UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-22472

(Investment Company Act File Number)

RiverNorth Opportunities Fund, Inc.

(Exact Name of Registrant as Specified in Charter)

1290 Broadway, Suite 1000

Denver, CO 80203

(Address of Principal Executive Offices)

Sareena Khwaja-Dixon

RiverNorth Opportunities Fund, Inc.

1290 Broadway, Suite 1000

Denver, Colorado 80203

(Name and address of agent for service)

(303) 623-2577

(Registrant’s Telephone Number)

Date of Fiscal Year End: July 31

Date of Reporting Period: July 31, 2020

| Item 1. | Reports to Shareholders. |

OPPORTUNISTIC INVESTMENT STRATEGIES

Annual Report

RIVERNORTH OPPORTUNITIES FUND, INC.

(RIV)

Investment Sub-Adviser:

RiverNorth Capital Management, LLC

325 N. LaSalle Street, Suite 645

Chicago, IL 60654 |  |

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website at www.rivernorthcef.com and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive all future shareholder reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank).

| RiverNorth Opportunities Fund, Inc. | Table of Contents |

| RiverNorth Opportunities Fund, Inc. | Performance Overview |

July 31, 2020 (Unaudited)

INVESTMENT OBJECTIVE

RiverNorth Opportunities Fund, Inc.’s (the “Fund”) investment objective is total return consisting of capital appreciation and current income.

PERFORMANCE OVERVIEW

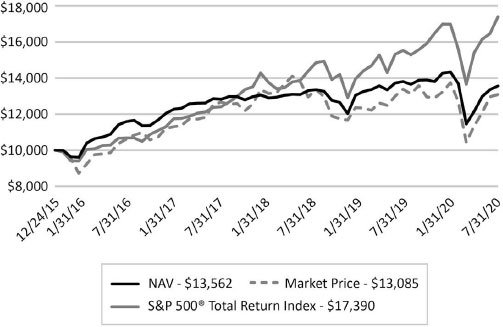

For the twelve month period ended July 31, 2020, the Fund returned -1.75% on a net asset value (“NAV”) basis and -2.22% on a market price basis. The S&P 500 Total Return Index returned 11.96% during the same period. The All Closed-end Fund Index(1) return was -1.49% on a NAV basis and -4.68% on a price basis over the twelve month period.

The Fund benefited from its exposure to equity and municipal bond closed-end funds, as these funds generally had positive NAV returns over the period. In addition, several of the Fund’s holdings announced corporate actions such as tender offers or liquidations, which resulted in discount narrowing.

The Fund’s exposure to closed-end funds that invest in energy related securities detracted from performance as these funds experienced both negative NAV performance and discount widening over the period. Also, the Fund’s hedging through taking short positions in US equity and credit focused exchange-traded funds (“ETFs”) detracted from performance, as both of these sectors posted positive returns over the period.

| (1) | All Closed-End Fund Index |

Discounts are based on Morningstar, Inc. un-weighted closed-end fund indexes, which are equal-weighted averages of all of the closed-end funds assigned to the categories below:

- All CEFs: all CEFs in the Morningstar domestic CEF universe.

PERFORMANCE as of July 31, 2020

| | CUMULATIVE | AVERAGE ANNUAL |

| TOTAL RETURNS(1) | 6 Months | 1 Year | 3 Year | Since

Inception(2) |

| RiverNorth Opportunities Fund, Inc. - NAV(3) | -5.38% | -1.75% | 1.80% | 6.84% |

| RiverNorth Opportunities Fund, Inc. - Market Price(4) | -4.83% | -2.22% | 1.44% | 6.01% |

| S&P 500® Total Return Index | 2.42% | 11.96% | 12.01% | 12.77% |

| (1) | Total returns assume reinvestment of all distributions. |

| (2) | The Fund commenced operations on December 24, 2015. |

| (3) | Performance returns are net of management fees and other Fund expenses. |

| (4) | Market price is the value at which the Fund trades on an exchange. This market price can be more or less than its NAV. |

Performance data quoted represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling (855) 830-1222 or by visiting www.rivernorthcef.com. Total return measures net investment income and capital gain or loss from portfolio investments. All performance shown assumes reinvestment of dividends and capital gains distributions.

| RiverNorth Opportunities Fund, Inc. | Performance Overview |

July 31, 2020 (Unaudited)

Total annual expense ratio as a percentage of net assets attributable to common shares as of July 31, 2020, is 1.54% (excluding dividend expense and line of credit expense). Including dividend expense and line of credit expense, the expense ratio is 2.06%.

The Fund is a closed-end fund and does not continuously issue shares for sale as open-end mutual funds do. The Fund now trades only in the secondary market. Investors wishing to buy or sell shares need to place orders through an intermediary or broker and additional charges or commissions will apply. The share price of a closed-end fund is based on the market’s value.

Distributions may be paid from sources of income other than ordinary income, such as net realized short-term capital gains, net realized long-term capital gains and return of capital. The actual amounts and sources of the amounts for tax reporting purposes will depend upon a Fund’s investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. If a distribution includes anything other than net investment income, the Fund provides a Section 19(a) notice of the best estimate of its distribution sources at that time. These estimates may not match the final tax characterization (for the full year’s distributions) contained in shareholders’ 1099-DIV forms after the end of the year.

S&P 500® Total Return Index – A market value weighted index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. This index is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. This index reflects the effects of dividend reinvestment.

Indices are unmanaged; their returns do not reflect any fees, expenses, or sales charges. An investor cannot invest directly in an index.

ALPS Advisors, Inc. is the investment adviser to the Fund.

RiverNorth Capital Management, LLC is the investment sub-adviser to the Fund. RiverNorth Capital Management, LLC is not affiliated with ALPS Advisors, Inc. or any of its affiliates.

Secondary market support provided to the Fund by ALPS Advisors, Inc.’s affiliate, ALPS Portfolio Solutions Distributor, Inc., a FINRA member.

| Annual Report | July 31, 2020 | 3 |

| RiverNorth Opportunities Fund, Inc. | Performance Overview |

July 31, 2020 (Unaudited)

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT

The graph below illustrates the growth of a hypothetical $10,000 investment assuming the purchase of common shares at the closing market price (NYSE: RIV) of $19.40 on December 24, 2015, and tracking its progress through July 31, 2020.

Past performance does not guarantee future results. Performance will fluctuate with changes in market conditions. Current performance may be lower or higher than the performance data shown. Performance information does not reflect the deduction of taxes that shareholders would pay on Fund distributions or the sale of Fund shares. An investment in the Fund involves risk, including loss of principal.

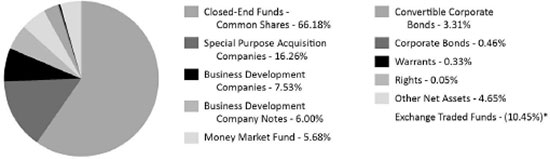

ASSET ALLOCATION as of July 31, 2020^

| ^ | Holdings are subject to change. |

| * | Represents securities sold short. |

Percentages are based on total net assets of the Fund.

| RiverNorth Opportunities Fund, Inc. | Performance Overview |

July 31, 2020 (Unaudited)

TOP TEN HOLDINGS* as of July 31, 2020

| | | % of Net Assets** |

| Voya Prime Rate Trust | | 7.25% |

| Barings BDC, Inc. | | 5.30% |

| PGIM Global High Yield Fund, Inc. | | 4.45% |

| BlackRock Debt Strategies Fund, Inc. | | 3.29% |

| Western Asset Global High Income Fund, Inc. | | 2.62% |

| DTF Tax-Free Income, Inc. | | 2.51% |

| Eaton Vance Limited Duration Income Fund | | 2.51% |

| Source Capital, Inc. | | 2.40% |

| Pershing Square Holdings Ltd. | | 2.38% |

| Eaton Vance Senior Income Trust | | 2.31% |

| | | 35.02% |

| * | Holdings are subject to change and exclude cash equivalents. Only long positions are listed. |

| ** | Percentages are based on total net assets, including securities sold short. |

| Annual Report | July 31, 2020 | 5 |

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| Description | | Shares | | | Value

(Note 2) | |

| CLOSED-END FUNDS - COMMON SHARES (66.18%) | | | | | | | | |

| Aberdeen Emerging Markets Equity Income Fund, Inc. | | | 309,605 | | | $ | 2,037,201 | |

| Aberdeen Total Dynamic Dividend Fund | | | 265,434 | | | | 2,094,274 | |

| Barings Corporate Investors | | | 52,111 | | | | 682,654 | |

| Barings Participation Investors | | | 32,746 | | | | 378,544 | |

| BlackRock Debt Strategies Fund, Inc. | | | 467,037 | | | | 4,576,963 | |

| BlackRock New York Municipal Bond Trust | | | 83,582 | | | | 1,337,220 | |

| BlackRock New York Municipal Income Quality Trust | | | 139,262 | | | | 1,898,141 | |

| BlackRock Resources & Commodities Strategy Trust | | | 433,992 | | | | 2,755,849 | |

| BrandywineGLOBAL - Global Income Opportunities Fund, Inc.(a) | | | 248,023 | | | | 3,107,728 | |

| Calamos Long/Short Equity & Dynamic Income Trust | | | 10,730 | | | | 164,062 | |

| Clough Global Opportunities Fund(a) | | | 267,846 | | | | 2,512,395 | |

| DTF Tax-Free Income, Inc. | | | 242,890 | | | | 3,490,159 | |

| Eagle Growth & Income Opportunities Fund(b) | | | 207,900 | | | | 2,609,145 | |

| Eaton Vance Floating-Rate Income Plus Fund | | | 227,905 | | | | 3,213,415 | |

| Eaton Vance Limited Duration Income Fund(a) | | | 300,378 | | | | 3,487,389 | |

| Eaton Vance Municipal Bond Fund | | | 92,342 | | | | 1,222,608 | |

| Eaton Vance Senior Income Trust | | | 565,194 | | | | 3,221,606 | |

| First Trust MLP and Energy Income Fund | | | 173,453 | | | | 905,425 | |

| First Trust New Opportunities MLP & Energy Fund | | | 73,540 | | | | 296,366 | |

| Highland Global Allocation Fund | | | 243,892 | | | | 1,548,714 | |

| Highland Income Fund | | | 262,087 | | | | 2,122,905 | |

| Invesco Dynamic Credit Opportunities Fund | | | 109,088 | | | | 975,247 | |

| Invesco High Income Trust II | | | 119,789 | | | | 1,488,977 | |

| Invesco Senior Income Trust | | | 363,506 | | | | 1,286,811 | |

| John Hancock Tax-Advantaged Global Shareholder Yield Fund | | | 13,439 | | | | 71,361 | |

| Kayne Anderson Midstream/Energy Fund, Inc. | | | 197,370 | | | | 878,296 | |

| Morgan Stanley Emerging Markets Domestic Debt Fund, Inc. | | | 11,998 | | | | 70,068 | |

| NexPoint Credit Strategies Fund | | | 253,635 | | | | 2,439,969 | |

| Nuveen Credit Strategies Income Fund | | | 240,520 | | | | 1,414,258 | |

| Nuveen Dividend Advantage Municipal Income Fund | | | 44,091 | | | | 700,606 | |

| Nuveen Georgia Quality Municipal Income Fund | | | 113,069 | | | | 1,423,539 | |

| Nuveen New York Municipal Value Fund 2 | | | 35,338 | | | | 492,647 | |

| Nuveen Quality Municipal Income Fund | | | 113,548 | | | | 1,663,478 | |

| Pershing Square Holdings Ltd. | | | 133,994 | | | | 3,309,652 | |

| PGIM Global High Yield Fund, Inc.(a) | | | 469,535 | | | | 6,188,471 | |

| PGIM High Yield Bond Fund, Inc. | | | 105,457 | | | | 1,444,761 | |

| PIMCO Energy & Tactical Credit Opportunities Fund | | | 182,236 | | | | 1,241,027 | |

| Royce Micro-Cap Trust, Inc. | | | 236,020 | | | | 1,793,752 | |

| Source Capital, Inc. | | | 93,302 | | | | 3,343,944 | |

| Special Opportunities Fund, Inc. | | | 71,074 | | | | 852,888 | |

| Templeton Global Income Fund | | | 190,690 | | | | 1,044,981 | |

| Voya Global Equity Dividend and Premium Opportunity Fund | | | 210,325 | | | | 1,047,419 | |

See Notes to Financial Statements.

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| Description | | Shares | | | Value

(Note 2) | |

| Voya Natural Resources Equity Income Fund | | | 326,468 | | | $ | 803,111 | |

| Voya Prime Rate Trust(a) | | | 2,308,076 | | | | 10,086,292 | |

| Wells Fargo Income Opportunities Fund | | | 97,672 | | | | 718,866 | |

| Western Asset Global High Income Fund, Inc. | | | 375,747 | | | | 3,652,261 | |

| | | | | | | | | |

| TOTAL CLOSED-END FUNDS - COMMON SHARES | | | | | | | | |

| (Cost $94,759,091) | | | | | | | 92,095,445 | |

| | | | | | | | | |

| BUSINESS DEVELOPMENT COMPANIES - COMMON SHARES (7.53%) | | | | | | | | |

| Bain Capital Specialty Finance, Inc. | | | 143,452 | | | | 1,444,561 | |

| Barings BDC, Inc.(a) | | | 969,372 | | | | 7,376,921 | |

| Golub Capital BDC, Inc. | | | 117,782 | | | | 1,393,361 | |

| Oaktree Specialty Lending Corp. | | | 57,226 | | | | 259,234 | |

| | | | | | | | | |

| TOTAL BUSINESS DEVELOPMENT COMPANIES - COMMON SHARES | | | | | | | | |

| (Cost $11,667,655) | | | | | | | 10,474,077 | |

| | | | | | | | | |

| BUSINESS DEVELOPMENT COMPANY NOTES (6.00%) | | | | | | | | |

| Capital Southwest Corp., 5.95%, 12/15/2022 | | | 13,532 | | | | 339,247 | |

| Monroe Capital Corp., 5.75%, 10/31/2023 | | | 31,867 | | | | 731,348 | |

| Oxford Square Capital Corp., 6.50%, 3/30/2024 | | | 117,106 | | | | 2,768,386 | |

| PennantPark Investment Corp., 5.50%, 10/15/2024 | | | 30,979 | | | | 702,913 | |

| Portman Ridge Finance Corp., 6.13%, 9/30/2022 | | | 35,346 | | | | 856,787 | |

| Stellus Capital Investment Corp., 5.75%, 9/15/2022 | | | 18,081 | | | | 426,531 | |

| THL Credit, Inc., 6.75%, 12/30/2022 | | | 33,487 | | | | 815,013 | |

| THL Credit, Inc., 6.13%, 10/30/2023 | | | 45,456 | | | | 1,069,580 | |

| TriplePoint Venture Growth BDC Corp., 5.75%, 7/15/2022 | | | 12,985 | | | | 313,979 | |

| WhiteHorse Finance, Inc., 6.50%, 11/30/2025 | | | 13,169 | | | | 322,904 | |

| | | | | | | | | |

| TOTAL BUSINESS DEVELOPMENT COMPANY NOTES | | | | | | | | |

| (Cost $8,081,613) | | | | | | | 8,346,687 | |

| Description | | Rate | | | Maturity

Date | | Principal

Amount | | | Value

(Note 2) | |

| CONVERTIBLE CORPORATE BONDS (3.31%) | | | | | | | | | | | | | | |

| BlackRock Capital Investment Corp. | | | 5.000 | % | | 06/15/22 | | $ | 1,426,565 | | | $ | 1,410,236 | |

| BlackRock TCP Capital Corp. | | | 4.625 | % | | 03/01/22 | | | 699,500 | | | | 694,254 | |

| Goldman Sachs BDC, Inc. | | | 4.500 | % | | 04/01/22 | | | 500,000 | | | | 502,499 | |

| New Mountain Finance Corp. | | | 5.750 | % | | 08/15/23 | | | 1,493,450 | | | | 1,482,192 | |

| Sixth Street Specialty Lending, Inc. | | | 4.500 | % | | 08/01/22 | | | 500,000 | | | | 511,109 | |

| | | | | | | | | | | | | | | |

| TOTAL CONVERTIBLE CORPORATE BONDS | | | | | | | | | | | | | | |

| (Cost $4,095,034) | | | | | | | | | | | | | 4,600,290 | |

See Notes to Financial Statements.

| Annual Report | July 31, 2020 | 7 |

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| Description | | Rate | | | Maturity

Date | | Principal

Amount | | | Value

(Note 2) | |

| CORPORATE BONDS (0.46%) | | | | | | | | | | | | | | |

| Business Development Corp. of America(c) | | | 4.850 | % | | 12/15/24 | | $ | 725,000 | | | $ | 645,752 | |

| | | | | | | | | | | | | | | |

| TOTAL CORPORATE BONDS | | | | | | | | | | | | | | |

| (Cost $725,000) | | | | | | | | | | | | | 645,752 | |

| Description | | Shares | | | Value

(Note 2) | |

| SPECIAL PURPOSE ACQUISITION COMPANIES - COMMON SHARES (16.26%)(d) | | | | | | | | |

| 8i Enterprises Acquisition Corp. | | | 23,872 | | | | 244,927 | |

| ACE Convergence Acquisition Corp. | | | 13,828 | | | | 138,557 | |

| Agba Acquisition, Ltd. | | | 30,883 | | | | 336,316 | |

| Alussa Energy Acquisition Corp. | | | 33,782 | | | | 345,759 | |

| Amplitude Healthcare Acquisition Corp. | | | 47,778 | | | | 498,325 | |

| Andina Acquisition Corp. III | | | 29,708 | | | | 303,319 | |

| Apex Technology Acquisition Corp. | | | 6,941 | | | | 79,717 | |

| Artius Acquisition, Inc. | | | 4,052 | | | | 41,006 | |

| ARYA Sciences Acquisition Corp. II | | | 1,285 | | | | 15,163 | |

| Brilliant Acquisition Corp. | | | 11,614 | | | | 116,024 | |

| Capstar Special Purpose Acquisition Corp. | | | 3,882 | | | | 39,402 | |

| CC Neuberger Principal Holdings I | | | 43,113 | | | | 461,309 | |

| Chardan Healthcare Acquisition 2 Corp. | | | 29,794 | | | | 309,858 | |

| Churchill Capital Corp. II | | | 56,978 | | | | 647,578 | |

| Churchill Capital Corp. IV | | | 54,359 | | | | 543,590 | |

| CIIG Merger Corp. | | | 19,510 | | | | 201,343 | |

| Collective Growth Corp. | | | 32,468 | | | | 326,628 | |

| Crescent Acquisition Corp. | | | 39,846 | | | | 404,437 | |

| dMY Technology Group, Inc. | | | 62,164 | | | | 704,940 | |

| E.Merge Technology Acquisition Corp. | | | 6,819 | | | | 68,190 | |

| East Resources Acquisition Co. | | | 27,991 | | | | 279,630 | |

| East Stone Acquisition Corp. | | | 41,399 | | | | 418,958 | |

| Far Point Acquisition Corp., Class A | | | 5,103 | | | | 52,204 | |

| FinTech Acquisition Corp. III | | | 35,478 | | | | 402,321 | |

| Flying Eagle Acquisition Corp. | | | 29,396 | | | | 340,994 | |

| Fortress Value Acquisition Corp. | | | 9,395 | | | | 110,862 | |

| Fusion Acquisition Corp. | | | 5,317 | | | | 53,436 | |

| Galileo Acquisition Corp. | | | 9,373 | | | | 98,885 | |

| GigCapital2, Inc. | | | 23,193 | | | | 257,674 | |

| GigCapital3, Inc. | | | 30,206 | | | | 308,101 | |

| Greenrose Acquisition Corp. | | | 74,128 | | | | 737,574 | |

| Greenvision Acquisition Corp. | | | 65,740 | | | | 696,515 | |

| GS Acquisition Holdings Corp. II | | | 963 | | | | 10,015 | |

| GX Acquisition Corp. | | | 21,598 | | | | 231,315 | |

| Haymaker Acquisition Corp. II | | | 15,939 | | | | 169,750 | |

| Healthcare Merger Corp. | | | 9,755 | | | | 106,329 | |

See Notes to Financial Statements.

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| Description | | Shares | | | Value

(Note 2) | |

| Hennessy Capital Acquisition Corp. IV | | | 44,040 | | | $ | 480,036 | |

| Insurance Acquisition Corp., Class A | | | 6,376 | | | | 68,287 | |

| InterPrivate Acquisition Corp. | | | 72,070 | | | | 734,393 | |

| Juniper Industrial Holdings, Inc. | | | 1,301 | | | | 13,947 | |

| Kensington Capital Acquisition Corp. | | | 15,468 | | | | 156,846 | |

| Landcadia Holdings II, Inc. | | | 37,799 | | | | 434,690 | |

| LF Capital Acquisition Corp., Class A | | | 33,437 | | | | 354,098 | |

| LifeSci Acquisition Corp. | | | 24,497 | | | | 255,994 | |

| LIV Capital Acquisition Corp. | | | 46,360 | | | | 472,872 | |

| Live Oak Acquisition Corp. | | | 32,285 | | | | 334,150 | |

| Malacca Straits Acquisition Co., Ltd. | | | 11,183 | | | | 111,718 | |

| Merida Merger Corp. I | | | 61,365 | | | | 600,763 | |

| Monocle Acquisition Corp. | | | 7,363 | | | | 75,618 | |

| Mountain Crest Acquisition Corp. | | | 10,930 | | | | 110,393 | |

| Netfin Acquisition Corp. | | | 25,065 | | | | 275,715 | |

| New Providence Acquisition Corp. | | | 16,868 | | | | 182,174 | |

| Newborn Acquisition Corp. | | | 26,810 | | | | 273,998 | |

| NewHold Investment Corp. | | | 54,555 | | | | 540,640 | |

| Orisun Acquisition Corp. | | | 36,130 | | | | 366,719 | |

| Osprey Technology Acquisition Corp. | | | 31,260 | | | | 335,263 | |

| Pershing Square Tontine Holdings, Ltd. | | | 30,921 | | | | 650,578 | |

| Pivotal Investment Corp. II | | | 30,504 | | | | 317,242 | |

| Property Solutions Acquisition Corp. | | | 61,679 | | | | 614,323 | |

| PropTech Acquisition Corp. | | | 24,696 | | | | 269,186 | |

| PTK Acquisition Corp. | | | 32,769 | | | | 327,133 | |

| Replay Acquisition Corp. | | | 21,524 | | | | 231,706 | |

| Roth CH Acquisition | Co. | | | 19,775 | | | | 203,683 | |

| SC Health Corp. | | | 5,789 | | | | 60,929 | |

| Schultze Special Purpose Acquisition Corp. | | | 30,224 | | | | 307,680 | |

| Silver Spike Acquisition Corp. | | | 25,306 | | | | 260,146 | |

| South Mountain Merger Corp. | | | 30,930 | | | | 337,137 | |

| Stable Road Acquisition Corp. | | | 13,092 | | | | 133,538 | |

| Sustainable Opportunities Acquisition Corp. | | | 16,121 | | | | 165,240 | |

| Thunder Bridge Acquisition II, Ltd. | | | 16,262 | | | | 178,882 | |

| Trine Acquisition Corp. | | | 30,246 | | | | 341,024 | |

| Tuscan Holdings Corp. | | | 43,548 | | | | 458,560 | |

| Tuscan Holdings Corp. II | | | 92,638 | | | | 942,128 | |

| Union Acquisition Corp. II | | | 5,982 | | | | 61,555 | |

| Yunhong International | | | 49,213 | | | | 490,654 | |

| | | | | | | | | |

| TOTAL SPECIAL PURPOSE ACQUISITION COMPANIES - COMMON SHARES | | | | | | | | |

| (Cost $21,502,600) | | | | | | | 22,630,589 | |

| | | | | | | | | |

| RIGHTS (0.05%)(d) | | | | | | | | |

| 8i Enterprises Acquisition Corp., Strike Price $11.50, Expires 12/31/2049 | | | 23,872 | | | | 14,469 | |

See Notes to Financial Statements.

| Annual Report | July 31, 2020 | 9 |

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| Description | | Shares | | | Value

(Note 2) | |

| Alberton Acquisition Corp., Strike Price $11.50, Expires 12/31/2049 | | | 22,730 | | | $ | 4,546 | |

| Andina Acquisition Corp. III, Strike Price $11.50, Expires 12/31/2049 | | | 29,708 | | | | 8,912 | |

| Big Rock Partners Acquisition Corp., Strike Price $11.50, Expires 12/31/2049 | | | 35,482 | | | | 11,354 | |

| HL Acquisitions Corp., Strike Price $11.50, Expires 07/19/2023 | | | 30,748 | | | | 18,443 | |

| Longevity Acquisition Corp., Strike Price $11.50, Expires 12/31/2049 | | | 24,043 | | | | 4,821 | |

| Orisun Acquisition Corp., Strike Price $11.50, Expires 12/31/2049 | | | 36,130 | | | | 7,226 | |

| Tottenham Acquisition I, Ltd., Strike Price $11.50, Expires 12/31/2049 | | | 24,729 | | | | 4,763 | |

| | | | | | | | | |

| TOTAL RIGHTS | | | | | | | | |

| (Cost $70,440) | | | | | | | 74,534 | |

| | | | | | | | | |

| WARRANTS (0.33%)(d) | | | | | | | | |

| 8i Enterprises Acquisition Corp., Strike Price $11.50, Expires 10/01/2025 | | | 23,872 | | | | 13,607 | |

| Alberton Acquisition Corp., Strike Price $11.50, Expires 11/21/2023 | | | 22,730 | | | | 2,955 | |

| Andina Acquisition Corp. III, Strike Price $11.50, Expires 03/06/2024 | | | 29,708 | | | | 8,321 | |

| Atlas Technical Consultants, Inc., Strike Price $11.50, Expires 11/26/2025 | | | 20,683 | | | | 9,928 | |

| Big Rock Partners Acquisition Corp., Strike Price $11.50, Expires 12/01/2022 | | | 17,741 | | | | 4,080 | |

| Brooge Energy, Ltd., Strike Price $11.50, Expires 07/14/2023 | | | 39,945 | | | | 30,158 | |

| Crescent Acquisition Corp., Strike Price $11.50, Expires 03/07/2024 | | | 19,923 | | | | 15,938 | |

| Far Point Acquisition Corp., Strike Price $11.50, Expires 06/03/2025 | | | 1,701 | | | | 817 | |

| Fortress Value Acquisition Corp., Strike Price $11.50, Expires 05/04/2027 | | | 3,131 | | | | 9,049 | |

| Graf Industrial Corp., Strike Price $11.50, Expires 12/31/2025 | | | 47,967 | | | | 94,975 | |

| Hennessy Capital Acquisition Corp. IV, Strike Price $11.50, Expires 09/25/2025 | | | 33,030 | | | | 59,454 | |

| HL Acquisitions Corp., Strike Price $11.50, Expires 07/19/2023 | | | 30,748 | | | | 21,524 | |

| Insurance Acquisition Corp., Strike Price $11.50, Expires 03/31/2024 | | | 3,188 | | | | 5,962 | |

| KBL Merger Corp. IV, Strike Price $11.50, Expires 07/01/2023 | | | 14,899 | | | | 2,235 | |

| KLDiscovery, Inc., Strike Price $11.50, Expires 12/01/2025 | | | 9,896 | | | | 2,227 | |

See Notes to Financial Statements.

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| | July 31, 2020 |

| | | | | | Value | |

| Description | | Shares | | | (Note 2) | |

| Landcadia Holdings II, Inc., Strike Price $11.50, Expires 05/09/2026 | | | 12,599 | | | $ | 35,277 | |

| Legacy Acquisition Corp., Strike Price $11.50, Expires 12/01/2022 | | | 29,594 | | | | 10,358 | |

| Leisure Acquisition Corp., Strike Price $11.50, Expires 12/28/2022 | | | 28,414 | | | | 8,808 | |

| LF Capital Acquisition Corp., Strike Price $11.50, Expires 06/28/2023 | | | 33,437 | | | | 18,808 | |

| Longevity Acquisition Corp., Strike Price $11.50, Expires 07/31/2025 | | | 24,043 | | | | 4,568 | |

| Megalith Financial Acquisition Corp., Strike Price $11.50, Expires 09/21/2023 | | | 35,972 | | | | 23,310 | |

| Merida Merger Corp. I, Strike Price $11.50, Expires 11/07/2026 | | | 30,682 | | | | 19,115 | |

| Meten EdtechX Education Group, Ltd., Strike Price $11.50, Expires 03/16/2025 | | | 16,106 | | | | 7,006 | |

| Monocle Acquisition Corp., Strike Price $11.50, Expires 06/12/2024 | | | 7,363 | | | | 2,298 | |

| Orisun Acquisition Corp., Strike Price $11.50, Expires 05/31/2024 | | | 36,130 | | | | 5,430 | |

| Schultze Special Purpose Acquisition Corp., Strike Price $11.50, Expires 12/31/2023 | | | 30,224 | | | | 12,090 | |

| Tenzing Acquisition Corp., Strike Price $11.50, Expires 08/23/2025 | | | 29,977 | | | | 10,792 | |

| Tottenham Acquisition I, Ltd., Strike Price $11.50, Expires 06/06/2025 | | | 24,729 | | | | 4,698 | |

| Trident Acquisitions Corp., Strike Price $11.50, Expires 06/14/2021 | | | 50,476 | | | | 11,155 | |

| Whole Earth Brands, Inc., Strike Price $11.50, Expires 06/25/2025 | | | 6,571 | | | | 4,929 | |

| | | | | | | | | |

| TOTAL WARRANTS | | | | | | | | |

| (Cost $322,593) | | | | | | | 459,872 | |

| Description | | 7-Day

Yield | | | Shares | | | Value

(Note 2) | |

| SHORT-TERM INVESTMENTS (5.68%) | | | | | | | | | | | | |

| State Street Institutional Treasury Money Market Fund | | | 0.094 | % | | | 7,899,256 | | | | 7,899,256 | |

| | | | | | | | | | | | | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | | | | | |

| (Cost $7,899,256) | | | | | | | | | | | 7,899,256 | |

| | | | |

| TOTAL INVESTMENTS (105.80%) | | | |

| (Cost $149,123,282) | | $ | 147,226,502 | |

| | | | | |

| Liabilities in Excess of Other Assets (-5.80%)(e) | | | (8,060,032 | ) |

| NET ASSETS (100.00%) | | $ | 139,166,470 | |

| See Notes to Financial Statements. | |

| Annual Report | July 31, 2020 | 11 |

| RiverNorth Opportunities Fund, Inc. | Statement of Investments |

| | July 31, 2020 |

SCHEDULE OF SECURITIES SOLD SHORT

| Description | | Shares | | | Value

(Note 2) | |

| EXCHANGE TRADED FUNDS - COMMON SHARES (-10.45%) | | | | | | | | |

| PowerShares Senior Loan Portfolio | | | (223,296 | ) | | $ | (4,832,126 | ) |

| iShares® iBoxx $ High Yield Corporate Bond Fund | | | (16,644 | ) | | | (1,421,231 | ) |

| SPDR Bloomberg Barclays High Yield Bond ETF | | | (50,000 | ) | | | (5,305,000 | ) |

| SPDR Bloomberg Barclays Short Term High Yield Bond ETF | | | (114,385 | ) | | | (2,979,729 | ) |

| | | | | | | | | |

| TOTAL EXCHANGE TRADED FUNDS - COMMON SHARES | | | | | | | (14,538,086 | ) |

| | | | | | | | | |

| TOTAL SECURITIES SOLD SHORT | | | | | | | | |

| (Proceeds $14,515,352) | | | | | | $ | (14,538,086 | ) |

| (a) | All or a portion of the security is pledged as collateral for securities sold short. As of July 31, 2020, the aggregate market value of those securities was $8,721,139 representing 6.27% of net assets. |

| (b) | On May 27, 2020 the Fund announced that it intended to dissolve, liquidate and distribute its net assets to shareholders. The first liquidating distribution was received subsequent to July 31, 2020. |

| (c) | Restricted security (see Note 7) |

| (d) | Non-income producing security. |

| (e) | Includes cash, in the amount of $14,837,493 which is being held as collateral for securities sold short. |

| See Notes to Financial Statements. | |

| 12 | www.rivernorthcef.com |

| RiverNorth Opportunities Fund, Inc. | |

| Statement of Assets and Liabilities | July 31, 2020 |

| ASSETS: | | | |

| Investments, at value | | $ | 147,226,502 | |

| Cash | | | 162,340 | |

| Deposit with broker for securities sold short | | | 14,837,493 | |

| Receivable for investments sold | | | 347,311 | |

| Interest receivable | | | 74,902 | |

| Dividends receivable | | | 119,752 | |

| Deferred offering costs (Note 6) | | | 153,635 | |

| Prepaid and other assets | | | 28,352 | |

| Total Assets | | | 162,950,287 | |

| | | | | |

| LIABILITIES: | | | | |

| Securities sold short (Proceeds $14,515,352) | | | 14,538,086 | |

| Loan payable (Note 4) | | | 7,500,000 | |

| Payable for borrowing | | | 3,969 | |

| Payable for investments purchased | | | 1,422,719 | |

| Payable to adviser | | | 127,357 | |

| Payable to administrator | | | 45,999 | |

| Accrued offering costs (Note 6) | | | 17,211 | |

| Payable to transfer agent | | | 11,796 | |

| Payable for director fees | | | 34,423 | |

| Payable for custodian fees | | | 8,295 | |

| Payable for professional fees | | | 57,729 | |

| Payable for printing fees | | | 12,907 | |

| Other payables | | | 3,326 | |

| Total Liabilities | | | 23,783,817 | |

| Net Assets | | $ | 139,166,470 | |

| | | | | |

| NET ASSETS CONSIST OF: | | | | |

| Paid-in capital | | $ | 145,581,792 | |

| Total distributable earnings/(accumulated deficit) | | | (6,415,322 | ) |

| Net Assets | | $ | 139,166,470 | |

| | | | | |

| PRICING OF SHARES: | | | | |

| Net Assets | | $ | 139,166,470 | |

| Shares of common stock outstanding (37,500,000 of shares authorized, at $0.0001 par value per share) | | | 9,348,465 | |

| Net asset value per share | | $ | 14.89 | |

| | | | | |

| Cost of Investments | | $ | 149,123,282 | |

| See Notes to Financial Statements. | |

| Annual Report | July 31, 2020 | 13 |

| RiverNorth Opportunities Fund, Inc. | Statement of Operations |

| | For the Year Ended July 31, 2020 |

| INVESTMENT INCOME: | | | |

| Interest | | $ | 280,433 | |

| Dividends | | | 6,146,509 | |

| Total Investment Income | | | 6,426,942 | |

| | | | | |

| EXPENSES: | | | | |

| Investment advisory fees | | | 1,432,725 | |

| Administration fees | | | 235,840 | |

| Transfer agent fees | | | 25,661 | |

| Dividend expense - short sales | | | 623,801 | |

| Interest expense on loan | | | 74,202 | |

| Commitment fee on loan | | | 17,500 | |

| Audit and tax fees | | | 24,000 | |

| Legal fees | | | 111,919 | |

| Custodian fees | | | 34,614 | |

| Director fees | | | 147,207 | |

| Printing fees | | | 59,797 | |

| Insurance fees | | | 25,473 | |

| Other expenses | | | 32,289 | |

| Total Expenses | | | 2,845,028 | |

| Net Investment Income | | | 3,581,914 | |

| | | | | |

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | | | | |

| Net realized gain/(loss) on: | | | | |

| Investments | | | (3,829,377 | ) |

| Securities sold short | | | 275,600 | |

| Long-term capital gains from other investment companies | | | 781,074 | |

| Net realized loss | | | (2,772,703 | ) |

| Net change in unrealized appreciation/depreciation on: | | | | |

| Investments | | | (2,812,413 | ) |

| Securities sold short | | | 59,429 | |

| Net change in unrealized appreciation/depreciation | | | (2,752,984 | ) |

| Net Realized and Unrealized Loss on Investments | | | (5,525,687 | ) |

| Net Decrease in Net Assets Resulting from Operations | | $ | (1,943,773 | ) |

| See Notes to Financial Statements. | |

| 14 | www.rivernorthcef.com |

| RiverNorth Opportunities Fund, Inc. |

| Statements of Changes in Net Assets |

| | | For the

Year Ended

July 31, 2020 | | | For the

Year Ended July 31, 2019 | |

| OPERATIONS: | | | | | | |

| Net investment income | | $ | 3,581,914 | | | $ | 3,648,170 | |

| Net realized gain/(loss) | | | (3,553,777 | ) | | | 1,175,519 | |

| Long-term capital gains from other investment companies | | | 781,074 | | | | 903,836 | |

| Net change in unrealized appreciation/depreciation | | | (2,752,984 | ) | | | 1,181,438 | |

| Net increase/(decrease) in net assets resulting from operations | | | (1,943,773 | ) | | | 6,908,963 | |

| | | | | | | | | |

| TOTAL DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

| From distributable earnings | | | (4,130,066 | ) | | | (6,910,189 | ) |

| From tax return of capital | | | (14,461,878 | ) | | | (7,993,528 | ) |

| Net decrease in net assets from distributions to shareholders | | | (18,591,944 | ) | | | (14,903,717 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS: | | | | | | | | |

| Proceeds from sales of shares, net of offering costs | | | 34,880,752 | | | | 30,737,892 | |

| Dividend Reinvestment | | | 157,190 | | | | 296,814 | |

| Net increase in net assets from capital share transactions | | | 35,037,942 | | | | 31,034,706 | |

| | | | | | | | | |

| Net Increase in Net Assets | | | 14,502,225 | | | | 23,039,952 | |

| | | | | | | | | |

| NET ASSETS: | | | | | | | | |

| Beginning of period | | | 124,664,245 | | | | 101,624,293 | |

| End of period | | $ | 139,166,470 | | | $ | 124,664,245 | |

| | | | | | | | | |

| OTHER INFORMATION: | | | | | | | | |

| Share Transactions: | | | | | | | | |

| Shares outstanding - beginning of period | | | 7,167,356 | | | | 5,330,225 | |

| Shares issued in connection with public offering | | | 2,171,093 | | | | 1,820,311 | |

| Shares issued as reinvestment of dividends | | | 10,016 | | | | 16,820 | |

| Shares outstanding - end of period | | | 9,348,465 | | | | 7,167,356 | |

| See Notes to Financial Statements. | |

| Annual Report | July 31, 2020 | 15 |

| RiverNorth Opportunities Fund, Inc. | Financial Highlights |

| For a share outstanding throughout the periods presented. |

| |

| Net asset value - beginning of period |

| Income/(loss) from investment operations: |

| Net investment income(b) |

| Net realized and unrealized gain/(loss) |

| Total income/(loss) from investment operations |

| Less distributions to shareholders: |

| From net investment income |

| From net realized gains |

| From tax return of capital |

| Total distributions |

| Capital share transactions: |

| Dilutive effect of rights offering |

| Common share offering costs charged to paid-in capital |

| Total capital share transactions |

| Net increase/(decrease) in net asset value |

| Net asset value - end of period |

| Market price - end of period |

| Total Return(g) |

| Total Return - Market Price(g) |

| Supplemental Data: |

| Net assets, end of period (in thousands) |

| Ratios to Average Net Assets (including dividend expense and line of credit expense) |

| Total expenses |

| Net investment income |

| Ratios to Average Net Assets (excluding dividend expense and line of credit expense) |

| Total expenses |

| Net investment income |

| Portfolio turnover rate |

| Borrowings at End of Period |

| Loan Payable (in thousands) |

| Asset Coverage Per $1,000 of loan payable (in thousands)(j) |

| See Notes to Financial Statements. | |

| 16 | www.rivernorthcef.com |

| RiverNorth Opportunities Fund, Inc. | Financial Highlights |

| For a share outstanding throughout the periods presented. |

For the

Year Ended

July 31, 2020 | | | For the

Year Ended

July 31, 2019 | | | For the

Period Ended

July 31, 2018(a) | | | For the

Year Ended

October 31, 2017 | | | For the Period

December 24, 2015

(Commencement of

Operations) to

October 31, 2016 | |

| $ | 17.39 | | | $ | 19.07 | | | $ | 20.48 | | | $ | 19.72 | | | $ | 19.40 | |

| | | | | | | | | | | | | | | | | | | |

| | 0.41 | | | | 0.55 | | | | 0.44 | | | | 0.42 | | | | 0.68 | |

| | (0.56 | ) | | | 0.29 | | | | 0.40 | | | | 2.23 | | | | 1.86 | |

| | (0.15 | ) | | | 0.84 | | | | 0.84 | | | | 2.65 | | | | 2.54 | |

| | | | | | | | | | | | | | | | | | | |

| | (0.51 | ) | | | (0.63 | ) | | | (0.47 | ) | | | (0.53 | ) | | | (1.73 | ) |

| | (0.00 | )(c) | | | (0.41 | ) | | | (1.34 | ) | | | (1.36 | ) | | | (0.45 | ) |

| | (1.60 | ) | | | (1.20 | ) | | | (0.08 | ) | | | — | | | | — | |

| | (2.11 | ) | | | (2.24 | ) | | | (1.89 | ) | | | (1.89 | ) | | | (2.18 | ) |

| | | | | | | | | | | | | | | | | | | |

| | (0.21 | )(d) | | | (0.26 | )(e) | | | (0.32 | )(f) | | | — | | | | — | |

| | (0.03 | ) | | | (0.02 | ) | | | (0.04 | ) | | | — | | | | (0.04 | ) |

| | (0.24 | ) | | | (0.28 | ) | | | (0.36 | ) | | | — | | | | (0.04 | ) |

| | (2.50 | ) | | | (1.68 | ) | | | (1.41 | ) | | | 0.76 | | | | 0.32 | |

| $ | 14.89 | | | $ | 17.39 | | | $ | 19.07 | | | $ | 20.48 | | | $ | 19.72 | |

| $ | 14.81 | | | $ | 17.38 | | | $ | 19.14 | | | $ | 20.50 | | | $ | 19.65 | |

| | (1.75 | %) | | | 3.77 | % | | | 2.56 | % | | | 14.11 | % | | | 13.67 | % |

| | (2.22 | %) | | | 3.33 | % | | | 2.84 | % | | | 14.63 | % | | | 9.87 | % |

| | | | | | | | | | | | | | | | | | | |

| $ | 139,166 | | | $ | 124,664 | | | $ | 101,624 | | | $ | 76,927 | | | $ | 74,036 | |

| | | | | | | | | | | | | | | | | | | |

| | 2.06 | % | | | 2.17 | % | | | 2.07 | %(h) | | | 2.21 | % | | | 1.69 | %(h) |

| | 2.59 | % | | | 3.11 | % | | | 3.03 | %(h) | | | 2.03 | % | | | 4.03 | %(h) |

| | | | | | | | | | | | | | | | | | | |

| | 1.54 | % | | | 1.56 | % | | | 1.72 | %(h) | | | 1.75 | % | | | N/A | |

| | 3.11 | % | | | 3.72 | % | | | 2.68 | %(h) | | | 1.57 | % | | | N/A | |

| | 133 | % | | | 76 | % | | | 74 | %(i) | | | 162 | % | | | 113 | %(i) |

| | | | | | | | | | | | | | | | | | | |

| | 7,500 | | | | — | | | | — | | | | — | | | | — | |

| | 19,556 | | | | — | | | | — | | | | — | | | | — | |

| See Notes to Financial Statements. | |

| Annual Report | July 31, 2020 | 17 |

| RiverNorth Opportunities Fund, Inc. | Financial Highlights |

| For a share outstanding throughout the periods presented. |

| (a) | Effective July 16, 2018, the Board approved changing the fiscal year-end of the Fund from October 31 to July 31. |

| (b) | Calculated using average shares throughout the period. |

| (c) | Less than ($0.005) per share. |

| (d) | Represents the impact of the Fund's rights offering of 2,163,193 common shares in November 2019 at a subscription price per share based on a formula. For more details please refer to Note 6 of the Notes to Financial Statements. |

| (e) | Represents the impact of the Fund's rights offering of 1,790,000 common shares in November 2018 at a subscription price per share based on a formula. For more details please refer to Note 6 of the Notes to Financial Statements. |

| (f) | Represents the impact of the Fund's rights offering of 1,564,710 common shares in November 2017 at a subscription price per share based on a formula. For more details please refer to Note 6 of the Notes to Financial Statements. |

| (g) | Total investment return is calculated assuming a purchase of a common share at the opening on the first day and a sale at closing on the last day of each period reported. For purposes of this calculation, dividends and distributions, if any, are assumed to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment returns do not reflect brokerage commissions, if any. Periods less than one year are not annualized. |

| (h) | Annualized. |

| (i) | Not annualized. |

| (j) | Calculated by subtracting the Fund's total liabilities (excluding the principal amount of Loan Payable) from the Fund's total assets and dividing by the principal amount of the Loan Payable and then multiplying by $1,000. |

| See Notes to Financial Statements. | |

| 18 | www.rivernorthcef.com |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

1. ORGANIZATION

RiverNorth Opportunities Fund, Inc. (the “Fund”) is a Maryland corporation registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Fund’s investment objective is total return consisting of capital appreciation and current income. The Fund seeks to achieve its investment objective by pursuing a tactical asset allocation strategy and opportunistically investing under normal circumstances in closed-end funds and exchange-traded funds (“ETFs” and collectively, “Underlying Funds”) with a focus on risk-adjusted returns. Underlying Funds also may include business development companies (“BDCs”) and special purpose acquisition companies (“SPACs”). All Underlying Funds are registered under the Securities Act of 1933, as amended (the “Securities Act”). The Fund incurs higher and additional expenses when it invests in Underlying Funds. There is also the risk that the Fund may suffer losses due to the investment practices or operations of the Underlying Funds. To the extent that the Fund invests in one or more Underlying Funds that concentrate in a particular industry, the Fund would be vulnerable to factors affecting that industry and the concentrating Underlying Funds’ performance, and that of the Fund, may be more volatile than Underlying Funds that do not concentrate. In addition, one Underlying Fund may purchase a security that another Underlying Fund is selling.

The Fund may be converted to an open-end investment company at any time if approved by two-thirds of the Fund's Board of Directors (the "Board") and at least two-thirds of the Fund’s total outstanding shares. If the Fund converted to an open-end investment company, it would be required to redeem all preferred stock of the Fund then outstanding (requiring in turn that it liquidate a portion of its investment portfolio). Conversion to open-end status could also require the Fund to modify certain investment restrictions and policies. The Board may at any time (but is not required to) propose conversion of the Fund to open-end status, depending upon its judgment regarding the advisability of such action in light of circumstances then prevailing.

The Fund’s Articles of Amendment and Restatement ("Charter") provides that, during calendar year 2021, the Fund will call a shareholder meeting for the purpose of voting to determine whether the Fund should convert to an open-end management investment company (such meeting date, as may be adjourned, the “Conversion Vote Date”). Such shareholder meeting may be adjourned or postponed in accordance with the By-Laws of the Fund to a date in calendar year 2021. A vote on such Conversion Vote Date to convert the Fund to an open-end management investment company under the Declaration requires approval by a majority of the Fund’s total outstanding shares. A majority is defined as greater than 50% of the Fund’s total outstanding shares. If approved by shareholders on the Conversion Vote Date, the Fund will seek to convert to an open-end management investment company within 12 months of such approval. If the requisite number of votes to convert the Fund to an open-end management investment company is not obtained on the Conversion Vote Date, the Fund will continue in operation as a closed-end management investment company.

Under normal circumstances, the Fund intends to maintain long positions in Underlying Funds, but may engage in short sales for investment purposes. When the Fund engages in a short sale, it sells a security it does not own and, to complete the sale, borrows the same security from a broker or other institution. The Fund may benefit from a short position when the shorted security decreases in value.

| Annual Report | July 31, 2020 | 19 |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

2. SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates: The preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures, including the disclosure of contingent assets and liabilities, in the financial statements during the period reported. Management believes the estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the Fund ultimately realizes upon sale of the securities. The Fund is considered an investment company under GAAP and follows the accounting and reporting guidance applicable to investment companies in the Financial Accounting Standards Board Accounting Standards Codification Topic 946. The financial statements have been prepared as of the close of the New York Stock Exchange (“NYSE”) on July 31, 2020.

Portfolio Valuation: The net asset value per share of the Fund is determined daily, on each day that the NYSE is open for trading, as of the close of regular trading on the NYSE (normally 4:00 p.m. New York time). The Fund’s net asset value per share is calculated by dividing the value of the Fund’s total assets, less its liabilities by the number of shares outstanding.

The Board has established the following procedures for valuation of the Fund’s assets under normal market conditions. Marketable securities listed on foreign or U.S. securities exchanges generally are valued at closing sale prices or, if there were no sales, at the mean between the closing bid and ask prices on the exchange where such securities are primarily traded. Fixed income securities, including corporate bonds and convertible corporate bonds are normally valued on the basis of quotes obtained from brokers and dealers or independent pricing services. If the independent primary or secondary pricing service is unable to provide a price for a security, if the price provided by the independent primary or secondary pricing service is deemed unreliable, or if events occurring after the close of the market for a security but before the time as of which the Fund values its shares would materially affect net asset value, such security will be valued at its fair value as determined in good faith under procedures approved by the Board.

When applicable, fair value of an investment is determined by the Fund’s Fair Valuation Committee as a designee of the Board. In fair valuing the Fund’s investments, consideration is given to several factors, which may include, among others, the following: the fundamental business data relating to the issuer, borrower, or counterparty; an evaluation of the forces which influence the market in which the investments are purchased and sold; the type, size and cost of the investment; the information as to any transactions in or offers for the investment; the price and extent of public trading in similar securities (or equity securities) of the issuer, or comparable companies; the coupon payments, yield data/cash flow data; the quality, value and saleability of collateral, if any, securing the investment; the business prospects of the issuer, borrower, or counterparty, as applicable, including any ability to obtain money or resources from a parent or affiliate and an assessment of the issuer’s, borrower’s, or counterparty’s management; the prospects for the industry of the issuer, borrower, or counterparty, as applicable, and multiples (of earnings and/or cash flow) being paid for similar businesses in that industry; one or more independent broker quotes for the sale price of the portfolio security; and other relevant factors.

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

Securities Transactions and Investment Income: Investment security transactions are accounted for on a trade date basis. Dividend income is recorded on the ex-dividend date. Interest income, which includes accretion of discounts and amortization of premiums, is accrued and recorded as earned. Realized gains and losses from securities transactions and unrealized appreciation and depreciation of securities are determined using the specific identification method for both financial reporting and tax purposes.

Fair Value Measurements: Investments in the Fund are recorded at their estimated fair value. The Fund discloses the classification of its fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments.

These inputs are categorized in the following hierarchy under applicable financial accounting standards:

| | Level 1 – | Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

| | Level 2 – | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and |

| | Level 3 – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. |

| Annual Report | July 31, 2020 | 21 |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

The following is a summary of the inputs used to value the Fund’s investments as of July 31, 2020:

| Investments in Securities at Value | | Level 1 -

Quoted Prices | | | Level 2 -

Other Significant

Observable

Inputs | | | Level 3 -

Significant

Unobservable

Inputs | | | Total | |

| Closed-End Funds - Common Shares | | $ | 89,486,300 | | | $ | 2,609,145 | | | $ | — | | | $ | 92,095,445 | |

| Business Development Companies - Common Shares | | | 10,474,077 | | | | — | | | | — | | | | 10,474,077 | |

| Business Development Company Notes | | | 8,346,687 | | | | — | | | | — | | | | 8,346,687 | |

| Convertible Corporate Bonds | | | — | | | | 4,600,290 | | | | — | | | | 4,600,290 | |

| Corporate Bonds | | | — | | | | 645,752 | | | | — | | | | 645,752 | |

| Special Purpose Acquisition Companies - Common Shares | | | 22,172,029 | | | | 458,560 | | | | — | | | | 22,630,589 | |

| Rights | | | 74,534 | | | | — | | | | — | | | | 74,534 | |

| Warrants | | | 459,872 | | | | — | | | | — | | | | 459,872 | |

| Short-Term Investments | | | 7,899,256 | | | | — | | | | — | | | | 7,899,256 | |

| Total | | $ | 138,912,755 | | | $ | 8,313,747 | | | $ | — | | | $ | 147,226,502 | |

| Other Financial Instruments | | | | | | | | | | | | | | | | |

| Liabilities: | | | | | | | | | | | | | | | | |

| Securities Sold Short | | | | | | | | | | | | | | | | |

| Exchange Traded Funds - Common Shares | | $ | (14,538,086 | ) | | $ | — | | | $ | — | | | $ | (14,538,086 | ) |

| Total | | $ | (14,538,086 | ) | | $ | — | | | $ | — | | | $ | (14,538,086 | ) |

The Fund did not have any securities that used significant unobservable inputs (Level 3) in determining fair value, and there were no transfers into or out of Level 3, during the year.

Short Sale Risks: The Fund and the Underlying Funds may engage in short sales. A short sale is a transaction in which a fund sells a security it does not own in anticipation that the market price of that security will decline. To establish a short position, a fund must first borrow the security from a broker or other institution. The fund may not always be able to borrow a security at a particular time or at an acceptable price. Accordingly, there is a risk that a fund may be unable to implement its investment strategy due to the lack of available securities or for other reasons. After selling a borrowed security, a fund is obligated to “cover” the short sale by purchasing and returning the security to the lender at a later date. The Fund and the Underlying Funds cannot guarantee that the security will be available at an acceptable price. Positions in shorted securities are speculative and more risky than long positions (purchases) in securities because the maximum sustainable loss on a security purchased is limited to the amount paid for the security plus the transaction costs, whereas there is no maximum attainable price of the shorted security. Therefore, in theory, securities sold short have unlimited risk. Short selling will also result in higher transaction costs (such as interest and dividends), and may result in higher taxes, which reduce a fund’s return.

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

Special Purpose Acquisition Company Risk: The Fund may invest in SPACs. SPACs are collective investment structures that pool funds in order to seek potential acquisition opportunities. Unless and until an acquisition is completed, a SPAC generally invests its assets (less an amount to cover expenses) in U.S. Government securities, money market fund securities and cash. SPACs and similar entities may be blank check companies with no operating history or ongoing business other than to seek a potential acquisition. Certain SPACs may seek acquisitions only in limited industries or regions. If an acquisition that meets the requirements for the SPAC is not completed within a predetermined period of time, the invested funds are returned to the entity’s shareholders. Investments in SPACs may be illiquid and/or be subject to restrictions on resale.

Private Debt Risk: The Fund may invest in notes issued by private funds (“private debt”). Private debt often may be illiquid and is typically not listed on an exchange and traded less actively than similar securities issued by public funds. For certain private debt, trading may only be possible through the assistance of the broker who originally brought the security to the market and has a relationship with the issuer. Due to the limited trading market, independent pricing services may be unable to provide a price for private debt, and as such the fair value of the securities may be determined in good faith under procedures approved by the Board, which typically will include the use of one or more independent broker quotes.

Rights and Warrants Risks: Warrants are securities giving the holder the right, but not the obligation, to buy the stock of an issuer at a given price (generally higher than the value of the stock at the time of issuance) during a specified period or perpetually. Warrants do not carry with them the right to dividends or voting rights with respect to the securities that they entitle their holder to purchase and they do not represent any rights in the assets of the issuer. As a result, warrants may be considered to have more speculative characteristics than certain other types of investments. In addition, the value of a warrant does not necessarily change with the value of the underlying securities and a warrant ceases to have value if it is not exercised prior to its expiration date.

Rights are usually granted to existing shareholders of a corporation to subscribe to shares of a new issue of common stock before it is issued to the public. The right entitles its holder to buy common stock at a specified price. Rights have similar features to warrants, except that the life of a right is typically much shorter, usually a few weeks.

During the year ended July 31, 2020, the Fund invested in rights and warrants, which are disclosed in the Statement of Investments.

| Annual Report | July 31, 2020 | 23 |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

The effect of derivative instruments on the Statement of Assets and Liabilities as of July 31, 2020:

| | | Asset Derivatives | | | |

| | | Statement of Assets and Liabilities | | | |

| Risk Exposure | | Location | | Value | |

| Equity Contracts (Rights) | | Investments, at value | | $ | 74,534 | |

| Equity Contracts (Warrants) | | Investments, at value | | | 459,872 | |

| | | | | $ | 534,406 | |

The effect of derivative instruments on the Statement of Operations for the year ended July 31, 2020:

| Risk Exposure | | Statement of Operations Location | | Realized

Gain/(Loss)

on Derivatives | | | Change in

Unrealized

Appreciation/

(Depreciation)

on Derivatives | |

| Equity Contracts (Rights) | | Net realized gain/(loss) on investments/ Net change in unrealized appreciation/depreciation on investments | | $ | (4,772 | ) | | $ | 39,878 | |

| Equity Contracts (Warrants) | | Net realized gain/(loss) on investments/ Net change in unrealized appreciation/depreciation on investments | | | 1,427,480 | | | | 126,266 | |

| Total | | | | $ | 1,422,708 | | | $ | 166,144 | |

The Fund’s average value of rights and warrants held for the year ended July 31, 2020 were $79,942 and $513,432 respectively.

Other: The Fund holds certain investments which pay dividends to their shareholders based upon available funds from operations. It is possible for these dividends to exceed the underlying investments’ taxable earnings and profits resulting in the excess portion of such dividends being designated as a return of capital. Distributions received from investments in securities that represent a return of capital or long-term capital gains are recorded as a reduction of the cost of investments or as a realized gain, respectively.

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

3. INVESTMENT ADVISORY AND OTHER AGREEMENTS

ALPS Advisors, Inc. (“AAI”) serves as the Fund’s investment adviser pursuant to an Investment Advisory Agreement with the Fund. As compensation for its services to the Fund, AAI receives an annual investment advisory fee of 1.00% based on the Fund’s average daily Managed Assets (as defined below). Pursuant to an Investment Sub-Advisory Agreement, AAI has retained RiverNorth Capital Management, LLC (“RiverNorth” or the "Sub-Adviser") as the Fund’s sub-adviser and AAI pays RiverNorth an annual fee of 0.85% based on the Fund’s average daily Managed Assets.

ALPS Fund Services, Inc. (‘‘AFS’’), an affiliate of AAI, serves as administrator to the Fund. Under an Administration, Bookkeeping and Pricing Services Agreement, AFS is responsible for calculating the net asset values, providing additional fund accounting and tax services, and providing fund administration and compliance-related services to the Fund. AFS is entitled to receive a monthly fee, accrued daily based on the Fund’s average Managed Assets, as defined below, plus a fixed fee for completion of certain regulatory filings and reimbursement for certain out-of-pocket expenses.

DST Systems, Inc. (‘‘DST’’), the parent company of AAI and AFS, serves as the Transfer Agent to the Fund. Under the Transfer Agency Agreement, DST is responsible for maintaining all shareholder records of the Fund. DST is entitled to receive an annual minimum fee of $22,500 plus out-ofpocket expenses. DST is a wholly-owned subsidiary of SS&C Technologies Holdings, Inc. (“SS&C”), a publicly traded company listed on the NASDAQ Global Select Market.

The Fund pays no salaries or compensation to its officers or to interested Directors employed by the Adviser or Sub-Adviser. For their services, the Directors of the Fund, which are not affiliated with the Adviser or Sub-Adviser, receive an annual retainer in the amount of $17,000, an additional $2,000 for attending each meeting of the Board and $1,000 for attending a special meeting of the Board. In addition, the Independent Chairman receives an additional $10,000 annually. The Directors, which are not affiliated with the Adviser or Sub-Adviser, are also reimbursed for all reasonable out-of-pocket expenses relating to attendance at meetings of the Board.

Certain officers of the Fund are also employees of AAI and AFS. A Director is an officer of RiverNorth.

Managed Assets: For these purposes, the term Managed Assets is defined as the total assets of the Fund, including assets attributable to leverage, minus liabilities (other than debt representing leverage and any preferred stock that may be outstanding), calculated as of 4:00 p.m. Eastern time on such day or as of such other time or times as the Board may determine in accordance with the provisions of applicable law and of the declaration and bylaws of the Fund and with resolutions of the Board as from time to time in force.

| Annual Report | July 31, 2020 | 25 |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

4. LEVERAGE

The Fund may use leverage for investment purposes, which may include the use of borrowings, the issuance of preferred stock, and/or the use of derivatives or other transactions that may provide leverage (such as the investment of proceeds received from selling securities short). The Fund may utilize leverage in an aggregate amount of up to 15% of the Fund’s Managed Assets immediately after such borrowings or issuance. However, the Fund is not required to decrease its use of leverage if leverage exceeds 15%, but is less than 20% of the Fund’s Managed Assets due solely to changes in market conditions. Based on market conditions at the time, the Fund may use such leverage in amounts that represent less than 15% of the Fund’s Managed Assets. The Sub-Adviser will assess whether or not to engage in leverage based on its assessment of conditions in the debt and credit markets. Leverage, if used, may take the form of a borrowing or the issuance of preferred stock, although the Fund currently anticipates that leverage will primarily be obtained through the use of bank borrowings or other similar term loans.

The provisions of the 1940 Act further provide that the Fund may borrow or issue notes or debt securities in an amount up to 33 1/3% of its total assets or may issue preferred shares in an amount up to 50% of the Fund’s total assets (including the proceeds from leverage). Notwithstanding each of the limits discussed above, the Fund may enter into derivatives or other transactions (e.g., total return swaps) that may provide leverage (other than through borrowings or the issuance of preferred stock), but which are not subject to the above foregoing limitations, if the Fund earmarks or segregates liquid assets (or enters into offsetting positions) in accordance with applicable SEC regulations and interpretations to cover its obligations under those transactions and instruments. However, these transactions will entail additional expenses (e.g., transaction costs) which will be borne by the Fund.

If the net rate of return on the Fund’s investments purchased with the leverage proceeds exceeds the interest or dividend rate payable on the leverage, such excess earnings will be available to pay higher dividends to the Fund’s stockholders. If the net rate of return on the Fund’s investments purchased with leverage proceeds does not exceed the costs of leverage, the return to stockholders will be less than if leverage had not been used. The use of leverage magnifies gains and losses to stockholders. Since the stockholders pay all expenses related to the issuance of debt or use of leverage, any use of leverage would create a greater risk of loss for stockholders than if leverage is not used. There can be no assurance that a leveraging strategy will be successful during any period in which it is employed.

The Fund has entered into a $15,000,000 secured committed line of credit agreement with State Street Bank and Trust Company (“SSB”), which by its terms expires on November 25, 2020, subject to the restrictions and terms of the credit agreement. As of July 31, 2020, the Fund has drawn down $7,500,000 from the SSB line of credit at an interest rate of 1.18%. For borrowing under this credit agreement, the Fund will be charged either an interest rate of:

| (1) | 1.00% (per annum) plus LIBOR (London Interbank Offered Rate) |

or

| (2) | as of any day, the higher of (a) 1.05% (per annum) plus the daily Federal Funds Rate as in effect on that day, or (b) 1.05% (per annum) plus the One-Month LIBOR as in effect on that day. |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

For borrowing under this credit agreement, the commitment fee on the daily unused loan balance of the line of credit accrues at a rate of 0.25%. The Fund pledges its investment securities as the collateral for the line of credit per the terms of the agreement. The average annualized interest rate charged, the average and the maximum outstanding loan payable for the year ended July 31, 2020 was as follows:

| Average Interest Rate* | | | 1.41 | % |

| Average Outstanding Loan Payable* | | $ | 14,172,794 | |

| Maximum Outstanding Loan Payable | | $ | 15,000,000 | |

| * | The average is calculated based on the actual number of days with an outstanding loan payable. |

5. DISTRIBUTIONS

The Fund intends to make regular monthly distributions to stockholders at a constant and fixed (but not guaranteed) rate that is reset annually to a rate equal to a percentage of the average of the Fund’s NAV per share (the “Distribution Amount”), as reported for the final five trading days of the preceding calendar year (the “Distribution Rate Calculation”). The Distribution Amount is set by the Board and may be adjusted from time to time. The Fund’s intention is that monthly distributions paid to stockholders throughout a calendar year will be at least equal to the Distribution Amount (plus any additional amounts that may be required to be included in a distribution for federal or excise tax purposes) and that, on the close of the calendar year, the Distribution Amount applicable to the following calendar year will be reset based upon the new results of the Distribution Rate Calculation.

Dividends and distributions may be payable in cash or shares of common stock, with stockholders having the option to receive additional common stock in lieu of cash. The Fund may at times, in its discretion, pay out less than the entire amount of net investment income earned in any particular period and may at times pay out such accumulated undistributed income in addition to net investment income earned in other periods in order to permit the fund to maintain a more stable level of distributions. As a result, the dividend paid by the Fund to common stockholders for any particular period may be more or less than the amount of net investment income earned by the Fund during such period. Any distribution that is treated as a return of capital generally will reduce a shareholder’s basis in his or her shares, which may increase the capital gain or reduce the capital loss realized upon the sale of such shares. Any amounts received in excess of a shareholder’s basis are generally treated as capital gain, assuming the shares are held as capital assets. The Fund’s ability to maintain a stable level of distributions to stockholders will depend on a number of factors, including the stability of income received from its investments and the costs of any leverage. As portfolio and market conditions change, the amount of dividends on the Fund’s common stock could change. For federal income tax purposes, the Fund is required to distribute substantially all of its net investment income each year to both reduce its federal income tax liability and to avoid a potential federal excise tax. The Fund intends to distribute all realized net capital gains, if any, at least annually.

| Annual Report | July 31, 2020 | 27 |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

6. CAPITAL TRANSACTIONS

The Fund’s authorized capital stock consists of 37,500,000 shares of common stock, $0.0001 par value per share, all of which is initially classified as common shares. Under the rules of the NYSE applicable to listed companies, the Fund is required to hold an annual meeting of stockholders in each year.

Under the Fund’s Charter, the Board is authorized to classify and reclassify any unissued shares of stock into other classes or series of stock and authorize the issuance of shares of stock without obtaining stockholder approval. Also, the Fund’s Board, with the approval of a majority of the entire Board, but without any action by the stockholders of the Fund, may amend the Fund’s Charter from time to time to increase or decrease the aggregate number of shares of stock of the Fund or the number of shares of stock of any class or series that the Fund has authority to issue.

The Fund issued 3,755,155 common shares in its initial public offering on December 24, 2015. These common shares were issued at $20.00 per share before the underwriting discount of $0.60 per share. Offering costs of $150,206 (representing $0.04 per common share) were offset against proceeds of the offerings and have been charged to paid-in capital of the common shares. AAI and RiverNorth agreed to pay those offering costs of the Fund (other than the sales load) that exceeded $0.04 per common share.

During the period ended July 31, 2018, and the years ended July 31, 2019 and July 31, 2020, the Board approved rights offerings to participating shareholders of record who were allowed to subscribe for new common shares of the Fund. Record date shareholders received one right for each common share held on the respective record dates. For every three rights held, a holder of the rights was entitled to buy one new common share of the Fund. Record date shareholders who fully exercised all rights initially issued to them in the primary subscription were entitled to buy those common shares that were not purchased by other record date shareholders. The Fund issued new shares of common stock at a subscription price that represents 95% of the market price per share, based on the average of the last reported sales price on the NYSE for the five trading days preceding the respective rights’ expiration date, for the October 12, 2017 rights offering. The Fund issued new shares of common stock at 95% of NAV per share for the October 4, 2018 and September 30, 2019 rights offerings. Offering costs were charged to paid-in-capital upon the exercise of the rights.

The shares of common stock issued, subscription price, and offering costs for the rights offerings were as follows:

| Record Date | | Expiration Date | | Shares of

common stock

issued | | | Subscription

price | | | Offering costs | |

| October 12, 2017 | | November 9, 2017 | | | 1,564,710 | | | $ | 19.54 | | | $ | 214,591 | |

| October 4, 2018 | | November 1, 2018 | | | 1,790,000 | | | $ | 16.93 | | | $ | 143,537 | |

| September 30, 2019 | | November 1, 2019 | | | 2,163,193 | | | $ | 16.20 | | | $ | 280,908 | |

On August 31, 2018, the Fund entered into a sales agreement with Jones Trading Institutional Services LLC (“Jones”), under which the Fund may from time to time offer and sell up to 3,300,000 of the Fund’s common stock in an "at-the-market" offering.

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

The shares of common stock issued, gross proceeds from the sale of shares, and commissions to Jones were as follows:

| Year Ended | | | Shares of common

stock issued | | | Gross

Proceeds | | | Commissions | | | Net Proceeds | |

| July 31, 2019 | | | | 30,311 | | | $ | 593,443 | | | $ | 7,424 | | | $ | 586,019 | |

| July 31, 2020 | | | | 7,900 | | | $ | 120,939 | | | $ | 1,513 | | | $ | 119,426 | |

Offering costs incurred through July 31, 2020 as a result of the Fund's shelf registration statement initially effective with the SEC on July 26, 2018 are approximately $588,862. The Fund's 2018 and 2019 rights offerings and the at-the-market offering were made under this shelf registration statement. Management estimates an additional $208,582 of costs expected to be incurred resulting in total offering costs of approximately $797,444. The Statement of Assets and Liabilities reflects the current offering costs of $153,635 as deferred offering costs. These offering costs, as well as offering costs incurred subsequent to July 31, 2020, will be charged to paid-in-capital upon the issuance of shares.

Additional shares of the Fund may be issued under certain circumstances, including pursuant to the Fund’s Automatic Dividend Reinvestment Plan, as defined within the Fund’s organizational documents. Additional information concerning the Automatic Dividend Reinvestment Plan is included within this report.

7. RESTRICTED SECURITIES

As of July 31, 2020, investments in securities included a security that is considered restricted. Restricted securities are often purchased in private placement transactions, are not registered under the Securities Act of 1933, and may have contractual restrictions on resale.

| Description | | Acquisition

Date | | Cost | | | Value | | | Value as

Percentage of

Net Assets | |

| Business Development Corp. of America | | 12/3/2019 | | $ | 725,000 | | | $ | 645,752 | | | | 0.46 | % |

| TOTAL | | | | $ | 725,000 | | | $ | 645,752 | | | | 0.46 | % |

8. PORTFOLIO INFORMATION

Purchases and Sales of Securities: For the year ended July 31, 2020, the cost of purchases and proceeds from sales of securities, excluding short-term securities, were $203,527,420, and $175,024,181, respectively.

| Annual Report | July 31, 2020 | 29 |

| RiverNorth Opportunities Fund, Inc. | Notes to Financial Statements |

July 31, 2020

9. TAXES

Classification of Distributions: Net investment income/(loss) and net realized gain/(loss) may differ for financial statement and tax purposes. The character of distributions made during the year from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or realized gain was recorded by the Fund.

The tax character of distributions paid during the years ended July 31, 2020 and July 31, 2019 was as follows:

| | | | |

| | | For the Year

Ended July 31, 2020 | |

| Ordinary Income | | $ | 4,006,046 | |

| Tax-Exempt Income | | | 124,020 | |

| Return of Capital | | | 14,461,878 | |

| Total | | $ | 18,591,944 | |

| | | For the Year

Ended July 31, 2019 | |

| Ordinary Income | | $ | 6,436,751 | |

| Tax-Exempt Income | | | 37,551 | |

| Long-Term Capital Gain | | | 435,887 | |

| Return of Capital | | | 7,993,528 | |

| Total | | $ | 14,903,717 | |

Components of Earnings: Tax components of distributable earnings are determined in accordance with income tax regulations which may differ from composition of net assets reported under accounting principles generally accepted in the United States. Accordingly, for the year ended July 31, 2020, certain differences were reclassified. The reclassifications were as follows:

| | |

| Paid-in capital | Total distributable earnings/(accumulated deficit) |

| $(265,093) | $265,093 |