As filed with the Securities and Exchange Commission on August 8, 2014

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22727

The Cushing MLP Infrastructure Fund

(Exact name of registrant as specified in charter)

8117 Preston Road, Suite 440 Dallas, TX 75225

(Address of principal executive offices) (Zip code)

Jerry V. Swank

8117 Preston Road, Suite 440 Dallas, TX 75225

(Name and address of agent for service)

214-692-6334

Registrant's telephone number, including area code

Date of fiscal year end: November 30

Date of reporting period: May 31, 2014

Item 1. Reports to Stockholders.

THE CUSHING® MLP INFRASTRUCTURE FUND

SEMI-ANNUAL REPORT

MAY 31, 2014 (Unaudited)

| The Cushing® MLP Infrastructure Fund | |

| TABLE OF CONTENTS | |

| | | |

| | | |

| | Unitholder Letter | 1 |

| | | |

| | Allocation of Portfolio Assets | 5 |

| | | |

| | Schedule of Investments | 6 |

| | | |

| | Statement of Assets and Liabilities | 8 |

| | | |

| | Statement of Operations | 9 |

| | | |

| | Statement of Changes in Net Assets | 10 |

| | | |

| | Statement of Cash Flows | 11 |

| | | |

| | Financial Highlights | 12 |

| | | |

| | Notes to Financial Statements | 13 |

| | | |

| | Additional Information | 17 |

| | | |

| | Board Approval of Investment Management Agreement | 19 |

The Cushing® MLP Infrastructure Fund

UNITHOLDER LETTER

Dear Fellow Unitholder,

For the six month fiscal period ended May 31, 2014, the Cushing® MLP Infrastructure Fund delivered a 22.0% total return, versus total return of 7.6% for the S&P 500 Index (Total Return).

The broader domestic equity market, as measured by the performance of the S&P 500 Index, as well as master limited partnerships (“MLPs”) specifically, performed well during the period. This followed the “taper-tantrum” which began in mid-2013 and negatively affected equities, particularly interest rate sensitive equity subsectors (such as REITs, utilities, and to a much lesser extent, MLPs). Contrary to many market pundits’ beliefs, the U.S. 10-year Treasury yield declined from a high of approximately 3% in December 2013 to below 2.5% by the end of May 2014. Absent one-time weather-related impacts in the calendar first quarter of 2014, the economy continued to perform reasonably well, supporting equity performance.

Overall fundamentals for MLPs continued to be generally positive, and the current and planned infrastructure build-out remained robust and active. Recent key themes that impacted MLPs during the period included: 1) continuing supply takeaway announcements such as new long-haul Bakken crude pipelines, a significant ethane export terminal project, numerous natural gas pipeline project proposals related to Marcellus/Utica takeaway, government clarification on condensate eligible for export and a change in the process for U.S. Department of Energy approval of planned non-Free Trade Agreement (“FTA”) liquefied natural gas (“LNG”) export projects; 2) mergers and acquisition activity and strategic restructurings, including several “drop-down” transactions and proposals for MLP consolidation; 3) initial public offerings and the ongoing “MLP-ification” trend (assets moving into MLP structures), including an important announcement by an energy “major” to form an MLP; and 4) positive fund flows into MLP-focused investment products.

A number of factors affected the Fund’s performance during the reporting period. In particular, the Fund benefited from overweight positions and favorable stock selection in the Natural Gas Gatherers and Processors, Natural Gas Transportation and Storage, Crude Oil and Refined Products, and General Partnerships (“GP”) subsectors. Specifically, the Fund benefitted from several “drop-down” MLPs within these subsectors. Three of the top five contributors for the six month period ending May 31, 2014 included Phillips 66 Partners LP (NYSE: PSXP), EQT Midstream Partners LP (NYSE: EQM) and MPLX LP (NYSE: MPLX), which are the underlying MLPs of their respective C-Corp. sponsors Phillips 66 (NYSE: PSX), EQT Corp (NYSE: EQT) and Marathon Petroleum Corp (NYSE: MPC). These MLPs benefit from predominately fixed fee contracts and visible growth opportunities driven by “drop-down” acquisitions from their respective sponsor, or “parent.”

Three stocks negatively contributed to performance for the period ending May 31, 2014. These included MarkWest Energy Partners LP (NYSE: MWE), Kinder Morgan Energy Partners LP (NYSE: KMP) and Alliance Holdings GP LP (NYSE: AHGP). For MWE, disappointing guidance and concerns regarding the returns on its Marcellus growth backlog hindered performance in the first half of the year; however, we remain positive on the story and current valuation and have taken the opportunity to increase exposure to the name. KMP experienced volatility in the period related to negative comments from a 3rd party research group as well as negative news articles in Barron’s. We disagree with several of the assertions made in these releases and continue to view Kinder as a core holding for the portfolio, particularly given its attractively positioned natural gas pipeline assets. Although minor, AHGP did negatively contribute to performance for the period. While we continue to believe Alliance is the best positioned coal company with a best in class management team, we decided to exit our position during the quarter as a result of poor trading liquidity and continued punitive regulations for the coal industry.

MLPs exposed to the build-out of crude oil infrastructure continued to benefit from the U.S. energy “Renaissance.” U.S. onshore crude oil production was significant for the period, which we believe not only supported continued volume growth for crude oil-levered MLPs, but also provided a wealth of infrastructure investment opportunities in order to satisfy producers’ needs to get their product to market.

Overall, we seek to strike an appropriate balance of investing the Fund’s assets in stable, higher yielding MLPs with lower yielding, high growth MLPs. Additionally, we generally seek to avoid outsized positions in any single name and prefer MLP equities with good trading liquidity.

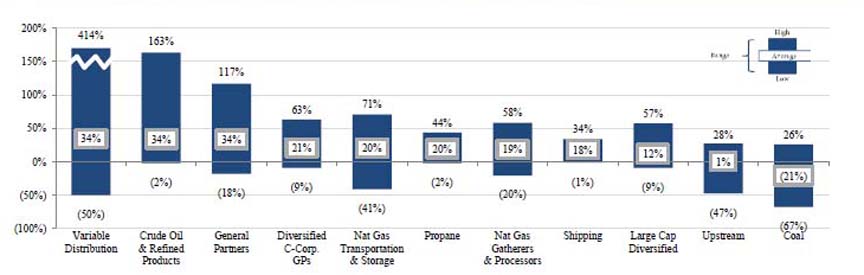

Solid MLP fundamentals contributed positive performance almost across the board as measured by the subsector averages. However, company/subsector specific issues and heightened investor scrutiny led to increased return dispersions within each subsector, as illustrated by the chart below. We believe this dispersion continues to underscore the importance of stock selection in the current MLP environment.

| Last Twelve Months Dispersion of Stock Performance By and Within Subsectors |

|

1) Depicts average, highest and lowest price return of constituents for each subsector for the period from June 1, 2013 through May 31, 2014. 2) Represents price performance only, does not include effect of distributions. 3) Source: Bloomberg. Based on universe of all publicly traded MLPs. |

Industry Overview and Themes

We want to stress that while the midstream industry continues to evolve in a dramatic fashion, what remains the same is that shifting dynamics create both challenges and opportunities for individual MLPs (which we refer to as the “haves” and the “have-nots”).

Energy Infrastructure Development Continues at a Rapid Pace. North American hydrocarbon production has disrupted traditional energy flow patterns and overwhelmed end use demand in many regional markets. The energy sector has responded proactively with large-scale infrastructure projects by midstream operators underpinned by capacity commitments and sales agreements from the upstream and downstream segments. A key example of this coordinated effort is the rapid development of natural gas transportation projects in the Marcellus and Utica shale plays, with nearly every major regional pipeline undertaking expansions and reversals as exploration and production (E&P) companies rush to secure takeaway capacity. Significant open seasons have been announced by Kinder Morgan Energy Partners (NYSE: KMP), Williams Partners LP (NYSE: WPZ), Boardwalk Pipeline Partners LP (NYSE: BWP), Equitable Midstream Partners LP (NYSE: EQM), Spectra Energy Partners LP (NYSE: SEP), Energy Transfer Partners LP (NYSE: ETP) and others.

The industry has also seen regulatory and project developments impacting the export landscape, which will provide a critical outlet valve for domestic production. Most notably, in late May 2014 the U.S. Department of Energy proposed a change to its authorization process for non-FTA LNG exports that would streamline approvals for projects that have completed a critical review by the U.S. Federal Energy Regulatory Commission. In April 2014, Enterprise Products Partners, LP (NYSE: EPD) announced the first large-scale U.S ethane export project, which, according to EPD, is expected to add 240,000 barrels per day (bpd) of natural gas liquids (NGL) export capacity.

On the crude oil front, the U.S. Department of Commerce recently issued a Commodity Classification Decision (CCD) confirming that lease condensate which has gone through a stabilization process is eligible for export. While the initial impact is likely small, this development could potentially help alleviate light oil saturation on the Gulf Coast and provide incremental project and service opportunities for certain midstream operators. In the Bakken shale, the industry may be closer to a large scale crude pipeline with recent open season announcements by ETP and EPD.

M&A and Restructurings Help Fuel Momentum. Several MLPs and their general partners announced sizeable M&A transactions, drop-down acquisitions and corporate restructurings during the first half of the year. Notable transactions include the $1.8 billion offer by ETP for Susser Petroleum Partners, LP (NYSE: SUSP). SUSP operates wholesale and retail fuel distribution businesses. Ultimately, we believe the benefit of this transaction and subsequent drop-downs will accrue to ETP’s parent and general partner, Energy Transfer Equity, LP (NYSE: ETE), which remains a top holding of the Fund.

In the biggest transaction of the year to date, Williams Companies, Inc. (NYSE: WMB) agreed to acquire the remaining 50% interest of Access Midstream Partners, LP’s (NYSE: ACMP) general partner as well a 27% limited partner interest in ACMP for $6 billion. The complete details of the transaction are complex, but upon completion, it will result in WMB dropping its last remaining operating assets into Williams Partners, LP (NYSE: WPZ), thereby becoming a “pure-play” general partnership, as well as accomplishing a reverse merger of WPZ into ACMP. We believe this will ultimately result in WPZ being one of the largest diversified midstream MLPs in the space.

IPOs and the Continued “MLP-ification” of the Energy Sector. Although the year-to-date pace of new MLP IPOs in 2014 has been slower than recent history, the sector saw the largest initial public offering to-date (based on asset size) with Enable Midstream Partners LP (NYSE: ENBL) raising approximately $500 million in April 2014. Energy assets continue to gravitate to the MLP structure as operators seek to maximize shareholder value by carving out portions of their operations and housing them in the tax advantaged MLP structure. For example, in April 2014, Westlake Chemical Corp (NYSE: WLK) announcing the planned offering for a proposed MLP, Westlake Chemical Partners, LP, consisting of ethylene production and pipeline assets, which would be the first of its kind. In addition to, numerous energy companies have filed or discussed the potential for an MLP carve-out including Dominion Resources, Inc. (NYSE: D) and Hess Corporation (NYSE: HES). We will continue to monitor the IPO landscape for strategic opportunities.

Open-end Mutual Fund Flows Provide Further Tailwind. Similar to 2013, asset flows into MLP-focused products continue to provide a positive tailwind to the MLP asset class. According to U.S. Capital Advisors, the calendar year five months ending May 2014 saw record inflows of $5.4 billion into U.S. MLP-focused open-end mutual funds, including an all-time record monthly inflow of $1.4 billion in April. Additionally, asset flows into Exchange Traded Funds (ETFs) and Exchange Traded Notes (ETNs) also continued to be healthy, raising approximately ~$1.9 billion on a cumulative basis for the five months ending May 2014.1 We continue to closely monitor these inflows as we believe this has been a significant contributor to strong performance in the MLP space.

This supply of new capital was matched reasonably well by the demand for capital from MLPs. According to a recent report by Wells Fargo2, MLPs raised $8.5 billion in equity and $20.3 billion in debt year-to-date through May 2014. MLPs are increasingly using at-the-market (ATM) equity distribution programs, which allows companies to efficiently issue equity into the secondary market on an as/when needed basis, minimizing market disruption and partially satisfying capital funding needs. According to the Wells Fargo report, approximately $942 million was raised through ATM programs calendar year-to-date. In short, the capital markets remained healthy and “wide open” for the asset class.

1 “USCA MLP Fund Flows May ‘14.” U.S. Capital Advisors, LLC. June 5, 2014. 2 Source: “MLP Monthly: May 2014.” Wells Fargo Securities Equity Research. June 5, 2014.

Closing

We remain convinced that the U.S. MLP midstream sector is in the early stages of a structural expansion cycle at the center of the U.S. Energy Renaissance, providing the critical link between the rapidly shifting patterns of hydrocarbon production and consumption. We recently traveled to the Texas Gulf Coast, including Freeport and Sweeny, to witness the expansion first hand, and found that the overall activity levels surpassed even our own expectations. We continue to seek to position the Fund to capitalize on the key midstream MLP themes enabling or benefitting from the Renaissance through careful stock selection. We believe there are favorable investment opportunities for the Fund over the balance of the year and that the MLP space will benefit from continued distribution growth, M&A and drop-down transactions and sustained institutional fund flows.

We at Swank Capital, LLC and Cushing® Asset Management, LP truly appreciate your support, and we look forward to continuing to help you achieve your investment goals.

Sincerely,

Jerry V. Swank

Chairman and Chief Executive Officer

The information in this report is not a complete analysis of every aspect of any market, sector, industry, security or the Fund itself. Statements of fact are from sources considered reliable, but the Fund makes no representation or warranty as to their completeness or accuracy. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. Please refer to the Schedule of Investments for a complete list of Fund holdings.

Past performance does not guarantee future results. An investment in the Fund involves risks. The Fund is nondiversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. The Fund will invest in Master Limited Partnerships (MLPs), which concentrate investments in the natural resource sector and are subject to the risks of energy prices and demand and the volatility of commodity investments. Damage to facilities and infrastructure of MLPs may significantly affect the value of an investment and may incur environmental costs and liabilities due to the nature of their business. MLPs are subject to significant regulation and may be adversely affected by changes in the regulatory environment. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. MLPs are subject to certain risks inherent in the structure of MLPs, including complex tax structure risks, the limited ability for election or removal of management, limited voting rights, potential dependence on parent companies or sponsors for revenues to satisfy obligations, and potential conflicts of interest between partners, members and affiliates. There is a risk to the future viability of the ongoing operation of MLPs that return investor’s capital in the form of distributions.

This performance update, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any security, which may be made only by means of a private placement memorandum which contains a description of material terms and risks.

The S&P 500 Index is an unmanaged index of common stocks that is frequently used as a general measure of stock market performance. The index does not include fees or expenses. It is not possible to invest directly in an index.

The Cushing® MLP Infrastructure Fund |

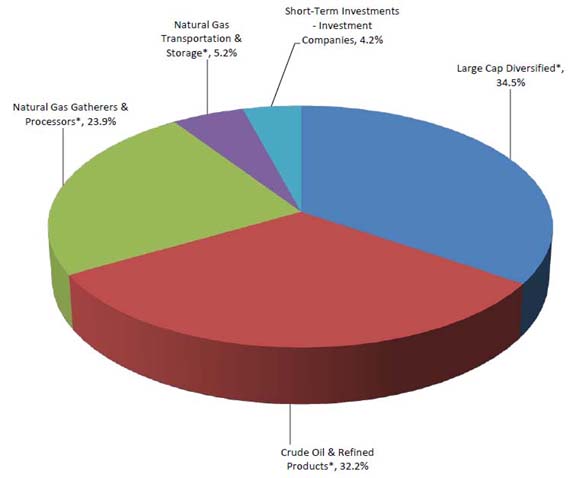

ALLOCATION OF PORTFOLIO ASSETS (1) |

| May 31, 2014 (Unaudited) |

| (Expressed as a Percentage of Total Investments) |

(1) Fund holdings and sector allocations are subject to change and there is no assurance that the Fund will continue to hold any particular security.

* Master Limited Partnerships and Related Companies

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund | | | | | | |

| SCHEDULE OF INVESTMENTS (Unaudited) | | | | | | |

| | | | |

| | | May 31, 2014 | |

| | | | | | | |

| | | Shares | | | Fair Value | |

Master Limited Partnerships and Related Companies - 97.0% (1) | | | | | | |

Crude Oil & Refined Products - 32.6% (1) | | | | | | |

United States - 32.6% (1) | | | | | | |

| Buckeye Partners, L.P. | | | 13,075 | | | $ | 1,025,864 | |

| Enable Midstream Partners, L.P. | | | 32,650 | | | | 829,310 | |

| Genesis Energy, L.P. | | | 24,800 | | | | 1,413,600 | |

| MPLX, L.P. | | | 29,300 | | | | 1,674,788 | |

| NuStar Energy L.P. | | | 21,475 | | | | 1,245,980 | |

| Phillips 66 Partners, L.P. | | | 29,000 | | | | 1,755,950 | |

| Rose Rock Midstream, L.P. | | | 21,144 | | | | 918,284 | |

| Sunoco Logistics Partners, L.P. | | | 18,825 | | | | 1,731,900 | |

| Tesoro Logistics, L.P. | | | 15,700 | | | | 1,094,290 | |

| | | | | | | | 11,689,966 | |

| | | | | | | | | |

Large Cap Diversified - 34.9% (1) | | | | | | | | |

United States - 34.9% (1) | | | | | | | | |

| Enbridge Energy Partners, L.P. | | | 18,150 | | | | 562,650 | |

| Energy Transfer Equity, L.P. | | | 18,150 | | | | 2,323,776 | |

| Energy Transfer Partners, L.P. | | | 26,275 | | | | 1,479,808 | |

| Enterprise Products Partners, L.P. | | | 27,800 | | | | 2,079,996 | |

| Kinder Morgan Energy Partners, L.P. | | | 15,725 | | | | 1,195,886 | |

| Magellan Midstream Partners, L.P. | | | 22,650 | | | | 1,854,582 | |

| ONEOK Partners, L.P. | | | 9,950 | | | | 548,245 | |

| Plains All American Pipeline, L.P. | | | 26,575 | | | | 1,500,690 | |

| Williams Partners, L.P. | | | 17,825 | | | | 946,686 | |

| | | | | | | | 12,492,319 | |

Natural Gas Gatherers & Processors - 24.2% (1) | | | | | | | | |

United States - 24.2% (1) | | | | | | | | |

| Access Midstream Partners, L.P. | | | 28,100 | | | | 1,770,019 | |

| Boardwalk Pipeline Partners, L.P. | | | 60,600 | | | | 1,059,894 | |

| DCP Midstream Partners, L.P. | | | 19,025 | | | | 1,021,833 | |

| Enlink Midstream Partners, L.P. | | | 33,850 | | | | 1,031,409 | |

| MarkWest Energy Partners, L.P. | | | 20,875 | | | | 1,293,206 | |

| Targa Resources Partners, L.P. | | | 14,975 | | | | 1,017,701 | |

| Western Gas Partners, L.P. | | | 20,534 | | | | 1,478,243 | |

| | | | | | | | 8,672,305 | |

Natural Gas Transportation & Storage - 5.3% (1) | | | | | | | | |

United States - 5.3% (1) | | | | | | | | |

| EQT Midstream Partners, L.P. | | | 22,975 | | | | 1,887,167 | |

| | | | | | | | 1,887,167 | |

| | | | | | | | | |

| Total Master Limited Partnerships and Related Companies (Cost $23,628,262) | | | | | | $ | 34,741,757 | |

| | | | | | | | | |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund | | | | | | | | |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) | | | | | | | | |

| | | | | | | | | |

| | | May 31, 2014 | |

| | | | | | | | | |

| | | Shares | | | Fair Value | |

Short-Term Investments - Investment Companies - 4.3% (1) | | | | | | | | |

United States - 4.3% (1) | | | | | | | | |

AIM Short-Term Treasury Portfolio Fund - Institutional Class, 0.01% (2) | | | 305,993 | | | $ | 305,993 | |

Fidelity Government Portfolio Fund - Institutional Class, 0.01% (2) | | | 305,993 | | | | 305,993 | |

Fidelity Money Market Portfolio - Institutional Class, 0.05% (2) | | | 305,992 | | | | 305,992 | |

First American Government Obligations Fund - Class Z, 0.01% (2) | | | 305,992 | | | | 305,992 | |

Invesco STIC Prime Portfolio, 0.01% (2) | | | 305,992 | | | | 305,992 | |

| Total Short-Term Investments (Cost $1,529,962) | | | | | | $ | 1,529,962 | |

| | | | | | | | | |

Total Investments - 101.3% (1) (Cost $25,158,224) | | | | | | $ | 36,271,719 | |

Liabilities in Excess of Other Assets - (1.3)% (1) | | | | | | | (465,392 | ) |

Total Net Assets Applicable to Common Unitholders - 100.0% (1) | | | | | | $ | 35,806,327 | |

| | | | | | | | | |

| | | | | | | | | |

| (1) | Calculated as a percentage of net assets applicable to common unitholders. |

| (2) | Rate reported is the current yield as of May 31, 2014. |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund | | | |

| STATEMENT OF ASSETS & LIABILITIES (Unaudited) | | | |

| | | | | |

| | | | | |

| | | May 31, 2014 |

| Assets | | | | |

| Investments at fair value (cost $25,158,224) | $ | 36,271,719 | |

| Other assets | | | 4,676 | |

| Total assets | | | 36,276,395 | |

| | | | | |

| Liabilities | | | | |

| Subscriptions received in advance | | 350,000 | |

| Payable to Adviser, net of waiver | | 30,200 | |

| Accrued expenses | | | 59,868 | |

| Other payables | | | 30,000 | |

| Total liabilities | | | 470,068 | |

| Net assets | | $ | 35,806,327 | |

| | | | | |

| Net Assets Consisting of | | | | |

| Additional paid-in capital | | $ | 18,709,383 | |

| Accumulated net investment income | | 2,497,659 | |

| Accumulated realized gain | | 3,485,790 | |

| Net unrealized appreciation on investments | | 11,113,495 | |

| Net assets | | $ | 35,806,327 | |

| | | | | |

| Net Asset Value, 32,252.67 units outstanding | $ | 1,110.18 | |

| | | | | |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund | | | |

| STATEMENT OF OPERATIONS (Unaudited) | | | |

| | | | | |

| | | | | |

| | | Period From December 1, 2013 Through May 31, 2014 |

| Investment Income | | | | |

Distribution income | | $ | 686,809 | |

| Interest income | | | 164 | |

| Total Investment Income | | 686,973 | |

| | | | | |

| Expenses | | | | |

| Advisory fees | | | 152,329 | |

| Administrator fees | | | 28,759 | |

| Professional fees | | | 22,500 | |

| Fund accounting fees | | | 15,837 | |

| Custodian fees and expenses | | 4,630 | |

| Transfer agent fees | | | 3,008 | |

| Trustees' fees | | | 1,500 | |

| Registration fees | | | 1,099 | |

| Other expenses | | | 13,353 | |

| Total Expenses | | | 243,015 | |

| Less: expense reimbursement by Adviser, net | | (7,042) | |

| Net Expenses | | | 235,973 | |

| Net Investment Income | | | 451,000 | |

| | | | | |

| | | | | |

| Realized and Unrealized Gain on Investments | | | |

| Net realized gain on investments | | 1,050,156 | |

| Net change in unrealized appreciation of investments | | 4,887,940 | |

| Net Realized and Unrealized Gain on Investments | | 5,938,096 | |

| Increase in Net Assets Resulting from Operations | $ | 6,389,096 | |

| | | | | |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund | | | | | | |

| STATEMENTS OF CHANGES IN NET ASSETS | | | | | | |

| | | | | | | |

| | | | | | | |

| | | Period From December 1, 2013 Through May 31, 2014 | | | Year Ended November 30, 2013 | |

| | | (Unaudited) | | | | |

| Operations | | | | | | |

| Net investment income | | $ | 451,000 | | | $ | 820,473 | |

Net realized gain on investments | | | 1,050,156 | | | | 1,896,691 | |

| Net change in unrealized appreciation of investments | | | 4,887,940 | | | | 4,362,963 | |

| Net increase in net assets resulting from operations | | | 6,389,096 | | | | 7,080,127 | |

| Dividends and Distributions to Common Unitholders | | | | | | | | |

| Net investment income | | | - | | | | - | |

| Return of capital | | | (643,490 | ) | | | (1,130,066 | ) |

| Total dividends and distributions to common unitholders | | | (643,490 | ) | | | (1,130,066 | ) |

| Capital Share Transactions (Note 7) | | | | | | | | |

| Proceeds from unitholder subscriptions | | | 2,051,991 | | | | 4,244,668 | |

| Distribution reinvestments | | | 239,835 | | | | 648,299 | |

| Payments for redemptions | | | (237,567 | ) | | | (1,948,418 | ) |

| Net increase in net assets from capital share transactions | | | 2,054,259 | | | | 2,944,549 | |

| Total increase in net assets | | | 7,799,865 | | | | 8,894,610 | |

| Net Assets | | | | | | | | |

| Beginning of period | | | 28,006,462 | | | | 19,111,852 | |

| End of period | | $ | 35,806,327 | | | $ | 28,006,462 | |

| Accumulated net investment income at the end of the period | | $ | 2,497,659 | | | $ | 2,046,659 | |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund |

| STATEMENT OF CASH FLOWS | |

| | | | |

| | | | |

| | | Period From December 1, 2013 Through May 31, 2014 | |

| OPERATING ACTIVITIES | | (Unaudited) | |

| | | | |

| Increase in Net Assets Resulting from Operations | | $ | 6,389,096 | |

| Adjustments to reconcile increase in net assets resulting from operations | | | | |

| to net cash used in operating activities | | | | |

| Net realized gain on sales of investments | | | (1,050,156 | ) |

| Net change in unrealized appreciation of investments | | | (4,887,940 | ) |

| Purchases of investments in securities | | | (4,581,476 | ) |

| Proceeds from sales of investments in securities | | | 2,985,033 | |

| Purchases of short-term investments | | | (624,371 | ) |

| Changes in operating assets and liabilities | | | | |

| Other assets | | | 17,402 | |

| Payable to Adviser, net of waiver | | | 15,362 | |

| Accrued expenses and other payables | | | (23,719 | ) |

| Net cash used in operating activities | | | (1,760,769 | ) |

| FINANCING ACTIVITIES | | | | |

| Proceeds from issuance of units, net of contributed securities | | | 2,401,991 | |

| Payments for redemptions of units | | | (237,567 | ) |

| Distributions paid | | | (403,655 | ) |

| Net cash provided by financing activities | | | 1,760,769 | |

| DECREASE IN CASH | | | - | |

| | | | | |

| CASH: | | | | |

| Beginning of period | | | - | |

| End of period | | $ | - | |

| | | | | |

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW AND NON-CASH INFORMATION | |

| Distribution reinvestment | | $ | 239,835 | |

| | | | | |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund | | | | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS | | | | | | | | | | | | | | | |

| | | Period From December 1, 2013 through May 31, 2014 | | | Year Ended November 30, 2013 | | | Year Ended November 30, 2012 | | | Year Ended November 30, 2011 | | | Period From March 1, 2010 (1) through November 30, 2010 | | |

| | | (Unaudited) | | | | | | | | | | | | | | |

Per Unit Data (2) | | | | | | | | | | | | | | | | |

| Net Asset Value, beginning of | | | | | | | | | | | | | | | | |

| period | | $ | 927.42 | | | $ | 723.54 | | | $ | 662.02 | | | $ | 619.78 | | | $ | 500.00 | | |

| Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 14.53 | | | | 28.01 | | | | 28.29 | | | | 29.24 | | | | 17.60 | | |

| Net realized and unrealized | | | | | | | | | | | | | | | | | | | | | |

| gain on investments | | | 189.41 | | | | 214.92 | | | | 69.18 | | | | 43.66 | | | | 102.18 | | |

Total increase from investment operations | | | 203.94 | | | | 242.93 | | | | 97.47 | | | | 72.90 | | | | 119.78 | | |

| Less Distributions: | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | - | | | | - | | | | - | | | | - | | | | - | | |

| Return of capital | | | (21.18 | ) | | | (39.05 | ) | | | (35.95 | ) | | | (30.66 | ) | | | - | | |

Total distributions to common stockholders | | | (21.18 | ) | | | (39.05 | ) | | | (35.95 | ) | | | (30.66 | ) | | | - | | |

| Net Asset Value, end of period | | $ | 1,110.18 | | | $ | 927.42 | | | $ | 723.54 | | | $ | 662.02 | | | $ | 619.78 | | |

| | | | | | | | | | | | | | | | | | | | | | |

Total Investment Return (3) | | | 22.0 | % | (4) | | 33.6 | % | | | 14.7 | % | | | 12.0 | % | | | 24.0% | (4) |

| Supplemental Data and Ratios | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period | | $ | 35,806,327 | | | $ | 28,006,462 | | | $ | 19,111,852 | | | $ | 12,137,783 | | | $ | 4,892,232 | | |

| | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average | | | | | | | | | | | | | | | | | | | | | |

net assets before waiver (5) | | | 1.5 | % | | | 1.9 | % | | | 1.8 | % | | | 1.6 | % | | | 7.5 | | % |

| | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average | | | | | | | | | | | | | | | | | | | | | |

net assets after waiver (5) | | | 1.5 | % | | | 1.5 | % | | | 1.2 | % | | | 1.0 | % | | | 1.0 | | % |

| | | | | | | | | | | | | | | | | | | | | | |

| Ratio of net investment | | | | | | | | | | | | | | | | | | | | | |

| income (loss) to average net | | | | | | | | | | | | | | | | | | | | | |

assets before waiver (5) | | | 2.8 | % | | | 2.8 | % | | | 3.4 | % | | | 4.0 | % | | | (2.2 | ) | % |

| | | | | | | | | | | | | | | | | | | | | | |

| Ratio of net investment | | | | | | | | | | | | | | | | | | | | | |

| income (loss) to average net | | | | | | | | | | | | | | | | | | | | | |

assets after waiver (5) | | | 2.8 | % | | | 3.2 | % | | | 4.0 | % | | | 4.6 | % | | | 4.3 | | % |

| | | | | | | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 9.76 | % | (4) | | 36.69 | % | | | 122.64 | % | | | 129.02 | % | | | 28.32% | (4) |

| (1) Commencement of operations. | | | | | | | |

| (2) Information presented relates to a unit outstanding for the entire period. |

| (3) Individual returns and ratios may vary based on the timing of capital transactions. |

| (4) Not annualized. | | | | | | | | |

| (5) All income and expenses are annualized for periods less than one full year . |

| | | | | | | | | | | | |

See Accompanying Notes to the Financial Statements.

The Cushing® MLP Infrastructure Fund

NOTES TO FINANCIAL STATEMENTS

May 31, 2014 (Unaudited)

The Cushing® MLP Infrastructure Fund (the "Fund"), was organized as a Delaware statutory trust pursuant to an agreement and declaration of trust dated January 15, 2010 (the “Declaration of Trust”). The Fund’s investment objective is to seek to produce current income and capital appreciation. The Fund commenced operations on March 1, 2010. Effective August 1, 2012, the Fund registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940. The Fund is managed by Cushing® Asset Management, LP (the “Adviser”).

| 2. | Significant Accounting Policies |

A. Basis of Presentation

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”) as detailed in the Financial Accounting Standards Board’s Accounting Standards Codification.

B. Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, recognition of distribution income and disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

C. Investment Valuation

The Fund uses the following valuation methods to determine fair value as either fair value for investments for which market quotations are available, or if not available, the fair value, as determined in good faith pursuant to such policies and procedures as may be approved by the Fund’s Board of Trustees (“Board of Trustees” or “Trustees”) from time to time. The valuation of the portfolio securities of the Fund currently includes the following processes:

(i) The fair value of each security listed or traded on any recognized securities exchange or automated quotation system will be the last reported sale price at the relevant valuation date on the composite tape or on the principal exchange on which such security is traded. If no sale is reported on that date, the Adviser utilizes, when available, pricing quotations from principal market markers. Such quotations may be obtained from third-party pricing services or directly from investment brokers and dealers in the secondary market.

(ii) The Fund’s non-marketable investments will generally be valued in such manner as the Adviser determines in good faith to reflect their fair values under procedures established by, and under the general supervision and responsibility of, the Board of Trustees. The pricing of all assets that are fair valued in this manner will be subsequently reported to and ratified by the Board of Trustees.

D. Security Transactions, Investment Income and Expenses

Security transactions are accounted for on the date the securities are purchased or sold (trade date). Realized gains and losses are reported on a specific identified cost basis. Interest income is recognized on an accrual basis. Distributions are recorded on the ex-dividend date. Distributions received from the Fund’s investments in master limited partnerships (“MLPs”) generally are comprised of ordinary income, capital gains and return of capital. The Fund records investment income on the ex-date of the distributions. These distributions are included in Distribution Income on the Statement of Operations.

Expenses are recorded on an accrual basis.

E. Dividends and Distributions to Unitholders

Dividends and distributions to unitholders are recorded on the ex-dividend date. The character of dividends and distributions to unitholders are comprised of 100 percent return of capital.

F. Federal Income Taxation

The Fund is treated as a partnership for Federal income tax purposes. Accordingly, no provision for Federal income taxes is reflected in the accompanying financial statements. The Fund does not record a provision for U.S. federal, state, or local income taxes because the unitholders report their share of the Fund’s income or loss on their income tax returns. The Fund files an income tax return in the U.S. federal jurisdiction, and may file income tax returns in various U.S. states. Generally, the Fund is subject to income tax examinations by major taxing authorities for all tax years since its inception.

In accordance with GAAP, the Fund is required to determine whether its tax positions are more likely than not to be sustained upon examination by the applicable taxing authority, based on the technical merits of the position. The tax benefit recognized is measured as the largest amount of benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement with the relevant taxing authorities. Based on its analysis, the Fund has determined that it has not incurred any liability for unrecognized tax benefits as of May 31, 2014. The Fund does not expect that its assessment regarding unrecognized tax benefits will materially change over the next twelve months. However, the Fund’s conclusions may be subject to review and adjustment at a later date based on factors including, but not limited to, questioning the timing and amount of deductions, the nexus of income among various tax jurisdictions, compliance with U.S. federal and U.S. state and foreign tax laws, and changes in the administrative practices and precedents of the relevant taxing authorities.

The difference between book basis and tax basis is attributable primarily to net unrealized appreciation on investments. The tax basis of the Fund’s investments as of May 31, 2014 was $25,158,224 and net unrealized appreciation was $11,113,495 (gross unrealized appreciation $11,189,096; gross unrealized depreciation $75,601).

G. Cash Flow Information

The Fund makes distributions from investments, which include the amount received as cash distributions from MLPs and common stock dividends. These activities are reported in the Statement of Changes in Net Assets, and additional information on cash receipts, payments and contributed securities is presented in the Statement of Cash Flows.

H. Indemnifications

Under the Fund’s organization documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund may enter into contracts that provide general indemnification to other parties. The Fund’s maximum exposure under such indemnification arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred, and may not occur.

| 3. | Concentrations of Risk |

The Fund’s investment objective is to seek a high level of after-tax total return, with an emphasis on current distributions to common unitholders. The Fund seeks to achieve its investment objective by investing, under normal market conditions, in MLPs.

In the normal course of business, substantially all of the Fund’s securities transactions, money balances, and security positions are transacted with the Fund’s custodian, U.S. Bank, N.A. The Fund is subject to credit risk to the extent any broker with whom it conducts business is unable to fulfill contractual obligations on its behalf. The Adviser monitors the financial conditions of such brokers.

| 4. | Agreements and Related Party Transactions |

The Fund has entered into an Investment Management Agreement (the “Agreement”) with the Adviser. Under the terms of the Agreement, the Fund pays the Adviser a management fee, calculated and payable monthly in advance, equal to 0.083% (1.0% per annum) of the net assets of the Fund determined as of the beginning of each calendar month for services and facilities provided by the Adviser to the Fund.

For the period ended May 31, 2014, the Adviser has agreed to waive a portion of its management fee and reimburse Fund expenses such that Fund operating expenses will not exceed 1.50%. For the period ended May 31, 2014, the Adviser earned $152,329 in advisory fees and waived fees and reimbursed Fund expenses in the amount of $7,042.

Waived fees and reimbursed Fund expenses, including prior year expenses, are subject to potential recovery by year of expiration. The Adviser’s waived fees and reimbursed expenses that are subject to potential recovery are as follows:

| Fiscal Year Incurred | | Amount Reimbursed | | | Amount Recouped | | | Amount Subject to Potential Recovery | | Expiration Date |

| November 30, 2012 | | $ | 42,533 | | | $ | 2,039 | | | $ | 40,494 | | November 30, 2015 |

| November 30, 2013 | | | 107,752 | | | | - | | | | 107,752 | | November 30, 2016 |

| November 30, 2014 | | | 9,081 | | | | - | | | | 9,081 | | November 30, 2017 |

| | | $ | 159,366 | | | $ | 2,039 | | | $ | 157,327 | | |

The Adviser paid for $30,000 of the organizational costs on behalf of the Fund. This is included in Other payables on the statement of assets and liabilities.

Jerry V. Swank, the founder and managing partner of the Adviser, is Chairman of the Fund’s Board of Trustees.

U.S. Bancorp Fund Services, LLC serves as the Fund’s administrator and transfer agent. The Fund pays the administrator a monthly fee computed at an annual rate of 0.07% of the first $100,000,000 of the Fund’s net assets, 0.04% on the next $200,000,000 of net assets and 0.04% on the balance of the Fund’s net assets, with a minimum annual fee of $45,000.

U.S. Bank, N.A. serves as the Fund’s custodian. The Fund pays the custodian a monthly fee computed at an annual rate of 0.004% of the Fund’s average daily market value, with a minimum annual fee of $4,800.

Certain unitholders are affiliated with the Fund. The aggregate value of the affiliated unitholders’ share of net assets at May 31, 2014 is approximately $571,000.

| 5. | Fair Value Measurements |

Various inputs that are used in determining the fair value of the Fund’s investments are summarized in the three broad levels listed below:

| · | Level 1 — quoted prices in active markets for identical securities |

| · | Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| · | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

These inputs are summarized in the three broad levels listed below.

| | | | | | Fair Value Measurements at Reporting Date Using | |

| | | Fair Value at | | | Quoted Prices in Active Markets for Identical Assets | | | Significant Other Observable Inputs | | | Significant Unobservable Inputs | |

| Description | | May 31, 2014 | | | (Level 1) | | | (Level 2) | | | (Level 3) | |

Assets Equity Securities | | | | | | | | | | | | |

Master Limited Partnerships and Related Companies (a) | | $ | 34,741,757 | | | $ | 34,741,757 | | | $ | - | | | $ | - | |

| Total Equity Securities | | | 34,741,757 | | | | 34,741,757 | | | | - | | | | - | |

Other Short-Term Investments | | | 1,529,962 | | | | 1,529,962 | | | | - | | | | - | |

| Total Other | | | 1,529,962 | | | | 1,529,962 | | | | - | | | | - | |

| Total Assets | | $ | 36,271,719 | | | $ | 36,271,719 | | | $ | - | | | $ | - | |

| (a) | All other industry classifications are identified in the Schedule of Investments. The Fund did not hold Level 3 investments at any time during the period ended May 31, 2014. |

During the period ended May 31, 2014, the Fund did not have any transfers between any of the levels of the fair value hierarchy.

| 6. | Investment Transactions |

For the period ended May 31, 2014, the Fund purchased (at cost) and sold securities (proceeds) in the amount of $4,581,476 and $2,985,033 (excluding short-term securities), respectively.

Common units of beneficial interest (“Common Units”) of the Fund may be offered or sold in a private placement to persons who satisfy the suitability standards set forth in the Fund’s confidential offering memorandum. The Fund generally offers Common Units on the first business day of each month. As of May 31, 2014, the Fund had 32,252.67 Common Units outstanding.

The Fund generally intends to pay distributions quarterly, in such amounts as may be determined from time to time by the Fund’s Board of Trustees. Unless a unitholder elects otherwise, distributions, if any, will be automatically reinvested in additional Common Units in the Fund. For the period ended May 31, 2014, the Fund issued 252.44 units through its dividend reinvestment plan.

The Adviser has evaluated the impact of all subsequent events on the Fund.

From June 1, 2014 through July 30, 2014, the Fund accepted additional subscriptions of approximately $620,000 and accepted redemptions of approximately $147,000. On July 17, 2014, the Fund issued a tender offer to repurchase up to 40% of the Fund’s outstanding units as of July 31, 2014.

On June 1, 2014, the Fund issued 120 units through its dividend reinvestment plan.

On June 30, 2014, KPMG LLP (“KPMG”) acquired certain assets of the Fund’s independent auditors, Rothstein Kass. As a result of this transaction, effective as of June 30, 2014, Rothstein Kass resigned as the independent auditors of the Fund. KPMG has indicated its desire to enter into an engagement to serve as the independent auditors of the Fund to the Fund’s Audit Committee. As of the date of this report, KPMG is in the process of its standard client evaluation procedures and has not yet presented a proposal to the Fund’s Board of Trustees. The Trustees will appoint a replacement auditor prior to the end of the Fund’s current fiscal year on November 30, 2014.

The Cushing® MLP Infrastructure Fund

ADDITIONAL INFORMATION (Unaudited)

May 31, 2014

Investment Policies and Parameters

The Commodity Futures Trading Commission (“CFTC”) amended Rule 4.5 which permits investment advisers to registered investment companies to claim an exclusion from the definition of commodity pool operator with respect to a fund provided certain requirements are met. In order to permit the Adviser to continue to claim this exclusion with respect to the Fund under the amended rule, the Fund limits its transactions in futures, options of futures and swaps (excluding transactions entered into for “bona fide hedging purposes,” as defined under CFTC regulations) such that either: (i) the aggregate initial margin and premiums required to establish its futures, options on futures and swaps do not exceed 5% of the liquidation value of the Fund’s portfolio, after taking into account unrealized profits and losses on such positions; or (ii) the aggregate net notional value of its futures, options on futures and swaps does not exceed 100% of the liquidation value of the Fund’s portfolio, after taking into account unrealized profits and losses on such positions. The Fund and the Adviser do not believe that complying with the amended rule will limit the Fund’s ability to use futures, options and swaps to the extent that it has used them in the past.

Trustee and Officer Compensation

The Fund does not currently compensate any of its trustees who are interested persons nor any of its officers. For the period ended May 31, 2014, each Trustee agreed to waive his annual retainer until the Fund’s assets exceed $100 million. During the period ended May 31, 2014, the aggregate compensation paid by the Fund to the independent trustees was $1,500. The Fund did not pay any special compensation to any of its trustees or officers. The Fund continuously monitors standard industry practices and this policy is subject to change. The Fund’s Statement of Additional Information includes additional information about the Trustees and is available, without charge, upon request by calling the Fund toll-free at (877) 653-1415 and on the SEC’s Web site at www.sec.gov.

Cautionary Note Regarding Forward-Looking Statements

This report contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Fund’s historical experience and its present expectations or projections indicated in any forward-looking statements. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; MLP industry risk; leverage risk; valuation risk; interest rate risk; tax risk; and other risks discussed in the Fund’s filings with the SEC. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Fund undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Fund’s investment objectives will be attained.

Proxy Voting Policies

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund and information regarding how the Fund voted proxies relating to the portfolio of securities during the 12-month period ended June 30 will be available to stockholders (i) without charge, upon request by calling the Fund toll-free at (877) 653-1415; and (ii) on the SEC’s Web site at www.sec.gov. The Fund was not registered with the SEC until August 1, 2012, therefore proxy voting information will be made available only from this date forward.

Form N-Q

The Fund files its complete schedule of portfolio holdings for the first and third quarters of each fiscal year with the SEC on Form N-Q. The Fund’s Form N-Q and statement of additional information are available without charge by visiting the SEC’s Web site at www.sec.gov from August 1, 2012 forward. In addition, you may review and copy the Fund’s Form N-Q at the SEC’s Public Reference Room in Washington D.C. You may obtain information on the operation of the Public Reference Room by calling (800) SEC-0330.

Privacy Policy

In order to conduct its business, the Fund collects and maintains certain nonpublic personal information about its stockholders of record with respect to their transactions in shares of the Fund’s securities. This information includes the stockholder’s address, tax identification or Social Security number, share balances, and dividend elections. We do not collect or maintain personal information about stockholders whose share balances of our securities are held in “street name” by a financial institution such as a bank or broker.

We do not disclose any nonpublic personal information about you, the Fund’s other stockholders or the Fund’s former stockholders to third parties unless necessary to process a transaction, service an account, or as otherwise permitted by law.

To protect your personal information internally, we restrict access to nonpublic personal information about the Fund’s stockholders to those employees who need to know that information to provide services to our stockholders. We also maintain certain other safeguards to protect your nonpublic personal information.

Householding

In an effort to decrease costs, the Fund intends to reduce the number of duplicate annual and semi-annual reports, proxy statements and other similar documents you receive by sending only one copy of each to those addresses shared by two or more accounts and to shareholders the Transfer Agent reasonably believes are from the same family or household. Once implemented, if you would like to discontinue householding for your accounts, please contact investor services at investorservices@usbank.com to request individual copies of these documents. Once the Transfer Agent receives notice to stop householding, the Transfer Agent will begin sending individual copies thirty days after receiving your request. This policy does not apply to account statements.

The Cushing® MLP Infrastructure Fund

Board Approval of Investment Management Agreement (Unaudited)

May 31, 2014

On May 21, 2014, the Board of Trustees of the Fund (members of which are referred to collectively as the “Trustees”) met in person to discuss, among other things, the approval of the Investment Management Agreement (the “Agreement”) between the Fund and Cushing® Asset Management, LP (the “Adviser”).

Activities and Composition of the Board

The Board of Trustees is comprised of four Trustees, three of whom are not “interested persons,” as such term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”), of the Fund (the “Independent Trustees”). The Board of Trustees is responsible for the oversight of the operations of the Fund and performs the various duties imposed by the 1940 Act on the trustees of investment companies. The Independent Trustees have retained independent legal counsel to assist them in connection with their duties. Prior to its consideration of the Agreement, the Board of Trustees received and reviewed information provided by the Adviser, including, among other things, comparative information about the fees and expenses and performance of certain other closed-end funds. The Board of Trustees also received and reviewed information responsive to requests from independent counsel to assist it in its consideration of the Agreement. Before the Board of Trustees voted on the approval of the Agreement, the Independent Trustees met with independent legal counsel during executive session and discussed the Agreement and related information.

Consideration of Nature, Extent and Quality of the Services

The Board of Trustees received and considered information regarding the nature, extent and quality of services provided to the Fund under the Agreement. The Board of Trustees reviewed certain background materials supplied by the Adviser in its presentation, including the Adviser’s Form ADV.

The Board of Trustees reviewed and considered the Adviser’s investment advisory personnel, its history as an asset manager and its performance and the amount of assets currently under management by the Adviser. The Board of Trustees also reviewed the research and decision-making processes utilized by the Adviser, including the methods adopted to seek to achieve compliance with the investment objectives, polices and restrictions of the Fund.

The Board of Trustees considered the background and experience of the Adviser’s management in connection with the Fund, including reviewing the qualifications, backgrounds and responsibilities of the management team primarily responsible for the day-to-day portfolio management of the Fund and the extent of the resources devoted to research and analysis of the Fund’s actual and potential investments.

The Board of Trustees also reviewed, among other things, the Adviser’s insider trading policies and procedures and its Code of Ethics. The Board of Trustees, including all of the Independent Trustees, concluded that the nature, extent and quality of services to be rendered by the Adviser under the Agreement were adequate.

Consideration of Advisory Fees and the Cost of the Services

The Board of Trustees reviewed and considered the contractual annual advisory fee to be paid by the Fund to the Adviser in light of the extent, nature and quality of the advisory services to be provided by the Adviser to the Fund.

The Board of Trustees considered the information they received comparing the Fund’s contractual annual advisory fee and overall expenses with (a) a peer group of competitor closed-end funds designated by the Adviser that manage publicly traded portfolios investing primarily in MLPs; and (b) other products managed by the Adviser. Given the small universe of managers and funds fitting within the criteria for the peer group, the Adviser did not believe that it would be beneficial to engage the services of an independent third-party to prepare the peer group analysis, and the Independent Trustees concurred with this approach.

Based on such information, the Board of Trustees noted that the Fund was a continuously offered closed-end fund that conducts periodic tender offers and did not have any identifiable peers or competitors, but that the fee structure of a 1.00% management fee compared favorably against both the open-end and listed closed-end fund peer group.

Consideration of Investment Performance

The Board of Trustees regularly reviews the performance of the Fund throughout the year. The Board of Trustees reviewed performance information comparing the performance of the Fund, net of fees, against benchmark indices and its peer group. The Board of Trustees concluded that the Fund had continued to generally outperform its various indices during the year-to-date, one year and three year periods.

Other Considerations

The Board of Trustees received and considered a historical, current and projected profitability analysis prepared by the Adviser based on the fees payable under the Agreement. The Board of Trustees considered the profits realized and anticipated to be realized by the Adviser in connection with the operation of the Fund and concluded that the profit, if any, anticipated to be realized by the Adviser in connection with the operation of the Fund is not unreasonable to the Fund.

The Board of Trustees considered whether economies of scale in the provision of services to the Fund had been or would be passed along to the shareholders under the Agreement. The Board of Trustees reviewed and considered any other incidental benefits derived or to be derived by the Adviser from its relationship with the Fund, including soft dollar arrangements or other so called “fall-out” benefits. The Board of Trustees concluded there were no material economics of scale or other incidental benefits accruing to the Adviser in connection with its relationship with the Fund.

Conclusion

In approving the Agreement and the fees charged under the Agreement, the Board of Trustees concluded that no single factor reviewed by the Board of Trustees was identified by the Board of Trustees to be determinative as the principal factor in whether to approve the Agreement. The summary set out above describes the most important factors, but not all of the matters, considered by the Board of Trustees in coming to its decision regarding the Agreement. On the basis of such information as the Board of Trustees considered necessary to the exercise of its reasonable business judgment and its evaluation of all of the factors described above, and after much discussion, the Board of Trustees concluded that each factor they considered, in the context of all of the other factors they considered, favored approval of the Agreement. It was noted that it was the judgment of the Board of Trustees that approval of the Agreement was consistent with the best interests of the Fund and its shareholders, and a majority of the Trustees and, voting separately, a majority of the Independent Trustees, approved the Agreement.

Item 2. Code of Ethics.

Not applicable for semi-annual reports.

Item 3. Audit Committee Financial Expert.

Not applicable for semi-annual reports.

Item 4. Principal Accountant Fees and Services.

Not applicable for semi-annual reports.

Item 5. Audit Committee of Listed Registrants.

Not applicable to registrants who are not listed issuers (as defined in Rule 10A-3 under the Securities Exchange Act of 1934).

Item 6. Investments.

| (a) | Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable for semi-annual reports.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable for semi-annual reports.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

| Period | (a) Total Number of Shares (or Units) Purchased | (b) Average Price Paid per Share (or Unit) | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs |

Month #1 12/01/2013-12/31/2013 | 0 | 0 | 0 | 0 |

Month #2 01/01/2014-01/31/2014 | 0 | 0 | 0 | 0 |

Month #3 02/01/2014-02/28/2014 | 0 | 0 | 0 | 0 |

Month #4 03/01/2014-03/31/2014 | 0 | 0 | 0 | 0 |

Month #5 04/01/2014-04/30/2014 | 0 | 0 | 0 | 0 |

Month #6 05/01/2014-05/31/2014 | 0 | 0 | 0 | 0 |

| Total | 0 | 0 | 0 | 0 |

*Footnote the date each plan or program was announced, the dollar amount (or share or unit amount) approved, the expiration date (if any) of each plan or program, each plan or program that expired during the covered period, each plan or program registrant plans to terminate or let expire.

Item 10. Submission of Matters to a Vote of Security Holders.

Not Applicable.

Item 11. Controls and Procedures.

| (a) | The Registrant’s President and Treasurer/Chief Financial Officer have reviewed the Registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940 (the “Act”)) as of a date within 90 days of the filing of this report, as required by Rule 30a-3(b) under the Act and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934. Based on their review, such officers have concluded that the disclosure controls and procedures are effective in ensuring that information required to be disclosed in this report is appropriately recorded, processed, summarized and reported and made known to them by others within the Registrant and by the Registrant’s service provider. |

| (b) | There were no changes in the Registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the Act) that occurred during the second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the Registrant's internal control over financial reporting. |

Item 12. Exhibits.

| (a) | (1) Any code of ethics or amendment thereto, that is the subject of the disclosure required by Item 2, to the extent that the registrant intends to satisfy Item 2 requirements through filing an exhibit. Not Applicable. |

(2) A separate certification for each principal executive and principal financial officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. Filed herewith.

(3) Any written solicitation to purchase securities under Rule 23c-1 under the Act sent or given during the period covered by the report by or on behalf of the registrant to 10 or more persons. Not applicable.

| (b) | Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. Furnished herewith. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

(Registrant) The Cushing MLP Infrastructure Fund

By (Signature and Title) /s/ Daniel L. Spears

Daniel L. Spears, President

Date August 8, 2014

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By (Signature and Title) /s/ Daniel L. Spears

Daniel L. Spears, President

Date August 8, 2014

By (Signature and Title) /s/ John H. Alban

John H. Alban, Treasurer & Chief Financial Officer

Date August 8, 2014