UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FormN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number811-22551

MAINSTAY MACKAY DEFINEDTERM

MUNICIPAL OPPORTUNITIES FUND

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212)576-7000

Date of fiscal year end: May 31

Date of reporting period: May 31, 2019

| Item 1. | Reports to Stockholders. |

MainStay MacKay DefinedTerm Municipal Opportunities Fund

Message from the President and Annual Report

May 31, 2019 | NYSE SymbolMMD

Beginning on January 1, 2021, paper copies of MainStay Fund annual and semiannual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from MainStay Funds or from your financial intermediary. Instead, the reports will be made available on the MainStay Funds’ website. You will be notified by mail and provided with a website address to access the report each time a new report is posted to the website.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and other communications from MainStay Funds electronically by calling toll-free 800-624-6782, by sending an e-mail to MainStayShareholderServices@nylim.com, or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper form free of charge. If you hold shares of a MainStay Fund directly, you can inform MainStay Funds that you wish to receive paper copies of reports by calling toll-free 800-624-6782 or by sending an e-mail to MainStayShareholderServices@nylim.com. If you hold shares of a MainStay Fund through a financial intermediary, please contact the financial intermediary to make this election. Your election to receive reports in paper form will apply to all MainStay Funds in which you are invested and may apply to all funds held with your financial intermediary.

| | | | | | | | |

| | | | | |

| Not FDIC/NCUA Insured | | Not a Deposit | | May Lose Value | | No Bank Guarantee | | Not Insured by Any Government Agency |

This page intentionally left blank

Message from the President

Macroeconomic and political uncertainties unsettled financial markets during the 12-month period ended May 31, 2019, leading to rising levels of volatility. However, most sectors of the fixed-income market, including municipal bonds, delivered positive results.

The reporting period began with strong U.S. economic expansion and moderate levels of growth in much of the developed world, accompanied by historically low interest rates and restrained inflation. Despite generally positive economic conditions, bonds struggled to gain ground as the U.S. Federal Reserve Board (Fed) gradually hiked its benchmark funds rate and signaled the prospect of further interest rate increases. The Fed’s outlook shifted in late 2019 over concerns regarding the pace of global economic growth and the potential impact of trade disputes between the United States and other nations, particularly China. Although equity markets fell in December in the face of a government shutdown, fixed-income instruments generally maintained their value as interest-rate concerns lessened.

Bonds moved broadly higher in January 2019 as trade tensions eased, the government reopened and the Fed adopted a more accommodative tone regarding the future direction of interest rates. The next three months experienced further gains across financial markets, supported by encouraging economic data and generally strong corporate earnings. Although equities and high-yield corporate bonds dipped in May 2019, in response to deepening tensions between the United States and China and renewed concerns regarding slowing global economic growth, municipal bonds and most other sectors of the fixed-income market continued to move higher.

For the reporting period as a whole, municipal bonds generally provided returns comparable to those of corporate bonds while experiencing lower levels of volatility. Higher credit quality, longer-duration securities led the group. Municipal bonds also benefited from positive state and local trends in revenue and economic growth. In particular, municipal bonds issued by Puerto Rico and the U.S. Virgin Islands rebounded strongly as the territories recovered from the impact of hurricanes that occurred in 2017.

Amid volatile conditions for most financial markets, we are pleased that MainStay MacKay DefinedTerm Municipal Opportunities Fund helped shareholders capitalize on opportunities in the municipal bond market. We remain sharply focused on providing you with the experienced and disciplined Fund management that we believe underpins an effective, long-term investment strategy. Whatever tomorrow’s investment environment brings, you can rely on our portfolio managers to pursue the Fund’s objectives with the energy and dedication you have come to expect.

Sincerely,

Kirk C. Lehneis

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Past performance is no guarantee of future results.

Not part of the Annual Report

Table of Contents

Certain material in this report may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates and information about possible or future results or events related to the Fund, market or regulatory developments. The views expressed herein are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed herein are subject to change at any time based upon economic, market, or other conditions and the Fund undertakes no obligation to update the views expressed herein.

Fund Performance and Statistics(Unaudited)

Performance data quoted represents past performance of Common shares of the Fund. Past performance is no guarantee of future results. Because of market volatility and other factors, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. For performance information current to the most recent month-end, please visit nylinvestments.com/mmd.

| | | | | | | | | | | | |

| Total Returns | | One Year | | | Five Years | | | Since Inception 6/26/12 | |

| | | |

| Net Asset Value (“NAV”)1 | | | 6.80 | % | | | 7.55 | % | | | 7.28 | % |

| | | |

| Market Price1 | | | 12.05 | | | | 9.01 | | | | 6.95 | |

| | | |

| Bloomberg Barclays Municipal Bond Index2 | | | 6.40 | | | | 3.58 | | | | 3.49 | |

| | | |

| Morningstar Muni National Long Category Average3 | | | 7.47 | | | | 5.25 | | | | 5.42 | |

| | | | | | | | | | |

| Fund Statistics (as of May 31, 2019) | | | | | | | | |

| | | |

| NYSE Symbol | | | MMD | | | Premium/Discount4 | | | 1.18 | % |

| | | |

| CUSIP | | | 56064K100 | | | Total Net Assets (millions) | | $ | 563.1 | |

| | | |

| Inception Date | | | 6/26/12 | | | Total Managed Assets (millions)5 | | $ | 894.2 | |

| | | |

| Market Price | | | $20.65 | | | Leverage6 | | | 37.0 | % |

| | | |

| NAV | | | $20.41 | | | Percent of AMT Bonds7 | | | 1.55 | % |

| 1. | Total returns assume dividends and capital gains distributions are reinvested. For periods of less than one year, total return is not annualized. |

| 2. | The Bloomberg Barclays Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. An investment cannot be made directly in an index. |

| 3. | The Morningstar Muni National Long Category Average is representative of funds that invest in bonds issued by various state and local governments to fund public projects. The income from these bonds is generally free from federal taxes. These portfolios have durations of more than 7 years. Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

| 4. | Premium/Discount is the percentage (%) difference between the market price and the NAV. When the market price exceeds the NAV, the Fund is |

| | trading at a premium. When the market price is less than the NAV, the Fund is trading at a discount. |

| 5. | “Managed Assets” is defined as the Fund’s total assets, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of creating effective leverage (i.e. tender option bonds) or Fund liabilities related to liquidation preference of any Preferred shares issued). |

| 6. | Leverage is based on the use of proceeds received from tender option bond transactions, issuance of Preferred shares, funds borrowed from banks or other institutions or derivative transactions, expressed as a percentage of Managed Assets. |

| 7. | Alternative Minimum Tax (“AMT”) is a separate tax computation under the Internal Revenue Code that, in effect, eliminates many deductions and credits and creates a tax liability for an individual who would otherwise pay little or no tax. |

Portfolio Composition as of May 31, 2019†(Unaudited)

| | | | |

| |

| Puerto Rico (a) | | | 17.8 | % |

| |

| Illinois | | | 11.5 | |

| |

| California | | | 10.5 | |

| |

| Michigan | | | 9.0 | |

| |

| Texas | | | 6.0 | |

| |

| Florida | | | 4.8 | |

| |

| New York | | | 4.6 | |

| |

| Virginia | | | 3.1 | |

| |

| U.S. Virgin Islands | | | 3.0 | |

| |

| Washington | | | 2.7 | |

| |

| Maryland | | | 2.6 | |

| |

| Pennsylvania | | | 2.6 | |

| |

| Nebraska | | | 2.4 | |

| |

| Kansas | | | 2.3 | |

| |

| South Carolina | | | 2.3 | |

| |

| Guam | | | 1.8 | |

| |

| Ohio | | | 1.8 | |

| |

| Rhode Island | | | 1.8 | |

| | | | |

| |

| Utah | | | 1.6 | % |

| |

| Nevada | | | 1.5 | |

| |

| Idaho | | | 0.7 | |

| |

| Massachusetts | | | 0.7 | |

| |

| North Dakota | | | 0.6 | |

| |

| New Hampshire | | | 0.5 | |

| |

| New Jersey | | | 0.4 | |

| |

| Colorado | | | 0.3 | |

| |

| District of Columbia | | | 0.3 | |

| |

| Wyoming | | | 0.3 | |

| |

| Arizona | | | 0.2 | |

| |

| Minnesota | | | 0.2 | |

| |

| Tennessee | | | 0.2 | |

| |

| Connecticut | | | 0.1 | |

| |

| Wisconsin | | | 0.1 | |

| |

| Other Assets, Less Liabilities | | | 1.7 | |

| | | | |

| |

| | | 100.0 | % |

| | | | |

See Portfolio of Investments beginning on page 9 for specific holdings within these categories. The Fund’s holdings are subject to change.

Top Ten Holdings or Issuers Held as of May 31, 2019#(Unaudited)

| 1. | Great Lakes Water Authority, Sewage Disposal System, Revenue Bonds, 5.00%–5.25%, due 7/1/32–7/1/39 |

| 2. | Texas Water Development Board, Revenue Bonds, 5.00%, due 4/15/49 |

| 3. | County of Orange FL Tourist Development Tax Revenue, Revenue Bonds, 4.00%, due 10/10/33 |

| 4. | Commonwealth of Puerto Rico, Public Improvement, Unlimited General Obligation, 4.50%–6.00%, due 7/1/19–7/1/37 (b) |

| 5. | Puerto Rico Highway & Transportation Authority, Revenue Bonds, 4.95%–5.50%, due 7/1/25–7/1/36 (b) |

| 6. | University of California, Regents Medical Center, Revenue Bonds, 5.00%, due 5/15/43 |

| 7. | Michigan Finance Authority, Trinity Health Corp., Revenue Bonds, 5.25%, due 12/1/41 |

| 8. | Chicago Board of Education, Unlimited General Obligation, 5.50%–7.00%, due 12/1/39–12/1/44 (b) |

| 9. | Maryland Health & Higher Educational Facilities Authority, Johns Hopkins Health System Obligated Group, Revenue Bonds, 5.00%, due 5/15/43 |

| 10. | Puerto Rico Sales Tax Financing Corp., Revenue Bonds, 4.50%–5.00%, due 7/1/34–7/1/58 |

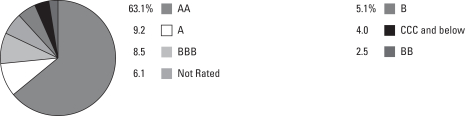

Credit Quality as of May 31, 2019‡(Unaudited)

Ratings apply to the underlying portfolio of bonds held by the Fund and are rated by an independent rating agency, such as Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. and/or Fitch Ratings, Inc. If the ratings provided by the ratings agencies differ, the higher rating will be utilized. If only one rating is provided, the available rating will be utilized. Securities that are unrated by the rating agencies are reflected as such in the breakdown. Unrated securities do not necessarily indicate low quality. S&P rates borrowers on a scale from AAA to D. AAA throughBBB- represent investment grade, while BB+ through D representnon-investment grade.

| † | As a percentage of Managed Assets. |

| # | Some of these holdings have been transferred to a Tender Option Bond (“TOB”) Issuer in exchange for the TOB residuals and cash. |

| ‡ | As a percentage of total investments. |

| (a) | As of May 31, 2019, 91.2% of the Puerto Rico municipal securities held by the Fund were insured and all bonds continue to pay full principal and interest. |

| (b) | Municipal security may feature credit enhancements, such as bond insurance. |

| | |

| 6 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund |

Portfolio Management Discussion and Analysis(Unaudited)

Questions answered by portfolio managers Robert DiMella, CFA, John Loffredo, CFA, Michael Petty, Scott Sprauer and David Dowden of MacKay Shields LLC, the Fund’s Subadvisor.

How did MainStay MacKay DefinedTerm Municipal Opportunities Fund perform relative to its benchmark and peer group during the 12 months ended May 31, 2019?

For the 12 months ended May 31, 2019, MainStay MacKay DefinedTerm Municipal Opportunities Fund returned 6.80% based on net asset value applicable to Common shares and 12.05% based on market price. At net asset value and at market price, the Fund outperformed the 6.40% return of the Bloomberg Barclays Municipal Bond Index. The Fund underperformed at net asset value and outperformed at market price the 7.47% return of the Morningstar Muni National Long Category Average.1

What factors affected the Fund’s relative performance during the reporting period?

The Fund’s performance relative to the Bloomberg Barclays Municipal Bond Index benefited from good security selection, particularly in Puerto Rico, Virgin Islands and Illinois-issued debt. The Fund’s barbell yield curve2 strategy further contributed to relative performance as the municipal yield curve continued to flatten in line with the U.S. Treasury yield curve. (Contributions take weightings and total returns into account.) Overweight exposure to insured bonds enhanced relative performance as well, as this sector outperformed the general municipal market.

How was the Fund’s leverage strategy implemented during the reporting period?

The Fund increased its leverage utilizing tender option bonds (TOBs)3 during the reporting period. Increasing the leverage allowed the Fund to reduce its spread4 duration5 risk and maintain an attractive dividend for Fund shareholders. This reduction in credit risk is in line with changes to the Fund’s allocation strategy over the past twelve months.

During the reporting period, how was the Fund’s performance materially affected by investments in derivatives?

The use of derivatives, specifically U.S. Treasury futures, allows the Fund to manage its effective duration and maximize an attractive tax-exempt stream of income for our shareholders. During the reporting period, the Fund’s investments in derivatives detracted from the Fund’s performance.

What was the Fund’s duration strategy during the reporting period?

The Fund maintained a slightly defensive duration profile compared to the Bloomberg Barclays Municipal Bond Index during the reporting period. As of May 31, 2019, the Fund’s modified duration to worst6 was 4.1 years unlevered, or 3.71 years leveraged.

During the reporting period, which sectors were the strongest positive contributors to the Fund’s relative performance and which sectors were particularly weak?

During the reporting period, the Fund’s relative performance benefited most significantly from underweight exposure to state general obligation and pre-refunded bonds, and from overweight exposure to special tax and water & sewer bonds. Both transportation and local general obligation bonds detracted from relative returns during the same period.

What were some of the Fund’s largest purchases and sales during the reporting period?

Some of the Fund’s largest purchases during the reporting period included relatively high-quality, intermediate-maturity bonds, which featured attractive spreads. In particular, the Fund increased its exposure to GNMA-backed state housing bonds, which are AA-rated,7 five-year average life bonds with attractive yields. One of the largest single issues purchased was in South Carolina Patriots Energy five-year mandatory put bonds, which are AA-rated. The largest sales executed during the reporting

| 1. | See page 5 for more information on benchmark and peer group returns. |

| 2. | The yield curve is a line that plots the yields of various securities of similar quality—typically U.S. Treasury issues—across a range of maturities. The U.S. Treasury yield curve serves as a benchmark for other debt and is used in economic forecasting. |

| 3. | Tender option bonds are obligations that grant the bondholder the right to require the issuer or a third party (e.g., a tender agent) to purchase the bonds, usually at par, at certain times or under certain conditions prior to maturity. The tender option right is usually available to the investor on a periodic basis. Often, these are floating-rate securities, with the put option exercisable on the dates when the floating rate changes. |

| 4. | The terms “spread” and “yield spread” may refer to the difference in yield between a security or type of security and comparable U.S. Treasury issues. The terms may also refer to the difference in yield between two specific securities or types of securities at a given time. |

| 5. | Duration is a measure of the price sensitivity of a fixed-income investment to changes in interest rates. Duration is expressed as a number of years and is considered a more accurate sensitivity gauge than average maturity. |

| 6. | Modified duration is inversely related to the approximate percentage change in price for a given change in yield. Duration to worst is the duration of a bond computed using the bond’s nearest call date or maturity, whichever comes first. This measure ignores future cash flow fluctuations due to embedded optionality. |

| 7. | An obligation rated ‘AA’ by Standard & Poor’s (“S&P”) is deemed by S&P to differ from the highest-rated obligations only to a small degree. In the opinion of S&P, the obligor’s capacity to meet its financial commitment on the obligation is very strong. When applied to Fund holdings, ratings are based solely on the creditworthiness of the bonds in the portfolio and are not meant to represent the security or safety of the Fund. |

period included lower credit quality bonds, such as tobacco-backed bonds and United Airline bonds, as well as bonds with long-dated maturities.

The purchases and sales cited above reflected our opinion that the prevailing environment of compressing credit spreads and a flattening yield curve provided an attractive opportunity to increase the Fund’s overall credit quality and to reduce its exposure to long-dated bonds.

How did the Fund’s sector weightings change during the reporting period?

During the reporting period, the Fund decreased its exposure most significantly to the hospital and pre-refunded sectors,

while increasing its exposure to the housing and water/sewer sectors.

How was the Fund positioned at the end of the reporting period?

As of May 31, 2019, the Fund held overweight exposure relative to the Bloomberg Barclays Municipal Bond Index in the special tax and leasing sectors, and underweight exposure to the pre-refunded and education sectors. Regarding credit quality, at the same point in time the Fund held overweight exposure to AA-rated securities and underweighted exposure to AAA- and A-rated securities.8 The Fund’s duration posture remained slightly defensive.

| 8. | An obligation rated ‘AAA’ has the highest rating assigned by S&P, and in the opinion of S&P, the obligor’s capacity to meet its financial commitment on the obligation is extremely strong. An obligation rated ‘A’ by S&P is deemed by S&P to be somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligations in higher-rated categories. In the opinion of S&P, however, the obligor’s capacity to meet its financial commitment on the obligation is still strong. When applied to Fund holdings, ratings are based solely on the creditworthiness of the bonds in the portfolio and are not meant to represent the security or safety of the Fund. |

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| | |

| 8 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund |

Portfolio of InvestmentsMay 31, 2019

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Municipal Bonds 156.0%† | |

Arizona 0.3% (0.2% of Managed Assets) | |

Phoenix Industrial Development Authority, Espiritu Community Development Corp., Revenue Bonds

Series A

6.25%, due 7/1/36 | | $ | 1,985,000 | | | $ | 1,985,854 | |

| | | | | | | | |

|

California 16.7% (10.5% of Managed Assets) | |

California Municipal Finance Authority, LAX Integrated Express Solutions Project, Revenue Bonds (a) | | | | | | | | |

Series A

5.00%, due 12/31/33 | | | 3,800,000 | | | | 4,517,250 | |

Series A

5.00%, due 12/31/34 | | | 4,000,000 | | | | 4,737,680 | |

City of Sacramento, California, Water, Revenue Bonds

5.00%, due 9/1/42 (b) | | | 19,500,000 | | | | 22,089,080 | |

Golden State Tobacco Securitization Corp., Asset-Backed, Revenue Bonds | | | | | | | | |

Series A-1

5.00%, due 6/1/34 | | | 8,000,000 | | | | 9,245,920 | |

Series A-2

5.30%, due 6/1/37 | | | 5,225,000 | | | | 5,340,055 | |

Riverside County Transportation Commission, Limited Tax, Revenue Bonds

Series A

5.25%, due 6/1/39 (b) | | | 19,100,000 | | | | 22,036,697 | |

Stockton Public Financing Authority, Parking & Capital Projects, Revenue Bonds

Insured: NATL-RE

4.80%, due 9/1/20 | | | 105,000 | | | | 105,189 | |

University of California, Regents Medical Center, Revenue Bonds

Series J

5.00%, due 5/15/43 (b) | | | 23,260,000 | | | | 25,797,203 | |

| | | | | | | | |

| | | | | | | 93,869,074 | |

| | | | | | | | |

Colorado 0.5% (0.3% of Managed Assets) | |

Dominion Water & Sanitation District, Revenue Bonds

6.00%, due 12/1/46 | | | 2,500,000 | | | | 2,689,250 | |

| | | | | | | | |

|

Connecticut 0.2% (0.1% of Managed Assets) | |

City of Hartford CT, Unlimited General Obligation

Series A

5.00%, due 4/1/31 | | | 1,000,000 | | | | 1,100,420 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

District of Columbia 0.5% (0.3% of Managed Assets) | |

Metropolitan Washington Airports Authority Dulles Toll Road, Revenue Bonds

Series C, Insured: AGC

6.50%, due 10/1/41 | | $ | 2,400,000 | | | $ | 3,090,960 | |

| | | | | | | | |

|

Florida 7.6% (4.8% of Managed Assets) | |

County of Orange FL Tourist Development Tax Revenue, Revenue Bonds

4.00%, due 10/10/33 (b) | | | 25,000,000 | | | | 27,746,299 | |

JEA Electric System, Revenue Bonds | | | | | | | | |

Series B

4.00%, due 10/1/38 | | | 645,000 | | | | 707,152 | |

Series C

5.00%, due 10/1/37 (b) | | | 12,980,000 | | | | 14,207,370 | |

| | | | | | | | |

| | | | | | | 42,660,821 | |

| | | | | | | | |

Guam 2.9% (1.8% of Managed Assets) | |

Guam Government, Business Privilege Tax, Revenue Bonds

Series B-1

5.00%, due 1/1/42 | | | 3,800,000 | | | | 3,946,300 | |

Guam Government, Waterworks Authority, Revenue Bonds

5.50%, due 7/1/43 | | | 7,550,000 | | | | 8,250,036 | |

Guam International Airport Authority, Revenue Bonds

Series C, Insured: AGM

6.00%, due 10/1/34 (a) | | | 3,425,000 | | | | 4,001,702 | |

| | | | | | | | |

| | | | | | | 16,198,038 | |

| | | | | | | | |

Idaho 1.0% (0.7% of Managed Assets) | |

Idaho Housing & Finance Association, Revenue Bonds

Series A, Insured: GNMA

4.50%, due 1/21/49 | | | 5,471,463 | | | | 5,805,386 | |

| | | | | | | | |

|

Illinois 18.3% (11.5% of Managed Assets) | |

Chicago Board of Education Dedicated Capital Improvement, Revenue Bonds

5.75%, due 4/1/34 | | | 8,000,000 | | | | 9,317,600 | |

Chicago Board of Education Dedicated Capital Improvement, Unlimited General Obligation (c) | | | | | | | | |

Series B

7.00%, due 12/1/42 | | | 3,500,000 | | | | 4,352,425 | |

Series A

7.00%, due 12/1/46 | | | 4,000,000 | | | | 4,960,960 | |

Chicago Board of Education, Unlimited General Obligation | | | | | | | | |

Series A, Insured: AGM

5.50%, due 12/1/39 (b) | | | 20,000,000 | | | | 21,519,800 | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | | | | 9 | |

Portfolio of InvestmentsMay 31, 2019 (continued)

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Municipal Bonds (continued) | |

Illinois 18.3% (11.5% of Managed Assets) (continued) | |

Chicago Board of Education, Unlimited General Obligation (continued) | | | | | | | | |

Series A

7.00%, due 12/1/44 | | $ | 2,880,000 | | | $ | 3,432,326 | |

Chicago O’Hare International Airport, Revenue Bonds

Insured: AGM

5.75%, due 1/1/38 | | | 5,000,000 | | | | 5,665,650 | |

Chicago, Illinois Wastewater Transmission, Revenue Bonds

Series C

5.00%, due 1/1/32 | | | 7,120,000 | | | | 7,979,455 | |

Chicago, Unlimited General Obligation | | | | | | | | |

Series C

5.00%, due 1/1/25 | | | 1,435,000 | | | | 1,509,075 | |

Series D

5.00%, due 1/1/29 | | | 500,000 | | | | 501,185 | |

Series A

5.25%, due 1/1/27 | | | 3,000,000 | | | | 3,342,030 | |

Series A

6.00%, due 1/1/38 | | | 4,430,000 | | | | 5,147,084 | |

Illinois Sports Facilities Authority, Revenue Bonds

Insured: AGM

5.25%, due 6/15/32 | | | 150,000 | | | | 167,301 | |

Public Building Commission of Chicago, Chicago Transit Authority, Revenue Bonds

Insured: AMBAC

5.25%, due 3/1/31 | | | 600,000 | | | | 718,416 | |

Sales Tax Securitization Corp., Revenue Bonds

Series C, Insured: BAM

5.25%, due 1/1/48 (b) | | | 11,000,000 | | | | 12,960,778 | |

State of Illinois, Unlimited General Obligation

5.25%, due 7/1/31 (b) | | | 20,000,000 | | | | 21,653,826 | |

| | | | | | | | |

| | | | | | | 103,227,911 | |

| | | | | | | | |

Kansas 3.7% (2.3% of Managed Assets) | |

Kansas Development Finance Authority, Adventist Health Sunbelt Obligated Group, Revenue Bonds

Series A

5.00%, due 11/15/32 (b) | | | 19,290,000 | | | | 20,915,751 | |

| | | | | | | | |

|

Maryland 4.1% (2.6% of Managed Assets) | |

Maryland Health & Higher Educational Facilities Authority, Johns Hopkins Health System Obligated Group, Revenue Bonds

Series C

5.00%, due 5/15/43 (b) | | | 20,870,000 | | | | 23,070,214 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Massachusetts 1.1% (0.7% of Managed Assets) | |

Commonwealth of Massachusetts, Limited General Obligation

Series A

5.25%, due 1/1/44 | | $ | 5,000,000 | | | $ | 6,214,350 | |

| | | | | | | | |

|

Michigan 14.2% (9.0% of Managed Assets) | |

Great Lakes Water Authority, Sewage Disposal System, Revenue Bonds | | | | | | | | |

Senior Lien-Series A

5.00%, due 7/1/32 | | | 1,500,000 | | | | 1,627,500 | |

Series B, Insured: AGM

5.00%, due 7/1/34 (b) | | | 24,940,000 | | | | 29,630,341 | |

Senior Lien-Series A

5.25%, due 7/1/39 | | | 5,000,000 | | | | 5,441,000 | |

Great Lakes Water Authority, Water Supply System, Revenue Bonds | | | | | | | | |

Senior Lien-Series C

5.00%, due 7/1/41 | | | 1,005,000 | | | | 1,055,180 | |

Senior Lien-Series A

5.25%, due 7/1/41 | | | 2,385,000 | | | | 2,542,029 | |

Senior Lien-Series A

5.75%, due 7/1/37 | | | 5,000,000 | | | | 5,401,850 | |

Michigan Finance Authority, Trinity Health Corp., Revenue Bonds

Series 2016

5.25%, due 12/1/41 (b) | | | 21,630,000 | | | | 25,391,032 | |

Michigan Public Educational Facilities Authority, Dr. Joseph F. Pollack, Revenue Bonds | | | | | | | | |

8.00%, due 4/1/30 | | | 1,195,000 | | | | 1,223,692 | |

8.00%, due 4/1/40 | | | 500,000 | | | | 511,475 | |

Michigan Tobacco Settlement Finance Authority, Revenue Bonds

Series A

6.00%, due 6/1/48 | | | 5,200,000 | | | | 5,200,104 | |

Wayne County Michigan, Capital Improvement, Limited General Obligation

Series A, Insured: AGM

5.00%, due 2/1/38 | | | 2,135,000 | | | | 2,140,145 | |

| | | | | | | | |

| | | | | | | 80,164,348 | |

| | | | | | | | |

Minnesota 0.4% (0.2% of Managed Assets) | |

Blaine Minnesota Senior Housing & Healthcare, Crest View Senior Community Project, Revenue Bonds

Series A

5.75%, due 7/1/35 | | | 2,000,000 | | | | 2,016,200 | |

| | | | | | | | |

|

Nebraska 3.9% (2.4% of Managed Assets) | |

Central Plains Energy, Project No. 3, Revenue Bonds

5.25%, due 9/1/37 (b) | | | 20,000,000 | | | | 21,816,700 | |

| | | | | | | | |

| | | | |

| 10 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Municipal Bonds (continued) | |

Nevada 2.4% (1.5% of Managed Assets) | |

City of Reno NV, Transportation Rail Access Project, Revenue Bonds | | | | | | | | |

Series B, Insured: AGM

5.00%, due 6/1/26 | | $ | 410,000 | | | $ | 485,206 | |

Series B, Insured: AGM

5.00%, due 6/1/27 | | | 430,000 | | | | 515,768 | |

City of Sparks, Tourism Improvement District No. 1, Senior Sales Tax Anticipation, Revenue Bonds

Series A

6.75%, due 6/15/28 | | | 12,500,000 | | | | 12,511,875 | |

| | | | | | | | |

| | | | | | | 13,512,849 | |

| | | | | | | | |

New Hampshire 0.7% (0.5% of Managed Assets) | |

Manchester Housing & Redevelopment Authority, Inc., Revenue Bonds

Series B, Insured: ACA

(zero coupon), due 1/1/24 | | | 4,740,000 | | | | 3,993,687 | |

| | | | | | | | |

|

New Jersey 0.6% (0.4% of Managed Assets) | |

New Jersey Economic Development Authority, The Goethals Bridge Replacement Project, Revenue Bonds Insured: AGM

5.125%, due 1/1/39 (a) | | | 500,000 | | | | 559,755 | |

New Jersey Housing & Mortgage Finance Agency, Revenue Bonds

Series C

4.75%, due 10/1/50 | | | 2,500,000 | | | | 2,773,475 | |

Tobacco Settlement Financing Corp., Revenue Bonds

Series A

5.00%, due 6/1/46 | | | 300,000 | | | | 335,931 | |

| | | | | | | | |

| | | | | | | 3,669,161 | |

| | | | | | | | |

New York 7.3% (4.6% of Managed Assets) | |

New York Liberty Development Corp., World Trade Center, Revenue Bonds Class 3

7.25%, due 11/15/44 (c) | | | 13,390,000 | | | | 15,992,213 | |

New York Transportation Development Corp., LaGuardia Airport Terminal B Redevelopment Project, Revenue Bonds

Series A, Insured: AGM

4.00%, due 7/1/36 (b) | | | 20,000,000 | | | | 21,179,900 | |

Riverhead Industrial Development Agency, Revenue Bonds

7.00%, due 8/1/43 | | | 3,395,000 | | | | 3,759,453 | |

| | | | | | | | |

| | | | | | | 40,931,566 | |

| | | | | | | | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

North Dakota 0.9% (0.6% of Managed Assets) | |

North Dakota Housing Finance Agency, Revenue Bonds

Series A

3.75%, due 7/1/38 | | $ | 4,710,000 | | | $ | 4,961,137 | |

| | | | | | | | |

|

Ohio 2.9% (1.8% of Managed Assets) | |

Buckeye Tobacco Settlement Financing Authority, Asset-Backed, Senior Turbo, Revenue Bonds | | | | | | | | |

Series A-2

5.125%, due 6/1/24 | | | 2,440,000 | | | | 2,326,320 | |

Series A-2

5.75%, due 6/1/34 | | | 2,425,000 | | | | 2,318,955 | |

Series A-2

5.875%, due 6/1/30 | | | 12,200,000 | | | | 11,645,266 | |

| | | | | | | | |

| | | | | | | 16,290,541 | |

| | | | | | | | |

Pennsylvania 4.1% (2.6% of Managed Assets) | |

Commonwealth Financing Authority PA, Tobacco Master Settlement Payment, Revenue Bonds

Insured: AGM

4.00%, due 6/1/39 | | | 3,000,000 | | | | 3,271,620 | |

Commonwealth of Pennsylvania, Certificates of Participation

Series A

5.00%, due 7/1/37 | | | 730,000 | | | | 865,210 | |

Harrisburg, Unlimited General Obligation

Series F, Insured: AMBAC

(zero coupon), due 9/15/21 | | | 305,000 | | | | 276,873 | |

Pennsylvania Economic Development Financing Authority, Capitol Region Parking System, Revenue Bonds

Series B

6.00%, due 7/1/53 (b) | | | 14,260,000 | | | | 16,524,569 | |

Philadelphia Authority for Industrial Development, Nueva Esperanza, Inc., Revenue Bonds

8.20%, due 12/1/43 | | | 2,000,000 | | | | 2,210,460 | |

| | | | | | | | |

| | | | | | | 23,148,732 | |

| | | | | | | | |

Puerto Rico 28.2% (17.8% of Managed Assets) | |

Children’s Trust Fund Puerto Rico Tobacco Settlement, Revenue Bonds

5.50%, due 5/15/39 | | | 12,965,000 | | | | 13,101,392 | |

Commonwealth of Puerto Rico, Aqueduct & Sewer Authority, Revenue Bonds | | | | | | | | |

Series A, Insured: AGC

5.00%, due 7/1/25 | | | 310,000 | | | | 316,578 | |

Series A, Insured: AGC

5.125%, due 7/1/47 | | | 3,550,000 | | | | 3,619,296 | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | | | | 11 | |

Portfolio of InvestmentsMay 31, 2019 (continued)

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Municipal Bonds (continued) | |

Puerto Rico 28.2% (17.8% of Managed Assets) (continued) | |

Commonwealth of Puerto Rico, Aqueduct &

Sewer Authority, Revenue Bonds (continued) | | | | | |

Series A

6.00%, due 7/1/38 | | $ | 10,000,000 | | | $ | 10,025,000 | |

Series A

6.00%, due 7/1/44 | | | 2,630,000 | | | | 2,636,575 | |

Commonwealth of Puerto Rico, Public Improvement, Unlimited General Obligation (d) | | | | | | | | |

Insured: AGM

4.50%, due 7/1/23 | | | 280,000 | | | | 280,451 | |

Series A, Insured: AGM

5.00%, due 7/1/35 | | | 7,840,000 | | | | 8,176,336 | |

Insured: AGM

5.125%, due 7/1/30 | | | 1,365,000 | | | | 1,391,645 | |

Series A, Insured: AGC

5.25%, due 7/1/23 | | | 145,000 | | | | 147,604 | |

Series A-4, Insured: AGM

5.25%, due 7/1/30 | | | 4,425,000 | | | | 4,517,836 | |

Series A, Insured: AGM

5.375%, due 7/1/25 | | | 1,340,000 | | | | 1,407,670 | |

Series A, Insured: AMBAC

5.50%, due 7/1/19 | | | 55,000 | | | | 55,099 | |

Series A, Insured: AGC

5.50%, due 7/1/32 | | | 255,000 | | | | 261,074 | |

Series C, Insured: AGM

5.50%, due 7/1/32 | | | 1,520,000 | | | | 1,553,166 | |

Series C, Insured: AGM

5.75%, due 7/1/37 | | | 5,440,000 | | | | 5,570,723 | |

Series C-7, Insured: NATL-RE

6.00%, due 7/1/27 | | | 2,615,000 | | | | 2,671,353 | |

Series A, Insured: AGM

6.00%, due 7/1/33 | | | 875,000 | | | | 903,429 | |

Series A, Insured: AGM

6.00%, due 7/1/34 | | | 755,000 | | | | 805,721 | |

Puerto Rico Convention Center District Authority, Revenue Bonds (d) | | | | | | | | |

Series A, Insured: AGC

4.50%, due 7/1/36 | | | 13,080,000 | | | | 13,095,958 | |

Series A, Insured: AGC

5.00%, due 7/1/27 | | | 635,000 | | | | 646,957 | |

Series A, Insured: AMBAC

5.00%, due 7/1/31 | | | 340,000 | | | | 343,101 | |

Puerto Rico Electric Power Authority, Revenue Bonds (d) | | | | | | | | |

Series DDD, Insured: AGM

3.625%, due 7/1/23 | | | 755,000 | | | | 754,992 | |

Series DDD, Insured: AGM

3.65%, due 7/1/24 | | | 2,830,000 | | | | 2,829,915 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Puerto Rico 28.2% (17.8% of Managed Assets) (continued) | |

Puerto Rico Electric Power Authority, Revenue Bonds (d) (continued) | | | | | | | | |

Series SS, Insured: NATL-RE

5.00%, due 7/1/19 | | $ | 4,800,000 | | | $ | 4,806,144 | |

Series PP, Insured: NATL-RE

5.00%, due 7/1/24 | | | 1,130,000 | | | | 1,142,114 | |

Series PP, Insured: NATL-RE

5.00%, due 7/1/25 | | | 165,000 | | | | 166,704 | |

Series TT, Insured: AGM

5.00%, due 7/1/27 | | | 310,000 | | | | 315,837 | |

Puerto Rico Highway & Transportation Authority, Revenue Bonds (d) | | | | | | | | |

Series AA-1, Insured: AGM

4.95%, due 7/1/26 | | | 6,195,000 | | | | 6,284,208 | |

Series D, Insured: AGM

5.00%, due 7/1/32 | | | 960,000 | | | | 972,029 | |

Series N, Insured: AMBAC

5.25%, due 7/1/31 | | | 3,485,000 | | | | 3,820,013 | |

Series CC, Insured: AGM

5.25%, due 7/1/32 | | | 2,075,000 | | | | 2,284,264 | |

Series CC, Insured: AGM

5.25%, due 7/1/33 | | | 455,000 | | | | 500,828 | |

Series CC, Insured: AGM

5.25%, due 7/1/34 | | | 2,685,000 | | | | 2,952,560 | |

Series N, Insured: AGC

5.25%, due 7/1/34 | | | 2,090,000 | | | | 2,298,269 | |

Series CC, Insured: AGM

5.25%, due 7/1/36 | | | 1,530,000 | | | | 1,671,755 | |

Series N, Insured: AGC, AGM

5.50%, due 7/1/25 | | | 575,000 | | | | 632,316 | |

Series CC, Insured: AGM

5.50%, due 7/1/29 | | | 235,000 | | | | 263,221 | |

Series N, Insured: AMBAC

5.50%, due 7/1/29 | | | 1,025,000 | | | | 1,146,719 | |

Series CC, Insured: AGM

5.50%, due 7/1/30 | | | 3,185,000 | | | | 3,566,467 | |

Puerto Rico Infrastructure Financing Authority, Revenue Bonds (d) | | | | | | | | |

Series C, Insured: AMBAC

5.50%, due 7/1/23 | | | 1,500,000 | | | | 1,611,570 | |

Series C, Insured: AMBAC

5.50%, due 7/1/24 | | | 335,000 | | | | 363,900 | |

Series C, Insured: AMBAC

5.50%, due 7/1/25 | | | 1,830,000 | | | | 2,006,723 | |

Series C, Insured: AMBAC

5.50%, due 7/1/26 | | | 660,000 | | | | 729,280 | |

Puerto Rico Municipal Finance Agency, Revenue Bonds | | | | | | | | |

Series A, Insured: AGM

5.00%, due 8/1/20 | | | 670,000 | | | | 676,888 | |

| | | | |

| 12 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Municipal Bonds (continued) | |

Puerto Rico 28.2% (17.8% of Managed Assets) (continued) | |

Puerto Rico Municipal Finance Agency, Revenue Bonds (continued) | | | | | | | | |

Series A, Insured: AGM

5.00%, due 8/1/21 | | $ | 810,000 | | | $ | 821,453 | |

Series A, Insured: AGM

5.00%, due 8/1/22 | | | 835,000 | | | | 850,072 | |

Series A, Insured: AGM

5.00%, due 8/1/27 | | | 2,770,000 | | | | 2,822,159 | |

Series A, Insured: AGM

5.00%, due 8/1/30 | | | 1,685,000 | | | | 1,708,759 | |

Series A, Insured: AGM

5.25%, due 8/1/21 | | | 230,000 | | | | 233,225 | |

Series C, Insured: AGC

5.25%, due 8/1/21 | | | 3,775,000 | | | | 3,934,985 | |

Puerto Rico Public Buildings Authority, Government Facilities, Revenue Bonds (d) | | | | | | | | |

Series F, Insured: AGC

5.25%, due 7/1/21 | | | 2,090,000 | | | | 2,175,293 | |

Series M-3, Insured: NATL-RE

6.00%, due 7/1/25 | | | 385,000 | | | | 429,294 | |

Series M-3, Insured: NATL-RE

6.00%, due 7/1/27 | | | 10,000,000 | | | | 10,174,800 | |

Puerto Rico Sales Tax Financing Corp Sales Tax Revenue, COFINA Senior Bonds, 2042 National Custodial Trust, Revenue Bonds | | | | | | | | |

Series 2007-A, Insured: NATL-RE

(zero coupon), due 8/1/42 | | | 67,782 | | | | 55,835 | |

Series 2007-A, Insured: NATL-RE

(zero coupon), due 8/1/42 | | | 205,840 | | | | 180,625 | |

Puerto Rico Sales Tax Financing Corp., Revenue Bonds | | | | | | | | |

Series A-1

4.50%, due 7/1/34 | | | 8,695,000 | | | | 8,934,112 | |

Series A-1

5.00%, due 7/1/58 | | | 13,440,000 | | | | 13,393,632 | |

| | | | | | | | |

| | | | | | | 159,037,924 | |

| | | | | | | | |

Rhode Island 2.9% (1.8% of Managed Assets) | |

Narragansett Bay Commission Wastewater System, Revenue Bonds

Series A

5.00%, due 9/1/38 (b) | | | 15,000,000 | | | | 16,439,250 | |

| | | | | | | | |

|

South Carolina 3.7% (2.3% of Managed Assets) | |

Patriots Energy Group Financing Agency, Gas Supply, Revenue Bonds

Series A

4.00%, due 10/1/48 (b)(e) | | | 10,000,000 | | | | 10,914,991 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

South Carolina 3.7% (2.3% of Managed Assets) (continued) | |

South Carolina Public Service Authority, Revenue Bonds | | | | | | | | |

Series A

5.00%, due 12/1/31 | | $ | 825,000 | | | $ | 952,908 | |

Series B

5.00%, due 12/1/41 | | | 7,500,000 | | | | 8,700,150 | |

South Carolina Public Service Authority, Santee Cooper Project, Revenue Bonds

Series B

5.125%, due 12/1/43 | | | 250,000 | | | | 276,425 | |

| | | | | | | | |

| | | | | | | 20,844,474 | |

| | | | | | | | |

Tennessee 0.4% (0.2% of Managed Assets) | |

Tennessee Housing & Development Agency, Residential Finance Program, Revenue Bonds

4.25%, due 1/1/50 | | | 2,000,000 | | | | 2,184,260 | |

| | | | | | | | |

|

Texas 9.5% (6.0% of Managed Assets) | |

Harris County Cultural Education Facilities Finance Corp., Houston Methodist Hospital, Revenue Bonds

Subseries C-2

2.25%, due 12/1/27 (f) | | | 1,400,000 | | | | 1,400,000 | |

Harris County-Houston Sports Authority, Revenue Bonds | | | | | | | | |

Series H, Insured: NATL-RE

(zero coupon), due 11/15/28 | | | 50,000 | | | | 37,552 | |

Series A, Insured: AGM, NATL-RE

(zero coupon), due 11/15/38 | | | 175,000 | | | | 78,181 | |

Series H, Insured: NATL-RE

(zero coupon), due 11/15/38 | | | 260,000 | | | | 108,199 | |

Texas Municipal Gas Acquisition & Supply Corp. III, Revenue Bonds

5.00%, due 12/15/32 (b) | | | 20,000,000 | | | | 21,596,798 | |

Texas Water Development Board, Revenue Bonds

Series B

5.00%, due 4/15/49 (b) | | | 25,000,000 | | | | 30,042,625 | |

| | | | | | | | |

| | | | | | | 53,263,355 | |

| | | | | | | | |

U.S. Virgin Islands 4.8% (3.0% of Managed Assets) | |

Virgin Islands Public Finance Authority, Gross Receipts Taxes Loan, Revenue Bonds | | | | | | | | |

Series A

5.00%, due 10/1/32 | | | 3,020,000 | | | | 2,831,250 | |

Series A, Insured: AGM

5.00%, due 10/1/32 | | | 2,690,000 | | | | 2,924,837 | |

Virgin Islands Public Finance Authority, Matching Fund Loan, Revenue Bonds | | | | | | | | |

Senior Lien-Series B

5.00%, due 10/1/24 | | | 1,685,000 | | | | 1,699,744 | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | | | | 13 | |

Portfolio of InvestmentsMay 31, 2019 (continued)

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

| Municipal Bonds (continued) | |

U.S. Virgin Islands 4.8% (3.0% of Managed Assets) (continued) | |

Virgin Islands Public Finance Authority, Matching

Fund Loan, Revenue Bonds (continued) | | | | | |

Series A-1

5.00%, due 10/1/24 | | $ | 1,145,000 | | | $ | 1,155,019 | |

Series A

5.00%, due 10/1/25 | | | 1,000,000 | | | | 1,007,500 | |

Series B

5.25%, due 10/1/29 | | | 1,180,000 | | | | 1,185,900 | |

Series A

6.625%, due 10/1/29 | | | 2,580,000 | | | | 2,576,775 | |

Virgin Islands Public Finance Authority, Revenue Bonds | | | | | | | | |

Series A

5.00%, due 10/1/29 | | | 2,980,000 | | | | 2,838,450 | |

Series A, Insured: AGM

5.00%, due 10/1/32 | | | 5,350,000 | | | | 5,817,055 | |

Virgin Islands Public Finance Authority, Senior Lien-Matching Fund Loan Note, Revenue Bonds | | | | | | | | |

Series A-1

4.50%, due 10/1/24 | | | 445,000 | | | | 439,994 | |

Senior Lien-Series B

5.00%, due 10/1/25 | | | 4,385,000 | | | | 4,417,887 | |

| | | | | | | | |

| | | | | | | 26,894,411 | |

| | | | | | | | |

Utah 2.5% (1.6% of Managed Assets) | |

Utah Housing Corp., Revenue Bonds | | | | | | | | |

Series A, Insured: GNMA

4.50%, due 1/21/49 | | | 6,962,160 | | | | 7,387,061 | |

Series C, Insured: GNMA

4.50%, due 3/21/49 | | | 6,477,342 | | | | 6,872,654 | |

| | | | | | | | |

| | | | | | | 14,259,715 | |

| | | | | | | | |

Virginia 4.9% (3.1% of Managed Assets) | |

Tobacco Settlement Financing Corp., Revenue Bonds

Series B1

5.00%, due 6/1/47 | | | 5,000,000 | | | | 4,941,850 | |

Virginia Commonwealth Transportation Board, Capital Projects, Revenue Bonds

5.00%, due 5/15/31 (b) | | | 20,315,000 | | | | 22,386,214 | |

| | | | | | | | |

| | | | | | | 27,328,064 | |

| | | | | | | | |

Washington 4.2% (2.7% of Managed Assets) | |

Washington Health Care Facilities Authority, Multicare Health System, Revenue Bonds

Series A

5.00%, due 8/15/44 (b) | | | 19,665,000 | | | | 21,148,265 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | | | | | | | |

Washington 4.2% (2.7% of Managed Assets) (continued) | |

Washington State Housing Finance Commission, Single Family Program, Revenue Bonds

Series 1N

4.00%, due 6/1/49 | | $ | 2,500,000 | | | $ | 2,702,400 | |

| | | | | | | | |

| | | | | | | 23,850,665 | |

| | | | | | | | |

Wisconsin 0.1% (0.1% of Managed Assets) | |

Public Finance Authority, Bancroft NeuroHealth Project, Revenue Bonds

Series A

5.00%, due 6/1/36 (c) | | | 500,000 | | | | 517,885 | |

| | | | | | | | |

|

Wyoming 0.5% (0.3% of Managed Assets) | |

Wyoming Community Development Authority, Revenue Bonds

Series 1

4.00%, due 12/1/48 | | | 2,500,000 | | | | 2,693,525 | |

| | | | | | | | |

Total Investments

(Cost $820,034,793) | | | 156.0 | % | | | 878,646,478 | |

Floating Rate Note Obligations (g) | | | (45.9 | ) | | | (258,475,000 | ) |

Fixed Rate Municipal Term Preferred Shares, at Liquidation Value | | | (12.4 | ) | | | (70,000,000 | ) |

Other Assets, Less Liabilities | | | 2.3 | | | | 12,927,013 | |

Net Assets Applicable to Common Shares | | | 100.0 | % | | $ | 563,098,491 | |

| † | Percentages indicated are based on Fund net assets applicable to Common Shares. |

| (a) | Interest on these securities was subject to alternative minimum tax. |

| (b) | All or portion of principal amount transferred to a Tender Option Bond ("TOB") Issuer in exchange for TOB Residuals and cash. |

| (c) | May be sold to institutional investors only under Rule 144A or securities offered pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended. |

| (d) | Bond insurance is paying principal and interest, since the issuer is in default. |

| (e) | Floating Rate—Rate shown was the rate in effect as of May 31, 2019. |

| (f) | Variable-rate demand notes (VRDNs)—Provide the right to sell the security at face value on either that day or within the rate-reset period. VRDNs will normally trade as if the maturity is the earlier put date, even though stated maturity is longer. The interest rate is reset on the put date at a stipulated daily, weekly, monthly, quarterly, or other specified time interval to reflect current market conditions. These securities do not indicate a reference rate and spread in their description. The maturity date shown is the final maturity. |

| (g) | Face value of Floating Rate Notes issued in TOB transactions. |

| | | | |

| 14 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

“Managed Assets” is defined as the Fund’s total assets, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of creating effective leverage (i.e. tender option bonds) or Fund liabilities related to liquidation preference of any preferred shares issued), which was $894,227,908 as of May 31, 2019.

The following abbreviations are used in the preceding pages:

ACA—ACA Financial Guaranty Corp.

AGC—Assured Guaranty Corp.

AGM—Assured Guaranty Municipal Corp.

AMBAC—Ambac Assurance Corp.

BAM—Build America Mutual Assurance Co.

GNMA—Government National Mortgage Association

NATL-RE—National Public Finance Guarantee Corp.

Futures Contracts

As of May 31, 2019, the Fund held the following futures contracts1:

| | | | | | | | | | | | | | | | | | | | |

Type | | Number of

Contracts | | | Expiration

Date | | | Value at

Trade Date | | | Current

Notional

Amount | | | Unrealized

Appreciation

(Depreciation)2 | |

| Short Contracts | | | | | | | | | | | | | | | | | | | | |

| 10-Year United States Treasury Note | | | (883 | ) | | | September 2019 | | | $ | (110,880,490 | ) | | $ | (111,920,250 | ) | | $ | (1,039,760 | ) |

| | | | | | | | | | | | | | | | | | | | |

| 1. | As of May 31, 2019, cash in the amount of $927,150 was on deposit with a broker or futures commission merchant for futures transactions. |

| 2. | Represents the difference between the value of the contracts at the time they were opened and the value as of May 31, 2019. |

The following is a summary of the fair valuations according to the inputs used as of May 31, 2019, for valuing the Fund’s assets and liabilities:

| | | | | | | | | | | | | | | | |

Description | | Quoted

Prices in

Active

Markets for

Identical

Assets

(Level 1) | | | Significant

Other

Observable

Inputs

(Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | | | Total | |

| | | | |

Asset Valuation Inputs | | | | | | | | | | | | | | | | |

| Investments in Securities (a) | | | | | | | | | | | | | | | | |

Municipal Bonds | | $ | — | | | $ | 878,646,478 | | | $ | — | | | $ | 878,646,478 | |

| | | | | | | | | | | | | | | | |

| | | | |

Liability Valuation Inputs | | | | | | | | | | | | | | | | |

| Other Financial Instruments | | | | | | | | | | | | | | | | |

Futures Contracts (b) | | $ | (1,039,760 | ) | | $ | — | | | $ | — | | | $ | (1,039,760 | ) |

| | | | | | | | | | | | | | | | |

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

| (b) | The value listed for these securities reflects unrealized appreciation (depreciation) as shown on the Portfolio of Investments. |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | | | | 15 | |

Statement of Assets and Liabilitiesas of May 31, 2019

| | | | |

| Assets | |

Investment in securities, at value

(identified cost $820,034,793) | | $ | 878,646,478 | |

Cash | | | 2,667,300 | |

Cash collateral on deposit at broker for futures contracts | | | 927,150 | |

Receivables: | | | | |

Interest | | | 13,212,432 | |

Common shares sold | | | 174,465 | |

Other assets | | | 31,735 | |

| | | | |

Total assets | | | 895,659,560 | |

| | | | |

| |

| Liabilities | | | | |

Payable for Floating Rate Note Obligations | | | 258,475,000 | |

Fixed Rate Municipal Term Preferred Shares, at liquidation value, Series A (a) | | | 35,000,000 | |

Fixed Rate Municipal Term Preferred Shares, at liquidation value, Series B (a) | | | 35,000,000 | |

Payables: | | | | |

Variation margin on futures contracts | | | 648,451 | |

Manager (See Note 3) | | | 456,252 | |

Professional fees | | | 104,286 | |

Shareholder communication | | | 24,636 | |

Custodian | | | 9,792 | |

Transfer agent | | | 6,230 | |

Interest expense and fees payable | | | 2,654,418 | |

Common share dividend payable | | | 174,476 | |

Accrued expenses | | | 7,528 | |

| | | | |

Total liabilities | | | 332,561,069 | |

| | | | |

Net assets applicable to Common shares | | $ | 563,098,491 | |

| | | | |

Common shares outstanding | | | 27,593,538 | |

| | | | |

Net asset value per Common share (Net assets applicable to Common shares divided by Common shares outstanding) | | $ | 20.41 | |

| | | | |

|

| Net assets applicable to Common Shares consist of | |

Common shares, $0.001 par value per share, unlimited number of shares authorized | | $ | 27,594 | |

Additional paid-in capital | | | 525,176,155 | |

| | | | |

| | | 525,203,749 | |

Total distributable earnings (loss) (b) | | | 37,894,742 | |

| | | | |

Net assets applicable to Common shares | | $ | 563,098,491 | |

| | | | |

| (a) | 350 authorized shares, $0.01 par value, liquidation preference of $100,000 per share (See Note 2). |

| | | | |

| 16 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Statement of Operationsfor the year ended May 31, 2019

| | | | |

| Investment Income (Loss) | |

Income | | | | |

Interest | | $ | 41,451,524 | |

| | | | |

Expenses | | | | |

Interest expense and fees | | | 8,016,553 | |

Manager (See Note 3) | | | 5,249,934 | |

Professional fees | | | 150,849 | |

Shareholder communication | | | 49,815 | |

Transfer agent | | | 41,641 | |

Custodian | | | 23,466 | |

Trustees | | | 13,005 | |

Miscellaneous | | | 128,829 | |

| | | | |

Total expenses | | | 13,674,092 | |

| | | | |

Net investment income (loss) | | | 27,777,432 | |

| | | | |

|

| Realized and Unrealized Gain (Loss) on Investments and Futures Contracts | |

Net realized gain (loss) on: | | | | |

Investment transactions | | | 1,768,483 | |

Futures transactions | | | (5,173,876 | ) |

| | | | |

Net realized gain (loss) on investments and futures transactions | | | (3,405,393 | ) |

| | | | |

Net change in unrealized appreciation (depreciation) on: | | | | |

Investments | | | 11,755,062 | |

Futures contracts | | | 259,166 | |

| | | | |

Net change in unrealized appreciation (depreciation) on investments and futures contracts | | | 12,014,228 | |

| | | | |

Net realized and unrealized gain (loss) on investments and futures transactions | | | 8,608,835 | |

| | | | |

Net increase (decrease) in net assets to Common shares resulting from operations | | $ | 36,386,267 | |

| | | | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | | | | 17 | |

Statements of Changes in Net Assets

for the years ended May 31, 2019 and May 31, 2018

| | | | | | | | |

| | | 2019 | | | 2018 | |

| Net Increase (Decrease) in Net Assets Applicable to Common Shares | |

Operations: | | | | | | | | |

Net investment income (loss) | | $ | 27,777,432 | | | $ | 28,823,580 | |

Net realized gain (loss) on investments and futures contracts | | | (3,405,393 | ) | | | 6,769,582 | |

Net change in unrealized appreciation (depreciation) on investments and futures contracts | | | 12,014,228 | | | | (6,718,596 | ) |

| | | | |

Net increase (decrease) in net assets applicable to Common shares resulting from operations | | | 36,386,267 | | | | 28,874,566 | |

| | | | |

Distributions to Common shareholders(1) | | | (28,254,807 | ) | | | | |

| | | | | | | | |

Dividends to Common shareholders from net investment income | | | | | | | (29,765,721 | ) |

| | | | | | | | |

Capital share transactions (Common shares): | | | | | | | | |

Net proceeds issued to shareholders resulting from reinvestment of dividends | | | 635,272 | | | | 151,997 | |

| | | | |

Increase (decrease) in net assets applicable to Common shares from capital share transactions | | | 635,272 | | | | 151,997 | |

| | | | |

Net increase (decrease) in net assets applicable to Common shares | | | 8,766,732 | | | | (739,158 | ) |

|

| Net Assets Applicable to Common Shares | |

Beginning of year | | | 554,331,759 | | | | 555,070,917 | |

| | | | |

End of year(2) | | $ | 563,098,491 | | | $ | 554,331,759 | |

| | | | |

| (1) | For the year ended May 31, 2019, the requirement to disclose dividends and distributions paid to Common shareholders from net investment income and/or net realized gain on investments was modified and are now presented together as distributions to Common shareholders (See Note 8). |

| (2) | End of year net assets includes undistributed (overdistributed) net investment income of $1,099,799 in 2018. The requirement to disclose the corresponding amount as of May 31, 2019 was eliminated (See Note 8). See Note 4 for tax basis of distributable earnings. |

| | | | |

| 18 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Statement of Cash Flows

for the year ended May 31, 2019

| | | | |

| Cash flows from operating activities: | |

Net increase in net assets resulting from operations | | $ | 36,386,267 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash from operating activities: | | | | |

Investments purchased | | | (243,414,258 | ) |

Investments sold | | | 231,690,003 | |

Amortization (accretion) of discount and premium, net | | | (131,279 | ) |

Increase in dividends and interest receivable | | | (371,977 | ) |

Decrease in other assets | | | 807 | |

Decrease in investment securities purchased payable | | | (4,710,000 | ) |

Increase in professional fees payable | | | 18,571 | |

Increase in custodian payable | | | 8,272 | |

Increase in shareholder communication payable | | | 696 | |

Increase in due to manager | | | 18,640 | |

Decrease in due to transfer agent | | | (4,040 | ) |

Increase in variation margin on futures contracts | | | 404,942 | |

Increase in accrued expenses | | | 5,759 | |

Increase in interest expense and fees payable | | | 453,038 | |

Net realized gain from investments | | | (1,768,483 | ) |

Net change in unrealized (appreciation) depreciation on investments | | | (11,755,062 | ) |

| | | | |

Net cash from operating activities | | | 6,831,896 | |

| | | | |

| |

| Cash flows used in financing activities: | | | | |

Net proceeds resulting from reinvestment of dividends | | | 460,807 | |

Proceeds from floating rate note obligations | | | 42,965,000 | |

Payments on floating rate note obligations | | | (20,830,000 | ) |

Cash distributions paid, net of change in Common share dividend payable | | | (28,244,624 | ) |

| | | | |

Net cash used in financing activities | | | (5,648,817 | ) |

| | | | |

Net increase in cash and restricted cash | | | 1,183,079 | |

Cash and restricted cash at beginning of year | | | 2,411,371 | |

| | | | |

Cash and restricted cash at end of year | | $ | 3,594,450 | |

| | | | |

|

| Supplemental disclosure of cash flow information: | |

Cash payments recognized as interest expense on the Fund’s Fixed Rate Municipal Term Preferred Shares for the year ended May 31, 2019, were $1,922,255.

The following tables provide a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sums to the total of the such amounts shown on the Statement of Cash Flows:

| | | | |

Cash and restricted cash at beginning of year

Cash | | $ | 1,399,371 | |

Cash collateral on deposit at broker for futures contracts | | | 1,012,000 | |

| | | | |

Total cash and restricted cash shown in the Statement of Cash Flows | | $ | 2,411,371 | |

| | | | |

| |

Cash and restricted cash at end of year

Cash | | $ | 2,667,300 | |

Cash collateral on deposit at broker for futures contracts | | | 927,150 | |

| | | | |

Total cash and restricted cash shown in the Statement of Cash Flows | | $ | 3,594,450 | |

| | | | |

Restricted cash consists of cash that has been segregated to cover the Fund’s collateral or margin obligations under derivative contracts. It is separately reported on the Statement of Assets and Liabilities as cash collateral on deposit at broker.

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | | | | 19 | |

Financial Highlightsselected per share data and ratios

| | | | | | | | | | | | | | | | | | | | |

| |

| | | Year ended May 31, | |

| | | | | |

| | | 2019 | | | 2018 | | | 2017 | | | 2016 | | | 2015 | |

| | | | | |

Net asset value at beginning of year applicable to Common shares | | $ | 20.11 | | | $ | 20.14 | | | $ | 20.61 | | | $ | 19.03 | | | $ | 18.76 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net investment income (loss) | | | 1.01 | | | | 1.05 | | | | 1.08 | | | | 1.11 | | | | 1.19 | |

| | | | | |

Net realized and unrealized gain (loss) on investments | | | 0.32 | | | | 0.00 | ‡ | | | (0.46 | ) | | | 1.65 | | | | 0.25 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total from investment operations | | | 1.33 | | | | 1.05 | | | | 0.62 | | | | 2.76 | | | | 1.44 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Dividends and distributions to Common shareholders | | | (1.03 | ) | | | (1.08 | ) | | | (1.09 | ) | | | (1.18 | ) | | | (1.17 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net asset value at end of year applicable to Common shares | | $ | 20.41 | | | $ | 20.11 | | | $ | 20.14 | | | $ | 20.61 | | | $ | 19.03 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Market price at end of year applicable to Common shares | | $ | 20.65 | | | $ | 19.41 | | | $ | 19.94 | | | $ | 19.66 | | | $ | 18.43 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Total investment return on net asset value (a) | | | 6.80 | % | | | 5.31 | % | | | 3.21 | % | | | 15.02 | % | | | 7.78 | % |

| | | | | |

Total investment return on market price (a) | | | 12.05 | % | | | 2.88 | % | | | 7.22 | % | | | 13.66 | % | | | 9.60 | % |

| | | | | |

| Ratios (to average net assets of Common shareholders)/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Net investment income (loss) | | | 5.03 | % | | | 5.21 | % | | | 5.35 | % | | | 5.73 | % | | | 6.17 | % |

| | | | | |

Net expenses (including interest expense and fees) | | | 2.47 | % | | | 2.11 | % | | | 1.83 | % | | | 1.58 | % | | | 1.56 | % |

| | | | | |

Interest expense and fees (b) | | | 1.45 | % | | | 1.10 | % | | | 0.85 | % | | | 0.59 | % | | | 0.57 | % |

| | | | | |

Portfolio turnover rate | | | 27 | % | | | 20 | % | | | 26 | % | | | 30 | % | | | 27 | % |

| | | | | |

Net assets applicable to Common shareholders end of year (in 000’s) | | $ | 563,098 | | | $ | 554,332 | | | $ | 555,071 | | | $ | 567,973 | | | $ | 524,395 | |

| | | | | |

Preferred shares outstanding at $100,000 liquidation preference, end of year (in 000’s) | | $ | 70,000 | | | $ | 70,000 | | | $ | 70,000 | | | $ | 70,000 | | | $ | 70,000 | |

| | | | | |

Assets coverage per Preferred share, end of year (c) | | $ | 904,426 | | | $ | 891,903 | | | $ | 892,958 | | | $ | 911,390 | | | $ | 849,136 | |

| | | | | |

| Average market value per Preferred share: | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Series A | | $ | 100,000 | | | $ | 100,006 | | | $ | 100,012 | | | $ | 100,015 | | | $ | 100,010 | |

| | | | | |

Series B | | $ | 100,000 | | | $ | 100,000 | | | $ | 100,000 | | | $ | 100,087 | | | $ | 100,012 | |

| ‡ | Less than one cent per share. |

| (a) | Total investment return on net asset value reflects the changes in net asset value during each period and assumes the reinvestment of dividends and distributions at net asset value on the last business day of each month. This percentage may be different from the total investment return on market value, due to differences between the market price and the net asset value. Actual reinvestment price may be based on market price or net asset value and therefore, differ from the price used in the calculation. For periods less than one year, total investment return is not annualized. |

| (b) | Interest expense and fees relate to the costs of tender option bond transactions (See Note 2 (H)) and the issuance of fixed rate municipal term preferred shares (See Note 2 (I)). |

| (c) | Calculated by subtracting the Fund’s total liabilities (not including the Preferred shares) from the Fund’s total assets, and dividing the result by the number of Preferred shares outstanding. |

| | | | |

| 20 | | MainStay MacKay DefinedTerm Municipal Opportunities Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Notes to Financial Statements

Note 1–Organization and Business

MainStay MacKay DefinedTerm Municipal Opportunities Fund (the “Fund”) was organized as a Delaware statutory trust on April 20, 2011, pursuant to an agreement and declaration of trust, which was amended and restated on June 4, 2015 (“Declaration of Trust”). The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a “diversified”, closed-end management investment company, as those terms are defined in the 1940 Act, as interpreted or modified by regulatory authorities having jurisdiction, from time to time. The Fund first offered Common shares through an initial public offering on June 26, 2012.

Pursuant to the terms of the Declaration of Trust, the Fund will commence the process of liquidation and dissolution at the close of business on December 31, 2024 (the “Termination Date”) unless otherwise extended by a majority of the Board of Trustees (the “Board”) (as discussed in further detail below). During the six-month period preceding the Termination Date or Extended Termination Date (as defined below), the Board may, without shareholder approval unless such approval is required by the 1940 Act, determine to (i) merge or consolidate the Fund so long as the surviving or resulting entity is an open-end registered investment company that is managed by the same investment adviser which serves as the investment adviser to the Fund at that time or is an affiliate of such investment adviser; or (ii) convert the Fund from a closed-end fund into an open-end registered investment company. Upon liquidation and termination of the Fund, shareholders will receive an amount equal to the Fund’s net asset value (“NAV”) at that time, which may be greater or less than the price at which Common shares were issued. The Fund’s investment objectives and policies are not designed to return to investors who purchased Common shares in the initial offering of such shares their initial investment on the Termination Date and such initial investors may receive more or less than their original investment upon termination.

Prior to the commencement of the six-month period preceding the Termination Date, a majority of the Board may extend the Termination Date for a period of not more than two years or such shorter time as may be determined (the “Extended Termination Date”), upon a determination that taking such actions as described in (i) or (ii) above would not, given prevailing market conditions, be in the best interests of the Fund’s shareholders. The Termination Date may be extended an unlimited number of times by the Board prior to the first business day of the sixth month before the next occurring Extended Termination Date.

The Fund’s primary investment objective is to seek current income exempt from regular U.S. Federal income taxes (but which may be includable in taxable income for purpose of the Federal alternative minimum tax). Total return is a secondary objective.

Note 2–Significant Accounting Policies

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard CodificationTopic 946 Financial Services—Investment Companies. The Fund prepares its financial statements in accordance with generally accepted

accounting principles (“GAAP”) in the United States of America and follows the significant accounting policies described below.

(A) Securities Valuation. Investments are usually valued as of the close of regular trading on the New York Stock Exchange (the “Exchange”) (usually 4:00 p.m. Eastern time) on each day the Fund is open for business (“valuation date”).

The Board adopted procedures establishing methodologies for the valuation of the Fund’s securities and other assets and delegated the responsibility for valuation determinations under those procedures to the Valuation Committee of the Fund (the “Valuation Committee”). The Board authorized the Valuation Committee to appoint a Valuation Subcommittee (the “Subcommittee”) to deal in the first instance with establishing the prices of securities for which market quotations are not readily available or the prices of which are not otherwise readily determinable under these procedures. The Subcommittee meets (in person, via electronic mail or via teleconference) on an as-needed basis. Subsequently, the Valuation Committee meets to ensure that actions taken by the Subcommittee were appropriate. The procedures state that, subject to the oversight of the Board and unless otherwise noted, the responsibility for theday-to-day valuation of portfolio assets (including fair value measurements for the Fund’s assets and liabilities) rests with New York Life Investment Management LLC (“New York Life Investments” or the “Manager”), aided to whatever extent necessary by the Subadvisor (as defined in Note 3(A)).

To assess the appropriateness of security valuations, the Manager, the Subadvisor or the Fund’s third-party service provider, who is subject to oversight by the Manager, regularly compares prior day prices, prices on comparable securities, and the sale prices to the prior and current day prices and challenges prices with changes exceeding certain tolerance levels with third party pricing services or broker sources. For those securities valued through either a standardized fair valuation methodology or a fair valuation measurement, the Subcommittee deals in the first instance with such valuation and the Valuation Committee reviews and affirms, if appropriate, the reasonableness of the valuation based on such methodologies and measurements on a regular basis after considering information that is reasonably available and deemed relevant by the Valuation Committee. Any action taken by the Subcommittee with respect to the valuation of a portfolio security or other asset is submitted for review and ratification (if appropriate) to the Valuation Committee and the Board at the next regularly scheduled meeting.

“Fair value” is defined as the price the Fund would reasonably expect to receive upon selling an asset or liability in an orderly transaction to an independent buyer in the principal or most advantageous market for the asset or liability. Fair value measurements are determined within a framework that establishes a three-tier hierarchy which maximizes the use of observable market data and minimizes the use of unobservable inputs to establish a classification of fair value measurements for disclosure purposes. “Inputs” refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, such as the risk inherent in a particular valuation technique used to measure fair value using a pricing model and/or the risk inherent in the inputs for the valuation technique. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund.

Notes to Financial Statements(continued)

Unobservable inputs reflect the Fund’s own assumptions about the assumptions market participants would use in pricing the asset or liability based on the information available. The inputs or methodology used for valuing assets or liabilities may not be an indication of the risks associated with investing in those assets or liabilities. The three-tier hierarchy of inputs is summarized below.

| • | | Level 1—quoted prices in active markets for an identical asset or liability |

| • | | Level 2—other significant observable inputs (including quoted prices for a similar asset or liability in active markets, interest rates and yield curves, prepayment speeds, credit risk, etc.) |

| • | | Level 3—significant unobservable inputs (including the Fund’s own assumptions about the assumptions that market participants would use in measuring fair value of an asset or liability) |

The level of an asset or liability within the fair value hierarchy is based on the lowest level of an input, both individually and in the aggregate, that is significant to the fair value measurement. As of May 31, 2019, the aggregate value by input level of the Fund’s assets and liabilities is included at the end of the Fund’s Portfolio of Investments.

The Fund may use third-party vendor evaluations, whose prices may be derived from one or more of the following standard inputs, among others:

| | |

• Benchmark yields | | • Reported trades |

• Broker/dealer quotes | | • Issuer spreads |

• Two-sided markets | | • Benchmark securities |

• Bids/offers | | • Reference data (corporate actions or material event notices) |

• Industry and economic events | | • Comparable bonds |

• Monthly payment information | | |