UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

| | | | |

x Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the Fiscal Year Ended December 31, 2014 |

| or | | | | |

¨ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission File Number: 333-185443

_________________________________________

Aleris Corporation

(Exact name of registrant as specified in its charter)

__________________________________________

|

| | | | |

| Delaware | | 27-1539594 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

25825 Science Park Drive, Suite 400

Cleveland, Ohio 44122-7392

(Address of principal executive offices) (Zip code)

(216) 910-3400

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: None

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

______________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes x No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

(Note: Registrant is a voluntary filer of reports required to be filed by certain companies under Sections 13 and 15(d) of the Securities Exchange Act of 1934 and has filed all reports that would have been required during the preceding 12 months, had it been subject to such filing requirements.)

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer¨ Non-accelerated filer x Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The registrant is a privately held corporation. As of June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, there was no established public trading market for the common stock of the registrant and therefore, an aggregate market value of the registrant’s common stock is not determinable.

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes x No¨

There were 31,357,493 shares of the registrant’s common stock, par value $0.01 per share, outstanding as of March 6, 2015.

DOCUMENTS INCORPORATED BY REFERENCE: None

|

| | |

| PART I | | Page |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| PART II | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | | |

| PART III | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| PART IV | | |

| Item 15. | | |

| | | |

| Signatures | | |

PART I

ITEM 1. BUSINESS.

General

Aleris Corporation is a Delaware corporation with its principal executive offices located in Cleveland, Ohio. We are a holding company and currently conduct our business and operations through our direct wholly owned subsidiary, Aleris International, Inc. and its consolidated subsidiaries. As used in this annual report on Form 10-K, unless otherwise specified or the context otherwise requires, “Aleris,” “we,” “our,” “us,” and the “Company” refer to Aleris Corporation and its consolidated subsidiaries. Aleris International, Inc. is referred to herein as “Aleris International.”

The Company is majority owned by Oaktree Capital Management, L.P. (“Oaktree”) or its respective subsidiaries. The investment funds managed by Oaktree or its respective subsidiaries that are invested in the Company are referred to collectively as the “Oaktree Funds.”

On February 27, 2015, we finalized the sale of our North American and European recycling and specification alloys businesses to Signature Group Holdings (“Signature”) and certain of its affiliates. These businesses include substantially all of the operations and assets previously reported in our Recycling and Specification Alloys North America (“RSAA”) and Recycling and Specification Alloys Europe (“RSEU”) segments. The sale includes 18 production facilities in North America and six in Europe.

On March 1, 2015, we finalized the sale of our Extrusions business to Sankyo Tateyama (“Sankyo”), a Japanese building products and extrusions manufacturer to sell our extrusions business. This business includes substantially all of the operations and assets previously reported in our Extrusions segment.

We have reported the recycling and specification alloys and extrusions businesses as discontinued operations for all periods presented, and reclassified the results of operations of these businesses into a single caption on the accompanying Consolidated Statements of Operations as “Income from discontinued operations, net of tax.” For additional information, see Note 18, “Discontinued Operations,” to our audited consolidated financial statements included elsewhere in this annual report on Form 10-K. Except as otherwise indicated, the discussion of the Company’s business and financial information throughout this annual report on Form 10-K refers to the Company’s continuing operations and the financial position and results of operations of its continuing operations, while the presentation and discussion of our cash flows reflects the combined cash flows from our continuing and discontinued operations.

Our segment disclosures exclude the previously reported RSAA, RSEU and Extrusions reportable segments for the years ended December 31, 2014, 2013 and 2012. Further, as our remaining operations consist solely of rolled products segments, our Rolled Products North America, Rolled Products Europe and Rolled Products Asia Pacific segments have been renamed to North America, Europe and Asia Pacific, respectively.

We make available on or through our website (www.aleris.com) our reports on Forms 10-K, 10-Q and 8-K, and amendments thereto, as soon as reasonably practicable after we electronically file (or furnish, as applicable) such material with the Securities and Exchange Commission (“SEC”). The SEC maintains an internet site that contains these reports at www.sec.gov. None of the websites referenced in this annual report on Form 10-K or the information contained therein is incorporated herein by reference.

Company Overview

We are a global leader in the manufacture and sale of aluminum rolled products, with 13 production facilities located throughout North America, Europe and China. Our business model strives to reduce the impact of aluminum price fluctuations on our financial results and protect and stabilize our margins, principally through pass-through pricing (market-based aluminum price plus a conversion fee) and derivative financial instruments. We possess a combination of low-cost, flexible and technically advanced manufacturing operations supported by an industry-leading research and development platform. Our facilities are strategically located to service our customers, which include a number of the world’s largest companies in the aerospace, automotive, transportation, building and construction, containers and packaging and metal distribution industries. For the year ended December 31, 2014, we generated revenues of $2.9 billion, of which approximately 58% were derived from North America, 34% were derived from Europe and the remaining 8% were derived from the rest of the world.

Company History

The Predecessor, as defined in Item 6. – “Selected Financial Data,” was formed at the end of 2004 through the merger of Commonwealth Industries, Inc. and IMCO Recycling, Inc. The Predecessor’s business grew through a combination of organic growth and strategic acquisitions, the most significant of which was the 2006 acquisition of the downstream aluminum business

of Corus Group plc (“Corus Aluminum”). The Corus Aluminum acquisition doubled its size and significantly expanded both its presence in Europe and its ability to manufacture higher value-added products, including aerospace and auto body sheet.

The Predecessor was acquired by Texas Pacific Group (“TPG”) in December 2006 and taken private. In 2007, it sold its zinc business in order to focus on its core aluminum business.

In 2009, the Predecessor, along with certain of its U.S. subsidiaries, filed voluntary petitions for Chapter 11 bankruptcy protection in the United States Bankruptcy Court for the District of Delaware. The bankruptcy filings were the result of a liquidity crisis brought on by the global recession and financial crisis. The Predecessor’s ability to respond to the liquidity crisis was constrained by its highly leveraged capital structure, which at filing included $2.7 billion of debt, resulting from the 2006 leveraged buyout of the Predecessor by TPG. As a result of the severe economic decline, the Predecessor experienced sudden and significant value reductions across each end-use industry it served and a precipitous decline in the London Metal Exchange (“LME”) price of aluminum. These factors reduced the availability of financing under the Predecessor’s revolving credit facility and required the posting of cash collateral on aluminum hedges. The Predecessor sought bankruptcy protection to alleviate its liquidity constraints and restructure its operations and financial position.

The Company was formed as a Delaware corporation in 2009 to acquire the assets and operations of the Predecessor upon emergence from bankruptcy. On June 1, 2010 (the “Emergence Date”), Aleris International emerged from Chapter 11 bankruptcy protection. TPG exited our business during this time and we received significant support from new equity investors, led by the Oaktree Funds, the majority owner of Aleris Corporation, as well as certain investment funds managed by affiliates of Apollo Management Holdings, L.P. (“Apollo”) and Sankaty Advisors, LLC (“Sankaty” and, together with the Oaktree Funds and Apollo, the “Investors”).

Business Segments

We report three operating segments based on the organizational structure that we use to evaluate performance, make decisions on resource allocations and perform business reviews of financial results. The Company’s operating segments (each of which is considered a reportable segment) are North America, Europe and Asia Pacific.

In addition to these reportable segments, we disclose corporate and other unallocated amounts, including the start-up expenses of Asia Pacific.

See Note 15, “Segment and Geographic Information,” to our audited consolidated financial statements included elsewhere in this annual report on Form 10-K for financial and geographic information about our segments.

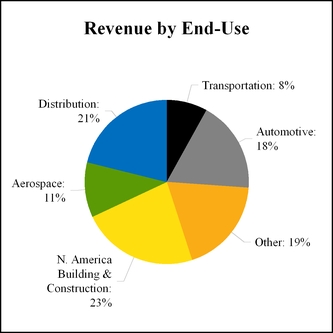

The following charts present the percentage of our consolidated revenue from continuing operations by reportable segment and by end-use for the year ended December 31, 2014:

North America

Our North America segment consists of nine manufacturing facilities located throughout the United States that produce rolled aluminum and coated products. Our North America segment produces rolled products for a wide variety of applications, including building and construction, distribution, transportation, automotive and other uses in the consumer durables general industrial segments. Except for depot sales, which are for standard size products, substantially all of our rolled aluminum products are manufactured to specific customer requirements, using direct-chill, continuous cast technologies that allow us to use and offer a variety of alloys and products for a number of end-uses. Specifically, those products are integrated into, among other applications, building products, truck trailers, gutters, appliances, cars and recreational vehicles.

We believe that many of our facilities are low cost, flexible and allow us to maximize our use of scrap with proprietary manufacturing processes providing us with a competitive advantage. Our rolling mills have the flexibility to use primary or scrap aluminum, which allows us to optimize input costs and maximize margins. For the year ended December 31, 2014, approximately 97% of our revenues were derived utilizing a formula pricing model which allows us to pass through risks from the volatility of aluminum price changes by charging a market-based aluminum price plus a conversion fee and we strive to manage the remaining key commodity risks through our hedging programs.

Our North America segment produces rolled aluminum products ranging from thickness (gauge) of 0.002 to 0.249 inches in widths of up to 72 inches. The following table summarizes our North America segment’s principal products and services, end-uses, major customers and competitors:

|

| | |

| Principal end use/product category | Major customers | Competitors |

| |

| • Building and construction (roofing, rainware and siding) | • American Construction Metals, Kaycan, Midwest Metals, Ply Gem Industries, Gentek Building Products, Rollex | • Jupiter Aluminum, JW Aluminum, Alcoa, Vulcan |

| • Metal distribution | • Ryerson, Thyssen-Krupp, Samuel & Son, Champagne Metals | • Alcoa, Novelis, Constellium, Empire, Ta-Chen, Asian-American, Metal Exchange |

• Transportation equipment (truck

trailers and bodies) | • Great Dane, Utility Trailer, Aluminum Line, Hyundai Translead | • Alcoa, Novelis, JW Aluminum |

• Consumer durables, specialty coil and sheet (cookware, fuel tanks, ventilation, cooling and

lamp bases) | • Brunswick Boat Group, ABB, Grimco, Cuprum Metales Laminados | • Alcoa, Novelis, Noranda, Skana Aluminum, Constellium |

| • Converter foil, fins and tray materials | • HFA, Reynolds, D&W Fine Pack | • JW Aluminum, Noranda, Novelis, Skana Aluminum, SAPA |

The following table presents segment metric tons shipped, segment revenues, segment commercial margin, segment income and segment Adjusted EBITDA for the years ended December 31, 2014, 2013 and 2012 for our North America segment:

|

| | | | | | | | | | | | |

| North America | | |

| (Dollars in millions, except per ton measures, | | For the years ended December 31, |

| volumes in thousands of tons) | | 2014 | | 2013 | | 2012 |

| Segment metric tons shipped | | 482.0 |

| | 372.3 |

| | 395.7 |

|

| Segment revenues | | $ | 1,561.8 |

| | $ | 1,194.8 |

| | $ | 1,299.7 |

|

| Segment commercial margin (1) | | $ | 569.0 |

| | $ | 447.2 |

| | $ | 479.3 |

|

| Segment commercial margin per ton shipped | | $ | 1,180.4 |

| | $ | 1,201.3 |

| | $ | 1,211.1 |

|

| Segment income | | $ | 94.6 |

| | $ | 81.8 |

| | $ | 117.6 |

|

| Segment Adjusted EBITDA (1) | | $ | 96.0 |

| | $ | 76.2 |

| | $ | 111.1 |

|

| Segment Adjusted EBITDA per ton shipped | | $ | 199.1 |

| | $ | 204.6 |

| | $ | 280.9 |

|

| Total segment assets | | $ | 790.9 |

| | $ | 524.7 |

| | |

(1) Segment commercial margin and segment Adjusted EBITDA are non-GAAP financial measures. See Item 7. – “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Our Segments” for a definition and discussion of segment commercial margin and segment Adjusted EBITDA and reconciliations to revenues and segment income, respectively.

Europe

Our Europe segment consists of two rolled aluminum products manufacturing facilities, located in Germany and Belgium, as well as an aluminum casting plant in Germany that produces rolling slab used by our Europe operations. Our Europe segment produces rolled products for a wide variety of technically sophisticated applications, including aerospace plate and sheet, brazing sheet (clad aluminum material used for, among other applications, vehicle radiators and HVAC systems), automotive sheet, and heat treated plate for engineering uses, as well as for other uses in the transportation, construction and packaging industries. Substantially all of our products are manufactured to specific customer requirements using direct-chill ingot cast technologies that allow us to use and offer a variety of alloys and products for a number of technically demanding end-uses.

Our Europe segment remelts primary ingots, internal scrap, purchased scrap and master alloys to produce rolled aluminum products ranging from thickness (gauge) of 0.00031 to 11.0 inches in widths of up to 138 inches. The following table summarizes our Europe segment’s principal products and services, end-uses, major customers and competitors:

|

| | |

| Principal end use/product category | Major customers | Competitors |

| |

| • Aircraft plate and sheet | • Airbus, Boeing, Bombardier,

Embraer, Dassault | • Alcoa, Constellium, Kaiser, AMAG |

| • Automotive body sheet (inner, outer and structural parts) | • VW Group, BMW, Daimler, Renault, Volvo | • Constellium, Novelis, Hydro, AMAG |

| • Brazing coil (heat exchanger materials for automotive and general industrial) | • Behr, Dana, HallaVisteon, Denso, Modine Chart | • Alcoa, Hydro, Gränges, AMAG, UACJ |

| • Industrial plate and sheet (tooling, molding, road & rail, shipbuilding, LNG, silos, anodizing qualities for architecture, multi-layer tubing, and general industry) | • Amari Group, Amco, ThyssenKrupp Materials, Euramax, Henco, Gilette, SAG, Linde, Multivac, RemiClaeys | • Alcoa, AMAG, Constellium, Hydro, Novelis |

The following table presents segment metric tons shipped, segment revenues, segment commercial margin, segment income and segment Adjusted EBITDA for the years ended December 31, 2014, 2013 and 2012 for our Europe segment:

|

| | | | | | | | | | | | |

| Europe | | |

| (Dollars in millions, except per ton measures, | | For the years ended December 31, |

| volumes in thousands of tons) | | 2014 | | 2013 | | 2012 |

| Segment metric tons shipped | | 334.9 |

| | 345.4 |

| | 298.9 |

|

| Segment revenues | | $ | 1,402.4 |

| | $ | 1,443.2 |

| | $ | 1,324.9 |

|

| Segment commercial margin (1) | | $ | 597.6 |

| | $ | 605.2 |

| | $ | 570.7 |

|

| Segment commercial margin per ton shipped | | $ | 1,784.6 |

| | $ | 1,752.2 |

| | $ | 1,909.5 |

|

| Segment income | | $ | 147.6 |

| | $ | 132.1 |

| | $ | 144.6 |

|

| Segment Adjusted EBITDA (1) | | $ | 120.7 |

| | $ | 115.3 |

| | $ | 136.7 |

|

| Segment Adjusted EBITDA per ton shipped | | $ | 360.5 |

| | $ | 333.9 |

| | $ | 457.4 |

|

| Total segment assets | | $ | 701.9 |

| | $ | 699.2 |

| | |

(1) Segment commercial margin and segment Adjusted EBITDA are non-GAAP financial measures. See Item 7. – “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Our Segments” for a definition and discussion of segment commercial margin and segment Adjusted EBITDA and reconciliations to revenues and segment income, respectively.

Asia Pacific

Our Asia Pacific segment consists of a state-of-the-art aluminum rolling mill in China (the “Zhenjiang rolling mill”), that produces value-added plate products for the aerospace, engineering, distribution, building and construction, and other transportation industry segments worldwide. We designed the mill with the capability to expand into other high value-added products with a wide variety of technically sophisticated applications. Construction of the mill was substantially complete in 2012 and limited production began in 2013. The mill continued to incur start-up expenses in 2014 as we increased volume to full production and obtained qualifications from our major aerospace customers. These start-up expenses represent operating losses incurred while the mill ramped up production, as well as expenses associated with obtaining certification to produce aircraft plate. Substantially all of our products are manufactured to specific customer requirements using direct-chill ingot cast technologies that allow us to use and offer a variety of alloys and products for a number of technically demanding end-uses. Segment loss and segment Adjusted EBITDA exclude start-up operating losses and expenses, as well as depreciation expense during the start-up period.

The following table summarizes our Asia Pacific segment’s principal products and services, end-uses, major customers and competitors:

|

| | |

| Principal end use/product category | Major customers | Competitors |

| |

| • Aircraft plate | • Avic, KAI, AMS | • Alcoa, Constellium, Chinalco, Kaiser |

| • Heat treated plate | • Hengtai, Avic, ThyssenKrupp | • Kumz, Alnan, UACJ |

| • Non heat treated plate | • Hengtai, Avic, ThyssenKrupp | • Kumz, Alnan, UACJ |

The following table presents segment metric tons shipped, segment revenues, segment commercial margin, segment loss and segment Adjusted EBITDA for the years ended December 31, 2014, 2013 and 2012 for our Asia Pacific segment:

|

| | | | | | | | |

| Asia Pacific | | |

| (Dollars in millions, except per ton measures, | | For the years ended December 31, |

| volumes in thousands of tons) | | 2014 | | 2013 |

| Segment metric tons shipped | | 12.8 |

| | 4.8 |

|

| Segment revenues | | $ | 52.7 |

| | $ | 20.7 |

|

| Segment commercial margin (1) | | $ | — |

| | $ | (0.3 | ) |

| Segment loss (2) | | $ | — |

| | $ | (0.2 | ) |

| Segment Adjusted EBITDA (1) (2) | | $ | — |

| | $ | (0.2 | ) |

| Total segment assets | | $ | 433.3 |

| | $ | 439.4 |

|

(1) Segment commercial margin and segment Adjusted EBITDA are non-GAAP financial measures. See Item 7. – “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Our Segments” for a definition and discussion of segment commercial margin and segment Adjusted EBITDA and reconciliations to revenues and segment income, respectively.

(2) Segment loss and segment Adjusted EBITDA exclude start-up operating losses and expenses, as well as depreciation expense during the start-up period. For the years ended December 31, 2014 and 2013, start-up expenses were $16.6 million and $31.6 million, respectively, and total depreciation expenses were $24.7 million and $17.2 million, respectively.

Industry Overview

Aluminum is a widely-used, attractive industrial material. Compared to several alternative metals such as steel and copper, aluminum is lightweight, has a high strength-to-weight ratio and is resistant to corrosion. Aluminum can be recycled repeatedly without any material decline in performance or quality. The recycling of aluminum delivers energy and capital investment savings relative to both the cost of producing primary aluminum and many other competing materials. The penetration of aluminum into a wide variety of applications continues to grow. We believe several factors support fundamental long-term growth in aluminum consumption generally and demand for those products we produce specifically, including urbanization in emerging economies, economic recovery in developed economies and an increasing global focus on sustainability.

The global aluminum industry consists of primary aluminum producers with bauxite mining, alumina refining and aluminum smelting capabilities; aluminum semi-fabricated products manufacturers, including aluminum casters, recyclers, extruders and flat rolled products producers; and integrated companies that are present across multiple stages of the aluminum production chain. The industry is cyclical and is affected by global economic conditions, industry competition and product development.

Primary aluminum prices are determined by worldwide forces of supply and demand and, as a result, are volatile. This volatility has a significant impact on the profitability of primary aluminum producers whose selling prices are typically based upon prevailing LME prices while their costs to manufacture are not highly correlated to LME prices. We participate in select segments of the aluminum fabricated products industry. We do not smelt aluminum, nor do we participate in other upstream activities, including mining bauxite or refining alumina. Since the majority of our products are sold on a market-based aluminum price plus conversion fee basis, we are less exposed to aluminum price volatility.

Sales and Marketing

Our products are sold to end-users, as well as to distributors, principally for use in the aerospace, automotive, transportation, building and construction, electrical, mechanical engineering, metal distribution and packaging industries. Backlog as of December 31, 2014 and 2013 was approximately $154.4 million and $79.9 million for North America and $265.2 million and $212.6 million for Europe.

Sales of rolled products are made through each segment’s own sales force, which are strategically located to provide international coverage, and through a broad network of sales offices and agents in North America, major European countries, as well as Asia and Australia. The majority of our customer sales agreements in these segments are for a term of one year or less.

Competition

The worldwide aluminum industry is highly competitive. Aluminum competes with other materials such as steel, plastic, composite materials and glass for various applications.

We compete in the production and sale of rolled aluminum sheet and plate. In the sectors in which we compete, the other industry leaders include Alcoa, Constellium, Novelis, Kaiser, Hydro, JW Aluminum and Jupiter Aluminum. In addition, we compete with imported products. We compete with other rolled products suppliers on the basis of quality, price, timeliness of delivery and customer service.

Raw Materials and Supplies

A significant portion of the aluminum metal used by our North America segment is purchased aluminum scrap that is acquired from aluminum scrap dealers or brokers. We believe that this segment is one of the largest users of aluminum scrap (other than beverage can scrap) in North America. The remaining requirements of this segment are met with purchased primary metal, including metal produced in the U.S. and internationally.

Our Europe segment relies on a number of European smelters for primary aluminum and rolling slab. Due to a shortage of internal slab casting capacity, we contract with smelters and other third parties to provide slab that meets our specifications.

Our Asia Pacific segment relies primarily on domestic smelters for primary aluminum. A portion of the raw material used by this segment is imported in order to meet quality requirements.

Energy Supplies

Our operations are fueled by natural gas and electricity, which represent the third largest component of our cost of sales, after metal and labor costs. We purchase the majority of our natural gas and electricity on a spot-market basis. However, in an effort to acquire the most favorable energy costs, we have secured some of our natural gas and electricity at fixed price commitments. We use forward contracts and options, as well as contractual price escalators, to reduce the risks associated with our natural gas requirements.

Research and Development

Our research and development organization includes three locations in Europe, one in Asia, and will include one in North America, with a support staff focused on new product and alloy offerings and process performance technology. Research and development expenses were $12.9 million, $12.4 million and $7.3 million for the years ended December 31, 2014, 2013 and 2012, respectively.

Patents and Other Intellectual Property

We hold patents registered in the United States and other countries relating to our business. In addition to patents, we also possess other intellectual property, including trademarks, tradenames, know-how, developed technology and trade secrets. Although we believe these intellectual property rights are important to the operations of our specific businesses, we do not consider any single patent, trademark, tradename, know-how, developed technology, trade secret or any group of patents, trademarks, tradenames, know-how, developed technology or trade secrets to be material to our business as a whole.

Seasonality

Certain of our products are seasonal. Demand in the rolled products business is generally stronger in the spring and summer seasons due to higher demand in the building and construction industry. This typically results in higher operating income in our second and third quarters, followed by our first and fourth quarters.

Employees

We had a total of approximately 5,100 employees, which includes approximately 1,700 employees engaged in administrative and supervisory activities and approximately 3,400 employees engaged in manufacturing, production and maintenance functions. In addition, collectively, approximately 65% of our U.S. employees and substantially all of our non-U.S. employees are covered by collective bargaining agreements. We believe our labor relations with employees have been satisfactory.

Environmental

Our operations are subject to federal, state, local and foreign environmental laws and regulations, which govern, among other things, air emissions, wastewater discharges, the handling, storage, and disposal of hazardous substances and wastes, the investigation or remediation of contaminated sites, and employee health and safety. These laws can impose joint and several liability for releases or threatened releases of hazardous substances upon statutorily defined parties, including us, regardless of

fault or the lawfulness of the original activity or disposal. Given the changing nature of environmental legal requirements, we may be required, from time to time, to install additional pollution control equipment, make process changes, or take other environmental control measures at some of our facilities to meet future requirements.

We have been named as a potentially responsible party in certain proceedings initiated pursuant to the Comprehensive Environmental Response, Compensation, and Liability Act (“Superfund”) and similar state statutes and may be named a potentially responsible party in other similar proceedings in the future. It is not anticipated that the costs incurred in connection with the presently pending proceedings will, individually or in the aggregate, have a material adverse effect on our financial condition or results of operations. Currently, and from time to time, we are a party to notices of violation brought by environmental agencies concerning the laws governing air emissions.

We are performing operations and maintenance at two Superfund sites for matters arising out of past waste disposal activity associated with closed facilities. We are also under orders to perform environmental remediation by agencies in four states and one non-U.S. country at seven sites.

Our aggregate accrual for environmental matters related to continuing operations was $24.4 million and $14.0 million at December 31, 2014 and 2013, respectively. Of these amounts, approximately $15.0 million and $6.3 million are indemnified at December 31, 2014 and 2013, respectively. Although the outcome of any such matters, to the extent they exceed any applicable accrual, could have a material adverse effect on our consolidated results of operations or cash flows for the applicable period, we currently believe that any such outcome would not have a material adverse effect on our consolidated financial condition, results of operations or cash flows.

In addition, we have asset retirement obligations related to continuing operations of $4.6 million and $4.1 million at December 31, 2014 and 2013, respectively, for costs related to the future removal of asbestos and costs to remove underground storage tanks. The related asset retirement costs are capitalized as long-lived assets (asset retirement cost), and are being amortized over the remaining useful life of the related asset. See Note 2, “Summary of Significant Accounting Policies,” and Note 8, “Asset Retirement Obligations,” to our audited consolidated financial statements included elsewhere in this annual report on Form 10-K.

The processing of scrap generates solid waste in the form of salt cake and baghouse dust. This material is disposed of at off-site landfills. If salt cake was ever classified as a hazardous waste in the U.S., the costs to manage and dispose of it would increase, which could result in significant increased expenditures.

Financial Information About Geographic Areas

See Note 15, “Segment and Geographic Information,” to our audited consolidated financial statements included elsewhere in this annual report on Form 10-K.

Our Bankruptcy

Any references in this annual report on Form 10-K to “our bankruptcy,” “our reorganization,” “our emergence from bankruptcy” or similar terms or phrases refer to the bankruptcy and reorganization of Aleris International as described in Item 6. – “Selected Financial Data.”

ITEM 1A. RISK FACTORS.

Risks Related to our Business

If we fail to implement our business strategy, our financial condition and results of operations could be adversely affected.

Our future financial performance and success depend in large part on our ability to successfully implement our business strategy. We cannot assure you that we will be able to successfully implement our business strategy or be able to continue improving our operating results. In particular, we cannot assure you that we will be able to achieve all operating cost savings targeted through focused productivity improvements and capacity optimization, further enhancements of our business and product mix, expansion in selected international regions, opportunistic pursuit of strategic acquisitions and management of key commodity exposures.

Furthermore, we cannot assure you that we will be successful in our growth efforts or that we will be able to effectively manage expanded or acquired operations. Our ability to achieve our expansion and acquisition objectives and to effectively manage our growth depends on a number of factors, such as our ability to introduce new products and end-use applications, increased competition, legal and regulatory developments, general economic conditions or an increase in operating costs. Any failure to successfully implement our business strategy could adversely affect our financial condition and results of operations. We may, in addition, decide to alter or discontinue certain aspects of our business strategy at any time.

Past and future acquisitions or divestitures may not be successful, which could adversely affect our financial condition.

As part of our strategy, we may continue to pursue acquisitions or strategic alliances, which may not be completed or, if completed, may not be ultimately beneficial to us. We also consider potential divestitures of non-strategic businesses from time to time. We prudently evaluate these opportunities as potential enhancements to our existing operating platforms and continue to consider strategic alternatives on an ongoing basis, including having discussions concerning potential acquisitions and divestitures that may be material.

There are numerous risks commonly encountered in business combinations, including the following:

| |

| ▪ | our ability to identify appropriate acquisition targets and to negotiate acceptable terms for their acquisition; |

| |

| ▪ | our ability to integrate new businesses into our operations; |

| |

| ▪ | the availability of capital on acceptable terms to finance acquisitions; |

| |

| ▪ | the ability to generate the cost savings or synergies anticipated; |

| |

| ▪ | the inaccurate assessment of undisclosed liabilities; |

| |

| ▪ | increasing demands on our operational systems; and |

| |

| ▪ | the amortization of acquired intangible assets. |

In addition, the process of integrating new businesses could cause the interruption of, or loss of momentum in, the activities of our existing businesses and the diversion of management’s attention. Any delays or difficulties encountered in connection with the integration of new businesses or divestiture of existing businesses could negatively impact our business and results of operations. Furthermore, any acquisition we may make could result in significant increases in our outstanding indebtedness and debt service requirements. The terms of our indebtedness may limit the acquisitions we can pursue.

There are numerous risks commonly encountered in divestitures, including the following:

| |

| ▪ | diversion of resources and management’s attention from the operation of our business, including providing on-going services to the divested business; |

| |

| ▪ | loss of key employees following such a transaction; |

| |

| ▪ | difficulties in the separation of operations, services, products and personnel; |

| |

| ▪ | retention of future liabilities as a result of contractual indemnity obligations; and |

| |

| ▪ | damage to our existing customer, supplier and other business relationships. |

In addition, sellers typically retain certain liabilities or indemnify buyers for certain matters such as lawsuits, tax liabilities, product liability claims and environmental matters. The magnitude of any such retained liability or indemnification obligation may be difficult to quantify at the time of the transaction, may involve conditions outside our control and ultimately may be material. Also, as is typical in divestiture transactions, third parties may be unwilling to release us from guarantees or other credit support provided prior to the sale of the divested assets. As a result, after a divestiture, we may remain secondarily liable for the obligations guaranteed or supported to the extent that the buyer of the assets fails to perform these obligations.

There can be no assurance that we will realize any anticipated benefits from any such acquisition or divestiture. If we do not realize any such anticipated benefits, our financial condition and results of operations could be materially adversely affected.

The cyclical nature of the metals industry, our end-use segments and our customers’ industries could limit our operating flexibility, which could negatively affect our financial condition and results of operations.

The metals industry in general is cyclical in nature. It tends to reflect and be amplified by changes in general and local economic conditions. These conditions include the level of economic growth, financing availability, the availability of affordable raw materials and energy sources, employment levels, interest rates, consumer confidence and housing demand. Historically, in periods of recession or periods of minimal economic growth, metals companies have often tended to underperform other sectors. We are particularly sensitive to trends in the transportation and building and construction industries, which are both seasonal, highly cyclical and dependent upon general economic conditions. For example, during recessions or periods of low growth, the transportation and building and construction industries typically experience major cutbacks in production, resulting in decreased demand for aluminum. This leads to significant fluctuations in demand and pricing for our products and services.

In addition, we derive a significant portion of our revenues from products sold to the aerospace industry, which is highly cyclical and tends to decline in response to overall declines in the general economy. The commercial aerospace industry is historically driven by demand from commercial airlines for new aircraft. Demand for commercial aircraft is influenced by airline industry profitability, trends in airline passenger traffic, the state of the U.S. and global economies and numerous other factors, including the effects of terrorism. A number of major airlines have undergone Chapter 11 bankruptcy or comparable

insolvency proceedings and experienced financial strain from volatile fuel prices. Despite existing backlogs, continued financial uncertainty in the industry, inadequate liquidity of certain airline companies, production issues and delays in the launch of new aircraft programs at major aircraft manufacturers, stock variations in the supply chain, terrorist acts or the increased threat of terrorism may lead to reduced demand for new aircraft that utilize our products, which could materially adversely affect our financial condition and results of operations.

Further, the demand for our automotive products is dependent on the production of cars, light trucks and heavy duty vehicles and trailers. The automotive industry is highly cyclical, as new vehicle demand is dependent on consumer spending and is tied closely to the strength of the overall economy. Production cuts by manufacturers may adversely affect the demand for our products. Many automotive related manufacturers and first tier suppliers are burdened with substantial structural costs, including pension, healthcare and labor costs that have resulted in severe financial difficulty, including bankruptcy, for several of them. A worsening of these companies’ financial condition or their bankruptcy could have further serious effects on the conditions of the markets, which directly affects the demand for our products. In addition, the loss of business with respect to, or a lack of commercial success of, one or more particular vehicle models for which we are a significant supplier could have a materially adverse impact on our financial condition and results of operations.

Because we generally have high fixed costs, our near-term profitability is significantly affected by decreased processing volume. Accordingly, reduced demand and pricing pressures may significantly reduce our profitability and adversely affect our financial condition. Economic downturns in regional and global economies or a prolonged recession in our principal industry segments have had a negative impact on our operations in the past and could have a negative impact on our future financial condition or results of operations. In addition, in recent years global economic and commodity trends have been increasingly correlated. Although we continue to seek to diversify our business on a geographic and industry end-use basis, we cannot assure you that diversification will significantly mitigate the effect of cyclical downturns.

Changes in the market price of aluminum impact the selling prices of our products and the benefit we gain from using scrap in our manufacturing process. Market prices of aluminum are dependent upon supply and demand and a variety of factors over which we have minimal or no control, including:

| |

| ▪ | regional and global economic conditions; |

| |

| ▪ | availability and relative pricing of metal substitutes; |

| |

| ▪ | environmental and conservation regulations; |

| |

| ▪ | seasonal factors and weather; and |

| |

| ▪ | import and export levels and/or restrictions. |

We may be unable to manage effectively our exposure to commodity price fluctuations, and our hedging activities may affect profitability in a changing metals price environment and subject our earnings to greater volatility from period-to-period.

Significant increases in the price of primary aluminum, aluminum scrap, alloys, hardeners, or energy would cause our cost of sales to increase significantly and, if not offset by product price increases, would negatively affect our financial condition and results of operations. We are substantial consumers of raw materials, and by far the largest input cost in producing our goods is the cost of aluminum. The cost of energy used by us is also substantial. Customers pay for our products based on the price of the aluminum contained in the products, plus a “rolling margin” or “conversion margin” fee (the “Price Margin”), or based on a fixed price. In general, we use this pricing mechanism to pass changes in the price of aluminum, and, sometimes, in the price of natural gas, through to our customers. In most end-uses and by industry convention, however, we offer our products at times on a fixed price basis as a service to the customer. This commitment to supply an aluminum-based product to a customer at a fixed price often extends months, but sometimes years, into the future. Such commitments require us to purchase raw materials in the future, exposing us to the risk that increased aluminum or natural gas prices will increase the cost of our products, thereby reducing or eliminating the Price Margin we receive when we deliver the product. These risks may be exacerbated by the failure of our customers to pay for products on a timely basis, or at all.

Furthermore, the North America and Europe segments are exposed to variability in the market price of a premium differential (referred to as “Midwest Premium” in the U.S. and “Duty Paid/Unpaid Rotterdam” in Europe) charged by industry participants to deliver aluminum from the smelter to the manufacturing facility. This premium differential also fluctuates in relation to several conditions, including the extent of warehouse financing transactions, which limit the amount of physical metal flowing to consumers and increases the price differential as a result. We have been experiencing greater volatility in the premium, which can also increase the variability in our earnings. In addition to impacting the price we pay for the raw materials we purchase, changing premium differentials impact our customers, who may delay purchases from us during times of uncertainty with respect to the premium differential or seek to purchase lower priced imported products which are not susceptible to the changes in these premium differentials. The North America and Europe segments follow a pattern of

increasing or decreasing their selling prices to customers in response to changes in the Midwest Premium and the Duty Paid/Unpaid Rotterdam.

Similarly, as we maintain large quantities of base inventory, significant decreases in the price of primary aluminum would reduce the realizable value of our inventory, negatively affecting our financial condition and results of operations. In addition, a drop in aluminum prices between the date of purchase and the final settlement date on derivative contracts used to mitigate the risk of price fluctuations may require us to post additional margin, which, in turn, could place a significant demand on our liquidity.

We purchase and sell LME forwards, futures and options contracts to seek to reduce our exposure to changes in aluminum, copper and zinc prices. The ability to realize the benefit of our hedging program is dependent upon factors beyond our control, such as counterparty risk as well as our customers making timely payment to us for product. In addition, at certain times, hedging options may be unavailable or not available on terms acceptable to us. In certain scenarios when market price movements result in a decline in value of our current derivatives position, our mark-to-market expense may exceed our credit line and counterparties may request the posting of cash collateral. Despite the use of LME forwards, futures and options contracts, we remain exposed to the variability in prices of aluminum scrap. While aluminum scrap is typically priced in relation to prevailing LME prices, it may also be priced at a discount to LME aluminum (depending upon the quality of the material supplied). This discount is referred to in the industry as the “scrap spread” and fluctuates depending upon industry conditions. In addition, we purchase forwards, futures or options contracts to reduce our exposure to changes in natural gas prices. We do not account for our forwards, futures, or options contracts as hedges of the underlying risks. As a result, unrealized gains and losses on our derivative financial instruments must be reported in our consolidated results of operations. The inclusion of such unrealized gains and losses in earnings may produce significant period to period earnings volatility that is not necessarily reflective of our underlying operating performance. See Item 7A. - “Quantitative and Qualitative Disclosures About Market Risk.”

We may encounter increases in the cost, or limited availability, of raw materials and energy, which could cause our cost of goods sold to increase thereby reducing operating results and limiting our operating flexibility.

We require substantial amounts of raw materials and energy in our business, consisting principally of primary aluminum, aluminum scrap, alloys and other materials, and energy, including natural gas. Any substantial increases in the cost of raw materials or energy could cause our operating costs to increase and negatively affect our financial condition and results of operations.

Aluminum scrap, primary aluminum, rolling slab and hardener prices are subject to significant cyclical price fluctuations. Metallics (primary aluminum and scrap aluminum) represent the largest component of our costs of sales. We purchase aluminum primarily from aluminum producers, aluminum scrap dealers and other intermediaries. We have limited control over the price or availability of these supplies.

The availability and price of aluminum scrap and rolling slab depend on a number of factors outside our control, including general economic conditions, international demand for metallics and internal recycling activities by primary aluminum producers and other consumers of aluminum. We rely on third parties for the supply of alloyed rolling slab for certain products. In the future, we may face an increased risk of supply to meet our demand due to issues with suppliers and their rising costs of production and their ability to sustain their business. Our inability to satisfy our future supply needs may impact our profitability and expose us to penalties as a result of contractual commitments with some of our customers. The availability and price of rolling slab could impact our margins and our ability to meet customer volumes. Increased regional and global demand for aluminum scrap can have the effect of increasing the prices that we pay for these raw materials thereby increasing our cost of sales. We may not be able to adjust the selling prices for our products to recover the increases in scrap prices. If scrap prices were to increase significantly without a commensurate increase in the traded value of the primary metals, our future financial condition and results of operations could be affected by higher costs and lower profitability.

After raw material and labor costs, utilities represent the third largest component of our cost of sales. The price of natural gas, and therefore the costs, can be particularly volatile. Price and volatility can differ by global region based on supply and demand, political issues and government regulation, among other things. As a result, our natural gas costs may fluctuate dramatically, and we may not be able to reduce the effect of higher natural gas costs on our cost of sales. If natural gas costs increase, our financial condition and results of operations may be adversely affected. Although we attempt to mitigate volatility in natural gas costs through the use of hedging and the inclusion of price escalators in certain of our long-term supply contracts, we may not be able to eliminate or reduce the effects of such cost volatility. Furthermore, in an effort to offset the effect of increasing costs, we may also limit our potential benefit from declining costs.

The profitability of our operations depends, in part, on the availability of an adequate source of supplies.

We depend on scrap for our operations and acquire our scrap inventory from numerous sources. These suppliers generally are not bound by long-term contracts and have no obligation to sell scrap metals to us. In periods of low industry prices, suppliers may elect to hold scrap and wait for higher prices. In addition, the slowdown in industrial production and consumer consumption in the U.S. during the previous economic crisis reduced the supply of scrap metal available to us. Furthermore, exports of scrap out of North America and Europe can negatively impact scrap availability and scrap spreads. If an adequate supply of scrap metal is not available to us, we would be unable to recycle metals at desired volumes and our results of operations and financial condition would be materially and adversely affected.

Our operating segments depend on external suppliers for rolling slab for certain products. The availability of rolling slab is dependent upon a number of factors, including general economic conditions, which can impact the supply of available rolling slab and LME pricing, where lower LME prices may cause certain rolling slab producers to curtail production. If rolling slab is less available, our margins could be impacted by higher premiums that we may not be able to pass along to our customers or we may not be able to meet the volume requirements of our customers, which may cause sales losses or result in damage claims from our customers. We maintain long-term contracts for certain volumes of our rolling slab requirements, for the remainder we depend on annual and spot purchases. If we enter into a period of persistent short supply, we could incur significant capital expenditures to internally produce 100% of our rolling slab requirements.

Our business requires substantial amounts of capital to operate; failure to maintain sufficient liquidity will have a material adverse effect on our financial condition and results of operations.

Our business requires substantial amounts of cash to operate and our liquidity can be adversely affected by a number of factors outside our control. Fluctuations in the LME prices for aluminum may result in increased cash costs for metal or scrap. In addition, if aluminum price movements result in a negative valuation of our current financial derivative positions, our counterparties may require posting of cash collateral. Furthermore, in an environment of falling LME prices, the borrowing base and availability under Aleris International’s asset backed multi-currency revolving credit facility (the “ABL Facility”) may shrink and constrain our liquidity.

The loss of certain members of our management may have an adverse effect on our operating results.

Our success will depend, in part, on the efforts of our senior management and other key employees. These individuals possess sales, marketing, engineering, manufacturing, financial and administrative skills that are critical to the operation of our business. If we lose or suffer an extended interruption in the services of one or more of our senior officers, our financial condition and results of operations may be negatively affected. Moreover, the pool of qualified individuals may be highly competitive and we may not be able to attract and retain qualified personnel to replace or succeed members of our senior management or other key employees, should the need arise.

Our internal controls over financial reporting and our disclosure controls and procedures may not prevent all possible errors that could occur.

Each quarter, our chief executive officer and chief financial officer evaluate our internal controls over financial reporting and our disclosure controls and procedures, which includes a review of the objectives, design, implementation and effect of the controls relating to the information generated for use in our financial reports. In the course of our controls evaluation, we seek to identify data errors or control problems and to confirm that appropriate corrective action, including process improvements, are being undertaken. The overall goals of these various evaluation activities are to monitor our internal controls over financial reporting and our disclosure controls and procedures and to make modifications as necessary. Our intent in this regard is that our internal controls over financial reporting and our disclosure controls and procedures will be maintained as dynamic systems that change (including with improvements and corrections) as conditions warrant. A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s objectives will be satisfied. These inherent limitations include the possibility that judgments in our decision-making could be faulty, and that isolated breakdowns could occur because of simple human error or mistake. We cannot provide absolute assurance that all possible control issues within our company have been detected. The design of our system of controls is based in part upon certain assumptions about the likelihood of events, and there can be no assurance that any design will succeed absolutely in achieving our stated goals. Because of the inherent limitations in any control system, misstatements could occur and not be detected.

If we were to lose order volumes from any of our largest customers, our sales volumes, revenues and cash flows could be reduced.

Our business is exposed to risks related to customer concentration. Our ten largest customers were responsible for approximately 28% of our consolidated revenues for the year ended December 31, 2014. No one customer accounted for more

than 10% of those revenues. A loss of order volumes from, or a loss of industry share by, any major customer could negatively affect our financial condition and results of operations by lowering sales volumes, increasing costs and lowering profitability. In addition, our strategy of having dedicated facilities and arrangements with customers subject us to the inherent risk of increased dependence on a single or a few customers with respect to these facilities. In such cases, the loss of such a customer, or the reduction of that customer’s business at one or more of our facilities, could negatively affect our financial condition and results of operations, and we may be unable to timely replace, or replace at all, lost order volumes. In addition, several of our customers have become involved in bankruptcy or insolvency proceedings and have defaulted on their obligations to us in recent years. Similar incidents in the future would adversely impact our financial conditions and results of operations.

We do not have long-term contractual arrangements with a substantial number of our customers, and our sales volumes and revenues could be reduced if our customers switch their suppliers.

Approximately 64% of our consolidated revenues for the year ended December 31, 2014 were generated from customers who do not have long-term contractual arrangements with us. These customers purchase products and services from us on a purchase order basis and may choose not to continue to purchase our products and services. Any significant loss of these customers or a significant reduction in their purchase orders could have a material negative impact on our sales volume and business.

Our business requires substantial capital investments that we may be unable to fulfill.

Our operations are capital intensive. The capital expenditures of our continuing operations were $121.4 million, $188.3 million, and $315.4 million for the years ended December 31, 2014, 2013 and 2012, respectively. Capital expenditures over the past three years include spending related to maintenance and our strategic initiatives, including the Zhenjiang rolling mill. In September 2014, we announced that we plan to invest approximately $350.0 million to upgrade our capabilities at our aluminum rolling mill in Lewisport, Kentucky in order to meet increasing demand for auto body sheet in North America. We may not generate sufficient operating cash flows and our external financing sources may not be available in an amount sufficient to enable us to make anticipated capital expenditures, service or refinance our indebtedness or fund other liquidity needs. If we are unable to make upgrades or purchase new plants and equipment, our financial condition and results of operations could be affected by higher maintenance costs, lower sales volumes due to the impact of reduced product quality, and other competitive influences.

Our Asia Pacific operations will require significant funding support that we may be unable to fulfill.

The Zhenjiang rolling mill began limited production in the beginning of 2013. We continued the start-up phase of that operation through 2014, growing our sales as the year progressed. The mill required funding for start-up expenses, residual capital expenditures, interest on third party debt and working capital, reaching an aggregate of $109.2 million in 2014. This funding was obtained from an RMB 410.0 million (or equivalent to approximately $66.8 million) revolving credit facility (the “Zhenjiang Revolver”) provided by the People’s Bank of China and with capital provided by us.

The Zhenjiang rolling mill incurred start-up expenses of approximately $16.6 million in 2014. These start-up expenses were tied to non-recurring operating losses incurred while the mill ramped up to full production, as well as expenses associated with obtaining certification to produce aircraft sheet and plate. The mill received several such certifications, and will exit the start-up phase of operations in the first quarter of 2015.

Furthermore, significant investment in the Zhenjiang rolling mill is needed to fund our anticipated sales growth in 2015. Working capital requirements are anticipated to be funded under the Zhenjiang Revolver and with capital provided by us. The Chinese government exercises significant control over economic growth in China through the allocation of resources, including imposing policies that impact particular industries or companies in different ways, so we may experience future disruptions to our access to capital in the Chinese market. In addition, we have to meet certain conditions to be able to draw on the Zhenjiang Revolver. We cannot be certain that we will be able to draw all amounts committed under the Zhenjiang Revolver in the future. We also may not generate sufficient operating cash flows and our external financing sources may not be available in an amount sufficient to enable us to fund the anticipated working capital needs of the Zhenjiang rolling mill. To the extent that funding is not available under the Zhenjiang Revolver, we may need to increase the amount of capital necessary to fund the Zhenjiang rolling mill from our own or other sources of capital. The availability of financing, as well as future actions or policies of the Chinese government, could materially affect the funding of our working capital needs in China, which may delay our ability to produce and sell material from the Zhenjiang rolling mill.

We may not be able to compete successfully in the industry segments we serve and aluminum may become less competitive with alternative materials, which could reduce our share of industry sales, sales volumes and selling prices.

Aluminum competes with other materials such as steel, plastic, composite materials and glass for various applications. Higher aluminum prices tend to make aluminum products less competitive with these alternative materials.

We compete in the production and sale of rolled aluminum products with a number of other aluminum rolling mills, including large, single-purpose sheet mills, continuous casters and other multi-purpose mills, some of which are larger and have greater financial and technical resources than we do. We compete with other rolled products suppliers, principally multipurpose mills, on the basis of quality, price, timeliness of delivery, technological innovation and customer service. Producers with a different cost basis may, in certain circumstances, have a competitive pricing advantage. In addition, a current or new competitor may also add or build new capacity, which could diminish our profitability by decreasing the equilibrium prices in our markets. Changes in regulation that have a disproportionately negative effect on us or our methods of production may also diminish our competitive advantage and industry position. In addition, technological innovation is important to our customers who require us to lead or keep pace with new innovations to address their needs.

As we increase our international business, we encounter the risk that non-U.S. governments could take actions to enhance local production or local ownership at our expense. In addition, new competitors could emerge globally in emerging or transitioning markets with abundant natural resources, low-cost labor and energy, and lower environmental and other standards. This may pose a significant competitive threat to our business. Our competitive position may also be affect by exchange rate fluctuations that may make our products less competitive.

Additional competition could result in a reduced share of industry sales or reduced prices for our products and services, which could decrease revenues or reduce volumes, either of which could have a negative effect on our financial condition and results of operations.

Our international operations expose us to certain risks inherent in doing business abroad.

We have operations in Germany, Belgium and China. We continue to explore opportunities to expand our international operations. Our international operations generally are subject to risks, including:

| |

| ▪ | changes in U.S. and international governmental regulations, trade restrictions and laws, including tax laws and regulations; |

| |

| ▪ | compliance with U.S. and foreign anti-corruption and trade control laws, such as the Foreign Corrupt Practices Act, export controls and economic sanction programs, including those administered by the U.S. Treasury Department’s Office of Foreign Assets Control; |

| |

| ▪ | currency exchange rate fluctuations; |

| |

| ▪ | tariffs and other trade barriers; |

| |

| ▪ | the potential for nationalization of enterprises or government policies favoring local production; |

| |

| ▪ | interest rate fluctuations; |

| |

| ▪ | high rates of inflation; |

| |

| ▪ | currency restrictions and limitations on repatriation of profits; |

| |

| ▪ | differing protections for intellectual property and enforcement thereof; |

| |

| ▪ | differing and, in some cases, more stringent labor regulations; |

| |

| ▪ | divergent environmental laws and regulations; and |

| |

| ▪ | political, economic and social instability. |

The occurrence of any of these events could cause our costs to rise, limit growth opportunities or have a negative effect on our operations and our ability to plan for future periods, and subject us to risks not generally prevalent in the U.S.

The financial condition and results of operations of some of our operating entities are reported in various currencies and then translated into U.S. dollars at the applicable exchange rate for inclusion in our consolidated financial statements. As a result, appreciation of the U.S. dollar against these currencies may have a negative impact on reported revenues and operating profit while depreciation of the U.S. dollar against these currencies may generally have a positive effect on reported revenues and operating profit. In addition, a portion of the revenues generated by our international operations are denominated in U.S. dollars, while the majority of costs incurred are denominated in local currencies. As a result, appreciation in the U.S. dollar may have a positive impact on margins at the time of sale and on the subsequent translation of the resulting accounts receivable until collection, while depreciation of the U.S. dollar may have the opposite effect.

Current environmental liabilities as well as the cost of compliance with, and liabilities under, health and safety laws could increase our operating costs and negatively affect our financial condition and results of operations.

Our operations are subject to federal, state, local and foreign environmental laws and regulations, which govern, among other things, air emissions, wastewater discharges, the handling, storage and disposal of hazardous substances and wastes, the remediation of contaminated sites and employee health and safety. Future environmental regulations could impose stricter compliance requirements on the industries in which we operate. Additional pollution control equipment, process changes, or other environmental control measures may be needed at some of our facilities to meet future requirements.

Financial responsibility for contaminated property can be imposed on us where current operations have had an environmental impact. Such liability can include the cost of investigating and remediating contaminated soil or ground water, fines and penalties sought by environmental authorities, and damages arising out of personal injury, contaminated property and other toxic tort claims, as well as lost or impaired natural resources. Certain environmental laws impose strict, and in certain circumstances joint and several, liability for certain kinds of matters, such that a person can be held liable without regard to fault for all of the costs of a matter even though others were also involved or responsible. The costs of all such matters have not been material to net income (loss) for any accounting period since January 1, 2010. However, future remedial requirements at currently owned or operated properties or adjacent areas could result in significant liabilities.

Changes in environmental requirements or changes in their enforcement could materially increase our costs. For example, if salt cake, a by-product from some of our operations, were to become classified as a hazardous waste in the U.S., the costs to manage and dispose of it would increase and could result in significant increased expenditures.

We could experience labor disputes that could disrupt our business.

Approximately 65% of our U.S. employees and substantially all of our non-U.S. employees, located primarily in Europe where union membership is common, are represented by unions or equivalent bodies and are covered by collective bargaining or similar agreements which are subject to periodic renegotiation. Although we believe that we will successfully negotiate new collective bargaining agreements when the current agreements expire, these negotiations may not prove successful, may result in a significant increase in the cost of labor, or may break down and result in the disruption or cessation of our operations.

Labor negotiations may not conclude successfully, and, in that case or any other, work stoppages or labor disturbances may occur. Any such stoppages or disturbances may have a negative impact on our financial condition and results of operations by limiting plant production, sales volumes and profitability.

New governmental regulation relating to greenhouse gas emissions may subject us to significant new costs and restrictions on our operations.

Climate change is receiving increasing attention worldwide. Many scientists, legislators and others attribute climate change to increased levels of greenhouse gases, including carbon dioxide, which has led to significant legislative and regulatory efforts to limit greenhouse gas emissions. There are legislative and regulatory initiatives in various jurisdictions that would regulate greenhouse gas emissions through a cap-and-trade system under which emitters would be required to buy allowances to offset emissions of greenhouse gas. In addition, several states, including states where we have manufacturing plants, are considering various greenhouse gas registration and reduction programs. Certain of our manufacturing plants use significant amounts of energy, including electricity and natural gas, and certain of our plants emit amounts of greenhouse gas above certain minimum thresholds that are likely to be affected by existing proposals. Greenhouse gas regulation could increase the price of the electricity we purchase, increase costs for our use of natural gas, potentially restrict access to or the use of natural gas, require us to purchase allowances to offset our own emissions or result in an overall increase in our costs of raw materials, any one of which could significantly increase our costs, reduce our competitiveness in a global economy or otherwise negatively affect our business, operations or financial results. While future emission regulation appears likely, it is too early to predict how this regulation may affect our business, operations or financial results.

Further aluminum industry consolidation could impact our business.

The aluminum industry has experienced consolidation over the past several years, and there may be further industry consolidation in the future. Although current industry consolidation has not negatively impacted our business, further consolidation in the aluminum industry could possibly have negative impacts that we cannot reliably predict.

Our operations present significant risk of injury or death. We may be subject to claims that are not covered by or exceed our insurance.

Because of the heavy industrial activities conducted at our facilities, there exists a risk of injury or death to our employees or other visitors, notwithstanding the safety precautions we take. Our operations are subject to regulation by various federal, state and local agencies responsible for employee health and safety, including the Occupational Safety and Health

Administration, which has from time to time levied fines against us for certain isolated incidents. While we have in place policies to minimize such risks, we may nevertheless be unable to avoid material liabilities for any employee death or injury that may occur in the future. These types of incidents may not be covered by or may exceed our insurance coverage and may have a material adverse effect on our results of operations and financial condition.

We are subject to unplanned business interruptions that may materially adversely affect our business.

Our operations may be materially adversely affected by unplanned events such as explosions, fires, war or terrorism, inclement weather, accidents, equipment, information technology systems and process failures, electrical blackouts or outages, transportation interruptions and supply interruptions. Operational interruptions at one or more of our production facilities could cause substantial losses and delays in our production capacity or increase our operating costs. In addition, replacement of assets damaged by such events could be difficult or expensive, and to the extent these losses are not covered by insurance or our insurance policies have significant deductibles, our financial position, results of operations and cash flows may be materially adversely affected by such events. Furthermore, because customers may be dependent on planned deliveries from us, customers that have to reschedule their own production due to our delivery delays may be able to pursue financial claims against us, and we may incur costs to correct such problems in addition to any liability resulting from such claims. Interruptions may also harm our reputation among actual and potential customers, potentially resulting in a loss of business.

Derivatives legislation could have an adverse impact on our ability to hedge risks associated with our business and on the cost of our hedging activities.