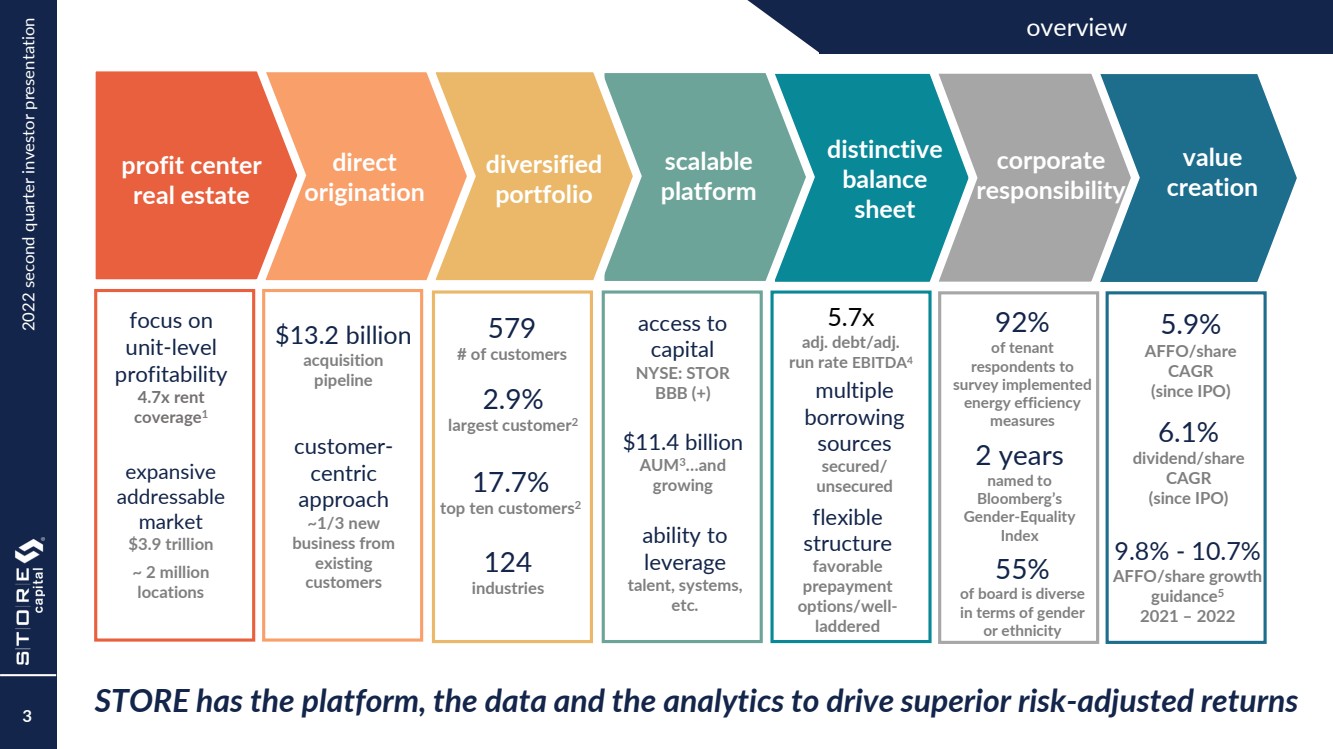

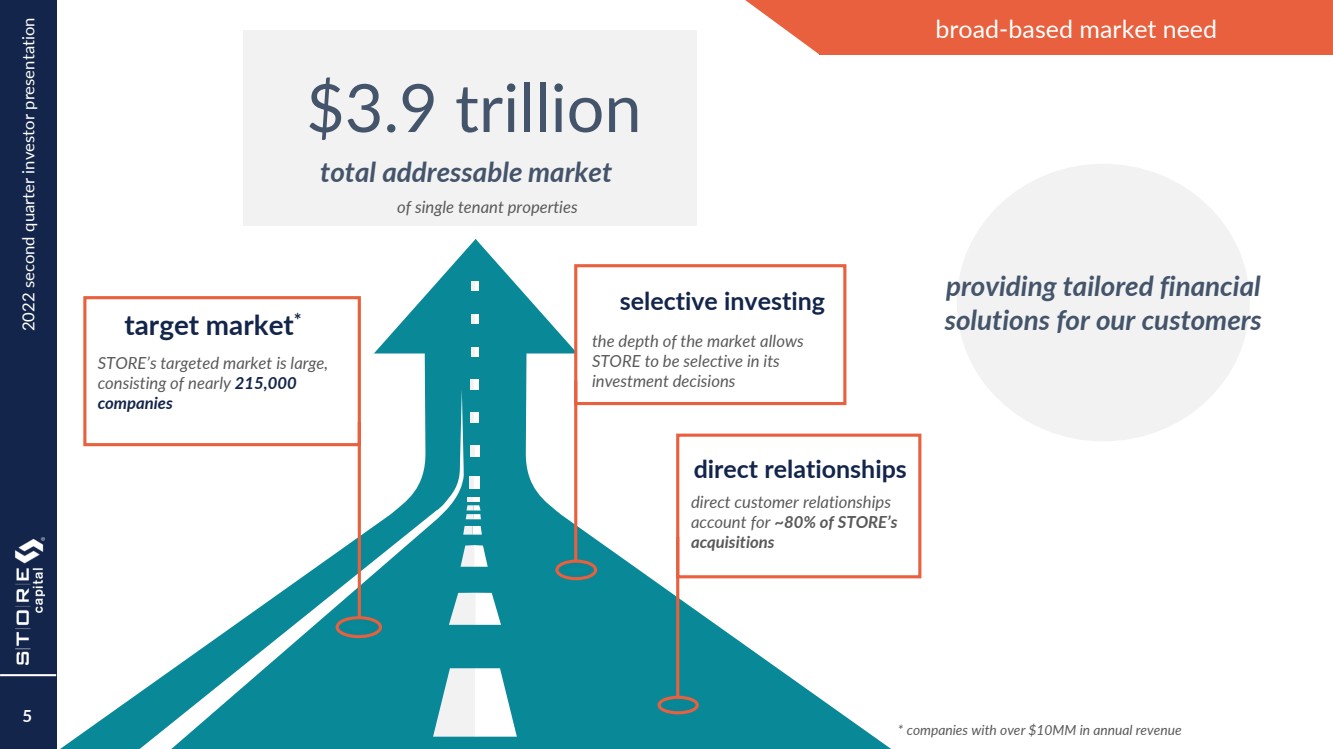

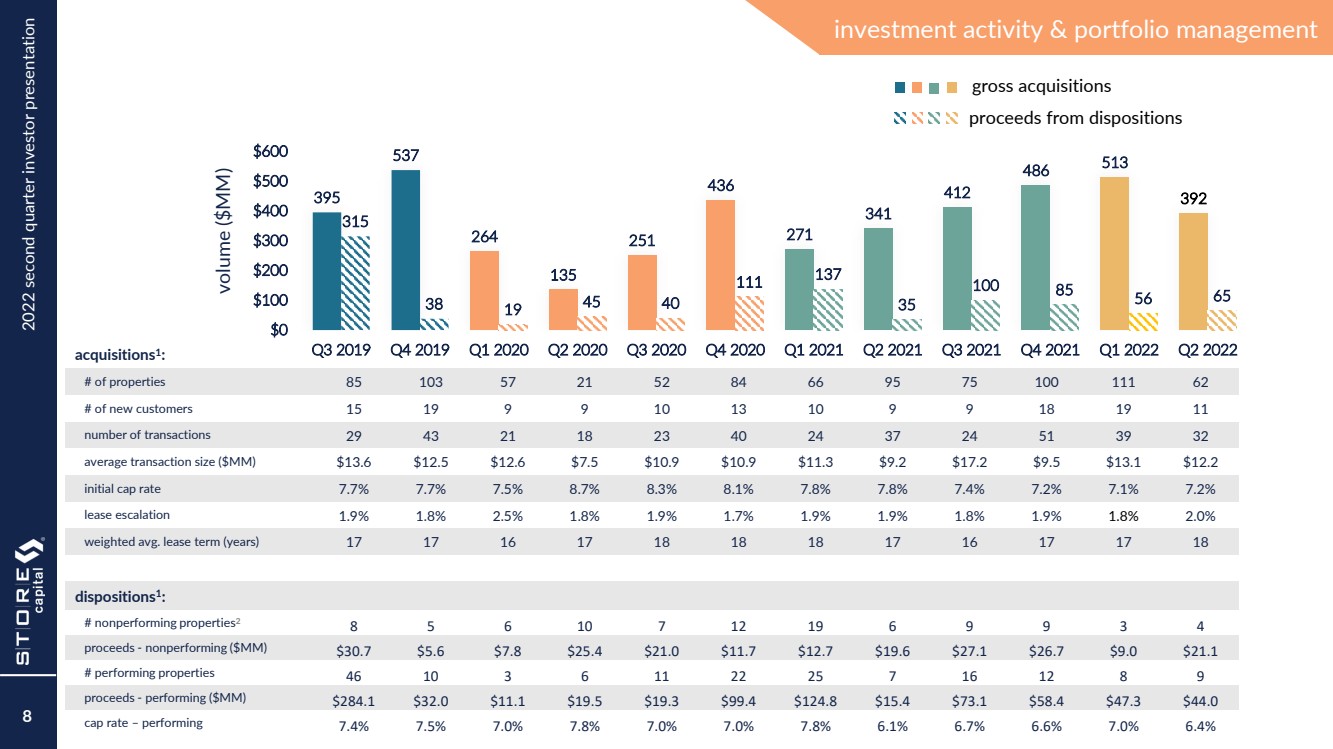

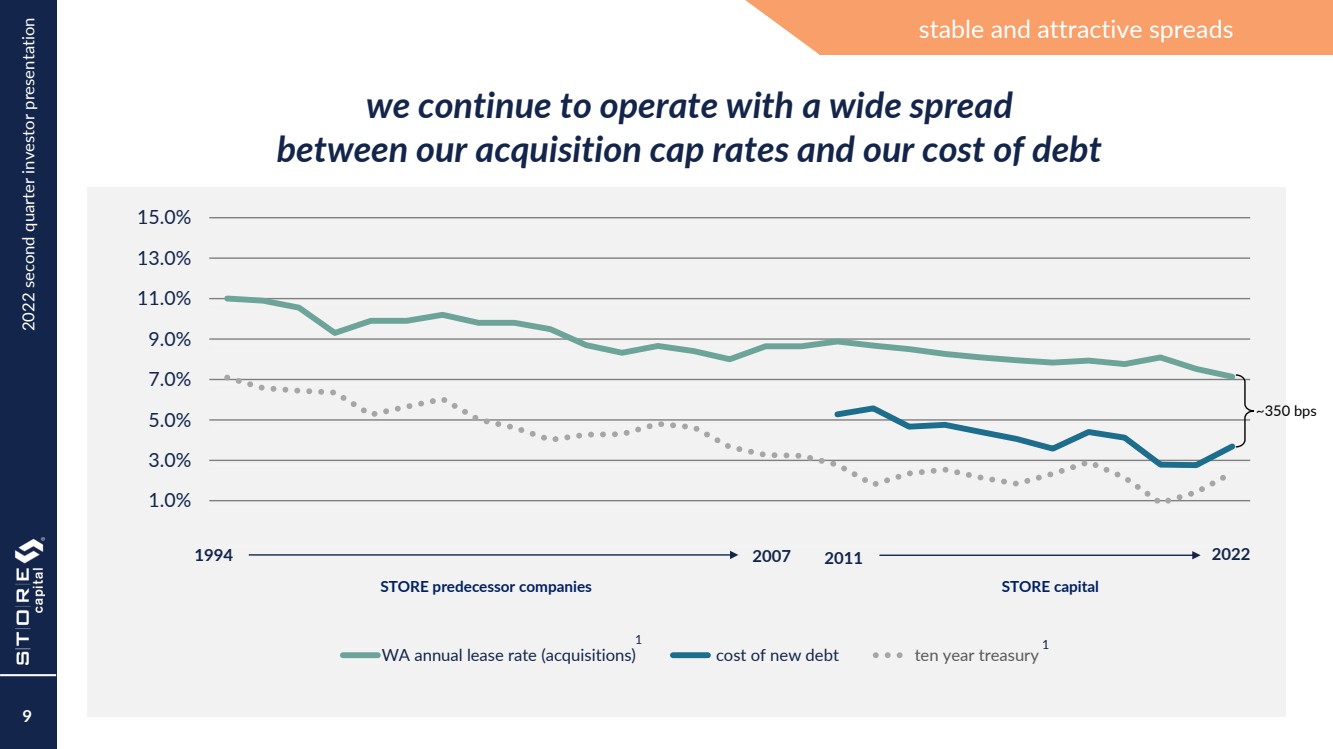

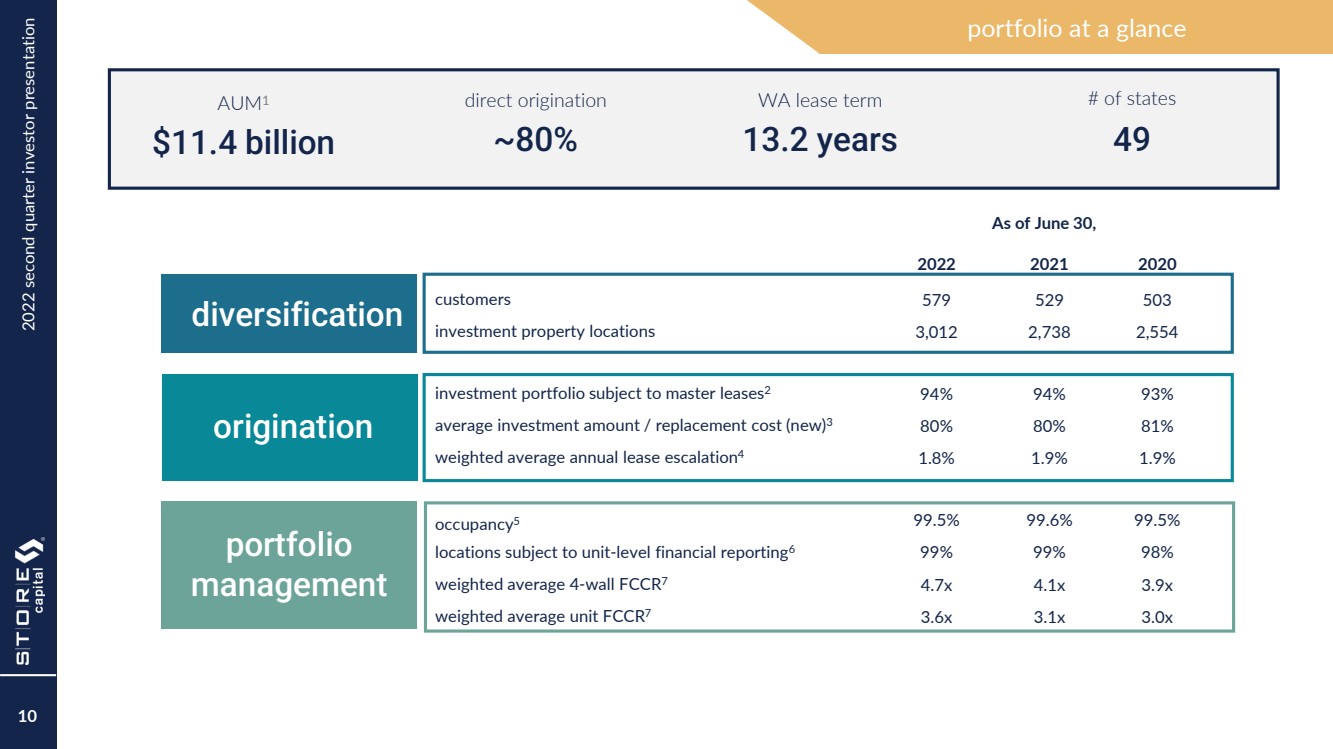

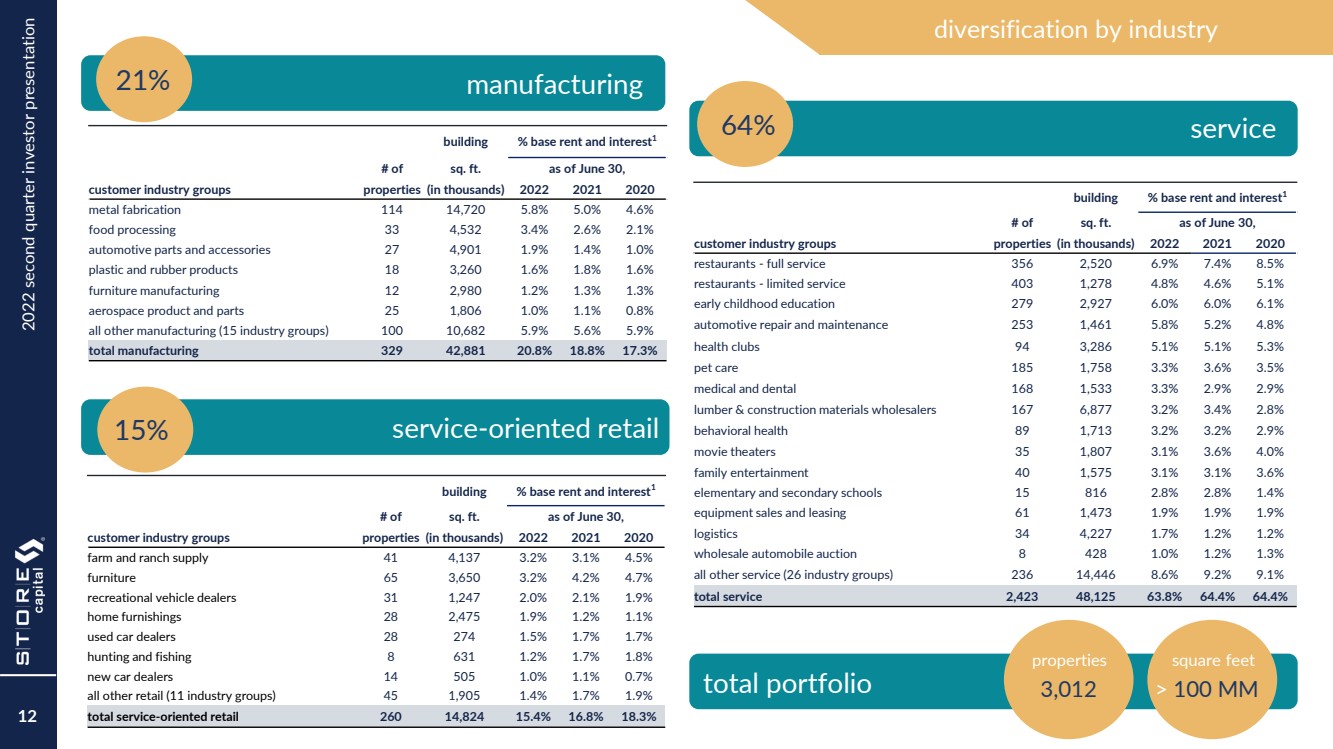

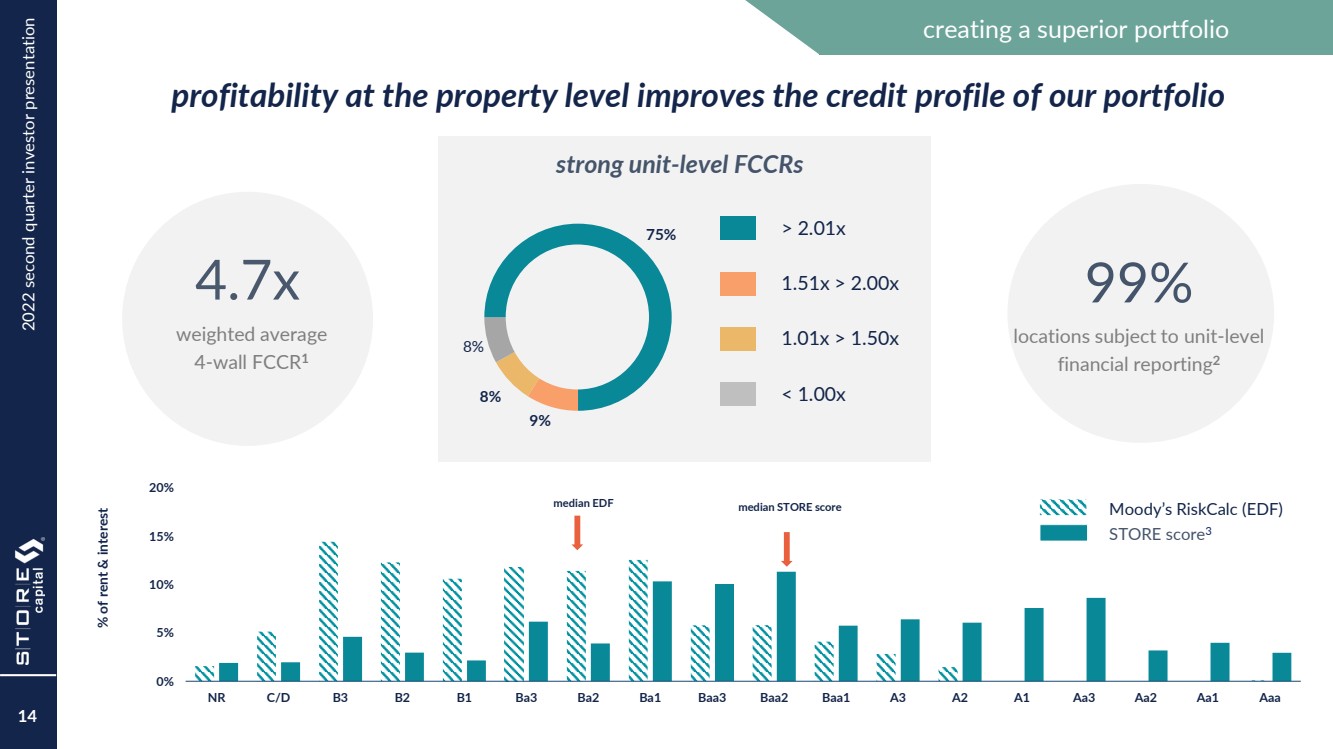

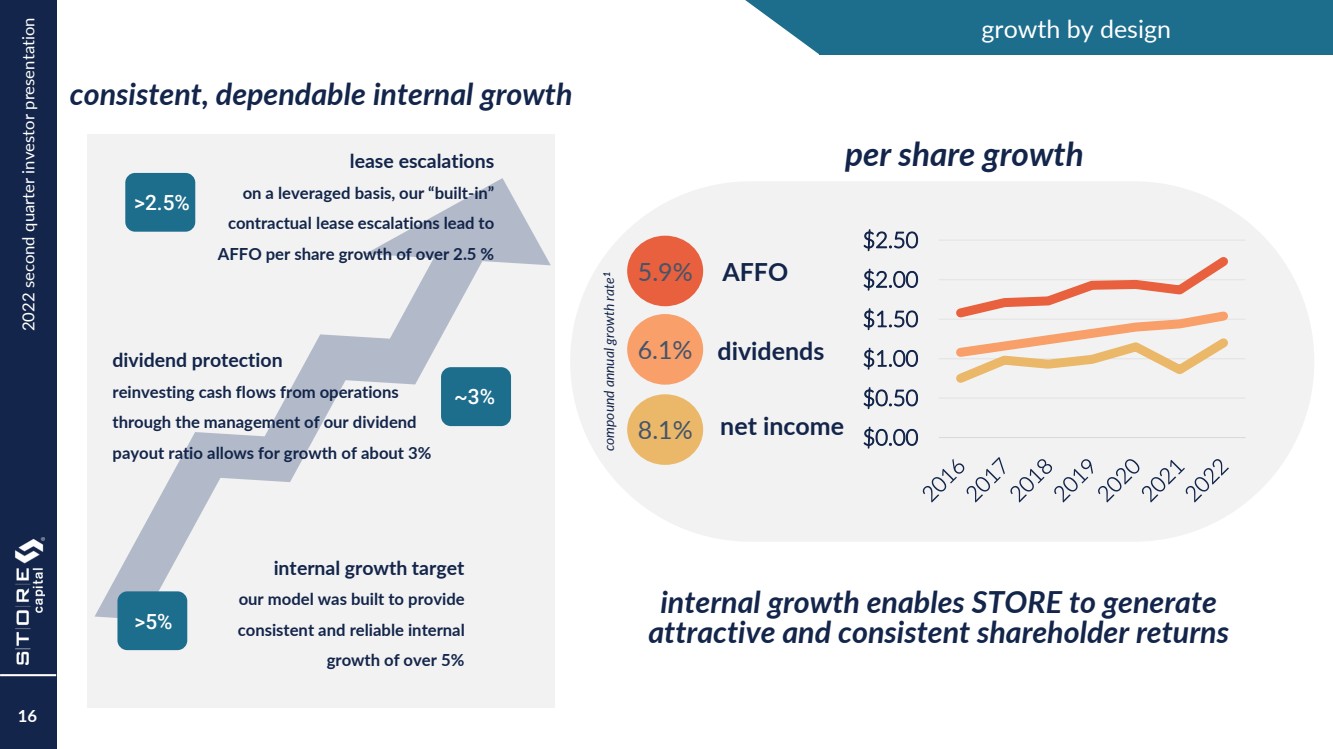

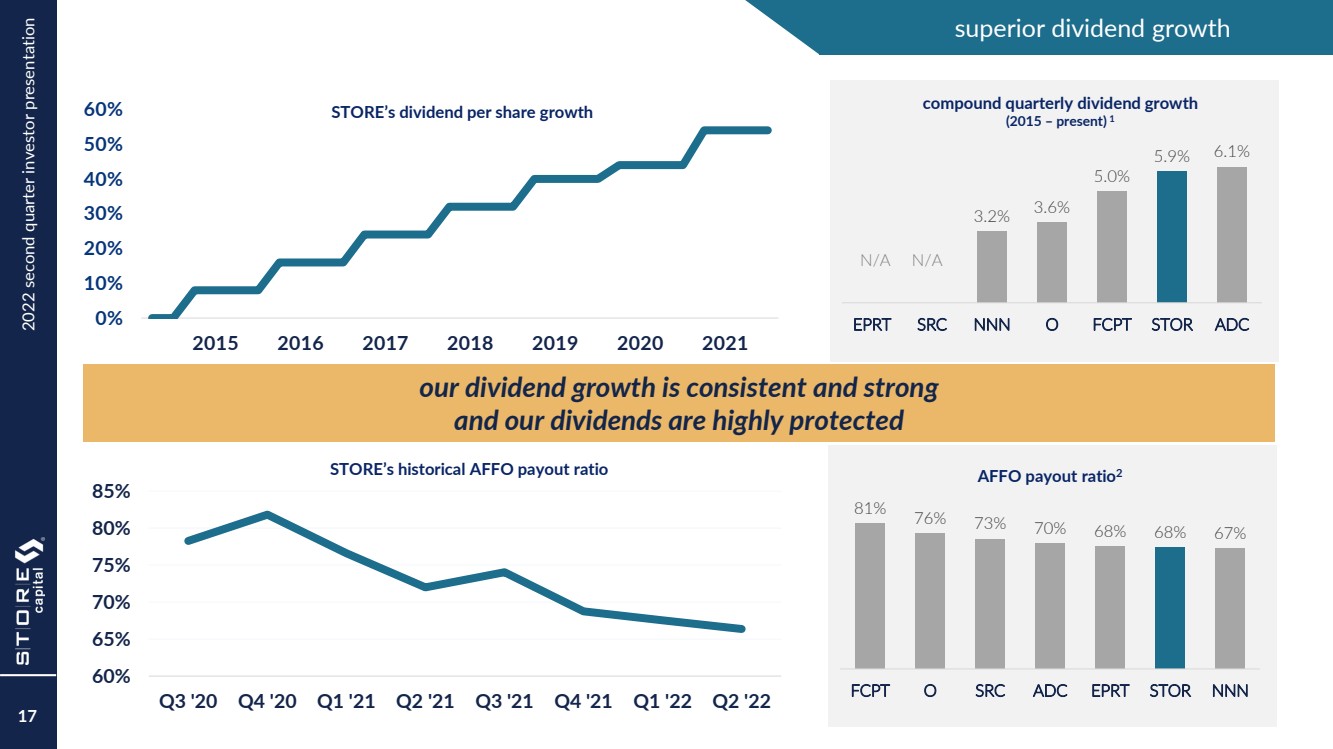

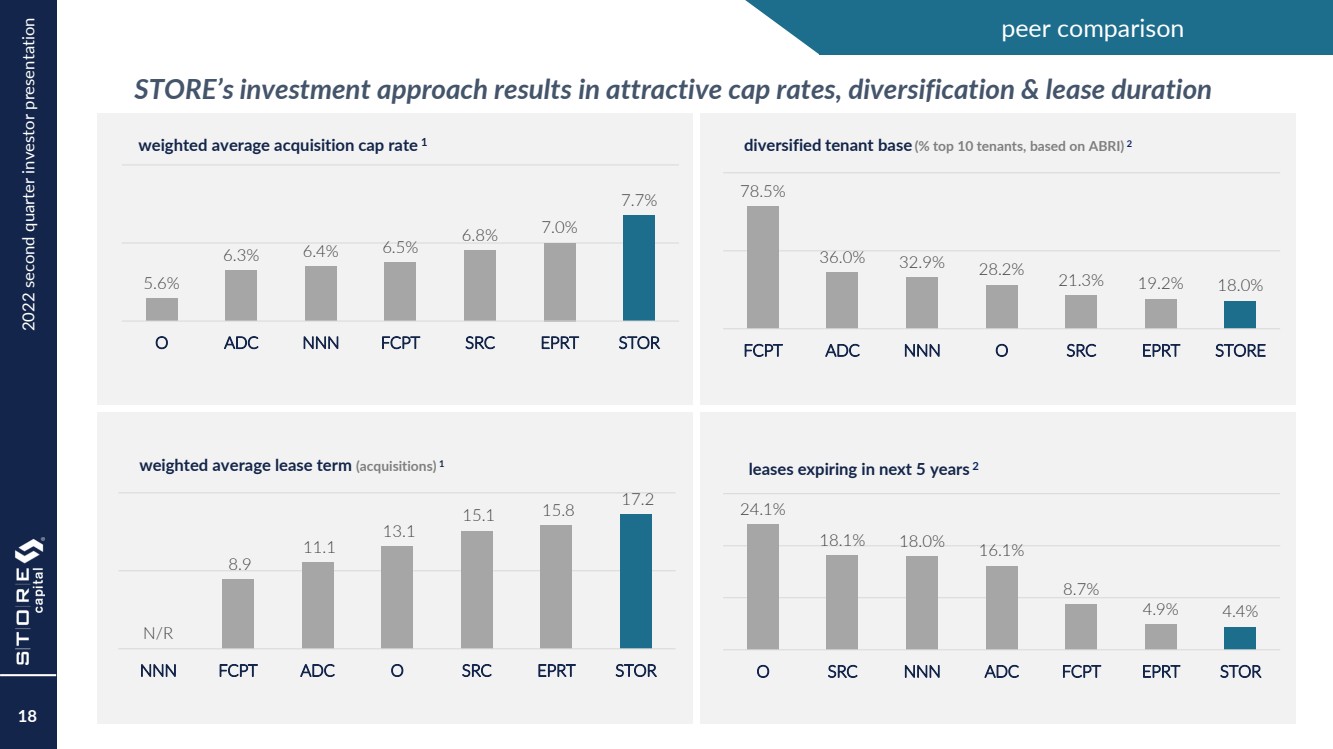

| 2022 second quarter investor presentation footnotes 24 Page 3: 1 Represents the weighted - average 4 - Wall coverage ratio of the portfolio as of June 30, 2022. The 4 - Wall coverage ratio refers to a unit’s FCCR before taking into account standardized corporate overhead expense. STORE also calculates a unit fixed charge coverage ratio generally as the ratio of (i) the unit’s EBITDAR, less a standardized corporate overhead expense based on estimated industry standards, to (ii) the unit’s total fixed charges, which are its lease expense, interest expense and scheduled principal payments on indebtedness (if applicable). The weighted average unit FCCR was 3.6x as of June 30, 2022. The median 4 - Wall coverage ratio and unit FCCR were 3.1x and 2.5x, respectively, as of June 30, 2022. 2 Denotes the percentage our largest customer or our top ten largest customers represent of our total base rent and interest as of June 30, 2022. See Page 11 for listing of top ten customers. 3 Assets Under Management (AUM) represents our total investment in real estate assets (gross of accumulated depreciation and amortization) as of June 30, 2022. 4 Refer to page 23 for definitions of non - GAAP financial measures and page 7 of the Company’s Earnings Supplement filed as Exhibit 99.2 to the Company’s Form 8 - K filed with the SEC on August 3, 2022 for a reconciliation to net income. 5 Represents the estimated growth rate in AFFO per diluted share based on the low - and high - points of our 2022 guidance as compared to AFFO per diluted share of $2.05 for the year ended December 31, 2021. See page 22 for discussion regarding use of Adjusted Funds from Operations. Page 6: 1 Represents the weighted average percentage change (by base rent and interest) in reported corporate revenues for the trailing 12 - month (or nine - month if 12 - month was not available) period as reported to STORE Capital for the fiscal periods ended at or near December 31, 2021 as compared to the same periods ended December 31, 2020. Excludes customers representing 5% of base rent and interest because applicable comparable data was not available. 2 Estimated based on total revenue per employee for all companies in the middle market (based on data reported by the National Center for the Middle Market for 2021) extrapolated to the aggregate total revenue of STORE’s customers. 3 Represents the number of locations operated by STORE’s customers as reported to STORE Capital as of December 31, 2021. Page 8: 1 Acquisitions represent both acquisitions of real estate and investment in loans and financing receivables. Dispositions represent the net proceeds received from the sale of real estate and lease termination fees received in conjunction with those sales. 2 Includes the number of properties sold that were vacant or not performing at the time of sale. Page 9: 1 Source: U.S. Treasury and Company Data. With respect to the STORE Predecessor Companies (FFCA and Spirit Finance) data, publicly available Company filings with the SEC. Page 10: 1 Assets Under Management (AUM) represents the Company’s total investment in real estate assets (gross of accumulated depreciation and amortization) as of June 30, 2022. 2 The percentage of investment portfolio subject to master leases represents the percentage (based on base rent and interest) of the investment portfolio in multiple properties with a single customer subject to master leases. Approximately 87% of the investment portfolio involves multiple properties with a single customer, whether or not subject to a master lease. 3 The average investment amount/replacement cost (new) represents the ratio of purchase price to replacement cost (new) at acquisition. 4 Weighted average annual lease escalation represents the weighted average annual escalation rate of the entire portfolio as if all escalations occurred annually. For escalations based on a formula including CPI, assumes the stated fixed percentage in the contract or assumes 1.5% if no fixed percentage is in the contract. For contracts with no escalations remaining in the current lease term, assumes the escalation in the extension term. Calculation excludes contracts representing less than 0.1% of base rent and interest where there are no further escalations remaining in the current lease term and there are no extension options. 5 STORE defines occupancy as a property being subject to a lease or loan contract. As of June 30, 2022, sixteen of our properties were vacant and not subject to a contract. 6 Of the 99% of our properties that are required to provide unit - level reporting, 93% have provided current obligated statements as of July 25, 2022. Page 10 – continued: 7 Represents the weighted - average 4 - Wall and unit fixed charge coverage ratio of the portfolio as of June 30, 2022, 2021 and 2020. The 4 - Wall coverage ratio refers to a unit’s FCCR before taking into account standardized corporate overhead expense. STORE also calculates a unit fixed charge coverage ratio generally as the ratio of (i) the unit’s EBITDAR, less a standardized corporate overhead expense based on estimated industry standards, to (ii) the unit’s total fixed charges, which are its lease expense, interest expense and scheduled principal payments on indebtedness (if applicable). The median 4 - Wall coverage ratio and unit FCCR were 3.1x and 2.5x, respectively, as of June 30, 2022, 3.0x and 2.4x, respectively, as of June 30, 2021 and 2.5x and 2.1x, respectively, as of June 30, 2020. Page 11: 1 Data as of June 30, 2022, by percentage of base rent and interest (based on rates in effect on June 30, 2022, for all leases, loans and financing receivables in place as of that date). Page 12: 1 Data as of June 30, 2022, 2021 and 2020, by percentage of base rent and interest (based on rates in effect on those dates, for all leases, loans and financing receivables in place as of those dates). Page 14: 1 Represents the weighted - average 4 - Wall coverage ratio of the portfolio as of June 30, 2022. The 4 - Wall coverage ratio refers to a unit’s FCCR before taking into account standardized corporate overhead expense. STORE also calculates a unit fixed charge coverage ratio generally as the ratio of (i) the unit’s EBITDAR, less a standardized corporate overhead expense based on estimated industry standards, to (ii) the unit’s total fixed charges, which are its lease expense, interest expense and scheduled principal payments on indebtedness (if applicable). The weighted average unit FCCR was 3.6x as of June 30, 2022. The median 4 - Wall coverage ratio and unit FCCR were 3.1x and 2.5x, respectively , as of June 30, 2022. 2 Of the 99% of our properties that are required to provide unit - level reporting, 93% have provided current obligated statements as of July 25, 2022. .. |