united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22549

Northern Lights Fund Trust II

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246

(Address of principal executive offices) (Zip code)

Kevin Wolf, Gemini Fund Services, LLC

80 Arkay Drive, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 12/31

Date of reporting period: 12/31/21

Item 1. Reports to Stockholders.

Annual Report – Shareholder Letter

Incredibly, 2021 began with a Democratic sweep of the two run-off elections for the Georgia Senate seats and a Mob Storms Capitol headline in giant type in the January 7 edition of The Wall Street Journal. And the year ended with the Federal Reserve tapering its bond buying program and suggesting that there may be two or three hikes in the Federal Funds rate in 2022, while COVID-19 cases hit records around the world, with Europe imposing new lockdowns over the Holidays and the U.S. seeing thousands of flights cancelled.

Yet, even with all the supposedly equity-unfriendly news, the major market averages turned in stellar performance. The broad-based Russell 3000 Growth Index returned 25.66%, while the S&P 500 gained 28.71%. Interestingly and more importantly, the Russell 3000 Value vs. Growth race was a virtual dead heat, with the former advancing 25.37%. For their part, the Al Frank Fund Investor Class returned 24.64% and the Al Frank Fund Advisor Class returned 24.98% for 2021.

Reasons for the advance primarily centered on better news on the health front with the COVID-19 vaccines proving very effective at warding off worse outcomes. With that tailwind, the U.S. and global economies continued a bounce back that began in Q3 2020, no doubt goosed by pent-up demand, substantial support from global central bankers and significant stimulus from Washington. As a result, corporate profit growth throughout 2021 was robust and stock prices responded favorably.

Keeping in mind that we have long adhered to a Value strategy, the lion’s share of our return in 2021 came from our exposure to the Information Technology sector, though traditional Value favorites like Financials and Industrials were the second and third best sectors on an absolute return basis. We also enjoyed very nice performance within the Energy and Real Estate sectors, though Health Care, Communication Services and Utilities proved to be a drag on our overall return.

Looking at specific stocks, Seagate Technology, Alphabet, Microsoft, Capital One Fin’l and Lam Research were the largest contributors to total return on an absolute basis, while Walt Disney, Nordstrom, Zimmer Biomet, Medtronic and Verizon Communications were the biggest negative contributors.

*****

Obviously, it was a tremendous year for U.S. equities, while the purportedly safer fixed income benchmarks ended in the red. The Bloomberg Barclays U.S. Aggregate Bond index had a negative total return of 1.54%, with the Bloomberg Barclays Global Aggregate Bond index skidding 4.71%. Certainly, we understand that not everyone can tolerate the ups and downs of stocks, so bonds have their place, but we like what our founder Al Frank wrote two decades ago when critiquing Warren Buffett’s comments at the 2001 Berkshire Hathaway Annual Meeting: I love his reaffirming that Modern Portfolio Theory’s concept of risk as quantified by beta (a measurement of volatility) is wrong [my word]. Arguably the most successful investor in the world, Buffett said, “If someone starts talking to you about beta, zip up your pocketbook…There are two kinds of risk: The risk that you could get a better return on your money elsewhere (opportunity cost) and the risk of permanent capital impairment (financial health).”

And therein lies the foundation of our continued enthusiasm for stocks. The low interest rate environment makes it difficult to get a better return elsewhere, while higher inflation and a less accommodative Federal Reserve amp the possibility that all those dollars in fixed income ETFs will suffer permanent impairment of capital.

14376457-UFD-01282022

To be sure, bonds and cash (there is $4.7 trillion currently hibernating in money market funds, with the certainty in the near-term of suffering a substantial loss of purchasing power) will always be part of most asset allocation mixes.

But for those who can stomach the inevitable short-term equity market gyrations (history shows that on average 5% setbacks happen three times per year, 10% corrections occur every 11 months and 20% Bear Markets take place every 3.5 years), we think the long-term rewards from stocks, especially the less expensive names that we have long championed, remain very compelling.

Of course, many have found out the hard way that the secret to success in stocks is not to get scared out of them, but Value has had an average annualized return of 13.3% per annum since 1927. What’s more, in addition to the valuation gap between Value and Growth being as wide today as it was at the peak of the Tech Bubble, our studies of the historical evidence suggests that higher inflation, rising interest rates and increased tax rates have previously coincided with superior performance for stocks that trade for lower valuation metrics than their pricier peers.

We expect the sledding to be tougher this year than last and we know the virus is far from conquered, supply chain woes continue to be a headwind and disconcerting geopolitical events are a constant worry, so as the Oracle of Omaha proclaims, “We don’t have to be smarter than the rest. We have to be more disciplined than the rest.”

While there is never an assurance that past is prologue, we continue to believe that those who stick with stocks through thick and thin will be rewarded in the fullness of time. Indeed, just since the end of the Great Financial Crisis in 2009, equites have managed to show handsome appreciation despite the Flash Crash, the Japan Tsunami, Standard & Poor’s downgrading the U.S. credit rating, Hurricane Sandy, the Taper Tantrum, the Ebola Scare, the Greek debt default, Brexit and the Trump victory and trade war, to name just a few of the headwinds overcome.

With more than 23 years of managing The Al Frank Fund, not to mention our 45 years of publishing The Prudent Speculator newsletter, we see no reason today to alter our disciplined approach. We remain comfortable in our basic risk mitigation tools of patiently buying and seeking to harvest a broadly diversified portfolio of what we believe are undervalued stocks, generally of dividend-paying companies, while modestly ebbing and flowing our cash position.

We appreciate the loyalty and trust you have put in our management and we do not take the market gyrations lightly. We are invested right alongside our Al Frank Fund shareholders!

14376457-UFD-01282022

Al Frank Fund

PORTFOLIO REVIEW (Unaudited)

December 31, 2021

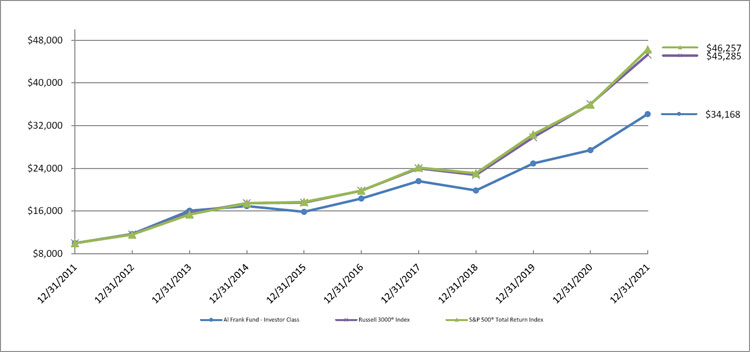

The Fund’s performance figures* for the periods ended December 31, 2021, compared to its benchmark:

| | | | Annualized | |

| | | | | Since Inception | Since Inception |

| | One Year | Five Year | Ten Year | (1/2/98) | (4/30/06) |

| Al Frank Fund - Investor Class** | 24.64% | 13.24% | 13.07% | 10.73% | N/A |

| Al Frank Fund - Advisor Class*** | 24.98% | 13.52% | 13.36% | N/A | 7.71% |

| S&P 500® Total Return Index**** | 28.71% | 18.47% | 16.55% | 8.85% | 10.83% |

| Russell 3000® Total Return Index***** | 25.66% | 17.97% | 16.30% | 8.96% | 10.70% |

Comparison of the Change in Value of a $10,000 Investment

Returns reflect the reinvestment of dividends and capital gains. Fee waivers are in effect. In the absence of fee waivers, returns would have been reduced. The performance data and graphs above do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gain distributions, or redemption of Fund shares. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 60 days or less. If it did, returns would have been reduced.

| * | Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data for the most recent month-end is available at www.alfrankfunds.com. The Fund’s total annual operating expenses are 1.68% for the Investor Class and 1.43% for the Advisor Class, respectively, per the May 1, 2021 prospectus. After fee waivers, the Fund’s total annual operating expenses are 1.49% for the Investor Class and 1.24% for the Advisor Class, respectively. |

| ** | Commencement of operations on January 2, 1998. |

| *** | Commencement of operations on April 30, 2006. |

| **** | The S&P Total Return 500® Index is a broad based unmanaged capitalization-weighted index of 500 stocks designed to represent the broad domestic market. You cannot invest directly in an index. |

| ***** | The Russell 3000® Total Return Index measures the performance of the largest 3,000 U.S. companies determined by total market capitalization. You cannot invest directly in an index. |

| Holdings By Asset Class as of December 31, 2021 | | % of Net Assets | |

| Information Technology | | | 23.5 | % |

| Financials | | | 16.6 | % |

| Industrials | | | 12.7 | % |

| Health Care | | | 11.8 | % |

| Consumer Discretionary | | | 10.0 | % |

| Communication Services | | | 6.2 | % |

| Materials | | | 5.0 | % |

| Consumer Staples | | | 4.5 | % |

| Energy | | | 3.6 | % |

| Real Estate | | | 3.3 | % |

| Utilities | | | 0.9 | % |

| Other, Cash & Cash Equivalents | | | 1.9 | % |

| | | | 100.0 | % |

Please refer to the Schedule of Investments in this annual report for a detailed analysis of the Fund’s holdings.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.1% | | | | |

| | | | | COMMUNICATION SERVICES — 6.2% | | | | |

| | | | | CABLE & SATELLITE - 1.2% | | | | |

| | 20,000 | | | Comcast Corporation, Class A | | $ | 1,006,600 | |

| | | | | | | | | |

| | | | | ENTERTAINMENT CONTENT - 1.7% | | | | |

| | 9,000 | | | Walt Disney Company (The)(a) | | | 1,394,010 | |

| | | | | | | | | |

| | | | | INTERNET MEDIA & SERVICES - 2.6% | | | | |

| | 750 | | | Alphabet, Inc., Class C(a) | | | 2,170,193 | |

| | | | | | | | | |

| | | | | TELECOMMUNICATIONS - 0.7% | | | | |

| | 11,000 | | | Verizon Communications, Inc. | | | 571,560 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | TOTAL COMMUNICATION SERVICES (Cost $1,695,843) | | | 5,142,363 | |

| | | | | | | | | |

| | | | | CONSUMER DISCRETIONARY — 10.0% | | | | |

| | | | | AUTOMOTIVE - 1.6% | | | | |

| | 22,500 | | | General Motors Company(a) | | | 1,319,175 | |

| | | | | | | | | |

| | | | | HOME & OFFICE PRODUCTS - 1.6% | | | | |

| | 5,500 | | | Whirlpool Corporation | | | 1,290,630 | |

| | | | | | | | | |

| | | | | HOME CONSTRUCTION - 1.7% | | | | |

| | 25,000 | | | MDC Holdings, Inc. | | | 1,395,750 | |

| | | | | | | | | |

| | | | | LEISURE FACILITIES & SERVICES - 0.9% | | | | |

| | 10,000 | | | Royal Caribbean Cruises Ltd.(a) | | | 769,000 | |

| | | | | | | | | |

| | | | | RETAIL - CONSUMER STAPLES - 1.4% | | | | |

| | 5,000 | | | Target Corporation | | | 1,157,200 | |

| | | | | | | | | |

| | | | | RETAIL - DISCRETIONARY - 2.8% | | | | |

| | 20,000 | | | Foot Locker, Inc. | | | 872,600 | |

| | 18,500 | | | Kohl’s Corporation | | | 913,715 | |

See accompanying notes to financial statements.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | CONSUMER DISCRETIONARY — 10.0% (Continued) | | | | |

| | | | | RETAIL - DISCRETIONARY - 2.8% (Continued) | | | | |

| | 25,000 | | | Nordstrom, Inc.(a) | | $ | 565,500 | |

| | | | | | | | 2,351,815 | |

| | | | | | | | | |

| | | | | TOTAL CONSUMER DISCRETIONARY (Cost $3,704,638) | | | 8,283,570 | |

| | | | | | | | | |

| | | | | CONSUMER STAPLES — 4.5% | | | | |

| | | | | FOOD - 1.2% | | | | |

| | 11,000 | | | Tyson Foods, Inc., Class A | | | 958,760 | |

| | | | | | | | | |

| | | | | RETAIL - CONSUMER STAPLES - 2.2% | | | | |

| | 20,000 | | | Kroger Company (The) | | | 905,200 | |

| | 6,500 | | | Walmart, Inc. | | | 940,485 | |

| | | | | | | | 1,845,685 | |

| | | | | WHOLESALE - CONSUMER STAPLES - 1.1% | | | | |

| | 13,500 | | | Archer-Daniels-Midland Company | | | 912,465 | |

| | | | | | | | | |

| | | | | TOTAL CONSUMER STAPLES (Cost $1,250,898) | | | 3,716,910 | |

| | | | | | | | | |

| | | | | ENERGY — 3.6% | | | | |

| | | | | OIL & GAS PRODUCERS - 3.6% | | | | |

| | 13,000 | | | EOG Resources, Inc. | | | 1,154,790 | |

| | 11,500 | | | Exxon Mobil Corporation | | | 703,685 | |

| | 19,000 | | | TotalEnergies S.E. - ADR | | | 939,740 | |

| | 5,000 | | | World Fuel Services Corporation | | | 132,350 | |

| | | | | | | | 2,930,565 | |

| | | | | | | | | |

| | | | | TOTAL ENERGY (Cost $2,655,341) | | | 2,930,565 | |

| | | | | | | | | |

| | | | | FINANCIALS — 16.6% | | | | |

| | | | | BANKING - 9.9% | | | | |

| | 30,000 | | | Bank of America Corporation | | | 1,334,700 | |

| | 30,000 | | | Fifth Third Bancorp | | | 1,306,500 | |

| | 12,500 | | | JPMorgan Chase & Company | | | 1,979,375 | |

See accompanying notes to financial statements.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | FINANCIALS — 16.6% (Continued) | | | | |

| | | | | BANKING - 9.9% (Continued) | | | | |

| | 60,000 | | | Old National Bancorp | | $ | 1,087,200 | |

| | 6,000 | | | PNC Financial Services Group, Inc. (The) | | | 1,203,120 | |

| | 22,000 | | | Truist Financial Corporation | | | 1,288,100 | |

| | | | | | | | 8,198,995 | |

| | | | | INSTITUTIONAL FINANCIAL SERVICES - 2.1% | | | | |

| | 4,500 | | | Goldman Sachs Group, Inc. (The) | | | 1,721,475 | |

| | | | | | | | | |

| | | | | INSURANCE - 2.9% | | | | |

| | 18,000 | | | MetLife, Inc. | | | 1,124,820 | |

| | 11,500 | | | Prudential Financial, Inc. | | | 1,244,760 | |

| | | | | | | | 2,369,580 | |

| | | | | SPECIALTY FINANCE - 1.7% | | | | |

| | 10,000 | | | Capital One Financial Corporation | | | 1,450,900 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | TOTAL FINANCIALS (Cost $5,535,984) | | | 13,740,950 | |

| | | | | | | | | |

| | | | | HEALTH CARE — 11.8% | | | | |

| | | | | BIOTECH & PHARMA - 6.2% | | | | |

| | 5,500 | | | Amgen, Inc. | | | 1,237,335 | |

| | 2,500 | | | Biogen, Inc.(a) | | | 599,800 | |

| | 7,500 | | | Johnson & Johnson | | | 1,283,025 | |

| | 11,000 | | | Merck & Company, Inc. | | | 843,040 | |

| | 20,000 | | | Pfizer, Inc. | | | 1,181,000 | |

| | | | | | | | 5,144,200 | |

| | | | | HEALTH CARE FACILITIES & SERVICES - 2.5% | | | | |

| | 18,000 | | | Cardinal Health, Inc. | | | 926,820 | |

| | 11,000 | | | CVS Health Corporation | | | 1,134,760 | |

| | 1 | | | Encompass Health Corporation | | | 65 | |

| | | | | | | | 2,061,645 | |

| | | | | MEDICAL EQUIPMENT & DEVICES - 3.1% | | | | |

| | 8,500 | | | Abbott Laboratories | | | 1,196,290 | |

| | 7,000 | | | Medtronic PLC | | | 724,150 | |

See accompanying notes to financial statements.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | HEALTH CARE — 11.8% (Continued) | | | | |

| | | | | MEDICAL EQUIPMENT & DEVICES - 3.1% (Continued) | | | | |

| | 5,000 | | | Zimmer Biomet Holdings, Inc. | | $ | 635,200 | |

| | | | | | | | 2,555,640 | |

| | | | | | | | | |

| | | | | TOTAL HEALTH CARE (Cost $6,351,639) | | | 9,761,485 | |

| | | | | | | | | |

| | | | | INDUSTRIALS — 12.7% | | | | |

| | | | | AEROSPACE & DEFENSE - 1.2% | | | | |

| | 2,750 | | | Lockheed Martin Corporation | | | 977,378 | |

| | | | | | | | | |

| | | | | COMMERCIAL SUPPORT SERVICES - 1.4% | | | | |

| | 12,000 | | | ManpowerGroup, Inc. | | | 1,167,960 | |

| | | | | | | | | |

| | | | | DIVERSIFIED INDUSTRIALS - 1.3% | | | | |

| | 6,500 | | | Eaton Corp PLC | | | 1,123,330 | |

| | | | | | | | | |

| | | | | ELECTRICAL EQUIPMENT - 1.2% | | | | |

| | 4,700 | | | Acuity Brands, Inc. | | | 995,084 | |

| | | | | | | | | |

| | | | | MACHINERY - 3.2% | | | | |

| | 6,500 | | | Caterpillar, Inc. | | | 1,343,810 | |

| | 3,734 | | | Deere & Company | | | 1,280,351 | |

| | | | | | | | 2,624,161 | |

| | | | | TRANSPORTATION & LOGISTICS - 3.2% | | | | |

| | 4,500 | | | FedEx Corporation | | | 1,163,880 | |

| | 5,000 | | | Norfolk Southern Corporation | | | 1,488,550 | |

| | | | | | | | 2,652,430 | |

| | | | | TRANSPORTATION EQUIPMENT - 1.2% | | | | |

| | 4,500 | | | Cummins, Inc. | | | 981,630 | |

| | | | | | | | | |

| | | | | TOTAL INDUSTRIALS (Cost $4,602,961) | | | 10,521,973 | |

See accompanying notes to financial statements.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | INFORMATION TECHNOLOGY — 23.5% | | | | |

| | | | | SEMICONDUCTORS - 7.1% | | | | |

| | 25,000 | | | Cohu, Inc.(a) | | $ | 952,250 | |

| | 18,000 | | | Intel Corporation | | | 927,000 | |

| | 2,150 | | | Lam Research Corporation | | | 1,546,173 | |

| | 7,000 | | | Micron Technology, Inc. | | | 652,050 | |

| | 10,000 | | | QUALCOMM, Inc. | | | 1,828,700 | |

| | | | | | | | 5,906,173 | |

| | | | | SOFTWARE - 4.3% | | | | |

| | 5,000 | | | Microsoft Corporation | | | 1,681,600 | |

| | 36,000 | | | NortonLifeLock, Inc. | | | 935,280 | |

| | 11,000 | | | Oracle Corporation | | | 959,310 | |

| | | | | | | | 3,576,190 | |

| | | | | TECHNOLOGY HARDWARE – 10.9% | | | | |

| | 13,000 | | | Apple, Inc. | | | 2,308,409 | |

| | 15,500 | | | Benchmark Electronics, Inc. | | | 420,050 | |

| | 18,000 | | | Cisco Systems, Inc. | | | 1,140,660 | |

| | 32,500 | | | Corning, Inc. | | | 1,209,975 | |

| | 30,000 | | | Juniper Networks, Inc. | | | 1,071,300 | |

| | 11,000 | | | NetApp, Inc. | | | 1,011,890 | |

| | 16,000 | | | Seagate Technology Holdings plc | | | 1,807,680 | |

| | | | | | | | 8,969,964 | |

| | | | | TECHNOLOGY SERVICES - 1.2% | | | | |

| | 7,100 | | | International Business Machines Corporation | | | 948,986 | |

| | 1,420 | | | Kyndryl Holdings, Inc.(a) | | | 25,702 | |

| | | | | | | | 974,688 | |

| | | | | | | | | |

| | | | | TOTAL INFORMATION TECHNOLOGY (Cost $6,310,815) | | | 19,427,015 | |

| | | | | | | | | |

| | | | | MATERIALS — 5.0% | | | | |

| | | | | CHEMICALS - 2.9% | | | | |

| | 4,800 | | | Albemarle Corporation | | | 1,122,096 | |

| | 7,500 | | | Celanese Corporation | | | 1,260,450 | |

| | | | | | | | 2,382,546 | |

See accompanying notes to financial statements.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | MATERIALS — 5.0% (Continued) | | | | |

| | | | | CONTAINERS & PACKAGING - 1.1% | | | | |

| | 20,500 | | | International Paper Company | | $ | 963,090 | |

| | | | | | | | | |

| | | | | METALS & MINING - 1.0% | | | | |

| | 13,000 | | | Newmont Corporation | | | 806,260 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | TOTAL MATERIALS (Cost $1,753,010) | | | 4,151,896 | |

| | | | | | | | | |

| | | | | REAL ESTATE — 3.3% | | | | |

| | | | | DATA CENTER REIT - 1.2% | | | | |

| | 5,500 | | | Digital Realty Trust, Inc. | | | 972,785 | |

| | | | | | | | | |

| | | | | HEALTH CARE REIT - 0.9% | | | | |

| | 40,000 | | | Physicians Realty Trust | | | 753,200 | |

| | | | | | | | | |

| | | | | RETAIL REIT - 1.2% | | | | |

| | 40,000 | | | Kimco Realty Corporation | | | 986,000 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | TOTAL REAL ESTATE (Cost $1,684,623) | | | 2,711,985 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | UTILITIES — 0.9% | | | | |

| | | | | ELECTRIC UTILITIES - 0.9% | | | | |

| | 10,000 | | | Pinnacle West Capital Corporation | | | 705,900 | |

| | | | | | | | | |

| | | | | TOTAL UTILITIES (Cost $804,992) | | | 705,900 | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCKS (Cost $36,350,744) | | | 81,094,612 | |

See accompanying notes to financial statements.

| AL FRANK FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2021 |

| Shares | | | | | Fair Value | |

| | | | | SHORT-TERM INVESTMENT — 2.0% | | | | |

| | | | | MONEY MARKET FUNDS – 2.0% | | | | |

| | 1,609,532 | | | Fidelity Government Portfolio, Institutional Class, 0.01% (Cost $1,609,532)(b) | | $ | 1,609,532 | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 100.1% (Cost $37,960,276) | | $ | 82,704,144 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS - (0.1)% | | | (70,959 | ) |

| | | | | NET ASSETS - 100.0% | | $ | 82,633,185 | |

| ADR | - American Depositary Receipt |

| PLC | - Public Limited Company |

| REIT | - Real Estate Investment Trust |

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven-day effective yield as of December 31, 2021. |

See accompanying notes to financial statements.

| Al Frank Fund |

| STATEMENT OF ASSETS AND LIABILITIES |

| December 31, 2021 |

| ASSETS | | | |

| Investment securities: | | | | |

| At cost | | $ | 37,960,276 | |

| At value | | $ | 82,704,144 | |

| Receivable for Fund shares sold | | | 68 | |

| Dividends and interest receivable | | | 82,440 | |

| Prepaid expenses & other assets | | | 24,638 | |

| TOTAL ASSETS | | | 82,811,290 | |

| | | | | |

| LIABILITIES | | | | |

| Payable for Fund shares redeemed | | | 68,606 | |

| Investment advisory fees payable | | | 50,739 | |

| Distribution (12b-1) fees payable | | | 15,418 | |

| Audit fees payable | | | 15,198 | |

| Payable to Related Parties | | | 21,569 | |

| Accrued expenses and other liabilities | | | 6,575 | |

| TOTAL LIABILITIES | | | 178,105 | |

| NET ASSETS | | $ | 82,633,185 | |

| | | | | |

| Net Assets Consist Of: | | | | |

| Paid in capital | | $ | 36,527,629 | |

| Accumulated earnings | | | 46,105,556 | |

| NET ASSETS | | $ | 82,633,185 | |

| | | | | |

| Net Asset Value Per Share: | | | | |

| Investor Class Shares: | | | | |

| Net Assets | | $ | 76,211,867 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 2,623,378 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (a) | | $ | 29.05 | |

| | | | | |

| Advisor Class Shares: | | | | |

| Net Assets | | $ | 6,421,318 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 220,537 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (a) | | $ | 29.12 | |

| (a) | Redemptions of shares held 60 days or less may be assessed a redemption fee of 2.00%. |

See accompanying notes to financial statements.

| Al Frank Fund |

| STATEMENT OF OPERATIONS |

| For the Year ended December 31, 2021 |

| INVESTMENT INCOME | | | |

| Dividends * | | $ | 1,658,725 | |

| Interest | | | 244 | |

| TOTAL INVESTMENT INCOME | | | 1,658,969 | |

| | | | | |

| EXPENSES | | | | |

| Investment advisory fees | | | 809,521 | |

| Distribution (12b-1) fees: | | | | |

| Investor Class | | | 188,044 | |

| Administration fees | | | 59,108 | |

| Transfer agent fees | | | 53,300 | |

| Fund accounting fees | | | 39,943 | |

| Trustees’ fees | | | 31,033 | |

| Shareholder reporting expense | | | 12,250 | |

| Legal fees | | | 31,365 | |

| Audit fees | | | 15,664 | |

| Compliance officer fees | | | 21,125 | |

| Registration fees | | | 51,865 | |

| Third party administrative servicing fees | | | 8,896 | |

| Custody fees | | | 4,281 | |

| Insurance expense | | | 7,677 | |

| Other expenses | | | 4,788 | |

| TOTAL EXPENSES | | | 1,338,860 | |

| | | | | |

| Less: Fees waived by the Adviser | | | (146,546 | ) |

| | | | | |

| NET EXPENSES | | | 1,192,314 | |

| NET INVESTMENT INCOME | | | 466,655 | |

| | | | | |

| REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | | | |

| Net realized gain from investments | | | 5,494,885 | |

| Net change in unrealized appreciation on investments | | | 11,209,338 | |

| | | | | |

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | | 16,704,223 | |

| | | | | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 17,170,878 | |

| * | Includes withholding tax of $7,192. |

See accompanying notes to financial statements.

| Al Frank Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | For the | | | For the | |

| | | Year Ended | | | Year Ended | |

| | | December 31, 2021 | | | December 31, 2020 | |

| FROM OPERATIONS | | | | | | | | |

| Net investment income | | $ | 466,655 | | | $ | 1,225,040 | |

| Net realized gain from investments | | | 5,494,885 | | | | 2,751,840 | |

| Net change in unrealized appreciation on investments | | | 11,209,338 | | | | 696,065 | |

| Net increase in net assets resulting from operations | | | 17,170,878 | | | | 4,672,945 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Total Distributions Paid | | | | | | | | |

| Investor Class | | | (4,785,124 | ) | | | (4,312,082 | ) |

| Advisor Class | | | (413,166 | ) | | | (360,213 | ) |

| Net decrease in net assets from distributions to shareholders | | | (5,198,290 | ) | | | (4,672,295 | ) |

| | | | | | | | | |

| FROM SHARES OF BENEFICIAL INTEREST | | | | | | | | |

| Proceeds from shares sold | | | | | | | | |

| Investor Class | | | 6,185,844 | | | | 980,140 | |

| Advisor Class | | | 2,825,329 | | | | 871,672 | |

| Net asset value of shares issued in reinvestment of distributions | | | | | | | | |

| Investor Class | | | 4,687,204 | | | | 4,219,822 | |

| Advisor Class | | | 408,732 | | | | 355,869 | |

| Payments for shares redeemed | | | | | | | | |

| Investor Class | | | (11,734,998 | ) | | | (11,912,286 | ) |

| Advisor Class | | | (2,966,989 | ) | | | (1,240,401 | ) |

| Redemption fee proceeds | | | | | | | | |

| Investor Class | | | 3,179 | | | | 246 | |

| Advisor Class | | | 223 | | | | 19 | |

| Net decrease in net assets from shares of beneficial interest | | | (591,476 | ) | | | (6,724,919 | ) |

| | | | | | | | | |

| TOTAL INCREASE/(DECREASE) IN NET ASSETS | | | 11,381,112 | | | | (6,724,269 | ) |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of Year | | | 71,252,073 | | | | 77,976,342 | |

| End of Year | | $ | 82,633,185 | | | $ | 71,252,073 | |

See accompanying notes to financial statements.

| Al Frank Fund |

| STATEMENTS OF CHANGES IN NET ASSETS (Continued) |

| | | For the | | | For the | |

| | | Year Ended | | | Year Ended | |

| | | December 31, 2021 | | | December 31, 2020 | |

| SHARE ACTIVITY - INVESTOR CLASS | | | | | | | | |

| Shares sold | | | 214,025 | | | | 45,937 | |

| Shares reinvested | | | 164,348 | | | | 171,120 | |

| Shares redeemed | | | (406,040 | ) | | | (571,389 | ) |

| Net decrease in shares of beneficial interest outstanding | | | (27,667 | ) | | | (354,332 | ) |

| | | | | | | | | |

| SHARE ACTIVITY - ADVISOR CLASS | | | | | | | | |

| Shares sold | | | 95,655 | | | | 40,024 | |

| Shares reinvested | | | 14,301 | | | | 14,402 | |

| Shares redeemed | | | (102,719 | ) | | | (58,442 | ) |

| Net increase/(decrease) in shares of beneficial interest outstanding | | | 7,237 | | | | (4,016 | ) |

See accompanying notes to financial statements.

| Al Frank Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year

| | | Investor Class | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | December 31, | | | December 31, | | | December 31, | | | December 31, | | | December 31, | |

| | | 2021 | | | 2020 | | | 2019 | | | 2018 | | | 2017 | |

| Net asset value, beginning of year | | $ | 24.87 | | | $ | 24.19 | | | $ | 20.72 | | | $ | 24.79 | | | $ | 23.27 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (1) | | | 0.16 | | | | 0.42 | | | | 0.30 | | | | 0.25 | | | | 0.32 | |

| Net realized and unrealized gain/(loss) on investments | | | 5.93 | | | | 1.99 | | | | 4.93 | | | | (2.16 | ) | | | 3.79 | |

| Total from investment operations | | | 6.09 | | | | 2.41 | | | | 5.23 | | | | (1.91 | ) | | | 4.11 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.18 | ) | | | (0.44 | ) | | | (0.31 | ) | | | (0.25 | ) | | | (0.31 | ) |

| Net realized gain on investments | | | (1.73 | ) | | | (1.29 | ) | | | (1.45 | ) | | | (1.91 | ) | | | (2.28 | ) |

| Total distributions | | | (1.91 | ) | | | (1.73 | ) | | | (1.76 | ) | | | (2.16 | ) | | | (2.59 | ) |

| Paid in capital from redemption fees (1)(4) | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

| Net asset value, end of year | | $ | 29.05 | | | $ | 24.87 | | | $ | 24.19 | | | $ | 20.72 | | | $ | 24.79 | |

| Total return (2) | | | 24.64 | % | | | 10.01 | % (5) | | | 25.47 | % (5) | | | (8.10 | )% (5) | | | 17.76 | % |

| Net assets, at end of year (000s) | | $ | 76,212 | | | $ | 65,936 | | | $ | 72,709 | | | $ | 68,373 | | | $ | 83,611 | |

| Ratio of gross expenses to average net assets (3) | | | 1.67 | % | | | 1.68 | % | | | 1.63 | % | | | 1.64 | % | | | 1.61 | % |

| Ratio of net expenses to average net assets | | | 1.49 | % | | | 1.49 | % | | | 1.49 | % | | | 1.49 | % | | | 1.50 | % |

| Ratio of net investment income to average net assets | | | 0.56 | % | | | 1.90 | % | | | 1.29 | % | | | 0.98 | % | | | 1.28 | % |

| Portfolio turnover rate | | | 5.10 | % | | | 3.72 | % | | | 1.78 | % | | | 16.28 | % | | | 22.16 | % |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (2) | Total returns shown exclude the effect of applicable redemption fees. Had the Adviser not waived a portion of the Fund’s expenses, total returns would have been lower. |

| (3) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Adviser. |

| (4) | Amount represents less than $0.005 per share. |

| (5) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

See accompanying notes to financial statements.

| Al Frank Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year

| | | Advisor Class | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | December 31, | | | December 31, | | | December 31, | | | December 31, | | | December 31, | |

| | | 2021 | | | 2020 | | | 2019 | | | 2018 | | | 2017 | |

| Net asset value, beginning of year | | $ | 24.92 | | | $ | 24.24 | | | $ | 20.76 | | | $ | 24.83 | | | $ | 23.30 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (1) | | | 0.24 | | | | 0.46 | | | | 0.36 | | | | 0.31 | | | | 0.38 | |

| Net realized and unrealized gain/(loss) on investments | | | 5.95 | | | | 2.01 | | | | 4.94 | | | | (2.15 | ) | | | 3.80 | |

| Total from investment operations | | | 6.19 | | | | 2.47 | | | | 5.30 | | | | (1.84 | ) | | | 4.18 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.26 | ) | | | (0.50 | ) | | | (0.37 | ) | | | (0.32 | ) | | | (0.37 | ) |

| Net realized gain on investments | | | (1.73 | ) | | | (1.29 | ) | | | (1.45 | ) | | | (1.91 | ) | | | (2.28 | ) |

| Total distributions | | | (1.99 | ) | | | (1.79 | ) | | | (1.82 | ) | | | (2.23 | ) | | | (2.65 | ) |

| Paid in capital from redemption fees (1)(4) | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | | | | 0.00 | |

| Net asset value, end of year | | $ | 29.12 | | | $ | 24.92 | | | $ | 24.24 | | | $ | 20.76 | | | $ | 24.83 | |

| Total return (2) | | | 24.98 | % | | | 10.24 | % | | | 25.78 | % | | | (7.83 | )% | | | 18.05 | % |

| Net assets, at end of year (000s) | | $ | 6,421 | | | $ | 5,316 | | | $ | 5,267 | | | $ | 5,033 | | | $ | 6,376 | |

| Ratio of gross expenses to average net assets (3) | | | 1.42 | % | | | 1.43 | % | | | 1.38 | % | | | 1.39 | % | | | 1.36 | % |

| Ratio of net expenses to average net assets | | | 1.24 | % | | | 1.24 | % | | | 1.24 | % | | | 1.24 | % | | | 1.25 | % |

| Ratio of net investment income to average net assets | | | 0.83 | % | | | 2.09 | % | | | 1.54 | % | | | 1.23 | % | | | 1.52 | % |

| Portfolio turnover rate | | | 5.10 | % | | | 3.72 | % | | | 1.78 | % | | | 16.28 | % | | | 22.16 | % |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (2) | Total returns shown exclude the effect of applicable redemption fees. Had the Adviser not waived a portion of the Fund’s expenses, total returns would have been lower. |

| (3) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Adviser. |

| (4) | Amount represents less than $0.005 per share. |

See accompanying notes to financial statements.

| Al Frank Fund |

| NOTES TO FINANCIAL STATEMENTS at December 31, 2021 |

NOTE 1 - ORGANIZATION

The Al Frank Fund (the “Fund”) is a diversified series of Northern Lights Fund Trust II (the “Trust”), which is registered under the Investment Company Act of 1940, as amended, (the “1940 Act”) as an open-end management investment company. The investment objective of the Al Frank Fund is long-term capital appreciation. The Al Frank Fund Investor and Advisor Classes commenced operations on January 2, 1998, and April 30, 2006, respectively.

Advisor Class Shares are offered primarily to qualified registered investment advisers, financial advisors and investors such as pension and profit sharing plans, employee benefit trusts, endowments, foundations and corporations. Advisor Class Shares may be purchased through certain financial intermediaries and mutual fund supermarkets that charge their customers transaction or other fees with respect to their customers’ investment in the Fund. The Fund may also be purchased by qualified investors directly through the Fund’s Transfer Agent. Wrap account programs established with broker-dealers or financial intermediaries may purchase Advisor Class Shares only if the program for which the shares are being acquired will not require the Fund to pay any type of distribution or administration payment to any third-party. A registered investment advisor may aggregate all client accounts investing in the Fund to meet the Advisor Class Shares investment minimum.

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update “ASU” 2013-08.

| A. | Security Valuation: All investments in securities are recorded at their estimated fair value, as described in Note 3. |

| B. | Federal Income Taxes: It is the Fund’s policy to continue to comply with the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its taxable income to shareholders. Therefore, no provision for Federal income taxes has been recorded. |

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years ended December 31, 2018 to December 31, 2020, or expected to be taken in the Fund’s December 31, 2021 year-end tax returns. The Fund identifies its major tax jurisdictions as U.S. Federal and the state of Ohio. For the years ended December 31, 2017 through December 31, 2018, the Fund’s jurisdictions included the state of Nebraska. The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

| C. | Security Transactions, Income and Distributions: Security transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost. Interest income is recorded on an accrual basis. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends are included in dividend income on the ex-dividend date at the fair market value of the shares received. |

Investment income, expenses (other than those specific to the class of shares), and realized and unrealized gains and losses on investments are allocated to the separate classes of the Fund’s shares

| Al Frank Fund |

| NOTES TO FINANCIAL STATEMENTS at December 31, 2021 (Continued) |

based upon their relative net assets on the date income is earned or expenses, realized and unrealized gains and losses are incurred. The Fund distributes substantially all net investment income, if any, and net realized capital gains, if any, annually. The amount of dividends and distributions to shareholders from net investment income and net realized capital gains is determined in accordance with Federal income tax regulations, which differs from accounting principles generally accepted in the United States of America. To the extent these book/tax differences are permanent, such amounts are reclassified within the capital accounts based on their Federal tax treatment.

| D. | Redemption Fees: The Fund charges a 2% redemption fee to shareholders who redeem shares held for 60 days or less. Such fees are retained by the Fund and accounted for as an addition to paid-in capital. For the year ended December 31, 2021, the Al Frank Fund assessed $3,402 in redemption fees. |

| E. | Expenses – Expenses of the Trust that are directly identifiable to a specific fund are charged to that fund. Expenses, which are not readily identifiable to a specific fund, are allocated in such a manner as deemed equitable, taking into consideration the nature and type of expense and the relative size of the fund in the Trust. |

| F. | Indemnification – The Trust indemnifies its officers and Trustees for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the risk of loss due to these warranties and indemnities appears to be remote. |

NOTE 3 - SECURITIES VALUATION

Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the primary exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price (“NOCP”). In the absence of a sale, such securities shall be valued at the mean between the current bid and ask prices on the day of valuation. Investments valued in currencies other than the U.S. dollar are converted to U.S. dollars using exchange rates obtained from pricing services. Investments in open-end investment companies are valued at net asset value. Short-term debt obligations having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost.

The Fund may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities will be valued using the “fair value” procedures approved by the Trust’s Board of Trustees (the “Board”). The Board has delegated execution of these procedures to a fair value committee composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) adviser. The committee may also enlist third party consultants such as a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist in determining a security-specific fair value. The Board has also engaged a third party valuation firm to attend valuation meetings held by the Trust, review minutes of such meetings and report to the Board on a quarterly basis. The Board reviews and ratifies the execution of this process and the resultant fair value prices at least quarterly to assure the process produces reliable results.

Fair Valuation Process – As noted above, the fair valuation committee is composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) adviser. The applicable investments are valued collectively via inputs from each of these groups. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source); (ii) securities for which, in the judgment of the adviser, the prices or values available do not represent the fair value of the instrument, factors which may cause the adviser to make such a judgment include, but are not limited to, the following: only a bid price or an asked price is available; the spread between bid and asked prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading, (iii) securities determined to be illiquid; and (iv) securities with respect to which an event that will affect the value thereof has occurred (a

| Al Frank Fund |

| NOTES TO FINANCIAL STATEMENTS at December 31, 2021 (Continued) |

“significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to a Fund’s calculation of its net asset value. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued via inputs from the adviser based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If the adviser is unable to obtain a current bid from such independent dealers or other independent parties, the fair value committee shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Fund’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Fund utilizes various methods to measure fair value of all of their investments on a recurring basis. GAAP establishes the hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of December 31, 2021 for the Fund’s assets measured at fair value:

| Al Frank Fund |

| NOTES TO FINANCIAL STATEMENTS at December 31, 2021 (Continued) |

| Al Frank Fund | |

| Common Stocks | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Communication Services | | $ | 5,142,363 | | | $ | — | | | $ | — | | | $ | 5,142,363 | |

| Consumer Discretionary | | | 8,283,570 | | | | — | | | | — | | | | 8,283,570 | |

| Consumer Staples | | | 3,716,910 | | | | — | | | | — | | | | 3,716,910 | |

| Energy | | | 2,930,565 | | | | — | | | | — | | | | 2,930,565 | |

| Financials | | | 13,740,950 | | | | — | | | | — | | | | 13,740,950 | |

| Health Care | | | 9,761,485 | | | | — | | | | — | | | | 9,761,485 | |

| Industrials | | | 10,521,973 | | | | — | | | | — | | | | 10,521,973 | |

| Information Technology | | | 19,427,015 | | | | — | | | | — | | | | 19,427,015 | |

| Materials | | | 4,151,896 | | | | — | | | | — | | | | 4,151,896 | |

| Real Estate | | | 2,711,985 | | | | — | | | | — | | | | 2,711,985 | |

| Utilities | | | 705,900 | | | | — | | | | — | | | | 705,900 | |

| Total Common Stocks | | | 81,094,612 | | | | — | | | | — | | | | 81,094,612 | |

| Short-Term Investment | | | | | | | | | | | | | | | | |

| Money Market Fund | | | 1,609,532 | | | | — | | | | — | | | | 1,609,532 | |

| Total Short-Term Investment | | | 1,609,532 | | | | — | | | | — | | | | 1,609,532 | |

| Total Investments | | $ | 82,704,144 | | | $ | — | | | $ | — | | | $ | 82,704,144 | |

There were no Level 3 securities held in the Fund during the year ended December 31, 2021.

NOTE 4 - INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES

Kovitz Investment Group Partners, LLC serves as the Fund’s investment adviser (the “Adviser”).

Pursuant to an investment advisory agreement with the Fund (the “Advisory Agreement”), the Adviser, under the oversight of the Board, directs the daily operations of the Fund and supervises the performance of administrative and professional services provided by others. As compensation for its services, the Fund pays the Adviser a management fee, computed and accrued daily and paid monthly, at an annual rate of 1.00% of the Fund’s average daily net assets (“Advisory Fees”).

For the year ended December 31, 2021, the Adviser earned $809,521 in Advisory Fees.

Pursuant to a written contract (the “Waiver Agreement”), the Adviser has agreed, at least until April 30, 2023, to waive a portion of its advisory fee and has agreed to reimburse the Fund for other expenses to the extent necessary so that the total expenses incurred by the Fund (excluding any front-end or contingent deferred loads, brokerage fees and commissions, acquired fund fees and expenses, borrowing costs, (such as interest and dividend expense on securities sold short) taxes and extraordinary expenses such as litigation) do not exceed 1.49% and 1.24% of the Fund’s average net assets for Investor Class and Advisor Class shares, respectively. Any such reduction made by the Adviser in its fees or payment of expenses which are the Fund’s obligation are subject to reimbursement by the Fund to the Adviser, if so requested by the Adviser, in subsequent fiscal years only if the aggregate amount actually paid by the Fund toward the operating expenses for such fiscal year (taking into account the reimbursement) would not cause the Fund to exceed the expense limitation in effect at the time of the waiver or currently in effect, whichever is lower. The Adviser is permitted to receive reimbursement from the Fund for fees it waived and Fund expenses it paid only if reimbursement is made within three years from the date the fees and expenses were initially waived or reimbursed. Any such reimbursement is also contingent upon the Board’s review and approval at the time the reimbursement is made. Such reimbursement may not be paid prior to the Fund’s payment of current ordinary operating expenses. For the year ended December 31, 2021, the Adviser waived its fees in the amount of $146,546.

| Al Frank Fund |

| NOTES TO FINANCIAL STATEMENTS at December 31, 2021 (Continued) |

Cumulative expenses subject to recapture pursuant to the aforementioned conditions expire as follows:

| | 12/31/2022 | | | 12/31/2023 | | | 12/31/2024 | |

| | $ | 105,460 | | | $ | 120,036 | | | $ | 146,546 | |

During the year ended December 31, 2021, $133,701 of previously waived fees expired unrecouped.

Distributor – The distributor for the Fund is Northern Lights Distributors LLC (the “Distributor”) and acts as the Fund’s principal underwriter in a continuous public offering of the Fund’s shares. The Board has adopted the Trust’s Master Distribution and Shareholder Servicing Plan for Investor Class shares (the “Investor Class Plan”) pursuant to Rule 12b-1 under the 1940 Act to pay for ongoing distribution-related activities or shareholder services. Under the Investor Class Plan, the Fund is permitted to pay a fee at an annual rate of 0.25% of the average daily net assets of the Fund’s Investor Class shares. The Fund pays the Distributor to provide compensation for ongoing distribution -related activities or services and/or maintenance of the Fund’s shareholder accounts, not otherwise required to be provided by the Adviser. The Plan is a compensation plan, which means that compensation is provided regardless of 12b-1 expenses incurred. For the year ended December 31, 2021, the Al Frank Fund Investor Class shares incurred 12b-1 fees of $188,044. For the year ended December 31, 2021, the Al Frank Fund Investor Class shares paid the Distributor underwriting fees of $0.

In addition, certain affiliates of the Distributor provide services to the Fund as follows:

Ultimus Fund Solutions, LLC (“UFS”), an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to separate servicing agreements with UFS, the Fund pays UFS customary fees for providing administration, fund accounting and transfer agency services to the Fund. Certain officers of the Trust are also officers of UFS, and are not paid any fees directly by the Fund for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”) – an affiliate of UFS and the Distributor, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives customary fees from the Fund.

Blu Giant, LLC (“Blu Giant”) – an affiliate of UFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Fund on an ad-hoc basis. For the provision of these services, Blu Giant receives customary fees from the Fund.

NOTE 5 – PURCHASES AND SALES OF SECURITIES

For the year ended December 31, 2021, the cost of purchases and the proceeds from sales of securities, excluding short-term securities, for the Fund was $3,963,736 and $9,211,404, respectively.

NOTE 6 - AGGREGATE UNREALIZED APPRECIATION & DEPRECIATION – TAX BASIS

| Cost for Federal Tax purposes | | $ | 37,953,916 | |

| | | | | |

| Unrealized Appreciation | | $ | 45,033,912 | |

| Unrealized Depreciation | | | (283,684 | ) |

| Tax Net Unrealized Appreciation | | $ | 44,750,228 | |

| Al Frank Fund |

| NOTES TO FINANCIAL STATEMENTS at December 31, 2021 (Continued) |

NOTE 7 – DISTRIBUTIONS TO SHAREHOLDERS AND TAX COMPONENTS OF CAPITAL

The tax character of portfolio distributions paid for the following years was as follows:

| | | Fiscal Year Ended | | | Fiscal Year Ended | |

| | | December 31, 2021 | | | December 31, 2020 | |

| Ordinary Income | | $ | 619,618 | | | $ | 1,350,709 | |

| Long-Term Capital Gain | | | 4,578,672 | | | | 3,321,586 | |

| | | $ | 5,198,290 | | | $ | 4,672,295 | |

As of December 31, 2021, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| Undistributed | | | Undistributed | | | | | | Capital Loss | | | Other | | | | | | Total | |

| Ordinary | | | Long-Term | | | Post | | | Carry | | | Book/Tax | | | Unrealized | | | Accumulated | |

| Income | | | Gains | | | October Loss | | | Forwards | | | Differences | | | Appreciation | | | Earnings | |

| $ | — | | | $ | 1,355,328 | | | $ | — | | | $ | — | | | $ | — | | | $ | 44,750,228 | | | $ | 46,105,556 | |

The difference between book basis and tax basis undistributed net investment income, accumulated net realized gain, and unrealized appreciation from investments is primarily attributable to the tax deferral of loss on wash sales and C-Corporation return of capital distributions.

NOTE 8 – CONTROL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of the Fund creates presumption of control of the Fund, under Section 2(a)(9) of the 1940 Act. As of December 31, 2021, Charles Schwab and Co. held approximately 28.5% of the voting securities of the Fund.

NOTE 9 – SUBSEQUENT EVENTS

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has determined that no events or transactions occurred requiring adjustment or disclosure in the financial statements.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Northern Lights Fund Trust II

and the Shareholders of Al Frank Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Al Frank Fund, a series of shares of beneficial interest in Northern Lights Fund Trust II (the “Fund”), including the schedule of investments, as of December 31, 2021, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, and the related notes (collectively referred to as the “financial statements” ). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2021, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2021 by correspondence with the custodian. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in the Northern Lights Fund Trust II since 2012.

Philadelphia, Pennsylvania

February 25, 2022

| Al Frank Fund |

| EXPENSE EXAMPLES at December 31, 2021 |

Generally, shareholders of mutual funds incur two types of costs: (1) transaction costs, redemption fees, and exchange fees, and (2) ongoing costs, including management fees, distribution and/or service fees, and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested in both the Investor Class and the Advisor Class at the beginning of the period and held for the entire period (7/1/21 – 12/31/21).

Actual Expenses

The first line of the tables below provides information about actual account values and actual expenses, with actual net expenses being limited to 1.49% and 1.24% per the operating expenses limitation agreement for the Al Frank Fund Investor Class and Advisor Class, respectively. Although the Fund does not charge a sales load or transaction fees, you will be assessed fees for outgoing wire transfers, returned checks, and stop payment orders at prevailing rates charged by Gemini Fund Services, LLC, the Funds’ transfer agent. The Example below includes, but is not limited to, management fees, 12b-1 fees, fund accounting, custody and transfer agent fees. You may use the information in the first line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $ 1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period’’ to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the tables below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund’s and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees, or exchange fees. Therefore, the second line of the tables is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these costs were included, your costs would have been higher.

| | | | | | | | | Expenses Paid | | | Expense Ratio |

| | | Beginning Account | | | Ending Account | | | During Period * | | | During Period ** |

| Actual | | Value 7/1/2021 | | | Value 12/31/2021 | | | 7/1/21-12/31/21 | | | 7/1/21-12/31/21 |

| Al Frank Fund | | | | | | | | | | | |

| | | Investor Class | | $ | 1,000.00 | | | $ | 1,042.70 | | | $ | 7.67 | | | 1.49% |

| | | Advisor Class | | | 1,000.00 | | | | 1,044.10 | | | | 6.39 | | | 1.24% |

| Hypothetical (5% return before Expenses) | | | | | | | | | | | | | | |

| Al Frank Fund | | | | | | | | | | | | | | |

| | | Investor Class | | $ | 1,000.00 | | | $ | 1,017.69 | | | $ | 7.58 | | | 1.49% |

| | | Advisor Class | | | 1,000.00 | | | | 1,018.95 | | | | 6.31 | | | 1.24% |

| * | Expenses are equal to the average account value over the period, multiplied by the Fund’s annualized expense ratio, multiplied by the number of days in the period (184) divided by the number of days in the fiscal year (365). |

| Al Frank Fund |

| SUPPLEMENTAL INFORMATION at December 31, 2021 (Unaudited) |

FACTORS CONSIDERED BY THE TRUSTEES IN THE APPROVAL OF THE RENEWAL OF THE INVESTMENT ADVISORY AGREEMENT

At a meeting (the “Meeting”) of the Board of Trustees (the “Board”) of Northern Lights Fund Trust II (the “Trust”) held on October 18 and 19, 2021, the Board, including the disinterested Trustees (the “Independent Trustees”), considered the approval of the renewal of the advisory agreement between Kovitz Investment Group Partners, LLC (“Kovitz”) and the Trust on behalf of the Al Frank Fund (the “Kovitz Advisory Agreement”)

��

Based on their evaluation of the information provided by Kovitz, in conjunction with the Al Frank Fund’s other service providers, the Board, by a unanimous vote (including a separate vote of the Independent Trustees), approved the Kovitz Advisory Agreement with respect to the Al Frank Fund.

In advance of the Meeting, the Board requested and received materials to assist them in considering the Kovitz Advisory Agreement. The materials provided contained information with respect to the factors enumerated below, including the Kovitz Advisory Agreement, a memorandum prepared by the Trust’s outside legal counsel discussing in detail the Trustees’ fiduciary obligations and the factors they should assess in considering the continuation of the Kovitz Advisory Agreement and comparative information relating to the advisory fee and other expenses of the Al Frank Fund. The materials also included due diligence materials relating to Kovitz (including due diligence questionnaires completed by Kovitz, select financial information of Kovitz, bibliographic information regarding Kovitz’s key management and investment advisory personnel, and comparative fee information relating to the Fund) and other pertinent information. At the Meeting, the Independent Trustees were advised by counsel that is experienced in Investment Company Act of 1940 matters and that is independent of fund management and met with such counsel separately from fund management.

The Board then reviewed and discussed the written materials that were provided in advance of the Meeting and deliberated on the approval of the renewal of the Kovitz Advisory Agreements with respect to the Al Frank Fund. The Board relied upon the advice of independent legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Kovitz Advisory Agreement and the weight to be given to each such factor. The conclusions reached by the Board were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the Kovitz Advisory Agreement. In considering the approval of the Kovitz Advisory Agreement, the Board reviewed and analyzed various factors that they determined were relevant, including the factors enumerated below.

Nature, Extent and Quality of Services. The Board reviewed materials provided by Kovitz related to the proposed renewal of the Kovitz Advisory Agreement, including its Form ADV and related schedules, a description of the manner in which investment decisions were made and executed, a review of the personnel performing services for the Al Frank Fund, including the individuals that primarily monitor and execute the investment process. The Board discussed the extent of the research capabilities, the quality of Kovitz’s compliance infrastructure and the experience of its investment advisory personnel. The Board noted that Kovitz was an experienced investment adviser with seasoned senior management and that the performance of the Al Frank Fund supported the quality and experience of the staff. Additionally, the Board received satisfactory responses from the representatives of Kovitz with respect to a series of important questions, including: whether Kovitz was involved in any lawsuits or pending regulatory actions; whether the advisory services provided to its other accounts would conflict with the advisory services provided to the Al Frank Fund; whether there were procedures in place to adequately allocate trades among its respective clients; and whether Kovitz’s CCO had processes in place to review the portfolio managers’ performance of their duties to ensure compliance under Kovitz’s compliance program. The Board reviewed the information provided on the practices for monitoring compliance with the Al Frank Fund’s investment limitations and discussed Kovitz’s compliance program with the CCO of the Trust. The Board noted that the CCO of the Trust continued to represent that Kovitz’s policies and procedures were reasonably designed to prevent violations of applicable federal securities laws. The Board also noted Kovitz’s representation that the prospectus and statement of additional information for the Al Frank Fund accurately describe the investment strategies of the Al Frank Fund. The Board then reviewed the capitalization of Kovitz based on financial information provided by and representations made by Kovitz and its representatives and concluded that Kovitz was sufficiently well- capitalized, or its principals have the ability to make additional contributions in order to meet its obligations to the Al Frank Fund. The Board concluded that Kovitz had sufficient

| Al Frank Fund |

| SUPPLEMENTAL INFORMATION at December 31, 2021 (Unaudited)(Continued) |

quality and depth of personnel, resources, investment methods and compliance policies and procedures essential to performing its duties under the Kovitz Advisory Agreement and that the nature, overall quality and extent of the advisory services to be provided by Kovitz to the Al Frank Fund were satisfactory.

Performance. The Board discussed the report prepared by Broadridge and reviewed the performance as compared to its peer group, Morningstar category and benchmark for the one year, three year, five year and since inception periods ended September 30, 2021 for the Al Frank Fund. The Board noted the Al Frank Fund outperformed its peer group median, Morningstar category median, and benchmark, the S&P 500 Index, for the one year and since inception periods, and outperformed its peer group median and Morningstar category median but underperformed its benchmark for the three and five year periods. The Board further noted the Al Frank Fund was the only fund in its peer group and Morningstar category to outperform the S&P 500 Index since 1998. After further discussion, the Board concluded that the performance of the Al Frank Fund was acceptable.

Fees and Expenses. As to the costs of the services provided by Kovitz, the Board reviewed and discussed the advisory fee and total operating expenses of the Al Frank Fund as compared to its peer group and its Morningstar category as presented in the Broadridge Report. The Board noted that the 1.00% advisory fee was at or near the high end of its Morningstar category and peer group although it was not the highest in its Morningstar category. The Board noted that the Al Frank Fund’s higher net expense ratio may be explained by relatively lower asset levels than some of its peers and less ability to benefit from economies of scale.

The Board then reviewed the contractual arrangements for the Al Frank Fund, which stated that Kovitz had agreed to waive or limit its advisory fee and/or reimburse expenses at least until April 30, 2023, in order to limit net annual operating expenses, exclusive of certain fees, so as not to exceed: 1.49% and 1.24% of the Al Frank Fund’s average net assets for Investor Class and Advisor Class shares, respectively, and found such arrangements to be beneficial to shareholders. The Board concluded that, based on Kovitz’s experience, expertise and services provided to the Al Frank Fund, the advisory fee charged by Kovitz, although at the high end the Al Frank Fund’s peer group, was not unreasonable.

Profitability. The Board also considered the level of profits that could be expected to accrue to Kovitz with respect to the Al Frank Fund based on profitability reports and profitability analyses provided by Kovitz. The Board also reviewed the selected financial information of Kovitz provided by Kovitz. After review and discussion, the Board concluded that the anticipated profit from Kovitz’s relationship with the Al Frank Fund was not excessive.

Economies of Scale. As to the extent to which the Al Frank Fund would realize economies of scale as it grows, and whether the fee levels reflect these economies of scale for the benefit of investors, the Board discussed the current size of the Al Frank Fund and Kovitz’s expectations for growth, and concluded that any material economies of scale would not be achieved in the near term.

Conclusion. The Board relied upon the advice of counsel, and their own business judgment in determining the material factors to be considered in evaluating the Kovitz Advisory Agreement and the weight to be given to each such factor. Accordingly, having requested and received such information from Kovitz as the Trustees believed to be reasonably necessary to evaluate the terms of the Kovitz Advisory Agreement, and as assisted by the advice of independent counsel, the Board, including a majority of the Independent Trustees voting separately, determined that (a) the terms of the Kovitz Advisory Agreement are not unreasonable; (b) the investment advisory fee payable pursuant to the Kovitz Advisory Agreement is not unreasonable; and (c) the Kovitz Advisory Agreement is in the best interests of the Al Frank Fund and its shareholders. Moreover, the Board noted that each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the Kovitz Advisory Agreement.

| Al Frank Fund |

| LIQUIDITY RISK MANAGEMENT PROGRAM (Unaudited) |

| December 31, 2021 |

The Fund has adopted and implemented a written liquidity risk management program as required by Rule 22e-4 (the “Liquidity Rule”) under the 1940 Act. The program is reasonably designed to assess and manage the Fund’s liquidity risk, taking into consideration, among other factors, the Fund’s investment strategy and the liquidity of its portfolio investments during normal and reasonably foreseeable stressed conditions; its short and long-term cash flow projections; and its cash holdings and access to other funding sources.

During the fiscal period ended December 31, 2021, the Trust’s Liquidity Risk Management Program Committee (the “Committee”) reviewed the Fund’s investments and determined that the Fund held adequate levels of cash and highly liquid investments to meet shareholder redemption activities in accordance with applicable requirements. Accordingly, the Committee concluded that (i) the Fund’s liquidity risk management program is reasonably designed to prevent violations of the Liquidity Rule and (ii) the Fund’s liquidity risk management program has been effectively implemented.

| Al Frank Fund |

| SUPPLEMENTAL INFORMATION at December 31, 2021 (Unaudited) |

The Trustees and the officers of the Trust are listed below with their present positions with the Trust and principal occupations over at least the last five years. The business address of each Trustee and Officer is 225 Pictoria Drive, Suite 450, Cincinnati, OH 45246. All correspondence to the Trustees and Officers should be directed to c/o Gemini Fund Services, LLC, P.O. Box 541150, Omaha, Nebraska 68154.

Independent Trustees

Name and

Year of Birth | Position/Term of

Office* | Principal Occupation

During the Past Five Years | Number of

Portfolios in

Fund

Complex

Overseen by

Trustee *** | Other Directorships held by

Trustee

During the Past Five Years |

Thomas T. Sarkany

1946 | Trustee Since October 2011 | President, TTS Consultants, LLC (financial services) (since 2010). | 1 | Director, Aquila Distributors; Trustee, Arrow ETF Trust; Trustee, Arrow Investments Trust; Trustee, Northern Lights Fund Trust IV |

Anthony H.Lewis