Anpulo Food, Inc.

Hangkong Road, Xiangfeng Town,

Laifeng County, Hubei 445700, China

January 30, 2014

Via EDGAR

Ryan Adams

Division of Corporation Finance

United States Securities and Exchange Commission

100 F Street N.E.

Washington, D.C. 20549

Re: Anpulo Food, Inc.

Amendment No. 1 to Registration Statement on Form S-1

Filed January 2, 2014

File No. 333-192006

Dear Mr. Adams:

We hereby submit the responses of Anpulo Food, Inc. (the “Company”) to the comments of the staff of the Division of Corporation Finance (the “Staff”) contained in your letter, dated January 16, 2014, to Wenping Luo of the Company in regard to the above-referenced Amendment No.1 to Registration Statement on Form S-1 filed on January 2, 2014 (“Form S-1”).

For convenience of reference, each Staff comment contained in your letter is reprinted below in italics, numbered to correspond with the paragraph numbers assigned in your letter, and is followed by the corresponding response of the Company. References herein to page numbers are to the page numbers in Amendment No. 2 to the Form S-1 (“Amendment No. 2”), filed with the Securities and Exchange Commission on January 30, 2014. Unless the context indicates otherwise, references in this letter to “we,” “us” and “our” refer to the Company on a consolidated basis. Capitalized terms not otherwise defined herein shall have the meanings ascribed to them in Amendment No.2, as amended by the amendment(s).

General

| 1. | We note your response to our prior comment 2. Please revise the prospectus to disclose that the resale offering is being registered pursuant to a “mutual understanding” between Mr. Luo and the selling shareholders. |

Response: We have revised the prospectus on page 30 to disclose that the resale offering is being registered pursuant to the mutual understandings between Mr. Luo or the Company and the selling shareholders, as the case may be.

| 2. | We note your response to our prior comment 3 and reissue in part. Please explain why there have been, and continue to be, substantial disclosure similarities between your filing and the periodic Exchange Act reports of Zhongpin Inc. For instance, much of the disclosure in the risk factors section and the products section appear to be substantially similar. |

Response: We have revised the risk factors section. We believe that the disclosure of the products section accurately describes our Company's products and, the similarity in our Company’s disclosure and Zhongpin’s disclosure is largely a result of the similarity in the two companies’ product offerings.

| 3. | We note your response to our prior comment 4. Please explain why you have not yet filed the appropriate Form 8-K and tell us when you plan to do so. |

Response: We have filed the current report on Form 8-K regarding the reverse acquisition and its related matters.

Registration Statement Cover Page

| 4. | We note your response to our prior comment 9. Please explain the applicability of Rule 416(a) to your offering, as there does not appear be any indications that the shares offered contain anti-dilution terms. |

Response: It is a common practice for companies to issue additional shares a result of stock splits, stock dividends, or similar transactions, without discrimination, to all of the existing shareholders of the same class of common equity of a company. We intend to follow this practice when effecting stock splits, declaring stock dividends, or similar transactions. Registering the additional amount of shares issuable resulting from stock split, stock dividends, or similar transactions, is a term customary to agreements, arrangement or understanding of share registration and, is in fact, an implied component of the understandings between Mr. Luo and the selling shareholders as well as the Company and the selling shareholders.

Third Party Data

| 5. | We note your response to our prior comment 11 and reissue. It does not appear the prospectus has been revised. Please remove the disclaimer that investors are “cautioned not to give undue weight to these estimates.” |

Response: We have revised to remove the disclaimer that investors are “cautioned not give undue weight to these estimates.”

Prospectus Summary, page 4

Overview, page 4

| 6. | We note your response to our prior comment 15. Please revise the last risk factor on page 13 to disclose that you no longer have a contract with your largest customer and discuss the attendant risks. |

Response: We have revised the discussed risk factor on page 10 to disclose that we no longer have a contract with our largest customer and the attendant risks.

2

Competitive Strengths, page 6

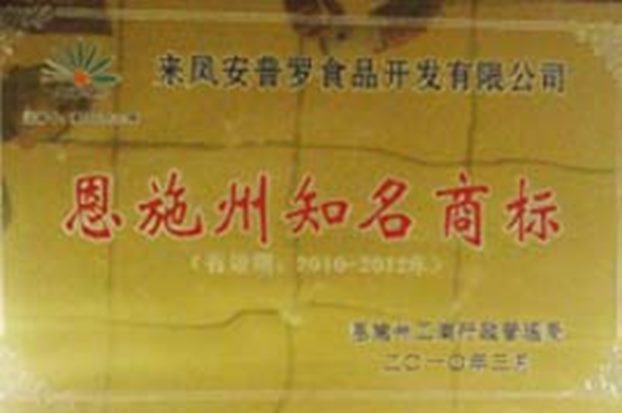

| 7. | We note your response to our prior comment 19 that your “Anpulo” brand name was recognized as a “Well-Known Tradename” by Enshi Tujia and Miao Autonomous Prefecture and your “Anpulo” branded chilled pork and frozen pork products were certified as a “Hubei Province Famous Brand Product.” Please provide us with copies of these documents. |

Response: We clarify that our “Anpulo” branded chilled pork and frozen pork products were certified as a “Premier Agricultural Product Brand” rather a “Hubei Province Famous Brand Product.” We have attached photocopies of the two certificates and their English translations as Exhibit A to this letter.

Our Growth Strategy, page 7

| 8. | To the extent that you discuss future business plans here and on page 47, such as your intentions to increase your market presence by adding more supermarket counters, seek collaboration with outside academic research forces to optimize and expand your product lines, educate consumers and participate in holidays and special occasion promotions, and construct new warehouses with walk-in coolers and freezers, the discussion should be balanced with a brief discussion on the time frame for implementing these future plans, the steps involved, and any obstacles involved before you can commence the planned operations. This includes the need for financing. If financing may not be available, please clarify that. |

Response: We have revised to include discussions on the time frame for implementing adding more supermarket counters, product development, and new warehouse construction and the need for additional financing to implement these future plans. We have also revised to clarify that the promotional activities are ongoing and the associated cost has been included in the selling expenses for the corresponding periods.

The Offering, page 8

| 9. | Please disclose the offering price here. |

Response: We have disclosed the offering price under the section titled “The Offering”.

Risk Factors, page 9

Risks Relating to Our Business, page 9

We utilize our exclusive network of independently operated specialty retail stores, page 13

| 10. | We note your response to our prior comment 23. We also note that you did not file the form of distribution agreement as an exhibit or add it to your exhibit index to be filed by subsequent amendment. Please revise accordingly. |

Response: We have filed a form of distribution agreement with specialty retail stores as Exhibit 10.7 to the prospectus.

3

Risks Relating To Conducting Business in China, page 19

If we do not complete remigration of equity pledge with SAIC local branch, page 20

| 11. | We note your response to our prior comment 27 and reissue in part. Please revise here to discuss the current status of the equity pledge registration process and your expectations regarding the timing of completion. |

Response: We have revised to discuss the current status of the equity pledge registration process and our expectations regarding the timing of completion.

Selling Shareholders, page 30

12. | We note your response to our prior comment 29 and reissue in part. Please file as exhibits any material agreements regarding these transactions. |

Response: In each case of shares-for-debt transactions and share grants to employees where the selling shareholders acquired the shares covered by this prospectus, no written agreement was entered into between Mr. Wenping Luo and the creditors or the Company and the employees.

Plan of Distribution, page 34

| 13. | We note your response to our prior comment 32 and reissue. Please revise to disclose that all of the selling shareholders “may be deemed” underwriters under the Securities Act. |

Response: We have revised to disclose that all of the selling shareholders may be deemed underwriters under the Securities Act.

Description of Securities, page 35

14. | Please revise the paragraph under the heading “Election of Directors” on page 36 to disclose your classified board arrangement. |

Response: We have revised the paragraph under the heading “Election of Directors” on page 36 to disclose our classified board arrangement.

Description of Business, page 41

Overview, page 41

15. | We note your response to our prior comment 34 and reissue in part. Please revise to disclose additional information concerning when you identified this company as a potential target and began negotiating a transaction. Also, please clarify whether you intend to amend your prior Exchange Act filings. |

Response: We will include the relevant disclosure by amendment. We will also advise our intention to amend our prior Exchange Act filings in our next correspondence letter.

4

Corporate History – Anpulo Laifeng, page 42

| 16. | Certain filings indicate that there was an An Puluo Food Development Co. Ltd., a hog farm in Enshi, China, that was owned by Wenping Luo and that was acquired by Tianli Agritech, Inc., in 2011. Please explain why there are no references to An Puluo Food Development Co. Ltd. in your corporate history or in Mr. Luo’s business experience disclosure on page 67. |

Response: An Puluo Food Development Co. Ltd. (“An Puluo”) is a variation of English translation of the name of Laifeng Anpulo (Group) Food Development Co., Ltd. (“Anpulo Laifeng”). In other words, An Puluo Food Development Co. Ltd. is Anpulo Laifeng.

We have revised our disclosure about to include the transactions between Anpulo Laifeng and Tianlil Agritech, Inc. and how we accounted these transactions in our financial statements.

5

Our Industry, page 45

17. | Please explain why you are relying on data from 2005 and 2009 in the second paragraph of this section. |

Response: We have revised to remove the data from 2005 and 2009.

Management’s Discussion and Analysis, page 55

18. | Please remove the reference to the Private Securities Litigation Reform Act of 1995 or explain why you believe the safe harbor applies to you. |

Response: We have revised to remove the reference to the Private Securities Litigation Reform Act of 1995.

Results of Operations, page 57

Comparison on Year Ended December 31, 2012 and 2011, page 58

Interest Expense, page 61

| 19. | We note the inclusion of the table detailing the effect of subsidy income on interest expense in your comparative discussion of the nine-months ended September 30, 2013 to 2012. Please tell us where similar disclosure is included in the annual comparative discussion within MD&A, or revise to include similar tabular disclosure. |

Response: We have revised to include the table detailing the effect of subsidy income on interest expense in the annual comparative discussion within MD&A.

Liquidity and Capital Resources, page 62

| 20. | Please revise your discussion of Operating Cash Flows for the nine-months ended September 30, 2013 to include the amounts of the impacts of increased operating expenses and reduced governmental subsidy on operating cash flow. |

Response: We have revised our discussion of Operating Cash Flow for the nine-months ended September 30, 2013 to include the amounts of the impacts of increased operating expenses and reduced governmental subsidy on operating cash flow.

21. | We note your response to our prior comment 55 and reissue in part. Specifically, we note that you did not revise your exhibit index to identify any material loans to be filed as exhibits. Please file any material loan agreements as exhibits to the registration statement. To the extent you intend to file such agreements in a subsequent amendment, please revise your exhibit index accordingly. |

Response: We have identified material loan agreements as exhibits to the registration statement. We will file these agreements by amendment. We will also identify the agreements for the renewed bank loans in next amendment.

6

Requirement for Additional Funding, page 62

| 22. | Please revise to disclose when you anticipate your cash reserves will run out and how much additional funding you need to meet your short and long-term funding requirements. |

Response: We have revised to disclose when we anticipate our cash reserves will run out and how much additional funding we need to meet our short and long-term funding requirements.

Directors, Executive Officers, Promoters and Control Persons, page 66

| 23. | We note your response to our prior comment 59. In spite of your response that there is no current or expected relationship between your business and Anpulo Food Development, Inc., please explain why the two companies were given substantially similar names. |

Response: We will provide response in our next correspondence letter.

| 24. | We note your response to our prior comment 60 and reissue. Please remove the knowledge qualifier on page 70 in your discussion of legal proceedings. Otherwise, please provide us with a legal analysis in support of your position, including a discussion of how the company is able to acquire knowledge. Refer to Item 401(f) of Regulation S-K. |

Response: We have revised to remove the knowledge qualifier.

Executive Compensation, page 72

25. | Please update your compensation related disclosure to include information for the recently completed fiscal year. |

Response: We have updated our compensation related disclosure to include information for the fiscal year ended December 31, 2013.

Security Ownership of Certain Beneficial Owners and Management, page 73

Certain Relationships and Related Transactions, page 74

26. | We note your response to our prior comment 62 and reissue in part. Please revise to disclose the total approximate dollar value of the amount involved in the reverse acquisition transaction. |

Response: We have revised to disclose the total approximate dollar value of the amount involved in the reverse acquisition transaction.

7

| 27. | We note your response to our prior comment 63 and reissue. The repayments of indebtedness in the amounts of $1.2 million and $2.2 million to related parties do not appear to be disclosed here. Please revise. |

Response: The repayments of indebtedness in the amounts of $1.2 million and $2.2 million to related parties were included by mistake. We have revised to clarify that during 2012 and 2011 we loaned an aggregate of $1.2 million and $2.2 million to Wenping Luo, the principal stockholder and President and Chief Executive Officer and a director of the Company, for his personal use.

| 28. | Please reconcile your disclosure on page 74 that “[t]he above loans would be in violation of the Sarbanes-Oxley Act of 2002, including Section 402’s prohibition against personal loans to directors and executive officers, either directly or indirectly, had they occurred after Anpulo Laifeng became a variable interest entity of our Company” with your disclosure on page F-12 that “[t]hese personal loans by us to Mr. Wenping Luo during 2012 violated the prohibitions of Section 402 of the Sarbanes-Oxley Act of 2002 from making loans to executive officers or directors.” |

Response: We have reconciled our disclosure.

| 29. | Please file the agreements related to the personal loans and advances as exhibits to the registration statement or explain why you are not required to do so. Refer to Item 601(b)(10) of Regulation S-K. |

Response: The Company and Mr. Luo did not enter into any written agreement regarding the personal loans and advances.

Note 10 – Subsidy Income, pages F-17 and F-33

| 30. | We note your response to our prior comment 67. Please revise your disclosure here and in MD&A to discuss how these subsidies are determined. Your discussion should include how you apply for subsidies from local authorities, including whether you apply based on debt you have outstanding, plans to incur debt to be used for expansion, or another basis. Your revised disclosure should also include tabular disclosure of individual subsidies received and the debt agreements to which they relate, for each period presented on the face of your annual and interim financial statements, as applicable. The aggregate of the items presented in this table should reconcile to the face of the statement of operations. Further, your disclosure in your discussion of subsidy income within Note 2 in both interim and annual financial statements should include whether you have recognized these subsidies on receipt or deferred these over the term of the related debt. Your response to us should include support for your accounting treatment. |

Response: We have revised our disclosures to discuss how these subsidies are determined. The subsidies for bank loan interest are recognized as an income upon receipt and used to against the current period bank loan interest expenses.

The subsidies for bank loan interest were recognized as an income upon receipt. We did not defer the income or recognize as receivables in advance because the amount of the subsidies and the releasing timing for them are unpredictable. The subsidies may be granted monthly, quarterly, or over longer intervals, depending on the local government’s financial budget.

The subsidies to bank loan interest expenses were subsequently used to offset our interest expenses during the comparable periods. The amount of subsidies is determined by the local government with consideration of the loan principals, interest rate, the number of days for which the bank loans are outstanding. The purpose of these subsidies is to lower the financing costs for companies located in less developed areas. With the subsidies, the actual interest expenses would be reduced. Considering the nature of the subsidies, the Company used them to offset its interest expenses.

8

The Company acknowledges that:

| ● | should the Commission or the staff, acting pursuant to delegated authority, declare the filing effective, it does not foreclose the Commission from taking any action with respect to the filing; |

| ● | the action of the Commission or the staff, acting pursuant to delegated authority, in declaring the filing effective, does not relieve the company from its full responsibility for the adequacy and accuracy of the disclosure in the filing; and |

| ● | the company may not assert staff comments and the declaration of effectiveness as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Sincerely,

| /s/ Wenping Luo | |

| Wenping Luo | |

| President and Chief Executive Officer |

9

Exhibit A

[English Translation]

| Laifeng Anpulo (Group) Food Development Co., Ltd. | |

Enshi Prefecture Well-known Trade Name | |

| (Effective from 2010 to 2012) | |

Enshi Prefecture Administration of Industry and Commerce March 2010 | |

[English Translation]

| Anpulo Chilled & Frozen Pork Products | |

Premier Agricultural Product Brand | |

The Communist Party of Laifeng County The People’s Government of Laifeng County March 2011 | |