UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22558

Brookfield Investment Funds

(Exact name of registrant as specified in charter)

Brookfield Place

250 Vesey Street, 15th Floor

New York, New York 10281-1023

(Address of principal executive offices) (Zip code)

Brian F. Hurley, Esq.

Brookfield Public Securities Group LLC

Brookfield Place

250 Vesey Street, 15th Floor

New York, New York 10281-1023

(Name and address of agent for service)

(855) 777-8001

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

ANNUAL REPORT

December 31, 2022

Brookfield Global Listed Infrastructure Fund

Brookfield Global Listed Real Estate Fund

Brookfield Real Assets Securities Fund

Brookfield Global Renewables & Sustainable Infrastructure Fund

* Please see inside front cover of the report for important information regarding delivery of shareholder reports.

IN PROFILE

Brookfield Public Securities Group LLC (the "Firm") is an SEC-registered investment adviser and represents the Public Securities platform of Brookfield Asset Management. The Firm provides global listed real assets strategies including real estate equities, infrastructure and energy infrastructure equities, multi-real-asset-class strategies and real asset debt. With approximately $22 billion of assets under management as of December 31, 2022, the Firm manages separate accounts, registered funds and opportunistic strategies for institutional and individual clients, including financial institutions, public and private pension plans, insurance companies, endowments and foundations, sovereign wealth funds and high net worth investors. The Firm is an indirect wholly-owned subsidiary of Brookfield Asset Management ULC with approximately $800 billion of assets under management as of December 31, 2022, an unlimited liability company formed under the laws of British Columbia, Canada ("BAM ULC"). Brookfield Corporation, a publicly traded company (NYSE: BN; TSX: BN), holds a 75% interest in BAM ULC, while Brookfield Asset Management Ltd., a publicly traded company (NYSE: BAM; TSX: BAMA) ("Brookfield Asset Management"), holds a 25% interest in BAM ULC. For more information, go to https://publicsecurities.brookfield.com/en.

Brookfield Investment Funds (the "Trust") is managed by Brookfield Public Securities Group LLC. The Trust uses its website as a channel of distribution of material company information. Financial and other material information regarding the Trust is routinely posted on and accessible at https://publicsecurities.brookfield.com/en.

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds' annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds' website (https://publicsecurities.brookfield.com/en), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically anytime by contacting your financial intermediary (such as a broker, investment adviser, bank or trust company) or, if you are a direct investor, by calling the Fund (toll-free) at 1-855-244-4859 or by sending an e-mail request to a Fund at publicsecurities.enquiries@brookfield.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with a Fund, you may call 1-855-244-4859 or send an email request to publicsecurities.enquiries@brookfield.com to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held within the fund complex if you invest directly with a Fund.

TABLE OF CONTENTS

Letter to Shareholders | | | 1 | | |

| About Your Funds' Expenses | | | 3 | | |

Brookfield Global Listed Infrastructure Fund | |

| Management Discussion of Fund Performance | | | 5 | | |

| Portfolio Characteristics | | | 9 | | |

| Schedule of Investments | | | 10 | | |

Brookfield Global Listed Real Estate Fund | |

| Management Discussion of Fund Performance | | | 13 | | |

| Portfolio Characteristics | | | 17 | | |

| Schedule of Investments | | | 18 | | |

Brookfield Real Assets Securities Fund | |

| Management Discussion of Fund Performance | | | 21 | | |

| Portfolio Characteristics | | | 29 | | |

| Schedule of Investments | | | 31 | | |

Brookfield Global Renewables & Sustainable Infrastructure Fund | |

| Management Discussion of Fund Performance | | | 43 | | |

| Portfolio Characteristics | | | 47 | | |

| Schedule of Investments | | | 48 | | |

| Statements of Assets and Liabilities | | | 51 | | |

| Statements of Operations | | | 52 | | |

| Statements of Changes in Net Assets | | | 53 | | |

Financial Highlights | |

| Brookfield Global Listed Infrastructure Fund | | | 55 | | |

| Brookfield Global Listed Real Estate Fund | | | 56 | | |

| Brookfield Real Assets Securities Fund | | | 57 | | |

| Brookfield Global Renewables & Sustainable Infrastructure Fund | | | 58 | | |

| Notes to Financial Statements | | | 59 | | |

| Report of Independent Registered Public Accounting Firm | | | 74 | | |

| Tax Information | | | 75 | | |

| Liquidity Risk Management Program | | | 76 | | |

| Information Concerning Trustees and Officers | | | 77 | | |

| Joint Notice of Privacy Policy | | | 80 | | |

This report is for shareholder information. This is not a prospectus intended for the use in the purchase or sale of Fund shares.

NOT FDIC INSURED | | MAY LOSE VALUE | | NOT BANK GUARANTEED | |

[THIS PAGE IS INTENTIONALLY LEFT BLANK]

Dear Shareholders,

We are pleased to provide the Annual Report for Brookfield Global Listed Infrastructure Fund (the "Infrastructure Fund"), Brookfield Global Listed Real Estate Fund (the "Global Real Estate Fund"), Brookfield Real Assets Securities Fund (the "Real Assets Securities Fund") and Brookfield Global Renewables & Sustainable Infrastructure Fund (the "Renewables Fund") (each, a "Fund," and collectively, the "Funds") for the year ended December 31, 2022.

Global financial markets experienced a historically challenging year in 2022. A war in Eastern Europe, soaring inflation and interest rate hikes to reign in costs resulted in steep losses across equities and fixed income. One of the few silver linings occurred at the very end of the year, when China announced faster-than-expected relaxing of COVID-19 restrictions.

The MSCI World Index declined 17.73% during the year, the steepest annual decline since 2008. The Barclays Global Aggregate Index fell 16.25% as the 10-Year U.S. Treasury Yield rose 236 basis points during the year. It was the largest annual increase on record (dating back to 1962). Conversely, the Bloomberg Commodity Index gained more than 16% as higher input and energy costs spurred global inflation.

2022 was a mixed year for real assets securities. Infrastructure securities lived up to their defensive nature, with utilities and energy infrastructure securities performing relatively well. Renewables, conversely, were negatively impacted by supply chain disruptions, rising costs of equipment and regulatory uncertainty. Global real estate securities underperformed broader markets, also experiencing their worst performance since 2008. No U.S. property types were immune from the downturn in 2022. The office, residential and industrial sectors posted the steepest declines, while mixed-use and retail landlords fared the best. Real asset high-yield and investment-grade securities performed roughly in-line with broad-market counterparts. Rate-sensitive issues (i.e., communications infrastructure) lagged, while those exposed to natural resources benefitted from strength in energy markets.

While 2022 was a challenging year across the board, we maintain that an allocation to real assets securities may provide long-term diversification to a broad investment portfolio. And return dispersions within the real assets sectors during 2022 highlight the importance of a diversified exposure across infrastructure, real estate and real asset debt.

We see tailwinds for listed real assets as 2023 kicks off. Our asset classes look especially inexpensive, after both stocks and bonds suffered in 2022; and we think valuations represent attractive entry points in many real asset sectors. Our teams see opportunities emerging across real assets around five key investment themes in 2023: Decarbonization; Deglobalization; Digitalization; Demand for quality; and Debt.

In addition to performance information and additional discussion on factors impacting the Funds, this report provides the Funds' audited financial statements and schedules of investments as of December 31, 2022.

We welcome your questions and comments and encourage you to contact our Investor Relations team at 1-855-777-8001 or visit us at https://publicsecurities.brookfield.com/en for more information.

Thank you for your support.

Sincerely,

| |

| |

Brian F. Hurley | | David W. Levi, CFA | |

President | | Chief Executive Officer | |

Brookfield Investment Funds | | Brookfield Public Securities Group LLC | |

2022 Annual Report

1

LETTER TO SHAREHOLDERS (continued)

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are primarily as of the close of business on December 31, 2022, and subject to change based on subsequent developments.

Must be preceded or accompanied by a prospectus.

Mutual fund investing involves risk. Principal loss is possible. Real assets includes real estate securities, infrastructure securities and natural resources securities. Property values may fall due to increasing vacancies or declining rents resulting from unanticipated economic, legal, cultural or technological developments. Infrastructure companies may be subject to a variety of factors that may adversely affect their business, including high interest costs, high leverage, regulation costs, economic slowdown, surplus capacity, increased competition, lack of fuel availability and energy conservation policies. Natural resources securities may be affected by numerous factors, including events occurring in nature, inflationary pressures and international politics.

Quasar Distributors, LLC is the distributor of Brookfield Investment Funds.

Brookfield Public Securities Group LLC

2

ABOUT YOUR FUNDS' EXPENSES (Unaudited)

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and contingent deferred sales charges and redemption fees on redemptions; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Fund Return

The table below provides information about actual account values and actual expenses. You may use the information on this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical account values and hypothetical expenses based on the Funds' actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Funds' actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with hypothetical examples that appear in shareholders' reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) and redemption fees. Therefore, the hypothetical account values and expenses in the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs overall would have been higher.

| | Annualized

Expense

Ratio(1) | | Beginning

Account

Value

(07/01/22) | | Ending

Account Value

(12/31/22) | | Expenses

Paid During

Period

(07/01/22–

12/31/22)(1) | |

INFRASTRUCTURE FUND | |

Actual | |

Class A Shares | | | 1.25 | % | | $ | 1,000.00 | | | $ | 988.70 | | | $ | 6.27 | | |

Class C Shares | | | 2.00 | % | | | 1,000.00 | | | | 984.40 | | | | 10.00 | | |

Class I Shares | | | 1.00 | % | | | 1,000.00 | | | | 989.30 | | | | 5.01 | | |

Hypothetical (assuming a 5% return before expenses) | |

Class A Shares | | | 1.25 | % | | | 1,000.00 | | | | 1,018.90 | | | | 6.36 | | |

Class C Shares | | | 2.00 | % | | | 1,000.00 | | | | 1,015.12 | | | | 10.16 | | |

Class I Shares | | | 1.00 | % | | | 1,000.00 | | | | 1,020.16 | | | | 5.09 | | |

GLOBAL REAL ESTATE FUND | |

Actual | |

Class A Shares | | | 1.20 | % | | $ | 1,000.00 | | | $ | 950.00 | | | $ | 5.90 | | |

Class C Shares | | | 1.95 | % | | | 1,000.00 | | | | 946.00 | | | | 9.56 | | |

Class I Shares | | | 0.95 | % | | | 1,000.00 | | | | 950.70 | | | | 4.67 | | |

Hypothetical (assuming a 5% return before expenses) | |

Class A Shares | | | 1.20 | % | | | 1,000.00 | | | | 1,019.16 | | | | 6.11 | | |

Class C Shares | | | 1.95 | % | | | 1,000.00 | | | | 1,015.38 | | | | 9.91 | | |

Class I Shares | | | 0.95 | % | | | 1,000.00 | | | | 1,020.42 | | | | 4.84 | | |

Past performance is no guarantee of future results.

2022 Annual Report

3

ABOUT YOUR FUNDS' EXPENSES (Unaudited) (continued)

| | Annualized

Expense

Ratio(1) | | Beginning

Account

Value

(07/01/22) | | Ending

Account Value

(12/31/22) | | Expenses

Paid During

Period

(07/01/22–

12/31/22)(1) | |

REAL ASSETS SECURITIES FUND | |

Actual | |

Class A Shares | | | 1.15 | % | | $ | 1,000.00 | | | $ | 983.00 | | | $ | 5.75 | | |

Class C Shares | | | 1.90 | % | | | 1,000.00 | | | | 980.10 | | | | 9.48 | | |

Class I Shares | | | 0.90 | % | | | 1,000.00 | | | | 984.40 | | | | 4.50 | | |

Hypothetical (assuming a 5% return before expenses) | |

Class A Shares | | | 1.15 | % | | | 1,000.00 | | | | 1,019.41 | | | | 5.85 | | |

Class C Shares | | | 1.90 | % | | | 1,000.00 | | | | 1,015.63 | | | | 9.65 | | |

Class I Shares | | | 0.90 | % | | | 1,000.00 | | | | 1,020.67 | | | | 4.58 | | |

RENEWABLES FUND | |

Actual | |

Class I Shares | | | 1.00 | % | | $ | 1,000.00 | | | $ | 998.00 | | | $ | 5.04 | | |

Hypothetical (assuming a 5% return before expenses) | |

Class I Shares | | | 1.00 | % | | | 1,000.00 | | | | 1,020.16 | | | | 5.09 | | |

(1) Expenses are equal to the Fund's annualized expense ratio by class multiplied by the average account value over the period, multiplied by 184/365 (to reflect a six-month period).

Past performance is no guarantee of future results.

Brookfield Public Securities Group LLC

4

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

For the year ended December 31, 2022, the Infrastructure Fund, Class I, had a total return of –5.36%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions. The Fund underperformed the FTSE Global Core Infrastructure 50/50 Index, which returned –4.15%.

By sector, stock selection and an underweight allocation within electricity transmission & distribution was the leading contributor to relative performance. Stock selection and overweight allocation to toll roads as well as stock selection and an underweight allocation to water also contributed. Conversely, stock selection and an underweight allocation to airports was the leading detractor to performance. Stock selection and an underweight allocation within renewables/electric generation as well as stock selection within communications also detracted.

By region, stock selection and an underweight allocation to the U.K was the leading contributor to relative performance. Stock selection and an overweight allocation to the U.S. and stock selection within Continental Europe also contributed. Conversely, stock selection and an underweight allocation to Asia Pacific was the leading detractor to relative performance. Stock selection within Latin America also detracted.

By security, an overweight allocation to Atlantia S.p.A (ticker: ATL.IM, sector: toll roads, region: Continental Europe) was the leading contributor to relative performance. The company was taken private during 2022. An overweight to PG&E Corporation (PCG, electricity transmission & distribution, U.S.) as well as an underweight allocation to American Tower Corporation (AMT, communication, U.S.) and also contributed. Conversely, an overweight allocation to Crown Castle Inc. (CCI, communications, U.S.) was the leading detractor to relative performance. An overweight allocation to Dominion Energy, Inc. (D, renewables/electric generation, U.S.) and a non-index allocation to Equitrans Midstream Corp. (ETRN, midstream, U.S.) also detracted.

INFRASTRUCTURE MARKET OVERVIEW

Listed infrastructure did experience volatility throughout the period but did prove more resilient and outperformed global equities. The FTSE Global Core Infrastructure 50/50 Index and the Dow Jones Brookfield Global Infrastructure Index returned –4.87% and –4.91%% respectively, outperforming the MSCI World, which returned –18.14%. Energy infrastructure was the clear leader within the sector, with the Alerian Midstream Energy Index returning 21.53%. Tightening supply/demand dynamics and rising commodity prices given the aftermath of the War in Ukraine were drivers of performance. In addition, U.S. Liquefied Natural Gas gained new strategic importance in terms of meeting global demand. Communications, largely driven by towers, were the laggard throughout the period as rising interest rates and valuation concerns weighed on performance.

OUTLOOK

As we head into 2023, we are actively watching developments around the following key issues:

1. Gas Storage levels in Europe: It's been a relatively mild winter so far, and we haven't seen huge storage drawdowns, factors that have helped keep power prices more stable in recent months. However, if there is an extended period of cold weather, or some kind of additional supply shock, and supply levels fall to unsustainable levels, we would expect to see a significant rise in power prices. Given already existing inflationary and interest rate pressures, rising power prices could contribute to a recession in the region. This would potentially impact our positioning around more economically sensitive subsectors.

2. China Reopening: We expect China to begin a period of reopening over the coming months. Increased mobility in and out of China could increase demand for commodities, notably liquefied natural gas, as well as be a positive for travel in the region.

3. Impacts from Legislation: We are already beginning to see a pickup in investment in carbon capture in the U.S. due to the Inflation Reduction Act. As this new technology becomes more profitable, many midstream assets could potentially be repurposed, creating investment opportunities for North American energy infrastructure companies.

Past performance is no guarantee of future results.

2022 Annual Report

5

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

CURRENT SECTOR VIEWS

Within utilities, we are more positive now toward companies in the U.S., where we feel uncertainties have been removed. We favor more defensive companies with potential catalysts in what may be a volatile environment. In Europe, we favor companies that may benefit from current power pricing dynamics. Regulation in the region is also opening opportunities around carbon capture and new technologies for select utilities.

Within utilities, we see value in U.S. gas utilities after the spike in gas prices pressured valuations. The consensus view is that elevated gas prices may hurt growth, as the rate of bill inflation may be driven by the cost of gas rather than capital investment and earnings growth within the utilities sector. We believe this prediction is an overreaction that assumes that gas prices will remain elevated and that North American natural gas producers will not ramp up production in a higher-price regime. We are cautious around water utilities given valuation concerns. We are taking advantage of select opportunities within electric utilities, particularly in Europe. Several of these names sold off over concerns around high power prices.

Within transports, we believe there are more attractive opportunities elsewhere, particularly due to potential for an economic slowdown. However, attractive valuation opportunities may emerge.

Within communications, our overweight stems from companies outside of the U.S. that we believe offer attractive risk-reward given stock-specific catalysts.

Within energy infrastructure, we favor natural gas-oriented assets in North America; however, after significant outperformance we see reasons to redeploy some capital elsewhere.

AVERAGE ANNUAL TOTAL RETURNS

As of December 31, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since Inception* | |

Class A (Excluding Sales Charge) | | | -5.61 | % | | | 3.93 | % | | | 4.83 | % | | | 5.88 | % | |

Class A (Including Sales Charge) | | | -10.12 | % | | | 2.93 | % | | | 4.32 | % | | | 5.41 | % | |

Class C (Excluding Sales Charge) | | | -6.35 | % | | | 3.14 | % | | | 4.03 | % | | | 4.45 | % | |

Class C (Including Sales Charge) | | | -7.23 | % | | | 3.14 | % | | | 4.03 | % | | | 4.45 | % | |

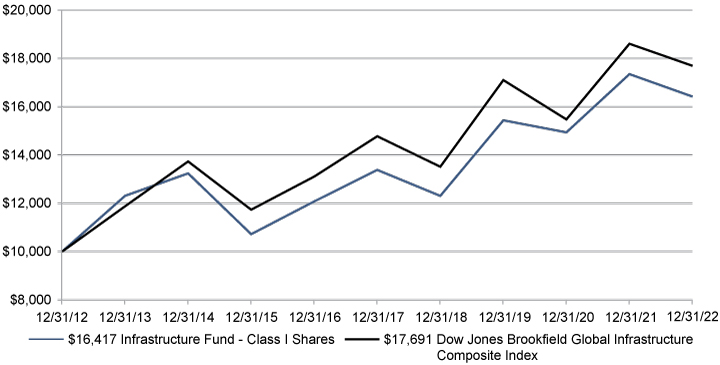

Class I Shares | | | -5.36 | % | | | 4.17 | % | | | 5.08 | % | | | 6.22 | % | |

FTSE Global Core Infrastructure 50/50 Index | | | -4.15 | % | | | 5.53 | % | | | N/A** | | | | N/A** | | |

Dow Jones Brookfield Global Infrastructure Composite Index | | | -4.91 | % | | | 3.67 | % | | | 5.87 | % | | | 6.86 | % | |

* Class A was incepted on December 29, 2011, Class C was incepted on May 1, 2012 and Class I was incepted on December 1, 2011. The Dow Jones Brookfield Global Infrastructure Composite Index references Class I's inception date.

** Data for the FTSE Global Core Infrastructure 50/50 Index is unavailable prior to its inception date of March 2, 2015.

The table and graphs do not reflect the deductions of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-244-4859. Performance shown including sales charge reflects the Class A maximum sales charge of 4.75%. A 1.00% Contingent Deferred Sales Charge (CDSC) would apply to redemptions made within 12 months of purchase of Class C shares. Performance data excluding sales charge does not reflect the deduction of the sales charge or CDSC and if reflected, the sales charge or fee would reduce the performance quoted.

On March 25, 2021, the Board of Trustees of Brookfield Investment Funds, on behalf of the Fund, approved a proposal to close the Fund's Class I Shares (the "Legacy Class I Shares"). Following the close of business on April 30, 2021, shareholders holding the Legacy Class I Shares had their shares automatically converted (the

Brookfield Public Securities Group LLC

6

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

"Conversion") into the Fund's Class Y Shares (the "Legacy Class Y Shares"). Following the Conversion, the Fund's Legacy Class Y Shares were renamed "Class I Shares" (the "Class I Shares"). As a result of the Conversion, the Fund's new Class I Shares adopted the Legacy Class Y Shares' performance and accounting history.

The Fund's gross and net expense ratios in the prospectus dated April 29, 2022 for Class A is 1.37% and 1.25%, Class C is 2.11% and 2.00% and Class I is 1.05% and 1.00%, respectively, for the year ended December 31, 2021.

The Adviser has contractually agreed to reimburse the Fund's expenses through April 30, 2023. There is no guarantee that such reimbursement will be continued after that date. Investment performance reflects fee waivers, expenses and reimbursements in effect. In the absence of such waivers, total return and NAV would be reduced.

The graphs below illustrate a hypothetical investment of $10,000 in the Infrastructure Fund—Class I Shares for the ten years ended December 31, 2022 compared to the Dow Jones Brookfield Global Infrastructure Composite Index.

Disclosure

The Fund's portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Infrastructure companies may be subject to a variety of factors that may adversely affect their business, including high interest costs, high leverage, regulation costs, economic slowdown, surplus capacity, increased competition, lack of fuel availability and energy conversation policies. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. The Fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. Investing in emerging markets may entail special risks relating to potential economic, political or social instability and the risks of nationalization, confiscation or the imposition of restrictions on foreign investment. Investments in debt securities typically decrease in value

Past performance is no guarantee of future results.

2022 Annual Report

7

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. Some securities held may be difficult to sell, particularly during times of market turmoil. If the Fund is forced to sell an illiquid asset to meet redemptions, it may be forced to sell at a loss. Investing in MLPs involves certain risks related to investing in the underlying assets of the MLPs and risks associated with pooled investment vehicles. Using derivatives exposes the Fund to additional risks, may increase the volatility of the Fund's net asset value and may not provide the result intended. Since the Fund will invest more than 25% of its total assets in securities in the Infrastructure industry, the Fund may be subject to greater volatility than a fund that is more broadly diversified.

The FTSE Global Core Infrastructure 50/50 Index gives participants an industry-defined interpretation of infrastructure and adjusts the exposure to certain infrastructure sub-sectors. The constituent weights are adjusted as part of the semi-annual review according to three broad industry sectors—50% Utilities, 30% Transportation including capping of 7.5% for railroads/railways and a 20% mix of other sectors including pipelines, satellites and telecommunication towers. Company weights within each group are adjusted in proportion to their investable market capitalization.

The Dow Jones Brookfield Global Infrastructure Composite Index is calculated and maintained by S&P Dow Jones Indexes and comprises infrastructure companies with at least 70% of their annual cash flows derived from owning and operating infrastructure assets, including MLPs. Brookfield has no direct role in the day-to-day management of any Brookfield cobranded indexes. The index does not reflect any fees, expenses or sales charges.

Indexes are not managed and an investor cannot invest directly in an index. Index performance is shown for illustrative purposes only and does not predict or depict the performance of the Fund.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2022 and subject to change based on subsequent developments.

Brookfield Public Securities Group LLC

8

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

Portfolio Characteristics (Unaudited)

December 31, 2022

ASSET ALLOCATION BY GEOGRAPHY | | Percent of

Total

Investments | |

United States | | | 55.0 | % | |

Canada | | | 7.9 | % | |

Spain | | | 7.2 | % | |

Australia | | | 6.0 | % | |

United Kingdom | | | 5.7 | % | |

China | | | 5.6 | % | |

Japan | | | 3.3 | % | |

Brazil | | | 2.2 | % | |

New Zealand | | | 2.2 | % | |

France | | | 2.1 | % | |

Germany | | | 1.5 | % | |

Chile | | | 0.7 | % | |

Italy | | | 0.6 | % | |

Total | | | 100.0 | % | |

ASSET ALLOCATION BY SECTOR | | Percent of

Total

Investments | |

Renewables/Electric Generation | | | 30.0 | % | |

Electricity Transmission & Distribution | | | 17.2 | % | |

Communications | | | 11.5 | % | |

Toll Roads | | | 9.6 | % | |

Rail | | | 7.5 | % | |

Midstream | | | 6.7 | % | |

Gas Utilities | | | 6.6 | % | |

Pipelines | | | 4.7 | % | |

Airports | | | 4.4 | % | |

Water | | | 1.8 | % | |

Total | | | 100.0 | % | |

TOP TEN HOLDINGS | | Percent of

Total

Investments | |

Transurban Group | | | 6.0 | % | |

NextEra Energy, Inc. | | | 5.7 | % | |

Enbridge, Inc. | | | 4.7 | % | |

American Electric Power Company, Inc. | | | 4.7 | % | |

Crown Castle, Inc. | | | 4.2 | % | |

PG&E Corp. | | | 3.8 | % | |

Eversource Energy | | | 3.5 | % | |

Entergy Corp. | | | 3.4 | % | |

Xcel Energy, Inc. | | | 3.3 | % | |

CenterPoint Energy, Inc. | | | 3.2 | % | |

2022 Annual Report

9

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

Schedule of Investments

December 31, 2022

| | | Shares | | Value | |

COMMON STOCKS – 97.4% | |

AUSTRALIA – 5.8% | |

Toll Roads – 5.8% | |

Transurban Group | | | 1,541,539 | | | $ | 13,562,261 | | |

Total AUSTRALIA | | | | | 13,562,261 | | |

BRAZIL – 2.2% | |

Electricity Transmission & Distribution – 2.2% | |

Equatorial Energia SA | | | 996,542 | | | | 5,104,385 | | |

Total BRAZIL | | | | | 5,104,385 | | |

CANADA – 7.7% | |

Midstream – 1.0% | |

AltaGas Ltd. | | | 128,677 | | | | 2,221,912 | | |

Pipelines – 4.6% | |

Enbridge, Inc. | | | 274,864 | | | | 10,742,838 | | |

Rail – 2.1% | |

Canadian Pacific Railway Ltd. | | | 65,970 | | | | 4,918,517 | | |

Total CANADA | | | | | 17,883,267 | | |

CHILE – 0.7% | |

Water – 0.7% | |

Aguas Andinas SA | | | 7,209,420 | | | | 1,660,564 | | |

Total CHILE | | | | | 1,660,564 | | |

CHINA – 5.5% | |

Communications – 1.8% | |

China Tower Corporation Ltd. (a) | | | 38,438,142 | | | | 4,124,680 | | |

Gas Utilities – 3.7% | |

China Resources Gas Group Ltd. | | | 1,265,100 | | | | 4,719,521 | | |

ENN Energy Holdings Ltd. | | | 275,533 | | | | 3,848,659 | | |

Total Gas Utilities | | | 8,568,180 | | |

Total CHINA | | | | | 12,692,860 | | |

FRANCE – 2.0% | |

Renewables/Electric Generation – 1.0% | |

Engie SA | | | 161,212 | | | | 2,306,305 | | |

Toll Roads – 1.0% | |

Vinci SA | | | 24,300 | | | | 2,422,386 | | |

Total FRANCE | | | | | 4,728,691 | | |

GERMANY – 1.5% | |

Renewables/Electric Generation – 1.5% | |

RWE AG | | | 78,950 | | | | 3,490,187 | | |

Total GERMANY | | | | | 3,490,187 | | |

ITALY – 0.6% | |

Renewables/Electric Generation – 0.6% | |

Hera SpA | | | 478,112 | | | | 1,289,565 | | |

Total ITALY | | | | | 1,289,565 | | |

See Notes to Financial Statements.

Brookfield Public Securities Group LLC

10

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

Schedule of Investments (continued)

December 31, 2022

| | | Shares | | Value | |

COMMON STOCKS (continued) | |

JAPAN – 3.2% | |

Rail – 3.2% | |

East Japan Railway Co. | | | 89,800 | | | $ | 5,114,824 | | |

West Japan Railway Co. | | | 55,043 | | | | 2,389,930 | | |

Total Rail | | | 7,504,754 | | |

Total JAPAN | | | | | 7,504,754 | | |

NEW ZEALAND – 2.1% | |

Airports – 2.1% | |

Auckland International Airport Ltd. (b) | | | 997,400 | | | | 4,946,700 | | |

Total NEW ZEALAND | | | | | 4,946,700 | | |

SPAIN – 7.0% | |

Airports – 2.1% | |

Aena SME SA (a) (b) | | | 39,500 | | | | 4,951,640 | | |

Communications – 2.4% | |

Cellnex Telecom SA (a) | | | 167,400 | | | | 5,552,847 | | |

Toll Roads – 2.5% | |

Ferrovial SA | | | 223,660 | | | | 5,856,008 | | |

Total SPAIN | | | | | 16,360,495 | | |

UNITED KINGDOM – 5.5% | |

Electricity Transmission & Distribution – 2.3% | |

National Grid PLC | | | 448,360 | | | | 5,371,091 | | |

Renewables/Electric Generation – 2.1% | |

Drax Group PLC | | | 299,865 | | | | 2,543,598 | | |

SSE PLC | | | 118,920 | | | | 2,445,833 | | |

Total Renewables/Electric Generation | | | 4,989,431 | | |

Water – 1.1% | |

Severn Trent PLC | | | 78,200 | | | | 2,498,357 | | |

Total UNITED KINGDOM | | | | | 12,858,879 | | |

UNITED STATES – 53.6% | |

Communications – 7.1% | |

American Tower Corp. | | | 11,200 | | | | 2,372,832 | | |

Crown Castle, Inc. | | | 70,100 | | | | 9,508,364 | | |

SBA Communications Corp. | | | 16,600 | | | | 4,653,146 | | |

Total Communications | | | 16,534,342 | | |

Electricity Transmission & Distribution – 12.2% | |

CenterPoint Energy, Inc. | | | 239,720 | | | | 7,189,203 | | |

Eversource Energy | | | 94,000 | | | | 7,880,960 | | |

PG&E Corp. (b) | | | 526,054 | | | | 8,553,638 | | |

Sempra Energy | | | 31,635 | | | | 4,888,873 | | |

Total Electricity Transmission & Distribution | | | 28,512,674 | | |

Gas Utilities – 2.7% | |

NiSource, Inc. | | | 232,310 | | | | 6,369,940 | | |

See Notes to Financial Statements.

2022 Annual Report

11

BROOKFIELD GLOBAL LISTED INFRASTRUCTURE FUND

Schedule of Investments (continued)

December 31, 2022

| | | Shares | | Value | |

COMMON STOCKS (continued) | |

Midstream – 5.6% | |

Cheniere Energy, Inc. | | | 40,943 | | | $ | 6,139,812 | | |

Equitrans Midstream Corp. | | | 590,062 | | | | 3,953,415 | | |

Targa Resources Corp. | | | 41,098 | | | | 3,020,703 | | |

Total Midstream | | | 13,113,930 | | |

Rail – 2.0% | |

CSX Corp. | | | 147,900 | | | | 4,581,942 | | |

Renewables/Electric Generation – 24.0% | |

Ameren Corp. | | | 67,100 | | | | 5,966,532 | | |

American Electric Power Company, Inc. | | | 112,936 | | | | 10,723,273 | | |

Entergy Corp. | | | 69,434 | | | | 7,811,325 | | |

FirstEnergy Corp. | | | 139,450 | | | | 5,848,533 | | |

NextEra Energy, Inc. | | | 153,850 | | | | 12,861,860 | | |

Public Service Enterprise Group, Inc. | | | 86,070 | | | | 5,273,509 | | |

Xcel Energy, Inc. | | | 107,500 | | | | 7,536,825 | | |

Total Renewables/Electric Generation | | | 56,021,857 | | |

Total UNITED STATES | | | | | 125,134,685 | | |

Total COMMON STOCKS

(Cost $208,671,004) | | | | | 227,217,293 | | |

Total Investments – 97.4%

(Cost $208,671,004) | | | | | 227,217,293 | | |

Other Assets in Excess of Liabilities – 2.6% | | | | | 5,970,862 | | |

TOTAL NET ASSETS – 100.0% | | | | $ | 233,188,155 | | |

The following notes should be read in conjunction with the accompanying Schedule of Investments.

(a) — Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration to qualified institutional buyers. As of December 31, 2022, the total value of all such securities was $14,629,167 or 6.3% of net assets.

(b) — Non-income producing security.

See Notes to Financial Statements.

Brookfield Public Securities Group LLC

12

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

For the year ended December 31, 2022, the Global Real Estate Fund, Class I, had a total return of –22.00%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions. The Fund outperformed the FTSE EPRA NAREIT Developed Index1, which returned –25.09%.

Over the past year, Continental Europe was the leading regional contributor to relative performance. The timing of overweight positions in select retail, office and hotel stocks contributed to relative returns. The Fund also maintained underweight exposure to sectors and regions historically perceived to be more defensive (which underperformed amid rising rates).

The U.S. was the second largest regional contributor. Performance was driven by the industrial sector, where overweight positions in a cold storage operator and a large, diversified landlord contributed positively to relative returns. Underweight exposure to the office also contributed as fundamentals remained challenged. Within net lease, positions in experiential and retail-focused landlords outperformed.

Conversely, Canada was a regional detractor, primarily driven by underweight exposure to outperforming stocks. Select overweight positions underperforming residential and office stocks detracted as well. The Fund experienced moderate relative underperformance in Australia, due to underweight positions in retail and diversified landlords, which outperformed.

Although the U.S. was a net contributor on a regional basis, security selection within the retail, residential and data centers sectors detracted from relative returns during the period.

GLOBAL REAL ESTATE MARKET OVERVIEW

For the year, the FTSE EPRA Nareit Developed Index declined nearly 25% in light of higher interest rates and an uncertain economic outlook. By region, Asia Pacific and North America were down roughly 11% and 25%, respectively, while Europe declined more than 40% for the year. No U.S. property types were immune from the downturn in 2022. The office, residential and industrial sectors posted the steepest declines, while mixed-use and retail landlords fared the best.2

OUTLOOK

There's little doubt that the inflation shock and subsequent spike in interest rates in 2022 created a more uncertain operating environment for businesses around the world, including real estate. However, the real estate sector has stable operating cash flow, which we expect to hold up well in a variety of economic environments. Given this stability of cash flows, we feel the selloff in global real estate equities has resulted in global real estate stocks trading at a steep discount to the value of the underlying real estate assets. As a result, we think current valuations present an attractive long-term entry point.

In the U.S., we currently see the best opportunities within the industrial, health care and residential sectors. We think the industrial sector may be supported by continued growth and attractive valuations. We view the health care sector favorably, based on positive fundamentals and a potentially moderating interest-rate environment. Within the residential sector, we continue to expect strong revenue growth and favor sunbelt exposure across all subsectors. Conversely, the office sector remains challenged broadly and we maintain a focus on high quality assets within our limited exposure to the sector. We also see less opportunity within net lease, given the higher cost of borrowing to fund growth.

Outside the U.S., the elimination and reduction of travel restrictions and social distancing measures throughout Asia is a positive and should improve mobility trends. Reduced travel restrictions from China could result in "revenge spending" and increased travel throughout the region. We think this stands to benefit high quality landlords and developers in the region. That said, we are monitoring the risks related to virus outbreaks and potential lockdowns, as well as domestic unrest and geopolitical conflicts in the region. Japan's reopening is also encouraging, but we're

Past performance is no guarantee of future results.

2022 Annual Report

13

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

mindful of monetary policy risks that could impact sentiment toward REITs and real estate companies in the country. The macro outlook continues to appear challenged in Europe although softening energy prices are helping to improve the outlook.

1 The FTSE EPRA Nareit Developed Index is a free-float adjusted, liquidity, size and revenue screened index designed to track the performance of listed real estate companies and REITs worldwide.

2 Sector returns represented by the FTSE Nareit US Real Estate Index Series Indices are not managed and an investor cannot invest directly in an index.

AVERAGE ANNUAL TOTAL RETURNS

As of December 31, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since Inception* | |

Class A (Excluding Sales Charge) | | | -22.21 | % | | | -1.11 | % | | | 3.10 | % | | | 4.25 | % | |

Class A (Including Sales Charge) | | | -25.90 | % | | | -2.07 | % | | | 2.60 | % | | | 3.78 | % | |

Class C (Excluding Sales Charge) | | | -22.78 | % | | | -1.85 | % | | | 2.33 | % | | | 3.48 | % | |

Class C (Including Sales Charge) | | | -23.54 | % | | | -1.85 | % | | | 2.33 | % | | | 3.48 | % | |

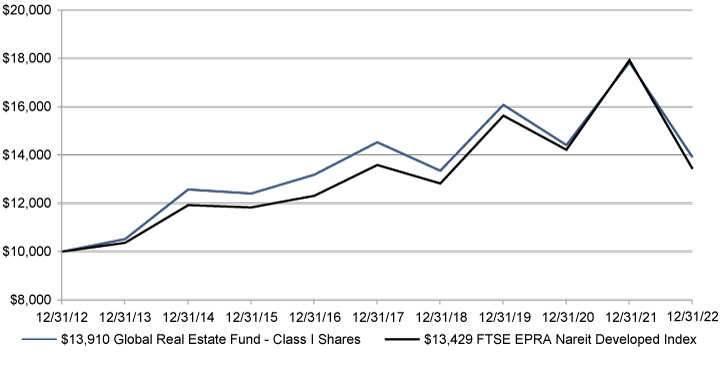

Class I | | | -22.00 | % | | | -0.86 | % | | | 3.36 | % | | | 5.76 | % | |

FTSE EPRA Nareit Developed Index Net | | | -25.09 | % | | | -0.23 | % | | | 2.99 | % | | | 5.07 | % | |

* Classes A and C were incepted on May 1, 2012 and Class I was incepted on December 1, 2011. The FTSE EPRA Nareit Developed Index Net references Class I's inception date.

The table and graphs do not reflect the deductions of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-244-4859. Performance shown including sales charge reflects the Class A maximum sales charge of 4.75%. A 1.00% Contingent Deferred Sales Charge (CDSC) would apply to redemptions made within 12 months of purchase of Class C shares. Performance data excluding sales charge does not reflect the deduction of the sales charge or CDSC and if reflected, the sales charge or fee would reduce the performance quoted.

On March 25, 2021, the Board of Trustees of Brookfield Investment Funds, on behalf of the Fund, approved a proposal to close the Fund's Class I Shares (the "Legacy Class I Shares"). Following the close of business on April 30, 2021, shareholders holding the Legacy Class I Shares had their shares automatically converted (the "Conversion") into the Fund's Class Y Shares (the "Legacy Class Y Shares"). Following the Conversion, the Fund's Legacy Class Y Shares were renamed "Class I Shares" (the "Class I Shares"). As a result of the Conversion, the Fund's new Class I Shares adopted the Legacy Class Y Shares' performance and accounting history.

The Fund's gross and net expense ratios in the prospectus dated April 29, 2022 for Class A is 1.27% and 1.20%, Class C is 2.01% and 1.95% and Class I is 0.94% and 0.95%, respectively for the year ended December 31, 2021.

The Adviser has contractually agreed to reimburse the Fund's expenses through April 30, 2023. There is no guarantee that such reimbursement will be continued after that date. Investment performance reflects fee waivers, expenses and reimbursements in effect. In the absence of such waivers, total return and NAV would be reduced.

Brookfield Public Securities Group LLC

14

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

The graphs below illustrate a hypothetical investment of $10,000 in the Global Real Estate Fund—Class I Shares for the ten years ended December 31, 2022 compared to the FTSE EPRA Nareit Developed Index.

Disclosure

The Fund's portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Investors should be aware of the risks involved with investing in a fund concentrating in REITs and real estate securities, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. Investing in emerging markets may entail special risks relating to potential economic, political or social instability and the risks of nationalization, confiscation or the imposition of restrictions on foreign investment. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. Some securities held may be difficult to sell, particularly during times of market turmoil. If the Fund is forced to sell an illiquid asset to meet redemptions, the Fund may be forced to sell at a loss. Using derivatives exposes the Fund to additional risks, may increase the volatility of the Fund's net asset value and may not provide the result intended. Since the Fund will invest more than 25% of its total assets in securities in the Real Estate industry, the Fund may be subject to greater volatility than a fund that is more broadly diversified.

The FTSE EPRA Nareit Developed Index Net (USD) is a free float-adjusted market-capitalization weighted index that is designed to measure the performance of listed real estate companies and real estate investment trusts (REITs) in developed markets. Investors cannot invest directly in indices or averages, and their performance does not reflect fees and expenses or taxes except the reinvestment of dividends net of withholding taxes nor represents

Past performance is no guarantee of future results.

2022 Annual Report

15

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

the performance of any fund. The Net benchmark presented is calculated on a total return basis net of foreign withholding taxes on dividends, and does not reflect fees, brokerage commissions, or other expenses. Net total return indexes reinvest dividends after the deduction of withholding taxes (for international indexes), using tax rates applicable to non-resident investors who do not benefit from double taxation treaties.

Indexes are not managed and an investor cannot invest directly in an index. Index performance is shown for illustrative purposes only and does not predict or depict the performance of the Fund.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2022 and subject to change based on subsequent developments.

Brookfield Public Securities Group LLC

16

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

Portfolio Characteristics (Unaudited)

December 31, 2022

ASSET ALLOCATION BY GEOGRAPHY | | Percent of

Total

Investments | |

United States | | | 65.5 | % | |

Japan | | | 7.8 | % | |

United Kingdom | | | 5.8 | % | |

Hong Kong | | | 5.6 | % | |

Singapore | | | 4.7 | % | |

Canada | | | 2.5 | % | |

Australia | | | 2.2 | % | |

France | | | 2.0 | % | |

Germany | | | 2.0 | % | |

Spain | | | 1.9 | % | |

Total | | | 100.0 | % | |

ASSET ALLOCATION BY SECTOR | | Percent of

Total

Investments | |

Residential | | | 16.6 | % | |

Industrial | | | 14.8 | % | |

Office | | | 11.1 | % | |

Retail | | | 10.1 | % | |

Healthcare | | | 9.6 | % | |

Diversified | | | 8.2 | % | |

Net Lease | | | 8.1 | % | |

Self Storage | | | 6.8 | % | |

Datacenters | | | 4.5 | % | |

Manufactured Homes | | | 3.6 | % | |

Hotel | | | 3.6 | % | |

Communications | | | 3.0 | % | |

Total | | | 100.0 | % | |

TOP TEN HOLDINGS | | Percent of

Total

Investments | |

Prologis, Inc. | | | 8.9 | % | |

Public Storage | | | 5.0 | % | |

UDR, Inc. | | | 3.8 | % | |

Healthpeak Properties, Inc. | | | 3.2 | % | |

Mid-America Apartment Communities, Inc. | | | 3.1 | % | |

Welltower, Inc. | | | 3.1 | % | |

Digital Realty Trust, Inc. | | | 2.8 | % | |

VICI Properties, Inc. | | | 2.7 | % | |

Wharf Real Estate Investment Company Ltd. | | | 2.5 | % | |

Mitsui Fudosan Company Ltd. | | | 2.5 | % | |

2022 Annual Report

17

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

Schedule of Investments

December 31, 2022

| | | Shares | | Value | |

COMMON STOCKS – 99.7% | |

AUSTRALIA – 2.2% | |

Manufactured Homes – 1.2% | |

Ingenia Communities Group | | | 1,742,400 | | | $ | 5,272,562 | | |

Self Storage – 1.0% | |

National Storage REIT | | | 2,765,328 | | | | 4,357,752 | | |

Total AUSTRALIA | | | | | 9,630,314 | | |

CANADA – 2.5% | |

Office – 0.7% | |

Allied Properties Real Estate Investment Trust | | | 162,518 | | | | 3,072,719 | | |

Residential – 1.8% | |

InterRent Real Estate Investment Trust | | | 836,809 | | | | 7,910,750 | | |

Total CANADA | | | | | 10,983,469 | | |

FRANCE – 2.0% | |

Office – 2.0% | |

Gecina SA | | | 85,477 | | | | 8,708,367 | | |

Total FRANCE | | | | | 8,708,367 | | |

GERMANY – 2.0% | |

Residential – 2.0% | |

Vonovia SE | | | 369,405 | | | | 8,701,833 | | |

Total GERMANY | | | | | 8,701,833 | | |

HONG KONG – 5.5% | |

Diversified – 3.0% | |

Sun Hung Kai Properties Ltd. | | | 735,179 | | | | 10,042,083 | | |

Swire Properties Ltd. | | | 1,287,526 | | | | 3,261,168 | | |

Total Diversified | | | 13,303,251 | | |

Retail – 2.5% | |

Wharf Real Estate Investment Company Ltd. | | | 1,906,710 | | | | 11,104,946 | | |

Total HONG KONG | | | | | 24,408,197 | | |

JAPAN – 7.8% | |

Hotel – 1.5% | |

Japan Hotel REIT Investment Corp. | | | 11,493 | | | | 6,759,079 | | |

Industrial – 1.2% | |

Mitsui Fudosan Logistics Park, Inc. | | | 1,382 | | | | 5,051,888 | | |

Office – 4.1% | |

Mitsui Fudosan Company Ltd. | | | 604,911 | | | | 11,055,943 | | |

Orix JREIT, Inc. | | | 4,762 | | | | 6,755,624 | | |

Total Office | | | 17,811,567 | | |

Residential – 1.0% | |

Comforia Residential REIT, Inc. | | | 1,955 | | | | 4,404,403 | | |

Total JAPAN | | | | | 34,026,937 | | |

See Notes to Financial Statements.

Brookfield Public Securities Group LLC

18

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

Schedule of Investments (continued)

December 31, 2022

| | | Shares | | Value | |

COMMON STOCKS (continued) | |

SINGAPORE – 4.7% | |

Diversified – 4.7% | |

CapitaLand Integrated Commercial Trust | | | 4,644,964 | | | $ | 7,084,555 | | |

City Developments Ltd. | | | 1,086,021 | | | | 6,676,122 | | |

Mapletree Pan Asia Commercial Trust | | | 5,345,087 | | | | 6,678,370 | | |

Total Diversified | | | 20,439,047 | | |

Total SINGAPORE | | | | | 20,439,047 | | |

SPAIN – 1.9% | |

Communications – 1.5% | |

Cellnex Telecom SA (a) | | | 196,800 | | | | 6,528,078 | | |

Diversified – 0.4% | |

Merlin Properties Socimi SA | | | 202,742 | | | | 1,901,490 | | |

Total SPAIN | | | | | 8,429,568 | | |

UNITED KINGDOM – 5.8% | |

Office – 2.3% | |

Derwent London PLC | | | 346,923 | | | | 9,929,423 | | |

Residential – 2.4% | |

Grainger PLC | | | 978,276 | | | | 2,988,329 | | |

The UNITE Group PLC | | | 697,825 | | | | 7,655,665 | | |

Total Residential | | | 10,643,994 | | |

Retail – 1.1% | |

Capital & Counties Properties PLC | | | 3,760,932 | | | | 4,855,324 | | |

Total UNITED KINGDOM | | | | | 25,428,741 | | |

UNITED STATES – 65.3% | |

Communications – 1.5% | |

Crown Castle, Inc. | | | 48,850 | | | | 6,626,014 | | |

Datacenters – 4.5% | |

Digital Realty Trust, Inc. | | | 122,638 | | | | 12,296,912 | | |

Equinix, Inc. | | | 11,480 | | | | 7,519,745 | | |

Total Datacenters | | | 19,816,657 | | |

Healthcare – 9.6% | |

CareTrust REIT, Inc. | | | 200,437 | | | | 3,724,119 | | |

Healthpeak Properties, Inc. | | | 565,951 | | | | 14,188,392 | | |

Ventas, Inc. | | | 231,203 | | | | 10,415,695 | | |

Welltower, Inc. | | | 206,843 | | | | 13,558,559 | | |

Total Healthcare | | | 41,886,765 | | |

Hotel – 2.0% | |

Host Hotels & Resorts, Inc. | | | 277,255 | | | | 4,449,943 | | |

Ryman Hospitality Properties, Inc. | | | 53,880 | | | | 4,406,306 | | |

Total Hotel | | | 8,856,249 | | |

See Notes to Financial Statements.

2022 Annual Report

19

BROOKFIELD GLOBAL LISTED REAL ESTATE FUND

Schedule of Investments (continued)

December 31, 2022

| | | Shares | | Value | |

COMMON STOCKS (continued) | |

Industrial – 13.6% | |

Americold Realty Trust, Inc. | | | 346,548 | | | $ | 9,810,774 | | |

Prologis, Inc. | | | 343,541 | | | | 38,727,377 | | |

Rexford Industrial Realty, Inc. | | | 201,980 | | | | 11,036,187 | | |

Total Industrial | | | 59,574,338 | | |

Manufactured Homes – 2.4% | |

Sun Communities, Inc. | | | 72,990 | | | | 10,437,570 | | |

Net Lease – 8.0% | |

Agree Realty Corp. | | | 148,042 | | | | 10,500,619 | | |

Essential Properties Realty Trust, Inc. | | | 180,951 | | | | 4,246,920 | | |

Spirit Realty Capital, Inc. | | | 221,833 | | | | 8,857,792 | | |

VICI Properties, Inc. | | | 358,649 | | | | 11,620,227 | | |

Total Net Lease | | | 35,225,558 | | |

Office – 2.0% | |

Boston Properties, Inc. | | | 49,008 | | | | 3,311,961 | | |

Highwoods Properties, Inc. | | | 197,244 | | | | 5,518,887 | | |

Total Office | | | 8,830,848 | | |

Residential – 9.4% | |

American Homes 4 Rent | | | 361,238 | | | | 10,887,713 | | |

Mid-America Apartment Communities, Inc. | | | 86,720 | | | | 13,614,173 | | |

UDR, Inc. | | | 426,165 | | | | 16,505,370 | | |

Total Residential | | | 41,007,256 | | |

Retail – 6.5% | |

Kimco Realty Corp. | | | 517,528 | | | | 10,961,243 | | |

Kite Realty Group Trust | | | 418,213 | | | | 8,803,384 | | |

Simon Property Group, Inc. | | | 72,880 | | | | 8,561,942 | | |

Total Retail | | | 28,326,569 | | |

Self Storage – 5.8% | |

CubeSmart | | | 92,924 | | | | 3,740,191 | | |

Public Storage | | | 77,492 | | | | 21,712,484 | | |

Total Self Storage | | | 25,452,675 | | |

Total UNITED STATES | | | | | 286,040,499 | | |

Total COMMON STOCKS

(Cost $443,188,568) | | | | | 436,796,972 | | |

Total Investments – 99.7%

(Cost $443,188,568) | | | | | 436,796,972 | | |

Other Assets in Excess of Liabilities – 0.3% | | | | | 1,332,369 | | |

TOTAL NET ASSETS – 100.0% | | | | $ | 438,129,341 | | |

The following notes should be read in conjunction with the accompanying Schedule of Investments.

(a) — Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration to qualified institutional buyers. As of December 31, 2022, the total value of all such securities was $6,528,078 or 1.5% of net assets.

See Notes to Financial Statements.

Brookfield Public Securities Group LLC

20

BROOKFIELD REAL ASSETS SECURITIES FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

For the year ended December 31, 2022, the Real Assets Securities Fund—Class I Shares had a total return of –10.14%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions, outperforming the Fund's Real Assets Custom Index Blend Benchmark,1 which returned –12.71%.

On an absolute basis, the real estate equities, infrastructure equities, real asset debt, REIT preferreds, and renewables equities sleeves all detracted from returns in the 12 months period ended December 31, 2022, while the energy midstream equities and commodities sleeves had positive returns. Relative to the benchmark, overall positive security selection and allocation effect both contributed to relative performance.

Relative Contributors

• Real estate equities driven by positive security selection, as well as underweight allocation to the underperforming real estate sector. Positive security selection was driven by the retail and hotels subsectors in the U.S., partially offset by Canada and Australia.

• Commodities due to an opportunistic allocation to the outperforming commodities sector during the partial period.

• REIT preferreds due to both underweight allocation and positive security selection.

• Real asset debt driven by underweight allocation to underperforming fixed income.

• Infrastructure equities due to positive security selection, partially offset by overweight allocation to the underperforming infrastructure sector. Positive security selection was driven by electricity transportation & distribution and toll roads subsectors, partially offset by airports and renewables/electric generation.

• Energy midstream equities due to positive security selection.

• Renewables equities due to an overweight allocation to the underperforming sector.

Relative Detractors

• No relative detractors at the sleeve level.

In the next section, we provide further detail on the performance of each asset class, along with our outlook for investing in real asset-related securities.

INFRASTRUCTURE EQUITIES

Listed infrastructure did experience volatility throughout the period but did prove more resilient and outperformed global equities. The FTSE Global Core Infrastructure 50/50 Index and the Dow Jones Brookfield Global Infrastructure Index returned –4.87% and –4.91% respectively, outperforming the MSCI World, which returned –18.14%. Energy infrastructure was the clear leader within the sector, with the Alerian Midstream Energy Index returning 21.53%. Tightening supply/demand dynamics and rising commodity prices given the aftermath of the War in Ukraine were drivers of performance. In addition, U.S. Liquefied Natural Gas gained new strategic importance in terms of meeting global demand. Communications, largely driven by towers, lagged throughout the period as rising interest rates and valuation concerns weighed on performance.

We are actively watching three topics as we begin 2023.

1. Gas Storage levels in Europe: It's been a relatively mild winter so far, and we haven't seen huge storage drawdowns, factors that have helped keep power prices more stable in recent months. However, if there is

Past performance is no guarantee of future results.

2022 Annual Report

21

BROOKFIELD GLOBAL RENEWABLES & SUSTAINABLE INFRASTRUCTURE FUND

an extended period of cold weather, or some kind of additional supply shock, and supply levels fall to unsustainable levels, we would expect to see a significant rise in power prices. Given already existing inflationary and interest rate pressures, rising power prices could contribute to a recession in the region. This would potentially impact our positioning around more economically sensitive subsectors.

2. China Reopening: We expect China to begin a period of reopening over the coming months. Increased mobility in and out of China could increase demand for commodities, notably liquefied natural gas, as well as be a positive for travel in the region.

3. Impacts from Legislation: We are already beginning to see a pickup in investment in carbon capture in the U.S. due to the Inflation Reduction Act. As this new technology becomes more profitable, many midstream assets could potentially be repurposed, creating investment opportunities for North American energy infrastructure companies.

Within utilities, we are more positive now toward companies in the U.S. where we feel uncertainties have been removed. We favor more defensive companies with potential catalysts in what may be a volatile environment. In Europe, we favor companies that may benefit from current power pricing dynamics. Regulation in the region is also opening opportunities around carbon capture and new technologies for select utilities. We also see value in U.S. gas utilities after the spike in gas prices pressured valuations. The consensus view is that elevated gas prices will hurt growth, as the rate of bill inflation will be driven by the cost of gas rather than capital investment and earnings growth within the utilities sector. We believe this is an overreaction that assumes that gas prices will remain elevated and that North American natural gas producers will not ramp up production in a higher-price regime. We are cautious around water utilities given valuation concerns. We are taking advantage of select opportunities within electric utilities, particularly in Europe. Several of these names sold off over concerns around high power prices. Within transports, we believe there are more attractive opportunities elsewhere, particularly due to potential for an economic slowdown. However, attractive valuation opportunities may emerge. Within communications, our overweight stems from companies outside of the U.S. that we believe offer attractive risk-reward given stock-specific catalysts. Within energy infrastructure, we favor natural gas-oriented assets in North America; however, after significant outperformance we see reasons to redeploy some capital elsewhere.

REAL ESTATE EQUITIES

For the year, the FTSE EPRA Nareit Developed Index declined nearly 25% in light of higher interest rates and an uncertain economic outlook. By region, Asia Pacific and North America were down roughly 11% and 25%, respectively, while Europe declined more than 40% for the year. No U.S. property types were immune from the downturn in 2022. The office, residential and industrial sectors posted the steepest declines, while mixed-use and retail landlords fared the best.

Overall, we continue to see positive rent growth across most U.S. property types. We anticipate this growth will continue throughout 2022, although the rate of growth may slow in the latter half of the year in select sectors. Real estate demand is robust across the board, and strongest in sectors like industrial, residential and self storage. A strong consumer is helping demand rebound in the retail sector, following the damage the sector experienced when the pandemic began. Despite the Omicron COVID-19 variant, hotel fundamentals have remained strong in our view. RevPAR (revenue per available room) trends have exhibited recent strength, driven by leisure travel demand. We anticipate these trends will improve further if a rebound in business and group travel occurs in 2022.

Outside the U.S., regional property recoveries will be contingent on local responses to COVID-19 outbreaks. As the virus becomes more of an endemic disease, we would expect responses like regional lockdowns or remote work orders to become less frequent. However, with the Omicron variant, we have learned that predicting local responses can be challenging. We believe we are positioned in the best property markets globally based on valuations and potential for long-term outperformance as the global economy reopens.

Brookfield Public Securities Group LLC

22

BROOKFIELD GLOBAL RENEWABLES & SUSTAINABLE INFRASTRUCTURE FUND

REAL ASSET DEBT

Real asset debt was negative in 2022, with the calendar year finishing as the worst year of performance for investment grade in more than 30 years of available data, as measured by the ICE BofA US Corporate Index. High yield2 had its second worst calendar year over the same period, as measured by the ICE BofA US High Yield Index. The U.S. 10-Year Treasury Yield increased to 3.87% at the end of the year from 1.51% a year ago, as the Federal Reserve System (or, the "Fed") hiked interest rates several times throughout the year.

We anticipate continued volatility in 2023, following 2022's unfortunate combination of significantly wider credit spreads and much higher Treasury rates. As a result, 2022 was one of the worst years on record in terms of performance for both high yield and investment grade credit.

As 2023 kicks off, the Fed appears to be nearing the end of its hiking program (Fed fund futures predict two to three hikes in 2023), inflation is trending down, COVID seems manageable, China's economy is reopening, commodity prices are off their highs, and valuations of credit look attractive. However, we remain cautious on the economic outlook given the continued strength of the U.S. economy and our expectation that the Fed may ultimately push the economy into a recession with its aggressive efforts to slow growth and tame inflation. Further, significant rate increases thus far have yet to be fully reflected in the economy, a process that could take multiple months. Additionally, geopolitical turmoil remains, U.S. political divisions are large, and economic indicators continue to send mixed signals.

We expect credit spreads to widen over the course of the year, as the impact of interest rate hikes is more fully absorbed into the economy, contributing to softer corporate earnings and a more restrained consumer. Additionally, the Fed has been vocal about having elevated rates for longer to prevent an inflation resurgence, suggesting the Fed may remain hawkish over the intermediate term. We continue to favor investment grade and up-in-quality high-yield credit with a neutral duration position.

OUTLOOK

We believe global growth may skew to the downside in 2023 amid persistent inflation and further tightening of financial conditions. We expect volatility to remain elevated until global growth eventually slows to coincide with target inflation, driving an end to monetary tightening. As a result, we are defensively positioned within our portfolio, with a modest overweight position in real asset debt, an underweight to real asset equities and little-to-no commodity exposure.

The material increase in bond yields over the past year has made real asset debt more attractive on a risk-adjusted basis. Within equities, we continue to favor infrastructure over real estate due to infrastructure's potential outperformance in down markets and tighter inflation linkage. Within infrastructure, we are most constructive on renewables and energy midstream equities, which we believe should benefit from the energy transition toward renewable power and the global push for energy security. Within real estate, although valuations appear attractive, we believe slowing economic growth may pressure this more cyclical sector further. We hold no direct exposure to commodities. While near-term supply/demand technicals may support energy commodities, slowing economic growth remains a headwind.

1 The Real Assets Custom Index Blend Benchmark, beginning 1/1/20, has consisted of 35% FTSE EPRA Nareit Developed Index, 5% ICE BofA Preferred Stock REITs 7% Constrained Index, 40% FTSE Global Core Infrastructure 50/50 Index, 5% Alerian Midstream Energy Index, and 15% ICE BofA USD Real Asset High Yield and Corporate Custom Index. For the period from 10/1/16 through 12/31/19, this Benchmark consisted of 35% FTSE EPRA Nareit Developed Index, 5% ICE BofA Preferred Stock REITs 7% Constrained Index, 40% Dow Jones Brookfield Global Infrastructure Index, 5% Alerian MLP Index, and 15% ICE BofA Global High Yield Index and ICE BofA Global Corporate Index, weighted 70% and 30%. For the period from 11/19/14 through 9/30/16, this Benchmark consisted of 33.33% DJ Brookfield Global Infrastructure Composite Index, 33.33% FTSE EPRA Nareit Developed Index, 13.33% ICE BofA Global High Yield Index and ICE BofA Global Corporate Index, weighted 70% and 30%, respectively, 10% S&P Global Natural Resources Index, 6.67% Bloomberg Commodity Index and 3.34% Barclays Global Inflation-Linked Index.

2 High-yield refers to the ICE BofAML U.S. High Yield Index which tracks the performance of U.S. dollar-denominated below-investment-grade corporate debt publicly issued in the U.S. domestic market. Investment-grade refers to the ICE BofAML U.S. Corporate Index which tracks the performance of U.S.-dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market.

2022 Annual Report

23

BROOKFIELD REAL ASSETS SECURITIES FUND

AVERAGE ANNUAL TOTAL RETURNS

As of December 31, 2022 | | 1 Year | | 5 Years | | Since Inception* | |

| Class A (Excluding Sales Charge) | | | -10.42 | % | | | 2.75 | % | | | 2.17 | % | |

| Class A (Including Sales Charge) | | | -14.69 | % | | | 1.76 | % | | | 1.56 | % | |

| Class C (Excluding Sales Charge) | | | -11.10 | % | | | 2.05 | % | | | 1.49 | % | |

| Class C (Including Sales Charge) | | | -11.98 | % | | | 2.05 | % | | | 1.49 | % | |

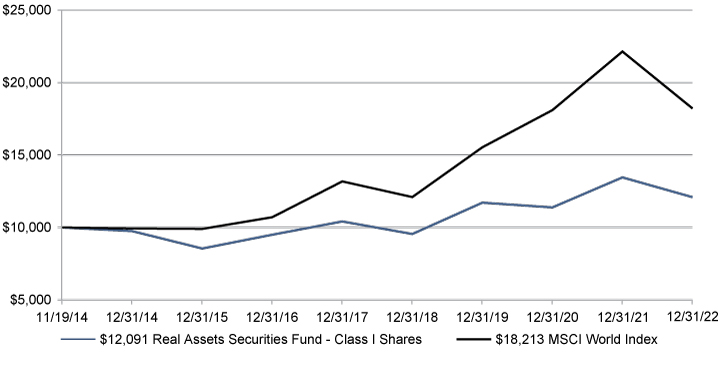

| Class I Shares | | | -10.14 | % | | | 3.03 | % | | | 2.37 | % | |

| MSCI World Index | | | -17.73 | % | | | 6.69 | % | | | 7.64 | % | |

| Real Assets Custom Index Blend Benchmark | | | -12.71 | % | | | 2.87 | % | | | 2.88 | % | |

| S&P Real Assets Index | | | -9.94 | % | | | 3.00 | % | | | N/A** | | |

* Classes A, C and I were incepted on November 19, 2014. The MSCI World Index and Real Assets Custom Index Blend Benchmark returns reference Class I's inception date.

** Data for the S&P Real Assets Index is unavailable prior to its inception date of December 31, 2015.

The table and graphs do not reflect the deductions of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-244-4859. Performance shown including sales charge reflects the Class A maximum sales charge of 4.75%. A 1.00% Contingent Deferred Sales Charge (CDSC) would apply to redemptions made within 12 months of purchase of Class C shares. Performance data excluding sales charge does not reflect the deduction of the sales charge or CDSC and if reflected, the sales charge or fee would reduce the performance quoted.

On March 25, 2021, the Board of Trustees of Brookfield Investment Funds, on behalf of the Fund, approved a proposal to close the Fund's Class I Shares (the "Legacy Class I Shares"). Following the close of business on April 30, 2021, shareholders holding the Legacy Class I Shares had their shares automatically converted (the "Conversion") into the Fund's Class Y Shares (the "Legacy Class Y Shares"). Following the Conversion, the Fund's Legacy Class Y Shares were renamed "Class I Shares" (the "Class I Shares"). As a result of the Conversion, the Fund's new Class I Shares adopted the Legacy Class Y Shares' performance and accounting history.

The Fund's gross and net expense ratios in the prospectus dated April 29, 2022 for Class A is 1.74% and 1.15%, Class C is 2.54% and 1.90% and Class I is 1.44% and 0.90%, respectively for the year ended December 31, 2021.

The Adviser has contractually agreed to reimburse the Fund's expenses through April 30, 2023. There is no guarantee that such reimbursement will be continued after that date. Investment performance reflects fee waivers, expenses and reimbursements in effect. In the absence of such waivers, total return and NAV would be reduced.

Brookfield Public Securities Group LLC

24

BROOKFIELD REAL ASSETS SECURITIES FUND

The graphs below illustrate a hypothetical investment of $10,000 in the Real Assets Securities Fund—Class I Shares from the commencement of investment operations on November 19, 2014 to December 31, 2022 compared to the MSCI World Index.

Disclosure

The Fund's portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Mutual fund investing involves risk. Principal loss is possible. The Fund will be closely linked to the real assets market. Real assets includes real estate securities, infrastructure securities and natural resources securities. Property values may fall due to increasing vacancies or declining rents resulting from unanticipated economic, legal, cultural or technological developments. REITs are dependent upon management skills and generally may not be diversified. REITs are subject to heavy cash flow dependency, defaults by borrowers and self liquidation. Infrastructure companies may be subject to a variety of factors that may adversely affect their business, including high interest costs, high leverage, regulation costs, economic slowdown, surplus capacity, increased competition, lack of fuel availability and energy conservation policies. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. The Fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. Investing in emerging markets may entail special risks relating to potential economic, political or social instability and the risks of nationalization, confiscation or the imposition of restrictions on foreign investment. The Fund invests in MLPs, which involves additional risks as compared to the risks of investing in common stock, including risks related to cash flow, dilution and voting rights. MLPs may trade less frequently than larger companies due to their smaller capitalizations which may result in erratic price movement or difficulty in buying or selling. Additional management fees and other expenses are associated with investing in MLPs. Additionally, investing in MLPs involves material income tax risks and certain other risks. Actual results, performance or events may be affected by, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) changes in laws and regulations and (5) changes in the policies of governments and/or regulatory authorities. Investing in MLPs may generate

Past performance is no guarantee of future results.

2022 Annual Report

25

BROOKFIELD REAL ASSETS SECURITIES FUND