UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | | |

| | For the fiscal year ended December 31, 2012 | |

| | | |

| | OR | |

| | | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | | |

| | For the transition period from ____________ to ____________ | |

| | | |

| | Commission file number: 333-167650 | |

GXS Worldwide, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 35-2181508 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| | |

| 9711 Washingtonian Boulevard, Gaithersburg, MD | 20878 |

| (Address of principal executive offices) | (Zip Code) |

301-340-4000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No R

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes £ No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes £ No R

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or shorter period that the registrant was required to submit and post such files). Yes R No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer £ | Accelerated filer £ | Non-accelerated filer R | Smaller reporting company £ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

As of March 27, 2013, the registrant had 1,000 outstanding shares of common stock, all of which was held by an affiliate of the registrant.

Documents incorporated by reference: None.

GXS WORLDWIDE, INC.

ANNUAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2012

| | | Page |

| | | |

| |

| | | |

| PART I | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| PART II | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| PART III | | |

| | |

| | |

| | |

| | |

| | |

| | | |

| PART IV | | |

| | |

| | | |

| | | |

| | | |

In this Annual Report, all references to “our,” “us,” “we,” “the Company” and “GXS” refer to GXS Worldwide, Inc. and its subsidiaries as a consolidated entity, unless the context otherwise requires or where otherwise indicated. All references to “Inovis” refer to Inovis International, Inc., which we acquired on June 2, 2010. All references to “RollStream” refer to RollStream, Inc., which the Company acquired on March 28, 2011. All references to “fiscal year 2012” or “2012” refer to the year ended December 31, 2012, all references to “fiscal year 2011” or “2011” refer to the year ended December 31, 2011.

We own or have rights to use various trademarks, trade names and service marks in conjunction with the operation of our business, including, but not limited to: GXS Trading Grid®, GXS ActiveSM Community (formerly known as GXS RollStreamTM), GXS ActiveSM Applications, BetweenMarkets, BizLink, BizManager, BizConnect, Inovis, Inovis Catalogue, TrustedLink and, in certain foreign jurisdictions, GXS and Tradanet.

Market and industry data and forecasts, used in this Annual Report on Form 10-K, were obtained from independent industry sources. Some data is also based on our good faith estimates. Although we believe these third-party sources to be reliable, we have not independently verified the data obtained from these sources and we cannot assure you of the accuracy or completeness of the data. Forecasts and other forward-looking information obtained from these sources and our estimates are subject to the same qualifications and uncertainties as the other forward-looking statements in this Annual Report on Form 10-K. The Gartner Report described herein (the “Gartner Report”) represents data, research opinions or viewpoints published as part of a syndicated subscription service by Gartner, Inc. (“Gartner”), and are not representations of fact. Each Gartner Report speaks as of its original publication date (and not as of the date of this Annual Report on Form 10-K) and the opinions expressed in the Gartner Report are subject to change without notice.

The common stock of GXS, Inc., GXS Worldwide, Inc.’s only direct subsidiary, is collateral for the Company’s 9.75% Senior Secured Notes due 2015 (the “Senior Secured Notes” or “notes”). Securities and Exchange Commission (“SEC”) Rule 3-16 of Regulation S-X (“Rule 3-16”) requires financial statements for each of the registrant’s affiliates whose securities constitute a substantial portion of the collateral for registered securities. The common stock of GXS, Inc. is considered to constitute a substantial portion of the collateral for the registered notes. Accordingly, the financial statements of GXS, Inc. would be required by Rule 3-16. Management does not believe the GXS, Inc. financial statements would add meaningful disclosure and has not included those financial statements herein, because they are substantially identical to the GXS Worldwide, Inc. financial statements and the total assets, revenues, operating income, net income (loss) and cash flows of GXS, Inc. are expected to continue to constitute substantially all of the corresponding amounts for GXS Worldwide, Inc. and its subsidiaries.

Certain statements contained in this Annual Report on Form 10-K and other materials we file with the SEC, or in other written or oral statements made or to be made by us, other than statements of historical fact, are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements give our current expectations or forecasts of future events. Words such as “may,” “assume,” “forecast,” “position,” “predict,” “strategy,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,” “project,” “budget,” “potential” or “continue,” and similar expressions are used to identify forward-looking statements. They can be affected by assumptions used or by known or unknown risks or uncertainties. Consequently, no forward-looking statements can be guaranteed. Actual results may vary materially. You are cautioned not to place undue reliance on any forward-looking statements. You should also understand that it is not possible to predict or identify all such risk factors and you should not consider the following list to be a complete statement of all potential risks and uncertainties. Risk factors that could cause our actual results to differ materially from the results contemplated by such forward-looking statements include:

| | · | our ability to maintain our prices at an acceptable level; |

| | · | increasing price, product and services competition by United States (“U.S.”) and foreign competitors, including new entrants and existing or expanded in-house information technology departments; |

| | · | rapid technological developments and changes and our ability to introduce competitive new products and services on a timely, cost effective basis; |

| | · | our mix of products and services; |

| | · | customer demand for our products and services; |

| | · | general domestic and international economic conditions and growth rates, including sluggish and recessionary economic conditions and exposure to customers in high economic risk sectors; |

| | · | declines in the creditworthiness of our customers or their ability to pay us on a timely basis; |

| | · | currency exchange rate fluctuations; |

| | · | our ability to market our products and services effectively; |

| | · | the length of life cycles for the products and services we offer; |

| | · | our ability to protect our intellectual property rights; |

| | · | our ability to protect against data security breaches and to protect our data centers and co-location data centers from damage; |

| | · | technical or other problems that adversely impact the availability and quality of our products and services or otherwise adversely affect the customer experience; |

| | · | our ability to attract and retain talent, especially in key technological areas; |

| | · | changes in U.S. and foreign governmental laws and regulations; |

| | · | the continued availability of financing in the amounts, at the times and on the terms required to support our future operations and our levels of indebtedness; |

| | · | our ability to comply with existing and future loan agreements; |

| | · | our ability to effectively implement our growth strategy; |

| | · | the outcome of existing or future litigation; |

| | · | our ability to negotiate acquisitions, dispositions and other transactions and to integrate assets and/or acquired companies and realize synergies successfully; and |

| | · | higher than expected costs or expenses arising from our acquisitions. |

This list of risk factors is not exhaustive, and new risk factors may emerge or changes to these risk factors may occur that would impact our business. Additional information regarding these and other risk factors may be contained in our filings with the SEC, especially on Forms 10-K, 10-Q and 8-K. All such risk factors are difficult to predict, and are subject to material uncertainties that may affect actual results and may be beyond our control. The forward-looking statements included in this Annual Report on Form 10-K are made only as of the date of this Annual Report on Form 10-K, and we undertake no obligation to update any of these forward-looking statements to reflect subsequent events or circumstances except to the extent required by applicable law.

All forward-looking statements are expressly qualified in their entirety by the foregoing cautionary statements.

PART I

Our Company

We are a leading global provider of business-to-business (“B2B”) integration solutions. Our solutions enable our customers to effectively manage the flow of electronic transaction information with their trading partners. We combine our global community of approximately 550,000 business partners, IT infrastructure, proprietary software-as-a-service (“SaaS”) applications and broad expertise to address the critical B2B challenges of our customers. By utilizing our B2B integration solutions, our customers realize a number of key benefits such as lower total cost of ownership, accelerated time to market and enhanced reliability and security.

B2B integration facilitates the exchange of transactions that occur between supply chain participants, such as manufacturers, retailers, distributors and financial institutions, and is central to a company’s ability to effectively collaborate with its partners. This exchange of information is becoming increasingly complex because of the globalization of supply chains, evolving business models and technologies, changing consumer buying habits and increasing regulatory and compliance requirements. Historically, most large organizations have managed many of their B2B integration needs in-house, which requires dedicated hardware, software and people. As B2B challenges intensify, global enterprises are increasingly seeking an integrated, outsourced solution to better focus resources on their core competencies.

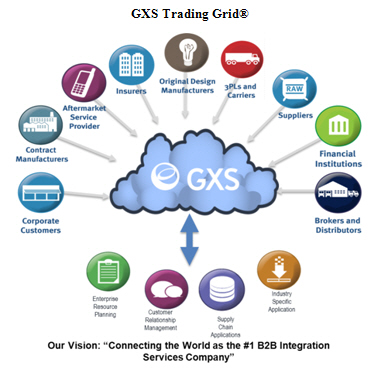

GXS Trading Grid®, our proprietary cloud-based platform, is the foundation of our B2B integration solutions. GXS Trading Grid® consists of the IT infrastructure, proprietary applications and a global community of over 550,000 business partners that enable the secure and reliable flow of transactions between business partners.

Through GXS Trading Grid®, we provide our core B2B integration solutions, Messaging Services and Managed Services. Messaging Services allows for the automated and reliable exchange of electronic transaction information such as purchase orders, invoices, shipment notices and other files, amongst businesses worldwide. Managed Services provides an end-to-end fully outsourced B2B integration solution to our customers, including program implementation, operational management, customer support and a suite of value-added SaaS applications, which we refer to as GXS ActiveSM Applications. GXS ActiveSM Applications are offered to customers across all of our service lines and enhance our

customers’ visibility into, and control of, their supply chains and supporting business processes. In addition, we have the B2B integration expertise and process experience to best serve our customers’ needs.

We have deep vertical expertise in a variety of key industries such as retail, consumer products, financial services, automotive, manufacturing and high-technology and serve a broad base of large, multinational enterprises. As of December 31, 2012, we had over 40,000 direct-billed, active customers on our platform across 61 countries, including more than 56% of the Forbes Global 1000. The majority of our revenue is generated through transaction processing and subscription service fees from both Messaging Services and Managed Services. Revenue from Managed Services, our fastest growing solution, grew at a three year compounded annual growth rate (“CAGR”) of 23.6% from 2009 to 2012 and represented approximately 37% of our total revenue for the year ended December 31, 2012. We believe customers view our solutions as essential to their day-to-day supply chain operations and they typically enter into long-term contracts with us. Our transaction processing and software maintenance fees, which are recurring in nature, represented approximately 85% of our total revenue for the year ended December 31, 2012. Additionally, approximately 92% of our top 50 customers, based on annual revenue in fiscal 2012, have been our customers for five or more years.

Our Opportunity

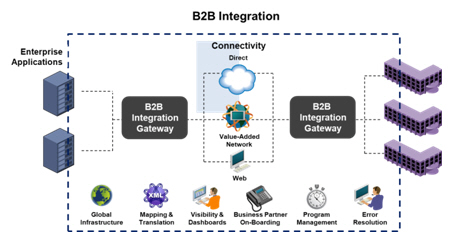

B2B integration is the exchange of transactions that occurs between supply chain participants, such as manufacturers, retailers, distributors and financial institutions, and it includes the network, software and people and processes that facilitate this exchange. Being able to exchange information with business partners is central to a company’s ability to build and manufacture products and deliver services with speed and quality, coordinate timely logistics and shipping activity, ensure accurate terms and payment, and better serve customers. Businesses using B2B integration derive significant benefits including gaining end-to-end supply chain visibility, eliminating excess inventory, tracking global shipments, optimizing the launch of new products, understanding customer purchasing trends and managing payments and cash flow. The chart below highlights the key components of B2B integration.

At its most basic level, a company that needs to send B2B transaction information from its internal system, such as an Enterprise Resource Planning (“ERP”) system or Warehouse Management System (“WMS”), to a business partner’s internal system, has to take into account several different factors before it can transmit that information. These include internal system differences, multiple transaction formats and standards, multiple communication protocols and a wide spectrum of security and encryption standards:

| | · | Internal system differences: A company and its business partners may both have different internal ERP systems – or even different versions of the same systems – and the company will have to convert the transaction information from its internal system into a format that can be received and understood by its business partners’ internal systems. |

| | · | Multiple B2B transaction formats and industry standards: There is a vast array of B2B transaction standards, including ANSI X.12 EDI, EDIFACT, RosettaNet and OAG XML, that can be used. Companies usually must conform to the format preferred by their customer. As a result, it is very common to find that multinational companies use multiple different formats to exchange information with their business partners. |

| | · | Multiple communications protocols: There is a wide variety of communication methods available for B2B transmission, such as MQ, AS2, FTP, and X-400, on which the company and its business partners would need to conform. |

| | · | Security and encryption: There is a spectrum of network and application security standards which may be adopted, and the company and its business partners would be required to agree on a common approach to ensure interoperability. |

As a result of these factors, companies are often required to install software behind their firewalls that allow them to convert transaction information into the selected standards and map their data formats into those of their trading partners. Once the company has the data in the required format, the company needs to establish a connection to its business partners. This could be a direct connection between businesses, a connection over a value-added B2B network such as through Messaging Services or another method such as a web portal connection over the Internet. Companies often utilize Value-Added Networks (“VAN”) for their connectivity given its reliability, security, scalability and cost benefits.

Given the challenges and evolving dynamics in the marketplace, there are several trends driving growth in B2B integration. These trends include the following:

Growing Complexity of Business Processes. Business processes are growing increasingly complex because of a paradigm shift in business models caused by the following factors:

| | · | Globalization of supply chains: Companies are expanding their operations, supply chains and trading partner relationships globally in order to target additional customers and also to exploit trends in off-shoring, outsourcing and contract manufacturing. As a result, businesses have to deal with a variety of languages, regulations and compliance requirements, and also be able to support their infrastructure across all the time zones in which they or their business partners operate. |

| | · | Digitization of business processes: The migration from paper-based to digitized business processes continues at a rapid pace, propelled by reduced costs and enhanced operating efficiency. This has led to a proliferation of both structured and unstructured electronic data that is often unique to a particular business and its supply chain and trading partners. Furthermore, there are a variety of global, industry-specific and regionally defined standards which govern the ability of companies to exchange information electronically with their trading partners. |

| | · | Changes in technology: There is a migration of technology infrastructure from legacy infrastructure to a more open, Internet-based infrastructure, which creates new challenges, such as the need for businesses to adhere to different security and encryption standards. |

| | · | Changing consumer buying habits: As consumers purchase more goods online and demand more customization and personalization of products, businesses need to change their processes to be responsive to these changing consumer buying habits. Businesses are transitioning from inventory-in-hand models to inventory-on-demand models in order to supply products and services in a more dynamic manner, decreasing working capital without affecting delivery time and quality. |

| | · | Increased regulatory, security and compliance requirements: Businesses have to comply with increasing regulatory, security and compliance requirements such as those put in place by governments and standards-setting organizations including tax, international trade and financial regulations. |

The growing complexity of business processes is leading to a significant increase in the number of global external partners that companies need to integrate with, including customers, suppliers, logistics carriers, distributors, financial institutions, governments and other supply chain participants. This complexity for sending transaction information from a single system at the business to a single system at one partner grows exponentially as businesses need to send and receive transaction information from and to many different systems, with thousands of global business partners, across various data and security standards, protocols and connections around the world.

Acceptance of SaaS and Cloud-based Delivery Models. Historically, most large organizations have managed many of their B2B integration services in-house. However, keeping up with the increasing complexity of business processes requires a substantial amount of dedicated B2B integration resources, such as IT infrastructure, software and dedicated employees. The evolution of SaaS and cloud-based delivery models, as evidenced by the success of Salesforce.com, Amazon Web Services, Workday and Google Docs, has increased the acceptance of these models by corporate IT

organizations. This has led to greater outsourcing of B2B integration processes to vendors who can deploy their solutions through SaaS and cloud-based delivery models. This outsourcing can create significant benefits, including access to new technology and features, lower total cost of ownership, accelerated time to market, improved customer satisfaction, and enhanced reliability and security.

Importance of Real-Time Information and Analytics. As digitization of business processes increases, the large volume of data produced by organizations is growing exponentially. According to a 2011 IBM report, 2.5 quintillion bytes of data are created every day, and 90 percent of the data in the world as of the date of the report had been created only in the prior two years. Businesses are beginning to realize the importance of accessing and analyzing these data on a real-time basis in order to gain valuable insights into their processes to improve efficiency, enhance quality and manage costs. According to Gartner, 34% of data in corporate ERP systems originates outside the enterprise with business partners from customers, suppliers, logistics providers and financial institutions. As a result, a robust B2B technology platform capable of supporting complex integration with business partners is required to support real time information and analytics. As business process complexity increases and multi-tier supply chains become more prevalent, the difficulty of gaining access to these data increases and the importance of a dedicated and scalable B2B technology platform grows substantially.

We believe the above trends are driving significant growth in the B2B integration services industry and increasing demand for our solutions. Gartner describes the B2B integration services industry as the multi-enterprise B2B market which is defined as a combination of B2B software and services that companies use to perform multi-enterprise integration with external business partners. Gartner estimates the multi-enterprise/B2B infrastructure market, which includes global B2B Messaging Services, B2B Managed Services and B2B Gateway Software, to be $3.5 billion in 2012. Between 2012 and 2016, Gartner expects the multi-enterprise/B2B infrastructure market will grow at a 9.3% CAGR to $5.0 billion. Over the same period, B2B Managed Services is expected to grow from $1.5 billion to $2.6 billion, a 14.0% CAGR. The following chart illustrates the market opportunity and growth characteristics of the B2B integration opportunity, as defined by Gartner.

|

| Source: Gartner “Competitive Landscape: Integration Brokerage” by Fabrizio Biscotti, Benoit J. Lheureux, Paolo Malinverno, November 26, 2012. |

We believe that the market opportunity as defined by Gartner only measures the current spending by businesses on external B2B solutions and that there is significant incremental opportunity from outsourcing of the existing in-house B2B spend. Based upon our interaction with customers, we estimate that large enterprises (those with more than $1 billion of annual revenue) spend an average of at least $5 million to $10 million per year on in-house B2B solutions, including spending on IT infrastructure, software and people. Hoovers estimates that there are currently over 6,500 businesses globally with more than $1 billion in revenue, which we believe implies a significant global market opportunity for outsourced B2B integration services.

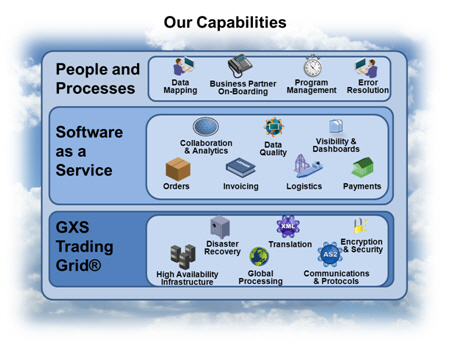

Our Capabilities

Our core B2B integration capabilities help our customers effectively manage the flow of electronic information with their trading partners, addressing the critical B2B challenges that global enterprises face every day. We combine GXS Trading Grid®, SaaS applications and people and processes to offer an integrated value proposition to our customers. We use our capabilities to tailor solutions to specific customer needs to drive high levels of reliability and scalability at lower overall total cost of ownership. We enable our customers to respond quickly and effectively to changes in their business model, gain insights into and maintain control of their mission-critical business processes and broaden the reach of their supply chain and business partner relationships.

GXS Trading Grid®. The key capability that underlies our solutions is GXS Trading Grid®, our proprietary cloud-based platform that connects over 550,000 business partners and processes billions of transactions. GXS Trading Grid® has specialized capabilities for automating, assembling, monitoring and improving mission-critical multi-enterprise business processes. Our platform today is a leading cloud computing infrastructure that supports continuous real-time information flows, while delivering low unit costs, enhanced scalability and high platform availability. In addition, GXS Trading Grid® is based on a multi-tenant, service-oriented architecture, which is highly scalable and allows us to add incremental volumes and customers at low marginal costs. Embedded in GXS Trading Grid®, our B2B gateway applications serve as the core engine of our service delivery platform. These applications provide communications protocols and data translation technology that enable transactions to flow seamlessly through our network. Our B2B gateway applications are sophisticated and offer several advanced features such as data visibility and monitoring as well as business partner on-boarding components that are valued by our customers. We believe GXS Trading Grid® is the industry standard in terms of size and breadth of capability and continues to grow as we add new customers and their trading partners.

Software-as-a-Service. Our SaaS applications offer our customers enhanced visibility and control of their supply chains and supporting business processes. These services, branded “GXS ActiveSM Applications,” are available on GXS Trading Grid®. Our GXS ActiveSM Applications utilize data from GXS Trading Grid® to provide information and insights into the customer’s supply chain that they are not able to typically get from their internal systems. GXS ActiveSM Applications support core business processes such as procure to pay, order to cash, logistics management, electronic invoicing and compliance, and data quality across a wide range of vertical industries and geographic territories. There are currently over 150,000 business partners utilizing our GXS ActiveSM Applications suite around the world.

People and Processes. We believe that our people are the leading experts in B2B integration and their knowledge of technology and region- and industry-specific standards, customs, regulations and business practices allows our customers to quickly

automate new processes, enter new regional markets and improve business performance. We use a proprietary framework for process management and have invested in the development of “world-class” business processes, procedures and tools that enable our employees to actively monitor, react to and solve complex B2B challenges. We leverage a global delivery platform to dynamically flex capacity to support trading partner on-boarding, data mapping, and customer support services cost efficiently. We also provide program and project management services, B2B integration consulting and dedicated support solutions to our customers around the world.

Our Core Solutions

Our core B2B integration solutions, Messaging Services and Managed Services, are delivered through GXS Trading Grid®. Together, Messaging and Managed Services represented over 80% of our total revenue for the year ended December 31, 2012.

Messaging Services. Messaging Services includes the secure, reliable exchange of structured business documents, such as purchase orders, invoices and shipment notices, from one business to another, primarily over the Internet. Businesses are provided one or more unique addresses to send and retrieve documents and files. A database is maintained that stores relationships between businesses, referred to as integration pairs or trading partner relationships. These relationships enable messages to flow securely between businesses. Customers use GXS Messaging Services to achieve benefits in security, improve utilization in networking resources, and gain independence in operating their internal systems. Messaging Services offers an alternative to customers who seek to avoid having business partners accessing their behind the firewall internal systems as well as avoid costly IT infrastructure investments needed to scale in parallel with the number of business partner connections. Messaging Services also offer customers an ability to operate their B2B activities on a schedule that does not have to synchronize with that of their business partners. Our Messaging Services solution achieved $214.6 million in total revenue for the year ending December 31, 2012.

Managed Services. Within the multi-enterprise integration market, the fastest growing segment is B2B managed services. Businesses use B2B managed services to extend or enhance a multi-enterprise business process or to outsource the management of a B2B process. A B2B program includes all of the hardware, software and people required to support a company’s business partners electronically, including customers, suppliers, shipment carriers and banks. GXS Managed Services offer an alternative delivery model designed for companies that may be struggling to achieve returns from B2B integration software investments or are unable to handle the considerable tasks associated with managing worldwide B2B programs. In our model, there is no need for our customers to purchase or manage B2B integration software, hardware or people. Instead, companies leverage GXS Trading Grid® by outsourcing the management of the underlying server hardware, storage platforms and B2B translation technology. Through this model, companies are able to achieve their B2B integration goals faster and at a lower cost than through in-house and software-based approaches. For example, in early 2013, Stanford University’s Global Supply Chain Management Forum determined that when our customers consider the overall value of B2B managed services, 96% of those surveyed indicated that these services increased the value of their B2B integration program. We have over 600 Managed Services customers today and in 2012, our Managed Services solution achieved $179.4 million in total revenue, growing at a CAGR of 23.6% in the last three years through 2012.

Our Growth Strategy

Our vision is to connect the world as the leading B2B integration services company. We intend to achieve our vision by delivering an unparalleled customer experience supported by our innovative cloud-based solutions and our talented employees. Our strategy to extend our leadership position focuses on the following:

Capitalize on Strong Demand for Managed Services. We believe the opportunity to extend an existing B2B process or to outsource a B2B process is the fastest growing opportunity in our industry, driven in large part by the need for customers to effectively manage the increasing complexity and cost of their global supply chains and improve their ability to serve customers. We intend to continue increasing our Managed Services solutions by leveraging our substantial global footprint and process domain knowledge to provide an integrated, outsourced solution at lower cost, with high quality and increased scalability. We estimate that we have a small percentage of the overall B2B spend of our existing 600 Managed Services customers and, as a result, we are well-positioned to increase our share of their B2B spend by expanding our relationship with them to encompass additional geographies, business units and business processes. In addition, we believe we have a significant opportunity to introduce Managed Services solutions to the approximately 5,900 businesses with over

$1 billion in revenue not currently using our Managed Services. To capture this opportunity, we have invested in additional sales and marketing resources to focus on new customer acquisition as well as to further penetrate our existing customers.

Cross-sell Our GXS ActiveSM Applications. We intend to cross-sell our GXS ActiveSM Applications solutions across our Messaging Services and Managed Services customers. The penetration of these applications amongst our global customer base is nascent, and we believe that there is significant opportunity to increase this penetration as a part of our sales strategy. Given the breadth of our GXS ActiveSM Applications portfolio across several business processes, we believe there is a strong opportunity to sell into new parts of the business including procurement, supply chain, accounting, treasury, and transportation & logistics. We believe increased adoption of our GXS ActiveSM Applications will enhance the value we provide our customers and allow us to build longer term relationships over time.

Expand Our GXS ActiveSM Applications. We intend to develop new GXS ActiveSM Applications and enhance the features in our existing GXS ActiveSM Applications in order to deliver more data and insights to our customers. We believe that the large amount of data that we manage for our customers related to their business transactions and process flows can be leveraged to provide business analytics tools and dashboards. We intend to continue developing our capabilities to aggregate, report and analyze data for our customers, in order to offer future value-added services that will help our customers better understand and manage their supply chain. We believe developing these tools will increase the attractiveness of our solutions for customers, and will provide us with a significant competitive advantage.

Invest in Our Platform. We will continue to invest in our platform to improve the speed, flexibility and capabilities of GXS Trading Grid®. Key investments in these areas include increasing the number of customer-facing resources we have in our professional and support services groups, investing in data center and technology upgrades and standardizing and making architectural platform enhancements to GXS Trading Grid®. We believe the outcome of these investments will be to increase our customer satisfaction and loyalty, lower operating costs, and create new revenue-generating opportunities through an improved ability to allow our customers to mix and match solutions. The enhanced architecture will also enable us to effectively monitor, analyze and report on the billions of transactions passing through GXS Trading Grid® .

Selectively Pursue Strategic Acquisitions. We intend to grow the scope and scale of our business by selectively pursuing acquisitions of companies with complementary products and technologies. Our strategy focuses on acquiring businesses that will increase the number of customers in new or existing geographic territories and industry verticals. We will also look for opportunities to enhance and extend the value of our GXS ActiveSM Applications portfolio by acquiring new technologies and capabilities that can be delivered through GXS Trading Grid®. We believe we have developed an internal competency regarding post-acquisition integration that allows us to achieve significant operating leverage when combining with businesses that we acquire.

Our Products and Services

Messaging Services. Messaging Services provide for the automated and reliable exchange of business documents such as purchase orders, invoices, shipment notices and other files, amongst businesses worldwide. Our Messaging Services solution allows customers to transmit and receive information to their business partners on GXS Trading Grid®, which has a community of over 550,000 business partners. Our Messaging Services include the following:

| | · | Diverse Protocols and Standards Support: Customers can access our network through the Internet, a private IP network, or third-party VANs. The network supports a vast array of contemporary B2B standards such as XML (e.g. RosettaNet, ebXML, etc.), ANSI X12, EDIFACT, TRADACOMS and binary files. In addition, we support a wide number of communication methods including AS2, AS3, SFTP, FTPS, HTTPS (web browser access), VPN, FTP Push, OFTP, local dial PPP, dial PPP 800 service, bisync and frame relay. |

| | · | High Performance and Availability: Our Messaging Services run on a high availability platform ensuring a reliable service for our customers and their trading community. |

| | · | Data Security: Our infrastructure ensures confidentiality and availability of data by providing integrity at every level including Internet or private network security, application backup protection and trading partner validation. |

| | · | Automated Process Management: Rules-based services enable customers to automate steps in their business processes, such as document delivery options, exception alerts, acknowledgment services and automated document routing. |

We charge our Messaging Services customers a fee for sending and receiving messages on our network. The majority of our Messaging Services revenue is billed against minimum monthly commitments pursuant to contracts with terms of between one and four years. In addition, Messaging Services customers who also are using a GXS ActiveSM Application will typically sign a multi-year subscription agreement for access to, and usage of, that application platform.

Managed Services. Through our cloud-based Managed Services solution, our comprehensive B2B outsourcing service, we perform all day-to-day management of the hosted cloud infrastructures, including systems health monitoring, data backup, network management, systems administration, database management, application support and disaster recovery. In a typical Managed Services implementation, our customers leverage GXS Trading Grid® and we identify, on-board, and test transactions flows with both our customers and their trading partners. We also manage all data mapping and translation tasks, perform change management and issue resolution with any trading community, and proactively troubleshoot and reprocess documents, if necessary, through GXS Trading Grid®. Our Managed Services solution includes the following services:

| | · | Mapping & Translation: B2B implementations require deep capabilities and expertise in ERP and internal systems integration in order to enable accurate informational flows and trading community collaboration. We manage all integration data-mapping and translation tasks, perform change management and issue resolution with business partners, and process critical production map changes on-demand. These mapping and translation services enable our customers to achieve proven cost, quality, and performance advantages over in-house approaches. |

| | · | Visibility & Dashboards: We offer a comprehensive suite of SaaS products for end-to-end visibility into the lifecycle of all B2B transactions. Features include transaction monitoring, tracking, error alerting, usage reporting and root cause analysis. In addition, our customers can receive timely and accurate transaction status alerts and monitor in-flight transactions for ensuring data quality and compliance. |

| | · | Business Partner On-Boarding: We provide an industry-leading combination of experienced B2B implementation professionals and robust community on-boarding tools to rapidly on-board business partners – regardless of size, internal systems complexity or geographic diversity – to ensure full participation amongst our customer’s trading communities. |

| | · | Program Management: Our experienced specialists work with our customers to ensure B2B program implementation success. We also provide day-to-day project management activities ranging from oversight of all production activities, including status reports and resource orchestration, to help manage change request activity and production incidents. |

| | · | Error Resolution: We deliver comprehensive and proactive error resolution management of B2B programs, including comprehensive global customer and trading community support. We offer support services in 12 languages worldwide, including transaction and systems health monitoring, exception management and incident management. |

Additionally, our Managed Services customers can elect to utilize one of our GXS ActiveSM Applications which layer additional value-added services onto their supply chain activities, such as data compliance, process control and document visibility. These services are built on GXS Trading Grid®. Examples of these Active Applications include GXS ActiveSM Invoice with Compliance, GXS ActiveSM Logistics, GXS ActiveSM Orders and GXS ActiveSM Community.

We charge our Managed Services customers a fee for sending and receiving messages on our network, as well as for access to and usage of value-added services and on-going B2B program management and support. We typically sign multi-year long-term contracts with our customers for our Managed Services solution. The majority of our Managed Service revenue is billed against minimum monthly commitments pursuant to contracts with terms of between three and five years. We currently have over 600 customers in our Managed Services service line, over 400 of whom were added in the last four years.

B2B Software and Services. Our B2B Software and Services solutions allow customers to deploy B2B integration gateways on their premises. Our B2B gateway software allows businesses to connect their internal systems and processes to their partners through an external network, such as our GXS Trading Grid®. Our software portfolio features specialized B2B integration gateways, managed file transfer, and high-performance and desktop EDI translators. Our B2B gateways are specifically designed for the unique needs of multi-enterprise B2B data flows, supporting any-to-any mapping and data translation. Additionally, our software portfolio includes Managed File Transfer (“MFT”) software designed exclusively

for secure and reliable file exchange of very large files, such as document images or marketing collateral, with business partners worldwide.

We typically charge our customers a one-time license fee for our software as well as an ongoing maintenance fee.

Data Synchronization. Our data synchronization technologies enable the exchange of product and price information between the suppliers of consumer products and the retailers that sell them. Product information typically consists of brand, description, price, promotion, packaging, weight, tax and regulatory data for each global trade item number (“GTIN”). Our services allow our customers to deploy data pools and electronic catalogue services, which provide a network to exchange information amongst their supply chain using a “publish and subscribe” model and thereby allow them to synchronize their supply chains onto a “single version of the truth” with respect to product or item information.

We typically charge our customers for access fees to our data synchronization catalogue services, as well as data transmission fees for sending and receiving messages to these catalogues across our network.

Custom Outsourcing Services. Custom Outsourcing Services allows our customers to outsource activities not directly related to supply chain activities but for which our outsourcing capabilities and expertise can provide greater value to our customers than they could otherwise realize by managing these applications themselves. This service line, which has been de-emphasized over the past several years, consists of applications developed to address specific customer business process challenges. Custom Outsourcing Services are delivered on a hosted basis for which we charge recurring subscription fees for access to and usage of these applications.

Our Customers

We provide our products and services to a large customer base across a number of different industries. We serve a combined trading community of over 550,000 business partners and have over 40,000 direct-billed, active customers on our platform across 61 countries. Our customers include approximately two-thirds of the Fortune 500 companies and over 56% of the Forbes Global 1000 companies. These customers range in size from small businesses to multinational corporations. We serve customers in a broad range of industries including retail, consumer products, financial services, automotive, manufacturing and high-technology.

Our customer base is well diversified, with our largest customer representing only 4% of our total revenues in 2012, and with the top ten and top fifty customers accounting for approximately 15% and 30% of our total revenues, respectively. The customer base is also well diversified across geographies with approximately 60% of our total 2012 revenues generated in North America; approximately 20% in Europe, Middle East and Africa (“EMEA”); approximately 11% in Asia Pacific (“ASPAC”); and approximately 9% in South America.

Sales and Marketing

We primarily market our solutions through our global direct sales force, which is organized along three lines: industry, geography and major account coverage. Our direct sales teams concentrate on developing new customers within a particular industry and region, as well as increasing the utilization and penetration of existing trading communities. Our direct sales teams are supported by a team of technical sales and marketing support personnel who assist in the sales process as needed. We also have resellers of our products and services in selected geographies and serving selected industry segments.

Our marketing activities are designed to build market awareness and create demand for our services and solutions through tradeshows, public relations, social media and other web-based marketing initiatives. Our product management teams manage each of our product lines and, together with our marketing communications group, focus on increasing awareness of specific services and solutions that we offer.

Our Data Infrastructure

We currently operate, or co-locate in, data centers around the world through which we have developed capacity planning, engineering, implementation and disaster recovery policies. These data centers service customers on a regional and global basis and house our data processing infrastructure. We believe our data processing infrastructure is sufficient to

effectively meet demand for the foreseeable future and to increase capacity as needed, and we have made, and will continue to make, significant investments in upgrading our data center locations and technology footprint.

Our data processing infrastructure is supported by well-trained operations professionals and strict procedures and guidelines for running mission-critical applications. These include: (1) a 24x7 global operations center located in Brook Park, Ohio to monitor operations, predict changes, and adjust configurations as required; (2) a 24x7 global customer support organization to provide communication and problem resolution; and (3) our certified operating environments and security policies (e.g., Statement on Standards for Attestation Engagements (“SSAE”) No. 16 certification).

Our telecommunications infrastructure is a high-speed digital network that connects us to our customers and facilitates the transport of multiple protocols via private lines and the Internet. We partner with a number of top tier telecommunications services providers for global network infrastructure and connectivity, and continually seek opportunities to enhance these relationships to improve our ability to respond to changing business needs and to lower our telecommunications and network infrastructure costs.

Our Intellectual Property

Our success and ability to compete are dependent, in part, upon our ability to adequately protect our proprietary technology and other intellectual property. In this regard, we rely on a combination of intellectual property rights, including patents, trademarks, copyrights, trade secrets and other intellectual property directly related to and important to our business. We also protect our proprietary technology, intellectual property and confidential information through the use of internal and external controls, including nondisclosure and confidentiality agreements with employees, contractors, business partners and advisors. Our policy is to apply for patents with respect to our technology and seek trademark registration of our marks from time to time when management determines that it is competitively advantageous and cost effective to do so.

In the U.S., we own 14 issued patents, 11 registered trademarks and approximately 100 registered copyrights. We also own a number of registered foreign trademarks and service marks.

While we do not believe that any one single patent, trademark, copyright or license is material to the success of our business as a whole, in the aggregate, these patents, trademarks, copyrights and licenses are material to our business.

Our Competition

We compete with numerous companies both nationally and internationally. Our competitors generally include:

| | · | Internal Information Technology Departments: We believe our most significant competitors are the in-house IT departments within our larger customers that attempt to “build it themselves” rather than engage with a third-party provider. We believe that the depth and breadth of our experience in B2B integration allows us to offer a faster, more attractive alternative to internally developed solutions which delivers higher quality at a lower cost to our customers. |

| | · | Multi-enterprise B2B Providers: Companies such as IBM, SAP, Liaison Technologies, E2Open, OpenText and SPS Commerce provide solutions in the B2B integration space. Given our scale and segment leadership position, we believe these integration providers lack the supply chain focus or business process expertise that we are able to provide through GXS Trading Grid®. |

| | · | On-Premise Software Vendors or ERP Providers: We believe companies such as IBM, Axway and Seeburger offer B2B functionality and/or ERP extensions that provide features similar to our products, but with less functionality than our Managed Services solution. We believe our solutions complement and improve the performance of on-premise software solutions, and our customers often find our cloud-based alternatives more attractive than behind-the-firewall software which involves significant internal resources and lengthy implementation cycles. |

| | · | Large Systems Integrators: Companies such as Accenture, HP/EDS, CSC and Hitachi offer end-to-end IT project outsourcing and development which occasionally involves B2B or supply chain functionality. Given our singular focus and expertise on B2B integration, we believe we are an attractive, ready-to-serve |

alternative to systems integrators attempting to build a custom solution from the ground up that may provide limited B2B functionality compared to our Managed Services solution. In fact, we are often engaged on a sub-contracted basis by large systems integrators to provide our standard suite of B2B services to meet an end-customer’s B2B integration needs.

Our Employees

As of December 31, 2012, we had 2,802 full-time employees. These employees consisted of:

| | · | 2,242 technical personnel engaged in maintaining or developing our services and solutions or performing related services; |

| | · | 224 administrative, finance and management personnel; and |

| | · | 336 corporate strategy, marketing, sales and sales support personnel. |

As of December 31, 2012, there were 1,098 employees located in the U.S., and the remaining 1,704 employees were in various other locations around the world, including: 838 in the Philippines; 235 in India; 191 in Brazil; and 189 in the United Kingdom (“U.K.”). We also had 208 full-time contractors, mostly in technical roles. None of our U.S. employees are represented by a labor union. We have not experienced any work stoppages and consider our employee relations to be good.

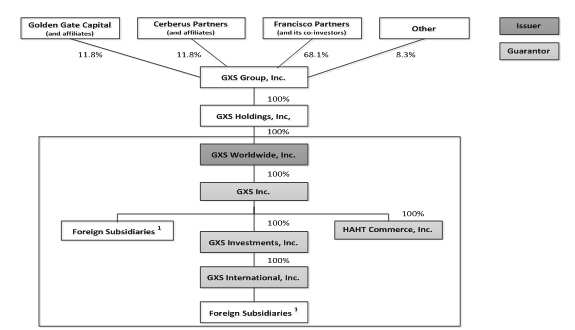

Our Corporate Structure

Our corporate structure can be summarized as follows:

________________

| 1. | Direct foreign subsidiaries of GXS, Inc. include foreign entities that were subsidiaries of Inovis International, Inc. (“Inovis”) prior to the merger with Inovis (the “Inovis Merger”), which became wholly owned subsidiaries of GXS, Inc. following the Merger. GXS, Inc. is a 100.0% shareholder of the majority of its direct and indirect foreign subsidiaries with the primary exceptions of GXS, Inc. (Korea) (85.0%) and EC1 Pte Ltd. (Singapore) (81.0%). |

Percentages are based on outstanding common stock as of December 31, 2012. Francisco Partners and its co-investors indirectly own approximately 68.1% of our outstanding common stock and Golden Gate Capital (and its affiliates) and Cerberus Partners (and its affiliates), private equity firms and the principal investors in Inovis prior to the Merger, each indirectly own approximately 11.8% of our outstanding common stock.

One member of our board of directors is appointed by, and is a partner of, Golden Gate Capital and one member is appointed by, and is a partner of, Cerberus Partners. The remaining seven board members are appointed by Francisco Partners, including Robert Segert, our current President and Chief Executive Officer. At December 31, 2012, one of the Francisco Partners’ board seats is vacant.

Corporate Information

The Company, GXS Worldwide, Inc. (formerly GXS Corporation), was incorporated in Delaware on September 9, 2002. Our principal executive offices are located at 9711 Washingtonian Boulevard, Gaithersburg, Maryland, and our telephone number is (301) 340-4000. We maintain a website at www.gxs.com. Information contained on our website is not incorporated by reference into this Annual Report on Form 10-K, or any other report filed with the SEC.

If any of the following risks occur, our business, results of operations or financial condition could be materially adversely affected. You should read the section captioned “Forward-Looking Statements” for a discussion of what types of statements are forward-looking as well as the significance of such statements in the context of this Annual Report on Form 10-K. The risks described below are not the only ones we face. Additional risks of which we are not presently aware or that we currently believe are immaterial may also harm our business, results of operations or financial condition.

Risk Factors Related to our Business

We have historically incurred substantial losses and we cannot guarantee that we will become profitable in the future.

We have incurred substantial losses since our acquisition by Francisco Partners and its co-investors in September 2002, primarily as a result of interest expense related to our indebtedness. As a result, we had a total accumulated deficit of approximately $277.4 million as of December 31, 2012. We may continue to incur losses and we cannot guarantee that we will report net income in the future.

Companies’ decisions to reduce expenditures on information technology may reduce demand for our products and services and cause our revenue to decline.

There can be no assurance that the level of spending on information technology in general will increase or remain at current levels in future periods. Lower spending on information technology or companies ceasing to outsource these services could result in reduced sales, reduced overall revenue and diminished margin levels and could impair our operating results in future periods. Decisions by our customers to defer investments in new technology solutions and software systems may cause a decrease in sales and may result in additional pricing pressure, which could have a material adverse effect on our business, results of operations and financial condition.

The markets in which we compete are highly competitive.

The markets for our products and services are increasingly global and competitive. As a result, we encounter intense competition in all parts of our business. We expect competition to increase in the future both from existing competitors and new companies that may enter our markets. In addition, we experience competition from in-house information technology departments when companies are determining whether to continue to outsource these services or perform them in-house. To remain competitive, we will need to invest continuously in product development, marketing, customer service and support and our service delivery infrastructure. However, we cannot be certain that new or established competitors or in-house information technology departments will not offer products and services that are superior to or lower in price than ours. We may not have sufficient resources to continue to invest in all areas of product development and marketing needed to maintain our competitive position. In addition, some of our competitors have greater name recognition, larger customer bases and greater financial, technical, sales, marketing and other resources than us, which may provide them with an advantage in developing or marketing new products and services. Although we have historically had a high customer retention and renewal rate, there can be no guarantee that we will continue to maintain this rate of retention and renewal in the future. In addition, in order to retain certain customers we have had to make certain pricing concessions and we expect this trend to continue.

We may need to change our pricing models to compete successfully.

The competition we face in selling our products and services, and general economic and business conditions, can put pressure on us to lower our prices. For example, as our Messaging Services business has become more commoditized, we have experienced pressure to reduce prices or provide additional services at no incremental charge. In addition, although many of our customers in our Managed Services business are subject to long-term contracts, they expect to share in the benefits of the decreasing cost of providing some of the services on the Managed Services platform. This often results in additional price pressure when these contracts come up for renewal.

If our competitors offer deep discounts on certain products or services or develop products and services that the marketplace considers more valuable, we may need to lower prices further or offer other favorable terms in order to

compete successfully. Furthermore, a shift by our customers towards products and services that are less expensive may also adversely affect pricing for our products. Any such changes could have a material adverse effect on our business, results of operations and financial condition.

In addition, to increase our revenues and achieve and maintain profitability, we must regularly add new customers or sell additional products and services to our existing customers. If prospective customers do not perceive our products or services to be of sufficiently high value and quality, we will not be able to attract the number and types of new customers that we are seeking or maintain our existing customers.

Our inability to adapt to rapid technological change could impair our ability to remain competitive.

The industry in which we compete is characterized by rapid technological change, frequent new product and service introductions and evolving industry standards. Our future success will depend in significant part on our ability to anticipate industry standards and to continue to enhance existing products and services and introduce and acquire new products and services on a timely basis to keep pace with technological developments. We expect that we will continue to incur expenses in the design, development and marketing of new products and services. Our competitors may implement new technologies before we are able to implement them, allowing our competitors to provide more effective products and services at lower prices.

We cannot provide assurance that we will be successful in developing, acquiring or marketing new or enhanced products or services that respond to technological change or evolving industry standards, that we will not experience difficulties that could delay or prevent the successful development, acquisition or marketing of such products or services or that our new or enhanced products and services will adequately meet the requirements of the marketplace and achieve market acceptance. Any delay or failure in the introduction of new or enhanced products or services, or the failure of such products or services to achieve market acceptance, could have a material adverse effect on our business, results of operations and financial condition.

Our products and services may not achieve market acceptance, which could cause our revenue to decline.

Deployment of our products and services requires interoperability with a variety of software applications and systems and, in some cases, the ability to process a high number of transactions. If our products and services fail to satisfy these demanding technological objectives, our customers may be dissatisfied and we may be unable to generate future sales. Failure to establish a significant base of customer references will significantly reduce our ability to sell our products and services to additional customers.

We are frequently required to enhance and update our products and services as a result of changing standards and technological developments, which makes it difficult to recover the cost of development and forces us to continually qualify new products with our customers.

For our products to be competitive, we must continually update and innovate with next-generation products. Over the last several years, the rate at which new technological developments have been introduced into the market has grown at a much more rapid pace than it had previously. Continually updated standards for the electronic exchange of information, such as those issued by the American National Standards Institute, have required us to produce enhancements to our products and services and provide some of our value-added solutions and related software with additional functionality. The frequency with which we must enhance our products makes it more difficult for us to recover the costs associated with product development because those costs must be recovered over increasingly shorter periods of time. We expect this trend to continue, and it may even accelerate. As a result, we may not be able to recover all of our product development costs, which could affect our profitability. Any failure or delay in our product development or quality assurance process could result in our losing sales until we are able to introduce the new product.

Risks associated with the evolving use of the Internet, including changing standards, competition, taxation, regulation and associated compliance efforts, may adversely impact our business.

The use of the Internet as a vehicle for electronic data interchange, (“EDI”), and related services currently raises numerous issues, including reliability, data security, data integrity and rapidly evolving standards. New competitors, which may include media, software vendors and telecommunications companies, offer products and services that utilize the

Internet in competition with our products and services and may be less expensive or process transactions and data faster and more efficiently. Internet-based commerce is subject to increasing regulation by federal, state and foreign governments, including in the areas of data privacy and breaches, and taxation. Laws and regulations relating to the solicitation, collection, processing or use of personal or consumer information could affect our customers’ ability to use and share data, potentially reducing demand for Internet-based solutions and restricting our ability to store, process, analyze and share data through the Internet. Taxation of services provided over the Internet and governmental restrictions on Internet usage and cloud-based services may be imposed in jurisdictions where we operate. Although we believe that the Internet will continue to provide opportunities to expand the use of our products and services, we cannot ensure that our efforts to exploit these opportunities will be successful or that increased usage of the Internet for business integration products and services or increased competition, taxation and regulation will not adversely affect our business, results of operations and financial condition.

Our growth is dependent upon the continued development of our direct sales force.

We believe that our future growth will depend on the continued development of our direct sales force and its ability to obtain new customers, particularly larger enterprises, and to maintain our existing customer base. Our ability to achieve significant growth in revenue in the future will depend, in large part, on our success in recruiting, training and retaining a sufficient number of direct sales personnel. New sales personnel require significant training and may, in some cases, take more than a year before becoming productive, if at all. If we are unable to hire and develop sufficient numbers of productive direct sales personnel, sales of our products and services will suffer and our growth will be impeded.

We encounter long sales cycles, particularly with our larger customers, and seasonality in sales, which could have an adverse effect on the amount, timing and predictability of our revenue.

Our products have lengthy sales cycles, which typically extend from four to twelve months and may in some instances take longer than one year. Potential and existing customers, particularly larger enterprises, often commit significant resources to an evaluation of available products and services and require us to expend substantial time and resources in connection with our sales efforts. The length of our sales cycles also varies depending on the type of customer to which we are selling, the product being sold and customer requirements. We may incur substantial sales and marketing expenses and expend significant management effort during this time, regardless of whether we make a sale. Many of the risks relating to sales processes are beyond our control, including:

| | · | our customers’ budgetary and scheduling constraints; |

| | · | the timing of our customers’ budget cycles and approval processes; |

| | · | our customers’ willingness to augment or replace their currently deployed software products or to outsource their B2B integration function; and |

| | · | general economic conditions. |

As a result of the lengthy and uncertain sales cycles of our products and services, it is difficult for us to predict when customers may purchase products or services from us, thereby affecting when we can recognize the associated revenue, and our results of operations may vary significantly and may be adversely affected. The length of our sales cycles makes us susceptible to having pending transactions delayed or terminated by our customers if they decide to delay or withdraw funding for IT projects. Our customers may decide to delay or withdraw funding for IT projects for various reasons, many of which are beyond our control, including global economic cycles and capital market fluctuations.

In addition, we may experience seasonality in the sales of our products and services. For instance, historically, the sales we realize in our first fiscal quarter have an aggregate value less than that of the sales we realize in our preceding fourth fiscal quarter. Seasonal variations in our sales may lead to significant fluctuations in our cash flows and deferred revenue on a quarterly basis. If we experience a delay in signing or a failure to sign a significant customer agreement in any particular quarter, then our results of operations for such quarter and for subsequent quarters may be below the expectations of securities analysts or investors, which may materially adversely affect our business.

Business disruptions could adversely affect our business, results of operations and financial condition.

Unexpected events, including natural disasters and severe weather events, could increase the cost of doing business or otherwise harm our business or our customers’ businesses. It is not possible for us to predict the occurrence or consequence of any such events. However, such events could reduce demand for our products and services or make it difficult or impossible for us to deliver our products and services to our customers.

We operate internationally, which exposes us to risks that are difficult to quantify.

Sales of our products and services outside the U.S. are significant. For the year ended December 31, 2012, we derived approximately 40.2% of our total revenues from customers outside of the U.S. Our ability to operate our business internationally in the future will depend upon, among other things, our ability to attract and retain talented and qualified managerial, technical and sales personnel, our ability to sell to customers outside of the U.S. and our ability to continue to manage our international operations. International operations are subject to the risks inherent in doing business abroad, including:

| | · | currency exchange rate fluctuations and changes in the proportion of our revenue and expenses denominated in foreign currencies; |

| | · | unexpected changes in laws, regulatory requirements and enforcement, including with respect to data protection and privacy, and the associated costs of compliance; |

| | · | longer payment cycles for collecting accounts receivable; |

| | · | potentially adverse tax consequences from operating in multiple jurisdictions; |

| | · | potential difficulties in repatriating earnings; |

| | · | political, social and economic instability, including inflation, recession and interest rates and discriminatory fiscal policies; |

| | · | global and regional economic slowdowns; |

| | · | localization of our products and services, including foreign language translation and support; |

| | · | difficulties in staffing and managing foreign operations and other labor problems; |

| | · | seasonal reductions in business activity; |

| | · | multiple regulatory requirements that are subject to change and that could restrict our ability to market or sell our products and services; |

| | · | enforcement of remedies in various jurisdictions; and |

| | · | potential difficulties in protecting intellectual property rights. |

Furthermore, the sale and shipment of products and the sale and provision of services across international borders subject us to extensive U.S. and foreign governmental trade regulations. Compliance with such regulations is costly and exposes us to penalties for non-compliance. Other laws and regulations that can significantly impact us include various anti-bribery laws, such as the U.S. Foreign Corrupt Practices Act and the U.K. Bribery Act, laws restricting business with suspected terrorists and anti-boycott laws. Any failure to comply with applicable legal and regulatory obligations could impact us in a variety of ways that include, but are not limited to, significant criminal, civil and administrative penalties, including imprisonment of individuals, fines and penalties, denial of export privileges, seizure of shipments and restrictions on certain business activities. Also, the failure to comply with applicable legal and regulatory obligations could result in the disruption of our shipping and sales activities.

If the market for our services does not develop or develops more slowly than we expect, our revenue may decline or fail to grow, and we may incur additional operating losses.

Our products and services rely on the acceptance and proliferation of B2B outsourcing and cloud services, which may not be widespread or happen in a timely fashion. Some companies may be reluctant or unwilling to use our products and

services for a number of reasons, including existing investments in services and technology. For example, supply chain management functions traditionally have been performed using purchased or licensed hardware and software implemented by each company in the supply chain. Because this traditional approach often requires significant initial investments to purchase the necessary technology and to establish systems that comply with customers’ unique requirements, suppliers may be unwilling to abandon their current options for our products and services.

Other factors that may limit market acceptance of our solutions include:

| | · | our ability to maintain high levels of customer satisfaction; |

| | · | our ability to maintain availability of service across all users of our products; |

| | · | the price, performance and availability of competing products; |

| | · | our ability to address confidentiality concerns about information stored outside of our customers’ controlled computing environments; and |

| | · | concerns about data protection and confidentiality of data processed or stored in the United States, for customers with headquarters or operations outside of the United States. |

If companies do not perceive or value the benefits of our products and services, or if companies are unwilling to accept our platform as an alternative to the traditional approach, the market for our products and services might not continue to develop or might develop more slowly than we expect, either of which would materially adversely affect our revenue and growth prospects.

Because we operate internationally, our results of operations will be affected by currency fluctuations.

Although the U.S. dollar is our reporting currency, a significant portion of our business is conducted in currencies other than the U.S. dollar, including but not limited to the Euro, British pound, Brazilian real, Japanese yen, Indian rupee, Philippine peso, and Canadian dollar. As a result, we must translate our overseas assets, liabilities, revenues and expenses into U.S. dollars at the then-applicable exchange rates. Approximately 40.2% of our consolidated revenue in 2012 was attributable to operations in non-U.S. dollar countries and translated into the U.S. dollar for reporting purposes. As a consequence, period-to-period changes in the average exchange rate in a particular currency versus the U.S. dollar can significantly affect reported revenue, costs and, to a lesser degree, operating results. In general, appreciation of the U.S. dollar relative to another currency has a negative effect on reported results of operations, while depreciation of the U.S. dollar has a positive effect, although such effects may be short term in nature. We continually monitor our exposure to currency risk; however we have no foreign currency hedging instruments in place. (See the section captioned “Foreign Currency Risk” within “Item 7A—Quantitative and Qualitative Disclosures about Market Risk.”)

We may experience product failures or other problems with new products, all of which could adversely impact our business.

Software products and application-based services as complex as those we offer may contain undetected errors or failures when first introduced or when new versions are released. If software errors are discovered after introduction, our software licensees may seek to assert claims of liability. We also could experience delays or lost revenues during the period required to correct the errors or loss of, or delay in, market acceptance, which could have a material adverse effect on our business, results of operations and financial condition.

We rely on intellectual property and proprietary rights to maintain our competitive position and, therefore, our failure to protect adequately our intellectual property and proprietary rights could adversely affect our business.