UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

——————————————————————

FORM 10-K

|

| |

| (Mark One) | |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR |

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _ to _

Commission File Number: _001-35897______________________________________

Voya Financial, Inc.

(Exact name of registrant as specified in its charter)

|

| |

Delaware (State or other jurisdiction of incorporation or organization) | 52-1222820 (IRS Employer Identification No.) |

|

| |

230 Park Avenue New York, New York (Address of principal executive offices) | 10169 (Zip Code) |

(212) 309-8200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| |

| Title of each class | Name on each exchange on which registered |

| Common Stock, $.01 Par Value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant (1) has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

| |

Large accelerated filer x | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company o |

| (Do not check if a smaller reporting company) | Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

As of June 30, 2017, the aggregate market value of the common stock of the registrant held by non-affiliates of the registrant was approximately $6.6 billion.

As of February 16, 2018, there were 172,003,659 shares of the registrant's common stock outstanding.

Documents incorporated by reference: Portions of Voya Financial, Inc.'s Proxy Statement for its 2018 Annual Meeting of Shareholders are incorporated by reference in the Annual Report on Form 10-K in response to Part III, Items 10, 11, 12, 13 and 14.

Voya Financial, Inc.

Form 10-K for the period ended December 31, 2017

| Table of Contents |

| | | |

| ITEM NUMBER | | | PAGE |

| | | PART I. | |

| | | | |

| Item 1. | | | |

| | | | |

| Item 1A. | | | |

| | | | |

| Item 1B. | | | |

| | | | |

| Item 2. | | | |

| | | | |

| Item 3. | | | |

| | | | |

| Item 4. | | | |

| | | | |

| | | PART II. | |

| | | | |

| Item 5. | | | |

| | | | |

| Item 6. | | | |

| | | | |

| Item 7. | | | |

| | | | |

| Item 7A. | | | |

| | | | |

| Item 8. | | | |

| | | | |

| Item 9. | | | |

| | | | |

| Item 9A. | | | |

| | | | |

| | | PART III. | |

| | | | |

| Item 10. | | | |

| | | | |

| Item 11. | | | |

| | | | |

| Item 12. | | | |

| | | | |

| Item 13. | | | |

| | | | |

| Item 14. | | | |

| | | | |

| | | PART IV. | |

| | | | |

| Item 15. | | | |

| | | | |

| |

| | | | |

| |

For the purposes of the discussion in this Annual Report on Form 10-K, the term Voya Financial, Inc. refers to Voya Financial, Inc. and the terms "Company," "we," "our," and "us" refer to Voya Financial, Inc. and its subsidiaries.

NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, including "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations," and "Business," contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements relating to future developments in our business or expectations for our future financial performance and any statement not involving a historical fact. Forward-looking statements use words such as "anticipate," "believe," "estimate," "expect," "intend," "plan," and other words and terms of similar meaning in connection with a discussion of future operating or financial performance. Actual results, performance or events may differ materially from those projected in any forward-looking statement due to, among other things, (i) general economic conditions, particularly economic conditions in our core markets, (ii) performance of financial markets, including emerging markets, (iii) the frequency and severity of insured loss events, (iv) mortality and morbidity levels, (v) persistency and lapse levels, (vi) interest rates, (vii) currency exchange rates, (viii) general competitive factors, (ix) changes in laws and regulations, (x) changes in the policies of governments and/or regulatory authorities, (xi) our ability to successfully complete the Transaction (as defined below) on the expected economic terms or at all, and (xii) other factors described in the section "Item 1A. Risk Factors."

The risks included here are not exhaustive. Current reports on Form 8-K and other documents filed with the Securities and Exchange Commission ("SEC") include additional factors that could affect our businesses and financial performance. Moreover, we operate in a rapidly changing and competitive environment. New risk factors emerge from time to time, and it is not possible for management to predict all such risk factors.

MARKET DATA

In this Annual Report on Form 10-K, we present certain market and industry data and statistics. This information is based on third-party sources which we believe to be reliable. Market ranking information is generally based on industry surveys and therefore the reported rankings reflect the rankings only of those companies who voluntarily participate in these surveys. Accordingly, our market ranking among all competitors may be lower than the market ranking set forth in such surveys. In some cases, we have supplemented these third-party survey rankings with our own information, such as where we believe we know the market ranking of particular companies who do not participate in the surveys.

In this Annual Report on Form 10-K, the term "customers" refers to retirement plan sponsors, retirement plan participants, institutional investment clients, retail investors, corporations or professional groups offering employee benefits solutions, insurance policyholders, annuity contract holders, individuals with contractual relationships with financial advisors and holders of Individual Retirement Accounts ("IRAs") or other individual retirement, investment or insurance products sold by us.

Market data sources used with respect to our various segments include:

Retirement. Our Retirement segment sources our market segment leadership positions within the retirement industry from market surveys conducted by LIMRA, an insurance and financial services industry organization, and industry-recognized publications such as Pensions & Investments and InvestmentNews.com. Retirement tracks market segment leadership positions by assets under management ("AUM") or assets under administration ("AUA"), number of defined contribution plans, number of defined contribution plan participant accounts, sales (takeover assets and contributions), and the number of producing broker-dealer representatives.

Investment Management. Our Investment Management segment sources our market segment leadership positions within the investment management industry from Morningstar fund data and industry-recognized publications such as Pension & Investments. Investment Management tracks market segment leadership positions by AUM; and by benchmark or peer median metrics, which, as presented, measure each investment product based on (i) rank above the median of its peer category within Morningstar (mutual funds) or eVestment (institutional composites) for unconstrained and fully-active investment products; or (ii) outperformance against its benchmark index for "index like", rules based, risk-constrained, or client-specific investment products.

Individual Life. Our Individual Life segment sources our market segment leadership positions within the individual life insurance industry primarily from LIMRA market surveys. Individual Life tracks market segment leadership positions by premiums sold.

Employee Benefits. Our Employee Benefits segment sources our market segment leadership positions within the employee benefits industry from LIMRA market surveys and MyHealthguide newsletter rankings. Stop loss market rankings are derived from MyHealthguide, which does not include most managed healthcare providers in their market positions survey. The MyHealthguide survey is a recurring publication that compiles a ranking of medical stop loss providers and their most recently sourced annual premium data. Employee Benefits tracks market segment leadership positions by new premiums and in-force premiums.

PART I

Item 1. Business

For the purposes of this discussion, the term Voya Financial, Inc. refers to Voya Financial, Inc. and the terms "Company," "we," "our," and "us" refer to Voya Financial, Inc. and its subsidiaries.

We are a premier retirement, investment and insurance company serving the financial needs of approximately 14.7 million individual and institutional customers in the United States as of December 31, 2017. Our vision is to be America’s Retirement Company™. Our approximately 6,300 employees (as of December 31, 2017) are focused on executing our mission to make a secure financial future possible—one person, one family and one institution at a time. Through our retirement, investment management and insurance businesses, we help our customers save, grow, protect and enjoy their wealth to and through retirement. We offer our products and services through a broad group of financial intermediaries, independent producers, affiliated advisors and dedicated sales specialists throughout the United States.

Our extensive scale and breadth of product offerings are designed to help Americans achieve their retirement savings, investment income and protection goals. Our strategy is centered on preparing customers for "Retirement Readiness"—being emotionally and economically secure and ready for their retirement. We believe that the rapid aging of the U.S. population, weakening of traditional social safety nets, shifting of responsibility for retirement planning from institutions to individuals and growth in total retirement account assets will drive significant demand for our products and services going forward. We believe that we are well positioned to deliver on this Retirement Readiness need.

We believe that we help our customers achieve three essential financial goals, as they plan for, invest for and protect their retirement years.

| |

| • | Plan. Our products enable our customers to save for retirement by establishing investment accounts through their employers or individually. |

| |

| • | Invest. We provide advisory programs, individual retirement accounts ("IRAs"), brokerage accounts, mutual funds and accumulation insurance products to help our customers achieve their financial objectives. Our income products such as target date funds, guaranteed income funds, IRAs, mutual funds and accumulation insurance products enable our customers to meet income needs through retirement and achieve wealth transfer objectives. |

| |

| • | Protect. Our specialized retirement and insurance products, such as stable value, indexed universal life ("IUL") and variable life products, allow our customers to protect against unforeseen life events and mitigate market risk. |

We tailor our products to meet the unique needs of our individual and institutional customers. Our individual businesses are primarily focused on the middle and mass affluent markets; however we serve customers across the full income spectrum, especially in our Institutional Retirement Plans business, Retail and Alternative Fund businesses, and Employee Benefits segment. Similarly, our institutional businesses serve a broad range of customers, with a wide variety of offerings for the small-mid, large and mega market segments across all industries.

We provide our principal products and services through four segments: Retirement, Investment Management, Individual Life and Employee Benefits. Activities not related to our business segments such as our corporate operations, corporate-level assets and financial obligations are included in Corporate. As of the fourth quarter of 2017, substantially all of our former Annuities and Closed Block Variable Annuity ("CBVA") segments have been reclassified as "Business Held for Sale/Discontinued Operations". We continue to operate these businesses until the closing of the Transaction described further under "–Organizational History and Structure–CBVA and Annuity Transaction".

The following table presents a summary of our key individual and institutional markets, how we define those markets, and the key products we sell in such markets.

Individual Markets

|

| | | |

| Market | Household Income Range | Investable Asset Range | Typical Customer Products |

| Mass Market | $50,000-$100,000 | <$100,000 | Mutual Funds IRAs |

| | | | |

| Middle Market & Mass Affluent | $100,000-$250,000 | $100,000-$2,000,000 | Universal Life Insurance Mutual Funds IRAs Financial Advisory |

| | | | |

| Affluent & Wealth Management Market | $250,000-$500,000 | >$2,000,000 | Universal Life Insurance Mutual Funds Separately Managed Accounts Alternative Funds IRAs Financial Advisory |

Institutional Markets

|

| | | |

| Market | Employee Size | Asset Range | Typical Customer Products |

| Small-Mid | 26-1,000 | $0-$75 million | Full Service Retirement Plans Retirement Recordkeeping Employee Benefits Investment Management Stable Value |

| | | | |

| Large | 1,000-10,000 | $75 million-$1 billion | Full Service Retirement Plans Retirement Recordkeeping Employee Benefits Investment Management Stable Value |

| | | | |

| Mega | >10,000 | >$1 billion | Full Service Retirement Plans Retirement Recordkeeping Employee Benefits Investment Management Stable Value |

Our Segments

Retirement is a leading provider of retirement services and products in the United States, offering tax-deferred, employer-sponsored (institutional) retirement savings plans and administrative services to approximately 48,600 plan sponsors covering approximately 5.2 million plan participant accounts in corporate, education, healthcare, other non-profit and government entities as of December 31, 2017. Our Retirement segment reaches customers through a broad distribution footprint comprising multiple sales channels, including affiliated representatives and thousands of non-affiliated sales agents, brokers and advisors as well as third-party administrators ("TPAs") and pension/specialty consultants. The segment serves a wide spectrum of employers ranging from small companies to the very largest corporations and government entities. Stable Value solutions are also offered to institutional plan sponsors where we may or may not be providing defined contribution plan services. Additionally, Retirement provides IRAs and other retail financial products as well as comprehensive financial planning and advisory services to individual customers. Retirement had $382.7 billion of AUM and AUA as of December 31, 2017, of which $122.6 billion was institutional full service business, $256.5 billion was institutional recordkeeping, stable value and pension risk transfer business and $3.6 billion was Retail Wealth Management business.

Investment Management. We are a prominent full-service asset manager with approximately $224.3 billion of AUM and $50.0 billion of AUA as of December 31, 2017, delivering client-oriented investment solutions and advisory services, serving both individual and institutional customers. We serve both individual and institutional customers, offering them domestic and international fixed income, equity, multi-asset and alternative investment products and solutions across a range of geographies, investment styles and capitalization spectrums.

| |

| • | As of December 31, 2017, we managed $142.3 billion in our commercial business (comprising $96.2 billion for third-party institutions and individual investors, and $46.1 billion in separate account assets for our other businesses) and $82.0 billion in general account assets for Voya Financial. |

| |

| • | As of December 31, 2017, 94%, 93%, and 79% of fixed income assets, 54%, 54%, and 57% of equity assets, and 88%, 96%, and 32% of Multi-Asset Strategies and Solutions ("MASS") assets outperformed benchmark or peer median returns on a 3-year, 5-year, and 10-year basis, respectively. Our retail mutual fund portfolio assets totaled $27.0 billion as of December 31, 2017. |

Individual Life provides wealth protection and transfer opportunities through universal and variable products, distributed primarily through a network of independent general agents and managing directors ("Aligned Distributors") to meet the needs of a broad range of customers from the middle-market through affluent market segments. We provide universal and variable life insurance products. Based on the LIMRA survey as of September 30, 2017, for premiums sold, our indexed universal life products ranked eighth. The rankings reflect our recent focus on selling more capital efficient products, such as IUL. As of December 31, 2017, the Individual Life distribution model is supported by approximately 100 Aligned Distributors with access to over 50,000 producers who are committed to promoting Voya products. As we announced in December 2017, we are currently conducting a strategic review of our Individual Life business.

Employee Benefits provides stop loss, group life, voluntary employee-paid and disability products to mid-sized and large businesses. Our products are distributed through national and regional benefits consultants, brokers, TPAs, enrollment firms and technology partners. We are a top tier provider of stop-loss insurance and currently rank eighth in the United States as reported by MyHealthguide through November 2017. We also hold top 20 positions in our voluntary and group life products as reported by LIMRA as of the third quarter of 2017.

CBVA and Annuities Businesses

As described below under "–Organizational History and Structure–CBVA and Annuity Transaction", in December 2017, we entered into a transaction to dispose of substantially all of our CBVA and Fixed and Fixed Indexed Annuities businesses and related assets (the "Transaction"). Until this Transaction closes, we remain responsible for the ongoing management of these businesses.

Annuities provides fixed and indexed annuities, investment-only products and payout annuities for pre-retirement wealth accumulation and post-retirement income management sold through multiple channels, and had $29.0 billion of AUM as of December 31, 2017. Following the closing of the Transaction, we will retain a small portion of our existing Annuities business, including approximately $6 billion in investment-only products.

CBVA. We previously separated CBVA business from our other operations, as part of a strategic decision to run-off, divest, or cease actively writing certain lines of business. Accordingly, CBVA was classified as a closed block and has been managed separately

from our other segments. In 2009, we decided to stop actively writing new retail variable annuity products with substantial guarantee features (the last policies were issued in early 2010) and placed this portfolio in run-off. We will retain a small stub of variable annuities business following the closing of the Transaction.

———————

As of December 31, 2017, on a consolidated basis, we had $554.5 billion in total AUM and AUA and total shareholders’ equity, excluding accumulated other comprehensive income/loss ("AOCI") and noncontrolling interests, of $7.3 billion. In addition, we had $(2,992) million of Net income (loss) available to Voya Financial, Inc.’s common shareholders for the year ended December 31, 2017 of which $(2,580) million was related to Income (loss) from discontinued operations, net of tax.

For the year ended December 31, 2017, we generated $528 million of Income (loss) from continuing operations before income taxes, and $528 million of Adjusted operating earnings before income taxes. Adjusted operating earnings before income taxes is a non-GAAP financial measure. For a reconciliation of Adjusted operating earnings before income taxes to Income (loss) before income taxes, see "Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations— Company Consolidated."

ORGANIZATIONAL HISTORY AND STRUCTURE

Our History

Prior to our initial public offering in May 2013, we were a wholly owned subsidiary of ING Groep N.V. ("ING Group"), a global financial institution based in the Netherlands.

Through ING Group, we entered the United States life insurance market in 1975 through the acquisition of Wisconsin National Life Insurance Company, followed in 1976 with ING Group's acquisition of Midwestern United Life Insurance Company and Security Life of Denver Insurance Company in 1977. ING Group significantly expanded its presence in the United States in the late 1990s and 2000s with the acquisitions of Equitable Life Insurance Company of Iowa (1997), Furman Selz, an investment advisory company (1997), ReliaStar Life Insurance Company (including Pilgrim Capital Corporation) (2000), Aetna Life Insurance and Annuity Company (including Aeltus Investment Management) (2000) and CitiStreet (2008). As of March 2015, ING Group has completely divested its ownership of Voya Financial, Inc. common stock, although it continues to hold warrants to acquire a certain number of our shares.

For additional information on the separation from ING Group, see the "Business, Basis of Presentation and Significant Accounting Policies" section in Part II, Item 7. of this Annual Report on Form 10-K.

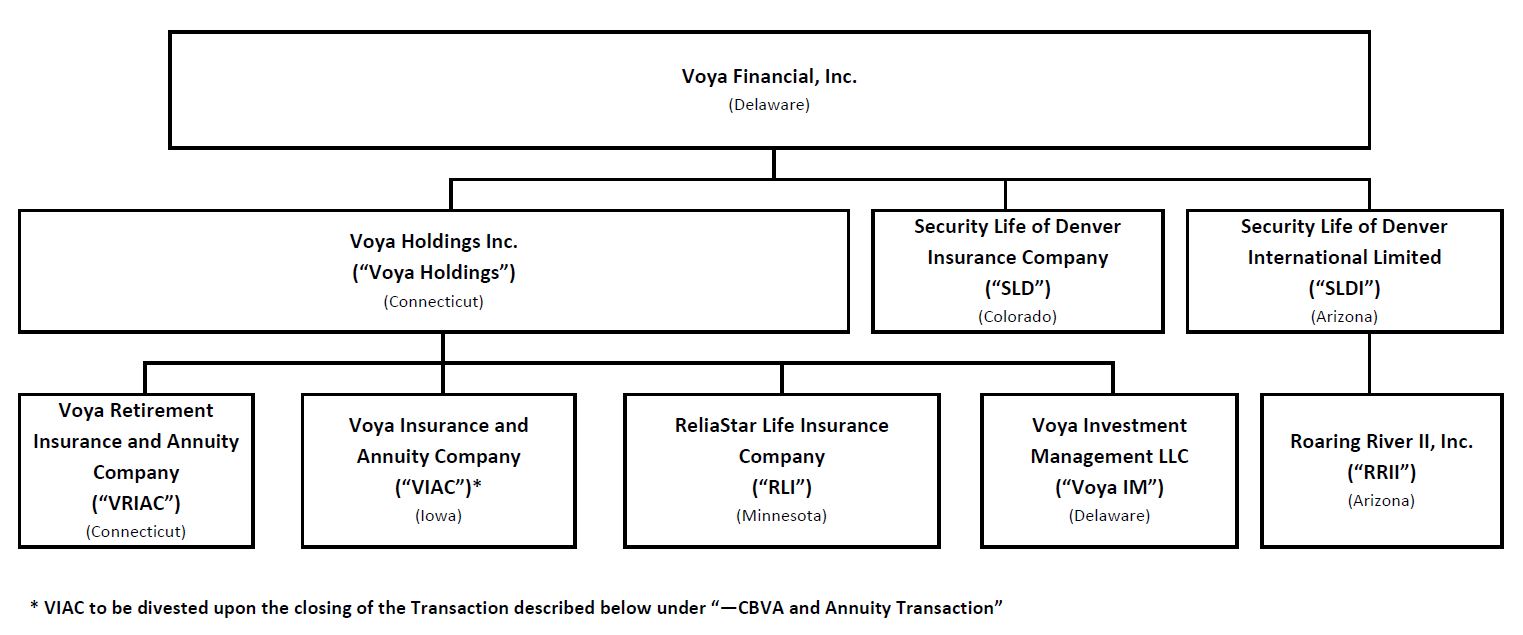

Our Organizational Structure

We are a holding company incorporated in Delaware in April 1999. We operate our businesses through a number of direct and indirect subsidiaries. The following organizational chart presents the ownership and jurisdiction of incorporation of our principal subsidiaries as of December 31, 2017:

The chart above presents:

| |

| • | Our principal intermediate holding company, Voya Holdings, which is the direct parent of a number of our insurance and non-insurance operating entities. |

| |

| • | Our principal operating entities that are the primary sources of cash distributions to Voya Financial, Inc. Specifically, these entities are our principal insurance operating companies (VRIAC, VIAC, SLD and RLI) and Voya Investment Management LLC, the holding company for entities that operate our Investment Management segment. |

| |

| • | SLDI and RRII, our Arizona captives. |

CBVA and Annuity Transaction

On December 20, 2017, we entered into a Master Transaction Agreement (the "MTA") with VA Capital Company LLC, a newly formed Delaware limited liability company ("VA Capital"), and Athene Holding Ltd., a Bermuda limited company ("Athene"), pursuant to which VA Capital's wholly owned subsidiary Venerable Holdings Inc. ("Venerable") will acquire certain of our assets, including all of the shares of the capital stock of VIAC, our Iowa-domiciled insurance subsidiary, and all of the membership interests of Directed Services LLC, an indirect broker-dealer subsidiary ("DSL"). This transaction will result in our disposition of substantially all of our variable annuity and fixed and fixed indexed annuity businesses and related assets (collectively, the "Transaction").

VA Capital is a holding company formed by affiliates of Apollo Global Management LLC ("Apollo") and Athene (collectively, the "Sponsors"). Reverence Capital Partners, L.P. and Crestview Advisors, L.L.C. are also investors in VA Capital, along with us, and under the MTA, at closing, we will acquire a 9.99% equity interest in VA Capital. In addition, after the closing, our other insurance subsidiaries will continue to own surplus notes issued by VIAC in aggregate principal amount of $350 million.

Following its acquisition of VIAC, Venerable will hold substantially all of the variable annuities in what was previously reported as our CBVA segment with account value of approximately $35 billion based on June 30, 2017 balances. We separated CBVA from our other operations in 2009 and 2010 placing them in run-off as part of a strategic decision to stop actively writing new retail variable annuity products with substantial guarantee features. Accordingly, this segment was classified as a closed block and was managed separately from our other segments.

Concurrent with the sale of VIAC, we will sell via reinsurance to Athene our individual fixed and fixed indexed annuities policies with approximately $19 billion of account value as of June 30, 2017, representing a significant majority of our fixed and fixed indexed annuities in force. We intend to cease manufacturing non-retirement-focused annuities after the Transaction closes. After the Transaction, VIAC or one of Venerable's other affiliates will administer most of the variable, fixed and fixed indexed annuities included in the Transaction, subject to some exceptions and transitional arrangements. Certain businesses in our former Annuities segment are not part of the transaction, including approximately $6 billion in investment-only products (primarily Select Advantage) that will be retained by us. We will also retain a small amount of existing variable annuities business.

As a a result of our entry into the Transaction, the operations that were reported in prior periods as our CBVA and Annuities segments have been reclassified as "Business Held for Sale and Discontinued Operations" in our financial statements and are no longer reported as individual segments. For additional information about this reclassification, see the Business Held for Sale and Discontinued Operations note in Part II, Item 8. of this Annual Report on Form 10-K.

The purchase price in the Transaction is equal to the difference between the Required Adjusted Book Value (as defined in the MTA) and the Statutory capital in VIAC at closing. The Required Adjusted Book Value is based on, subject to certain adjustments, the Conditional Trail Expectation ("CTE") 95 standard which is a statistical tail risk measure under the Standard & Poor's ("S&P") model which follows the Risk Based capital C-3 Phase II guidelines as stipulated by the National Association of Insurance Commissioners ("NAIC").

Under the terms of the Transaction, VIAC will, at or prior to the closing of the Transaction, undertake certain restructuring transactions with several current affiliates in order to transfer businesses and assets into and out of the Company. These restructuring transactions will include internal reinsurance of VIAC's life insurance and employee benefits businesses, the recapture of VIAC's variable annuity business from an affiliated reinsurer, the transfer of real and personal property and the settlement of outstanding amounts under existing affiliate agreements.

The MTA contains limits on the amount of additional capital we could be required to contribute to meet any increases in the Required Adjusted Book Value and on the amount of capital in excess of such amount that VA Capital could be required to compensate us for if such excess capital were to become trapped in VIAC prior to Transaction closing, in each case subject to certain termination rights.

In connection with the closing of the Transaction, Voya IM or its affiliated advisors will enter into one or more agreements to perform asset management services for Venerable as part of the Transaction. As part of the agreements, Voya IM or its affiliated advisors will serve as the preferred asset management partner for Venerable. Under the agreements, subject to certain criteria, Voya IM or its affiliated advisors will manage certain assets, including, for a minimum of five years following the closing of the Transaction, certain general account assets. Voya has also agreed to provide certain transitional services to Venerable for up to 24 months after the closing of the Transaction.

The Transaction is expected to close in the second or third quarter of 2018, subject to conditions specified in the MTA, including the receipt of required regulatory approvals, and other conditions.

OUR BUSINESSES

Retirement

Our Retirement segment is focused on meeting the needs of individuals in preparing for and sustaining a secure retirement through employer-sponsored plans and services, as well as through individual account rollover plans and comprehensive financial product offerings and planning and advisory services. We are well positioned in the marketplace, with our industry-leading Institutional Retirement Plans business and our Retail Wealth Management business having a combined $382.7 billion of AUM and AUA as of December 31, 2017, of which $66.3 billion were in proprietary assets.

Our Institutional Retirement Plans business offers tax-deferred employer-sponsored retirement savings plan and administrative services to corporations of all sizes, public and private school systems, higher education institutions, hospitals and healthcare facilities, not-for-profit organizations and state and local governments. We also offer stable value products to institutional plan sponsors where we may or may not be providing defined contribution plan services. This broad-based institutional business crosses many sectors of the economy, which provides diversification that helps insulate us from downturns in particular industries. In the defined contribution market, we provide services to approximately 48,600 plan sponsors covering approximately 5.2 million plan participant accounts as of December 31, 2017.

Our Retail Wealth Management business, with AUM and AUA of $3.6 billion as of December 31, 2017, focuses on the rapidly expanding retiree market as well as on pre-retirees within our defined contribution plans. This business offers retail financial products and comprehensive financial planning and advisory services to help individuals manage their retirement savings and income needs.

Our Retirement segment earns revenue principally from asset and participant-based advisory and recordkeeping fees. Retirement generated Adjusted operating earnings before income taxes of $456 million for the year ended December 31, 2017. Our Investment Management segment also earns arm’s-length market-based fees from the management of the general account and mutual fund assets supporting Institutional Retirement Plans and certain Retail Wealth Management rollover products and advisory solutions. Distribution of Investment Management products and services using the Retirement segment continues to present a growth opportunity for our Retirement and Investment Management segments.

We will continue to focus on growing our retirement platform by driving increases in our Institutional Retirement Plans business through focused sales and retention efforts, and by leveraging our Retail Wealth Management business to deepen relationships with our Institutional Retirement Plan participants. We will also continue to place a strong emphasis on capital and cost management while also growing our distribution platform and achieving a diversified retirement product mix.

An important element of our Retirement strategy is to leverage the extensive customer base to which we have access through our Institutional Retirement Plans business in order to grow our Retail Wealth Management and Investment Management businesses. We are therefore focused on building long-term relationships with our plan participants, especially when initiated through service touch points such as plan enrollments and rollovers, which will enable us to offer such participant's individual retirement and investment management solutions both during and after the term of their plan participation.

Institutional Retirement Plans

Products and Services

We are one of only a few providers that offer tax-deferred institutional retirement savings plans, services and support to the full spectrum of businesses, ranging from small to mega-sized plans and across all markets and code sections. These plans may either be offered as full service options or recordkeeping services products. We also offer stable value investment options to institutional clients where we may or may not be providing defined contribution plan services.

Full-service retirement products provide recordkeeping and plan administration services, tailored award-winning participant communications and education programs, myOrangeMoney® digital capabilities for sponsors and plan participants (plus mobile capabilities for participants), trustee services and institutional and retail investments. Offerings include a wide variety of investment and administrative products for defined contribution plans for tax-advantaged retirement savings, as well as nonqualified executive benefit plans and employer stock option plans. Plan sponsors may select from a variety of investment structures and products, such as general account, separate account, mutual funds, stable value or collective investment trusts and a variety of underlying asset types (including their own employer stock) to best meet the needs of their employees. A broad selection of funds is available for our products in all asset categories from over 150 fund families, including the Voya family of mutual funds managed by our Investment Management segment. Our full-service retirement plan offerings are also supported by financial planning and investment advisory services offered through our Retail Wealth Management business or through third parties (e.g., Morningstar) to help prepare individuals for retirement through customer-focused personalized and objective investment advice.

Recordkeeping service products provide recordkeeping and plan administration support for a sponsor base that includes multi-employer corporate plans, large-mega corporations and state and local governments. Our recordkeeping retirement plan offerings are also supported by award-winning participant communications and education programs, myOrangeMoney® digital capabilities for sponsors and plan participants (plus mobile capabilities for participants), as well as financial planning and investment advisory services offered through our Retail Wealth Management business and Voya Retirement Advisors (our registered investment advisor group serving in-plan participants with the in-plan advisory services program).

Stable value investment options may be offered within our full service institutional plans, or as investment-only options within our recordkeeping services plans or within other vendor plans. Our product offering includes both separate account guaranteed investment contracts ("GICs") and synthetic GICs managed by either proprietary or outside investment managers.

Pension risk transfer group annuity solutions were previously offered to institutional plan sponsors who needed to transfer their defined benefit plan obligations to us. We discontinued sales of these solutions in late 2016 to better align our business activities to our strategic priorities, but continue to manage existing policies and assets.

The following chart presents our Institutional Retirement Plans product/service models and corresponding AUM and AUA, key markets in which we compete, primary defined contribution plan Internal Revenue Code sections and core products offered for each market segment.

|

| | | | |

| Product/Service Model | AUM/AUA (as of December 31, 2017) | Key Market Segments/Product Lines | Primary Internal Revenue Code section | Core Products* |

| Full Service Plans | $122.6 billion | Small-Mid Corporate | 401(k) | Voya MAP Select, Voya Framewor(k) |

| | | K-12 Education | 403(b) | Voya Custom Choice II, Voya Framewor(k) |

| | | Higher Education | 403(b) | Voya Retirement Choice II, Voya Retirement Plus II, Voya Framewor(k) |

| | | Healthcare & Other Non-Profits | 403(b) | Voya Retirement Choice II, Voya Retirement Plus II, Voya Framewor(k) |

| | | Government (local and state) | 457 | RetireFlex-SA, RetireFlex-MF, Voya Health Reserve Account, Voya Framewor(k) |

| Recordkeeping and Stable Value Business | $256.5 billion** | Small-Mid Corporate | 401(k) | *** |

| | Large-Mega Corporate | 401(k) | *** |

| | | Government (local and state) | 457 | *** |

| | | Stable Value**** | 401(k) 403(b) 457(b) | Separate Account and Synthetic GICs |

* Core products actively being sold today.

** Assets include a small block of pension risk transfer business which is no longer an active offering

*** Offerings include administration services and investment options such as mutual funds, commingled trusts and separate accounts.

**** Sold across all market segments with a strong focus on Large Corporate

In 2017, we launched an enhanced version of our Voya Framewor(k) product, making it the first product in the history of our business that can be sold across both full service corporate and tax-exempt markets. It is a mutual fund program offered to fund qualified retirement plans, and it gives plan advisors and third party administrators who work with us a uniform and consistent product experience across multiple plan markets. The product is distinguished by its flexible recordkeeping platform and contains over 200 funds from well-known fund families for smaller plans or can be provided as an open architecture investment platform for larger plans (which offers most funds for which trades are cleared through the National Securities Clearing Corporation). This product also includes our general account and various stable value investment options.

In addition to Voya Framewor(k), we offer products customized to each of the full service corporate market and the full service tax exempt market.

For plans in the full service corporate market, our core product is Voya MAP Select, a group funding agreement/group annuity contract offered to fund qualified retirement plans. The product contains over 200 funds from well-known fund families for smaller plans or can be provided as an open architecture investment platform for larger plans (which offers most funds for which trades are cleared through the National Securities Clearing Corporation). This product also includes our general account and various stable value investment options.

For plans in the full service tax-exempt market, we offer a variety of products, that include the following:

| |

| • | Voya Retirement Choice II and RetireFlex-MF, retail mutual fund products which provide flexible funding vehicles and are designed to provide a diversified menu of mutual funds in addition to a guaranteed option (available through a group fixed annuity contract or stable value product). |

| |

| • | Voya Retirement Plus II and Voya Custom Choice II, registered group annuity products featuring variable investment options held in a variable annuity separate account and a fixed investment option held in the general account. |

| |

| • | RetireFlex-SA, an unregistered group annuity product which features variable investment options held in a variable annuity separate account and a guaranteed option (available through a group fixed annuity contract or stable value product). |

Markets and Distribution

Our Institutional Retirement Plans business can be categorized into two primary markets: Corporate and Tax Exempt. Both markets utilize our myOrangeMoney® participant-facing digital capabilities as a centerpiece to help shift the mindset of plan participants from focusing only on accumulation to focusing on both accumulation and adequate income in retirement. Additionally, a broad suite of financial wellness offerings, including retirement planning, guidance and advisory products, tools and services are offered to help our plan participants in all markets reach their retirement goals. A brief description of each market, including sub segments and areas of particular focus, are as follows:

Corporate Markets:

| |

| • | Small-Mid Corporate Market. In this market we offer full service solutions to defined contribution plans of small-mid-sized corporations (i.e., typically less than 1,000 employees). Our comprehensive product offers an open architecture investment platform, comprehensive fiduciary solutions, dedicated and proactive service teams and product and service innovations leveraged from our expertise across multiple market segments (all sizes of plans as well as code sections). Furthermore, we offer a unique enrollment experience through our myOrangeMoney® digital capabilities that helps engage and inform plan participants with retirement savings and income goals. |

| |

| • | Large-Mega Corporate Market. In this market we offer recordkeeping services to defined contribution plans of large to mega-sized corporations. Our solutions and capabilities support the most complex retirement plans with a special focus on client relationship management, tailored communication campaigns and education and enrollment support to help employers prepare their employees for retirement. We are dedicated to providing engaging information through innovative technology-based tools and award winning print materials to help plan participants achieve a secure and dignified retirement. |

Tax Exempt Markets:

| |

| • | Education Market. We offer comprehensive full service offerings to both public and private K-12 educational entities as well as public and private higher education institutions. In the United States, we rank fourth in both the K-12 and higher education markets by assets as of September 30, 2017. Our support to plan sponsors with solutions to reduce administrative burden, deep technical and regulatory expertise, and strong on-site service teams plus a broad suite of financial wellness products, tools, and services for participants, continue to strengthen our position as one of the top providers in this market. |

| |

| • | Healthcare/Other Non Profits Market. In this market we service hospitals, healthcare organizations and not-for-profit entities by offering full service solutions for a variety of plan types. We offer solutions that reduce sponsors' administrative burdens and provide them with deep technical and fiduciary expertise. Additionally, we offer on-site service teams to assist plan sponsors with their plans and to assist their employees with understanding and taking advantage of their plan benefits. We also provide tailored communications, education and enrollment support plus a broad suite of financial wellness products, tools and services in order to better prepare plan participants for retirement. |

| |

| • | Government Market. We provide both full service and recordkeeping services offerings to small and large governmental entities (e.g., state and local government) with a client base that spans all 50 states plus US territories. For large governmental sponsors, we offer recordkeeping services that meet the most complex of needs, while also offering extensive participant communication and retirement education support, including a broad suite of financial wellness products, tools and services. We also offer a broad range of proprietary, non-proprietary and stable value investment options. Our flexibility |

and expertise help make us the fourth ranked provider in this market in the United States based on AUM and AUA as of September 30, 2017.

Products for Institutional Retirement Plans are distributed nationally through multiple unaffiliated channels supported by our employee wholesale field force and dedicated sales teams and via other affiliated distribution through our owned broker-dealer. We offer localized support to distribution partners and their clients during and after the sales process as well as a broad selection of investment options with flexibility of choice and comprehensive fiduciary solutions to help their clients meet or exceed plan guidelines and responsibilities.

Unaffiliated Distribution:

| |

| • | Independent Sales Agents. As of December 31, 2017, we work with more than 5,000 sales agents who primarily sell fixed annuity products from multiple vendors in the education market. Activities by these representatives are centered on increasing participant enrollments and deferral amounts in our existing K-12 education segment plans. |

| |

| • | Brokers and Advisors. Over 12,000 wirehouse and independent regional and local brokers, specialty retirement plan advisors plus registered investment advisors (as of December 31, 2017) are the primary distributors of our small-mid corporate market products, but they also distribute products to the education, healthcare and government markets. These producers typically present their clients (i.e., employers seeking a defined contribution plan for their employees) with plan options from multiple vendors for comparison and may also help with employee enrollment and education. |

| |

| • | TPAs. As of December 31, 2017, we have long-standing relationships with over 1,200 TPAs who work with a variety of retirement plan providers and are selling and/or service partners for our small-mid corporate markets and select tax exempt markets plans. While TPAs typically focus on providing plan services only (such as administration and compliance testing), some also initiate and complete the sales process. TPAs also play a vital role as the connecting point between our wholesale team and unaffiliated producers who seek references for determining which providers they should recommend to their clients. |

Affiliated Distribution:

| |

| • | Voya Financial Advisors ("VFA"). Our owned broker-dealer is one of the top thirteen broker-dealers in the United States as determined by the total number of licensed and producing representatives. As of December 31, 2017, VFA provided licensing and operational support to approximately 1,800 field and phone-based representatives. The field based financial planning and advisory representatives support sales of products, financial planning and advisory services for the Retirement segment. A closely affiliated sub-set of the field-based channel focuses primarily on driving enrollment and contribution activity within our education, healthcare and government market institutional plans. They also provide in-plan education and guidance plus retail sold-financial advisory services to help individuals in these markets meet their retirement savings and income goals. The home office phone-based representatives focus on providing education, guidance and rollover support services to our institutional plan participants. |

| |

| • | Wholesale Field Force. Locally based employee wholesalers focus on expanding and strengthening relationships with unaffiliated distribution partners and third party administrators who sell and service our institutional plan offerings to employers across the nation. |

| |

| • | Dedicated Voya Sales Teams. We have employee sales teams that work with more than 80 different pension/specialty consulting firms that represent employers in corporate and tax-exempt markets seeking large-mega institutional plans and/or stable value solutions. Additionally, as mentioned above for VFA, we have salaried phone-based sales teams that focus on supporting our institutional plan participants across all markets. |

Competition

Our Institutional Retirement Plans business competes with other large, well-established insurance companies, asset managers, record keepers and diversified financial institutions. Competition varies in all market segments as few institutions are able to compete across all markets as we do. The following chart presents a summary of the current competitive landscape in the markets where we offer our Institutional Retirement Plans and stable value:

|

| | |

| Market/Product Segment | Competitive Landscape | Select Competitors |

| | | |

| Small-Mid Corporate | Primary competitors are mutual fund companies and insurance-based providers with third-party administration relationships | Empower Fidelity |

| | | |

| K-12 Education | Competitors are primarily insurance-based providers that focus on school districts across the nation | AXA VALIC |

| | | |

| Higher Education | Competitors are 403(b) plan providers, asset managers and some insurance-based providers | TIAA-CREF Fidelity |

| | | |

| Healthcare & Other Non-Profits | Competition varies across 403(b) plan providers, asset managers and some insurance-based providers | Fidelity TIAA-CREF |

| | | |

| Government | Compete primarily with insurance-based providers but also asset managers and 457 providers | Empower Nationwide |

| | | |

| Recordkeeping | Primarily bid against asset managers and business consulting services firms, but also compete with some payroll firms and insurance-based providers | Fidelity Empower |

| | | |

| Stable Value | Primarily compete with select insurance companies who are also dedicated to the Stable value market, but also with certain banking institutions | Prudential MetLife |

Our full-service Institutional Retirement Plans business competes primarily based on pricing for value delivered, the breadth of our service and investment offerings, technical/regulatory expertise, industry experience, local enrollment and financial wellness support, investment flexibility and our ability to offer industry tailored product features to meet the retirement income needs of our clients. Regarding the large plan recordkeeping only business, we have seen industry concentration in recent years as a result of mergers among several industry providers seeking to increase scale, improve cost efficiencies and enter new market segments. As a result, we emphasize our strong sponsor relationships, flexible value-added services, ability to customize recordkeeping and administration services to match client needs, and technical and regulatory expertise as our competitive strengths. Additionally, we compete across all institutional markets with our broad suite of products, tools, services, including myOrangeMoney® retirement income focused digital and mobile capabilities, to help employers support the retirement preparedness and financial needs of their employees. Our long standing experience in the retirement market underscored by strong stable value expertise allows us to effectively compete against existing and new providers.

Underwriting and Pricing

We price our institutional and individual retirement products based on long-term assumptions that include investment returns, mortality, persistency and operating costs. We establish target returns for each product based upon these factors and the expected amount of regulatory and rating agency capital that we must hold to support these contracts over their projected lifetime. We monitor and manage pricing and sales mix to achieve target returns. It may take new business several years before it is profitable, depending on the nature and life of the product, and returns are subject to variability as actual results may differ from pricing assumptions. We seek to mitigate investment risk by actively managing market and credit risks associated with investments and through asset/liability matching portfolio management.

Retail Wealth Management

Products and Services

Our Retail Wealth Management business offers a variety of investments and protection products, along with holistic advice and guidance delivered through field-based financial planning and advisory representatives and home office phone-based representatives. Our current investment solutions include a variety of mutual fund custodial IRA products, managed accounts and advisory programs, plus brokerage accounts.

The primary focus of our Retirement segment is to serve approximately 5.2 million defined contribution plan participant accounts (as of December 31, 2017). We also seek to capitalize on our access to these individuals through our Institutional Retirement Plans business by utilizing our Retail Wealth Management business to deepen our relationships with them for the long-term. We believe that our ability to offer an integrated approach to an individual customer’s entire financial picture, while saving for or living in retirement, presents a compelling reason for our Institutional Retirement Plans participants to use us as their principal investment and retirement plan provider. Through our broad range of advisory programs, our financial advisers have access to a wide set of solutions for our customers for building investment portfolios, including stocks, bonds and mutual funds, as well as managed accounts. These experienced advisers work with customers to select a program to meet their financial needs that takes into consideration each individual’s time horizon, goals and attitudes towards risk.

Markets and Advisory Services

Retail Wealth Management products, financial planning and advisory services are primarily sold through our group of nearly 1,800 representatives licensed through our Voya Financial Advisors ("VFA") broker-dealer. These VFA representatives help provide cohesiveness between our Institutional Retirement Plans and Retail Wealth Management businesses and are grouped into two primary categories: field-based and home office phone-based representatives. Field-based representatives are registered sales and investment advisory representatives that drive both fee-based and commissioned sales. They provide face-to-face interaction with individuals seeking retail investment products (e.g., rollover products) as well as financial planning and advisory solutions. Home office phone-based representatives focus on assisting participants in our institutional retirement plans, primarily for our large recordkeeping plans. While these representatives offer more simplified rollover products and advisory services than offered by the field-based representatives, they are highly trained in providing financial advice that helps customers transition through life stage and job-related changes.

In an effort to develop a path for our VFA representatives to offer holistic retirement planning solutions to participants in our Institutional Retirement Plans, we partner with our institutional clients to engage, educate, advise and motivate their employees to take action that will better prepare them for successful retirement outcomes.

Competition

Our Retail Wealth Management advisory services and product solutions compete for rollover and other asset consolidation opportunities against integrated financial services companies and independent broker-dealers who also offer individual retirement products, all of which currently have more market share than insurance-based providers in this space. Primary competitors to our Retail Wealth Management business are, in the phone-based channel, Fidelity, Schwab, and Vanguard, and in the field-based channel, LPL Financial, Ameriprise, Commonwealth, Cambridge, Cetera, and Bank of America Merrill Lynch.

Our Retail Wealth Management advisory services and product solutions are competitively priced and compete based on our consultative approach, simplicity of design and a fund and investment selection process that includes proprietary and non-proprietary investment options. The advisory services and product solutions are primarily targeted towards existing institutional plan participants, which allow us to benefit from our extensive relationships with large corporate and tax-exempt plan sponsors, our small and mid-corporate market plan sponsors and other qualified plan segments in healthcare, higher education and K-12 education.

Underwriting and Pricing

We price our institutional and individual retirement products based on long-term assumptions that include investment returns and operating costs. We establish target returns for each product based upon these factors and the expected amount of regulatory and rating agency capital that we must hold to support these contracts over their projected lifetime. We monitor and manage pricing and sales mix to achieve target returns. It may take new business several years before it is profitable, depending on the nature and life of the product, and returns are subject to variability as actual results may differ from pricing assumptions. We seek to mitigate

investment risk by actively managing market and credit risks associated with investments and through asset/liability matching portfolio management.

Investment Management

We offer domestic and international fixed income, equity, multi-asset and alternatives products and solutions across market sectors, investment styles and capitalization spectrums through our actively managed, full-service investment management business. Multiple investment platforms are backed by a fully integrated business support infrastructure that lowers expense and creates operating efficiencies and business leverage and scalability at low marginal cost. As of December 31, 2017, our Investment Management segment managed $96.2 billion for third-party institutions and individual investors, $46.1 billion in separate account assets for our other segments (including CBVA) and $82.0 billion in general account assets. Upon closing of the Transaction, our general account AUM will decline by approximately $28 billion, a portion of which will be offset by approximately $10 billion of additional third-party AUM associated with our management of the general account assets of Venerable. See "–Organizational History and Structure–CBVA and Annuity Transaction".

We are committed to reliable and responsible investing and delivering research-driven, risk-adjusted, client-oriented investment strategies and solutions and advisory services across asset classes, geographies and investment styles. Through our institutional distribution channel and our Voya-affiliate businesses, we serve a variety of institutional clients, including public, corporate and Taft-Hartley Act defined benefit and defined contribution retirement plans, endowments and foundations, and insurance companies. We also serve individual investors by offering our mutual funds and separately managed accounts through an intermediary-focused distribution platform or through affiliate and third-party retirement platforms.

Investment Management’s primary source of revenue is management fees collected on the assets we manage. These fees typically are based upon a percentage of AUM. In certain investment management fee arrangements, we may also receive performance-based incentive fees when the return on AUM exceeds certain benchmark returns or other performance hurdles. In addition, and to a lesser extent, Investment Management collects administrative fees on outside managed assets that are administered by our mutual fund platform, and distributed primarily by our Retirement segment. Investment Management also receives fees as the primary investment manager of our general account, which is managed on an arm’s-length pricing basis. Finally, Investment Management generates revenues from a portfolio of capital investments. Investment Management generated Adjusted operating earnings before income taxes of $248 million for the year ended December 31, 2017.

The success of our platform begins with providing our clients continued strong investment performance. In addition to investment performance, our focus is on client "solutions" and income and outcome-oriented products which include target date funds. We expect that strong investment performance combined with superior client service through a solution orientation will result in AUM growth.

| |

| • | As of December 31, 2017, 94%, 93%, and 79% of fixed income assets, 54%, 54%, and 57% of equity assets, and 88%, 96%, and 32% of Multi-Asset Strategies and Solutions ("MASS") assets outperformed benchmark or peer median returns on a 3-year, 5-year, and 10-year basis, respectively. Our retail mutual fund portfolio assets totaled $27.0 billion as of December 31, 2017. |

We are also focused on capitalizing on the Retirement segment's leading market position and have established dedicated retirement resources within our Investment Management intermediary-focused distribution team to work with Retirement and have enhanced our MASS investment platform (described below) to increase focus on retirement products such as our target date and target risk portfolios, which we believe will capture an increased proportion of retirement flows going forward.

Other key strategic initiatives for growth include: improved distribution productivity, sub-advisory mandates for Investment Management capabilities on others' platforms; leveraging partnerships with financial intermediaries and consultants; long-term expansion of our international investment capabilities; opportunistic launching of capital markets products such as collateralized loan obligations ("CLOs") and Closed End Mutual Funds; and prudent expansion of our private equity business.

Products and Services

Investment Management delivers products and services that are manufactured by traditional and specialty investment platforms. The traditional platforms are fixed income, equities and MASS. The specialty investment platforms are senior bank loans and alternatives.

Fixed Income. Investment Management’s fixed income platform manages assets for our general account, as well as for domestic and international institutional and retail investors. As of December 31, 2017, there were $127.6 billion in AUM on the fixed income platform, of which $82.0 billion were general account assets. Through the fixed income platform clients have access to money market funds, investment-grade corporate debt, government bonds, residential mortgage-backed securities ("RMBS"), commercial mortgage-backed securities ("CMBS"), asset-backed securities ("ABS"), high yield bonds, private and syndicated debt instruments, commercial mortgages and preferred securities. Each sector within the platform is managed by seasoned investment professionals supported by significant credit, quantitative and macro research and risk management capabilities.

Equities. The equities platform is a multi-cap and multi-style research-driven platform comprising both fundamental and quantitative equity strategies for institutional and retail investors. As of December 31, 2017, there were $61.5 billion in AUM on the equities platform covering both domestic and international markets including Real Estate. Our fundamental equity capabilities are bottom-up and research driven, and cover growth, value, and core strategies in the large, mid and small cap spaces. Our quantitative equity capabilities are used to create quantitative and enhanced indexed strategies, support other fundamental equity analysis, and create extension products.

MASS. Investment Management’s MASS platform offers a variety of investment products and strategies that combine multiple asset classes using asset allocation techniques. The objective of the MASS platform is to develop customized solutions that meet specific, and often unique, goals of investors and that dynamically change over time in response to changing markets and client needs. Utilizing core capabilities in asset allocation, manager selection, asset/liability modeling, risk management and financial engineering, the MASS team has developed a suite of target date and target risk funds that are distributed through our Retirement segment and to institutional and retail investors. These funds can incorporate multi-manager funds. The MASS team also provides pension risk management, strategic and tactical asset allocation, liability-driven investing solutions and investment strategies that hedge out specific market exposures (e.g., portable alpha) for clients.

Senior Bank Loans. Investment Management’s senior bank loan group is an experienced manager of below-investment grade floating-rate loans, actively managing diversified portfolios of loans made by major banks around the world to non-investment grade corporate borrowers. Senior in the capital structure, these loans have a first lien on the borrower’s assets, typically giving them stronger credit support than unsecured corporate bonds. The platform offers institutional, retail and structured products (e.g., CLOs), including on-shore and off-shore vehicles with assets of $24.6 billion as of December 31, 2017.

Alternatives. Investment Management’s primary alternatives platform is Pomona Capital. Pomona Capital specializes in investing in private equity funds in three ways: by purchasing secondary interests in existing partnerships; by investing in new partnerships; and by co-investing alongside buyout funds in individual companies. As of December 31, 2017, Pomona Capital managed assets totaling $8.6 billion across a suite of eight limited partnerships and the Pomona Investment Fund, a registered investment fund launched in May, 2015 that is available to accredited investors. In addition, Investment Management offers select alternative and hedge funds leveraging our core debt and equity investment capabilities.

The following chart presents asset and net flow data as of December 31, 2017, broken out by Investment Management’s five investment platforms as well as by major client segment:

|

| | | | | | | |

| | AUM | | Net Flows |

| | As of | | Year Ended |

| | December 31, 2017 | | December 31, 2017 |

| | $ in billions | | $ in millions |

| Investment Platform | | | |

| Fixed income | $ | 127.6 |

| | $ | 2,518 |

|

| Equities | 61.5 |

| | (4,724 | ) |

| Senior Bank Loans | 24.6 |

| | 1,923 |

|

| Alternatives | 10.6 |

| | 674 |

|

| Total | $ | 224.3 |

| (1) | $ | 391 |

|

MASS (1) | 29.7 |

| | (1,183 | ) |

| | | | |

| Client Segment | | | |

| Retail | $ | 69.8 |

| | $ | (5,878 | ) |

| Institutional | 72.5 |

| | 5,413 |

|

| General Account | 82.0 |

| (4) | N/A |

|

Mutual Funds Manager Re-assignments (2) | N/A |

| | 857 |

|

| Total | $ | 224.3 |

| | $ | 391 |

|

Voya Financial affiliate sourced, excluding CBVA(3) | $ | 35.8 |

| | $ | (120 | ) |

CBVA (3) | 20.7 |

| | (4,505 | ) |

| |

(1) | $23.3 billion of MASS assets are included in the fixed income, equity and senior bank loan AUM figures presented above. The balance of MASS assets, $6.4 billion, is managed by third parties and we earn only a modest, market-rate fee on these assets. |

| |

(2) | Represents the re-assignment of mutual fund management contracts to Voya Investment Management from external managers. The AUM related to the re-assignments are included in the retail segment above. |

| |

(3) | Assets sourced from Voya Financial, including CBVA, are also included in the retail and institutional markets segments above. |

| |

(4) | Upon closing of the Transaction, our general account AUM will decline by approximately $28 billion, a portion of which will be offset by approximately $10 billion of additional third-party AUM associated with our management of the general account assets of Venerable. See "–Organizational History and Structure–CBVA and Annuity Transaction". |

Markets and Distribution

We serve our institutional clients through a dedicated sales and service platform and for certain international regions, through selling agreements with a former affiliated party and for sponsored structured products through the arranger. We serve individual investors through an intermediary-focused distribution platform, consisting of business development and wholesale forces that partner with banks, broker-dealers and independent financial advisers, as well as our affiliate and third-party retirement platforms.

With the exception of Pomona Capital and structured products, the different products and strategies associated with our investment platforms are distributed and serviced by these Retail and Institutional client-focused segments as follows:

| |

| • | Retail client segment: Open- and closed-end funds through affiliate and third-party distribution platforms, including wirehouses, brokerage firms, and independent and regional broker-dealers. As of December 31, 2017, total AUM from these channels was $69.8 billion. Historically, AUM derived from our CBVA business has been included in the total AUM from this retail client segment. |

| |

| • | Institutional client segment: Individual and pooled accounts, targeting defined benefit, defined contribution recordkeeping and retirement plans, Taft Hartley and endowments and foundations. As of December 31, 2017, Investment Management had approximately 319 institutional clients, representing $72.5 billion of AUM primarily in separately managed accounts and collective investment trusts. |

Investment Management manages a variety of variable portfolio, mutual fund and stable value assets, sold through our Retirement, Individual Life and Employee Benefits segments, together with our Annuities business. As of December 31, 2017, total AUM

from these channels and our CBVA business was $56.5 billion with the majority of the assets gathered through our Retirement segment.

As described above under "–Organizational History and Structure–CBVA and Annuity Transaction" as a result of the Transaction, Voya IM or its affiliated advisors will enter into one or more agreements to serve as the preferred asset management partner for Venerable for at least five years following the closing of the Transaction.

Competition

Investment Management competes with a wide array of asset managers and institutions in the highly fragmented U.S. investment management industry. In our key market segments, Investment Management competes on the basis of, among other things, investment performance, investment philosophy and process, product features and structure and client service. Our principal competitors include insurance-owned asset managers such as Principal Global Investors (Principal Financial Group), Prudential and Ameriprise, bank-owned asset managers such as J.P. Morgan Asset Management, as well as "pure-play" asset managers including PIMCO, Invesco, Wellington, Legg Mason, T. Rowe Price, Franklin Templeton, and Fidelity.

Individual Life

Our Individual Life segment has a broad independent distribution footprint and manufactures competitive products, with a focus on indexed universal life. We offer indexed, fixed, and variable universal life insurance products targeted to the middle market through the mass affluent markets. We continually evaluate changes to our product portfolio in light of market conditions and in recent years have suspended sales of our Term Life and Indexed Universal Life-Guaranteed Death Benefit ("IUL-GDB") products. Applications for these products were accepted through the end of 2016. These changes reflect our continued effort to focus on capital efficient products and drive greater value to our shareholders. As we announced in December 2017, we are currently conducting a strategic review of our Individual Life business.

As of September 30, 2017, we were the eighth largest writer of indexed universal life products in the United States based on premiums sold or written. Our strong market positions have allowed us to properly scale our business to achieve greater profitability. As of December 31, 2017, Individual Life’s in-force book comprised nearly 1 million policies and gross premiums and deposits of approximately $1.8 billion.

The Individual Life segment generates revenue on its products from premiums, investment income, expense load, mortality charges and other policy charges, along with some asset-based fees. Profits are driven by the spread between investment income earned and interest credited to policyholders, plus the difference between premiums and mortality charges collected and benefits and expenses paid. Our Individual Life segment generated Adjusted operating earnings before income taxes of $92 million for the year ended December 31, 2017.

We intend to achieve our earnings growth in our Individual Life segment by focusing on growing our earnings drivers. Our earnings drivers include growing our in-force block of business by adding new businesses that meet our profit and capital requirements, combined with effectively managing our in-force block to meet our profitability objectives. They also include focusing on improving our investment margins, growing our mortality profits and fully exploiting our technological capability in order to continue to reduce new business unit costs and underwriting expense. In addition, we will further our financial objectives by continuing to utilize reinsurance to actively manage our risk and capital profile with the goal of controlling exposure to losses, reducing volatility and protecting capital. We aim to maximize earnings and capital efficiency in part by relieving the reserve strain for certain of our term and universal life products by means of reinsurance arrangements and other financing transactions. We also look to transfer certain blocks of business through reinsurance in order to more effectively manage our capital. For example, in 2015 and 2014 we reinsured two in-force blocks comprising approximately 325,000 term life insurance policies, representing approximately $190.0 billion of life insurance in-force and backed by approximately $2.7 billion in statutory reserves, to a third-party reinsurer.

Products and Services

Our Individual Life segment currently offers products that include IUL, universal life ("UL"), and variable universal life ("VUL") insurance. These offerings are designed to address customer needs for death benefit protection, tax-advantaged wealth transfer and accumulation, premium financing, business planning, executive benefits and supplemental retirement income. We believe that our combination of product solutions is well-suited for the middle-market through the mass-affluent and makes us a full service provider to our independent distribution partners.

IUL. For customers looking for an opportunity for a higher return in a low rate environment, we offer IUL products, which, along with death benefit protection, provide customers the opportunity for growth through potentially stronger surrender values than traditional UL products. These IUL products link to both fixed and indexed crediting strategies and offer protection from downside risk through a minimum interest guarantee, helping customers who seek solutions that would be advantageous for providing supplemental retirement income, payment of college costs or executive benefits. Indexed products are the fastest growing new product segment and are a major focus of our product and distribution effort as they are less capital intensive and provide attractive returns.

UL. Accumulation-focused universal life products feature the opportunity to build tax-deferred cash value that can be accessed by customers via loans and withdrawals for future needs. This money grows income tax-deferred, meaning no federal or state income taxes apply while it accumulates. The compounding tax-deferred interest can be an attractive feature to policyholders. These products help policyholders meet longer-range goals like college funding, supplemental retirement income and leaving a legacy for heirs. Other features include flexible premium payments that can change to meet policyholders’ evolving financial needs.

VUL. For customers seeking greater growth potential and more control over their investments, we offer an individual variable universal life insurance product designed to provide long-term cash accumulation potential with the ability to add optional riders that provide guarantees and more flexibility. We offer customers the ability to choose from individual variable investment options, which range from conservative to aggressive stock and bond investments managed by respected investment management firms in the industry or from diverse asset allocation solutions designed to match a customer’s risk tolerance.

The following chart presents data on our in-force face amount and total gross premiums and deposits received by product:

|

| | | | | | | |

| | In-Force Face | | Total gross premiums |