united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22483

Copeland Trust

(Exact name of Registrant as specified in charter)

Eight Tower Bridge, 161 Washington St., Suite #1325 Conshohocken, PA 19428

(Address of principal executive offices) (Zip code)

Gemini Fund Services, LLC, 80 Arkay Drive Suite 10, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: (631) 470-2619

Date of fiscal year end: 11/30

Date of reporting period: 11/30/20

Item 1. Reports to Stockholders.

| Copeland | ||

| Dividend Growth Fund | ||

| (formerly, Copeland Risk Managed Dividend Growth Fund) | ||

| Copeland | ||

| SMID Cap | ||

| Dividend Growth Fund | ||

| Annual Report | ||

| November 30, 2020 | ||

| Investor Information: 1-888-9-COPELAND | ||

| This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer of sale or solicitation of an offer to buy shares of the Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. | ||

| Distributed by Northern Lights Distributors, LLC | ||

| Member FINRA | ||

Copeland Dividend Growth Fund

Annual Report

November 30, 2020

Dear Fellow Shareholders,

Copeland Capital Management is pleased to review the performance of the Copeland Dividend Growth Fund for the fiscal year beginning December 1, 2019 through November 30, 2020. Unless otherwise stated herein, all data and statistics that follow are as of November 30, 2020.

During the twelve-month period, the Class I shares of the Fund delivered a 2.4% return versus the 17.5% advance posted by the S&P 500 Index. The underperformance was wholly attributable to the average cash and cash equivalent position of 22% held by the Fund over the course of the measurement period. The defensive posture was triggered by the violent peak-to-trough market decline of 34% over the course of just 34 days in late February through March 23, 2020. The rapid downdraft, fueled by the U.S. outbreak of the Coronavirus, stands as the fastest 30% plus market decline in history.

All nine of our proprietary sector signals registered a negative reading as we moved into April, leading the Fund to rein in its overall equity exposure level to 50%. Defying all expectations, the market staged a sharp rally of over +60% from the market low through November 30, 2020. While the Fund added equity exposure over the balance of the year, the initial V-shaped nature of the recovery was a decided drag on performance. Perhaps most importantly, since November 16, 2020, the Fund no longer applies a sector rotation strategy and now maintains a substantially fully invested position under normal conditions and will continue to do so from this point onward, in an effort to reduce the impact of potential violent market whipsaws on the Fund, which have characterized the investment climate in recent years.

Our stock selection in the Financials sector of the market bolstered Fund returns while those in the Information Technology sector were a drag. Bucking the overall Fund trend, Information Technology holding Apple Inc. (AAPL, 2.4% of holdings) rose a sharp 79% during the period. This consumer electronics behemoth has posted strong growth amidst the backdrop of the global pandemic. Work-from-home trends bolstered sales of iPads and Mac computers, which rose 31% and 22%, respectively in the most recently reported quarter. In addition, highly valued services revenue, given its recurring nature, grew over 15% versus the prior year to top $13 billion. A second standout performer, Financials sector constituent MSCI Inc. (MSCI, 1.1% of holdings), advanced over 57% during the period despite a 6% downdraft in the broader Financials sector. This provider of index, portfolio construction and risk management tools has benefitted from an ongoing shift towards passive, index-based investing. A focus on Environmental, Social and Governance (ESG) investing has also proven to be a windfall to MSCI, as this area continues to attract outsized attention and client assets. The aforementioned tailwinds have fueled a steep five-year compound annual growth rate in revenues and earnings at MSCI of 10% and 28%, respectively. With 74% of revenues coming from recurring subscriptions and a customer retention rate of nearly 95%, the exemplary results posted by MSCI appear to us to be poised to continue for the foreseeable future.

On the downside, Fund holding Diamondback Energy (FANG, 0.0% of holdings) was the worst performer in the Fund, falling over 78% while we held a position in the company. This oil and gas exploration company was sharply impacted by an unfolding oil price war between Russia and Saudi Arabia which triggered a halving of the price of West Texas Intermediate (“WTI”) crude oil from $61 per barrel at the start of the year, to under $30 per barrel during the month of March. Amidst fears surrounding a potential dividend cut, we elected to exit our position in the shares. Healthcare sector constituent, U.S. Physical Therapy (USPH, 0.0% of holdings) was also a laggard as shares retreated over 40% during the period. The operator of outpatient physical therapy clinics suffered as the pandemic forced clinics to either close or experience sharply reduced patient volumes, by as much as 50%. The company took steps to weather the

1

downturn including lay-offs, salary reductions and lease renegotiations. Nevertheless, we elected to eliminate our position is the shares as the company reported that an upcoming suspension of the dividend was likely.

Looking back over the prior twelve-month period, it is striking that the market has climbed over 17% in the face of the Coronavirus pandemic. $2.2 trillion in economic stimulus in the form of the Coronavirus Aid, Relief, and Economic Stability (CARES) Act, coupled with aggressive monetary easing from the Federal Reserve, provided the initial fuel for the market recovery. More recently, news of forthcoming successful COVID-19 vaccines from both Pfizer and Moderna, propelled the equity markets to gain nearly 11% in the month of November. Looking forward, we believe that the equity market outlook is clouded by the crosscurrents of a potential end to the global pandemic, juxtaposed against the financial and human toll exacted by the virus.

Regardless of the future path taken by the equity market, we at Copeland remain intently focused on the long-term prospects of companies held in the Fund, with a particular emphasis on the capacity of each to continue to grow its dividend over time. We continue to favor companies that we believe retain noteworthy competitive advantages in their respective industries, generate steady and growing cash flows, and are overseen by managements with capital allocation discipline and an eye on the shareholder. With dividend growth equities having lagged the broader market indices of late, we find the present environment to be particularly attractive for the high quality, cash generative companies in which we invest. Longer term, we look forward to maintaining a substantially invested investment position under normal conditions, in an attempt to reap the potential rewards historically afforded by equity securities, in general and dividend growth securities in particular.

Thank you for the confidence you have placed in Copeland and for your investment in the Copeland Dividend Growth Fund.

The views and opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed. The Fund holdings discussed herein are for informational purposes only and should not be perceived as investment recommendations by Copeland Capital Management. Holdings are subject to change, may not represent current holdings and are subject to risk. Performance data quoted here represents past performance. Past performance is no guarantee of future results. The return quoted reflects fee waivers and expense reimbursements in effect and would have been lower in their absence. Current performance may be lower or higher than the performance quoted above. The risks of investing in the Copeland Funds vary from fund to fund; to see the risks of investing in an individual fund, please refer to that fund’s latest prospectus.

You cannot invest directly in any index. Index returns do not include a deduction for fees or expenses. The S&P 500® Index is a market-capitalization-weighted index of the stocks of 500 leading companies in major industries of the U.S. economy.

1017-NLD-1/21/2021

2

Copeland SMID Cap Dividend Growth Fund

Annual Report

November 30, 2020

Dear Fellow Shareholders,

Copeland Capital Management is pleased to review the performance of the Copeland SMID Cap Dividend Growth Fund for the fiscal year beginning December 1, 2019 through November 30, 2020. Unless otherwise stated herein, all data and statistics that follow are as of November 30, 2020.

During the twelve-month period ended November 30, 2020, Class I shares of the Fund delivered a +5.0% return, versus the +13.9% advance posted by the Russell 2500 Index. The Fund outperformed the benchmark during the first half of the year, when the Covid-19 pandemic spread across the globe and led to a massive decline in equity markets, including a 40% decline among SMID cap equities from mid-February through the lows of mid-March. Unprecedented fiscal stimulus was quickly enacted that supported the unemployed as well as impaired businesses, while the Federal Reserve stepped in to ensure that the bond markets and banks kept the lending markets functioning. Meanwhile the health care industry was called to action and, far more quickly than expected, was able to deliver pharmaceuticals and start to develop vaccines that could target the virus, which engendered optimism in the markets. The result was a remarkable stock market rebound that continued through the period’s end. SMID Cap equities were more significantly impaired than their larger cap counterparts during the decline, and then led the accelerating rally that closed the period as investors grew more confident that massive stimulus would lead to a strong recovery in both the economy and corporate earnings. The Fund lagged the benchmark during the recovery, which is an unsurprising outcome given the typical preference of investors for higher risk, lower quality, speculative investments following a deep recession.

We believe our dividend growth strategy behaved as it was designed, delivering resiliency during the downdrafts while reasonably participating in the rebounds, aided in both instances by strong rates of dividend growth.

Our stock selection in the Financials sector most significantly aided Fund returns. MarketAxess Holdings (MKTX, 1.6%), which operates an innovative electronic trading platform for fixed income securities, rallied as market share gains were evident in the company’s rapidly expanding trading volumes. We believe that robust earnings growth, projected to reach 44% for the year, should enable the company to extend its 10-year streak of raising its dividend. Discover Financial Services (DFS, 0.0%), a leading provider or credit cards and lending to consumers and small businesses, provided significant appreciation from the Fund’s timely purchase of shares near the market low in March. Expectations for large credit losses proved overly pessimistic as the government supported consumers and the economy quickly rebounded. The Fund also benefited from stocks with exposure to activities that were enhanced by the changing spending habits of consumers during the pandemic, such as Pool Corporation (POOL, 1.5%). As the dominant distributor of pool supplies and equipment in the United States, the company’s sales and profits accelerated during the year as consumers were spending their leisure time at home.

The Fund’s selections within the Health Care sector were a drag on performance, despite appreciating as a group by over 13%. However, biotechnology stocks, which are a material weighting in the benchmark, returned on average 86% during the period as investors speculated on the winners of the Covid-19 vaccine arms race. Similarly, while the Fund’s Technology stocks rose as a group by nearly 18%, they lagged the average return of 39% among the Technology stocks in the benchmark. We believe that both of these examples reflect the market’s short-term preference for speculative investments to the detriment of resilient dividend growth companies. Finally, Ryman Hospitality Properties (RHP, 0.0%) declined significantly during March when hotels were closed, and conferences were cancelled as the pandemic worsened. As a result of our belief that the dividend was at risk, the stock was sold from the portfolio.

3

Looking forward, we believe that the equity market outlook is clouded by the crosscurrents of a potential end to the global pandemic, juxtaposed against the financial and human toll exacted by the virus and valuations in some corners of the market that have reached historically high levels. With dividend growth equities having lagged the broader market indices of late, we find the present environment to be particularly attractive for the high quality, cash generative companies in which we invest.

Regardless of the future path taken by the equity market, we at Copeland we remain intently focused on the long-term prospects of companies held in the Fund, with a particular emphasis on the capacity of each to continue to grow its dividend over time. We continue to favor companies that we believe retain noteworthy competitive advantages in their respective industries, are cash generative, and are overseen by managements with capital allocation discipline and an eye on the shareholder. By owning a diversified portfolio of such companies, we hope to deliver better than benchmark returns over time, but with less volatility than is typically found when owning SMID Cap stocks.

Thank you for the confidence you have placed in Copeland and for your investment in the Copeland SMID Cap Dividend Growth Fund.

The views and opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed. The Fund holdings discussed herein are for informational purposes only and should not be perceived as investment recommendations by Copeland Capital Management. Holdings are subject to change, may not represent current holdings and are subject to risk. Performance data quoted here represents past performance. Past performance is no guarantee of future results. The return quoted reflects fee waivers and expense reimbursements in effect and would have been lower in their absence. Current performance may be lower or higher than the performance quoted above. The risks of investing in the Copeland Funds vary from fund to fund; to see the risks of investing in an individual fund, please refer to that fund’s latest prospectus.

You cannot invest directly in any index. Index returns do not include a deduction for fees or expenses. The Russell 2500 Index is comprised of the bottom 2500 companies in the Russell 3000 Index. The Russell 3000 Index measures the performance of the 3000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

1017-NLD-1/21/2021

4

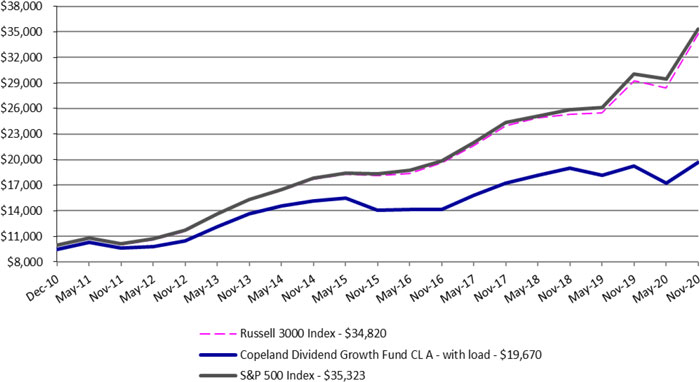

| Copeland Dividend Growth Fund |

| Portfolio Review (Unaudited) |

| December 28, 2010* through November 30, 2020 |

Performance of a $10,000 Investment (as of November 30, 2020)

| Average Annualized | Since | Since | Since | ||

| Total Returns as of | Inception | Inception | Inception | ||

| November 30, 2020 | One Year | Five Year | Class A * | Class C * | Class I * |

| Copeland Dividend Growth Fund: | |||||

| Class A | |||||

| Without sales charge | 2.24% | 6.91% | 7.70% | — | — |

| With sales charge + | -3.65% | 5.65% | 7.06% | — | — |

| Class C | 1.51% | 6.11% | — | 7.49% | — |

| Class I | 2.40% | 7.07% | — | — | 7.50% |

| S&P 500 Index | 17.46% | 13.99% | 13.56% | 14.72% | 14.17% |

| Russell 3000 Index | 19.02% | 13.95% | 13.40% | 14.68% | 14.03% |

| * | Class A shares commenced operations on December 28, 2010. Class C commenced operations on January 5, 2012. Class I commenced operations March 1, 2013. |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The S&P 500 Index is an unmanaged market capitalization-weighted index which is comprised of 500 of the largest U.S. domiciled companies and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

The Russell 3000 Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. The performance and returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or redemption of Fund shares. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. For performance information current to the most recent month-end please call toll-free 1-888-9-COPELAND (1-888-926-7352). Additional information can be found by visiting our website, www.copelandfunds.com. The Fund’s gross annual operating expense ratio, as stated in the current prospectus, is 1.49%, 2.24%, and 1.34%,for Class A, Class C, and Class I shares, respectively, and its net annual operating expense ratio is 1.20%, 1.95%, and 1.05%, for Class A, Class C, and Class I shares, respectively. These ratios can fluctuate and may differ from the expense ratios disclosed in the Financial Highlights section of this report. The Fund’s investment adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until December 31, 2021, to ensure that total annual fund operating expenses after fee deferral and/or reimbursement (exclusive of any taxes, leverage interest, borrowing interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expense on securities sold short, acquired fund fees and expenses or extraordinary expenses such as litigation) will not exceed 1.20%, 1.95% and 1.05% of Class A, Class C and Class I shares, respectively, subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after the fees have been deferred or reimbursed) if such recoupment can be achieved without exceeding the lesser of the expense limitation in effect at the time of the deferral and at the time of the repayment. Prior to November 16, 2020, the expense limitations were 1.45%, 2.20%, and 1.30% of Class A, Class C and Class I shares, respectively.

5

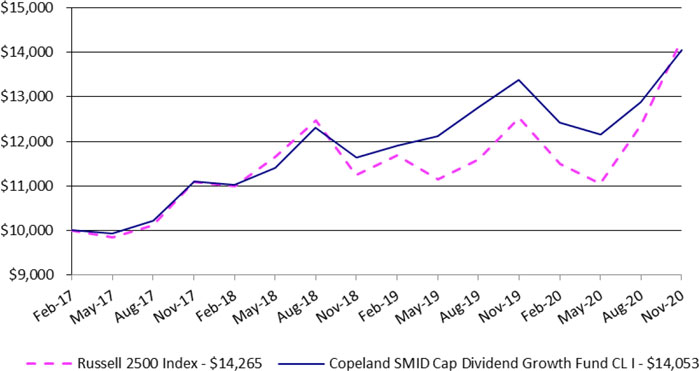

| Copeland SMID Cap Dividend Growth Fund |

| Portfolio Review (Unaudited) |

| February 27, 2017* through November 30, 2020 |

Performance of a $10,000 Investment (as of November 30, 2020)

| Since | Since | ||

| Total Returns as of | Inception | Inception | |

| November 30, 2020 | One Year | Class I * | Class A * |

| Copeland SMID Cap Dividend Growth Fund: | |||

| Class I | 4.98% | 9.48% | — |

| Class A | |||

| Without sales charge | 4.73% | — | 10.72% |

| With sales charge + | -1.31% | — | 7.12% |

| Russell 2500 Index | 13.86% | 9.92% | 13.65% |

| * | Class I shares commenced operations February 27, 2017. Class A commenced operations February 11, 2019 |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The Russell 2500 Index is comprised of the smallest 2500 companies in the Russell 3000 Index. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market. Investors cannot invest directly in an index or benchmark.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. The performance and returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or redemption of Fund shares. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. For performance information current to the most recent month-end please call toll-free 1-888-9-COPELAND (1-888-926-7352). Additional information can be found by visiting our website, www.copelandfunds.com. The Fund’s gross annual operating expense ratio, as stated in the current prospectus is 3.04% and 1.18% for Class A and Class C shares, respectively, and its net annual operating expense ratio is 1.20% and 0.95% for Class A and Class I shares, respectively. This ratio can fluctuate and may differ from the expense ratio disclosed in the Financial Highlights section of this report. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, until at least March 31, 2021, to ensure that total annual fund operating expenses after fee deferral and/or reimbursement (exclusive of any taxes, leverage interest, borrowing interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expense on securities sold short, acquired fund fees and expenses or extraordinary expenses such as litigation) will not exceed 1.20% and 0.95% of Class A and Class I shares, respectively, subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after the fees have been deferred or reimbursed) if such recoupment can be achieved without exceeding the lesser of the expense limitation in effect at the time of the deferral and at the time of the repayment.

6

| Copeland Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS |

| November 30, 2020 |

| Shares | Security | Market Value | ||||||

| COMMON STOCK - 98.8% | ||||||||

| AEROSPACE & DEFENSE - 2.4% | ||||||||

| 5,652 | Huntington Ingalls Industries, Inc. | $ | 905,394 | |||||

| 2,206 | Lockheed Martin Corporation | 805,190 | ||||||

| 1,710,584 | ||||||||

| ASSET MANAGEMENT - 2.6% | ||||||||

| 5,190 | Ameriprise Financial, Inc. | 961,396 | ||||||

| 1,229 | BlackRock, Inc. | 858,272 | ||||||

| 1,819,668 | ||||||||

| BANKING - 2.5% | ||||||||

| 8,468 | JPMorgan Chase & Company | 998,208 | ||||||

| 16,392 | Truist Financial Corporation | 760,917 | ||||||

| 1,759,125 | ||||||||

| BIOTECHNOLOGY & PHARMACEUTICALS - 1.5% | ||||||||

| 6,627 | Zoetis, Inc. | 1,062,838 | ||||||

| CABLE & SATELLITE - 4.0% | ||||||||

| 450 | Cable One, Inc. | 891,302 | ||||||

| 18,679 | Comcast Corporation | 938,433 | ||||||

| 149,538 | Sirius XM Holdings, Inc. | 970,502 | ||||||

| 2,800,237 | ||||||||

| CHEMICALS - 3.0% | ||||||||

| 1,790 | Air Products and Chemicals, Inc. | 501,451 | ||||||

| 2,537 | Ecolab, Inc. | 563,594 | ||||||

| 2,489 | Quaker Chemical Corporation | 614,783 | ||||||

| 568 | Sherwin-Williams Company (The) | 424,654 | ||||||

| 2,104,482 | ||||||||

| COMMERCIAL SUPPORT SERVICES - 2.4% | ||||||||

| 4,389 | UniFirst Corporation | 811,438 | ||||||

| 8,110 | Waste Connections, Inc. | 843,278 | ||||||

| 1,654,716 | ||||||||

| ELECTRIC UTILITIES - 1.9% | ||||||||

| 43,408 | Algonquin Power & Utilities Corporation | 680,637 | ||||||

| 9,160 | NextEra Energy, Inc. | 674,084 | ||||||

| 1,354,721 | ||||||||

| ELECTRICAL EQUIPMENT - 1.2% | ||||||||

| 13,061 | Otis Worldwide Corporation | 874,303 | ||||||

| ENGINEERING & CONSTRUCTION - 1.4% | ||||||||

| 8,254 | Tetra Tech, Inc. | 984,290 | ||||||

| FOOD - 2.8% | ||||||||

| 4,743 | J & J Snack Foods Corporation | 689,585 | ||||||

| 8,961 | Lamb Weston Holdings, Inc. | 648,597 | ||||||

| 3,290 | McCormick & Company, Inc. | 615,164 | ||||||

| 1,953,346 | ||||||||

| GAS & WATER UTILITIES - 1.0% | ||||||||

| 4,363 | American Water Works Company, Inc. | 669,197 | ||||||

| HEALTH CARE FACILITIES & SERVICES - 8.5% | ||||||||

| 2,236 | Chemed Corporation | 1,069,367 | ||||||

| 16,377 | Encompass Health Corporation | 1,319,659 | ||||||

| 18,515 | Ensign Group, Inc. (The) | 1,330,673 | ||||||

| 9,231 | Quest Diagnostics, Inc. | 1,144,459 | ||||||

| 3,400 | UnitedHealth Group, Inc. | 1,143,556 | ||||||

| 6,007,714 | ||||||||

| HOME CONSTRUCTION - 1.3% | ||||||||

| 12,372 | DR Horton, Inc. | 921,714 | ||||||

| HOUSEHOLD PRODUCTS - 0.9% | ||||||||

| 7,011 | Church & Dwight Company, Inc. | 615,355 | ||||||

| INDUSTRIAL SUPPORT SERVICES - 1.3% | ||||||||

| 18,417 | Fastenal Company | 910,721 | ||||||

| INSURANCE - 1.3% | ||||||||

| 8,954 | Allstate Corporation (The) | 916,442 | ||||||

The accompanying notes are an integral part of these financial statements.

7

| Copeland Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| November 30, 2020 |

| Shares | Security | Market Value | ||||||

| COMMON STOCK - 98.8% (Continued) | ||||||||

| LEISURE FACILITIES & SERVICES - 2.7% | ||||||||

| 2,173 | Domino’s Pizza, Inc. | $ | 853,055 | |||||

| 10,690 | Starbucks Corporation | 1,047,834 | ||||||

| 1,900,889 | ||||||||

| LEISURE PRODUCTS - 1.6% | ||||||||

| 14,666 | Brunswick Corporation | 1,094,670 | ||||||

| MEDICAL EQUIPMENT & DEVICES - 5.2% | ||||||||

| 10,345 | Medtronic plc | 1,176,227 | ||||||

| 6,376 | ResMed, Inc. | 1,336,410 | ||||||

| 5,915 | STERIS plc | 1,146,386 | ||||||

| 3,659,023 | ||||||||

| OIL & GAS PRODUCERS - 0.6% | ||||||||

| 24,239 | Cabot Oil & Gas Corporation | 424,667 | ||||||

| PUBLISHING & BROADCASTING - 1.4% | ||||||||

| 9,287 | Nexstar Media Group, Inc. | 977,457 | ||||||

| REITS - 3.6% | ||||||||

| 3,052 | Alexandria Real Estate Equities, Inc. | 499,704 | ||||||

| 1,894 | American Tower Corporation | 437,893 | ||||||

| 688 | Equinix, Inc. | 480,080 | ||||||

| 4,017 | Innovative Industrial Properties, Inc. | 617,252 | ||||||

| 11,254 | NexPoint Residential Trust, Inc. | 498,665 | ||||||

| 2,533,594 | ||||||||

| RETAIL - CONSUMER STAPLES - 3.2% | ||||||||

| 3,462 | Casey’s General Stores, Inc. | 628,976 | ||||||

| 1,761 | Costco Wholesale Corporation | 689,907 | ||||||

| 4,377 | Dollar General Corporation | 956,725 | ||||||

| 2,275,608 | ||||||||

| RETAIL - DISCRETIONARY - 3.9% | ||||||||

| 6,002 | Advance Auto Parts, Inc. | 886,495 | ||||||

| 3,361 | Home Depot, Inc. (The) | 932,375 | ||||||

| 6,566 | Tractor Supply Company | 924,558 | ||||||

| 2,743,428 | ||||||||

| SEMICONDUCTORS - 6.7% | ||||||||

| 3,192 | Broadcom, Inc. | 1,281,843 | ||||||

| 4,539 | CMC Materials, Inc. | 700,277 | ||||||

| 8,089 | Texas Instruments, Inc. | 1,304,351 | ||||||

| 6,243 | Universal Display Corporation | 1,429,897 | ||||||

| 4,716,368 | ||||||||

| SOFTWARE - 3.7% | ||||||||

| 3,571 | Intuit, Inc. | 1,257,063 | ||||||

| 6,229 | Microsoft Corporation | 1,333,442 | ||||||

| 2,590,505 | ||||||||

| SPECIALTY FINANCE - 3.0% | ||||||||

| 16,186 | Aaron’s Holdings Company, Inc. | 1,018,585 | ||||||

| 14,545 | Discover Financial Services | 1,107,893 | ||||||

| 2,126,478 | ||||||||

| TECHNOLOGY HARDWARE - 5.2% | ||||||||

| 14,028 | Apple, Inc. | 1,670,033 | ||||||

| 26,022 | AudioCodes Ltd. | 727,835 | ||||||

| 7,415 | Motorola Solutions, Inc. | 1,271,895 | ||||||

| 3,669,763 | ||||||||

| TECHNOLOGY SERVICES - 15.0% | ||||||||

| 5,275 | Accenture plc | 1,313,950 | ||||||

| 8,534 | Automatic Data Processing, Inc. | 1,483,892 | ||||||

| 14,146 | Booz Allen Hamilton Holding Corporation | 1,227,731 | ||||||

| 8,567 | Broadridge Financial Solutions, Inc. | 1,258,321 | ||||||

| 9,468 | CDW Corporation/DE | 1,235,479 | ||||||

| 3,615 | FactSet Research Systems, Inc. | 1,206,542 | ||||||

| 1,490 | MarketAxess Holdings, Inc. | 803,378 | ||||||

| 1,907 | MSCI, Inc. | 780,764 | ||||||

| 5,802 | Visa, Inc. | 1,220,451 | ||||||

| 10,530,508 | ||||||||

The accompanying notes are an integral part of these financial statements.

8

| Copeland Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| November 30, 2020 |

| Shares | Security | Market Value | ||||||

| COMMON STOCK - 98.8% (Continued) | ||||||||

| TELECOMMUNICATIONS - 0.9% | ||||||||

| 10,779 | Cogent Communications Holdings, Inc. | $ | 626,691 | |||||

| TRANSPORTATION & LOGISTICS - 1.2% | ||||||||

| 4,163 | Union Pacific Corporation | 849,585 | ||||||

| WHOLESALE - CONSUMER STAPLES - 0.9% | ||||||||

| 9,243 | Calavo Growers, Inc. | 662,076 | ||||||

| TOTAL COMMON STOCK (Cost - $60,043,955) | 69,500,763 | |||||||

| TOTAL INVESTMENTS - 98.8% (Cost - $60,043,955) | $ | 69,500,763 | ||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES - 1.2% | 864,299 | |||||||

| NET ASSETS - 100.0% | $ | 70,365,062 | ||||||

plc - Public Limited Company

REITs - Real Estate Investment Trusts

| Portfolio Composition as of November 30, 2020 | ||||

| Sector | Percent of Net Assets | |||

| Technology | 30.6 | % | ||

| Health Care | 15.2 | % | ||

| Industrials | 9.9 | % | ||

| Consumer Discretionary | 9.5 | % | ||

| Financials | 9.4 | % | ||

| Consumer Staples | 7.8 | % | ||

| Communications | 6.3 | % | ||

| Real Estate | 3.6 | % | ||

| Materials | 3.0 | % | ||

| Utilities | 2.9 | % | ||

| Energy | 0.6 | % | ||

| Other Assets in Excess of Liabilities | 1.2 | % | ||

| Net Assets | 100.0 | % | ||

The accompanying notes are an integral part of these financial statements.

9

| Copeland SMID Cap Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS |

| November 30, 2020 |

| Shares | Security | Market Value | ||||||

| COMMON STOCK - 96.5% | ||||||||

| AEROSPACE & DEFENSE - 1.4% | ||||||||

| 1,982 | Huntington Ingalls Industries, Inc. | $ | 317,497 | |||||

| ASSET MANAGEMENT - 3.1% | ||||||||

| 5,872 | Cohen & Steers, Inc. | 415,561 | ||||||

| 16,805 | Kennedy-Wilson Holdings, Inc. | 268,544 | ||||||

| 684,105 | ||||||||

| BANKING - 4.6% | ||||||||

| 12,525 | Bank OZK | 350,199 | ||||||

| 18,301 | Home BancShares, Inc. | 338,752 | ||||||

| 5,145 | Prosperity Bancshares, Inc. | 323,260 | ||||||

| 1,012,211 | ||||||||

| CABLE & SATELITE - 1.5% | ||||||||

| 164 | Cable One, Inc. | 324,830 | ||||||

| CHEMICALS - 2.0% | ||||||||

| 1,774 | Quaker Chemical Corporation | 438,178 | ||||||

| COMMERCIAL SUPPORT SERVICES - 2.6% | ||||||||

| 7,418 | ABM Industries, Inc. | 285,593 | ||||||

| 1,556 | UniFirst Corporation | 287,673 | ||||||

| 573,266 | ||||||||

| ELECTRIC UTILITIES - 1.3% | ||||||||

| 18,485 | Algonquin Power & Utilities Corporation | 289,845 | ||||||

| ELECTRICAL EQUIPMENT - 6.2% | ||||||||

| 4,660 | Badger Meter, Inc. | 384,170 | ||||||

| 5,533 | BWX Technologies, Inc. | 314,717 | ||||||

| 4,386 | Cognex Corporation | 329,564 | ||||||

| 1,467 | Littelfuse, Inc. | 352,858 | ||||||

| 1,381,309 | ||||||||

| ENGINEERING & CONSTRUCTION - 2.6% | ||||||||

| 2,725 | Exponent, Inc. | 226,202 | ||||||

| 2,972 | Tetra Tech, Inc. | 354,411 | ||||||

| 580,613 | ||||||||

| FOOD - 2.9% | ||||||||

| 2,213 | J & J Snack Foods Corporation | 321,748 | ||||||

| 4,299 | Lamb Weston Holdings, Inc. | 311,162 | ||||||

| 632,910 | ||||||||

| GAS & WATER UTILITIES - 2.4% | ||||||||

| 3,242 | American States Water Company | 239,324 | ||||||

| 8,253 | UGI Corporation | 292,816 | ||||||

| 532,140 | ||||||||

| HEALTH CARE FACILITIES & SERVICES - 7.2% | ||||||||

| 735 | Chemed Corporation | 351,514 | ||||||

| 4,266 | Encompass Health Corporation | 343,754 | ||||||

| 8,008 | Ensign Group, Inc. (The) | 575,535 | ||||||

| 2,686 | Quest Diagnostics, Inc. | 333,010 | ||||||

| 1,603,813 | ||||||||

| HOME CONSTRUCTION - 0.7% | ||||||||

| 4,648 | KB Home | 163,610 | ||||||

| INDUSTRIAL SUPPORT SERVICES - 1.9% | ||||||||

| 5,042 | MSC Industrial Direct Company, Inc. | 420,099 | ||||||

| INSTITUTIONAL FINANCIAL SERVICES - 1.4% | ||||||||

| 8,480 | Lazard Ltd. | 316,474 | ||||||

| INSURANCE - 1.3% | ||||||||

| 3,013 | Globe Life, Inc. | 280,510 | ||||||

The accompanying notes are an integral part of these financial statements.

10

| Copeland SMID Cap Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| November 30, 2020 |

| Shares | Security | Market Value | ||||||

| COMMON STOCK - 96.5% (Continued) | ||||||||

| INTERNET MEDIA & SERVICES - 0.5% | ||||||||

| 1,588 | Shutterstock, Inc. | $ | 109,191 | |||||

| LEISURE FACILITIES & SERVICES - 2.0% | ||||||||

| 822 | Domino’s Pizza, Inc. | 322,693 | ||||||

| 852 | Wingstop, Inc. | 108,468 | ||||||

| 431,161 | ||||||||

| LEISURE PRODUCTS - 1.9% | ||||||||

| 5,541 | Brunswick Corporation | 413,580 | ||||||

| MACHINERY - 4.4% | ||||||||

| 1,374 | Nordson Corporation | 280,035 | ||||||

| 2,129 | Snap-on, Inc. | 374,385 | ||||||

| 3,624 | Toro Company (The) | 328,733 | ||||||

| 983,153 | ||||||||

| MEDICAL EQUIPMENT & DEVICES - 3.8% | ||||||||

| 2,910 | LeMaitre Vascular, Inc. | 114,625 | ||||||

| 12,447 | Luminex Corporation | 295,367 | ||||||

| 2,198 | STERIS plc | 425,994 | ||||||

| 835,986 | ||||||||

| OIL & GAS PRODUCERS - 1.8% | ||||||||

| 17,121 | Cabot Oil & Gas Corporation | 299,960 | ||||||

| 2,595 | Diamondback Energy, Inc. | 103,696 | ||||||

| 403,656 | ||||||||

| PUBLISHING & BROADCASTING - 1.6% | ||||||||

| 3,317 | Nexstar Media Group, Inc. | 349,114 | ||||||

| REITS - 6.9% | ||||||||

| 2,129 | Alexandria Real Estate Equities, Inc. | 348,581 | ||||||

| 8,490 | Americold Realty Trust | 289,764 | ||||||

| 2,082 | Innovative Industrial Properties, Inc. | 319,920 | ||||||

| 6,881 | NexPoint Residential Trust, Inc. | 304,897 | ||||||

| 4,631 | QTS Realty Trust, Inc. | 275,128 | ||||||

| 1,538,290 | ||||||||

| RETAIL - CONSUMER STAPLES - 1.5% | ||||||||

| 1,803 | Casey’s General Stores, Inc. | 327,569 | ||||||

| RETAIL - DISCRETIONARY - 4.4% | ||||||||

| 1,936 | Advance Auto Parts, Inc. | 285,947 | ||||||

| 6,819 | Monro, Inc. | 320,561 | ||||||

| 2,557 | Tractor Supply Company | 360,051 | ||||||

| 966,559 | ||||||||

| SEMICONDUCTORS - 5.3% | ||||||||

| 2,338 | CMC Materials, Inc. | 360,707 | ||||||

| 5,526 | Power Integrations, Inc. | 394,501 | ||||||

| 1,800 | Universal Display Corporation | 412,272 | ||||||

| 1,167,480 | ||||||||

| SPECIALTY FINANCE - 2.0% | ||||||||

| 7,164 | Aaron’s Holdings Company, Inc. | 450,831 | ||||||

| TECHNOLOGY HARDWARE - 1.1% | ||||||||

| 8,889 | AudioCodes Ltd. | 248,625 | ||||||

| TECHNOLOGY SERVICES - 9.4% | ||||||||

| 2,060 | Broadridge Financial Solutions, Inc. | 302,573 | ||||||

| 975 | FactSet Research Systems, Inc. | 325,416 | ||||||

| 1,762 | Jack Henry & Associates, Inc. | 283,435 | ||||||

| 4,018 | ManTech International Corporation | 309,266 | ||||||

| 647 | MarketAxess Holdings, Inc. | 348,850 | ||||||

| 3,877 | MAXIMUS, Inc. | 278,407 | ||||||

| 1,210 | Morningstar, Inc. | 242,121 | ||||||

| 2,090,068 | ||||||||

The accompanying notes are an integral part of these financial statements.

11

| Copeland SMID Cap Dividend Growth Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| November 30, 2020 |

| Shares | Security | Market Value | ||||||

| COMMON STOCK - 96.5% (Continued) | ||||||||

| TELECOMMUNICATIONS - 1.3% | ||||||||

| 4,925 | Cogent Communications Holdings, Inc. | $ | 286,340 | |||||

| TRANSPORTATION & LOGISTICS - 1.1% | ||||||||

| 1,927 | Landstar System, Inc. | 253,246 | ||||||

| WHOLESALE - CONSUMER STAPLES - 2.9% | ||||||||

| 4,390 | Calavo Growers, Inc. | 314,456 | ||||||

| 10,830 | Core-Mark Holding Company, Inc. | 337,788 | ||||||

| 652,244 | ||||||||

| WHOLESALE - DISCRETIONARY - 1.5% | ||||||||

| 974 | Pool Corporation | 337,111 | ||||||

| TOTAL COMMON STOCK (Cost - $19,081,974) | 21,395,614 | |||||||

| TOTAL INVESTMENTS - 96.5% (Cost - $19,081,974) | $ | 21,395,614 | ||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES - 3.5% | 768,237 | |||||||

| NET ASSETS - 100.00% | $ | 22,163,851 | ||||||

plc - Public Limited Company

REITs - Real Estate Investment Trusts

| Portfolio Composition as of November 30, 2020 | ||||

| Sector | Percent of Net Assets | |||

| Industrials | 20.4 | % | ||

| Technology | 15.8 | % | ||

| Financials | 12.4 | % | ||

| Health Care | 11.0 | % | ||

| Consumer Discretionary | 10.4 | % | ||

| Consumer Staples | 7.3 | % | ||

| Real Estate | 6.9 | % | ||

| Communications | 4.8 | % | ||

| Utilities | 3.7 | % | ||

| Materials | 2.0 | % | ||

| Energy | 1.8 | % | ||

| Other Assets in Excess of Liabilities | 3.5 | % | ||

| Net Assets | 100.0 | % | ||

The accompanying notes are an integral part of these financial statements.

12

| Copeland Trust |

| STATEMENTS OF ASSETS AND LIABILITIES |

| November 30, 2020 |

| Copeland SMID | ||||||||

| Copeland Dividend | Cap Dividend | |||||||

| Growth Fund | Growth Fund | |||||||

| Assets: | ||||||||

| Investments, at Cost | $ | 60,043,955 | $ | 19,081,974 | ||||

| Investments in Securities, at Market Value | $ | 69,500,763 | $ | 21,395,614 | ||||

| Cash | 807,831 | 622,401 | ||||||

| Dividends and Interest Receivable | 104,931 | 59,414 | ||||||

| Due from Investment Adviser | 39,086 | 92,233 | ||||||

| Receivable for Fund Shares Sold | 19,579 | 7,278 | ||||||

| Prepaid Expenses and Other Assets | 51,804 | 20,902 | ||||||

| Total Assets | 70,523,994 | 22,197,842 | ||||||

| Liabilities: | ||||||||

| Payable for Fund Shares Redeemed | 49,895 | — | ||||||

| Accrued Audit Fees | 15,289 | 6,466 | ||||||

| Accrued Distribution Fees | 16,301 | 21 | ||||||

| Payable to Related Parties | 27,450 | 11,330 | ||||||

| Other Accrued Expenses | 49,997 | 16,174 | ||||||

| Total Liabilities | 158,932 | 33,991 | ||||||

| Net Assets | $ | 70,365,062 | $ | 22,163,851 | ||||

| Composition of Net Assets: | ||||||||

| At November 30, 2020, Net Assets consisted of: | ||||||||

| Paid-in-Capital | $ | 62,738,773 | $ | 19,881,890 | ||||

| Accumulated Earnings (Loss) | 7,626,289 | 2,281,961 | ||||||

| Net Assets | $ | 70,365,062 | $ | 22,163,851 | ||||

| Class A Shares: | ||||||||

| Net Assets | $ | 18,799,786 | $ | 108,247 | ||||

| Shares Outstanding (no par value; unlimited number of shares authorized) | 1,568,609 | 8,239 | ||||||

| Net Asset Value and Redemption Price Per Share* | $ | 11.99 | $ | 13.14 | ||||

| Offering Price Per Share (NAV/$0.9425) Includes a Maximum Sales Charge of 5.75% | $ | 12.72 | $ | 13.94 | ||||

| Class C Shares: | ||||||||

| Net Assets | $ | 15,401,276 | ||||||

| Shares Outstanding (no par value; unlimited number of shares authorized) | 1,343,329 | |||||||

| Net Asset Value, Offering Price and Redemption Price Per Share* | $ | 11.47 | ||||||

| Class I Shares: | ||||||||

| Net Assets | $ | 36,164,000 | $ | 22,055,604 | ||||

| Shares Outstanding (no par value; unlimited number of shares authorized) | 3,052,318 | 1,672,736 | ||||||

| Net Asset Value, Offering Price and Redemption Price Per Share* | $ | 11.85 | $ | 13.19 | ||||

| * | The Funds charge a 1.00% fee on shares redeemed less than 30 days after purchase or if shares held less than 30 days are redeemed for the Funds’ minimum balance requirement. |

The accompanying notes are an integral part of these financial statements.

13

| Copeland Trust |

| STATEMENTS OF OPERATIONS |

| For the Year Ended November 30, 2020 |

| Copeland SMID | ||||||||

| Copeland Dividend | Cap Dividend | |||||||

| Growth Fund | Growth Fund | |||||||

| Investment Income: | ||||||||

| Dividend Income | $ | 1,291,470 | $ | 294,195 | ||||

| Interest Income | 74,037 | 4,419 | ||||||

| Less: Foreign Taxes Withholding | (27,457 | ) | (2,334 | ) | ||||

| Total Investment Income | 1,338,050 | 296,280 | ||||||

| Expenses: | ||||||||

| Investment Advisory Fees | 869,705 | 110,259 | ||||||

| Distribution Fees - Class C | 184,964 | — | ||||||

| Distribution Fees - Class A | 60,013 | 133 | ||||||

| Trustees’ Fees | 140,466 | 26,760 | ||||||

| Administration Fees | 88,051 | 22,003 | ||||||

| Legal Fees | 84,296 | 17,223 | ||||||

| Chief Compliance Officer Fees | 149,779 | 34,729 | ||||||

| Fund Accounting Fees | 51,631 | 33,139 | ||||||

| Registration & Filing Fees | 97,020 | 32,363 | ||||||

| Transfer Agent Fees | 41,390 | 24,818 | ||||||

| Non-Rule 12B-1 Shareholder Service Fees - Class A and Class C | 39,495 | 974 | ||||||

| Shareholder Service Fees- Class I | 36,116 | 2,111 | ||||||

| Printing Expenses | 30,543 | 5,260 | ||||||

| Custody Fees | 24,017 | 37,573 | ||||||

| Insurance Expense | 19,564 | 1,798 | ||||||

| Audit Fees | 15,916 | 6,992 | ||||||

| Miscellaneous Expenses | 9,752 | 7,642 | ||||||

| Total Expenses | 1,942,718 | 363,777 | ||||||

| Less: Fees Waived/Reimbursed by Adviser | (610,939 | ) | (223,713 | ) | ||||

| Net Expenses | 1,331,779 | 140,064 | ||||||

| Net Investment Income | 6,271 | 156,216 | ||||||

| Net Realized and Unrealized Gain (Loss) on Investments: | ||||||||

| Net Realized Loss on: | ||||||||

| Securities | (1,840,706 | ) | (177,079 | ) | ||||

| Net Change in Unrealized Appreciation (Depreciation) on Securities | (1,252,707 | ) | 1,606,726 | |||||

| Foreign Currency Transactions | (51 | ) | — | |||||

| (1,252,758 | ) | 1,606,726 | ||||||

| Net Realized and Unrealized Gain (Loss) on Investments | (3,093,464 | ) | 1,429,647 | |||||

| Net Increase (Decrease) in Net Assets Resulting From Operations | $ | (3,087,193 | ) | $ | 1,585,863 | |||

The accompanying notes are an integral part of these financial statements.

14

| Copeland Dividend Growth Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year | Year | |||||||

| Ended | Ended | |||||||

| November 30, 2020 | November 30, 2019 | |||||||

| Operations: | ||||||||

| Net Investment Income | $ | 6,271 | $ | 888,564 | ||||

| Net Realized Gain (Loss) on Investments | (1,840,706 | ) | 25,079,273 | |||||

| Net Change in Unrealized Depreciation on investments and foreign currency transactions | (1,252,758 | ) | (25,884,106 | ) | ||||

| Net Increase (Decrease) in Net Assets Resulting From Operations | (3,087,193 | ) | 83,731 | |||||

| Distributions to Shareholders From: | ||||||||

| Total Distributions Paid | ||||||||

| Class A | (6,494,529 | ) | (3,753,431 | ) | ||||

| Class C | (4,425,567 | ) | (2,354,930 | ) | ||||

| Class I | (11,471,495 | ) | (6,061,800 | ) | ||||

| Total Distributions to Shareholders | (22,391,591 | ) | (12,170,161 | ) | ||||

| Beneficial Interest Transactions: | ||||||||

| Class A | ||||||||

| Proceeds from Shares Issued | 498,957 | 1,578,190 | ||||||

| Distributions Reinvested | 6,043,037 | 3,503,569 | ||||||

| Cost of Shares Redeemed | (17,118,388 | ) | (17,085,621 | ) | ||||

| Redemption Fees | 3 | 481 | ||||||

| Total Class A Shares | (10,576,391 | ) | (12,003,381 | ) | ||||

| Class C | ||||||||

| Proceeds from Shares Issued | 241,114 | 612,453 | ||||||

| Distributions Reinvested | 4,347,841 | 2,329,578 | ||||||

| Cost of Shares Redeemed | (9,389,864 | ) | (7,724,642 | ) | ||||

| Redemption Fees | 5 | 79 | ||||||

| Total Class C Shares | (4,800,904 | ) | (4,782,532 | ) | ||||

| Class I | ||||||||

| Proceeds from Shares Issued | 8,248,914 | 15,245,576 | ||||||

| Distributions Reinvested | 11,247,291 | 5,921,432 | ||||||

| Cost of Shares Redeemed | (37,065,774 | ) | (30,395,830 | ) | ||||

| Redemption Fees | 168 | 94 | ||||||

| Total Class I Shares | (17,569,401 | ) | (9,228,728 | ) | ||||

| Total Beneficial Interest Transactions | (32,946,696 | ) | (26,014,641 | ) | ||||

| Decrease in Net Assets | (58,425,480 | ) | (38,101,071 | ) | ||||

| Net Assets: | ||||||||

| Beginning of Year | 128,790,542 | 166,891,613 | ||||||

| End of Year | $ | 70,365,062 | $ | 128,790,542 | ||||

| Share Activity: | ||||||||

| Class A | ||||||||

| Shares Issued | 44,691 | 119,196 | ||||||

| Distributions Reinvested | 515,617 | 256,296 | ||||||

| Shares Redeemed | (1,579,723 | ) | (1,263,441 | ) | ||||

| Total Class A Shares | (1,019,415 | ) | (887,949 | ) | ||||

| Class C | ||||||||

| Shares Issued | 21,875 | 47,575 | ||||||

| Distributions Reinvested | 384,765 | 175,552 | ||||||

| Shares Redeemed | (903,727 | ) | (590,670 | ) | ||||

| Total Class C Shares | (497,087 | ) | (367,543 | ) | ||||

| Class I | ||||||||

| Shares Issued | 756,637 | 1,158,415 | ||||||

| Distributions Reinvested | 972,108 | 437,975 | ||||||

| Shares Redeemed | (3,395,792 | ) | (2,281,806 | ) | ||||

| Total Class I Shares | (1,667,047 | ) | (685,416 | ) | ||||

The accompanying notes are an integral part of these financial statements.

15

| Copeland SMID Cap Dividend Growth Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year | For the Year/Period | |||||||

| Ended | Ended | |||||||

| November 30, 2020 | November 30, 2019 * | |||||||

| Operations: | ||||||||

| Net Investment Income | $ | 156,216 | $ | 47,797 | ||||

| Net Realized Gain (Loss) on Investments and Foreign Currency Transactions | (177,079 | ) | 130,998 | |||||

| Net Change in Unrealized Appreciation on Investments | 1,606,726 | 663,357 | ||||||

| Net Increase in Net Assets Resulting From Operations | 1,585,863 | 842,152 | ||||||

| Distributions to Shareholders From: | ||||||||

| Total Distributions Paid | ||||||||

| Class A | (646 | ) | — | |||||

| Class I | (187,956 | ) | (39,614 | ) | ||||

| Total Distributions to Shareholders | (188,602 | ) | (39,614 | ) | ||||

| Beneficial Interest Transactions: | ||||||||

| Class A * | ||||||||

| Proceeds from Shares Issued | 87,691 | 31,929 | ||||||

| Distributions Reinvested | 646 | — | ||||||

| Cost of Shares Redeemed | (19,121 | ) | — | |||||

| Redemption Fees | 3 | — | ||||||

| Total Class A Shares | 69,219 | 31,929.00 | ||||||

| Class I | ||||||||

| Proceeds from Shares Issued | 12,007,820 | 10,235,537 | ||||||

| Distributions Reinvested | 181,961 | 35,745 | ||||||

| Cost of Shares Redeemed | (3,430,600 | ) | (203,729 | ) | ||||

| Redemption Fees | 658 | 60 | ||||||

| Total Class I Shares | 8,759,839 | 10,067,613 | ||||||

| Total Beneficial Interest Transactions | 8,829,058 | 10,099,542 | ||||||

| Increase in Net Assets | 10,226,319 | 10,902,080 | ||||||

| Net Assets: | ||||||||

| Beginning of Year | 11,937,532 | 1,035,452 | ||||||

| End of Year | $ | 22,163,851 | $ | 11,937,532 | ||||

| Share Activity: | ||||||||

| Class A | ||||||||

| Shares Issued | 6,974 | 2,684 | ||||||

| Distributions Reinvested | 52 | — | ||||||

| Shares Redeemed | (1,471 | ) | — | |||||

| Total Class A Shares | 5,555 | 2,684 | ||||||

| Class I | ||||||||

| Shares Issued | 1,023,263 | 856,574 | ||||||

| Distributions Reinvested | 14,557 | 3,328 | ||||||

| Shares Redeemed | (298,189 | ) | (16,542 | ) | ||||

| Total Class I Shares | 739,631 | 843,360 | ||||||

| * | Class A commenced operations on February 11, 2019 |

The accompanying notes are an integral part of these financial statements.

16

| Copeland Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout each year presented. |

| Class A | ||||||||||||||||||||

| Year | Year | Year | Year | Year | ||||||||||||||||

| Ended | Ended | Ended | Ended | Ended | ||||||||||||||||

| November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017 | November 30, 2016 | ||||||||||||||||

| Net Asset Value, Beginning of Year | $ | 14.25 | $ | 15.18 | $ | 14.38 | $ | 12.27 | $ | 13.38 | ||||||||||

| Increase From Operations: | ||||||||||||||||||||

| Net investment income (a) | 0.01 | 0.10 | 0.04 | 0.06 | — | |||||||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.48 | ) | 0.05 | 1.38 | 2.51 | 0.07 | ||||||||||||||

| Other capital changes | 0.73 | (d) | — | — | — | — | ||||||||||||||

| Total from operations | 0.26 | 0.15 | 1.42 | 2.57 | 0.07 | |||||||||||||||

| Distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | (0.09 | ) | (0.01 | ) | (0.03 | ) | (0.09 | ) | (0.05 | ) | ||||||||||

| Net realized gains | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | (1.13 | ) | ||||||||||

| Total distributions | (2.52 | ) | (1.08 | ) | (0.62 | ) | (0.46 | ) | (1.18 | ) | ||||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| Net Asset Value, End of Year | $ | 11.99 | $ | 14.25 | $ | 15.18 | $ | 14.38 | $ | 12.27 | ||||||||||

| Total Return (c) | 2.24 | % | 1.32 | % | 10.33 | % | 21.63 | % | 0.49 | % | ||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||

| Net assets, end of year (in 000’s) | $ | 18,800 | $ | 36,870 | $ | 52,779 | $ | 64,666 | $ | 82,165 | ||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||

| before reimbursement | 2.13 | % | 1.74 | % | 1.71 | % | 1.82 | % | 1.62 | % | ||||||||||

| net of reimbursement | 1.44 | % | 1.45 | % | 1.45 | % | 1.45 | % | 1.45 | % | ||||||||||

| Ratio of net investment income to average net assets | 0.10 | % | 0.70 | % | 0.28 | % | 0.47 | % | 0.01 | % | ||||||||||

| Portfolio turnover rate | 170 | % | 244 | % | 30 | % | 27 | % | 201 | % | ||||||||||

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. Sales loads are not reflected in total return. |

| (d) | As required by SEC standard per share data calculation methodology, this represents a balancing figure derived from the other amounts in the financial highlights tables that captures all other changes affecting net asset value per share. |

The accompanying notes are an integral part of these financial statements.

17

| Copeland Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout each year presented. |

| Class C | ||||||||||||||||||||

| Year | Year | Year | Year | Year | ||||||||||||||||

| Ended | Ended | Ended | Ended | Ended | ||||||||||||||||

| November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017 | November 30, 2016 | ||||||||||||||||

| Net Asset Value, Beginning of Year | $ | 13.73 | $ | 14.76 | $ | 14.06 | $ | 12.01 | $ | 13.17 | ||||||||||

| Increase From Operations: | ||||||||||||||||||||

| Net investment loss (a) | (0.07 | ) | (0.01 | ) | (0.07 | ) | (0.04 | ) | (0.09 | ) | ||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.30 | ) | 0.05 | 1.36 | 2.46 | 0.06 | ||||||||||||||

| Other capital changes | 0.54 | (d) | — | — | — | — | ||||||||||||||

| Total from operations | 0.17 | 0.04 | 1.29 | 2.42 | (0.03 | ) | ||||||||||||||

| Distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | — | — | — | — | — | |||||||||||||||

| Net realized gains | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | (1.13 | ) | ||||||||||

| Total distributions | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | (1.13 | ) | ||||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| Net Asset Value, End of Year | $ | 11.47 | $ | 13.73 | $ | 14.76 | $ | 14.06 | $ | 12.01 | ||||||||||

| Total Return (c) | 1.51 | % | 0.54 | % | 9.55 | % | 20.68 | % | (0.30 | )% | ||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||

| Net assets, end of year (in 000’s) | $ | 15,401 | $ | 25,271 | $ | 32,597 | $ | 35,487 | $ | 43,859 | ||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||

| before reimbursement | 2.88 | % | 2.49 | % | 2.45 | % | 2.57 | % | 2.38 | % | ||||||||||

| net of reimbursement | 2.19 | % | 2.20 | % | 2.20 | % | 2.20 | % | 2.20 | % | ||||||||||

| Ratio of net investment loss to average net assets | (0.67 | )% | (0.05 | )% | (0.46 | )% | (0.28 | )% | (0.74 | )% | ||||||||||

| Portfolio turnover rate | 170 | % | 244 | % | 30 | % | 27 | % | 201 | % | ||||||||||

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (d) | As required by SEC standard per share data calculation methodology, this represents a balancing figure derived from the other amounts in the financial highlights tables that captures all other changes affecting net asset value per share. |

The accompanying notes are an integral part of these financial statements.

18

| Copeland Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout each year presented. |

| Class I | ||||||||||||||||||||

| Year | Year | Year | Year | Year | ||||||||||||||||

| Ended | Ended | Ended | Ended | Ended | ||||||||||||||||

| November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017 | November 30, 2016 | ||||||||||||||||

| Net Asset Value, Beginning of Year | $ | 14.12 | $ | 15.08 | $ | 14.30 | $ | 12.24 | $ | 13.38 | ||||||||||

| Increase From Operations: | ||||||||||||||||||||

| Net investment income (a) | 0.03 | 0.11 | 0.07 | 0.08 | 0.01 | |||||||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.38 | ) | 0.06 | 1.37 | 2.49 | 0.08 | ||||||||||||||

| Other capital changes | 0.63 | (d) | — | — | — | — | ||||||||||||||

| Total from operations | 0.28 | 0.17 | 1.44 | 2.57 | 0.09 | |||||||||||||||

| Distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | (0.12 | ) | (0.06 | ) | (0.07 | ) | (0.14 | ) | (0.10 | ) | ||||||||||

| Net realized gains | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | (1.13 | ) | ||||||||||

| Total distributions | (2.55 | ) | (1.13 | ) | (0.66 | ) | (0.51 | ) | (1.23 | ) | ||||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| Net Asset Value, End of Year | $ | 11.85 | $ | 14.12 | $ | 15.08 | $ | 14.30 | $ | 12.24 | ||||||||||

| Total Return (c) | 2.40 | % | 1.43 | % | 10.56 | % | 21.72 | % | 0.67 | % | ||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||

| Net assets, end of year (in 000’s) | $ | 36,164 | $ | 66,649 | $ | 81,516 | $ | 75,097 | $ | 81,750 | ||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||

| before reimbursement | 1.98 | % | 1.58 | % | 1.53 | % | 1.57 | % | 1.37 | % | ||||||||||

| net of reimbursement | 1.29 | % | 1.30 | % | 1.30 | % | 1.30 | % | 1.30 | % | ||||||||||

| Ratio of net investment income to average net assets | 0.23 | % | 0.85 | % | 0.45 | % | 0.62 | % | 0.11 | % | ||||||||||

| Portfolio turnover rate | 170 | % | 244 | % | 30 | % | 27 | % | 201 | % | ||||||||||

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (d) | As required by SEC standard per share data calculation methodology, this represents a balancing figure derived from the other amounts in the financial highlights tables that captures all other changes affecting net asset value per share. |

The accompanying notes are an integral part of these financial statements.

19

| Copeland SMID Cap Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout the year/period presented. |

| Class A | ||||||||

| Year | �� | Period | ||||||

| Ended | Ended | |||||||

| November 30, 2020 | November 30, 2019 * | |||||||

| Net Asset Value, Beginning of Year/Period | $ | 12.73 | $ | 11.10 | ||||

| Increase From Operations: | ||||||||

| Net investment income (a) | 0.10 | 0.10 | ||||||

| Net gain from securities (both realized and unrealized) | 0.50 | 1.53 | ||||||

| Total from operations | 0.60 | 1.63 | ||||||

| Distributions to shareholders from: | ||||||||

| Net investment income | (0.05 | ) | — | |||||

| Net realized gains | (0.14 | ) | — | |||||

| Total distributions | (0.19 | ) | — | |||||

| Redemption fees (b) | 0.00 | 0.00 | ||||||

| Net Asset Value, End of Year/Period | $ | 13.14 | $ | 12.73 | ||||

| Total Return (c) | 4.73 | % | 14.68 | % (e) | ||||

| Ratios/Supplemental Data | ||||||||

| Net assets, end of year/period (in 000’s) | $ | 108 | $ | 34 | ||||

| Ratio of expenses to average net assets: | ||||||||

| before reimbursement | 2.72 | % | 3.04 | % (d) | ||||

| net of reimbursement | 1.20 | % | 1.20 | % (d) | ||||

| Ratio of net investment income to average net assets | 0.87 | % | 0.82 | % (d) | ||||

| Portfolio turnover rate | 49 | % | 22 | % (e) | ||||

| * | Class A commenced operations on February 11, 2019. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period/year. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (d) | Annualized. |

| (e) | Not annualized. |

The accompanying notes are an integral part of these financial statements.

20

| Copeland SMID Cap Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

| Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout the year/period presented. |

| Class I | ||||||||||||||||

| Year | Year | Year | Period | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017* | |||||||||||||

| Net Asset Value, Beginning of Year/Period | $ | 12.76 | $ | 11.54 | $ | 11.10 | $ | 10.00 | ||||||||

| Increase From Operations: | ||||||||||||||||

| Net investment income (a) | 0.13 | 0.13 | 0.10 | 0.06 | ||||||||||||

| Net gain from securities (both realized and unrealized) | 0.50 | 1.53 | 0.42 | 1.04 | ||||||||||||

| Total from operations | 0.63 | 1.66 | 0.52 | 1.10 | ||||||||||||

| Distributions to shareholders from: | ||||||||||||||||

| Net investment income | (0.06 | ) | (0.08 | ) | (0.07 | ) | — | |||||||||

| Net realized gains | (0.14 | ) | (0.36 | ) | (0.01 | ) | — | |||||||||

| Total distributions | (0.20 | ) | (0.44 | ) | (0.08 | ) | — | |||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

| Net Asset Value, End of Year/Period | $ | 13.19 | $ | 12.76 | $ | 11.54 | $ | 11.10 | ||||||||

| Total Return (c) | 4.98 | % | 15.12 | % | 4.76 | % | 11.00 | % (e) | ||||||||

| Ratios/Supplemental Data | ||||||||||||||||

| Net assets, end of year/period (in 000’s) | $ | 22,056 | $ | 11,903 | $ | 1,035 | $ | 616 | ||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||

| before reimbursement | 2.47 | % | 3.18 | % | 10.14 | % | 12.96 | % (d) | ||||||||

| net of reimbursement | 0.95 | % | 0.95 | % | 0.95 | % | 0.95 | % (d) | ||||||||

| Ratio of net investment income to average net assets | 1.06 | % | 1.09 | % | 0.90 | % | 0.83 | % (d) | ||||||||

| Portfolio turnover rate | 49 | % | 22 | % | 26 | % | 21 | % (e) | ||||||||

| * | Class I commenced operations on February 27, 2017. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period/year. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (d) | Annualized. |

| (e) | Not annualized. |

The accompanying notes are an integral part of these financial statements.

21

| Copeland Trust |

| NOTES TO FINANCIAL STATEMENTS |

| November 30, 2020 |

| 1. | ORGANIZATION |

Copeland Dividend Growth Fund (the “Dividend Growth Fund”), formerly, the Copeland Risk Managed Dividend Growth Fund, and Copeland SMID Cap Dividend Growth Fund (the “SMID Fund”) are diversified series of Copeland Trust (the “Trust”). The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”) as an open-end management investment company. The Trust was organized as a statutory trust on September 10, 2010, under the laws of the State of Delaware.

The Dividend Growth Fund currently offers Class A, Class C and Class I shares. The SMID Fund currently offers Class A and Class I shares. The Dividend Growth Fund’s Class A shares commenced operations on December 28, 2010, Class C shares commenced operations on January 5, 2012 and Class I shares commenced operations on March 1, 2013. The SMID Fund’s Class I shares commenced operations on February 27, 2017 and Class A shares commenced operations on February 11, 2019. Class A shares are offered at net asset value plus a maximum sales charge of 5.75%. Purchases of $1,000,000 or more may be subject to a maximum contingent deferred sales charge of 1.00% on shares redeemed within 18 months. Class C and Class I shares are offered at net asset value. Each class represents an interest in the same assets of the Funds and classes are identical except for differences in their sales charge structures and ongoing service and distribution charges. All classes of shares have equal voting privileges except that each class has exclusive voting rights with respect to its service and/or distribution plans. The Funds’ income, expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Funds in preparation of their financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Funds are investment companies and accordingly follow the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update ASU 2013-08.

SECURITY VALUATION

The Funds’ securities are valued at the last sale price on the exchange in which such securities are primarily traded, as of the close of business on the day the securities are being valued. In the absence of a sale on the primary exchange, such securities shall be valued at the last mean on the primary exchange. NASDAQ traded securities are valued using the NASDAQ Official Closing Price (“NOCP”). Investments valued in currencies other than the U.S. dollar are converted to U.S. dollars using exchange rates obtained from pricing services. Short-term investments that mature in 60 days or less may be valued at amortized cost.

If market quotations are not readily available, securities will be valued at their fair market value as determined in good faith by the adviser in accordance with procedures approved by the Trust’s Board of Trustees (the “Board”) and evaluated by the Board as to the reliability of the fair value method used. The procedures consider, among others, the following factors to determine a security’s fair value: the nature and pricing history, if any, of the security; whether any dealer quotations for the security are available; and possible valuation methodologies that could be used to determine the fair value of the security.

The Funds utilize various methods to measure the fair value of their investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods.

22

| Copeland Trust |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| November 30, 2020 |

The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Funds have the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of November 30, 2020 for the Funds’ assets measured at fair value:

| Copeland Dividend Growth Fund | ||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common Stock* | $ | 69,500,763 | $ | — | $ | — | $ | 69,500,763 | ||||||||

| Total | $ | 69,500,763 | $ | — | $ | — | $ | 69,500,763 | ||||||||

| Copeland SMID Cap Dividend Growth Fund | ||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common Stock* | $ | 21,395,614 | $ | — | $ | — | $ | 21,395,614 | ||||||||

| Total | $ | 21,395,614 | $ | — | $ | — | $ | 21,395,614 | ||||||||

The Funds did not hold any Level 3 securities during the period.

| * | Please refer to the Portfolio of Investments for Industry Classification. |

SECURITY TRANSACTIONS AND INVESTMENT INCOME

Investment security transactions are accounted for on a trade date basis. Cost is determined and gains and losses are based upon the specific identification method for both financial statement and federal income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on the accrual basis. Purchase discounts and premiums on securities are accreted and amortized over the life of the respective securities.

FEDERAL INCOME TAXES

The Funds intend to continue to comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and will distribute all of their taxable income, if any, to shareholders. Accordingly, no provision for Federal income taxes is required in the financial statements.

23

| Copeland Trust |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| November 30, 2020 |

The Funds recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Funds’ tax positions, and has concluded that there are no significant uncertain tax positions taken or expected to be taken that would require recognition in the financial statements related to the open tax years (2017-2019) or expected to be taken in the Funds’ 2020 tax returns. The Funds identify their major tax jurisdictions as U.S. Federal and foreign jurisdictions where the Funds may make investments; however, the Funds are not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

DIVIDEND-PAYING STOCK RISK

The Fund’s emphasis on dividend-paying stocks could cause the Fund to underperform similar funds that invest without consideration of a company’s track record of paying dividends. Stocks of companies with a history of paying dividends may not participate in a broad market advance to the same degree as most other stocks, and a sharp rise in interest rates or economic downturn could cause a company to unexpectedly reduce or eliminate its dividend. If the amount a company pays out as a dividend exceeds its earnings and profits, the excess will be treated as a return of capital and the Fund’s tax basis in the stock will be reduced. A reduction in the Fund’s tax basis in such stock will increase the amount of gain (or decrease the amount of loss) recognized by the Fund on a subsequent sale of the stock.

MARKET RISK

Overall securities market risks may affect the value of individual securities in which the Fund invests. Factors such as foreign and domestic economic growth and market conditions, interest rate levels, and political events affect the securities markets.

REIT RISK

An equity REIT’s performance depends on the types and locations of the rental properties it owns and on how well it manages those properties. Real estate values rise and fall in response to a variety of factors, including local, regional and national economic conditions, changes in interest rates and property taxes.

SMALL AND MEDIUM CAPITALIZATION RISK

The value of a small or medium capitalization company securities may be subject to more abrupt or erratic market movements than those of larger, more established companies or the market averages in general.

FOREIGN CURRENCY

The accounting records of the Funds are maintained in U.S. dollars. Investment securities and other assets and liabilities denominated in a foreign currency, and income receipts and expense payments, if any, are translated into U.S. dollars using the prevailing exchange rate at the London market close. Purchases and sales of securities are translated into U.S. dollars at the contractual currency rates established at the approximate time of the trade. Net realized gains and losses on foreign currency transactions represent net gains and losses from currency realized between the trade and settlement dates on securities transactions and the difference between income accrued versus income received. The effects of changes in foreign currency exchange rates on investments in securities are included with the net realized and unrealized gain or loss on investment securities.

FORWARD CURRENCY CONTRACTS

If foreign securities are purchased, the Funds generally enter into forward currency exchange contracts in order to eliminate ongoing foreign currency exchange rate risks. If foreign securities are sold, the foreign currency proceeds are typically repatriated into US dollars. Any realized gains and losses between trade date and settlement date from contract transactions are included as a component of net realized gains (losses) from foreign currency transactions in the Statements of Operations. The Funds did not hold any forward currency contracts as of November 30, 2020.

CONCENTRATION OF RISK

Investing in securities of foreign issuers and currency transactions may involve certain considerations and risks not typically associated with investments in the United States. These risks include revaluation of currencies, adverse fluctuations in foreign currency values and possible adverse political, social and economic developments, including those particular to a specific industry, country or region. These conditions could cause the securities and their markets to be less liquid and prices more volatile than those of comparable U.S. companies and U.S. government securities.

24

| Copeland Trust |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| November 30, 2020 |

DISTRIBUTIONS TO SHAREHOLDERS

Distributions from investment income, if any, are declared and paid annually and are recorded on the ex-dividend date. The Funds will declare and pay net realized capital gains, if any, annually. The character of income and gains to be distributed is determined in accordance with income tax regulations, which may differ from GAAP. These “book/tax” differences are considered either temporary (i.e., deferred losses, capital loss carry forwards) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require classification.

EXPENSES

Expenses of the Trust that are directly identifiable to a specific Fund are charged to that Fund. Expenses, which are not readily identifiable to a specific Fund, are allocated in such a manner as deemed equitable, taking into consideration the nature and type of expense and the relative sizes of the Funds in the Trust.

INDEMNIFICATION