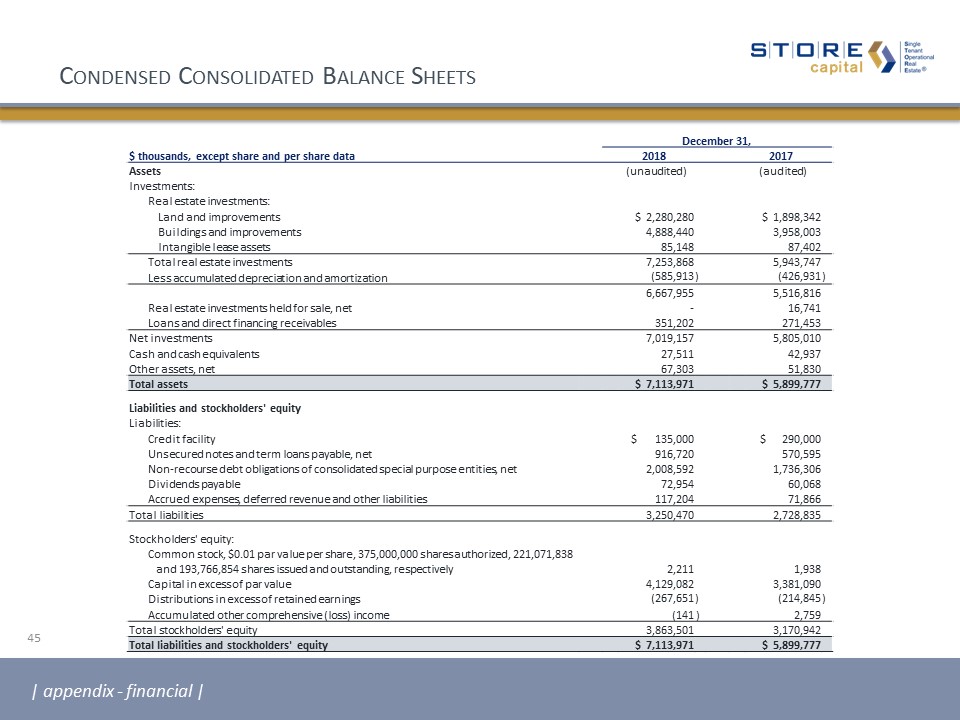

Condensed Consolidated Balance Sheets December 31, $ thousands, except share and per share data 2018 2017 Assets (unaudited) (audited) Investments: Real estate investments: Land and improvements $ 2,280,280 $ 1,898,342 Buildings and improvements 4,888,440 3,958,003 Intangible lease assets 85,148 87,402 Total real estate investments 7,253,868 5,943,747 Less accumulated depreciation and amortization (585,913 ) (426,931 ) 6,667,955 5,516,816 Real estate investments held for sale, net - 16,741 Loans and direct financing receivables 351,202 271,453 Net investments 7,019,157 5,805,010 Cash and cash equivalents 27,511 42,937 Other assets, net 67,303 51,830 Total assets $ 7,113,971 $ 5,899,777 Liabilities and stockholders' equity Liabilities: Credit facility $ 135,000 $ 290,000 Unsecured notes and term loans payable, net 916,720 570,595 Non-recourse debt obligations of consolidated special purpose entities, net 2,008,592 1,736,306 Dividends payable 72,954 60,068 Accrued expenses, deferred revenue and other liabilities 117,204 71,866 Total liabilities 3,250,470 2,728,835 Stockholders' equity: Common stock, $0.01 par value per share, 375,000,000 shares authorized, 221,071,838 and 193,766,854 shares issued and outstanding, respectively 2,211 1,938 Capital in excess of par value 4,129,082 3,381,090 Distributions in excess of retained earnings (267,651 ) (214,845 ) Accumulated other comprehensive (loss) income (141 ) 2,759 Total stockholders' equity 3,863,501 3,170,942 Total liabilities and stockholders' equity $ 7,113,971 $ 5,899,777 45 | appendix - financial |