EXHIBIT 99.2

January 25, 2021

CONFIDENTIAL This presentation contains forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 , as amended, including, without limitation, those that contain, or are identified by, words such as “outlook”, “guidance”, “believes”, “expects”, “potential” , “ continues”, “may”, “will”, “should”, “predicts”, “intends”, “plans”, “estimates”, “anticipates”, “could” or the negative version of these words or other comparabl e w ords. Forward - looking statements include, without limitation, projections, predictions, expectations, or beliefs about future events or results and are not st ate ments of historical fact, including the Company’s expectations regarding its financial condition, statements relating to the Transaction, the Financing and anticipat ed benefits resulting therefrom, the performance of PSP and the success of PSP its strategic growth plans if the Transaction and/or the Financing are consummated, wh ich are subject to various significant risks and uncertainties, many of which are outside of the control of the Company and the effects of the coronavir us (COVID - 19) pandemic on economic conditions and the industry in general, the success of its financing efforts and the financial position and operatin g r esults of the Company. Such forward - looking statements are based on various assumptions as of the time they are made, and are inherently subject to known an d unknown risks, uncertainties and other factors that may cause actual results, performance or achievements to be materially different from any future resul ts, performance or achievements expressed or implied by such forward - looking statements. Forward - looking statements are often accompanied by words that convey p rojected future events or outcomes such as “expect,” “believe,” “estimate,” “plan,” “project,” “anticipate,” “intend,” “will,” “may,” “view,” “opportun ity ,” “potential,” or words of similar meaning or other statements concerning opinions or judgment of the Company or its management about future events. Although th e C ompany believes that its expectations with respect to forward - looking statements are based upon reasonable assumptions within the bounds of its existing knowledge of its business and operations, there can be no assurance that actual results, performance, or achievements of the Company will not differ materi all y from any projected future results, performance or achievements expressed or implied by such forward - looking statements. Actual future results, performance or achievements may differ materially from historical results or those anticipated depending on a variety of factors, many of which are beyond the contr ol of the Company. Additional factors that could cause actual results to differ materially from forward - looking statements include, among others, the risk that the Tr ansaction and/or the Financing may not be completed in a timely manner or at all, which may adversely affect the business and stock price of the Company; the ri sk of any event, change or other circumstance that could give rise to the termination of the equity purchase agreement; the effect of the announcement or pend enc y of the Transaction on the ability of the Company and PSP to retain and hire key personnel and maintain relationships with their franchisees, customers, su ppliers, partners and others with whom they do business, or on their respective operating results and business generally; risks associated with the diversion o f m anagement’s attention from ongoing business operations due to the Transaction and/or the Financing; legal proceedings related to the Transaction and/or the Financing; costs, charges or expenses resulting from the Transaction and/or the Financing; growth of the franchise base at PSP; the strength of the econom y; changes in the overall level of consumer spending; the performance of the products and services of the Company and PSP within the prevailing retail or other bus iness environment; implementation of the strategy of the Company and PSP; maintaining appropriate levels of inventory; changes in tax policy; or th e failure to satisfy any of the other conditions to the completion of the Transaction and/or the Financing. We refer you to the “Risk Factors” and “Managemen t’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s Transition Report on Form 10 - K/T for the transition per iod ended December 28, 2019, and comparable sections of the Company’s Quarterly Reports on Form 10 - Q and other filings, which have been filed with the SEC an d are available on the SEC’s website at www.sec.gov. All of the forward - looking statements made in this press release are expressly qualified by the cautiona ry statements contained or referred to herein. The actual results or developments anticipated may not be realized or, even if substantially realized, th ey may not have the expected consequences to or effects on the Company or its business or operations. Readers are cautioned not to rely on the forward - lookin g statements contained in this press release. Forward - looking statements speak only as of the date they are made and the Company does not undertake any obligat ion to update, revise or clarify these forward - looking statements, whether as a result of new information, future events or otherwise. Forward Looking Statements 2

CONFIDENTIAL Transaction summary 3 • Franchise Group, Inc. (“FRG" or the "Company") signed a definitive agreement to acquire Pet Supplies Plus (“PSP”) for $700 million in cash – FRG estimates that the net present value of the tax benefit related to the Transaction is approximately $100 million • PSP is headquartered in Livonia, MI and is a leading U.S. pet care franchisor; the Company has over 520 locations, including over 300 franchised locations • On a combined basis, Franchise Group will operate over 4,600 locations that are either Company - run or operated pursuant to a franchising agreement – Combined 2020 estimated revenue of ~$3 billion, with FRG and PSP system wide sales of ~$3.6 billion • FRG has obtained commitments from lenders to provide $1.3 billion of debt financing to refinance FRG’s existing term loan and provide acquisition financing for the Transaction • Pro forma for the transaction, FRG will have Net Total Leverage of under 3.4x

CONFIDENTIAL Key investment highlights 4 • Adds diversification to Franchise Group’s capex - light, strong cash generating franchise business model – ~60% of PSP is already franchised – Pro forma for PSP, ~67% of all FRG locations will be franchised • Unique and strong operator – Differentiated in - store and omnichannel platform with same day delivery – Diversified revenue stream – in - store services, self - distribution, private label – Deep pipeline of franchising and refranchising opportunities including independent conversions – Opportunity to continue to delver through refranchising • Strong unit economics – 2 to 3 - year payback on a ~$500k investment – Average of ~$185k unit level contribution to PSP from a franchise unit and over $250k per corporate location • Strong growth profile with franchise backlog provides visibility into near - term growth – Over 185 units in backlog, with many in LOI, signed leases, or onboarding; the remaining are in site selection – Diversified revenue model comprised of corporate store revenue, royalties and revenue from internal distribution to franchisees with over 50% of cash flow coming from the franchise system • Defensible category with economic resilience • Experienced and strong management team with franchising expertise • Opportunity to drive incremental operating efficiencies on the FRG platform

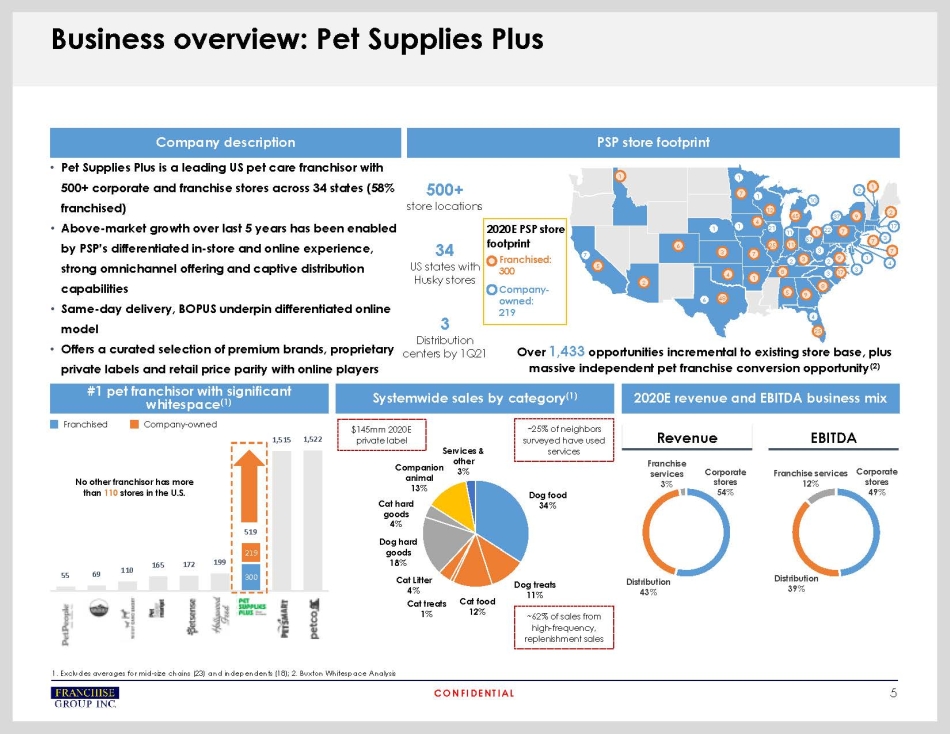

CONFIDENTIAL Business overview: Pet Supplies Plus Company description PSP store footprint • Pet Supplies Plus is a leading US pet care franchisor with 500+ corporate and franchise stores across 34 states (58% franchised) • Above - market growth over last 5 years has been enabled by PSP’s differentiated in - store and online experience, strong omnichannel offering and captive distribution capabilities • Same - day delivery, BOPUS underpin differentiated online model • Offers a curated selection of premium brands, proprietary private labels and retail price parity with online players 500+ store locations 34 US states with Husky stores 3 Distribution centers by 1Q21 300 219 55 69 110 165 172 199 519 1,515 1,522 No other franchisor has more than 110 stores in the U.S. Franchised Company - owned Dog food 34% Dog treats 11% Cat food 12% Cat treats 1% Cat Litter 4% Dog hard goods 18% Cat hard goods 4% Companion animal 13% Services & other 3% ~25% of neighbors surveyed have used services ~62% of sales from high - frequency, replenishment sales $145mm 2020E private label #1 pet franchisor with significant whitespace (1) Systemwide sales by category (1) 2020E revenue and EBITDA business mix Over 1,433 opportunities incremental to existing store base, plus massive independent pet franchise conversion opportunity (2) 7 5 2 1 6 6 48 3 4 1 7 4 1 1 12 1 21 25 5 9 4 25 8 2 3 2 9 8 45 10 1 7 11 11 57 1 22 7 9 37 1 2 2 17 3 7 7 4 1 3 3 17 3 5 1. Excludes averages for mid - size chains (23) and independents (18); 2. Buxton Whitespace Analysis Corporate stores 54% Distribution 43% Franchise services 3% Corporate stores 49% Distribution 39% Franchise services 12% Revenue EBITDA 2020E PSP store footprint Franchised: 300 Company - owned: 219

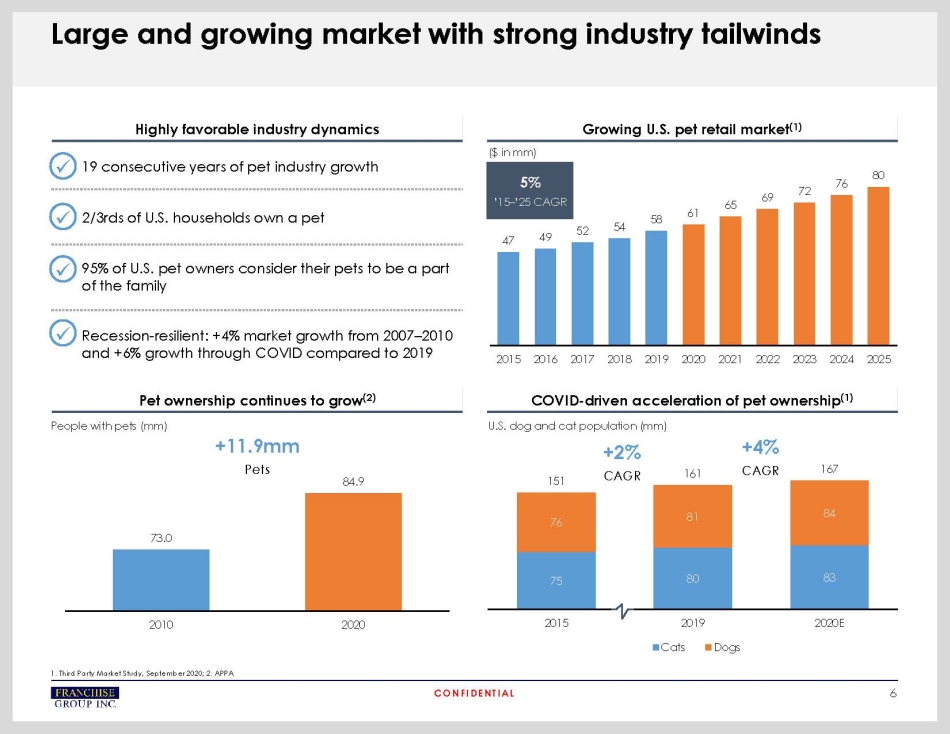

CONFIDENTIAL 6 Highly favorable industry dynamics Growing U.S. pet retail market (1) Pet ownership continues to grow (2) COVID - driven acceleration of pet ownership (1) • 19 consecutive years of pet industry growth • 2/3rds of U.S. households own a pet • 95% of U.S. pet owners consider their pets to be a part of the family • Recession - resilient: +4% market growth from 2007 – 2010 and +6% growth through COVID compared to 2019 x x x x 73.0 84.9 2010 2020 75 80 83 76 81 84 151 161 167 2015 2019 2020E Cats Dogs 47 49 52 54 58 61 65 69 72 76 80 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 ($ in mm) 5% ’15 – ’25 CAGR U.S. dog and cat population (mm) People with pets (mm) +2% CAGR +4% CAGR +11.9mm Pets 1. Third Party Market Study, September 2020; 2. APPA Large and growing market with strong industry tailwinds

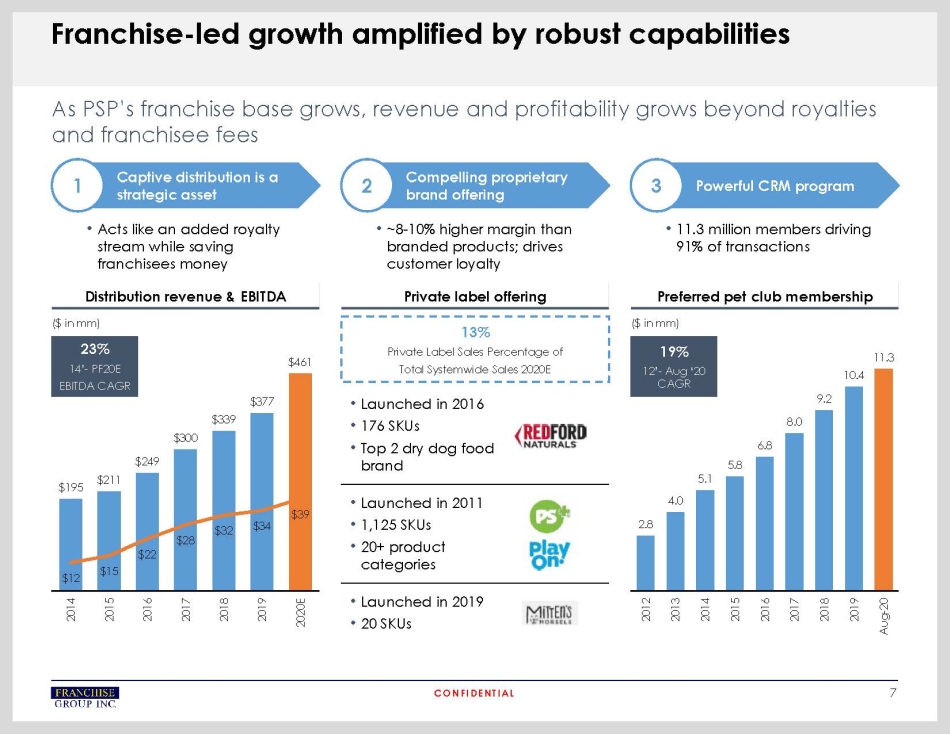

CONFIDENTIAL Captive distribution is a strategic asset Compelling proprietary brand offering Powerful CRM program As PSP’s franchise base grows, revenue and profitability grows beyond royalties and franchisee fees Franchise - led growth amplified by robust capabilities 1 2 3 • Acts like an added royalty stream while saving franchisees money • ~8 - 10% higher margin than branded products; drives customer loyalty • 11.3 million members driving 91% of transactions Distribution revenue & EBITDA Private label offering Preferred pet club membership ($ in mm) ($ in mm) 23% 14’ - PF20E EBITDA CAGR 19% 12’ - Aug ‘20 CAGR $195 $211 $249 $300 $339 $377 $461 $12 $15 $22 $28 $32 $34 $39 2014 2015 2016 2017 2018 2019 2020E 2.8 4.0 5.1 5.8 6.8 8.0 9.2 10.4 11.3 2012 2013 2014 2015 2016 2017 2018 2019 Aug-20 13% Private Label Sales Percentage of Total Systemwide Sales 2020E • Launched in 2016 • 176 SKUs • Top 2 dry dog food brand • Launched in 2011 • 1,125 SKUs • 20+ product categories • Launched in 2019 • 20 SKUs 7

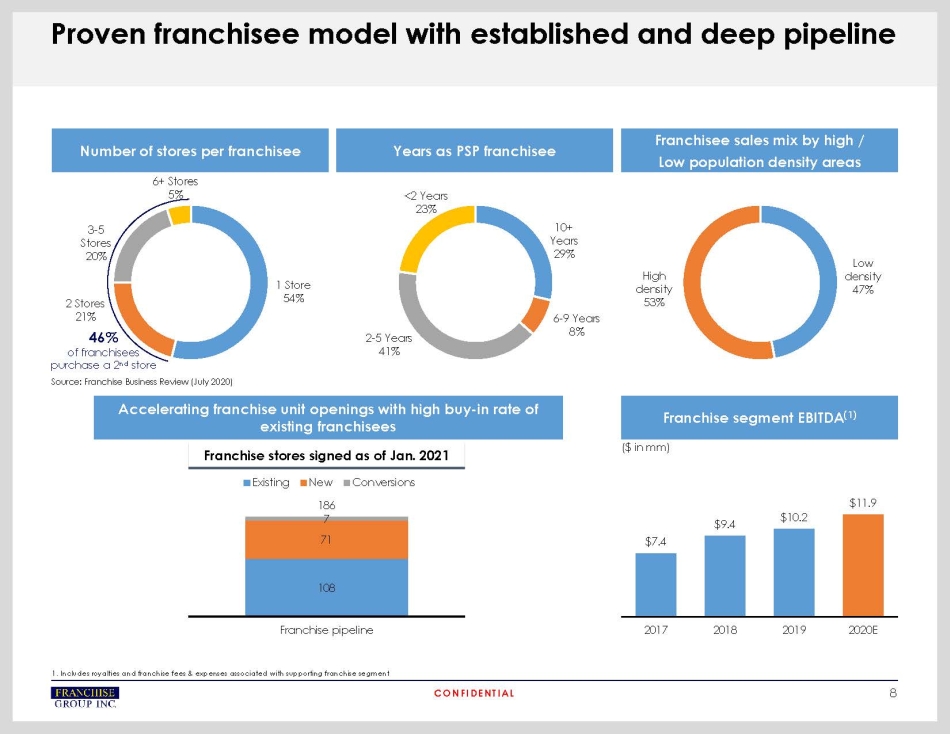

CONFIDENTIAL Proven franchisee model with established and deep pipeline Number of stores per franchisee Years as PSP franchisee Franchisee sales mix by high / Low population density areas 1 Store 54% 2 Stores 21% 3 - 5 Stores 20% 6+ Stores 5% 46% of franchisees purchase a 2 nd store 10+ Years 29% 6 - 9 Years 8% 2 - 5 Years 41% <2 Years 23% Low density 47% High density 53% Accelerating franchise unit openings with high buy - in rate of existing franchisees Franchise segment EBITDA (1) Source: Franchise Business Review (July 2020) Franchise stores signed as of Jan. 2021 108 71 7 186 Franchise pipeline Existing New Conversions ($ in mm) $7.4 $9.4 $10.2 $11.9 2017 2018 2019 2020E 8 1. Includes royalties and franchise fees & expenses associated with supporting franchise segment

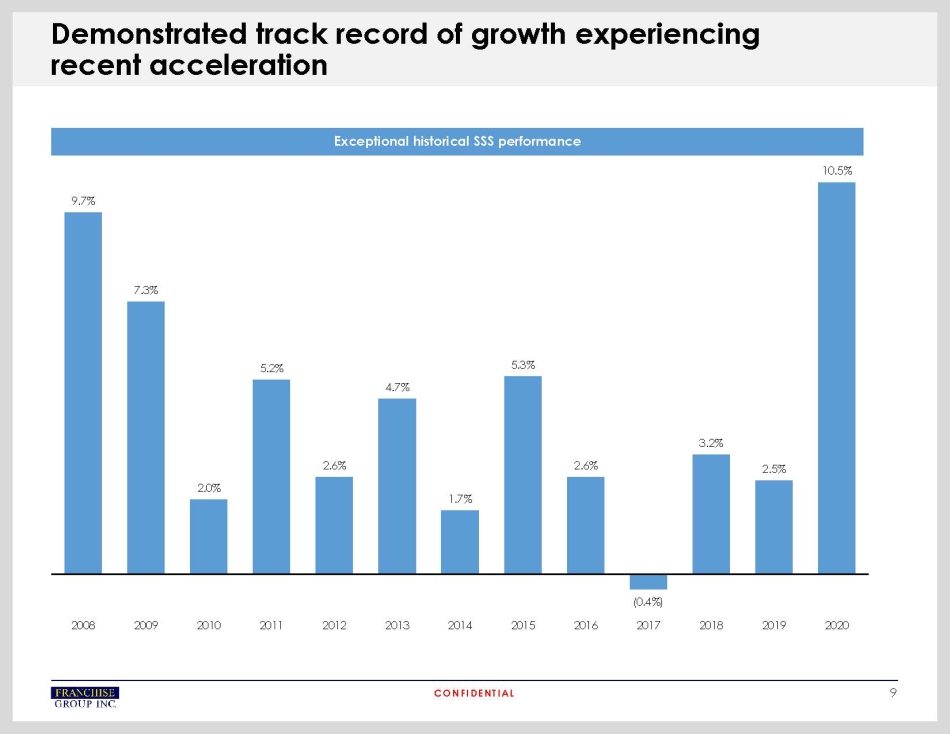

CONFIDENTIAL Demonstrated track record of growth experiencing recent acceleration Exceptional historical SSS performance 9.7% 7.3% 2.0% 5.2% 2.6% 4.7% 1.7% 5.3% 2.6% (0.4%) 3.2% 2.5% 10.5% 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 9

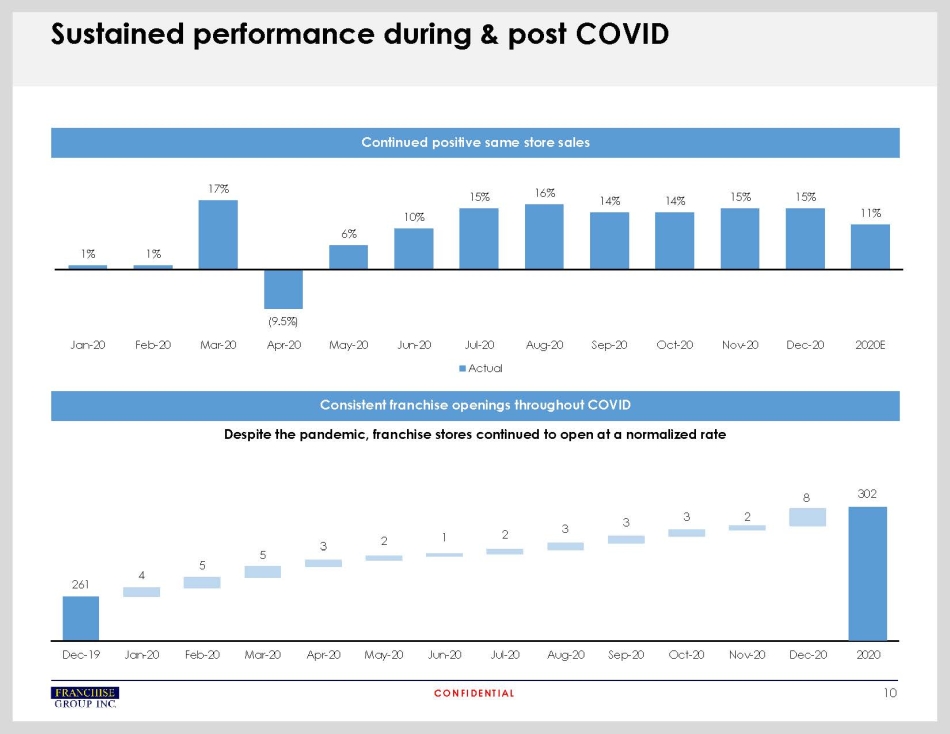

CONFIDENTIAL Sustained performance during & post COVID Continued positive same store sales Consistent franchise openings throughout COVID 1% 1% 17% (9.5%) 6% 10% 15% 16% 14% 14% 15% 15% 11% Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 2020E Actual 261 302 4 5 5 3 2 1 2 3 3 3 2 8 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 2020 Despite the pandemic, franchise stores continued to open at a normalized rate 10

CONFIDENTIAL PSP is complimentary with Franchise Group’s core strategy Leading platform of franchised or franchisable concepts, producing asset light recurring revenue 1 Synergistic platform drives significant revenue and cost synergies across portfolio concepts 2 Disciplined, value - based acquisition strategy targeting asset - light businesses with superior cash flow 4 Resilient throughout economic cycles and COVID - 19 pandemic 3 Committed to a conservative financial policy and a refranchising strategy that creates significant cash inflows 5 Experienced management team with strong shareholder alignment 6 11