As filed with the Securities and Exchange Commission on May 25, 2010.

REGISTRATION No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

D. MEDICAL INDUSTRIES LTD.

(Exact name of registrant as specified in its charter)

| | | | |

| State of Israel | | 3841 | | Not Applicable |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial

Classification Code Number) | | (I.R.S. Employer

Identification No.) |

7 Zabotinsky St.

Moshe Aviv Tower

Ramat-Gan 52520

Israel

+972 (3) 611-4514

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Corporation Service Company

1180 Avenue of the Americas, Suite 210

New York, NY 10036

(800) 927-9801

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| | | | | | |

Cheryl V. Reicin, Esq.

Torys LLP

237 Park Avenue

New York, New York 10017.3142 U.S.A.

Tel: (212) 880-6000

Fax: (212) 682-0200 | | Yoram L. Cohen, Adv.

Dana Livneh-Zemer, Adv.

Yoram L. Cohen, Ashlagi, Eshel

Amot Investments Tower

17th Floor – 2 Weizman St.

Tel-Aviv 64239

Israel

Tel: +972 (3) 6931900

Fax: +972 (3) 6931919 | | C. Brophy Christensen, Jr., Esq.

O’Melveny & Myers LLP

Two Embarcadero Center 28th Floor

San Francisco 94111

California U.S.A

Tel: (415) 984-8793

Fax: (415) 984-8701 | | Benjamin M. Sandler, Adv.

Barry P. Levenfeld, Adv.

Yigal Arnon & Co.

22 Rivlin St.

PO Box 69

Jerusalem 91000

Israel

Tel: +972 (2) 6239200

Fax: +972 (2) 6239233 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ¨

CALCULATION OF REGISTRATION FEE

| | | | |

| |

Title of each class of

securities to be registered | | Proposed maximum aggregate

offering price (1)(2) | | Amount of registration fee |

Ordinary shares, par value NIS 0.32 per share (3) | | | | |

Warrants to purchase ordinary shares (4) | | | | |

Ordinary shares, par value NIS 0.32 per share (5) | | | | |

Total | | $29,600,000 | | $2,110.48 |

| |

| |

| (1) | Estimated solely for the purpose of determining the amount of registration fee. |

| (2) | In accordance with Rule 457(o) under the Securities Act, the number of ordinary shares being registered and the proposed maximum offering price per share are not included in this table. |

| (3) | Includes ordinary shares that the underwriters may purchase to cover over-allotments, if any. |

| (4) | Warrants of the registrant to be issued to the underwriters, exercisable to purchase ordinary shares equal to 5% of the ordinary shares sold in the offering, excluding ordinary shares that the underwriters may purchase to cover over-allotments, if any. |

| (5) | Ordinary shares issuable to the underwriters upon exercise of warrants of the registrant, exercisable at a price per share equal to 125% of the initial public offering price per share and expiring five years from the effective date of this registration statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares this registration statement effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION, DATED MAY 25, 2010 |

D. Medical Industries Ltd.

Ordinary Shares

We are offering ordinary shares, par value NIS 0.32 per share, or our ordinary shares.

This is the initial public offering of our ordinary shares in the United States. We currently expect the initial public offering price of our ordinary shares to be between US$ and US$ per ordinary share.

Our ordinary shares are listed in Israel on the Tel-Aviv Stock Exchange, or the TASE, under the symbol “DMDC.” On May 20, 2010, the closing price of our ordinary shares on the TASE was NIS 30.70 per ordinary share, or US$8.04 per ordinary share, based on the representative rate of exchange on May 20, 2010 as published by the Bank of Israel, being NIS 3.819 = US$1.00, and after giving effect to a 32-for-one reverse stock split of our ordinary shares that we effected on April 28, 2010.

We have applied to have our ordinary shares listed on The NASDAQ Capital Market under the symbol “DMED.”

Investing in our ordinary shares involves certain risks. See “Risk Factors” beginning on page 10 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities. Neither the Securities and Exchange Commission nor any other regulatory body, including any state securities commission, has approved or disapproved of an investment in these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| | | | |

| | | Per

Ordinary

Share | | Total |

Public offering price | | US$ | | US$ |

Underwriting discounts and commissions(1) | | US$ | | US$ |

Proceeds, before expenses, to us | | US$ | | US$ |

| (1) | See “Underwriting” for a description of compensation payable to the underwriters. |

We have granted a 45-day option to Rodman & Renshaw, LLC and ThinkEquity LLC, or the underwriters, to purchase up to an additional ordinary shares, or the over-allotment shares, from us at the initial public offering price less the underwriting discount to cover over-allotments, if any, on the same terms as set forth in this prospectus. If the underwriters exercise their right to purchase all of such additional ordinary shares, we estimate that we will receive gross proceeds of approximately US$ million from the sale of our ordinary shares being offered and net proceeds of approximately US$ million after deducting approximately US$ million for underwriting discounts and commissions, based on an assumed public offering price of US$ per ordinary share, the midpoint of the range shown above. The shares issuable upon exercise of the underwriters’ option are identical to those offered by this prospectus and have been registered under the registration statement of which this prospectus forms a part.

In connection with the offering of our ordinary shares under this prospectus, or this offering, we have also agreed to issue to the underwriters warrants to purchase a number of our ordinary shares equal to 5% of our ordinary shares sold in this offering, excluding the over-allotment shares, exercisable at a price per ordinary share equal to 125% of the initial public offering price per ordinary share and expiring five years from the effective date of the registration statement of which this prospectus forms a part.

The underwriters expect to deliver our ordinary shares to purchasers in this offering on or about , 2010.

| | |

| Rodman & Renshaw, LLC | | ThinkEquity LLC |

The date of this prospectus is , 2010

You should rely only on the information contained in this prospectus and any free writing prospectus which we file with the Securities and Exchange Commission. We have not, and the underwriters have not, authorized anyone to provide you with information different from that contained in this prospectus or any such free writing prospectus. We are offering to sell, and seeking offers to buy, our ordinary shares only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our ordinary shares.

TABLE OF CONTENTS

i

PROSPECTUS SUMMARY

You should read the following summary together with the entire prospectus. This summary may not contain all of the information that you should consider before deciding to invest in our ordinary shares. You should read this entire prospectus carefully, including the risks of investing in our ordinary shares that we discuss under “Risk Factors” and including the more detailed information in “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and our audited consolidated financial statements and related notes appearing elsewhere in this prospectus. In this prospectus, unless the context otherwise requires, the term “D. Medical” refers to D. Medical Industries Ltd., and the terms the “Company,” “we,” “us,” and “our” refer to D. Medical Industries Ltd. and its subsidiaries, Nilimedix Ltd., or Nilimedix, G-Sense Ltd., or G-Sense, and Medx-Set Ltd., or Medx-Set. The term “NIS” refers to new Israeli Shekels, and the terms “dollar,” “US$” or “$” refer to U.S. dollars. Unless otherwise indicated, U.S. dollar translations of NIS amounts presented in this prospectus are translated using the rate of NIS 3.775 to US$1.00, the representative rate of exchange as of December 31, 2009 as published by the Bank of Israel. Unless otherwise indicated, we have adjusted all of the numbers and prices relating to our ordinary shares in this prospectus to reflect a 32-for-one reverse stock split of our ordinary shares that we effected on April 28, 2010. See “Reverse Stock Split.”

D. Medical Industries Ltd.

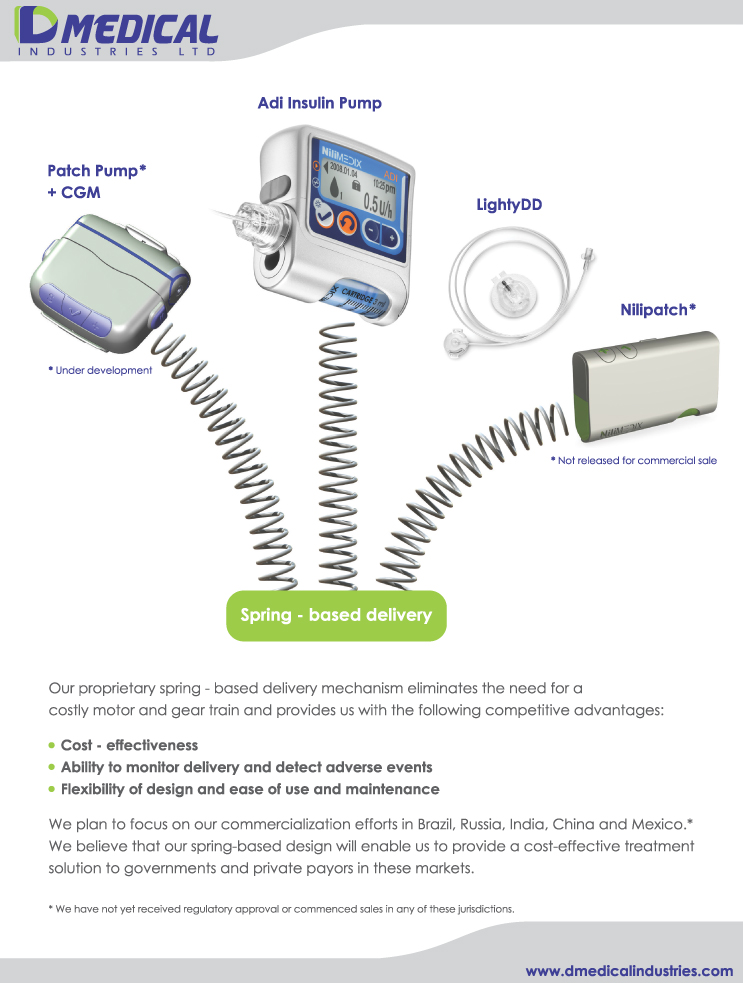

We are a medical device company engaged through our subsidiaries in the research, development, manufacture and sale of innovative products for diabetes treatment and drug delivery. We have developed durable and semi-disposable insulin pumps, which continuously infuse insulin into a patient’s body using our proprietary spring-based delivery technology. We believe that our spring-based delivery mechanism is cost-effective compared to a costly motor and gear train and allows us to incorporate certain advantageous functions and design features in our insulin pumps.

The International Diabetes Federation, or the IDF, estimates that diabetes currently affects 6.4% of people worldwide and that by 2030, this percentage will have increased to 7.7%. If not treated correctly, diabetes can cause blindness, kidney failure, nervous system damage, lower-limb amputations and even death. According to various studies, including studies published in Diabetes Care’s November 1999, November 2002, February 2008 and June 2008 issues, insulin pump therapy is the most efficacious type of therapy for patients who take insulin daily. According to The Wall Street Journal, the worldwide market for insulin delivery systems (such as insulin pumps, syringes and pens) is estimated to be US$1.6 billion, with revenues increasing year over year.

Most currently available insulin pumps are costly and have what we believe are performance and design limitations related to their motor and gear train insulin delivery system. Our proprietary spring-based design, which eliminates the need for a costly motor and gear train, has allowed us to develop products that we believe offer a cost-effective treatment solution for governments and private payors. In addition, our spring-based delivery technology monitors the actual delivery of insulin and is able to detect and alert a patient to air bubbles and other adverse occurrences, such as occlusions, which could impair the accurate delivery of insulin. Furthermore, the design of our insulin pumps has allowed us to substantially reduce their size and weight and has enabled us to include all moving parts in a disposable element, which we believe reduces concerns relating to wear and tear.

We commenced sales and marketing operations in late 2009 and are currently selling our Adi durable insulin pump, or Adi insulin pump, to our distributors in the Netherlands, Belgium and the Czech Republic. We have also engaged distributors in Sweden, Mexico and China to sell and market our products in those countries, and, subject to our receipt of the necessary regulatory approvals, we intend to begin selling our products in these markets in the near future. During the fourth quarter of 2009, we commenced sales of our LightyDD insulin

1

infusion sets, or LightyDD infusion sets, which are compatible with most other manufacturers’ durable insulin pumps, to our distributors in the Netherlands and Belgium. During the first quarter of 2010, we also commenced sales of our LightyDD infusion sets to our distributor in the Czech Republic. Our LightyDD infusion sets include unique features, such as our proprietary detach-detect mechanism, which alerts a patient when the infusion set detaches from the patient’s body. We have also developed a semi-disposable insulin patch pump, or Nilipatch insulin patch pump, and have commenced its commercialization process by transitioning it from a research and development product to a product that we can sell in large quantities. This process, which we expect to complete by the beginning of 2011, entails the finalization of our Nilipatch insulin patch pump’s commercial design and layout (which includes the incorporation of a user-friendly interface and casing into its design and the development of a manufacturing process that would allow us to manufacture it in large quantities), the launch of a marketing campaign, the engagement and training of appropriate distributors, and the submission of applications for its initial regulatory approvals. We intend to provide a four-year warranty for our Nilipatch insulin patch pump.

While we intend to roll out our products initially in Europe, we also plan to focus on our commercialization efforts in Brazil, Russia, India and China, or, collectively, the BRIC countries, and Mexico, and have already entered into distribution agreements with respect to Mexico and China. Although we have not obtained the required regulatory approvals and do not presently sell our products in the BRIC countries and Mexico, we believe that our spring-based design will enable us to provide a cost-effective treatment solution to governments and private payors in these markets.

Our research and development operations are ongoing and are focused on creating the next generation of our insulin pumps, including a simplified semi-disposable insulin pump specifically designed to treat Type 2 diabetes patients who typically do not begin using insulin until later in life and, therefore, are generally less amenable to complex insulin delivery technology. We are also focused on developing a device that will combine a continuous glucose monitoring system and an insulin pump on the same patch.

Additionally, through our subsidiary, NextGen Biomed Ltd., or NextGen, we hold an indirect controlling interest in Sindolor Medical Ltd., or Sindolor Medical, which is developing pain alleviation products. NextGen is a holding company, which is publicly traded on the TASE, and may invest in other medical device opportunities.

During 2009, we incurred net losses of NIS 19 million (US$5 million) and generated revenues of NIS 368 thousand (US$97 thousand), all of which revenues were generated during the fourth quarter of 2009.

Industry Background

Diabetes is a chronic, life-threatening disease for which there is no known cure. Diabetes is caused by the body’s inability to produce or effectively utilize the hormone insulin, which prevents the body from adequately regulating blood glucose levels. The IDF estimates that diabetes currently affects 285 million people worldwide and that by 2030, diabetes will affect 438 million people worldwide.

According to the Diabetes Atlas, Fourth Edition, 2009, as published by the IDF, or the Diabetes Atlas, estimated global healthcare expenditures associated with the treatment and prevention of diabetes and its complications are expected to total at least US$376 billion in 2010 and in excess of US$490 billion by 2030. According to the Diabetes Atlas, there is a large disparity in spending for diabetes treatment among regions and countries with more than 80% of estimated global diabetes expenditures made in higher-income countries rather than in lower- and middle-income countries where over 70% of people with diabetes live.

According to the American Diabetes Association, or the ADA, diabetes was the seventh leading cause of death listed on U.S. death certificates in 2006 and can cause many short- and long-term complications if not treated properly. Diabetes is typically classified into two major groups: Type 1 diabetes and Type 2 diabetes,

2

which account for 5 to 10% and 90 to 95%, respectively, of all diagnosed cases of diabetes in the United States. Type 1 diabetes patients must take insulin daily, while Type 2 diabetes patients may require diet and nutrition management, exercise, oral medications and/or the administration of insulin to regulate blood glucose levels. According to various studies, including studies published in Diabetes Care’s November 1999, November 2002, February 2008 and June 2008 issues, insulin pump therapy is the most efficacious type of therapy for patients who take insulin daily.

The insulin pumps currently offered by our competitors use a motor and a gear train to administer insulin. These motor and gear train insulin pumps have a long history of use and their users enjoy a familiar, well-established device. However, we believe that motor and gear train insulin pumps have certain limitations as discussed elsewhere in this prospectus. We believe that, as a result of these limitations, the utilization of insulin pump therapy still lags that of conventional insulin delivery therapies. To our knowledge, durable insulin pumps currently on the market are generally intended to be used over a period of four years, which is the standard warranty period for such devices.

Our Strengths

We are able to offer insulin pump therapy without a motor and gear train, which we believe provides us with the following competitive advantages:

Cost-Effectiveness

We believe that our spring-based design, which eliminates the need for a costly motor and gear train, results in a cost-effective treatment solution and will enable us to:

| | • | | price our products competitively and provide governments and private payors, particularly in the BRIC countries and Mexico, with cost-effective treatment solutions; and |

| | • | | potentially develop a cost-effective insulin delivery device for Type 2 diabetes patients. |

Ability to Monitor Delivery and Detect Adverse Events

Our proprietary spring-based delivery technology monitors the actual delivery of insulin and is able to detect and alert a patient to air bubbles and other adverse consequences, such as occlusions, which could impair the accurate delivery of insulin.

Flexibility of Design and Ease of Use and Maintenance

Our proprietary spring-based delivery technology provides us with flexibility in designing our products, allowing us to:

| | • | | achieve substantial weight and size reduction in our insulin pumps, resulting in a device that is less obtrusive for patients; |

| | • | | incorporate fewer movable components in our insulin pumps, resulting in greater ease of use for patients; and |

| | • | | design a disposable element incorporating all moving parts, which increases ease of maintenance and decreases the wear and tear on our durable insulin pumps. |

In addition, our LightyDD infusion sets, which are compatible with most other manufacturers’ insulin pumps currently on the market, include unique features, such as our proprietary detach-detect mechanism that alerts a patient when an infusion set detaches from their body.

3

Our Strategy

Our goal is to gain a significant share of the worldwide market for insulin pump therapy and related disposables, primarily in the BRIC countries, Mexico and Europe. To achieve our goal, we intend to employ the following strategies:

| | • | | leverage the cost-effectiveness of our spring-based design to penetrate markets in the BRIC countries and Mexico; |

| | • | | achieve higher margins by utilizing distributors and avoiding the costs associated with maintaining a direct sales force; |

| | • | | roll out our products initially in Europe; |

| | • | | continue our research and development efforts; |

| | • | | streamline our manufacturing capabilities to further minimize our material costs; |

| | • | | create a presence for our products in the United States; and |

| | • | | leverage our proprietary spring-based delivery technology for use in other drug therapies. |

Our Challenges

Since we have only recently commenced sales of our products and have a limited operating history and manufacturing capabilities, we are subject to certain potential challenges, including:

| | • | | we face intense competition in the medical devices industry; |

| | • | | our limited manufacturing capabilities may restrict or delay our ability to leverage the cost-effectiveness of our spring-based design; |

| | • | | our clinical trials have been limited; |

| | • | | our lack of regulatory approvals in the BRIC countries and Mexico where we plan to focus our commercialization efforts; and |

| | • | | our current customer base is narrow and we have a limited history of the use of our products and, consequently, we may not be aware of problems and/or inefficiencies inherent in our products. |

For further details and additional information regarding potential challenges we face, see “Risk Factors.”

Reverse Stock Split

Our shareholders approved a 32-for-one reverse stock split of our ordinary shares that we effected on April 28, 2010. No fractional ordinary shares were issued in connection with the stock split, and all such fractional interests were rounded to the nearest whole number of ordinary shares. The number of shares issuable upon the exercise of outstanding options and warrants relating to our ordinary shares has been adjusted to reflect the reverse stock split throughout this prospectus.

Corporate Information

Our registered office is located at 7 Zabotinsky St., Moshe Aviv Tower, Ramat-Gan 52520, Israel. Our telephone number is +972 (3) 611-4514. Our website address is www.dmedicalindustries.com. The information on, or accessible through, our website does not constitute part of this prospectus.

We have proprietary rights to the trademark “Nilimedix” and have applied to register the trademark “Spring” in the United States and the European Union. We reserve all rights to our trademarks, regardless of the manner in which we refer to them in this prospectus. All other trademarks, trade names and service marks appearing in this prospectus are the property of their respective owners.

4

Our agent for service of process in the United States is Corporation Service Company located at 1180 Avenue of the Americas, Suite 210, New York, NY 10036.

Industry and Market Data Information

This prospectus includes statistical data, market data and other industry data and forecasts, which we obtained from market research, publicly available information and independent industry publications and reports that we believe to be reliable sources. These industry publications generally state that they obtain their information from sources that they believe to be reliable, but they do not guarantee the accuracy and completeness of the information. Although we believe that these sources are reliable, we have not independently verified the information contained in such publications.

Our History and Corporate Structure

We were incorporated as a private company in the State of Israel in 1992 under the name Pe’er Lifts and Industries (92) Ltd. In January 1994, we changed our name to Ram Zur Industries Ltd. and in August 1994 became a public company by offering our ordinary shares to the public in Israel and listing our ordinary shares on the TASE. In January 2001, we changed our name to Arit Systems Ltd., and, in January 2005, we changed our name to our current name – D. Medical Industries Ltd.

We commenced operations as a medical device company in late 2004 through our investment in Nilimedix. We formed our subsidiaries, G-Sense and Medx-Set, in April 2005 and January 2008, respectively. Our subsidiary, NextGen, is a holding company, publicly traded on the TASE, which holds a controlling interest in Sindolor Medical through Sindolor Holdings Ltd., or Sindolor Holdings. Sindolor Medical is currently developing pain alleviation products. In May 2007, we purchased a direct interest in Sindolor Medical, which simultaneously acquired the intellectual property rights that it is currently using to develop pain alleviation products. Due to the difficulties we encountered with respect to raising capital for Sindolor Medical, we entered into agreements in August 2009 pursuant to which we obtained a controlling interest in NextGen, an Israeli publicly-traded company, in consideration for, among other things, our holdings in Sindolor Medical. As a public company, NextGen is better positioned to raise funds from the public, particularly for the activities of Sindolor Medical, and it may invest in other medical device opportunities in the future. See “Business—Sindolor Medical” for a more detailed description of Sindolor Medical. All of our subsidiaries were incorporated in the State of Israel.

We operate mainly through our subsidiary, Nilimedix, which has developed our core proprietary technology, the spring-based delivery mechanism, and is now focused on manufacturing and marketing our Adi insulin pump, as well as the final stages of development of our Nilipatch insulin patch pump. Nilimedix also operates in conjunction with MedxSet on manufacturing and marketing our LightyDD infusion sets. G-Sense focuses on researching and developing a continuous glucose monitoring system and intends to cooperate with Nilimedix to develop a combined continuous glucose monitoring and insulin pump device on one patch.

5

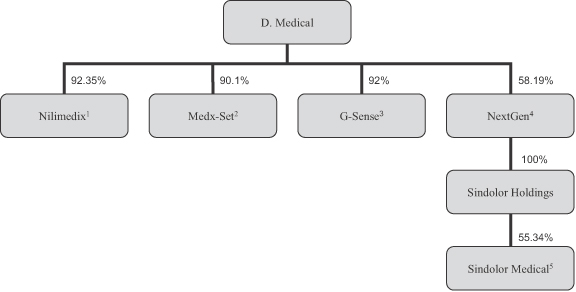

Our corporate structure is illustrated below:

| * | The percentages in the chart above reflect our ownership percentages on a fully-diluted basis. |

| 1. | The other shareholders of Nilimedix are: three former employees, including Avraham Shkalim (one of Nilimedix’ founders), David Vita and Gal Eshed; Beteiligungs GmbH, a German company that performed services for Nilimedix; Art Modern Inc., a British Virgin Island’s company; Yosef Reich; and Einat Reich. These minority shareholders of Nilimedix have the right to convert their shares in Nilimedix into our ordinary shares. See “Related Party Transactions—Transactions with Our Affiliates and Associates.” |

| 2. | The other shareholder of Medx-Set is Avraham Shkalim. |

| 3. | Mr. Avraham Shkalim has the right to receive options in G-Sense upon the occurrence of certain events, which are described in more detail under “Related Party Transactions—Transactions with Our Affiliates and Associates—Transactions with G-Sense.” |

| 4. | The remaining 41.81% interest in NextGen is publicly held. |

| 5. | Sindolor Medical’s minority shareholders consist of 18 shareholders, including the three former principal shareholders of Sindolor Medical who hold a combined 27.32% of Sindolor Medical on a fully-diluted basis. |

6

The Offering

Ordinary shares offered: | ordinary shares |

Ordinary shares to be outstanding after this offering | ordinary shares |

Over-allotment option | We have granted the underwriters a 45-day option to purchase up to an additional ordinary shares from us at the initial public offering price less the underwriting discount to cover over-allotments, if any, on the same terms as set forth in this prospectus. |

Use of proceeds | We currently intend to use the net proceeds that we will receive from this offering to expand our sales and marketing operations, expand our manufacturing capabilities, finalize the research, development and commercialization of our Nilipatch insulin pump, and for working capital and general corporate purposes. We may also use a portion of the net proceeds to fund possible investments in, or acquisitions of, complementary businesses, products or technologies. See “Use of Proceeds.” |

Risk factors | Investing in our ordinary shares involves a high degree of risk and purchasers of our ordinary shares may lose part or all of their investment. See “Risk Factors” and the other information included elsewhere in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our ordinary shares. |

Proposed NASDAQ Capital Market symbol | “DMED” |

The number of ordinary shares that will be outstanding after this offering is based on 6,071,367 ordinary shares outstanding as of March 31, 2010.

The number of ordinary shares referred to above to be outstanding after this offering and, unless otherwise indicated, the other information in this prospectus excludes:

| | • | | 211,406 ordinary shares issuable upon the exercise of 211,406 warrants outstanding as of March 31, 2010 at a weighted average exercise price of NIS 29.71 (US$7.87) per ordinary share; |

| | • | | 268,607 ordinary shares issuable upon the exercise of 268,607 options granted to employees outstanding as of March 31, 2010 at a weighted average exercise price of NIS 28.21 (US$7.47); and |

| | • | | ordinary shares issuable upon the exercise of warrants to be issued to the underwriters in connection with this offering. |

Unless otherwise indicated, the information in this prospectus:

| | • | | reflects a 32-for-one reverse stock split of our ordinary shares that we effected on April 28, 2010; and |

| | • | | assumes no exercise of the underwriters’ over-allotment option to purchase up to ordinary shares from us at the initial public offering price less the underwriting discount to cover over-allotments. |

7

Summary Consolidated Financial Data

The following tables present our summary consolidated statements of comprehensive loss for the three years ended December 31, 2009 and our summary consolidated statements of financial position as of December 31, 2009. Our summary consolidated statements of comprehensive loss for the three years ended December 31, 2009 and our summary consolidated statements of financial position as of December 31, 2009 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. We prepare our consolidated financial statements in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or the IASB. Our audited consolidated financial statements for the year ended December 31, 2008 were our first audited consolidated financial statements that were prepared in accordance with IFRS and in compliance with IFRS 1 “First Time Adoption of International Financial Reporting Standards.” Accordingly, the transition date for implementation of IFRS on our consolidated financial statements is January 1, 2007, and the comparative numbers for the year ended December 31, 2007, which are presented in our audited consolidated financial statements included elsewhere in this prospectus, were re-presented to reflect the retroactive adoption of IFRS as of the transition date. Prior to our adoption of IFRS, we prepared our consolidated financial statements in accordance with Israeli generally accepted accounting principles. Our historical results are not necessarily indicative of results to be expected in any future periods. You should read this information together with “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited consolidated financial statements and related notes included elsewhere in this prospectus.

Consolidated Statements of Comprehensive Loss Data

| | | | | | | | | | | | |

| | | Year ended December 31, | |

| | | 2009 | | | 2009 | | | 2008 | | | 2007 | |

| | | Convenience

translation into US$

(Note 1(c)) | | | NIS | |

| | | (In thousands, except per share information) | |

CONTINUING OPERATIONS: | | | | | | | | | | | | |

Sales | | 97 | | | 368 | | | — | | | — | |

Cost of sales | | 174 | | | 657 | | | — | | | — | |

| | | | | | | | | | | | |

Gross loss | | 77 | | | 289 | | | — | | | — | |

Research and development expenses, net | | 3,495 | | | 13,193 | | | *14,658 | | | *8,759 | |

Selling and marketing expenses | | 185 | | | 698 | | | — | | | — | |

General and administrative expenses | | 1,474 | | | 5,563 | | | *3,045 | | | *2,720 | |

Other (income) expenses, net | | (189 | ) | | (714 | ) | | 3,193 | | | 441 | |

| | | | | | | | | | | | |

Operating loss | | 4,965 | | | 19,029 | | | 20,896 | | | 11,920 | |

| | | | | | | | | | | | |

Finance income | | (64 | ) | | (243 | ) | | (1,035 | ) | | (571 | ) |

Fair value losses (gains) on warrants at fair value through profit or loss | | (65 | ) | | (244 | ) | | (7,950 | ) | | 10,358 | |

Finance costs | | 125 | | | 473 | | | 1,287 | | | 1,020 | |

| | | | | | | | | | | | |

Finance (income) costs, net | | (4 | ) | | (14 | ) | | (7,698 | ) | | 10,807 | |

| | | | | | | | | | | | |

LOSS AND TOTAL COMPREHENSIVE LOSS FOR THE YEAR | | 5,038 | | | 19,015 | | | 13,198 | | | 22,727 | |

| | | | | | | | | | | | |

ATTRIBUTABLE TO: | | | | | | | | | | | | |

Owners of the parent | | 4,884 | | | 18,435 | | | 10,040 | | | 20,744 | |

Minority interest | | 154 | | | 580 | | | 3,158 | | | 1,983 | |

| | | | | | | | | | | | |

| | 5,038 | | | 19,015 | | | 13,198 | | | 22,727 | |

| | | | | | | | | | | | |

LOSS PER SHARE ATTRIBUTABLE TO THE EQUITY HOLDERS OF THE COMPANY DURING THE YEAR | | | | | | | | | | | | |

Basic and Diluted | | 1.03 | | | 3.89 | | | 2.41 | | | 5.87 | |

| | | | | | | | | | | | |

| * | Reclassified (2007–75,000 NIS and 2008–147,000 NIS) in order to properly reflect the classification of shipment costs. |

8

Consolidated Statements of Financial Position Data

| | | | | | |

| | | Year ended December 31, 2009 | |

| | | Convenience translation into US$

(In thousands) (Note 1(c)) | | | NIS (In thousands) | |

| | | Actual | | | Actual | |

Cash and cash equivalents | | 6,460 | | | 24,388 | |

Working capital | | 5,942 | | | 22,435 | |

Intangible assets, net | | 3,836 | | | 14,482 | |

Total assets | | 11,433 | | | 43,165 | |

Provision for royalties to the Israeli Office of the Chief Scientist | | 1,072 | | | 4,048 | |

Total liabilities | | 3,663 | | | 13,832 | |

Accumulated losses | | (37,998 | ) | | (143,442 | ) |

Total equity | | 7,770 | | | 29,333 | |

9

RISK FACTORS

Investing in our ordinary shares involves a high degree of risk. You should carefully consider the following risk factors, as well as the financial and other information in this prospectus, before deciding to invest in our ordinary shares. If any of the following risks actually occurs, our business, financial condition and results of operations could be materially adversely affected. In such case, the trading price of our ordinary shares could decline and you may lose all or part of your investment in our ordinary shares.

Risks Related to Our Business

We have a history of losses, may incur future losses and may not achieve profitability.

We have incurred net losses in each fiscal year since we commenced operations as a medical device company in late 2004. We incurred net losses of NIS 19 million (US$5 million) in 2009, NIS 13.2 million (US$3.5 million) in 2008 and NIS 22.7 million (US$6 million) in 2007. As of December 31, 2009, our accumulated deficit was NIS 143.4 million (US$38 million). Our losses could continue for the foreseeable future as we expand our commercialization efforts for our products, increase our marketing and selling expenses, continue to invest in research and development and incur additional costs as a result of being a public company in the United States. The extent of our future operating losses and the timing of becoming profitable are highly uncertain, and we may never achieve or sustain profitability.

We have a limited operating history and we may not succeed in generating significant revenues.

Since commencing our operations as a medical device company, we have focused on the research and development of our products and have a limited operating history. We have only recently commenced sales of our Adi insulin pump and LightyDD infusion sets in several countries in Europe and our other products are in various stages of research and development. We may not succeed in generating significant revenues and the future success of our business cannot be determined at this time. In addition, we have very limited experience in commercializing our products and face a number of challenges with respect to our commercialization efforts, including, among others:

| | • | | we may not have adequate financial or other resources; |

| | • | | we may not be able to manufacture our products in commercial quantities, at an adequate quality or at an acceptable cost; |

| | • | | we may not be able to establish adequate sales, marketing and distribution channels; |

| | • | | healthcare professionals and patients may not accept our products; |

| | • | | we may not be aware of possible complications from the continued use of our products since we have limited clinical experience with respect to the actual use of our products; |

| | • | | technological breakthroughs in diabetes monitoring, treatment and prevention may reduce the demand for our products; |

| | • | | changes in the market for insulin pumps, new alliances between existing market participants and the entrance of new market participants may interfere with our market penetration efforts; |

| | • | | third-party payors may not agree to reimburse patients for any or all of the purchase price of our products, which may adversely affect patients’ willingness to purchase our products; |

| | • | | uncertainty as to market demand may result in inefficient pricing of our products; |

| | • | | we may face third party claims of intellectual property infringement; |

10

| | • | | we may fail to obtain or maintain regulatory approvals for our products in our target markets or may face adverse regulatory or legal actions relating to our products even if regulatory approval is obtained; and |

| | • | | we are dependent upon the results of ongoing clinical studies relating to our products and the products of our competitors. |

The occurrence of any one or more of these events may limit our ability to successfully commercialize our products, which in turn could have a material adverse effect on our business, financial condition and results of operations.

We expect to derive substantially all of our revenues in the near future from sales of a few products and our inability to successfully commercialize these products, or any subsequent decline in demand for these products, could severely harm our ability to generate revenues.

We currently rely solely on the successful commercialization of our Adi insulin pump and LightyDD infusion sets to generate revenues and, consequently, we are vulnerable to fluctuations in demand for these products. Fluctuations in demand may be due to many factors, including, among others:

| | • | | market acceptance of a new product, including healthcare professionals’ and patients’ preferences; |

| | • | | development of similarly cost-effective insulin pumps by our competitors; |

| | • | | development delays of our information technology platform that will allow physicians and patients to download and manage information regarding the use of our insulin pumps; |

| | • | | technological innovations in diabetes monitoring, treatment and prevention; |

| | • | | adverse medical events for patients using our products, whether actually resulting from the use of our products or not; |

| | • | | changes in regulatory policies toward insulin pumps; |

| | • | | changes in regulatory approval or clearance requirements for our products; |

| | • | | third party claims of intellectual property infringement; and |

| | • | | budget constraints of diabetes patients and the availability of reimbursement or insurance coverage from third-party payors for these products. |

In addition, the demand for our LightyDD infusion sets may also be adversely affected by the following factors:

| | • | | increases in market acceptance of insulin patch pumps, which do not require infusion sets; and |

| | • | | adverse responses from certain of our competitors to the offering of our LightyDD infusion sets as a generic device that is compatible with their pumps. |

If we are unable to successfully commercialize our Adi insulin pump and LightyDD infusion sets, or if demand for these products declines, our business and ability to generate revenues could be severely harmed.

If healthcare professionals do not recommend our products to their patients, our products may not achieve market acceptance and we may not become profitable.

Diabetes patients are generally referred by their healthcare professional to a specified device and insulin pumps are purchased by prescription. If healthcare professionals, including physicians and diabetes educators, do not recommend or prescribe our products to their patients, our products may not achieve market acceptance and

11

we may not become profitable. In addition, physicians have historically been slow to change their medical treatment practices because of perceived liability risks arising from the use of new products. Delayed adoption of our products by healthcare professionals could lead to a delayed adoption by patients and third-party payors. Healthcare professionals may not recommend or prescribe our products until, among others:

| | • | | there is sufficient long-term clinical evidence to convince them to alter their existing treatment methods and device recommendations; |

| | • | | there are recommendations from other prominent physicians, diabetes educators and/or diabetes associations that our products are safe and effective; |

| | • | | we obtain favorable data from clinical studies for our products; |

| | • | | reimbursement or insurance coverage from third party payors is available; and |

| | • | | they become familiar with the complexities of an insulin pump. |

We cannot predict when, if ever, healthcare professionals and patients may adopt the use of our products. Since we have only begun to commercialize our products, long-term clinical evidence is not yet available. Even if favorable data is obtained from clinical studies for our products, there can be no assurance that prominent physicians, diabetes educators and/or diabetes associations would endorse our products or that future clinical studies will continue to produce favorable data regarding our products. In addition, prolonged market experience may also be a pre-requisite to reimbursement or insurance coverage from third-party payors. If our products do not achieve an adequate level of acceptance by patients, healthcare professionals and third-party payors, we may not generate significant product revenues and we may not become profitable.

In the event that we are not successful in penetrating the markets of the BRIC countries and Mexico, we will not be able to implement a key component of our current growth strategy.

Our current growth strategy depends to a large extent on our ability to successfully commercialize our products in the BRIC countries and Mexico. However, we have limited experience in penetrating markets, in general, and no experience in penetrating the markets of the BRIC countries and Mexico, in particular. See “—We have a limited operating history and we may not succeed in generating significant revenues.” Our ability to penetrate these markets is subject to a number of risks and uncertainties, including, among others, difficulties predicting trends and patient preferences, the potential for political and economic instability and the still evolving nature of healthcare systems. We also believe that the overall level of awareness of the clinical advantages of insulin pump therapy in these markets is low and that, in effect, we will need to create demand for our insulin pumps in these markets. We can provide no assurance that we will be successful in increasing awareness of the clinical advantages of insulin pump therapy in these markets or creating demand for our products. Even if we succeed in increasing such awareness, diabetes patients may not be able to afford even a cost-effective product if the purchasing power in these markets does not increase as we expect. As a result, we may not be able to generate substantial sales of our products in these markets. If we are unable to maximize our opportunities in the BRIC countries and Mexico, our business, financial condition and results of operations could be materially adversely affected.

We face competition from numerous competitors, most of whom have longer operating histories and far greater resources than we have, which may make it more difficult for us to achieve significant market penetration in our target markets and, eventually, the United States, and which may allow them to introduce competing products.

The medical device industry is intensely competitive, subject to rapid change and significantly affected by new product introductions and other market activities of industry participants, particularly in the United States and Europe. Our products compete with a number of existing insulin delivery devices and other methods for the treatment of diabetes and our success depends on our ability to effectively compete in this global market. Most of our competitors are large, well-capitalized companies with significantly larger market shares and resources than

12

we have and they are able to spend more aggressively on product development, marketing, sales and other product initiatives than we can. Medtronic MiniMed, a division of Medtronic, Inc., has been the market leader in insulin pumps for many years and has the majority share of the conventional insulin pump market in the United States and Europe. Other significant suppliers in the United States are Animas Corporation, a division of Johnson & Johnson, and Roche Disetronic, a division of Roche Diagnostics, which also holds a significant market share in Europe. Although significantly smaller in size, Insulet Corporation, or Insulet, is increasingly becoming a major participant in the medical device industry.

Many of these and other competitors have, among others:

| | • | | significantly greater brand recognition; |

| | • | | established relationships with healthcare professionals, customers and third-party payors; |

| | • | | established distribution networks and channel penetration; |

| | • | | additional product lines and the ability to offer rebates or bundle products to offer higher discounts or other incentives to gain a competitive advantage; and/or |

| | • | | greater financial and human resources for product development, sales and marketing, customer support and intellectual property litigation. |

Our ability to compete effectively in our market depends upon our ability to distinguish our company and our products from our competitors and their products based on various factors, including, among others:

| | • | | brand name recognition; |

| | • | | compliance with supply obligations and customer support; |

| | • | | customer retention rates; |

| | • | | intellectual property protection; |

| | • | | the success and timing of new product development and introductions; and |

| | • | | the development of successful distribution channels. |

In addition, because most of our competitors have significantly greater product development resources than us, they or other well-capitalized companies may at any time develop additional products for the treatment of diabetes, which could render our products obsolete or substantially reduce our revenues. For example, market participants are working to develop additional cost-effective insulin delivery methods, such as an insulin spray, which Generex Biotechnology Corp. has already launched in India, and an inhaled insulin product, which MannKind Corporation has developed. Although we believe that these products are less effective in treating diabetes and do not compete directly with insulin pump therapy, their successful launch could adversely affect the demand for our products and, consequently, our business, financial condition and results of operations.

With respect to diabetes treatment options, we also compete with multiple daily injection therapy, or MDI therapy, which utilizes substantially less expensive delivery methods than insulin therapy supported by our insulin pumps, such as insulin pen injectors and insulin syringe and needle sets. More recently, MDI therapy has been made more effective by the introduction of long-acting insulin analogs by both Sanofi-Aventis and Novo Nordisk A/S, and further improvements in the effectiveness of MDI therapy may result in fewer diabetes patients converting from MDI therapy to insulin pump therapy than we expect. In that case, sales of our products may be negatively affected and we may face pricing pressure to remain competitive with MDI therapy, either of which could adversely affect our business, financial condition and results of operations.

13

If we are unable to establish adequate sales, marketing and distribution channels with third parties, our business, financial condition and results of operations could be adversely affected.

We currently do not intend to establish a direct sales force to market and sell our products. Therefore, we must enter into arrangements with third parties to conduct sales and marketing activities on our behalf. Such arrangements usually result in lower profit margins for us compared to marketing and selling our products directly. We have recently entered into several agreements with distributors in Europe, China and Mexico to distribute our products and are dependent on their efforts for the successful distribution of our Adi insulin pump and LightyDD infusion sets in their respective markets. Although most of our agreements provide for exclusivity, we cannot be certain that our future agreements will be exclusive in nature. In that case, our future distributors will be able to market and sell competing products, which may have an adverse effect on our sales and revenues. In addition, our distributor in the Netherlands and Belgium has not agreed to distribute our products on an exclusive basis in these markets and may distribute the products of our competitors. We can provide no assurance that our current or future distributors will be successful or effective in selling and marketing our products. If we fail to create effective marketing and distribution channels, our ability to generate revenue and achieve our anticipated growth could be adversely affected. Furthermore, if these distributors experience financial or other difficulties, sales of our products could be reduced, and our business, financial condition and results of operations could be materially adversely affected.

We have limited manufacturing capabilities and if we are unable to scale our manufacturing operations to meet anticipated market demand, our growth could be limited and our business, financial condition and results of operations could be materially adversely affected.

We currently have limited resources, facilities and experience in commercially manufacturing sufficient quantities of our products to meet the demand we expect from our expanded commercialization efforts. We expect to face certain technical challenges as we increase manufacturing capacity, including, among others, equipment design and automation, material procurement, lower than expected yields and increased scrap costs, as well as challenges related to maintaining quality control and assurance standards. Furthermore, we may encounter similar or unforeseen challenges initiating and later expanding production of our new products, such as our Nilipatch insulin patch pump. If we are unable to scale our manufacturing capabilities to meet market demand, our growth could be limited and our business, financial condition and results of operations could be materially adversely affected.

We are dependent upon third-party suppliers, making us vulnerable to supply problems and price fluctuations.

We rely on a number of third-party suppliers to manufacture the components of our Adi insulin pump and LightyDD infusion sets and expect to continue to rely on such suppliers to manufacture components for our Nilipatch insulin patch pump when we begin its commercialization. Although none of our third-party suppliers is a sole-source supplier, we currently do not have a second-source supplier for any of our components. We also do not have supply agreements with our third-party suppliers and we generally make our purchases on a purchase order basis. Our third-party suppliers may encounter problems during manufacturing due to a variety of reasons, including, among others, failure to follow specific protocols and procedures, failure to comply with applicable regulations, equipment malfunctions and environmental factors, any of which could delay or impede their ability to meet our demand for components. Our reliance on third-party suppliers also subjects us to additional risks that could harm our business, including, among others:

| | • | | we may not be able to obtain an adequate supply of our components in a timely manner or on commercially reasonable terms; |

| | • | | since we are not a major customer of many of our third-party suppliers, these suppliers may prioritize other customers’ needs over ours; |

| | • | | our third-party suppliers, especially new suppliers, may make manufacturing errors that may not be detected by our quality assurance testing, which could negatively affect the efficacy or safety of our products or cause shipment delays due to such errors; and |

14

| | • | | our suppliers may encounter financial or other hardships unrelated to our demand, which could inhibit their ability to fulfill our orders and meet our requirements. |

In the future, we may approach alternative third-party suppliers to manufacture our components. However, we can provide no assurance that a new third-party supplier will be able to manufacture exactly the same component to our custom specifications, which may require us to redesign a product and potentially re-submit an application for clearance to the FDA and other applicable regulatory authorities. Any interruption or delay in obtaining components from our third-party suppliers, or our inability to obtain products from alternate suppliers at acceptable prices in a timely manner, could impair our ability to meet the demand of our customers and cause them to cancel orders or switch to competing products, which, in turn, could harm our business, financial condition and results of operations.

In addition, after we establish the manufacturing procedures for each of our products, we may also enter into contract manufacturing arrangements with third parties to manufacture and assemble complete products. In that case, we will maintain only limited in-house manufacturing capabilities with respect to such products and our contract manufacturing arrangements may subject us to risks similar to those described above for our third-party suppliers.

Insulin pumps are complex medical devices that require intensive training and care; any misuse of our insulin pumps could damage our reputation, subject us to product liability claims and otherwise have a material adverse effect on our business, financial condition and results of operation.

Insulin pumps are complex medical devices that require training and care. Although our distributors are required to ensure that our products are only prescribed for diabetes patients who have been identified as capable of properly handling such devices and only after successfully completing comprehensive user training by a competent tutor, the potential for misuse of our products still exists due to their complexity. Such misuse could result in adverse medical events for patients which could damage our reputation, subject us to costly product liability litigation and otherwise have a material adverse effect on our business, financial condition and results of operations.

Insulin pumps are automated machines susceptible to malfunction which may result in severe adverse medical events. If manufacturers of insulin pumps are not able to reduce the occurrence of malfunctions, or if insulin pumps are perceived to be riskier than other insulin delivery devices, the market for insulin pumps may suffer and our business, financial condition and results of operations could be materially adversely affected.

Insulin pumps are automated machines susceptible to malfunctions. The United States Food and Drug Administration, or the FDA, has recently reported that there is an increasing trend in software and hardware malfunctions in insulin pumps from several manufacturers. Since insulin pumps are used by diabetes patients who require daily intake of insulin in order to control their blood glucose levels, malfunctions in the operation of insulin pumps could result in improper blood glucose levels and lead to severe adverse medical events and even death. The FDA has examined nearly 17,000 reports of health and other problems related to insulin pumps from 2006 through 2009. Although the reports do not prove a device caused a particular problem, such reports could result in a perception among diabetes patients that insulin pumps are riskier than other insulin delivery devices. In addition, the FDA has indicated that these reports signal a need for additional investigation and requested that insulin pump manufacturers provide additional data and information when filing adverse event reports about potential insulin pump problems. In order to obtain additional data, the FDA could impose additional requirements or require additional testing of insulin pumps prior to approving or clearing the devices for use or for ensuring their continuing commercial availability. If manufacturers of insulin pumps are not able to reduce the occurrence of malfunctions or if insulin pumps are perceived to be riskier than other insulin delivery devices, the market for insulin pumps may suffer and our business, financial condition and results of operations could be materially adversely affected.

15

Our clinical experience to date may not have revealed certain potential long-term complications from our products, which could subject us to product liability claims if our products malfunction in the future.

Our clinical trials have been limited to relatively few patients over a relatively short period of time. For example, the durability of our Adi insulin pump, which includes technology that is new and sophisticated and is expected to operate properly over a period of four years, has not been tested over an actual period of four years but rather by an accelerated lab study. In addition, we have a limited history of the use of our products and our customer base is not wide. Therefore, we have a limited ability to discover in advance problems and/or inefficiencies concerning our products and we cannot assure you that their long-term use would not result in unanticipated complications. Furthermore, the interim results from our current pre-clinical studies and clinical trials may not be indicative of the clinical results obtained when we examine the patients at later dates. If unanticipated long-term side-effects result from the use of our products, or if our products do not function as expected over time, we could be subject to liability claims and our products would not be widely adopted.

Our products under development may not achieve market acceptance, which could adversely affect our opportunities for growth.

We consider our Nilipatch insulin patch pump to be an evolution of our Adi insulin pump and currently plan to base our U.S. market penetration and our next-generation insulin pumps on this device. If our Nilipatch insulin patch pump does not achieve market acceptance in the United States and elsewhere, our growth and ability to generate significant revenues could be limited. Our Nilipatch insulin patch pump may not achieve market acceptance for a number of reasons, including, among others:

| | • | | market acceptance of a new product may be slow; |

| | • | | healthcare professionals and patients may prefer existing or other new products; |

| | • | | technological innovations in diabetes monitoring, treatment and prevention could limit the advantages presented by our Nilipatch insulin patch pump and/or could change the market for diabetes treatment such that the demand for insulin pump therapy is reduced; |

| | • | | adverse medical events for patients using our products, whether actually resulting from the use of our products or not, could limit demand for our Nilipatch insulin patch pump; |

| | • | | changes in regulatory policies toward insulin patch pumps could limit our ability to market our Nilipatch insulin patch pump in certain markets; |

| | • | | third party claims of intellectual property infringement could require us to change our products or could otherwise adversely affect our ability to successfully penetrate the market; and |

| | • | | budget constraints of diabetes patients and the availability of reimbursement or insurance coverage from third-party payors could limit demand for insulin pump therapy. |

In addition, we are continuing our research and development efforts for a continuous glucose monitoring system and a device that includes an insulin pump and continuous glucose monitoring system on one patch. If we are unable to complete the development of these devices, obtain required approvals or clearances and/or successfully commercialize them, our anticipated growth and development could be hindered. The successful development of these products subjects us to a number of challenges, including, among others:

| | • | | technological challenges related to the development of a continuous glucose monitoring system, which we may not be able to overcome; |

| | • | | receipt of FDA and other international regulatory approval, clearance or registration for a continuous glucose monitoring system as a replacement to finger stick measurement, which, to our knowledge, has not been granted in any jurisdiction to date; |

16

| | • | | patients may not recognize the benefits of continuous glucose monitoring and may be unwilling to change their current treatment regimens; |

| | • | | the invasive nature of a continuous glucose monitoring system compared to self-monitored glucose testing devices, including single-point finger stick devices; |

| | • | | costs of disposables required for continuous glucose monitoring compared to daily finger stick measurement, which could prove significant if reimbursement by third-party payors is not available; |

| | • | | technological challenges related to hosting both the insulin pump and the continuous glucose monitoring system within the same minimized device, which we may not be able to overcome; |

| | • | | receipt of FDA and other international regulatory approval, clearance or registration for our combined device or for all of our combined device’s specifications; |

| | • | | the need to continually improve and upgrade a first-generation device and our ability to compile long-term clinical data; or |

| | • | | continued development of, or our ability to gain access to, the algorithms on which the development of a continuous glucose monitoring depends. |

Substantially all of our operations are currently conducted at a single location near Haifa, Israel and any disruption at our facility could materially adversely affect our business, financial condition and results of operations.

Substantially all of our operations are conducted at a single location near Haifa, Israel. We take precautions to safeguard our facility, including obtaining insurance coverage and implementing health and safety protocols and off-site storage of computer data. However, a natural or other disaster, such as a fire or flood or an armed conflict involving Israel, could damage or destroy our facility and our manufacturing equipment or inventory, cause substantial delays in our operations and otherwise cause us to incur additional unanticipated expenses. In addition, the insurance we maintain against fires, floods and other natural disasters may not be adequate to cover our losses in any particular case. Furthermore, we may not be reimbursed for losses resulting from armed conflicts or terrorist attacks in Israel. With or without insurance, damage to our facility, our other property or to any of our suppliers, whether located in Israel or elsewhere, due to fire, a natural disaster or casualty event or an armed conflict, could materially adversely affect our business, financial condition and results of operations. See also “Risks Related to Our Operations in Israel—Conditions in Israel could adversely affect our business.”

We currently intend to engage a third party service provider to develop and later manage our information technology platform, which would allow healthcare professionals and patients to download and manage the data logs from our insulin pumps. If the development of this information technology platform is not successful or completed in a timely manner, or if we do not manage the personal and health information we compile in accordance with government regulations, market acceptance of our products could be limited and we may be subject to regulatory sanctions.

We intend to engage a third party service provider to develop and later manage the information technology platform for our insulin pumps, which would allow healthcare professionals and patients to download and manage the data logs from our insulin pumps. This information technology platform is preferred by physicians who need to review, monitor and adjust the diabetes treatment of their patients based on the performance of their insulin pumps. If the development of this information technology platform is not successful or completed in a timely manner, market acceptance of our insulin pumps may be limited due to the importance of this feature.

After the third-party service provider has completed the development of our information technology platform, we expect that it will also manage the platform’s operation and continue to upgrade its performance. This information technology platform is expected to hold personal and health information of a patient. The confidentiality of such information is generally protected by government regulations, which prescribe civil and criminal liabilities if violated. If our information technology platform does not properly protect patient

17

information, demand for our products could be adversely affected and we may be subject to civil and criminal sanctions, which could materially adversely affect our business, financial condition and results of operations. See also “Risks Related to Our Industry Regulation and Pricing—If we are found to have violated laws protecting the confidentiality of patient health information, we could be subject to civil or criminal penalties, which could increase our liabilities and damage our reputation or otherwise materially adversely affect our business, financial condition and results of operations.”

We intend to sell our products worldwide and, if we are unable to manage our international operations, our business, financial condition and results of operations could be materially adversely affected.

Our headquarters and all of operations and employees are located in Israel but we intend to market our products globally. Accordingly, we are subject to risks associated with global operations and our international sales and operations will require significant management attention and financial resources. In addition, our international sales and operations will subject us to risks inherent in international business activities, many of which are beyond our control and include, among others:

| | • | | foreign certification, registration and other regulatory requirements; |

| | • | | customs clearance and shipping delays; |

| | • | | import and export controls; |

| | • | | trade restrictions (mostly in Arab countries); |

| | • | | multiple and possibly overlapping tax structures; |

| | • | | difficulty forecasting the results of our international operations and managing our inventory due to our reliance on third-party distributors; |

| | • | | differing laws and regulations, business and clinical practices, third-party payor reimbursement policies and patient preferences; |

| | • | | differing intellectual property protection among countries; |

| | • | | difficulties staffing and managing our international operations; |

| | • | | difficulties in penetrating markets in which our competitors’ products are more established; |

| | • | | currency exchange rate fluctuations; and |

| | • | | political and economic instability, war or acts of terrorism. |

If we are unable to manage our international operations effectively, our business, financial condition and results of operations could be materially adversely affected.

Technological breakthroughs in diabetes monitoring, treatment or prevention could reduce the demand for our insulin pumps; if we are unable to successfully complete the development and commercialization of our combined continuous glucose monitoring and insulin pump device, we could be at a competitive disadvantage.

Diabetes treatment is subject to rapid technological change and product innovation. Our ability to become and remain competitive depends in large part upon our ability to develop and market cost-effective new products and technologies that meet diabetes patients’ needs in a timely manner. A number of companies, medical researchers and existing pharmaceutical companies are pursuing new insulin delivery devices, delivery technologies, sensing technologies, procedures, drugs and other therapies for monitoring, treating and/or preventing insulin-dependent diabetes. Successful developments by our competitors or others could reduce the demand for our insulin pumps. Furthermore, if we are unable to successfully complete the development of our continuous glucose monitoring system and a device that will host both our insulin pump and continuous glucose monitoring system on one patch, we may be at a competitive disadvantage and our business, financial condition and results of operations could be materially adversely affected.

18

If we do not effectively manage our growth, our ability to increase sales and cash flow will be limited.

We have only recently begun to commercialize our Adi insulin pump and LightyDD infusion sets. If the commercialization of these and our other future products is successful, our business will need to grow. Continued growth would subject us to numerous challenges, including, among others:

| | • | | implementing appropriate operational and financial systems and controls; |

| | • | | expanding our manufacturing capacity and scaling up production; |

| | • | | expanding our sales and marketing capabilities; |

| | • | | managing our international operations effectively; |

| | • | | providing adequate training and supervision to maintain high quality standards; and |

| | • | | preserving our culture and values. |

In addition, our expected growth will continue to place additional significant demands on our management and our financial and operational resources. If we are unable to manage our growth, our business, financial condition and results of operations could be materially adversely affected.

Consolidation in the healthcare industry could materially adversely affect our future revenues and operating income.

The medical device industry has experienced a significant amount of consolidation resulting in increased competition and pricing pressures. In addition, group purchasing organizations and integrated health delivery networks have served to concentrate purchasing decisions for some customers, which has placed additional pricing pressure on medical device manufacturers and suppliers. Further consolidation in the industry and concentrated purchasing decisions could exert additional pressure on the prices of our products and could materially adversely affect our future revenues and operating income.

We may be subject to product liability lawsuits, which could result in expensive and time-consuming litigation, payment of substantial damages, and an increase in our insurance rates.

If our current or future products are found to be defectively designed, manufactured or labeled, or contain defective components or are misused, or if someone claims any of the foregoing, whether or not meritorious, we may become subject to substantial and costly litigation. Any misuse of our devices or failure to adhere to the operating guidelines of our insulin pumps and our insulin infusion sets could cause significant harm to patients, including death. In addition, if our operating guidelines are found to be inadequate, we may be subject to liability claims. Such claims could divert management’s attention from day-to-day responsibilities, be expensive to defend and result in sizable damage awards against us. We maintain product liability insurance to protect against these risks, but we may not have sufficient insurance coverage for all future product liability claims. Any such claims brought against us, whether or not meritorious, could increase our product liability insurance rates or prevent us from securing continuing coverage at reasonable rates, or at all, could damage our reputation in the industry and could reduce our revenues. Product liability claims in excess of our insurance coverage would be paid out of cash reserves, which could materially adversely affect our business, financial condition and results of operations.

We may require additional funding in order to complete the commercialization of our Adi insulin pump and LightyDD infusion sets and the development and commercialization of our other products under development.

Our current operations have consumed substantial amounts of cash. We expect that we will need to continue to spend substantial amounts in order to complete the commercialization of our Adi insulin pump and LightyDD infusion sets and the development of our Nilipatch insulin patch pump and combined continuous glucose monitoring and insulin pump device. Although we intend to use the proceeds of this offering to finance some of

19

these operations, we currently expect that we may need to raise additional funds in the future. Additional financing may not be available to us on a timely basis on terms acceptable to us, or at all. In addition, any additional financing may be dilutive to our shareholders or may require us to grant a lender a security interest in our assets.

Furthermore, if adequate additional financing on acceptable terms is not available, we may not be able to commercialize our Adi insulin pump and LightyDD infusion sets at the rate we desire and we may have to delay development or commercialization of our other products. Alternatively, we may be required to license to third parties the rights to commercialize products or technologies that we would otherwise seek to commercialize on our own. We also may have to reduce marketing, customer support or other resources devoted to our products. Any of these factors could materially adversely affect our business, financial condition and results of operations.

We depend on third parties to manage our pre-clinical and clinical studies and trials and to perform related data collection and analysis and, as a result, we may face costs and delays that are outside of our control.