united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22483

Copeland Trust

(Exact name of registrant as specified in charter)

161 Washington St., Suite 1325, Conshohocken, PA 19428

(Address of principal executive offices) (Zip code)

Gemini Fund Services, LLC., 80 Arkay Drive Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2616

Date of fiscal year end: 11/30

Date of reporting period: 5/31/15

Item 1. Reports to Stockholders.

| | | |

| | | |

| | Copeland | |

| | Risk Managed | |

| | Dividend Growth Fund | |

| | | |

| | Copeland | |

| | International Risk Managed | |

| | Dividend Growth Fund | |

| | | |

| | Semi-Annual Report | |

| | May 31, 2015 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | Investor Information: 1-888-9-COPELAND | |

| | | |

| | This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer of sale or solicitation of an offer to buy shares of the Copeland Risk Managed Dividend Growth Fund or the Copeland International Risk Managed Dividend Growth Fund. Such offering is made only by prospectus, which includes details as to offering price and other material information. | |

| | | |

| | | |

| | Distributed by Northern Lights Distributors, LLC

Member FINRA | |

| | | |

Copeland Risk Managed Dividend Growth Fund Semi-Annual Report

May 31, 2015

Dear Fellow Shareholders:

Copeland Capital Management is pleased to review the performance of the Risk Managed Dividend Growth Fund from December 1, 2014 through May 31, 2015.

During the six month period, the Fund delivered a positive 2.3% return, largely in line with the 3.0% advance posted by the S&P 500 Index. We are pleased with the performance, which came during a period when dividend growth stocks in general, as measured by the NASDAQ US Broad Dividend Achievers Index, posted negative returns.

The Fund maintained a zero weighting in the Energy sector throughout the period, as dictated by our quantitative sector overlay. Our lack of exposure during the six months proved to be beneficial as oil prices slid roughly nine percent and the Energy sector posted a modest loss. On the flipside, our overweight position in Utilities, by virtue of our equal weighted sector methodology, was a drag on performance as the rate sensitive sector fell modestly in an otherwise up market during the period. Health Care was the top performing market sector and not surprisingly was the source of the strongest contributors to Fund performance during the period. Denmark based Novo Nordisk (NVO, 0.0%, sold during period) led the charge in advancing over 23% during the period. A dominant player in the treatment of diabetes, Novo Nordisk resubmitted an FDA filing for its drug Tresiba in April. The drug, which could launch in the U.S. as early as next year, complements an already robust pipeline focused on treatments in the areas of diabetes, obesity and hemophilia. Also benefitting from a strong backdrop for Health Care stocks was United Health Group (UNH, 2.2%) which advanced over 22% during the period. This diversified healthcare provider is enjoying strong growth across its benefits, services, technology and prescription platforms, adding service to over one million additional individuals in the first quarter alone. It recently agreed to acquire pharmacy benefit manager Catamaran, bringing additional scale to the existing pharmacy business. United Healthcare recently hiked its dividend by a robust 33%.

In contrast to the Health Care sector, stock selection within the Industrial and Materials sectors of the market was a slight headwind to Fund performance. Union Pacific (UNP, 1.8%) declined nearly 13% over the six month stretch as the company fell prey to weakness across the broader railroad segment of the market. Softening energy prices weighed upon shipments of coal, fracturing sand and crude oil. The west coast port strike further eroded results. Longer term, we expect Union Pacific’s diverse revenue base to benefit from continued growth in the North American economy. Within Industrials, gas distributor Airgas (ARG, 2.0%) retreated roughly 11% during the period. The company has reported a string of weaker than expected results as lower commodity prices weigh upon customer orders in the energy, chemicals and manufacturing spaces. We believe that acquisitions, e-commerce initiatives, and a potential rebound in commodity prices should bolster the company’s fortunes in the long term.

After a strong run in recent years, the equity markets have taken on a more muted tone of late, moving largely sideways in recent months. Expectations surrounding a long awaited U.S. Federal Reserve rate hike have gained renewed strength as a tightening in monetary policy before year end is viewed to us as increasingly likely. While equity market returns in general tend to compress during periods of rising rates, dividend growth stocks have historically maintained their performance edge relative to non dividend payers in such a backdrop. In our view, it is typically the highest yielding equities, as opposed to those demonstrating elevated rates of dividend growth, that suffer as bonds become a more attractive alternative. Given our focus on dividend growth as opposed to dividend yield, we are optimistic that the Fund will continue to post attractive risk adjusted returns going forward.

Irrespective of the near term market trends, we at Copeland remain intently focused on the long-term prospects of companies held in the Fund, with a particular emphasis on the capacity of each to continue to grow the dividend over time. We continue to favor companies that we believe retain noteworthy competitive advantages in their respective industries, are cash generative, and are overseen by managements with capital allocation discipline and an eye on the shareholder. In addition, we continue to scour the domestic universe of consistent dividend growers

in order to identify new potential investments for the Fund. It is our belief that our dividend growth philosophy, with its balance of growth orientation and defensive characteristics, will serve shareholders well in the future.

Thank you for the confidence you have placed in Copeland and for your investment in the Risk Managed Dividend Growth Fund.

May 31, 2015

The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principle value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. The Fund’s investment adviser has contractually agreed to reduce its fees and/or absorb expenses of the fund, at least until March 31, 2016, to ensure that the net annual fund operating expenses will not exceed 1.45% for CDGRX, 2.20% for CDCRX and 1.30% for CDIVX, subject to possible recoupment from the Fund in future years. Without the agreement, the expense ratio would be 1.46% for CDGRX, 2.21% for CDCRX and is currently 1.24% for CDIVX. The maximum sales charge (load) for Class A is 5.75%. Please review the Fund’s prospectus for more detail on the expense waiver. Results shown reflect the waiver, without which the results could have been lower. A Fund’s performance, especially for very short periods of time, should not be the sole factor in making your investment decisions. For performance information current to the most recent month end, please call toll free 1-888-9-COPELAND. Additional information can be found by visiting our website, www.copelandfunds.com.

The S&P 500 Index: an unmanaged composite of 500 large capitalization companies. This index is widely used by professional investors as a performance benchmark for large cap stocks. You cannot invest directly in an index.

The NASDAQ US Broad Dividend Achievers Index: comprised of US exchange traded stocks that have increased their annual dividend payments for the last ten or more years. Companies are selected based on liquidity and is calculated using a modified market capitalization weighting methodology. You cannot invest directly in an Index.

Holdings are for informational purposes only and should not be deemed a recommendation to buy. Holdings are subject to change, may not be representative of current holdings, and are subject to risk.

NLD Review Code: 1282-NLD-7/16/2015

* Footnote: Cash percentage may differ from the Generally Accepted Accounting

Principals reflected in the Portfolio of Investments.

| Top Five Performers | % of Portfolio |

| thru 5/31/15 | at 5/31/15 |

| Novo-Nordisk A/S Spon ADR (NVO) | 0.0% |

| UnitedHealth Group, Inc (UNH) | 2.2% |

| Nu Skin Enterprises, Inc (NUS) | 1.4% |

| Bank of the Ozarks (OZRK) | 2.1% |

| Kroger Company (KR) | 1.9% |

| | |

| Bottom Five Performers | % of Portfolio |

| thru 5/31/15 | at 5/31/15 |

| Caterpillar, Inc (CAT) | 0.0% |

| Union Pacific Corp (UNP) | 1.8% |

| Airgas, Inc (ARG) | 2.0% |

| Genesis Energy L.P. (GEL) | 0.0% |

| Polaris Industries, Inc (PII) | 1.7% |

| | |

| Top Ten Holdings - 5/31/15 | % of Portfolio |

| UnitedHealth Group, Inc (UNH) | 2.2% |

| Valspar Corporation (VAL) | 2.2% |

| Bank of the Ozarks (OZRK) | 2.1% |

| Avago Technologies, LTD (AVGO) | 2.1% |

| UGI Corporation (UGI) | 2.1% |

| Wyndham Worldwide Corp (WYN) | 2.1% |

| Monsanto Corp (MON) | 2.0% |

| Cardinal Health, Inc (CAH) | 2.0% |

| Airgas, Inc (ARG) | 2.0% |

| Lazard, LTD (LAZ) | 2.0% |

Holdings are for informational purposes only and should not be deemed a recommendation to buy. Holdings are subject to change, may not be representative of current holdings, and are subject to risk.

Copeland International Risk Managed Dividend Growth Fund Semi-Annual Report to Shareholders May 31, 2015

Dear Fellow Shareholders:

The Copeland International Risk Managed Dividend Growth Fund delivered a 3.7% return during the six months ended May 31, 2015, the first half of the Fund’s Fiscal Year. This compared favorably to the 3.2% return achieved by the Fund’s benchmark, the MSCI All Country World ex-US Index. In a particularly volatile market climate overseas, the Fund’s favorable results were broad based, with all but two sectors of the market contributing positively to relative performance. This outcome was achieved in spite of a drag from cash holdings, a function of the Fund’s risk management approach, which enabled the Fund to deliver below-market volatility during the time period.

The sectors contributing most to Fund performance during the time period were Consumer Discretionary, Financials, and Information Technology. Given the market’s anticipation of the launch of quantitative easing by the European Central Bank, which was launched early in 2015, it is not surprising that these three economically sensitive segments of the market delivered the biggest boost to results. Among Consumer Discretionary holdings, the biggest gainer was Eclat Textile (3.7%) in Taiwan, a leading manufacturer of performance fabrics. At the forefront of technology in fabric performance, Eclat’s products provide improved functionality including quick dry fabrics, protection from UV rays, and anti bacterial features. It increased its dividend by 42% over the past year. Cogeco Cable (1.6%) in Canada, a broadband provider in Ontario and Quebec, was a laggard as many local market participants shifted focus to the short term recovery in energy prices. Among Financials, Capitec Bank Holdings (0.0%, sold during period) in South Africa was the best performer while held during the past six months. The company has enjoyed extremely rapid growth in its unsecured consumer lending operations. Siam Commercial Bank (2.1%), one of the Fund’s leading gainers last year, has been weak thus far in 2015 on the heels of slowing asset growth and EPS, which is representative of the overall banking sector in Thailand. Avago Technologies (4.0%), the Singapore based semiconductor maker, was the biggest contributor to results within the Information Technology segment of the Fund. Historically a highly successful consolidator within the industry, we believe that the company’s recently announced acquisition of Broadcom, a dominant player in semiconductors for wireless applications and broadband connectivity, provides substantial scope for future growth at the firm.

Results within the Health Care and Industrials sectors detracted from results in the Fund during the most recent half year period. Coloplast (0.0%, sold in period), the Danish medical products firm, was a laggard following marked gains in the prior year. After a number of years of substantial growth in its core colostomy segment, the company’s growth appears to be moderating in the intermediate term. A bright spot in the Health Care sector was Fresenius SE & Co. (2.6%), Germany’s diversified health care services company, which is enjoying improving reimbursement trends within Fresenius Medical Care, its kidney dialysis subsidiary. Canadian National Railway (1.7%), a longstanding holding in the Fund, was a weak performer during the period on the heels of a number of earnings disappointments among the quoted North American rails. The Japanese security services company Secom (0.0%, sold in the period) was a positive contributor within the Industrials sector of the market.

Cash also had a negative impact on Fund performance during the past six months. Under normal market conditions, the Fund targets an 80% weight in Developed Markets and 20% in Emerging Markets. Within each of the Developed Market and Emerging Market regions, the Fund utilizes Copeland’s risk management overlay to determine sector allocation. Copeland’s quantitative model generates “buy” and “sell” sector signals in each region based on volatility adjusted moving averages. The Fund takes an equal weighted approach to all “buy” rated sectors in the quantitative model, irrespective of their relative weights within the benchmark. No investment exposure is maintained in sectors with a “sell” signal. As a result, “sell” signals in all of the Developed Market sectors and most of the Emerging Market sectors at the start of the Semi Annual period resulted in a substantial cash balance in the Fund of 85% as of November 30, 2014. By the end of the six month period, “buy” signals had re emerged in all sectors in the Developed and Emerging Markets, which led to the Fund being fully invested as of May 31, 2015. As intermittent rallies during the period coincided with cash holdings within the Fund, there was somewhat of a headwind from cash balances over the past six months. Nonetheless, the Fund’s cash position materially reduced the Fund’s volatility during the time period.

Looking to the balance of 2015 and beyond, we retain our optimistic view of the prospects for international dividend growth investing over the long run. While investors are likely to be faced with a shift to tighter monetary policy by the US Federal Reserve by year end, providing a somewhat unclear path for non-US equities, we believe our Fund is well suited for investors seeking to maintain long-term exposure to the international equity asset class. Should overall market volatility remain elevated in the short term, we believe that the Fund’s risk management techniques should provide some scope for limiting exposure to potential declines in overseas share prices.

Thank you for your support of the Copeland International Risk Managed Dividend Growth Fund.

May 31, 2015

The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principle value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. The Fund’s investment adviser has contractually agreed to reduce its fees and/or absorb expenses of the fund, at least until March 31, 2016, to ensure that the net annual fund operating expenses will not exceed 1.60% for IDVGX, 2.35% for IDVCX and 1.45% for IDVIX, subject to possible recoupment from the Fund in future years. Without the agreement, the expense ratio would be 1.61% for IDVGX, 2.36% for IDVCX and 1.46% for IDVIX. The maximum sales charge (load) for Class A is 5.75%. Please review the Fund’s prospectus for more detail on the expense waiver. Results shown reflect the waiver, without which the results could have been lower. A Fund’s performance, especially for very short periods of time, should not be the sole factor in making your investment decisions. For performance information current to the most recent month end, please call toll free 1-888-9-COPELAND. Additional information can be found by visiting our website, www.copelandfunds.com.

MSCI All Country World Ex US Index (“MSCI ACWI Ex US”) – This Index is a market capitalization weighted index designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. It includes both developed and emerging markets. Morgan Stanley Capital International is the owner of the trademark service marks and copyrights of the MSCI ACWI Ex US.

Holdings are for informational purposes only and should not be deemed a recommendation to buy. Holdings are subject to change, may not be representative of current holdings, and are subject to risk.

NLD Review Code: 1281-NLD-7/16/2015

* Footnote: Cash percentage may differ from the Generally Accepted Accounting

Principals reflected in the Portfolio of Investments.

| Top Five Performers | % of Portfolio |

| thru 5/31/15 | at 5/31/15 |

| Capitec Bank Holdings, LTD | 0.0% |

| Eclat Textile Company, LTD | 3.8% |

| Rightmove, PLC | 2.6% |

| Betfair Group, PLC | 3.0% |

| Novo Nordisk, A/S-B | 2.2% |

| | |

| Bottom Five Performers | % of Portfolio |

| thru 5/31/15 | at 5/31/15 |

| Siam Commercial Bank Pub Co | 2.1% |

| Canadian National Railway Co | 1.7% |

| Cogeco Cable, Inc | 1.6% |

| Coloplast-B | 0.0% |

| Life Healthcare Group Holdings | 0.0% |

| | |

| Top Ten Holdings - 5/31/15 | % of Portfolio |

| Avago Technologies, LTD | 4.0% |

| Eclat Textile Company, LTD | 3.8% |

| Gildan Activewear, Inc | 3.2% |

| BT Group, PLC | 3.0% |

| Betfair Group, PLC | 3.0% |

| Imperial Tobacco Group, PLC | 2.9% |

| Capita, PLC | 2.8% |

| TPG Telecom, LTD | 2.8% |

| Fresenius SE & Co KGAA | 2.6% |

| Rightmove, PLC | 2.6% |

Holdings are for informational purposes only and should not be deemed a recommendation to buy.

Holdings are subject to change, may not be representative of current holdings, and are subject to risk.

| Copeland Risk Managed Dividend Growth Fund | |

| Portfolio Review (Unaudited) | |

| December 28, 2010* through May 31, 2015 | |

| Average Annualized | | | | | | | | Since | | Since | | Since |

| Total Returns as of | | Six | | | | Three | | Inception | | Inception | | Inception |

| May 31, 2015 | | Months** | | One Year | | Year | | Class A* | | Class C* | | Class I* |

| Copeland Risk Managed | | | | | | | | | | | | |

| Dividend Growth Fund: | | | | | | | | | | | | |

| Class A | | | | | | | | | | | | |

| Without sales charge | | 2.31% | | 6.15% | | 16.53% | | 11.92% | | — | | — |

| With sales charge+ | | (3.55)% | | 0.08% | | 14.25% | | 10.43% | | — | | — |

| Class C | | 1.93% | | 5.37% | | 15.67% | | — | | 14.02% | | — |

| Class I | | 2.47% | | 6.45% | | — | | — | | — | | 15.02% |

| S&P 500 Index | | 2.97% | | 11.81% | | 19.67% | | 14.78% | | 18.25% | | 18.11% |

| Russell 3000 | | 3.67% | | 11.86% | | 19.92% | | 14.67% | | 18.49% | | 18.15% |

| * | Class A shares commenced operations on December 28, 2010. Class C commenced operations on January 5, 2012. Class I commenced operations March 1, 2013. |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The S&P 500 Index is an unmanaged market capitalization-weighted index which is comprised of 500 of the largest U.S. domiciled companies and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

The Russell 3000 Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. The Domestic Fund’s gross annual operating expense ratio, as stated in the current prospectus, is 1.46%, 2.21%, and 1.24%,for Class A, Class C, and Class I shares, respectively, and its net annual operating expense ratio is 1.45%, 2.20%, and 1.24%, for Class A, Class C, and Class I shares, respectively. These ratios can fluctuate and may differ from the expense ratios disclosed in the Financial Highlights section of this report. The Fund’s investment adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until March 31, 2016, to ensure that the net annual fund operating expenses will not exceed 1.45%, 2.20% and 1.30% of Class A, Class C and Class I shares, respectively, subject to possible recoupment from the Fund in future years. The graph does not reflect the deduction of taxes that a shareholder would have to pay on fund distributions or the redemption of the fund shares. For performance information current to the most recent month end, please call 1-888-9-COPELAND.

| Copeland International Risk Managed Dividend Growth Fund |

| Portfolio Review (Unaudited) |

| December 17, 2012* through May 31, 2015 |

| Average Annualized | | | |

| Total Returns as of | Six | | Since |

| May 31, 2015 | Months** | One Year | Inception* |

| Copeland International Risk Managed | | | |

| Dividend Growth Fund: | | | |

| Class A | | | |

| Without sales charge | 3.72% | (2.17)% | 6.64% |

| With sales charge+ | (2.26)% | (7.80)% | 4.09% |

| Class C | 3.42% | (2.87)% | 5.89% |

| Class I | 3.81% | (2.00)% | 6.75% |

| MSCI ACW ex US Index (net) | 3.16% | (0.90)% | 7.65% |

| * | The Fund commenced operations December 17, 2012. |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The MSCI All Country World ex US (net) Index is a free float-adjusted market capitalization index designed to measure equity market performance in the global developed and emerging markets excluding holdings in the United States and is net of any withholding taxes. Investors cannot invest directly in an index or benchmark.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. The International Fund’s gross annual operating expense ratio, as stated in the current prospectus is 2.34%, 3.09%, and 2.19%, for Class A, Class C, and Class I shares, respectively, and its net annual operating expense ratio is 1.61%, 2.36%, and 1.46% for its Class A, Class C, and Class I shares, respectively. These ratios can fluctuate and may differ from the expense ratios disclosed in the Financial Highlights section of this report. The Fund’s investment adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until March 31, 2016, to ensure that the net annual fund operating expenses will not exceed 1.60%, 2.35% and 1.45% of Class A, Class C and Class I shares, respectively, subject to possible recoupment from the Fund in future years. The graph does not reflect the deduction of taxes that a shareholder would have to pay on fund distributions or the redemption of the fund shares. For performance information current to the most recent month end, please call 1-888-9-COPELAND.

| Copeland Risk Managed Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Unaudited) |

| May 31, 2015 |

| Shares | | | | | Market Value | |

| | | | | | | | | |

| | | | | COMMON STOCK - 99.44% | | | | |

| | | | | AEROSPACE/DEFENSE - 1.66% | | | | |

| | 65,754 | | | Lockheed Martin Corp. | | $ | 12,374,903 | |

| | | | | | | | | |

| | | | | AGRICULTURE - 1.67% | | | | |

| | 235,590 | | | Archer Daniels Midland Co. | | | 12,450,932 | |

| | | | | | | | | |

| | | | | BANKS - 2.12% | | | | |

| | 359,239 | | | Bank of the Ozarks, Inc. | | | 15,795,739 | |

| | | | | | | | | |

| | | | | BIOTECHNOLOGY - 1.52% | | | | |

| | 72,616 | | | Amgen, Inc. | | | 11,346,976 | |

| | | | | | | | | |

| | | | | CHEMICALS - 11.32% | | | | |

| | 144,656 | | | Airgas, Inc. | | | 14,746,233 | |

| | 122,332 | | | Ecolab, Inc. | | | 14,025,364 | |

| | 100,276 | | | Int’l. Flavors & Fragrance, Inc. | | | 11,936,855 | |

| | 128,738 | | | Monsanto Co. | | | 15,059,771 | |

| | 27,256 | | | NewMarket Corp. | | | 12,548,935 | |

| | 192,800 | | | Valspar Corp. | | | 16,091,088 | |

| | | | | | | | 84,408,246 | |

| | | | | COMMERCIAL SERVICES - 1.46% | | | | |

| | 128,531 | | | CEB, Inc. | | | 10,872,437 | |

| | | | | | | | | |

| | | | | COMPUTERS - 1.81% | | | | |

| | 207,770 | | | Jack Henry & Associates, Inc. | | | 13,521,672 | |

| | | | | | | | | |

| | | | | DISTRIBUTION/WHOLESALE - 1.84% | | | | |

| | 57,169 | | | WW Grainger, Inc. | | | 13,739,426 | |

| | | | | | | | | |

| | | | | DIVERSIFIED FINANCIAL SERVICES - 7.17% | | | | |

| | 99,798 | | | Ameriprise Financial, Inc. | | | 12,433,833 | |

| | 261,609 | | | Lazard Ltd. | | | 14,534,996 | |

| | 153,928 | | | T Rowe Price Group, Inc. | | | 12,420,450 | |

| | 205,381 | | | Visa, Inc. - Cl. A | | | 14,105,567 | |

| | | | | | | | 53,494,846 | |

| | | | | ELECTRIC - 6.96% | | | | |

| | 263,509 | | | Eversource Energy | | | 12,977,818 | |

| | 367,179 | | | ITC Holdings Corp. | | | 12,957,747 | |

| | 127,604 | | | NextEra Energy, Inc. | | | 13,058,993 | |

| | 267,731 | | | Wisconsin Energy Corp. | | | 12,926,053 | |

| | | | | | | | 51,920,611 | |

| | | | | ELECTRONICS - 1.90% | | | | |

| | 205,720 | | | TE Connectivity Ltd. | | | 14,194,680 | |

| | | | | | | | | |

| | | | | FOOD - 1.93% | | | | |

| | 197,346 | | | Kroger Co. | | | 14,366,789 | |

| | | | | | | | | |

| | | | | FOREST PRODUCTS & PAPER - 1.12% | | | | |

| | 161,333 | | | International Paper Co. | | | 8,361,889 | |

| | | | | | | | | |

| | | | | GAS - 3.80% | | | | |

| | 432,589 | | | New Jersey Resources Corp. | | | 13,007,951 | |

| | 410,655 | | | UGI Corp. | | | 15,358,497 | |

| | | | | | | | 28,366,448 | |

The accompanying notes are an integral part of these financial statements.

| Copeland Risk Managed Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2015 |

| Shares | | | | | Market Value | |

| | | | | | | | | |

| | | | | HEALTHCARE PRODUCTS - 1.59% | | | | |

| | 155,325 | | | Medtronic PLC | | $ | 11,854,404 | |

| | | | | | | | | |

| | | | | HEALTHCARE SERVICES - 5.67% | | | | |

| | 114,968 | | | Chemed Corp. | | | 14,277,876 | |

| | 150,848 | | | Quest Diagnostics, Inc. | | | 11,348,295 | |

| | 138,578 | | | UnitedHealth Group, Inc. | | | 16,658,461 | |

| | | | | | | | 42,284,632 | |

| | | | | HOUSEHOLD PRODUCTS/WARES - 1.72% | | | | |

| | 153,065 | | | Church & Dwight Co., Inc. | | | 12,852,868 | |

| | | | | | | | | |

| | | | | INSURANCE - 1.63% | | | | |

| | 114,123 | | | ACE Ltd. | | | 12,151,817 | |

| | | | | | | | | |

| | | | | LEISURE TIME - 1.71% | | | | |

| | 89,043 | | | Polaris Industries, Inc. | | | 12,737,601 | |

| | | | | | | | | |

| | | | | LODGING - 2.05% | | | | |

| | 180,074 | | | Wyndham Worldwide Corp. | | | 15,290,083 | |

| | | | | | | | | |

| | | | | MACHINERY DIVERSIFIED - 3.68% | | | | |

| | 100,945 | | | Cummins, Inc. | | | 13,683,095 | |

| | 170,361 | | | Nordson Corp. | | | 13,783,909 | |

| | | | | | | | 27,467,004 | |

| | | | | MEDIA - 3.14% | | | | |

| | 215,341 | | | Comcast Corp. | | | 12,489,778 | |

| | 162,837 | | | Scripps Networks Interactive | | | 10,911,707 | |

| | | | | | | | 23,401,485 | |

| | | | | MISCELLANEOUS MANUFACTURING - 1.90% | | | | |

| | 116,753 | | | Parker Hannifin Corp. | | | 14,060,564 | |

| | | | | | | | | |

| | | | | PHARMACEUTICALS - 5.46% | | | | |

| | 169,565 | | | Cardinal Health, Inc. | | | 14,950,546 | |

| | 129,304 | | | Mead Johnson Nutrition | | | 12,581,279 | |

| | 219,288 | | | Teva Pharmaceutical Industries Ltd. - ADR | | | 13,179,209 | |

| | | | | | | | 40,711,034 | |

| | | | | REITS - 3.48% | | | | |

| | 152,572 | | | American Tower Corp. | | | 14,157,156 | |

| | 326,952 | | | Omega Healthcare Investors, Inc. | | | 11,780,081 | |

| | | | | | | | 25,937,237 | |

| | | | | RETAIL - 10.33% | | | | |

| | 208,115 | | | Brinker International, Inc. | | | 11,483,787 | |

| | 97,301 | | | Costco Wholesale Corp. | | | 13,874,150 | |

| | 140,272 | | | CVS Caremark Corp. | | | 14,361,047 | |

| | 129,246 | | | Home Depot, Inc. | | | 14,400,589 | |

| | 201,097 | | | Nu Skin Enterprises, Inc. | | | 10,175,508 | |

| | 199,667 | | | TJX Cos, Inc. | | | 12,854,561 | |

| | | | | | | | 77,149,642 | |

| | | | | SEMICONDUCTORS - 3.67% | | | | |

| | 103,383 | | | Avago Technologies Ltd. | | | 15,307,921 | |

| | 173,171 | | | QUALCOMM, Inc. | | | 12,066,555 | |

| | | | | | | | 27,374,476 | |

| | | | | SOFTWARE - 1.72% | | | | |

| | 236,476 | | | Broadridge Financial Solutions | | | 12,812,270 | |

The accompanying notes are an integral part of these financial statements.

| Copeland Risk Managed Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2015 |

| Shares | | | | | Market Value | |

| | | | | | | | | |

| | | | | TELECOMMUNICATIONS - 3.57% | | | | |

| | 165,184 | | | Harris Corp. | | $ | 13,085,876 | |

| | 273,109 | | | Verizon Communications, Inc. | | | 13,502,509 | |

| | | | | | | | 26,588,385 | |

| | | | | TRANSPORTATION - 1.84% | | | | |

| | 135,810 | | | Union Pacific Corp. | | | 13,704,587 | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCK | | | 741,593,683 | |

| | | | | (Cost - $638,977,803) | | | | |

| | | | | | | | | |

| | | | | SHORT TERM INVESTMENTS - 0.42% | | | | |

| | 3,153,213 | | | Federated Treasury Obligations Fund, 0.01% + | | | 3,153,213 | |

| | | | | TOTAL SHORT-TERM INVESTMENTS | | | | |

| | | | | (Cost - $3,153,213) | | | | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 99.86% | | | | |

| | | | | (Cost - $642,131,016) (a) | | $ | 744,746,896 | |

| | | | | OTHER ASSETS LESS LIABILITIES - 0.14% | | | 1,073,378 | |

| | | | | NET ASSETS - 100.00% | | $ | 745,820,274 | |

| + | Money market fund; Interest rate reflects seven-day effective yield on May 31, 2015. |

ADR - American Depositary Receipt.

REITS - Real Estate Investment Trusts

| (a) | Represents cost for financial reporting purposes. Aggregate cost for federal tax purposes is $640,879,392 and differs from value by net unrealized appreciation (depreciation) of securities as follows: |

| Unrealized Appreciation: | | $ | 115,490,233 | |

| Unrealized Depreciation: | | | (11,622,730 | ) |

| Net Unrealized Appreciation: | | $ | 103,867,503 | |

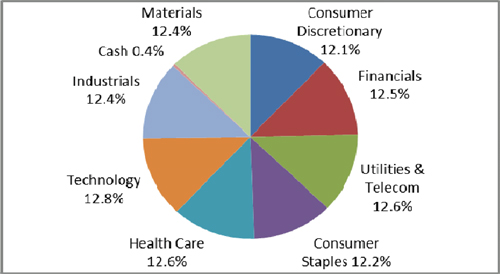

| Portfolio Composition as of May 31, 2015 (Unaudited) | |

| | Percent of Net Assets | |

| Consumer, Non-cyclical | | | 21.02 | % |

| Consumer, Cyclical | | | 15.94 | % |

| Financial | | | 14.40 | % |

| Basic Materials | | | 12.44 | % |

| Industrial | | | 10.97 | % |

| Utilities | | | 10.77 | % |

| Technology | | | 7.20 | % |

| Communications | | | 6.70 | % |

| Short-Term Investments | | | 0.42 | % |

| Other Assets Less Liabilities | | | 0.14 | % |

| Net Assets | | | 100.00 | % |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Unaudited) |

| May 31, 2015 |

| Shares | | | | | Market Value | |

| | | | | | | | | |

| | | | | COMMON STOCK - 97.19% | | | | |

| | | | | AEROSPACE/DEFENSE - 2.15% | | | | |

| | 11,286 | | | Safran SA | | $ | 797,270 | |

| | | | | | | | | |

| | | | | AGRICULTURE - 2.86% | | | | |

| | 20,605 | | | Imperial Tobacco Group PLC | | | 1,060,638 | |

| | | | | | | | | |

| | | | | AIRLINES - 1.82% | | | | |

| | 27,513 | | | EasyJet PLC | | | 675,891 | |

| | | | | | | | | |

| | | | | APPAREL - 6.89% | | | | |

| | 37,308 | | | Gildan Activewear, Inc. | | | 1,177,062 | |

| | 94,000 | | | Eclat Textile Co. Ltd. | | | 1,380,305 | |

| | | | | | | | 2,557,367 | |

| | | | | AUTO PARTS & EQUIPMENT - 1.96% | | | | |

| | 3,619 | | | Hyundai Mobis Co. Ltd. | | | 728,912 | |

| | | | | | | | | |

| | | | | BANKS - 4.22% | | | | |

| | 160,111 | | | Siam Commercial Bank PCL | | | 752,354 | |

| | 66,062 | | | Skandinaviska Enskilda Banken AB | | | 815,428 | |

| | | | | | | | 1,567,782 | |

| | | | | BEVERAGES - 2.04% | | | | |

| | 6,297 | | | Anheuser Busch InBev NV | | | 759,310 | |

| | | | | | | | | |

| | | | | BUILDING MATERIALS - 2.26% | | | | |

| | 11,255 | | | Imerys SA | | | 840,955 | |

| | | | | | | | | |

| | | | | CHEMICALS - 2.20% | | | | |

| | 6,867 | | | Int’l. Flavors & Fragrance, Inc. | | | 817,448 | |

| | | | | | | | | |

| | | | | COMMERCIAL SERVICES - 2.81% | | | | |

| | 54,462 | | | Capita Group PLC | | | 1,041,725 | |

| | | | | | | | | |

| | | | | COMPUTERS - 2.16% | | | | |

| | 6,478 | | | Ingenico S.A. | | | 801,868 | |

| | | | | | | | | |

| | | | | DIVERSIFIED FINANCIAL SERVICES - 4.44% | | | | |

| | 118,241 | | | Aberdeen Asset Management PLC | | | 807,118 | |

| | 34,366 | | | Close Brothers Group PLC | | | 840,353 | |

| | | | | | | | 1,647,471 | |

| | | | | ENGINEERING & CONSTRUCTION - 1.84% | | | | |

| | 82,932 | | | Cheung Kong Infrastructure Holdings Ltd. | | | 683,777 | |

| | | | | | | | | |

| | | | | ENTERTAINEMENT - 2.94% | | | | |

| | 26,808 | | | Betfair Group PLC | | | 1,090,895 | |

| | | | | | | | | |

| | | | | FOOD - 2.37% | | | | |

| | 11,772 | | | Kerry Group PLC | | | 879,322 | |

| | | | | | | | | |

| | | | | GAS - 2.03% | | | | |

| | 26,275 | | | Enagas SA | | | 754,698 | |

| | | | | | | | | |

| | | | | HAND/MACHINE TOOLS - 2.16% | | | | |

| | 232,748 | | | Techtronic Industries Co. Ltd. | | | 800,365 | |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2015 |

| Shares | | | | | Market Value | |

| | | | | | | | | |

| | | | | HEALTHCARE PRODUCTS - 4.43% | | | | |

| | 47,143 | | | Smith & Nephew PLC | | $ | 834,618 | |

| | 10,604 | | | Medtronic PLC | | | 809,297 | |

| | | | | | | | 1,643,915 | |

| | | | | HEALTHCARE SERVICES - 2.61% | | | | |

| | 15,224 | | | Fresenius SE & Co KGaA | | | 970,534 | |

| | | | | | | | | |

| | | | | HOUSEHOLD PRODUCTS/WARES - 2.31% | | | | |

| | 7,178 | | | Henkel AG & Co KGaA | | | 858,712 | |

| | | | | | | | | |

| | | | | INSURANCE - 2.11% | | | | |

| | 7,363 | | | ACE Ltd. | | | 784,012 | |

| | | | | | | | | |

| | | | | INTERNET - 4.65% | | | | |

| | 18,948 | | | Rightmove PLC | | | 967,859 | |

| | 37,993 | | | Tencent Holdings Ltd. | | | 757,921 | |

| | | | | | | | 1,725,780 | |

| | | | | MEDIA - 1.63% | | | | |

| | 11,445 | | | Cogeco Cable, Inc. | | | 603,555 | |

| | | | | | | | | |

| | | | | OIL & GAS - 8.27% | | | | |

| | 110,672 | | | BP PLC | | | 764,583 | |

| | 85,006 | | | Dragon Oil | | | 883,041 | |

| | 19,896 | | | Sasol LTD | | | 703,245 | |

| | 24,764 | | | Suncor Energy, Inc. | | | 721,002 | |

| | | | | | | | 3,071,871 | |

| | | | | OIL & GAS SERVICES - 1.90% | | | | |

| | 6,014 | | | Core Laboratories NV | | | 706,525 | |

| | | | | | | | | |

| | | | | PHARMACEUTICALS - 4.30% | | | | |

| | 14,288 | | | Novo Nordisk A/S | | | 810,068 | |

| | 13,079 | | | Teva Pharmaceutical Industries Ltd. - ADR | | | 786,048 | |

| | | | | | | | 1,596,116 | |

| | | | | RETAIL - 3.47% | | | | |

| | 18,050 | | | Alimentation Couche-Tard, Inc. | | | 700,603 | |

| | 83,143 | | | Clicks Group Ltd. | | | 589,171 | |

| | | | | | | | 1,289,774 | |

| | | | | SEMICONDUCTORS - 3.94% | | | | |

| | 9,868 | | | Avago Technologies Ltd. | | | 1,461,155 | |

| | | | | | | | | |

| | | | | TELECOMMUNICATIONS - 8.74% | | | | |

| | 163,440 | | | BT Group PLC | | | 1,116,039 | |

| | 18,323 | | | KDDI Corp. | | | 412,480 | |

| | 39,927 | | | MTN Group Ltd. | | | 706,893 | |

| | 146,788 | | | TPG Telecom Ltd. | | | 1,009,577 | |

| | | | | | | | 3,244,989 | |

| | | | | TRANSPORTATION - 1.68% | | | | |

| | 10,586 | | | Canadian National Railway Co. | | | 625,494 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCK | | | 36,088,126 | |

| | | | | (Cost - $34,981,563) | | | | |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2015 |

| Shares | | | | | Market Value | |

| | | | | | | | | |

| | | | | SHORT-TERM INVESTMENTS - 1.09% | | | | |

| | 402,865 | | | Federated Treasury Obligations Fund, 0.01% + | | $ | 402,865 | |

| | | | | TOTAL SHORT-TERM INVESTMENTS | | | | |

| | | | | (Cost - $402,865) | | | | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 98.28% | | | | |

| | | | | (Cost - $35,384,428) (a) | | $ | 36,490,991 | |

| | | | | OTHER ASSETS LESS LIABILITIES - 1.72% | | | 637,991 | |

| | | | | NET ASSETS - 100.00% | | $ | 37,128,982 | |

| + | Money market fund; Interest rate reflects seven day effective yield on May 31, 2015. |

ADR - American Depositary Receipt.

| (a) | Represents cost for financial reporting purposes. Aggregate cost for federal tax purposes is $35,386,224 and differs from value by net unrealized appreciation (depreciation) of securities as follows: |

| Unrealized Appreciation: | | $ | 1,990,684 | |

| Unrealized Depreciation: | | | (885,917 | ) |

| Net Unrealized Appreciation: | | $ | 1,104,767 | |

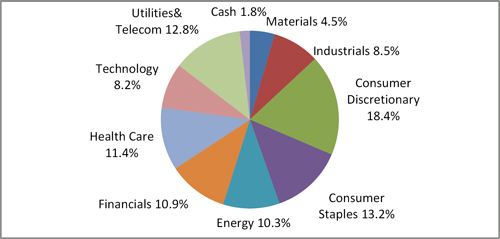

| Portfolio Composition as of May 31, 2015 (Unaudited) |

| | | Percent of Net Assets | |

| Consumer, Non-cyclical | | | 23.73 | % |

| Consumer, Cyclical | | | 17.08 | % |

| Communications | | | 15.01 | % |

| Financial | | | 10.77 | % |

| Energy | | | 10.18 | % |

| Industrial | | | 10.09 | % |

| Technology | | | 6.10 | % |

| Basic Materials | | | 2.20 | % |

| Utilities | | | 2.03 | % |

| Short-Term Investments | | | 1.09 | % |

| Other Assets Less Liabilties | | | 1.72 | % |

| Net Assets | | | 100.00 | % |

The accompanying notes are an integral part of these financial statements.

| Copeland Trust |

| STATEMENTS OF ASSETS AND LIABILITIES (Unaudited) |

| May 31, 2015 |

| | | | | | Copeland | |

| | | Copeland Risk | | | International Risk | |

| | | Managed Dividend | | | Managed Dividend | |

| | | Growth Fund | | | Growth Fund | |

| Assets: | | | | | | | | |

| Investments, at Cost | | $ | 642,131,016 | | | $ | 35,384,428 | |

| Investments in Securities, at Market Value | | $ | 744,746,896 | | | $ | 36,490,991 | |

| Foreign Cash (Cost $63,743) | | | — | | | | 63,481 | |

| Dividends and Interest Receivable | | | 1,722,158 | | | | 73,893 | |

| Receivable for Securities Sold | | | 532,262 | | | | 860,542 | |

| Receivable for Fund Shares Sold | | | 945,744 | | | | 245,416 | |

| Prepaid Expenses and Other Assets | | | 42,143 | | | | 17,446 | |

| Total Assets | | | 747,989,203 | | | | 37,751,769 | |

| | | | | | | | | |

| Liabilities: | | | | | | | | |

| Payable for Securities Purchased | | | — | | | | 583,217 | |

| Payable for Fund Shares Redeemed | | | 1,432,493 | | | | 1,229 | |

| Payable to Investment Adviser | | | 581,317 | | | | 17,518 | |

| Accrued Distribution Fees | | | 137,161 | | | | 8,286 | |

| Accrued Expenses and Other Liabilities | | | 17,958 | | | | 12,537 | |

| Total Liabilities | | | 2,168,929 | | | | 622,787 | |

| | | | | | | | | |

| Net Assets | | $ | 745,820,274 | | | $ | 37,128,982 | |

| | | | | | | | | |

| Composition of Net Assets: | | | | | | | | |

| At May 31, 2015, Net Assets consisted of: | | | | | | | | |

| Paid in Capital | | $ | 595,488,759 | | | $ | 36,266,344 | |

| Undistributed Net Investment Income | | | 5,029,791 | | | | 52,283 | |

| Accumulated Net Realized Gain (Loss) From Security and Foreign Currency Transactions | | | 42,685,824 | | | | (295,004 | ) |

| Net Unrealized Appreciation on Investments and Foreign Currency Translations | | | 102,615,900 | | | | 1,105,359 | |

| Net Assets | | $ | 745,820,274 | | | $ | 37,128,982 | |

The accompanying notes are an integral part of these financial statements.

| Copeland Funds |

| STATEMENT OF ASSETS AND LIABILITIES (Unaudited) (Continued) |

| May 31, 2015 |

| | | | | | Copeland | |

| | | Copeland Risk | | | International Risk | |

| | | Managed Dividend | | | Managed Dividend | |

| | | Growth Fund | | | Growth Fund | |

| Class A Shares: | | | | | | | | |

| Net Assets | | $ | 301,471,555 | | | $ | 14,496,095 | |

| Shares Outstanding (no par value; unlimited number of shares authorized) | | | 20,020,604 | | | | 1,238,792 | |

| | | | | | | | | |

| Net Asset Value and Redemption Price Per Share* | | $ | 15.06 | | | $ | 11.70 | |

| Offering Price Per Share (NAV/0.9425) Includes a Maximum Sales Charge of 5.75% | | $ | 15.98 | | | $ | 12.41 | |

| | | | | | | | | |

| Class C Shares: | | | | | | | | |

| Net Assets | | $ | 99,630,804 | | | $ | 7,161,425 | |

| Shares Outstanding (no par value; unlimited number of shares authorized) | | | 6,696,361 | | | | 622,693 | |

| | | | | | | | | |

| Net Asset Value, Offering Price and Redemption Price Per Share* | | $ | 14.88 | | | $ | 11.50 | |

| | | | | | | | | |

| Class I Shares: | | | | | | | | |

| Net Assets | | $ | 344,717,915 | | | $ | 15,471,462 | |

| Shares Outstanding (no par value; unlimited number of shares authorized) | | | 22,897,001 | | | | 1,318,725 | |

| | | | | | | | | |

| Net Asset Value, Offering Price and Redemption Price Per Share* | | $ | 15.06 | | | $ | 11.73 | |

| * | The Funds charge a 1.00% fee on shares redeemed less than 30 days after purchase or if shares held less than 30 days are redeemed for failure to maintain the Funds’ minimum balance requirement. |

The accompanying notes are an integral part of these financial statements.

| Copeland Trust |

| STATEMENTS OF OPERATIONS (Unaudited) |

| For the Six Months Ended May 31, 2015 |

| | | | | | Copeland | |

| | | Copeland Risk | | | International Risk | |

| | | Managed Dividend | | | Managed Dividend | |

| | | Growth Fund | | | Growth Fund | |

| Investment Income: | | | | | | | | |

| Dividend Income (Less $74,906 and $46,714 Foreign Taxes Withholding, respectively) | | $ | 8,431,917 | | | $ | 335,219 | |

| Interest Income | | | 348 | | | | 608 | |

| Total Investment Income | | | 8,432,265 | | | | 335,827 | |

| | | | | | | | | |

| Expenses: | | | | | | | | |

| Investment Advisory Fees | | | 3,644,275 | | | | 178,241 | |

| Distribution Fees - Class C | | | 468,011 | | | | 32,928 | |

| Distribution Fees - Class A | | | 384,810 | | | | 16,350 | |

| Administration Fees | | | 203,379 | | | | 12,086 | |

| Sub-Transfer Agent Fees | | | 154,302 | | | | 9,204 | |

| Trustees’ Fees | | | 85,110 | | | | 10,942 | |

| Transfer Agent Fees | | | 66,838 | | | | 8,447 | |

| Fund Accounting Fees | | | 57,393 | | | | 17,809 | |

| Registration & Filing Fees | | | 37,041 | | | | 29,534 | |

| Legal Fees | | | 25,963 | | | | 3,832 | |

| Shareholder Servicing Fees-Class I | | | 24,042 | | | | 4,157 | |

| Custody Fees | | | 22,462 | | | | 8,975 | |

| Chief Compliance Officer Fees | | | 15,106 | | | | 675 | |

| Insurance Expense | | | 10,377 | | | | 499 | |

| Audit Fees | | | 7,644 | | | | 7,644 | |

| Printing Expenses | | | 39,551 | | | | 4,216 | |

| Miscellaneous Expenses | | | 11,473 | | | | 2,472 | |

| Total Expenses | | | 5,257,777 | | | | 348,011 | |

| Less: Fees Waived by Adviser | | | (15,914 | ) | | | (74,226 | ) |

| Net Expenses | | | 5,241,863 | | | | 273,785 | |

| Net Investment Income | | | 3,190,402 | | | | 62,042 | |

| | | | | | | | | |

| Net Realized and Unrealized Gain (Loss) on Investments and Foreign Currencies: | | | | | | | | |

| Net Realized Gain (Loss) on: | | | | | | | | |

| Security Transactions and FX gain on securities | | | 32,105,868 | | | | 720,381 | |

| Foreign Currency Transactions | | | — | | | | (339,927 | ) |

| Foreign Currency Exchange Contracts | | | (495 | ) | | | (250,349 | ) |

| | | | 32,105,373 | | | | 130,105 | |

| Net Change in Unrealized Appreciation (Depreciation) on: | | | | | | | | |

| Securities | | | (19,038,757 | ) | | | 833,506 | |

| Foreign Currency Exchange Contracts | | | — | | | | (47 | ) |

| | | | (19,038,757 | ) | | | 833,459 | |

| Net Realized and Unrealized Gain on Investments and Foreign Currency Transactions | | | 13,066,616 | | | | 963,564 | |

| | | | | | | | | |

| Net Increase in Net Assets Resulting From Operations | | $ | 16,257,018 | | | $ | 1,025,606 | |

The accompanying notes are an integral part of these financial statements.

| Copeland Risk Managed Dividend Growth Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | | Six Months | | | Year | |

| | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | |

| Operations: | | (Unaudited) | | | | | |

| Net Investment Income | | $ | 3,190,402 | | | $ | 2,734,686 | |

| Net Realized Gain on Investments and Foreign Currency Transactions | | | 32,105,373 | | | | 36,819,961 | |

| Net Change in Unrealized Appreciation (Depreciation) on Investments | | | (19,038,757 | ) | | | 23,805,769 | |

| Net Increase in Net Assets Resulting From Operations | | | 16,257,018 | | | | 63,360,416 | |

| | | | | | | | | |

| Distributions to Shareholders From: | | | | | | | | |

| Net Investment Income | | | | | | | | |

| Class A ($0.03 and $0.07 per share, respectively) | | | (582,684 | ) | | | (2,128,885 | ) |

| Class C ($0.00 and $0.01 per share, respectively) | | | — | | | | (26,502 | ) |

| Class I ($0.08 and $0.09 per share, respectively) | | | (1,641,478 | ) | | | (43,875 | ) |

| | | | (2,224,162 | ) | | | (2,199,262 | ) |

| Net Realized Gains | | | | | | | | |

| Class A ($0.54 and $0.36 per share, respectively) | | | (11,402,466 | ) | | | (10,574,310 | ) |

| Class C ($0.54 and $0.36 per share, respectively) | | | (3,176,732 | ) | | | (1,480,815 | ) |

| Class I ($0.54 and $0.36 per share, respectively) | | | (11,322,635 | ) | | | (1,481,472 | ) |

| | | | (25,901,833 | ) | | | (13,536,597 | ) |

| Total Distributions to Shareholders | | | (28,125,995 | ) | | | (15,735,859 | ) |

| | | | | | | | | |

| Beneficial Interest Transactions: | | | | | | | | |

| Class A | | | | | | | | |

| Proceeds from Shares Issued (2,320,776 and 11,526,750 shares, respectively) | | | 34,886,917 | | | | 167,652,562 | |

| Distributions Reinvested (800,438 and 869,050 shares, respectively) | | | 11,326,183 | | | | 11,968,903 | |

| Cost of Shares Redeemed (4,308,810 and 22,447,035 shares, respectively) | | | (64,264,252 | ) | | | (334,690,753 | ) |

| Redemption Fees | | | 2,256 | | | | 13,216 | |

| Total Class A Shares | | | (18,048,896 | ) | | | (155,056,072 | ) |

| | | | | | | | | |

| Class C | | | | | | | | |

| Proceeds from Shares Issued (1,126,530 and 2,568,214 shares, respectively) | | | 16,712,782 | | | | 37,280,654 | |

| Distributions Reinvested (223,798 and 105,769 shares, respectively) | | | 3,137,637 | | | | 1,470,487 | |

| Cost of Shares Redeemed (526,513 and 516,659 shares, respectively) | | | (7,835,744 | ) | | | (7,526,347 | ) |

| Redemption Fees | | | 687 | | | | 2,119 | |

| Total Class C Shares | | | 12,015,362 | | | | 31,226,913 | |

| | | | | | | | | |

| Class I | | | | | | | | |

| Proceeds from Shares Issued (4,613,145 and 21,863,906 shares, respectively) | | | 69,314,098 | | | | 329,026,096 | |

| Distributions Reinvested (835,056 and 95,258 shares, respectively) | | | 12,053,677 | | | | 1,419,743 | |

| Cost of Shares Redeemed (3,492,659 and 1,507,222 shares, respectively) | | | (52,308,617 | ) | | | (22,508,416 | ) |

| Redemption Fees | | | 2,404 | | | | 2,967 | |

| Total Class I Shares | | | 29,061,562 | | | | 307,940,390 | |

| | | | | | | | | |

| Total Beneficial Interest Transactions | | | 23,028,028 | | | | 184,111,231 | |

| | | | | | | | | |

| Increase in Net Assets | | | 11,159,051 | | | | 231,735,788 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of Period | | | 734,661,223 | | | | 502,925,435 | |

| End of Period** | | $ | 745,820,274 | | | $ | 734,661,223 | |

| | | | | | | | | |

| | | | | | | | | |

| ** Includes undistributed net investment income of: | | $ | 5,029,791 | | | $ | 4,063,551 | |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | | Six Months | | | Year | |

| | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | |

| Operations: | | (Unaudited) | | | | |

| Net Investment Income | | $ | 62,042 | | | $ | 88,601 | |

| Net Realized Gain (Loss) on Investments and Foreign Currency Transactions | | | 130,105 | | | | (552,474 | ) |

| Net Change in Unrealized Appreciation on Investments and Foreign Currency Transactions | | | 833,459 | | | | 179,023 | |

| Net Increase in Net Assets Resulting From Operations | | | 1,025,606 | | | | (284,850 | ) |

| | | | | | | | | |

| Distributions to Shareholders From: | | | | | | | | |

| Net Realized Gains | | | | | | | | |

| Class A ($0.00 and $0.01 per share, respectively) | | | — | | | | (4,935 | ) |

| Class C ($0.00 and $0.01 per share, respectively) | | | — | | | | (1,132 | ) |

| Class I ($0.00 and $0.01 per share, respectively) | | | — | | | | (495 | ) |

| Total Distributions to Shareholders | | | — | | | | (6,562 | ) |

| | | | | | | | | |

| Beneficial Interest Transactions: | | | | | | | | |

| Class A | | | | | | | | |

| Proceeds from Shares Issued (491,873 and 919,353 shares, respectively) | | | 5,717,885 | | | | 10,535,089 | |

| Distributions Reinvested (0 and 447 shares, respectively) | | | — | | | | 4,843 | |

| Cost of Shares Redeemed (835,200 and 74,613 shares, respectively) | | | (9,359,716 | ) | | | (851,912 | ) |

| Redemption Fees | | | 717 | | | | 191 | |

| Total Class A Shares | | | (3,641,114 | ) | | | 9,688,211 | |

| | | | | | | | | |

| Class C | | | | | | | | |

| Proceeds from Shares Issued (211,116 and 376,084 shares, respectively) | | | 2,355,545 | | | | 4,244,082 | |

| Distributions Reinvested (0 and 101 shares, respectively) | | | — | | | | 1,094 | |

| Cost of Shares Redeemed (101,327 and 19,352 shares, respectively) | | | (1,130,410 | ) | | | (212,969 | ) |

| Redemption Fees | | | 325 | | | | 51 | |

| Total Class C Shares | | | 1,225,460 | | | | 4,032,258 | |

| | | | | | | | | |

| Class I | | | | | | | | |

| Proceeds from Shares Issued (617,308 and 1,145,091 shares, respectively) | | | 7,074,210 | | | | 13,253,639 | |

| Distributions Reinvested (0 and 46 shares, respectively) | | | — | | | | 495 | |

| Cost of Shares Redeemed (411,686 and 108,892 shares, respectively) | | | (4,676,707 | ) | | | (1,232,933 | ) |

| Redemption Fees | | | 602 | | | | 74 | |

| Total Class I Shares | | | 2,398,105 | | | | 12,021,275 | |

| | | | | | | | | |

| Total Beneficial Interest Transactions | | | (17,549 | ) | | | 25,741,744 | |

| | | | | | | | | |

| Increase in Net Assets | | | 1,008,057 | | | | 25,450,332 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of Period | | | 36,120,925 | | | | 10,670,593 | |

| End of Period** | | $ | 37,128,982 | | | $ | 36,120,925 | |

| | | | | | | | | |

| | | | | | | | | |

| ** Includes accumulated net investment income (loss) of: | | $ | 52,283 | | | $ | (9,759 | ) |

The accompanying notes are an integral part of these financial statements.

| Copeland Risk Managed Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| |

| |

| The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. |

| | | Class A | |

| | | Six Months | | | Year | | | Year | | | Year | | | Period | |

| | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | | | November 30, 2013 | | | November 30, 2012 | | | November 30, 2011* | |

| | | (Unaudited) | | | | | | | | | | | | | |

| Net Asset Value, Beginning of Period | | $ | 15.31 | | | $ | 14.20 | | | $ | 10.99 | | | $ | 10.18 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | |

| Increase From Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (a) | | | 0.06 | | | | 0.07 | | | | 0.10 | | | | 0.14 | | | | 0.07 | |

| Net gain from securities (both realized and unrealized) | | | 0.26 | | | | 1.47 | | | | 3.17 | | | | 0.77 | | | | 0.15 | |

| Total from operations | | | 0.32 | | | | 1.54 | | | | 3.27 | | | | 0.91 | | | | 0.22 | |

| | | | | | | | | | | | | | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.03 | ) | | | (0.07 | ) | | | (0.04 | ) | | | (0.10 | ) | | | (0.04 | ) |

| Net realized gains | | | (0.54 | ) | | | (0.36 | ) | | | (0.02 | ) | | | — | | | | — | |

| Total distributions | | | (0.57 | ) | | | (0.43 | ) | | | (0.06 | ) | | | (0.10 | ) | | | (0.04 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Redemption fees | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) |

| | | | | | | | | | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 15.06 | | | $ | 15.31 | | | $ | 14.20 | | | $ | 10.99 | | | $ | 10.18 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Return (b) | | | 2.31 | % | | | 11.14 | % | | | 29.87 | % | | | 9.01 | % | | | 2.19 | % (d) |

| | | | | | | | | | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in 000’s) | | $ | 301,472 | | | $ | 324,664 | | | $ | 443,822 | | | $ | 293,049 | | | $ | 107,431 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | | | | | | | | | |

| before reimbursement | | | 1.46 | % (c) | | | 1.46 | % | | | 1.55 | % | | | 1.57 | % | | | 2.88 | % (c) |

| net of reimbursement | | | 1.45 | % (c) | | | 1.45 | % | | | 1.45 | % | | | 1.45 | % | | | 1.45 | % (c) |

| Ratio of net investment income to average net assets | | | 0.86 | % (c) | | | 0.48 | % | | | 0.81 | % | | | 1.31 | % | | | 0.73 | % (c) |

| Portfolio turnover rate | | | 35 | % (d) | | | 44 | % | | | 39 | % | | | 139 | % | | | 382 | % (d) |

| * | Class A commenced operations on December 28, 2010. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (e) | Less than $0.01 per share. |

The accompanying notes are an integral part of these financial statements.

| Copeland Risk Managed Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| |

| |

| The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. |

| | | Class C | |

| | | Six Months | | | Year | | | Year | | | Period | |

| | | Ended | | | Ended | | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | | | November 30, 2013 | | | November 30, 2012 * | |

| | | (Unaudited) | | | | | | | | | | |

| Net Asset Value, Beginning of Period | | $ | 15.16 | | | $ | 14.10 | | | $ | 10.96 | | | $ | 10.23 | |

| | | | | | | | | | | | | | | | | |

| Increase From Operations: | | | | | | | | | | | | | | | | |

| Net investment income (loss) (a) | | | 0.01 | | | | (0.04 | ) | | | 0.01 | | | | 0.07 | |

| Net gain from securities (both realized and unrealized) | | | 0.25 | | | | 1.47 | | | | 3.15 | | | | 0.72 | |

| Total from operations | | | 0.26 | | | | 1.43 | | | | 3.16 | | | | 0.79 | |

| | | | | | | | | | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | | | | | | | | | |

| Net investment income | | | — | | | | (0.01 | ) | | | 0.00 | (e) | | | (0.06 | ) |

| Net realized gains | | | (0.54 | ) | | | (0.36 | ) | | | (0.02 | ) | | | — | |

| Total distributions | | | (0.54 | ) | | | (0.37 | ) | | | (0.02 | ) | | | (0.06 | ) |

| | | | | | | | | | | | | | | | | |

| Redemption fees | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) |

| | | | | | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 14.88 | | | $ | 15.16 | | | $ | 14.10 | | | $ | 10.96 | |

| | | | | | | | | | | | | | | | | |

| Total Return (b) | | | 1.93 | % | | | 10.36 | % | | | 28.89 | % | | | 7.77 | % (d) |

| | | | | | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | | | | | |

| Net assets, end of period (in 000’s) | | $ | 99,631 | | | $ | 89,017 | | | $ | 52,399 | | | $ | 24,459 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | | | | | |

| before reimbursement | | | 2.21 | % (c) | | | 2.21 | % | | | 2.30 | % | | | 2.34 | % (c) |

| net of reimbursement | | | 2.20 | % (c) | | | 2.20 | % | | | 2.20 | % | | | 2.20 | % (c) |

| Ratio of net investment income to average net assets | | | 0.11 | % (c) | | | (0.27 | )% | | | 0.06 | % | | | 0.70 | % (c) |

| Portfolio turnover rate | | | 35 | % (d) | | | 44 | % | | | 39 | % | | | 139 | % (d) |

| * | Class C commenced operations on January 5, 2012. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (e) | Less than $0.01 per share. |

The accompanying notes are an integral part of these financial statements.

| Copeland Risk Managed Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| |

| |

| The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. |

| | | Class I | |

| | | Six Months | | | Year | | | Period | |

| | | Ended | | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | | | November 30, 2013 * | |

| | | (Unaudited) | | | | | | | |

| Net Asset Value, Beginning of Period | | $ | 15.34 | | | $ | 14.22 | | | $ | 11.89 | |

| | | | | | | | | | | | | |

| Increase From Operations: | | | | | | | | | | | | |

| Net investment income (a) | | | 0.08 | | | | 0.13 | | | | 0.09 | |

| Net gain from securities (both realized and unrealized) | | | 0.26 | | | | 1.44 | | | | 2.29 | |

| Total from operations | | | 0.34 | | | | 1.57 | | | | 2.38 | |

| | | | | | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | | | | | |

| Net investment income | | | (0.08 | ) | | | (0.09 | ) | | | (0.03 | ) |

| Net realized gains | | | (0.54 | ) | | | (0.36 | ) | | | (0.02 | ) |

| Total distributions | | | (0.62 | ) | | | (0.45 | ) | | | (0.05 | ) |

| | | | | | | | | | | | | |

| Redemption fees | | | 0.00 | (e) | | | 0.00 | (e) | | | — | |

| | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 15.06 | | | $ | 15.34 | | | $ | 14.22 | |

| | | | | | | | | | | | | |

| Total Return (b) | | | 2.47 | % | | | 11.38 | % | | | 20.04 | % (d) |

| | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | |

| Net assets, end of period (in 000’s) | | $ | 344,718 | | | $ | 320,981 | | | $ | 6,704 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | |

| before reimbursement | | | 1.21 | % (c) | | | 1.24 | % | | | 1.30 | % (c) |

| net of reimbursement | | | 1.21 | % (c) | | | 1.24 | % | | | 1.30 | % (c) |

| Ratio of net investment income to average net assets | | | 1.11 | % (c) | | | 0.63 | % | | | 1.06 | % (c) |

| Portfolio turnover rate | | | 35 | % (d) | | | 44 | % | | | 39 | % (d) |

| * | Class I commenced operations on March 1, 2013. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (e) | Less than $0.01 per share. |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| |

| |

| The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. |

| | | Class A | |

| | | Six Months | | | Year | | | Period | |

| | | Ended | | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | | | November 30, 2013 * | |

| | | (Unaudited) | | | | | | | |

| Net Asset Value, Beginning of Period | | $ | 11.28 | | | $ | 11.01 | | | $ | 10.00 | |

| | | | | | | | | | | | | |

| Increase From Operations: | | | | | | | | | | | | |

| Net investment income (a) | | | 0.02 | | | | 0.06 | | | | 0.04 | |

| Net gain from securities (both realized and unrealized) | | | 0.40 | | | | 0.22 | | | | 0.97 | |

| Total from operations | | | 0.42 | | | | 0.28 | | | | 1.01 | |

| | | | | | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | | | | | |

| Net realized gains | | | — | | | | (0.01 | ) | | | — | |

| Total distributions | | | — | | | | (0.01 | ) | | | — | |

| | | | | | | | | | | | | |

| Redemption fees | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) |

| | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 11.70 | | | $ | 11.28 | | | $ | 11.01 | |

| | | | | | | | | | | | | |

| Total Return (b) | | | 3.72 | % | | | 2.51 | % | | | 10.10 | % (d) |

| | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | |

| Net assets, end of period (in 000’s) | | $ | 14,496 | | | $ | 17,840 | | | $ | 8,116 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | |

| before reimbursement | | | 2.06 | % (c) | | | 2.33 | % | | | 7.74 | % (c) |

| net of reimbursement | | | 1.60 | % (c) | | | 1.60 | % | | | 1.60 | % (c) |

| Ratio of net investment income to average net assets | | | 0.61 | % (c) | | | 0.48 | % | | | 0.36 | % (c) |

| Portfolio turnover rate | | | 105 | % (d) | | | 211 | % | | | 68 | % (d) |

| * | Class A commenced operations on December 17, 2012. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (e) | Less than $0.01 per share. |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| |

| |

| The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. |

| | | Class C | |

| | | Six Months | | | Year | | | Period | |

| | | Ended | | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | | | November 30, 2013 * | |

| | | (Unaudited) | | | | | | | |

| Net Asset Value, Beginning of Period | �� | $ | 11.12 | | | $ | 10.95 | | | $ | 10.00 | |

| | | | | | | | | | | | | |

| Increase From Operations: | | | | | | | | | | | | |

| Net investment loss (a) | | | (0.01 | ) | | | (0.04 | ) | | | (0.03 | ) |

| Net gain from securities (both realized and unrealized) | | | 0.39 | | | | 0.22 | | | | 0.98 | |

| Total from operations | | | 0.38 | | | | 0.18 | | | | 0.95 | |

| | | | | | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | | | | | |

| Net realized gains | | | — | | | | (0.01 | ) | | | — | |

| Total distributions | | | — | | | | (0.01 | ) | | | — | |

| | | | | | | | | | | | | |

| Redemption fees | | | 0.00 | (e) | | | 0.00 | (e) | | | — | |

| | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 11.50 | | | $ | 11.12 | | | $ | 10.95 | |

| | | | | | | | | | | | | |

| Total Return (b) | | | 3.42 | % | | | 1.61 | % | | | 9.50 | % (d) |

| | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | |

| Net assets, end of period (in 000’s) | | $ | 7,161 | | | $ | 5,706 | | | $ | 1,708 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | |

| before reimbursement | | | 2.81 | % (c) | | | 3.08 | % | | | 8.49 | % (c) |

| net of reimbursement | | | 2.35 | % (c) | | | 2.35 | % | | | 2.35 | % (c) |

| Ratio of net investment income to average net assets | | | (0.14 | )% (c) | | | (0.27 | )% | | | (0.39 | )% (c) |

| Portfolio turnover rate | | | 105 | % (d) | | | 211 | % | | | 68 | % (d) |

| * | Class C commenced operations on December 17, 2012. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (e) | Less than $0.01 per share. |

The accompanying notes are an integral part of these financial statements.

| Copeland International Risk Managed Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| |

| |

| The table below sets forth financial data for one share of beneficial interest outstanding throughout each period presented. |

| | | Class I | |

| | | Six Months | | | Year | | | Period | |

| | | Ended | | | Ended | | | Ended | |

| | | May 31, 2015 | | | November 30, 2014 | | | November 30, 2013 * | |

| | | (Unaudited) | | | | | | | |

| Net Asset Value, Beginning of Period | | $ | 11.30 | | | $ | 11.02 | | | $ | 10.00 | |

| | | | | | | | | | | | | |

| Increase From Operations: | | | | | | | | | | | | |

| Net investment income (a) | | | 0.04 | | | | 0.06 | | | | 0.06 | |

| Net gain from securities (both realized and unrealized) | | | 0.39 | | | | 0.23 | | | | 0.96 | |

| Total from operations | | | 0.43 | | | | 0.29 | | | | 1.02 | |

| | | | | | | | | | | | | |

| Distributions to shareholders from: | | | | | | | | | | | | |

| Net realized gains | | | — | | | | (0.01 | ) | | | — | |

| Total distributions | | | — | | | | (0.01 | ) | | | — | |

| | | | | | | | | | | | | |

| Redemption fees | | | (0.00 | ) (e) | | | (0.00 | ) (e) | | | (0.00 | ) (e) |

| | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 11.73 | | | $ | 11.30 | | | $ | 11.02 | |

| | | | | | | | | | | | | |

| Total Return (b) | | | 3.81 | % | | | 2.60 | % | | | 10.20 | % (d) |

| | | | | | | | | | | | | |

| Ratios/Supplemental Data | | | | | | | | | | | | |

| Net assets, end of period (in 000’s) | | $ | 15,471 | | | $ | 12,575 | | | $ | 847 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | |

| before reimbursement | | | 1.91 | % (c) | | | 2.18 | % | | | 17.85 | % (c) |

| net of reimbursement | | | 1.45 | % (c) | | | 1.45 | % | | | 1.45 | % (c) |

| Ratio of net investment income to average net assets | | | 0.76 | % (c) | | | 0.63 | % | | | 0.59 | % (c) |

| Portfolio turnover rate | | | 105 | % (d) | | | 211 | % | | | 68 | % (d) |

| * | Class I commenced operations on December 17, 2012. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (e) | Less than $0.01 per share. |

The accompanying notes are an integral part of these financial statements.

| Copeland Trust |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) |

| May 31, 2015 |

| |

Copeland Risk Managed Dividend Growth Fund (the “Domestic Fund”) is a non diversified series of Copeland Trust (the “Trust”) and Copeland International Risk Managed Dividend Growth Fund (the “International Fund”) is a diversified series of the Trust. The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”) as an open-end management investment company. The Trust was organized as a statutory trust on September 10, 2010 under the laws of the State of Delaware. The investment objective of each fund is to seek long-term capital appreciation and income while preserving capital. Each Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services—Investment Companies”.

The Funds currently offer Class A, Class C and Class I shares. Domestic Fund’s Class A shares commenced operations on December 28, 2010, Class C shares commenced operations on January 5, 2012 and Class I shares commenced operations on March 1, 2013. International Fund’s Class A, Class C and Class I shares commenced operations on December 17, 2012. Class A shares are offered at net asset value plus a maximum sales charge of 5.75%. Purchases of $1,000,000 or more may be subject to a maximum contingent deferred sales charge of 1.00% on shares redeemed within 18 months. Class C and Class I shares are offered at net asset value. Each class represents an interest in the same assets of the Funds and classes are identical except for differences in their sales charge structures and ongoing service and distribution charges. All classes of shares have equal voting privileges except that each class has exclusive voting rights with respect to its service and/or distribution plans. The Funds’ income, expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Funds in preparation of their financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Funds follow the specialized accounting and reporting requirements under GAAP that are applicable to investment companies.

Security Valuation – The Funds’ securities are valued at the last sale price on the exchange in which such securities are primarily traded, as of the close of business on the day the securities are being valued. In the absence of a sale on the primary exchange, such securities shall be valued at the last bid on the primary exchange. NASDAQ traded securities are valued using the NASDAQ Official Closing Price (“NOCP”). Investments valued in currencies other than the U.S. dollar are converted to U.S. dollars using exchange rates obtained from pricing services.

If market quotations are not readily available, securities will be valued at their fair market value as determined in good faith by the adviser in accordance with procedures approved by the Trust’s Board of Trustees (the “Board”) and evaluated by the Board as to the reliability of the fair value method used. The procedures consider, among others, the following factors to determine a security’s fair value: the nature and pricing history (if any) of the security; whether any dealer quotations for the security are available; and possible valuation methodologies that could be used to determine the fair value of the security.

The Funds utilize various methods to measure the fair value of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Funds have the ability to access.

| Copeland Trust |

| NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued) |

| May 31, 2015 |

| |

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.