UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

June 20, 2018

YATRA ONLINE, INC.

1101-03, 11th Floor, Tower-B,

Unitech Cyber Park,

Sector 39, Gurgaon, Haryana 122002,

India

(Address, Including ZIP Code, and Telephone Number,

Including Area Code, of Registrant’s Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F x Form 40-F o

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): o

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): o

Yatra Online, Inc. (the “Company”) is filing the below risk factors and business description in this Report on Form 6-K for purposes of updating the risk factor and business description disclosure contained in its most recent Annual Report on Form 20-F (Registration No. 001-37968), filed with the Securities and Exchange Commission (the “SEC”) on June 30, 2017, and its reports filed under the Securities Exchange Act of 1934, as amended, as the case may be. All references in this Report on Form 6-K to “we,” “us,” “our,” “Company” and “Yatra” refer to Yatra Online, Inc. and its subsidiaries, unless stated otherwise or the context otherwise requires.

RISK FACTORS

The actual results of the Company could differ materially from those anticipated in any forward-looking statements identified in the Company’s reports filed with the SEC as a result of a number of factors, including those described in the below updated risk factors. The updated risk factors should be carefully considered along with any other risk factors related to the Company’s business identified in the Company’s other reports filed with the SEC. The occurrence of any one or more of these risks could materially and adversely affect the Company’s business, financial condition and results of operations.

Risks Related to Our Business and Industry

We have a history of operating losses.

We have a history of losses and may continue to incur operating and net losses for the foreseeable future. Yatra’s net losses were INR 4,052.0 million for fiscal year 2018 as compared to a loss of INR 5,937.0 million in fiscal year 2017 and a loss of INR 1,243.3 million in fiscal year 2016. If our revenues grow slower than anticipated, or if our operating expenses exceed expectations, then we may not be able to achieve profitability in the near future or at all, which may depress the price of our ordinary shares.

The Indian travel industry is highly competitive and we may not be able to effectively compete in the future.

The Indian travel industry is highly competitive. Our success depends upon our ability to compete effectively against numerous established and emerging competitors, including other online travel agencies, or OTAs, traditional offline travel companies, travel research companies, payment wallets, search engines and meta-search companies, both in India and abroad, such as Agoda Company Pte. Ltd., Booking.com B.V., Cleartrip Pvt. Ltd., Expedia Southeast Asia Pte. Ltd., Le Travenues Technology Pvt. Ltd. India, MakeMyTrip (India) Pvt. Ltd., and One97 Communications Limited. Our competitors may have significantly greater financial, marketing, personnel and other resources than we have. Factors affecting our competitive success include price, availability of travel products, ability to package travel products across multiple suppliers, brand recognition, customer service and customer care, fees charged to customers, ease of use, accessibility, reliability and innovation. If we are not able to compete effectively against our competitors, our business and results of operations may be adversely affected. In January 2017, MakeMyTrip and Ibibo Group Holdings (Singapore) Pte. Ltd. completed a merger that combined the two businesses under MakeMyTrip. To the extent this merger enhances MakeMyTrip’s ability to compete with us, particularly in India, our market share, business and results of operations could be adversely affected.

Large, established Internet search engines with a global presence and meta-search companies who can aggregate travel search results compete against us for customers. Certain of our competitors have launched brand marketing campaigns to increase their visibility with customers. Some of our competitors have significantly greater financial, marketing, personnel and other resources than we do and certain of our competitors have a longer history of established businesses and reputations in the Indian travel market (particularly in the Hotels and Packages business) as compared with us. Some meta-search sites, including TripAdvisor, Trivago and Kayak, offer users the ability to make reservations directly on their websites, which may reduce the amount of traffic and transactions available to us through referrals from these sites. If additional meta-search sites begin to offer the ability to make reservations directly, that will further affect our ability to generate traffic to our sites. From time to time, we may be required to reduce service fees and Net Revenue Margins in order to compete effectively and maintain or gain market share.

2

We may also face increased competition from new entrants in our industry. The travel industry is extremely dynamic and new channels of distribution in the travel industry may negatively affect our market share. Additional sources of competition include large companies that offer online travel services as one part of their business model, such as Amazon.com Inc. and Alibaba Group Holding Ltd, as well as “daily deal” websites, such as Groupon, Inc.’s Getaways, or peer-to-peer inventory sources, such as Airbnb Inc., HomeAway.com, Inc. and Oravel Stays Pvt. Ltd., which provide home and apartment rentals as an alternative to hotel rooms. The growth of peer-to-peer inventory sources could affect the demand for our services in facilitating reservations at hotels. We cannot assure you that we will be able to successfully compete against existing or new competitors in our existing lines of business as well as new lines of business into which we may venture. If we are not able to compete effectively, our business and results of operations may be adversely affected.

In addition, many airlines, hotels, car rental companies and tour operators have call centers and have established their own travel distribution websites and mobile applications. Suppliers may offer advantages for customers to book directly, such as member-only fares, bonus miles or loyalty points, which could make their offerings more attractive to customers. Some low-cost airlines distribute their online supply exclusively through their own websites and other airlines have stopped providing inventory to certain online channels and attempt to drive customers to book directly on their websites by eliminating or limiting sales of certain airline tickets through third party distributors. Additionally, airline suppliers are increasingly promoting hotel supply on their websites in connection with airline tickets. If we are unable to compete effectively with travel supplier-related channels or other competitors, our business and results of operations may be adversely affected.

We also face increasing competition from search engines like Google, Bing and Yahoo!. Search engines have grown in popularity and may offer comprehensive travel planning or shopping capabilities, which may drive more traffic directly to the websites of our suppliers or competitors. Google has increased its focus on appealing to travel customers through its launches of Google Places, Google Flights and Google Hotel Price Ads. Google’s efforts around these products, as well as possible future developments, may change or undermine our ability to obtain prominent placement in paid or unpaid search results at a reasonable cost or at all.

There can be no assurance that we will be able to compete successfully against any current and future competitors or on emerging platforms, or provide differentiated products and services to our customer base. Increasing competition from current and emerging competitors, the introduction of new technologies and the continued expansion of existing technologies, such as meta-search and other search engine technologies, may force us to make changes to our business models, which could affect our financial condition and results of operations. Increased competition has resulted in and may continue to result in reduced margins, as well as loss of customers, transactions and brand recognition.

The slowdown in Indian economic growth and other declines or disruptions in the Indian economy in general and travel industry in particular could adversely affect our business and financial performance.

Substantially all of our operations are located in India and, therefore, our financial performance and growth are necessarily dependent on economic conditions prevalent in India. The Indian economy may be materially and adversely affected by political instability or regional conflicts, a general rise in interest rates, inflation, and adverse economic conditions occurring elsewhere in the world, such as a slowdown in economic growth in China, the repercussions from the June 2016 United Kingdom referendum to withdraw from the European Union and other matters. While the Indian economy has grown significantly in recent years, it has experienced a slowdown in its economic growth a few quarters ago. The Indian economy could be further adversely impacted by inflationary pressures, any increase or volatility in oil prices, currency depreciation, the poor performance of its large agricultural and manufacturing sectors, trade deficits, recent initiatives by the Indian government towards demonetization of certain Indian currency, the Indian government’s recent implementation of a

3

comprehensive nationwide goods and services tax (‘GST’) regime, and other factors. India also faces major challenges in sustaining its growth, which include the need for substantial infrastructure development and improving access to healthcare and education.

In the past, economic slowdowns in the Indian economy may have harmed the travel industry as customers had less disposable income for their travels, especially holiday travel. If there is a slowdown in the India’s economic growth it will likely have a material adverse effect on the demand for the travel products we sell and, as a result, on our financial condition and results of operations. We do nearly all of our business with a wide variety of travel-related companies based in India, including airlines, large hotel chains and others. We are exposed to risks associated with these Indian businesses, including bankruptcies, restructurings, consolidations and alliances of its partners, the credit worthiness of these partners, and the possible obligation to make payments to our partners. For example, the Indian airline industry in recent years has experienced significant losses and has undergone bankruptcies, restructurings, consolidations and other similar events. Future bankruptcies and increasing consolidation could create challenges for our relationships with airlines, including by reducing the profitability of our airline ticketing business.

If the growth in the Indian travel industry cannot be sustained or the Indian economy as a whole continues to experience a slowdown in growth, our business and results of operations could be adversely affected.

The travel industry is particularly sensitive to safety concerns, and terrorist attacks, regional conflicts, health concerns, natural calamities or other catastrophic events could have a negative impact on the Indian travel industry and cause our business to suffer.

The travel industry is particularly sensitive to safety concerns, such as terrorist attacks, regional conflicts, health concerns, natural calamities or other catastrophic events. Our business has in the past declined and may in the future decline after incidents, such as those described below, that cause travelers to be concerned about their safety. Decreased travel expenditures could reduce the demand for our services, thereby causing a reduction in revenue.

India has experienced terror attacks in the past, including the coordinated attacks in 2008 in multiple locations in Mumbai, and may experience similar attacks in the future. In recent years, hotels, airlines, airports and cruises have been the targets of terrorist attacks, including in the Gulf of Aden, India, Spain, Egypt, Russia, Turkey, Sri Lanka, France, United Kingdom and Belgium. As many terrorist attacks tend to be focused on tourists or tourist destinations, such acts, even those outside of India or other neighboring countries, may result in a decline in the travel industry and adversely impact our business and prospects.

In addition, South Asia has, from time to time, experienced instances of civil unrest and hostilities among neighboring countries, including between India and Pakistan. There have also been incidents in and near India such as troop mobilizations along the border. Such military activity or other adverse social and political events in India in the future could adversely affect the Indian economy by disrupting communications and making travel more difficult. Resulting political tensions could create a greater perception that investments in Indian companies involve a high degree of risk and could have an adverse impact on our business and the price of our ordinary shares. Furthermore, if India were to become engaged in armed hostilities, we may not be able to continue our operations. The occurrence of any of these events may result in a loss of business confidence and have an adverse effect on our business and results of operations.

The outbreak of severe illnesses, such as the Ebola virus, Middle East Respiratory Syndrome, Severe Acute Respiratory Syndrome, malaria, H1N1 influenza virus, avian flu and the Zika virus, could materially affect the travel industry, reduce our revenues and adversely impact travel behavior, particularly if they were to persist for an extended period.

4

India has experienced natural calamities such as earthquakes, tsunamis, floods and drought in past years. For example, in September 2014, the state of Jammu and Kashmir in northern India, a popular tourism destination, experienced widespread floods and landslides, and in April 2015, an earthquake occurred in the Federal Democratic Republic of Nepal with aftershocks and landslides subsequently affecting the country. The extent and severity of these natural disasters determines their impact on the Indian economy. Substantially all of our operations and employees are located in India and there can be no assurance that we will not be affected by natural disasters in the future. Furthermore, if any of these natural disasters occur in tourist destinations in India, travel to and within India could be adversely affected, which could have an adverse impact on our business and results of operations.

The occurrence of any of these events could result in changes to customers’ travel plans and related costs and lost revenue for our company, as well as the risk of a prolonged and substantial decrease in travel volume, any of which could have a material adverse effect on our business, financial condition and results of operations.

Our business and financial results are subject to fluctuations in currency exchange rates.

Given the nature of our business, any fluctuation in the value of the Indian rupee against the U.S. dollar, Euro, British pound sterling or other major currencies will affect customers’ travel behavior and, therefore, will have an impact on our results of operations. For example, in fiscal year 2016, the drop in the average value of the Indian rupee as compared to the U.S. dollar adversely impacted the Indian travel industry as it made outbound travel for Indian consumers more expensive. In addition, our exposure to foreign currency risk also arises in respect of our non-Indian rupee-denominated trade and other receivables, trade and other payables, and cash and cash equivalents. We currently do not have any hedging agreements or similar arrangements with any counter-party to cover our exposure to any fluctuations in foreign exchange rates.

We have not previously operated as a public company, and fulfilling our obligations as a U.S. reporting company may be expensive and time consuming.

As a U.S. reporting company, we will incur significant legal, accounting and other expenses. For example, prior to becoming a U.S. reporting company, we had not previously been required to prepare or file periodic and other reports with the SEC or to comply with the other requirements of U.S. federal securities laws applicable to public companies. We have not previously been required to establish and maintain disclosure controls and procedures such as Section 404 of the Sarbanes Oxley Act of 2002 and internal controls over financial reporting applicable to a public company with securities registered in the United States. Compliance with reporting and corporate governance obligations from which foreign private issuers are not exempt may require members of our management and our finance and accounting staff to divert time and resources from other responsibilities to ensuring these additional regulatory requirements are fulfilled and may increase our legal, insurance and financial compliance costs. We cannot predict or estimate the amount of additional costs we may incur or the timing of such costs. In addition, if we fail to comply with any significant rule or requirement associated with being a public company, such failure could result in the loss of investor confidence and could harm our reputation and cause the market price of our ordinary shares to decline.

Our internal controls over financial reporting are not yet required to meet all of the standards contemplated by Section 404 of the Sarbanes-Oxley Act, and failure to achieve and maintain effective internal controls over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act could have a material adverse effect on our business and ordinary share price.

Our internal controls over financial reporting currently do not meet all of the standards contemplated by Section 404 of the Sarbanes-Oxley Act that eventually we will be required to meet. Because currently we do not have comprehensive documentation of our internal controls and have not

5

yet tested our internal controls in accordance with Section 404, we cannot conclude in accordance with Section 404 that we do not have a material weakness in our internal controls or a combination of significant deficiencies that could result in the conclusion that we have a material weakness in our internal controls. We will be required to document, review and, if appropriate, improve our internal controls and procedures in anticipation of eventually being subject to the requirements of Section 404 of the Sarbanes-Oxley Act, which will require annual management assessments of the effectiveness of our internal controls over financial reporting beginning with the filing of our second annual report with the SEC and, when we cease to be an EGC, an attestation report by our independent auditors evaluating these assessments.

Matters impacting our internal controls may cause us to be unable to report our financial information on a timely basis and thereby subject us to adverse regulatory consequences, including sanctions by the SEC. There also could be a negative reaction in the financial markets due to a loss of investor confidence in us and the reliability of our consolidated financial statements. Confidence in the reliability of our consolidated financial statements also could suffer if we or our independent registered public accounting firm were to report a material weakness in our internal controls over financial reporting. This could materially adversely affect us and lead to a decline in the price of our ordinary shares.

Our business depends on our relationships with a broad range of travel suppliers, and any adverse changes in these relationships, or our inability to enter into new relationships, could negatively affect our business and results of operations.

We rely significantly on our relationships with airlines, hotels, railways, bus lines, activity vendors, global distribution system, or GDS, service providers and other travel suppliers to enable us to offer our customers comprehensive access to travel services and products. Adverse changes in any of our relationships with travel suppliers, or the inability to enter into new relationships with travel suppliers, could reduce the amount of inventory that we may be able to offer. Our arrangements with travel suppliers are not typically subject to long-term commitments and may not remain in effect on current or similar terms, and the net impact of future pricing options may adversely impact our revenue. Travel suppliers are increasingly focused on driving online demand to their own websites and may cease to supply us with the same level of access to travel inventory in the future.

A significant change in our relationships with our major suppliers for a sustained period of time, including an inability by any travel supplier to fulfill their payment obligation to us in a timely manner or a supplier’s complete withdrawal of inventory, could have a material adverse effect on our business, financial condition or results of operations. Furthermore, no assurance can be given that our travel suppliers will not further reduce or eliminate fees or commissions or attempt to charge us for content, terminate our contracts, make their products or services unavailable to us as part of exclusive arrangements with our competitors or default on or dispute their payment or other obligations towards us, any of which could reduce our revenue and Net Revenue Margins or may require us to initiate legal or arbitration proceedings to enforce their contractual payment obligations, which may adversely affect our business and results of operations.

Some of our airline suppliers (including our GDS service providers) may reduce or eliminate the commission and other fees they pay to us for the sale of air tickets, and this could adversely affect our business and results of operations.

In our Air Ticketing business, we generate revenue through commissions and incentive payments from airline suppliers, service fees charged to our customers and fees from our GDS service providers. Our airline suppliers may reduce or eliminate the commissions and incentive payments they pay to us. To the extent any of our airline suppliers further reduce or eliminate the commissions or incentive payments they pay to us in the future, our revenue may be further reduced unless we are able to

6

adequately mitigate such reduction by increasing the service fees we charge to our customers in a sustainable manner. Any increase in service fees, to mitigate reductions in or elimination of commissions or otherwise, may also result in a loss of potential customers. Further, our arrangements with the airlines that supply air tickets to us may limit the amount of service fees that we are able to charge our customers. Our business would also be negatively impacted if competition or regulation in the travel industry causes us to reduce or eliminate our service fees.

We rely on third-party systems and service providers, and any disruption or adverse change in their business may have a material adverse effect on our business.

We currently rely on a variety of third-party systems, service providers and software companies, including the GDS and other electronic central reservation systems used by airlines, various offline and online channel managing systems and reservation systems used by hotels and accommodation suppliers and aggregators, systems used by Indian Railways, and systems used by bus and car operators and aggregators, as well as other technologies used by payment gateway providers. In particular, we rely on third parties to:

· assist in conducting searches for airfares and process air ticket bookings;

· process hotel reservations;

· process credit card, debit card, net banking and e-wallet payments;

· provide computer infrastructure critical to our business; and

· provide customer relationship management, or CRM, software services.

These third parties are subject to general business risks, including system downtime, hacker attack, fraudulent access, natural disaster, human error or other causes leading to unexpected business interruptions. Any interruption in these or other third party services or deterioration in their performance could impair the quality of our service. For example, technical glitches in third party systems may result in the information provided by us to our customers, such as the availability of hotel rooms on a central reservations system of a hotel supplier, to not be accurate, and we may incur monetary and/or reputational loss as a result. Furthermore, if our arrangements with any of these third parties are suspended, terminated or no longer available on commercially acceptable terms, we may not be able to find an alternate source of support on a timely basis and on commercially reasonable terms, or at all.

Our success is also dependent on our ability to maintain our relationships with these third-party systems and service providers, including our technology partners. In the event our arrangements with any of these third parties are impaired or terminated, we may not be able to find an alternative source of systems support on a timely basis or on commercially reasonable terms, which could result in significant additional costs or disruptions to our business.

We may not be able to adequately control and ensure the quality of travel products and services sourced from our travel suppliers. If there is any deterioration in the quality of their performance, our customers may seek damages from us and not continue using our online platform.

As we increase the number of third party services available through our platform, we may not be able to adequately monitor or assure the quality of these services, and increases in customer dissatisfaction may adversely impact our business.

In 2015, we launched a marketplace platform that enables us to sell our own inventory and the inventory of third party vendors to provide travelers a wider selection of products and services on a single platform. This platform allows third party suppliers or travel services to manage and sell products and services on yatra.com directly to consumers. We may not be able to adequately monitor these third

7

party vendors to ensure that they provide high-quality travel products and services to our customers on a consistent basis. Certain travel service providers may lack adequate quality control for their travel products and customer service. Similarly, we cannot ensure that every travel service provider has obtained, and duly maintained, all of the licenses and permits required for it to provide travel products to consumers.

The actions that we take to monitor and enhance the performance of our travel suppliers may be inadequate to timely discover these quality issues. There may be customer complaints and litigation against us due to our travel suppliers’ failure to provide satisfactory travel products or services. If our travelers are dissatisfied with the travel products and services provided by third party vendors they find through our marketplace platform, they may reduce their use of, or completely forgo, our marketplace platform as well as our core platform, including our mobile apps. They may also demand refunds of their payments to us or claim compensation from us for damages suffered as a result of our travel suppliers’ performance or misconduct. Increases in customer dissatisfaction with third party vendors could damage our brand, reduce our traffic and materially and adversely affect our business and results of operations.

Failure to maintain the quality of customer services could harm our reputation and our ability to retain existing customers and attract new customers, which may materially and adversely affect our business, financial condition and results of operations.

Our business is significantly affected by the overall size of our customer base, which in turn is determined by, among other factors, their experience with our customer services. As such, the quality of customer services is critical to retaining our existing customers and attracting new customers. If we fail to provide quality customer services, our customers may be less inclined to book travel products and services with us or recommend us to new customers, and may switch to our competitors. Failure to maintain the quality of customer services could harm our reputation and our ability to retain existing customers and attract new customers, which may materially and adversely affect our business, financial condition and results of operations.

We depend on a small number of airline suppliers in India for a significant percentage of our Air Ticketing revenue.

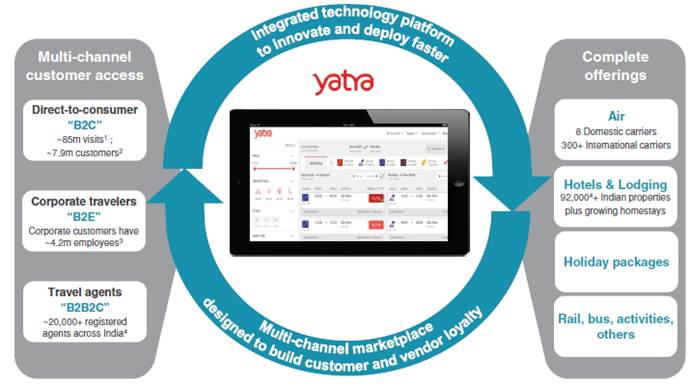

Our growth strategy is heavily dependent on the continued expansion of our Air Ticketing business and our airline supplier relationships. We currently provide our customers with access to eight domestic airlines as well as over 300 international airlines; however, a substantial portion of our Air Ticketing revenue is represented by five domestic airlines. Our dependence on a limited number of domestic airlines means that a reduction or elimination in base commissions and incentive payments by one or more of these airlines could have a material adverse effect on our revenue. Furthermore, our reliance on these Indian airlines exposes us to the risks associated with the domestic airline industry, such as rising fuel costs, high taxes, currency depreciation and liquidity constraints. In addition, our reliance on these airlines increases their bargaining power in price and contract negotiations, and further consolidation of domestic airline suppliers may exacerbate these trends. If one or all of these domestic airlines exert significant price and margin pressure on us, it could materially and adversely affect our business, financial condition and results of operations.

Any failure to maintain the quality of our brand and reputation could have a material adverse effect on our business.

We have invested considerable time and resources in developing and promoting our “Yatra” brand. We expect to continue to spend on maintaining the high quality of our brand in order to compete against a large and growing number of competitors. We also believe that the strength of our brand is one of our key assets that will allow us to expand into new geographies, such as Tier 2 and Tier 3 cities

8

in India, where our brand is not as well known. These efforts may not be successful and, even if we are successful in our branding efforts, such efforts may not be cost-effective. If we are unable to maintain or enhance consumer awareness of our brands or generate demand in a cost-effective manner, it could have a material adverse effect on our business and financial performance.

In addition, we receive significant media coverage in India and other geographic markets. We could receive unfavorable publicity regarding, for example, our practices relating to personnel, business, operating, accounting, prospects, business ethics, privacy and data protection, product changes, competitive pressures, the accuracy of user-generated content, product quality, litigation or regulatory activity,. Such allegations could adversely affect our reputation with our users and advertisers. Such allegations, directly or indirectly against us, may be posted in internet chat-rooms or on blogs or any website by anyone, and may even be posted on an anonymous basis. We may be required to spend significant time and incur substantial costs in response to such allegations or other detrimental conduct, and there is no assurance that we will be able to conclusively refute each of them within a reasonable period of time, or at all. Such potential negative publicity also could have an adverse effect on the size, engagement and loyalty of our user base and result in decreased revenue, which could adversely affect our business and results of operations.

We are exposed to the proceedings or claims arising from travel-related accidents or customer misconducts during their travels, the occurrence of which may be beyond our control.

Accidents are a leading cause of mortality and morbidity among tourists. We are exposed to risks of our customers’ claims arising from or relating to travel-related accidents. As we enter into contracts with our customers directly, our customers typically take actions against us for the damages they suffer during their travels. However, such accidents may result from the negligence or misconduct of our travel suppliers or other service providers, over which we have no or limited control. See also “—Risks Related to Our Business and Industry—We may not be able to adequately control and ensure the quality of travel products and services sourced from our travel suppliers. If there is any deterioration in the quality of their performance, our customers may seek damages from us and not continue using our online platform.” However, there is no assurance that such insurance or indemnification will be sufficient to cover all of our losses. In addition, some of the travel-related accidents result from adventure activities undertaken by our customers during their travels, such as scuba diving, white water rafting, wind surfing and skiing. Furthermore, we may be affected by our customer misconduct during their travels, over which we have no or limited control. However, such accidents and misconduct, even if not resulting from our or our travel suppliers’ negligence or misconduct, could create a public perception that we are less reliable than our competitors, which would harm our reputation, and could adversely affect our business and results of operations.

We may be subject to legal or administrative proceedings regarding our travel products and services, information provided on our online platform or other aspects of our business operations, which may be time-consuming to defend and affect our reputation.

From time to time, we have become and may in the future become a party to various legal or administrative proceedings arising in the ordinary course of our business, including breach of contract claims, anti-competition claims and other matters. Such proceedings are inherently uncertain and their results cannot be predicted with certainty. Regardless of the outcome and merit of such proceedings, any such legal action could have an adverse impact on our business because of defense costs, negative publicity, diversion of management’s attention and other factors. In addition, it is possible that an unfavorable resolution of one or more legal or administrative proceedings, whether in India or in another jurisdiction, could materially and adversely affect our financial position, results of operations or cash flows in a particular period or damage our reputation. In addition, our online platform contains information about our travel products and services, vacation destinations and other travel-related topics. It is possible that if any content accessible on our online platform contains errors or false or misleading information, our customers may take actions against us.

9

We rely on assumptions and estimates to calculate certain of our key metrics, and real or perceived inaccuracies in such metrics may harm our reputation and negatively affect our business.

We believe that certain metrics are key to our business, including travel expenditures, customers, repeat customers, total transaction volume, customer traffic, monthly visitors, app downloads, travel agents and bookings. As the industry in which we operate continues to evolve, the metrics by which we evaluate our business may change over time. While these numbers are based on what we believe to be reasonable estimates, our internal tools have a number of limitations and our methodologies for tracking these metrics may change over time. For example, a single person may have multiple accounts or browse the Internet on multiple browsers or devices, some users may restrict our ability to accurately identify them across visits, some mobile applications automatically contact our servers for regular updates with no user action, and we are not always able to capture user information on all of our platforms. As such, the calculations of our traffic and monthly visitors may not accurately reflect the number of people actually visiting our platforms. Also, if the internal tools we use to track these metrics under-count or over-count performance or contain algorithmic or other technical errors, the data and/or reports we generate may not be accurate. In addition, historically, certain metrics were calculated by independent third parties, and have not been verified by us. We calculate metrics using internal tools, which are not independently verified by a third party. In addition, we continue to improve upon our tools and methodologies to capture data and believe that our current metrics are more accurate; however, the improvement of these tools and methodologies could cause inconsistencies between current data and previously reported data, which could confuse investors or lead to questions about the integrity of the data.

The roll-out of new features, improvements and strategies may not meet our expectations.

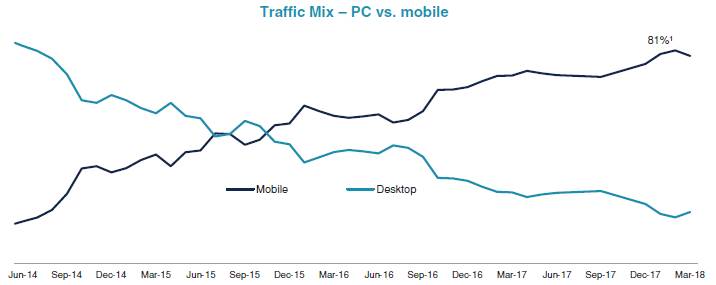

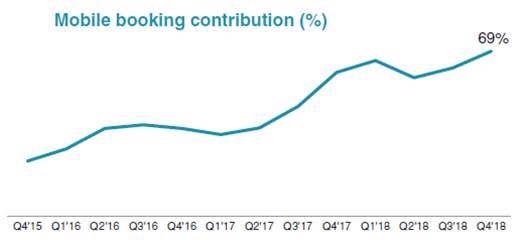

We are constantly working to improve our websites and mobile applications and roll-out new features to improve our user experience, attract new users, expand our market reach and develop new sources of revenue. However, there is no guarantee that these initiatives will ultimately be successful and, if they are not, our business and results of operations may be materially adversely affected. For example, in 2014 we launched our eCash program to reward customers for repeat purchases. Customers accumulate eCash points on travel booked through us, and these points work as a currency that can be redeemed by customers during future bookings. This program may not have the positive impact on total transaction volume and customer retention that we originally anticipated. For example, we currently expect that customers who book business travel through our corporate platform will receive the eCash points associated with that travel. However, if the eCash is held by the employer rather than the employee, the impact of this initiative may not be as significant as expected. Even if we are able to successfully adopt new features, improvements or strategies, the impact of such initiatives may take longer to develop than we expect or not develop at all. For example, we are moving rapidly toward a “Mobile First” business model. However we can provide no assurance that we will not experience delays or disruptions as we implement this initiative or that, once we have successfully done so, the market opportunity for a “Mobile First” business will not have changed in a way that could negatively impact our “Mobile First” business, our efforts to attract new customers and our results of operations.

The online homestay market is rapidly evolving and if we fail to compete successfully, our business and results of operations may suffer.

We recently added homestays through our Yatra and Travelguru websites. The online homestay market is a rapidly evolving market. Since we began offering such services, there have been and continue to be significant business, marketing and regulatory developments. Operating in new and relatively untested markets requires significant management attention and financial resources. We cannot provide any assurance that our efforts to expand in this market will be successful, and the

10

investment and additional resources required to establish operations and manage growth may not produce the desired financial results.

We may not be successful in pursuing strategic partnerships and acquisitions, and future partnerships and acquisitions may not bring us anticipated benefits.

Part of our growth strategy is the pursuit of strategic partnerships and acquisitions. There can be no assurance that we will succeed in implementing this strategy as we are subject to many factors which are beyond our control, including our ability to identify, attract and successfully execute suitable acquisition opportunities and partnerships. This strategy may also subject us to uncertainties and risks, including acquisition and financing costs, potential ongoing and unforeseen or hidden liabilities, diversion of management resources and the costs of integrating acquired businesses. We could face difficulties integrating the technology of acquired businesses with our existing technology, and employees of the acquired business into various departments and ranks in our company, and it could take substantial time and effort to integrate the business processes being used in the acquired businesses with our existing business processes. Moreover, there is no assurance that such partnerships or acquisitions will achieve our intended objectives or enhance our business. Any such failure could negatively impact our ability to compete in the travel industry and have a material adverse effect on our business or results of operations.

In the quarter ended September 30, 2017, Yatra Online Private Limited, a subsidiary of Yatra Online, Inc., acquired Air Travel Bureau Limited (“ATB”), India’s largest independent corporate travel services provider. As we integrate ATB into the Yatra portfolio, there may be unexpected costs and difficulties in integrating the two businesses.

As we increase our sales efforts toward larger corporate customers and B2B2C travel agents, our sales cycle, customer support efforts and collection efforts may become more time consuming and expensive.

In recent years, we have increased our sales efforts toward larger corporate customers, including leading organizations from around India. The ATB acquisition was part of this effort. As we attempt to capitalize on this investment and increase our sales efforts targeted to large corporate customers, we expect to face greater costs, longer sales cycles and less predictability in completing some of our sales. Additionally, we may face challenges integrating the disparate sales approaches and strategies of the formerly separate ATB and Yatra segments. Furthermore, if a prospective corporate customer’s decision to use our travel services is an enterprise-wide decision, these sales may require us to provide greater education to the prospective customer. Consequently, these customers may require us to devote greater sales, implementation and customer support resources to them.

In addition, we are trying to increase our sales efforts to the B2B2C (business to business to consumer) segment by making inroads in India’s large and fragmented network of travel agents. We are currently trying to make inroads to this market via organic growth. To the extent that we cannot help these travel agents provide their clients with time and money-saving opportunities, the growth in this segment may slow. Slower growth in this segment may hinder our efforts to reach customers in smaller markets, such as the Tier 2 and Tier 3 markets in India, who often utilize intermediaries such as travel agents to arrange their travel.

As part of these efforts to attract corporate and B2B2C travel agents and retail customers, we typically extend credit periods to certain segments of our customer base. We may experience difficulty collecting payment fully and in a timely manner on our outstanding accounts receivable from our customers. As a result, we may face a greater risk of non-payment of our accounts receivable and, as our corporate travel business and B2B2C travel agents business grows in scale, we may need to make increased provisions for doubtful accounts. We cannot provide any assurance that we will be able to

11

increase our corporate customer base and B2B2C travel agents, and our sales efforts to obtain such customers may become time consuming, costly and harmful to our business and results of operations.

Our failure to raise additional capital or generate cash flows necessary to expand our operations and invest in new technologies in the future could reduce our ability to compete successfully and harm our results of operations.

We believe that our existing cash and cash equivalents will be sufficient to meet our anticipated cash requirements for at least the next 12 months. However, we may need to raise additional funds, and we may not be able to obtain additional debt or equity financing on favorable terms, if at all. If we raise additional equity financing, our shareholders may experience significant dilution of their ownership interests and the value of our ordinary shares could decline. If we engage in debt financing, we may be required to accept terms that restrict our ability to incur additional indebtedness, force us to maintain specified liquidity or other ratios or restrict our ability to pay dividends or make acquisitions. In addition, the availability of funds depends in significant measure on capital markets and liquidity factors over which we exert no control. In light of periodic uncertainty in the capital and credit markets, we can provide no assurance that sufficient financing will be available on desirable terms or at all to fund investments, acquisitions, stock repurchases, dividends, debt refinancing or other corporate needs, or that our counterparties in any such financings would honor their contractual commitments. If we need additional capital and cannot raise it on acceptable terms, or at all, we may not be able to execute on our growth strategy, which could reduce our ability to compete successfully and harm our business and results of operations.

Raising additional capital may cause dilution to our shareholders, restrict our operations or require us to relinquish substantial rights.

To the extent that we raise additional capital through the sale of equity or convertible debt securities, your ownership interest will be diluted, and the terms of these new securities may include liquidation or other preferences that adversely affect your rights as a holder of our ordinary shares. Debt financing, if available at all, may involve agreements that include covenants limiting or restricting our ability to take specific actions such as incurring additional debt, making capital expenditures, or declaring dividends, and may be secured by all or a portion of our assets. Further, we may incur substantial costs in pursuing future capital and/or financing, including investment banking fees, legal fees, accounting fees, printing and distribution expenses and other costs and such efforts may divert our management from their day-today activities, which may compromise our ability to develop and market our products. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition.

We could be negatively affected by changes in Internet search engine algorithms and dynamics, or search engine disintermediation.

We rely heavily on Internet search engines, such as Google and Yahoo! India, to generate traffic to our websites, principally through the purchase of travel-related keywords. Search engines, including Google, frequently update and change the logic that determines the placement and display of results of a user’s search, such that the purchased or algorithmic placement of links to our websites can be negatively affected. In addition, a search engine could, for competitive or other purposes, alter its search algorithms or results, causing our websites to place lower in search query results. If a major search engine changes its algorithms in a manner that negatively affects the search engine ranking of our websites or those of our partners, or if competitive dynamics impact the cost or effectiveness of our search engine optimization or search engine monetization in a negative manner, our business and financial performance would be adversely affected, potentially to a material extent. Furthermore, our

12

failure to successfully manage our search engine optimization and search engine monetization strategies could result in a substantial decrease in traffic to our websites, as well as increased costs if we were to replace free traffic with paid traffic. In addition, to the extent that Google, Yahoo! India or other leading search or metasearch engines in India disrupt the businesses of OTAs or travel content providers by offering comprehensive travel planning or shopping capabilities, or refer those leads to suppliers directly, or to other favored partners, there could be a material adverse impact on our business. To the extent these actions have a negative effect on our search traffic, whether on desktop, tablet or mobile devices, our business and results of operations could be adversely affected.

Any inability or failure to adapt to technological developments, the evolving competitive landscape or industry trends could harm our business and competitiveness.

We depend upon the use of sophisticated information technology and systems. Our competitiveness and future results depend on our ability to maintain and make timely and cost-effective enhancements, upgrades and additions to our products, services, technologies and systems in response to new technological developments, industry standards and trends and customer demands. Adapting to new technological and marketplace developments may require substantial expenditures and lead time and we cannot guarantee that projected benefits will actually materialize. We may experience difficulties that could delay or prevent the successful development, marketing and implementation of enhancements, upgrades and additions. Moreover, we may fail to maintain, upgrade or introduce new products, services, technologies and systems as quickly as our competitors or in a cost-effective manner. In addition, the travel industry is marked by continuous innovation and the development of new products, services and technologies. As a result, in order to maintain its competitiveness, we must continue to invest significant resources to continually improve the speed, accuracy and comprehensiveness of our travel offerings. Changes to our technology platforms or increases in our investments in technology could adversely affect our results of operations. If we face material delays in adapting to technological developments, our customers may forego the use of our services in favor of those of our competitors. Any of these events could have a material adverse effect on our business and results of operations.

Our success depends on maintaining the integrity of our systems and infrastructure, which may suffer from failures, capacity constraints, business interruptions and forces outside of our control.

Our business relies significantly on computer systems to facilitate and process transactions and we have experienced rapid growth in consumer traffic to our websites and through our mobile apps. However, we may not be able to maintain and improve the efficiency, reliability and integrity of our systems. Unexpected increases in the volume of our business could exceed system capacity, resulting in service interruptions, outages and delays. Such constraints can also lead to the deterioration of our services or impair our ability to process transactions. System interruptions may prevent us from efficiently providing services to our customers, travel suppliers or other third parties, which could cause damage to our reputation and result in us losing customers and revenues or cause us to incur litigation costs and liabilities. Although we contractually limit our liability for damages, we cannot guarantee that we will not be subject to lawsuits or other claims for compensation from our customers in connection with such outages for which we may not be indemnified or compensated.

Our systems may also be susceptible to external damage or disruption. Our systems could be damaged or disrupted by power, hardware, software or telecommunication failures, human errors, natural events including floods, hurricanes, fires, winter storms, earthquakes and tornadoes, terrorism, break-ins, hostilities, war or similar events. Computer viruses, denial of service attacks, physical or electronic break-ins and similar disruptions affecting the Internet, telecommunication services or our systems could cause service interruptions or the loss of critical data, and could prevent us from providing timely services. Failure to efficiently provide services to customers or other third parties could

13

cause damage to our reputation and result in the loss of customers and revenues, significant recovery costs or litigation and liabilities. Moreover, such risks might increase as we expand our business and as the tools and techniques involved become more sophisticated. Disasters affecting our facilities, systems or personnel might be expensive to remedy and could significantly diminish our reputation and our brands, and we may not have adequate insurance to cover such costs.

Our use of open source software could adversely affect our ability to offer our products and services and subject us to possible litigation.

We use open source software in connection with our development of technology infrastructure. From time to time, companies that use open source software have faced claims challenging the use of open source software and/or compliance with open source license terms. We could be subject to suits by parties claiming ownership of what we believe to be open source software, or claiming noncompliance with open source licensing terms. Some open source licenses require users who distribute software containing open source to make available all or part of such software, which in some circumstances could include valuable proprietary code of the user. While we monitor the use of open source software and try to ensure that none is used in a manner that would require us to disclose our proprietary source code or that would otherwise breach the terms of an open source agreement, such use could inadvertently occur, in part because open source license terms are often ambiguous. Any requirement to disclose our proprietary source code or pay damages for breach of contract could be harmful to our business, results of operations or financial condition, and could help our competitors develop travel products and services that are similar to or better than ours.

We are exposed to risks associated with the payments business, including online security and credit card fraud.

The secure transmission of confidential information over the Internet is essential in maintaining customer and supplier confidence in us. Security breaches, whether instigated internally or externally on our system or other Internet-based systems, could significantly harm our business. We currently require customers to guarantee their transactions with their credit cards online. We rely on licensed encryption and authentication technology to effect secure transmission of confidential customer information, including credit card numbers, over the Internet. However, advances in technology or other developments could result in a compromise or breach of the technology that we use to protect customer and transaction data. We incur substantial expense to protect against and remedy security breaches and their consequences. However, our security measures may not prevent security breaches and we may be unsuccessful in or incur additional costs in connection with implementing a remediation plan to address these potential exposures.

We also have agreements with banks and certain companies that process customer credit card transactions for the facilitation of customer bookings of travel services from us. If any of these third parties experience business interruptions or otherwise are unable to provide the services we need, or if they increase the fees associated with those services, we will be adversely impacted. In addition, the online payment gateway for certain of our sales made through our mobile platform and through international credit and debit cards are secured by the respective card’s security features and we may be liable for credit card acceptance on our websites. We may also be subject to other payment disputes with our customers for such sales. If we are unable to combat the use of fraudulent credit cards, our revenue from such sales would be susceptible to demands from the relevant banks and credit card processing companies, and our results of operations and financial condition could be adversely affected.

14

Our processing, storage, use and disclosure of customer data of our customers or visitors to our website could give rise to liabilities as a result of governmental regulation, conflicting legal requirements, differing views of personal privacy rights or data security breaches.

In the processing of our customer transactions, we receive and store a large volume of customer information. Such information is increasingly subject to legislation and regulations in various jurisdictions and governments are increasingly acting to protect the privacy and security of personal information that is collected, processed and transmitted in or from the governing jurisdiction, for example, the recent enactment of European General Data Protection Regulations. We could be adversely affected if legislation or regulations are expanded or amended to require changes in our business practices or if governing jurisdictions interpret or implement their legislation or regulations in ways that negatively affect our business. As privacy and data protection become more sensitive issues in India, we may also become exposed to potential liabilities. For example, under the Indian Information Technology Act, 2000, as amended, we are subject to civil liability for wrongful loss or gain arising from any negligence by us in implementing and maintaining reasonable security practices and procedures with respect to sensitive personal data or information on our computer systems, networks, databases and software. India has also implemented privacy laws, including the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, 2011, which impose limitations and restrictions on the collection, use and disclosure of personal information. Any liability we may incur for violation of such laws and regulations and related costs of compliance and other burdens may adversely affect our business and results of operations.

We cannot guarantee that our security measures will prevent data breaches. Companies that handle such information have also been subject to investigations, lawsuits and adverse publicity due to allegedly improper disclosure of personally identifiable information. Security breaches could damage our reputation, cause interruptions in our operations, expose us to a risk of loss or litigation and possible liability, and could also cause customers and potential customers to lose confidence in the security of our transactions, which would have a negative effect on the demand for our services and products. Moreover, public perception concerning security and privacy on the Internet could adversely affect customers’ willingness to use our websites or mobile applications. A publicized breach of security in India or in other countries in which we have operations, even if it only affects other companies conducting business over the Internet, could inhibit the growth of the Internet as a means of conducting commercial transactions, and, therefore, our business.

These and other privacy and security developments that are difficult to anticipate could adversely affect our business, financial condition and results of operations.

Intellectual property rights are important to our business and we cannot be sure that our intellectual property is protected from copying or use by others, and we may be subject to third party claims for intellectual property rights infringement.

Our intellectual property rights are important to our business. We rely on a combination of copyright and trademark laws, trade secrets, confidentiality procedures and contractual provisions to protect our intellectual property. Our websites and mobile applications rely on content and in-house customizations and enhancements of third party technology, much of which is not subject to intellectual property protection. We protect our logos, brand name, websites’ domain names and, to a more limited extent, our content by relying on copyrights, trademarks, trade secret laws and confidentiality agreements. We have inter alia applied for trademark registration of our logos, and word marks for yatra.com in India and such applications are currently pending with the Registry of Trademarks. We have filed responses to objections raised by the Registry of Trademarks to certain of these applications. We have also filed oppositions with the Registry of Trademarks against certain trademarks in pursuance of the protection of our trademarks. Even with all of these precautions, there can be no assurance that our intellectual property will be protected. It is possible for someone else to copy or otherwise obtain

15

and use our content, techniques and technology without our authorization or to develop similar technology. While our domain names cannot be copied, another party could create an alternative domain name resembling ours that could be passed off as our domain name.

Our efforts to protect our intellectual property may not be adequate. Unauthorized parties may infringe upon or misappropriate our services or proprietary information. In addition, the global nature of the Internet makes it difficult to control the ultimate destination of our services. The misappropriation or duplication of our intellectual property could disrupt our ongoing business, distract our management and employees, reduce our revenues and increase our expenses. In the future, litigation may be necessary to enforce our intellectual property rights or to determine the validity and scope of the proprietary rights of others. Any such litigation could be time consuming and costly.

We could be subject to intellectual property infringement claims as the number of our competitors grows and the content and functionality of our websites or other service offerings overlap with competitive offerings. As competition in our industry increases and the functionality of technology offerings further overlaps, such claims and counterclaims could increase. There can be no assurance that we have not or will not inadvertently infringe on the intellectual property rights of third parties. Our defenses against these claims, even if not meritorious, could be expensive and divert management’s attention from operating our business. If we become liable to third parties for infringing their intellectual property rights, we could be required to pay a substantial award as damage and forced to develop non-infringing technology, obtain a license or cease selling the applications that contain the infringing technology. We may be unable to develop non-infringing technology or obtain a license on commercially reasonable terms or at all.

Our quarterly results may fluctuate for a variety of reasons, including the seasonality in the leisure travel industry, and may not fully reflect the underlying performance of our business.

Our quarterly operating results may vary significantly in the future, and period-to-period comparisons of its operating results may not be meaningful. Additionally, our growth may mask the seasonality of our business. Accordingly, the results of any one quarter should not be relied upon as an indication of future performance. Our quarterly financial results may fluctuate as a result of a variety of factors, many of which are outside of our control and, as a result, may not fully reflect the underlying performance of our business. For example, we tend to experience higher revenue from our Hotels and Packages business in the second and fourth calendar quarters of each year, which coincide with the summer holiday travel season and the year-end holiday travel season for our customers in India and other markets. In our Air Ticketing business, we may have higher revenues in a particular quarter arising out of periodic discounted sales of tickets by our suppliers. Other factors that may cause fluctuations in our quarterly financial results include, but are not limited to:

· foreign exchange rates;

· our ability to attract new customers and cross-sell to existing customers;

· the amount and timing of operating expenses related to the maintenance and expansion of our business, operations and infrastructure;

· general economic, industry and market conditions;

· changes in our pricing policies or those of our competitors and suppliers; and

· the timing and success of new services and service introductions by us and our competitors or any other change in the competitive dynamics of the Indian travel industry, including consolidation among competitors, customers or strategic partners.

Fluctuations in quarterly results may negatively impact the value of our ordinary shares and make quarter-to-quarter comparisons of our results less meaningful.

16

We may need to make additional investments in the event of any slowdowns or disruptions in ongoing efforts to upgrade Internet infrastructure in India.

The majority of our bookings are made through our Indian website and mobile offerings. According to Internet World Stats, India had 462 million Internet users as of December 2017. There can be no assurance that Internet penetration in India will increase in the future, as slowdowns or disruptions in upgrading efforts for infrastructure in India could reduce the rate of increase in the use of the Internet. As such, we may need to make additional investments in alternative distribution channels. Further, any slowdown or negative deviation in the anticipated increase in Internet penetration in India may adversely affect our business and results of operations.

Our large shareholders exercise significant influence over our company and may have interests that are different from those of our other shareholders.

As of May 31, 2018, MIHI LLC, Macquarie Corporate Holdings Pty Limited, Valiant Capital Management, L.P., Valiant Capital Management, LLC, and Apple Orange LLC, Noyac Path LLC, Periscope, LLC, Terrapin Partners Employee Partnership 3, LLC and Terrapin Partners Green Employee Partnership, LLC (collectively, the Terrapin Sponsors) and certain of their affiliated entities (including Nathan Leight), E-18 Limited, Capital18 Fincap Private Limited, Pandara Trust Scheme I, IDG Ventures India Fund II LLC, Intel Foundation, Reliance Capital Limited, Vertex Asia Fund Pte. Ltd., Rajasthan Trustee Company Pvt Ltd A/c SME Tech Fund RVCF Trust II and Fuh Hwa Securities Investment Trust Co., Ltd. beneficially own approximately 60.73% of the issued and outstanding shares of our company (or approximately 53.05% of the shares of our company, assuming the exercise or conversion of all of our outstanding warrants), based on information known to us or ascertained by us from public filings made by such shareholders. By virtue of such significant shareholdings, these shareholders have the ability to exercise significant influence over our company and our affairs and business, including the election of directors, the timing and payment of dividends, the adoption and amendments to our memorandum and articles of association, the approval of a merger or sale of substantially all of our assets and the approval of most other actions requiring the approval of our shareholders. The interests of these shareholders may be different from or conflict with the interests of our other shareholders and their influence may result in the delay or prevention of a change of management or control of our company, even if such a transaction may be beneficial to our other shareholders.

The loss of one or more of our key personnel could harm our business.

Our future success depends upon the continued contributions of our senior corporate management and other key employees. In particular, the contributions of Dhruv Shringi, our Chief Executive Officer, and Alok Vaish, our Chief Financial Officer, are critical to our overall management. We have entered into employment agreements with these individuals as well as other members of senior management, which contain non-compete provisions that extend for 18 months following the termination of such executive officer’s employment. If we cannot retain the services of these individuals or other key personnel, our business could be seriously harmed.

Our ability to attract, train and retain qualified employees is critical to our business and results of operations.

Our business and future success depends, to a significant extent, on our ability to attract and train new employees and to retain and motivate our existing employees. Competition remains intense for well-qualified employees in certain aspects of our business, including software engineers, developers, product management and development personnel with expertise in the online travel or search industry. Our industry is characterized by high demand and intense competition for talent. We may be required to increase our levels of employee compensation more rapidly than in the past to remain competitive in attracting the quality of employees that our business requires. If we do not succeed in attracting

17

well-qualified employees or retaining or motivating existing employees, our business and results of operations could be adversely affected.

Inaccurate information from suppliers of hotel room inventory may lead to customer complaints.

Our customers that purchase hotel room inventory online through our websites may rely on the description of the accommodation presented on such websites to ascertain the quality of amenities and services provided at the relevant accommodation. We receive information utilized in the accommodation description on our websites directly from the accommodation provider. To the extent that the information presented on our websites does not reflect the actual quality of amenities and services at the accommodation, we may face customer complaints that may have an adverse effect on our reputation and the likelihood of repeat customers, which in turn may adversely affect our business and results of operations.

There can be no assurance that our acquisition of the balance of ATB’s outstanding shares will be consummated in the anticipated timeframe, on the terms described herein, or at all, or that we will be able to successfully integrate any assets we acquire from ATB.

On August 4, 2017, we, through our subsidiary Yatra Online Private Limited, acquired a majority of the outstanding shares of ATB pursuant to the ATB Purchase Agreement for an upfront payment of approximately INR 510 million. The acquisition of the balance of ATB’s outstanding shares is expected to occur in the third quarter of the 2018 calendar year. Based on the terms of the ATB Purchase Agreement and management estimates, we expect the total purchase price to be between INR 1,469 million to INR 1,796 million. The acquisition of the remaining ATB shares will be financed through a combination of cash on hand and borrowings under our debt facility. However, we cannot assure you that any debt financing that we require to complete the acquisition of ATB’s outstanding shares will be available on terms acceptable to us, or at all, and there can be no assurances that we will consummate the purchase of ATB’s outstanding shares on the terms described herein, or at all. Failure to complete the acquisition of ATB’s remaining outstanding shares would prevent us from realizing the anticipated benefits of this acquisition. In addition, the market price of our ordinary shares may reflect various market assumptions as to whether we will complete the acquisition of ATB outstanding shares. Consequently, any delay or failure to complete the purchase could result in a significant change in the market price of our ordinary shares.

We may fail to realize all of the anticipated benefits of our Business Combination or our ATB acquisition.

The success of the Business Combination will depend, in part, on our ability to successfully manage and deploy the cash received upon the consummation of the Business Combination. Although we intend to use the cash received upon the consummation of the Business Combination to expand further our position in the Indian market and strengthen our leadership position in the markets for online travel services, there can be no assurance that we will be able to achieve our intended objectives or enhance our business.

The success of our acquisition of ATB will depend, in large part, on our ability to successfully integrate ATB’s technologies, operations and systems, which may be a complex, costly and time-consuming process. We may face additional integration challenges including:

· difficulties in achieving anticipated cost savings, synergies, business opportunities and growth prospects from the acquisition;

· difficulties in conforming standards, controls, procedures and accounting and other policies, business cultures and compensation structures;

· difficulties in the assimilation of employees; and

18

· difficulties in managing the expanded operations of a significantly larger company.

Any one of these factors could result in increased costs, decreases in the amount of expected revenues and diversion of management’s time and energy, which could adversely affect our business, financial condition and results of operations and result in us becoming subject to litigation. In addition, even if ATB is integrated successfully, the full anticipated benefits of this acquisition may not be realized, including the synergies, cost savings or sales or growth opportunities that are anticipated. These benefits may not be achieved within the anticipated time frame, or at all. Further, additional unanticipated costs may be incurred in the integration process. All of these factors could cause reductions in our earnings per share, decrease or delay the expected accretive effect of the acquisition and negatively impact the price of shares of our ordinary share. As a result, it cannot be assured that our acquisition of ATB will result in the realization of the full anticipated benefits.

We may be required to take write-downs or write-offs, restructuring and impairment or other charges that could have a significant negative effect on our financial condition, results of operations and share price, which could cause you to lose some or all of your investment.

We may be required to take write-down or write-offs of assets, restructure our operations, or incur impairment or other charges that could result in reporting losses. Even though these charges may be non-cash items and not have an immediate impact on our liquidity, the fact that charges of this nature are reported could contribute to negative market perceptions about our company or our securities. In addition, charges of this nature may cause our company to violate net worth or other covenants to which we may become subject. Accordingly, our shareholders could suffer a reduction in the value of their securities. Such shareholders are unlikely to have a remedy for such reduction in value unless they are able to successfully claim that the reduction was due to the breach by our officers or directors of a duty of care or other fiduciary duty owed to them, or if they are able to successfully bring a private claim under securities laws that this Report on Form 6-K contained an actionable material misstatement or material omission.

The Internal Revenue Service, or the IRS, may not agree to treat us as a foreign corporation for U.S. federal income tax purposes.

Although we are incorporated in the Cayman Islands, the IRS may assert that we should be treated as a U.S. corporation (and, therefore, a U.S. tax resident) for U.S. federal income tax purposes pursuant to Section 7874 of the Internal Revenue Code of 1986, as amended, or the Code. For U.S. federal income tax purposes, a corporation generally is considered a tax resident in the jurisdiction of its organization or incorporation. Because we are a Cayman Islands incorporated entity, we would generally be classified as a foreign corporation (and, therefore, a non-U.S. tax resident) under these rules. Section 7874 of the Code provides an exception under which a foreign incorporated entity may, in certain circumstances, be treated as a U.S. corporation for U.S. federal income tax purposes.

For our company to be treated as a foreign corporation for U.S. federal income tax purposes under Section 7874 of the Code, immediately after the Business Combination, either (i) the former stockholders of Terrapin must have owned (within the meaning of Section 7874 of the Code) less than 80% (by both vote and value) of our ordinary shares by reason of holding shares in Terrapin immediately prior to the Business Combination, or (ii) we must have substantial business activities in the Cayman Islands (taking into account the activities of our expanded affiliated group).

Based on the rules for determining share ownership under Section 7874 of the Code, we believe that the shareholders of Terrapin should be treated as having owned less than 80% of our ordinary shares after the Business Combination and that, therefore, we should be treated as a foreign corporation for U.S. federal income tax purposes, although no assurances can be given in this regard. If we were to be treated as a U.S. corporation, income we earned would become subject to U.S. taxation,

19

and the gross amount of any dividend payments to our non-U.S. shareholders could be subject to 30% U.S. withholding tax, depending on the application of any income tax treaty that might apply to reduce such withholding tax.