UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT

PURSUANT TO SECTION 13

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2017

Commission file number 001-37777

GRUPO SUPERVIELLE S.A. |

(Exact name of Registrant as specified in its charter) |

|

SUPERVIELLE GROUP S.A. |

(Translation of Registrant’s name into English) |

|

REPUBLIC OF ARGENTINA |

(Jurisdiction of incorporation or organization) |

|

Bartolomé Mitre 434, 5th Floor C1036AAH Buenos Aires Republic of Argentina |

(Address of principal executive offices) |

|

Alejandra Naughton Bartolomé Mitre 434, 5th Floor C1036AAH Buenos Aires Republic of Argentina Tel: 54-11-4340-3053 Email: Alejandra.Naughton@supervielle.com.ar |

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each Class |

| Name of each Exchange on which Registered |

American Depositary Shares, each representing 5 Class B shares of Grupo Supervielle S.A. |

| New York Stock Exchange |

Class B shares of Grupo Supervielle S.A. |

| New York Stock Exchange* |

*Not for trading, but only in connection with the registration of American Depositary Shares pursuant to the requirements of the New York Stock Exchange.

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2017 was:

Title of class |

| Number of shares outstanding |

Class B ordinary shares, nominal value Ps.1.00 per share |

| 329,984,134 |

Class A ordinary shares, nominal value Ps.1.00 per share |

| 126,738,188 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

x Yes o No

If this report is an annual or transitional report, indicate by check mark if the registrant is not required to file reports pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934.

o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days:

x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Not applicable.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated Filer x |

| Accelerated Filer o |

| Non-Accelerated Filer o |

| Emerging Growth Company o |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP o |

| IFRS o |

| Other x |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

o Item 17 x Item 18

If this is an Annual Report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o Yes x No

1 | ||

|

|

|

1 | ||

|

|

|

1 | ||

|

|

|

1 | ||

|

|

|

6 | ||

|

|

|

6 | ||

|

|

|

6 | ||

|

|

|

32 | ||

|

|

|

37 | ||

|

|

|

41 | ||

|

|

|

136 | ||

|

|

|

137 | ||

|

|

|

158 | ||

|

|

|

158 | ||

|

|

|

205 | ||

|

|

|

213 | ||

|

|

|

213 | ||

|

|

|

214 | ||

|

|

|

215 | ||

|

|

|

216 | ||

|

|

|

216 | ||

|

|

|

239 | ||

|

|

|

239 | ||

|

|

|

240 | ||

|

|

|

242 | ||

|

|

|

243 | ||

|

|

|

243 | ||

|

|

|

245 | ||

|

|

|

246 | ||

|

|

|

247 | ||

|

|

|

247 | ||

|

|

|

247 | ||

|

|

|

254 | ||

|

|

|

254 | ||

|

|

|

256 | ||

|

|

|

263 | ||

|

|

|

263 | ||

|

|

|

263 | ||

|

|

|

263 | ||

|

|

|

263 |

269 | ||

|

|

|

269 | ||

|

|

|

269 | ||

|

|

|

269 | ||

|

|

|

269 | ||

|

|

|

270 | ||

|

|

|

Material Modifications to the Rights of Security Holders and Use of Proceeds | 270 | |

|

|

|

270 | ||

|

|

|

272 | ||

|

|

|

272 | ||

|

|

|

272 | ||

|

|

|

273 | ||

|

|

|

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 273 | |

|

|

|

273 | ||

|

|

|

273 | ||

|

|

|

276 | ||

|

|

|

276 | ||

|

|

|

276 | ||

|

|

|

277 |

CERTAIN DEFINED TERMS AND CONVENTIONS

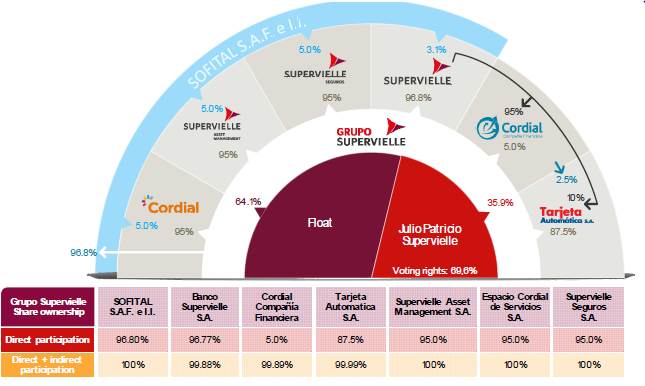

In this annual report, we use the terms “we,” “us,” “our” and the “Group” to refer to Grupo Supervielle S.A. and its consolidated subsidiaries, including Banco Supervielle S.A., unless otherwise indicated. References to “Grupo Supervielle” mean Grupo Supervielle S.A. References to the “Bank” mean Banco Supervielle S.A. and its consolidated subsidiaries. References to “Tarjeta” mean Tarjeta Automática S.A. References to “Cordial Microfinanzas” mean Cordial Microfinanzas S.A. References to “SAM” mean Supervielle Asset Management S.A. References to “Adval” mean Adval S.A. References to “Sofital” mean Sofital S.A.F.e I.I. References to “CCF” mean Cordial Compañía Financiera S.A. References to “Supervielle Seguros” mean Supervielle Seguros S.A. References to “Espacio Cordial” or “Cordial Servicios” mean Espacio Cordial Servicios S.A. References to “Viñas del Monte” mean Viñas del Monte S.A.

References to “Class B shares” refer to shares of our Class B common stock, all with a par value of Ps.1.00 per share and references to “ADSs” are to American depositary shares, each representing five Class B shares, except where the context requires otherwise.

The term “Argentina” refers to the Republic of Argentina. The terms “Argentine government” or the “government” refers to the federal government of Argentina, the term “Central Bank” refers to the Banco Central de la República Argentina, or the Argentine Central Bank, and the term “CNV” refers to the Argentine Comisión Nacional de Valores, or the Argentine securities regulator. “U.S. GAAP” refers to generally accepted accounting principles in the United States of America (“United States” or “U.S.”), “Argentine GAAP” refers to generally accepted accounting principles in Argentina and “Argentine Banking GAAP” refers to the accounting rules of the Central Bank. The term “GDP” refers to gross domestic product and all references in this annual report to GDP growth are to real GDP growth, the term “CPI” refers to the consumer price index and the term “WPI” refers to the wholesale price index. The term “customers” refers to individuals or entities that have at least one of our products without any requirement of customer activity during any time period. The term “active customer” refers to customers that had activity in the previous 90 days. Unless the context otherwise requires, the term “financial institutions” refers to institutions regulated by the Central Bank. The term “Argentine banks” refers to banks that operate in Argentina. The term “Argentine private banks” refers to banks that are not controlled or owned by the Argentine federal government or any Argentine provincial, municipality or city government. The term “private domestically-owned banks” refers to private banks that are controlled by Argentine shareholders. For information up to December 31, 2017, the term “small businesses” refers to individuals and businesses with annual sales of up to Ps.40.0 million, the term “SMEs” refers to individuals and businesses with annual sales over Ps.40.0 million and below Ps.200.0 million, the term “middle-market companies” refers to companies with annual sales over Ps.200.0 million and below Ps.1.0 billion and the term “large corporates” refers to companies with annual sales over Ps.1.0 billion. For information since January 1, 2018, the term “small businesses” refers to individuals and businesses with annual sales up to Ps.70.0 million, the term “SMEs” refers to individuals and businesses with annual sales over Ps.70.0 million and below Ps.550.0 million, the term “middle-market companies” refers to companies with annual sales over Ps.550.0 million and below Ps.2.0 billion amd the term “large corporates” refers to companies with annual sales over Ps.2.0 billion. The term “ROAE” refers to return on average shareholders’ equity. ROAE is frequently used by financial institutions as a benchmark to measure profitability compared to peers but not as a benchmark to determine returns for investors, which is affected by multiple factors that ROAE does not consider.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Statements

We maintain our financial books and records in Pesos and prepare our consolidated financial statements in Argentina in conformity with Argentine Banking GAAP, as these are the rules and regulations applied by the Bank, our main subsidiary. Argentine Banking GAAP differs in certain significant respects from U.S. GAAP and from Argentine GAAP. Our consolidated financial statements as of December 31, 2017 and 2016 and for each of the three years ended December 31, 2017, 2016 and 2015 have been audited, as stated in the report appearing herein, and are included in this annual report and referred to as our “audited consolidated financial statements.” Note 35 to our audited consolidated financial statements provides a description of the principal differences between Argentine

Banking GAAP and U.S. GAAP, as they relate to us, and a reconciliation to U.S. GAAP of net income and shareholders’ equity as of December 31, 2017 and 2016, and for the years ended December 31, 2017, 2016 and 2015. Unless otherwise indicated, all financial information of our company included in this annual report is stated on a consolidated basis under Argentine Banking GAAP. Our audited consolidated financial statements as of December 31, 2017 have been approved by our ordinary and extraordinary shareholders’ meeting held on April 24, 2018.

Currencies and Rounding

The terms “U.S. dollar” and “U.S. dollars” and the symbol “U.S.$” refer to the legal currency of the United States. The terms “Peso” and “Pesos” and the symbol “Ps.” refer to the legal currency of Argentina.

We have translated certain of the Peso amounts contained in this annual report into U.S. dollars for convenience purposes only. Unless otherwise indicated, the rate used to translate such amounts as of December 31, 2017 was Ps.18.7742 to U.S.$1.00, which was the reference exchange rate reported by the Central Bank for U.S. dollars as of December 29, 2017. The Federal Reserve Bank of New York does not report a noon buying rate for Pesos. The U.S. dollar equivalent information presented in this annual report is provided solely for the convenience of investors and should not be construed as implying that the Peso amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate. See “Exchange Rates” for more detailed information regarding the translation of Pesos into U.S. dollars.

Certain figures included in this annual report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that precede them.

Market Share and Other Information

We make statements in this annual report about our competitive position and market share in, and the market size of, the Argentine banking industry. We have made these statements on the basis of statistics and other information derived from the Central Bank’s publications and other third-party sources that we believe are reliable. Although we have no reason to believe any of this information or these reports are inaccurate in any material respect, we have not independently verified the competitive position, market share and market size or market growth data provided by third parties or by industry or general publications.

In January 2007, the Instituto Nacional de Estadísticas y Censos (the National Statistics and Census Institute, or “INDEC”), which is the only institution in Argentina with the statutory authority to produce official nationwide statistics, modified the methodology used to calculate certain of its indices. On January 8, 2016, the Macri administration issued Decree No. 55/2016 declaring a state of administrative emergency with respect to the national statistical system and the INDEC until December 31, 2016. During this state of emergency, the INDEC suspended the publication of certain statistical data until it completed a reorganization of its technical and administrative structure capable of producing sufficient and reliable statistical information. Following the implementation of certain methodological reforms and the adjustment of macroeconomic statistics on the basis of these reforms, on June 15, 2016, the INDEC published the INDEC Report including revised GDP data for the years 2004 through 2015. As of the date of this annual report, the INDEC has resumed publishing certain revised data, including GDP, foreign trade, poverty and balance of payment statistics. As of the date of this annual report, the Argentine government has not renewed the state of administrative emergency declared by means of the Decree No. 55/2016.

FORWARD-LOOKING STATEMENTS

This annual report contains estimates and forward-looking statements, principally in “Item 3.D Risk Factors”, “Item 5.A Operating Results”, and “Item 4.B Business overview.” We have based these forward-looking statements largely on our current beliefs, expectations and projections about future courses of action, events and financial trends affecting our business. Many important factors, in addition to those discussed elsewhere in this annual report, could cause our actual results to differ substantially from those anticipated in our forward-looking statements, including, among others:

(i) changes in general economic, financial, business, political, legal, social or other conditions in Argentina or elsewhere in Latin America or changes in either developed or emerging markets;

(ii) changes in capital markets in general that may affect policies or attitudes toward lending to or investing in Argentina or Argentine companies, including expected or unexpected turbulence or volatility in domestic and international financial markets;

(iii) changes in regional, national and international business and economic conditions, including inflation;

(iv) changes in interest rates and the cost of deposits, which may, among other things, affect margins;

(v) unanticipated increases in financing or other costs or the inability to obtain additional debt or equity financing on attractive terms, which may limit our ability to fund existing operations and to finance new activities;

(vi) changes in government regulation, including tax and banking regulations;

(vii) adverse legal or regulatory disputes or proceedings;

(viii) the interpretation by judicial courts of the new Argentine Civil and Commercial Code;

(ix) credit and other risks of lending, such as increases in defaults by borrowers;

(x) fluctuations and declines in the value of Argentine public debt;

(xi) increased competition in the banking, financial services, credit card services, asset management and related industries;

(xii) a loss of market share by any of our main businesses;

(xiii) increase in the allowances for loan losses;

(xiv) technological changes or an inability to implement new technologies, changes in consumer spending and saving habits;

(xv) ability to implement our business strategy;

(xvi) fluctuations in the exchange rate of the Peso; and

(xvii) other factors discussed under “Item 3.D Risk Factors” in this annual report.

The words “believe,” “may,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “forecast” and similar words are intended to identify forward-looking statements. Forward-looking statements include information concerning our possible or assumed future results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements speak only as of the date they were made, and we do not undertake any

obligation to update publicly or to revise any forward-looking statements after we distribute this annual report because of new information, future events or other factors, except as required by applicable law. In light of the risks and uncertainties described above, the forward-looking events and circumstances discussed in this annual report might not occur and do not constitute guarantees of future performance. Because of these uncertainties, you should not make any investment decisions based on these estimates and forward-looking statements.

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3.A. Selected Financial Data

The following tables present selected consolidated financial data for us for each of the periods indicated. You should read this information in conjunction with our audited consolidated financial statements and related notes beginning on page F-1, and the information under “Item 5.A Operating Results” included elsewhere in this annual report.

Our audited consolidated financial statements do not include any effect of inflation other than the adjustments to non-monetary assets through February 28, 2003.

The selected consolidated financial data as of December 31, 2017 and 2016 and for the three years in the period ended December 31, 2017 has been derived from our audited consolidated financial statements included in this annual report. The selected consolidated financial data as of December 31, 2015, 2014 and 2013 and for the years ended December 31, 2014 and 2013 has been derived from our audited consolidated financial statements, which are not included in this annual report. Our audited consolidated financial statements as of December 31, 2017 and 2016 and for the three years ended December 31, 2017 have been audited by Price Waterhouse & Co. S.R.L., member firm of the PricewaterhouseCoopers network, independent accountants, whose audit report is included elsewhere in this annual report.

We maintain our financial books and records in Pesos and prepare and publish our audited consolidated financial statements in Argentina in conformity with Argentine Banking GAAP as these are the rules and regulations applied by the Bank, our main subsidiary, which differ in certain significant respects from U.S. GAAP, and from Argentine GAAP. Note 35 to our audited consolidated financial statements provides a description of the principal differences between Argentine Banking GAAP and U.S. GAAP, as they relate to us, and a reconciliation to U.S. GAAP of net income and shareholders’ equity as of December 31, 2017 and 2016 and for the years ended December 31, 2017, 2016 and 2015.

On February 12, 2014, the Central Bank, through Communication “A” 5541, established the general guidelines towards conversion to International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) for preparing financial statements of the entities under its supervision with the temporary exception of paragraph 5.5 “Impairment” of IFRS 9 “Financial Instruments” (IFRS as issued by the IASB as adopted by the Central Bank). Note 33 to our audited consolidated financial statements provides a description of the principal differences between Argentine Banking GAAP and IFRS, as they relate to us, and a reconciliation to IFRS of shareholders’ equity as of December 31, 2017 and January 1, 2017 and of net income for the year ended December 31, 2017.

Solely for convenience, Peso amounts as of and for the year ended December 31, 2017 have been translated into U.S. dollars. The rate used to translate such amounts as of December 31, 2017 was Ps.18.7742 to U.S.$1.00, which was the reference exchange rate reported by the Central Bank for U.S. dollars as of December 29, 2017. U.S. dollar equivalent information should not be construed to imply that the Peso amounts represent, or could have been or could be converted into, U.S. dollars at such rates or any other rate.

|

| Grupo Supervielle S.A. |

| ||||||||||||||||

|

| Year ended December 31, |

| ||||||||||||||||

|

| 2017 |

| 2017 |

| 2016 |

| 2015 |

| 2014 |

| 2013 |

| ||||||

|

| (in thousands of Pesos or U.S. dollars, as indicated) |

| ||||||||||||||||

Consolidated Income Statement Data |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Argentine Banking GAAP: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Financial income(1) |

| U.S.$ | 825,317 |

| Ps. | 15,494,671 |

| Ps. | 10,794,579 |

| Ps. | 6,741,744 |

| Ps. | 4,751,352 |

| Ps. | 3,045,380 |

|

Financial expenses(2) |

| (329,936 | ) | (6,194,288 | ) | (4,866,525 | ) | (3,386,050 | ) | (2,464,526 | ) | (1,303,916 | ) | ||||||

Gross financial margin |

| 495,381 |

| 9,300,383 |

| 5,928,054 |

| 3,355,694 |

| 2,286,826 |

| 1,741,464 |

| ||||||

Loan loss provisions |

| (96,951 | ) | (1,820,169 | ) | (1,057,637 | ) | (543,844 | ) | (356,509 | ) | (350,535 | ) | ||||||

Services fee income |

| 264,899 |

| 4,973,272 |

| 3,527,516 |

| 2,835,708 |

| 2,162,820 |

| 1,765,659 |

| ||||||

Services fee expenses |

| (79,676 | ) | (1,495,848 | ) | (1,080,660 | ) | (778,492 | ) | (610,341 | ) | (421,587 | ) | ||||||

Income from insurance activities |

| 25,517 |

| 479,061 |

| 606,143 |

| 175,947 |

| 8,513 |

| — |

| ||||||

Administrative expenses |

| (446,923 | ) | (8,390,622 | ) | (6,060,281 | ) | (4,261,402 | ) | (3,013,842 | ) | (2,287,201 | ) | ||||||

Income from financial transactions |

| 162,248 |

| 3,046,077 |

| 1,863,135 |

| 783,611 |

| 477,467 |

| 447,800 |

| ||||||

Miscellaneous income |

| 29,074 |

| 545,842 |

| 429,884 |

| 367,165 |

| 190,005 |

| 129,245 |

| ||||||

Miscellaneous losses |

| (20,053 | ) | (376,480 | ) | (458,946 | ) | (213,427 | ) | (91,761 | ) | (95,734 | ) | ||||||

Non-controlling interests result |

| (314 | ) | (5,897 | ) | (22,166 | ) | (16,079 | ) | (13,707 | ) | (10,556 | ) | ||||||

Income before income tax |

| 170,955 |

| 3,209,542 |

| 1,811,907 |

| 921,270 |

| 562,004 |

| 470,755 |

| ||||||

Income tax |

| (41,146 | ) | (772,483 | ) | (500,603 | ) | (247,161 | ) | (199,084 | ) | (97,765 | ) | ||||||

Net income for the fiscal period |

| 129,809 |

| 2,437,059 |

| 1,311,304 |

| 674,109 |

| 362,920 |

| 372,990 |

| ||||||

U.S. GAAP: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Net income |

| 88,812 |

| 1,697,481 |

| 1,025,868 |

| 676,076 |

| 301,514 |

| 398,815 |

| ||||||

|

| Grupo Supervielle S.A. |

| ||||||||||||||||

|

| As of December 31, |

| ||||||||||||||||

|

| 2017 |

| 2017 |

| 2016 |

| 2015 |

| 2014 |

| 2013 |

| ||||||

|

| (in thousands of Pesos or U.S. dollars, as indicated) |

| ||||||||||||||||

Consolidated Balance Sheet Data |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Argentine Banking GAAP: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Cash and due from banks |

| U.S.$ | 592,807 |

| Ps. | 11,129,475 |

| Ps. | 8,166,132 |

| Ps. | 6,808,591 |

| Ps. | 3,649,084 |

| Ps. | 2,662,592 |

|

Government and corporate securities |

| 817,400 |

| 15,346,036 |

| 2,360,044 |

| 931,881 |

| 1,008,080 |

| 483,990 |

| ||||||

Loans: |

| 2,927,122 |

| 54,954,373 |

| 34,896,509 |

| 20,148,261 |

| 14,596,580 |

| 11,292,289 |

| ||||||

to the non-financial public sector |

| 1,737 |

| 32,607 |

| 4,306 |

| 8,778 |

| 12,666 |

| 15,699 |

| ||||||

to the financial sector |

| 22,337 |

| 419,366 |

| 473,414 |

| 181,734 |

| 3,514 |

| 36,029 |

| ||||||

To the non-financial private sector and foreign residents: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Overdrafts |

| 192,650 |

| 3,616,843 |

| 3,110,097 |

| 1,634,870 |

| 993,284 |

| 679,085 |

| ||||||

Promissory Notes(3) |

| 825,316 |

| 15,494,647 |

| 9,426,568 |

| 5,984,777 |

| 5,583,705 |

| 4,472,631 |

| ||||||

Mortgage loans |

| 82,548 |

| 1,549,765 |

| 78,057 |

| 50,032 |

| 69,554 |

| 83,660 |

| ||||||

Automobile and other secured loans |

| 16,710 |

| 313,724 |

| 65,076 |

| 104,469 |

| 168,603 |

| 225,901 |

| ||||||

Personal loans |

| 789,283 |

| 14,818,163 |

| 9,916,776 |

| 6,018,601 |

| 3,631,840 |

| 2,970,622 |

| ||||||

Credit card loans |

| 424,308 |

| 7,966,037 |

| 6,678,578 |

| 5,677,922 |

| 3,688,328 |

| 2,410,111 |

| ||||||

Other |

| 623,635 |

| 11,708,248 |

| 5,595,356 |

| 953,574 |

| 793,192 |

| 684,219 |

| ||||||

Accrued Interest, adjustments and exchange rate differences receivable |

| 74,450 |

| 1,397,740 |

| 773,961 |

| 428,600 |

| 357,844 |

| 257,689 |

| ||||||

Documented interest |

| (44,161 | ) | (829,086 | ) | (324,795 | ) | (277,488 | ) | (287,605 | ) | (200,345 | ) | ||||||

Other unapplied charges |

| (4 | ) | (83 | ) | (1,738 | ) | (295 | ) | (1,322 | ) | (1,012 | ) | ||||||

Allowances |

| (81,686 | ) | (1,533,598 | ) | (899,147 | ) | (617,313 | ) | (417,023 | ) | (342,000 | ) | ||||||

Other receivables from financial transactions |

| 349,490 |

| 6,561,396 |

| 3,772,736 |

| 2,461,813 |

| 2,263,612 |

| 1,742,721 |

| ||||||

|

| Grupo Supervielle S.A. |

| ||||||||||||||||

|

| As of December 31, |

| ||||||||||||||||

|

| 2017 |

| 2017 |

| 2016 |

| 2015 |

| 2014 |

| 2013 |

| ||||||

|

| (in thousands of Pesos or U.S. dollars, as indicated) |

| ||||||||||||||||

Receivables from financial leases |

| 134,184 |

| 2,519,201 |

| 1,527,855 |

| 1,074,977 |

| 583,846 |

| 511,880 |

| ||||||

Other assets |

| 184,338 |

| 3,460,797 |

| 2,482,766 |

| 1,620,294 |

| 1,139,992 |

| 724,659 |

| ||||||

Total assets |

| 5,005,341 |

| 93,971,278 |

| 53,206,042 |

| 33,045,817 |

| 23,241,194 |

| 17,418,131 |

| ||||||

Average Assets(4) |

| 3,707,170 |

| 69,599,142 |

| 41,467,412 |

| 26,961,165 |

| 20,066,019 |

| 14,645,841 |

| ||||||

Liabilities and shareholders’ equity |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Deposits: |

| U.S.$ | 3,008,758 |

| Ps. | 56,487,027 |

| Ps. | 35,897,864 |

| Ps. | 23,716,577 |

| Ps. | 16,892,730 |

| Ps. | 12,819,178 |

|

Non-financial public sector |

| 328,731 |

| 6,171,661 |

| 2,587,253 |

| 1,182,559 |

| 1,441,506 |

| 1,018,547 |

| ||||||

Financial sector |

| 836 |

| 15,702 |

| 9,326 |

| 250,981 |

| 150,817 |

| 100,973 |

| ||||||

Non-financial private sector and foreign residents |

| 2,679,191 |

| 50,299,664 |

| 33,301,285 |

| 22,283,037 |

| 15,300,407 |

| 11,699,658 |

| ||||||

Checking accounts |

| 302,532 |

| 5,679,805 |

| 4,361,405 |

| 3,042,376 |

| 2,622,055 |

| 2,034,593 |

| ||||||

Savings accounts |

| 1,575,513 |

| 29,578,994 |

| 13,205,937 |

| 7,753,696 |

| 5,352,593 |

| 3,640,102 |

| ||||||

Time deposits |

| 693,233 |

| 13,014,886 |

| 11,677,322 |

| 10,034,025 |

| 6,651,006 |

| 5,426,409 |

| ||||||

Investment accounts |

| 13,582 |

| 255,000 |

| 375,000 |

| 664,900 |

| 75,750 |

| 144,100 |

| ||||||

Other |

| 94,330 |

| 1,770,979 |

| 3,681,621 |

| 788,040 |

| 599,003 |

| 454,454 |

| ||||||

Other liabilities from financial transactions and other miscellaneous liabilities |

| 1,189,289 |

| 22,327,956 |

| 10,273,230 |

| 6,884,700 |

| 4,586,728 |

| 3,204,585 |

| ||||||

Non-controlling interests |

| 612 |

| 11,497 |

| 103,397 |

| 70,830 |

| 54,750 |

| 41,960 |

| ||||||

Total liabilities |

| 4,198,660 |

| 78,826,480 |

| 46,274,491 |

| 30,672,107 |

| 21,534,208 |

| 16,065,723 |

| ||||||

Average Liabilities(4) |

| 3,196,853 |

| 60,018,357 |

| 36,480,913 |

| 24,866,415 |

| 18,464,430 |

| 14,433,187 |

| ||||||

Shareholders’ equity |

| 806,681 |

| 15,144,798 |

| 6,931,551 |

| 2,373,710 |

| 1,706,986 |

| 1,352,408 |

| ||||||

Total liabilities and shareholders’ equity |

| 5,005,341 |

| 93,971,278 |

| 53,206,042 |

| 33,045,817 |

| 23,241,194 |

| 17,418,131 |

| ||||||

Average shareholders’ equity(4) |

| 510,317 |

| 9,580,785 |

| 4,986,499 |

| 2,094,750 |

| 1,601,589 |

| 1,212,654 |

| ||||||

U.S. GAAP: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Total assets |

| 5,086,829 |

| 95,501,145 |

| 54,513,168 |

| 35,122,426 |

| 26,166,663 |

| 19,531,312 |

| ||||||

Total liabilities |

| 4,346,180 |

| 81,596,047 |

| 48,014,492 |

| 32,858,882 |

| 24,626,175 |

| 18,247,809 |

| ||||||

Total shareholders’ equity |

| 740,649 |

| 13,905,098 |

| 6,498,676 |

| 2,263,544 |

| 1,540,488 |

| 1,283,503 |

| ||||||

(1) Includes gains related to non-deliverable forward (“NDF”) hedging transactions, which totaled Ps.0 million, Ps.0 million, Ps.228.2 million, Ps.0, and Ps.86.9 million, as of December 31, 2017, 2016, 2015, 2014 and 2013, respectively.

(2) Includes expenses related to NDF hedging transactions, which totaled Ps.71.3 million, Ps. 39.0 million, Ps.0, Ps.96.2 million, and Ps.0, as of December 31, 2017, 2016, 2015, 2014 and 2013, respectively.

(3) Consists of unsecured checks and accounts receivable deriving from factoring transactions, and unsecured corporate loans which totaled Ps.5,238.4 million, Ps.3,102.8 million, Ps.2,399.3 million, Ps.1,547.5 million and Ps.979.9 million as of December 31, 2017, 2016, 2015, 2014 and 2013, respectively.

(4) Calculated on a daily basis.

|

| Grupo Supervielle S.A. |

| ||||||||

|

| Year ended December 31, |

| ||||||||

|

| 2017 |

| 2016 |

| 2015 |

| 2014 |

| 2013 |

|

Selected Consolidated Ratios: |

|

|

|

|

|

|

|

|

|

|

|

Argentine Banking GAAP: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest margin(1) |

| 19.1 | % | 20.6 | % | 18.1 | % | 17.4 | % | 16.4 | % |

Net financial margin(2) |

| 17.8 | % | 19.2 | % | 16.4 | % | 15.1 | % | 15.8 | % |

Net fee income ratio(3) |

| 29.8 | % | 34.0 | % | 40.0 | % | 40.6 | % | 43.6 | % |

Efficiency ratio(4) |

| 63.3 | % | 67.5 | % | 76.2 | % | 78.3 | % | 74.1 | % |

Fee income as a percentage of administrative expense |

| 47.2 | % | 50.4 | % | 52.4 | % | 51.8 | % | 58.8 | % |

Return on average equity(5) |

| 25.4 | % | 26.3 | % | 32.2 | % | 22.7 | % | 30.8 | % |

Return on average assets(6) |

| 3.5 | % | 3.2 | % | 2.5 | % | 1.8 | % | 2.5 | % |

Cost/Assets |

| 12.1 | % | 14.6 | % | 15.8 | % | 15.0 | % | 15.6 | % |

Basic earnings per share (in Pesos)(7) |

| 6.20 |

| 4.10 |

| 4.42 |

| 2.92 |

| 3.00 |

|

Diluted earnings per share (in Pesos) |

| 6.20 |

| 4.10 |

| 4.42 |

| 2.92 |

| 3.00 |

|

Basic earnings per share (in U.S.$) |

| 0.33 |

| 0.26 |

| 0.34 |

| 0.34 |

| 0.46 |

|

Diluted earnings per share (in U.S.$) |

| 0.33 |

| 0.26 |

| 0.34 |

| 0.34 |

| 0.46 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Liquidity |

|

|

|

|

|

|

|

|

|

|

|

Loans as a percentage of total deposits(8) |

| 104.5 | % | 104.0 | % | 92.2 | % | 92.4 | % | 94.8 | % |

Loans as a percentage of total assets(8) |

| 62.8 | % | 70.2 | % | 66.1 | % | 67.1 | % | 69.8 | % |

Liquid assets as a percentage of total deposits(9) |

| 45.9 | % | 27.0 | % | 32.6 | % | 26.5 | % | 24.5 | % |

LCR Pro forma(14) |

| 113.9 | % | 128.0 | % | 113.1 | % | 71.0 | % | N/A |

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital |

|

|

|

|

|

|

|

|

|

|

|

Total equity as a percentage of total assets |

| 16.1 | % | 13.0 | % | 7.2 | % | 7.3 | % | 7.8 | % |

Average equity as a percentage of average assets |

| 13.8 | % | 12.0 | % | 7.8 | % | 8.0 | % | 8.3 | % |

Total liabilities as a multiple of total shareholders’ equity |

| 5.2 |

| 6.7 |

| 12.9 |

| 12.6 |

| 11.9 |

|

Tangible equity ratio(10) |

| 15.8 | % | 12.6 | % | 6.5 | % | 6.5 | % | 6.7 | % |

Regulatory capital/ Risk weighted assets(11) |

| 13.9 | % | 12.5 | % | 8.7 | % | 8.9 | % | 9.0 | % |

Regulatory capital/ Risk weighted assets Pro forma |

| 19.6 | % | 13.8 | % | 8.7 | % | 8.9 | % | 9.0 | % |

Risk weighted assets/total assets |

| 80.1 | % | 92.4 | % | 103.8 | % | 113.3 | % | 113.3 | % |

Tier 1 Capital / Risk weighted assets(12) |

| 12.6 | % | 10.9 | % | 6.7 | % | 6.9 | % | 6.7 | % |

Tier 1 Pro forma(13) |

| 18.4 | % | 12.3 | % | 6.7 | % | 6.9 | % | 6.7 | % |

|

|

|

|

|

|

|

|

|

|

|

|

Asset Quality |

|

|

|

|

|

|

|

|

|

|

|

Non-performing loans as a percentage of total loans(15) |

| 2.8 | % | 2.8 | % | 3.2 | % | 3.0 | % | 3.0 | % |

Allowances as a percentage of total loans |

| 2.6 | % | 2.4 | % | 2.9 | % | 2.7 | % | 2.9 | % |

Cost of risk(16) |

| 4.2 | % | 4.0 | % | 3.1 | % | 2.9 | % | 3.8 | % |

Allowances as a percentage of non-performing loans(15) |

| 91.8 | % | 87.1 | % | 89.7 | % | 88.9 | % | 94.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

Other Data |

|

|

|

|

|

|

|

|

|

|

|

Dividends paid to the common shares (Ps. million)(17) |

| 243.7 |

| 65.5 |

| 19.2 |

| 2.7 |

| 4.5 |

|

Dividends paid to the preferred shares (Ps. million) |

| — |

| — |

| 6.0 |

| 4.7 |

| 3.9 |

|

Dividends per common share (Ps.) |

| 0.5 |

| 0.2 |

| 0.1 |

| 0.0 |

| 0.0 |

|

Dividends per preferred share (Ps.)(18) |

| — |

| — |

| 1.9 |

| 2.9 |

| 2.4 |

|

Employees |

| 5,320 |

| 4,982 |

| 4,843 |

| 4,579 |

| 4,570 |

|

Branches and sales points(19) |

| 326 |

| 320 |

| 325 |

| 322 |

| 353 |

|

ATMs and self-service terminals(19) |

| 704 |

| 661 |

| 649 |

| 632 |

| 588 |

|

(1) Net interest income divided by average interest-earning assets.

(2) Gross financial margin divided by average interest-earning assets.

(3) Net services fee income divided by the sum of gross financial margin and net services fee income.

(4) Administrative expenses divided by the sum of gross financial margin, services fee income and expenses and income from insurance activities.

(5) Net income divided by average shareholders’ equity, calculated on a daily basis and measured in local currency.

(6) Net income divided by average assets, calculated on a daily basis and measured in local currency.

(7) Basic earnings per share (in Pesos) are based upon the weighted average of Grupo Supervielle’s outstanding shares, which were Ps.392.8 million for the year ended December 31, 2017, Ps.319.8 million for the year ended December 31, 2016, Ps.151.8 million for the year ended

December 31, 2015, Ps.122.9 million for the year ended December 31, 2014 and Ps.122.9 million for the year ended December 31, 2013. In January 2016, the stock of preferred shares was converted to Class B shares.

(8) Loans include loans and receivables from financial leases.

(9) Liquid assets include cash, securities issued by the Central Bank (Las Letras del Banco Central (LEBAC) and NOBACs) and other government securities.

(10) (Total equity - Intangible assets)/(Total assets - Intangible assets). Intangible assets as of December 31, 2017, 2016, 2015, 2014 and 2013 amounted to Ps.324.5 million, Ps.285.5 million, Ps.252.0 million, Ps.216.0 million and Ps.197.0 million, respectively.

(11) Regulatory capital divided by risk weighted assets taking into account operational and market risk since 2013. This ratio applies only to the Bank and CCF on a consolidated basis and does not include the liquidity held at the holding company level.

(12) Tier 1 capital divided by risk weighted assets taking into account credit risk, operational and market risk since 2013.

(13) As of December 31, 2017 and December 31, 2016, Tier 1 Pro Forma includes Ps.4.3 billion and Ps.805.0 million, respectively, from the IPO proceeds retained at the Grupo Supervielle level, which are available for further capital injections in its subsidiaries.

(14) LCR ratio includes the net liquidity held at the holding company level.

(15) Non-performing loans include all principal amounts of loans to borrowers classified as “3-with problems/medium risk”, “4-high risk of insolvency/high risk”, “5-uncollectible”, and “6-uncollectible, classified as such under regulatory requirements” under the Central Bank loan classification system. See “ Item 4.D Property, plants and equipment—Selected Statistical Information—Loans and Financings—Portfolio Classification.”

(16) Loan Loss Provisions divided by Average Loans.

(17) Dividend in relation with the result of each year, declared and paid in the following year.

(18) In January 2016, all shares of preferred stock were converted to Class B shares. No dividends on the preferred shares were paid in 2017 or 2016.

(19) As of the date of this annual report, we have 340 branches and aales points and 714 ATMs and self-service terminals.

Exchange Rates

From April 1, 1991 until the end of 2001, Law No. 23,928 (the “Convertibility Law”) established a regime under which the Central Bank was obliged to sell U.S. dollars at a fixed rate of one Peso per U.S. dollar. On January 6, 2002, the Argentine Congress enacted Law No. 25,561 (as amended and supplemented, the “Public Emergency Law”), formally ending the regime of the Convertibility Law, abandoning over ten years of U.S. dollar-Peso parity and eliminating the requirement that the Central Bank’s reserves in gold, foreign currency and foreign currency denominated debt be at all times equivalent to 100% of the monetary base.

The Public Emergency Law, which ceased to be in effect on December 31, 2017, granted the Argentine government the power to set the exchange rate between the Peso and foreign currencies and to issue regulations related to the foreign exchange market. The state of emergency on social matters was further extended until December 31, 2019. Following a brief period during which the Argentine government established a temporary dual exchange rate system, pursuant to the Public Emergency Law, the Peso has been allowed to float freely against other currencies since February 2002, although the Central Bank has the power to intervene by buying and selling foreign currency for its own account, a practice in which it engages on a regular basis.

From 2011 to 2015, the Argentine government increased controls on exchange rates and the transfer of funds into and out of Argentina. With the tightening of exchange controls beginning in late 2011, in particular with the introduction of measures that allowed limited access to foreign currency by private companies and individuals (such as requiring an authorization of AFIP to access the foreign currency exchange market), the implied exchange rate, as reflected in the quotations for Argentine securities that trade in foreign markets, compared to the corresponding quotations in the local market, increased significantly over the official exchange rate. Most foreign exchange restrictions were lifted in December 2015, May 2016 and August 2016, reestablishing Argentine residents’ rights to purchase and remit outside of Argentina foreign currency with no maximum amount and without specific allocation or the need to obtain prior approval. As a result, since December 2015 the substantial spread between the official exchange rate and the implicit exchange rate derived from securities transactions has substantially decreased.

After several years of moderate variations in the nominal exchange rate, in 2012 the Peso lost approximately 14.0% of its value with respect to the U.S. dollar. This was followed in 2013 and 2014 by a devaluation of the Peso with respect to the U.S. dollar that exceeded 30.0%, including a loss of approximately 24.0% in January 2014. In 2015, the Peso lost approximately 52.0% of its value with respect to the U.S. dollar, including a 10.0% devaluation from January 1, 2015 to September 30, 2015 and a 38.0% devaluation during the last quarter of the year 2015, mainly concentrated after December 16, 2015. In 2016 and 2017, the Peso lost approximately 21.9% and 18.4% of its value against the U.S. dollar, respectively. In the first two months of 2018, the Peso lost approximately 7.1% of its value against the U.S. dollar.

The following table sets forth the annual high, low, average and period-end exchange rates for the periods indicated, expressed in Pesos per U.S. dollar and not adjusted for inflation. There can be no assurance that the Peso will not depreciate or appreciate again in the future. The Federal Reserve Bank of New York does not report a noon buying rate for Pesos.

|

| Exchange Rates |

| ||||||

|

| High(1) |

| Low(1) |

| Average(1)(2) |

| Period-end(1)(3) |

|

2013 |

| 6.5180 |

| 4.9228 |

| 5.4789 |

| 6.5180 |

|

2014 |

| 8.5555 |

| 6.5430 |

| 8.1188 |

| 8.5520 |

|

2015 |

| 13.7633 |

| 8.5537 |

| 9.2689 |

| 13.0050 |

|

2016 |

| 16.0392 |

| 13.0692 |

| 14.7794 |

| 15.8502 |

|

2017 |

| 18.8300 |

| 15.1742 |

| 16.5665 |

| 18.7742 |

|

October 2017 |

| 17.6775 |

| 17.3217 |

| 17.4528 |

| 17.6713 |

|

November 2017 |

| 17.6700 |

| 17.3307 |

| 17.4925 |

| 17.3845 |

|

December 2017 |

| 18.8300 |

| 17.2600 |

| 17.7001 |

| 18.7742 |

|

2018 |

|

|

|

|

|

|

|

|

|

January 2018 |

| 19.6500 |

| 18.4100 |

| 19.0200 |

| 19.6500 |

|

February 2018 |

| 20.1600 |

| 19.4700 |

| 19.8409 |

| 20.1150 |

|

March 2018 |

| 20.3875 |

| 20.1433 |

| 20.2378 |

| 20.1433 |

|

April 2018 (through April 25, 2018) |

| 20.2595 |

| 20.1450 |

| 20.1955 |

| 20.2595 |

|

(1) Reference exchange rate published by the Central Bank.

(2) Based on daily averages.

(3) The exchange rate used in our audited consolidated financial statements.

Item 3.B Capitalization and indebtedness

Not applicable.

Item 3.C Reasons for the offer and use of proceeds

Not applicable.

You should carefully consider the risks described below, as well as the other information in this annual report. Our business, results of operations, financial condition or prospects could be materially and adversely affected if any of these risks occurs. In general, investors take more risk when they invest in the securities of issuers in emerging markets such as Argentina than when they invest in the securities of issuers in the United States and other more developed markets. The risks described below are those known to us and that as of the date of this annual report believe may materially affect us.

Risks Relating to Argentina

Substantially all of our operations, property and customers are located in Argentina. As a result, the quality of our assets, our financial condition and the results of our operations are dependent upon the macroeconomic, regulatory, social and political conditions prevailing in Argentina from time to time. These conditions include growth rates, inflation rates, exchange rates, taxes, foreign exchange controls, changes to interest rates, changes to government policies, social instability, and other political, economic or international developments either taking place in, or otherwise affecting, Argentina.

Economic and political instability in Argentina may adversely and materially affect our business, results of operations and financial condition.

The Argentine economy has experienced significant volatility in recent decades, characterized by periods of low or negative growth, high levels of inflation and currency devaluation. As a consequence, our business and operations have been, and could in the future be, affected from time to time to varying degrees by economic and political developments and other material events affecting the Argentine economy, such as: inflation; price controls; foreign exchange controls; fluctuations in foreign currency exchange rates and interest rates; governmental policies

regarding spending and investment, national, provincial or municipal tax increases and other initiatives increasing government involvement with economic activity; civil unrest and local security concerns. You should make your own investigation into Argentina’s economy and its prevailing conditions before making an investment in us.

During 2001 and 2002, Argentina went through a period of severe political, economic and social crisis. Among other consequences, the crisis resulted in Argentina defaulting on its foreign debt obligations, introducing emergency measures and numerous changes in economic policies that affected utilities, financial institutions, and many other sectors of the economy. Argentina also suffered a significant real devaluation of the Peso, which in turn caused numerous Argentine private sector debtors with foreign currency exposure to default on their outstanding debt. After recovering significantly from the 2001-2002 crisis, the pace of growth of Argentina’s economy diminished, suggesting uncertainty as to whether the growth experienced between 2003 and 2011 was sustainable. Economic growth was initially fueled by a significant devaluation of the Peso, the availability of excess production capacity resulting from a long period of deep recession and high commodity prices. In spite of the growth following the 2001-2002 crisis, the economy has suffered a sustained erosion of direct investment and capital investment. The global economic crisis of 2008 led to a sudden economic decline in Argentina during 2009, accompanied by inflationary pressures, devaluation of the Peso and a drop in consumer and investor confidence. Real GDP growth recovered in 2010 and 2011, with GDP increasing to 9.5% and 8.4%, respectively. However, GDP growth slowed to 0.8% in 2012 and then grew by 2.3% in 2013. According to the revised calculation of the 2004 GDP published by INDEC on June 24, 2016, GDP increased 8.9% in 2005, 8.0% in 2006, 9.0% in 2007, 4.1% in 2008 and decreased 5.9% in 2009. In 2010 and 2011, GDP grew 10.1% and 6.0%, respectively and decreased 1.0% in 2012. GDP grew 2.4% in 2013, contracted 2.5% in 2014, grew 2.6% in 2015 and decreased 2.2% in 2016. However, during 2017, Argentina’s real GDP increased by 2.9% compared to 2016, according to the information published by INDEC on March 21, 2018.

Economic conditions in Argentina from 2012 to 2015 included increased inflation, continued demand for wage increases, a rising fiscal deficit and limitations on Argentina’s ability to service its restructured debt in accordance with its terms due to its ongoing litigation with holdout creditors. In addition, beginning in the second half of 2011, an increase in local demand for foreign currency caused the Argentine government to strengthen its foreign exchange controls, most of which were eased by the Macri Administration. See “—The implementation in the future of new exchange controls, restrictions on transfers abroad and capital inflow restrictions could limit the availability of international credit and could threaten the financial system, which may adversely affect the Argentine economy and, as a result, our business.”

Since 2007, the INDEC has experienced a process of institutional and methodological reforms that have given rise to controversy with respect to the reliability of the information that it produces including inflation, GDP and unemployment data. Reports published by the International Monetary Fund (“IMF”) state that their staff uses alternative measures of inflation for macroeconomic surveillance, including data produced by private sources, which have shown inflation rates considerably higher than those published by the INDEC since 2007. The IMF has also censured Argentina for failing to make sufficient progress, as required under the Articles of Agreement of the IMF, in adopting remedial measures to address the quality of official data, including inflation and GDP data. In February 2014, the INDEC released a new inflation index, known as National Urban Consumer Price Index (Indice de Precios al Consumidor Nacional Urbano) that measures prices on goods across the country and replaces the previous index that only measured inflation in the urban sprawl of the City of Buenos Aires. Even though the new methodology brought inflation statistics closer to those estimated by private sources, material differences between official inflation data and private estimates remained in 2015. On January 2016, based on its determination that INDEC had failed to produce reliable statistical information, the Macri administration declared a state of administrative emergency for the national statistical system and INDEC until December 31, 2016, which was not renewed. As consequence of the declaration of emergency, the INDEC ceased publishing certain statistical data until June 16, 2016, when it resumed publishing inflation rates, and began to release revised data, including GDP, poverty, foreign trade and balance of payments statistics, among others. See “—If the current levels of inflation continue, the Argentine economy and our financial position and business could be adversely affected.”

After recovering significantly from the 2001-2002 crisis, the pace of growth of Argentina’s economy diminished, suggesting uncertainty as to whether the growth experienced between 2003 and 2011 was sustainable. Economic growth was initially fueled by a significant devaluation of the Peso, the availability of excess production capacity resulting from a long period of deep recession and high commodity prices. In spite of the growth following the

2001-2002 crisis, the economy suffered a sustained erosion of direct investment and capital investment. The global economic crisis of 2008 led to a sudden economic decline in Argentina during 2009, accompanied by inflationary pressures, devaluation of the Peso and a drop in consumer and investor confidence.

Economic conditions in Argentina from 2012 to 2015 included increased inflation, continued demand for wage increases, a rising fiscal deficit and limitations on Argentina’s ability to service its restructured debt in accordance with its terms due to its ongoing litigation with holdout creditors. In addition, beginning in the second half of 2011, an increase in local demand for foreign currency caused the Argentine government to strengthen its foreign exchange controls. However, as of the issuance of Communication “A” 6037 by the Central Bank, which became effective on August 9, 2016, the government eliminated the monthly caps to the acquisition of foreign currency for non-specific purposes (Atesoramiento). During 2014, 2015, 2016 and 2017 the government imposed price controls on certain goods and services to control inflation. These price controls will remain in effect until April 2018, but as of the date of this annual report, there is uncertainty regarding what other specific actions will be taken to control inflation.

Presidential and Congressional elections in Argentina took place on October 25, 2015, and a runoff election (ballotage) between the two leading Presidential candidates was held on November 22, 2015, which resulted in Mr. Mauricio Macri being elected President of Argentina. The Macri administration assumed office on December 10, 2015.

Since assuming office, the Macri administration has implemented several significant economic and policy reforms, including those related to foreign exchange, the INDEC, financial policy, foreign currency-denominated bonds, foreign trade reforms, amendment to the Capital Markets Law, Tax Amnesty Law, correction of monetary imbalances, retiree program, fiscal policy, national electricity state of emergency and reforms, tariff increases and increase in minimum income.

Congressional elections were held in October 22, 2017 and President Macri’s governing coalition obtained the largest share of votes at the national level. However, even when the number of coalition members in Congress increased (holding in the aggregate 107 of a total of 257 seats in the House of Representatives and 24 of a total of 72 seats in the Senate), it still lacks a majority in either chamber of the Argentine Congress and, as a result, some or all of the Macri administration’s reforms aimed at improving the economy and investment environment (including the reduction of the fiscal deficit, reduction of the inflation rate and fiscal and labor reforms, among others) may not be implemented, which could adversely affect the continued improvement of the economy and investment environment. Any lack of ability of the Macri administration to adequately implement its measures as a consequence of the lack of sufficient political support could adversely affect the economy and the financial situation of Argentina, and, in turn our business, our financial and patrimonial situation and our results of operations. Argentina’s economy has undergone a significant slowdown, and any further decline in Argentina’s rate of economic growth could adversely affect our business, financial condition and results of operations. On the other hand, on November 16, 2017, the Argentine government, the governors of the majority of the Argentine provinces, including the Province of Buenos Aires, and the Head of Government of the City of Buenos Aires entered into an agreement pursuant to which guidelines were established in order to harmonize the tax structures of the different provinces and the City of Buenos Aires. Among other commitments, the provinces and the City of Buenos Aires agreed to gradually reduce the tax rates applicable to stamp tax and turnover tax within a five-year period, and withdraw their judicial claims against the Argentine government in connection with the federal co-participation regime. In exchange for this, the Argentine government, among other commitments, agreed to (i) compensate the provinces and the City of Buenos Aires (provided they enter into the agreement) for the effective reduction of its resources in 2018, resulting from the proposed elimination of section 104 of the Income Tax Law, quarterly updating such compensation in the following years, and (ii) issue a 11-year bond whose funds generate services for Ps.5,000 million in 2018 and Ps.12,000 every year starting from 2019, to be distributed among all the provinces, with the exception of the Province of Buenos Aires and the City of Buenos Aires, according to the effective distribution coefficients resulting from the federal co-participation regime. The provincial governments which took part in this agreement have committed to file, within the next 30 days after the execution of the agreement, the necessary draft bills for its implementation and authorize their respective executive branches to ensure its fulfilment. This agreement is effective in those provinces where their respective legislative branches have passed it. On December 22, the Argentine Congress passed the projects on fiscal consensus and fiscal liability (“Consenso Fiscal” and “Ley de Responsabilidad Fiscal”, respectively), with some amendments.

On November 13, 2017, the Argentine government submitted a draft bill to Congress concerning a series of amendments to the Capital Markets Law, the Mutual Funds Law No. 24,083 and the Argentine Negotiable Obligations Law, among others. Furthermore, the bill provides for the amendment of certain tax provisions, regulations relating to derivatives and the promotion of a financial inclusion program. As of the date of this annual report the draft bill is under consideration by the Argentine Congress and has not yet been approved.

On December 27, 2017, the Argentine Congress approved a tax reform that came into force on December 29, 2017 as Law No. 27,430 (the “Tax Reform Law”). The reform is intended to eliminate certain of the existing complexities and inefficiencies of the Argentine tax regime, diminish tax evasion, increase the coverage of income tax as applied to individuals and encourage investment while sustaining its medium and long term efforts aimed at restoring fiscal balance. The reform is part of a larger program announced by President Macri intended to increase the competitiveness of the Argentine economy (including by reducing the fiscal deficit) as well as employment, and diminish poverty on a sustainable basis. The main aspects of the Tax Reform Law include: (i) interest and capital gains realized by individuals that are Argentine tax residents on sales of real estate (subject to certain exceptions, including a primary residence exemption) acquired after the enactment of the bill will be subject to tax at the rate of 15%, calculated on the acquisition cost adjusted for inflation; (ii) income obtained from currently exempt bank deposits and sales of securities (including government securities) by individuals that are Argentine tax residents will be subject to tax at the rate of (a) 5% in the case of those denominated in pesos, subject to fixed interest rate and not indexed, and (b) 15% for those denominated in a foreign currency or indexed; income obtained from the sales of shares made on a stock exchange will remain exempt, subject to compliance with certain requirements; (iii) corporate income tax will initially decline to 30% in 2019 and 2020 and to 25% starting in 2021 and withholding taxes will be assessed on certain dividends or distributed profits bringing the total effective tax rate on corporate profits to 35%; (iv) social security contributions will be gradually increased to 19.5% starting in 2022, in lieu of the differential scales currently in effect; (v) the percentage of tax debits and credits that can be credited towards income tax will be gradually increased over a five year period, from the current 17% for credits to 100% for credits and debits; and (vi) holders of notes issued by the federal government, the provinces and municipalities of Argentina and the City of Buenos Aires that are not Argentine tax residents will be exempt from Argentine income taxes on interest and capital gains to the extent such beneficiaries do not reside in or channel their funds through non-cooperating jurisdictions. The non-cooperating jurisdictions list will be prepared and published by the executive branch. Short-term notes issued by the Central Bank (LEBACs) are outside the scope of these exemptions applicable to non-Argentine residents. The aforementioned amendments have been in force since January 1, 2018.

On January 10, 2018, the Macri administration issued Emergency Decree No. 27/2018 aimed at simplifying, expediting and promoting efficiency in the procedures within administrative entities and agencies, avoiding any unnecessary bureaucracy and expenses. The decree modifies and simplifies regulatory frameworks related to companies, transportation, trademark and patent procedures, transportation, digital signature, access to credit and work promotion.

As of the date of this annual report, the impact that these measures have had and any future measures taken by the Macri administration will have on the Argentine economy as a whole and the financial sector in particular cannot be predicted. We believe that the effect of the planned liberalization of the economy will be positive for our business by stimulating economic activity but it is not possible to predict such effect with certainty and such liberalization could also be disruptive to the economy and fail to benefit or harm our business.

Inflation, any decline in GDP and/or other future economic, social and political developments in Argentina, over which we have no control, may adversely affect our financial condition or results of operations.

A decline in international demand for Argentine products, a lack of stability and competitiveness of the Peso against other currencies, a decline in confidence among consumers and foreign and domestic investors, a higher rate of inflation and future political uncertainties, among other factors, may affect the development of the Argentine economy, which could lead to reduced demand for our services and adversely affect our business, financial condition and results of operations.

If the current levels of inflation continue, the Argentine economy and our financial position and business could be adversely affected.

Argentina has confronted inflationary pressures since 2007. According to INDEC data, the CPI grew 9.5% in 2011, 10.8% in 2012, 10.9% in 2013, 24.0% in 2014 and 11.9% in the ten-month period ended October 31, 2015. The INDEC did not publish the CPI for the period between November 2015 and April 2016, and resumed publishing inflation rates using its new methodology for calculating CPI starting in June 2016, reporting increases of 4.2%, 3.1%, 2.0%, 0.2%, 1.1%, 2.4%, 1.6% and 1.2% during the months of May, June, July, August, September, October, November and December 2016, respectively.

According to unrevised INDEC data, the WPI increased 14.6% in 2010, 12.7% in 2011, 13.1% in 2012, 14.8% in 2013, 28.3% in 2014 and 10.6% in the ten-month period ended October 31, 2015. The INDEC did not publish the WPI for the last two months of 2015, and resumed publishing WPI data in May 2016, reporting that the WPI grew 34.5% in 2016.

The Argentine government declared a state of administrative emergency of the national statistical system and the INDEC —the official agency in charge of the system- until December 31, 2016 through Decree No. 55/2016, which was not renewed. During the implementation of rearrangement measures of its technical and administrative structure, the INDEC used official CPI figures and other statistics published by the Province of San Luis and the City of Buenos Aires. Despite the INDEC reforms, there is uncertainty as to (i) whether the official data will be sufficiently corrected, (ii) in what timeframe such data will be corrected and (iii) what effects these reforms will have on the Argentine economy. The Macri administration released an alternative CPI index based on data from the City of Buenos Aires and the Province of San Luis. According to the available public information based on data from the City of Buenos Aires, CPI grew 26.6% in 2013, 38.0% in 2014, 26.9% in 2015, 41.0% in 2016 and 26.1% in 2017, while according to the data of the Province of San Luis, CPI grew 31.9% in 2013, 39.0% in 2014, 31.6% in 2015, 31.4% in 2016 and 24.3% in 2017.

On June 15, 2016, the INDEC resumed publishing inflation rates -which was previously suspended due to the state of administrative emergency on the national statistical system. The INDEC reported an increase of 4.2% in CPI for May 2016, while the CPI measured by the Argentine Congress reported an increase of 3.5%. Additionally, the INDEC published revised GDP data for the years 2005 through 2015, registering differences of up to 20 points between the original information reported by the prior administration and the revised information.

According to CPI figures of the INDEC, inflation was 16.9% between May and December 2016. The INDEC reported a cumulative variation of the CPI of 24.8% for 2017, while the CPI measured by the Argentine Congress registered an increase of 24.6%. The CPI variation was of 1.8%, 2.4% and 2.3% for the months of January, February and March 2018, respectively, compared to the previous month.

Also, on September 26, 2016, the Central Bank presented the inflation targeting regime, a system that seeks to offer a predictable and stable unit of value for inflation. In accordance with the data published by the Central Bank, the original year-on-year inflation targets were 12% to 17% for 2017; from 8% to 12% by 2018; and from 3.5% to 6.5% by 2019. However, on December 27, 2017, the Central Bank updated its inflation target regime by adopting the inflation targets set by the Ministry of the Treasury for the next three years, including targets of 15% for 2018, 10% for 2019 and 5% by the end of 2020.

In the past, inflation has materially undermined the Argentine economy and the government’s ability to generate conditions that fostered economic growth. In addition, high inflation or a high level of volatility with respect to the same may materially and adversely affect the business volume of the financial system and prevent the growth of intermediation activity levels. This result, in turn, could adversely affect the level of economic activity and employment.

A high inflation rate also affects Argentina’s competitiveness abroad, real salaries, employment, consumption and interest rates. A high level of uncertainty with regard to these economic variables, and a general lack of stability in terms of inflation, could lead to shortened contractual terms and affect the ability to plan and make decisions. This may have a negative impact on economic activity and on the income of consumers and their purchasing power, all of which could materially and adversely affect our financial position, results of operations and business. The Argentine

government’s adjustments to electricity and gas tariffs, as well as the increase in the price of gasoline have impacted prices creating additional inflationary pressures.

The Macri administration has announced its intention to reduce the primary fiscal deficit as a percentage of GDP and to reduce the government’s dependence on financing from the Central Bank. If structural inflationary imbalances cannot be addressed and current levels of inflation persist, it could adversely affect the Argentine economy and financial situation.

Inflation rates could escalate in the future. There is uncertainty regarding the effects that the measures adopted, or that may be adopted in the future, by the Argentine government to control inflation may have. See “—Government intervention in the Argentine economy could adversely affect our results of operations or financial condition.”

If the high levels of inflation continue, the Argentine economy may be considered hyperinflationary for purposes of IAS 29, which could have an impact on our audited consolidated financial statements and other financial information, and we may need to adjust or restate our audited consolidated financial statements and other information.

On February 12, 2014, the Central Bank, through Communication “A” 5541, established the general guidelines towards conversion to IFRS as issued by the International Accounting Standards Board (IASB) for preparing financial statements of the entities under its supervision. We are in a convergence process towards such standards, which will be mandatory as from fiscal year starting on January 1, 2018. International Accounting Standard 29 (IAS 29), which is applicable to IFRS, but not to Argentine Banking GAAP, requires that financial statements of any entity whose functional currency is the currency of a hyperinflationary economy, whether based on the historical cost method or on the current cost method, be stated in terms of the measuring unit current at the end of the reporting period. IAS 29 does not establish a set inflation rate beyond which an economy is deemed to be experiencing hyperinflation. However, hyperinflation is commonly understood to occur when changes in price levels are close to or exceed 100% on a cumulative basis over the prior three years, along with the presence of several other macroeconomic-related qualitative factors. Despite the high inflation rates in Argentina in recent years, we conducted an analysis pursuant to the criteria set forth in IAS 29, and based solely on such internal review we do not currently believe that Argentina qualifies as a hyperinflationary economy for any of the years included in this annual report. We reassess inflation data periodically to determine whether this belief continues to be applicable. However, certain macroeconomic indicators have experienced a significant annual variation, a fact that must be considered when evaluating and interpreting our results of operations and financial condition as reflected in our audited consolidated financial statements included in this annual report.

Although we do not believe the current rate of inflation rises to the level required for Argentina to be considered a hyperinflationary economy under IAS 29, if inflation rates continue to escalate in the future, the Peso may qualify as a currency of a hyperinflationary economy, in which case our audited Consolidated Financial Statements and other financial information as from the IFRS transition date (as defined below), may need to be adjusted or restated by applying a general price index and expressed in the measuring unit (i.e., the hyperinflationary currency) current at the end of each reporting period. We cannot determine at this time the impact that this would have on our results of operations and financial condition.

The Argentine government’s ability to obtain financing from international markets is limited, which may impair its ability to implement reforms and foster economic growth, which may negatively impact our financial condition or cash flows.

In 2005 and 2010, Argentina conducted exchange offers to restructure part of its sovereign debt that had been in default since the end of 2001. As a result of these exchange offers, Argentina restructured over 92% of its eligible defaulted debt. In April 2016, the Argentine government settled U.S.$4.2 billion outstanding principal amount of untendered debt.

As of the date of this annual report, litigation initiated by bondholders that have not accepted Argentina’s settlement offer continues in several jurisdictions, although the size of the claims involved has decreased significantly. As of September 30, 2017, the amount of the Argentine government’s non-restructured debt was of approximately U.S.$107.1 million based on the most recent publicly available data.

Although the vacating of the pari passu injunctions removed a material obstacle to access to capital markets by the Argentine government, as evidenced by successful bond issuances in April 2016 and January 2017, future transactions may be affected as litigation with holdout bondholders continues, which in turn could affect the Argentine government’s ability to implement certain expected reforms and foster economic growth, which may have a direct impact on our ability to access international credit markets, thus affecting our ability to finance our operations and growth.

Fluctuations in the value of the Peso could adversely affect the Argentine economy, and consequently our results of operations or financial condition.