united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22554

Vertical Capital Income Fund

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

Corporation Trust Center

1209 Orange Street

Wilmington, Delaware 19801

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2616

Date of fiscal year end: 9/30

Date of reporting period: 9/30/20

Item 1. Reports to Stockholders.

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | Vertical Capital Income Fund | | |

| | | | | |

| | | | | |

| | | | | |

| | | VCIF | | |

| | | Cusip: 92535C104 | | |

| | | | | |

| | | | | |

| | | Annual Report | | |

| | | September 30, 2021 | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | Investor Information: 1-866-277-VCIF | | |

| | | | | |

| | | | | |

| | | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | | |

| | | |

| | | | | |

| | This report and the financial statements contained herein are submitted for the general information of shareholders. Nothing contained herein is to be considered an offer of sale or solicitation of an offer to buy shares of the Vertical Capital Income Fund. | |

| | | |

| | | |

| | | | | |

Managed Distribution Plan Disclosure

In December 2020, the Board of Trustees (the “Board”), acting pursuant to a Securities and Exchange Commission exemptive order, approved a Managed Distribution Plan (the “Plan”) for Vertical Capital Income Fund (the “Fund”). Pursuant to the Plan, the Fund pays a minimum monthly distribution to shareholders at a stated annual rate as a percentage of the three-month average net asset value (“NAV”) of the Fund’s shares prior to the month of distribution. The distribution is calculated as 8% of the previous three-month average NAV, divided by 12. Payment of monthly distributions under the Fund’s Plan commenced in January 2021.

The Plan is subject to periodic review by the Board, and the Board may amend the terms of the Plan including amending the annual rate of payment or may terminate the Plan at any time without prior notice to the Fund’s shareholders. The Fund’s distribution rate may be affected by numerous factors, including changes in realized and projected market returns, Fund performance, and other factors. There can be no assurance that an unanticipated change in market conditions or other unforeseen factors will not result in a change in the Fund’s distribution rate at a future time. The Fund does not believe there are any reasonably foreseeable circumstances that would cause the termination of the Plan. The amendment or termination of the Plan could have an adverse effect on the market price of a Fund’s shares.

You should not draw any conclusions about the Fund’s investment performance from the amount of these distributions or from the terms of the Fund’s Managed Distribution Plan.

November 19, 2021

Dear Shareholder,

We are pleased to report to you the results of another six-month period for the Vertical Capital Income Fund (the “Fund”). Consistent with the Managed Distribution Plan (the “Plan”) and our investment objective to seek income, the Fund made monthly distributions aggregating approximately $1.11 per share for the year ended September 30, 2021. Included in that amount was a special distribution of approximately $0.22 per share paid in December 2020 as a result of net capital gains realized on loan sales and loan payoffs during the Fund’s last fiscal year ended September 30, 2020. In alignment with the Plan’s policy, the Fund will pay net capital gains realized on loan sales and loan payoffs included in the monthly distributions rather than only as a special December distribution going forward.

The Fund’s net asset value (“NAV)” per share was $12.05 at the September 30, 2020 and $11.69 per share at September 30, 2021. In comparison, the Fund’s traded share price was $9.93 at the beginning of the fiscal year and $10.49 at September 30, 2021, reflecting discounts to NAV of 18% and 10%. The management team is encouraged and would like to continue to see the narrowing of discount after the announcement in December of the Plan.

For the year ended September 30, 2021 the Fund produced a total return, based on its traded share price, of 17.59% compared to one of its key benchmarks, the Bloomberg Barclays U.S. Mortgage Backed Securities Index, which reported a total return of -0.43%. (Please see the definition of the index that accompanies the performance table that immediately follows this letter.) The SEC Yield per share as of September 30, 2021 was 2.92%. In comparison the Fund produced a total return based on its NAV per share for the same period of 6.52%. Since inception, the Fund has produced an annualized total return of 6.84% based on its NAV.

Update on Economic Outlook

The Mortgage Bankers Association forecasts purchase mortgage originations to grow 9% to a new record of $1.73 trillion in 2022. This comes after an initial anticipated 14% decline in 2021. MBA also expects refinance originations will slow further next year, decreasing by 62% to $860 billion from $2.26 trillion in 2021.

Forecasters expect mortgage originations to total $ 2.59 trillion in 2022. In 2023, mortgage originations are expected to decrease to $ 2.53 trillion though purchase originations are forecasted to reach new successive records in 2022 and 2023. Meanwhile, higher mortgage rates and fewer eligible homeowners will lead to further declines in refinance volume.

MBA’s baseline forecast is for mortgage rates to rise, with the 30-year, fixed-rate mortgage expected to end 2021 at 3.1% before increasing to 4.0% by the end of 2022.

We are seeing forecasters assume continued strong economic growth amidst the eventual easing of supply chain constraints that have restricted some economic activity this year. The economy and specifically the labor market rebounded in 2021, though the overall growth did not meet expectations. Challenges including stubborn supply chain issues, fueling inflation, decreased consumer spending, led to record number job openings at almost 11 million unfilled job openings in the economy.

Amongst the recent headlines, the Feds steps toward tapering asset purchases and removing monetary policy accommodation should come as no surprise. The biggest news from the FOMC’s most recent meeting was the change in projections. A majority of members now see the first interest rate hike in 2022 and possibly three rate hikes in 2023, a faster pace than had been previously projected.

Fund Strategy

There is almost $16 trillion of U.S. residential mortgage debt outstanding, of which approximately $ 11 trillion is secured by one-to-four family residences. The balance is represented by mortgage debt on multi-family, non-farm/non-residential and farm properties. The Fund invests as a secondary market participant in the one-to-four family residential whole loan market. This market historically boasts a deep roster of institutional participants, along with a diverse universe of sellers and reasons for sale. As such, we are comfortable that we will continue to see an adequate supply of investment opportunities. The Fund generates monthly cash distributions from interest income earned on the Fund’s loan portfolio, net of the costs to operate. Costs include fees paid to third parties for loan servicing and custodial, valuation, audit and legal services, as well as fees to the advisor to manage the Fund. As noted above, the Fund made aggregated distributions for the fiscal year of approximately $1.11 per share.

The Fund also generates capital gains when it sells loans at a price that is excess of its adjusted cost basis or when loans originally purchased at a discount to their unpaid principal balance (“UPB”) pay off in full before maturity of the loan. Asset sales and loan payoffs can occur anytime throughout the year; however, the Fund has historically made a single distribution in December of each year in order to fully account for all net long-term and short-term capital gains and losses during its taxable period. Most of these distributions have been subject to lower long-term capital gain tax rates; thereby, potentially increasing the after-tax yield to our shareholders. As noted above, the capital gain distribution during the fiscal year was $0.22 per share and going forward the Fund will pay net realized capital gains in the monthly distributions rather than only as a special December distribution.

The Fund meets its investment objective primarily by investing in mortgage notes secured by first liens on residential real estate. The Fund only invests in “whole loans” and does not invest in tranches of RMBS. Investing as a first mortgage lender in whole loans allows the Fund to deal directly with any borrower who is delinquent, in default or needs to restructure their loan for any reason. The Fund can decide on a case by case basis how best to work with the borrower to secure repayment of all amounts due the Fund, which is not always the case in RMBS. This direct interaction has been a significant benefit over the years when the Fund has had to manage assets with borrowers affected by crises, such as COVID-19,hurricanes, floods or fires.

The Fund pursues investment opportunities in many types of residential mortgage whole loans. Some known as “Scratch and Dent” are “conforming” loans with typical original terms of 25 or 30 years that would have otherwise qualified for purchase by one of the Government Sponsored Enterprises (“GSEs”), like Fannie Mae or Freddie Mac, but were rejected for technical defects in the application or documentation process. Others are non-qualified loans (“Non QM”), which do not meet the criteria for purchase or origination by a GSE. In addition, there are “Fix and Flip” loans, which typically have 12-24 month terms and “Rental and Bridge” loans which typically have 24-60 month terms. Loans can be performing, re-performing (loans that were non-performing at one point and have now become performing), long-term, short-term, fixed rate or adjustable.

As always, we are appreciative of your continued support and we look forward to working on your behalf.

Regards,

Katherine L. Hawkins

Portfolio Manager

| Vertical Capital Income Fund |

| PORTFOLIO REVIEW |

| September 30, 2021 |

| |

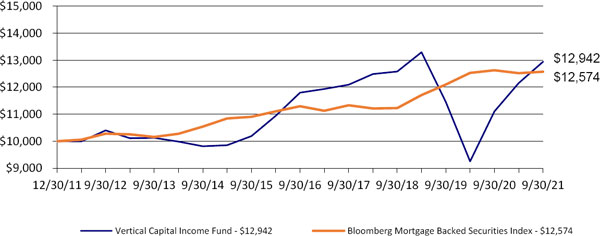

PERFORMANCE OF A $10,000 INVESTMENT

(Based upon Net Asset Value)

The Fund’s performance figures for the period ended September 30, 2021, compared to its

benchmark:

| | One Year | Three Years | Five Years | Since Inception* |

| Vertical Capital Income Fund-NAV | 6.52% | 4.60% | 4.11% | 6.84% |

| Vertical Capital Income Fund-Market Price ** | 17.59% | 0.95% | 1.87% | 2.68% |

| | | | | |

| Bloomberg Mortgage Backed Securities Index | (0.43)% | 3.85% | 2.17% | 2.38% |

| * | The Fund commenced operations on December 30, 2011. The performance of the Fund is based on average annual returns. |

| ** | The calculation is made using the NAV until the initial Market Price on May 30, 2019. |

The Bloomberg Mortgage Backed Securities Index is an unmanaged index composed of securities backed by U.S. government agency guaranteed mortgage pools of Ginnie Mae, Freddie Mac and Fannie Mae. Investors cannot invest directly in an index or benchmark. The mortgage notes held by the Fund are not guaranteed by any U.S. government agency.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the Adviser not waived its fees and reimbursed a portion of the Fund’s expenses. For performance information current to the most recent month-end, please call 1-866-277-VCIF.

PORTFOLIO COMPOSITION***

| Mortgage Notes | | | 99.9 | % |

| Other Investments | | | 0.1 | % |

| | | | 100.0 | % |

| | | | | |

*** Based on Investments at Value as of September 30, 2021.

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% | | | | | | | | | | | | |

| | 46,518 | | | Loan ID 200012 | | ARM | | 9.8000 | | | 07/01/37 | | | $ | 47,449 | |

| | 32,025 | | | Loan ID 200016 | | ARM | | 10.3750 | | | 01/01/31 | | | | 32,666 | |

| | 42,802 | | | Loan ID 200018 | | Fixed | | 7.0000 | | | 01/01/33 | | | | 43,658 | |

| | 96,419 | | | Loan ID 200023 | | Fixed | | 5.8750 | | | 12/01/50 | | | | 89,660 | |

| | 200,824 | | | Loan ID 200026 | | Fixed | | 4.7500 | | | 01/01/50 | | | | 204,840 | |

| | 188,600 | | | Loan ID 200029 | | Fixed | | 6.3100 | | | 07/01/37 | | | | 192,372 | |

| | 523,826 | | | Loan ID 200035 | | Fixed | | 4.6250 | | | 11/01/50 | | | | 527,261 | |

| | 103,801 | | | Loan ID 200041 | | Fixed | | 4.8750 | | | 08/01/39 | | | | 105,320 | |

| | 36,598 | | | Loan ID 200042 | | Fixed | | 7.0000 | | | 12/01/37 | | | | 37,330 | |

| | 43,815 | | | Loan ID 200043 | | Fixed | | 6.1250 | | | 07/01/39 | | | | 44,691 | |

| | 46,639 | | | Loan ID 200048 | | Fixed | | 5.5000 | | | 08/01/39 | | | | 47,572 | |

| | 48,824 | | | Loan ID 200054 | | Fixed | | 8.2500 | | | 03/01/39 | | | | 49,800 | |

| | 73,291 | | | Loan ID 200055 | | Fixed | | 10.0000 | | | 01/05/36 | | | | 74,757 | |

| | 28,103 | | | Loan ID 200060 | | Fixed | | 5.7500 | | | 08/01/39 | | | | 28,665 | |

| | 157,871 | | | Loan ID 200076 | | Fixed | | 4.2500 | | | 12/01/41 | | | | 96,032 | |

| | 12,934 | | | Loan ID 200078 | | Fixed | | 7.0000 | | | 08/01/36 | | | | 13,192 | |

| | 131,184 | | | Loan ID 200079 | | Fixed | | 5.0000 | | | 02/01/59 | | | | 122,899 | |

| | 61,999 | | | Loan ID 200082 | | Fixed | | 8.2500 | | | 04/01/40 | | | | 61,421 | |

| | 165,469 | | | Loan ID 200084 | | Fixed | | 7.0000 | | | 03/01/39 | | | | 158,676 | |

| | 213,064 | | | Loan ID 200087 | | Fixed | | 6.0000 | | | 03/01/51 | | | | 210,358 | |

| | 110,204 | | | Loan ID 200088 | | Fixed | | 7.0000 | | | 06/01/39 | | | | 95,475 | |

| | 248,053 | | | Loan ID 200089 | | Fixed | | 3.8750 | | | 03/01/52 | | | | 217,313 | |

| | 268,848 | | | Loan ID 200090 | | Fixed | | 4.5000 | | | 11/01/36 | | | | 185,470 | |

| | 67,546 | | | Loan ID 200102 | | Fixed | | 8.2500 | | | 03/01/40 | | | | 68,897 | |

| | 102,803 | | | Loan ID 200110 | | Fixed | | 8.2500 | | | 08/01/39 | | | | 104,859 | |

| | 66,323 | | | Loan ID 200128 | | Fixed | | 4.7100 | | | 07/01/37 | | | | 62,139 | |

| | 432,350 | | | Loan ID 200129 | | Fixed | | 4.6250 | | | 03/01/52 | | | | 395,742 | |

| | 109,968 | | | Loan ID 200135 | | Fixed | | 4.3750 | | | 12/01/42 | | | | 108,700 | |

| | 71,168 | | | Loan ID 200141 | | Fixed | | 4.2500 | | | 02/01/42 | | | | 69,658 | |

| | 371,510 | | | Loan ID 200145 | | Fixed | | 4.6250 | | | 08/01/51 | | | | 349,103 | |

| | 88,635 | | | Loan ID 200152 | | ARM | | 3.0000 | | | 09/01/37 | | | | 84,203 | |

| | 136,846 | | | Loan ID 200158 | | Fixed | | 3.6250 | | | 12/01/42 | | | | 129,809 | |

| | 175,168 | | | Loan ID 200165 | | Fixed | | 4.3750 | | | 12/01/41 | | | | 173,371 | |

| | 19,029 | | | Loan ID 200169 | | Fixed | | 6.9230 | | | 09/01/34 | | | | 19,410 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 80,054 | | | Loan ID 200174 | | Fixed | | 7.3400 | | | 04/01/37 | | | $ | 81,655 | |

| | 45,270 | | | Loan ID 200175 | | Fixed | | 9.6000 | | | 05/01/37 | | | | 46,175 | |

| | 4,807 | | | Loan ID 200177 | | Fixed | | 8.0000 | | | 01/11/22 | | | | 4,904 | |

| | 104,065 | | | Loan ID 200181 | | Fixed | | 7.5000 | | | 06/01/41 | | | | 67,086 | |

| | 65,934 | | | Loan ID 200184 | | Fixed | | 4.3750 | | | 12/01/42 | | | | 65,132 | |

| | 25,480 | | | Loan ID 200185 | | Fixed | | 5.3750 | | | 06/01/42 | | | | 25,990 | |

| | 48,605 | | | Loan ID 200186 | | Fixed | | 5.1250 | | | 08/01/42 | | | | 49,577 | |

| | 146,468 | | | Loan ID 200194 | | Fixed | | 4.7500 | | | 09/01/41 | | | | 147,730 | |

| | 229,189 | | | Loan ID 200195 | | Fixed | | 3.8750 | | | 03/01/42 | | | | 221,330 | |

| | 36,254 | | | Loan ID 200198 | | Fixed | | 5.2500 | | | 10/01/42 | | | | 36,979 | |

| | 33,662 | | | Loan ID 200201 | | Fixed | | 5.1250 | | | 08/01/41 | | | | 34,335 | |

| | 18,821 | | | Loan ID 200206 | | Fixed | | 3.9900 | | | 12/01/42 | | | | 18,265 | |

| | 40,044 | | | Loan ID 200208 | | Fixed | | 4.2500 | | | 01/01/43 | | | | 39,371 | |

| | 163,797 | | | Loan ID 200209 | | Fixed | | 3.8750 | | | 08/01/42 | | | | 158,100 | |

| | 128,598 | | | Loan ID 200217 | | Fixed | | 5.2500 | | | 07/01/40 | | | | 131,170 | |

| | 65,507 | | | Loan ID 200218 | | Fixed | | 4.2500 | | | 12/01/41 | | | | 64,567 | |

| | 45,113 | | | Loan ID 200228 | | Fixed | | 4.6250 | | | 08/01/42 | | | | 45,118 | |

| | 105,032 | | | Loan ID 200243 | | Fixed | | 3.7500 | | | 04/01/43 | | | | 100,339 | |

| | 23,087 | | | Loan ID 200244 | | Fixed | | 5.0000 | | | 05/01/42 | | | | 23,409 | |

| | 80,651 | | | Loan ID 200286 | | Fixed | | 4.5000 | | | 07/01/43 | | | | 80,184 | |

| | 86,721 | | | Loan ID 200287 | | Fixed | | 4.3750 | | | 07/01/43 | | | | 85,677 | |

| | 181,452 | | | Loan ID 200296 | | Fixed | | 3.2500 | | | 02/01/43 | | | | 166,977 | |

| | 30,233 | | | Loan ID 200313 | | Fixed | | 8.5000 | | | 03/01/28 | | | | 30,837 | |

| | 258,169 | | | Loan ID 200315 | | ARM | | 3.3750 | | | 06/01/37 | | | | 252,121 | |

| | 58,253 | | | Loan ID 200317 | | Fixed | | 7.0000 | | | 09/01/32 | | | | 59,418 | |

| | 240,423 | | | Loan ID 200330 | | Fixed | | 7.0000 | | | 08/01/37 | | | | 169,318 | |

| | 88,110 | | | Loan ID 200332 | | Fixed | | 5.7750 | | | 10/01/37 | | | | 89,872 | |

| | 83,773 | | | Loan ID 200334 | | Fixed | | 7.0000 | | | 01/01/33 | | | | 85,448 | |

| | 252,203 | | | Loan ID 200335 | | Fixed | | 5.0000 | | | 11/01/52 | | | | 257,247 | |

| | 40,313 | | | Loan ID 200338 | | ARM | | 10.5000 | | | 08/01/29 | | | | 41,119 | |

| | 16,513 | | | Loan ID 200340 | | Fixed | | 7.0000 | | | 03/01/30 | | | | 16,844 | |

| | 53,232 | | | Loan ID 200348 | | Fixed | | 6.5000 | | | 07/01/38 | | | | 54,297 | |

| | 59,728 | | | Loan ID 200352 | | Fixed | | 7.0000 | | | 08/01/30 | | | | 60,922 | |

| | 58,617 | | | Loan ID 200358 | | Fixed | | 5.0000 | | | 04/01/25 | | | | 59,072 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 59,030 | | | Loan ID 200361 | | Fixed | | 7.5000 | | | 01/01/34 | | | $ | 60,211 | |

| | 78,807 | | | Loan ID 200366 | | Fixed | | 6.2500 | | | 03/01/34 | | | | 80,383 | |

| | 148,325 | | | Loan ID 200368 | | Fixed | | 4.5000 | | | 04/01/36 | | | | 148,593 | |

| | 62,997 | | | Loan ID 200374 | | ARM | | 7.0000 | | | 05/01/34 | | | | 59,847 | |

| | 170,749 | | | Loan ID 200380 | | Fixed | | 4.2200 | | | 04/01/49 | | | | 168,995 | |

| | 270,281 | | | Loan ID 200384 | | Fixed | | 5.0000 | | | 11/01/47 | | | | 242,355 | |

| | 131,982 | | | Loan ID 200385 | | Fixed | | 8.2500 | | | 01/01/40 | | | | 134,622 | |

| | 184,871 | | | Loan ID 200390 | | Fixed | | 4.7800 | | | 04/16/47 | | | | 173,397 | |

| | 136,562 | | | Loan ID 200391 | | Fixed | | 4.0000 | | | 01/13/35 | | | | 134,128 | |

| | 58,978 | | | Loan ID 200392 | | Fixed | | 10.0000 | | | 06/05/34 | | | | 56,029 | |

| | 75,048 | | | Loan ID 200395 | | Fixed | | 4.8600 | | | 04/01/47 | | | | 44,250 | |

| | 65,200 | | | Loan ID 200396 | | Fixed | | 10.0000 | | | 02/01/36 | | | | 66,504 | |

| | 52,687 | | | Loan ID 200397 | | ARM | | 3.1250 | | | 09/01/37 | | | | 51,898 | |

| | 54,570 | | | Loan ID 200399 | | Fixed | | 4.9800 | | | 06/01/37 | | | | 55,658 | |

| | 38,801 | | | Loan ID 200403 | | Fixed | | 8.3000 | | | 10/15/32 | | | | 39,578 | |

| | 49,587 | | | Loan ID 200404 | | Fixed | | 8.1000 | | | 05/01/37 | | | | 50,579 | |

| | 81,504 | | | Loan ID 200405 | | Fixed | | 4.8700 | | | 12/01/35 | | | | 82,493 | |

| | 109,924 | | | Loan ID 200406 | | Fixed | | 4.8750 | | | 10/01/51 | | | | 111,747 | |

| | 327,450 | | | Loan ID 200409 | | Fixed | | 6.0000 | | | 02/01/49 | | | | 300,703 | |

| | 94,444 | | | Loan ID 200411 | | Fixed | | 8.2750 | | | 06/01/37 | | | | 96,333 | |

| | 60,223 | | | Loan ID 200417 | | Fixed | | 7.0000 | | | 05/01/35 | | | | 61,427 | |

| | 141,183 | | | Loan ID 200420 | | Fixed | | 4.2250 | | | 04/10/38 | | | | 139,531 | |

| | 67,674 | | | Loan ID 200421 | | Fixed | | 7.7100 | | | 08/01/37 | | | | 69,028 | |

| | 115,359 | | | Loan ID 200423 | | Fixed | | 4.5000 | | | 06/01/43 | | | | 114,584 | |

| | 198,038 | | | Loan ID 200430 | | Fixed | | 3.6250 | | | 07/01/43 | | | | 187,341 | |

| | 257,808 | | | Loan ID 200432 | | Fixed | | 4.8750 | | | 05/01/43 | | | | 260,263 | |

| | 90,203 | | | Loan ID 200433 | | Fixed | | 4.2500 | | | 08/01/43 | | | | 88,692 | |

| | 188,017 | | | Loan ID 200435 | | Fixed | | 4.6250 | | | 11/01/52 | | | | 189,993 | |

| | 38,980 | | | Loan ID 200439 | | Fixed | | 5.0000 | | | 08/01/41 | | | | 39,669 | |

| | 123,099 | | | Loan ID 200445 | | Fixed | | 5.2500 | | | 02/01/39 | | | | 125,561 | |

| | 26,712 | | | Loan ID 200447 | | Fixed | | 5.8750 | | | 11/04/34 | | | | 27,246 | |

| | 72,163 | | | Loan ID 200448 | | Fixed | | 5.7500 | | | 05/01/42 | | | | 73,606 | |

| | 127,663 | | | Loan ID 200449 | | Fixed | | 5.0000 | | | 02/01/42 | | | | 119,636 | |

| | 315,239 | | | Loan ID 200451 | | Fixed | | 6.2500 | | | 07/01/38 | | | | 321,544 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 167,682 | | | Loan ID 200460 | | Fixed | | 7.0000 | | | 07/01/41 | | | $ | 171,036 | |

| | 356,613 | | | Loan ID 200462 | | Fixed | | 6.0000 | | | 07/01/45 | | | | 363,746 | |

| | 210,544 | | | Loan ID 200465 | | Fixed | | 6.5000 | | | 07/01/37 | | | | 214,755 | |

| | 101,915 | | | Loan ID 200468 | | Fixed | | 5.6250 | | | 12/01/44 | | | | 32,192 | |

| | 113,556 | | | Loan ID 200469 | | Fixed | | 6.5000 | | | 07/01/37 | | | | 115,827 | |

| | 230,092 | | | Loan ID 200474 | | Fixed | | 5.7500 | | | 11/01/50 | | | | 234,694 | |

| | 180,777 | | | Loan ID 200476 | | Fixed | | 6.0000 | | | 09/01/50 | | | | 184,392 | |

| | 101,408 | | | Loan ID 200489 | | Fixed | | 4.0000 | | | 03/01/43 | | | | 98,533 | |

| | 179,164 | | | Loan ID 200491 | | Fixed | | 5.5000 | | | 10/01/39 | | | | 182,747 | |

| | 249,830 | | | Loan ID 200494 | | Fixed | | 4.6250 | | | 10/01/43 | | | | 250,237 | |

| | 178,785 | | | Loan ID 200500 | | Fixed | | 5.8750 | | | 02/01/37 | | | | 182,360 | |

| | 59,615 | | | Loan ID 200507 | | Fixed | | 4.5000 | | | 09/01/42 | | | | 59,323 | |

| | 88,905 | | | Loan ID 200517 | | Fixed | | 8.0000 | | | 05/01/39 | | | | 88,905 | |

| | 179,723 | | | Loan ID 200518 | | Fixed | | 3.0000 | | | 12/01/50 | | | | 165,115 | |

| | 100,315 | | | Loan ID 200527 | | Fixed | | 4.5000 | | | 12/01/43 | | | | 99,794 | |

| | 94,795 | | | Loan ID 200532 | | Fixed | | 3.2500 | | | 07/01/43 | | | | 87,203 | |

| | 36,049 | | | Loan ID 200545 | | Fixed | | 4.3750 | | | 02/01/29 | | | | 35,620 | |

| | 120,425 | | | Loan ID 200564 | | Fixed | | 4.8750 | | | 05/01/39 | | | | 122,190 | |

| | 83,776 | | | Loan ID 200573 | | Fixed | | 3.7500 | | | 09/01/42 | | | | 80,054 | |

| | 118,082 | | | Loan ID 200574 | | Fixed | | 4.8750 | | | 01/01/44 | | | | 119,550 | |

| | 162,564 | | | Loan ID 200578 | | Fixed | | 4.7500 | | | 08/01/40 | | | | 161,423 | |

| | 42,760 | | | Loan ID 200579 | | Fixed | | 4.8750 | | | 05/01/42 | | | | 29,530 | |

| | 151,244 | | | Loan ID 200580 | | Fixed | | 4.1250 | | | 11/01/41 | | | | 148,246 | |

| | 288,044 | | | Loan ID 200586 | | Fixed | | 3.5000 | | | 01/01/43 | | | | 270,498 | |

| | 58,444 | | | Loan ID 200593 | | Fixed | | 3.8750 | | | 06/01/42 | | | | 56,399 | |

| | 34,145 | | | Loan ID 200597 | | Fixed | | 5.6250 | | | 02/01/44 | | | | 34,827 | |

| | 64,620 | | | Loan ID 200604 | | Fixed | | 3.5000 | | | 01/01/43 | | | | 60,665 | |

| | 112,113 | | | Loan ID 200612 | | Fixed | | 4.5000 | | | 02/01/43 | | | | 111,488 | |

| | 307,548 | | | Loan ID 200616 | | Fixed | | 4.8750 | | | 02/01/44 | | | | 311,021 | |

| | 149,275 | | | Loan ID 200630 | | Fixed | | 5.2500 | | | 09/01/43 | | | | 152,261 | |

| | 206,355 | | | Loan ID 200634 | | Fixed | | 4.3750 | | | 01/01/44 | | | | 204,060 | |

| | 106,916 | | | Loan ID 200645 | | Fixed | | 5.0000 | | | 04/01/44 | | | | 108,642 | |

| | 126,857 | | | Loan ID 200649 | | Fixed | | 4.3750 | | | 03/01/44 | | | | 125,320 | |

| | 117,376 | | | Loan ID 200650 | | Fixed | | 4.8750 | | | 05/01/44 | | | | 118,849 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 200,531 | | | Loan ID 200651 | | Fixed | | 3.6250 | | | 07/01/43 | | | $ | 189,610 | |

| | 123,405 | | | Loan ID 200655 | | Fixed | | 3.3750 | | | 05/01/43 | | | | 114,540 | |

| | 165,734 | | | Loan ID 200656 | | Fixed | | 6.8750 | | | 11/01/45 | | | | 157,447 | |

| | 136,936 | | | Loan ID 200657 | | Fixed | | 4.8750 | | | 08/01/51 | | | | 139,009 | |

| | 158,259 | | | Loan ID 200660 | | Fixed | | 5.8750 | | | 03/01/38 | | | | 161,424 | |

| | 190,160 | | | Loan ID 200662 | | Fixed | | 5.0000 | | | 03/01/44 | | | | 193,005 | |

| | 62,435 | | | Loan ID 200663 | | Fixed | | 4.7500 | | | 05/01/44 | | | | 62,915 | |

| | 141,272 | | | Loan ID 200669 | | Fixed | | 5.2500 | | | 04/01/44 | | | | 144,097 | |

| | 42,121 | | | Loan ID 200670 | | Fixed | | 4.3750 | | | 02/01/29 | | | | 41,644 | |

| | 279,921 | | | Loan ID 200674 | | Fixed | | 4.5000 | | | 05/01/44 | | | | 278,790 | |

| | 231,326 | | | Loan ID 200679 | | Fixed | | 5.0000 | | | 04/01/44 | | | | 232,915 | |

| | 172,253 | | | Loan ID 200682 | | Fixed | | 4.8750 | | | 05/01/44 | | | | 174,162 | |

| | 114,639 | | | Loan ID 200684 | | Fixed | | 4.8750 | | | 04/01/44 | | | | 116,118 | |

| | 208,504 | | | Loan ID 200685 | | Fixed | | 4.8750 | | | 05/01/44 | | | | 210,562 | |

| | 200,848 | | | Loan ID 200690 | | Fixed | | 4.2500 | | | 04/01/44 | | | | 197,609 | |

| | 220,774 | | | Loan ID 200692 | | Fixed | | 4.6250 | | | 07/01/44 | | | | 220,531 | |

| | 96,129 | | | Loan ID 200694 | | Fixed | | 4.5000 | | | 09/01/43 | | | | 95,652 | |

| | 42,079 | | | Loan ID 200696 | | Fixed | | 3.7500 | | | 10/01/42 | | | | 40,293 | |

| | 79,293 | | | Loan ID 200700 | | Fixed | | 4.2500 | | | 02/01/44 | | | | 77,876 | |

| | 86,713 | | | Loan ID 200704 | | Fixed | | 4.3750 | | | 03/01/43 | | | | 85,586 | |

| | 45,699 | | | Loan ID 200709 | | Fixed | | 4.3750 | | | 04/01/43 | | | | 45,186 | |

| | 102,444 | | | Loan ID 200710 | | Fixed | | 4.5000 | | | 07/01/44 | | | | 100,009 | |

| | 559,918 | | | Loan ID 200714 | | Fixed | | 4.1750 | | | 11/01/36 | | | | 553,291 | |

| | 183,736 | | | Loan ID 200716 | | ARM | | 3.0900 | | | 08/01/37 | | | | 181,717 | |

| | 128,035 | | | Loan ID 200720 | | ARM | | 3.5000 | | | 04/01/42 | | | | 119,680 | |

| | 142,879 | | | Loan ID 200726 | | Fixed | | 4.3750 | | | 09/01/37 | | | | 107,744 | |

| | 181,656 | | | Loan ID 200732 | | Fixed | | 4.1250 | | | 09/01/27 | | | | 178,836 | |

| | 91,117 | | | Loan ID 200735 | | Fixed | | 4.5000 | | | 06/01/44 | | | | 90,641 | |

| | 131,230 | | | Loan ID 200736 | | Fixed | | 4.7500 | | | 05/01/44 | | | | 129,637 | |

| | 158,654 | | | Loan ID 200742 | | Fixed | | 4.2500 | | | 04/01/43 | | | | 155,703 | |

| | 54,373 | | | Loan ID 200753 | | Fixed | | 5.2500 | | | 05/01/44 | | | | 55,460 | |

| | 47,332 | | | Loan ID 200755 | | Fixed | | 4.2500 | | | 06/01/43 | | | | 46,568 | |

| | 167,910 | | | Loan ID 200756 | | Fixed | | 4.8750 | | | 11/01/43 | | | | 169,883 | |

| | 162,922 | | | Loan ID 200771 | | Fixed | | 4.5000 | | | 04/01/43 | | | | 150,542 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 39,987 | | | Loan ID 200775 | | Fixed | | 4.2500 | | | 04/01/43 | | | $ | 39,286 | |

| | 72,976 | | | Loan ID 200776 | | Fixed | | 4.2500 | | | 03/01/44 | | | | 71,621 | |

| | 48,792 | | | Loan ID 200777 | | Fixed | | 4.7500 | | | 06/01/44 | | | | 48,904 | |

| | 152,633 | | | Loan ID 200781 | | Fixed | | 4.6250 | | | 09/01/44 | | | | 152,131 | |

| | 76,368 | | | Loan ID 200783 | | Fixed | | 4.7500 | | | 09/01/44 | | | | 76,813 | |

| | 101,305 | | | Loan ID 200785 | | Fixed | | 4.5000 | | | 08/01/44 | | | | 100,796 | |

| | 205,690 | | | Loan ID 200786 | | Fixed | | 4.6250 | | | 07/01/44 | | | | 206,208 | |

| | 39,383 | | | Loan ID 200787 | | Fixed | | 4.7500 | | | 09/01/44 | | | | 39,595 | |

| | 184,727 | | | Loan ID 200791 | | Fixed | | 4.8750 | | | 06/01/44 | | | | 186,383 | |

| | 81,569 | | | Loan ID 200795 | | Fixed | | 6.7500 | | | 08/01/36 | | | | 83,200 | |

| | 68,643 | | | Loan ID 200796 | | Fixed | | 5.8800 | | | 12/01/53 | | | | 37,716 | |

| | 55,764 | | | Loan ID 200799 | | Fixed | | 4.0000 | | | 02/05/53 | | | | 53,251 | |

| | 61,051 | | | Loan ID 200800 | | Fixed | | 4.0000 | | | 01/01/53 | | | | 50,643 | |

| | 145,572 | | | Loan ID 200805 | | Fixed | | 4.6250 | | | 07/01/50 | | | | 129,327 | |

| | 53,685 | | | Loan ID 200808 | | Fixed | | 4.2500 | | | 11/01/50 | | | | 44,636 | |

| | 112,093 | | | Loan ID 200809 | | Fixed | | 5.0000 | | | 04/01/50 | | | | 104,007 | |

| | 220,100 | | | Loan ID 200814 | | Fixed | | 8.2500 | | | 07/01/39 | | | | 224,502 | |

| | 271,314 | | | Loan ID 200817 | | Fixed | | 5.0000 | | | 01/01/50 | | | | 240,298 | |

| | 189,069 | | | Loan ID 200821 | | Fixed | | 4.2500 | | | 08/01/44 | | | | 186,049 | |

| | 73,241 | | | Loan ID 200823 | | Fixed | | 4.2500 | | | 09/01/44 | | | | 72,028 | |

| | 200,733 | | | Loan ID 200824 | | Fixed | | 4.2500 | | | 08/01/44 | | | | 197,257 | |

| | 95,814 | | | Loan ID 200826 | | Fixed | | 4.3750 | | | 09/01/44 | | | | 94,557 | |

| | 175,799 | | | Loan ID 200830 | | ARM | | 1.2500 | | | 07/01/44 | | | | 161,870 | |

| | 38,306 | | | Loan ID 200831 | | Fixed | | 4.2500 | | | 10/01/44 | | | | 37,560 | |

| | 303,302 | | | Loan ID 200832 | | Fixed | | 4.2500 | | | 10/01/44 | | | | 292,756 | |

| | 143,807 | | | Loan ID 200834 | | Fixed | | 4.1250 | | | 07/01/43 | | | | 140,468 | |

| | 267,198 | | | Loan ID 200844 | | Fixed | | 4.5000 | | | 07/01/43 | | | | 265,642 | |

| | 177,498 | | | Loan ID 200846 | | Fixed | | 4.3750 | | | 11/01/43 | | | | 175,787 | |

| | 95,196 | | | Loan ID 200853 | | Fixed | | 5.0000 | | | 04/01/37 | | | | 97,091 | |

| | 172,272 | | | Loan ID 200856 | | Fixed | | 6.5000 | | | 06/01/42 | | | | 166,057 | |

| | 248,272 | | | Loan ID 200858 | | Fixed | | 5.0000 | | | 01/01/53 | | | | 253,238 | |

| | 147,383 | | | Loan ID 200860 | | Fixed | | 3.8750 | | | 03/01/52 | | | | 140,275 | |

| | 244,614 | | | Loan ID 200866 | | Fixed | | 3.4000 | | | 05/01/53 | | | | 231,816 | |

| | 105,590 | | | Loan ID 200867 | | Fixed | | 4.5800 | | | 09/01/53 | | | | 105,971 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 170,609 | | | Loan ID 200880 | | Fixed | | 4.2500 | | | 06/01/43 | | | $ | 167,585 | |

| | 53,476 | | | Loan ID 200883 | | Fixed | | 3.3750 | | | 05/01/28 | | | | 49,674 | |

| | 73,925 | | | Loan ID 200886 | | Fixed | | 4.2500 | | | 10/01/44 | | | | 72,621 | |

| | 207,008 | | | Loan ID 200887 | | Fixed | | 4.7500 | | | 09/01/44 | | | | 208,100 | |

| | 186,105 | | | Loan ID 200891 | | Fixed | | 4.2500 | | | 10/01/44 | | | | 182,340 | |

| | 223,061 | | | Loan ID 200892 | | Fixed | | 3.7500 | | | 09/01/43 | | | | 213,123 | |

| | 175,728 | | | Loan ID 200897 | | Fixed | | 4.7500 | | | 10/01/44 | | | | 176,826 | |

| | 357,156 | | | Loan ID 200907 | | ARM | | 3.1400 | | | 08/01/47 | | | | 345,834 | |

| | 98,050 | | | Loan ID 200908 | | Fixed | | 4.0000 | | | 06/01/49 | | | | 96,698 | |

| | 118,315 | | | Loan ID 200909 | | Fixed | | 4.8700 | | | 04/01/47 | | | | 112,400 | |

| | 631,924 | | | Loan ID 200912 | | Fixed | | 4.5000 | | | 03/01/37 | | | | 632,566 | |

| | 54,391 | | | Loan ID 200913 | | Fixed | | 4.2500 | | | 05/01/47 | | | | 53,859 | |

| | 134,500 | | | Loan ID 200914 | | Fixed | | 2.8750 | | | 12/01/47 | | | | 124,683 | |

| | 80,294 | | | Loan ID 200916 | | Fixed | | 4.0000 | | | 10/01/37 | | | | 77,400 | |

| | 149,870 | | | Loan ID 200917 | | Fixed | | 4.8750 | | | 01/01/51 | | | | 152,219 | |

| | 82,847 | | | Loan ID 200921 | | ARM | | 3.6250 | | | 07/01/51 | | | | 81,783 | |

| | 395,395 | | | Loan ID 200922 | | Fixed | | 3.3400 | | | 09/01/53 | | | | 378,433 | |

| | 115,686 | | | Loan ID 200928 | | Fixed | | 4.8000 | | | 02/01/41 | | | | 117,228 | |

| | 176,584 | | | Loan ID 200940 | | Fixed | | 3.2500 | | | 02/01/43 | | | | 162,466 | |

| | 101,642 | | | Loan ID 200941 | | Fixed | | 3.7800 | | | 01/01/43 | | | | 95,373 | |

| | 242,538 | | | Loan ID 200942 | | Fixed | | 4.0000 | | | 04/01/43 | | | | 235,556 | |

| | 94,470 | | | Loan ID 200944 | | Fixed | | 4.5000 | | | 02/01/44 | | | | 93,836 | |

| | 259,334 | | | Loan ID 200947 | | Fixed | | 4.0000 | | | 02/01/43 | | | | 251,881 | |

| | 138,388 | | | Loan ID 200948 | | Fixed | | 4.6250 | | | 05/01/61 | | | | 138,329 | |

| | 248,525 | | | Loan ID 200956 | | Fixed | | 5.0000 | | | 08/01/51 | | | | 253,450 | |

| | 375,262 | | | Loan ID 200959 | | Fixed | | 4.0000 | | | 11/01/42 | | | | 364,776 | |

| | 133,513 | | | Loan ID 200966 | | Fixed | | 4.8750 | | | 07/01/44 | | | | 134,981 | |

| | 330,977 | | | Loan ID 200969 | | Fixed | | 4.8750 | | | 08/01/43 | | | | 334,944 | |

| | 140,499 | | | Loan ID 200974 | | Fixed | | 4.2500 | | | 10/01/44 | | | | 138,095 | |

| | 324,954 | | | Loan ID 200977 | | Fixed | | 4.8750 | | | 09/01/44 | | | | 308,706 | |

| | 152,889 | | | Loan ID 200993 | | Fixed | | 2.0040 | | | 07/15/49 | | | | 131,443 | |

| | 51,121 | | | Loan ID 200996 | | Fixed | | 2.5000 | | | 08/01/48 | | | | 45,121 | |

| | 116,907 | | | Loan ID 201005 | | Fixed | | 4.7500 | | | 07/01/41 | | | | 117,818 | |

| | 38,756 | | | Loan ID 201006 | | Fixed | | 6.8750 | | | 03/01/38 | | | | 39,532 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 83,521 | | | Loan ID 201007 | | Fixed | | 7.1250 | | | 04/01/37 | | | $ | 85,192 | |

| | 71,281 | | | Loan ID 201010 | | Fixed | | 5.5000 | | | 04/01/39 | | | | 71,281 | |

| | 42,157 | | | Loan ID 201012 | | Fixed | | 7.5000 | | | 12/01/38 | | | | 43,000 | |

| | 51,238 | | | Loan ID 201013 | | Fixed | | 7.5000 | | | 12/01/38 | | | | 52,052 | |

| | 102,451 | | | Loan ID 201016 | | Fixed | | 6.5000 | | | 05/01/46 | | | | 104,500 | |

| | 57,848 | | | Loan ID 201022 | | ARM | | 2.3750 | | | 05/01/37 | | | | 54,175 | |

| | 124,316 | | | Loan ID 201023 | | Fixed | | 6.4500 | | | 02/01/36 | | | | 126,802 | |

| | 98,385 | | | Loan ID 201027 | | ARM | | 9.5380 | | | 03/01/37 | | | | 100,353 | |

| | 129,747 | | | Loan ID 201032 | | Fixed | | 4.5000 | | | 11/01/44 | | | | 128,713 | |

| | 76,937 | | | Loan ID 201036 | | Fixed | | 4.3750 | | | 12/01/44 | | | | 76,030 | |

| | 63,645 | | | Loan ID 201037 | | Fixed | | 8.2500 | | | 07/01/39 | | | | 64,918 | |

| | 85,606 | | | Loan ID 201041 | | Fixed | | 3.7500 | | | 11/01/52 | | | | 82,855 | |

| | 103,094 | | | Loan ID 201043 | | Fixed | | 4.0000 | | | 04/01/39 | | | | 98,169 | |

| | 157,435 | | | Loan ID 201044 | | Fixed | | 4.8700 | | | 03/29/37 | | | | 159,854 | |

| | 96,568 | | | Loan ID 201045 | | Fixed | | 3.3750 | | | 07/01/37 | | | | 84,807 | |

| | 276,448 | | | Loan ID 201046 | | Fixed | | 3.0000 | | | 10/01/58 | | | | 155,047 | |

| | 103,107 | | | Loan ID 201047 | | Fixed | | 3.6250 | | | 04/01/53 | | | | 96,306 | |

| | 61,678 | | | Loan ID 201053 | | Fixed | | 3.8600 | | | 07/01/53 | | | | 60,085 | |

| | 189,302 | | | Loan ID 201054 | | Fixed | | 2.4000 | | | 05/17/50 | | | | 162,686 | |

| | 144,947 | | | Loan ID 201057 | | Fixed | | 4.3750 | | | 01/01/50 | | | | 144,483 | |

| | 103,381 | | | Loan ID 201058 | | Fixed | | 4.2500 | | | 08/01/37 | | | | 102,367 | |

| | 92,666 | | | Loan ID 201060 | | ARM | | 2.3750 | | | 07/01/35 | | | | 89,479 | |

| | 77,154 | | | Loan ID 201061 | | Fixed | | 5.0000 | | | 02/01/50 | | | | 74,397 | |

| | 106,482 | | | Loan ID 201063 | | Fixed | | 4.0000 | | | 09/01/47 | | | | 104,241 | |

| | 213,294 | | | Loan ID 201066 | | Fixed | | 4.2500 | | | 12/01/46 | | | | 211,369 | |

| | 399,371 | | | Loan ID 201067 | | Fixed | | 4.7500 | | | 01/01/44 | | | | 401,987 | |

| | 61,739 | | | Loan ID 201069 | | Fixed | | 4.6250 | | | 12/01/44 | | | | 61,812 | |

| | 71,016 | | | Loan ID 201072 | | Fixed | | 3.5000 | | | 03/01/28 | | | | 66,717 | |

| | 86,282 | | | Loan ID 201075 | | Fixed | | 4.3750 | | | 10/01/44 | | | | 85,230 | |

| | 214,175 | | | Loan ID 201084 | | Fixed | | 5.0000 | | | 08/01/38 | | | | 200,469 | |

| | 144,272 | | | Loan ID 201091 | | Fixed | | 4.1250 | | | 01/01/45 | | | | 140,523 | |

| | 232,164 | | | Loan ID 201092 | | Fixed | | 5.2500 | | | 04/01/46 | | | | 236,807 | |

| | 128,874 | | | Loan ID 201093 | | Fixed | | 4.1250 | | | 02/01/45 | | | | 116,459 | |

| | 320,361 | | | Loan ID 201101 | | Fixed | | 4.6250 | | | 03/01/45 | | | | 314,714 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 137,191 | | | Loan ID 201103 | | ARM | | 2.7500 | | | 05/01/44 | | | $ | 130,828 | |

| | 146,971 | | | Loan ID 201104 | | Fixed | | 4.3750 | | | 04/01/45 | | | | 145,321 | |

| | 66,718 | | | Loan ID 201107 | | Fixed | | 5.1500 | | | 02/01/36 | | | | 68,053 | |

| | 148,024 | | | Loan ID 201111 | | Fixed | | 4.8750 | | | 04/01/50 | | | | 136,440 | |

| | 75,287 | | | Loan ID 201113 | | Fixed | | 5.7500 | | | 12/01/52 | | | | 76,793 | |

| | 114,669 | | | Loan ID 201114 | | Fixed | | 8.0870 | | | 05/01/54 | | | | 116,962 | |

| | 471,032 | | | Loan ID 201115 | | Fixed | | 4.0000 | | | 02/01/51 | | | | 460,868 | |

| | 74,854 | | | Loan ID 201122 | | Fixed | | 4.7500 | | | 11/01/48 | | | | 75,801 | |

| | 208,195 | | | Loan ID 201124 | | Fixed | | 4.7500 | | | 04/01/40 | | | | 210,373 | |

| | 68,319 | | | Loan ID 201127 | | ARM | | 2.5000 | | | 04/01/37 | | | | 65,764 | |

| | 105,030 | | | Loan ID 201130 | | Fixed | | 4.8500 | | | 12/01/37 | | | | 106,019 | |

| | 114,091 | | | Loan ID 201131 | | Fixed | | 8.2500 | | | 05/01/53 | | | | 116,372 | |

| | 155,645 | | | Loan ID 201132 | | Fixed | | 4.2500 | | | 07/01/37 | | | | 142,367 | |

| | 178,092 | | | Loan ID 201134 | | Fixed | | 4.6250 | | | 10/01/53 | | | | 166,242 | |

| | 165,677 | | | Loan ID 201139 | | Fixed | | 3.0000 | | | 11/01/53 | | | | 151,993 | |

| | 78,182 | | | Loan ID 201143 | | Fixed | | 3.5000 | | | 11/01/37 | | | | 69,461 | |

| | 124,581 | | | Loan ID 201146 | | Fixed | | 4.8750 | | | 08/01/54 | | | | 125,398 | |

| | 103,607 | | | Loan ID 201147 | | Fixed | | 4.1250 | | | 11/01/51 | | | | 98,026 | |

| | 86,193 | | | Loan ID 201148 | | Fixed | | 3.9500 | | | 10/01/42 | | | | 84,763 | |

| | 308,169 | | | Loan ID 201149 | | Fixed | | 5.0000 | | | 05/01/58 | | | | 165,731 | |

| | 88,407 | | | Loan ID 201155 | | Fixed | | 5.0000 | | | 11/01/53 | | | | 58,688 | |

| | 60,393 | | | Loan ID 201156 | | Fixed | | 5.0000 | | | 04/01/50 | | | | 55,348 | |

| | 187,869 | | | Loan ID 201160 | | Fixed | | 4.9200 | | | 10/01/49 | | | | 176,328 | |

| | 357,294 | | | Loan ID 201163 | | Fixed | | 4.7500 | | | 12/01/49 | | | | 305,824 | |

| | 156,759 | | | Loan ID 201164 | | Fixed | | 4.2500 | | | 11/01/51 | | | | 153,560 | |

| | 400,964 | | | Loan ID 201168 | | Fixed | | 3.8750 | | | 04/01/52 | | | | 370,421 | |

| | 50,731 | | | Loan ID 201170 | | Fixed | | 4.3750 | | | 07/01/37 | | | | 50,524 | |

| | 101,832 | | | Loan ID 201173 | | Fixed | | 4.2800 | | | 11/01/47 | | | | 79,307 | |

| | 121,955 | | | Loan ID 201176 | | Fixed | | 4.2500 | | | 07/01/53 | | | | 121,203 | |

| | 289,697 | | | Loan ID 201179 | | Fixed | | 4.7500 | | | 05/01/51 | | | | 264,802 | |

| | 252,045 | | | Loan ID 201181 | | Fixed | | 4.5000 | | | 04/01/34 | | | | 253,198 | |

| | 124,733 | | | Loan ID 201183 | | Fixed | | 3.5000 | | | 10/01/52 | | | | 119,301 | |

| | 58,748 | | | Loan ID 201184 | | Fixed | | 4.0000 | | | 06/01/49 | | | | 57,903 | |

| | 230,649 | | | Loan ID 201185 | | Fixed | | 7.2500 | | | 10/01/53 | | | | 235,262 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 76,151 | | | Loan ID 201187 | | Fixed | | 5.0000 | | | 11/01/48 | | | $ | 55,480 | |

| | 574,603 | | | Loan ID 201196 | | Fixed | | 4.3750 | | | 11/01/36 | | | | 572,349 | |

| | 304,867 | | | Loan ID 201199 | | Fixed | | 5.1250 | | | 11/01/46 | | | | 310,965 | |

| | 135,489 | | | Loan ID 201205 | | Fixed | | 4.6250 | | | 01/01/45 | | | | 135,463 | |

| | 105,232 | | | Loan ID 201208 | | Fixed | | 4.6250 | | | 04/01/45 | | | | 104,990 | |

| | 164,310 | | | Loan ID 201209 | | Fixed | | 4.2500 | | | 04/01/45 | | | | 161,517 | |

| | 387,912 | | | Loan ID 201212 | | Fixed | | 4.6250 | | | 03/01/61 | | | | 388,359 | |

| | 180,471 | | | Loan ID 201213 | | Fixed | | 4.8750 | | | 08/01/44 | | | | 181,761 | |

| | 490,475 | | | Loan ID 201214 | | ARM | | 2.7500 | | | 09/01/43 | | | | 463,232 | |

| | 57,471 | | | Loan ID 201221 | | Fixed | | 3.2500 | | | 05/01/43 | | | | 25,578 | |

| | 44,580 | | | Loan ID 201222 | | Fixed | | 5.1250 | | | 01/01/45 | | | | 45,272 | |

| | 144,697 | | | Loan ID 201240 | | Fixed | | 4.2500 | | | 10/01/45 | | | | 141,368 | |

| | 272,073 | | | Loan ID 201241 | | Fixed | | 4.3750 | | | 07/01/45 | | | | 269,547 | |

| | 101,178 | | | Loan ID 201243 | | Fixed | | 4.6250 | | | 11/01/45 | | | | 101,160 | |

| | 367,461 | | | Loan ID 201244 | | Fixed | | 4.5000 | | | 06/01/45 | | | | 365,869 | |

| | 104,139 | | | Loan ID 201245 | | Fixed | | 4.7500 | | | 08/01/44 | | | | 104,926 | |

| | 92,673 | | | Loan ID 201248 | | Fixed | | 4.8750 | | | 07/01/44 | | | | 93,481 | |

| | 457,480 | | | Loan ID 201249 | | Fixed | | 4.6250 | | | 03/01/59 | | | | 455,452 | |

| | 194,203 | | | Loan ID 201254 | | Fixed | | 7.2500 | | | 05/01/60 | | | | 198,087 | |

| | 215,167 | | | Loan ID 201255 | | ARM | | 6.7500 | | | 06/01/35 | | | | 219,470 | |

| | 158,910 | | | Loan ID 201260 | | Fixed | | 4.7500 | | | 09/01/45 | | | | 159,502 | |

| | 46,218 | | | Loan ID 201263 | | Fixed | | 4.7500 | | | 10/01/45 | | | | 46,402 | |

| | 134,986 | | | Loan ID 201266 | | Fixed | | 4.5000 | | | 02/01/46 | | | | 133,749 | |

| | 138,284 | | | Loan ID 201270 | | Fixed | | 4.1250 | | | 02/01/45 | | | | 135,004 | |

| | 233,622 | | | Loan ID 201271 | | Fixed | | 4.5000 | | | 06/01/45 | | | | 232,601 | |

| | 222,957 | | | Loan ID 201273 | | Fixed | | 4.5000 | | | 12/01/45 | | | | 220,875 | |

| | 199,689 | | | Loan ID 201274 | | Fixed | | 4.1250 | | | 10/01/45 | | | | 194,607 | |

| | 23,213 | | | Loan ID 201285 | | Fixed | | 4.6250 | | | 11/01/28 | | | | 23,677 | |

| | 283,805 | | | Loan ID 201291 | | Fixed | | 5.0000 | | | 08/01/45 | | | | 263,195 | |

| | 113,638 | | | Loan ID 201294 | | Fixed | | 4.6250 | | | 02/01/46 | | | | 111,856 | |

| | 707,440 | | | Loan ID 201296 | | Fixed | | 4.2500 | | | 02/01/46 | | | | 690,912 | |

| | 66,880 | | | Loan ID 201301 | | Fixed | | 4.5500 | | | 10/01/44 | | | | 66,649 | |

| | 125,215 | | | Loan ID 201302 | | Fixed | | 4.2500 | | | 05/01/45 | | | | 122,773 | |

| | 137,229 | | | Loan ID 201305 | | Fixed | | 4.6250 | | | 08/01/44 | | | | 137,268 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 107,527 | | | Loan ID 201306 | | Fixed | | 3.8750 | | | 09/01/45 | | | $ | 103,209 | |

| | 163,889 | | | Loan ID 201307 | | Fixed | | 4.2500 | | | 10/01/48 | | | | 160,945 | |

| | 57,800 | | | Loan ID 201308 | | Fixed | | 4.6250 | | | 11/01/45 | | | | 57,652 | |

| | 149,805 | | | Loan ID 201309 | | Fixed | | 4.0000 | | | 09/01/45 | | | | 145,185 | |

| | 299,638 | | | Loan ID 201313 | | Fixed | | 4.6250 | | | 01/01/46 | | | | 299,869 | |

| | 150,771 | | | Loan ID 201316 | | Fixed | | 4.5000 | | | 02/01/46 | | | | 149,815 | |

| | 159,252 | | | Loan ID 201319 | | Fixed | | 4.3750 | | | 10/01/45 | | | | 157,441 | |

| | 126,903 | | | Loan ID 201324 | | Fixed | | 5.2500 | | | 04/01/46 | | | | 129,442 | |

| | 164,463 | | | Loan ID 201326 | | Fixed | | 4.6250 | | | 03/01/46 | | | | 164,468 | |

| | 176,813 | | | Loan ID 201328 | | Fixed | | 4.2500 | | | 11/01/45 | | | | 111,684 | |

| | 342,480 | | | Loan ID 201333 | | Fixed | | 3.8750 | | | 11/01/45 | | | | 328,270 | |

| | 177,920 | | | Loan ID 201336 | | Fixed | | 4.7500 | | | 01/01/46 | | | | 175,243 | |

| | 222,635 | | | Loan ID 201350 | | Fixed | | 4.0000 | | | 06/01/45 | | | | 161,225 | |

| | 61,114 | | | Loan ID 201352 | | Fixed | | 4.8750 | | | 03/01/45 | | | | 61,505 | |

| | 464,928 | | | Loan ID 201354 | | Fixed | | 3.3750 | | | 07/01/46 | | | | 449,180 | |

| | 126,349 | | | Loan ID 201355 | | Fixed | | 5.2500 | | | 12/01/45 | | | | 128,876 | |

| | 140,821 | | | Loan ID 201358 | | Fixed | | 4.8750 | | | 07/01/45 | | | | 142,331 | |

| | 104,314 | | | Loan ID 201364 | | Fixed | | 3.8750 | | | 04/01/46 | | | | 100,112 | |

| | 316,063 | | | Loan ID 201365 | | Fixed | | 4.2500 | | | 10/01/45 | | | | 309,078 | |

| | 169,946 | | | Loan ID 201370 | | Fixed | | 4.2500 | | | 07/01/46 | | | | 166,311 | |

| | 94,066 | | | Loan ID 201371 | | Fixed | | 4.1250 | | | 04/01/46 | | | | 91,119 | |

| | 243,719 | | | Loan ID 201372 | | Fixed | | 4.6250 | | | 08/01/46 | | | | 243,638 | |

| | 134,075 | | | Loan ID 201375 | | Fixed | | 4.5000 | | | 06/01/45 | | | | 133,477 | |

| | 255,023 | | | Loan ID 201377 | | Fixed | | 3.8750 | | | 05/01/46 | | | | 251,834 | |

| | 295,834 | | | Loan ID 201381 | | Fixed | | 4.8750 | | | 07/01/45 | | | | 299,111 | |

| | 130,097 | | | Loan ID 201385 | | Fixed | | 4.6250 | | | 12/01/45 | | | | 130,097 | |

| | 216,000 | | | Loan ID 201390 | | Fixed | | 5.1250 | | | 09/01/45 | | | | 220,320 | |

| | 371,940 | | | Loan ID 201391 | | Fixed | | 5.1250 | | | 10/01/45 | | | | 371,391 | |

| | 406,399 | | | Loan ID 201393 | | Fixed | | 3.7500 | | | 04/01/56 | | | | 402,921 | |

| | 69,665 | | | Loan ID 201394 | | Fixed | | 6.7000 | | | 06/01/34 | | | | 71,058 | |

| | 80,770 | | | Loan ID 201395 | | Fixed | | 6.3000 | | | 07/01/44 | | | | 17,583 | |

| | 80,327 | | | Loan ID 201400 | | Fixed | | 4.7500 | | | 07/01/44 | | | | 80,868 | |

| | 84,272 | | | Loan ID 201401 | | Fixed | | 4.7500 | | | 10/01/44 | | | | 84,814 | |

| | 87,981 | | | Loan ID 201403 | | Fixed | | 4.7500 | | | 08/01/44 | | | | 79,128 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 126,261 | | | Loan ID 201404 | | Fixed | | 4.7500 | | | 10/01/44 | | | $ | 126,401 | |

| | 67,313 | | | Loan ID 201405 | | Fixed | | 5.2500 | | | 08/01/44 | | | | 68,660 | |

| | 51,310 | | | Loan ID 201406 | | Fixed | | 4.2500 | | | 06/01/46 | | | | 50,123 | |

| | 227,789 | | | Loan ID 201407 | | Fixed | | 4.8750 | | | 01/01/46 | | | | 230,476 | |

| | 153,743 | | | Loan ID 201411 | | Fixed | | 4.7500 | | | 12/01/45 | | | | 154,544 | |

| | 134,726 | | | Loan ID 201412 | | Fixed | | 5.7500 | | | 12/01/45 | | | | 137,421 | |

| | 315,251 | | | Loan ID 201413 | | Fixed | | 4.5000 | | | 07/01/45 | | | | 313,949 | |

| | 68,811 | | | Loan ID 201414 | | Fixed | | 4.2500 | | | 07/01/44 | | | | 64,230 | |

| | 51,282 | | | Loan ID 201415 | | Fixed | | 8.0000 | | | 04/01/34 | | | | 52,308 | |

| | 55,638 | | | Loan ID 201417 | | Fixed | | 6.0000 | | | 08/01/37 | | | | 56,750 | |

| | 38,299 | | | Loan ID 201419 | | Fixed | | 10.0000 | | | 11/01/33 | | | | 39,065 | |

| | 53,768 | | | Loan ID 201422 | | Fixed | | 4.6250 | | | 10/01/46 | | | | 53,406 | |

| | 500,901 | | | Loan ID 201428 | | ARM | | 2.5000 | | | 04/01/45 | | | | 474,176 | |

| | 92,399 | | | Loan ID 201434 | | Fixed | | 4.3750 | | | 06/01/46 | | | | 91,298 | |

| | 84,528 | | | Loan ID 201436 | | Fixed | | 4.3750 | | | 05/01/45 | | | | 83,519 | |

| | 127,376 | | | Loan ID 201437 | | Fixed | | 4.7500 | | | 05/01/46 | | | | 43,298 | |

| | 168,824 | | | Loan ID 201439 | | Fixed | | 5.0000 | | | 12/01/45 | | | | 171,622 | |

| | 299,996 | | | Loan ID 201440 | | Fixed | | 4.6250 | | | 07/01/46 | | | | 187,409 | |

| | 281,518 | | | Loan ID 201442 | | Fixed | | 4.8750 | | | 12/01/45 | | | | 283,792 | |

| | 47,869 | | | Loan ID 201444 | | Fixed | | 4.5000 | | | 11/01/44 | | | | 47,489 | |

| | 237,305 | | | Loan ID 201447 | | Fixed | | 4.8750 | | | 10/01/44 | | | | 239,375 | |

| | 86,369 | | | Loan ID 201449 | | Fixed | | 4.0000 | | | 08/01/44 | | | | 83,632 | |

| | 209,427 | | | Loan ID 201451 | | Fixed | | 4.2500 | | | 06/01/45 | | | | 205,185 | |

| | 219,960 | | | Loan ID 201458 | | Fixed | | 3.8750 | | | 09/01/46 | | | | 206,394 | |

| | 252,345 | | | Loan ID 201461 | | Fixed | | 4.1250 | | | 12/01/44 | | | | 240,382 | |

| | 279,991 | | | Loan ID 201464 | | Fixed | | 4.3750 | | | 06/01/45 | | | | 271,452 | |

| | 95,747 | | | Loan ID 201465 | | Fixed | | 5.1250 | | | 12/01/44 | | | | 97,458 | |

| | 262,438 | | | Loan ID 201470 | | Fixed | | 4.3750 | | | 10/01/44 | | | | 258,890 | |

| | 210,508 | | | Loan ID 201471 | | Fixed | | 4.5000 | | | 01/01/45 | | | | 209,054 | |

| | 287,147 | | | Loan ID 201473 | | Fixed | | 4.5000 | | | 02/01/45 | | | | 286,046 | |

| | 91,119 | | | Loan ID 201475 | | ARM | | 6.6250 | | | 09/01/36 | | | | 10,806 | |

| | 133,930 | | | Loan ID 201476 | | ARM | | 8.5000 | | | 02/01/37 | | | | 127,234 | |

| | 75,471 | | | Loan ID 201477 | | Fixed | | 6.7500 | | | 11/01/36 | | | | 76,981 | |

| | 100,790 | | | Loan ID 201478 | | Fixed | | 4.6250 | | | 10/01/45 | | | | 100,683 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 140,433 | | | Loan ID 201482 | | Fixed | | 4.6250 | | | 02/01/51 | | | $ | 139,763 | |

| | 277,606 | | | Loan ID 201483 | | Fixed | | 4.1250 | | | 12/01/45 | | | | 269,926 | |

| | 71,864 | | | Loan ID 201484 | | Fixed | | 4.5000 | | | 10/01/46 | | | | 71,091 | |

| | 57,001 | | | Loan ID 201485 | | Fixed | | 5.7500 | | | 03/01/38 | | | | 58,141 | |

| | 157,767 | | | Loan ID 201487 | | Fixed | | 4.6250 | | | 02/01/52 | | | | 160,922 | |

| | 86,392 | | | Loan ID 201489 | | Fixed | | 4.7500 | | | 03/01/46 | | | | 86,726 | |

| | 72,708 | | | Loan ID 201499 | | Fixed | | 4.7500 | | | 05/01/45 | | | | 73,294 | |

| | 99,246 | | | Loan ID 201502 | | Fixed | | 5.2500 | | | 04/01/44 | | | | 101,231 | |

| | 140,316 | | | Loan ID 201503 | | Fixed | | 5.0000 | | | 07/01/46 | | | | 142,516 | |

| | 423,189 | | | Loan ID 201504 | | Fixed | | 4.5000 | | | 07/01/45 | | | | 421,301 | |

| | 86,598 | | | Loan ID 201505 | | ARM | | 4.0000 | | | 09/01/46 | | | | 86,684 | |

| | 289,339 | | | Loan ID 201506 | | Fixed | | 5.0000 | | | 02/01/47 | | | | 293,781 | |

| | 210,352 | | | Loan ID 201508 | | Fixed | | 5.0000 | | | 02/01/47 | | | | 213,977 | |

| | 116,578 | | | Loan ID 201513 | | Fixed | | 4.0000 | | | 01/01/46 | | | | 116,578 | |

| | 71,817 | | | Loan ID 201515 | | Fixed | | 5.1250 | | | 04/01/47 | | | | 72,704 | |

| | 90,291 | | | Loan ID 201519 | | Fixed | | 4.7500 | | | 09/01/45 | | | | 90,947 | |

| | 74,956 | | | Loan ID 201523 | | Fixed | | 5.1250 | | | 07/01/45 | | | | 76,424 | |

| | 365,667 | | | Loan ID 201533 | | Fixed | | 4.7500 | | | 05/01/46 | | | | 365,843 | |

| | 39,950 | | | Loan ID 201534 | | Fixed | | 4.8750 | | | 05/01/47 | | | | 40,125 | |

| | 313,851 | | | Loan ID 201535 | | Fixed | | 4.8750 | | | 08/01/47 | | | | 313,851 | |

| | 191,104 | | | Loan ID 201551 | | Fixed | | 4.5000 | | | 02/01/47 | | | | 157,881 | |

| | 129,795 | | | Loan ID 201552 | | Fixed | | 4.0000 | | | 08/01/47 | | | | 129,795 | |

| | 45,436 | | | Loan ID 201556 | | Fixed | | 4.9900 | | | 12/01/47 | | | | 46,030 | |

| | 125,921 | | | Loan ID 201558 | | Fixed | | 4.5000 | | | 08/01/47 | | | | 125,921 | |

| | 100,663 | | | Loan ID 201579 | | Fixed | | 4.7500 | | | 12/01/36 | | | | 100,964 | |

| | 80,979 | | | Loan ID 201581 | | Fixed | | 4.1250 | | | 10/01/46 | | | | 78,896 | |

| | 82,105 | | | Loan ID 201583 | | Fixed | | 5.2500 | | | 08/01/47 | | | | 82,105 | |

| | 42,604 | | | Loan ID 201585 | | Fixed | | 5.5000 | | | 03/01/48 | | | | 43,456 | |

| | 368,517 | | | Loan ID 201586 | | Fixed | | 4.6250 | | | 05/01/47 | | | | 365,099 | |

| | 299,061 | | | Loan ID 201587 | | Fixed | | 4.3750 | | | 01/01/48 | | | | 294,425 | |

| | 34,192 | | | Loan ID 201589 | | Fixed | | 5.3750 | | | 06/01/48 | | | | 34,848 | |

| | 138,286 | | | Loan ID 201590 | | Fixed | | 5.2000 | | | 05/01/48 | | | | 83,535 | |

| | 303,727 | | | Loan ID 201591 | | Fixed | | 5.3750 | | | 08/01/48 | | | | 309,801 | |

| | 63,206 | | | Loan ID 201598 | | Fixed | | 6.0000 | | | 01/01/37 | | | | 64,471 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 326,185 | | | Loan ID 201599 | | Fixed | | 5.0000 | | | 07/01/38 | | | $ | 249,747 | |

| | 44,013 | | | Loan ID 201600 | | Fixed | | 6.0000 | | | 01/01/36 | | | | 40,829 | |

| | 34,603 | | | Loan ID 201602 | | Fixed | | 5.0000 | | | 04/20/32 | | | | 35,295 | |

| | 58,454 | | | Loan ID 201604 | | Fixed | | 8.5000 | | | 01/01/48 | | | | 48,860 | |

| | 67,431 | | | Loan ID 201605 | | Fixed | | 8.7500 | | | 03/01/48 | | | | 68,779 | |

| | 88,284 | | | Loan ID 201606 | | Fixed | | 9.9900 | | | 05/01/48 | | | | 90,050 | |

| | 43,017 | | | Loan ID 201610 | | Fixed | | 9.9900 | | | 07/01/48 | | | | 8,089 | |

| | 58,983 | | | Loan ID 201611 | | Fixed | | 9.9900 | | | 07/01/48 | | | | 10,636 | |

| | 253,556 | | | Loan ID 201612 | | Fixed | | 8.9900 | | | 10/01/25 | | | | 258,627 | |

| | 493,192 | | | Loan ID 201615 | | Fixed | | 10.5000 | | | 01/01/22 | | | | 503,056 | |

| | 29,217 | | | Loan ID 201624 | | Fixed | | 11.0000 | | | 07/22/28 | | | | 27,757 | |

| | 42,754 | | | Loan ID 201627 | | Fixed | | 10.4500 | | | 02/19/47 | | | | 43,609 | |

| | 48,825 | | | Loan ID 201628 | | Fixed | | 11.0000 | | | 07/25/40 | | | | 49,802 | |

| | 36,864 | | | Loan ID 201629 | | Fixed | | 11.0000 | | | 03/06/33 | | | | 36,864 | |

| | 46,187 | | | Loan ID 201630(a) | | Fixed | | 9.9500 | | | 01/28/20 | | | | 43,878 | |

| | 42,247 | | | Loan ID 201631 | | Fixed | | 9.9500 | | | 07/25/31 | | | | 40,134 | |

| | 64,026 | | | Loan ID 201634 | | Fixed | | 7.9500 | | | 02/28/48 | | | | 60,824 | |

| | 64,724 | | | Loan ID 201635 | | Fixed | | 9.9500 | | | 03/14/46 | | | | 66,018 | |

| | 74,835 | | | Loan ID 201636 | | Fixed | | 9.4500 | | | 05/13/31 | | | | 76,332 | |

| | 97,809 | | | Loan ID 201637 | | Fixed | | 11.0000 | | | 05/22/45 | | | | 99,766 | |

| | 137,453 | | | Loan ID 201638 | | Fixed | | 8.5000 | | | 09/19/44 | | | | 140,202 | |

| | 315,769 | | | Loan ID 201639 | | Fixed | | 5.0000 | | | 09/01/48 | | | | 315,769 | |

| | 336,572 | | | Loan ID 201640 | | Fixed | | 5.1250 | | | 04/01/49 | | | | 341,416 | |

| | 158,632 | | | Loan ID 201641(a) | | DSI | | 10.5000 | | | 06/01/20 | | | | 150,700 | |

| | 669,302 | | | Loan ID 201645(a) | | Fixed | | 8.0000 | | | 07/01/20 | | | | 104,172 | |

| | 40,318 | | | Loan ID 201647 | | Fixed | | 6.0000 | | | 10/01/31 | | | | 40,034 | |

| | 30,481 | | | Loan ID 201648 | | Fixed | | 7.1500 | | | 08/14/30 | | | | 26,203 | |

| | 53,823 | | | Loan ID 201649 | | Fixed | | 4.8000 | | | 02/20/30 | | | | 54,758 | |

| | 36,032 | | | Loan ID 201650 | | Fixed | | 7.0000 | | | 11/14/31 | | | | 36,753 | |

| | 49,853 | | | Loan ID 201651 | | Fixed | | 7.0000 | | | 12/01/36 | | | | 34,086 | |

| | 247,013 | | | Loan ID 201652 | | Fixed | | 5.0000 | | | 10/01/36 | | | | 115,615 | |

| | 194,023 | | | Loan ID 201653 | | Fixed | | 4.2500 | | | 06/01/48 | | | | 194,023 | |

| | 434,849 | | | Loan ID 201654 | | Fixed | | 4.8750 | | | 07/01/49 | | | | 438,817 | |

| | 146,040 | | | Loan ID 201655 | | Fixed | | 7.7000 | | | 01/01/49 | | | | 148,961 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 118,938 | | | Loan ID 201656 | | Fixed | | 4.6250 | | | 06/01/49 | | | $ | 117,412 | |

| | 241,523 | | | Loan ID 201657 | | Fixed | | 5.2500 | | | 11/01/48 | | | | 246,353 | |

| | 81,666 | | | Loan ID 201661 | | Fixed | | 5.5000 | | | 08/01/49 | | | | 82,503 | |

| | 128,232 | | | Loan ID 201662 | | Fixed | | 5.3750 | | | 09/01/48 | | | | 130,407 | |

| | 417,162 | | | Loan ID 201663 | | Fixed | | 4.7500 | | | 10/01/48 | | | | 417,162 | |

| | 19,186 | | | Loan ID 201664 | | Fixed | | 10.0000 | | | 08/01/33 | | | | 19,186 | |

| | 41,196 | | | Loan ID 201665 | | Fixed | | 9.9900 | | | 08/01/48 | | | | 42,020 | |

| | 17,960 | | | Loan ID 201666 | | Fixed | | 10.0000 | | | 06/01/33 | | | | 18,319 | |

| | 16,620 | | | Loan ID 201667 | | Fixed | | 10.0000 | | | 07/01/33 | | | | 16,952 | |

| | 15,591 | | | Loan ID 201668 | | Fixed | | 9.7500 | | | 11/01/33 | | | | 15,903 | |

| | 55,350 | | | Loan ID 201670 | | Fixed | | 8.0000 | | | 09/15/48 | | | | 55,350 | |

| | 22,544 | | | Loan ID 201671 | | Fixed | | 9.0000 | | | 09/15/48 | | | | 22,544 | |

| | 21,037 | | | Loan ID 201672 | | Fixed | | 9.9000 | | | 10/15/48 | | | | 21,458 | |

| | 51,243 | | | Loan ID 201673 | | Fixed | | 9.9900 | | | 06/01/48 | | | | 52,268 | |

| | 23,808 | | | Loan ID 201674 | | Fixed | | 9.9000 | | | 12/01/48 | | | | 24,284 | |

| | 111,143 | | | Loan ID 201676 | | Fixed | | 9.6250 | | | 10/01/48 | | | | 113,366 | |

| | 79,678 | | | Loan ID 201677 | | Fixed | | 9.2500 | | | 11/01/48 | | | | 81,271 | |

| | 23,854 | | | Loan ID 201678 | | Fixed | | 10.0000 | | | 08/01/48 | | | | 24,331 | |

| | 42,464 | | | Loan ID 201679 | | Fixed | | 7.7000 | | | 03/01/47 | | | | 43,313 | |

| | 39,219 | | | Loan ID 201680 | | Fixed | | 9.9000 | | | 09/15/48 | | | | 40,003 | |

| | 176,056 | | | Loan ID 201682 | | Fixed | | 5.0000 | | | 07/01/48 | | | | 96,547 | |

| | 401,670 | | | Loan ID 201684 | | Fixed | | 4.5000 | | | 08/01/49 | | | | 396,414 | |

| | 283,403 | | | Loan ID 201685 | | Fixed | | 5.5000 | | | 02/01/49 | | | | 289,071 | |

| | 99,972 | | | Loan ID 201686 | | Fixed | | 4.2500 | | | 07/01/49 | | | | 97,025 | |

| | 105,413 | | | Loan ID 201687 | | Fixed | | 5.5000 | | | 07/01/48 | | | | 92,899 | |

| | 205,040 | | | Loan ID 201689 | | Fixed | | 4.5000 | | | 04/01/49 | | | | 202,504 | |

| | 162,144 | | | Loan ID 201692 | | Fixed | | 8.4900 | | | 11/01/29 | | | | 165,387 | |

| | 302,227 | | | Loan ID 201695 | | Fixed | | 8.9000 | | | 12/01/21 | | | | 308,271 | |

| | 64,423 | | | Loan ID 201696 | | Fixed | | 5.1250 | | | 10/01/48 | | | | 65,637 | |

| | 123,279 | | | Loan ID 201697 | | Fixed | | 6.1250 | | | 04/01/49 | | | | 125,745 | |

| | 82,484 | | | Loan ID 201698 | | Fixed | | 4.3750 | | | 12/01/47 | | | | 80,672 | |

| | 263,036 | | | Loan ID 201699 | | Fixed | | 5.5220 | | | 09/01/49 | | | | 268,297 | |

| | 320,544 | | | Loan ID 201700 | | Fixed | | 6.1250 | | | 06/01/49 | | | | 326,955 | |

| | 61,901 | | | Loan ID 201701 | | Fixed | | 5.0000 | | | 08/01/49 | | | | 61,921 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 53,667 | | | Loan ID 201703 | | Fixed | | 6.6000 | | | 12/01/48 | | | $ | 54,741 | |

| | 177,622 | | | Loan ID 201707 | | Fixed | | 4.8750 | | | 08/01/49 | | | | 177,392 | |

| | 203,973 | | | Loan ID 201709 | | Fixed | | 5.3250 | | | 09/01/49 | | | | 205,185 | |

| | 146,189 | | | Loan ID 201710 | | Fixed | | 6.7000 | | | 11/01/49 | | | | 153,498 | |

| | 720,051 | | | Loan ID 201711 | | Fixed | | 4.8750 | | | 10/01/49 | | | | 719,354 | |

| | 183,604 | | | Loan ID 201713 | | Fixed | | 10.1110 | | | 12/01/49 | | | | 174,424 | |

| | 111,083 | | | Loan ID 201715 | | Fixed | | 10.1300 | | | 12/01/49 | | | | 113,305 | |

| | 236,189 | | | Loan ID 201716 | | Fixed | | 10.1500 | | | 12/01/49 | | | | 240,913 | |

| | 433,412 | | | Loan ID 201717 | | Fixed | | 6.5000 | | | 12/01/48 | | | | 442,080 | |

| | 116,207 | | | Loan ID 201719 | | Fixed | | 4.7500 | | | 09/01/49 | | | | 116,207 | |

| | 136,579 | | | Loan ID 201720 | | Fixed | | 4.3750 | | | 04/01/49 | | | | 134,689 | |

| | 248,381 | | | Loan ID 201724 | | Fixed | | 5.3750 | | | 01/01/49 | | | | 138,941 | |

| | 76,403 | | | Loan ID 201725 | | Fixed | | 8.4900 | | | 12/01/22 | | | | 72,583 | |

| | 55,011 | | | Loan ID 201726 | | Fixed | | 8.4900 | | | 12/01/22 | | | | 52,261 | |

| | 73,955 | | | Loan ID 201728 | | Fixed | | 9.4900 | | | 01/01/22 | | | | 75,434 | |

| | 127,498 | | | Loan ID 201732 | | Fixed | | 5.1250 | | | 05/01/47 | | | | 127,660 | |

| | 77,813 | | | Loan ID 201733 | | Fixed | | 5.2500 | | | 04/01/44 | | | | 79,369 | |

| | 125,501 | | | Loan ID 201739 | | ARM | | 7.1250 | | | 04/01/48 | | | | 111,981 | |

| | 226,960 | | | Loan ID 201741 | | ARM | | 8.0000 | | | 07/01/48 | | | | 231,500 | |

| | 139,998 | | | Loan ID 201743 | | Fixed | | 5.4990 | | | 09/01/48 | | | | 142,798 | |

| | 291,810 | | | Loan ID 201744 | | Fixed | | 5.6250 | | | 05/01/49 | | | | 291,810 | |

| | 367,574 | | | Loan ID 201746 | | Fixed | | 4.8750 | | | 07/01/49 | | | | 367,673 | |

| | 542,989 | | | Loan ID 201750 | | Fixed | | 6.1250 | | | 04/01/50 | | | | 553,848 | |

| | 1,099,726 | | | Loan ID 201753 | | Fixed | | 4.8750 | | | 04/01/50 | | | | 1,114,223 | |

| | 601,798 | | | Loan ID 201755 | | Fixed | | 5.7500 | | | 03/01/50 | | | | 613,834 | |

| | 249,285 | | | Loan ID 201756 | | Fixed | | 5.0000 | | | 03/01/50 | | | | 252,269 | |

| | 273,435 | | | Loan ID 201757 | | ARM | | 5.1250 | | | 04/01/50 | | | | 277,371 | |

| | 415,886 | | | Loan ID 201758 | | Fixed | | 5.8750 | | | 03/01/50 | | | | 423,455 | |

| | 259,204 | | | Loan ID 201759 | | ARM | | 5.7500 | | | 03/01/50 | | | | 266,387 | |

| | 256,519 | | | Loan ID 201761 | | Fixed | | 6.8750 | | | 02/01/50 | | | | 261,649 | |

| | 423,170 | | | Loan ID 201762 | | Fixed | | 5.9900 | | | 03/01/50 | | | | 431,634 | |

| | 145,196 | | | Loan ID 201763 | | Fixed | | 7.3750 | | | 04/01/50 | | | | 148,100 | |

| | 216,209 | | | Loan ID 201767 | | Fixed | | 5.2500 | | | 07/01/49 | | | | 216,209 | |

| | 188,538 | | | Loan ID 201768 | | Fixed | | 6.7500 | | | 04/01/50 | | | | 192,309 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 214,768 | | | Loan ID 201770 | | Fixed | | 9.3750 | | | 04/01/50 | | | $ | 219,064 | |

| | 350,700 | | | Loan ID 201772 | | Fixed | | 8.1250 | | | 03/01/50 | | | | 368,235 | |

| | 753,632 | | | Loan ID 201773 | | ARM | | 5.5000 | | | 06/01/49 | | | | 768,705 | |

| | 710,532 | | | Loan ID 201776 | | Fixed | | 6.6250 | | | 01/01/50 | | | | 724,742 | |

| | 124,912 | | | Loan ID 201777 | | Fixed | | 5.8750 | | | 04/01/49 | | | | 127,411 | |

| | 250,000 | | | Loan ID 201779 | | Fixed | | 10.5000 | | | 07/01/22 | | | | 255,000 | |

| | 442,725 | | | Loan ID 201780 | | Fixed | | 6.1250 | | | 04/01/50 | | | | 450,056 | |

| | 124,600 | | | Loan ID 201783 | | Interest Only | | 7.5000 | | | 09/01/25 | | | | 129,073 | |

| | 307,079 | | | Loan ID 201784 | | Fixed | | 6.7500 | | | 04/01/50 | | | | 322,433 | |

| | 273,000 | | | Loan ID 201785 | | Interest Only | | 8.0000 | | | 08/31/23 | | | | 286,650 | |

| | 935,000 | | | Loan ID 201787 | | ARM | | 6.3460 | | | 03/01/60 | | | | 953,700 | |

| | 253,485 | | | Loan ID 201795 | | Interest Only | | 7.5000 | | | 10/31/25 | | | | 266,159 | |

| | 247,000 | | | Loan ID 201797 | | Fixed | | 10.9900 | | | 12/01/21 | | | | 247,000 | |

| | 752,300 | | | Loan ID 201800 | | Interest Only | | 7.5000 | | | 12/31/23 | | | | 739,746 | |

| | 36,152 | | | Loan ID 201802 | | Fixed | | 4.2500 | | | 10/01/29 | | | | 33,944 | |

| | 26,450 | | | Loan ID 201803 | | Fixed | | 7.0500 | | | 09/01/34 | | | | 26,979 | |

| | 174,777 | | | Loan ID 201804 | | Fixed | | 4.0000 | | | 03/01/58 | | | | 175,825 | |

| | 109,410 | | | Loan ID 201805 | | Fixed | | 4.3750 | | | 08/01/59 | | | | 111,342 | |

| | 27,848 | | | Loan ID 201806 | | DSI | | 9.0000 | | | 06/01/26 | | | | 28,405 | |

| | 72,101 | | | Loan ID 201807 | | Fixed | | 5.0000 | | | 08/01/43 | | | | 64,962 | |

| | 119,383 | | | Loan ID 201808 | | Fixed | | 3.8750 | | | 06/01/60 | | | | 119,319 | |

| | 164,554 | | | Loan ID 201809 | | Fixed | | 3.7500 | | | 11/01/59 | | | | 161,272 | |

| | 75,137 | | | Loan ID 201810 | | Fixed | | 3.7500 | | | 02/01/42 | | | | 73,927 | |

| | 62,120 | | | Loan ID 201811 | | DSI | | 11.8300 | | | 05/01/35 | | | | 63,362 | |

| | 32,160 | | | Loan ID 201812 | | Fixed | | 9.2400 | | | 02/01/27 | | | | 32,803 | |

| | 75,885 | | | Loan ID 201813 | | DSI | | 6.0000 | | | 01/01/39 | | | | 55,405 | |

| | 49,550 | | | Loan ID 201814 | | DSI | | 7.7400 | | | 03/01/33 | | | | 50,541 | |

| | 67,273 | | | Loan ID 201815 | | Fixed | | 8.0000 | | | 09/01/33 | | | | 68,619 | |

| | 51,896 | | | Loan ID 201816 | | Fixed | | 4.6250 | | | 04/01/29 | | | | 49,301 | |

| | 98,437 | | | Loan ID 201817 | | Fixed | | 4.1250 | | | 10/01/34 | | | | 98,576 | |

| | 57,205 | | | Loan ID 201818 | | Fixed | | 10.3900 | | | 12/01/41 | | | | 58,349 | |

| | 54,618 | | | Loan ID 201819 | | Fixed | | 3.8750 | | | 11/01/29 | | | | 54,627 | |

| | 94,726 | | | Loan ID 201820 | | Fixed | | 3.7500 | | | 01/01/60 | | | | 94,121 | |

| | 67,267 | | | Loan ID 201821 | | Fixed | | 6.4500 | | | 05/01/30 | | | | 68,613 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 48,649 | | | Loan ID 201822 | | DSI | | 8.9200 | | | 01/01/36 | | | $ | 45,696 | |

| | 72,775 | | | Loan ID 201823 | | Fixed | | 9.6250 | | | 03/01/40 | | | | 73,820 | |

| | 278,604 | | | Loan ID 201824 | | DSI | | 8.5000 | | | 10/01/37 | | | | 277,322 | |

| | 126,203 | | | Loan ID 201825 | | Fixed | | 3.8750 | | | 03/01/40 | | | | 115,970 | |

| | 62,828 | | | Loan ID 201826 | | Fixed | | 8.4980 | | | 11/01/30 | | | | 64,085 | |

| | 31,131 | | | Loan ID 201827 | | Fixed | | 10.7800 | | | 03/01/26 | | | | 31,753 | |

| | 29,411 | | | Loan ID 201828 | | Fixed | | 8.2490 | | | 10/01/30 | | | | 29,999 | |

| | 111,631 | | | Loan ID 201829 | | DSI | | 10.4600 | | | 08/01/37 | | | | 113,864 | |

| | 33,034 | | | Loan ID 201830 | | DSI | | 10.5550 | | | 10/01/26 | | | | 33,695 | |

| | 62,633 | | | Loan ID 201831 | | DSI | | 11.1100 | | | 02/01/38 | | | | 63,885 | |

| | 53,852 | | | Loan ID 201832 | | Fixed | | 6.2500 | | | 06/01/34 | | | | 41,617 | |

| | 38,088 | | | Loan ID 201833 | | DSI | | 12.6790 | | | 06/01/23 | | | | 38,850 | |

| | 60,835 | | | Loan ID 201834 | | DSI | | 9.1500 | | | 04/01/38 | | | | 62,052 | |

| | 37,829 | | | Loan ID 201835 | | DSI | | 7.5000 | | | 01/01/27 | | | | 38,585 | |

| | 29,250 | | | Loan ID 201836 | | DSI | | 8.8360 | | | 07/01/27 | | | | 29,835 | |

| | 46,391 | | | Loan ID 201837 | | DSI | | 6.9960 | | | 09/01/31 | | | | 47,319 | |

| | 46,394 | | | Loan ID 201838 | | DSI | | 9.0700 | | | 07/01/27 | | | | 47,322 | |

| | 43,442 | | | Loan ID 201839 | | DSI | | 11.1100 | | | 08/01/39 | | | | 44,311 | |

| | 67,521 | | | Loan ID 201840 | | DSI | | 10.8700 | | | 10/01/41 | | | | 68,871 | |

| | 42,079 | | | Loan ID 201841 | | Fixed | | 10.0600 | | | 05/01/25 | | | | 42,920 | |

| | 73,353 | | | Loan ID 201842 | | DSI | | 11.0300 | | | 03/01/28 | | | | 74,820 | |

| | 35,069 | | | Loan ID 201843 | | Fixed | | 9.1800 | | | 08/01/31 | | | | 35,771 | |

| | 48,441 | | | Loan ID 201844 | | DSI | | 11.4900 | | | 11/01/28 | | | | 49,410 | |

| | 21,497 | | | Loan ID 201845 | | DSI | | 7.0000 | | | 02/01/24 | | | | 21,927 | |

| | 42,777 | | | Loan ID 201846 | | Fixed | | 8.4960 | | | 05/01/34 | | | | 43,633 | |

| | 127,408 | | | Loan ID 201847 | | Fixed | | 2.3750 | | | 06/01/33 | | | | 115,711 | |

| | 54,776 | | | Loan ID 201848 | | DSI | | 4.2900 | | | 11/01/32 | | | | 55,872 | |

| | 52,125 | | | Loan ID 201849 | | DSI | | 4.4800 | | | 06/01/35 | | | | 53,167 | |

| | 93,944 | | | Loan ID 201850 | | Fixed | | 4.6250 | | | 10/01/42 | | | | 94,617 | |

| | 124,298 | | | Loan ID 201851 | | DSI | | 4.5000 | | | 08/30/23 | | | | 126,784 | |

| | 95,923 | | | Loan ID 201853 | | DSI | | 4.9100 | | | 02/01/34 | | | | 97,842 | |

| | 85,998 | | | Loan ID 201855 | | DSI | | 4.3900 | | | 07/01/36 | | | | 87,718 | |

| | 46,194 | | | Loan ID 201856 | | Fixed | | 7.9000 | | | 06/01/37 | | | | 41,302 | |

| | 51,835 | | | Loan ID 201857 | | Fixed | | 3.2500 | | | 04/01/35 | | | | 42,985 | |

VERTICAL CAPITAL INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

September 30, 2021

| Principal | | | | | | | Coupon Rate | | | | | | |

| Amount ($) | | | | | Loan Type | | (%) | | Maturity | | | Fair Value | |

| | | | | LOANS — 93.9% (Continued) | | | | | | | | | | | | |

| | | | | MORTGAGE LOANS (PRIVATE) — 93.9% (Continued) |

| | 368,606 | | | Loan ID 201858 | | Fixed | | 4.6250 | | | 02/01/59 | | | $ | 375,978 | |

| | 592,500 | | | Loan ID 201859 | | Interest Only | | 7.5000 | | | 12/31/25 | | | | 604,350 | |

| | 123,867 | | | Loan ID 201861 | | Fixed | | 5.0000 | | | 05/01/40 | | | | 123,867 | |

| | 22,916 | | | Loan ID 201862 | | DSI | | 10.0000 | | | 05/01/27 | | | | 23,375 | |

| | 21,273 | | | Loan ID 201864 | | DSI | | 7.0560 | | | 01/01/35 | | | | 21,699 | |

| | 28,236 | | | Loan ID 201865 | | Fixed | | 6.4990 | | | 01/01/32 | | | | 28,801 | |

| | 52,575 | | | Loan ID 201866 | | Fixed | | 4.8750 | | | 01/01/44 | | | | 53,175 | |

| | 34,371 | | | Loan ID 201867 | | DSI | | 4.2300 | | | 12/01/32 | | | | 33,734 | |

| | 55,468 | | | Loan ID 201868 | | DSI | | 7.5360 | | | 09/01/34 | | | | 52,695 | |

| | 18,611 | | | Loan ID 201869 | | DSI | | 8.3900 | | | 07/01/24 | | | | 18,983 | |

| | 15,264 | | | Loan ID 201870 | | DSI | | 9.4800 | | | 02/01/23 | | | | 15,569 | |

| | 9,467 | | | Loan ID 201871 | | Fixed | | 9.9700 | | | 05/01/26 | | | | 9,656 | |

| | 34,703 | | | Loan ID 201872 | | DSI | | 8.1000 | | | 09/01/38 | | | | 35,397 | |

| | 17,235 | | | Loan ID 201873 | | Fixed | | 6.6480 | | | 02/01/27 | | | | 17,580 | |

| | 25,272 | | | Loan ID 201874 | | DSI | | 10.5400 | | | 05/01/27 | | | | 25,778 | |

| | 9,489 | | | Loan ID 201875 | | Fixed | | 10.9800 | | | 06/01/30 | | | | 9,679 | |

| | 15,667 | | | Loan ID 201876 | | Fixed | | 8.3100 | | | 02/01/27 | | | | 15,980 | |

| | 7,672 | | | Loan ID 201877 | | DSI | | 9.8300 | | | 11/01/28 | | | | 7,825 | |

| | 27,132 | | | Loan ID 201878 | | DSI | | 9.0500 | | | 08/01/24 | | | | 27,675 | |

| | 12,872 | | | Loan ID 201879 | | Fixed | | 9.3100 | | | 10/01/26 | | | | 13,130 | |

| | 21,434 | | | Loan ID 201881 | | DSI | | 4.5900 | | | 05/01/26 | | | | 21,343 | |

| | 11,151 | | | Loan ID 201882 | | Fixed | | 8.3100 | | | 04/01/27 | | | | 11,374 | |

| | 29,352 | | | Loan ID 201883 | | Fixed | | 4.6250 | | | 06/01/33 | | | | 29,575 | |