As filed with the Securities and Exchange Commission on June 7, 2012

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22378

DoubleLine Funds Trust

(Exact name of registrant as specified in charter)

333 South Grand Avenue, Suite 1800

Los Angeles, CA 90071

(Address of principal executive offices) (Zip code)

Ronald R. Redell

President

DoubleLine Funds Trust

333 South Grand Avenue, Suite 1800

Los Angeles, CA 90071

(Name and address of agent for service)

(213) 633-8200

Registrant’s telephone number, including area code

Date of fiscal year end: March 31

Date of reporting period: March 31, 2012

Item 1. Reports to Stockholders.

Annual Report

March 31, 2012

DoubleLine Total Return Bond Fund

DBLTX (I-share)

DLTNX (N-share)

DoubleLine Core Fixed Income Fund

DBLFX (I-share)

DLFNX (N-share)

DoubleLine Emerging Markets Fixed Income Fund

DBLEX (I-share)

DLENX (N-share)

DoubleLine Multi-Asset Growth Fund

DMLIX (I-share)

DMLAX (A-share)

DoubleLine Low Duration Bond Fund

DBLSX (I-share)

DLSNX (N-share)

| | |

| DoubleLine Capital LP | | 333 S. Grand Avenue 18th Floor Los Angeles, California 90071 doubleline.com |

Table of Contents

| | | | | | |

| | Annual Report | | March 31, 2012 | | 3 |

President’s Letter

Dear DoubleLine Funds Shareholder:

On behalf of the team at DoubleLine, I am pleased to deliver this Annual Report. On the following pages, you will find specific information regarding each Fund’s operations and holdings. Investor assets in the DoubleLine Funds grew to $25 billion as of March 31, 2012. In this challenging economic and market environment, DoubleLine continues to strive to deliver superior risk-adjusted returns while working to avoid crossing the double line of risk on the road to successful investing.

Highlights of Financial Markets through our Annual reporting period

| | · | | Agency Mortgage-Backed Securities (Agency MBS): Lower-coupon pass-throughs were the best-performing portion of the MBS Index for the one year period ending March 31, 2012, with higher coupons underperforming. Longer-duration Agency Collateralized Mortgage Obligations (Agency CMOs) outperformed over shorter-duration CMOs as Government interest rates fell across the curve. These securities also benefitted from high income streams over the period. |

| | · | | Non-Agency MBS: Overall non-Agency MBS prices were slightly down over the period with prime-backed securities being the best performing collateral. All fixed-rate non-Agency mortgage-backed securities continued to benefit from high income cash flows due to their discounted dollar prices. |

| | · | | Treasuries: Government yields declined sharply over the period. A steady but gradual rally early in the period turned explosive in August and September on a combination of weaker-than-expected economic data, aggressive monetary accommodation by the Federal Reserve and intensified European sovereign debt concerns. The 10-year Treasury note moved from a yield above 3.50% at the start of the period to 3.00% in late July and then fell in dramatic fashion to an all-time low closing yield of 1.71% in late September. Treasury yields found a new equilibrium around 2.00% and traded in a narrow range through the remainder of the period. The 10-year yield moved as high as 2.40% in March as investors expressed their disappointment over a perceived Fed retreat from further monetary stimulus. The period ended with additional Fed action still a possibility and renewed anxiety over eurozone sovereign debt with Spain now the focus. |

| | · | | Corporates: Both investment grade and high yield corporate bond markets experienced tremendous volatility during the second and third quarters of 2011, driven primarily by concerns regarding the European debt crisis, the U.S. debt ceiling debate and the subsequent loss of the vaunted AAA rating of US sovereign debt. The tone of the corporate market changed considerably, however, in the first quarter of 2012 as investors adopted a “yield grab” mentality with higher beta (lower-rated) sectors of each market generally outperforming. Investors became more cautious toward the end of the quarter, perhaps remembering that 2011 started out in much the same way and mindful of the fact that Europe’s issues embed ample potential for further dislocating shocks. |

| | · | | Emerging Markets Debt: Government sovereign bonds outperformed among the EM subsectors. External sovereign bonds (sovereign bonds denominated in US Dollars), represented by the JP Morgan Emerging Markets Bond Index – Global Diversified (EMBI GD), returned 10.94% over the one year period, with comparable returns in the investment grade subindex of 11.15% and in the non-investment grade subindex of 10.60%. Positive returns were broad-based, with the best- and worst-performing regions within the index being Latin |

| | America 15.50% and Europe 5.41%, respectively. Both external sovereign and corporate EM debt benefitted from a decline in the 10-year U.S. Treasury yield of 126 bps. EM corporates underperformed EM sovereign debt as the JP Morgan Corporate Emerging Markets Bond Index-Broad Diversified (CEMBI BD) spread widened by 81 bps over the period versus the EMBI GD, which saw its spread widen by 53 bps. Within the corporate EM space, the high grade credits within the CEMBI BD outperformed their high yield counterparts over the period by 6.78%. Government local currency bonds were the weakest performer: the JP Morgan Global Bond Index Emerging Markets Broad Diversified returned 3.34% over the period, with the bulk of the return coming from carry, offsetting currency depreciation across the index. The weakest-performing regions within the index were Europe and the Middle East with returns of -3.28% and -0.46% respectively. |

| | · | | Commodities: As measured by the Standard & Poor’s Goldman Sachs Commodity Index Excess Return, the broad-based commodities market posted a 6.2% decline for the one year period. Positive returns in 14 of the 24 commodities in the index during the first quarter of 2012 helped reduce the trailing twelve-month loss. By far the worst performing commodity was natural gas as it continued to struggle with a material supply and demand imbalance brought on by an unseasonably warm winter. |

Performance:

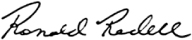

DoubleLine Total Return Bond Fund

For the year ended March 31, 2012, the DoubleLine Total Return Bond Fund “I” share has outperformed the Barclays’ Capital U.S. Aggregate Bond Index (“Barclays US Aggregate Index”) by 2.47% (10.18% versus 7.71%). This outperformance was due to both major sectors of the portfolio: the Agency MBS and the non-Agency MBS. The longer duration of the Agency MBS portion of the Fund drove the outperformance of that sector. The non-Agency MBS sector has continued to generate high income streams, which more than offset the slight price decline in that sector over the period.

| | | | | | |

| Period Ended: 3-31-2012 | | | | 1 year

(Annualized) | |

I-Share | | | | | 10.18% | |

N-Share | | | | | 9.83% | |

Barclays US Aggregate Index | | | | | 7.71% | |

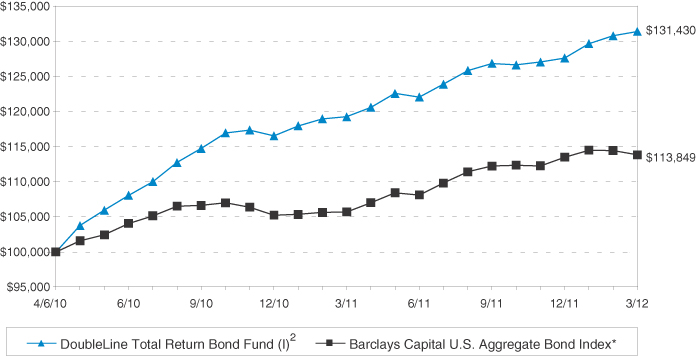

DoubleLine Core Fixed Income Fund

The DoubleLine Core Fixed Income Fund “I” share outperformed the Barclays US Aggregate Index by 3.48% (11.19% versus 7.71%) for the one year period ending March 31, 2012. The Fund’s outperformance over the period was due to both the allocation across the various sectors of the fixed income market and security selection. The allocation to Emerging Markets drove a portion of the Fund’s outperformance along with the outperformance of both the MBS and Corporate sectors of the U.S. market.

| | | | | | |

| Period Ended: 3-31-12 | | | | 1 year

(Annualized) | |

I-Share | | | | | 11.19% | |

N-Share | | | | | 10.85% | |

Barclays US Aggregate Index | | | | | 7.71% | |

| | | | | | |

| | Annual Report | | March 31, 2012 | | 5 |

President’s Letter (Cont.)

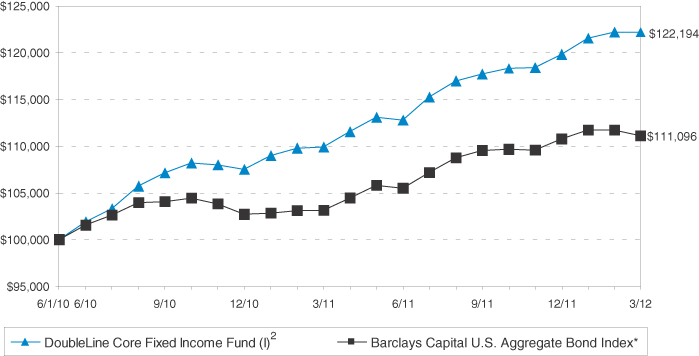

DoubleLine Emerging Markets Fixed Income Fund

The DoubleLine Emerging Markets Fixed Income Fund “I” share underperformed the JP Morgan EMBI Global Diversified Index by 2.98% (7.96% versus 10.94%) for the one year period ending March 31, 2012. Despite positive performance by both EM corporate and sovereign/quasi sovereign debt for the year, driven by a more than 100 bps decline in the 10-year U.S. Treasury yield, the Fund’s underperformance was driven predominately by corporate debt spread widening of 81 bps versus sovereign and quasi-sovereign debt spread widening of 53 bps. In addition, the Fund’s performance was affected by weaker returns from its high yield corporate positions versus the benchmark’s high yield sovereign and quasi-sovereign positions.

| | | | | | |

| Period Ended: 3-31-12 | | | | 1 year

(Annualized) | |

I-Share | | | | | 7.96% | |

N-Share | | | | | 7.71% | |

JP Morgan Emerging Markets Bond Global Diversified Index | | | | | 10.94% | |

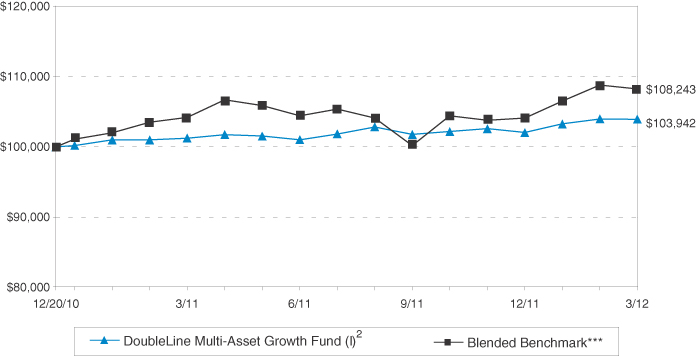

DoubleLine Multi-Asset Growth Fund

The DoubleLine Multi-Asset Growth Fund “I” share underperformed the Blended Benchmark (60% Barclays US Aggregate Index/25% Morgan Stanley Capital International All Country World Index/15% S&P Goldman Sachs Commodity Index Total Return) by 1.23% (2.67% versus 3.90%) for the one year period ending March 31, 2012. The underperformance was largely due to a large cash position held throughout the reporting period, and an underweight in global equities.

| | | | | | |

| Period Ended: 3-31-12 | | | | 1 year

(Annualized) | |

I-Share | | | | | 2.67% | |

A-Share | | | | | | |

No Load | | | | | 2.57% | |

With Load | | | | | -1.79% | |

Blended Benchmark* | | | | | 3.90% | |

| * | Blended Benchmark: 60% Barclays US Aggregate Index/25% Morgan Stanley Capital International All Country World Index/15% S&P Goldman Sachs Commodity Index Total Return. |

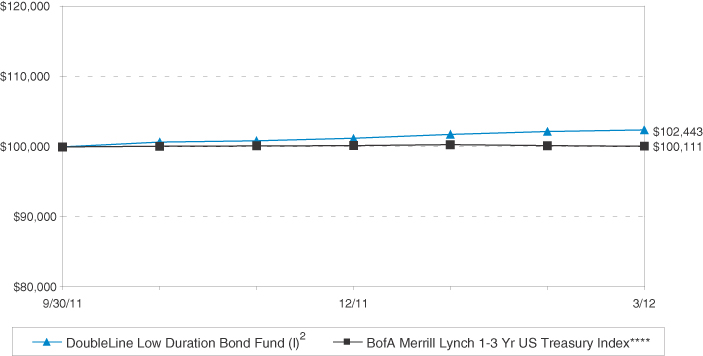

DoubleLine Low Duration Bond Fund

The DoubleLine Low Duration Bond Fund “I” share outperformed the BofA Merrill Lynch 1-3 Year US Treasury Index by 2.33% (2.44% versus 0.11%) for the six-month period ending March 31, 2012. The outperformance of the Fund was due to allocations across various fixed income sectors. Specifically, allocations to MBS, Commercial MBS, as well as Emerging Markets, none of which are represented in the BofA Merrill Lynch 1-3 Year US Treasury Index, drove the outperformance of the Fund.

| | | | | | |

| Period Ended: 3-31-12 | | | | From

9-30-2011

(inception)

to 3-31-12

(Annualized) | |

I-Share | | | | | 2.44% | |

N-Share | | | | | 2.25% | |

BofA ML 1-3 Year US Treasury Index | | | | | 0.11% | |

On behalf of the team at DoubleLine, we thank you for your support of the Funds and the trust you have placed in us. If you have any questions please do not hesitate to call 877-DLINE11 (354-6311) or visit our website at www.doublelinefunds.com.

Sincerely,

Ronald R. Redell

President

May 1, 2012

Past Performance is not a guarantee of future results.

Opinions expressed herein are as of March 31, 2012 and are subject to change at any time, are not guaranteed and should not be considered investment advice.

The performance shown assumes the reinvestment of all dividends and distributions and does not reflect any reductions for taxes. Investment performance reflects fee waivers in effect. In the absence of such waivers, total return would be reduced.

Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Please refer to the Schedule of Investments for a complete list of fund holdings.

This report is for the information of shareholders of the Funds. It may also be used as sales literature when preceded or accompanied by the current prospectus.

Investments in debt securities typically decrease when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset-Backed and Mortgage-Backed securities include additional risks that investors should note, including credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Investments in lower rated and certain non-rated securities present a greater risk of loss to principal and interest than higher rated securities. The Emerging Markets Fixed Income Fund and the Multi-Asset Growth Fund are non-diversified meaning each may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, these Funds may be more susceptible to any single economic, political or regulatory event than a more diversified fund, and a decline in the market value of one of the Fund’s investments may affect that Fund’s value more than if the Fund were a diversified fund. The Core Fixed Income Fund, Emerging Markets Fixed Income Fund and Multi-Asset Growth Fund may invest in foreign securities, which involve political, economic, and currency risks, greater volatility, and differences in accounting methods. These risks are greater for investments in emerging markets. The Funds may invest in securities related to real estate, which may decline in value as a result of factors affecting the real estate industry. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. The Funds’ investments in derivatives potentially could lose more than the amount invested. Commodity-linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. For more details regarding the risks of the Funds, please consult the current prospectus.

| | | | | | |

| | Annual Report | | March 31, 2012 | | 7 |

President’s Letter (Cont.)

JP Morgan Emerging Markets Bond (EMBI) Global Diversified Index—This index is an uniquely-weighted version of the EMBI Global. It limits the weights of those index countries with larger debt supplies by only including specified portions of these countries’ eligible current face amounts of debt outstanding. The countries covered in the EMBI Global Diversified are identical to those covered by EMBI Global.

Morgan Stanley Capital International All Country World Index—This index is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI All Country World Index Ex-U.S. includes both developed and emerging markets.

Standard & Poor’s Goldman Sachs Commodity Index (GSCI) Excess Return—This Index measures the returns accrued from investing in uncollateralized nearby commodity futures.

JP Morgan Corporate Emerging Markets Bond Index—Broad Diversified (CEMBI GD)—This index is a market capitalization weighted index consisting of US-denominated Emerging Market corporate bonds. It is a liquid global corporate benchmark representing Asia, Latin America, Europe and the Middle East/Africa.

JP Morgan Emerging Markets Bond Index—Global Diversified (EMBI GD)—This index tracks total returns for US dollar denominated debt instruments issued by emerging market sovereign entities, including Brady bonds, loans and Eurobonds, and quasi-sovereign entities.

Barclays Capital US Aggregate Bond Index—This index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the US investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis.

Standard & Poor’s Goldman Sachs Commodity Index (GSCI) Total Return—This is a composite index of commodity sector returns which represents a broadly diversified, unleveraged, long-only position in commodity futures. This index’s components qualify for inclusion in the index based on liquidity measures and are weighted in relation to their global production levels, making the index a valuable economic indicator and commodities market benchmark.

BofA Merrill Lynch 1-3 Year US Treasury Index—This Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years.

JP Morgan Global Bond Index Emerging Markets—JP Morgan Global Bond Index Emerging Markets (GBI-EM) Broad Diversified—The GBI-EM is a benchmark that tracks local currency bonds issued by emerging markets governments. The GBI-EM Broad Diversified is the all-encompassing index containing all eligible countries with eligible instruments.

A direct investment cannot be made in an index. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses applicable to mutual fund investments.

A basis point (bps) equals 0.01%.

Duration is a commonly used measure of the potential volatility of the price of a debt security, or the aggregate market value of a portfolio of debt securities, prior to maturity. Securities with a longer duration generally have more volatile prices than securities of comparable quality with a shorter duration.

Correlation is a statistical measure of how two securities move in relation to each other.

Beta is a measure of the historical price volatility of a security, portfolio or other asset and the asset’s correlation relative to a given market or market index. A higher beta security or portfolio generally has more volatility than the market as a whole. A lower beta security or portfolio generally has less volatility than the market as a whole.

The DoubleLine Funds are distributed by Quasar Distributors, LLC.

DoubleLine® is a registered trademark of DoubleLine Capital LP.

This commentary may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to a Fund and market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein.

DoubleLine has no obligation to provide revised assessments in the event of changed circumstances. While we have gathered this information from sources believed to be reliable, DoubleLine cannot guarantee the accuracy of the information provided. Securities or sectors discussed are not recommendations and are presented as examples of issue selection or portfolio management processes. They have been picked for comparison or illustration purposes only. No security or sector mentioned within this material is either offered for sale or purchase. DoubleLine reserves the right to change its investment perspective and outlook without notice as market conditions dictate or as additional information becomes available.

Investment strategies may not achieve the desired results due to implementation lag, other timing factors, portfolio management decision making, economic or market conditions or other unanticipated factors. The views and forecasts expressed in this material are as of the date indicated, are subject to change without notice, may not come to pass and do not represent a recommendation or offer of any particular security, strategy, or investment. Past performance is no guarantee of future results.

| | |

| Schedule of Investments DoubleLine Total Return Bond Fund | | March 31, 2012 |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| | COLLATERALIZED LOAN OBLIGATIONS 0.1% | |

| |

| | | | Atrium Corporation, | |

| $ | 3,104,125 | | | Series 3A-A1 | | | 0.82% | #^ | | | 10/27/2016 | | | | 3,057,563 | |

| |

| | | | Avenue Ltd., | |

| | 9,668,357 | | | Series 2004-1A-A1L | | | 0.85% | #^ | | | 02/15/2017 | | | | 9,560,071 | |

| |

| | | | Black Diamond Ltd., | |

| | 2,008,833 | | | Series 2005-1A-A1 | | | 0.74% | #^ | | | 06/20/2017 | | | | 1,943,546 | |

| |

| | | | Galaxy Ltd., | |

| | 6,833,432 | | | Series 2005-5A-A1 | | | 0.82% | #^ | | | 10/20/2017 | | | | 6,696,763 | |

| |

| | | | Gulf Stream Compass Ltd., | |

| | 663,229 | | | Series 2002-1A-A | | | 1.05% | #^ | | | 12/19/2014 | | | | 658,255 | |

| |

| | | | Marathon Financing B.V., | |

| | 206,662 | | | Series 2006-1A-A1 | | | 0.75% | #^ | | | 10/05/2026 | | | | 200,690 | |

| |

| | | | Sargas II Ltd., | |

| | 5,999,718 | | | Series 2006-1A-D | | | 1.81% | #^ | | | 10/20/2018 | | | | 5,924,721 | |

| | 2,142,756 | | | Series 2006-1X-D | | | 1.81% | # | | | 10/20/2018 | | | | 2,115,972 | |

| | | | | | | | | | | | | | | | |

| | | | Total Collateralized Loan Obligations

(Cost $30,152,806) | | | | 30,157,581 | |

| | | | | | | | | | | | | | | | |

| | NON-AGENCY COLLATERALIZED MORTGAGE OBLIGATIONS 37.4% | |

| |

| | | | ACE Securities Corporation, | |

| | 43,345,728 | | | Series 2006-HE1-A2C | | | 0.43% | # | | | 02/25/2036 | | | | 39,899,548 | |

| |

| | | | Adjustable Rate Mortgage Trust, | |

| | 6,200,000 | | | Series 2005-2-6M2 | | | 1.22% | # | | | 06/25/2035 | | | | 2,667,420 | |

| | 9,685,729 | | | Series 2005-7-3A1 | | | 5.12% | # | | | 10/25/2035 | | | | 7,345,429 | |

| | 49,855,496 | | | Series 2006-1-2A1 | | | 3.23% | # | | | 03/25/2036 | | | | 29,343,774 | |

| | 45,037,130 | | | Series 2007-1-3A1 | | | 5.66% | # | | | 03/25/2037 | | | | 28,976,417 | |

| | 6,980,848 | | | Series 2007-3-1A1 | | | 3.56% | #^ | | | 11/25/2037 | | | | 3,549,070 | |

| |

| | | | Aegis Asset Backed Securities Trust, | |

| | 663,255 | | | Series 2003-2-M2 | | | 2.79% | # | | | 11/25/2033 | | | | 456,561 | |

| | 6,291,428 | | | Series 2004-1-M2 | | | 2.27% | # | | | 04/25/2034 | | | | 4,247,724 | |

| | 935,144 | | | Series 2004-2-M2 | | | 1.54% | # | | | 06/25/2034 | | | | 448,131 | |

| |

| | | | American General Mortgage Loan Trust, | |

| | 12,000,000 | | | Series 2010-1-A3 | | | 5.65% | #^ | | | 03/25/2058 | | | | 12,643,656 | |

| | 12,000,000 | | | Series 2010-1-A4 | | | 5.65% | #^ | | | 03/25/2058 | | | | 12,416,064 | |

| |

| | | | American Home Mortgage Investment Trust, | |

| | 7,875,251 | | | Series 2005-1-7A2 | | | 2.74% | # | | | 06/25/2045 | | | | 5,482,065 | |

| | 15,164,258 | | | Series 2005-4-3A1 | | | 0.54% | # | | | 11/25/2045 | | | | 9,344,686 | |

| | 3,073,793 | | | Series 2006-2-3A4 | | | 6.60% | # | | | 06/25/2036 | | | | 1,625,203 | |

| | 14,306,054 | | | Series 2007-A-13A1 | | | 6.10% | #^ | | | 01/25/2037 | | | | 8,338,591 | |

| |

| | | | Amortizing Residential Collateral Trust, | |

| | 20,063,163 | | | Series 2002-BC7-M1 | | | 1.44% | # | | | 10/25/2032 | | | | 12,420,462 | |

| |

| | | | Argent Securities, Inc., | |

| | 707,783 | | | Series 2004-W6-M1 | | | 0.79% | # | | | 05/25/2034 | | | | 531,128 | |

| |

| | | | Asset Backed Securities Corporation Home Equity Loan Trust, | |

| | 8,249,312 | | | Series 2003-HE6-M1 | | | 1.22% | # | | | 11/25/2033 | | | | 6,293,643 | |

| | 1,795,165 | | | Series 2004-HE3-M2 | | | 1.92% | # | | | 06/25/2034 | | | | 1,231,973 | |

| |

| | | | Asset Securitization Corporation, | |

| | 1,941,045 | | | Series 1997-D5-A2 | | | 7.15% | # | | | 02/14/2043 | | | | 1,959,157 | |

| |

| | | | Banc of America Alternative Loan Trust, | |

| | 10,088,435 | | | Series 2005-10-4A1 | | | 5.75% | | | | 11/25/2035 | | | | 8,773,554 | |

| | 8,177,100 | | | Series 2005-5-2CB1 | | | 6.00% | | | | 06/25/2035 | | | | 6,548,381 | |

| | 14,450,914 | | | Series 2005-6-2CB2 | | | 6.00% | | | | 07/25/2035 | | | | 13,043,540 | |

| | 5,757,026 | | | Series 2005-6-4CB1 | | | 6.50% | | | | 07/25/2035 | | | | 4,770,747 | |

| | 5,551,791 | | | Series 2005-8-2CB1 | | | 6.00% | | | | 09/25/2035 | | | | 4,538,875 | |

| | 4,526,961 | | | Series 2006-5-CB14 | | | 6.00% | # | | | 06/25/2046 | | | | 3,172,977 | |

| | 8,019,598 | | | Series 2006-6-CB3 | | | 6.00% | | | | 06/25/2046 | | | | 6,226,572 | |

| | 24,250,000 | | | Series 2006-7-A4 | | | 6.00% | # | | | 10/25/2036 | | | | 16,139,139 | |

| | 13,232,498 | | | Series 2006-8-1A1 | | | 6.26% | #I/F I/O | | | 11/25/2036 | | | | 2,332,548 | |

| | 4,570,516 | | | Series 2006-8-1A2 | | | 0.69% | # | | | 11/25/2036 | | | | 2,542,322 | |

| | 20,595,119 | | | Series 2006-9-1CB1 | | | 6.00% | | | | 01/25/2037 | | | | 13,762,122 | |

| | 3,445,984 | | | Series 2007-2-2A1 | | | 6.00% | | | | 06/25/2037 | | | | 1,950,906 | |

| |

| | | | Banc of America Commercial Mortgage, Inc., | |

| | 5,303,000 | | | Series 2002-2-G | | | 5.85% | ^ | | | 07/11/2043 | | | | 5,370,974 | |

| | 236,917,192 | | | Series 2005-4-XP | | | 0.35% | # I/O | | | 07/10/2045 | | | | 306,097 | |

| | 255,498,198 | | | Series 2006-1-XP | | | 0.35% | # I/O | | | 09/10/2045 | | | | 493,623 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Banc of America Commercial Mortgage, Inc., (Cont.) | |

| $ | 108,440,121 | | | Series 2006-4-XP | | | 0.61% | # I/O | | | 07/10/2046 | | | | 658,448 | |

| | 334,442,425 | | | Series 2007-5-XW | | | 0.58% | #^ I/O | | | 02/10/2051 | | | | 5,112,621 | |

| |

| | | | Banc of America Funding Corporation, | |

| | 367,764 | | | Series 2005-6-2A9 | | | 5.50% | | | | 10/25/2035 | | | | 370,232 | |

| | 24,918,339 | | | Series 2006-2-3A1 | | | 6.00% | | | | 03/25/2036 | | | | 23,534,736 | |

| | 925,380 | | | Series 2006-2-4A1 | | | 22.07% | #I/F | | | 03/25/2036 | | | | 1,129,655 | |

| | 4,091,469 | | | Series 2006-2-6A2 | | | 5.50% | | | | 03/25/2036 | | | | 4,056,188 | |

| | 8,053,938 | | | Series 2006-3-6A1 | | | 6.32% | # | | | 03/25/2036 | | | | 8,240,084 | |

| | 5,026,806 | | | Series 2006-7-T2A5 | | | 6.04% | # | | | 10/25/2036 | | | | 3,058,580 | |

| | 5,147,681 | | | Series 2006-7-T2A8 | | | 5.91% | # | | | 10/25/2036 | | | | 3,109,068 | |

| | 4,743,186 | | | Series 2006-8T2-A8 | | | 6.10% | # | | | 10/25/2036 | | | | 3,241,555 | |

| | 2,660,797 | | | Series 2006-B-7A1 | | | 5.59% | # | | | 03/20/2036 | | | | 2,128,841 | |

| | 25,119,237 | | | Series 2006-D-6A1 | | | 5.27% | # | | | 05/20/2036 | | | | 16,087,779 | |

| | 2,684,166 | | | Series 2006-G-2A1 | | | 0.46% | # | | | 07/20/2036 | | | | 2,149,154 | |

| | 1,404,948 | | | Series 2006-H-3A1 | | | 5.98% | # | | | 09/20/2046 | | | | 1,010,384 | |

| | 3,180,485 | | | Series 2007-1-TA10 | | | 5.84% | # | | | 01/25/2037 | | | | 1,983,877 | |

| | 4,436,723 | | | Series 2007-3-TA1B | | | 5.83% | # | | | 04/25/2037 | | | | 3,161,700 | |

| | 6,017,729 | | | Series 2007-5-1A1 | | | 5.50% | | | | 07/25/2037 | | | | 4,280,675 | |

| | 6,657,890 | | | Series 2009-R14-3A | | | 16.00% | #^ I/F | | | 06/26/2035 | | | | 7,426,541 | |

| | 6,107,936 | | | Series 2009-R15A-4A2 | | | 5.75% | ^ | | | 12/26/2036 | | | | 3,703,901 | |

| | 4,849,231 | | | Series 2010-R1-3A | | | 13.91% | #^ I/F | | | 07/26/2036 | | | | 4,201,859 | |

| |

| | | | Banc of America Mortgage Securities, Inc., | |

| | 5,182,677 | | | Series 2004-K-4A1 | | | 5.25% | # | | | 12/25/2034 | | | | 4,825,894 | |

| | 18,693,438 | | | Series 2006-1-A9 | | | 6.00% | | | | 05/25/2036 | | | | 15,491,402 | |

| | 6,458,077 | | | Series 2007-1-2A5 | | | 5.75% | | | | 01/25/2037 | | | | 6,321,847 | |

| |

| | | | BCAP LLC Trust, | |

| | 8,539,798 | | | Series 2007-AA2-2A7 | | | 6.00% | | | | 04/25/2037 | | | | 6,003,162 | |

| | 9,245,501 | | | Series 2007-AA2-2A8 | | | 5.75% | | | | 04/25/2037 | | | | 6,381,503 | |

| | 18,000,000 | | | Series 2008-RR3-A1B | | | 6.62% | # | | | 10/25/2036 | | | | 13,700,817 | |

| | 7,486,436 | | | Series 2010-RR10-5A1 | | | 7.78% | #^ | | | 04/27/2037 | | | | 6,101,445 | |

| | 13,735,685 | | | Series 2010-RR12-3A15 | | | 7.39% | #^ | | | 08/26/2037 | | | | 12,876,813 | |

| | 3,350,000 | | | Series 2010-RR5-2A3 | | | 6.10% | #^ | | | 04/26/2037 | | | | 3,063,240 | |

| |

| | | | BCRR Trust, | |

| | 10,500,000 | | | Series 2010-LEAF-32A | | | 4.23% | ^ | | | 12/22/2032 | | | | 10,458,903 | |

| |

| | | | Bear Stearns Adjustable Rate Mortgage Trust, | |

| | 23,586,515 | | | Series 2006-4-4A1 | | | 5.65% | # | | | 10/25/2046 | | | | 18,416,268 | |

| |

| | | | Bear Stearns Alt-A Trust, | |

| | 7,055,875 | | | Series 2004-11-2A3 | | | 2.74% | # | | | 11/25/2034 | | | | 5,788,615 | |

| | 31,024,482 | | | Series 2006-6-2A1 | | | 4.99% | # | | | 11/25/2036 | | | | 18,791,917 | |

| |

| | | | Bear Stearns Asset Backed Securities Trust, | |

| | 19,075,927 | | | Series 2004-AC4-A2 | | | 5.50% | # | | | 08/25/2034 | | | | 19,535,562 | |

| | 48,179,469 | | | Series 2005-AC2-1A | | | 5.25% | # | | | 04/25/2035 | | | | 44,894,641 | |

| | 15,508,228 | | | Series 2005-AC2-2A1 | | | 5.25% | # | | | 04/25/2035 | | | | 14,400,219 | |

| | 24,363,485 | | | Series 2006-AC1-1A1 | | | 5.75% | # | | | 02/25/2036 | | | | 16,320,611 | |

| | 3,435,926 | | | Series 2007-SD1-1A2A | | | 6.00% | | | | 10/25/2036 | | | | 2,465,258 | |

| | 1,866,649 | | | Series 2007-SD1-1A3A | | | 6.50% | | | | 10/25/2036 | | | | 1,239,133 | |

| | 10,649,887 | | | Series 2007-SD1-23A1 | | | 5.53% | # | | | 10/25/2036 | | | | 7,528,847 | |

| |

| | | | Bear Stearns Commercial Mortgage Securities, Inc., | |

| | 2,041,141 | | | Series 2001-TOP2-C | | | 6.83% | # | | | 02/15/2035 | | | | 2,049,344 | |

| | 4,047,311 | | | Series 2002-TOP8-A2 | | | 4.83% | | | | 08/15/2038 | | | | 4,086,325 | |

| | 10,000,000 | | | Series 2004-BA5A-G | | | 0.94% | #^ | | | 09/15/2019 | | | | 9,982,580 | |

| | 11,000,000 | | | Series 2004-BA5A-H | | | 1.19% | #^ | | | 09/15/2019 | | | | 10,973,545 | |

| | 19,175,000 | | | Series 2004-PWR3-A4 | | | 4.72% | | | | 02/11/2041 | | | | 20,160,461 | |

| | 10,370,000 | | | Series 2004-PWR4-A3 | | | 5.47% | # | | | 06/11/2041 | | | | 11,143,898 | |

| | 38,525,969 | | | Series 2004-PWR5-X2 | | | 1.05% | # I/O | | | 07/11/2042 | | | | 181,727 | |

| | 101,324,329 | | | Series 2004-PWR6-X2 | | | 0.85% | # I/O | | | 11/11/2041 | | | | 507,128 | |

| | 16,500,000 | | | Series 2004-T14-A4 | | | 5.20% | # | | | 01/12/2041 | | | | 17,551,710 | |

| | 92,744,349 | | | Series 2004-T16-X2 | | | 0.95% | # I/O | | | 02/13/2046 | | | | 452,129 | |

| | 19,890,951 | | | Series 2005-PWR7-X2 | | | 0.39% | # I/O | | | 02/11/2041 | | | | 50,304 | |

| | 10,000,000 | | | Series 2007-PW17-AM | | | 5.92% | # | | | 06/11/2050 | | | | 10,511,125 | |

| | 12,815,000 | | | Series 2007-PW17-AMFL | | | 0.93% | #^ | | | 06/11/2050 | | | | 10,832,026 | |

| | 14,958,018 | | | Series 2007-T28-A2 | | | 5.59% | | | | 09/11/2042 | | | | 15,121,464 | |

| |

| | | | Capital Trust, | |

| | 20,553,184 | | | Series 2005-3A-A2 | | | 5.16% | ^ | | | 06/25/2035 | | | | 20,681,641 | |

| |

| | | | CD Commercial Mortgage Trust, | |

| | 4,258,175 | | | Series 2005-CD1-A2FL | | | 0.36% | # | | | 07/15/2044 | | | | 4,246,680 | |

| | 6,931,054 | | | Series 2006-CD2-AAB | | | 5.54% | # | | | 01/15/2046 | | | | 7,134,349 | |

| | 5,149,993 | | | Series 2007-CD4-ASB | | | 5.28% | | | | 12/11/2049 | | | | 5,367,266 | |

| | 560,758,638 | | | Series 2007-CD5-XP | | | 0.32% | #^ I/O | | | 11/15/2044 | | | | 2,830,710 | |

| | | | | | |

| The accompanying notes are an integral part of these financial statements | | Annual Report | | March 31, 2012 | | 9 |

Schedule of Investments DoubleLine Total Return Bond Fund (Cont.)

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Centex Home Equity, | |

| $ | 2,750,000 | | | Series 2004-A-AF5 | | | 5.43% | # | | | 01/25/2034 | | | | 2,717,363 | |

| |

| | | | Chase Funding Mortgage Loan Asset-Backed Certificates, | |

| | 4,088,871 | | | Series 2003-4-2M1 | | | 1.14% | # | | | 03/25/2033 | | | | 2,378,093 | |

| |

| | | | Chase Mortgage Finance Corporation, | |

| | 22,000,000 | | | Series 2005-A1-2A4 | | | 2.80% | # | | | 12/25/2035 | | | | 17,875,330 | |

| | 27,787,960 | | | Series 2007-A2-6A4 | | | 4.02% | # | | | 07/25/2037 | | | | 24,310,519 | |

| | 10,000,000 | | | Series 2007-S3-1A5 | | | 6.00% | | | | 05/25/2037 | | | | 8,279,445 | |

| | 4,971,177 | | | Series 2007-S3-2A1 | | | 5.50% | | | | 05/25/2037 | | | | 4,893,379 | |

| | 12,316,072 | | | Series 2007-S5-1A18 | | | 6.00% | | | | 07/25/2037 | | | | 10,315,277 | |

| |

| | | | Chaseflex Trust, | |

| | 1,928,562 | | | Series 2006-1-A2A | | | 5.94% | # | | | 06/25/2036 | | | | 1,885,716 | |

| | 8,378,327 | | | Series 2006-1-A5 | | | 6.16% | # | | | 06/25/2036 | | | | 7,844,820 | |

| | 13,331,898 | | | Series 2006-2-A2B | | | 0.44% | # | | | 09/25/2036 | | | | 8,641,790 | |

| | 10,682,448 | | | Series 2007-1-1A1 | | | 6.50% | | | | 02/25/2037 | | | | 6,541,071 | |

| | 22,354,549 | | | Series 2007-M1-2F4 | | | 6.35% | # | | | 08/25/2037 | | | | 15,408,756 | |

| |

| | | | Citi Mortgage Alternative Loan Trust, | |

| | 13,140,552 | | | Series 2006-A2-A2 | | | 6.00% | | | | 05/25/2036 | | | | 8,324,671 | |

| | 8,968,323 | | | Series 2006-A5-3A3 | | | 6.00% | | | | 10/25/2036 | | | | 6,678,652 | |

| | 13,710,486 | | | Series 2007-A1-1A5 | | | 6.00% | | | | 01/25/2037 | | | | 8,888,940 | |

| | 6,684,769 | | | Series 2007-A1-1A7 | | | 6.00% | | | | 01/25/2037 | | | | 4,333,947 | |

| | 17,103,840 | | | Series 2007-A1-1A9 | | | 5.16% | #I/F I/O | | | 01/25/2037 | | | | 2,933,290 | |

| | 15,375,039 | | | Series 2007-A3-1A1 | | | 6.00% | # | | | 03/25/2037 | | | | 10,865,271 | |

| | 35,382,889 | | | Series 2007-A3-1A3 | | | 5.16% | #I/F I/O | | | 03/25/2037 | | | | 5,996,324 | |

| | 13,865,796 | | | Series 2007-A3-1A4 | | | 5.75% | | | | 03/25/2037 | | | | 9,630,814 | |

| | 3,623,904 | | | Series 2007-A5-1A11 | | | 6.00% | | | | 05/25/2037 | | | | 2,550,690 | |

| | 1,909,884 | | | Series 2007-A8-A1 | | | 6.00% | | | | 10/25/2037 | | | | 1,401,683 | |

| |

| | | | Citicorp Mortgage Securities, Inc., | |

| | 31,719,661 | | | Series 2005-1-1A4 | | | 5.50% | | | | 02/25/2035 | | | | 32,226,780 | |

| | 6,903,552 | | | Series 2006-7-1A1 | | | 6.00% | | | | 12/25/2036 | | | | 6,129,516 | |

| |

| | | | Citicorp Residential Mortgage Securities, Inc., | |

| | 6,594,000 | | | Series 2006-2-A5 | | | 6.04% | # | | | 09/25/2036 | | | | 5,550,829 | |

| |

| | | | Citigroup Commercial Mortgage Trust, | |

| | 8,409,649 | | | Series 2006-C4-ASB | | | 5.92% | # | | | 03/15/2049 | | | | 8,949,409 | |

| | 5,220,575 | | | Series 2006-C5-AMP3 | | | 5.68% | #^ | | | 10/15/2049 | | | | 4,903,898 | |

| | 7,000,000 | | | Series 2009-RR1-CA4B | | | 5.32% | # ^ | | | 12/17/2049 | | | | 7,004,407 | |

| |

| | | | Citigroup Mortgage Loan Trust, Inc., | |

| | 6,263,092 | | | Series 2005-5-2A2 | | | 5.75% | | | | 08/25/2035 | | | | 4,471,732 | |

| | 2,876,026 | | | Series 2005-9-21A1 | | | 5.50% | | | | 11/25/2035 | | | | 2,294,614 | |

| | 7,506,436 | | | Series 2006-FX1-A6 | | | 5.85% | # | | | 10/25/2036 | | | | 4,987,231 | |

| | 3,825,000 | | | Series 2006-WF1-A2D | | | 5.92% | # | | | 03/25/2036 | | | | 2,202,850 | |

| | 21,282,978 | | | Series 2006-WF2-A2D | | | 6.16% | # | | | 05/25/2036 | | | | 12,092,616 | |

| | 2,132,869 | | | Series 2007-12-2A1 | | | 6.50% | ^ | | | 10/25/2036 | | | | 1,434,489 | |

| | 2,222,541 | | | Series 2007-2-2A | | | 6.00% | | | | 11/25/2036 | | | | 2,138,424 | |

| | 2,747,739 | | | Series 2007-9-2A2 | | | 6.50% | ^ | | | 05/25/2037 | | | | 1,417,833 | |

| | 9,179,907 | | | Series 2007-OPX1-A3A | | | 5.97% | # | | | 01/25/2037 | | | | 4,750,409 | |

| | 103,383,695 | | | Series 2007-WFH3-A2 | | | 0.40% | # | | | 06/25/2037 | | | | 76,236,739 | |

| | 20,000,000 | | | Series 2008-AR4-1A1B | | | 3.04% | # ^ | | | 11/25/2038 | | | | 11,188,950 | |

| | 4,562,003 | | | Series 2010-12-3A1 | | | 4.00% | ^ | | | 04/25/2037 | | | | 4,662,824 | |

| | 4,152,827 | | | Series 2010-2-5A1 | | | 5.50% | # ^ | | | 12/25/2035 | | | | 4,287,409 | |

| | 205,000,000 | | | Series 2010-8-5A4 | | | 11.27% | # ^ | | | 11/25/2036 | | | | 146,574,999 | |

| | 35,636,905 | | | Series 2010-8-5A6 | | | 4.00% | ^ | | | 11/25/2036 | | | | 36,671,783 | |

| | 171,000,000 | | | Series 2010-8-6A4 | | | 9.57% | # ^ | | | 12/25/2036 | | | | 113,928,749 | |

| | 161,494,456 | | | Series 2010-8-76I2 | | | 1.00% | ^ I/O | | | 06/25/2037 | | | | 3,718,426 | |

| | 151,506,267 | | | Series 2010-8-7A4 | | | 9.26% | # ^ | | | 06/25/2037 | | | | 107,281,587 | |

| | 10,058,213 | | | Series 2011-12-1A1 | | | 3.50% | # ^ | | | 04/25/2036 | | | | 10,132,710 | |

| | 13,654,060 | | | Series 2011-12-3A1 | | | 5.59% | ^ | | | 09/25/2047 | | | | 13,791,304 | |

| |

| | | | Commercial Mortgage Acceptance Corporation, | |

| | 20,183,738 | | | Series 1998-C2-F | | | 5.44% | # ^ | | | 09/15/2030 | | | | 20,971,045 | |

| |

| | | | Commercial Mortgage Pass-Through Certificates, | |

| | 97,520,000 | | | Series 2002-LC4-XA | | | 2.72% | # ^ I/O | | | 12/10/2044 | | | | 15,512,506 | |

| | 308,623,006 | | | Series 2005-LP5-XC | | | 0.23 | # ^ I/O | | | 05/10/2043 | | | | 2,979,755 | |

| | 2,500,000 | | | Series 2006-CN2A-A2FX | | | 5.45% | ^ | | | 02/05/2019 | | | | 2,432,413 | |

| | 1,346,220 | | | Series 2007-C9-A2 | | | 5.81% | # | | | 12/10/2049 | | | | 1,353,231 | |

| |

| | | | Countrywide Alternative Loan Trust, | |

| | 58,680,472 | | | Series 2004-36CB-1A1 | | | 6.00% | | | | 02/25/2035 | | | | 49,495,599 | |

| | 14,513,108 | | | Series 2005-20CB-2A1 | | | 0.74% | # | | | 07/25/2035 | | | | 10,052,766 | |

| | 29,630,929 | | | Series 2005-20CB-2A2 | | | 4.76% | # I/F I/O | | | 07/25/2035 | | | | 3,753,699 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Countrywide Alternative Loan Trust, (Cont.) | |

| $ | 4,730,907 | | | Series 2005-20CB-4A1 | | | 5.25% | | | | 07/25/2020 | | | | 4,575,270 | |

| | 10,687,216 | | | Series 2005-26CB-A11 | | | 12.61% | # I/F | | | 07/25/2035 | | | | 10,837,614 | |

| | 15,131,043 | | | Series 2005-28CB-1A2 | | | 0.99% | # | | | 08/25/2035 | | | | 10,411,875 | |

| | 3,670,488 | | | Series 2005-28CB-3A6 | | | 6.00% | | | | 08/25/2035 | | | | 2,570,791 | |

| | 1,935,854 | | | Series 2005-60T1-A7 | | | 34.16% | # I/F | | | 12/25/2035 | | | | 3,073,819 | |

| | 2,789,314 | | | Series 2005-64CB-1A14 | | | 5.50% | | | | 12/25/2035 | | | | 1,976,236 | |

| | 40,483,404 | | | Series 2005-64CB-1A4 | | | 5.50% | | | | 12/25/2035 | | | | 28,682,593 | |

| | 7,154,321 | | | Series 2005-73CB-1A5 | | | 1.04% | # | | | 01/25/2036 | | | | 4,626,016 | |

| | 17,998,791 | | | Series 2005-73CB-1A6 | | | 4.46% | # I/F I/O | | | 01/25/2036 | | | | 2,305,998 | |

| | 3,895,399 | | | Series 2005-79CB-A5 | | | 5.50% | | | | 01/25/2036 | | | | 2,426,637 | |

| | 8,323,262 | | | Series 2005-85CB-2A6 | | | 20.75% | # I/F | | | 02/25/2036 | | | | 10,519,595 | |

| | 5,188,809 | | | Series 2005-86CB-A5 | | | 5.50% | | | | 02/25/2036 | | | | 3,610,137 | |

| | 11,113,981 | | | Series 2005-J10-1A11 | | | 5.50% | | | | 10/25/2035 | | | | 8,975,006 | |

| | 2,739,158 | | | Series 2005-J10-1A13 | | | 0.94% | # | | | 10/25/2035 | | | | 1,752,909 | |

| | 1,582,908 | | | Series 2005-J10-1A15 | | | 5.50% | | | | 10/25/2035 | | | | 1,452,876 | |

| | 4,128,144 | | | Series 2005-J11-1A3 | | | 5.50% | | | | 11/25/2035 | | | | 3,885,087 | |

| | 3,356,243 | | | Series 2005-J11-6A1 | | | 6.50% | | | | 09/25/2032 | | | | 2,931,126 | |

| | 4,874,521 | | | Series 2005-J13-2A5 | | | 0.72% | # | | | 11/25/2035 | | | | 3,542,648 | |

| | 9,749,041 | | | Series 2005-J13-2A6 | | | 4.78% | # I/F I/O | | | 11/25/2035 | | | | 1,306,048 | |

| | 7,479,655 | | | Series 2005-J1-7A1 | | | 5.50% | | | | 01/25/2020 | | | | 6,876,013 | |

| | 4,241,440 | | | Series 2005-J2-1A5 | | | 0.74% | # | | | 04/25/2035 | | | | 3,093,687 | |

| | 13,050,584 | | | Series 2005-J2-1A6 | | | 4.76% | # I/F I/O | | | 04/25/2035 | | | | 1,955,663 | |

| | 10,583,420 | | | Series 2006-12CB-A3 | | | 5.75% | # | | | 05/25/2036 | | | | 6,226,707 | |

| | 4,962,102 | | | Series 2006-15CB-A1 | | | 6.50% | | | | 06/25/2036 | | | | 3,000,266 | |

| | 3,991,963 | | | Series 2006-18CB-A12 | | | 0.84% | # | | | 07/25/2036 | | | | 1,928,078 | |

| | 3,991,963 | | | Series 2006-18CB-A13 | | | 5.26% | # I/F I/O | | | 07/25/2036 | | | | 688,874 | |

| | 3,882,154 | | | Series 2006-19CB-A15 | | | 6.00% | | | | 08/25/2036 | | | | 2,931,368 | |

| | 6,261,151 | | | Series 2006-24CB-A11 | | | 5.75% | | | | 06/25/2036 | | | | 4,061,399 | |

| | 17,485,393 | | | Series 2006-24CB-A14 | | | 6.91% | # I/F I/O | | | 06/25/2036 | | | | 4,164,064 | |

| | 14,694,760 | | | Series 2006-24CB-A22 | | | 6.00% | | | | 06/25/2036 | | | | 9,695,860 | |

| | 15,771,892 | | | Series 2006-24CB-A5 | | | 0.84% | # | | | 06/25/2036 | | | | 7,917,238 | |

| | 5,940,989 | | | Series 2006-26CB-A17 | | | 6.25% | | | | 09/25/2036 | | | | 3,473,741 | |

| | 7,568,927 | | | Series 2006-26CB-A9 | | | 6.50% | | | | 09/25/2036 | | | | 4,728,089 | |

| | 16,032,052 | | | Series 2006-29T1-1A2 | | | 6.25% | | | | 10/25/2036 | | | | 10,417,699 | |

| | 2,037,886 | | | Series 2006-29T1-2A12 | | | 44.58% | # I/F | | | 10/25/2036 | | | | 3,447,840 | |

| | 1,248,248 | | | Series 2006-29T1-2A23 | | | 32.32% | # I/F | | | 10/25/2036 | | | | 1,823,076 | |

| | 14,448,718 | | | Series 2006-30T1-1A2 | | | 6.25% | | | | 11/25/2036 | | | | 11,377,015 | |

| | 9,173,134 | | | Series 2006-32CB-A1 | | | 0.91% | # | | | 11/25/2036 | | | | 4,485,667 | |

| | 15,300,788 | | | Series 2006-32CB-A2 | | | 5.09% | # I/F I/O | | | 11/25/2036 | | | | 2,487,983 | |

| | 5,965,532 | | | Series 2006-36T2-2A1 | | | 6.25% | | | | 12/25/2036 | | | | 3,960,347 | |

| | 5,369,999 | | | Series 2006-39CB-1A10 | | | 6.00% | | | | 01/25/2037 | | | | 3,614,799 | |

| | 26,634,649 | | | Series 2006-39CB-2A2 | | | 6.31% | # I/F I/O | | | 01/25/2037 | | | | 5,672,664 | |

| | 9,070,355 | | | Series 2006-39CB-2A4 | | | 0.69% | # | | | 01/25/2037 | | | | 1,635,598 | |

| | 9,298,768 | | | Series 2006-40T1-1A11 | | | 6.00% | | | | 01/25/2037 | | | | 6,702,733 | |

| | 14,313,600 | | | Series 2006-40T1-1A4 | | | 5.21% | # I/F I/O | | | 01/25/2037 | | | | 2,254,943 | |

| | 10,387,906 | | | Series 2006-45T1-1A4 | | | 0.84% | # | | | 02/25/2037 | | | | 5,233,126 | |

| | 10,387,906 | | | Series 2006-45T1-1A5 | | | 5.16% | # I/F I/O | | | 02/25/2037 | | | | 1,742,817 | |

| | 4,584,948 | | | Series 2006-6CB-1A4 | | | 5.50% | | | | 05/25/2036 | | | | 3,338,548 | |

| | 28,569,319 | | | Series 2006-J1-1A3 | | | 5.50% | | | | 02/25/2036 | | | | 20,165,768 | |

| | 4,360,828 | | | Series 2006-J4-2A2 | | | 6.00% | | | | 07/25/2036 | | | | 2,836,516 | |

| | 2,721,498 | | | Series 2007-11T1-A24 | | | 38.45% | # I/F | | | 05/25/2037 | | | | 4,550,762 | |

| | 28,645,213 | | | Series 2007-16CB-2A1 | | | 0.69% | # | | | 08/25/2037 | | | | 12,487,365 | |

| | 8,294,938 | | | Series 2007-16CB-2A2 | | | 52.57% | # I/F | | | 08/25/2037 | | | | 18,254,477 | |

| | 27,398,250 | | | Series 2007-17CB-1A10 | | | 28.79% | # I/F | | | 08/25/2037 | | | | 43,722,382 | |

| | 4,518,742 | | | Series 2007-18CB-2A25 | | | 6.00% | | | | 08/25/2037 | | | | 3,263,243 | |

| | 2,506,543 | | | Series 2007-19-1A10 | | | 37.55% | # I/F | | | 08/25/2037 | | | | 3,740,853 | |

| | 61,595,163 | | | Series 2007-19-2A1 | | | 6.50% | | | | 08/25/2037 | | | | 34,250,021 | |

| | 13,231,634 | | | Series 2007-21CB-2A2 | | | 27.43% | # I/F | | | 09/25/2037 | | | | 17,199,097 | |

| | 49,563,590 | | | Series 2007-22-2A16 | | | 6.50% | | | | 09/25/2037 | | | | 34,661,801 | |

| | 23,095,188 | | | Series 2007-4CB-2A1 | | | 7.00% | | | | 03/25/2037 | | | | 8,535,959 | |

| | 16,617,788 | | | Series 2007-5CB-1A18 | | | 5.41% | # I/FI/O | | | 04/25/2037 | | | | 3,040,946 | |

| | 16,617,789 | | | Series 2007-5CB-1A23 | | | 0.79% | # | | | 04/25/2037 | | | | 7,859,583 | |

| | 1,162,015 | | | Series 2007-8CB-A12 | | | 38.75% | # I/F | | | 05/25/2037 | | | | 1,876,257 | |

| | 1,240,433 | | | Series 2007-8CB-A8 | | | 38.63% | # I/F | | | 05/25/2037 | | | | 1,989,929 | |

| | 1,714,928 | | | Series 2007-9T1-1A4 | | | 0.74% | # | | | 05/25/2037 | | | | 786,336 | |

| | 1,714,928 | | | Series 2007-9T1-1A5 | | | 5.26% | # I/F I/O | | | 05/25/2037 | | | | 258,800 | |

| | 46,974,224 | | | Series 2007-9T1-1A6 | | | 6.00% | | | | 05/25/2037 | | | | 30,507,903 | |

| | 4,845,915 | | | Series 2007-9T1-2A1 | | | 6.00% | | | | 05/25/2037 | | | | 3,194,406 | |

| | 5,684,239 | | | Series 2007-9T1-3A1 | | | 5.50% | | | | 05/25/2022 | | | | 5,050,531 | |

| | 27,432,533 | | | Series 2007-HY5R-2A1A | | | 5.54% | # | | | 03/25/2047 | | | | 26,498,771 | |

| |

| | | | Countrywide Asset-Backed Certificates, | |

| | 6,970,439 | | | Series 2003-BC6-M1 | | | 1.07% | # | | | 11/25/2033 | | | | 6,135,864 | |

| | 3,673,360 | | | Series 2005-13-AF3 | | | 5.43% | # | | | 04/25/2036 | | | | 2,759,846 | |

| | 3,153,692 | | | Series 2006-2-2A2 | | | 0.43% | # | | | 06/25/2036 | | | | 2,698,864 | |

| | | | | | |

| 10 | | DoubleLine Funds | | | | The accompanying notes are an integral part of these financial statements |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Countrywide Home Loans, | |

| $ | 9,301,476 | | | Series 2002-32-2A6 | | | 5.00% | | | | 01/25/2018 | | | | 9,575,075 | |

| | 12,708,642 | | | Series 2005-20-A8 | | | 5.25% | | | | 10/25/2035 | | | | 10,858,708 | |

| | 44,812,669 | | | Series 2005-23-A1 | | | 5.50% | | | | 11/25/2035 | | | | 40,486,925 | |

| | 3,722,972 | | | Series 2005-27-2A1 | | | 5.50% | | | | 12/25/2035 | | | | 3,317,275 | |

| | 6,887,824 | | | Series 2005-28-A7 | | | 5.25% | | | | 01/25/2019 | | | | 5,999,453 | |

| | 59,587,093 | | | Series 2005-HYB1-4A1 | | | 2.84% | # | | | 03/25/2035 | | | | 43,249,325 | |

| | 5,617,646 | | | Series 2005-HYB8-1A1 | | | 2.68% | # | | | 12/20/2035 | | | | 3,950,363 | |

| | 14,070,932 | | | Series 2005-J3-2A4 | | | 4.50% | | | | 09/25/2035 | | | | 11,871,505 | |

| | 9,700,000 | | | Series 2005-J4-A5 | | | 5.50% | | | | 11/25/2035 | | | | 8,705,823 | |

| | 3,250,670 | | | Series 2005-R1-1AF1 | | | 0.60% | #^ | | | 03/25/2035 | | | | 2,558,503 | |

| | 3,291,150 | | | Series 2005-R1-1AS | | | 5.69% | #^ I/O | | | 03/25/2035 | | | | 454,804 | |

| | 6,112,333 | | | Series 2006-J3-A4 | | | 5.50% | | | | 05/25/2036 | | | | 5,779,339 | |

| | 2,960,972 | | | Series 2007-15-1A16 | | | 6.25% | | | | 09/25/2037 | | | | 2,565,818 | |

| | 12,855,439 | | | Series 2007-15-1A29 | | | 6.25% | | | | 09/25/2037 | | | | 11,101,089 | |

| | 3,437,941 | | | Series 2007-18-1A1 | | | 6.00% | | | | 11/25/2037 | | | | 3,100,171 | |

| | 41,342,306 | | | Series 2007-7-A1 | | | 6.00% | | | | 06/25/2037 | | | | 36,381,953 | |

| | 13,112,448 | | | Series 2007-7-A2 | | | 5.75% | | | | 06/25/2037 | | | | 11,547,090 | |

| | 25,529,480 | | | Series 2007-8-1A4 | | | 6.00% | | | | 01/25/2038 | | | | 20,837,328 | |

| | 7,000,000 | | | Series 2007-9-A11 | | | 5.75% | | | | 07/25/2037 | | | | 6,107,710 | |

| | 68,095,670 | | | Series 2007-J1-2A1 | | | 6.00% | | | | 02/25/2037 | | | | 47,982,013 | |

| | 3,201,367 | | | Series 2007-J3-A1 | | | 0.74% | # | | | 07/25/2037 | | | | 2,077,492 | |

| | 16,006,834 | | | Series 2007-J3-A2 | | | 5.26% | # I/F I/O | | | 07/25/2037 | | | | 2,746,121 | |

| |

| | | | Credit Suisse First Boston Mortgage Backed Trust, | |

| | 7,319,131 | | | Series 2006-3-A4B | | | 6.11% | # | | | 11/25/2036 | | | | 4,112,558 | |

| | 5,364,929 | | | Series 2006-4-A6A | | | 5.68% | # | | | 12/25/2036 | | | | 3,128,277 | |

| | 17,110,916 | | | Series 2007-1-1A1A | | | 5.90% | # | | | 05/25/2037 | | | | 9,293,691 | |

| |

| | | | Credit Suisse First Boston Mortgage Securities Corporation, | |

| | 3,050,000 | | | Series 1998-C2-F | | | 6.75% | #^ | | | 11/15/2030 | | | | 3,309,980 | |

| | 7,887,000 | | | Series 2001-CF2-F | | | 6.56% | ^ | | | 02/15/2034 | | | | 7,860,618 | |

| | 1,235,000 | | | Series 2001-CF2-G | | | 6.93% | ^ | | | 02/15/2034 | | | | 1,219,411 | |

| | 642,460 | | | Series 2002-34-CB2 | | | 5.87% | # | | | 01/25/2033 | | | | 581,695 | |

| | 209,230 | | | Series 2002-CKN2-A3 | | | 6.13% | | | | 04/15/2037 | | | | 209,060 | |

| | 14,867,607 | | | Series 2002-CKS4-A2 | | | 5.18% | | | | 11/15/2036 | | | | 14,993,737 | |

| | 4,567,977 | | | Series 2003-CPN1-A2 | | | 4.60% | | | | 03/15/2035 | | | | 4,651,865 | |

| | 532,508 | | | Series 2004-AR8-2A1 | | | 2.71% | # | | | 09/25/2034 | | | | 526,321 | |

| | 6,702,959 | | | Series 2005-10-5A4 | | | 5.50% | | | | 11/25/2035 | | | | 5,024,960 | |

| | 1,992,259 | | | Series 2005-10-5A5 | | | 5.50% | | | | 11/25/2035 | | | | 1,545,597 | |

| | 15,761,867 | | | Series 2005-12-7A1 | | | 7.00% | | | | 01/25/2036 | | | | 7,212,788 | |

| | 2,780,304 | | | Series 2005-5-2A11 | | | 5.00% | | | | 07/25/2035 | | | | 2,769,347 | |

| | 188,235,819 | | | Series 2005-C2-ASP | | | 0.74% | #^ I/O | | | 04/15/2037 | | | | 91,106 | |

| | 10,277,652 | | | Series 2005-C4-A3 | | | 5.12% | # | | | 08/15/2038 | | | | 10,304,152 | |

| | 57,164,307 | | | Series 2005-C4-ASP | | | 0.39% | #^ I/O | | | 08/15/2038 | | | | 56,993 | |

| |

| | | | Credit Suisse Mortgage Capital Certificates, | |

| | 8,697,446 | | | Series 2005-1R-2A5 | | | 5.75% | ^ | | | 12/26/2035 | | | | 6,987,380 | |

| | 37,832,328 | | | Series 2006-1-2A1 | | | 6.00% | | | | 02/25/2036 | | | | 26,675,159 | |

| | 6,216,883 | | | Series 2006-2-3A1 | | | 6.50% | | | | 03/25/2036 | | | | 3,861,309 | |

| | 7,516,789 | | | Series 2006-2-5A1 | | | 0.94% | # | | | 03/25/2036 | | | | 4,198,878 | |

| | 42,015,395 | | | Series 2006-2-5A2 | | | 5.06% | # I/F I/O | | | 03/25/2036 | | | | 7,718,568 | |

| | 23,685,731 | | | Series 2006-2-5A4 | | | 6.00% | | | | 03/25/2036 | | | | 17,095,389 | |

| | 7,209,024 | | | Series 2006-3-4A3 | | | 5.50% | | | | 04/25/2036 | | | | 6,419,848 | |

| | 9,708,213 | | | Series 2006-4-1A8 | | | 6.00% | # | | | 05/25/2036 | | | | 6,010,476 | |

| | 33,940,951 | | | Series 2006-4-4A1 | | | 7.00% | | | | 05/25/2036 | | | | 14,896,191 | |

| | 32,132,139 | | | Series 2006-4-6A1 | | | 6.00% | | | | 05/25/2036 | | | | 27,860,958 | |

| | 27,756,748 | | | Series 2006-6-1A4 | | | 6.00% | | | | 07/25/2036 | | | | 19,389,088 | |

| | 16,438,712 | | | Series 2006-6-3A1 | | | 7.00% | | | | 07/25/2036 | | | | 6,221,773 | |

| | 1,140,941 | | | Series 2006-7-3A11 | | | 6.00% | | | | 08/25/2036 | | | | 923,509 | |

| | 3,384,352 | | | Series 2006-9-2A1 | | | 5.50% | | | | 11/25/2036 | | | | 2,931,952 | |

| | 11,349,771 | | | Series 2006-9-4A1 | | | 6.00% | | | | 11/25/2036 | | | | 10,058,831 | |

| | 4,805,246 | | | Series 2006-9-6A15 | | | 38.45% | # I/F | | | 11/25/2036 | | | | 7,348,017 | |

| | 5,963,456 | | | Series 2006-TF2A-SVA1 | | | 0.47% | #^ | | | 10/15/2021 | | | | 5,618,240 | |

| | 15,535,993 | | | Series 2007-1-1A4 | | | 6.13% | # | | | 02/25/2037 | | | | 9,589,739 | |

| | 32,512,710 | | | Series 2007-1-3A1 | | | 6.00% | | | | 02/25/2022 | | | | 25,292,190 | |

| | 18,378,040 | | | Series 2007-1-5A14 | | | 6.00% | | | | 02/25/2037 | | | | 14,324,065 | |

| | 4,180,984 | | | Series 2007-2-2A1 | | | 5.00% | | | | 03/25/2037 | | | | 4,086,626 | |

| | 11,112,517 | | | Series 2007-5-2A5 | | | 5.00% | | | | 08/25/2037 | | | | 9,499,569 | |

| | 1,357,495,400 | | | Series 2007-C1-ASP | | | 0.57% | # I/O | | | 02/15/2040 | | | | 10,194,790 | |

| | 5,125,847 | | | Series 2009-1R-4A2 | | | 4.86% | #^ | | | 07/20/2035 | | | | 3,915,732 | |

| | 7,303,608 | | | Series 2010-1R-5A1 | | | 5.00% | #^ | | | 01/27/2036 | | | | 7,570,536 | |

| | 64,085,130 | | | Series 2010-2R-4A17 | | | 8.01% | #^ | | | 03/26/2037 | | | | 36,989,424 | |

| | 97,400,000 | | | Series 2010-4R-3A17 | | | 9.94% | #^ | | | 06/26/2037 | | | | 67,561,413 | |

| | 48,088,546 | | | Series 2010-4R-8A17 | | | 9.94% | #^ | | | 06/26/2037 | | | | 33,812,331 | |

| | 11,053,210 | | | Series 2010-6R-2A6A | | | 6.25% | ^ | | | 07/26/2037 | | | | 11,132,622 | |

| | 34,804,009 | | | Series 2010-7R-4A17 | | | 8.22% | #^ | | | 04/26/2037 | | | | 22,436,178 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Credit-Based Asset Servicing and Securitization LLC, | |

| $ | 1,313,745 | | | Series 2005-CB6-A4 | | | 5.16% | # | | | 07/25/2035 | | | | 1,207,782 | |

| | 9,750,000 | | | Series 2007-MX1-A3 | | | 5.83% | #^ | | | 12/25/2036 | | | | 7,537,540 | |

| |

| | | | Crest Ltd., | |

| | 2,326,995 | | | Series 2003-2A-A1 | | | 0.95% | #^ | | | 12/28/2018 | | | | 2,143,744 | |

| |

| | | | DBUBS Mortgage Trust, | |

| | 205,360,869 | | | Series 2011-LC2A-XA | | | 1.62% | #^ I/O | | | 07/10/2044 | | | | 15,443,035 | |

| |

| | | | Deutsche ALT-A Securities, Inc. Mortgage Loan Trust, | |

| | 40,759,000 | | | Series 2005-4-A5 | | | 5.50% | # | | | 09/25/2035 | | | | 29,982,443 | |

| | 3,626,687 | | | Series 2005-5-1A6 | | | 34.16% | # I/F | | | 11/25/2035 | | | | 4,809,731 | |

| | 3,375,539 | | | Series 2005-5-2A1 | | | 0.44% | # | | | 11/25/2035 | | | | 1,637,226 | |

| | 10,187,743 | | | Series 2005-5-2A2 | | | 5.06% | # I/F I/O | | | 11/25/2035 | | | | 965,725 | |

| | 2,406,393 | | | Series 2006-AB2-A2 | | | 6.16% | # | | | 06/25/2036 | | | | 1,430,669 | |

| | 4,868,230 | | | Series 2006-AB4-A1A | | | 6.01% | # | | | 10/25/2036 | | | | 2,806,634 | |

| | 4,842,813 | | | Series 2006-AB4-A3 | | | 5.90% | # | | | 10/25/2036 | | | | 2,772,832 | |

| | 7,155,086 | | | Series 2006-AB4-A3A1 | | | 5.90% | # | | | 10/25/2036 | | | | 4,096,770 | |

| | 14,290,526 | | | Series 2006-AB4-A6A1 | | | 5.87% | # | | | 10/25/2036 | | | | 8,163,549 | |

| | 26,987,425 | | | Series 2006-AF1-A3 | | | 0.42% | # | | | 04/25/2036 | | | | 23,503,497 | |

| | 5,766,438 | | | Series 2007-1-1A2 | | | 0.40% | # | | | 08/25/2037 | | | | 5,567,516 | |

| | 68,000,000 | | | Series 2007-1-1A3A | | | 0.45% | # | | | 08/25/2037 | | | | 42,981,576 | |

| |

| | | | Deutsche Mortgage Securities, Inc., | |

| | 42,947,546 | | | Series 2006-PR1-3A1 | | | 11.79% | #^ I/F | | | 04/15/2036 | | | | 45,041,702 | |

| | 12,361,153 | | | Series 2006-PR1-4AI1 | | | 11.77% | #^ I/F | | | 04/15/2036 | | | | 13,525,924 | |

| | 20,270,568 | | | Series 2006-PR1-4AI2 | | | 14.14% | #^ I/F | | | 04/15/2036 | | | | 23,009,411 | |

| | 951,114 | | | Series 2006-PR1-5AI1 | | | 18.62% | #^ I/F | | | 04/15/2036 | | | | 1,072,770 | |

| | 8,219,554 | | | Series 2006-PR1-5AI3 | | | 12.23% | #^ I/F | | | 04/15/2036 | | | | 7,934,091 | |

| | 136,058,203 | | | Series 2006-PR1-5AI4 | | | 11.79% | #^ I/F | | | 04/15/2036 | | | | 146,512,029 | |

| |

| | | | DLJ Commercial Mortgage Corporation, | |

| | 1,158,406 | | | Series 1998-CF1-B4 | | | 7.60% | #^ | | | 02/15/2031 | | | | 1,185,606 | |

| | 4,000,000 | | | Series 2000-CKP1-B1 | | | 7.95% | # | | | 11/10/2033 | | | | 4,038,162 | |

| |

| | | | Ellington Loan Acquisition Trust, | |

| | 2,747,160 | | | Series 2007-1-A2A2 | | | 1.04% | #^ | | | 05/27/2037 | | | | 2,515,501 | |

| |

| | | | Extended Stay American Trust, | |

| | 35,675,676 | | | Series 2010-ESHA-A | | | 2.95% | ^ | | | 11/05/2027 | | | | 36,121,836 | |

| | 284,734,527 | | | Series 2010-ESHA-XA1 | | | 3.33% | #^ I/O | | | 01/05/2013 | | | | 6,047,192 | |

| | 102,500,000 | | | Series 2010-ESHA-XB1 | | | 1.37% | #^ I/O | | | 01/05/2016 | | | | 854,235 | |

| |

| | | | First Horizon Alternative Mortgage Securities, | |

| | 21,544,309 | | | Series 2005-AA4-1A1 | | | 2.35% | # | | | 05/25/2035 | | | | 14,386,643 | |

| | 3,998,809 | | | Series 2005-FA8-2A1 | | | 5.00% | | | | 11/25/2020 | | | | 3,861,322 | |

| | 1,063,017 | | | Series 2006-FA1-1A6 | | | 0.99% | # | | | 04/25/2036 | | | | 1,003,944 | |

| | 6,645,469 | | | Series 2006-FA2-1A5 | | | 6.00% | | | | 05/25/2036 | | | | 4,608,433 | |

| | 1,877,033 | | | Series 2006-FA7-A8 | | | 6.25% | | | | 12/25/2036 | | | | 1,374,651 | |

| | 21,834,986 | | | Series 2006-RE1-A1 | | | 5.50% | | | | 05/25/2035 | | | | 18,696,076 | |

| | 2,651,524 | | | Series 2007-FA3-A4 | | | 6.00% | | | | 06/25/2037 | | | | 1,732,736 | |

| | 2,811,692 | | | Series 2007-FA4-1A13 | | | 6.25% | | | | 08/25/2037 | | | | 1,800,070 | |

| | 4,078,310 | | | Series 2007-FA4-1A5 | | | 6.25% | | | | 08/25/2037 | | | | 2,610,970 | |

| |

| | | | First Horizon Asset Securities, Inc., | |

| | 722,757 | | | Series 2005-6-1A1 | | | 5.50% | | | | 11/25/2035 | | | | 731,360 | |

| |

| | | | First Union Commercial Mortgage Securities, Inc., | |

| | 4,636,001 | | | Series 2000-C2-G | | | 8.70% | # | | | 10/15/2032 | | | | 4,638,011 | |

| | 1,500,000 | | | Series 2001-C1-F | | | 6.84% | | | | 03/15/2033 | | | | 1,517,663 | |

| |

| | | | GE Capital Commercial Mortgage Corporation, | |

| | 707,088 | | | Series 2002-2-A3 | | | 5.35% | | | | 08/11/2036 | | | | 711,637 | |

| | 7,000,000 | | | Series 2004-C3-B | | | 5.51% | # | | | 07/10/2039 | | | | 7,434,945 | |

| | 8,273,000 | | | Series 2007-C1-AAB | | | 5.48% | | | | 12/10/2049 | | | | 8,651,763 | |

| |

| | | | GMAC Commercial Mortgage Securities, Inc., | |

| | 4,240,180 | | | Series 2001-C1-D | | | 7.03% | # | | | 04/15/2034 | | | | 4,235,090 | |

| | 102,790 | | | Series 2003-C3-A3 | | | 4.65% | | | | 04/10/2040 | | | | 103,684 | |

| | 4,935,838 | | | Series 2004-C3-A4 | | | 4.55% | | | | 12/10/2041 | | | | 4,991,610 | |

| |

| | | | GMAC Mortgage Corporation Loan Trust, | |

| | 1,449,181 | | | Series 2004-J2-A6 | | | 16.30% | # I/F | | | 06/25/2034 | | | | 1,529,255 | |

| |

| | | | Greenwich Capital Commercial Funding Corporation, | |

| | 6,575,000 | | | Series 2003-C2-B | | | 5.03% | | | | 01/05/2036 | | | | 6,837,681 | |

| | 4,000,000 | | | Series 2003-C2-C | | | 5.07% | # | | | 01/05/2036 | | | | 4,139,286 | |

| | 7,936,000 | | | Series 2004-FL2A-D | | | 0.55% | #^ | | | 11/05/2019 | | | | 7,806,961 | |

| | 6,500,000 | | | Series 2004-FL2A-G | | | 0.72% | #^ | | | 11/05/2019 | | | | 5,874,895 | |

| |

| | | | GS Mortgage Securities Corporation, | |

| | 2,903,855 | | | Series 2008-2R-1A1 | | | 7.50% | #^ | | | 09/25/2036 | | | | 2,590,784 | |

| | | | | | |

| The accompanying notes are an integral part of these financial statements | | Annual Report | | March 31, 2012 | | 11 |

Schedule of Investments DoubleLine Total Return Bond Fund (Cont.)

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | GS Mortgage Securities Corporation II, | |

| $ | 219,029,179 | | | Series 2006-GG6-XC | | | 0.15% | #^ I/O | | | 04/10/2038 | | | | 339,714 | |

| | 36,295,184 | | | Series 2011-GC3-X | | | 1.32% | #^ I/O | | | 03/10/2044 | | | | 1,976,799 | |

| | 118,552,949 | | | Series 2012-GC6-XA | | | 2.41% | #^ I/O | | | 01/10/2045 | | | | 16,935,111 | |

| |

| | | | GSAA Home Equity Trust, | |

| | 1,746,291 | | | Series 2005-12-AF3 | | | 5.07% | # | | | 09/25/2035 | | | | 1,632,665 | |

| | 47,133,245 | | | Series 2005-7-AF2 | | | 4.48% | # | | | 05/25/2035 | | | | 45,662,711 | |

| | 45,361,000 | | | Series 2005-7-AF3 | | | 4.75% | # | | | 05/25/2035 | | | | 41,703,338 | |

| | 15,791,129 | | | Series 2006-10-AF3 | | | 5.98% | # | | | 06/25/2036 | | | | 8,950,736 | |

| | 11,301,982 | | | Series 2006-10-AF4 | | | 6.30% | # | | | 06/25/2036 | | | | 6,403,839 | |

| | 22,316,110 | | | Series 2006-15-AF4 | | | 5.96% | # | | | 09/25/2036 | | | | 12,137,163 | |

| | 3,634,366 | | | Series 2006-18-AF3A | | | 5.77% | # | | | 11/25/2036 | | | | 2,081,547 | |

| | 7,525,471 | | | Series 2006-18-AF6 | | | 5.68% | # | | | 11/25/2036 | | | | 3,993,075 | |

| | 1,747,712 | | | Series 2006-4-4A1 | | | 0.34% | # | | | 03/25/2036 | | | | 1,687,579 | |

| | 16,074,589 | | | Series 2007-10-A1A | | | 6.00% | | | | 11/25/2037 | | | | 11,727,594 | |

| | 7,171,306 | | | Series 2007-10-A2A | | | 6.50% | | | | 11/25/2037 | | | | 4,609,676 | |

| |

| | | | GSMPS Mortgage Loan Trust, | |

| | 26,805,642 | | | Series 2005-RP2-1AF | | | 0.59% | #^ | | | 03/25/2035 | | | | 22,040,430 | |

| | 26,805,642 | | | Series 2005-RP2-1AS | | | 5.26% | #^ I/O | | | 03/25/2035 | | | | 3,809,334 | |

| | 14,770,971 | | | Series 2005-RP3-1AF | | | 0.59% | #^ | | | 09/25/2035 | | | | 11,640,537 | |

| | 14,770,971 | | | Series 2005-RP3-1AS | | | 5.11% | #^ I/O | | | 09/25/2035 | | | | 2,219,532 | |

| | 56,930,173 | | | Series 2006-RP1-1AS | | | 4.98% | #^ I/O | | | 01/25/2036 | | | | 9,080,852 | |

| | 56,930,173 | | | Series 2006-RP1-AF1 | | | 0.59% | #^ | | | 01/25/2036 | | | | 45,062,424 | |

| |

| | | | GSR Mortgage Loan Trust, | |

| | 12,921,222 | | | Series 2005-1F-3A3 | | | 6.00% | | | | 01/25/2035 | | | | 12,859,161 | |

| | 2,537,711 | | | Series 2005-6F-3A5 | | | 6.00% | | | | 07/25/2035 | | | | 2,570,958 | |

| | 28,578,071 | | | Series 2005-6F-3A9 | | | 6.66% | # I/F I/O | | | 07/25/2035 | | | | 5,796,662 | |

| | 2,959,437 | | | Series 2005-6F-4A1 | | | 0.74% | # | | | 07/25/2035 | | | | 2,555,546 | |

| | 3,091,509 | | | Series 2005-7F-3A1 | | | 0.74% | # | | | 09/25/2035 | | | | 2,622,132 | |

| | 8,958,849 | | | Series 2005-8F-4A1 | | | 6.00% | | | | 11/25/2035 | | | | 7,517,836 | |

| | 13,041,887 | | | Series 2006-1F-1A2 | | | 5.50% | | | | 02/25/2036 | | | | 12,952,857 | |

| | 3,909,021 | | | Series 2006-2F-2A3 | | | 5.75% | | | | 02/25/2036 | | | | 3,584,619 | |

| | 8,459,669 | | | Series 2006-2F-3A3 | | | 6.00% | | | | 02/25/2036 | | | | 6,657,984 | |

| | 44,523,738 | | | Series 2006-6F-2A3 | | | 6.00% | | | | 07/25/2036 | | | | 36,312,648 | |

| | 45,587,171 | | | Series 2006-7F-2A1 | | | 6.00% | | | | 08/25/2036 | | | | 38,851,780 | |

| | 20,629,049 | | | Series 2006-7F-3A4 | | | 6.25% | | | | 08/25/2036 | | | | 16,735,708 | |

| | 21,824,826 | | | Series 2006-9F-2A1 | | | 6.00% | | | | 10/25/2036 | | | | 19,935,113 | |

| | 967,134 | | | Series 2006-9F-8A1 | | | 5.50% | | | | 08/25/2021 | | | | 926,835 | |

| | 20,028,270 | | | Series 2007-1F-2A2 | | | 5.50% | | | | 01/25/2037 | | | | 19,189,106 | |

| | 119,109,502 | | | Series 2007-4F-3A11 | | | 6.00% | | | | 07/25/2037 | | | | 99,351,438 | |

| |

| | | | Harborview Mortgage Loan Trust, | |

| | 6,590,982 | | | Series 2005-14-3A1A | | | 2.90% | # | | | 12/19/2035 | | | | 4,562,983 | |

| |

| | | | Home Equity Asset Trust, | |

| | 2,791,416 | | | Series 2003-3-M1 | | | 1.53% | # | | | 08/25/2033 | | | | 2,114,246 | |

| | 5,094,557 | | | Series 2004-7-M2 | | | 1.23% | # | | | 01/25/2035 | | | | 4,170,692 | |

| |

| | | | Homebanc Mortgage Trust, | |

| | 3,711,372 | | | Series 2005-1-M2 | | | 0.73% | # | | | 03/25/2035 | | | | 2,341,187 | |

| | 7,536,634 | | | Series 2006-1-3A1 | | | 5.56% | # | | | 04/25/2037 | | | | 6,145,835 | |

| |

| | | | HSBC Asset Loan Obligation, | |

| | 5,728,470 | | | Series 2006-2-2A1 | | | 5.50% | | | | 12/25/2021 | | | | 5,313,322 | |

| | 98,829,578 | | | Series 2007-2-3A6 | | | 6.00% | | | | 09/25/2037 | | | | 81,952,203 | |

| | 14,546,308 | | | Series 2007-AR1-3A1 | | | 6.12% | # | | | 01/25/2037 | | | | 10,926,830 | |

| |

| | | | IMPAC Trust, | |

| | 2,621,703 | | | Series 2002-9F-A1 | | | 5.22% | # | | | 12/25/2032 | | | | 2,667,091 | |

| |

| | | | Indymac Mortgage Loan Trust, | |

| | 53,127,504 | | | Series 2006-AR3-1A1 | | | 2.76% | # | | | 12/25/2036 | | | | 35,544,160 | |

| | 18,259,346 | | | Series 2007-A-1 | | | 6.00% | | | | 08/25/2037 | | | | 15,294,658 | |

| | 1,354,706 | | | Series 2007-F2-1A2 | | | 6.00% | | | | 07/25/2037 | | | | 1,043,560 | |

| | 40,168,352 | | | Series 2007-F2-2A1 | | | 6.50% | | | | 07/25/2037 | | | | 21,587,356 | |

| |

| | | | Jefferies & Company, Inc., | |

| | 12,088,599 | | | Series 2010-R1-1A1 | | | 6.00% | #^ | | | 03/26/2037 | | | | 12,754,233 | |

| | 2,674,086 | | | Series 2010-R6-1A2 | | | 6.00% | ^ | | | 09/26/2037 | | | | 2,669,914 | |

| |

| | | | JP Morgan Alternative Loan Trust, | |

| | 30,335,154 | | | Series 2005-S1-2A11 | | | 6.00% | | | | 12/25/2035 | | | | 23,620,983 | |

| | 9,724,803 | | | Series 2005-S1-2A9 | | | 6.00% | | | | 12/25/2035 | | | | 7,572,383 | |

| | 9,666,684 | | | Series 2006-S1-1A8 | | | 5.75% | | | | 03/25/2036 | | | | 6,562,760 | |

| | 6,500,000 | | | Series 2006-S2-A4 | | | 6.19% | # | | | 05/25/2036 | | | | 3,306,612 | |

| | 14,745,000 | | | Series 2006-S4-A3A | | | 5.78% | # | | | 12/25/2036 | | | | 12,706,526 | |

| |

| | | | JP Morgan Chase Commercial Mortgage Securities Corporation, | |

| | 6,000,000 | | | Series 2001-C1-F | | | 7.12% | #^ | | | 10/12/2035 | | | | 6,012,360 | |

| | 4,870,007 | | | Series 2001-CIB2-C | | | 6.74% | # | | | 04/15/2035 | | | | 4,879,810 | |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | JP Morgan Chase Commercial Mortgage Securities Corporation, (Cont.) | |

| $ | 683,696 | | | Series 2001-CIBC-E | | | 7.30% | # | | | 03/15/2033 | | | | 683,585 | |

| | 10,000,000 | | | Series 2001-CIBC-F | | | 7.77% | # | | | 03/15/2033 | | | | 9,978,610 | |

| | 4,711,671 | | | Series 2002-CIB5-A2 | | | 5.16% | | | | 10/12/2037 | | | | 4,774,334 | |

| | 2,000,000 | | | Series 2003-LN1-D | | | 5.20% | # | | | 10/15/2037 | | | | 2,007,400 | |

| | 1,125,000 | | | Series 2004-C3-A4 | | | 4.66% | | | | 01/15/2042 | | | | 1,124,861 | |

| | 1,300,238 | | | Series 2004-CB8-A1A | | | 4.16% | ^ | | | 01/12/2039 | | | | 1,353,701 | |

| | 29,447,000 | | | Series 2004-CBX-A5 | | | 4.65% | | | | 01/12/2037 | | | | 29,809,080 | |

| | 24,549,452 | | | Series 2004-CBX-X1 | | | 0.89% | #^ I/O | | | 01/12/2037 | | | | 384,874 | |

| | 256,052,501 | | | Series 2005-LDP3-X2 | | | 0.30% | # I/O | | | 08/15/2042 | | | | 217,901 | |

| | 115,190,026 | | | Series 2005-LDP4-X1 | | | 0.16% | #^ I/O | | | 10/15/2042 | | | | 842,845 | |

| | 306,356,627 | | | Series 2006-CB14-X2 | | | 0.16% | # I/O | | | 12/12/2044 | | | | 217,513 | |

| | 338,005,296 | | | Series 2006-CB16-X2 | | | 0.70% | # I/O | | | 05/12/2045 | | | | 2,461,355 | |

| | 2,885,662 | | | Series 2006-FL1-AG | | | 0.71% | #^ | | | 02/15/2020 | | | | 2,452,831 | |

| | 167,953,486 | | | Series 2006-LDP8-X | | | 0.74% | # I/O | | | 05/15/2045 | | | | 3,377,881 | |

| | 10,000,000 | | | Series 2007-C1-ASB | | | 5.86% | | | | 02/15/2051 | | | | 10,823,015 | |

| | 187,161,488 | | | Series 2007-CB18-X | | | 0.43% | # I/O | | | 06/12/2047 | | | | 2,333,249 | |

| | 2,965,535 | | | Series 2007-CB20-ASB | | | 5.69% | | | | 02/12/2051 | | | | 3,197,717 | |

| | 1,125,488,194 | | | Series 2007-CB20-X1 | | | 0.21% | #^ I/O | | | 02/12/2051 | | | | 11,556,513 | |

| | 15,000,000 | | | Series 2011-CCHP-A | | | 2.60% | #^ | | | 07/15/2028 | | | | 14,980,568 | |

| | 5,000,000 | | | Series 2011-CCHP-B | | | 3.50% | #^ | | | 07/15/2028 | | | | 4,964,548 | |

| | 4,774,171 | | | Series 2011-PLSD-A1 | | | 2.19% | ^ | | | 11/13/2044 | | | | 4,844,418 | |

| |

| | | | JP Morgan Commercial Mortgage Finance Corporation, | |

| | 306,670 | | | Series 1997-C5-F | | | 7.56% | | | | 09/15/2029 | | | | 310,379 | |

| |

| | | | JP Morgan Mortgage Acquisition Corporation, | |

| | 16,000,000 | | | Series 2006-CH2-AF3 | | | 5.46% | # | | | 10/25/2036 | | | | 8,841,936 | |

| | 6,332,368 | | | Series 2006-WF1-A5 | | | 6.41% | # | | | 07/25/2036 | | | | 3,329,866 | |

| | 15,000,000 | | | Series 2007-CH1-AF5 | | | 5.73% | # | | | 11/25/2036 | | | | 10,995,158 | |

| |

| | | | JP Morgan Mortgage Trust, | |

| | 214,761 | | | Series 2003-A1-4A2 | | | 4.50% | # | | | 10/25/2033 | | | | 214,320 | |

| | 6,091,659 | | | Series 2005-S2-2A13 | | | 5.50% | | | | 09/25/2035 | | | | 6,065,903 | |

| | 6,385,011 | | | Series 2006-S2-3A3 | | | 6.00% | | | | 07/25/2036 | | | | 5,115,722 | |

| | 22,126,506 | | | Series 2006-S4-A8 | | | 0.62% | # | | | 01/25/2037 | | | | 14,664,242 | |

| | 22,126,506 | | | Series 2006-S4-A9 | | | 6.38% | # I/F I/O | | | 01/25/2037 | | | | 4,565,481 | |

| | 6,094,560 | | | Series 2007-A2-2A1 | | | 2.88% | # | | | 04/25/2037 | | | | 4,559,389 | |

| | 3,829,464 | | | Series 2007-S3-1A9 | | | 6.00% | | | | 08/25/2037 | | | | 3,028,853 | |

| | 15,765,695 | | | Series 2007-S3-2A2 | | | 5.50% | | | | 08/25/2022 | | | | 15,003,393 | |

| |

| | | | JP Morgan Research Trust, | |

| | 27,546,803 | | | Series 2010-1-1A4 | | | 6.00% | ^ | | | 02/26/2037 | | | | 14,212,663 | |

| | 20,452,000 | | | Series 2010-2-3A9 | | | 6.00% | ^ | | | 07/26/2036 | | | | 9,583,255 | |

| | 9,683,162 | | | Series 2010-8-2A3 | | | 4.50% | #^ | | | 11/26/2034 | | | | 9,848,996 | |

| | 9,228,491 | | | Series 2012-2-3A3 | | | 2.59% | #^ | | | 10/26/2036 | | | | 9,179,580 | |

| |

| | | | LB-UBS Commercial Mortgage Trust, | |

| | 565,000 | | | Series 2004-C2-A4 | | | 4.37% | | | | 03/15/2036 | | | | 595,554 | |

| | 120,192,562 | | | Series 2005-C2-XCP | | | 0.47% | # I/O | | | 04/15/2040 | | | | 17,188 | |

| | 53,494,286 | | | Series 2005-C5-XCP | | | 0.61% | # I/O | | | 09/15/2040 | | | | 102,388 | |

| | 178,101,667 | | | Series 2006-C7-XCL | | | 0.34% | #^ I/O | | | 11/15/2038 | | | | 3,179,471 | |

| | 784,305,145 | | | Series 2007-C7-XCL | | | 0.12% | #^ I/O | | | 09/15/2045 | | | | 6,678,358 | |

| |

| | | | Lehman Mortgage Trust, | |

| | 9,233,471 | | | Series 2005-2-3A5 | | | 5.50% | | | | 12/25/2035 | | | | 7,009,996 | |

| | 16,571,761 | | | Series 2005-3-2A1 | | | 6.00% | | | | 01/25/2036 | | | | 15,529,911 | |

| | 2,573,034 | | | Series 2005-3-2A3 | | | 5.50% | | | | 01/25/2036 | | | | 2,515,669 | |

| | 8,391,878 | | | Series 2005-3-2A7 | | | 6.00% | | | | 01/25/2036 | | | | 7,348,839 | |

| | 4,723,113 | | | Series 2006-1-1A1 | | | 0.99% | # | | | 02/25/2036 | | | | 2,954,810 | |

| | 14,169,338 | | | Series 2006-1-1A2 | | | 4.51% | # I/F I/O | | | 02/25/2036 | | | | 2,264,491 | |

| | 7,155,121 | | | Series 2006-1-3A4 | | | 5.50% | | | | 02/25/2036 | | | | 6,355,136 | |

| | 10,314,981 | | | Series 2006-4-1A3 | | | 5.16% | # I/F I/O | | | 08/25/2036 | | | | 1,433,984 | |

| | 6,555,978 | | | Series 2006-4-1A4 | | | 6.00% | | | | 08/25/2036 | | | | 4,617,825 | |

| | 14,877,443 | | | Series 2006-5-2A1 | | | 0.59% | # | | | 09/25/2036 | | | | 5,139,457 | |

| | 30,989,551 | | | Series 2006-5-2A2 | | | 6.91% | # I/F I/O | | | 09/25/2036 | | | | 8,100,470 | |

| | 28,352,294 | | | Series 2006-6-3A9 | | | 5.50% | | | | 10/25/2036 | | | | 18,526,665 | |

| | 7,269,118 | | | Series 2006-7-2A2 | | | 0.69% | # | | | 11/25/2036 | | | | 3,012,279 | |

| | 21,606,397 | | | Series 2006-7-2A5 | | | 6.31% | # I/F I/O | | | 11/25/2036 | | | | 5,035,025 | |

| | 7,587,871 | | | Series 2006-9-1A19 | | | 29.57% | # I/F | | | 01/25/2037 | | | | 11,225,054 | |

| | 8,429,576 | | | Series 2006-9-1A5 | | | 0.84% | # | | | 01/25/2037 | | | | 4,301,958 | |

| | 25,038,680 | | | Series 2006-9-1A6 | | | 4.91% | # I/F I/O | | | 01/25/2037 | | | | 4,061,449 | |

| | 9,579,941 | | | Series 2006-9-2A1 | | | 0.62% | # | | | 01/25/2037 | | | | 3,983,100 | |

| | 21,236,270 | | | Series 2006-9-2A2 | | | 6.38% | # I/F I/O | | | 01/25/2037 | | | | 4,663,750 | |

| | 23,271,947 | | | Series 2007-10-2A1 | | | 6.50% | | | | 01/25/2038 | | | | 20,869,375 | |

| | 6,783,090 | | | Series 2007-2-1A1 | | | 5.75% | | | | 02/25/2037 | | | | 4,676,737 | |

| | 6,315,096 | | | Series 2007-4-2A11 | | | 0.57% | # | | | 05/25/2037 | | | | 2,135,292 | |

| | 21,580,803 | | | Series 2007-4-2A8 | | | 6.43% | # I/F I/O | | | 05/25/2037 | | | | 6,126,190 | |

| | | | | | |

| 12 | | DoubleLine Funds | | | | The accompanying notes are an integral part of these financial statements |

| | | | | | | | | | | | | | | | |

PRINCIPAL

AMOUNT | | | SECURITY DESCRIPTION | | RATE | | | MATURITY | | | VALUE $ | |

| |

| | | | Lehman Mortgage Trust, (Cont.) | |

| $ | 2,500,317 | | | Series 2007-4-2A9 | | | 0.57% | # | | | 05/25/2037 | | | | 1,222,249 | |

| | 33,824,146 | | | Series 2007-5-11A1 | | | 5.98% | # | | | 06/25/2037 | | | | 22,346,260 | |

| | 5,003,298 | | | Series 2007-5-4A3 | | | 38.63% | # I/F | | | 08/25/2036 | | | | 7,890,914 | |

| | 1,793,746 | | | Series 2007-5-7A3 | | | 7.50% | | | | 10/25/2036 | | | | 1,600,764 | |

| | 1,795,568 | | | Series 2007-6-1A8 | | | 6.00% | | | | 07/25/2037 | | | | 1,406,133 | |

| |

| | | | Lehman XS Trust, | |

| | 3,850,296 | | | Series 2005-10-2A3B | | | 5.55% | # | | | 01/25/2036 | | | | 2,849,592 | |

| | 16,500,000 | | | Series 2005-4-2A3A | | | 5.00% | # | | | 10/25/2035 | | | | 9,052,882 | |

| | 6,831,690 | | | Series 2006-11-2A1 | | | 0.37% | # | | | 06/25/2046 | | | | 6,206,744 | |

| | 6,660,938 | | | Series 2006-5-2A4A | | | 5.89% | # | | | 04/25/2036 | | | | 5,674,679 | |

| |

| | | | MASTR Adjustable Rate Mortgages Trust, | |

| | 8,031,513 | | | Series 2005-2-2A1 | | | 2.59% | # | | | 03/25/2035 | | | | 5,189,755 | |

| |

| | | | MASTR Alternative Loans Trust, | |

| | 3,983,617 | | | Series 2005-2-3A1 | | | 6.00% | | | | 03/25/2035 | | | | 3,775,784 | |

| | 2,758,515 | | | Series 2005-5-2A3 | | | 5.50% | | | | 07/25/2025 | | | | 2,729,820 | |

| | 11,154,327 | | | Series 2005-6-1A5 | | | 5.50% | | | | 12/25/2035 | | | | 8,963,930 | |

| | 5,784,059 | | | Series 2006-3-1A2 | | | 6.25% | | | | 07/25/2036 | | | | 4,407,381 | |

| | 14,378,709 | | | Series 2007-1-1A5 | | | 5.75% | | | | 10/25/2036 | | | | 12,274,946 | |

| | 13,107,285 | | | Series 2007-1-2A7 | | | 6.00% | | | | 10/25/2036 | | | | 10,926,502 | |

| |

| | | | MASTR Asset Backed Securities Trust, | |

| | 4,975,000 | | | Series 2003-OPT1-M3 | | | 4.37% | # | | | 12/25/2032 | | | | 3,389,552 | |

| | 10,359,579 | | | Series 2006-NC1-A3 | | | 0.43% | # | | | 01/25/2036 | | | | 8,778,433 | |

| |

| | | | MASTR Asset Securitization Trust, | |

| | 1,161,420 | | | Series 2003-1-30B2 | | | 5.75% | | | | 02/25/2033 | | | | 1,159,860 | |

| | 1,262,629 | | | Series 2007-1-1A1 | | | 5.50% | | | | 11/25/2037 | | | | 1,080,513 | |

| | 11,853,232 | | | Series 2007-1-1A3 | | | 6.25% | | | | 11/25/2037 | | | | 9,981,660 | |

| |

| | | | MASTR Seasoned Securitization Trust, | |

| | 1,467,394 | | | Series 2005-2-1A4 | | | 6.00% | | | | 10/25/2032 | | | | 1,326,725 | |

| | 4,147,709 | | | Series 2005-2-2A1 | | | 0.64% | # | | | 10/25/2032 | | | | 3,428,907 | |

| |

| | | | Merrill Lynch Mortgage Investors Trust, | |

| | 207,162,991 | | | Series 1998-C1-IO | | | 0.69% | # I/O | | | 11/15/2026 | | | | 5,490,751 | |

| | 7,293,259 | | | Series 2006-F1-1A2 | | | 6.00% | | | | 04/25/2036 | | | | 6,195,838 | |

| |

| | | | Merrill Lynch Mortgage Trust, | |

| | 19,000,000 | | | Series 2003-KEY1-A4 | | | 5.24% | # | | | 11/12/2035 | | | | 20,058,576 | |

| | 326,744,301 | | | Series 2004-BPC1-XP | | | 1.06% | #^ I/O | | | 10/12/2041 | | | | 246,365 | |

| | 10,000,000 | | | Series 2004-KEY2-A4 | | | 4.86% | # | | | 08/12/2039 | | | | 10,751,895 | |

| | 326,291,328 | | | Series 2005-MCP1-XP | | | 0.83% | # I/O | | | 06/12/2043 | | | | 2,645,244 | |

| |

| | | | Merrill Lynch/Countrywide Commercial Mortgage Trust, | |

| | 2,593,761 | | | Series 2006-4-A2FL | | | 0.36% | # | | | 12/12/2049 | | | | 2,592,988 | |

| |

| | | | Morgan Stanley Capital, Inc., | |