | | | | 02/25/2022 | | | | 36,653,192 | |

| | 11,721,527 | | | Series 2007-5 | | | 5.00% | | | | 08/25/2037 | | | | 10,796,828 | |

| | 5,125,847 | | | Series 2009-1R | | | 4.86% | #^ | | | 07/26/2035 | | | | 3,203,654 | |

| |

| | | | Credit-Based Asset Servicing and Securitization, | |

| | 1,445,893 | | | Series 2005-CB6-A4 | | | 5.16% | # | | | 06/25/2035 | | | | 1,357,562 | |

| | 9,750,000 | | | Series 2007-MX1-A3 | | | 5.83% | #^ | | | 12/25/2036 | | | | 7,929,626 | |

| |

| | | | Deutsche ALT-A Securities Inc. Alternate Loan, | |

| | 40,759,000 | | | Series 2005-4-A5 | | | 5.50% | # | | | 09/25/2035 | | | | 32,847,739 | |

| | 3,626,687 | | | Series 2005-5-1A6 | | | 34.10% | # I/F | | | 11/25/2035 | | | | 4,681,979 | |

| | 3,783,741 | | | Series 2005-5-2A1 | | | 0.45% | # | | | 11/25/2035 | | | | 2,617,174 | |

| | 11,419,740 | | | Series 2005-5-2A2 | | | 5.05% | # I/F I/O | | | 11/25/2035 | | | | 1,477,878 | |

| | 12,955,254 | | | Series 2007-1-A7 | | | 0.41% | # | | | 08/25/2037 | | | | 12,208,085 | |

| | 3,400,361 | | | Series 2006-AF1-A3 | | | 0.43% | # | | | 04/25/2036 | | | | 2,611,273 | |

| |

| | | | Deutsche ALT-B Securities Inc. Mortgage Loan Trust, | |

| | 2,500,000 | | | Series 2006-AB2-A2 | | | 6.16% | # | | | 06/25/2036 | | | | 1,705,916 | |

| | 5,763,601 | | | Series 2006-AB4-A1A | | | 6.01% | # | | | 10/25/2036 | | | | 3,409,913 | |

| | 5,733,509 | | | Series 2006-AB4-A3 | | | 5.90% | # | | | 10/25/2036 | | | | 3,363,924 | |

| | 8,498,665 | | | Series 2006-AB4-A3A1 | | | 5.90% | # | | | 10/25/2036 | | | | 4,986,286 | |

| | 2,677,182 | | | Series 2006-AB4-A6A1 | | | 5.87% | # | | | 10/25/2036 | | | | 1,699,248 | |

| |

| | | | Deutsche Mortgage Securities, Inc., | |

| | 22,927,328 | | | Series 2006-PR1-4A12 | | | 14.10% | #^ I/F | | | 04/15/2036 | | | | 25,334,697 | |

| | 13,965,830 | | | Series 2006-PR1-4AI1 | | | 11.80% | #^ I/F | | | 04/15/2036 | | | | 14,773,236 | |

| | 148,038,686 | | | Series 2006-PR1-5A14 | | | 11.80% | #^ I/F | | | 04/15/2036 | | | | 154,284,141 | |

| | 1,037,181 | | | Series 2006-PR1-5AI1 | | | 18.60% | #^ I/F | | | 04/15/2036 | | | | 1,061,096 | |

| | 8,944,189 | | | Series 2006-PR1-5AI3 | | | 12.20% | #^ I/F | | | 04/15/2036 | | | | 8,692,223 | |

| |

| | | | DLJ Commercial Mortgage Corporation, | |

| | 4,000,000 | | | Series 2000-CKP1-B1 | | | 7.95% | # | | | 11/10/2033 | | | | 3,996,697 | |

| |

| | | | Ellington Loan Acquisition Trust, | |

| | 4,588,613 | | | Series 2007-1-A2A2 | | | 1.05% | #^ | | | 05/25/2037 | | | | 4,257,705 | |

| |

| | | | Extended Stay American Trust, | |

| | 290,115,558 | | | Series 2010-ESH-XA1 | | | 3.33% | #^ I/O | | | 01/05/2013 | | | | 14,953,600 | |

| | 102,500,000 | | | Series 2010-ESH-XB1 | | | 1.37% | #^ I/O | | | 01/05/2016 | | | | 2,069,701 | |

| |

| | | | First Horizon Alternative Mortgage Securities, | |

| | 1,213,964 | | | Series 2006-FA1-1A6 | | | 1.00% | # | | | 09/25/2034 | | | | 1,022,769 | |

| | 7,446,394 | | | Series 2006-FA2-1A5 | | | 6.00% | | | | 05/25/2036 | | | | 6,037,250 | |

| | 2,182,271 | | | Series 2006-FA7-A8 | | | 6.25% | | | | 12/25/2036 | | | | 1,653,035 | |

| | 25,339,823 | | | Series 2006-RE1-A1 | | | 5.50% | | | | 05/25/2035 | | | | 22,535,135 | |

| | 2,970,551 | | | Series 2007-FA3-A4 | | | 6.00% | | | | 06/25/2037 | | | | 2,058,203 | |

| |

| | | | First Horizon Mortgage Trust, | |

| | 166,243 | | | Series 2005-2-1A6 | | | 22.90% | # I/F | | | 06/25/2032 | | | | 167,776 | |

| | 1,235,145 | | | Series 2005-6-1A1 | | | 5.50% | | | | 11/25/2035 | | | | 1,236,224 | |

| |

| | | | First Union Commercial Mortgage Securities, Inc., | |

| | 8,000,000 | | | Series 2000-C2-G | | | 8.65% | # | | | 10/15/2032 | | | | 7,986,002 | |

| | 1,500,000 | | | Series 2001-C1-F | | | 6.84% | | | | 03/15/2033 | | | | 1,503,049 | |

| |

| | | | GE Capital Commercial Mortgage Corporation, | |

| | 1,676,984 | | | Series 2004-C2 | | | 0.76% | #^ I/O | | | 03/10/2040 | | | | 34 | |

| |

| | | | GMAC Commercial Mortgage Securities, Inc., | |

| | 348,783 | | | Series 2003-C3 | | | 4.65% | | | | 04/10/2040 | | | | 360,950 | |

| | 2,388,875 | | | Series 2004-C1 | | | 1.01% | #^ I/O | | | 03/10/2038 | | | | 65 | |

| | 54,153,612 | | | Series 2004-C2 | | | 0.56% | #^ I/O | | | 08/10/2038 | | | | 80,635 | |

| | 9,000,000 | | | Series 2004-C3 | | | 4.55% | | | | 12/10/2041 | | | | 9,116,321 | |

| | 134,194,710 | | | Series 2004-C3 | | | 0.79% | # I/O | | | 12/10/2041 | | | | 494,306 | |

| |

| | | | GMAC Mortgage Corporation Loan Trust, | |

| | 2,836,897 | | | Series 2004-J2-A6 | | | 16.30% | # I/F | | | 06/25/2034 | | | | 2,956,497 | |

| |

| | | | Greenwich Capital Commercial Funding Corporation, | |

| | 6,500,000 | | | Series 2004-FL2 | | | 0.74% | #^ | | | 11/05/2019 | | | | 6,208,497 | |

| | 7,936,000 | | | Series 2004-FL2-F | | | 0.57% | #^ | | | 11/05/2019 | | | | 7,797,618 | |

| |

| | | | GS Mortgage Securities Corporation, | |

| | 3,352,303 | | | Series 2008-2R-1A1 | | | 7.50% | #^ | | | 09/25/2036 | | | | 2,955,264 | |

| |

| | | | GS Mortgage Securities Corporation II, | |

| | 6,750,000 | | | Series 2001-GS3-D | | | 6.74% | #^ | | | 08/05/2018 | | | | 6,853,648 | |

| | 36,698,949 | | | Series 2011-GC3-X | | | 1.35% | #^ I/O | | | 03/10/2021 | | | | 1,909,010 | |

| | | | | | |

| The accompanying notes are an integral part of these financial statements | | Annual Report | | March 31, 2011 | | 11 |

| | |

| |

| Schedule of Investments DoubleLine Total Return Bond Fund (Cont.) | | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | GSAA Home Equity Trust, | |

| $ | 2,445,082 | | | Series 2005-12-AF3 | | | 5.07% | # | | | 09/25/2035 | | | | 2,343,187 | |

| | 45,361,000 | | | Series 2005-7-AF3 | | | 4.75% | # | | | 05/25/2035 | | | | 38,238,347 | |

| | 16,688,832 | | | Series 2006-10-AF3 | | | 5.98% | # | | | 06/25/2036 | | | | 10,171,017 | |

| | 11,944,483 | | | Series 2006-10-AF4 | | | 6.30% | # | | | 06/25/2036 | | | | 7,328,394 | |

| | 9,115,724 | | | Series 2006-15-AF4 | | | 5.96% | # | | | 09/25/2036 | | | | 5,844,706 | |

| | 3,936,728 | | | Series 2006-18-AF3A | | | 5.77% | # | | | 11/25/2036 | | | | 2,454,207 | |

| | 8,083,328 | | | Series 2006-18-AF6 | | | 5.68% | # | | | 11/25/2036 | | | | 4,657,703 | |

| | 7,461,627 | | | Series 2006-4-4A1 | | | 0.35% | # | | | 03/25/2036 | | | | 6,809,626 | |

| | 8,149,448 | | | Series 2007-10-A2A | | | 6.50% | | | | 11/25/2037 | | | | 5,879,085 | |

| |

| | | | GSMPS Mortgage Loan Trust, | |

| | 29,582,470 | | | Series 2005-RP2-1AF | | | 0.60% | #^ | | | 03/25/2035 | | | | 25,575,569 | |

| | 29,582,470 | | | Series 2005-RP2-1AS | | | 5.40% | #^ I/O | | | 03/25/2035 | | | | 4,081,008 | |

| | 16,084,450 | | | Series 2005-RP3-1AF | | | 0.60% | #^ | | | 09/25/2035 | | | | 13,846,243 | |

| | 16,084,450 | | | Series 2005-RP3-1AS | | | 5.27% | #^ I/O | | | 09/25/2035 | | | | 2,299,972 | |

| |

| | | | GSR Mortgage Loan Trust, | |

| | 1,956,545 | | | Series 2005-6F-3A16 | | | 5.50% | | | | 07/25/2035 | | | | 1,957,184 | |

| | 2,789,347 | | | Series 2005-6F-3A16 | | | 6.00% | | | | 07/25/2035 | | | | 2,677,883 | |

| | 35,616,345 | | | Series 2005-6F-3A9 | | | 6.65% | # I/F I/O | | | 07/25/2035 | | | | 6,007,790 | |

| | 3,680,936 | | | Series 2005-6F-4A1 | | | 0.75% | # | | | 06/25/2035 | | | | 3,499,687 | |

| | 4,027,331 | | | Series 2005-7F-3A1 | | | 0.75% | # | | | 09/25/2035 | | | | 3,556,874 | |

| | 4,410,708 | | | Series 2006-2F-2A3 | | | 5.75% | | | | 02/25/2036 | | | | 3,844,009 | |

| | 1,388,876 | | | Series 2006-9F-8A1 | | | 5.50% | | | | 08/25/2021 | | | | 1,341,959 | |

| |

| | | | Gulf Stream Compass Ltd., | |

| | 2,185,700 | | | Series 2002-1A-A | | | 0.89% | #^ | | | 12/19/2014 | | | | 2,147,451 | |

| |

| | | | Harborview Mortgage Loan Trust, | |

| | 7,272,569 | | | Series 2005-14-3A1A | | | 2.94% | # | | | 12/19/2035 | | | | 5,855,869 | |

| |

| | | | Home Equity Asset Trust, | |

| | 6,375,000 | | | Series 2004-7 | | | 0.91% | # | | | 01/25/2035 | | | | 5,576,232 | |

| |

| | | | Home Equity Mortgage Trust, | |

| | 3,142,370 | | | Series 2003-3-M1 | | | 1.54% | # | | | 08/25/2033 | | | | 2,621,186 | |

| |

| | | | Homebanc Mortgage Trust, | |

| | 3,950,570 | | | Series 2005-1 | | | 0.74% | # | | | 03/25/2035 | | | | 2,907,721 | |

| | 8,805,488 | | | Series 2006-1 | | | 5.74% | # | | | 04/25/2037 | | | | 7,369,850 | |

| |

| | | | HSI Asset Loan Obligation, | |

| | 10,061,620 | | | Series 2006-2-2A1 | | | 5.50% | | | | 12/25/2021 | | | | 9,391,214 | |

| |

| | | | IMPAC Trust, | |

| | 2,882,921 | | | Series 2002-9F-A1 | | | 5.22% | # | | | 12/25/2032 | | | | 2,882,405 | |

| |

| | | | Indymac Mortgage Loan Trust, | |

| | 1,616,395 | | | Series 2007-F2-1A2 | | | 6.00% | | | | 07/25/2037 | | | | 1,311,481 | |

| |

| | | | Jefferies & Company Research Trust, | |

| | 3,385,862 | | | Series 2010-R6-1A2 | | | 6.00% | ^ | | | 09/26/2037 | | | | 3,386,190 | |

| |

| | | | JMAC Company, | |

| | 14,429,434 | | | Series 2010-R1-1A1 | | | 6.00% | #^ | | | 03/26/2037 | | | | 14,663,912 | |

| |

| | | | JP Morgan Alternative Loan Trust, | |

| | 11,003,867 | | | Series 2005-S1-2A9 | | | 6.00% | | | | 12/25/2035 | | | | 9,446,672 | |

| | 1,991,656 | | | Series 2006-A6-1A2 | | | 0.32% | # | | | 11/25/2036 | | | | 1,961,732 | |

| | 10,165,776 | | | Series 2006-S1-1A8 | | | 5.75% | | | | 03/25/2036 | | | | 7,749,234 | |

| | 6,500,000 | | | Series 2006-S2-A4 | | | 6.19% | # | | | 05/25/2036 | | | | 3,272,792 | |

| | 14,745,000 | | | Series 2006-S4-A3A | | | 5.78% | # | | | 12/25/2036 | | | | 13,429,193 | |

| |

| | | | JP Morgan Chase, | |

| | 193,752,465 | | | Series 2007-CIBC18-X | | | 0.44% | # I/O | | | 06/12/2047 | | | | 2,624,552 | |

| |

| | | | JP Morgan Chase Commercial Mortgage Securities Trust, | |

| | 6,000,000 | | | Series 2001-C1-F | | | 7.05% | #^ | | | 10/12/2035 | | | | 6,065,935 | |

| | 12,671,000 | | | Series 2001-CBC1-E | | | 7.07% | # | | | 03/15/2033 | | | | 12,656,617 | |

| | 10,000,000 | | | Series 2001-CBC1-F | | | 7.54% | # | | | 03/15/2033 | | | | 9,975,039 | |

| | 5,000,000 | | | Series 2001-CIC2-C | | | 6.74% | # | | | 04/15/2035 | | | | 5,025,850 | |

| |

| | | | JP Morgan Commercial Mortgage Certificates, | |

| | 1,075,594 | | | Series 1997-C5-F | | | 7.56% | | | | 09/15/2029 | | | | 1,119,021 | |

| | 1,153,497 | | | Series 2003-CIBC7-A3 | | | 4.45% | | | | 01/12/2038 | | | | 1,154,933 | |

| | 30,537,572 | | | Series 2004-CBX-X1 | | | 0.54% | #^ I/O | | | 01/12/2037 | | | | 533,641 | |

| | 11,680,000 | | | Series 2004-CIBC10-A5 | | | 4.65% | | | | 01/12/2037 | | | | 12,056,173 | |

| | 322,071,828 | | | Series 2005-LDP3-X2 | | | 0.31% | # I/O | | | 08/15/2042 | | | | 864,119 | |

| | 134,475,570 | | | Series 2005-LDP4-X1 | | | 0.17% | #^ I/O | | | 10/15/2042 | | | | 954,064 | |

| | 337,964,573 | | | Series 2006-CIBC14-X2 | | | 0.16% | # I/O | | | 12/12/2044 | | | | 531,179 | |

| | 106,980,598 | | | Series 2006-CIBC16-X2 | | | 0.71% | # I/O | | | 05/12/2045 | | | | 1,275,305 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | JP Morgan Mortgage Acquisition Trust, | |

| $ | 16,000,000 | | | Series 2006-CH2-AF3 | | | 5.46% | | | | 10/25/2036 | | | | 9,837,016 | |

| | 25,430,821 | | | Series 2006-S4-A8 | | | 0.63% | # | | | 01/25/2037 | | | | 16,990,319 | |

| | 25,430,821 | | | Series 2006-S4-A9 | | | 6.37% | # I/F I/O | | | 01/25/2037 | | | | 4,179,500 | |

| | 6,841,000 | | | Series 2006-WF1-A5 | | | 6.41% | # | | | 07/25/2036 | | | | 4,180,901 | |

| |

| | | | JP Morgan Mortgage Trust, | |

| | 2,955,902 | | | Series 2003-A1-4A2 | | | 4.50% | # | | | 10/25/2033 | | | | 2,982,542 | |

| | 4,000,000 | | | Series 2007-S3-1A9 | | | 6.00% | | | | 08/25/2037 | | | | 3,347,040 | |

| | 27,530,684 | | | Series 2007-S3-2A2 | | | 5.50% | | | | 08/25/2022 | | | | 26,004,645 | |

| |

| | | | JP Morgan Research Trust, | |

| | 27,546,803 | | | Series 2010-1-1A4 | | | 6.00% | #^ | | | 02/26/2037 | | | | 14,558,485 | |

| | 12,470,275 | | | Series 2010-8-2A3 | | | 4.50% | ^ | | | 11/26/2034 | | | | 12,244,563 | |

| |

| | | | LB-UBS Commercial Mortgage Trust, | |

| | 54,376,003 | | | Series 2005-C1-XCP | | | 0.87% | # I/O | | | 02/15/2040 | | | | 334,086 | |

| | 177,695,140 | | | Series 2005-C2-XCP | | | 0.51% | # I/O | | | 04/15/2040 | | | | 478,195 | |

| | 58,366,115 | | | Series 2005-C5-XCP | | | 0.60% | # I/O | | | 09/15/2040 | | | | 370,502 | |

| | 203,093,794 | | | Series 2006-C7-XCL | | | 0.40% | #^ I/O | | | 11/15/2038 | | | | 3,172,914 | |

| |

| | | | Lehman Mortgage Trust, | |

| | 4,167,382 | | | Series 2005-3-2A3 | | | 5.50% | | | | 01/25/2036 | | | | 3,929,687 | |

| | 5,180,487 | | | Series 2006-1-1A1 | | | 1.01% | # | | | 02/25/2036 | | | | 3,554,521 | |

| | 15,541,460 | | | Series 2006-1-1A2 | | | 4.50% | # I/F I/O | | | 02/25/2036 | | | | 1,660,164 | |

| | 6,773,067 | | | Series 2006-1-3A4 | | | 5.50% | | | | 02/25/2036 | | | | 5,901,715 | |

| | 13,690,414 | | | Series 2006-4-1A3 | | | 5.15% | # I/F I/O | | | 08/25/2036 | | | | 1,640,873 | |

| | 8,701,331 | | | Series 2006-4-1A4 | | | 6.00% | | | | 08/25/2036 | | | | 6,036,387 | |

| | 16,876,017 | | | Series 2006-5-2A1 | | | 0.60% | # | | | 09/25/2036 | | | | 8,017,424 | |

| | 35,152,560 | | | Series 2006-5-2A2 | | | 6.90% | # I/F I/O | | | 09/25/2036 | | | | 6,580,784 | |

| | 8,116,052 | | | Series 2006-7-2A2 | | | 0.70% | # | | | 11/25/2036 | | | | 4,302,790 | |

| | 23,844,403 | | | Series 2006-7-2A5 | | | 6.30% | # I/F I/O | | | 11/25/2036 | | | | 3,903,717 | |

| | 8,872,986 | | | Series 2006-9-1A19 | | | 24.50% | # I/F | | | 01/25/2037 | | | | 12,028,920 | |

| | 9,368,550 | | | Series 2006-9-1A5 | | | 0.85% | # | | | 01/25/2037 | | | | 5,593,277 | |

| | 28,246,864 | | | Series 2006-9-1A6 | | | 4.90% | # I/F I/O | | | 01/25/2037 | | | | 4,101,238 | |

| | 10,365,645 | | | Series 2006-9-2A1 | | | 0.63% | # | | | 01/25/2037 | | | | 5,096,223 | |

| | 24,588,614 | | | Series 2006-9-2A2 | | | 6.37% | # I/F I/O | | | 01/25/2037 | | | | 4,176,774 | |

| | 7,815,812 | | | Series 2007-2-1A1 | | | 5.75% | | | | 03/25/2037 | | | | 5,864,966 | |

| | 6,885,908 | | | Series 2007-4-2A11 | | | 0.58% | # | | | 05/25/2037 | | | | 2,960,941 | |

| | 24,442,818 | | | Series 2007-4-2A8 | | | 6.42% | # I/F I/O | | | 05/25/2037 | | | | 4,223,536 | |

| | 2,982,926 | | | Series 2007-4-2A9 | | | 0.58% | # | | | 05/25/2037 | | | | 1,342,317 | |

| | 36,875,348 | | | Series 2007-5-11A1 | | | 6.09% | # | | | 06/25/2037 | | | | 24,715,222 | |

| | 1,905,261 | | | Series 2007-5-7A3 | | | 7.50% | | | | 10/25/2036 | | | | 1,896,650 | |

| | 1,970,957 | | | Series 2007-6-1A8 | | | 6.00% | | | | 07/25/2037 | | | | 1,619,181 | |

| |

| | | | Lehman XS Trust, | |

| | 4,363,245 | | | Series 2005-10-2A3B | | | 5.55% | # | | | 01/25/2036 | | | | 3,545,649 | |

| | 16,500,000 | | | Series 2005-4-2A3A | | | 5.00% | # | | | 10/25/2035 | | | | 11,433,411 | |

| | 799,114 | | | Series 2006-19-A1 | | | 0.35% | # | | | 12/25/2036 | | | | 768,029 | |

| | 7,153,425 | | | Series 2006-5-2A4A | | | 5.89% | | | | 04/25/2036 | | | | 6,029,683 | |

| |

| | | | Marathon Financing B.V., | |

| | 1,396,908 | | | Series 2006-1-A1 | | | 0.67% | #^ | | | 10/05/2026 | | | | 1,372,462 | |

| |

| | | | MASTR Adjustable Rate Mortgages Trust, | |

| | 8,778,713 | | | Series 2005-2-2A1 | | | 2.49% | # | | | 03/25/2035 | | | | 5,984,690 | |

| |

| | | | MASTR Alternative Loans Trust, | |

| | 4,537,855 | | | Series 2005-2-3A1 | | | 6.00% | | | | 03/25/2035 | | | | 4,562,427 | |

| | 3,748,589 | | | Series 2005-5-2A3 | | | 5.50% | | | | 07/25/2025 | | | | 3,621,102 | |

| | 14,890,148 | | | Series 2007-1-2A7 | | | 6.00% | | | | 10/25/2036 | | | | 13,170,433 | |

| |

| | | | MASTR Asset Backed Securities Trust, | |

| | 4,975,000 | | | Series 2003-OPT1-M3 | | | 4.37% | # | | | 12/25/2032 | | | | 3,717,718 | |

| |

| | | | MASTR Asset Securitization Trust, | |

| | 1,574,161 | | | Series 2003-1-30B2 | | | 5.75% | | | | 02/25/2033 | | | | 1,573,629 | |

| | 1,770,057 | | | Series 2007-1-1A1 | | | 5.50% | | | | 11/25/2037 | | | | 1,672,698 | |

| |

| | | | MASTR Seasoned Securitization Trust, | |

| | 1,382,286 | | | Series 2005-2-1A4 | | | 6.00% | | | | 10/25/2032 | | | | 1,283,483 | |

| | 4,725,776 | | | Series 2005-2-2A1 | | | 0.65% | # | | | 10/25/2032 | | | | 4,149,396 | |

| |

| | | | Merrill Lynch Mortgage Trust, | |

| | 428,125,242 | | | Series 2004-BPC1-XP | | | 0.93% | #^ I/O | | | 10/12/2041 | | | | 3,243,777 | |

| | 369,172,635 | | | Series 2005-MCP1-ASB | | | 0.83% | # I/O | | | 06/12/2043 | | | | 5,041,422 | |

| |

| | | | Morgan Stanley Capital, Inc., | |

| | 1,485,000 | | | Series 1999-LIFE1-G | | | 7.07% | #^ | | | 04/15/2033 | | | | 1,489,973 | |

| | 2,122,335 | | | Series 2003-NC6-M2 | | | 3.17% | # | | | 06/25/2033 | | | | 1,894,726 | |

| | 192,365,029 | | | Series 2004-HQ4-X2 | | | 0.51% | #^ I/O | | | 04/14/2040 | | | | 1,060,393 | |

| | 219,735,831 | | | Series 2005-IQ9-X2 | | | 1.26% | #^ I/O | | | 07/15/2056 | | | | 1,879,840 | |

| | 931,748 | | | Series 2005-RR6-A2 | | | 0.47% | #^ | | | 05/24/2043 | | | | 924,760 | |

| | | | | | | | |

| 12 | | DoubleLine Funds | | | | | The accompanying notes are an integral part of these financial statements | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Morgan Stanley Capital, Inc., (Cont.) | |

| $ | 9,373,542 | | | Series 2007-HQ12-A2 | | | 0.51% | # | | | 04/12/2049 | | | | 8,853,402 | |

| | 18,747,084 | | | Series 2007-HQ12-A2FX | | | 5.78% | # | | | 06/12/2012 | | | | 19,215,762 | |

| |

| | | | Morgan Stanley Mortgage Loan Trust, | |

| | 5,337,985 | | | Series 2005-10-1A1 | | | 0.95% | # | | | 12/25/2035 | | | | 3,886,745 | |

| | 2,703,007 | | | Series 2005-6AR-1A1 | | | 0.53% | # | | | 11/25/2035 | | | | 2,333,502 | |

| | 8,508,520 | | | Series 2006-11-1A6 | | | 6.23% | # | | | 08/25/2036 | | | | 4,635,088 | |

| | 25,034,811 | | | Series 2006-11-2A1 | | | 6.00% | | | | 08/25/2036 | | | | 19,445,552 | |

| | 12,838,160 | | | Series 2006-17XS-A3A | | | 5.65% | # | | | 10/25/2046 | | | | 8,538,172 | |

| | 3,830,040 | | | Series 2006-17XS-A6 | | | 5.58% | # | | | 10/25/2046 | | | | 2,339,007 | |

| | 1,947,545 | | | Series 2006-2-2A3 | | | 5.75% | | | | 02/25/2036 | | | | 1,724,871 | |

| | 7,491,810 | | | Series 2006-7-4A7 | | | 6.00% | | | | 06/25/2036 | | | | 5,732,261 | |

| | 5,860,598 | | | Series 2007-1XS-2A3 | | | 5.92% | # | | | 09/25/2046 | | | | 3,417,508 | |

| | 4,460,103 | | | Series 2007-1XS-2A4A | | | 6.08% | # | | | 09/25/2046 | | | | 3,017,849 | |

| | 3,990,809 | | | Series 2007-3XS-1A2A | | | 5.62% | # | | | 01/25/2047 | | | | 3,454,790 | |

| | 13,347,125 | | | Series 2007-3XS-2A3S | | | 5.86% | # | | | 01/25/2047 | | | | 8,785,151 | |

| | 7,806,809 | | | Series 2007-3XS-2A4S | | | 5.96% | # | | | 01/25/2047 | | | | 5,169,083 | |

| |

| | | | Morgan Stanley Re-Remic Trust, | |

| | 7,916,879 | | | Series 2010-R9-1A | | | 4.00% | ^ | | | 08/26/2036 | | | | 8,117,623 | |

| | 9,474,955 | | | Series 2010-R9-1B | | | 7.67% | #^ | | | 08/26/2036 | | | | 5,258,600 | |

| |

| | | | Multi Security Asset Trust, | |

| | 7,500,000 | | | Series 2005-RR4-A3 | | | 5.00% | ^ | | | 11/28/2035 | | | | 7,275,000 | |

| |

| | | | New York Mortgage Trust, | |

| | 2,310,755 | | | Series 2005-2-A | | | 0.58% | # | | | 08/25/2035 | | | | 2,076,125 | |

| |

| | | | Nomura Asset Acceptance Corporation, | |

| | 3,191,114 | | | Series 2005-AP1-2A5 | | | 4.86% | # | | | 02/25/2035 | | | | 2,904,311 | |

| |

| | | | Nomura Asset Alternative Loan Trust, | |

| | 23,146,703 | | | Series 2006-AF1-IA2 | | | 6.16% | # | | | 05/25/2036 | | | | 13,218,781 | |

| | 4,703,824 | | | Series 2006-AF1-IA3 | | | 6.41% | | | | 05/25/2036 | | | | 2,633,024 | |

| | 25,553,497 | | | Series 2006-AP1-A2 | | | 5.52% | # | | | 01/25/2036 | | | | 18,203,404 | |

| | 5,000,000 | | | Series 2006-AP1-A3 | | | 5.65% | | | | 01/25/2036 | | | | 3,445,295 | |

| | 2,650,476 | | | Series 2006-WF1-A2 | | | 5.76% | # | | | 06/25/2036 | | | | 1,664,605 | |

| |

| | | | Nomura Home Equity Loan Trust, | |

| | 24,349,412 | | | Series 2006-AF1-A2 | | | 5.80% | # | | | 10/25/2036 | | | | 11,949,291 | |

| | 4,574,651 | | | Series 2007-1-1A1 | | | 6.06% | # | | | 02/25/2037 | | | | 2,422,690 | |

| | 18,735,525 | | | Series 2007-1-1A3 | | | 5.99% | # | | | 02/25/2037 | | | | 10,253,466 | |

| |

| | | | Option One Mortgage Loan Trust, | |

| | 1,598,695 | | | Series 2002-2-A | | | 0.79% | # | | | 06/25/2032 | | | | 1,346,145 | |

| | 8,410,261 | | | Series 2004-3-M3 | | | 0.90% | # | | | 11/25/2034 | | | | 6,910,274 | |

| |

| | | | PHH Alternative Mortgage Trust, | |

| | 2,677,440 | | | Series 2007-2-3A1 | | | 6.00% | | | | 05/25/2037 | | | | 2,296,618 | |

| |

| | | | PNC Mortgage Acceptance Corporation, | |

| | 425,824 | | | Series 1999-CM1-B3 | | | 7.10% | ^ | | | 12/10/2032 | | | | 425,678 | |

| |

| | | | Popular ABS Mortgage Pass-Through Trust, | |

| | 1,594,020 | | | Series 2005-5-AF6 | | | 5.33% | # | | | 11/25/2035 | | | | 1,353,788 | |

| |

| | | | Prime Mortgage Trust, | |

| | 8,092,445 | | | Series 2006-1-2A5 | | | 6.00% | | | | 06/25/2036 | | | | 7,652,378 | |

| | 6,324,223 | | | Series 2006-DR1-2A1 | | | 5.50% | ^ | | | 05/25/2035 | | | | 5,715,981 | |

| |

| | | | Prudential Commercial Mortgage Trust, | |

| | 2,361,363 | | | Series 2003-PWR1-A1 | | | 3.67% | | | | 02/11/2036 | | | | 2,367,147 | |

| |

| | | | Prudential Mortgage Capital Funding, LLC, | |

| | 2,000,000 | | | Series 2001-C1-F | | | 7.40% | #^ | | | 05/10/2034 | | | | 2,000,347 | |

| |

| | | | Renaissance Home Equity Loan Trust, | |

| | 1,994,294 | | | Series 2006-1-AF6 | | | 5.75% | # | | | 05/25/2036 | | | | 1,492,175 | |

| | 11,300,000 | | | Series 2006-4-AF4 | | | 5.47% | # | | | 01/25/2037 | | | | 6,404,343 | |

| | 22,252,000 | | | Series 2006-4-AF5 | | | 5.69% | # | | | 01/25/2037 | | | | 12,973,139 | |

| | 18,490,000 | | | Series 2007-2-AF2 | | | 5.68% | # | | | 06/25/2037 | | | | 10,015,266 | |

| | 10,000,000 | | | Series 2007-2-AF5 | | | 6.20% | # | | | 06/25/2037 | | | | 5,935,100 | |

| |

| | | | Residential Accredit Loans, Inc., | |

| | 1,437,869 | | | Series 2005-QS12-A11 | | | 48.40% | # I/F | | | 08/25/2035 | | | | 2,315,346 | |

| | 7,038,177 | | | Series 2005-QS13-1A6 | | | 5.50% | | | | 09/25/2035 | | | | 6,031,253 | |

| | 11,486,541 | | | Series 2005-QS13-A1 | | | 0.95% | # | | | 09/25/2035 | | | | 7,803,244 | |

| | 47,094,819 | | | Series 2005-QS13-A2 | | | 4.80% | # I/F I/O | | | 09/25/2035 | | | | 6,355,097 | |

| | 21,921,597 | | | Series 2005-QS14-2A1 | | | 6.00% | | | | 09/25/2035 | | | | 17,040,469 | |

| | 11,111,626 | | | Series 2005-QS15-IIA | | | 6.00% | | | | 10/25/2035 | | | | 6,879,247 | |

| | 12,691,503 | | | Series 2005-QS16-A1 | | | 0.95% | # | | | 11/25/2035 | | | | 8,980,285 | |

| | 12,691,503 | | | Series 2005-QS16-A2 | | | 4.55% | # I/F I/O | | | 11/25/2035 | | | | 1,315,487 | |

| | 5,654,468 | | | Series 2005-QS17-A1 | | | 6.00% | | | | 12/25/2035 | | | | 4,393,349 | |

| | 4,241,656 | | | Series 2005-QS17-A10 | | | 6.00% | | | | 12/25/2035 | | | | 3,117,506 | |

| | 12,609,349 | | | Series 2005-QS17-A2 | | | 1.10% | # | | | 12/25/2035 | | | | 8,188,549 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| $ | 12,609,349 | | | Series 2005-QS17-A4 | | | 4.90% | # I/F I/O | | | 12/25/2035 | | | | 1,497,032 | |

| | 10,145,872 | | | Series 2005-QS17-A6 | | | 6.00% | | | | 12/25/2035 | | | | 7,456,947 | |

| | 7,889,981 | | | Series 2005-QS1-A5 | | | 5.50% | | | | 01/25/2035 | | | | 6,791,289 | |

| | 5,228,124 | | | Series 2005-QS9-A1 | | | 0.75% | # | | | 06/25/2035 | | | | 4,331,697 | |

| | 13,070,310 | | | Series 2005-QS9-A4 | | | 4.75% | # I/F I/O | | | 06/25/2035 | | | | 1,490,891 | |

| | 4,788,247 | | | Series 2006-QS10-A4 | | | 5.75% | | | | 08/25/2036 | | | | 3,180,928 | |

| | 5,448,073 | | | Series 2006-QS12-1A1 | | | 6.50% | | | | 09/25/2036 | | | | 3,703,486 | |

| | 12,465,761 | | | Series 2006-QS12-2A18 | | | 5.75% | | | | 09/25/2036 | | | | 8,340,672 | |

| | 5,245,824 | | | Series 2006-QS1-A6 | | | 40.90% | # I/F | | | 01/25/2036 | | | | 7,431,916 | |

| | 7,619,883 | | | Series 2006-QS4-A8 | | | 1.36% | # I/F | | | 04/25/2036 | | | | 5,721,512 | |

| | 15,329,181 | | | Series 2006-QS5-A3 | | | 6.00% | | | | 05/25/2036 | | | | 11,165,101 | |

| | 29,533,818 | | | Series 2006-QS8-A1 | | | 6.00% | | | | 08/25/2036 | | | | 19,282,940 | |

| | 51,215,952 | | | Series 2006-QS8-A5 | | | 5.30% | # I/F I/O | | | 08/25/2036 | | | | 6,391,141 | |

| | 5,290,550 | | | Series 2007-QS1-1A4 | | | 6.00% | | | | 01/25/2037 | | | | 3,585,792 | |

| | 2,293,965 | | | Series 2007-QS2-A6 | | | 6.25% | | | | 01/25/2037 | | | | 1,574,685 | |

| | 4,392,656 | | | Series 2007-QS5-A5 | | | 0.55% | # | | | 03/25/2037 | | | | 2,212,783 | |

| | 14,589,015 | | | Series 2007-QS5-A8 | | | 6.45% | # I/F I/O | | | 03/25/2037 | | | | 2,253,642 | |

| | 3,910,146 | | | Series 2007-QS6-A13 | | | 52.90% | # I/F | | | 04/25/2037 | | | | 6,655,775 | |

| | 27,752,113 | | | Series 2007-QS6-A6 | | | 6.25% | | | | 04/25/2037 | | | | 18,841,562 | |

| |

| | | | Residential Asset Securities Corporation, | |

| | 3,688,414 | | | Series 06-KS4-A3 | | | 0.40% | # | | | 6/25/2036 | | | | 3,374,978 | |

| | 1,194,955 | | | Series 2002-KS1-AI6 | | | 6.08% | | | | 06/25/2032 | | | | 1,041,972 | |

| | 4,539,611 | | | Series 2003-KS11-MI1 | | | 5.13% | | | | 01/25/2034 | | | | 3,708,483 | |

| |

| | | | Residential Asset Securitization Trust, | |

| | 7,886,095 | | | Series 2004-RS5-AI6 | | | 5.55% | # | | | 05/25/2034 | | | | 6,497,133 | |

| | 2,790,842 | | | Series 2004-RS8-AI4 | | | 5.06% | | | | 06/25/2032 | | | | 2,752,949 | |

| | 2,490,932 | | | Series 2004-RS9-AI4 | | | 4.77% | # | | | 10/25/2032 | | | | 2,219,249 | |

| | 3,185,923 | | | Series 2004-RS9-II6 | | | 4.72% | # | | | 07/25/2034 | | | | 2,644,701 | |

| | 4,832,771 | | | Series 2004-RZ2-AI4 | | | 5.35% | # | | | 02/25/2033 | | | | 3,849,416 | |

| | 11,392,768 | | | Series 2005-A11-2A4 | | | 6.00% | | | | 10/25/2035 | | | | 6,835,661 | |

| | 11,856,050 | | | Series 2005-A12-A7 | | | 4.75% | # I/F I/O | | | 11/25/2035 | | | | 1,346,517 | |

| | 8,959,961 | | | Series 2005-A12-A8 | | | 0.80% | # | | | 11/25/2035 | | | | 6,479,768 | |

| | 8,075,768 | | | Series 2005-A7-A3 | | | 5.50% | | | | 06/25/2035 | | | | 7,368,674 | |

| | 12,760,028 | | | Series 2005-A8CB-A11 | | | 6.00% | | | | 07/25/2035 | | | | 11,490,526 | |

| | 16,793,287 | | | Series 2005-A8CB-A2 | | | 4.75% | # I/F I/O | | | 07/25/2035 | | | | 1,681,267 | |

| | 7,550,000 | | | Series 2005-RS1-AI5 | | | 5.41% | # | | | 12/25/2034 | | | | 5,887,071 | |

| | 2,241,494 | | | Series 2006-A1-1A3 | | | 6.00% | | | | 04/25/2036 | | | | 1,758,380 | |

| | 2,499,984 | | | Series 2006-A4-2A5 | | | 6.00% | | | | 05/25/2036 | | | | 1,746,030 | |

| | 4,519,596 | | | Series 2006-A8-1A1 | | | 6.00% | | | | 08/25/2036 | | | | 3,364,773 | |

| | 13,772,520 | | | Series 2006-R1-A1 | | | 27.40% | # I/F | | | 01/25/2046 | | | | 15,346,498 | |

| | 2,261,802 | | | Series 2007-A3-1A2 | | | 44.50% | # I/F | | | 04/25/2037 | | | | 3,540,667 | |

| | 40,430,875 | | | Series 2007-A5-1A4 | | | 5.85% | # I/F I/O | | | 05/25/2037 | | | | 6,118,704 | |

| | 10,390,237 | | | Series 2007-A5-1A6 | | | 0.65% | # | | | 05/25/2037 | | | | 4,566,467 | |

| |

| | | | Residential Funding Mortgage Securities Trust, | |

| | 2,647,663 | | | Series 2005-S9-A8 | | | 5.50% | | | | 12/25/2035 | | | | 2,528,846 | |

| | 1,039,025 | | | Series 2006-S5-A15 | | | 6.00% | | | | 06/25/2036 | | | | 890,737 | |

| | 18,000,000 | | | Series 2007-S1-A7 | | | 6.00% | | | | 01/25/2037 | | | | 15,763,563 | |

| | 4,500,000 | | | Series 2007-S4-A1 | | | 6.00% | | | | 04/25/2037 | | | | 3,901,322 | |

| | 19,760,548 | | | Series 2007-SA1-4A | | | 5.89% | | | | 02/25/2037 | | | | 15,833,139 | |

| |

| | | | Salomon Brothers Mortgage Securities, | |

| | 3,000,000 | | | Series 2000-C3-F | | | 7.60% | # | | | 12/18/2033 | | | | 2,970,601 | |

| | 4,860,000 | | | Series 2001-C1-C | | | 6.73% | # | | | 12/18/2035 | | | | 4,852,786 | |

| | 3,000,000 | | | Series 2001-C1-E | | | 6.31% | # | | | 12/18/2035 | | | | 2,991,676 | |

| |

| | | | Sequoia Mortgage Trust, | |

| | 685,952 | | | Series 2003-4-2A1 | | | 0.60% | # | | | 07/20/2033 | | | | 660,577 | |

| |

| | | | Soundview Home Loan, | |

| | 7,732,845 | | | Series 2007-1 | | | 0.34% | # | | | 03/25/2037 | | | | 7,531,199 | |

| |

| | | | Structured Asset Securities Corporation, | |

| | 21,217,196 | | | Series 2002-BC7-M1 | | | 1.05% | # | | | 10/25/2032 | | | | 15,503,829 | |

| | 1,382,376 | | | Series 2003-18XS-A6 | | | 4.04% | | | | 06/25/2033 | | | | 1,392,911 | |

| | 10,035,860 | | | Series 2005-14-1A1 | | | 0.55% | # | | | 07/25/2035 | | | | 9,181,487 | |

| | 3,608,083 | | | Series 2005-14-1A4 | | | 23.40% | # I/F | | | 07/25/2035 | | | | 4,313,126 | |

| |

| | | | Suntrust Alternative Loan Trust, | |

| | 2,428,372 | | | Series 2005-1F-2A3 | | | 5.75% | | | | 12/25/2035 | | | | 2,040,071 | |

| | 5,187,847 | | | Series 2006-1F-1A3 | | | 6.00% | | | | 04/25/2036 | | | | 3,319,592 | |

| |

| | | | Thornburg Mortgage Securities Trust, | |

| | 3,128,766 | | | Series 2003-6-A2 | | | 1.25% | # | | | 12/25/2033 | | | | 2,506,348 | |

| |

| | | | TIAA Real Estate CDO, | |

| | 10,000,000 | | | Series 2002-1 | | | 1.56% | #^ | | | 05/22/2037 | | | | 9,500,000 | |

| |

| | | | Wachovia Bank Commercial Mortgage Trust, | |

| | 6,425,084 | | | Series 2006-C23-APB | | | 5.45% | | | | 01/15/2045 | | | | 6,511,382 | |

| | | | | | |

| The accompanying notes are an integral part of these financial statements | | Annual Report | | March 31, 2011 | | 13 |

| | |

| |

| Schedule of Investments DoubleLine Total Return Bond Fund (Cont.) | | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Washington Mutual Mortgage Pass Through Certificates, | |

| $ | 3,837,331 | | | Series 2002-MS9-CB1 | | | 5.79% | # | | | 12/25/2032 | | | | 3,677,253 | |

| | 14,281,856 | | | Series 2005-1-2A | | | 6.00% | | | | 03/25/2035 | | | | 12,017,103 | |

| | 2,518,702 | | | Series 2005-5-CB12 | | | 47.90% | # I/F | | | 07/25/2035 | | | | 4,122,709 | |

| | 8,156,175 | | | Series 2005-5-CB6 | | | 0.85% | # | | | 07/25/2035 | | | | 5,508,081 | |

| | 9,351,556 | | | Series 2005-9-CX | | | 5.50% | I/O | | | 11/25/2035 | | | | 1,319,095 | |

| | 7,826,246 | | | Series 2006-1-3A2 | | | 5.75% | | | | 02/25/2036 | | | | 6,720,558 | |