In our view, both midstream master limited partnership (“MLP”) management teams and investors have appropriately recalibrated expectations using realistic commodity price assumptions (i.e. approximately $50/bbl crude). We also think investors have become more comfortable in this environment, assuming the recovery plays out as expected (the consensus is for a modest supply-driven price recovery closer to year-end—but with prices ultimately settling much lower than pre-crash ranges). To be clear, while there are areas of weakness, such as certain natural gas gatherers & processors facing currently very depressed natural gas liquids prices and declining volumes, it is important to recognize that the broad trend for the overall midstream group remains stable. Overall, there appears to be a modest reduction of future expected growth as volumes and projects are in many cases simply “pushed to the right” - in other words, not an absolute reduction of current cash flows.

Importantly, there are parts of the midstream energy industry that may benefit in a lower crude oil price environment. Refined products pipelines systems have traditionally done very well in a supply-driven low crude price environment as consumers are incentivized to purchase more fuel. Crude oil storage and terminalling can benefit as the contango forward curve incentivizes producers and marketers to fully utilize all available storage. Natural gas infrastructure can benefit from robust investment primarily to get record Marcellus/Utica production to new markets in the Northeast and Southeast (e.g. gas powered utility demand) and South for LNG exports. Retail propane and retail fuel margins can also benefit as underlying commodity price drop (cost of goods) is slower to be reflected in the retail price (sales price).

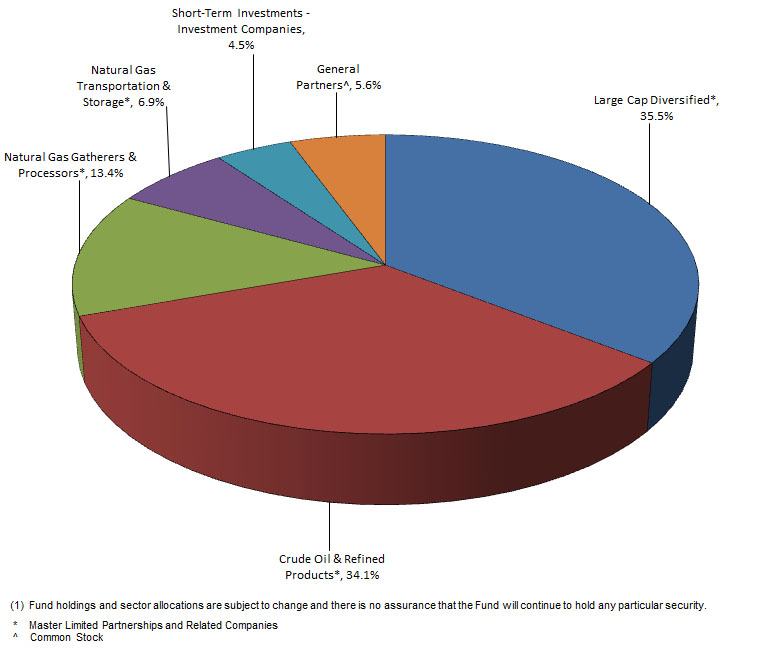

Turning to the Fund’s performance for the period, the Fund benefited from overweight exposure to holdings in the Crude Oil & Refined Products, General Partners and Natural Gas Transportation and Storage subsectors. Portfolio holdings in the Crude Oil & Refined Products subsector contributed the strongest performance in large part due to the outsized actual and estimated distribution growth for its constituents relative to other MLPs. Additionally, this subsector represented the largest average weight for the Fund as well as the largest overweight subsector versus the AMZ during the period.

The Cushing® MLP Infrastructure Fund

NOTES TO FINANCIAL STATEMENTS

May 31, 2015 (Unaudited)

The Cushing® MLP Infrastructure Fund (the "Fund"), was organized as a Delaware statutory trust pursuant to an agreement and declaration of trust dated January 15, 2010 (the “Declaration of Trust”). The Fund’s investment objective is to seek a high level of after-tax total return, with an emphasis on current distributions paid to its unitholders. The Fund commenced operations on March 1, 2010. Effective August 1, 2012, the Fund registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940. The Fund is managed by Cushing® Asset Management, LP (the “Adviser”).

| 2. | Significant Accounting Policies |

A. Basis of Presentation

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”) as detailed in the Financial Accounting Standards Board’s Accounting Standards Codification.

B. Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, recognition of distribution income and disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

C. Investment Valuation

The Fund uses the following valuation methods to determine fair value as either fair value for investments for which market quotations are available, or if not available, the fair value, as determined in good faith pursuant to such policies and procedures as may be approved by the Fund’s Board of Trustees (“Board of Trustees” or “Trustees”) from time to time. The valuation of the portfolio securities of the Fund currently includes the following processes:

(i) The fair value of each security listed or traded on any recognized securities exchange or automated quotation system will be the last reported sale price at the relevant valuation date on the composite tape or on the principal exchange on which such security is traded. If no sale is reported on that date, the Adviser utilizes, when available, pricing quotations from principal market markers. Such quotations may be obtained from third-party pricing services or directly from investment brokers and dealers in the secondary market.

(ii) The Fund’s non-marketable investments will generally be valued in such manner as the Adviser determines in good faith to reflect their fair values under procedures established by, and under the general supervision and responsibility of, the Board of Trustees. The pricing of all assets that are fair valued in this manner will be subsequently reported to and ratified by the Board of Trustees.

D. Security Transactions, Investment Income and Expenses

Security transactions are accounted for on the date the securities are purchased or sold (trade date). Realized gains and losses are reported on a specific identified cost basis. Interest income is recognized on an accrual basis. Distributions are recorded on the ex-dividend date. Distributions received from the Fund’s investments in master limited partnerships (“MLPs”) generally are comprised of ordinary income, capital gains and return of capital. The Fund records investment income on the ex-date of the distributions. These distributions are included in Distribution Income on the Statement of Operations.

Expenses are recorded on an accrual basis.

E. Dividends and Distributions to Unitholders

Dividends and distributions to unitholders are recorded on the ex-dividend date. The character of dividends and distributions to unitholders are comprised of 100 percent return of capital.

F. Federal Income Taxation

The Fund is treated as a partnership for Federal income tax purposes. Accordingly, no provision for Federal income taxes is reflected in the accompanying financial statements. The Fund does not record a provision for U.S. federal, state, or local income taxes because the unitholders report their share of the Fund’s income or loss on their income tax returns.

The Fund files an income tax return in the U.S. federal jurisdiction, and may file income tax returns in various U.S. states. Generally, the Fund is subject to income tax examinations by major taxing authorities for all tax years since its inception.

In accordance with GAAP, the Fund is required to determine whether its tax positions are more likely than not to be sustained upon examination by the applicable taxing authority, based on the technical merits of the position. The tax benefit recognized is measured as the largest amount of benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement with the relevant taxing authorities. Based on its analysis, the Fund has determined that it has not incurred any liability for unrecognized tax benefits as of May 31, 2015. The Fund does not expect that its assessment regarding unrecognized tax benefits will materially change over the next twelve months. However, the Fund’s conclusions may be subject to review and adjustment at a later date based on factors including, but not limited to, questioning the timing and amount of deductions, the nexus of income among various tax jurisdictions, compliance with U.S. federal and U.S. state and foreign tax laws, and changes in the administrative practices and precedents of the relevant taxing authorities.

The difference between book basis and tax basis is attributable primarily to net unrealized appreciation on investments. The tax basis of the Fund’s investments as of May 31, 2015 was $29,060,286 and net unrealized appreciation was $8,496,112 (gross unrealized appreciation $8,832,175; gross unrealized depreciation $336,063).

G. Cash Flow Information

The Fund makes distributions from investments, which include the amount received as cash distributions from MLPs and common stock dividends. These activities are reported in the Statement of Changes in Net Assets, and additional information on cash receipts and payments is presented in the Statement of Cash Flows.

H. Indemnifications

Under the Fund’s organization documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund may enter into contracts that provide general indemnification to other parties. The Fund’s maximum exposure under such indemnification arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred, and may not occur.

| 3. | Concentrations of Risk |

The Fund’s investment objective is to seek a high level of after-tax total return, with an emphasis on current distributions paid to its unitholders. The Fund seeks to achieve its investment objective by investing, under normal market conditions, in MLPs.

In the normal course of business, substantially all of the Fund’s securities transactions, money balances, and security positions are transacted with the Fund’s custodian, U.S. Bank, N.A. The Fund is subject to credit risk to the extent any broker with whom it conducts business is unable to fulfill contractual obligations on its behalf. The Adviser monitors the financial conditions of such brokers.

| 4. | Agreements and Related Party Transactions |

The Fund has entered into an Investment Management Agreement (the “Agreement”) with the Adviser. Under the terms of the Agreement, the Fund pays the Adviser a management fee, calculated and payable monthly in advance, equal to 0.083% (1.0% per annum) of the net assets of the Fund determined as of the beginning of each calendar month for services and facilities provided by the Adviser to the Fund.

For the period ended May 31, 2015, the Adviser agreed to waive a portion of its management fee and reimburse Fund expenses such that Fund operating expenses would not exceed 1.50%. For the period ended May 31, 2015, the Adviser earned $178,597 in advisory fees and waived fees and reimbursed Fund expenses in the amount of $35,802.

Waived fees and reimbursed Fund expenses, including prior year expenses, are subject to potential recovery by year of expiration. The Adviser’s waived fees and reimbursed expenses that are subject to potential recovery are as follows:

| Fiscal Year Incurred | | Amount Reimbursed | | Amount Recouped | | Amount Subject to Potential Recovery | | Expiration Date | |

| November 30, 2012 | | $ 42,533 | | $ 10,487 | | $ 32,046 | | November 30, 2015 | |

| November 30, 2013 | | 107,752 | | - | | 107,752 | | November 30, 2016 | |

| November 30, 2014 | | 21,221 | | - | | 21,221 | | November 30, 2017 | |

| November 30, 2015 | | 35,802 | | - | | 35,802 | | November 30, 2018 | |

| | | $ 207,308 | | $ 10,487 | | $ 196,821 | | | |

U.S. Bancorp Fund Services, LLC serves as the Fund’s administrator and transfer agent. The Fund pays the administrator a monthly fee computed at an annual rate of 0.07% of the first $100,000,000 of the Fund’s net assets, 0.04% on the next $200,000,000 of net assets and 0.04% on the balance of the Fund’s net assets, with a minimum annual fee of $45,000.

U.S. Bank, N.A. serves as the Fund’s custodian. The Fund pays the custodian a monthly fee computed at an annual rate of 0.004% of the Fund’s average daily market value, with a minimum annual fee of $4,800.

Certain unitholders are affiliated with the Fund. The aggregate value of the affiliated unitholders’ share of net assets at May 31, 2015 is approximately $703,000.

| 5. | Fair Value Measurements |

Various inputs that are used in determining the fair value of the Fund’s investments are summarized in the three broad levels listed below:

| · | Level 1 — quoted prices in active markets for identical securities |

| · | Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| · | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

These inputs are summarized in the three broad levels listed below.

| | | Fair Value Measurements at Reporting Date Using |

| | | Fair Value as of | | Quoted Prices in Active Markets for Identical Assets | Significant Other Observable Inputs | Significant Unobservable Inputs |

| | Description | May 31, 2015 | | (Level 1) | (Level 2) | (Level 3) |

| | Assets Equity Securities Common Stock | $ 2,099,394 | | $ 2,099,394 | $ - | $ - |

| | Master Limited Partnerships and Related Companies (a) | 33,786,509 | | 33,786,509 | - | - |

| | Total Equity Securities | 35,885,903 | | 35,885,903 | - | - |

| | Other Short-Term Investments | 1,670,495 | | 1,670,495 | - | - |

| | Total Other | 1,670,495 | | 1,670,495 | - | - |

| | Total Assets | $ 37,556,398 | | $ 37,556,398 | $ - | $ - |

| (a) | All other industry classifications are identified in the Schedule of Investments. The Fund did not hold Level 3 investments at any time during the period ended May 31, 2015. |

During the period ended May 31, 2015, the Fund did not have any transfers between any of the levels of the fair value hierarchy.

| 6. | Investment Transactions |

For the period ended May 31, 2015, the Fund purchased (at cost) and sold securities (proceeds) in the amount of $5,121,361 and $2,663,690 (excluding short-term securities), respectively.

Units of beneficial interest (“Units”) of the Fund may be offered or sold in a private placement to persons who satisfy the suitability standards set forth in the Fund’s confidential offering memorandum. The Fund generally offers Units on the first business day of each month. As of May 31, 2015, the Fund had 34,344.81 Units outstanding.

The Fund generally intends to pay distributions quarterly, in such amounts as may be determined from time to time by the Fund’s Board of Trustees. Unless a unitholder elects otherwise, distributions, if any, will be automatically reinvested in additional Units in the Fund. For the period ended May 31, 2015, the Fund issued 262.35 units through its dividend reinvestment plan.

The Adviser has evaluated the impact of all subsequent events on the Fund.

From June 1, 2015 through July 30, 2015, the Fund accepted additional subscriptions of $350,000 and accepted redemptions of approximately $365,000. On July 15, 2015, the Fund commenced a tender offer to repurchase up to 40% of the Fund’s outstanding units as of July 31, 2015.

On July 1, 2015, the Fund issued 144.19 units through its dividend reinvestment plan.

Effective as of July 1, 2015, the Fund converted to a "master/feeder" structure by contributing substantially all of its investable assets less cash retained by the Fund (the “Transferred Assets”) to The Cushing® MLP Infrastructure Master Fund (the “Master Fund”) in exchange for Master Fund units with an aggregate net asset value equal to the aggregate value of the Transferred Assets. The Fund will pursue its investment objective by investing all or substantially all of its investable assets in the Master Fund The Master Fund is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940 and has the same investment objectives as the Fund.

The Cushing® MLP Infrastructure Fund

ADDITIONAL INFORMATION (Unaudited)

May 31, 2015

Investment Policies and Parameters

The Commodity Futures Trading Commission (“CFTC”) amended Rule 4.5 which permits investment advisers to registered investment companies to claim an exclusion from the definition of commodity pool operator with respect to a fund provided certain requirements are met. In order to permit the Adviser to continue to claim this exclusion with respect to the Fund under the amended rule, the Fund limits its transactions in futures, options of futures and swaps (excluding transactions entered into for “bona fide hedging purposes,” as defined under CFTC regulations) such that either: (i) the aggregate initial margin and premiums required to establish its futures, options on futures and swaps do not exceed 5% of the liquidation value of the Fund’s portfolio, after taking into account unrealized profits and losses on such positions; or (ii) the aggregate net notional value of its futures, options on futures and swaps does not exceed 100% of the liquidation value of the Fund’s portfolio, after taking into account unrealized profits and losses on such positions. The Fund and the Adviser do not believe that complying with the amended rule will limit the Fund’s ability to use futures, options and swaps to the extent that it has used them in the past.

Trustee and Officer Compensation

The Fund does not currently compensate any of its trustees who are interested persons nor any of its officers. During the period ended May 31, 2015, the aggregate compensation paid by the Fund to each independent trustee was $6,647. The Fund did not pay any special compensation to any of its trustees or officers. The Fund continuously monitors standard industry practices and this policy is subject to change. The Fund’s Statement of Additional Information includes additional information about the Trustees and is available, without charge, upon request by calling the Fund toll-free at (877) 653-1415 and on the SEC’s Web site at www.sec.gov.

Cautionary Note Regarding Forward-Looking Statements

This report contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Fund’s historical experience and its present expectations or projections indicated in any forward-looking statements. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; MLP industry risk; leverage risk; valuation risk; interest rate risk; tax risk; and other risks discussed in the Fund’s filings with the SEC. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Fund undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Fund’s investment objectives will be attained.

Proxy Voting Policies

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund and information regarding how the Fund voted proxies relating to the portfolio of securities during the 12-month period ended June 30 will be available to stockholders (i) without charge, upon request by calling the Fund toll-free at (877) 653-1415; and (ii) on the SEC’s Web site at www.sec.gov. The Fund was not registered with the SEC until August 1, 2012, therefore proxy voting information is only made available from this date forward.

Form N-Q

The Fund files its complete schedule of portfolio holdings for the first and third quarters of each fiscal year with the SEC on Form N-Q. The Fund’s Form N-Q and statement of additional information are available without charge by visiting the SEC’s Web site at www.sec.gov from August 1, 2012 forward. In addition, you may review and copy the Fund’s Form N-Q at the SEC’s Public Reference Room in Washington D.C. You may obtain information on the operation of the Public Reference Room by calling (800) SEC-0330.

Privacy Policy

In order to conduct its business, the Fund collects and maintains certain nonpublic personal information about its stockholders of record with respect to their transactions in shares of the Fund’s securities. This information includes the stockholder’s address, tax identification or Social Security number, share balances, and dividend elections. We do not collect or maintain personal information about stockholders whose share balances of our securities are held in “street name” by a financial institution such as a bank or broker.

We do not disclose any nonpublic personal information about you, the Fund’s other stockholders or the Fund’s former stockholders to third parties unless necessary to process a transaction, service an account, or as otherwise permitted by law.

To protect your personal information internally, we restrict access to nonpublic personal information about the Fund’s stockholders to those employees who need to know that information to provide services to our stockholders. We also maintain certain other safeguards to protect your nonpublic personal information.

Householding

In an effort to decrease costs, the Fund intends to reduce the number of duplicate annual and semi-annual reports, proxy statements and other similar documents you receive by sending only one copy of each to those addresses shared by two or more accounts and to shareholders the Transfer Agent reasonably believes are from the same family or household. Once implemented, if you would like to discontinue householding for your accounts, please contact investor services at investorservices@usbank.com to request individual copies of these documents. Once the Transfer Agent receives notice to stop householding, the Transfer Agent will begin sending individual copies thirty days after receiving your request. This policy does not apply to account statements.

The Cushing® MLP Infrastructure Fund

Board Approval of Investment Management Agreement (Unaudited)

May 31, 2015

On May 21, 2015, the Board of Trustees of the Fund (members of which are referred to collectively as the “Trustees”) met in person to discuss, among other things, the approval of the Investment Management Agreement (the “Agreement”) between the Fund and Cushing® Asset Management, LP (the “Adviser”).

Activities and Composition of the Board

The Board of Trustees is comprised of four Trustees, three of whom are not “interested persons,” as such term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”), of the Fund (the “Independent Trustees”). The Board of Trustees is responsible for the oversight of the operations of the Fund and performs the various duties imposed by the 1940 Act on the trustees of investment companies. The Independent Trustees have retained independent legal counsel to assist them in connection with their duties. Prior to its consideration of the Agreement, the Board of Trustees received and reviewed information provided by the Adviser. The Board of Trustees also received and reviewed information responsive to requests from independent counsel to assist it in its consideration of the Agreement. Before the Board of Trustees voted on the approval of the Agreement, the Independent Trustees met with independent legal counsel during executive session and discussed the Agreement and related information.

Consideration of Nature, Extent and Quality of the Services

The Board of Trustees received and considered information regarding the nature, extent and quality of services provided to the Fund under the Agreement. The Board of Trustees reviewed certain background materials supplied by the Adviser in its presentation, including the Adviser’s Form ADV.

The Board of Trustees reviewed and considered the Adviser’s investment advisory personnel, its history as an asset manager and its performance and the amount of assets currently under management by the Adviser. The Board of Trustees also reviewed the research and decision-making processes utilized by the Adviser, including the methods adopted to seek to achieve compliance with the investment objectives, policies and restrictions of the Fund.

The Board of Trustees considered the background and experience of the Adviser’s management in connection with the Fund, including reviewing the qualifications, backgrounds and responsibilities of the management team primarily responsible for the day-to-day portfolio management of the Fund and the extent of the resources devoted to research and analysis of the Fund’s actual and potential investments.

The Board of Trustees also reviewed, among other things, the Adviser’s conflict of interest policies, insider trading policies and procedures and its Code of Ethics. The Board of Trustees, including all of the Independent Trustees, concluded that the nature, extent and quality of services to be rendered by the Adviser under the Agreement were adequate.

Consideration of Advisory Fees and the Cost of the Services

The Board of Trustees reviewed and considered the contractual annual advisory fee to be paid by the Fund to the Adviser in light of the extent, nature and quality of the advisory services to be provided by the Adviser to the Fund.

The Board of Trustees considered the information they received comparing the Fund’s contractual annual advisory fee and overall expenses with (a) a peer group of competitor closed-end funds determined by the Adviser; and (b) other accounts or vehicles managed by the Adviser. Given the small universe of managers and funds fitting within the criteria for the peer group, the Adviser did not believe that it would be beneficial to engage the services of an independent third-party to prepare the peer group analysis, and the Independent Trustees concurred with this approach.

Based on such information, the Board of Trustees determined that the Fund’s management fee and total expense ratio were significantly below the peer group median. The Board of Trustees also concluded that the fees charged by the Adviser to the Fund relative to comparable accounts of the Adviser employing similar strategies were reasonable in light of the differences between the types of clients, the kinds of costs incurred by the Adviser, and other considerations faced by the Adviser in competing for and servicing such clients.

Consideration of Investment Performance

The Board of Trustees regularly reviews the performance of the Fund throughout the year. The Board of Trustees reviewed performance information comparing the performance of the Fund against benchmark indices and its peer group. The Board of Trustees noted that the Fund continued to outperform its benchmark index, with significant outperformance in the 1-year and 3-year periods.

Other Considerations

The Board of Trustees received and considered a profitability analysis prepared by the Adviser based on the fees payable by the Fund under the Agreement. The Board of Trustees considered the profits realized and anticipated to be realized by the Adviser in connection with the operation of the Fund and concluded that the profit, if any, anticipated to be realized by the Adviser in connection with the operation of the Fund is not unreasonable to the Fund.

The Board of Trustees considered whether economies of scale in the provision of services to the Fund had been or would be passed along to the shareholders under the Agreement. The Board of Trustees reviewed and considered any other incidental benefits derived or to be derived by the Adviser from its relationship with the Fund, including soft dollar arrangements or other so called “fall-out benefits.” The Board of Trustees concluded there were no material economies of scale or other incidental benefits accruing to the Adviser in connection with its relationship with the Fund.

Conclusion

In approving the Agreement and the fees charged under the Agreement, the Board of Trustees concluded that no single factor reviewed by the Board of Trustees was identified by the Board of Trustees to be determinative as the principal factor in whether to approve the Agreement. The summary set out above describes the most important factors, but not all of the matters, considered by the Board of Trustees in coming to its decision regarding the Agreement. On the basis of such information as the Board of Trustees considered necessary to the exercise of its reasonable business judgment and its evaluation of all of the factors described above, and after much discussion, the Board of Trustees concluded that each factor they considered, in the context of all of the other factors they considered, favored approval of the Agreement. It was noted that it was the judgment of the Board of Trustees that approval of the Agreement was consistent with the best interests of the Fund and its shareholders. A majority of the Trustees and, voting separately, a majority of the Independent Trustees, approved the Agreement.

The Board of Trustees also considered an amendment to the Agreement (the “Amendment”) to be implemented in connection with the conversion of the Fund to a master/feeder structure, in which the Fund would invest substantially all of its investable assets in The Cushing® MLP Infrastructure Master Fund (the “Master Fund”), a registered closed-end investment company that has the same investment objective and substantially the same investment policies as the Fund. The Amendment provides that for so long as the Fund invests through the Master Fund, the Adviser will not be entitled to any management fee from the Fund with respect to the portion of the Fund’s assets that are so invested. If the Fund does not invest through the Master Fund, the Fund will continue to pay a management fee to the Adviser of 1.00% per annum of the Fund’s Managed Assets payable monthly in arrears. The Board of Trustees determined that approving the Amendment was consistent with the best interests of the Fund and its unitholders.

The Cushing® MLP Infrastructure Master Fund

Board Approval of Investment Management Agreement (Unaudited)

May 31, 2015

On May 21, 2015, the Board of Trustees of The Cushing® MLP Infrastructure Master Fund (the “Master Fund”) (members of which are referred to collectively as the “Trustees”) met in person to discuss, among other things, the approval of the Investment Management Agreement (the “Agreement”) between the Master Fund and Cushing® Asset Management, LP (the “Adviser”).

Activities and Composition of the Board

The Board of Trustees is comprised of four Trustees, three of whom are not “interested persons,” as such term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”), of the Master Fund (the “Independent Trustees”). The Board of Trustees is responsible for the oversight of the operations of the Master Fund and performs the various duties imposed by the 1940 Act on the trustees of investment companies. The Independent Trustees have retained independent legal counsel to assist them in connection with their duties. Prior to its consideration of the Agreement, the Board of Trustees received and reviewed information provided by the Adviser. The Board of Trustees also received and reviewed information responsive to requests from independent counsel to assist it in its consideration of the Agreement. Before the Board of Trustees voted on the approval of the Agreement, the Independent Trustees met with independent legal counsel during executive session and discussed the Agreement and related information.

Consideration of Nature, Extent and Quality of the Services

The Board of Trustees received and considered information regarding the nature, extent and quality of services provided to the Master Fund under the Agreement. The Board of Trustees reviewed certain background materials supplied by the Adviser in its presentation, including the Adviser’s Form ADV.

The Board of Trustees reviewed and considered the Adviser’s investment advisory personnel, its history as an asset manager and its performance and the amount of assets currently under management by the Adviser. The Board of Trustees also reviewed the research and decision-making processes utilized by the Adviser, including the methods adopted to seek to achieve compliance with the investment objectives, policies and restrictions of the Master Fund.

The Board of Trustees considered the background and experience of the Adviser’s management in connection with the Master Fund, including reviewing the qualifications, backgrounds and responsibilities of the management team primarily responsible for the day-to-day portfolio management of the Master Fund and the extent of the resources devoted to research and analysis of the Master Fund’s actual and potential investments.

The Board of Trustees also reviewed, among other things, the Adviser’s conflict of interest policies, insider trading policies and procedures and its Code of Ethics. The Board of Trustees, including all of the Independent Trustees, concluded that the nature, extent and quality of services to be rendered by the Adviser under the Agreement were adequate.

Consideration of Advisory Fees and the Cost of the Services

The Board of Trustees reviewed and considered the contractual annual advisory fee to be paid by the Master Fund to the Adviser in light of the extent, nature and quality of the advisory services to be provided by the Adviser to the Master Fund.

The Board of Trustees considered the information they received comparing the Master Fund’s contractual annual advisory fee and overall expenses with (a) a peer group of competitor closed-end funds determined by the Adviser; and (b) other accounts or vehicles managed by the Adviser. Given the small universe of managers and funds fitting within the criteria for the peer group, the Adviser did not believe that it would be beneficial to engage the services of an independent third-party to prepare the peer group analysis, and the Independent Trustees concurred with this approach.

Based on such information, the Board of Trustees determined that although the peer group was of limited utility because of the significant differences between the Master Fund and the other funds in the peer group, the Master Fund’s proposed management fee and total expense ratio were significantly below the peer group median, and the proposed management fee was identical to the current management fee for The Cushing® MLP Infrastructure Master Fund, which was expected to be converted to a “feeder fund” that would invest substantially all of its investable assets in the Master Fund. The Board noted that under the proposed master/feeder structure, the feeder funds would not pay a management fee to the Adviser. The Board of Trustees also concluded that the fees charged by the Adviser to each fund relative to comparable accounts of the Adviser employing similar strategies were reasonable in light of the differences between the types of clients, the kinds of costs incurred by the Adviser, and other considerations faced by the Adviser in competing for and servicing such clients.

Consideration of Investment Performance

The Board of Trustees regularly reviews the performance of The Cushing® MLP Infrastructure Fund throughout the year. The Board of Trustees reviewed performance information comparing the performance of The Cushing® MLP Infrastructure Fund against benchmark indices and its peer group. The Board of Trustees noted that The Cushing® MLP Infrastructure Fund had outperformed its benchmark index, with significant outperformance in the 1-year and 3-year periods, and the proposed strategy of the Fund would be identical to the current strategy of The Cushing® MLP Infrastructure Fund.

Other Considerations

The Board of Trustees received and considered a profitability analysis prepared by the Adviser based on the fees payable by The Cushing® MLP Infrastructure Fund. The Board noted that under the proposed master/feeder structure, the feeder funds would not pay a management fee to the Adviser. The Board of Trustees considered the profits that could be anticipated to be realized by the Adviser in connection with the operation of the Master Fund and concluded that the profit, if any, anticipated to be realized by the Adviser in connection with the operation of the Master Fund is not unreasonable to the Master Fund.

The Board of Trustees considered whether economies of scale in the provision of services to the Master Fund had been or would be passed along to the shareholders under the Agreement. The Board of Trustees reviewed and considered any other incidental benefits derived or to be derived by the Adviser from its relationship with the Master Fund, including soft dollar arrangements or other so called “fall-out benefits.” The Board of Trustees concluded there were no material economies of scale or other incidental benefits accruing to the Adviser in connection with its relationship with the Master Fund.

Conclusion

In approving the Agreement and the fees charged under the Agreement, the Board of Trustees concluded that no single factor reviewed by the Board of Trustees was identified by the Board of Trustees to be determinative as the principal factor in whether to approve the Agreement. The summary set out above describes the most important factors, but not all of the matters, considered by the Board of Trustees in coming to its decision regarding the Agreement. On the basis of such information as the Board of Trustees considered necessary to the exercise of its reasonable business judgment and its evaluation of all of the factors described above, and after much discussion, the Board of Trustees concluded that each factor they considered, in the context of all of the other factors they considered, favored approval of the Agreement. It was noted that it was the judgment of the Board of Trustees that approval of the Agreement was consistent with the best interests of the Master Fund and its shareholders. A majority of the Trustees and, voting separately, a majority of the Independent Trustees, approved the Agreement.

Item 2. Code of Ethics.

Not applicable for semi-annual reports.

Item 3. Audit Committee Financial Expert.

Not applicable for semi-annual reports.

Item 4. Principal Accountant Fees and Services.

Not applicable for semi-annual reports.

Item 5. Audit Committee of Listed Registrants.

Not applicable to registrants who are not listed issuers (as defined in Rule 10A-3 under the Securities Exchange Act of 1934).

Item 6. Investments.

| (a) | Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable for semi-annual reports.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable for semi-annual reports.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

| Period | (a) Total Number of Shares (or Units) Purchased | (b) Average Price Paid per Share (or Unit) | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs |

Month #1 12/01/2014-12/31/2014* | 0 | 0 | 0 | 0 |

Month #2 01/01/2015-01/31/2015 | 0 | 0 | 0 | 0 |

Month #3 02/01/2015-02/28/2015 | 0 | 0 | 0 | 0 |

Month #4 03/01/2015-03/31/2015^ | 0 | 0 | 0 | 0 |

Month #5 04/01/2015-04/30/2015 | 0 | 0 | 0 | 0 |

Month #6 05/01/2015-05/31/2015 | 0 | 0 | 0 | 0 |

| Total | 0 | 0 | 0 | 0 |

*The Fund issued a tender offer on October 16, 2014. The tender offer enabled up to $14,985,133 to be redeemed by shareholders. The tendered shares were paid out at the December 31, 2014 net asset value per share.

^The Fund issued a tender offer on January 13, 2015. The tender offer enabled up to $13,994,704 to be redeemed by shareholders. The tendered shares were paid out at the March 31, 2015 net asset value per share.

Item 10. Submission of Matters to a Vote of Security Holders.

Not Applicable.

Item 11. Controls and Procedures.

| (a) | The Registrant’s President and Treasurer/Chief Financial Officer have reviewed the Registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940 (the “Act”)) as of a date within 90 days of the filing of this report, as required by Rule 30a-3(b) under the Act and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934. Based on their review, such officers have concluded that the disclosure controls and procedures are effective in ensuring that information required to be disclosed in this report is appropriately recorded, processed, summarized and reported and made known to them by others within the Registrant and by the Registrant’s service provider. |

| (b) | There were no changes in the Registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the Act) that occurred during the second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the Registrant's internal control over financial reporting. |

Item 12. Exhibits.

| (a) | (1) Any code of ethics or amendment thereto, that is the subject of the disclosure required by Item 2, to the extent that the registrant intends to satisfy Item 2 requirements through filing an exhibit. Not Applicable. |

(2) A separate certification for each principal executive and principal financial officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. Filed herewith.

(3) Any written solicitation to purchase securities under Rule 23c-1 under the Act sent or given during the period covered by the report by or on behalf of the registrant to 10 or more persons. Not applicable.

| (b) | Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. Furnished herewith. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

(Registrant) The Cushing MLP Infrastructure Fund

By (Signature and Title) /s/ Daniel L. Spears

Daniel L. Spears, President

Date August 5, 2015

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By (Signature and Title) /s/ Daniel L. Spears

Daniel L. Spears, President

Date August 5, 2015

By (Signature and Title) /s/ John H. Alban

John H. Alban, Treasurer & Chief Financial Officer

Date August 5, 2015