WWW.GUGGENHEIMINVESTMENTS.COM/GEQ

. . .YOUR LINK TO THE LATEST, MOST UP-TO-DATE INFORMATION ABOUT GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND

The shareholder report you are reading right now is just the beginning of the story. Online at www.guggenheiminvestments.com/geq, you will find:

| • | Daily, weekly and monthly data on share prices, net asset values, distributions and more |

| | |

| • | Portfolio overviews and performance analyses |

| | |

| • | Announcements, press releases and special notices |

| | |

| • | Fund and adviser contact information |

Guggenheim Partners Investment Management, LLC and Guggenheim Funds Investment Advisors, LLC are continually updating and expanding shareholder information services on the Fund’s website in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment in the Fund.

DEAR SHAREHOLDER

We thank you for your investment in the Guggenheim Equal Weight Enhanced Equity Income Fund (the “Fund”). This report covers the Fund’s performance for the semiannual period ended June 30, 2013.

The Fund’s investment objective is to provide a high level of risk-adjusted total return with an emphasis on current income.

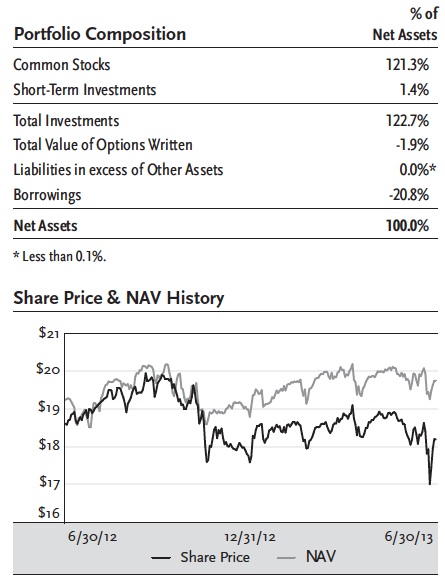

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the six-month period ended June 30, 2013, the Fund provided a total return on an NAV basis of 8.22% and a total return based on market price of 7.46%. The closing price of the Fund’s shares as of June 30, 2013, was $18.19, which represented a discount of 7.90% to the NAV of $19.75. The closing price of the Fund’s shares as of December 31, 2012, was $17.73, which represented a discount of 7.03% to the NAV of $19.07. Past performance does not guarantee future results. The market price of the Fund’s shares fluctuates from time to time, and at any given time it may be higher or lower than the Fund’s NAV. NAV performance data reflects fees and expenses of the Fund.

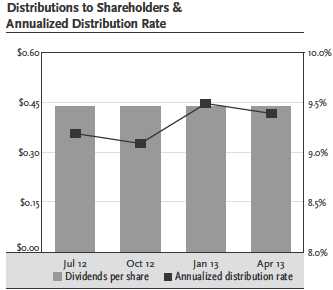

The Fund paid distributions of $0.4375 in January and April of 2013. The most recent distribution represents an annualized distribution rate of 9.62% based on the Fund’s last closing market price of $18.19 on June 30, 2013.

Guggenheim Funds Investment Advisors, LLC (“GFIA” or the “Adviser”) serves as the investment adviser to the Fund. Guggenheim Partners Investment Management, LLC serves as the Fund’s Options Strategy Sub-Adviser, responsible for the management of the Fund’s options strategy. Security Investors, LLC serves as the Equity Strategy Sub-Adviser, responsible for managing the underlying equity portfolio. Each of the Adviser and the two Sub-Advisers is an affiliate of Guggenheim Partners, LLC (“Guggenheim”), a global diversified financial services firm.

The Fund seeks to achieve its investment objective primarily through a two-part strategy. Under normal circumstances, the Fund invests substantially all of its managed assets in a portfolio of common stocks included in the S&P 500 Equal Weight™ Index in equal weight. In addition, the Fund utilizes a call option writing strategy to seek to generate current income and potentially mitigate overall portfolio volatility.

In connection with the implementation of its strategy, the Fund currently uses leverage through a credit facility provided by a large multi-national financial institution. As of June 30, 2013, the amount of leverage was approximately 17% of the Fund’s total assets (including the proceeds of leverage). Although the use of financial leverage by the Fund may create an opportunity for increased return for the common shares, it also results in additional risks and can magnify the effect of any losses. There can be no assurance that a leveraging strategy will be successful during any period during which it is employed.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 27 of this report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the quarterly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at the greater of NAV per share or 95% of the market price per share. The DRIP provides a cost effective means to accumulate additional shares and enjoy the potential benefits of compounding returns over time.

To learn more about the Fund’s performance and investment strategy for the period ended June 30, 2013, we encourage you to read the Questions & Answers section of the report, which begins on page 4.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at guggenheiminvestments.com/geq.

Sincerely,

Donald C. Cacciapaglia

Chief Executive Officer

Guggenheim Equal Weight Enhanced Equity Income Fund

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 3 |

| QUESTIONS & ANSWERS | June 30, 2013 |

Guggenheim Equal Weight Enhanced Equity Income Fund (the “Fund”) is managed by a team of seasoned investment professionals. Guggenheim Funds Investment Advisors, LLC (the “Adviser”) is responsible for overall management of the Fund. Guggenheim Partners Investment Management, LLC (“GPIM”) is the Fund’s investment sub-adviser responsible for the management of the Fund’s options strategy (“Options Strategy Sub-Adviser”). The options strategy is managed by a team that includes Farhan Sharaff, Assistant Chief Investment Officer; Jayson Flowers, Senior Managing Director; and Jamal Pesaran, CFA, Portfolio Manager. Security Investors, LLC (“Security Investors”) is the sub-adviser responsible for managing the underlying equity portfolio (“Equity Strategy Sub-Adviser”). The team at Security Investors includes Ryan Harder, CFA, Portfolio Manager, and James R. King, CFA, Portfolio Manager.

The Adviser, the Options Strategy Sub-Adviser and the Equity Strategy Sub-Adviser are all affiliates of Guggenheim Partners, LLC (“Guggenheim”), a global diversified financial services firm. In the following interview, the investment team discusses the market environment and the Fund’s performance for the six-month period ended June 30, 2013.

Please describe the Fund’s investment objective and strategy.

The Fund’s investment objective is to provide a high level of risk-adjusted total return with an emphasis on current income. The Fund seeks to achieve its investment objective primarily through a two-part strategy. Under normal circumstances, the Fund invests substantially all of its managed assets in a portfolio of common stocks included in the S&P 500 Equal Weight™ Index (the “Index”) in equal weight. In addition, the Fund utilizes a call option writing strategy to seek to generate current income and potentially mitigate overall portfolio volatility.

The Index has the same constituents as the S&P 500® Index (“S&P 500”), a capitalization-weighted index comprised of 500 common stocks, chosen by Standard & Poor’s Financial Services LLC on a statistical basis, but each company in the Index is assigned an equal weight rather than a weight based on its relative market capitalization. The Fund’s equity portfolio is rebalanced quarterly so that each stock in the Fund’s portfolio has the same target weighting. While the Fund generally expects to invest in substantially all of the stocks included in the Index, the Fund may also seek to obtain exposure through investments in other investment funds, other securities and/or financial instruments that are intended to correlate with or replicate the characteristics of exposure to stocks included in the Index or the Index generally.

The Fund utilizes a call option writing strategy to seek to generate current income and potentially mitigate overall portfolio volatility. The Fund’s options strategy follows the Options Strategy Sub-Adviser’s proprietary dynamic rules-based methodology, GPIM’s “Portable Volatility Monetization Strategy”SM. The Options Strategy Sub-Adviser expects to implement the Fund’s options strategy by selling (i.e., writing) call options on securities indices, exchange-traded funds (“ETFs”) that track securities indices, baskets of securities and other instruments, which will include securities that are not held by the Fund. As this strategy involves uncovered option writing, it may result in less volatility mitigation than, and may be subject to more risks compared to, option strategies involving writing options on securities held by the Fund. There can be no assurance that the Fund’s use of call options will be successful.

The Fund currently employs leverage through a credit facility provided by a large multi-national financial institution. As of June 30, 2013, the amount of leverage was approximately 17% of the Fund’s total assets. Although financial leverage may create an opportunity for increased return for shareholders, it also results in additional risks and can magnify the effect of any losses. There is no assurance that the strategy will be successful. If income and gains earned on securities purchased with the financial leverage proceeds are greater than the cost of the financial leverage, common shareholders’ return will be greater than if financial leverage had not been used. Conversely, if the income or gains from the securities purchased with the proceeds of financial leverage are less than the cost of the financial leverage, common shareholders’ return will be less than if financial leverage had not been used.

Please provide an overview of the economic and market environment during the six months ended June 30, 2013.

Monetary accommodation from the world’s central banks and continued improvement in the U.S. housing and labor markets benefited the overall U.S. economy for the six months ended June 30, 2013. However, speculation about the end of quantitative easing in May and June, along with growing fundamental risk in Japan and China, led to a selloff in fixed income and equity markets. For most of the period, equity markets were strong and abundant liquidity and steady quantitative easing had produced a benign credit environment with low default rates.

Housing was the primary locomotive of U.S. economic growth in the period. Housing-related activity, including private residential investment, personal expenditures on household durable goods and utilities, as well as the wealth effect on consumption from home price appreciation, has contributed positively to GDP since 1Q2011. However, housing’s contribution remains dependent on the maintenance of extremely low mortgage rates, which have recently begun moving higher.

Overshadowing solid job gains in the period was slow improvement in the unemployment rate. The participation rate has been relatively flat over the past six months, and in general, has been declining. A bright spot has been the private sector, where the U.S. economy is currently adding jobs at a rate that is over 20% higher than that of the prior expansion.

4 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

| QUESTIONS& ANSWERS continued | June 30, 2013 |

A number of global central banks implemented interest rate cuts during the period, owing to sluggish global economic growth and continuing weakness in commodity prices. The world is still in a deflationary environment, which has given policymakers a great deal of leeway to extend and expand accommodative monetary policies aimed at stimulating output.

The rise in volatility late in the period was in large part a result of shifting market sentiment, but, fundamentally, economic growth in the U.S. has not changed materially. With ongoing weakness in growth and inflation, global central banks are expected to maintain accommodative policies for the foreseeable future.

For the six-month period ended June 30, 2013, the return of the Standard & Poor’s 500 Index (the “S&P 500”) was 13.82%, and in mid-May reached an all-time high. The Chicago Board Options Exchange Market Volatility Index (the “VIX”) was down by 6.44% for the period. The VIX is a key measure of market expectations of near-term volatility conveyed by the S&P 500 stock index option prices. Remaining at multi-year lows, it touched its low of the period in March before spiking to a period high in June, when markets became unsettled.

How did the Fund perform for the six-month period ended June 30, 2013?

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the six-month period ended June 30, 2013, the Fund provided a total return on an NAV basis of 8.22% and a total return based on market price of 7.46%. The closing price of the Fund’s shares as of June 30, 2013, was $18.19, which represented a discount of 7.90% to the NAV of $19.75. The closing price of the Fund’s shares as of December 31, 2012, was $17.73, which represented a discount of 7.03% to the NAV of $19.07. The widening discount of the Fund over the period may be a reflection of lack of analyst coverage of the strategy. Past performance does not guarantee future results. The market price of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV. NAV performance data reflects fees and expenses of the Fund.

The Fund paid distributions of $0.4375 in January and April of 2013. The most recent dividend represents an annualized distribution rate of 9.62% based on the Fund’s last closing market price of $18.19 on June 30, 2013. Past performance does not guarantee future results.

In comparison, the return of the S&P 500 Equal Weight Index was 16.20% and the return of the capitalization-weighted S&P 500 Index was 13.82% for the six months ended June 30, 2013. The outperformance of the Equal Weight Index versus the S&P 500 generally reflects the weaker performance of the largest stocks in the S&P 500 during the period.

What was the nature of the January and April 2013 distributions?

When the January and April 2013 distributions were paid, the majority of the distributions were characterized as return of capital. A final determination of the tax character of distributions paid by the Fund in 2013 will be reported to shareholders in January 2014 on Form 1099-DIV.

The Fund utilizes a strategy that writes calls against a dynamically levered long underlying exposure. As markets have been pushing higher over the past few quarters, the Fund has seen gains in the underlying holdings, which have not been realized, and at the same time realized some short-term capital losses in the call options, which results from paying more to repurchase call options that were previously sold. But on a total return basis, the Fund has sufficient unrealized gains via appreciation of underlying holdings to more than offset any losses on the call options and cover the distribution. It is expected that a portion of these gains in the underlying holdings could be realized over time.

What drove performance for the equal-weighted Index versus its capitalization-weighted version?

Because an equal-weighted index holds the same dollar amount of each member security, it will tend to underweight larger stocks and overweight smaller stocks when compared to a capitalization-weighted index with the same members. As a result, equal-weighted indices tend to outperform during periods when the very largest stocks underperform mid- and small-caps. This period was no exception.

The largest single contributor to the outperformance of the S&P 500 Equal Weight Index was Apple, Inc. During the first half of 2013, Apple’s stock suffered a loss of just over 25% and, as a result, was knocked from the top spot in the capitalization-weighted S&P 500. During those six months, the maker of iPhones and iPads had a substantial weighting of well over 3% of the capitalization-weighted S&P 500 Index and dragged down performance by nearly a full percent. Meanwhile, the Equal Weight S&P 500 Index held Apple in a much smaller weighting, and was largely unaffected by the steep drop in price.

Among sectors, consumer discretionary stocks were the best performers in the Equal Weight S&P 500 Index, and also contributed the most to outperformance versus the capitalization-weighted version. While the performance advantage was well distributed throughout the sector, a few stocks stood out. Best Buy, with a gain of 133%, and Netflix, up 127%, led the sector and the broader index for the six-month period. While neither gets much weight in the cap-weighted S&P 500, the equal-weighted version overweights them substantially, allowing the pair to contribute nearly 20 basis points each to performance.

On the other end of the spectrum, some of the biggest detractors from relative performance were the large pharmaceutical stocks. Compared to the cap-weighted S&P 500, the Equal Weight S&P 500 Index was

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 5 |

| QUESTIONS& ANSWERS continued | June 30, 2013 |

substantially underweighted in health care giants Johnson & Johnson, Pfizer and Merck. Underweighted positions in these three largest health care companies collectively hurt the Equal Weight S&P 500's relative performance by over half a percent.

What role did the option strategy play in performance for the period?

The Fund writes call options on indices rather than individual stocks. Moreover, the option portfolio does not have to equal the full portfolio, but can be adjusted depending on GPIM’s view of market conditions.

Under normal market conditions, the Fund seeks overall portfolio volatility that, after taking into account the Fund’s option writing strategy and use of leverage, approximates that of the broad equity market. During the period, the options portfolio helped reduce the risk of the Fund, as measured by standard deviation of returns.

Markets with gradual drifts higher and low levels of implied volatility, as experienced during the most recent quarter, create the biggest challenges for the strategy. The strategy typically benefits from choppy, range-bound markets where uncertainty is present, causing call option premiums to rise.

How did the Fund’s leverage affect performance during this period?

The strong performance of the underlying index contributed to outperformance for the strategy for the period, with leverage also benefitting the strategy. To lower the risk of the strategy and the risk of leverage, GPIM aims to reduce leverage in strong up markets (accompanied by low implied volatility) or when the market is near its highs of the period, and may add leverage when the market is at period lows or selling off. The extreme underlying moves experienced over the quarter challenged the strategy, and GPIM’s management of the leverage, as described, protected the portfolio and lowered the risk of the strategy.

Index Definitions

Indices are unmanaged and reflect no expenses. It is not possible to invest directly in an index.

The Chicago Board Options Exchange Market Volatility Index is a key measure of market expectations of near-term volatility conveyed by the S&P 500 stock index option prices.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Standard & Poor’s 500 Equal Weight Index has the same constituents as the S&P 500, but each company is assigned a fixed equal weight.

Risks and Other Considerations

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind. The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass.

There can be no assurance that the Fund will achieve its investment objectives. The value of the Fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value. Risk is inherent in all investing, including the loss of your entire principal. Therefore, before investing you should consider the risks carefully.

Please see guggenheiminvestments.com/geq for a detailed discussion about Fund risks and considerations.

6 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

| | | |

Fund Statistics | | |

Share Price | | $18.19 |

Common Share Net Asset Value | | $19.75 |

Premium/(Discount) to NAV | | -7.90% |

Net Assets ($000) | | $173,215 |

| |

Total Returns | | |

(Inception 10/27/11) | Market | NAV |

Six Months | 7.46% | 8.22% |

One Year | 7.09% | 12.21% |

Since Inception - average annual | 2.56% | 10.47% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. The NAV total returns reflect the Fund's total annual expenses. For the most recent month-end performance figures, please visit www.guggenheiminvestments.com/geq. The investment return and principal value of an investment will fluctuate with changes in the market conditions and other factors so that an investor's shares, when sold, may be worth more or less than their original cost.

| | |

Sector Breakdown* | % of Common Stocks |

Consumer, Non-cyclical | 19.9% |

Financial | 16.1% |

Consumer, Cyclical | 13.5% |

Industrial | 12.8% |

Technology | 9.8% |

Energy | 8.7% |

Communications | 8.1% |

Utilities | 6.1% |

Basic Materials | 4.8% |

Diversified | 0.2% |

*Securities are classified by sectors that represent broad groupings of industries.

Portfolio composition and sector breakdown are subject to change daily. For more information, please visit www.guggenheiminvestments.com/geq. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 7 |

PORTFOLIO OF INVESTMENTS (Unaudited) | June 30, 2013 |

| | | | |

Number | | | |

of Shares | | Description | Value |

| | | Common Stocks – 121.3% | |

| | | Basic Materials – 5.9% | |

4,400 | | Air Products & Chemicals, Inc.(a) | $ 402,908 |

4,419 | | Airgas, Inc.(a) | 421,838 |

52,202 | | Alcoa, Inc.(a) | 408,220 |

15,329 | | Allegheny Technologies, Inc.(a) | 403,306 |

2,297 | | CF Industries Holdings, Inc.(a) | 393,936 |

23,894 | | Cliffs Natural Resources, Inc.(a) | 388,278 |

12,464 | | Dow Chemical Co.(a) | 400,967 |

5,968 | | Eastman Chemical Co.(a) | 417,820 |

5,044 | | Ecolab, Inc.(a) | 429,698 |

8,047 | | EI du Pont de Nemours & Co.(a) | 422,468 |

6,773 | | FMC Corp.(a) | 413,559 |

14,335 | | Freeport-McMoRan Copper & Gold, Inc.(a) | 395,789 |

5,402 | | International Flavors & Fragrances, Inc.(a) | 406,014 |

9,346 | | International Paper Co.(a) | 414,122 |

6,286 | | LyondellBasell Industries NV (Netherlands)(a) | 416,510 |

11,866 | | MeadWestvaco Corp.(a) | 404,749 |

4,012 | | Monsanto Co.(a) | 396,386 |

7,327 | | Mosaic Co.(a) | 394,266 |

12,771 | | Newmont Mining Corp.(a) | 382,491 |

9,482 | | Nucor Corp.(a) | 410,760 |

2,755 | | PPG Industries, Inc.(a) | 403,360 |

3,594 | | Praxair, Inc.(a) | 413,885 |

2,314 | | Sherwin-Williams Co.(a) | 408,652 |

5,203 | | Sigma-Aldrich Corp.(a) | 418,113 |

23,692 | | United States Steel Corp.(a) | 415,320 |

| | | | 10,183,415 |

| | | Communications – 9.8% | |

1,547 | | Amazon.com, Inc.(a) (b) | 429,587 |

11,803 | | AT&T, Inc.(a) | 417,826 |

28,874 | | Cablevision Systems Corp., Class A(a) | 485,661 |

8,882 | | CBS Corp., Class B(a) | 434,063 |

11,760 | | CenturyLink, Inc.(a) | 415,716 |

17,595 | | Cisco Systems, Inc.(a) | 427,734 |

10,667 | | Comcast Corp., Class A(a) | 446,734 |

28,410 | | Corning, Inc.(a) | 404,274 |

6,025 | | Crown Castle International Corp.(a) (b) | 436,150 |

6,837 | | Directtv(a) (b) | 421,296 |

5,548 | | Discovery Communications, Inc., Class A(a) (b) | 428,361 |

8,263 | | eBay, Inc.(a) (b) | 427,362 |

7,308 | | Expedia, Inc.(a) | 439,577 |

5,729 | | F5 Networks, Inc.(a) (b) | 394,155 |

100,443 | | Frontier Communications Corp.(a) | 406,794 |

16,961 | | Gannett Co., Inc.(a) | 414,866 |

485 | | Google, Inc., Class A(a) (b) | 426,979 |

8,507 | | Harris Corp.(a) | 418,970 |

29,213 | | Interpublic Group of Cos., Inc.(a) | 425,049 |

29,913 | | JDS Uniphase Corp.(a) (b) | 430,149 |

22,251 | | Juniper Networks, Inc.(a) (b) | 429,667 |

7,445 | | Motorola Solutions, Inc.(a) | 429,800 |

1,982 | | NetFlix, Inc.(a) (b) | 418,380 |

19,831 | | News Corp. Class A, Class A(a) (b) | 303,414 |

6,754 | | Omnicom Group, Inc.(a) | 424,624 |

519 | | priceline.com, Inc.(a) (b) | 429,281 |

6,369 | | Scripps Networks Interactive, Inc., Class A(a) | 425,194 |

57,905 | | Sprint Nextel Corp.(a) (b) | 406,493 |

18,958 | | Symantec Corp.(a) | 425,986 |

4,078 | | Time Warner Cable, Inc.(a) | 458,693 |

7,375 | | Time Warner, Inc.(a) | 426,423 |

6,648 | | TripAdvisor, Inc.(a) (b) | 404,664 |

1,825 | | Twenty-First Century Fox, Inc. | 52,907 |

13,547 | | Twenty-First Century Fox, Inc., Class A | 441,632 |

9,412 | | VeriSign, Inc.(a) (b) | 420,340 |

8,299 | | Verizon Communications, Inc.(a) | 417,772 |

6,347 | | Viacom, Inc., Class B(a) | 431,913 |

6,644 | | Walt Disney Co.(a) | 419,569 |

875 | | Washington Post Co., Class B(a) | 423,299 |

51,007 | | Windstream Corp.(a) | 393,264 |

16,128 | | Yahoo!, Inc.(a) (b) | 404,974 |

| | | | 16,919,592 |

| | | Consumer, Cyclical – 16.4% | |

8,694 | | Abercrombie & Fitch Co., Class A(a) | 393,404 |

9,618 | | AutoNation, Inc.(a) (b) | 417,325 |

1,000 | | AutoZone, Inc.(a) (b) | 423,690 |

5,964 | | Bed Bath & Beyond, Inc.(a) (b) | 422,848 |

15,774 | | Best Buy Co., Inc.(a) | 431,103 |

5,014 | | BorgWarner, Inc.(a) (b) | 431,956 |

9,132 | | CarMax, Inc.(a) (b) | 421,533 |

12,525 | | Carnival Corp. (Panama)(a) | 429,482 |

1,151 | | Chipotle Mexican Grill, Inc.(a) (b) | 419,367 |

9,302 | | Cintas Corp.(a) | 423,613 |

7,244 | | Coach, Inc.(a) | 413,560 |

3,819 | | Costco Wholesale Corp.(a) | 422,267 |

7,180 | | CVS Caremark Corp.(a) | 410,552 |

8,068 | | Darden Restaurants, Inc.(a) | 407,273 |

8,276 | | Delphi Automotive PLC (Jersey)(a) | 419,510 |

8,282 | | Dollar General Corp.(a) (b) | 417,661 |

8,630 | | Dollar Tree, Inc.(a) (b) | 438,749 |

17,743 | | DR Horton, Inc.(a) | 377,571 |

6,704 | | Family Dollar Stores, Inc.(a) | 417,726 |

8,889 | | Fastenal Co.(a) | 407,561 |

27,577 | | Ford Motor Co.(a) | 426,616 |

4,059 | | Fossil Group, Inc.(a) (b) | 419,335 |

See notes to financial statements.

8 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

PORTFOLIO OF INVESTMENTS (Unaudited) continued | June 30, 2013 |

| | | | |

Number | | | |

of Shares | | Description | Value |

| | | Consumer, Cyclical (continued) | |

10,866 | | GameStop Corp., Class A(a) | $ 456,699 |

10,220 | | Gap, Inc.(a) | 426,481 |

12,362 | | General Motors Co.(a) (b) | 411,778 |

5,390 | | Genuine Parts Co.(a) | 420,797 |

27,685 | | Goodyear Tire & Rubber Co.(a) (b) | 423,304 |

7,977 | | Harley-Davidson, Inc.(a) | 437,299 |

8,208 | | Harman International Industries, Inc.(a) | 444,874 |

9,613 | | Hasbro, Inc.(a) | 430,951 |

5,534 | | Home Depot, Inc.(a) | 428,719 |

24,572 | | International Game Technology(a) | 410,598 |

24,387 | | JC Penney Co., Inc.(a) (b) | 416,530 |

11,281 | | Johnson Controls, Inc.(a) | 403,747 |

8,128 | | Kohl's Corp.(a) | 410,545 |

10,860 | | Lennar Corp., Class A(a) | 391,395 |

8,346 | | Limited Brands, Inc.(a) | 411,041 |

10,298 | | Lowe's Cos., Inc.(a) | 421,188 |

8,742 | | Macy's, Inc.(a) | 419,616 |

10,398 | | Marriott International, Inc., Class A(a) | 419,767 |

9,480 | | Mattel, Inc.(a) | 429,539 |

4,307 | | McDonald's Corp.(a) | 426,393 |

15,601 | | Newell Rubbermaid, Inc.(a) | 409,526 |

6,850 | | NIKE, Inc., Class B(a) | 436,208 |

7,191 | | Nordstrom, Inc.(a) | 431,029 |

3,800 | | O'Reilly Automotive, Inc.(a) (b) | 427,956 |

7,965 | | PACCAR, Inc.(a) | 427,402 |

6,123 | | PetSmart, Inc.(a) | 410,180 |

20,320 | | Pulte Group, Inc.(a) (b) | 385,470 |

3,438 | | PVH Corp.(a) | 429,922 |

2,448 | | Ralph Lauren Corp.(a) | 425,316 |

6,536 | | Ross Stores, Inc.(a) | 423,598 |

30,561 | | Southwest Airlines Co.(a) | 393,931 |

26,426 | | Staples, Inc.(a) | 419,116 |

6,462 | | Starbucks Corp.(a) | 423,196 |

6,388 | | Starwood Hotels & Resorts Worldwide, Inc.(a) | 403,658 |

6,140 | | Target Corp.(a) | 422,800 |

5,616 | | Tiffany & Co.(a) | 409,069 |

8,407 | | TJX Cos., Inc.(a) | 420,854 |

10,368 | | Urban Outfitters, Inc.(a) (b) | 417,001 |

2,266 | | VF Corp.(a) | 437,474 |

8,448 | | Walgreen Co.(a) | 373,402 |

5,661 | | Wal-Mart Stores, Inc.(a) | 421,688 |

3,281 | | Whirlpool Corp.(a) | 375,215 |

1,666 | | WW Grainger, Inc.(a) | 420,132 |

7,210 | | Wyndham Worldwide Corp.(a) | 412,628 |

3,137 | | Wynn Resorts Ltd.(a) | 401,536 |

5,962 | | Yum! Brands, Inc.(a) | 413,405 |

| | | | 28,405,675 |

| | | Consumer, Non-cyclical – 24.2% | |

11,514 | | Abbott Laboratories(a) | 401,608 |

9,810 | | Abbvie, Inc.(a) | 405,545 |

3,353 | | Actavis, Inc.(a) (b) | 423,216 |

10,756 | | Adt Corp.(a) | 428,627 |

7,003 | | Aetna, Inc.(a) | 444,944 |

4,597 | | Alexion Pharmaceuticals, Inc.(a) (b) | 424,027 |

4,190 | | Allergan, Inc.(a) | 352,966 |

11,913 | | Altria Group, Inc.(a) | 416,836 |

7,717 | | AmerisourceBergen Corp.(a) | 430,840 |

4,351 | | Amgen, Inc.(a) | 429,270 |

12,814 | | Archer-Daniels-Midland Co.(a) | 434,523 |

6,233 | | Automatic Data Processing, Inc.(a) | 429,204 |

9,849 | | Avery Dennison Corp.(a) | 421,144 |

18,542 | | Avon Products, Inc.(a) | 389,938 |

6,004 | | Baxter International, Inc.(a) | 415,897 |

6,485 | | Beam, Inc.(a) | 409,268 |

4,298 | | Becton Dickinson and Co.(a) | 424,771 |

1,999 | | Biogen IDEC, Inc.(a) (b) | 430,186 |

44,570 | | Boston Scientific Corp.(a) (b) | 413,164 |

9,058 | | Bristol-Myers Squibb Co.(a) | 404,802 |

6,061 | | Brown-Forman Corp., Class B(a) | 409,421 |

9,463 | | Campbell Soup Co.(a) | 423,848 |

8,861 | | Cardinal Health, Inc.(a) | 418,239 |

11,214 | | CareFusion Corp.(a) (b) | 413,236 |

3,552 | | Celgene Corp.(a) (b) | 415,264 |

6,218 | | Cigna Corp.(a) | 450,744 |

4,964 | | Clorox Co.(a) | 412,707 |

10,508 | | Coca-Cola Co.(a) | 421,476 |

11,729 | | Coca-Cola Enterprises, Inc.(a) | 412,392 |

7,206 | | Colgate-Palmolive Co.(a) | 412,832 |

12,434 | | ConAgra Foods, Inc.(a) | 434,320 |

8,149 | | Constellation Brands, Inc., Class A(a) (b) | 424,726 |

6,430 | | Covidien PLC (Ireland)(a) | 367,796 |

627 | | Covidien PLC (Ireland)(b) (c) | 35,864 |

3,817 | | CR Bard, Inc.(a) | 414,832 |

3,289 | | DaVita HealthCare Partners, Inc.(a) (b) | 397,311 |

10,336 | | DENTSPLY International, Inc.(a) | 423,363 |

9,033 | | Dr Pepper Snapple Group, Inc.(a) | 414,886 |

6,055 | | Edwards Lifesciences Corp.(a) (b) | 406,896 |

8,143 | | Eli Lilly & Co.(a) | 399,984 |

6,971 | | Equifax, Inc.(a) | 410,801 |

6,197 | | Estee Lauder Cos., Inc., Class A(a) | 407,577 |

6,843 | | Express Scripts Holding Co.(a) (b) | 422,145 |

10,319 | | Forest Laboratories, Inc.(a) (b) | 423,079 |

8,600 | | General Mills, Inc.(a) | 417,358 |

8,115 | | Gilead Sciences, Inc.(a) (b) | 415,569 |

14,806 | | H&R Block, Inc.(a) | 410,867 |

See notes to financial statements.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 9 |

PORTFOLIO OF INVESTMENTS (Unaudited) continued | June 30, 2013 |

| | | | |

Number | | | |

of Shares | | Description | Value |

| | | Consumer, Non-cyclical (continued) | |

4,754 | | Hershey Co.(a) | $ 424,437 |

10,563 | | Hormel Foods Corp.(a) | 407,521 |

11,697 | | Hospira, Inc.(a) (b) | 448,111 |

5,237 | | Humana, Inc.(a) | 441,898 |

850 | | Intuitive Surgical, Inc.(a) (b) | 430,593 |

14,651 | | Iron Mountain, Inc.(a) | 389,863 |

4,116 | | JM Smucker Co.(a) | 424,565 |

4,991 | | Johnson & Johnson(a) | 428,527 |

6,598 | | Kellogg Co.(a) | 423,790 |

4,332 | | Kimberly-Clark Corp.(a) | 420,810 |

7,613 | | Kraft Foods Group, Inc.(a) | 425,338 |

12,184 | | Kroger Co.(a) | 420,835 |

4,239 | | Laboratory Corp. of America Holdings(a) (b) | 424,324 |

5,716 | | Life Technologies Corp.(a) (b) | 423,041 |

9,658 | | Lorillard, Inc.(a) | 421,861 |

742 | | MasterCard, Inc., Class A(a) | 426,279 |

5,866 | | McCormick & Co., Inc.(a) | 412,732 |

7,744 | | McGraw-Hill Cos., Inc.(a) | 411,903 |

3,709 | | McKesson Corp.(a) | 424,681 |

5,211 | | Mead Johnson Nutrition Co.(a) | 412,868 |

8,009 | | Medtronic, Inc.(a) | 412,223 |

8,840 | | Merck & Co., Inc.(a) | 410,618 |

8,547 | | Molson Coors Brewing Co., Class B(a) | 409,059 |

14,219 | | Mondelez International, Inc.(a) | 405,668 |

7,153 | | Monster Beverage Corp.(a) (b) | 434,687 |

6,814 | | Moody's Corp.(a) | 415,177 |

13,379 | | Mylan, Inc.(a) (b) | 415,150 |

10,936 | | Patterson Cos., Inc.(a) | 411,194 |

11,413 | | Paychex, Inc.(a) | 416,803 |

5,161 | | PepsiCo, Inc.(a) | 422,118 |

3,573 | | Perrigo Co.(a) | 432,332 |

14,571 | | Pfizer, Inc.(a) | 408,134 |

4,601 | | Philip Morris International, Inc.(a) | 398,539 |

5,432 | | Procter & Gamble Co.(a) | 418,209 |

16,135 | | Quanta Services, Inc.(a) (b) | 426,932 |

6,769 | | Quest Diagnostics, Inc.(a) | 410,404 |

1,789 | | Regeneron Pharmaceuticals, Inc.(a) (b) | 402,310 |

8,755 | | Reynolds American, Inc.(a) | 423,479 |

12,619 | | Robert Half International, Inc.(a) | 419,329 |

17,400 | | Safeway, Inc.(a) | 411,684 |

31,076 | | SAIC, Inc.(a) | 432,889 |

9,408 | | St Jude Medical, Inc.(a) | 429,287 |

6,307 | | Stryker Corp.(a) | 407,937 |

12,296 | | Sysco Corp.(a) | 420,031 |

9,081 | | Tenet Healthcare Corp.(a) (b) | 418,634 |

18,067 | | Total System Services, Inc.(a) | 442,280 |

16,584 | | Tyson Foods, Inc., Class A(a) | 425,877 |

6,644 | | UnitedHealth Group, Inc.(a) | 435,049 |

6,155 | | Varian Medical Systems, Inc.(a) (b) | 415,155 |

5,423 | | WellPoint, Inc.(a) | 443,818 |

24,905 | | Western Union Co.(a) | 426,125 |

8,251 | | Whole Foods Market, Inc.(a) | 424,761 |

5,445 | | Zimmer Holdings, Inc.(a) | 408,048 |

13,663 | | Zoetis, Inc.(a) | 422,050 |

| | | | 41,848,276 |

| | | Diversified – 0.2% | |

15,270 | | Leucadia National Corp.(a) | 400,379 |

| | | Energy – 10.6% | |

4,923 | | Anadarko Petroleum Corp.(a) | 423,033 |

4,993 | | Apache Corp.(a) | 418,563 |

9,209 | | Baker Hughes, Inc.(a) | 424,811 |

6,095 | | Cabot Oil & Gas Corp., Class A(a) | 432,867 |

6,826 | | Cameron International Corp.(a) (b) | 417,478 |

20,496 | | Chesapeake Energy Corp.(a) | 417,708 |

3,524 | | Chevron Corp.(a) | 417,030 |

6,945 | | ConocoPhillips(a) | 420,173 |

13,267 | | Consol Energy, Inc.(a) | 359,536 |

23,786 | | Denbury Resources, Inc.(a) (b) | 411,974 |

7,803 | | Devon Energy Corp.(a) | 404,820 |

6,311 | | Diamond Offshore Drilling, Inc.(a) | 434,134 |

7,299 | | Ensco PLC, Class A (United Kingdom)(a) | 424,218 |

3,217 | | EOG Resources, Inc.(a) | 423,615 |

5,320 | | EQT Corp.(a) | 422,248 |

4,680 | | Exxon Mobil Corp.(a) | 422,838 |

7,621 | | FMC Technologies, Inc.(a) (b) | 424,337 |

9,874 | | Halliburton Co.(a) | 411,943 |

6,968 | | Helmerich & Payne, Inc.(a) | 435,152 |

6,426 | | Hess Corp.(a) | 427,265 |

11,033 | | Kinder Morgan, Inc.(a) | 420,909 |

12,328 | | Marathon Oil Corp.(a) | 426,302 |

5,324 | | Marathon Petroleum Corp.(a) | 378,323 |

6,723 | | Murphy Oil Corp.(a) | 409,363 |

26,659 | | Nabors Industries Ltd. (Bermuda)(a) | 408,149 |

6,091 | | National Oilwell Varco, Inc.(a) | 419,670 |

18,839 | | Newfield Exploration Co.(a) (b) | 450,065 |

11,288 | | Noble Corp. (Switzerland)(a) | 424,203 |

7,320 | | Noble Energy, Inc.(a) | 439,493 |

4,614 | | Occidental Petroleum Corp.(a) | 411,707 |

9,560 | | Oneok, Inc.(a) | 394,924 |

25,261 | | Peabody Energy Corp.(a) | 369,821 |

6,642 | | Phillips 66(a) | 391,280 |

2,891 | | Pioneer Natural Resources Co.(a) | 418,472 |

14,482 | | QEP Resources, Inc.(a) | 402,310 |

See notes to financial statements.

10 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

PORTFOLIO OF INVESTMENTS (Unaudited) continued | June 30, 2013 |

| | | | |

Number | | | |

of Shares | | Description | Value |

| | | Energy (continued) | |

5,777 | | Range Resources Corp.(a) | $ 446,678 |

12,676 | | Rowan Companies PLC (United Kingdom)(a) (b) | 431,871 |

5,919 | | Schlumberger Ltd. (Curacao)(a) | 424,156 |

11,599 | | Southwestern Energy Co.(a) (b) | 423,711 |

12,343 | | Spectra Energy Corp.(a) | 425,339 |

7,416 | | Tesoro Corp.(a) | 388,005 |

11,152 | | Valero Energy Corp.(a) | 387,755 |

12,725 | | Williams Cos., Inc.(a) | 413,181 |

22,308 | | WPX Energy, Inc.(a) (b) | 422,514 |

| | | | 18,301,944 |

| | | Financial – 19.5% | |

4,788 | | ACE Ltd. (Switzerland)(a) | 428,430 |

7,371 | | Aflac, Inc.(a) | 428,403 |

9,043 | | Allstate Corp.(a) | 435,149 |

5,809 | | American Express Co.(a) | 434,281 |

9,340 | | American International Group, Inc.(a) (b) | 417,498 |

5,481 | | American Tower Corp., REIT(a) | 401,045 |

5,178 | | Ameriprise Financial, Inc.(a) | 418,797 |

6,532 | | AON PLC (United Kingdom)(a) | 420,334 |

14,651 | | Apartment Investment & Management Co., Class A, REIT(a) | 440,115 |

8,384 | | Assurant, Inc.(a) | 426,829 |

3,149 | | AvalonBay Communities, Inc., REIT(a) | 424,832 |

32,430 | | Bank of America Corp.(a) | 417,050 |

14,551 | | Bank of New York Mellon Corp.(a) | 408,156 |

12,930 | | BB&T Corp.(a) | 438,068 |

3,713 | | Berkshire Hathaway, Inc., Class B(a) (b) | 415,559 |

1,570 | | BlackRock, Inc.(a) | 403,255 |

3,851 | | Boston Properties, Inc., REIT(a) | 406,165 |

6,947 | | Capital One Financial Corp.(a) | 436,341 |

18,697 | | CBRE Group, Inc., Class A(a) (b) | 436,762 |

21,505 | | Charles Schwab Corp.(a) | 456,550 |

4,911 | | Chubb Corp.(a) | 415,716 |

9,179 | | Cincinnati Financial Corp.(a) | 421,316 |

8,611 | | Citigroup, Inc.(a) | 413,070 |

5,705 | | CME Group, Inc.(a) | 433,466 |

11,349 | | Comerica, Inc.(a) | 452,031 |

8,954 | | Discover Financial Services(a) | 426,569 |

37,053 | | E*Trade Financial Corp.(a) (b) | 469,090 |

7,524 | | Equity Residential, REIT(a) | 436,842 |

23,150 | | Fifth Third Bancorp(a) | 417,858 |

2,880 | | Franklin Resources, Inc.(a) | 391,738 |

38,534 | | Genworth Financial, Inc., Class A(a) (b) | 439,673 |

2,603 | | Goldman Sachs Group, Inc.(a) | 393,704 |

14,515 | | Hartford Financial Services Group, Inc.(a) | 448,805 |

9,226 | | HCP, Inc., REIT(a) | 419,229 |

6,292 | | Health Care REIT, Inc., REIT(a) | 421,753 |

24,614 | | Host Hotels & Resorts, Inc., REIT(a) | 415,238 |

51,129 | | Hudson City Bancorp, Inc.(a) | 468,341 |

56,290 | | Huntington Bancshares, Inc.(a) | 443,565 |

2,448 | | IntercontinentalExchange, Inc.(a) (b) | 435,155 |

12,646 | | Invesco Ltd. (Bermuda)(a) | 402,143 |

7,977 | | JPMorgan Chase & Co.(a) | 421,106 |

40,717 | | KeyCorp(a) | 449,516 |

19,259 | | Kimco Realty Corp., REIT(a) | 412,720 |

12,994 | | Legg Mason, Inc.(a) | 402,944 |

12,275 | | Lincoln National Corp.(a) | 447,669 |

9,507 | | Loews Corp.(a) | 422,111 |

4,135 | | M&T Bank Corp.(a) | 462,085 |

6,809 | | Macerich Co., REIT(a) | 415,145 |

10,609 | | Marsh & McLennan Cos., Inc.(a) | 423,511 |

9,641 | | MetLife, Inc.(a) | 441,172 |

16,410 | | Morgan Stanley(a) | 400,896 |

13,002 | | NASDAQ OMX Group, Inc.(a) | 426,336 |

7,420 | | Northern Trust Corp.(a) | 429,618 |

10,472 | | NYSE Euronext(a) | 433,541 |

30,805 | | People's United Financial, Inc.(a) | 458,995 |

8,965 | | Plum Creek Timber Co., Inc., REIT(a) | 418,397 |

5,970 | | PNC Financial Services Group, Inc.(a) | 435,332 |

11,144 | | Principal Financial Group, Inc.(a) | 417,343 |

17,160 | | Progressive Corp.(a) | 436,207 |

11,016 | | ProLogis, Inc., REIT(a) | 415,524 |

6,015 | | Prudential Financial, Inc.(a) | 439,275 |

2,793 | | Public Storage, REIT(a) | 428,251 |

47,202 | | Regions Financial Corp.(a) | 449,835 |

2,552 | | Simon Property Group, Inc., REIT(a) | 403,012 |

18,445 | | SLM Corp.(a) | 421,653 |

6,417 | | State Street Corp.(a) | 418,453 |

13,634 | | SunTrust Banks, Inc.(a) | 430,425 |

5,775 | | T Rowe Price Group, Inc.(a) | 422,441 |

6,555 | | Torchmark Corp.(a) | 426,993 |

5,161 | | Travelers Cos., Inc.(a) | 412,467 |

15,270 | | Unum Group(a) | 448,481 |

12,108 | | US Bancorp(a) | 437,704 |

6,019 | | Ventas, Inc., REIT(a) | 418,080 |

2,342 | | Visa, Inc., Class A(a) | 428,001 |

5,116 | | Vornado Realty Trust, REIT(a) | 423,861 |

10,554 | | Wells Fargo & Co.(a) | 435,564 |

14,984 | | Weyerhaeuser Co., REIT(a) | 426,894 |

13,647 | | XL Group PLC (Ireland)(a) | 413,777 |

15,721 | | Zions Bancorporation(a) | 454,022 |

| | | | 33,768,278 |

See notes to financial statements.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 11 |

PORTFOLIO OF INVESTMENTS (Unaudited) continued | June 30, 2013 |

| | | | |

Number | | | |

of Shares | | Description | Value |

| | | Industrial – 15.5% | |

3,817 | | 3M Co.(a) | $ 417,389 |

9,632 | | Agilent Technologies, Inc.(a) | 411,864 |

5,563 | | Amphenol Corp., Class A(a) | 433,580 |

9,781 | | Ball Corp.(a) | 406,303 |

10,749 | | Bemis Co., Inc.(a) | 420,716 |

4,162 | | Boeing Co.(a) | 426,355 |

5,055 | | Caterpillar, Inc.(a) | 416,987 |

7,503 | | CH Robinson Worldwide, Inc.(a) | 422,494 |

16,995 | | CSX Corp.(a) | 394,114 |

3,650 | | Cummins, Inc.(a) | 395,879 |

6,780 | | Danaher Corp.(a) | 429,174 |

4,993 | | Deere & Co.(a) | 405,681 |

5,394 | | Dover Corp.(a) | 418,898 |

6,564 | | Eaton Corp. PLC (Ireland)(a) | 431,977 |

7,551 | | Emerson Electric Co.(a) | 411,832 |

11,074 | | Expeditors International of Washington, Inc.(a) | 420,923 |

4,277 | | FedEx Corp.(a) | 421,627 |

17,343 | | FLIR Systems, Inc.(a) | 467,742 |

7,522 | | Flowserve Corp.(a) | 406,263 |

6,949 | | Fluor Corp.(a) | 412,145 |

12,570 | | Garmin Ltd. (Switzerland)(a) | 454,532 |

5,434 | | General Dynamics Corp.(a) | 425,645 |

18,021 | | General Electric Co.(a) | 417,907 |

5,421 | | Honeywell International, Inc.(a) | 430,102 |

6,034 | | Illinois Tool Works, Inc.(a) | 417,372 |

7,511 | | Ingersoll-Rand PLC (Ireland)(a) | 417,011 |

21,827 | | Jabil Circuit, Inc.(a) | 444,834 |

7,592 | | Jacobs Engineering Group, Inc.(a) (b) | 418,547 |

8,020 | | Joy Global, Inc.(a) | 389,211 |

3,832 | | Kansas City Southern(a) | 406,039 |

4,927 | | L-3 Communications Holdings, Inc.(a) | 422,441 |

13,132 | | Leggett & Platt, Inc.(a) | 408,274 |

3,936 | | Lockheed Martin Corp.(a) | 426,899 |

20,388 | | Masco Corp.(a) | 397,362 |

14,329 | | Molex, Inc.(a) | 420,412 |

5,565 | | Norfolk Southern Corp.(a) | 404,297 |

5,114 | | Northrop Grumman Corp.(a) | 423,439 |

15,264 | | Owens-Illinois, Inc.(a) (b) | 424,187 |

6,208 | | Pall Corp.(a) | 412,397 |

4,351 | | Parker Hannifin Corp.(a) | 415,085 |

7,098 | | Pentair Ltd. (Switzerland)(a) | 409,484 |

12,828 | | PerkinElmer, Inc.(a) | 416,910 |

1,926 | | Precision Castparts Corp.(a) | 435,295 |

6,288 | | Raytheon Co.(a) | 415,763 |

12,445 | | Republic Services, Inc.(a) | 422,383 |

4,889 | | Rockwell Automation, Inc.(a) | 406,471 |

6,574 | | Rockwell Collins, Inc.(a) | 416,857 |

3,518 | | Roper Industries, Inc.(a) | 437,007 |

6,826 | | Ryder System, Inc.(a) | 414,953 |

17,750 | | Sealed Air Corp.(a) | 425,113 |

4,656 | | Snap-On, Inc.(a) | 416,153 |

5,337 | | Stanley Black & Decker, Inc.(a) | 412,550 |

3,984 | | Stericycle, Inc.(a) (b) | 439,952 |

9,332 | | TE Connectivity Ltd. (Switzerland)(a) | 424,979 |

15,995 | | Textron, Inc.(a) | 416,670 |

4,980 | | Thermo Fisher Scientific, Inc.(a) | 421,457 |

12,725 | | Tyco International Ltd. (Switzerland)(a) | 419,289 |

2,700 | | Union Pacific Corp.(a) | 416,556 |

4,934 | | United Parcel Service, Inc., Class B(a) | 426,691 |

4,508 | | United Technologies Corp.(a) | 418,974 |

7,895 | | Vulcan Materials Co.(a) | 382,197 |

10,682 | | Waste Management, Inc.(a) | 430,805 |

4,298 | | Waters Corp.(a) (b) | 430,015 |

15,630 | | Xylem, Inc.(a) | 421,072 |

| | | | 26,825,532 |

| | | Technology – 11.9% | |

5,262 | | Accenture PLC, Class A (Ireland)(a) | 378,654 |

9,895 | | Adobe Systems, Inc.(a) (b) | 450,817 |

107,581 | | Advanced Micro Devices, Inc.(a) (b) | 438,931 |

9,959 | | Akamai Technologies, Inc.(a) (b) | 423,755 |

13,127 | | Altera Corp.(a) | 433,060 |

9,429 | | Analog Devices, Inc.(a) | 424,871 |

985 | | Apple, Inc.(a) | 390,139 |

27,507 | | Applied Materials, Inc.(a) | 410,129 |

12,080 | | Autodesk, Inc.(a) (b) | 409,995 |

9,397 | | BMC Software, Inc.(a) (b) | 424,181 |

12,544 | | Broadcom Corp., Class A(a) | 423,485 |

14,999 | | CA, Inc.(a) | 429,421 |

4,315 | | Cerner Corp.(a) (b) | 414,628 |

6,922 | | Citrix Systems, Inc.(a) (b) | 417,604 |

6,731 | | Cognizant Technology Solutions Corp., Class A(a) (b) | 421,428 |

9,448 | | Computer Sciences Corp.(a) | 413,539 |

31,657 | | Dell, Inc.(a) | 422,621 |

4,292 | | Dun & Bradstreet Corp.(a) | 418,255 |

19,434 | | Electronic Arts, Inc.(a) (b) | 446,399 |

17,120 | | EMC Corp.(a) | 404,374 |

9,713 | | Fidelity National Information Services, Inc.(a) | 416,105 |

9,480 | | First Solar, Inc.(a) (b) | 424,040 |

4,872 | | Fiserv, Inc.(a) (b) | 425,862 |

17,133 | | Hewlett-Packard Co.(a) | 424,898 |

17,010 | | Intel Corp.(a) | 411,982 |

2,096 | | International Business Machines Corp.(a) | 400,567 |

7,371 | | Intuit, Inc.(a) | 449,853 |

7,608 | | KLA-Tencor Corp.(a) | 423,994 |

See notes to financial statements.

12 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

PORTFOLIO OF INVESTMENTS (Unaudited) continued | June 30, 2013 |

| | | | |

Number | | | |

of Shares | | Description | Value |

| | | Technology (continued) | |

9,003 | | Lam Research Corp.(a) (b) | $ 399,193 |

11,648 | | Linear Technology Corp.(a) | 429,112 |

57,986 | | LSI Corp.(a) (b) | 414,020 |

11,445 | | Microchip Technology, Inc.(a) | 426,326 |

33,219 | | Micron Technology, Inc.(a) (b) | 476,029 |

12,322 | | Microsoft Corp.(a) | 425,479 |

11,184 | | NetApp, Inc.(a) | 422,532 |

29,537 | | NVIDIA Corp.(a) | 414,404 |

12,551 | | Oracle Corp.(a) | 385,567 |

29,052 | | Pitney Bowes, Inc.(a) | 426,483 |

6,905 | | Qualcomm, Inc.(a) | 421,757 |

9,253 | | Red Hat, Inc.(a) (b) | 442,478 |

11,286 | | Salesforce.com, Inc.(a) (b) | 430,899 |

7,208 | | SanDisk Corp.(a) (b) | 440,408 |

9,696 | | Seagate Technology PLC (Ireland)(a) | 434,672 |

7,558 | | Teradata Corp.(a) (b) | 379,638 |

24,445 | | Teradyne, Inc.(a) (b) | 429,499 |

11,947 | | Texas Instruments, Inc.(a) | 416,592 |

6,636 | | Western Digital Corp.(a) | 412,029 |

46,579 | | Xerox Corp.(a) | 422,472 |

10,902 | | Xilinx, Inc.(a) | 431,828 |

| | | | 20,655,004 |

| | | Utilities – 7.3% | |

34,293 | | AES Corp.(a) | 411,173 |

9,861 | | AGL Resources, Inc.(a) | 422,642 |

12,430 | | Ameren Corp.(a) | 428,089 |

9,315 | | American Electric Power Co., Inc.(a) | 417,126 |

17,877 | | CenterPoint Energy, Inc.(a) | 419,931 |

15,469 | | CMS Energy Corp.(a) | 420,293 |

7,331 | | Consolidated Edison, Inc.(a) | 427,471 |

7,564 | | Dominion Resources, Inc.(a) | 429,786 |

6,339 | | DTE Energy Co.(a) | 424,776 |

6,267 | | Duke Energy Corp.(a) | 423,023 |

8,990 | | Edison International(a) | 432,958 |

6,191 | | Entergy Corp.(a) | 431,389 |

13,839 | | Exelon Corp.(a) | 427,348 |

11,059 | | FirstEnergy Corp.(a) | 412,943 |

7,373 | | Integrys Energy Group, Inc.(a) | 431,542 |

5,315 | | NextEra Energy, Inc.(a) | 433,066 |

14,560 | | NiSource, Inc.(a) | 416,998 |

10,061 | | Northeast Utilities(a) | 422,763 |

15,698 | | NRG Energy, Inc.(a) | 419,137 |

20,901 | | Pepco Holdings, Inc.(a) | 421,364 |

9,385 | | PG&E Corp.(a) | 429,176 |

7,365 | | Pinnacle West Capital Corp.(a) | 408,537 |

14,551 | | PPL Corp.(a) | 440,314 |

12,990 | | Public Service Enterprise Group, Inc.(a) | | 424,253 |

8,571 | | SCANA Corp.(a) | | | 420,836 |

5,275 | | Sempra Energy(a) | | | 431,285 |

9,526 | | Southern Co.(a) | | | 420,382 |

24,459 | | TECO Energy, Inc.(a) | | | 420,450 |

10,294 | | Wisconsin Energy Corp.(a) | | | 421,951 |

14,407 | | Xcel Energy, Inc.(a) | | | 408,294 |

| | | | | | 12,699,296 |

| | | Total Common Stocks – 121.3% | | | |

| | | (Cost $179,658,869) | | | 210,007,391 |

| | | Short Term Investments – 1.4% | | |

| | | Money Market Fund – 1.4% | | | |

2,488,749 | | Dreyfus Treasury Prime Cash Management Institutional | |

| | | Shares, 12/31/2050 | | | |

| | | (Cost $2,488,749) | | | 2,488,749 |

| | | Total Investments – 122.7% | | | |

| | | (Cost $182,147,618) | | | 212,496,140 |

| | | Liabilities in excess of Other Assets – 0.0%* | | (65,243) |

| | | Total Value of Options Written – (1.9%) (Premiums | |

| | | received $2,907,556) | | | (3,215,880) |

| | | Borrowings – (20.8% of Net Assets or 16.9% of Total | |

| | | Investments) | | | (36,000,000) |

| | | Net Assets – 100.0% | | | $173,215,017 |

| |

Contracts | | | | | |

(100 shares | | | Expiration | Exercise | |

per contract) | | Options Written (b) | Month | Price | Value |

| | | Call Options Written – (1.9%) | | | |

640 | | Energy Select Sector SPDR Fund | July 2013 | $ 79.00 | $ (63,360) |

2,616 | | Financial Select Sector SPDR Fund | July 2013 | 19.00 | (166,116) |

1,572 | | iShares Russell 2000 Index Fund | July 2013 | 96.00 | (316,758) |

1,180 | | Industrial Select Sector SPDR Fund | July 2013 | 42.00 | (125,670) |

1,412 | | Powershares QQQ Trust Series 1 | July 2013 | 72.00 | (86,838) |

632 | | S&P 500 Index | July 2013 | 1,605.00 | (1,390,400) |

1,359 | | SPDR Dow Jones Industrial | | | |

| | | Average ETF | July 2013 | 148.00 | (318,006) |

1,449 | | SPDR Midcap 400 ETF Trust | July 2013 | 210.00 | (514,395) |

661 | | SPDR S&P Retail ETF | July 2013 | 76.00 | (100,472) |

900 | | SPDR S&P Retail ETF | July 2013 | 77.00 | (97,280) |

1,626 | | Technology Select Sector SPDR | | | |

| | | Fund | July 2013 | 31.00 | (36,585) |

| | | Total Value of Call Options Written – (1.9%) | | |

| | | Premiums received ($2,907,556) | | | $(3,215,880) |

See notes to financial statements.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 13 |

PORTFOLIO OF INVESTMENTS (Unaudited) continued | June 30, 2013 |

NV – Publicly Traded Company

PLC – Public Limited Company

REIT – Real Estate Investment Trust

* Less than 0.1%.

(a) All or a portion of these securities have been physically segregated in connection with borrowings. As of June 30, 2013, the total amount segregated was $212,484,608.

(b) Non-income producing security.

(c) When-issued or delayed delivery security.

Securities are classified by sectors that represent broad grouping of industries.

See notes to financial statements.

14 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

STATEMENT OF ASSETS AND LIABILITIES (Unaudited) | June 30, 2013 |

| | | |

Assets | | |

Investments, at value (cost $182,147,618) | $ | 212,496,140 | |

Receivable for securities sold | | 489,456 | |

Dividends receivable | | 241,863 | |

Other assets | | 7,118 | |

Total assets | | 213,234,577 | |

Liabilities | | | |

Borrowings | | 36,000,000 | |

Options written, at value (premiums received of $2,907,556) | | 3,215,880 | |

Payable for securities purchased | | 392,297 | |

Advisory fee payable | | 158,642 | |

Custodian bank | | 24,009 | |

Interest due on borrowings | | 21,328 | |

Administration fee payable | | 4,352 | |

Accrued expenses and other liabilities | | 203,052 | |

Total liabilities | | 40,019,560 | |

Net Assets | $ | 173,215,017 | |

Composition of Net Assets | | | |

Common shares, $.01 par value per share; unlimited number of shares authorized, | | | |

8,770,121 shares issued and outstanding | $ | 87,701 | |

Additional paid-in capital | | 156,387,971 | |

Accumulated net realized loss on investments and options | | (5,896,637 | ) |

Accumulated net unrealized appreciation on investments and options | | 30,040,198 | |

Distributions in excess of net investment income | | (7,404,216 | ) |

Net Assets | $ | 173,215,017 | |

Net Asset Value (based on 8,770,121 common shares outstanding) | $ | 19.75 | |

See notes to financial statements.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 15 |

STATEMENT OF OPERATIONS For the six months ended June 30, 2013 (Unaudited) | June 30, 2013 |

| | | | | | |

Investment Income | | | | | |

Dividends (net of foreign withholding taxes of $1,598) | $ | 1,675,495 | | | | |

Less return of capital distributions received | | (1,037 | ) | | | |

Total income | | | | | $ | 1,674,458 | |

Expenses | | | | | | | |

Advisory fee | | 984,025 | | | | | |

Interest expense | | 152,677 | | | | | |

Professional fees | | 63,680 | | | | | |

Custodian fee | | 36,794 | | | | | |

Fund accounting | | 35,871 | | | | | |

Trustees' fees and expenses | | 32,762 | | | | | |

Administrative fee | | 26,966 | | | | | |

Licensing fee | | 24,862 | | | | | |

Printing expense | | 16,441 | | | | | |

Insurance | | 10,935 | | | | | |

NYSE listing fee | | 10,498 | | | | | |

Transfer agent fee | | 8,874 | | | | | |

Miscellaneous | | 433 | | | | | |

Total expenses | | | | | | 1,404,818 | |

Net investment income | | | | | | 269,640 | |

Realized and Unrealized Gain (Loss) on Investments and Options | | | | | | | |

Net realized gain (loss) on: | | | | | | | |

Investments | | | | | | 15,614,326 | |

Options | | | | | | (14,579,519 | ) |

Net change in unrealized appreciation (depreciation) on: | | | | | | | |

Investments | | | | | | 12,860,257 | |

Options | | | | | | (492,466 | ) |

Net realized and unrealized gain on investments and options | | | | | | 13,402,598 | |

Net Increase in Net Assets Resulting from Operations | | | | | $ | 13,672,238 | |

See notes to financial statements.

16 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

STATEMENTS OF CHANGES IN NET ASSETS | June 30, 2013 |

| | | | | | | | | |

| | | | | | | | For the Period | |

| For the Six Months | | | For the Period | | | October 27, 2011** | |

| Ended June 30, 2013 | | | Year Ended | | | through | |

| | (unaudited) | | | December 31, 2012* | | | June 30, 2012 | |

Increase in Net Assets Resulting from Operations | | | | | | | | |

Net investment income | $ | 269,640 | | | $ | 1,062,564 | | | $ | 757,920 | |

Net realized gain (loss) on investments and options | | 1,034,807 | | | | (6,890,949 | ) | | | 2,783,860 | |

Net change in unrealized appreciation on investments and options | | 12,367,791 | | | | 11,984,063 | | | | 5,688,344 | |

Net increase in net assets resulting from operations | | 13,672,238 | | | | 6,155,678 | | | | 9,230,124 | |

Distributions to Shareholders | | | | | | | | | | | |

From and in excess of net investment income | | (7,673,856 | ) | | | (962,285 | ) | | | (3,695,304 | ) |

Return of capital | | – | | | | (6,705,060 | ) | | | (3,965,531 | ) |

| | | (7,673,856 | ) | | | (7,667,345 | ) | | | (7,660,835 | ) |

Capital Share Transactions | | | | | | | | | | | |

Net proceeds from the issuance of common shares | | – | | | | – | | | | 167,125,000 | |

Reinvestment of dividends | | – | | | | 283,929 | | | | – | |

Common share offering costs charged to paid-in capital | | – | | | | – | | | | (350,000 | ) |

Net increase from capital share transactions | | – | | | | 283,929 | | | | 166,775,000 | |

Total increase (decrease) in net assets | | 5,998,382 | | | | (1,227,738 | ) | | | 168,344,289 | |

Net Assets: | | | | | | | | | | | |

Beginning of period | | 167,216,635 | | | | 168,444,373 | | | | 100,084 | |

End of period (including distributions in excess of net | | | | | | | | | | | |

investment income of $7,404,216, $0 and $0, respectively) | $ | 173,215,017 | | | $ | 167,216,635 | | | $ | 168,444,373 | |

| * | Fiscal year end changed from June 30 to December 31. |

| ** | Commencement of investment operations |

See notes to financial statements.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 17 |

STATEMENT OF CASH FLOWS For the six months ended June 30, 2013 (Unaudited) | June 30, 2013 |

| | | | |

Cash Flows from Operating Activities: | | | |

Net increase in net assets resulting from operations | | $ | 13,672,238 | |

Adjustments to Reconcile Net Increase in Net Assets Resulting from Operations to | | | | |

Net Cash Provided by Operating and Investing Activities: | | | | |

Net unrealized appreciation on investments | | | (12,860,257 | ) |

Net unrealized depreciation on options | | | 492,466 | |

Net realized gain on investments | | | (15,614,326 | ) |

Net realized loss on options | | | 14,579,519 | |

Purchase of long-term investments | | | (156,886,024 | ) |

Cost of written options closed | | | (29,642,617 | ) |

Premiums received on call options written | | | 16,029,715 | |

Proceeds from sale of long-term investments | | | 175,078,430 | |

Net purchases of short-term investments | | | (239,056 | ) |

Increase in dividends receivable | | | (36,065 | ) |

Increase in receivable for securities sold | | | (82,660 | ) |

Increase in other assets | | | (7,118 | ) |

Decrease in tax reclaims receivable | | | 1,308 | |

Decrease in investments purchased payable | | | (14,253 | ) |

Decrease in dividends payable | | | (761,936 | ) |

Decrease in advisory fee payable | | | (13,638 | ) |

Increase in custodian bank | | | 1,680 | |

Decrease in administration fee payable | | | (366 | ) |

Decrease in interest due on borrowings | | | (15,804 | ) |

Return of capital distributions received | | | 1,037 | |

Decrease in accrued expenses and other liabilities | | | (8,417 | ) |

Net Cash Provided by Operating and Investing Activities | | | 3,673,856 | |

Cash Flows From Financing Activities: | | | | |

Proceeds from borrowings | | | 45,500,000 | |

Payments made on borrowings | | | (41,500,000 | ) |

Distributions to shareholders | | | (7,673,856 | ) |

Net Cash Used in Financing Activities | | | (3,673,856 | ) |

Net change in cash | | | – | |

Cash at Beginning of Period | | | – | |

Cash at End of Period | | $ | – | |

Supplemental Disclosure of Cash Flow Information: Cash paid during the period for interest | | $ | 168,481 | |

Supplemental Disclosure of Non Cash Operating Activity: Options exercised during the period | | $ | 908,708 | |

See notes to financial statements.

18 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

| | | | | | | | | | |

| | | | | | | | | For the Period | |

| | | For the Six Months | | | For the Period | | | October 27, 2011** | |

Per share operating performance | | Ended June 30, 2013 | | | Year Ended | | | through | |

for a common share outstanding throughout the period | | (unaudited) | | | December 31, 2012* | | | June 30, 2012 | |

Net asset value, beginning of period | | $ | 19.07 | | | $ | 19.24 | | | $ | 19.10 | (a) |

Investment operations | | | | | | | | | | | | |

Net investment income (b) | | | 0.03 | | | | 0.12 | | | | 0.09 | |

Net realized and unrealized gain on investments and options | | | 1.53 | | | | 0.59 | | | | 0.97 | |

Total from investment operations | | | 1.56 | | | | 0.71 | | | | 1.06 | |

Common shares’ offering expenses charged to paid-in-capital | | | – | | | | – | | | | (0.04 | ) |

Distributions to Shareholders | | | | | | | | | | | | |

From and in excess of net investment income | | | (0.88 | ) | | | (0.11 | ) | | | (0.42 | ) |

Return of capital | | | – | | | | (0.77 | ) | | | (0.46 | ) |

Total distributions to shareholders | | | (0.88 | ) | | | (0.88 | ) | | | (0.88 | ) |

Net asset value, end of period | | $ | 19.75 | | | $ | 19.07 | | | $ | 19.24 | |

Market value, end of period | | $ | 18.19 | | | $ | 17.73 | | | $ | 18.61 | |

Total investment return (c) | | | | | | | | | | | | |

Net asset value | | | 8.22 | % | | | 3.69 | % | | | 5.30 | % |

Market value | | | 7.46 | % | | | -0.35 | % | | | -2.57 | % |

Ratios and supplemental data | | | | | | | | | | | | |

Net assets end of period (thousands) | | $ | 173,215 | | | $ | 167,217 | | | $ | 168,444 | |

Ratios to Average Net Assets: | | | | | | | | | | | | |

Total expenses, excluding interest expense | | | 1.46 | %(d) | | | 1.54 | %(d) | | | 1.59 | %(d) |

Total expenses, including interest expense | | | 1.64 | %(d) | | | 1.78 | %(d) | | | 1.80 | %(d) |

Net investment income, including interest expense | | | 0.32 | %(d) | | | 1.25 | %(d) | | | 0.71 | %(d) |

Portfolio Turnover(e) | | | 79 | % | | | 54 | % | | | 31 | % |

Senior Indebtedness: | | | | | | | | | | | | |

Total Borrowings outstanding (in thousands) | | $ | 36,000 | | | $ | 32,000 | | | $ | 34,000 | |

Asset Coverage per $1,000 of indebtedness(f) | | $ | 5,812 | | | $ | 6,226 | | | $ | 5,954 | |

| * | Fiscal year end changed from June 30 to December 31. |

| ** | Commencement of investment operations. |

| (a) | Before deduction of offering expenses charged to capital. |

| (b) | Based on average shares outstanding. |

| (c) | Total investment return is calculated assuming a purchase of a common share at the beginning of the period and a sale on the last day of the period reported either at net asset value (NAV) or market price per share. Dividends and distributions are assumed to be reinvested at NAV for NAV returns or the prices obtained under the Fund's Dividend Reinvestment Plan market value returns. Total investment return does not reflect brokerage commissions. A return calculated for a period of less than one year is not annualized. |

| (d) | Annualized. |

| (e) | Portfolio turnover is not annualized for periods of less than one year. |

| (f) | Calculated by subtracting the Fund's total liabilities (not including borrowings) from the Fund's total assets and dividing by the total borrowings. |

See notes to financial statements.

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 19 |

NOTES TO FINANCIAL STATEMENTS (Unaudited) | June 30, 2013 |

Note 1 – Organization:

Guggenheim Equal Weight Enhanced Equity Income Fund (the “Fund”) was organized as a Delaware statutory trust on July 11, 2011. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Fund’s investment objective is to provide a high level of risk-adjusted total return with an emphasis on current income. There can be no assurance that the Fund will achieve its investment objectives. The Fund’s investment objective is considered fundamental and may not be changed without shareholder approval.

Note 2 – Accounting Policies:

The preparation of the financial statements in accordance with U.S. generally accepted accounting principles (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates.

The following is a summary of significant accounting policies consistently followed by the Fund.

(a) Valuation of Investments

The Fund values equity securities at the last reported sale price on the principal exchange or in the principal over-the-counter (“OTC”) market in which such securities are traded, as of the close of regular trading on the New York Stock Exchange (“NYSE”) on the day the securities are being valued or, if there are no sales, at the mean between the last available bid and ask prices on that day. Securities traded on the NASDAQ are valued at the NASDAQ Official Closing Price. Preferred stocks are valued at their sales price as of the close of the exchange on which they are traded. Preferred stocks for which the last price is not available are valued at the mean between the last available bid and ask prices on that day. Equity index options are valued at the mean between the last available bid and ask prices on the primary exchange on which they are traded. Exchange-traded options are valued at the mean of the best bid and ask prices at the close on those exchanges on which they are traded. The Fund values money market funds at net asset value. Short-term securities with remaining maturities of 60 days or less, at the time of purchase, are valued at amortized cost, which approximated market value.

For those securities where quotations or prices are not available, the valuations are determined in accordance with procedures established in good faith by management and approved by the Board of Trustees (“Trustees”). A valuation committee consisting of representatives from investments, fund administration, legal and compliance is responsible for the oversight of the valuation process of the Fund and convenes monthly, or more frequently as needed. The valuation committee reviews monthly Level 3 fair valued securities methodology, price overrides, broker quoted securities price source changes, illiquid securities, unchanged valuations, halted securities, price challenges, fair valued securities sold and back testing trade prices in relation to prior day closing prices. On a quarterly basis, the valuations and methodologies of all Level 3 fair valued securities are presented to the Fund’s Trustees.

Valuations in accordance with these procedures are intended to reflect each security’s (or asset’s) “fair value.” Fair value is defined as the price that the Fund would receive to sell an investment or pay to transfer a liability in an orderly transaction with an independent buyer in the principal market, or in the absence of a principal market, the most advantageous market for the investment or liability. Each such determination is based on a consideration of all relevant factors, which are likely to vary from one pricing context to another. Examples of such factors may include, but are not limited to: (i) the type of security, (ii) the initial cost of the security, (iii) the existence of any contractual restrictions on the security’s disposition, (iv) the price and extent of public trading in similar securities of the issuer or of comparable companies, (v) quotations or evaluated prices from broker-dealers and/or pricing services, (vi) information obtained from the issuer, analysts, and/or the appropriate stock exchange (for exchange traded securities), (vii) an analysis of the company’s financial statements, and (viii) an evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold (e.g. the existence of pending merger activity, public offerings or tender offers that might affect the value of the security).

There are three different categories for valuations. Level 1 valuations are those based upon quoted prices in active markets. Level 2 valuations are those based upon quoted prices in inactive markets or based upon significant observable inputs (e.g. yield curves; benchmark interest rates; indices). Level 3 valuations are those based upon unobservable inputs (e.g. discounted cash flow analysis; non-market based methods used to determine fair valuation).

The Fund values Level 1 securities using readily available market quotations in active markets. Money market funds are valued at net asset value. The fund values Level 2 fixed income securities using independent pricing providers who employ matrix pricing models utilizing market prices, broker quotes and prices of securities with comparable maturities and qualities. The Fund values Level 2 equity securities using various observable market inputs as described above. The Fund did not have any Level 2 or Level 3 securities during the six months ended June 30, 2013.

Transfers between valuation levels, if any, are in comparison to the valuation levels at the end of the previous fiscal year, and are effective as of the beginning of the period.

20 | GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT |

NOTES TO FINANCIAL STATEMENTS (Unaudited) continued | June 30, 2013 |

The following table represents the Fund’s investments carried on the Statement of Assets and Liabilities by caption and by level within the fair value hierarchy at June 30, 2013.

| | | | | | | | | | | | | |

Description | | | | | | | | | | | | |

(value in $000s) | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Assets: | | | | | | | | | | | | |

Common Stocks | | $ | 210,007 | | | $ | – | | | $ | – | | | $ | 210,007 | |

Money Market Fund | | | 2,489 | | | | – | | | | – | | | | 2,489 | |

Total | | $ | 212,496 | | | $ | – | | | $ | – | | | $ | 212,496 | |

Liabilities: | | | | | | | | | | | | | | | | |

Call Options Written | | $ | 3,216 | | | $ | – | | | $ | – | | | $ | 3,216 | |

Total | | $ | 3,216 | | | $ | – | | | $ | – | | | $ | 3,216 | |

During the six months ended June 30, 2013, there were no transfers between levels.

(b) Investment Transactions and Investment Income

Investment transactions are accounted for on the trade date. Realized gains and losses on investments are determined on the identified cost basis. Dividend income is recorded net of applicable withholding taxes on the ex-dividend date and interest income is recorded on an accrual basis. Discounts on debt securities purchased are accreted to interest income over the lives of the respective securities using the effective interest method. Premiums on debt securities purchased are amortized to interest income up to the next call date of the respective securities using the effective interest method.

(c) Options

The Fund will utilize a call option writing strategy to seek to generate current income and potentially mitigate overall portfolio volatility. The option strategy will include writing (i.e. selling) call options on securities indices, exchange-traded funds that track securities indices, baskets of securities and other instruments, which will include securities that are not held by the Fund.

An option on a security is a contract that gives the holder of the option, in return for a premium, the right to buy from (in the case of a call) or sell to (in the case of a put) the writer of the option the security underlying the option at a specific exercise or “strike” price. The writer of an option on a security has an obligation upon exercise of the option to deliver the underlying security upon payment of the exercise price (in the case of a call) or to pay the exercise price upon delivery of the underlying security (in the case of a put). When an option is written, the premium received is recorded as an asset with an equal liability and is subsequently marked to market to reflect the current market value of the option written. These liabilities are reflected as options written in the Statement of Assets and Liabilities. Premiums received from writing options which expire unexercised are recorded on the expiration date as a realized gain. The difference between the premium received and the amount paid on effecting a closing purchase transaction, including brokerage commissions, is also treated as a realized gain, or if the premium is less than the amount paid for the closing purchase transactions, as a realized loss. If an option is exercised, the premium is added to the cost of the purchase (in the case of a put) or proceeds from the sale of the underlying security (in case of a call) in determining whether there has been a realized gain or loss.

As the seller of an index call option, the Fund receives cash (the premium) from the purchaser. The purchaser of an index call option has the right to any appreciation in the value of the index over a fixed price (the exercise price) on or before a certain date in the future (the expiration date). The Fund, in effect, agrees to sell the potential appreciation in the value of the relevant index over the exercise price in exchange for the premium. If, at or before expiration, the purchaser exercises the call option sold by the Fund, the Fund will pay the purchaser the difference between the cash value of the index and the exercise price of the index option (the exercise settlement amount). The premium, the exercise price and the market value of the index determine the gain or loss realized by the Fund as the seller of the index call option.

Options on an index differ from options on securities because (i) the exercise of an index option requires cash payments and does not involve the actual purchase or sale of securities, (ii) the holder of an index call option has the right to receive cash (instead of securities) upon exercise of the option in an amount equal to the amount by which the level of the index exceeds the exercise price and (iii) index options reflect price-fluctuations in a group of securities or segments of the securities market rather than price fluctuations in a single security.

(d) Distributions

The Fund declares and pays quarterly distributions to shareholders. Any net realized long-term capital gains are distributed annually. Distributions to shareholders are recorded on the ex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from GAAP.

Note 3 – Investment Advisory Agreement, Sub-Advisory Agreement and Other Agreements:

Pursuant to an Investment Advisory Agreement between the Fund and Guggenheim Funds Investment Advisors, LLC (“GFIA” or the “Adviser”), the Adviser furnishes offices, necessary facilities and equipment, provides personnel, including certain officers required for the Fund’s administrative management and compensates the officers or trustees of the Fund who are affiliates of the Adviser. As compensation for these services, the Fund pays the Adviser a fee, payable monthly, in an amount equal to 1.00% of the Fund’s average daily managed assets (net assets plus any assets attributable to financial leverage).

|

| GEQ | GUGGENHEIM EQUAL WEIGHT ENHANCED EQUITY INCOME FUND SEMIANNUAL REPORT | 21 |

NOTES TO FINANCIAL STATEMENTS (Unaudited) continued | June 30, 2013 |

The Fund and the Adviser have entered into a Sub-Advisory Agreement (the “Options Strategy Sub-Advisory Agreement”) with Guggenheim Partners Investment Management, LLC (“GPIM”). GPIM is responsible for the management of the Fund’s options strategy. Under the terms of the Options Strategy Sub-Advisory Agreement, the Adviser pays monthly to GPIM a fee at the annual rate of 0.50% of the Fund’s average daily managed assets.