Exhibit 99.53

FORM 51 – 102F2

ANNUAL INFORMATION FORM

Year ended March 31, 2011

June 28, 2011

TABLE OF CONTENTS

| FORWARD LOOKING STATEMENTS | 1 |

| MINERAL RESERVE AND RESOURCE ESTIMATES | 1 |

| CORPORATE STRUCTURE | 2 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 2 |

| DESCRIPTION OF THE BUSINESS | 8 |

| Risk Factors | 8 |

| Mineral Properties | 14 |

| DIVIDENDS | 35 |

| CAPITAL STRUCTURE | 35 |

| MARKET FOR SECURITIES | 37 |

| ESCROWED SHARES | 37 |

| DIRECTORS AND OFFICERS | 37 |

| Director and Officer Information | 37 |

| Shareholdings of Directors and Officers | 39 |

| Corporate Cease Trade Orders or Bankruptcies | 39 |

| Penalties or Sanctions | 39 |

| Conflicts of Interest | 40 |

| LEGAL PROCEEDINGS | 40 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 40 |

| REGISTRAR AND TRANSFER AGENT | 40 |

| MATERIAL CONTRACTS | 40 |

| INTEREST OF EXPERTS | 41 |

| AUDIT COMMITTEE INFORMATION | 42 |

| ADDITIONAL INFORMATION | 44 |

-i-

FORWARD LOOKING STATEMENTS

This Annual Information Form (“AIF”) contains forward-looking statements concerning Timmins Gold Corp. (the “Company”) and its plans for its properties and other matters, within the meaning of applicable Canadian securities laws. Forward-looking statements include, but are not limited to, statements with respect to commercial mining operations, anticipated metal recoveries, projected quantities of future metal production, anticipated production rates and mine life, operating efficiencies, capital budgets, costs and expenditures and conversion of mineral resources to proven and probable reserves, analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management.

Statements concerning proven and probable reserves and mineral resource estimates may also be deemed to constitute forward-looking statements to the extent that they involve estimates of the mineralization that will be encountered if the property is developed, and in the case of mineral resources or proven and probable reserves, such statements reflect the conclusion based on certain assumptions that the mineral deposit can be economically exploited. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as "expects" or "does not expect", "is expected", "anticipates" or "does not anticipate", "plans", "estimates" or "intends", or stating that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved) are not statements of historical fact and may be "forward-looking statements." Forward-looking statements are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements.

Some of the important risks and uncertainties that could affect forward looking statements are described in this AIF under "Description of Business – Risk Factors". Should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking statements. Forward-looking statements are made based on management's beliefs, estimates and opinions on the date the statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change. Investors are cautioned against attributing undue certainty to forward-looking statements.

MINERAL RESERVE AND RESOURCE ESTIMATES

All mineral reserve and resource estimates contained in this AIF are calculated in accordance with National Instrument 43-101, Standards of Disclosure for Mineral Projects (“NI 43-101”) of the Canadian Securities Administrators (“CSA”) and Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) Standards. “Indicated mineral resource” and “inferred mineral resource” have a great amount of uncertainty as to their existence and economic and legal feasibility. It cannot be assumed that all or any part of an “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category of resource. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories or in the measured mineral resource category will ever be converted into proven and probable reserves.

1

CORPORATE STRUCTURE

Timmins Gold Corp. was incorporated pursuant to the Business Corporations Act (British Columbia) on March 17, 2005.

The Company’s registered and records office is located at Suite 1900 – 570 Granville Street, Vancouver, British Columbia, V6C 3P1. The Company’s head office and business office is located at Suite 1900 – 570 Granville Street, Vancouver, British Columbia, V6C 3P1. The Company’s head office in Mexico is located at Blvd. Solidaridad #335 A, Edificio ‘A’ – Primera Planta Local 3, Col Palmar del Sol, Hermosillo, Sonora, Mexico, 83270. The Company also maintains field offices at the San Francisco Mine site, near Estacion Llano, Sonora and Magdalena de Kino, Sonora.

The Company has two wholly owned subsidiaries: Timmins Goldcorp Mexico, S.A. de C.V. (“Timmins Mexico”) and Molimentales del Noroeste, S.A. de C.V. (“Molimentales”). Timmins Mexico was incorporated pursuant to the laws of Mexico on March 23, 2005 and is the entity through which the Company conducts its Mexican operations. Molimentales was acquired from Geomaque de Mexico, S.A. de C.V., (“Geomaque”) pursuant to an acquisition agreement dated March 20, 2007, and was incorporated pursuant to the laws of Mexico for the principal purpose of holding the mineral concessions and infrastructure that constitute the San Francisco Gold Mine (the “Mine”).

GENERAL DEVELOPMENT OF THE BUSINESS

Overview

The Company is a gold mining and exploration company engaged in exploration, mine development and the mining and extraction of precious metals, primarily gold. The Company’s primary asset and only material mineral property is the San Francisco Gold Property located in Sonora, Mexico, which includes the Company’s only operating mine (the “Mine”). The Company attained commercial production at the Mine on April 1, 2010 and the ramp-up to full production is proceeding as planned.

The Mine was previously developed and operated by Geomaque. In 2005 the Company entered into an agreement to acquire a 100% interest in the Mine for total consideration of $5.0 million and 10.0 million common shares of the Company. In addition, the Company was required to purchase certain mining and processing equipment for C$4.2 million including Mexican value added tax. Most of the equipment and facilities at the Mine have been refurbished and are being used in operations. As at March 31, 2011, the remaining liability is $1,672,560, with a related restricted cash balance of $1,716,170. See Note 7 of our consolidated financial statement for a description for the amount outstanding.

On March 31, 2008, Micon International Limited, an independent mineral engineering firm, (“Micon”) and Independent Mining Consultants, Inc., an independent mineral engineering firm, (“IMC”) produced an independent pre-feasibility study on the San Francisco Mine entitled NI 43-101 F1 Technical Report on the Preliminary Feasibility Study for the San Francisco Gold Project, Sonora, Mexico (the “Pre-Feasibility Study”). The Pre-Feasibility Study was updated on January 16, 2009. The Pre-Feasibility Study recommended development and re-commissioning of the Mine, and concluded that it was an advanced-stage exploration project with significant economic potential. On November 30, 2010, Micon produced an independent technical report on the Mine entitled NI 43-101 F1 Technical Report – Updated Resources and Reserves and Mine Plan for the San Francisco Gold Mine, Sonora, Mexico, (the “Report”). The Report concluded that the Mine and property merit further exploration and supports the Company’s proposed exploration plans.

2

During fiscal 2008 and 2009 the Company focused its efforts on successfully arranging financing for the construction and re-commissioning of the Mine. During this period, construction of a new secondary and tertiary crushing system at the Mine was completed and testing was undertaken. The gold extraction plant was refurbished and tested, and mine infrastructure for the Mine, including its power supply and connection to civil works, was put in place. In addition, a third drill program was implemented with the objective of expanding the known mineral resources at the Mine. During fiscal 2009 the Company also completed a regional exploration program consisting of geological mapping and sampling, soil geochemistry and ground and airborne geophysics. Work proceeded on the new heap leach pads with liners being placed on the first eight hectares, and emergency pond and channel liners were also installed. During 2009, the assay lab at the Mine became operational and processed samples from drilling activity in support of planning for expansion of the existing open pit. The Company commenced pre-stripping waste in the fourth quarter of 2009, and at that time it also commenced the crushing and leaching of ore.

During fiscal 2010, commercial production began in April and the ramp-up to full production at the Mine proceeded as planned. Based on drill success, and an increased resource estimate provided in November 2010, a decision was made to expand crushing capacity to 18,000 tonnes per day. Additional equipment has been added to achieve the new targeted production level. In order to reach the new production level, three new carbon columns were built, additional water rights have been purchased, a new module has been added to the secondary and tertiary crushers and additional mining equipment has been delivered. Currently three Komatsu shovels, one Caterpillar loader and sixteen 91 tonne Caterpillar trucks are on site for full scale open pit extraction of materials, including ore and waste, at a current average rate of 75,000 tonnes per day. The Company’s targeted level of production of 18,000 tonnes of ore per day to the heap leach pads is expected by July, 2011 as the crusher expansion will be fully operational by that date. See “Production, Reserves and Resources”, below.

The crush size of the ore being stacked on the heap leach pads is 100% less than ½ inch. This crush size is projected to attain recoveries of approximately 70% on average. Leach extraction is proceeding with no visible pooling or channeling. Preliminary indications from early production indicate that the targeted metallurgical recoveries of 70% will be attained. See “Processing”, below.

All mining activities at the Mine are carried out by a mining contractor. The contractor provides all the required mining equipment and personnel required to meet production targets. The Company provides contract supervision, geology, engineering and planning and survey services to the Company’s employees.

3

Production, Reserves and Resources

The table below shows the production rates that have been achieved since the commencement of operations at the Mine.

| | Apr-Jun | | | Jul-Sep | | | Oct-Dec | | | Jan-Mar | | | Total / | |

Category | | 2010 | | | 2010 | | | 2010 | | | 2011 | | | Average | |

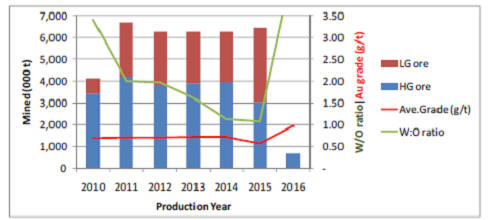

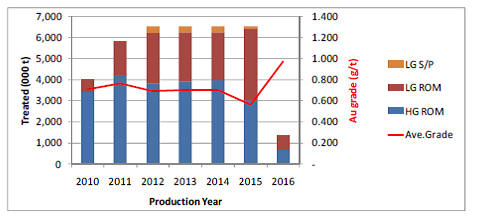

Ore (Dry tonnes) | | 905,296 | | | 1,090,768 | | | 1,208,678 | | | 1,207,339 | | | 4,412,081 | |

Average Grade (g/t Au) | | 0.7180 | | | 0.817 | | | 0.939 | | | 0.895 | | | 0.852 | |

Waste Mined | | 4,077,568 | | | 3,878,015 | | | 4,568,616 | | | 5,096,932 | | | 17,621,131 | |

Total Mined (tonnes) | | 4,982,864 | | | 4,968,783 | | | 5,777,294 | | | 6,304,271 | | | 22,033,212 | |

Strip Ratio | | 4.5 | | | 3.6 | | | 3.8 | | | 4.2 | | | 4.0 | |

Gold ounces Recoverable | | 14,145 | | | 19,374 | | | 25,033 | | | 24,088 | | | 82,640 | |

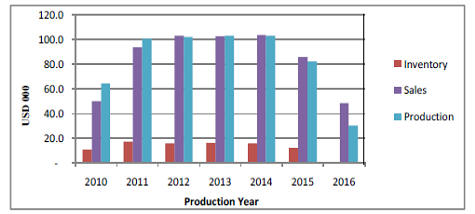

Gold ounces Sold | | 11,319 | | | 15,682 | | | 20,031 | | | 15,730 | | | 62,761 | |

Days | | 91 | | | 92 | | | 92 | | | 90 | | | 365 | |

Average Ore Processed (t/d) | | 9,948 | | | 11,856 | | | 13,138 | | | 13,415 | | | 12,088 | |

Total Mined (t/d) | | 54,757 | | | 54,009 | | | 62,797 | | | 70,047 | | | 60,365 | |

For the twelve months ended March 31, 2011, the Company sold 62,761 ounces of gold and sold 33,874 ounces of silver.

Mineral Resource Estimates

MINERAL RESOURCES THAT ARE NOT MINERAL RESERVES DO NOT HAVE DEMONSTRATED ECONOMIC VIABILITY. IN ADDITION, INFERRED MINERAL RESOURCES ARE CONSIDERED TOO SPECULATIVE GEOLOGICALLY TO HAVE THE ECONOMIC ANALYSIS APPLIED TO THEM THAT WOULD ENABLE THEM TO BE CATEGORIZED AS MINERAL RESERVES. SEE “MINERAL RESERVE AND RESOURCE ESTIMATES”.

In November 2010, following a step out drill program, the Company announced a significant increase in its resource estimate for the Mine. The new resource estimates are illustrated in the table below. The updated mineral resource estimates were completed by Mr. William Lewis, B.Sc. P.Geo and Ing. Alan San Martin, MAusIMM of Micon. The mineral resource estimate was based on a gold price of $1,100 per ounce and a 0.131 g/t gold cutoff grade, and utilizes all drill results available at August 31, 2010.

| | | Resources | | | Ore Grade | | | Contained Gold | |

| Resource Classification | | (000 t) | | | (g/t Au) | | | (oz) | |

| Measured Mineral Resource | | 19,089 | | | 0.797 | | | 489,000 | |

| Indicated Mineral Resource | | 23,044 | | | 0.658 | | | 495,000 | |

| Total | | 42,531 | | | 0.720 | | | 984,000 | |

| | | | | | | | | | |

| Inferred Mineral Resource | | 10,308 | | | 0.628 | | | 208,000 | |

4

Estimates of the mineral resources at the Mine were initially published in the Pre-Feasibility Study. Prior to this, in 2006, the Company engaged IMC to estimate the mineral resources for the Mine using the historical Geomaque data along with the results of the Company’s 2005 and 2006 exploration drilling programs. IMC developed a three-dimensional block model and used floating cone techniques to develop a mineral resource within a constrained pit outline. To fulfill the criterion for potential economic viability, only material lying within a floating cone pit shell at a gold price of $500 per ounce and additional cost and recovery parameters developed by the Company and IMC WAS reported as a mineral resource. The drilling database the Company provided to IMC consists of 1,133 drill holes amounting to 116,000 meters of drilling. There are 62,137 sample intervals of which 61,346 were assayed for gold. The sampling interval is predominantly 2 meters (86% of the intervals), though about 7% of the intervals are 1.5 meters in length, and about 3% of the intervals are 1 meter in length. The initial resource estimates contained in the Pre-Feasibility Study were as follows.

| | | | Resources | | | Gold | | | Contained | |

| | Resource Classification | | (000 t) | | | (g/t Au) | | | Gold (oz) | |

| | Measured Mineral Resource | | 5,352 | | | 0.912 | | | 156,930 | |

| | Indicated Mineral Resource | | 22,296 | | | 0.781 | | | 559,860 | |

| | Total | | 27,648 | | | 0.806 | | | 716,790 | |

| | | | | | | | | | | |

| | Inferred Mineral Resource | | 2,506 | | | 0.788 | | | 63,490 | |

Mineral Reserve Estimate

In November 2010, following a step out drill program, the Company announced a significant increase in its reserve estimate for the Mine, as shown in the table below. This revised reserve estimate constitutes a 28% increase in contained gold from the previous estimate. The updated mineral reserve estimates were completed by Mr. Mani Verma, M.Eng, P.Eng, of Micon. The mineral reserves were based on a gold price of $900 per ounce, a 0.16 g/t gold cutoff grade and a weighted average recovery of 70%. In addition to the tonnages presented below, total waste rock within the final pit outline is estimated at 95.34 million tonnes. The reserve includes a dilution factor of 12% according to the type of mineralization and the size of the blocks modeled.

| Reserve Classification | | Reserves (000 t) | | | Ore Grade (g/t) | | | Contained Gold (oz) | |

| Proven | | 17,194 | | | 0.756 | | | 418,000 | |

| Probable | | 17,738 | | | 0.635 | | | 362,000 | |

| Total | | 34,932 | | | 0.695 | | | 780,000 | |

The table below shows the mineral reserve estimates of the Pre-Feasibility Study. These mineral reserve estimates were made as of February 29, 2008. Micon classified both the measured and indicated mineral resources within the open pit as a probable mineral reserve. In addition to the Mine tonnage, total waste rock within the final pit outline is estimated to be 46.0 Mt, giving a stripping ratio (waste to ore ratio) of 2.0:1.

| | | | | | | Gold | | | | | | | | | | |

| | | | Reserve | | | Cut-Off | | | Reserve | | | Grade | | | Gold | |

| | Case | | Class | | | (g/t) | | | (000 t) | | | (g/t) | | | (000 oz) | |

| | High Grade Crusher Feed | | Probable | | | 0.50 | | | 12,000 | | | 1.05 | | | 403.7 | |

5

| | | | | | Gold | | | | | | | | | | |

| | | Reserve | | | Cut-Off | | | Reserve | | | Grade | | | Gold | |

| Case | | Class | | | (g/t) | | | (000 t) | | | (g/t) | | | (000 oz) | |

| Low Grade Crusher Feed | | Probable | | | 0.23 | | | 4,653 | | | 0.88 | | | 132.0 | |

| Sub-total Crusher Feed | | Probable | | | | | | 16,653 | | | 1.01 | | | 535.7 | |

| Low Grade ROM Leach | | Probable | | | 0.28 | | | 5,981 | | | 0.39 | | | 75.3 | |

| Grand Total | | Probable | | | | | | 22,634 | | | 0.84 | | | 611.0 | |

Strategy

The Company’s activities during the fiscal year ended March 31, 2011 focused on optimizing and expanding the operations at the Mine. The Company continued to maintain its property rights with respect to all of its property interests but did not undertake any significant activity on areas outside of the Mine. Although the Company evaluates other opportunities as they are presented, its principal focus is to increase production at the Mine and generate positive cash flows from operations. The Company also plans to continue its drilling program to seek to expand reserves at the Mine. The drilling conducted during the period from January 1 to June 30, 2010 was concentrated in three areas: (i) northwest of the main ore body, (ii) southeast of the main ore body, and (iii) along the southwest flank of the pit. The additional measured and indicated resources announced in November, 2010 were located contiguous to the northwest, the southeast and the southwest of the existing pit limits. From July 2010 to March 31, 2011, the Company drilled an additional 55,000 meters in the same areas. The Company currently has eight drill rigs operating around the Mine and one drill rig exploring targets outside of the Mine area. The Company is targeting a drilling rate of between 25,000 and 30,000 meters per month for the period from June to the end of December, 2011. The total expenditures for the next phase of exploration, including other related payments such as assays are estimated to be approximately $2.5 million per month which is being funded from cash flow from operations.

Regional exploration on the Company’s 70,000 hectare land package in and around the Mine is also being undertaken. Drill results to date indicate that the zone of mineralization extends to the west, northwest and southeast of the currently defined resource and remains open along strike in each direction and at depth. Regional exploration on the Company’s land holdings in and around the Mine is also being planned.

From July, 2010 to the end of March, 2011, the Company drilled 63,000 meters in the same areas. The Company currently has nine drill rigs (six reverse circulation and three core) operating around the mine and is targeting 25,000 to 30,000 meters of drilling per month for the period from June 30, 2011 to December 31, 2011.

Based on the conclusions of the Report, the Company expects that open pit mining will continue at the Mine until early 2016 and that the Company’s sustaining capital expenditure requirements will be approximately $10.6 million over that period, assuming we achieve production of 18,000 tonnes of ore per day to the heap leach pads.

6

The following table shows a summary of our projected operating costs over the expected life of the Mine, based on the conclusions of the Report:

| | | | | | LOM | | | LOM | |

| | | LOM Total | | | Average | | | Average | |

| | | $ millions | | | $ /t | | | $ /oz Au | |

| Mining costs | | 159.8 | | | 4.79 | | | 297.68 | |

| Crushing costs | | 49.0 | | | 1.47 | | | 91.36 | |

| Leach costs | | 32.4 | | | 0.97 | | | 60.37 | |

| ADR costs | | 8.2 | | | 0.25 | | | 15.22 | |

| Metallurgy and Lab costs | | 2.4 | | | 0.07 | | | 4.53 | |

| General & Admin costs | | 10.7 | | | 0.32 | | | 19.88 | |

| Total operating cost | | 262.5 | | | 7.88 | | | 489.05 | |

Gold Sales

The Company delivers gold and silver in doré form to an internationally respected precious metal refinery in North America where the doré may, at the Company’s option, be converted into London Good Delivery metal, or alternatively, be sold to the refiner. Gold is delivered to the refinery by armoured, insured carriers. If metal is returned to the Company, it is then sold to international bullion dealers.

Expansion Plans

The Company reviews merger and acquisition opportunities on an ongoing basis. In late September, 2010 the Company was unsuccessful in a merger proposal with Capital Gold Corporation. (“Capital Gold”). The Company will continue to review expansion opportunities as they arise.

Financings

During fiscal 2011, the Company did not raise any capital from the issuance of equity or debt instruments.

In June, 2011, subsequent to the end of fiscal 2011, the Company replaced and restructured its debt. Under the previous arrangement, Sprott Asset Management LP, (“SAM”) for and on behalf of certain of the Sprott funds, agreed to provide US$15 million financing in senior secured notes (the “Notes”). The Notes were used to pay down existing debt, and to pay for existing equipment and for general working capital to complete development and the commissioning of operations at the Mine. The Notes were to be repaid in 12 equal monthly installments commencing in August, 2010. Each payment was to be equal to the value at the time of payment of 1,667 ounces of gold (20,004 ounces total). The Noteholders were granted an aggregate of 3 million share purchase warrants exercisable for a period of 24 months at an exercise price of CDN$0.80 per share, 2 million of which remain unexercised.

The new credit agreement with Sprott Resource Lending Partnership LP allowed the Company to deliver the final five payments totaling 8,335 ounces of gold to SAM and has provided a further C$5.6 million in working capital. The new credit agreement provides for a lump sum payment of principal on maturity in 14 months, with interest paid at the rate of 1% per month.

7

During fiscal 2011 the Company received an aggregate of $6,677,222 through the exercise of incentive stock options issued pursuant to the Company’s stock option plan and through the exercise of share purchase warrants issued in connection with previous financings.

DESCRIPTION OF THE BUSINESS

General

The Company is a gold mining and exploration company engaged in exploration, mine development and the mining and extraction of precious metals, primarily gold. The Company’s primary asset and only material mineral property is the Mine located in Sonora, Mexico. In April, 2010 commercial gold production commenced at the Mine. The ramp-up to full production proceeded as planned however the Company has expanded production. Construction of three new carbon columns is complete and the expansion of the crushing systems by the addition of a new module is being tested. Preliminary production statistics for the first year of commercial production were a total of 62,761 ounces of gold and 33,874 ounces of silver sold. Total material moved during the year was 22 million tonnes and total ore mined and crushed during the year was 4.4 million tonnes.

Risk Factors

Financial Capability and Additional Financing

The Company currently has limited financial resources, limited operating income and no assurance that adequate funding will be available to further its exploration and development of its projects. The Company anticipates that from the profitable operation of the Mine, sufficient cash will be generated to fund the activities of the Company in the normal course. Although the Company has been successful in the past in financing its activities through the sale of equity securities, there can be no assurance that it will be able to obtain sufficient financing in the future to carry out exploration and development work on its properties. The ability of the Company to arrange additional financing in the future will depend, in part, on the prevailing capital market conditions as well as the business performance of the Company, especially the Mine.

8

Fluctuating Mineral Prices

The Company’s revenues are expected to be, in large part, derived from the sale of gold, and possibly other by-product or co-product metals. The price of gold and other commodities has fluctuated widely in recent years and is affected by factors beyond the control of the Company including, but not limited to, international economic and political trends, currency exchange fluctuations, economic inflation and expectations for the level of economic inflation in the consuming economies, interest rates, global and local economic health and trends, speculative activities and changes in the supply of gold due to new mine developments, mine closures, as well as advances in various production technologies. All of these factors will impact the viability of the Company’s exploration projects in a manner that is impossible to predict with certainty.

Limited Operating History

The Company was incorporated on March 17, 2005 and completed its IPO in July 2006. Consequently the Company has limited operating history.

No History of Earnings

This is the Company’s first year of commercial operations. Previously, the Company had suffered losses since its inception.

No History of or Dividends

The Company has not paid dividends on its common shares since incorporation and does not anticipate doing so in the foreseeable future. Payment of any future dividends will be at the discretion of the Company’s board of directors after taking into account many factors, including operating results, financial condition and anticipated cash needs.

Political and Regulatory Framework in Mexico

In the past, Mexico has been subject to political instability, changes and uncertainties, which may cause changes to existing governmental regulations affecting mineral exploration and mining activities. The Company's operations and properties are subject to a variety of governmental regulations including worker health and safety, employment standards, waste disposal, protection of historic and archaeological sites, mine development, protection of endangered and protected species and other matters. The Company’s activities relating to the Mine are subject to, among other things, Mexican mining law; regulations promulgated by SEMARNAP, Mexico's environmental protection agency; DCM, the Mexican Department of Economy – Director General of Mines; and the regulations of CONAGUA, the Comision National del Aqua with respect to water rights. Mexican regulators have broad authority to shut down and/or levy fines against facilities that do not comply with regulations or standards. The Company’s mineral exploration and mining activities in Mexico may be adversely affected in varying degrees by changing government regulations relating to the mining industry or shifts in political conditions that increase the costs related to the Company’s activities or maintaining its properties. Operations may also be affected in varying degrees by government regulations with respect to restrictions on production, price controls, export controls, income taxes, expropriation of property, environmental legislation and mine safety. Mexico's status as a developing country may make it more difficult for the Company to obtain the required financing for its projects.

9

Operating in Mexico

The Company’s properties are in Mexico, which is a developing country, and consequently it may be difficult for the Company to obtain the necessary financing for its planned exploration or development activities in Mexico. The Company also hires and plans to hire some of its employees or consultants in Mexico to assist the Company to conduct its operations in accordance with local Mexican law. The Company also plans to purchase certain supplies and retain the services of various companies in Mexico to meet its future business plans. It may be difficult to find or hire qualified people in the mining industry who are situated in Mexico, or to obtain all of the necessary services or expertise in Mexico, or to conduct operations on its projects at reasonable rates. If qualified people and services or expertise cannot be obtained in Mexico, the Company may need to seek and obtain those services from people located outside of Mexico which will require work permits and compliance with applicable laws and could result in delays and higher costs to the Company.

Exploration, Mine Development, Mining and Production

Resource exploration, mine development and the production of metals is a speculative business, characterized by a number of significant risks including, among other things, unprofitable efforts resulting not only from the failure to discover mineral deposits, but also from finding mineral deposits that, though present, are insufficient in quantity and quality to return a profit from production. The production and marketability of minerals acquired or discovered by the Company may be affected by numerous factors which are beyond the control of the Company and which cannot be accurately predicted, such as market fluctuations, the proximity and capacity of milling facilities, the recovery of metals from ore, mineral markets and processing equipment, and such other factors as government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals, and environmental protection, the combination of some or all of which may result in the Company not receiving an adequate return on investment capital.

Most of the Company’s properties are in the exploration and development stages and only the Mine has mineralization considered as a probable mineral reserve pursuant to CIM definitions. Production has commenced at the Mine, however, the Company’s other properties would only be developed if favorable exploration results are obtained. The business of exploration for minerals and mining involves a high degree of risk. Few properties that are explored are ultimately developed into producing mines.

There is no assurance that the Company's future mineral exploration and development activities will result in any additional discoveries of commercial bodies of ore. The long-term profitability of the Company's operations will in part be directly related to the costs and success of its exploration programs, which may be affected by a number of factors. Substantial expenditures are required to establish reserves through drilling and to develop the mining and processing facilities and infrastructure at any site chosen for mining. Although substantial benefits may be derived from the discovery of a major mineralized deposit, no assurance can be given that minerals will be discovered in sufficient quantities to justify commercial operations or that the funds required for development can be obtained on a timely basis.

There is no assurance that the regulatory authorities, including the Toronto Stock Exchange (the “Exchange”) will approve the acquisition of any additional properties by the Company, whether by way of option or otherwise.

Uninsurable Risks

In the course of exploration, development and production of mineral properties, certain risks, and in particular, unexpected or unusual geological operating conditions including rock bursts, cave-ins, fires, flooding and earthquakes may occur. It is not always possible to fully insure against such risks and the Company may decide not to take out insurance against such risks as a result of high premiums or for other reasons. Should such liabilities arise, they could reduce or eliminate any future profitability and result in increasing costs and a decline in the value of the securities of the Company.

10

Environmental and Safety Regulations and Risks

Environmental laws and regulations may affect the operations of the Company. These laws and regulations set various standards regulating certain aspects of health and environmental quality. They provide for penalties and other liabilities for the violation of such standards and establish, in certain circumstances, obligations to rehabilitate current and former facilities and locations where operations are or were conducted. Furthermore, the permission to operate could be withdrawn temporarily where there is evidence of serious breaches of health and safety, or even permanently, in the case of extreme breaches. Significant liabilities could be imposed on the Company for damages, clean-up costs or penalties in the event of certain discharges into the environment, environmental damage caused by previous owners of acquired properties or noncompliance with environmental laws or regulations. In all major developments, the Company generally relies on recognized designers and construction firms from which the Company will, in the first instance, seek indemnities. In addition, the Company intends to minimize these risks by taking steps to ensure compliance with environmental, health and safety laws and regulations, and operating to international environmental standards. There is also a risk that the environmental laws and regulations in Mexico become more onerous, making the Company’s operations in that country more expensive.

Mining Titles

The ability of the Company to carry out successful mining activities will depend on a number of factors, one of the most critical factors being its ability to obtain tenure to its properties to the satisfaction of international lending institutions. The issue of any such licenses must be in accordance with Mexican law and, in particular, the relevant mining legislation. No guarantee can be given that these tenures will be granted to the Company, or if they are granted, that the Company will be in a position to comply with all conditions that are imposed. Furthermore, while it is common practice that permits and licenses may be renewed or transferred into other forms of licenses appropriate for ongoing operations, no guarantee can be given that a renewal or a transfer will be granted to the Company or, if they are granted, that the Company will be in a position to comply with all conditions that are imposed.

The Company is satisfied, based on its due diligence that its rights to the properties are valid and exist. There can be no assurance, however, that the Company’s rights will not be challenged by third parties claiming an interest in the properties.

Mineral Reserves and Resources Estimates

The mineral reserves and resources estimates in this AIF and disclosed by the Company in general are only estimates and no assurance can be given that any particular level of recovery of minerals will be realized. The Company relies on laboratory-based recovery models to project estimated recoveries by ore type at optimal crush sizes. Actual gold recoveries in a commercial heap leach operation may exceed or fall short of projected laboratory test results. In addition, the grade of mineralization ultimately mined may differ from the one indicated by the drilling results and the difference may be material. Production can be affected by such factors as permitting regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations, inaccurate or incorrect geological, metallurgical or engineering work and work interruptions, among other things. Short term factors, such as the need for an orderly development of deposits or the processing of new or different grades, may have an adverse effect on mining operations or the results of those operations.

11

There can be no assurance that minerals recovered in small scale laboratory tests will be duplicated in large scale tests under on-site conditions or in production scale operations. Material changes in proven and probable reserves or resources, grades, waste-to-ore ratios or recovery rates may affect the economic viability of projects. The estimated proven and probable reserves and resources disclosed by the Company should not be interpreted as assurances of mine life ore of the profitability of future operations.

The Company has engaged expert independent technical consultants to advise it on, among other things, mineral reserves and resources and project engineering at the Mine. The Company believes these experts are competent and that they have and will carry out their work in accordance with all internationally recognized industry standards. If, however, the work conducted and to be conducted by these experts is ultimately found to be incorrect or inadequate in any material respect, the Company may experience delays and increased costs.

Production Estimates

The Company prepares estimates of mine production for the Mine in Mexico. The Company cannot give any assurance that it will achieve its production estimates. The failure of the Company to achieve its production estimates could have a material and adverse effect on any or all of its future cash flows, results of operations and financial condition. These production estimates are dependent on, among other things, the accuracy of mineral reserve estimates, the accuracy of assumptions regarding ore grades and recovery rates, ground conditions and physical characteristics of ores and the accuracy of estimates rates and costs of mining and processing.

The Company’s actual production may vary from its estimates for a variety of reasons, including: actual ore mined varying from estimates of grade, tonnage, dilution and metallurgical and other characteristics; short-term operating factors such as the need for sequential development of ore bodies and the processing of new or different ore grades from those planned; mine failures, slope failures or equipment failures; industrial accidents; natural phenomena such as inclement weather conditions, floods, droughts, rock slides and earthquakes; encountering unusual or unexpected geological conditions; changes in power costs and potential power shortages; shortages of principal supplies needed for operation, including explosives, fuels, chemical reagents, water, equipment parts and lubricants; labor shortages or strikes; civil disobedience and protests; and restrictions or regulations imposed by government agencies or other changes in the regulatory environments. Such occurrences could result in damage to mineral properties, interruptions in production, injury or death to persons, damage to property of the Company or others, monetary losses and legal liabilities. These factors may cause a mineral deposit that has been mined profitably in the past to become unprofitable, forcing the Company to cease production.

Mine Development

The Company’s ability to sustain its present levels of gold production is dependent upon the identification of additional reserves at the Mine. If the Company is unable to develop new ore bodies, it will not be able to sustain or increase present production levels. Reduced production could have a material and adverse impact on future cash flows, results of operations and financial conditions.

Competitive Conditions

The mining industry is intensely competitive in all its phases, and the Company competes with other companies that have greater financial resources and technical facilities. Competition in the precious metals mining industry is primarily for mineral-rich properties which can be developed and produced economically; the technical expertise to find, develop, and produce such properties; the labour to operate the properties; and the capital for the purpose of financing development of such properties. Many competitors not only explore for and mine precious metals, but conduct refining and marketing operations on a world-wide basis and some of these companies have much greater financial and technical resources than the Company. Such competition may result in the Company being unable to acquire desired properties, recruit or retain qualified employees, or acquire the capital necessary to fund its operations and develop its properties. The Company's inability to compete with other mining companies for these mineral deposits could have a material adverse effect on the Company’s results of operation and business.

12

Management

The success of the Company is currently largely dependent on the performance of its management and staff. The loss of the services of these critical persons could have a materially adverse effect on the Company’s business and prospects. There is no assurance the Company can maintain the services of its management and staff or other qualified personnel required to operate its business. Failure to do so could have a material adverse affect on the Company and its prospects.

Dilution

There are a number of outstanding options and warrants pursuant to which additional common shares of the Company may be issued in the future. Exercise of such options and warrants may result in dilution to the Company’s shareholders. In addition, if the Company raises additional funds through the sale of equity securities, shareholders may have their investment further diluted.

Price Volatility of Publicly Traded Securities

In recent years, the securities markets in the United States and Canada have experienced a high level of price and volume volatility, and the market prices of securities of many companies have experienced wide fluctuations in price which have not necessarily been related to the operating performance, underlying asset values or prospects of such companies. There can be no assurance that continual fluctuations in price will not occur. Any quoted market for the common shares may be subject to market trends generally, notwithstanding any potential success of the Company in creating revenues, cash flows or earnings.

Political Conditions

Regardless of the economic viability of the Company’s property interests, factors such as political instability, terrorism, expropriation by governments, or the imposition of new regulations or tax laws may prevent or restrict mining of some or all of any deposits which the Company may find. All of the Company’s property interests are located in Mexico and if a dispute arises regarding the Company’s property interests, the Company cannot rely on Canadian legal standards in defending or advancing its interests.

Foreign Currency Exchange

Currency exchange rate fluctuations may adversely affect the Company’s financial position and results. The Company does not currently have in place a formal policy for managing or controlling foreign currency risks.

13

Conflicts of Interest

Some of the directors and officers are engaged and will continue to be engaged in the search for additional business opportunities on behalf of other companies, and situations may arise where these directors and officers will be in direct competition with the Company. Conflicts, if any, will be dealt with in accordance with the relevant provisions of the Business Corporations Act (British Columbia). Some of the directors and officers of the Company are or may become directors or officers of other companies engaged in other business ventures. In order to avoid the possible conflict of interest which may arise between the directors’ duties to the Company and their duties to the other companies on whose boards they serve, the directors and officers of the Company have agreed to the following:

| 1. | participation in other business ventures offered to the directors will be allocated between the various companies and on the basis of prudent business judgment and the relative financial abilities and needs of the companies to participate; |

| | |

| 2. | no commissions or other extraordinary consideration will be paid to such directors and officers; and |

| | |

| 3. | business opportunities formulated by or through other companies in which the directors and officers are involved will not be offered to the Company except on the same or better terms than the basis on which they are offered to third party participants. |

In addition, the Company’s Corporate Governance and Nominating Committee has developed, and the board of directors has adopted, guidelines which require all Company directors to disclose all conflicts of interest and potential conflicts of interest to the Company.

Mineral Properties

For a complete description of the Property see the report entitled NI 43-101 F1 Technical Report Updated Resources and Reserves and Mine Plan for the San Francisco Gold Mine Sonora, Mexico dated November 30, 2010 (the “Report”), prepared by Micon International Limited of Toronto, Ontario (“Micon”) and the study, entitled NI 43-101 F1 Technical Report on the Preliminary Feasibility Study for the San Francisco Gold Project , Sonora, Mexico, dated March 31, 2008 and amended January 13, 2009 (the “Pre-feasibility Study”), prepared by Micon and Independent Mining Consultants, Inc. of Tucson, Arizona (“IMC”) and the report titled NI 43-101 Technical Report and Resource Estimate for the San Francisco Gold Property, Estacion Llano, Sonora, Mexico, dated February 23, 2007 (the “2007 Report”), prepared by Micon and IMC. The Qualified Persons responsible for the Report are William J. Lewis, B.Sc., P.Geo., Ing. Alan J. San Martin, MAusIMM, Mani Verma, P.Eng., Christopher A. Jacobs, CEng MIMMM and Richard M. Gowans, B.Sc., P.Eng. of Micon. The Qualified Persons responsible for the Pre-feasibility Study are William J. Lewis, B.Sc., P.Geo., R. James Leader, P.Eng., Christopher A. Jacobs, CEng MIMMM and Ian R. Ward, P.Eng. of Micon and Michael G. Hester, FAusIMM, of IMC. The Qualified Persons responsible for the 2007 Report are William J. Lewis, B.Sc., P.Geo. of Micon and Michael G. Hester, FAusIMM, of IMC.

Each of the Report, the Pre-feasibility Study and the 2007 Report have been filed with Canadian securities regulatory authorities on SEDAR (available at www.sedar.com).

The Mine is the Company’s only material mineral property as defined by National Instrument 43-101 (“NI 43-101”). Please also refer to the Company’s Management’s Discussions and Analysis, news releases and other public documents filed with Canadian securities regulatory authorities on SEDAR (available at www.sedar.com) for current information on the Mine.

14

San Francisco Gold Project

The following is the summary from the Report.

GENERAL

Timmins Gold Corp. (TSX-V:TMM) (TMM) has retained Micon International Limited (Micon) to conduct an audit of its resource and reserve estimation and prepare an update of its 2008/2009 preliminary feasibility study on the San Francisco project in the state of Sonora, Mexico. The purpose of this Technical Report is to support disclosure of the results of Micon’s resource and reserve audit and the updated preliminary feasibility study, compliant with Canadian National Instrument (NI) 43-101.

Previously, Micon prepared a Technical Report, entitled “NI 43-101 Technical Report on the Preliminary Feasibility Study for the San Francisco Gold Property, Estación Llano, Sonora, Mexico”, describing the preliminary feasibility study on the San Francisco project, dated March 31, 2008 and amended January 13, 2009.

PROPERTY DESCRIPTION AND LOCATION

The San Francisco property is situated in the north central portion of the state of Sonora, Mexico, approximately 150 km north of the state capital, Hermosillo. In this report, the term San Francisco project (the project) refers to the area within the exploitation or mining concessions optioned by TMM, while the term San Francisco property (the property) refers to the entire land package (mineral exploitation and exploration concessions) optioned and owned by TMM.

The project is comprised of two previously mined open pits (San Francisco and La Chicharra), together with heap leach processing facilities and associated infrastructure located close to the San Francisco pit.

TMM advises that it holds its interest in the San Francisco property through its wholly-owned Mexican subsidiary Timmins Goldcorp Mexico, S.A. de C.V. (Timmins). Timmins originally acquired the rights to the exploitation concessions on April 18, 2005, upon signing an option agreement with Geomaque de Mexico, S.A. de C.V. (Geomaque de Mexico). The option agreement has now been superseded by an acquisition agreement. The purchase price was set at USD 5,000,000 plus 10,000,000 shares at a deemed price of USD 0.50 per share. The existing equipment had an additional purchase price of USD 3,500,000 plus value added tax (VAT), which amount is due without interest at the end of the three years from May, 2007. A portion of the equipment purchase price remains outstanding. The security documentation to place a lien against the equipment is being finalized.

15

In 2005, Timmins staked a number of exploration concessions surrounding the exploitation concessions. Interspersed within the Timmins concessions were four mineral concessions controlled by other parties, but these do not impact the main area of interest covering the San Francisco project. All concessions are subject to a semi-annual fee and the filing of reports in May of each year covering the work accomplished on the property between January and December of the preceding year. The total semi-annual fee payable to the Mexican government for the group of concessions is presently estimated to be USD 72,929.

The Mexican mining laws were changed in 2005 and, as a result of these changes, all mineral concessions granted by the Dirección General de Minas (DGM) became mining concessions and there are no longer separate specifications for a mineral exploration or exploitation concession. A second change to the mining laws was that all mining concessions are granted for 50 years provided that the concessions remain in good standing. As part of this change, all former exploration concessions which were previously granted for 6 years became eligible for the 50-year term.

In 2006, Timmins concluded an access agreement with an agrarian community (an “Ejido” in Mexico) called Los Chinos whereby Timmins was granted access privileges to 674 ha, the use of the Ejido’s roads, as well as being able to perform all exploration work on the area covered by the agreement. The agreement is for a period of 10 years with an option to extend the access beyond the 10-year period. In consideration for the Ejido granting the access privileges to a portion of its land, Timmins paid the Ejido the sum of USD 30,000.

ACCESSIBILITY, CLIMATE, PHYSIOGRAPHY, LOCAL RESOURCES AND INFRASTRUCTURE

The project is located in the Arizona-Sonora desert in the northern portion of the Mexican state of Sonora, 2 km west of the town of Estación Llano (Estación), approximately 150 km north of Hermosillo and 120 km south of the United States/Mexico border city of Nogales along Highway 15 (Pan American highway). The closest accommodations are located in Santa Ana, a small city located 21 km to the north on Highway 15.

The climate at the project site ranges from semi-arid to arid. The average ambient temperature is 21°C, with minimum and maximum temperatures of -5ºC and 50ºC, respectively. The average rainfall for the area is 330 millimetres (mm) with an upper extreme of 880 mm. The desert vegetation surrounding the San Francisco mine is composed of low lying scrub, thickets and various types of cacti, with the vegetation type classified as Sarrocaulus Thicket.

Physiographically, the San Francisco property is situated within the southern Basin and Range Province, characterized by elongate, northwest-trending ranges separated by wide alluvial valleys. The San Francisco mine is located in a relatively flat area of the desert with the topography ranging between 700 and 750 m above sea level.

HISTORY

After conducting exploration on the project between 1983 and 1992, Compania Fresnillo S.A. de C.V. (Fresnillo) sold the property in 1992 to Geomaque Explorations Ltd. (Geomaque). After conducting further exploration, Geomaque decided to bring the project into production in 1995. Due to economic conditions, mining ceased and the operation entered into the leach-only mode in November, 2000. In May, 2002, the last gold pour was conducted; the plant was mothballed, and clean-up activities at the mine site began.

16

In 2003, Geomaque sought and received shareholder approval to amalgamate the corporation under a new Canadian company, Defiance Mining Corporation (Defiance). On November 24, 2003, Defiance sold its Mexican subsidiaries (Geomaque de Mexico and Mina San Francisco), which held the San Francisco gold mine, to the Astiazaran family of Sonora and their private company for a total consideration of USD 235,000.

Since June, 2006, the Astiazaran family and their company Desarrollos Prodesa S.A. de C.V. have been extracting sand and gravel intermittently from both the waste dumps and the leach pads for use in highway construction as well as other construction projects.

Timmins acquired an option to earn an interest in the property in early 2005, whereupon Timmins conducted a review of the available data and started a reverse circulation drilling program in August and September, 2005. This was followed by a second drilling program comprised of both reverse circulation and diamond drilling in 2006, based on the results of the 2005 drilling program.

GEOLOGICAL SETTING AND MINERALIZATION

The San Francisco project is a gold occurrence with trace to small amounts of other metallic minerals. The gold occurs in granitic gneiss and the deposit contains principally free gold and occasionally electrum. The associated mineralogy, the possibility of associated tourmaline, the style of mineralization, and fluid inclusion studies suggest that the San Francisco deposits may be of mesothermal origin.

The San Francisco deposits are roughly tabular with multiple phases of gold mineralization. The deposits strike 60° west to 65° west, dip to the northeast, range in thickness from 4 to 50 m, extend over 1,500 m along strike and are open ended. Another deposit, the La Chicharra zone, was mined during the last two years of production, as a separate pit.

EXPLORATION AND OTHER PROGRAMS

After acquiring the project, Timmins undertook a review of all available geological data surrounding the previous mining areas and identified a number of immediate exploration targets both to the northwest and to the southeast of the San Francisco pit which required further work. Timmins also spent the first few months staking the surrounding area and laying out an appropriate drilling program with the objective of confirming and extending the known mineralization around the open pit.

17

Beginning in 2005 and continuing to the present time, TMM/Timmins has been conducting aggressive exploration programs to delineate and expand on the known mineralization at the San Francisco mine. The exploration drilling programs have primarily been concentrated around the existing pits but other mineral exposures previously identified by Geomaque, as well as new areas identified by TMM/Timmins, been have targeted as well.

As a result of the successful exploration campaigns around the existing pits, TMM/Timmins has been able to expand on the previously known mineralization, to re-open the San Francisco mine and expand the resources and reserves.

Between 2008 and 2010 Timmins also conducted a number of other exploration programs such as geochemical soil and chip sampling, an air magnetic and radiometric survey, a natural source audio-frequency magnetotelluric survey (NSAMT) and a structural review of the San Francisco gold deposit.

The TMM/Timmins budget for the next phase of exploration for the San Francisco mine is the result of the successful 2009-2010 drilling program. Infill and exploration drilling will continue for the remainder of 2010 and into 2011 in order to expand the mineral resources and reserves.

Of particular interest is the southeast extension where the last section line of drilling (200E) contained three RC holes which were drilled to maximum depth of 170 m. Two of the three holes intersected mineralization, with hole TF-810 intersecting three mineralized intervals of low grade and narrow thickness: 1.52 m grading 0.31 g/t gold; 1.52 m grading 0.24 g/t gold and 1.52 m grading 0.41 g/t gold. Hole TF-812, located 50 m to the north on the same section line intersected 9.12 m grading 0.98 g/t gold and 6.08 m grading 0.52 g/t gold. All mineralized intervals were located within the first 60 m from surface and are related to a chargeability anomaly open at depth for a further 300 m. TMM/Timmins has outlined a further core drilling program totalling 5,000 m.

Near the perimeter of the pit, infill drilling has been planned to follow-up previous mineralized intersections that could increase the resources immediately east and north of the San Francisco pit and the new pit limit which resulted from the recent resource update. The infill drill program outlined by Timmins is comprised of approximately 30,000 m of reverse circulation drilling.

A program of exploration has been also outlined to define and test at least 4 of the 13 targets to the north of the San Francisco pit: these are the most favourable targets when geochemistry, lithology, structural lineament and relationship with the northwest mineral trend are considered. Timmins has estimated that this program will be approximately 30,000 m, involving a combination of reverse circulation drilling and a mobile RAB drill to acquire fast samples to outline drill targets for the RC drill.

The total expenditures for the next phase of exploration, including other related payments such as access, are estimated to USD 6.1 million.

18

RESOURCE AND RESERVE ESTIMATES

Mineral Resource Estimate

The resource estimate completed by Timmins in July, 2010 and audited by Micon in August/September, 2010 is compliant with the current CIM standards and definitions specified by NI 43-101, and supersedes the March, 2008 resource estimate for the San Francisco mine.

Both Canadian NI 43-101 and the Australasian Joint Ore Reserves Committee (JORC) code state that mineral resources must meet the condition of “a reasonable prospect for eventual economic extraction.” For open pit material, Timmins utilized Lerchs Grossman pit shell geometry at reasonable long term prices, and reasonable costs and recovery assumptions, as meeting this condition for mineral resources. The resource is based on a pit shell at a gold price of USD 1,100/oz and additional cost and recovery parameters developed by Timmins which meet the conditions for classification of the material as a mineral resource. Pit optimization was based on Measured, Indicated and Inferred resources.

Table 1.1 summarizes the economic parameters used for the analysis. The parameters are a combination of Independent Mining Consultants, Inc. (IMC) and Timmins inputs taking into account the actual costs obtained from the first year of operation.

Pit bench heights were set at 6.0 m (the block height of the 3-D block model). Base case slope angles used for the pit optimization were based on inter-ramp angles recommended by Golder Associates (December, 1996 report) and adjusted to allow for haul roads of 25 m width.

Table 1.1

Pit Optimization Parameters for the San Francisco Project

| Costs (USD) | Rock Densities and Recoveries |

| Description | Units | Amount | Name | Code | Density | Recovery

% |

| Waste mining cost | $/t | 1.70 | Diorite | 2 | 2.72 | 60.50 |

| Ore mining cost | $/t ore | 1.70 | Gneiss | 4 | 2.75 | 70.70 |

| Process cost | $/t ore | 2.83 | Granite | 5 | 2.76 | 84.50 |

| G & A cost | $/t ore | 0.42 | Schist | 6 | 2.75 | 65.37 |

| Total Cost | $/t ore | 4.95 | Lamprophrite Dyke | 8 | 2.76 | 60.50 |

| Gold price | $/oz | 1,100 | Gabbro | 11 | 2.81 | 60.53 |

| | | | General Recovery | | 70.00 |

Table provided by Timmins Goldcorp Mexico, S.A. de C.V.

The mineral resource, as estimated by Timmins, is presented in Table 1.2. This resource estimate includes the undiluted mineral reserve material as of August 31, 2010.

19

Table 1.2

Mineral Resource Estimate for the San Francisco Project

(Inclusive of Mineral Reserves)

(Cut-off Grade of 0.131 g/t Gold, USD 1,100 Gold Price)

| Resource Classification | Tonnes (x 1,000) | Gold Grade (g/t) | Contained Gold

(oz) |

| Measured | 19,089 | 0.797 | 489,000 |

| Indicated | 23,442 | 0.658 | 495,000 |

| Total Measured and Indicated | 42,531 | 0.720 | 984,000 |

| Inferred | 10,308 | 0.628 | 208,000 |

Micon believes that no environmental, permitting, legal, title, taxation, socioeconomic, marketing or political issues exist which would adversely affect the Mineral Resources estimated above, at this time. However, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. The figures in Table 1.2 have been rounded to reflect that they are an estimate.

The Mineral Resource estimate has been reviewed and audited by Micon. It is Micon’s opinion that the August 31, 2010 Mineral Resource estimate has been prepared in accordance with the CIM standards and definitions for Mineral Resource estimates and that TMM/Timmins can use this estimate as a basis for further exploration and economic evaluation of the San Francisco mine project.

Mineral Reserve

Having established a Measured and Indicated mineral resource estimate from the initial pit optimization analysis, Timmins then designed an open pit with haul roads capable of accepting trucks in the 91-t class, and prepared a production schedule and second pit optimization for the extraction of the measured and indicated mineral resources.

Mining recovery for the San Francisco deposit has been assumed to be 99% based on open pit mining methods. Micon agrees with the mining recovery as initially presented, although this number may change based on actual year-to-year reconciliation studies.

The dilution for the San Francisco deposit is defined according to the type of mineralization and the size of the modelled blocks. The deposit varies in size and shape of the mineralization from one bench to another. The potential dilution varies for each of the blocks due to the proportion of waste in contact with the economic material. Therefore, the larger economic zones carry a lower percent of dilution than the smaller zones.

Timmins believes that its current method for estimating dilution is a close approximation of what can be expected during the operational period of the mine. The method consists of identifying sub-economic blocks in contact with ore blocks and adding 30% of this material as mining dilution.

20

An overall average of 12% dilution was estimated for the pit. Table 1.3 presents the total reserves estimated within the pit design outline, including the mine recovery and dilution factors.

Table 1.3

Mineral Reserves within the San Francisco Pit Design (August 31, 2010)

at USD 900/oz and after Mining Recovery and Dilution

| In Pit Reserves | In Pit Waste |

| Classification | Tonnes

(x 1,000) | Grade

(g/t) | Contained

Ounces | Waste

Tonnes

(x ,000) | Total

Tonnes

(x ,000) | Stripping

Ratio |

| Proven | 17,194 | 0.756 | 418,000 | | | |

| Probable | 17,738 | 0.635 | 362,000 | | | |

| Total | 34,932 | 0.695 | 780,000 | 60,417 | 95,349 | 1.73 |

The Proven and Probable Reserves in Table 1.3 have been derived from the Measured and Indicated mineral resources summarized in Table 1.2 and account for mining recovery and dilution. The figures in Table 1.3 have been rounded to reflect that they are an estimate.

The Mineral Reserve estimate has been reviewed and audited by Micon. It is Micon’s opinion that the August 31, 2010 Mineral Reserve estimate has been prepared in accordance with the CIM standards and definitions for Mineral Reserve estimates and that TMM/Timmins can use this estimate as a basis for further exploration and economic evaluation of the San Francisco mine project.

The San Francisco mine commenced commercial production in April, 2010. To the end of September, 2010, the mine had sold 26,999 ounces of gold.

OPERATIONAL DATA

Open Pit Design

Geotechnical Studies and Pit Design Criteria

The most recent geotechnical study carried out on the San Francisco pit was conducted by Golder Associates in December, 1996 for the previous owners of the property, Geomaque de Mexico. Golder’s scope of work was to carry out site investigations, testing and analysis to develop final slope angle recommendations for the pit design.

The recommended overall slope angles ranged from 37° for single 6 m benches along the northeast facing slopes to a maximum slope of 56° for double benching in schist units. In its report Golder presented a table of recommended inter-ramp slope angles and catch bench widths to achieve the recommended overall slope angles.

21

Timmins used this information when carrying out the pit optimization analysis and included an allowance for 25 m ramp widths in the overall slope angles.

Hydrological Considerations

Micon has no information on hydrology in the pit area. At the time of Micon’s visit, the pit floor was under water but this was understood to represent accumulated precipitation rather than inflows of groundwater. The existing pit walls were generally dry, with a few minor seepages along shear zones.

Phased Pit Designs

In 2010, the three-phase open pit design was extended to incorporate additional, recently discovered resources to the northwest of the existing pit outline. The ultimate pit design is based on the USD 900/oz gold optimized pit shell.

Both the ultimate pit design and interim mining phases conform to the current topography, including the existing pit outline. The interim phase boundaries were adjusted to ensure mineable bench widths and include ramps for access and haulage by 91-t trucks.

Mining phases were designed to have a balanced waste distribution during the mine life and continuous availability of ore.

For the mine plan and production schedule, tonnages within the initial mining phase were adjusted to match the current pit outline. Phase one extends down to the bench on elevation 590. Then, the phase two push back will expand the pit about 280 m west and deepen the pit to the bench at elevation 536. The third phase and ultimate pit outline has a 120 m push back on the north wall and the final pit bottom is at bench elevation 464.

Waste Rock Management

Existing waste rock dumps are located to the south of the San Francisco open pit, close to the pit rim and the dumps cannot be extended to the north. They are also limited to the east by a property boundary and to the west by ground not yet condemned by exploration drilling. With the re-establishment of the operations, these existing dumps will be extended further south, where adequate space does exist. For the expansion of the reserves, additional waste dump volume is required and a site located northwest of the pit has been identified that would contain the majority of waste rock produced during the mine life. Currently, a condemnation drilling program is underway in this area.

Mine Production Schedule

Using the phased pit designs described above, Timmins has developed a mine production schedule that is based on producing a minimum of 18,000 tonnes of ore per day. The mine plan has been developed on monthly intervals for the initial 16-month period to December 2011, on a quarterly basis for 2012 and annually for the remainder of the mine life to 2015.

22

The mine schedule considers ore between the internal cut-off of 0.16 g/t gold and 0.5 g/t gold as low grade, and high grade ore to be above 0.5 g/t gold. Blended ore will be fed to the crusher.

Mine Operations

All mining activities are being carried out by the contractor, Peal Mexico, S.A. de C.V., of Navojoa, Mexico. The contractor provides all the mining equipment and personnel required to produce the tonnage mandated by Timmins, in accordance with the mining plan.

Mining Contract

Under the contract dated May 23, 2007 and updated August 14, 2008, the contractor’s performance of mining operations at the San Francisco mine includes the following: drilling and blasting, loading and transportation of waste rock and ore, pit drainage, building slopes and roads as needed, scaling of pit walls to design limits, maintenance of equipment, and providing safe and orderly working conditions. The contractor is obliged to supply and maintain appropriate principal and auxiliary mining equipment and personnel.

Owner Mining Requirements

Mining engineering and design services are provided by Timmins. These services include:

- Obtaining of all permits and licences for mining.

- Mine design and planning, grade control and surveying services.

- Supply of electric power, water and telecommunications.

- Security services, safety plans and personnel and first aid stations.

Timmins provides contract supervision, geology, engineering, planning and survey services using its own employees.

Conclusion

Micon has reviewed the resource and reserve estimates, the mine design, the mining schedule and the contract terms, including the contractor’s ability to meet the mining schedule, and concludes that the estimations and designs have been properly carried out and that the contractor is capable of meeting the schedule.

PROCESSING

Crushing and Conveying

Ore extracted from the pit is transported in haulage trucks with a capacity of 91 tonnes, which feed directly into the gyratory primary crusher with dimensions of 42” x 65”. The crusher has nominal capacity of 1,200 t/h. The crushed product is then transported on conveyor belts to a stockpile with a capacity of 10,000 tonnes.

23

Two feeders beneath the stockpile deliver the ore to a conveyor belt for transport to the secondary crushing circuit. The ore is screened at ½”. Screen undersize reports to the final product, while screen oversize is fed to two secondary crushers.

Product from the secondary crushers is transported on conveyor belts to the tertiary crushing circuit, which consists of two tertiary crushers operating in closed circuit with ½” screens. Undersize from the screens is delivered to the leach pad.

An additional crusher and screen, both for the tertiary circuit and with the same specifications as the existing ones, are planned to be installed to increase throughput from 12,000 t/d to 18,000 t/d.

Leach Pad

The current leach pad occupies approximately 40 ha and is divided into 7 sections. Material from the crushing plant is transported to the leach pad on overland conveyors and deposited on the pad with a stacker forming 6 m lifts. A bulldozer passes on top of the lifts to level the surface. The irrigation pipelines are then installed, through which the leach solution is distributed over the entire surface of the lift.

Leach solution infiltrates the crushed ore, dissolving gold and silver. The solution percolates to the bottom of the lift and flows to the canal that carries the pregnant solution to the storage pond from which it is pumped to the ADR plant.

Barren solution exiting the ADR plant flows to a storage pond. Fresh water is added to the barren solution to replace losses during the process, and sodium cyanide is added before the solution is pumped back to the leach pad.

Due to the increase in mineral reserves and the planned increase in production capacity, an additional 35.2 ha will be prepared to construct a new leach pad.

Absorption/Desorption/Recovery Plant

Pregnant solution is fed to the adsorption plant which consists of 2 lines of carbon columns each with 5 tanks through which the carbon is advanced counter-currently. Gold is adsorbed on the carbon to a concentration of approximately 5,000 g/t. Desorption of the carbon is achieved in a Zedra circuit using stainless steel electrodes in a stainless steel electrolytic cell.

A new line of carbon columns with 5 tanks and a flow of 3,500 g/m is planned to be installed to accommodate the increase in production capacity.

Manpower for the processing section of the project is currently 147.

24

General Manpower and Infrastructure

The current total workforce for the San Francisco mine stands at 267.

Office space for the mine is provided in a structure of approximately 450 m2 located southeast of the ADR plant. The building has adequate working space for the on-site mine administration and also provides basic catering and ablution facilities.

A vehicle workshop south of the ADR plant and north of the open pit occupies more than 660 m2 and accommodates the off-road haul trucks, excavators and ancillary vehicles used in the mining operation.

A general warehouse of approximately 200 m2 located north of the ADR plant accommodates process reagents and mechanical spares. Bulk lime for the heap leach process is stored in a silo near the crushing plant.

Electrical Power Supply

Electrical power to the mine is delivered through a 33 kV overhead line from the utility company, Comisión Federal de Electricidad (CFE). From the main metering point, the power is distributed to the crushing and screening plant and other site infrastructure at 480/220/110 V. At the crushing and screening plant, separate transformers feed the principal equipment.

The current electrical power supply is sufficient for the planned production capacity of 18,000 t/d of ore.

Water Supply

The current demand of fresh water is 2 000 m3/d, of which 1,100 m3/d are for the leach area and ADR plant and 900 m3/d for the mine and services.

The Comisión Nacional del Agua (CONAGUA) authorized the total and definitive transfer of the rights for two concession titles to exploit and use national water previously held by Geomaque de Mexico, to Timmins’ Mexican subsidiary Molimentales del Noroeste, S. A. de C. V. (Molimentales) on May 30, 2008. Molimentales acquired an additional 2 water rights concessions in August, 2010.

Environmental Considerations

The Secretaría de Medio Ambiente y Recursos Naturales (SEMARNAT) determined that the project as described in the environmental impact assessment (Manifiesto de Impacto Ambiental – Modalidad Particular) and a level 2 environmental risk study (Estudio de Riesgo Ambiental Nivel 2) for San Francisco mine submitted on December 17, 2007, is environmentally viable, and authorized the project with conditions specifically regarding reforestation and groundwater monitoring on August 1, 2008. Groundwater monitoring is currently being performed monthly on four monitoring wells to determine the level of cyanide. Reforestation activities have continued every month with three specific species: palo fierro, palo verde and mezquite.

25

On May 30, 2008, SEMARNAT registered Molimentales as a generator of hazardous waste. Molimentales is complying with hazardous waste management standards using an on-site storage facility exclusively for hazardous waste which is collected by an accredited company. The mine contractor, Peal Mexico, was registered by SEMARNAT as a generator of hazardous waste on August 26, 2010, and is responsible for the management of the hazardous waste generated by the mining operations.

Due to the proposed increase in in production capacity from 12,000 t/d to 18,000 t/d of ore, Molimentales will update all of its environmental permits to include the additional use of land.

ECONOMIC EVALUATION

Micon conducted the economic evaluation of the San Francisco project based on the information supplied to it by TMM and its subsidiary Timmins.

Macro-Economic Assumptions

Economic analysis of the San Francisco project has been carried out in United States dollars (USD). Conversion of local Mexican costs, principally labour and power, has been made at the rate of MXN 12.50/:USD 1.00, which is considered appropriate given recent trends in actual rates (see Figure 1.1) .

Figure 1.1

Exchange Rate (MXN/USD) 2010

26

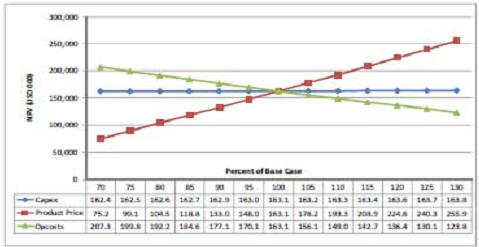

The cash flow projection has been made in constant, third quarter 2010 money terms. The net cash flows have been discounted to year-end 2010 for the purposes of calculating net present value (NPV). A base discount rate of 8.0% per year has been selected as most likely to represent the weighted average cost of capital to the project. Other rates are provided for ease of comparison.

Metal Price Forecast

Revenue projections are based on a constant gold price of USD 1,000/oz in real terms, closely approximating the 3-year trailing average price but significantly lower than spot prices at the time of writing (see Figure 1.2) .. Accordingly, the sensitivity of the project to gold price in a range of up to USD 1,400/oz has also been evaluated. A price of USD 17/oz has been used for the minor amount of silver produced.

Figure 1.2

Spot Gold Price

Royalties and Taxes

Micon understands that no liability for NSR royalty interests in the San Francisco mine has extended to the present owners. Therefore, no royalty has been provided for.