Exhibit 99.7

January 2025 Presentation to Spirit

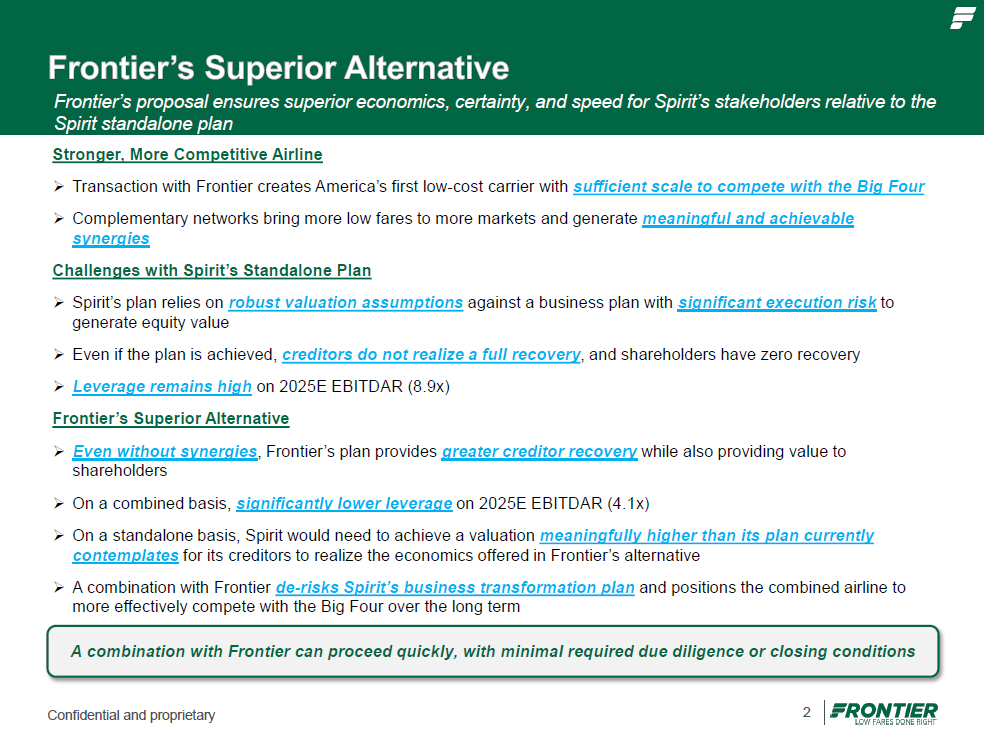

2 Confidential and proprietary Frontier’s proposal ensures superior economics, certainty, and speed for Spirit’s stakeholders relative to the Spirit standalone plan Stronger, More Competitive Airline » Transaction with Frontier creates America’s first low - cost carrier with sufficient scale to compete with the Big Four » Complementary networks bring more low fares to more markets and generate meaningful and achievable synergies Challenges with Spirit’s Standalone Plan » Spirit’s plan relies on robust valuation assumptions against a business plan with significant execution risk to generate equity value » Even if the plan is achieved, creditors do not realize a full recovery , and shareholders have zero recovery » Leverage remains high on 2025E EBITDAR (8.9x) Frontier’s Superior Alternative » Even without synergies , Frontier’s plan provides greater creditor recovery while also providing value to shareholders » On a combined basis, significantly lower leverage on 2025E EBITDAR (4.1x) » On a standalone basis, Spirit would need to achieve a valuation meaningfully higher than its plan currently contemplates for its creditors to realize the economics offered in Frontier’s alternative » A combination with Frontier de - risks Spirit’s business transformation plan and positions the combined airline to more effectively compete with the Big Four over the long term A combination with Frontier can proceed quickly, with minimal required due diligence or closing conditions

Strategic Ra ti ona l e • Compelling industrial logic • Creates the first formidable low - cost challenger to the Big Four • Combination benefits all stakeholders

4 Confidential and proprietary Providing More Stable Career Prospects for Team Members • Provides better career opportunities with increasing complexity and scope • Brings together two cohesive and customer - focused cultures Compelling Proposal to Acquire Spirit To Create America’s First At - Scale, Low - Cost Competitor to Big Four Creating a Stronger Airline with Long - Term Viability to Compete More Effectively • 5 th largest U.S. airline , growing to 100M annual passengers and 400+ aircraft within a few years • Top three carrier in more than half of the top 25 U.S. airports • Meaningfully increases presence in numerous major U.S. markets Offering More Low Fares and Premium Options to Travelers • Provides more low fares to more consumers , enabling billions in savings compared to prices charged by Big Four • Improves frequent flyer and loyalty programs as well as a more diversified product with premium options • Enables more reliable service through operating efficiencies • Enhances travel experience for customers Delivering Value for Financial Stakeholders • Creates compelling financial opportunity for Spirit creditors and shareholders • Provides greater value and recovery relative to Spirit standalone restructuring plan Significant Synergy Potential • Opportunity to participate in upside potential from owning a larger, more competitive airline with estimated synergies of $600M+

5 Unite d A m eri c a n De lta S o u t hwe s t F ront i e r + S pi r it P F A la s k a / J et B lu e S p i r i t F ront i e r A llegiant Hawaiian Stronger Airline with Long - Term Viability to Compete Against Big Four Frontier + Spirit C o m bin e d 5th largest U.S. airline , growing to 100M annual passengers and 400+ aircraft within a few years Top three carrier in more than half of the top 25 U.S. airports Consumers Win: Low Fares with Premium Options 2023 Available Seat Miles » Provides more low fares to more consumers, enabling billions in savings compared to prices charged by Big Four » Improves frequent flyer and loyalty programs as well as a more diversified product with premium options » Enables more reliable service through operating efficiencies » Enhances travel experience for customers Source: Company filings. Confidential and proprietary

6 Confidential and proprietary Consumers & Communities • Offers more low fares to more consumers across a meaningfully increased presence in the U.S., offering significant network connections • Creates thousands of new markets and enables customers to save billions compared to prices charged by the Big Four • Improves loyalty and frequent flyer programs to offer a diversified product and offer an enhanced travel experience with more reliable service • Creates America’s first low - cost carrier with sufficient scale to compete with the Big Four Team M em b ers • Creates more sustainable career opportunities for frontline team members as part of a more stable, faster growing airline • Brings together two cohesive and customer - focused cultures Stakeholders • Delivers meaningful value for financial stakeholders of both Frontier and Spirit • Creates a compelling financial opportunity for Spirit creditors and shareholders through a transaction more favorable than the current proposed Plan of Reorganization • Opportunity to participate in upside potential from owning a larger, more competitive airline with estimated synergies of $600M+

C o m pa ri ng the Plans • Across any reasonable set of assumptions, Frontier’s alternative provides more value to Spirit’s stakeholders • Significant chance of impairment for Spirit stakeholders under standalone plan at more reasonable valuation assumptions • Frontier’s alternative provides value to the common shareholders who receive zero otherwise under the standalone plan • Synergies with Frontier are known , credible , and substantiated by historical precedents, helping derisk recovery values

8 Confidential and proprietary Source: Spirit Disclosure Statement (Chapter 11 Plan of Reorganization), filed as of December 18, 2024. Notes: Spirit RSA and Frontier Proposal reflect $350mm equity rights offering. Recovery rates for senior secured notes and convertible notes are based on principal value and share of equity rights offering. Recovery rates exclude impact from other secured / priority claims. (1) Figures include $600mm of run - rate synergies. (2) Net leverage reflects net debt as of 02/28/2025 divided by 2025E Pro forma EBITDAR incl. 50% credit for synergies. (3) Reflects Spirit equity ownership split of 76% senior secured noteholders, 24% convertible notes. (4) Illustrative equity ownership split of 65% senior secured noteholders, 30% convertible notes, 5% common stock. (5) Per share figures based on Spirit basic shares outstanding as of November 14, 2024; rounded to the nearest $0.05. ($ in millions) Spirit Standalone Restructuring Frontier Proposal Creditor Consideration $400 $840 Exit Secured Notes 11.0% Cash / 8.0% Cash + 4.0% PIK (specifics to be discussed) 11.0% Cash / 8.0% Cash + 4.0% PIK Coupon 19.0% of PF Frontier + Spirit 100% of Spirit % Ownership Frontier + Spirit Spirit Pro Forma Entity $11,059 $5,411 Revenue (FY26) $3,476 (1) $1,041 EBITDAR (FY26) $9,356 $5,937 Net Debt (2/28/2025) 4.1x 8.9x Net Leverage (2) $600 -- Run - Rate Synergies es the same valuation $13,161 irit’s standalone plan $806 Frontier’s proposal us assumptions as Sp Equity Value (@ 6.5x EBITDAR FY26 per RSA Plan) $2,901 $1,646 Total Value to Stakeholders Recovery % (4) (Incl. Synergies) Recovery % (4) (Excl. Synergies) Recovery % (3) Recovery 141% 106% 95% Senior Secured Notes 137% 100% 56% Convertible Notes $1.15 / share $0.80 / share $0.00 / share Common Stock (5)

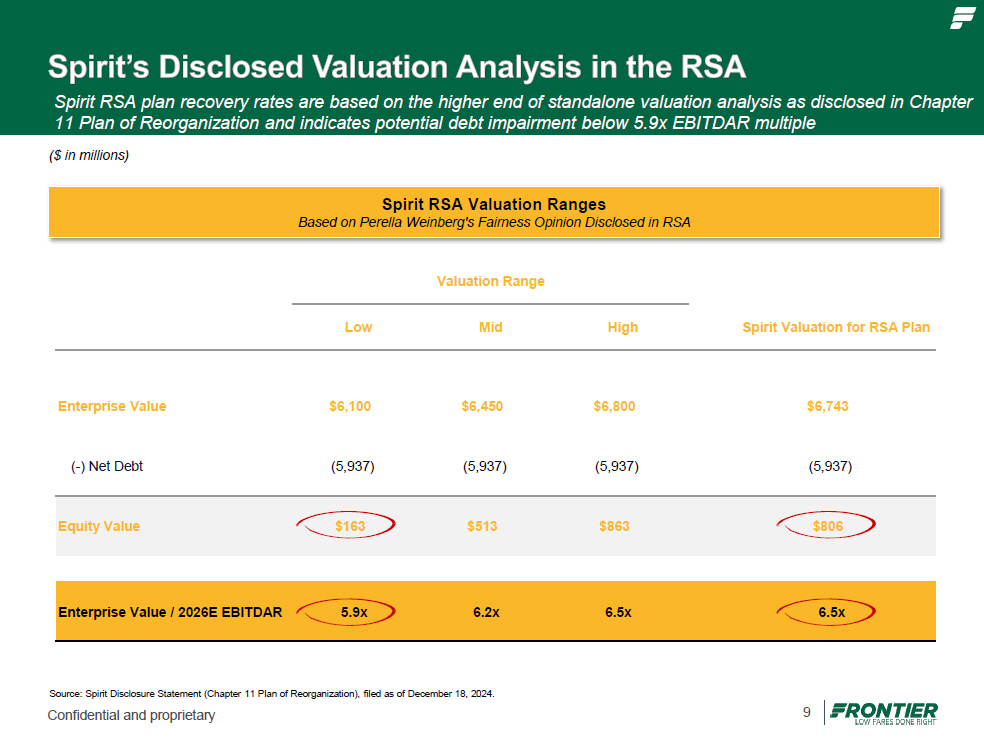

9 Spirit RSA Valuation Ranges Based on Perella Weinberg's Fairness Opinion Disclosed in RSA Spirit RSA plan recovery rates are based on the higher end of standalone valuation analysis as disclosed in Chapter 11 Plan of Reorganization and indicates potential debt impairment below 5.9x EBITDAR multiple ($ in millions) Valuation Range Spirit Valuation for RSA Plan High Mid Low $6,743 $6,800 $6,450 $6,100 Enterprise Value (5,937) (5,937) (5,937) ( 5,937) ( - ) Net Debt $806 $863 $513 $163 Equity Value 6.5x 6.5x 6.2x 5.9x Enterprise Value / 2026E EBITDAR Source: Spirit Disclosure Statement (Chapter 11 Plan of Reorganization), filed as of December 18, 2024. Confidential and proprietary

10 Confidential and proprietary Spirit Standalone Restructuring As of 02/28/2025, $840mm Exit Secured Notes Frontier Proposal (Excluding Synergies) $400mm Exit Secured Notes; 19.0% Ownership to Spirit; $1,835mm Frontier EBITDAR Frontier Proposal (Incl. $600mm of Synergies) $400mm Exit Secured Notes; 19.0% Ownership to Spirit; $1,835mm Frontier EBITDAR At the same valuation multiples as Spirit RSA analysis; Frontier Proposal creates significantly greater value than Spirit Standalone Restructuring Plan ($ in millions); FY26 EBITDAR Multiples Source: Spirit Disclosure Statement (Chapter 11 Plan of Reorganization), filed as of December 18, 2024. Notes: Spirit RSA and Frontier Proposal reflect $350mm equity rights offering. Recovery rates for senior secured notes and convertible notes are based on principal value and share of equity rights offering. Recovery rates exclude impact from other secured / priority claims. (1) Median industry multiple based on Southwest Airlines, JetBlue Airways, Frontier Airlines, Allegiant, and Sun Country Airlines. 4.1x Spirit Standalone Frontier + Spirit Net Leverage Net Debt as of 02/28/2025 divided by FY25 EBITDAR 8.9x Equity Value Exit Secured Notes -- $539 $700 Equity Interest -- -- $613 Sr. Secured Sr. Secured Noteholders -- $539 $1,313 % Recovery -- 39% 95% Exit Secured Notes -- $89 $140 Equity Interest -- -- $194 Convert Convertible Noteholders -- $89 $334 % Recovery -- 15% 56% Equity Value Valuation Multiple 4.5x 5.5x 6.5x $3,586 $6,462 $9,274 Exit Secured Notes $333 $333 $333 Equity Interest $442 $796 $1,142 Sr. Secured Sr. Secured Noteholders $775 $1,129 $1,475 % Recovery 56% 81% 106% Exit Secured Notes $67 $67 $67 Equity Interest $206 $371 $532 Convert Convertible Noteholders $272 $437 $599 % Recovery 45% 73% 100% Valuation Multiple 6.5x 5.5x 4.5x $13,161 $9,762 $6,286 Equity Value Exit Secured Notes $333 $333 $333 Equity Interest $774 $1,202 $1,620 Sr. Secured Sr. Secured Noteholders $1,107 $1,535 $1,954 % Recovery 80% 111% 141% Exit Secured Notes $67 $67 $67 Equity Interest $361 $560 $755 Convert Convertible Noteholders $427 $627 $822 % Recovery 71% 105% 137% Frontier Median (1) RSA Plan Valuation Multiple 4.5x 5.5x 6.5x -- -- $806

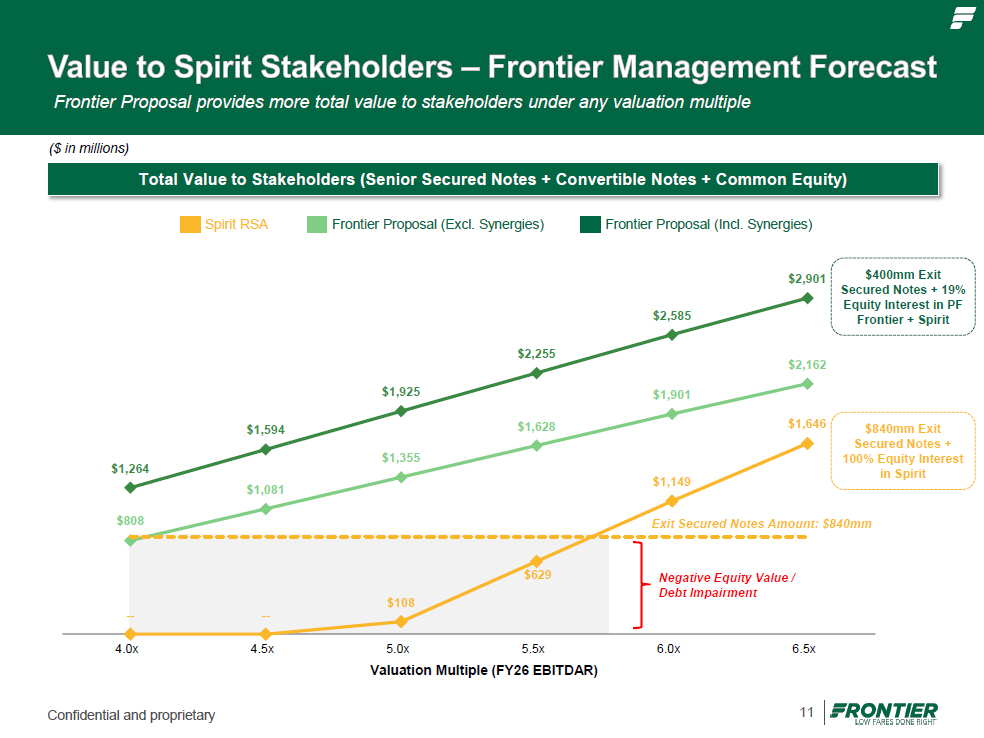

11 Confidential and proprietary Spirit RSA Frontier Proposal (Excl. Synergies) Frontier Proposal (Incl. Synergies) $840mm Exit Secured Notes + 100% Equity Interest in Spirit $400mm Exit Secured Notes + 19% Equity Interest in PF Frontier + Spirit ($ in millions) Total Value to Stakeholders (Senior Secured Notes + Convertible Notes + Common Equity) -- $108 $629 $1,149 $1,646 $808 $1,081 $1,355 $1,628 $1,901 $2,162 $1,264 $1,594 $1,925 $2,255 $2,585 $2,901 Exit Secured Notes Amount: $840mm -- 4. 0x 4. 5x 6. 0x 6. 5x 5.0x 5.5x Valuation Multiple (FY26 EBITDAR) Negative Equity Value / Debt Impairment Frontier Proposal provides more total value to stakeholders under any valuation multiple

Analysis Based on Analyst Es ti ma t es • Even using conservative estimates, the Frontier proposal provides significantly more value than the standalone plan • Net leverage at emergence is 4.2x less for the combined company than standalone (8.9x Standalone vs. 4.7x Pro Forma) • Noteholders have potential to recover 100 % of value when factoring in synergies • Even at lower end of valuation range, equity holders receive positive recovery

13 Confidential and proprietary Spirit Standalone Restructuring As of 02/28/2025, $840mm Exit Secured Notes Frontier Proposal (Incl. $600mm of Synergies) $400mm Exit Secured Notes; 19.0% Ownership to Spirit; $1,251mm Frontier EBITDAR Even under more conservative analyst estimates, the Frontier Proposal creates significantly greater value than Spirit Standalone Restructuring Plan in almost every scenario ($ in millions); FY26 EBITDAR Multiples Source: Spirit Disclosure Statement (Chapter 11 Plan of Reorganization), filed as of December 18, 2024. Frontier analyst estimates based on FactSet consensus as of January 24, 2025. Notes: Spirit RSA and Frontier Proposal reflect $350mm equity rights offering. Recovery rates for senior secured notes and convertible notes are based on principal value and share of equity rights offering. Recovery rates exclude impact from other secured / priority claims. (1) Median industry multiple based on Southwest Airlines, JetBlue Airways, Frontier Airlines, Allegiant, and Sun Country Airlines. RSA Plan Frontier Median (1) Valuation Multiple 4 . 5 x 5 . 5 x 6 . 5x Equity Value -- -- $806 Exit Secured Notes -- $539 $700 Equity Interest -- -- $613 Sr. Secured Sr. Secured Noteholders -- $539 $1,313 % Recovery -- 39% 95% Exit Secured Notes -- $89 $140 Equity Interest -- -- $194 Convert Convertible Noteholders -- $89 $334 % Recovery -- 15% 56% Valuation Multiple 4 . 5 x 5 . 5 x 6 . 5x Equity Value $3,658 $6,550 $9,378 Exit Secured Notes $333 $333 $333 Equity Interest $450 $806 $1,155 Sr. Secured Sr. Secured Noteholders $784 $1,140 $1,488 % Recovery 57% 82% 107% Exit Secured Notes $67 $67 $67 Equity Interest $210 $376 $538 Convert Convertible Noteholders $277 $443 $605 % Recovery 46% 74% 101%

14 Confidential and proprietary $840mm Exit Secured Notes + 100% Equity Interest in Spirit $400mm Exit Secured Notes + 19% Equity Interest in PF Frontier + Spirit Negative Equity Value / Debt Impairment Spirit RSA Frontier Proposal (Incl. Synergies) Frontier Proposal provides more total value to stakeholders except in the unlikely scenario where no synergies are realized and pro forma valuation multiple is greater than 6.1x ($ in millions) Total Value to Stakeholders (Senior Secured Notes + Convertible Notes + Common Equity) -- -- $108 $629 $1,646 $820 $1,095 $1,370 $1,645 $1,919 $2,182 $1,149 Take - Back Debt Amount:$840mm 4. 0x 4. 5x 6. 0x 6. 5x 5.0x 5.5x Valuation Multiple (FY26 EBITDAR)

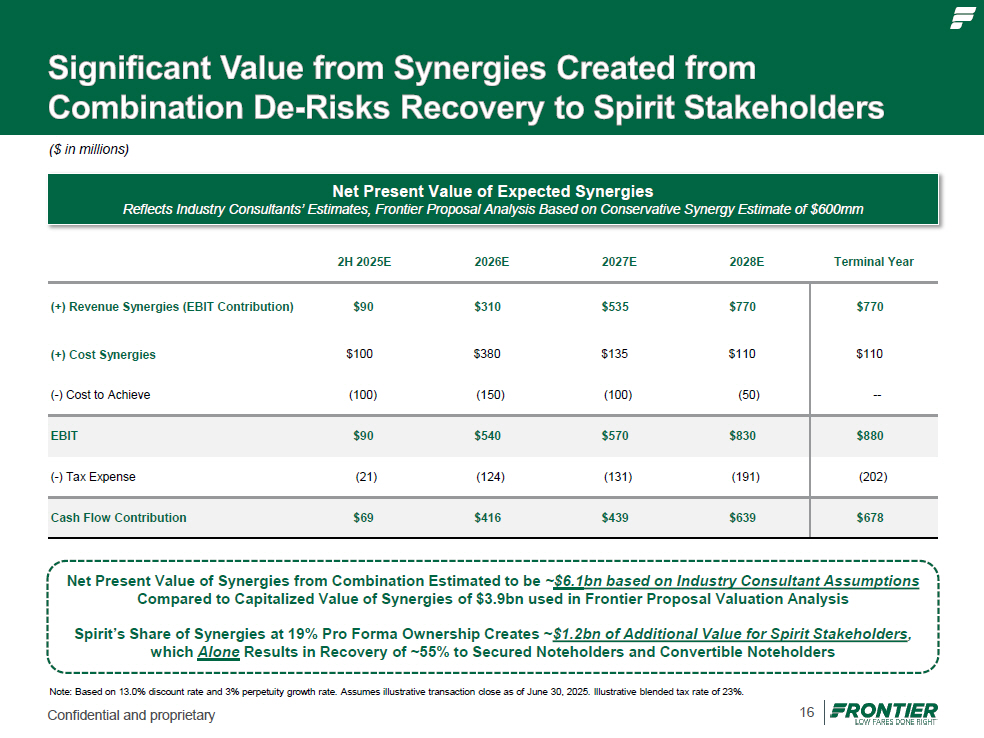

S i gn ifi ca n t Synergy Potential • Assumed synergies of $600mm is a conservative metric compared to credible industry consultants’ estimates • Net present value of synergies from combination forecast to be ~$5.7bn based on industry consultants’ assumptions

16 Confidential and proprietary ($ in millions) Net Present Value of Expected Synergies Reflects Industry Consultants’ Estimates, Frontier Proposal Analysis Based on Conservative Synergy Estimate of $600mm $770 $770 $535 $310 $90 (+) Revenue Synergies (EBIT Contribution) $110 $110 $135 $380 $100 (+) Cost Synergies -- (50) (100) (150) (100) ( - ) Cost to Achieve $880 $830 $570 $540 $90 EBIT (202) (191) (131) (124) (21) ( - ) Tax Expense $678 $639 $439 $416 $69 Cash Flow Contribution 2H 2025E 2026E 2027E 2028E Terminal Year Net Present Value of Synergies from Combination Estimated to be ~ $6.1bn based on Industry Consultant Assumptions Compared to Capitalized Value of Synergies of $3.9bn used in Frontier Proposal Valuation Analysis Spirit’s Share of Synergies at 19% Pro Forma Ownership Creates ~ $1.2bn of Additional Value for Spirit Stakeholders , which Alone Results in Recovery of ~55% to Secured Noteholders and Convertible Noteholders Note: Based on 13.0% discount rate and 3% perpetuity growth rate. Assumes illustrative transaction close as of June 30, 2025. Illustrative blended tax rate of 23%.

Next Steps • Minimal confirmatory due diligence required • Transaction can proceed towards an expedited announcement

18 Confidential and proprietary • Given extensive diligence conducted to date, Frontier envisions an expedited due diligence process that may be completed in approximately 5 - 10 days • Key diligence items include : – Sales performance relative to plan – Confirmation of latest Pratt & Whitney agreement – Updated 2 - year cash flow forecast, inclusive of Chapter 11 costs – Disclosure of any material contract or business changes – Tax considerations, including any Chapter 11 impact to NOLs