Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR/A

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22497

HUNTINGTON STRATEGY SHARES

(Exact name of registrant as specified in charter)

2960 NORTH MERIDIAN STREET, SUITE 300, INDIANAPOLIS, IN 46208

(Address of principal executive offices) (Zip code)

CITI FUND SERVICES OHIO, INC., 3435 STELZER ROAD, COLUMBUS, OH 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: 855-477-3837

Date of fiscal year end: April 30

Date of reporting period: April 30, 2014

Table of Contents

Item 1. Reports to Stockholders.

The Form N-CSR for Huntington Strategy Shares for the year ended April 30, 2014 is being amended with this filing to reflect the addition of a disclosure in the annual report to shareholders. The report now includes information related to the Board of Trustees’ consideration of the investment advisory agreement with Huntington Asset Advisors, Inc.

Table of Contents

Annual Shareholder Report

APRIL 30, 2014

Table of Contents

| Page | ||||

| 1 | ||||

| 5 | ||||

| 6 | ||||

| 11 | ||||

| 13 | ||||

| 14 | ||||

| 15 | ||||

| 16 | ||||

| 18 | ||||

| 23 | ||||

| 24 | ||||

| 29 | ||||

Table of Contents

Message from the Chief Investment Officer

Dear Shareholder:

It was without question that weather played a significant role in the performance of the U.S. economy during the first quarter of 2014. With much of the nation under winter advisories and the agricultural production areas of central California under extreme drought conditions, there was a detrimental effect on certain industries and economic sectors. Housing starts were certainly impacted as they started the year at a 999k pace, slipped to 880k in January, but recovered to 946k by March. Likewise, capacity utilization slipped from 79.2% in December to 78.8% in February, which was consistent with the Institute of Supply Management manufacturing numbers that dropped from a year-end 57 level to 53.7 in March.

The employment picture wasn’t much better with unemployment in December standing at 6.7% and remaining so through the first quarter. The average weekly manufacturing hours worked slipped slightly during the quarter as well. Consequently, most economists predicted a much slower GDP growth than the 2.6% of the final quarter of 2013. In fact, the final GDP for the first quarter of 2014 was revised downward to a surprising -2.9%. With liquidity still in the system and some degree of ‘pent up demand’ from the weather impact, there is a higher level of expectations for economic activity in the second quarter to make up for the weakness of the first quarter of 2014.

Irrespective of the economy, however, the equity markets continued their expansionary advance of 2013, albeit at a much more measured pace. The market is experiencing an aggressive merger and acquisition mantra as corporations seek to consolidate to provide greater economies of scale and develop new growth outlets in the slow growth economy. Another by-product of this consolidation effort is the concept of ‘inversion’ where domestic corporations are moving offshore to reduce corporate tax rates. As part of our dynamic investment process, we continually monitor and evaluate these macro-economic trends and their impact on financial sectors and stock selection within the ETFs.

Within this challenging environment, the Huntington Strategy Shares ETFs continued to provide positive returns for our shareholders. For the year-to-date period ended April 30, 2014, the Huntington US Equity Rotation Strategy ETF (HUSE) rose 0.40% based on net asset value and the Huntington EcoLogical

Strategy ETF (HECO) gained 1.19% based on net asset value. For the one-year period ended April 30, 2014, the returns expanded 20.19% and 19.31% based on net asset value, respectively. Since inception, both HUSE and HECO have contributed more than a 20% return on an annualized basis to shareholders, based on net asset value. As a result of their strong performance, Huntington Strategy Shares ETFs were highlighted in two articles in nationally recognized publications during the first quarter of 2014.

As the number of actively managed ETFs continues to grow and more investors are comfortable including them in their investment portfolios, we are proud to offer these two innovative strategies that have the potential to outperform the markets. For more insights from our ETF Manager, Martina Cheung, please take a moment to read the Management’s Discussion of Fund Performance. As always, we appreciate your investment in HECO and HUSE and will continue to seek to control risk, while providing opportunities to add value to our shareholders with the highest level of attention to the disciplines we have employed for several decades. We appreciate your confidence and your continued support.

Sincerely,

B. Randolph Bateman

President & Chief Investment Officer

Huntington Asset Advisors, Inc.

This material represents the manager’s assessment of the Funds and market environment at a specific time and should not be relied upon by the reader as research, tax or investment advice.

Message from the Chief Investment Officer

Table of Contents

| Huntington US Equity Rotation Strategy ETF | April 30, 2014 |

Management’s Discussion of Fund Performance

ETF Manager: Martina Cheung, CFA and CMT

Senior Vice President and Fund Manager

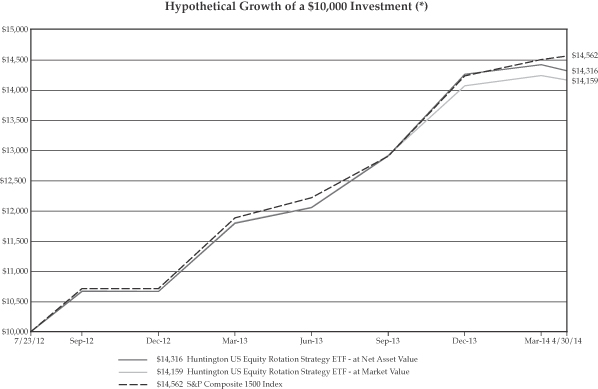

For the fiscal year ended April 30, 2014, the US Equity Rotation Strategy ETF (HUSE) generated a positive return of 20.19% at net asset value. This compared to a return of 20.44% for the Standard & Poor’s Composite 1500 Index (S&P 1500)1, the Fund’s benchmark for the same period.

The strategy employed by HUSE is to benchmark 70% of the portfolio to the S&P 1500 Index, and invest the remaining 30% in the stocks of the three sectors of the S&P 1500 Index that we believe have the best chance of outperforming the S&P 1500 index. HUSE seeks to take advantage of the significant volatility that exists between the different sectors of the index to potentially produce alpha2.

Over the past twelve-month period ended April 30, 2014, the stock market, as measured by the Standard & Poor’s 500 Index, exceeded its record high achieved in 2000. This was accomplished with a great deal of volatility among sectors. The strategy of this actively managed ETF is to benefit from this volatility, which also occurred in the S&P 1500. The three sectors we chose to over-weight were Industrials, Technology and Healthcare. Industrials and Technology were over-weighted in an attempt to take advantage of the volatility, while the more defensive Healthcare sector was chosen to potentially protect the portfolio from downside risk.

This strategy worked well through mid-March of 2014. During that time frame, selective Industrials groups, as well as the Technology and Healthcare holdings, helped HUSE to outperform the S&P 1500 index. Unfortunately, style rotation since mid-March of 2014 worked against HUSE as investors took profit from selective groups that had been the best performers in 2013, including Internet software and Biotechnology. The ensuing sharp decline in these selective groups negatively impacted performance and resulted in HUSE underperforming its benchmark for the year ended April 30, 2014. Although the underperformance was unfortunate, we believe the strategy employed by HUSE is sound and has the potential to result in outperformance over an extended period of time.

| (1) | The S&P Composite 1500 Index is a broad equity index based on the S&P 500, S&P MidCap 400, and S&P SmallCap 600 indices. Thus, the S&P Composite 1500 Index includes the top large cap, mid cap and small cap stocks, representing about 85% of the entire U.S. equity market. An investor cannot invest directly in an index. |

| (2) | Alpha is a measure of performance on a risk-adjusted basis. Alpha takes the volatility (price risk) of a mutual fund and compares its risk adjusted performance to a benchmark index. The excess return of the fund relative to the return of the benchmark index is a fund’s alpha. |

ETF Risk. The Fund is an actively-managed ETF and the Fund’s NAV will fluctuate based on changes in the prices of the securities it owns. The market price of Fund shares will fluctuate based on changes in the Fund’s NAV as well as changes in the supply and demand of its shares in the secondary market. It is also possible that an active secondary market for Fund shares may not develop and market trading in the Fund shares may be halted under certain circumstances.

You should consider an investment in the Fund as a long-term investment. The Fund’s returns will fluctuate over long and short periods.

This material represents the manager’s assessment of the Fund and market environment as of April 30, 2014 and should not be relied upon by the reader as research, tax or investment advice, is subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to exchange traded fund investments. In addition, the Fund’s returns do not reflect sales charges that an investor in the Fund may pay. If these sales charges were reflected, performance would have been lower.

Annual Shareholder Report

1

Table of Contents

Huntington US Equity Rotation Strategy ETF (Continued)

INVESTMENT OBJECTIVE

The Huntington US Equity Rotation Strategy ETF seeks to achieve capital appreciation.

FUND PERFORMANCE (AS OF 4/30/14)

| Average Annual Total Returns | Expense Ratios (a) | |||||||||||||||

| One Year | Inception (b) | Gross | Net | |||||||||||||

US Equity Rotation Strategy ETF (HUSE) — Total Return (at Net Asset Value) (c) | 20.19 | % | 22.47 | % | 4.42 | % | 0.95 | % | ||||||||

US Equity Rotation Strategy ETF (HUSE) — Total Return (at Market Value) (d) | 18.79 | % | 21.71 | % | N/A | N/A | ||||||||||

S&P 1500 Index (e) | 20.44 | % | 23.67 | % | N/A | N/A | ||||||||||

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://www.huntingtonstrategyshares.com

| * | The chart represents historical performance of a hypothetical investment of $10,000 in the Huntington US Equity Rotation Strategy ETF and represents the reinvestment of dividends and capital gains in the Fund. |

| (a) | The gross expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated August 28, 2013. However, the Advisor has agreed to contractual waivers in effect through August 31, 2014 and has agreed to limit total annual fund operating expenses to the net expense ratios shown. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2014 can be found in the financial highlights. |

| (b) | Commencement of operations July 23, 2012 |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from any primary listing market (e.g., NYSE and NASDAQ) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. |

| (e) | The S&P Composite 1500 Index is a broad equity index based on the S&P 500, S&P MidCap 400, and S&P SmallCap 600 indices. Thus, the S&P Composite 1500 Index includes the top large cap, mid cap and small cap stocks, representing about 85% of the entire U.S. equity market. An investor cannot invest directly in an index. |

Annual Shareholder Report

2

Table of Contents

| Huntington EcoLogical Strategy ETF | April 30, 2014 |

Management’s Discussion of Fund Performance

ETF Manager: Martina Cheung, CFA and CMT

Senior Vice President and Fund Manager

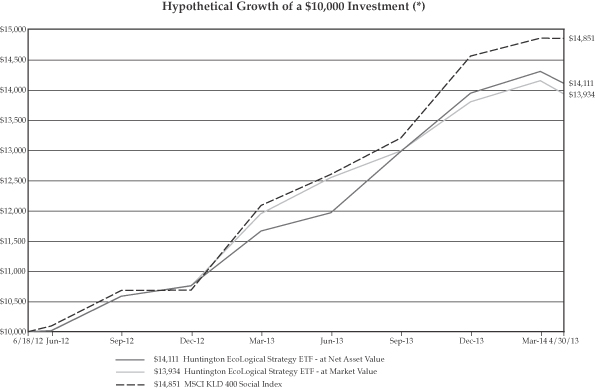

For the fiscal year ended April 30, 2014, the Huntington EcoLogical Strategy ETF (HECO) generated a positive return of 19.31% at net asset value. This compared to a return of 20.36% for the MSCI KLD 400 Social Index1, the Fund’s benchmark for the same period.

Over the past twelve-month period, the stock market, as measured by the Standard & Poor’s 500 Index, exceeded its record high achieved in 2000. Performance benefitted from the strong overall market. Stocks that contributed most in the year were BorgWarner Inc. (BWA), Hain Celestial Group, Inc. (HAIN), and MasTec, Inc. (MTZ). BorgWarner engages in producing engine and transmission parts that help cars to be more environmentally friendly while improving car performance. Hain Celestial continues to innovate in the market for natural and organic foods. MasTec is well positioned for a build-out in smart infrastructure. MasTec’s engineers build and maintain gas pipelines, electricity grid transmission lines, and telecom networks.

Performance was negatively impacted by names such as Chart Industries, Inc. (GTLS) and Questar Corporation (STR). Chart Industries, Inc. was sold due to the delay of certain projects and weakness in some areas of the market, which may put pressure on the company’s earnings. Questar was also sold, as the company’s upside potential may be limited by the potential slowdown in operating growth of one of its divisions.

Sustainability and environmental stewardship continue to grow in importance across the globe. We feel that the companies in the portfolio are well positioned with regard to these growing themes. The portfolio maintains a high quality growth bias. We tend to invest in companies that are better stewards of the environment and better stewards of capital. We believe that these policies will be rewarded over time, and may lead to higher profits and higher market share. This belief guides our investment process.

| (1) | The MSCI KLD 400 Social Index is based on the MSCI USA Investable Market Index (IMI), its parent index, which includes large-, mid- and small-cap constituents in the U.S. The index includes companies in the parent index with high Environmental, Social and Governance (ESG) ratings, while excluding companies involved in alcohol, tobacco, gambling, firearms, nuclear power and military weapons production. An investor cannot invest directly in an index. |

Ecological Investment Risk. The Fund’s ecological investment criteria limit the types of investments the Fund may make. This could cause the Fund to underperform other funds that do not have an ecological focus.

ETF Risk. The Fund is an actively-managed ETF and the Fund’s NAV will fluctuate based on changes in the prices of the securities it owns. The market price of Fund shares will fluctuate based on changes in the Fund’s NAV as well as changes in the supply and demand of its shares in the secondary market. It is also possible that an active secondary market for Fund shares may not develop and market trading in the Fund shares may be halted under certain circumstances.

You should consider an investment in the Fund as a long-term investment. The Fund’s returns will fluctuate over long and short periods.

This material represents the manager’s assessment of the Fund and market environment as of April 30, 2014 and should not be relied upon by the reader as research, tax or investment advice, is subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent. Information about the Fund’s holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to exchange traded fund investments. In addition, the Fund’s returns do not reflect sales charges that an investor in the Fund may pay. If these sales charges were reflected, performance would have been lower.

Annual Shareholder Report

3

Table of Contents

Huntington EcoLogical Strategy ETF (Continued)

INVESTMENT OBJECTIVE

The Huntington EcoLogical Strategy ETF seeks to achieve capital appreciation.

FUND PERFORMANCE (AS OF 4/30/14)

| Average Annual Total Returns | Expense Ratios (a) | |||||||||||||||

| One Year | Inception (b) | Gross | Net | |||||||||||||

EcoLogical Strategy ETF (HECO) — Total Return (at Net Asset Value) (c) | 19.31 | % | 20.27 | % | 4.21 | % | 0.95 | % | ||||||||

EcoLogical Strategy ETF (HECO) — Total Return (at Market Value) (d) | 17.61 | % | 19.46 | % | N/A | N/A | ||||||||||

MSCI KLD 400 Social Index (e) | 20.36 | % | 23.63 | % | N/A | N/A | ||||||||||

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://www.huntingtonstrategyshares.com

| * | The chart represents historical performance of a hypothetical investment of $10,000 in the Huntington EcoLogical Strategy ETF and represents the reinvestment of dividends and capital gains in the Fund. |

| (a) | The gross expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated August 28, 2013. However, the Advisor has agreed to contractual waivers in effect through August 31, 2014 and has agreed to limit total annual fund operating expenses to the net expense ratios shown. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2014 can be found in the financial highlights. |

| (b) | Commencement of operations June 18, 2012 |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from any primary listing market (e.g., NYSE and NASDAQ) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. |

| (e) | The MSCI KLD 400 Social Index is based on the MSCI USA Investable Market Index (IMI), its parent index, which includes large-, mid- and small-cap constituents in the U.S. The index includes companies in the parent index with high Environmental, Social and Governance (ESG) ratings, while excluding companies involved in alcohol, tobacco, gambling, firearms, nuclear power and military weapons production. An investor cannot invest directly in an index. |

Annual Shareholder Report

4

Table of Contents

| Expense Examples (Unaudited) | April 30, 2014 |

As a Fund shareholder, you may incur two types of costs: (1) transaction costs, including commissions on trading, as applicable; and (2) ongoing costs, including advisory fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The expense examples below are based on an investment of $1,000 invested at November 1, 2013 and held through the period ended April 30, 2014.

The Actual Expense figures in the table below provide information about actual account values and actual expenses. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Actual Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

The Hypothetical Expense figures in the table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the examples are useful in comparing ongoing costs only and will not help you determine the relative total cost of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Fund | Beginning 11/1/13 | Actual Ending Account Value 4/30/14 | Hypothetical 4/30/14 | Actual Expenses Paid During the Period (1)(2) | Total Return | Hypothetical Expenses Paid During the Period (2)(3) | Annualized Expense Ratio During Period | |||||||||||||||||||

Huntington US Equity Rotation Strategy ETF | $1,000.00 | $ | 1,065.30 | $ | 1,020.08 | $ | 4.86 | 6.53 | % | $ | 4.76 | 0.95 | % | |||||||||||||

Huntington EcoLogical Strategy ETF | 1,000.00 | 1,045.00 | 1,020.08 | 4.82 | 4.50 | % | 4.76 | 0.95 | % | |||||||||||||||||

| (1) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period multiplied by 181/365 (to reflect the one half year period). |

| (2) | Expenses are equal to the average hypothetical account value over the period multiplied by the Fund’s annualized expense ratio, multiplied by the number of days in the most recent fiscal half-year divided by the number of days in the fiscal year (to reflect the one-half year period). |

| (3) | Represents the hypothetical 5% annual return before taxes. |

Annual Shareholder Report

5

Table of Contents

| Huntington US Equity Rotation Strategy ETF | April 30, 2014 |

| Portfolio of Investments Summary Table | (unaudited) |

| Percentage of Market Value | ||||

Consumer Discretionary | 8.6% | |||

Consumer Staples | 6.7% | |||

Energy | 6.8% | |||

Financials | 11.7% | |||

Health Care | 22.1% | |||

Industrials | 16.4% | |||

Information Technology | 21.2% | |||

Materials | 2.6% | |||

Telecommunication Services | 1.7% | |||

Utilities | 2.2% | |||

Total | 100.0% | |||

Portfolio holdings and allocations are subject to change. As of April 30, 2014, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the preceding Portfolio of Investments which are computed using the Fund’s total net assets.

| Shares | Market Value | |||||||||

| Common Stocks — 96.2% | |||||||||

| Consumer Discretionary — 8.3% | |||||||||

| 112 | Abercrombie & Fitch Co., Class A | $ | 4,117 | |||||||

| 84 | Advance Auto Parts, Inc. | 10,188 | ||||||||

| 154 | Amazon.com, Inc. † | 46,836 | ||||||||

| 224 | American Eagle Outfitters, Inc. | 2,589 | ||||||||

| 308 | Ann, Inc. † | 12,071 | ||||||||

| 140 | Bed Bath & Beyond, Inc. † | 8,698 | ||||||||

| 210 | Best Buy Co., Inc. | 5,445 | ||||||||

| 280 | Cato Corp., Class A | 7,977 | ||||||||

| 364 | CBS Corp., Class B | 21,025 | ||||||||

| 14 | Chipotle Mexican Grill, Inc. † | 6,979 | ||||||||

| 140 | Coach, Inc. | 6,251 | ||||||||

| 1,176 | Comcast Corp., Class A | 60,870 | ||||||||

| 36 | CST Brands, Inc. | 1,175 | ||||||||

| 364 | DIRECTV † | 28,246 | ||||||||

| 168 | Discovery Communications, Inc., Class A † | 12,751 | ||||||||

| 112 | Dollar Tree, Inc. † | 5,832 | ||||||||

| 84 | Expedia, Inc. | 5,963 | ||||||||

| 98 | Family Dollar Stores, Inc. | 5,758 | ||||||||

| 126 | Foot Locker, Inc. | 5,863 | ||||||||

| 2,030 | Ford Motor Co. | 32,785 | ||||||||

| 70 | Fossil Group, Inc. † | 7,466 | ||||||||

| 210 | Gap, Inc. | 8,253 | ||||||||

| 448 | Goodyear Tire & Rubber Co. | 11,290 | ||||||||

| 490 | H & R Block, Inc. | 13,926 | ||||||||

| 182 | Harley-Davidson, Inc. | 13,457 | ||||||||

| 700 | Home Depot, Inc. | 55,658 | ||||||||

| 378 | Interpublic Group of Cos., Inc. | 6,585 | ||||||||

| 261 | Johnson Controls, Inc. | 11,781 | ||||||||

| 154 | L Brands, Inc. | 8,347 | ||||||||

| 140 | Lennar Corp., Class A | 5,403 | ||||||||

| 602 | Lowe’s Cos., Inc. | 27,638 | ||||||||

| 238 | Macy’s, Inc. | 13,668 | ||||||||

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Consumer Discretionary — (Continued) | |||||||||

| 196 | Marriott International, Inc., Class A | $ | 11,354 | |||||||

| 406 | McDonald’s Corp. | 41,161 | ||||||||

| 224 | McGraw-Hill Cos., Inc. | 16,560 | ||||||||

| 1,960 | Monarch Casino & Resort, Inc. † | 31,438 | ||||||||

| 40 | Murphy USA, Inc. † | 1,700 | ||||||||

| 28 | Netflix, Inc. † | 9,017 | ||||||||

| 266 | News Corp., Class A † | 4,527 | ||||||||

| 336 | NIKE, Inc., Class B | 24,511 | ||||||||

| 1,733 | Office Depot, Inc. † | 7,088 | ||||||||

| 70 | O’Reilly Automotive, Inc. † | 10,415 | ||||||||

| 70 | PetSmart, Inc. | 4,738 | ||||||||

| 28 | Priceline.com, Inc. † | 32,417 | ||||||||

| 70 | Ralph Lauren Corp. | 10,596 | ||||||||

| 126 | Ross Stores, Inc. | 8,578 | ||||||||

| 56 | Sherwin-Williams Co. | 11,191 | ||||||||

| 336 | Starbucks Corp. | 23,728 | ||||||||

| 140 | Starwood Hotels & Resorts Worldwide, Inc. | 10,731 | ||||||||

| 336 | Target Corp. | 20,748 | ||||||||

| 154 | Tempur-Pedic International, Inc. † | 7,728 | ||||||||

| 182 | Time Warner Cable, Inc. | 25,746 | ||||||||

| 476 | Time Warner, Inc. | 31,635 | ||||||||

| 336 | TJX Cos., Inc. | 19,548 | ||||||||

| 84 | Tractor Supply Co. | 5,648 | ||||||||

| 1,135 | Twenty-First Century Fox, Inc., Class A | 36,343 | ||||||||

| 168 | V.F. Corp. | 10,263 | ||||||||

| 294 | Viacom, Inc., Class B | 24,984 | ||||||||

| 852 | Walt Disney Co. | 67,598 | ||||||||

| 84 | Whirlpool Corp. | 12,883 | ||||||||

| 112 | Wyndham Worldwide Corp. | 7,990 | ||||||||

| 196 | Yum! Brands, Inc. | 15,090 | ||||||||

| 1,020,845 | ||||||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

6

Table of Contents

| Huntington US Equity Rotation Strategy ETF | (Continued) |

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Consumer Staples — 6.5% | |||||||||

| 1,022 | Altria Group, Inc. | $ | 40,992 | |||||||

| 420 | Archer-Daniels-Midland Co. | 18,367 | ||||||||

| 322 | Avon Products, Inc. | 4,920 | ||||||||

| 210 | Clorox Co. | 19,047 | ||||||||

| 2,044 | Coca-Cola Co. | 83,375 | ||||||||

| 448 | Colgate-Palmolive Co. | 30,150 | ||||||||

| 224 | Costco Wholesale Corp. | 25,912 | ||||||||

| 630 | CVS Caremark Corp. | 45,814 | ||||||||

| 476 | Hillshire Brands Co. | 16,969 | ||||||||

| 994 | Hormel Foods Corp. | 47,405 | ||||||||

| 294 | J & J Snack Foods Corp. | 27,518 | ||||||||

| 126 | Keurig Green Mountain, Inc. | 11,804 | ||||||||

| 210 | Kimberly-Clark Corp. | 23,573 | ||||||||

| 297 | Kraft Foods Group, Inc. | 16,887 | ||||||||

| 140 | Lancaster Colony Corp. | 13,283 | ||||||||

| 210 | Lorillard, Inc. | 12,478 | ||||||||

| 896 | Mondelez International, Inc. | 31,942 | ||||||||

| 98 | Monster Beverage Corp. † | 6,562 | ||||||||

| 728 | PepsiCo, Inc. | 62,528 | ||||||||

| 756 | Philip Morris International, Inc. | 64,586 | ||||||||

| 1,022 | Procter & Gamble Co. | 84,366 | ||||||||

| 126 | The Estee Lauder Cos., Inc., Class A | 9,144 | ||||||||

| 392 | Walgreen Co. | 26,617 | ||||||||

| 756 | Wal-Mart Stores, Inc. | 60,261 | ||||||||

| 196 | Whole Foods Market, Inc. | 9,741 | ||||||||

| 794,241 | ||||||||||

| Energy — 6.6% | |||||||||

| 252 | Anadarko Petroleum Corp. | 24,953 | ||||||||

| 196 | Apache Corp. | 17,013 | ||||||||

| 238 | Baker Hughes, Inc. | 16,636 | ||||||||

| 392 | Cabot Oil & Gas Corp. | 15,398 | ||||||||

| 378 | Chesapeake Energy Corp. | 10,868 | ||||||||

| 812 | Chevron Corp. | 101,921 | ||||||||

| 560 | ConocoPhillips | 41,613 | ||||||||

| 182 | CONSOL Energy, Inc. | 8,101 | ||||||||

| 280 | Denbury Resources, Inc. | 4,710 | ||||||||

| 210 | Devon Energy Corp. | 14,700 | ||||||||

| 48 | Energy Transfer Partners | 2,649 | ||||||||

| 280 | EOG Resources, Inc. | 27,440 | ||||||||

| 1,974 | Exxon Mobil Corp. | 202,156 | ||||||||

| 448 | Halliburton Co. | 28,255 | ||||||||

| 112 | Helmerich & Payne, Inc. | 12,169 | ||||||||

| 182 | Hess Corp. | 16,227 | ||||||||

| 168 | HollyFrontier Corp. | 8,835 | ||||||||

| 280 | Kinder Morgan, Inc. | 9,145 | ||||||||

| 364 | Marathon Oil Corp. | 13,159 | ||||||||

| 182 | Marathon Petroleum Corp. | 16,917 | ||||||||

| 154 | Murphy Oil Corp. | 9,768 | ||||||||

| 252 | Nabors Industries, Ltd. | 6,431 | ||||||||

| 210 | National Oilwell Varco, Inc. | 16,491 | ||||||||

| 224 | Noble Energy, Inc. | 16,079 | ||||||||

| 350 | Occidental Petroleum Corp. | 33,513 | ||||||||

| 196 | Peabody Energy Corp. | 3,726 | ||||||||

| 84 | Pioneer Natural Resources Co. | 16,235 | ||||||||

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Energy — (Continued) | |||||||||

| 168 | QEP Resources, Inc. | $ | 5,156 | |||||||

| 154 | Range Resources Corp. | 13,929 | ||||||||

| 602 | Schlumberger, Ltd. | 61,134 | ||||||||

| 238 | Southwestern Energy Co. † | 11,395 | ||||||||

| 336 | The Williams Cos., Inc. | 14,169 | ||||||||

| 322 | Valero Energy Corp. | 18,409 | ||||||||

| 819,300 | ||||||||||

| Financials — 11.1% | |||||||||

| 224 | ACE, Ltd. | 22,920 | ||||||||

| 280 | AFLAC, Inc. | 17,562 | ||||||||

| 308 | Allstate Corp. | 17,541 | ||||||||

| 560 | American Express Co. | 48,960 | ||||||||

| 392 | American International Group, Inc. | 20,827 | ||||||||

| 182 | Ameriprise Financial, Inc. | 20,317 | ||||||||

| 756 | Apartment Investment and Management Co., Class A | 23,307 | ||||||||

| 5,054 | Bank of America Corp. | 76,518 | ||||||||

| 644 | Bank of New York Mellon Corp. | 21,812 | ||||||||

| 406 | BB&T Corp. | 15,156 | ||||||||

| 812 | Berkshire Hathaway, Inc., Class B † | 104,625 | ||||||||

| 84 | BlackRock, Inc. | 25,284 | ||||||||

| 322 | Capital One Financial Corp. | 23,796 | ||||||||

| 336 | CBOE Holdings, Inc. | 17,929 | ||||||||

| 294 | CBRE Group, Inc., Class A † | 7,832 | ||||||||

| 686 | Charles Schwab Corp. | 18,213 | ||||||||

| 196 | Chubb Corp. | 18,048 | ||||||||

| 1,330 | Citigroup, Inc. | 63,720 | ||||||||

| 322 | Discover Financial Services | 18,000 | ||||||||

| 546 | eHealth, Inc. † | 22,872 | ||||||||

| 686 | Fifth Third Bancorp | 14,138 | ||||||||

| 294 | Franklin Resources, Inc. | 15,391 | ||||||||

| 266 | Goldman Sachs Group, Inc. | 42,513 | ||||||||

| 378 | Hartford Financial Services Group, Inc. | 13,559 | ||||||||

| 280 | HCP, Inc. | 11,721 | ||||||||

| 532 | Host Hotels & Resorts, Inc. | 11,411 | ||||||||

| 322 | Invesco, Ltd. | 11,338 | ||||||||

| 1,708 | J.P. Morgan Chase & Co. | 95,614 | ||||||||

| 56 | Jones Lang LaSalle, Inc. | 6,490 | ||||||||

| 952 | KeyCorp | 12,985 | ||||||||

| 238 | Lincoln National Corp. | 11,545 | ||||||||

| 434 | Marsh & McLennan Cos., Inc. | 21,401 | ||||||||

| 532 | MetLife, Inc. | 27,850 | ||||||||

| 210 | Moody’s Corp. | 16,485 | ||||||||

| 826 | Morgan Stanley | 25,548 | ||||||||

| 210 | Northern Trust Corp. | 12,653 | ||||||||

| 266 | PNC Financial Services Group | 22,355 | ||||||||

| 476 | Potlatch Corp. | 18,197 | ||||||||

| 308 | Prologis, Inc. | 12,514 | ||||||||

| 322 | Prudential Financial, Inc. | 25,979 | ||||||||

| 84 | Public Storage, Inc. | 14,743 | ||||||||

| 826 | Regions Financial Corp. | 8,376 | ||||||||

| 518 | Safety Insurance Group, Inc. | 27,822 | ||||||||

| 154 | Simon Property Group, Inc. | 26,673 | ||||||||

| 112 | SL Green Realty Corp. | 11,728 | ||||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

7

Table of Contents

| Huntington US Equity Rotation Strategy ETF | (Continued) |

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Financials — (Continued) | |||||||||

| 322 | State Street Corp. | $ | 20,788 | |||||||

| 336 | SunTrust Banks, Inc. | 12,855 | ||||||||

| 238 | Travelers Cos., Inc. | 21,558 | ||||||||

| 196 | T. Rowe Price Group, Inc. | 16,097 | ||||||||

| 840 | U.S. Bancorp | 34,255 | ||||||||

| 882 | Urstadt Biddle Properties, Class A | 18,002 | ||||||||

| 168 | Vornado Realty Trust | 17,237 | ||||||||

| 2,296 | Wells Fargo & Co. | 113,974 | ||||||||

| 420 | Weyerhaeuser Co. | 12,537 | ||||||||

| 1,391,571 | ||||||||||

| Health Care — 21.5% | |||||||||

| 719 | Abbott Laboratories | 27,854 | ||||||||

| 719 | AbbVie, Inc. | 37,446 | ||||||||

| 238 | Aetna, Inc. | 17,005 | ||||||||

| 238 | Agilent Technologies, Inc. | 12,862 | ||||||||

| 961 | Alexion Pharmaceuticals, Inc. † | 152,030 | ||||||||

| 211 | Allergan, Inc. | 34,992 | ||||||||

| 364 | Allscripts Healthcare Solutions, Inc. † | 5,540 | ||||||||

| 344 | Amgen, Inc. | 38,442 | ||||||||

| 296 | Baxter International, Inc. | 21,546 | ||||||||

| 784 | Becton, Dickinson & Co. | 88,615 | ||||||||

| 590 | Biogen Idec, Inc. † | 169,401 | ||||||||

| 801 | Bristol-Myers Squibb Co. | 40,122 | ||||||||

| 199 | Celgene Corp. † | 29,255 | ||||||||

| 1,484 | Cerner Corp. † | 76,129 | ||||||||

| 438 | Cooper Cos., Inc. | 57,776 | ||||||||

| 168 | Covance, Inc. † | 14,831 | ||||||||

| 322 | Covidien PLC | 22,943 | ||||||||

| 1,862 | CryoLife, Inc. | 16,907 | ||||||||

| 140 | DaVita, Inc. † | 9,702 | ||||||||

| 624 | Edwards Lifesciences Corp. † | 50,837 | ||||||||

| 574 | Eli Lilly & Co. | 33,923 | ||||||||

| 370 | Express Scripts Holding Co. † | 24,635 | ||||||||

| 431 | Gilead Sciences, Inc. † | 33,829 | ||||||||

| 1,080 | Henry Schein, Inc. † | 123,367 | ||||||||

| 420 | Hologic, Inc. † | 8,814 | ||||||||

| 126 | Hospira, Inc. † | 5,771 | ||||||||

| 969 | Humana, Inc. | 106,348 | ||||||||

| 1,106 | IDEXX Laboratories, Inc. † | 139,842 | ||||||||

| 21 | Intuitive Surgical, Inc. † | 7,596 | ||||||||

| 1,358 | Johnson & Johnson | 137,551 | ||||||||

| 42 | Mallinckrodt PLC † | 2,992 | ||||||||

| 767 | McKesson Corp. | 129,768 | ||||||||

| 484 | Medtronic, Inc. | 28,469 | ||||||||

| 1,267 | Merck & Co., Inc. | 74,196 | ||||||||

| 480 | Mettler-Toledo International, Inc. † | 111,897 | ||||||||

| 336 | Mylan Laboratories, Inc. † | 17,062 | ||||||||

| 2,640 | Neogen Corp. † | 110,285 | ||||||||

| 770 | Perrigo Co. PLC | 111,542 | ||||||||

| 2,859 | Pfizer, Inc. | 89,430 | ||||||||

| 57 | Regeneron Pharmaceuticals, Inc. † | 16,923 | ||||||||

| 1,093 | Salix Pharmaceuticals, Ltd. † | 120,229 | ||||||||

| 210 | St. Jude Medical, Inc. | 13,329 | ||||||||

| 210 | Stryker Corp. | 16,328 | ||||||||

| 931 | Thermo Fisher Scientific, Inc. | 106,134 | ||||||||

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Health Care — (Continued) | |||||||||

| 1,618 | UnitedHealth Group, Inc. | $ | 121,415 | |||||||

| 126 | Vertex Pharmaceuticals, Inc. † | 8,530 | ||||||||

| 182 | WellPoint, Inc. | 18,324 | ||||||||

| 2,642,764 | ||||||||||

| Industrials — 15.9% | |||||||||

| 320 | 3M Co. | 44,509 | ||||||||

| 140 | ADT Corp. | 4,234 | ||||||||

| 56 | Allegiant Travel Co. | 6,577 | ||||||||

| 70 | Allegion PLC | 3,455 | ||||||||

| 1,638 | Altra Industrial Motion Corp. | 55,954 | ||||||||

| 1,298 | Ametek, Inc. | 68,430 | ||||||||

| 336 | Boeing Co. | 43,351 | ||||||||

| 140 | C.H. Robinson Worldwide, Inc. | 8,246 | ||||||||

| 322 | Caterpillar, Inc. | 33,939 | ||||||||

| 616 | CSX Corp. | 17,384 | ||||||||

| 140 | Cummins, Inc. | 21,119 | ||||||||

| 333 | Danaher Corp. | 24,436 | ||||||||

| 252 | Deere & Co. | 23,522 | ||||||||

| 574 | Dxp Enterprises, Inc. † | 64,983 | ||||||||

| 358 | Eaton Corp. PLC | 26,005 | ||||||||

| 392 | Emerson Electric Co. | 26,726 | ||||||||

| 1,928 | Fastenal Co. | 96,554 | ||||||||

| 154 | FedEx Corp. | 20,983 | ||||||||

| 934 | Flowserve Corp. | 68,229 | ||||||||

| 182 | Fluor Corp. | 13,778 | ||||||||

| 140 | General Cable Corp. | 3,587 | ||||||||

| 168 | General Dynamics Corp. | 18,388 | ||||||||

| 4,788 | General Electric Co. | 128,749 | ||||||||

| 392 | Honeywell International, Inc. | 36,417 | ||||||||

| 300 | Illinois Tool Works, Inc. | 25,569 | ||||||||

| 210 | Ingersoll-Rand PLC | 12,558 | ||||||||

| 210 | ITT Corp. | 9,059 | ||||||||

| 112 | Joy Global, Inc. | 6,763 | ||||||||

| 84 | Kansas City Southern Industries, Inc. | 8,474 | ||||||||

| 467 | Kirby Corp. † | 46,990 | ||||||||

| 918 | L-3 Communications Holdings, Inc. | 105,909 | ||||||||

| 112 | Lincoln Electric Holdings, Inc. | 7,483 | ||||||||

| 154 | Lockheed Martin Corp. | 25,278 | ||||||||

| 336 | Masco Corp. | 6,750 | ||||||||

| 803 | Norfolk Southern Corp. | 75,908 | ||||||||

| 140 | Northrop Grumman Corp. | 17,011 | ||||||||

| 1,335 | Old Dominion Freight Line † | 80,941 | ||||||||

| 70 | Oshkosh Truck Corp. | 3,886 | ||||||||

| 266 | PACCAR, Inc. | 17,019 | ||||||||

| 140 | Parker Hannifin Corp. | 17,763 | ||||||||

| 63 | Pentair, Ltd. | 4,680 | ||||||||

| 184 | Precision Castparts Corp. | 46,569 | ||||||||

| 196 | Raytheon Co. | 18,714 | ||||||||

| 98 | Rockwell Automation, Inc. | 11,680 | ||||||||

| 280 | Rollins, Inc. | 8,422 | ||||||||

| 84 | Roper Industries, Inc. | 11,672 | ||||||||

| 588 | Southwest Airlines Co. | 14,212 | ||||||||

| 126 | Stanley Black & Decker, Inc. | 10,822 | ||||||||

| 210 | Textron, Inc. | 8,589 | ||||||||

| 1,120 | Toro Co. | 71,164 | ||||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

8

Table of Contents

| Huntington US Equity Rotation Strategy ETF | (Continued) |

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Industrials — (Continued) | |||||||||

| 280 | Tyco International, Ltd. | $ | 11,452 | |||||||

| 532 | Union Pacific Corp. | 101,308 | ||||||||

| 448 | United Parcel Service, Inc., Class B | 44,128 | ||||||||

| 490 | United Rentals, Inc. † | 45,977 | ||||||||

| 392 | United Technologies Corp. | 46,385 | ||||||||

| 243 | W.W. Grainger, Inc. | 61,819 | ||||||||

| 980 | Wabtec Corp. | 73,058 | ||||||||

| 364 | Waste Management, Inc. | 16,180 | ||||||||

| 1,933,747 | ||||||||||

| Information Technology — 20.3% | |||||||||

| 277 | Accenture PLC, Class A | 22,221 | ||||||||

| 322 | Adobe Systems, Inc. † | 19,864 | ||||||||

| 154 | Akamai Technologies, Inc. † | 8,173 | ||||||||

| 280 | Altera Corp. | 9,106 | ||||||||

| 728 | Amphenol Corp. | 69,416 | ||||||||

| 559 | Apple Computer, Inc. | 329,860 | ||||||||

| 838 | ASML Holding NV NYS | 68,204 | ||||||||

| 196 | Autodesk, Inc. † | 9,412 | ||||||||

| 294 | Automatic Data Processing, Inc. | 22,920 | ||||||||

| 233 | Cardtronics, Inc. † | 7,801 | ||||||||

| 2,394 | Cisco Systems, Inc. | 55,325 | ||||||||

| 96 | Citrix Systems, Inc. † | 5,694 | ||||||||

| 364 | Cognizant Technology Solutions Corp. † | 17,437 | ||||||||

| 840 | Corning, Inc. | 17,564 | ||||||||

| 140 | Cree, Inc. † | 6,604 | ||||||||

| 476 | eBay, Inc. † | 24,671 | ||||||||

| 336 | Electronic Arts, Inc. † | 9,509 | ||||||||

| 910 | EMC Corp. | 23,478 | ||||||||

| 42 | Equinix, Inc. † | 7,888 | ||||||||

| 728 | ExlService Holdings, Inc. † | 20,598 | ||||||||

| 752 | F5 Networks, Inc. † | 79,088 | ||||||||

| 2,100 | Fiserv, Inc. † | 127,638 | ||||||||

| 1,708 | Gartner Group, Inc. † | 117,750 | ||||||||

| 181 | Google, Inc., Class C † | 95,325 | ||||||||

| 181 | Google, Inc., Class A † | 96,813 | ||||||||

| 924 | Hewlett-Packard Co. | 30,547 | ||||||||

| 1,092 | Ingram Micro, Inc., Class A † | 29,440 | ||||||||

| 2,198 | Intel Corp. | 58,665 | ||||||||

| 462 | International Business Machines Corp. | 90,769 | ||||||||

| 149 | Intuit, Inc. | 11,287 | ||||||||

| 1,694 | Jack Henry & Associates, Inc. | 93,441 | ||||||||

| 322 | Juniper Networks, Inc. † | 7,950 | ||||||||

| 448 | Lam Research Corp. † | 25,809 | ||||||||

| 350 | MasterCard, Inc., Class A | 25,743 | ||||||||

| 1,284 | Measurement Specialties, Inc. † | 82,626 | ||||||||

| 742 | Micron Technology, Inc. † | 19,381 | ||||||||

| 3,178 | Microsoft Corp. | 128,390 | ||||||||

| 224 | NetApp, Inc. | 7,977 | ||||||||

| 504 | NVIDIA Corp. | 9,309 | ||||||||

| 1,610 | Oracle Corp. | 65,817 | ||||||||

| 56 | OSI Systems, Inc. † | 3,125 | ||||||||

| 420 | Paychex, Inc. | 17,560 | ||||||||

| 3,136 | PC-Tel, Inc. | 25,872 | ||||||||

| 714 | Qualcomm, Inc. | 56,199 | ||||||||

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Information Technology — (Continued) | |||||||||

| 84 | Rackspace Hosting, Inc. † | $ | 2,438 | |||||||

| 94 | Red Hat, Inc. † | 4,573 | ||||||||

| 238 | Rovi Corp. † | 5,305 | ||||||||

| 1,130 | Salesforce.com, Inc. † | 58,365 | ||||||||

| 1,180 | SanDisk Corp. | 100,265 | ||||||||

| 2,003 | Seagate Technology PLC | 105,317 | ||||||||

| 81 | Teradata Corp. † | 3,682 | ||||||||

| 630 | Texas Instruments, Inc. | 28,634 | ||||||||

| 252 | Trimble Navigation, Ltd. † | 9,684 | ||||||||

| 221 | Visa, Inc., Class A | 44,777 | ||||||||

| 182 | Western Digital Corp. | 16,040 | ||||||||

| 1,050 | Xerox Corp. | 12,695 | ||||||||

| 644 | XO Group, Inc. † | 6,839 | ||||||||

| 742 | Yahoo!, Inc. † | 26,675 | ||||||||

| 2,487,555 | ||||||||||

| Materials — 2.4% | |||||||||

| 112 | Albemarle Corp. | 7,508 | ||||||||

| 700 | Alcoa, Inc. | 9,429 | ||||||||

| 112 | Allegheny Technologies, Inc. | 4,614 | ||||||||

| 56 | CF Industries Holdings, Inc. | 13,730 | ||||||||

| 308 | Clearwater Paper Corp. † | 18,908 | ||||||||

| 98 | Cliffs Natural Resources, Inc. | 1,737 | ||||||||

| 70 | Cytec Industries, Inc. | 6,672 | ||||||||

| 574 | Dow Chemical Co. | 28,643 | ||||||||

| 462 | E.I. Du Pont de Nemours & Co. | 31,102 | ||||||||

| 196 | Ecolab, Inc. | 20,509 | ||||||||

| 434 | Freeport-McMoRan Copper & Gold, Inc. | 14,916 | ||||||||

| 154 | Hawkins, Inc. | 5,575 | ||||||||

| 210 | International Paper Co. | 9,797 | ||||||||

| 182 | Koppers Holdings, Inc. | 7,771 | ||||||||

| 238 | Monsanto Co. | 26,347 | ||||||||

| 168 | Mosaic Co. | 8,407 | ||||||||

| 196 | Newmont Mining Corp. | 4,867 | ||||||||

| 238 | Nucor Corp. | 12,317 | ||||||||

| 224 | Olympic Steel, Inc. | 5,905 | ||||||||

| 154 | Owens-Illinois, Inc. † | 4,894 | ||||||||

| 70 | PPG Industries, Inc. | 13,553 | ||||||||

| 140 | Praxair, Inc. | 18,277 | ||||||||

| 84 | Reliance Steel & Aluminum Co. | 5,949 | ||||||||

| 70 | Rock-Tenn Co., Class A | 6,693 | ||||||||

| 42 | Royal Gold, Inc. | 2,780 | ||||||||

| 238 | Sealed Air Corp. | 8,166 | ||||||||

| 168 | United States Steel Corp. | 4,371 | ||||||||

| 303,437 | ||||||||||

| Telecommunication Services — 1.6% | |||||||||

| 210 | American Tower Corp. | 17,539 | ||||||||

| 2,870 | AT&T, Inc. | 102,459 | ||||||||

| 392 | Sprint Corp. † | 3,332 | ||||||||

| 1,512 | Verizon Communications, Inc. | 70,656 | ||||||||

| 193,986 | ||||||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

9

Table of Contents

| Huntington US Equity Rotation Strategy ETF | (Continued) |

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Utilities — 2.0% | |||||||||

| 1,568 | American States Water Co. | $ | 47,604 | |||||||

| 434 | Edison International | 24,547 | ||||||||

| 1,078 | El Paso Electric Co. | 40,770 | ||||||||

| 672 | Exelon Corp. | 23,540 | ||||||||

| 490 | New Jersey Resources Corp. | 24,368 | ||||||||

| 285 | NextEra Energy, Inc. | 28,457 | ||||||||

| 336 | NRG Energy, Inc. | 10,994 | ||||||||

| 182 | Sempra Energy | 17,947 | ||||||||

| 742 | Southern Co. | 34,006 | ||||||||

| 252,233 | ||||||||||

| Total Common Stocks (Cost $9,746,574) | $ | 11,839,679 | |||||||

| Total Investments — 96.2% | $ | 11,839,679 | |||||||

| Other Assets less Liabilities — 3.8% | 467,312 | ||||||||

| Net Assets — 100.0% | $ | 12,306,991 | |||||||

| † | Non-income producing security |

NYS — New York Shares

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

10

Table of Contents

| Huntington EcoLogical Strategy ETF | April 30, 2014 |

| Portfolio of Investments Summary Table | (unaudited) |

| Percentage of Market Value | ||||

Consumer Discretionary | 16.7% | |||

Consumer Staples | 15.6% | |||

Energy | 3.6% | |||

Financials | 4.7% | |||

Health Care | 11.1% | |||

Industrials | 16.2% | |||

Information Technology | 22.5% | |||

Materials | 4.3% | |||

Utilities | 5.3% | |||

Total | 100.0% | |||

Portfolio holdings and allocations are subject to change. As of April 30, 2014, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the preceding Portfolio of Investments which are computed using the Fund’s total net assets.

Portfolio of Investments

| Shares | Market Value | |||||||||

| Common Stocks — 94.6% | |||||||||

| Consumer Discretionary — 15.8% | |||||||||

| 12,520 | BorgWarner, Inc. | $ | 777,993 | |||||||

| 720 | Chipotle Mexican Grill, Inc. † | 358,920 | ||||||||

| 12,362 | Ford Motor Co. | 199,646 | ||||||||

| 13,644 | LKQ Corp. † | 397,313 | ||||||||

| 5,126 | NIKE, Inc., Class B | 373,942 | ||||||||

| 6,480 | Starbucks Corp. | 457,618 | ||||||||

| 3,360 | V.F. Corp. | 205,262 | ||||||||

| 2,770,694 | ||||||||||

| Consumer Staples — 14.8% | |||||||||

| 2,240 | Costco Wholesale Corp. | 259,123 | ||||||||

| 2,510 | CVS Caremark Corp. | 182,527 | ||||||||

| 15,500 | Darling International, Inc. † | 310,155 | ||||||||

| 8,020 | Hain Celestial Group, Inc. † | 689,881 | ||||||||

| 5,576 | Lifeway Foods, Inc. | 83,696 | ||||||||

| 3,320 | McCormick & Co., Inc. | 236,384 | ||||||||

| 3,626 | Whitewave Foods Co. † | 100,404 | ||||||||

| 14,320 | Whole Foods Market, Inc. | 711,705 | ||||||||

| 2,573,875 | ||||||||||

| Energy — 3.4% | |||||||||

| 14,880 | Spectra Energy Corp. | 590,885 | ||||||||

| Financials — 4.4% | |||||||||

| 4,000 | CBRE Group, Inc., Class A † | 106,560 | ||||||||

| 2,923 | Jones Lang LaSalle, Inc. | 338,746 | ||||||||

| 4,100 | T. Rowe Price Group, Inc. | 336,733 | ||||||||

| 782,039 | ||||||||||

| Health Care — 10.5% | |||||||||

| 2,780 | Becton, Dickinson & Co. | 314,223 | ||||||||

| 900 | Biogen Idec, Inc. † | 258,408 | ||||||||

| 2,000 | Cerner Corp. † | 102,600 | ||||||||

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Health Care — (Continued) | |||||||||

| 2,805 | Gilead Sciences, Inc. † | $ | 220,164 | |||||||

| 1,398 | Henry Schein, Inc. † | 159,693 | ||||||||

| 1,250 | Humana, Inc. | 137,188 | ||||||||

| 4,880 | Johnson & Johnson | 494,295 | ||||||||

| 1,900 | Varian Medical Systems, Inc. † | 151,145 | ||||||||

| 1,837,716 | ||||||||||

| Industrials — 15.3% | |||||||||

| 11,170 | Air Lease Corp. | 400,668 | ||||||||

| 1,380 | Cummins, Inc. | 208,173 | ||||||||

| 2,720 | Fastenal Co. | 136,218 | ||||||||

| 3,501 | Illinois Tool Works, Inc. | 298,390 | ||||||||

| 14,420 | MasTec, Inc. † | 570,743 | ||||||||

| 600 | Middleby Corp. † | 151,488 | ||||||||

| 830 | Norfolk Southern Corp. | 78,460 | ||||||||

| 8,860 | Quanta Services, Inc. † | 312,581 | ||||||||

| 5,100 | Tennant Co. | 325,329 | ||||||||

| 7,558 | TETRA Tech, Inc. † | 216,688 | ||||||||

| 2,698,738 | ||||||||||

| Information Technology — 21.1% | |||||||||

| 2,928 | Accenture PLC, Class A | 234,884 | ||||||||

| 1,028 | Apple Computer, Inc. | 606,613 | ||||||||

| 5,400 | ARM Holdings PLC ADR | 245,808 | ||||||||

| 15,560 | eBay, Inc. † | 806,475 | ||||||||

| 200 | Google, Inc., Class C † | 105,332 | ||||||||

| 200 | �� | Google, Inc., Class A † | 106,976 | |||||||

| 8,364 | Qualcomm, Inc. | 658,330 | ||||||||

| 1,810 | SAP AG ADR | 146,592 | ||||||||

| 9,640 | Texas Instruments, Inc. | 438,138 | ||||||||

| 9,564 | Veeco Instruments, Inc. † | 353,581 | ||||||||

| 3,702,729 | ||||||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

11

Table of Contents

| Huntington EcoLogical Strategy ETF | (Continued) |

| Shares | Market Value | |||||||||

| Common Stocks — (Continued) | |||||||||

| Materials — 4.1% | |||||||||

| 3,086 | Ball Corp. | $ | 173,402 | |||||||

| 3,480 | Ecolab, Inc. | 364,147 | ||||||||

| 1,810 | Sigma-Aldrich Corp. | 174,140 | ||||||||

| 711,689 | ||||||||||

| Utilities — 5.2% | |||||||||

| 4,660 | NextEra Energy, Inc. | 465,301 | ||||||||

| 9,810 | Questar Corp. | 238,187 | ||||||||

| 1,920 | Sempra Energy | 189,331 | ||||||||

| 892,819 | ||||||||||

| Total Common Stocks (Cost $13,227,953) | $ | 16,561,184 | |||||||

| Total Investments — 94.6% | $ | 16,561,184 | |||||||

| Other Assets less Liabilities — 5.4% | 951,149 | ||||||||

| Net Assets — 100.0% | $ | 17,512,333 | |||||||

| † | Non-income producing security |

| ADR | American Depositary Receipt |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

12

Table of Contents

| Statements of Assets and Liabilities | April 30, 2014 |

| Huntington US Equity Rotation Strategy ETF | Huntington EcoLogical Strategy ETF | |||||||

| Assets: | ||||||||

Investments, at value (Cost $9,746,574 and $13,227,953) | $ | 11,839,679 | $ | 16,561,184 | ||||

Cash | 457,074 | 974,187 | ||||||

Dividends and interest receivable | 8,949 | 11,411 | ||||||

Receivable for investments sold | 199,269 | — | ||||||

Receivable from advisor | 5,383 | 7,878 | ||||||

Prepaid expenses | 1,342 | 1,371 | ||||||

Total Assets | 12,511,696 | 17,556,031 | ||||||

| Liabilities: | ||||||||

Payable for investments purchased | 167,501 | — | ||||||

Accrued expenses: | ||||||||

Administration | 12,238 | 12,831 | ||||||

Administrative support fees | 2,735 | 3,694 | ||||||

Compliance services | 214 | 286 | ||||||

Fund accounting | 728 | 96 | ||||||

Custodian | 2,206 | 448 | ||||||

Legal and audit fees | 16,302 | 21,783 | ||||||

Trustee | 1,070 | 1,430 | ||||||

Printing | 1,514 | 2,186 | ||||||

Other | 197 | 944 | ||||||

Total Liabilities | 204,705 | 43,698 | ||||||

Net Assets | $ | 12,306,991 | $ | 17,512,333 | ||||

| Net Assets consist of: | ||||||||

Capital | $ | 9,794,296 | $ | 14,075,648 | ||||

Accumulated net investment income (loss) | 13,792 | 5,377 | ||||||

Accumulated net realized gains (loss) on investments | 405,798 | 98,077 | ||||||

Net unrealized appreciation (depreciation) on investments | 2,093,105 | 3,333,231 | ||||||

Net Assets | $ | 12,306,991 | $ | 17,512,333 | ||||

Net Assets: | $ | 12,306,991 | $ | 17,512,333 | ||||

Shares of Beneficial Interest Outstanding (unlimited number of shares authorized, no par value): | 350,001 | 503,999 | ||||||

Net Asset Value (offering and redemption price per share): | $ | 35.16 | $ | 34.75 | ||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

13

Table of Contents

| Statements of Operations | For the year ended April 30, 2014 |

| Huntington US Equity Rotation Strategy ETF | Huntington EcoLogical Strategy ETF | |||||||

| Investment Income: | ||||||||

Dividend income | $ | 189,548 | $ | 181,174 | ||||

Total Investment Income | 189,548 | 181,174 | ||||||

| Expenses: | ||||||||

Advisory fees | 76,579 | 93,416 | ||||||

Administration fees | 67,318 | 78,436 | ||||||

Administrative support fees | 36,484 | 41,271 | ||||||

Fund accounting fees | 10,559 | 1,903 | ||||||

Custodian fees | 3,760 | 2,127 | ||||||

Trustee fees | 4,497 | 5,572 | ||||||

Compliance services fees | 665 | 869 | ||||||

Legal and audit fees | 39,762 | 48,151 | ||||||

Printing fees | 9,997 | 13,709 | ||||||

Amortization of deferred offering costs | 8,305 | 4,803 | ||||||

Other fees | 26,503 | 33,686 | ||||||

Total Expenses before fee reductions | 284,429 | 323,943 | ||||||

Expenses contractually waived or reimbursed by the Advisor | (154,843 | ) | (171,029 | ) | ||||

Reimbursement of offering costs by Advisor | (8,305 | ) | (4,803 | ) | ||||

Total Net Expenses | 121,281 | 148,111 | ||||||

Net Investment Income (Loss) | 68,267 | 33,063 | ||||||

| Realized and Unrealized Gains (Losses) on Investments: | ||||||||

Net realized gains (losses) on investments | 551,948 | 218,468 | ||||||

Net realized gains (losses) on in-kind redemptions of investments | 785,788 | 435,440 | ||||||

Change in unrealized appreciation/depreciation on investments | 816,287 | 2,030,051 | ||||||

Net Realized and Unrealized Gains (Losses) on Investments | 2,154,023 | 2,683,959 | ||||||

Change in Net Assets Resulting From Operations | $ | 2,222,290 | $ | 2,717,022 | ||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

14

Table of Contents

| Statements of Changes in Net Assets |

| Huntington US Equity Rotation Strategy ETF | Huntington EcoLogical Strategy ETF | |||||||||||||||

| Year Ended April 30, 2014 | For the period July 23, 2012(a) through April 30, 2013 | Year Ended April 30, 2014 | For the period June 18, 2012(a) through April 30, 2013 | |||||||||||||

| From Investment Activities: | ||||||||||||||||

| Operations: | ||||||||||||||||

Net investment income | $ | 68,267 | $ | 47,686 | $ | 33,063 | $ | 42,482 | ||||||||

Net realized gains on investments | 1,337,736 | 6,277 | 653,908 | 2,652 | ||||||||||||

Change in unrealized appreciation/depreciation on investments | 816,287 | 1,276,818 | 2,030,051 | 1,303,180 | ||||||||||||

Change in net assets resulting from operations | 2,222,290 | 1,330,781 | 2,717,022 | 1,348,314 | ||||||||||||

| Distributions to Shareholders From: | ||||||||||||||||

Net investment income | (71,442 | ) | (33,261 | ) | (33,136 | ) | (40,615 | ) | ||||||||

Net realized gains on investments | (96,570 | ) | — | (132,285 | ) | — | ||||||||||

Change in net assets from distributions | (168,012 | ) | (33,261 | ) | (165,421 | ) | (40,615 | ) | ||||||||

| Capital Transactions: | ||||||||||||||||

Proceeds from shares issued | 2,416,485 | 11,111,003 | 6,939,790 | 8,885,192 | ||||||||||||

Cost of shares redeemed | (3,276,607 | ) | (1,295,713 | ) | (1,657,988 | ) | (613,936 | ) | ||||||||

Change in net assets from capital transactions | (860,122 | ) | 9,815,290 | 5,281,802 | 8,271,256 | |||||||||||

Change in net assets | 1,194,156 | 11,112,810 | 7,833,403 | 9,578,955 | ||||||||||||

| Net Assets: | ||||||||||||||||

Beginning of period | 11,112,835 | 25 | 9,678,930 | 99,975 | ||||||||||||

End of period | $ | 12,306,991 | $ | 11,112,835 | $ | 17,512,333 | $ | 9,678,930 | ||||||||

Accumulated net investment income (loss) | $ | 13,792 | $ | 17,173 | $ | 5,377 | $ | 5,450 | ||||||||

| Share Transactions: | ||||||||||||||||

Issued | 75,000 | 425,000 | 225,000 | 350,000 | ||||||||||||

Redeemed | (100,000 | ) | (50,000 | ) | (50,000 | ) | (25,000 | ) | ||||||||

Change in shares | (25,000 | ) | 375,000 | 175,000 | 325,000 | |||||||||||

| (a) | Commencement of operations. |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

15

Table of Contents

| Financial Highlights | Huntington Strategy Shares |

| Net Asset Value, beginning of period | Net investment income | Net realized and unrealized gains on investments | Total from investment activities | Distributions from net investment income | Distributions from net realized gains from investment transactions | Total distributions | Net Asset Value, end of period | |||||||||||||||||||||||||

| Huntington US Equity Rotation Strategy ETF | ||||||||||||||||||||||||||||||||

Year Ended April 30, 2014 | $ | 29.63 | 0.18 | 5.80 | 5.98 | (0.19 | ) | (0.26 | ) | (0.45 | ) | $ | 35.16 | |||||||||||||||||||

July 23, 2012(f) through April 30, 2013 | $ | 25.00 | 0.17 | 4.59 | 4.76 | (0.13 | ) | — | (0.13 | ) | $ | 29.63 | ||||||||||||||||||||

| Huntington EcoLogical Strategy ETF | ||||||||||||||||||||||||||||||||

Year Ended April 30, 2014 | $ | 29.42 | 0.06 | 5.62 | 5.68 | (0.07 | ) | (0.28 | ) | (0.35 | ) | $ | 34.75 | |||||||||||||||||||

June 18, 2012(f) through April 30, 2013 | $ | 25.00 | 0.13 | 4.42 | 4.55 | (0.13 | ) | — | (0.13 | ) | $ | 29.42 | ||||||||||||||||||||

| (a) | Not annualized for periods less than one year. |

| (b) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. |

| (c) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from any primary listing market (e.g., NYSE Arca) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. |

| (d) | Annualized for periods less than one year. |

| (e) | If applicable, certain fees were waived and/or reimbursed. If such waivers/reimbursements had not occurred, the ratios would have been as indicated. |

| (f) | Commencement of operations. |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

16

Table of Contents

| Total return(a)(b) | Total return at market(a)(c) | Ratio of Net Expenses to Average Net Assets(d) | Ratio of Gross Expenses to Average Net Assets(d) | Ratio of Net Investment Income to Average Net Assets(d)(e) | Net Assets at end of period (000’s) | Portfolio turnover(a) | ||||||||||||||||||||

| 20.19 | % | 18.79 | % | 0.95 | % | 2.26 | % | 0.53 | % | $ | 12,307 | 39 | % | |||||||||||||

| 19.11 | % | 19.19 | % | 0.95 | % | 4.42 | % | 0.82 | % | $ | 11,113 | 13 | % | ||||||||||||

| 19.31 | % | 17.61 | % | 0.95 | % | 2.08 | % | 0.21 | % | $ | 17,512 | 10 | % | |||||||||||||

| 18.27 | % | 18.47 | % | 0.95 | % | 4.21 | % | 0.63 | % | $ | 9,679 | 16 | % | ||||||||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

17

Table of Contents

April 30, 2014

| (1) | Organization |

Huntington Strategy Shares (the “Trust”) was organized on September 1, 2010 as a Delaware statutory trust and is registered under the Investment Company Act of 1940 (the “1940 Act”), as an open-end management investment company. The Declaration of Trust permits the Trust to issue an unlimited number of shares of beneficial interest (“Shares”) in one or more series representing interests in separate portfolios of securities. Currently, the Trust offers its Shares in two separate series: Huntington US Equity Rotation Strategy ETF (the “US Equity Rotation Strategy ETF”) and Huntington EcoLogical Strategy ETF (the “EcoLogical Strategy ETF”) (individually referred to as a “Fund”, or collectively as the “Funds.”). Each Fund is an actively managed exchange-traded fund. The investment objective of both Funds is to seek capital appreciation, and the Funds do not seek to replicate a specified index. The Funds’ prospectus provides a description of each Fund’s investment objectives, policies, and strategies. The assets of each Fund are segregated and a shareholder’s interest is limited to the Fund in which shares are held.

Shares of each of the Funds are listed and traded on the NYSE Arca, Inc. Market prices for the Shares may be different from their net asset value (“NAV”). Each Fund issues and redeems Shares on a continuous basis at NAV only in large blocks of Shares, currently 25,000 Shares, called “Creation Units.” Creation Units are issued and redeemed principally in-kind for securities included in a specified universe. Once created, Shares generally trade in the secondary market at market prices that change throughout the day in amounts less than a Creation Unit.

Under the Trust’s organizational documents, its officers and Board of Trustees (“the Board”) are indemnified against certain liabilities arising out of the performance of their duties to the Funds. In addition, in the normal course of business, the Trust may enter into contracts with vendors and others that provide for general indemnifications. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust. However, based on experience, the Trust expects that risk of loss to be remote.

| (2) | Significant Accounting Policies |

The following is a summary of significant accounting policies consistently followed by each Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”). The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amount of assets, liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts

of income and expenses for the period. Actual results could differ from those estimates.

| A. | Investment Valuations |

The Funds hold investments at fair value. Fair value is defined as the price that would be expected to be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The valuation techniques used to determine fair value are further described below.

Security values are ordinarily obtained through the use of independent pricing services, in accordance with procedures adopted by the Trust’s Board. Pursuant to these procedures, the Funds may use a pricing service, bank, or broker-dealer experienced in such matters to value the Funds’ securities. When reliable market quotations are not readily available for any security, the fair value of that security will be determined by a committee established by the Board in accordance with procedures adopted by the Board. The fair valuation process is designed to value the subject security at the price the Funds would reasonably expect to receive upon its current sale. Additional consideration is given to securities that have experienced a decrease in the volume or level of activity or to circumstances that indicate that a transaction is not orderly.

The Trust has a three-tier fair value hierarchy that is dependent upon the various “inputs” used to determine the value of the Funds’ investments. The valuation techniques described below maximize the use of observable inputs and minimize the use of unobservable inputs in determining fair value. These inputs are summarized in the three broad levels listed below:

| • | Level 1—Quoted prices in active markets for identical assets. |

| • | Level 2—Other observable pricing inputs at the measurement date (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). |

| • | Level 3—Significant unobservable pricing inputs at the measurement date (including the Funds’ own assumptions in determining the fair value of investments). |

The inputs or methodology used for valuing investments are not necessarily an indication of the risk associated with investing in those investments.

Equity securities (including foreign equity securities) traded on a securities exchange are valued at the last reported sales price on the principal exchange. Equity securities quoted by NASDAQ are valued at the NASDAQ official closing price. If there is no reported sale on the principal exchange, and in the case of over-the-counter securities, equity securities are valued at a bid price estimated by the security pricing service. In each of these

Annual Shareholder Report

18

Table of Contents

Notes to Financial Statements (Continued)

situations, valuations are typically categorized as Level 1 in the fair value hierarchy.

Debt securities (corporate, municipal, foreign bonds and U.S. Government and agency securities) are valued using various inputs including benchmark yields, reported trades, broker/dealer quotes, issuer spreads, two-sided markets, benchmark securities, bids, offers, reference

data, and industry and market events, and are typically categorized as Level 2 in the fair value hierarchy.

The following is a summary of the inputs used to value the Funds’ investments as of April 30, 2014, while the breakdown, by category, of common stocks is disclosed in the Portfolio of Investments for each Fund.

| Level 1 | Total Investments | |||||||

US Equity Rotation Strategy ETF | ||||||||

Common Stocks(1) | $ | 11,839,679 | $ | 11,839,679 | ||||

|

|

|

| |||||

Total Investments | $ | 11,839,679 | $ | 11,839,679 | ||||

|

|

|

| |||||

EcoLogical Strategy ETF | ||||||||

Common Stocks(1) | $ | 16,561,184 | $ | 16,561,184 | ||||

|

|

|

| |||||

Total Investments | $ | 16,561,184 | $ | 16,561,184 | ||||

|

|

|

| |||||

| (1) | Please see Portfolio of Investments for industry classifications. |

The Trust’s policy is to disclose transfers between fair value hierarchy levels based on valuations at the end of the reporting period. There were no transfers between Levels 1, 2, or 3 for the year ended April 30, 2014. As of April 30, 2014, no securities were categorized as Level 2 or Level 3.

| B. | Security Transactions and Related Income |

Investment transactions are accounted for no later than the first calculation of the NAV on the business day following the trade date. For financial reporting purposes, however, security transactions are accounted for on the trade date on the last business day of the reporting period. Discounts and premiums on securities purchased are amortized over the lives of the respective securities. Securities gains and losses are calculated on the identified cost basis. Interest income and expenses are accrued daily. Dividends, less foreign tax withholding (if any), are recorded on the ex-dividend date.

| C. | Dividends and Distributions to Shareholders |

Dividends from net investment income, if any, are declared and paid annually. Net realized capital gains, if any, are distributed at least annually.

The amount of dividends from net investment income and net realized gains are determined in accordance with the federal income tax regulations, which may differ from GAAP. These “book/tax” differences are either considered temporary or permanent in nature. To the extent these differences are permanent in nature (e.g., distributions and income received from pass-through investments), such amounts are reclassified within the capital accounts based on their nature for federal income tax purposes; temporary differences do not require reclassification. Temporary differences are primarily due to return of capital from investments.

The Funds may own shares of real estate investments trusts (“REITs”) which report information on the source of their distributions annually. Distributions received from investments in REITs in excess of income from underlying investments are recorded as realized gain and/or as a reduction to the cost of the individual REIT.

| D. | Allocation of Expenses |

Expenses directly attributable to a Fund are charged to that Fund. Expenses not directly attributable to a Fund are allocated proportionally among both Funds within the Trust in relation to the net assets of each Fund or on another reasonable basis. The Trust may share expenses with the Huntington Funds Trust. Those expenses that are shared are allocated proportionally among each of the Trusts or on another reasonable basis.

| (3) | Investment Advisory and Other Contractual Services |

| A. | Investment Advisory Fees |

Huntington Asset Advisors, Inc. (the “Advisor”), a wholly-owned subsidiary of The Huntington National Bank (“Huntington”), serves as the Funds’ investment advisor. Huntington is a direct wholly-owned subsidiary of Huntington Bancshares Incorporated. The Advisor receives a fee for its services, computed daily and paid monthly, of 0.60% of each Fund’s average daily net assets.

The Advisor has contractually agreed to reduce its fees and/or reimburse each Fund’s expenses (excluding interest, taxes, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses) in order to limit total annual fund operating expenses after fee waivers and expense reimbursement to 0.95% of each Fund’s average annual daily net assets (“Expense Cap”). The Expense Cap will remain in effect until at least August 31, 2014. The Expense Cap may be terminated

Annual Shareholder Report

19

Table of Contents

Notes to Financial Statements (Continued)

earlier only upon the approval of the Board. The Advisor may recoup fees reduced or expenses reimbursed at any time within three years from the year such expenses were incurred, so long as the repayment does not cause the Expense Cap to be exceeded.

As of April 30, 2014, the Advisor may recoup amounts from the Funds as follows:

| Expires 04/30/16 | Expires 4/30/2017 | Total | ||||||||||

US Equity Rotation Strategy ETF | $ | 202,689 | $ | 154,843 | $ | 357,532 | ||||||

EcoLogical Strategy ETF | 219,439 | 171,029 | 390,468 | |||||||||

| B. | Administration, Transfer Agent and Accounting Fees |

Citi Fund Services Ohio, Inc. (“Citi”) provides financial administration, transfer agency and portfolio accounting services to the Trust. Citi performs certain services on behalf of the Trust including but not limited to: (1) preparing and filing the Trust’s periodic financial reports on forms prescribed by the Securities and Exchange Commission (“SEC”); (2) calculating Fund expenses and making required disbursements; (3) calculating Fund performance data; and (4) providing certain compliance support services. As portfolio accountant, Citi maintains certain financial records of the Trust and provides accounting services to each Fund which includes the daily calculation of each Fund’s NAV. Citi also performs certain other services on behalf of the Trust including providing financial information for the Trust’s federal and state tax returns and financial reports required to be filed with the SEC. For these services, each Fund pays Citi a fee accrued daily and paid monthly based on a percentage of each Fund’s average net assets, subject to a minimum annual fee. The fees are as follows:

—0.04% of the first $500 million in aggregate net assets of the Funds

—0.035% of the aggregate net assets of the next $500 million

—0.02% of the aggregate assets in excess of $1 billion