UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22551

NYLI MACKAY DEFINEDTERM

MUNICIPAL OPPORTUNITIES FUND

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: May 31

Date of reporting period: November 30, 2024

FORM N-CSR

| Item 1. | Reports to Stockholders. |

NYLI MacKay DefinedTerm Muni Opportunities Fund

(formerly known as MainStay MacKay DefinedTerm Municipal Opportunities Fund)

Semiannual Report

Unaudited | November 30, 2024 | NYSE Symbol MMD

Sign up for e-delivery of your shareholder reports. For full details on e-delivery, including who can participate and what you can receive via e-delivery,

please log in to www.computershare.com/investor.

| Not FDIC/NCUA Insured | Not a Deposit | May Lose Value | No Bank Guarantee | Not Insured by Any Government Agency |

This page intentionally left blank

Certain material in this report may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates and information about possible or future results or events related to the Fund, market or regulatory developments. The views expressed herein are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed herein are subject to change at any time based upon economic, market, or other conditions and the Fund undertakes no obligation to update the views expressed herein.

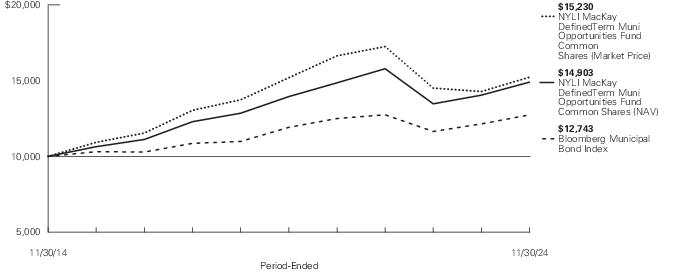

Fund Performance and Statistics (Unaudited)

Performance data quoted represents past performance of Common shares of the Fund. Past performance is no guarantee of future results. Because of market volatility and other factors, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate. For performance information current to the most recent month-end, please visit newyorklifeinvestments.com/mmd.

The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or the sale of Fund shares.

| Average Annual Total Returns for the Period-Ended November 30, 2024* |

| | Six

Months1 | One

Year | Five

Years | Ten

Years |

| Net Asset Value (“NAV”)2 | 4.47% | 6.13% | 1.33% | 4.07% |

| Market Price2 | 1.56 | 6.65 | 0.13 | 4.34 |

| Bloomberg Municipal Bond Index3 | 4.54 | 4.93 | 1.35 | 2.45 |

| Morningstar Muni National Long Category Average4 | 6.30 | 8.44 | 0.70 | 2.85 |

| * | Returns for indices reflect no deductions for fees, expenses or taxes, except for foreign withholding taxes where applicable. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 1. | Not annualized. |

| 2. | Total returns assume dividends and capital gains distributions are reinvested. |

| 3. | The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 4. | The Morningstar Muni National Long Category Average is representative of funds that invest in bonds issued by various state and local governments to fund public projects. The income from these bonds is generally free from federal taxes. These funds have durations of more than 7 years. Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

| 4 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

Fund Statistics as of November 30, 2024 (Unaudited)

| NYSE Symbol | MMD | Premium/Discount 1 | (5.57)% |

| CUSIP | 56064K100 | Total Net Assets (millions) | $320.1 |

| Inception Date | 6/26/2012 | Total Managed Assets (millions)2 | $475.5 |

| Market Price | $16.10 | Leverage 3 | 32.32% |

| NAV | $17.05 | Percent of AMT Bonds4 | 16.51% |

| 1. | Premium/Discount is the percentage (%) difference between the market price and the NAV. When the market price exceeds the NAV, the Fund is trading at a premium. When the market price is less than the NAV, the Fund is trading at a discount. |

| 2. | “Managed Assets” is defined as the Fund’s total assets, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of creating effective leverage (i.e. tender option bonds) or Fund liabilities related to liquidation preference of any Preferred shares issued). |

| 3. | Leverage is based on the use of proceeds received from tender option bond transactions, issuance of Preferred shares, funds borrowed from banks or other institutions or derivative transactions, expressed as a percentage of Managed Assets. |

| 4. | Alternative Minimum Tax (“AMT”) is a separate tax computation under the Internal Revenue Code that, in effect, eliminates many deductions and credits and creates a tax liability for an individual who would otherwise pay little or no tax, expressed as a percentage of Managed Assets. |

Portfolio Composition as of November 30, 2024† (Unaudited)

| Illinois | 14.8% |

| New York | 11.2 |

| California | 11.0 |

| Puerto Rico1 | 9.3 |

| Pennsylvania | 4.6 |

| Texas | 4.0 |

| Florida | 3.6 |

| Alabama | 3.4 |

| U.S. Virgin Islands | 3.4 |

| Massachusetts | 3.3 |

| Nevada | 3.3 |

| Connecticut | 3.2 |

| New Jersey | 2.9 |

| Michigan | 2.8 |

| Nebraska | 2.3 |

| Virginia | 2.3% |

| Missouri | 2.1 |

| South Carolina | 2.0 |

| Washington | 1.5 |

| Georgia | 1.4 |

| Kentucky | 1.3 |

| Wisconsin | 1.2 |

| West Virginia | 1.0 |

| Colorado | 1.0 |

| District of Columbia | 0.5 |

| Arizona | 0.3 |

| Other Assets, Less Liabilities | 2.3 |

| | 100.0% |

| † | As a percentage of Managed Assets. |

| 1. | As of November 30, 2024, 28.6% of the Puerto Rico municipal securities held by the Fund were insured and all bonds continue to pay full principal and interest. |

See Portfolio of Investments beginning on page 7 for specific holdings within these categories. The Fund's holdings are subject to change.

Top Ten Holdings and/or Issuers Held as of November 30, 2024 (excluding short-term investments)# (Unaudited)

| 1. | Puerto Rico Sales Tax Financing Corp., 4.55%-5.00%, due 7/1/40–7/1/58 |

| 2. | Chicago Board of Education, 5.75%-7.00%, due 4/1/34–12/1/46 |

| 3. | Black Belt Energy Gas District (The), 5.00%, due 3/1/55 |

| 4. | Los Angeles Department of Water And Power, 5.00%, due 7/1/48 |

| 5. | Connecticut State Health & Educational Facilities Authority, 2.80%, due 7/1/42 |

| 6. | City of Chicago, 5.50%-6.00%, due 1/1/38–1/1/49 |

| 7. | Pennsylvania Economic Development Financing Authority, 5.75%, due 12/31/62 (a) |

| 8. | San Francisco City & County Airport Commission, 5.00%, due 5/1/33–5/1/46 |

| 9. | Las Vegas Valley Water District, 5.00%, due 6/1/53 |

| 10. | New York Transportation Development Corp., 4.00%, due 7/1/36 (a) |

| # | Some of these holdings have been transferred to a Tender Option Bond (“TOB”) Issuer in exchange for TOB Residuals and cash. |

| (a) | Municipal security may feature credit enhancements, such as bond insurance. |

Credit Quality as of November 30, 2024^ (Unaudited)

^ As a percentage of total investments.

Ratings apply to the underlying portfolio of bonds held by the Fund and are rated by an independent rating agency, such as Standard & Poor’s (“S&P”), Moody’s Investors Service, Inc. and/or Fitch Ratings, Inc. If the ratings provided by the ratings agencies differ, the higher rating will be utilized. If only one rating is provided, the available rating will be utilized. Securities that are unrated by the rating agencies are reflected as such in the breakdown. Unrated securities do not necessarily indicate low quality. S&P rates borrowers on a scale from AAA to D. AAA through BBB- represent investment grade, while BB+ through D represent non-investment grade.

| 6 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

Portfolio of Investments November 30, 2024† (Unaudited)

| | Principal

Amount | Value |

| Municipal Bonds 145.1% |

| Alabama 5.1% (3.4% of Managed Assets) |

| Black Belt Energy Gas District (The), Gas Project, Revenue Bonds | | |

| Series D | | |

| 5.00%, due 3/1/55 (a)(b) | $ 15,000,000 | $ 16,311,596 |

| Arizona 0.5% (0.3% of Managed Assets) |

| City of Phoenix, Espiritu Community Development Corp., Revenue Bonds | | |

| Series A | | |

| 6.25%, due 7/1/36 | 1,555,000 | 1,548,574 |

| California 16.3% (11.0% of Managed Assets) |

| Calexico Unified School District, Unlimited General Obligation | | |

| Insured: BAM | | |

| 3.00%, due 8/1/52 | 3,600,000 | 2,914,327 |

| Los Angeles Department of Water And Power, Water System, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 7/1/48 (b) | 15,000,000 | 15,679,459 |

| Regents of the University of California, Medical Center Pooled, Revenue Bonds | | |

| Series P | | |

| 5.00%, due 5/15/47 | 1,220,000 | 1,345,202 |

| San Diego County, Regional Airport Authority, Revenue Bonds | | |

| Series B | | |

| 5.00%, due 7/1/46 (c) | 3,250,000 | 3,410,294 |

| San Diego County Regional Airport Authority, Airport, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 7/1/56 (b) | 5,500,000 | 5,891,518 |

| San Francisco City & County Airport Commission, San Francisco International Airport, Revenue Bonds | | |

| Series B | | |

| 5.00%, due 5/1/46 (b)(c) | 9,500,000 | 9,585,271 |

| San Francisco City & County Airport Commission, San Francisco International Airport, Revenue Bonds, Second Series | | |

| Series C | | |

| 5.00%, due 5/1/33 (c) | 3,000,000 | 3,327,808 |

| | Principal

Amount | Value |

| California |

| Trustees of The California State University, Systemwide, Revenue Bonds | | |

| Series A | | |

| 5.25%, due 11/1/53 (b) | $ 8,780,000 | $ 9,941,572 |

| | | 52,095,451 |

| Colorado 1.5% (1.0% of Managed Assets) |

| Copper Ridge Metropolitan District, Revenue Bonds | | |

| 5.00%, due 12/1/39 | 3,950,000 | 3,884,523 |

| Sterling Ranch Community Authority Board, Metropolitan District No. 2, Revenue Bonds | | |

| Series A | | |

| 4.25%, due 12/1/50 | 1,000,000 | 943,926 |

| | | 4,828,449 |

| Connecticut 4.7% (3.2% of Managed Assets) |

| Connecticut State Health & Educational Facilities Authority, Yale University, Revenue Bonds | | |

| Series A | | |

| 2.80%, due 7/1/42 (d) | 15,000,000 | 15,000,000 |

| District of Columbia 0.8% (0.5% of Managed Assets) |

| Metropolitan Washington Airports Authority, Dulles Toll Road, Revenue Bonds, Second Lien | | |

| Series C, Insured: AGC | | |

| 6.50%, due 10/1/41 (e) | 2,400,000 | 2,551,797 |

| Florida 5.3% (3.6% of Managed Assets) |

| City of Miami Beach, Unlimited General Obligation | | |

| 4.00%, due 5/1/49 | 10,000,000 | 9,931,480 |

| County of Broward, Airport System, Revenue Bonds | | |

| 5.00%, due 10/1/42 (c) | 4,500,000 | 4,592,814 |

| County of Broward, Tourist Development Tax, Revenue Bonds | | |

| Insured: BAM | | |

| 4.00%, due 9/1/51 | 2,550,000 | 2,556,418 |

| | | 17,080,712 |

Portfolio of Investments November 30, 2024† (Unaudited) (continued)

| | Principal

Amount | Value |

| Georgia 2.0% (1.4% of Managed Assets) |

| Municipal Electric Authority of Georgia, Revenue Bonds | | |

| Series A, Insured: AGM | | |

| 5.00%, due 7/1/55 | $ 6,175,000 | $ 6,536,416 |

| Illinois 22.0% (14.8% of Managed Assets) |

| Chicago Board of Education, Unlimited General Obligation | | |

| Series A | | |

| 7.00%, due 12/1/44 | 2,880,000 | 2,941,092 |

| Chicago Board of Education, Dedicated Capital Improvement, Revenue Bonds | | |

| 5.75%, due 4/1/34 | 8,000,000 | 8,347,863 |

| Chicago Board of Education, Dedicated Capital Improvement, Unlimited General Obligation (f) | | |

| Series A | | |

| 7.00%, due 12/1/46 | 4,000,000 | 4,276,989 |

| Series B | | |

| 7.00%, due 12/1/42 | 3,500,000 | 3,759,543 |

| City of Chicago, Unlimited General Obligation | | |

| Series A | | |

| 5.50%, due 1/1/49 | 5,000,000 | 5,152,564 |

| Series A | | |

| 6.00%, due 1/1/38 | 7,180,000 | 7,445,817 |

| Series E | | |

| 5.50%, due 1/1/42 | 2,000,000 | 1,999,951 |

| Metropolitan Pier & Exposition Authority, McCormick Place Expansion Project, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 6/15/57 | 4,665,000 | 4,759,617 |

| Series B-1, Insured: AGM | | |

| (zero coupon), due 6/15/43 | 10,000,000 | 4,704,290 |

| Sales Tax Securitization Corp., Revenue Bonds | | |

| Series C, Insured: BAM | | |

| 5.25%, due 1/1/48 (b) | 11,000,000 | 11,514,023 |

| State of Illinois, Unlimited General Obligation | | |

| 5.50%, due 5/1/39 (b) | 8,380,000 | 9,091,691 |

| Will County School District No. 114, Manhattan, Unlimited General Obligation | | |

| Insured: BAM | | |

| 5.50%, due 9/1/52 | 6,000,000 | 6,584,012 |

| | | 70,577,452 |

| | Principal

Amount | Value |

| Kentucky 2.0% (1.3% of Managed Assets) |

| Kentucky Bond Development Corp., Kentucky Communications Network Authority, Revenue Bonds | | |

| Insured: BAM | | |

| 5.00%, due 9/1/44 (b) | $ 5,975,000 | $ 6,327,742 |

| Massachusetts 4.9% (3.3% of Managed Assets) |

| Commonwealth of Massachusetts, Unlimited General Obligation | | |

| Series C | | |

| 5.00%, due 10/1/52 | 3,500,000 | 3,782,514 |

| Commonwealth of Massachusetts Transportation Fund, Rail Enhancement Program, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 6/1/53 (b) | 3,535,000 | 3,838,509 |

| Massachusetts School Building Authority Senior Dedicated Sales Tax, Social Bonds, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 8/15/45 (b) | 7,500,000 | 8,069,220 |

| | | 15,690,243 |

| Michigan 4.1% (2.8% of Managed Assets) |

| Michigan Finance Authority, Bronson Health Care Group Obligated Group, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 5/15/54 | 5,000,000 | 5,067,416 |

| State of Michigan, Trunk Line, Revenue Bonds | | |

| 5.50%, due 11/15/44 (b) | 7,000,000 | 8,093,948 |

| | | 13,161,364 |

| Missouri 3.2% (2.1% of Managed Assets) |

| Kansas City Industrial Development Authority, Airport, Revenue Bonds | | |

| Series B | | |

| 5.00%, due 3/1/54 (c) | 10,000,000 | 10,213,970 |

| Nebraska 3.4% (2.3% of Managed Assets) |

| Omaha City Airport Authority, Airport Facilities, Revenue Bonds | | |

| Insured: AGC | | |

| 5.25%, due 12/15/49 (b) | 10,000,000 | 10,867,245 |

| 8 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

| | Principal

Amount | Value |

| Nevada 4.9% (3.3% of Managed Assets) |

| County of Clark, Regional Transportation Commission of Southern Nevada Motor Fuel Tax, Revenue Bonds | | |

| 3.00%, due 7/1/42 | $ 4,090,000 | $ 3,661,779 |

| Las Vegas Valley Water District, Water Bonds, Unlimited General Obligation | | |

| Series A | | |

| 5.00%, due 6/1/53 (b) | 11,000,000 | 11,920,648 |

| | | 15,582,427 |

| New Jersey 4.3% (2.9% of Managed Assets) |

| New Jersey Economic Development Authority, State of New Jersey, Revenue Bonds | | |

| Series A | | |

| 4.00%, due 11/1/39 | 3,400,000 | 3,439,189 |

| New Jersey Economic Development Authority, United Airlines, Inc., Revenue Bonds | | |

| 5.25%, due 9/15/29 | 4,290,000 | 4,294,677 |

| New Jersey Transportation Trust Fund Authority, Transportation Program, Revenue Bonds | | |

| Series AA | | |

| 5.25%, due 6/15/43 | 4,595,000 | 4,875,647 |

| Series BB | | |

| 4.00%, due 6/15/44 | 1,000,000 | 1,001,638 |

| | | 13,611,151 |

| New York 16.7% (11.2% of Managed Assets) |

| Metropolitan Transportation Authority, Revenue Bonds | | |

| Series C-1 | | |

| 5.25%, due 11/15/56 | 7,100,000 | 7,202,308 |

| New York State Dormitory Authority, State of New York Personal Income Tax, Revenue Bonds | | |

| Series E | | |

| 4.00%, due 3/15/38 | 2,000,000 | 2,067,708 |

| New York Transportation Development Corp., Laguardia Gateway Partners LLC, Revenue Bonds | | |

| Series A, Insured: AGM | | |

| 4.00%, due 7/1/36 (c) | 12,000,000 | 11,907,382 |

| Port Authority of New York & New Jersey, Revenue Bonds | | |

| Series 231 | | |

| 5.50%, due 8/1/52 (b)(c) | 10,000,000 | 10,953,899 |

| | Principal

Amount | Value |

| New York |

| Riverhead Industrial Development Agency, Riverhead Charter School, Revenue Bonds | | |

| Series A | | |

| 7.00%, due 8/1/43 | $ 3,395,000 | $ 3,402,640 |

| State of New York Dormitory Authority, Personal Income Tax, General Purpose, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 3/15/41 (b) | 9,450,000 | 10,401,646 |

| Triborough Bridge & Tunnel Authority, MTA Bridges & Tunnels, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 11/15/49 (b) | 7,000,000 | 7,431,770 |

| | | 53,367,353 |

| Pennsylvania 6.9% (4.6% of Managed Assets) |

| Allentown Neighborhood Improvement Zone Development Authority, City Center Project, Revenue Bonds | | |

| 5.00%, due 5/1/42 (f) | 1,000,000 | 1,008,791 |

| Pennsylvania Economic Development Financing Authority, Penndot Major Bridges Package One Project (The), Revenue Bonds | | |

| Insured: AGM | | |

| 5.75%, due 12/31/62 (b)(c) | 12,465,000 | 13,673,652 |

| Southeastern Pennsylvania Transportation Authority, Asset Improvement Program, Revenue Bonds | | |

| 5.25%, due 6/1/43 (b) | 6,500,000 | 7,253,305 |

| | | 21,935,748 |

| Puerto Rico 13.8% (9.3% of Managed Assets) |

| Children's Trust Fund, Asset-Backed, Revenue Bonds | | |

| 5.50%, due 5/15/39 | 9,455,000 | 9,505,233 |

| Commonwealth of Puerto Rico, Unlimited General Obligation | | |

| Series A-1 | | |

| 4.00%, due 7/1/33 | 8,500,000 | 8,474,649 |

| Puerto Rico Commonwealth Aqueduct & Sewer Authority, Revenue Bonds, Senior Lien | | |

| Series A | | |

| 5.00%, due 7/1/33 (f) | 2,500,000 | 2,669,472 |

Portfolio of Investments November 30, 2024† (Unaudited) (continued)

| | Principal

Amount | Value |

| Puerto Rico (continued) |

| Puerto Rico Municipal Finance Agency, Revenue Bonds | | |

| Series A, Insured: AGM | | |

| 5.00%, due 8/1/27 | $ 1,280,000 | $ 1,288,392 |

| Series A, Insured: AGM | | |

| 5.00%, due 8/1/30 | 1,685,000 | 1,696,124 |

| Puerto Rico Sales Tax Financing Corp., Sales Tax, Revenue Bonds | | |

| Series A-1 | | |

| 4.55%, due 7/1/40 | 2,500,000 | 2,509,109 |

| Series A-1 | | |

| 5.00%, due 7/1/58 | 17,940,000 | 18,020,979 |

| | | 44,163,958 |

| South Carolina 3.0% (2.0% of Managed Assets) |

| South Carolina Public Service Authority, Santee Cooper, Revenue Bonds | | |

| Series E, Insured: AGM | | |

| 5.75%, due 12/1/52 (b) | 8,500,000 | 9,515,377 |

| Texas 5.9% (4.0% of Managed Assets) |

| City of Georgetown, Utility System, Revenue Bonds | | |

| Insured: AGM | | |

| 5.25%, due 8/15/52 (b) | 7,500,000 | 8,100,451 |

| Texas Private Activity Bond Surface Transportation Corp., NTE Mobility Partners LLC, Revenue Bonds, Senior Lien | | |

| 5.50%, due 12/31/58 (b)(c) | 10,000,000 | 10,855,685 |

| | | 18,956,136 |

| U.S. Virgin Islands 5.0% (3.4% of Managed Assets) |

| Matching Fund Special Purpose Securitization Corp., United States Virgin Islands Federal Excise Tax, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 10/1/30 | 1,570,000 | 1,666,720 |

| Series A | | |

| 5.00%, due 10/1/32 | 1,570,000 | 1,648,740 |

| Series A | | |

| 5.00%, due 10/1/39 | 4,710,000 | 4,904,791 |

| Virgin Islands Public Finance Authority, United States Virgin Islands Federal Excise Tax, Revenue Bonds | | |

| Series A | | |

| 5.00%, due 10/1/29 (f) | 2,980,000 | 2,958,019 |

| | Principal

Amount | Value |

| U.S. Virgin Islands |

Virgin Islands Public Finance Authority, United States Virgin Islands Federal Excise Tax, Revenue Bonds

(continued) | | |

| Series A | | |

| 5.00%, due 10/1/32 | $ 2,625,000 | $ 2,592,749 |

| Series A, Insured: AGM-CR | | |

| 5.00%, due 10/1/32 | 2,300,000 | 2,322,205 |

| | | 16,093,224 |

| Virginia 3.3% (2.3% of Managed Assets) |

| Hampton Roads Transportation Accountability Commission, Roads Transportation Fund, Revenue Bonds, Senior Lien | | |

| Series A | | |

| 5.25%, due 7/1/60 (b) | 10,000,000 | 10,703,316 |

| Washington 2.2% (1.5% of Managed Assets) |

| State of Washington, Unlimited General Obligation | | |

| Series C | | |

| 5.00%, due 2/1/46 | 6,500,000 | 7,054,150 |

| West Virginia 1.5% (1.0% of Managed Assets) |

| West Virginia Hospital Finance Authority, Vandalia Health, Inc. Obligated Group, Revenue Bonds | | |

| Series B, Insured: AGM | | |

| 5.375%, due 9/1/53 | 4,500,000 | 4,932,372 |

| 10 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

| | Principal

Amount | | Value |

| Wisconsin 1.8% (1.2% of Managed Assets) |

| Public Finance Authority, Ultimate Medical Academy Project, Revenue Bonds | | | |

| Series A | | | |

| 5.00%, due 10/1/39 (f) | $ 5,750,000 | | $ 5,820,924 |

Total Investments

(Cost $445,192,617) | 145.1% | | 464,527,147 |

| Floating Rate Note Obligations (g) | (48.0) | | (153,690,000) |

| Other Assets, Less Liabilities | 2.9 | | 9,276,586 |

| Net Assets Applicable to Common Shares | 100.0% | | $ 320,113,733 |

| † | Percentages indicated are based on Fund net assets applicable to Common shares. |

| (a) | Coupon rate may change based on changes of the underlying collateral or prepayments of principal. Rate shown was the rate in effect as of November 30, 2024. |

| (b) | All or portion of principal amount transferred to a Tender Option Bond (“TOB”) Issuer in exchange for TOB Residuals and cash. |

| (c) | Interest on these securities was subject to alternative minimum tax. |

| (d) | Variable-rate demand notes (VRDNs)—Provide the right to sell the security at face value on either that day or within the rate-reset period. VRDNs will normally trade as if the maturity is the earlier put date, even though stated maturity is longer. The interest rate is reset on the put date at a stipulated daily, weekly, monthly, quarterly, or other specified time interval to reflect current market conditions. These securities do not indicate a reference rate and spread in their description. The maturity date shown is the final maturity. |

| (e) | Step coupon—Rate shown was the rate in effect as of November 30, 2024. |

| (f) | May be sold to institutional investors only under Rule 144A or securities offered pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended. |

| (g) | Face value of Floating Rate Notes issued in TOB transactions. |

"Managed Assets" is defined as the Fund’s total assets minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of creating effective leverage (i.e. tender option bonds) or Fund liabilities related to liquidation preference of any preferred shares issued), which was $475,466,535 as of November 30, 2024.

| Abbreviation(s): |

| AGC—Assured Guaranty Corp. |

| AGM—Assured Guaranty Municipal Corp. |

| BAM—Build America Mutual Assurance Co. |

| CR—Custodial Receipts |

| MTA—Metropolitan Transportation Authority |

The following is a summary of the fair valuations according to the inputs used as of November 30, 2024, for valuing the Fund’s assets:

| Description | Quoted

Prices in

Active

Markets for

Identical

Assets

(Level 1) | | Significant

Other

Observable

Inputs

(Level 2) | | Significant

Unobservable

Inputs

(Level 3) | | Total |

| Asset Valuation Inputs | | | | | | | |

| Investments in Securities (a) | | | | | | | |

| Municipal Bonds | $ — | | $ 464,527,147 | | $ — | | $ 464,527,147 |

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

Statement of Assets and Liabilities as of November 30, 2024 (Unaudited)

| Assets |

Investment in securities, at value

(identified cost $445,192,617) | $464,527,147 |

| Cash | 11,688,844 |

| Receivables: | |

| Investment securities sold | 26,749,550 |

| Interest | 6,266,434 |

| Other assets | 90,343 |

| Total assets | 509,322,318 |

| Liabilities |

| Payable for Floating Rate Note Obligations | 153,690,000 |

| Payables: | |

| Investment securities purchased | 33,498,820 |

| Manager (See Note 3) | 289,777 |

| Professional fees | 38,591 |

| Custodian | 12,827 |

| Transfer agent | 4,420 |

| Trustees | 91 |

| Accrued expenses | 11,257 |

| Interest expense and fees payable | 1,662,802 |

| Total liabilities | 189,208,585 |

| Net assets applicable to Common shares | $320,113,733 |

| Common shares outstanding | 18,779,453 |

| Net asset value per Common share (Net assets applicable to Common shares divided by Common shares outstanding) | $ 17.05 |

| Net Assets Applicable to Common Shares Consist of |

| Common shares, $0.001 par value per share, unlimited number of shares authorized | $ 18,779 |

| Additional paid-in-capital | 377,281,376 |

| | 377,300,155 |

| Total distributable earnings (loss) | (57,186,422) |

| Net assets applicable to Common shares | $320,113,733 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 12 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

Statement of Operations for the six months ended November 30, 2024 (Unaudited)

| Investment Income (Loss) |

| Income | |

| Interest | $13,675,971 |

| Expenses | |

| Manager (See Note 3) | 1,967,188 |

| Interest expense and fees | 3,739,129 |

| Professional fees | 113,549 |

| Shareholder communication | 28,665 |

| Custodian | 18,907 |

| Transfer agent | 12,887 |

| Trustees | 5,530 |

| Miscellaneous | 39,339 |

| Total expenses | 5,925,194 |

| Net investment income (loss) | 7,750,777 |

| Realized and Unrealized Gain (Loss) |

| Net realized gain (loss) on investments | 4,878,212 |

Net change in unrealized appreciation (depreciation)

on investments | 5,942,442 |

| Net realized and unrealized gain (loss) | 10,820,654 |

Net increase (decrease) in net assets to Common shares

resulting from operations | $18,571,431 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

13

Statements of Changes in Net Assets

for the six months ended November 30, 2024 (Unaudited) and the year ended May 31, 2024

| | Six months

ended

November 30,

2024 | Year

ended

May 31,

2024 |

| Increase (Decrease) in Net Assets Applicable to Common Shares |

| Operations: | | |

| Net investment income (loss) | $ 7,750,777 | $ 13,935,029 |

| Net realized gain (loss) | 4,878,212 | (4,718,410) |

| Net change in unrealized appreciation (depreciation) | 5,942,442 | 3,448,511 |

| Net increase (decrease) in net assets applicable to Common shares resulting from operations | 18,571,431 | 12,665,130 |

| Distributions to Common shareholders | (9,504,805) | (21,360,388) |

Capital share transactions

(Common shares): | | |

| Net proceeds issued to shareholders resulting from reinvestment of dividends | — | 311,212 |

| Cost of shares repurchased and retired through tender offer | (154,509,566) | — |

| Increase (decrease) in net assets applicable to Common shares from capital share transactions | (154,509,566) | 311,212 |

| Net increase (decrease) in net assets applicable to Common shares | (145,442,940) | (8,384,046) |

| Net Assets Applicable to Common Shares |

| Beginning of period | 465,556,673 | 473,940,719 |

| End of period | $ 320,113,733 | $465,556,673 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 14 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

Statement of Cash Flows

for the six months ended November 30, 2024 (Unaudited)

| Cash Flows From (Used in) Operating Activities: |

| Net increase in net assets resulting from operations | $ 18,571,431 |

| Adjustments to reconcile net increase in net assets resulting from operations to net cash used in operating activities: | |

| Investments purchased | (79,618,920) |

| Investments sold | 272,764,281 |

| Amortization (accretion) of discount and premium, net | 1,508,354 |

| Increase in investment securities sold receivable | (26,749,550) |

| Decrease in interest receivable | 3,107,154 |

| Increase in other assets | (66,226) |

| Increase in investment securities purchased payable | 33,498,820 |

| Decrease in professional fees payable | (60,042) |

| Increase in custodian payable | 4,006 |

| Decrease in shareholder communication payable | (4,638) |

| Increase in due to Trustees | 91 |

| Decrease in due to manager | (47,525) |

| Increase in due to transfer agent | 209 |

| Increase in accrued expenses | 9,348 |

| Decrease in interest expense and fees payable | (847,537) |

| Net realized gain from investments | (4,878,212) |

| Net change in unrealized (appreciation) depreciation on unaffiliated investments | (5,942,442) |

| Net cash from operating activities | 211,248,602 |

| Cash Flows From (Used in) Financing Activities: |

| Cost of shares repurchased and retired through tender offer | (154,509,566) |

| Proceeds from floating rate note obligations | 24,265,000 |

| Payments on floating rate note obligations | (61,085,000) |

| Cash distributions paid, net of change in Common share dividend payable | (9,504,805) |

| Net cash used in financing activities | (200,834,371) |

| Net increase in cash | 10,414,231 |

| Cash at beginning of period | 1,274,613 |

| Cash at end of period | $ 11,688,844 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

15

Financial Highlights selected per share data and ratios

| | Six months

ended

November 30,

2024* | | Year Ended May 31, |

| | 2024 | | 2023 | | 2022 | | 2021 | | 2020 |

| Net asset value at beginning of period applicable to Common shares | $ 16.67 | | $ 16.98 | | $ 18.27 | | $ 21.26 | | $ 19.79 | | $ 20.41 |

| Net investment income (loss) | 0.28 | | 0.50 | | 0.53 | | 0.93 | | 1.01 | | 0.99 |

| Net realized and unrealized gain (loss) | 0.46 | | (0.04) | | (0.83) | | (2.90) | | 1.48 | | (0.59) |

| Total from investment operations | 0.74 | | 0.46 | | (0.30) | | (1.97) | | 2.49 | | 0.40 |

| Dividends and distributions to Common shareholders | (0.36) | | (0.77) | | (0.99) | | (1.02) | | (1.02) | | (1.02) |

| Net asset value at end of period applicable to Common shares | $ 17.05 | | $ 16.67 | | $ 16.98 | | $ 18.27 | | $ 21.26 | | $ 19.79 |

| Market price at end of period applicable to Common shares | $ 16.10 | | $ 16.20 | | $ 17.00 | | $ 18.80 | | $ 22.89 | | $ 20.94 |

| Total investment return on market price (a) | 1.56% | | (0.11)% | | (4.16)% | | (13.62)% | | 14.79% | | 6.62% |

| Total investment return on net asset value (a) | 4.47% | | 2.76% | | (1.49)% | | (9.68)% | | 12.82% | | 1.94% |

Ratios (to average net assets of Common shareholders)/

Supplemental Data: | | | | | | | | | | | |

| Net investment income (loss) | 3.33%†† | | 2.98% | | 3.09% | | 4.56% | | 4.88% | | 4.44% |

| Net expenses (including interest expense and fees) | 2.54%†† | | 2.88% | | 2.89% | | 1.79% | | 1.64% | | 2.33% |

| Interest expense and fees (b) | 1.60%†† | | 1.92% | | 1.84% | | 0.76% | | 0.61% | | 1.31% |

| Portfolio Turnover Rate | 13%(c) | | 32%(c) | | 42%(c) | | 46% | | 20% | | 38%(c) |

| Net assets applicable to Common shareholders at end of period (in 000’s) | $ 320,114 | | $ 465,557 | | $ 473,941 | | $ 508,811 | | $ 590,652 | | $ 547,744 |

Preferred shares outstanding at $100,000 liquidation preference,

end of period (in 000’s) (d)(e) | $ — | | $ — | | $ — | | $ — | | $ — | | $ 70,000 |

| Assets coverage per Preferred share, end of period (d)(e) | $ — | | $ — | | $ — | | $ — | | $ — | | $ 882,491(f) |

| Average market value per Preferred share: | | | | | | | | | | | |

| Series A (d) | $ — | | $ — | | $ — | | $ — | | $ — | | $ 100,000 |

| Series B (e) | $ — | | $ — | | $ — | | $ — | | $ — | | $ 99,999 |

| * | Unaudited. |

| †† | Annualized. |

| (a) | Total investment return on market price is calculated assuming a purchase of a Common share at the market price on the first day and a sale on the last day business day of each month. Dividends and distributions are assumed to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return on net asset value reflects the changes in net asset value during each period and assumes the reinvestment of dividends and distributions at net asset value on the last business day of each month. This percentage may be different from the total investment return on market price, due to differences between the market price and the net asset value. For periods less than one year, total investment return is not annualized. |

| (b) | Interest expense and fees relate to the costs of tender option bond transactions (See Note 2(G)) and the issuance of fixed rate municipal term preferred shares, where applicable, for the six months ended November 30, 2024 and for years ended May 31, 2024, 2023, 2022, 2021 and 2020, respectively. |

| (c) | The portfolio turnover rate includes variable rate demand notes. |

| (d) | Redeemed on June 15, 2020. |

| (e) | Redeemed on December 15, 2020. |

| (f) | Calculated by subtracting the Fund’s total liabilities (not including the Preferred shares) from the Fund’s total assets, and dividing the result by the number of Preferred shares outstanding. |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| 16 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

Notes to Financial Statements (Unaudited)

Note 1-Organization and Business

NYLI MacKay DefinedTerm Muni Opportunities Fund (formerly known as MainStay MacKay DefinedTerm Municipal Opportunities Fund) (the “Fund”) was organized as a Delaware statutory trust on April 20, 2011, pursuant to an agreement and declaration of trust, which was most recently amended and restated on December 3, 2024 (“Declaration of Trust’’). The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a “diversified”, closed-end management investment company, as those terms are defined in the 1940 Act, as interpreted or modified by regulatory authorities having jurisdiction, from time to time. The Fund first offered Common shares through an initial public offering on June 26, 2012.

At a meeting held on June 4-5, 2024, the Board of Trustees of the Fund (the “Board”) (as discussed in further detail below) approved an amendment and restatement of the Declaration of Trust to reflect a change in the name of the Fund to NYLI MacKay DefinedTerm Muni Opportunities Fund and to allow the Board to implement, upon completion of an Eligible Tender Offer (as defined below), a new Termination Date (as defined below) to replace December 31, 2024, as the Termination Date (as defined below). An “Eligible Tender Offer” is defined as a tender offer by the Fund to purchase 100% of the then outstanding Common shares of the Fund at a price equal to the net asset value (“NAV”) per Common share calculated in accordance with the Fund’s valuation procedures as of the date specified in the tender offer, with the expiration date of the tender offer being as of a date within twelve months preceding the Termination Date (as defined below). The amendments became effective as of August 28, 2024. In addition, the Board conditionally approved December 31, 2036 as the new Termination Date, or the date the Fund will commence the process of liquidation and dissolution (the "Termination Date"), to take effect in the event that the Fund completes an Eligible Tender Offer prior to December 31, 2024. The new Termination Date allowed shareholders the opportunity to maintain their investment in the Fund and its exposure to a leveraged strategy focused on tax-exempt income producing securities in lieu of the previously scheduled termination of the Fund.

On October 17, 2024, the Fund conducted a tender offer, which allowed shareholders to offer up to 100% of their shares for repurchase for cash at a price per share equal to 100% of the NAV per share determined on the date the tender offer expired. In the tender offer, 9,147,341 Common shares were tendered, representing approximately 32.8% of the Fund’s Common shares outstanding. Properly tendered shares were repurchased at $16.89 per share, which was the NAV of the Fund as of the close of ordinary trading on the New York Stock Exchange (the "Exchange") on the expiration date, November 14, 2024.

As a result of the successful completion of the Eligible Tender Offer, which resulted in the Fund's net assets totaling greater than or equal to

$200 million (the "Termination Threshold"), the following was implemented:

• The Board has approved, and the Fund’s Agreement and Declaration of Trust was amended to reflect, a new 12-year term for the Fund with a termination date of December 31, 2036.

• New York Life Investment Management LLC, the investment adviser to the Fund, will waive 0.06% of the Fund’s management fee from December 31, 2024, until December 31, 2025. As a result of the waiver, the Fund’s net management fee, which is applied to managed assets, would be reduced from 0.60% to 0.54%.

Pursuant to the terms of the Declaration of Trust, the Fund will commence the process of liquidation and dissolution at the close of business on December 31, 2036, the Termination Date, unless otherwise extended by a majority of the Board. During the six-month period preceding the Termination Date or Extended Termination Date (as defined below), the Board may, without shareholder approval unless such approval is required by the 1940 Act, cause the Fund to (i) merge or consolidate the Fund so long as the surviving or resulting entity is an open-end registered investment company, as defined by the 1940 Act, or is a series thereof, that is managed by the same investment adviser which serves as the investment adviser to the Fund at that time or is an affiliate of such investment adviser; or (ii) convert the Fund from a closed-end company into an open-end registered investment company. Upon liquidation and termination of the Fund, shareholders will receive an amount equal to the Fund’s NAV at that time, which may be greater or less than the price at which Common shares were issued. The Fund’s investment objectives and policies are not designed to return to investors who purchased Common shares in the initial offering of such shares their initial investment on the Termination Date and such initial investors may receive more or less than their original investment upon termination.

Prior to the commencement of the six-month period preceding the Termination Date, a majority of the Board may approve an extension of the dissolution date of the Fund to a date after the Termination Date for a period of not more than two years or such shorter time as may be determined (the “Extended Termination Date”), upon a determination that taking such actions as described in (i) or (ii) above would not, given prevailing market conditions, be in the best interests of the Fund’s shareholders. The Termination Date may be extended one or more times by the Board prior to the first business day of the sixth month before the next occurring Extended Termination Date.

The Fund's primary investment objective is to seek current income exempt from regular U.S. Federal income taxes (but which may be includable in taxable income for the purpose of the Federal alternative minimum tax). Total return is a secondary objective.

Note 2–Significant Accounting Policies

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification

Notes to Financial Statements (Unaudited) (continued)

Topic 946 Financial Services—Investment Companies. The Fund prepares its financial statements in accordance with generally accepted accounting principles (“GAAP”) in the United States of America and follows the significant accounting policies described below.

(A) Securities Valuation. Investments are usually valued as of the close of regular trading on the Exchange (usually 4:00 p.m. Eastern time) on each day the Fund is open for business ("valuation date").

Pursuant to Rule 2a-5 under the 1940 Act, the Board has designated New York Life Investment Management LLC (“New York Life Investments” or the "Manager") as its Valuation Designee (the "Valuation Designee"). The Valuation Designee is responsible for performing fair valuations relating to all investments in the Fund’s portfolio for which market quotations are not readily available; periodically assessing and managing material valuation risks; establishing and applying fair value methodologies; testing fair valuation methodologies; evaluating and overseeing pricing services; ensuring appropriate segregation of valuation and portfolio management functions; providing quarterly, annual and prompt reporting to the Board, as appropriate; identifying potential conflicts of interest; and maintaining appropriate records. The Valuation Designee has established a valuation committee ("Valuation Committee") to assist in carrying out the Valuation Designee’s responsibilities and establish prices of securities for which market quotations are not readily available. The Fund’s and the Valuation Designee's policies and procedures ("Valuation Procedures") govern the Valuation Designee’s selection and application of methodologies for determining and calculating the fair value of Fund investments. The Valuation Designee may value the Fund's portfolio securities for which market quotations are not readily available and other Fund assets utilizing inputs from pricing services and other third-party sources. The Valuation Committee meets (in person, via electronic mail or via teleconference) on an ad-hoc basis to determine fair valuations and on a quarterly basis to review fair value events with respect to certain securities for which market quotations are not readily available, including valuation risks and back-testing results, and to preview reports to the Board.

The Valuation Committee establishes prices of securities for which market quotations are not readily available based on such methodologies and measurements on a regular basis after considering information that is reasonably available and deemed relevant by the Valuation Committee. The Board shall oversee the Valuation Designee and review fair valuation materials on a prompt, quarterly and annual basis and approve proposed revisions to the Valuation Procedures.

Investments for which market quotations are not readily available are valued at fair value as determined in good faith pursuant to the Valuation Procedures. A market quotation is readily available only when that quotation is a quoted price (unadjusted) in active markets for identical investments that the Fund can access at the measurement date, provided that a quotation will not be readily available if it is not reliable. "Fair value" is defined as the price the Fund would reasonably expect to receive upon selling an asset or liability in an orderly transaction to an independent buyer in the principal or most advantageous market for the asset or

liability. Fair value measurements are determined within a framework that establishes a three-tier hierarchy that maximizes the use of observable market data and minimizes the use of unobservable inputs to establish a classification of fair value measurements for disclosure purposes. "Inputs" refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, such as the risk inherent in a particular valuation technique used to measure fair value using a pricing model and/or the risk inherent in the inputs for the valuation technique. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions market participants would use in pricing the asset or liability based on the information available. The inputs or methodology used for valuing assets or liabilities may not be an indication of the risks associated with investing in those assets or liabilities. The three-tier hierarchy of inputs is summarized below.

| • | Level 1—quoted prices (unadjusted) in active markets for an identical asset or liability |

| • | Level 2—other significant observable inputs (including quoted prices for a similar asset or liability in active markets, interest rates and yield curves, prepayment speeds, credit risk, etc.) |

| • | Level 3—significant unobservable inputs (including the Fund's own assumptions about the assumptions that market participants would use in measuring fair value of an asset or liability) |

The level of an asset or liability within the fair value hierarchy is based on the lowest level of an input, both individually and in the aggregate, that is significant to the fair value measurement. The aggregate value by input level of the Fund’s assets and liabilities as of November 30, 2024, is included at the end of the Portfolio of Investments.

The Fund may use third-party vendor evaluations, whose prices may be derived from one or more of the following standard inputs, among others:

| • Benchmark yields | • Reported trades |

| • Broker/dealer quotes | • Issuer spreads |

| • Two-sided markets | • Benchmark securities |

| • Bids/offers | • Reference data (corporate actions or material event notices) |

| • Industry and economic events | • Comparable bonds |

| • Monthly payment information | |

An asset or liability for which a market quotation is not readily available is valued by methods deemed reasonable in good faith by the Valuation Committee, following the Valuation Procedures to represent fair value. Under these procedures, the Valuation Designee generally uses a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant information. The Valuation Designee may also use an income-based valuation approach in which the anticipated future cash flows of the asset or liability are discounted to calculate fair value. Fair

| 18 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

value represents a good faith approximation of the value of a security. Fair value determinations involve the consideration of a number of subjective factors, an analysis of applicable facts and circumstances and the exercise of judgment. As a result, it is possible that the fair value for a security determined in good faith in accordance with the Valuation Procedures may differ from valuations for the same security determined for other funds using their own valuation procedures. Although the Valuation Procedures are designed to value a security at the price the Fund may reasonably expect to receive upon the security's sale in an orderly transaction, there can be no assurance that any fair value determination thereunder would, in fact, approximate the amount that the Fund would actually realize upon the sale of the security or the price at which the security would trade if a reliable market price were readily available. During the six-month period ended November 30, 2024, there were no material changes to the fair value methodologies.

Securities which may be valued in this manner include, but are not limited to: (i) a security for which trading has been halted or suspended or otherwise does not have a readily available market quotation on a given day; (ii) a debt security that has recently gone into default and for which there is not a current market quotation; (iii) a security of an issuer that has entered into a restructuring; (iv) a security that has been delisted from a national exchange; (v) a security subject to trading collars for which no or limited trading takes place; and (vi) a security whose principal market has been temporarily closed at a time when, under normal conditions, it would be open. Securities valued in this manner are generally categorized as Level 2 or 3 in the hierarchy.

Municipal debt securities are valued at the evaluated mean prices supplied by a pricing agent or broker selected by the Valuation Designee, in consultation with the Subadvisor. The evaluations are market-based measurements processed through a pricing application and represents the pricing agent's good faith determination as to what a holder may receive in an orderly transaction under market conditions. The rules-based logic utilizes valuation techniques that reflect participants' assumptions and vary by asset class and per methodology, maximizing the use of relevant observable data including quoted prices for similar assets, benchmark yield curves and market corroborated inputs. The evaluated bid or mean prices are deemed by the Valuation Designee, in consultation with the Subadvisor, to be representative of market values, at the regular close of trading of the Exchange on each valuation date. Municipal debt securities purchased on a delayed delivery basis are marked to market daily until settlement at the forward settlement date. Municipal debt securities are generally categorized as Level 2 in the hierarchy.

The information above is not intended to reflect an exhaustive list of the methodologies that may be used to value portfolio investments. The Valuation Procedures permit the use of a variety of valuation methodologies in connection with valuing portfolio investments. The methodology used for a specific type of investment may vary based on the market data available or other considerations. The methodologies summarized above may not represent the specific means by which portfolio investments are valued on any particular business day.

(B) Income Taxes. The Fund's policy is to comply with the requirements of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), applicable to regulated investment companies and to distribute all of its taxable income to the shareholders of the Fund within the allowable time limits.

The Manager evaluates the Fund’s tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in the financial statements. Recognition of tax benefits of an uncertain tax position is permitted only to the extent the position is “more likely than not” to be sustained assuming examination by taxing authorities. The Manager analyzed the Fund's tax positions taken on federal, state and local income tax returns for all open tax years (for up to three tax years) and has concluded that no provisions for federal, state and local income tax are required in the Fund's financial statements. The Fund's federal, state and local income tax and federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state and local departments of revenue.

(C) Dividends and Distributions to Common Shareholders. Dividends and distributions are recorded on the ex-dividend date. The Fund intends to declare dividends from net investment income at least monthly and declares and pays distributions from net realized capital gains, if any, at least annually. Dividends and distributions are determined in accordance with federal income tax regulations and may differ from determinations using GAAP. For information on the Fund’s dividend reinvestment plan (unaudited), please see page 24.

(D) Security Transactions and Investment Income. The Fund records security transactions on the trade date. Realized gains and losses on security transactions are determined using the identified cost method. Interest income is accrued as earned using the effective interest rate method. Discounts and premiums on securities purchased by the Fund, other than temporary cash investments that mature in 60 days or less at the time of purchase, are accreted and amortized, respectively, using the effective interest rate method.

The Fund may place a debt security on non-accrual status and reduce related interest income by ceasing current accruals and writing off all or a portion of any interest receivables when the collection of all or a portion of such interest has become doubtful. A debt security is removed from non-accrual status when the issuer resumes interest payments or when collectability of interest is reasonably assured.

(E) Expenses. The expenses borne by the Fund, including those of related parties to the Fund, are shown in the Statement of Operations. Certain expenses of the Fund are allocated in proportion to other funds within the New York Life Investments Group of Funds.

Notes to Financial Statements (Unaudited) (continued)

(F) Use of Estimates. In preparing financial statements in conformity with GAAP, the Manager makes estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates and assumptions.

(G) Tender Option Bonds. The Fund may leverage its assets through the use of proceeds received from tender option bond (“TOB”) transactions. In a TOB transaction, a tender option bond trust (a “TOB Issuer”) is typically established, which forms a special purpose trust into which the Fund, or an agent on behalf of the Fund, transfers municipal bonds or other municipal securities (“Underlying Securities”). A TOB Issuer typically issues two classes of beneficial interests: short-term floating rate notes (“TOB Floaters”) with a fixed principal amount representing a senior interest in the Underlying Securities, and which are sold to third party investors, and residual interest municipal tender option bonds (“TOB Residuals”) representing a subordinate interest in the Underlying Securities, and which are generally issued to the Fund. The interest rate on the TOB Floaters resets periodically, usually weekly, to a prevailing market rate, and holders of the TOB Floaters are granted the option to tender their TOB Floaters back to the TOB Issuer for repurchase at their principal amount plus accrued interest thereon periodically, usually daily or weekly. The Fund may invest in both TOB Floaters and TOB Residuals. The Fund may not invest more than 5% of its Managed Assets (as defined in Note 3(A)) in any single TOB Issuer. The Fund may invest in both TOB Floaters and TOB Residuals issued by the same TOB Issuer.

Typically, a fund serves as the sponsor of the TOB issuer (“Fund-sponsored TOB”). Under this structure, a fund establishes, structures and “sponsors” the TOB Issuer in which it holds TOB Residuals. The Fund uses this or a similar structure for any TOB in which it invests. In connection with Fund-sponsored TOBs, the fund sponsoring the Fund-sponsored TOB (“Fund Sponsor”) may contract with a third-party to perform some or all of the Fund Sponsor’s duties as sponsor. Regardless of whether the Fund Sponsor delegates any of its sponsorship duties to a third party, the Fund Sponsor’s expanded role under the Fund-sponsored TOB structure may increase the Fund Sponsor’s operational and regulatory risk. If the third-party is unable to perform its obligations as an administrative agent, the Fund Sponsor itself would be subject to such obligations or would need to secure a replacement agent. The obligations that the Fund Sponsor may be required to undertake could include reporting and recordkeeping obligations under the Internal Revenue Code and federal securities laws and contractual obligations with other TOB service providers. The Fund may serve as a Fund Sponsor to a Fund-sponsored TOB. If the Fund serves as a Fund Sponsor, it would be subject to the obligations discussed above and the risks attendant to such obligations.

Under the Fund-sponsored TOB structure, the TOB Issuer receives Underlying Securities from the Fund through (or as) the Fund Sponsor and then issues TOB Floaters to third party investors and TOB Residuals to the Fund. The Fund is paid the cash (less transaction expenses, which are borne by the Fund) received by the TOB Issuer from the sale of TOB

Floaters and typically will invest the cash in additional municipal bonds or other investments permitted by its investment policies. TOB Floaters may have first priority on the cash flow from the securities held by the TOB Issuer and are enhanced with a liquidity support arrangement from a bank or an affiliate of the sponsor (the “liquidity provider”), which allows holders to tender their position back to the TOB Issuer at par (plus accrued interest). The Fund, in addition to receiving cash from the sale of TOB Floaters, also receives TOB Residuals. TOB Residuals provide the Fund with the right to (1) cause the holders of TOB Floaters to tender their notes to the TOB Issuer at par (plus accrued interest), and (2) acquire the Underlying Securities from the TOB Issuer. In addition, all voting rights and decisions to be made with respect to any other rights relating to the Underlying Securities deposited in the TOB Issuer are passed through to the Fund, as the holder of TOB Residuals. Such a transaction, in effect, creates exposure for the Fund to the entire return of the Underlying Securities deposited in the TOB Issuer, with a net cash investment by the Fund that is less than the value of the Underlying Securities deposited in the TOB Issuer. This multiplies the positive or negative impact of the Underlying Securities’ return within the Fund (thereby creating leverage). Income received from TOB Residuals will vary inversely with the short-term rate paid to holders of TOB Floaters and in most circumstances, TOB Residuals represent substantially all of the Underlying Securities’ downside investment risk and also benefits disproportionately from any potential appreciation of the Underlying Securities’ value. The amount of such increase or decrease is a function, in part, of the amount of TOB Floaters sold by the TOB Issuer of these securities relative to the amount of TOB Residuals that it sells. The greater the amount of TOB Floaters sold relative to TOB Residuals, the more volatile the income paid on TOB Residuals will be. The price of TOB Residuals will be more volatile than that of the Underlying Securities because the interest rate is dependent on not only the fixed coupon rate of the Underlying Securities, but also on the short-term interest rate paid on TOB Floaters.

For TOB Floaters, generally, the interest rate earned will be based upon the market rates for municipal securities with maturities or remarketing provisions that are comparable in duration to the periodic interval of the tender option, which may vary from weekly, to monthly, to extended periods of one year or multiple years. Since the option feature has a shorter term than the final maturity or first call date of the Underlying Securities deposited in the TOB Issuer, the Fund, if it is the holder of the TOB Floaters, relies upon the terms of the agreement with the financial institution furnishing the option as well as the credit strength of that institution. As further assurance of liquidity, the terms of the TOB Issuer provide for a liquidation of the Underlying Security deposited in the TOB Issuer and the application of the proceeds to pay off the TOB Floaters.

The TOB Issuer may be terminated without the consent of the Fund upon the occurrence of certain events, such as the bankruptcy or default of the issuer of the Underlying Securities deposited in the TOB Issuer, a substantial downgrade in the credit quality of the issuer of the securities deposited in the TOB Issuer, the inability of the TOB Issuer to obtain liquidity support for the TOB Floaters, a substantial decline in the market value of the Underlying Securities deposited in the TOB Issuer, or the

| 20 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

inability of the sponsor to remarket any TOB Floaters tendered to it by holders of the TOB Floaters. In such an event, the TOB Floaters would be redeemed by the TOB Issuer at par (plus accrued interest) out of the proceeds from a sale of the Underlying Securities deposited in the TOB Issuer. If this happens, the Fund would be entitled to the assets of the TOB Issuer, if any, that remain after the TOB Floaters have been redeemed at par (plus accrued interest). If there are insufficient proceeds from the sale of these Underlying Securities to redeem all of the TOB Floaters at par (plus accrued interest), the liquidity provider or holders of the TOB Floaters would bear the losses on those securities and there would be no recourse to the Fund’s assets (unless the Fund held a recourse TOB Residual).

To the extent that the remarketing agent and/or the liquidity provider is a banking entity, the TOB may face heightened liquidity risks due to restrictions applicable to banking entities under the Volcker Rule. The Volcker Rule generally prohibits banking entities from engaging in proprietary trading or from acquiring or retaining an ownership interest in, or sponsoring, a hedge fund or private equity fund (a “Covered Fund”). TOB Issuers are often structured as a Covered Fund, and therefore, a banking entity that is a remarketing agent would not be able to repurchase tendered TOB Floaters for its own account upon a failed remarketing. In the event of a failed remarketing, a banking entity serving as liquidity provider may loan the necessary funds to the TOB Issuer to purchase the tendered TOB Floaters. The TOB Issuer, not the Fund Sponsor or the Fund, would be the borrower and the loan from the liquidity provider will be secured by the purchased TOB Floaters now held by the TOB Issuer. However, the Fund Sponsor and the Fund would bear the risk of loss with respect to any liquidity shortfall to the extent it entered into a reimbursement agreement with the liquidity provider. If a TOB Issuer in which the Fund invests experiences adverse events in connection with a failed remarketing of TOB Floaters or a liquidity shortfall, the Fund would experience a loss.

For financial reporting purposes, Underlying Securities that are deposited into a TOB Issuer are treated as investments of the Fund, and are presented in the Fund’s Portfolio of Investments. Outstanding TOB Floaters issued by a TOB Issuer are presented as a liability at their face value as “Payable for Floating Rate Note Obligations” in the Fund’s Statement of Assets and Liabilities. The face value of the TOB Floaters approximates their fair value of the floating rate notes. Interest income from the Underlying Securities are recorded by the Fund on an accrual basis. Interest expense incurred on the TOB Floaters and other expenses related to remarketing, administration and trustee services to a TOB Issuer are recognized as a component of “Interest expense and fees” in the Statement of Operations.

At November 30, 2024, the aggregate value of the Underlying Securities transferred to the TOB Issuer and the related liability for TOB Floaters were as follows:

Underlying

Securities Transferred

to TOB Issuers | Liability for

Floating Rate Note

Obligations |

| $216,021,541 | $153,690,000 |

During the six-month period ended November 30, 2024, the Fund's average TOB Floaters outstanding and the daily weighted average interest rate, including fees, were as follows:

Average

Floating Rate Note

Obligations Outstanding | Daily Weighted

Average

Interest Rate |

| $182,658,525 | 2.05% |

(H) Statement of Cash Flows. The cash amount shown in the Fund’s Statement of Cash Flows is the amount included in the Fund’s Statement of Assets and Liabilities and represents the cash on hand at its custodian and restricted cash, if any, as of November 30, 2024.

(I) Municipal Bond Risk. The Fund may invest more heavily in municipal bonds from certain cities, states, territories or regions than others, which may increase the Fund’s exposure to losses resulting from economic, political, regulatory occurrences, or declines in tax revenue impacting these particular cities, states, territories or regions. In addition, many state and municipal governments that issue securities are under significant economic and financial stress and may not be able to satisfy their obligations, and these events may be made worse in an adverse economic environment. The Fund may invest a substantial amount of its assets in municipal bonds whose interest is paid solely from revenues of similar projects, such as tobacco settlement bonds. If the Fund concentrates its investments in this manner, it assumes the legal and economic risks relating to such projects and this may have a significant impact on the Fund’s investment performance.

The Fund maintains exposures to the territory Puerto Rico as of November 30, 2024, that represent 13.8% of the Fund’s net assets, of which 28.6% are insured. Certain issuers in which the Fund may invest have experienced significant financial difficulties and the continuation or reoccurrence of these difficulties may impair their ability to service debt. As of November 30, 2024, the Puerto Rico Electric Power Authority (“PREPA”) remains in bankruptcy. The continued delay in resolving the PREPA bankruptcy could delay needed investment into public power generation and distribution assets, which are an essential component to a productive economy. Failure to provide reliable electricity could result in the Commonwealth’s inability to service debt on other municipal territorial investments the Fund does hold.

Despite significant challenges from the Covid pandemic and 2017 Irma and Maria hurricanes, Federal Covid and Hurricane Disaster relief funding have aided the Commonwealth economy. However, there is no guarantee that the Commonwealth will be able to continue to utilize remaining federal disaster recovery funding given labor and project management

Notes to Financial Statements (Unaudited) (continued)

challenges. Puerto Rico also faces longer term declining demographic trends, which could impair the ability for the territory to service its municipal debt obligations.

(J) Indemnifications. Under the Fund’s organizational documents, its officers and trustees are indemnified against certain liabilities that may arise out of performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts with third-party service providers that contain a variety of representations and warranties and that may provide general indemnifications. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. The Manager believes that the risk of loss in connection with these potential indemnification obligations is remote. However, there can be no assurance that material liabilities related to such obligations will not arise in the future, which could adversely impact the Fund.

Note 3–Fees and Related Party Transactions

(A) Manager and Subadvisor. New York Life Investments, a registered investment adviser and an indirect, wholly-owned subsidiary of New York Life Insurance Company ("New York Life"), serves as the Fund's Manager, pursuant to an Amended and Restated Management Agreement ("Management Agreement"). The Manager provides offices, conducts clerical, recordkeeping and bookkeeping services and keeps most of the financial and accounting records required to be maintained by the Fund. Except for the portion of salaries and expenses that are the responsibility of the Fund, the Manager pays the salaries and expenses of all personnel affiliated with the Fund and certain operational expenses of the Fund. The Fund reimburses New York Life Investments in an amount equal to the portion of the compensation of the Chief Compliance Officer attributable to the Fund. MacKay Shields LLC ("MacKay Shields" or the "Subadvisor"), a registered investment adviser and an indirect, wholly-owned subsidiary of New York Life, serves as the Subadvisor to the Fund and is responsible for the day-to-day portfolio management of the Fund. Pursuant to the terms of a Subadvisory Agreement ("Subadvisory Agreement") between New York Life Investments and MacKay Shields, New York Life Investments pays for the services of the Subadvisor.

Under the Management Agreement, the Fund pays the Manager a monthly fee for the services performed and the facilities furnished at an annual rate of 0.60% of the “Managed Assets”. Managed Assets is defined as the Fund’s total assets, minus the sum of its accrued liabilities (other than Fund liabilities incurred for the purpose of creating effective leverage (i.e. tender option bonds) or Fund liabilities related to liquidation preference of any Preferred shares issued).

During the six-month period ended November 30, 2024, New York Life Investments earned fees from the Fund in the amount of $1,967,188 and paid the Subadvisor in the amount of $983,594.

JPMorgan Chase Bank, N.A. ("JPMorgan") provides sub-administration and sub-accounting services to the Fund pursuant to an agreement with New York Life Investments. These services include calculating the daily

NAVs of the Fund, maintaining the general ledger and sub-ledger accounts for the calculation of the Fund's NAVs, and assisting New York Life Investments in conducting various aspects of the Fund's administrative operations. For providing these services to the Fund, JPMorgan is compensated by New York Life Investments.

Pursuant to an agreement between the Fund and New York Life Investments, New York Life Investments is responsible for providing or procuring certain regulatory reporting services for the Fund. The Fund will reimburse New York Life Investments for the actual costs incurred by New York Life Investments in connection with providing or procuring these services for the Fund.

(B) Transfer, Dividend Disbursing and Shareholder Servicing Agent. Computershare Trust Company, N.A. (“Computershare”), 150 Royall Street, Canton, Massachusetts, 02021, is the Fund’s transfer, dividend disbursing and shareholder servicing agent pursuant to an agreement between the Fund and Computershare.

Note 4-Federal Income Tax

As of November 30, 2024, the cost and unrealized appreciation (depreciation) of the Fund’s investment portfolio, including applicable derivative contracts and other financial instruments, as determined on a federal income tax basis, were as follows:

| | Federal Tax

Cost | Gross

Unrealized

Appreciation | Gross

Unrealized

(Depreciation) | Net

Unrealized

Appreciation/

(Depreciation) |

| Investments in Securities | $448,772,739 | $16,489,476 | $(735,068) | $15,754,408 |

As of May 31, 2024, for federal income tax purposes, capital loss carryforwards of $79,961,337, as shown in the table below, were available to the extent provided by the regulations to offset future realized gains of the Fund. Accordingly, no capital gains distributions are expected to be paid to shareholders until net gains have been realized in excess of such amounts.

Capital Loss

Available Through | Short-Term

Capital Loss

Amounts (000’s) | Long-Term

Capital Loss

Amounts (000’s) |

| Unlimited | $42,825 | $37,136 |

During the year ended May 31, 2024 the tax character of distributions paid to Common shareholders (as reflected in the Statements of Changes in Net Assets) was as follows:

| | 2024 | |

| Distributions paid from: | Ordinary

Income | Exempt

Interest

Dividends |

| Common shares | $332,587 | $21,027,801 |

| 22 | NYLI MacKay DefinedTerm Muni Opportunities Fund |

Note 5–Custodian

JPMorgan is the custodian of cash and securities held by the Fund. Custodial fees are charged to the Fund based on the Fund's net assets and/or the market value of securities held by the Fund and the number of certain transactions incurred by the Fund.

Note 6–Purchases and Sales of Securities (in 000’s)

During the six-month period ended November 30, 2024, purchases and sales of securities, other than short-term securities, were $79,619 and $272,764, respectively.

Note 7–Capital Share Transactions

Transactions in capital shares for the six-month period ended November 30, 2024 and the year ended May 31, 2024, were as follows:

| Common Shares | Shares | Amount |

| Six months ended November 30, 2024: | | |

Shares repurchased and retired through

tender offer (a) | (9,147,341) | $(154,509,566) |

| Year ended May 31, 2024: | | |

| Shares issued to shareholders in reinvestment of distributions (b) | 18,793 | $ 311,212 |

| (a) | Tender offer price on expiration date November 14, 2024, was $16.89 per Common share and represented approximately 32.8% of the Fund's Common shares outstanding. |

| (b) | See Note 2(C) for information on the Fund’s dividend reinvestment plan. |

Note 8–Subsequent Events

In connection with the preparation of the financial statements of the Fund for the six-month period ended November 30, 2024, events and transactions subsequent to November 30, 2024, through the date the financial statements were issued have been evaluated by the Manager for possible adjustment and/or disclosure. No subsequent events requiring financial statement adjustment or disclosure have been identified, other than the following:

On December 2, 2024, the Fund declared a dividend in the amount of $0.06 per Common share, payable on December 31, 2024, to shareholders of record on December 16, 2024.

On January 2, 2025, the Fund declared a dividend in the amount of $0.06 per Common share, payable on January 31, 2025, to shareholders of record on January 15, 2025.

Dividend Reinvestment Plan (Unaudited)

Pursuant to the Fund’s Dividend Reinvestment Plan (the “Plan”) shareholders whose shares are registered in their own name may “opt-in” to the Plan and elect to reinvest all or a portion of their distributions in the Common shares by providing the required enrollment notice to Computershare Trust Company, N.A., the Plan Administrator (“Plan Administrator”). Shareholders whose shares are held in the name of a broker or other nominee may have distributions reinvested only if such a service is provided by the broker or the nominee or if the broker or the nominee permits participation in the Plan. Shareholders whose shares are held in the name of a broker or other nominee should contact the broker or nominee for details. A shareholder may terminate participation in the Plan at any time by notifying the Plan Administrator before the record date of the next distribution through the Internet, by telephone or in writing. All distributions to shareholders who do not participate in the Plan, or have elected to terminate their participation in the Plan, will be paid by check mailed directly to the record holder by or under the direction of the Plan Administrator when the Fund declares a distribution.