UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22671

ALLIANCEBERNSTEIN MULTI-MANAGER

ALTERNATIVE FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: March 31, 2014

Date of reporting period: March 31, 2014

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

ALLIANCEBERNSTEIN

MULTI-MANAGER ALTERNATIVE FUND

ANNUAL REPORT

MARCH 31, 2014

Table of Contents

Before investing in the fund a prospective investor should consider carefully the fund’s investment objectives and policies, charges, expenses and risks. These and other matters of importance to prospective investors are contained in the fund’s prospectus, an additional copy of which may be obtained by visiting our website at www.bernstein.com and clicking on “Investments”, then “Stocks” or “Bonds”, then “Prospectuses, SAIs and Shareholder Reports” or by calling your financial advisor or by calling Bernstein’s mutual fund shareholder help line at 212.756.4097. Please read the prospectus carefully before investing.

For performance information current to the most recent month-end, please call (collect) (212) 486-5800.

This shareholder report must be preceded or accompanied by the prospectus for individuals who are not shareholders of the fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit www.alliancebernstein.com, or go to the Securities and Exchange Commission’s website at www.sec.gov, or call AllianceBernstein at 800.227.4618.

The fund will file its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available on the Commission’s website at www.sec.gov. The fund’s Form N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C.; information on the operation of the Public Reference Room may be obtained by calling 800.SEC.0330.

Investment Products Offered: · Are Not FDIC Insured · May Lose Value · Are Not Bank Guaranteed

Annual Report

May 15, 2014

This report provides certain performance data for AllianceBernstein Multi-Manager Alternative Fund (the “Fund”) for the annual reporting period ended March 31, 2014.

Investment Objectives and Policies

The investment objective of the Fund is to seek long-term capital appreciation. There can be no assurance that the Fund will achieve its investment objective, be able to structure its investments as anticipated, or that its returns will be positive over any period of time. The Fund is not intended as a complete investment program for investors.

The Fund seeks to achieve its investment objective primarily by allocating its assets among investments in a diversified portfolio of private investment vehicles, commonly referred to as hedge funds. The Fund invests primarily in hedge funds pursuing the following strategies: long/short equity, event driven, credit/distressed, emerging markets, global macro and other strategies. For more information on these strategies, please see “Portfolio of Investments” on pages 5-6. For more information regarding the Fund’s risks, please see “Disclosures and Risks” on page 2 and “Note E—Risks Involved in Investing in the Fund” of the Notes to Financial Statements on pages 17-18.

Investment Results

The Fund outperformed the Hedge Fund Research Index (“HFRI”) Fund of Fund Composite Index for the six- and 12-month periods ended March 31, 2014. Over both periods, all strategies but global macro contributed positively to results. Event driven and long/short equity strategies were the top performing strategies during both periods. Record levels of cash on corporate balance sheets and an ability to issue debt at low rates provided a positive backdrop for event-related activity. Meanwhile, long/short equity managers were able to generate returns primarily through fundamental security selection as intra-stock correlations, which had been near historical highs, began to normalize. The global macro funds that we invest with outperformed peers who employ this approach for the 12 months ended March 31, 2014, as measured by the HFRI Macro Index, yet were down modestly.

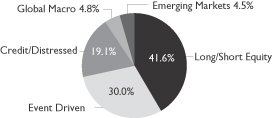

As of March 31, 2014, the Fund was allocated: 41% to long/short equity among 18 managers; 30% to event driven among 13 managers; 19% to credit/distressed among 9 managers; 5% among 2 emerging markets managers; and 5% among 2 global macro managers.

Market Review and Investment Strategy

The capital markets were uneven in the 12 months ending March 31, 2014. Global developed-market stocks posted a banner year, fueled by generally brighter macroeconomic signals, an investor migration toward risk assets (until late in the period), and easy-monetary policies from the central banks. At the same time, emerging-market stocks ended the period modestly in the red, the victim of slowing economies and widespread political turmoil.

Bonds, both taxable and municipal, ended the 12-month period essentially flat, with yields at first moving up and then partially retracing their steps at some key maturities.

Meanwhile, the Fund’s performance was in between lackluster bonds and surging developed-market stocks: an outcome consistent with our expectations for hedge funds in a bull market. In line with our goal to capitalize on return opportunities across the spectrum and limit risk, our portfolio remains highly diversified by manager and by fund strategy.

Disclosures and Risks

AllianceBernstein Multi-Manager Alternative Fund Shareholder Information

Benchmark Disclosure

The HFRI Fund of Funds Composite Index is an equal-weighted performance index that includes over 650 constituent funds of hedge funds that report their monthly net-of-fee returns to Hedge Fund Research, have at least $50 million under management and have been actively trading for at least 12 months. The HFRI Fund of Funds Composite Index does not reflect the fees and expenses of the Fund or a similar mutual fund portfolio. An investor cannot invest directly in the index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word about Risk

An investment in the Fund’s shares may be speculative in that it involves a high degree of risk and should not constitute a complete investment program. Before making an investment decision, you should carefully consider the following risk factors, together with the other information contained in the Fund’s prospectus. At any point in time, an investment in the Fund’s shares may be worth less than the original amount invested, even after taking into account the distributions paid, if any, and the ability of shareholders to reinvest distributions. If any of the risks discussed in the prospectus occurs, the Fund’s results of operations could be materially and adversely affected. If this were to happen, the price of Fund shares could decline significantly and you could lose all or a part of your investment.

Investment in this Fund is highly speculative and involves substantial risk, including loss of principal, and therefore may not be suitable for all investors.

General Risk Factors. Underlying portfolios may exhibit high volatility, and investors may lose all or substantially all of their investment. Investments in illiquid assets and foreign markets and the use of short sales, options, leverage, futures, swaps, and other derivative instruments may create special risks and substantially increase the impact and likelihood of adverse price movements. Interests in underlying portfolios are subject to limitations on transferability and are illiquid, and no secondary market for interests typically exists or is likely to develop. Underlying portfolios are typically not registered with securities regulators and are therefore generally subject to little or no regulatory oversight. Performance compensation may create an incentive to make riskier or more speculative investments. Underlying portfolios typically charge higher fees than many other types of investments, which can offset trading profits, if any. There can be no assurance that any underlying portfolios will achieve its investment objectives.

Tax Risks. The Fund intends to be treated as a regulated investment company (a “RIC”) under the Internal Revenue Code. However, in order to qualify as a RIC and also to avoid having to pay an “excise tax,” the Fund will be subject to certain limitations on its investments and operations, including a requirement that a specified proportion of its income come from qualifying sources, an asset diversification requirement, and minimum distribution requirements. Satisfaction of the various requirements requires significant support and information from the underlying portfolio funds, and such support and information may not be available, sufficient, verifiable, or provided on a timely basis.

Limited Operating History. The Fund has little operating history upon which prospective investors can evaluate the performance of the Fund. There can be no assurance that the Fund will achieve its investment objective. The past investment performance of other accounts managed by the Investment Manager and its affiliates should not be construed as an indication of the future results of an investment in the Fund.

Fund of Funds Considerations. The Fund will have no control rights over and limited transparency into the investment programs of the underlying funds in which it invests. In valuing the Portfolio’s holdings, the Investment Manager will generally rely on financial information provided by underlying funds, which may be unaudited, estimated, and/or may not involve third parties. The Fund’s investment opportunities may be limited as a result of withdrawal terms or anticipated liquidity needs (e.g., withdrawal restrictions imposed by underlying hedge funds may delay, preclude, or involve expense in connection with portfolio adjustments by the Investment Manager).

These risks are more fully discussed in the Fund’s prospectus.

An Important Note About Historical Performance

The performance on the following page represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes.

| | |

| 2 | | AllianceBernstein Multi-Manager Alternative Fund |

Historical Performance

The Fund vs. HFRI FOF Composite

| | | | | | | | |

| | | RETURNS | |

| PERIODS ENDED MARCH 31, 2014 | | 6 MONTHS | | | 12 MONTHS | |

AllianceBernstein Multi-Manager Alternative Fund | | | 5.02 | % | | | 8.04 | % |

HFRI FOF Composite | | | 4.19 | % | | | 5.98 | % |

The Fund’s prospectus fee table shows the Fund’s total annual operating expense ratios as 7.96%, (including the Fund’s proportionate share of underlying fund fees and expenses) gross of any fee waivers or expense reimbursements. Contractual fee waivers and/or expense reimbursements served to limit the Fund’s annual operating expenses to 7.67%. These waivers/reimbursements may not be terminated prior to July 31, 2014. The Financial Highlights section of this report sets forth expense ratio data for the current reporting period; the expense ratios shown above may differ from the expense ratios in the Financial Highlights sections since they are based on different time periods.

See Disclosures, Risks and Note about Historical Performance on page 2.

Portfolio Summary—March 31, 2014 (Unaudited)

| | | | |

| Net Assets ($mil): $980.5 | | | | |

| Underlying Portfolio Strategy Breakdown* | | | | |

| | | | |

| * | | All data are as of March 31, 2014. The Fund’s strategy breakdown is expressed as a percentage of total investments and may vary over time. Investments other than Underlying Portfolios constitute less than 0.1% of Fund Investments. |

| | |

| 4 | | AllianceBernstein Multi-Manager Alternative Fund |

Portfolio of Investments—March 31, 2014

| | | | | | | | | | | | |

| Underlying Portfolios | | | | Fair Value ($) | | | % Net

Assets | | | Liquidity* |

Long/Short Equity | | | | | | | | | | | | |

Aravt Global Fund Ltd. | | | | $ | 14,089,291 | | | | 1.4 | % | | Semi-Annual |

Cadian Offshore Fund Ltd. | | | | | 20,348,442 | | | | 2.1 | | | Semi-Annual |

Coatue Offshore Fund, Ltd. | | | | | 27,407,103 | | | | 2.8 | | | Quarterly |

Corvex Offshore Ltd. | | | | | 27,395,872 | | | | 2.8 | | | Quarterly |

Criterion Horizons Offshore, Ltd. | | | | | 24,378,033 | | | | 2.5 | | | Monthly |

Egerton Long-Short Fund (USD) Limited | | | | | 14,858,897 | | | | 1.5 | | | Monthly |

Falcon Edge Global, Ltd | | | | | 28,571,171 | | | | 2.9 | | | Quarterly |

JANA Nirvana Offshore Fund, Ltd. | | | | | 25,235,607 | | | | 2.6 | | | Quarterly |

Luminus Energy Partners Ltd. | | | | | 17,770,238 | | | | 1.8 | | | Quarterly |

Nokota Capital Offshore Fund, Ltd. | | | | | 27,423,730 | | | | 2.8 | | | Quarterly |

OrbiMed Partners, Ltd. | | | | | 28,062,599 | | | | 2.9 | | | Quarterly |

Pershing Square International, Ltd. | | | | | 14,941,839 | | | | 1.5 | | | Quarterly |

Sheffield International Partners, Ltd. | | | | | 20,809,198 | | | | 2.1 | | | Biennially |

Starboard Leaders Fund LP | | | | | 5,027,524 | | | | 0.5 | | | Monthly |

Starboard Value and Opportunity Fund Ltd | | | | | 20,778,997 | | | | 2.1 | | | Quarterly |

Think Investments Offshore Ltd. | | | | | 19,163,983 | | | | 2.0 | | | Semi-Annual |

Tybourne Equity (Offshore) Fund | | | | | 27,870,519 | | | | 2.8 | | | Quarterly |

Wellington Management Investors (Bermuda), Ltd. | | | | | 22,279,400 | | | | 2.3 | | | Semi-Annual |

White Elm Capital Offshore, Ltd. | | | | | 22,051,904 | | | | 2.3 | | | Semi-Annual |

| | | | | | | | | | | | |

Total | | | | | 408,464,347 | | | | 41.7 | | | |

| | | | | | | | | | | | |

Event Driven | | | | | | | | | | | | |

Canyon Balanced Fund (Cayman), Ltd. | | | | | 31,750,723 | | | | 3.2 | | | Quarterly |

CQS Directional Opportunities Feeder Fund Limited | | | | | 25,244,215 | | | | 2.6 | | | Monthly |

Empyrean Capital Overseas Fund, Ltd. | | | | | 10,782,211 | | | | 1.1 | | | Quarterly |

Fir Tree International Value Fund, Ltd. | | | | | 30,188,393 | | | | 3.1 | | | Biennially |

Indaba Capital Partners (Cayman), LP | | | | | 20,674,982 | | | | 2.1 | | | Quarterly |

King Street Capital, Ltd. | | | | | 27,177,295 | | | | 2.8 | | | Quarterly |

Luxor Capital Partners Offshore, Ltd. | | | | | 24,545,803 | | | | 2.5 | | | Biennially |

Manikay Offshore Fund, Ltd. | | | | | 22,115,671 | | | | 2.3 | | | Quarterly |

Pentwater Event Fund Ltd. | | | | | 25,023,188 | | | | 2.5 | | | Monthly |

Roystone Capital Offshore Fund Ltd. | | | | | 9,999,264 | | | | 1.0 | | | Quarterly |

Senator Global Opportunity Offshore Fund, Ltd | | | | | 24,314,130 | | | | 2.5 | | | Quarterly |

TBC Offshore Ltd. | | | | | 19,698,671 | | | | 2.0 | | | Quarterly |

Third Point Offshore Fund, Ltd. | | | | | 23,066,138 | | | | 2.3 | | | Quarterly |

| | | | | | | | | | | | |

Total | | | | | 294,580,684 | | | | 30.0 | | | |

| | | | | | | | | | | | |

Credit/Distressed | | | | | | | | | | | | |

Claren Road Credit Fund, Ltd. | | | | | 27,464,626 | | | | 2.8 | | | Quarterly |

Halcyon Offshore Asset-Backed Value Fund Ltd. | | | | | 13,237,373 | | | | 1.4 | | | Quarterly |

JMB Capital Partners Offshore, Ltd. | | | | | 25,841,485 | | | | 2.6 | | | Annual |

Oaktree Value Opportunities (Cayman) Fund, Ltd. | | | | | 17,593,735 | | | | 1.8 | | | Partial Liquidity Every 1.5 Years |

Panning Overseas Fund, Ltd. | | | | | 26,732,597 | | | | 2.7 | | | Quarterly |

Saba Capital Offshore Fund, Ltd. | | | | | 16,030,139 | | | | 1.6 | | | Quarterly |

Silver Point Capital Offshore Fund, Ltd. | | | | | 28,447,676 | | | | 2.9 | | | Annual |

Stone Lion Fund Ltd. | | | | | 23,605,138 | | | | 2.4 | | | Quarterly |

Wingspan Overseas Fund, Ltd | | | | | 8,364,373 | | | | 0.9 | | | Quarterly |

| | | | | | | | | | | | |

Total | | | | | 187,317,142 | | | | 19.1 | | | |

| | | | | | | | | | | | |

Global Macro | | | | | | | | | | | | |

Brevan Howard Multi-Strategy Fund Limited | | | | | 22,654,084 | | | | 2.3 | | | Monthly |

MKP Opportunity Offshore, Ltd. | | | | | 24,134,251 | | | | 2.5 | | | Monthly |

| | | | | | | | | | | | |

Total | | | | | 46,788,335 | | | | 4.8 | | | |

| | | | | | | | | | | | |

Portfolio of Investments (continued)

| | | | | | | | | | | | | | |

| Underlying Portfolios | | | | | Fair Value ($) | | | % Net

Assets | | | Liquidity* |

Emerging Markets | | | | | | | | | | | | | | |

Discovery Global Opportunity Fund, Ltd | | | | | | $ | 25,352,770 | | | | 2.6 | % | | Semi-Annual |

Spinnaker Global Emerging Markets Holdings, Ltd. | | | | | | | 19,296,482 | | | | 2.0 | | | Annual |

| | | | | | | | | | | | | | |

Total | | | | | | | 44,649,252 | | | | 4.6 | | | |

| | | | | | | | | | | | | | |

Total Underlying Portfolios

(cost $898,032,601) | | | | | | | 981,799,760 | | | | 100.2 | | | |

| | | | | | | | | | | | | | |

| | | Shares | | | | | | | | | |

Common Stocks | | | | | | | | | | | | | | |

Herbalife, Ltd.

(cost $481,148) | | | 7,531 | | | | 431,301 | | | | 0.0 | | | |

| | | | | | | | | | | | | | |

Total Investments | | | | | | | | | | | | | | |

(cost $898,513,749) | | | | | | | 982,231,061 | | | | 100.2 | % | | |

Liabilities in excess of other assets | | | | | | | (1,693,831 | ) | | | (0.2 | ) | | |

| | | | | | | | | | | | | | |

Net Assets | | | | | | $ | 980,537,230 | | | | 100.0 | % | | |

| | | | | | | | | | | | | | |

* The investment strategies and liquidity of the Underlying Portfolios in which the Fund invests are as follows:

Long/Short Equity Underlying Portfolios seek to buy securities with the expectation that they will increase in value (called “going long”) and sell securities short in the expectation that they will decrease in value (“going short”). Underlying Portfolios within this strategy are generally subject to 30 – 90 day redemption notice periods. The Underlying Portfolios have monthly to biennial liquidity. The majority of the managers have initial lockups of less than a year and a half. Private investment vehicles within the strategy may have lock up periods of up to five years.

Credit/Distressed Underlying Portfolios invest in a variety of fixed income and other securities, including bonds (corporate and government), bank debt, asset-backed financial instruments, mortgage-backed securities and mezzanine and distressed securities, as well as securities of distressed companies and high yield securities. Underlying Portfolios within this strategy are generally subject to 45 – 90 day redemption notice periods. The Underlying Portfolios have monthly to one and a half years’ liquidity. Private investment vehicles within the strategy may have lock up periods of up to three years.

Event Driven Underlying Portfolios seek to take advantage of information inefficiencies resulting from a particular corporate event, such as a takeover, liquidation, bankruptcy, tender offer, buyback, spin-off, exchange offer, merger or other type of corporate reorganization. Underlying Portfolios within this strategy are generally subject to 60 – 180 day redemption notice periods. The Underlying Portfolios have monthly to biennial liquidity. Private investment vehicles within the strategy may have lock up periods of up to two years.

Emerging Markets Underlying Portfolios invest in a range of emerging markets asset classes including debt, equity and currencies, and may use a broad array of hedging techniques involving both emerging markets and non-emerging markets securities with the intention of reducing volatility and enhancing returns. Underlying Portfolios within this strategy are generally subject to 60 – 120 day redemption notice periods. The Underlying Portfolios have semi-annual to annual liquidity. Private investment vehicles within the strategy may have lock up periods of up to three years.

Global Macro Underlying Portfolios aim to identify and exploit imbalances in global economics and asset classes, typically utilizing macroeconomic and technical market factors rather than “bottom-up” individual security analysis. Underlying Portfolios within this strategy are generally subject to 60 – 90 day redemption notice periods. The Underlying Portfolios have monthly liquidity. Private investment vehicles within the strategy may have lock up periods of up to two years.

The Fund may also make direct investments in securities (other than securities of Underlying Portfolios), options, futures, options on futures, swap contracts, or other derivative or financial instruments.

See Notes to Financial Statements.

| | |

| 6 | | AllianceBernstein Multi-Manager Alternative Fund |

Statement of Assets and Liabilities—March 31, 2014

| | | | |

| |

| ASSETS | | | | |

Investments, at value (cost $898,513,749) | | $ | 982,231,061 | |

Cash (see Note A2) | | | 51,069,835 | |

Investment in Underlying Portfolios paid in advance (see Note A2) | | | 21,000,000 | |

| | | | |

Total assets | | | 1,054,300,896 | |

| | | | |

| |

| LIABILITIES | | | | |

Subscriptions received in advance | | | 64,403,480 | |

Payable for shares of beneficial interest redeemed | | | 7,557,007 | |

Management fee payable | | | 1,363,213 | |

Transfer Agent fee payable | | | 16,709 | |

Accrued expenses | | | 423,257 | |

| | | | |

Total liabilities | | | 73,763,666 | |

| | | | |

NET ASSETS | | $ | 980,537,230 | |

| | | | |

| |

| COMPOSITION OF NET ASSETS | | | | |

Shares of beneficial interest, at par | | $ | 85,944 | |

Additional paid-in capital | | | 925,143,124 | |

Distributions in excess of net investment income | | | (26,437,251 | ) |

Accumulated net realized loss on investment transactions | | | (1,971,899 | ) |

Net unrealized appreciation on investments | | | 83,717,312 | |

| | | | |

NET ASSETS | | $ | 980,537,230 | |

| | | | |

SHARES OF BENEFICIAL INTEREST OUTSTANDING—UNLIMITED SHARES AUTHORIZED, WITH PAR VALUE OF $.001 | | | | |

(based on 85,944,028 shares outstanding) | | $ | 11.41 | |

| | | | |

See Notes to Financial Statements.

Statement of Operations—for the year ended March 31, 2014

| | | | | | | | |

| | |

| INVESTMENT INCOME | | | | | | | | |

Dividends from common stocks | | | | | | $ | 4,519 | |

| | | | | | | | |

Expenses | | | | | | | | |

Management fee (see Note B) | | $ | 10,335,776 | | | | | |

Custodian | | | 370,016 | | | | | |

Administrative | | | 268,002 | | | | | |

Offering expenses | | | 223,970 | | | | | |

Legal | | | 205,574 | | | | | |

Registration fees | | | 168,022 | | | | | |

Transfer agency | | | 137,810 | | | | | |

Trustees’ fees | | | 83,753 | | | | | |

Audit and Tax | | | 74,600 | | | | | |

Printing | | | 33,030 | | | | | |

Miscellaneous | | | 429,423 | | | | | |

| | | | | | | | |

Total expenses | | | 12,329,976 | | | | | |

Less: expenses waived and reimbursed by the Investment Manager (see Note B) | | | (271,569 | ) | | | | |

| | | | | | | | |

Net expenses | | | | | | | 12,058,407 | |

| | | | | | | | |

Net investment loss | | | | | | | (12,053,888 | ) |

| | | | | | | | |

| | |

| REALIZED AND UNREALIZED GAIN ON INVESTMENT TRANSACTIONS | | | | | | | | |

Net realized gain on investment transactions | | | | | | | 343,057 | |

Net change in unrealized appreciation/depreciation of investment transactions | | | | | | | 66,207,214 | |

| | | | | | | | |

Net gain on investment transactions | | | | | | | 66,550,271 | |

| | | | | | | | |

Net increase in net assets from operations | | | | | | $ | 54,496,383 | |

| | | | | | | | |

See Notes to Financial Statements.

| | |

| 8 | | AllianceBernstein Multi-Manager Alternative Fund |

Statement of Changes in Net Assets

| | | | | | | | |

| | | YEAR ENDED

MARCH 31, 2014 | | | OCTOBER 1, 2012(a)

TO MARCH 31, 2013 | |

| | |

| INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS | | | | | | | | |

Net investment loss | | $ | (12,053,888 | ) | | $ | (1,602,807 | ) |

Net realized gain on investment transactions | | | 343,057 | | | | 0 | |

Net change in unrealized appreciation/depreciation of investment transactions | | | 66,207,214 | | | | 17,510,098 | |

| | | | | | | | |

Net increase in net assets from operations | | | 54,496,383 | | | | 15,907,291 | |

| | | | | | | | |

| | |

| DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS FROM | | | | | | | | |

Net investment income | | | (12,368,064 | ) | | | (412,492 | ) |

Net realized gain on investment transactions | | | (2,314,956 | ) | | | 0 | |

| | |

| TRANSACTIONS IN SHARES OF BENEFICIAL INTEREST | | | | | | | | |

Net increase (see Note D) | | | 630,204,556 | | | | 294,924,512 | |

| | | | | | | | |

Total increase | | | 670,017,919 | | | | 310,419,311 | |

| | |

| NET ASSETS | | | | | | | | |

Beginning of period | | | 310,519,311 | | | | 100,000 | |

| | | | | | | | |

End of period (including distributions in excess of net investment income of ($26,437,251) and ($2,015,299), respectively) | | $ | 980,537,230 | | | $ | 310,519,311 | |

| | | | | | | | |

(a) Commencement of operations.

See Notes to Financial Statements.

Statement of Cash Flows—for the year ended March 31, 2014

| | | | |

Cash flows from operating activities | | | | |

Net increase (decrease) in net assets from operations | | $ | 54,496,383 | |

Adjustments to reconcile net increase (decrease) in net assets resulting

from operations to net cash used in operating activities: | | | | |

Purchases of investments | | | (605,355,296 | ) |

Sales of investments | | | 2,184,604 | |

Net realized (gain)/loss from investment transactions | | | (343,057 | ) |

Net change in unrealized appreciation/depreciation on investment transactions | | | (66,207,214 | ) |

Decrease in investments in Underlying Portfolios paid in advance | | | 5,000,000 | |

Decrease in deferred offering expense | | | 223,970 | |

Increase in management fee payable | | | 1,063,179 | |

Increase in accrued expenses | | | 218,649 | |

| | | | |

Net cash used in operating activities | | | (608,718,782 | ) |

| | | | |

Cash flows from financing activities | | | | |

Subscriptions, including change in subscriptions received in advance | | | 647,401,234 | |

Redemptions, net of payable for shares of beneficial interest redeemed | | | (14,773,054 | ) |

Distributions | | | (1,385,649 | ) |

| | | | |

Net cash provided by financing activities | | | 631,242,531 | |

| | | | |

Net change in cash | | | 22,523,749 | |

Cash at beginning of year | | | 28,546,086 | |

| | | | |

Cash at end of year | | $ | 51,069,835 | |

| | | | |

Supplemental disclosure of cash flow information:

Noncash financing activities not included herein consist of reinvestment of dividends of $13,297,371.

In accordance with U.S. GAAP, the Fund has included a Statement of Cash Flows as a result of its substantial investments in Level 3 securities throughout the period.

See Notes to Financial Statements.

| | |

| 10 | | AllianceBernstein Multi-Manager Alternative Fund |

Financial Highlights

Selected data for a share of beneficial interest outstanding throughout each period:

| | | | | | | | |

| | | YEAR ENDED

MARCH 31, 2014 | | | OCTOBER 1, 2012(a)

TO MARCH 31, 2013 | |

Net asset value, beginning of period | | $ | 10.75 | | | $ | 10.00 | |

| | | | | | | | |

Income from investment operations | | | | | | | | |

Net investment loss (b)(c) | | | (.20 | ) | | | (.09 | ) |

Net realized and unrealized gain on investment transactions | | | 1.06 | | | | .87 | |

| | | | | | | | |

Net increase in net asset value from operations | | | .86 | | | | .78 | |

| | | | | | | | |

Less: Dividends and Distributions | | | | | | | | |

Dividends from net investment income | | | (.17 | ) | | | (.03 | ) |

Distributions from net realized gain on investment transactions | | | (.03 | ) | | | 0 | |

| | | | | | | | |

Total dividends and distributions | | | (.20 | ) | | | (.03 | ) |

| | | | | | | | |

Net asset value, end of period | | $ | 11.41 | | | $ | 10.75 | |

| | | | | | | | |

Total return | | | | | | | | |

Total investment return based on net asset value (d) | | | 8.04% | | | | 7.81% | |

| | |

| RATIOS/SUPPLEMENTAL DATA | | | | | | | | |

Net assets, end of period (000’s omitted) | | | $980,537 | | | | $310,519 | |

Ratio to average net assets of: | | | | | | | | |

Expenses, net of waivers/reimbursements (c)(e) | | | 1.75% | | | | 1.75% | (f) |

Expenses, before waivers/reimbursements (e) | | | 1.79% | | | | 2.38% | (f) |

Net investment loss (c)(e) | | | (1.75 | )% | | | (1.75 | )% (f) |

Portfolio turnover rate | | | 0% | (g) | | | 0% | |

| (a) | | Commencement of operations. |

| (b) | | Based on average shares outstanding. |

| (c) | | Net of fees and expenses waived/reimbursed by the Investment Manager. |

| (d) | | Total investment return is calculated assuming a purchase of beneficial shares on the opening of the first day and a sale on the closing of the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation, to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return calculated for a period of less than one year is not annualized. |

| (e) | | The expense and net investment loss ratios do not include income earned or expenses incurred by the Fund through its Underlying Portfolios. |

| (f) | | Annualized, except for certain non-recurring fees. |

| (g) | | Amount is less than .50%. |

See Notes to Financial Statements.

Notes to Financial Statements

| NOTE A | Significant Accounting Policies |

AllianceBernstein Multi-Manager Alternative Fund (the “Fund”) is a statutory trust formed under the laws of the State of Delaware and registered under the Investment Company Act of 1940 as a non-diversified, closed-end management investment company. The Fund commenced operations on October 1, 2012. The Fund’s investment objective is to seek long-term capital appreciation. There can be no assurance that the Fund will achieve its investment objective, be able to structure its investments as anticipated, or that its returns will be positive over any period of time. The Fund is not intended as a complete investment program for investors. The Fund seeks to achieve its investment objective primarily by allocating its assets among investments in private investment vehicles (“Underlying Portfolios”), commonly referred to as hedge funds, that are managed by unaffiliated asset managers that employ a broad range of investment strategies. The financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates, and such differences could be material. The following is a summary of significant accounting policies followed by the Fund.

| 1. | | Valuation of Investments |

The Fund’s Board of Trustees (the “Board”) has approved pricing and valuation policies and procedures pursuant to which the Fund’s investments in Underlying Portfolios are valued at fair value (the “Valuation Procedures”). Among other matters, the Valuation Procedures set forth the Fund’s valuation policies and the mechanisms and processes to be employed on a monthly basis to implement such policies. In accordance with the Valuation Procedures, fair value of an Underlying Portfolio as of each valuation time ordinarily is the value determined as of such month-end for each Underlying Portfolio in accordance with the Underlying Portfolio’s valuation policies and reported at the time of the Fund’s valuation.

On a monthly basis, the Fund generally uses the net asset value (“NAV”), provided by the Underlying Portfolios, to determine the fair value of all Underlying Portfolios which (a) do not have readily determinable fair values and (b) either have the attributes of an investment company or prepare their financial statements consistent with measurement principles of an investment company. As a general matter, the fair value of the Fund’s interest in an Underlying Portfolio represents the amount that the Fund could reasonably expect to receive from an Underlying Portfolio if its interest were redeemed at the time of valuation. In the unlikely event that an Underlying Portfolio does not report a month-end value to the Fund on a timely basis, the Fund would determine the fair value of such Underlying Portfolio based on the most recent value reported by the Underlying Portfolio, and any other relevant information available at the time the Fund values its portfolio. In making a fair value determination, the Fund will consider all appropriate information reasonably available to it at the time and that Alliance Bernstein L.P. (the “Investment Manager”) believes to be reliable. The Fund may consider factors such as, among others: (i) the price at which recent subscriptions for or redemptions of the Underlying Portfolio’s interests were effected; (ii) information provided to the Fund by the manager of an Underlying Portfolio, or the failure to provide such information as the Underlying Portfolio manager agreed to provide in the Underlying Portfolio’s offering materials or other agreements with the Fund; (iii) relevant news and other sources; and (iv) market events. In addition, when an Underlying Portfolio imposes extraordinary restrictions on redemptions, or when there have been no recent subscriptions for Underlying Portfolio interests, the Fund may determine that it is appropriate to apply a discount to the NAV reported by the Underlying Portfolio. The use of different factors and estimation methodologies could have a significant effect on the estimated fair value and could be material to the financial statements.

In general, the market values of securities which are readily available and deemed reliable are determined as follows: securities listed on a national securities exchange (other than securities listed on the NASDAQ Stock Market, Inc. (“NASDAQ”)) or on a foreign securities exchange are valued at the last sale price at the close of the exchange or foreign securities exchange. If there has been no sale on such day, the securities are valued at the last traded price from the previous day. Securities listed on more than one exchange are valued by reference to the principal exchange on which the securities are traded; securities listed only on NASDAQ are valued in accordance with the NASDAQ Official Closing Price; listed or over the counter (“OTC”) market put or call options are valued at the mid level between the current bid and ask prices. If either a current bid or current ask price is unavailable, the Investment Manager will have discretion to determine the best valuation (e.g. last trade price in the case of listed options); open futures are valued using the closing settlement price or, in the absence of such a price, the most recent quoted bid price. If there are no quotations available for the day of valuation, the last available closing settlement price is used.

| | |

| 12 | | AllianceBernstein Multi-Manager Alternative Fund |

Securities for which market quotations are not readily available (including restricted securities) or are deemed unreliable are valued at fair value. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, analysis of the issuer’s financial statements or other available documents. In addition, the Fund may use fair value pricing for securities primarily traded in non-U.S. markets because most foreign markets close well before the Fund values its securities at 4:00 p.m., Eastern Time. The earlier close of the foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred between the close of the foreign markets and the time at which the Fund values its securities which may materially affect the value of securities trading in such markets. To account for this, the Fund may frequently value many of its foreign equity securities using fair value prices based on third party vendor modeling tools to the extent available.

The Investment Manager has established a Valuation Committee (the “Committee”) made up of representatives of portfolio management, fund accounting, compliance and risk management which operates under the Valuation Procedures and is responsible for overseeing the pricing and valuation of all securities held in the Fund. The Committee’s responsibilities include: 1) fair value determinations (and oversight of any third parties to whom any responsibility for fair value determinations is delegated), and 2) regular monitoring of the Valuation Procedures and modification or enhancement of the Valuation Procedures (or recommendation of the modification of the Valuation Procedures) as the Committee believes appropriate. Prior to investing in any Underlying Portfolio, and periodically thereafter, the Investment Manager will conduct a due diligence review of the valuation methodology utilized by the Underlying Portfolio. In addition, there are several processes outside of the pricing process that are used to monitor valuation issues including: 1) performance and performance attribution reports are monitored for anomalous impacts based upon benchmark performance, and 2) portfolio managers review all portfolios for performance and analytics.

U.S. GAAP establishes a framework for measuring fair value, and a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability. Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions that market participants would use in pricing the asset or liability based on the best information available in the circumstances. Each investment is assigned a level based upon the observability of the inputs which are significant to the overall valuation. The three-tier hierarchy of inputs is summarized below.

| | • | | Level 1—quoted prices in active markets for identical investments |

| | • | | Level 2—other significant observable inputs (including the Fund’s ability to redeem from an Underlying Portfolio within the near term of the reporting date at fair value) |

| | • | | Level 3—significant unobservable inputs (including those investments in Underlying Portfolios which have restrictions on redemptions due to lock-up periods or redemption restrictions such that the Fund cannot redeem within the near term of the reporting date) |

Valuations reflected in this report are as of the report date. As a result, changes in valuation due to market events and/or issuer related events after the report date and prior to issuance of the report are not reflected herein.

| | | | | | | | | | | | | | | | |

INVESTMENTS IN SECURITIES: | | LEVEL 1 | | | LEVEL 2 | | | LEVEL 3 | | | TOTAL | |

Assets: | | | | | | | | | | | | | | | | |

Underlying Portfolios: | | | | | | | | | | | | | | | | |

Long/Short Equity | | $ | — | | | $ | 131,084,371 | | | $ | 277,379,976 | | | $ | 408,464,347 | |

Event Driven | | | — | | | | 48,310,353 | | | | 246,270,331 | | | | 294,580,684 | |

Credit/Distressed | | | — | | | | 53,176,843 | | | | 134,140,299 | | | | 187,317,142 | |

Global Macro | | | — | | | | 46,788,335 | | | | — | | | | 46,788,335 | |

Emerging Markets | | | — | | | | — | | | | 44,649,252 | | | | 44,649,252 | |

Common Stocks | | | 431,301 | | | | — | | | | — | | | | 431,301 | |

Total Investments in Securities | | $ | 431,301 | | | $ | 279,359,902 | | | $ | 702,439,858 | | | $ | 982,231,061 | |

Notes to Financial Statements (continued)

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value.

| | | | | | | | | | | | |

| | | LONG/SHORT EQUITY | | | EVENT DRIVEN | | | CREDIT/DISTRESSED | |

Balance as of 3/31/13 | | $ | 88,043,362 | | | $ | 65,890,112 | | | $ | 40,795,432 | |

Realized gain (loss) | | | — | | | | — | | | | — | |

Change in unrealized appreciation/depreciation | | | 18,161,494 | | | | 17,380,219 | | | | 8,847,335 | |

Purchases | | | 182,000,000 | | | | 163,000,000 | | | | 94,500,000 | |

Sales | | | — | | | | — | | | | — | |

Transfers in to Level 3 | | | — | | | | — | | | | — | |

Transfers out of Level 3 | | | (10,824,880 | )^ | | | — | | | | (10,002,468 | )^^ |

| | | | | | | | | | | | |

Balance as of 3/31/14 | | $ | 277,379,976 | | | $ | 246,270,331 | | | $ | 134,140,299 | |

| | | | | | | | | | | | |

Net change in unrealized appreciation/depreciation from Investments held as of 3/31/14* | | $ | 18,161,494 | | | $ | 17,380,219 | | | $ | 8,847,335 | |

| | | EMERGING MARKETS | | | TOTAL | | | | |

Balance as of 3/31/13 | | $ | 26,058,029 | | | $ | 220,786,935 | | | | | |

Realized gain (loss) | | | — | | | | — | | | | | |

Change in unrealized appreciation/depreciation | | | 1,591,223 | | | | 45,980,271 | | | | | |

Purchases | | | 17,000,000 | | | | 456,500,000 | | | | | |

Sales | | | — | | | | — | | | | | |

Transfers in to Level 3 | | | — | | | | — | | | | | |

Transfers out of Level 3 | | | — | | | | (20,827,348 | ) | | | | |

| | | | | | | | | | | | |

Balance as of 3/31/14 | | $ | 44,649,252 | | | $ | 702,439,858 | | | | | |

| | | | | | | | | | | | |

Net change in unrealized appreciation/depreciation from Investments held as of 3/31/14* | | $ | 1,591,223 | | | $ | 45,980,271 | | | | | |

| | ^ | An amount of $10,824,880 was transferred out of Level 3 into Level 2 due to a result of the expiration of the lock-up period during the reporting period. |

| | ^^ | An amount of $10,002,468 was transferred out of Level 3 into Level 2 due to a result of the expiration of the lock-up period during the reporting period. |

| | * | The unrealized appreciation/depreciation is included in net change in unrealized appreciation/depreciation of investment transactions in the accompanying statement of operations. |

As of March 31, 2014, the Fund has committed to purchase the following Underlying Portfolios for effective date April 1, 2014.

| | | | |

Underlying Investment | | Amount Committed | |

Aravt Global Fund Ltd.* | | $ | 10,000,000 | |

Coatue Offshore Fund, Ltd.* | | | 2,000,000 | |

Criterion Horizons Offshore, Ltd. | | | 3,000,000 | |

Discovery Global Opportunity Fund, Ltd.* | | | 2,000,000 | |

Falcon Edge Global, Ltd. | | | 2,000,000 | |

JMB Capital Partners Offshore, Ltd. | | | 3,000,000 | |

Jana Nirvana Offshore Fund, Ltd.* | | | 2,000,000 | |

Luxor Capital Partners Offshore, Ltd.* | | | 2,000,000 | |

Nokota Capital Offshore Fund, Ltd. | | | 2,000,000 | |

Oaktree Value Opportunities (Cayman) Fund, Ltd. | | | 5,000,000 | |

Panning Overseas Fund, Ltd. | | | 3,000,000 | |

Roystone Capital Offshore Fund Ltd. | | | 5,000,000 | |

Senator Global Opportunity Offshore Fund, Ltd. | | | 8,000,000 | |

Spinnaker Global Emerging Markets Holdings, Ltd. | | | 2,000,000 | |

Wingspan Overseas Fund, Ltd.* | | | 3,000,000 | |

| | | | |

| | $ | 54,000,000 | |

| | | | |

| | * | Investments paid in advance amounted to $21,000,000. |

| | |

| 14 | | AllianceBernstein Multi-Manager Alternative Fund |

It is the Fund’s policy to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its investment company taxable income and net realized gains, if any, to shareholders. Therefore, no provisions for federal income or excise taxes are required. The Fund intends to continue to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986 as they apply to regulated investment companies. By so complying, the Fund will not be subject to federal and state income taxes to the extent that all of its income is distributed.

In accordance with U.S. GAAP requirements regarding accounting for uncertainties in income taxes, management has analyzed the Fund’s tax positions taken or expected to be taken on federal and state income tax returns for the all open tax years (all years since inception of the Fund) and has concluded that no provision for income tax is required in the Fund’s financial statements.

| 4. | | Investment Income and Investment Transactions |

Income and capital gain distributions, if any, are recorded on the ex-dividend date. Investment transactions are accounted for on the trade date or effective date. Investment gains and losses are determined on the identified cost basis.

Expenses included in the accompanying statements of operations do not include any expenses of the Underlying Portfolios.

| 6. | | Dividends and Distributions |

Dividends and distributions to shareholders, if any, are recorded on the ex-dividend date. Income dividends and capital gains distributions are determined in accordance with federal tax regulations and may differ from those determined in accordance with U.S. GAAP. To the extent these differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax basis treatment; temporary differences do not require such reclassification.

| 7. | | Organization and Offering Expenses |

Offering costs of $415,576 were deferred and amortized on a straight line basis over a one year period starting from October 1, 2012 (commencement of the Fund’s operations).

| NOTE B | Management Fee and Other Transactions with Affiliates |

Under the terms of the investment advisory agreement (the “Advisory Agreement”), the Fund pays the Investment Manager a management fee at an annual rate of 1.50% of an aggregate of the Fund’s net assets determined as of the last day of a calendar month and adjusted for subscriptions and repurchases accepted as of the first day of the subsequent month, (the “Management Fee”). The Management Fee is payable in arrears as of the last day of the subsequent month.

The Investment Manager has agreed to waive its fees and bear certain expenses through July 31, 2014 to the extent necessary to limit total operating expenses, excluding the Management Fee, extraordinary expenses, interest expenses, taxes, brokerage commissions and other transaction costs, and Underlying Portfolio fees and expense, on an annual basis to 0.25% of average monthly net assets (1.75% including Management Fee). For the year ended March 31, 2014, such reimbursement/waiver amounted to $271,569. Under an Expense Limitation Agreement between the Investment Manager and the Fund, fees waived and expenses borne by the Investment Manager are subject to repayment by the Fund until September 30, 2015. No repayment will be made that would cause the Fund’s total annualized operating expenses to exceed the net fee percentage set forth above or would exceed the amount of offering expenses as recorded by the Fund on or before September 30, 2013. At March 31, 2014, the amount eligible for repayment by the Fund, subject to the terms of the Expense Limitation Agreement, is $415,576.

Under a separate Administrative Agreement, the Fund may use the Investment Manager and its personnel to provide certain administrative services to the Fund and, in such event, the services and payments will be subject to approval by the Fund’s Board. For the year ended March 31, 2014, such fees amounted to $268,002.

Notes to Financial Statements (continued)

The Fund may engage one or more distributors to solicit investments in the Fund. Sanford C. Bernstein & Company LLC (“Bernstein”), an affiliate of the Investment Manager, has been selected as initial distributor of the Fund under a Distribution Services Agreement. The Distribution Services Agreement does not call for any payments to be made to Bernstein by the Fund.

The Fund compensates AllianceBernstein Investor Services, Inc. (“ABIS”), a wholly-owned subsidiary of the Investment Manager, under a Transfer Agency Agreement for providing personnel and facilities to perform transfer agency services for the Fund. Such compensation paid to ABIS amounted to $137,810 for the year ended March 31, 2014.

| NOTE C | Investment Transactions |

Purchases and sales of investments, aggregated $605,355,296 and $2,184,604, respectively, for the year ended March 31, 2014.

The cost of investments for federal income tax purposes, gross unrealized appreciation and unrealized depreciation are as follows:

| | | | |

Cost | | $ | 935,890,746 | |

| | | | |

Gross unrealized appreciation | | $ | 88,949,479 | |

Gross unrealized depreciation | | | (42,609,164 | ) |

| | | | |

Net unrealized appreciation | | $ | 46,340,315 | |

| | | | |

| NOTE D | Shares of Beneficial Interest |

During the year ended March 31, 2014 and the period ended March 31, 2013 the Fund issued 1,172,608 and 37,739 shares, respectively, in connection with the Fund’s dividend reinvestment plan.

Subscriptions and Repurchases

Generally, initial and additional subscriptions for shares may be accepted as of the first day of each month. The Fund reserves the right to reject any subscription for shares. The Fund intends to repurchase shares from shareholders in accordance with written tenders by shareholders at those times, in those amounts, and on such terms and conditions as the Board of Trustees may determine in its sole discretion. When a repurchase offer occurs, a shareholder will generally be required to provide notice of their tender of shares for repurchase to the Fund more than three months in advance of the date that the shares will be valued for repurchase (the “Valuation Date”). Valuation Dates are generally expected to be the last business days of March, June, September or December, and payment for tendered shares will generally be made by the Fund approximately 45 days following the Valuation Date.

Transactions in shares of beneficial interest were as follows for the year ended March 31, 2014 and the period ended March 31, 2013:

| | | | | | | | | | | | | | | | | | |

| | | |

| | | SHARES | | | | | AMOUNT | |

| | | | | | | | | | | | | | | | | | |

| | | YEAR ENDED

MARCH 31, 2014 | | | OCTOBER 1, 2012(a)

TO

MARCH 31, 2013 | | | | | YEAR ENDED

MARCH 31, 2014 | | | OCTOBER 1, 2012(a)

TO

MARCH 31, 2013 | |

Shares sold | | | 57,803,640 | | | | 28,910,370 | | | | | $ | 638,396,570 | | | $ | 295,379,869 | |

Shares issued in reinvestment of dividends and distributions | | | 1,172,608 | | | | 37,739 | | | | | | 13,297,371 | | | | 385,319 | |

Shares redeemed | | | (1,912,127 | ) | | | (78,202 | ) | | | | | (21,489,385 | ) | | | (840,676 | ) |

| | | | | | | | | | | | | | | | | | |

Net increase | | | 57,064,121 | | | | 28,869,907 | | | | | $ | 630,204,556 | | | $ | 294,924,512 | |

| | | | | | | | | | | | | | | | | | |

| | (a) | Commencement of operations. |

| | |

| 16 | | AllianceBernstein Multi-Manager Alternative Fund |

| NOTE E | Risks Involved in Investing in the Fund |

Limitations on the Fund’s ability to withdraw its assets from Underlying Portfolios may limit the Fund’s ability to repurchase its shares. For example, many Underlying Portfolios impose lock-up periods prior to allowing withdrawals, which can be two years or longer. After expiration of the lock-up period, withdrawals typically are permitted only on a limited basis, such as monthly, quarterly, semi-annually or annually. Many Underlying Portfolios may also indefinitely suspend redemptions or establish restrictions on the ability to fully receive proceeds from redemptions through the application of a redemption restriction or “gate”. In instances where the primary source of funds to repurchase shares will be withdrawals from Underlying Portfolios, the application of these lock-ups and withdrawal limitations may significantly limit the Fund’s ability to repurchase its shares. Although the Investment Manager will seek to select Underlying Portfolios that offer the opportunity to have their shares or units redeemed within a reasonable timeframe, there can be no assurance that the liquidity of the investments of such Underlying Portfolios will always be sufficient to meet redemption requests as, and when, made.

The Fund invests primarily in Underlying Portfolios that are not registered under the 1940 Act and invest in and actively trade securities and other financial instruments using different strategies and investment techniques that may involve significant risks. Such risks include those related to the volatility of the equity, credit, and currency markets, the use of leverage associated with certain investment strategies, derivative contracts and in connection with short positions, the potential illiquidity of certain instruments and counterparty and broker arrangements.

Some of the Underlying Portfolios in which the Fund invests may invest all or a portion of their assets in securities that are illiquid or are subject to an anticipated event. These Underlying Portfolios may create “side pockets” in which to hold these securities. Side pockets are series or classes of shares which are not redeemable by the investors but which are automatically redeemed or converted back into the Underlying Portfolio’s regular series or classes of shares upon the realization of those securities or the happening of some other liquidity event with respect to those securities.

These “side pockets” can often be held for long periods before they are realized, and may therefore be much less liquid than the general liquidity offered on the Underlying Portfolio’s regular series or classes of shares. Should the Fund seek to liquidate its investment in an Underlying Portfolio that maintains investments in a side pocket arrangement or that holds a substantial portion of its assets in illiquid securities, the Fund might not be able to fully liquidate its investments without delay, which could be considerable. In such cases, during the period until the Fund is permitted to fully liquidate the investment in the Underlying Portfolio, the value of the investment could fluctuate.

The Underlying Portfolios may utilize leverage in pursuit of achieving a potentially greater investment return. The use of leverage exposes an Underlying Portfolio to additional risk including (i) greater losses from investments than would otherwise have been the case had the Underlying Portfolio not used leverage to make the investments; (ii) margin calls or interim margin requirements may force premature liquidations of investment positions; and (iii) losses on investments where the investment fails to earn a return that equals or exceeds the Underlying Portfolio’s cost of leverage related to such investment. In the event of a sudden, precipitous drop in the value of an Underlying Portfolio’s assets, the Underlying Portfolio might not be able to liquidate assets quickly enough to repay its borrowings, further magnifying the losses incurred by the Underlying Portfolio.

The Underlying Portfolios may invest in securities of foreign companies that involve special risks and considerations not typically associated with investments in the United States, due to concentrated investments in a limited number of countries or regions, which may vary throughout the year depending on the Underlying Portfolio. Such concentrations may subject the Underlying Portfolios to additional risks resulting from political or economic conditions in such countries or regions, and the possible imposition of adverse governmental laws or currency exchange restrictions could cause the securities and their markets to be less liquid and their prices to be more volatile than those of comparable U.S. securities.

The Underlying Portfolios may invest a higher percentage of their assets in specific sectors of the market in order to achieve a potentially greater investment return. As a result, the Underlying Portfolios may be more susceptible to economic, political and regulatory developments in a particular sector of the market, positive or negative, and may experience increased volatility of the Underlying Portfolio’s net asset value.

The Fund invests in a limited number of Underlying Portfolios. Such concentration may result in additional risk. Various risks are also associated with an investment in the Fund, including risks relating to compensation arrangements and risks relating to limited liquidity of the Interests.

Notes to Financial Statements (continued)

The Fund is subject to credit risk arising from its transactions with its custodian, State Street Bank and Trust, related to holding the Fund’s cash. This credit risk arises to the extent that the custodian may be unable to fulfill its obligation to return the Fund’s cash held in its custody.

In the normal course of business, the Fund enters into contracts that contain a variety of representations which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

The tax character of distributions paid during the fiscal year ended March 31, 2014 and the fiscal period ended March 31, 2013 were as follows:

| | | | | | | | |

| | | 2014 | | | 2013 | |

Distributions paid from: | | | | | | | | |

Ordinary income | | $ | 12,368,064 | | | $ | 412,492 | |

Long-Term Capital Gain | | | 2,314,956 | | | | 0 | |

| | | | | | | | |

Total taxable distributions paid | | $ | 14,683,020 | | | $ | 412,492 | |

| | | | | | | | |

As of March 31, 2014, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| | | | |

Undistributed ordinary income | | $ | 2,291,091 | |

Undistributed capital gain | | | 6,676,756 | |

Unrealized appreciation/(depreciation) | | | 46,340,315 | (a) |

| | | | |

Total accumulated earnings/(deficit) | | $ | 55,308,162 | |

| | | | |

| | (a) | The difference between book-basis and tax-basis unrealized appreciation/(depreciation) is attributable primarily to the tax treatment of Passive Foreign Investment Companies (PFICs) and partnerships. |

For tax purposes, net capital losses may be carried over to offset future capital gains, if any. Funds are permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an indefinite period and such losses will retain their character as either short-term or long-term capital losses. As of March 31, 2014, the Fund did not have any capital loss carryforwards.

During the current fiscal period there were no permanent differences that resulted in adjustments to distributions in excess of net investment income or additional-paid in capital.

The Fund is a party to a $75 million revolving credit facility (the “Facility”) intended to provide short term financing, if necessary, subject to certain restrictions in connection with, among other matters, abnormal redemption activity. Commitment fees related to the Facility are paid by Fund and are included in miscellaneous expenses in the statement of operations. The Fund entered into the Facility on October 3, 2013. During the period October 3, 2013 to March 31, 2014, the Fund did not utilize the Facility.

Management has evaluated subsequent events for possible recognition or disclosure in the financial statements through the date the financial statements are issued. Management has determined that there are no material events that would require disclosure in the Fund’s financial statements through this date.

| | |

| 18 | | AllianceBernstein Multi-Manager Alternative Fund |

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

AllianceBernstein Multi-Manager Alternative Fund

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations, of changes in net assets and of cash flows and the financial highlights present fairly, in all material respects, the financial position of AllianceBernstein Multi-Manager Alternative Fund (the “Fund”) at March 31, 2014, the results of its operations and its cash flows for the year then ended, and the changes in its net assets and the financial highlights for the year then ended and for the period October 1, 2012 (commencement of operations) through March 31, 2013, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of underlying portfolio funds and securities at March 31, 2014 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

New York, New York

May 29, 2014

Tax Information (Unaudited)

For Federal income tax purposes, the following information is furnished with respect to the earnings of the Fund for the fiscal year ended March 31, 2014. For such taxable year, the Fund designates $2,314,956 or the maximum amount required as capital gain dividends.

Shareholders should not use the above information to prepare their income tax returns. The information necessary to complete your income tax returns will be included with your Form 1099-DIV which will be sent to you separately in January 2015.

| | |

| 20 | | AllianceBernstein Multi-Manager Alternative Fund |

AllianceBernstein Multi-Manager Alternative Fund

BOARDOF TRUSTEES

Carter “Terry” F. Wolfe(1)

Chairman

Christopher J. Bricker

President and Chief Executive Officer

Lawrence D. Haber(1)

Jeanette Loeb(1)

OFFICERS

Philip L. Kirstein

Senior Vice President and Independent Compliance Officer

Marc H. Gamsin(2)

Vice President

Greg Outcalt(2)

Vice President

Michael H. Conn

Vice President

Emilie D. Wrapp

Secretary

Joseph J. Mantineo

Treasurer and Chief Financial Officer

Stephen M. Woetzel

Controller

Vincent S. Noto

Chief Compliance Officer

CUSTODIAN

State Street Bank and Trust Company

One Lincoln Street

Boston, MA 02111

DISTRIBUTOR

Sanford C. Bernstein & Company, LLC

1345 Avenue of the Americas

New York, NY 10105

TRANSFER AGENT

AllianceBernstein Investor Services, Inc.

P.O. Box 786003

San Antonio, TX 78278-6003

Toll-Free (800) 221-5672

LEGAL COUNSEL

Willkie Farr & Gallagher LLP

787 Seventh Avenue

New York, NY 10019

INDEPENDENT REGISTEREDPUBLIC ACCOUNTING FIRM

PricewaterhouseCoopers LLP

300 Madison Avenue

New York, NY 10017

(1) Member of the Audit Committee and the Governance and Nominating Committee.

(2) The day-to-day management of, and investment decisions for, the Fund’s portfolio are made by the Investment Manager’s Alternative Investment Management Group. Messrs. Gamsin and Outcalt are the investment professionals with the most significant responsibility for the day-to-day management of the Fund’s portfolio.

Management of the Fund

| | | | | | | | |

BOARDOF TRUSTEES INFORMATION |

The business and affairs of the Fund are managed under the direction of the Board of Trustees. Certain information concerning the Fund’s Trustees is set forth below. |

Name, Address,* Age,

(Year Elected**) | | Principal Occupation(s)

During Past Five Years | | Portfolios

Overseen

By Trustee | | | Other Public Company

Trusteeships/Directorships

Held By Trustee

During the Past Five Years |

INTERESTED TRUSTEE | | | | | | |

Christopher J. Bricker*** 45 (2012) | | Senior Vice President of the Investment Manager since prior to 2009; Senior Managing Director and Head of Product Development since December 2009. | | | 1 | | | None |

INDEPENDENT TRUSTEES | | | | | | |

Lawrence D. Haber# 62 (2012) | | Formerly, Chief Operating Officer and Member of the Management Committee at Credit Suisse Asset Management from 2004 to 2008. | | | 1 | | | None |

| | | |

Jeanette Loeb# 61 (2012) | | Formerly, Chairman and Chief Executive Officer of PetCareRx (e-commerce pet pharmacy) from 2002 to 2011. | | | 1 | | | Apollo Investment Corp. since August 2011 |

| | | |

Carter “Terry” F. Wolfe# 75 (2012) | | Formerly, Managing Director of Paloma Partners (hedge fund) from 2000 to 2011. He served as Vice President and Chief Investment Officer of Howard Hughes Medical Institute from 1994 to 1999. | | | 1 | | | None |

* The address for each of the Fund’s Trustees is c/o AllianceBernstein L.P., Attention: Emilie D. Wrapp, 1345 Avenue of the Americas, New York, NY 10105.

** There is no stated term of office for the Fund’s Trustees. Each Trustee serves until his or her successor is elected and qualifies or until his or her death, resignation, or removal as provided in the Declaration of Trust, Bylaws or by statute.

*** Mr. Bricker is an “interested person”, as defined in the Investment Company Act, due to his position as a Senior Vice President of the Investment Manager.

# Member of the Audit Committee and the Governance and Nominating Committee.

| | |

| 22 | | AllianceBernstein Multi-Manager Alternative Fund |

Officers of the Fund

Certain information concerning the Fund’s Officers is listed below.

| | | | |

| Name, Address,* and Age | | Position(s)

Held With Fund | | Principal Occupation

During Past Five Years |

Christopher J. Bricker, 45 | | President and Chief Executive Officer | | See biography above. |

| | |

Philip L. Kirstein, 69 | | Senior Vice President and Independent Compliance Officer | | Senior Vice President and Independent Compliance Officer of the AB Advised Funds, with which he has been associated since prior to 2009. |

| | |

Marc H. Gamsin, 58 | | Vice President | | Senior Vice President of the Investment Manager** and Head of its Alternative Investment Management Group since October 2010. Prior thereto, he was the President of SunAmerica Alternative Investments beginning prior to 2009. |

| | |

Greg Outcalt, 52 | | Vice President | | Senior Vice President of the Investment Manager ** and Deputy Chief Investment Officer of its Alternative Investment Management Group, with which he has been associated since October 2010. Prior thereto, he was Executive Vice President of SunAmerica Alternative Investments beginning prior to 2009. |

| | |

Michael H. Conn, 35*** | | Vice President | | Vice President of the Investment Manager** and Chief Operating Officer of its Alternative Investment Management Group, with which he has been associated since December 2013. Prior thereto, he was associated with The TCW Group, Inc., as Managing Director and Head of Corporate Strategy and Development since prior to 2009. |

| | |

Emilie D. Wrapp, 58 | | Secretary | | Senior Vice President, Assistant General Counsel and Assistant Secretary of AllianceBernstein Investments, Inc. (“ABI”),** with which she has been associated since prior to 2009. |

| | |

Joseph J. Mantineo, 55 | | Treasurer and Chief Financial Officer | | Senior Vice President of AllianceBernstein Investor Services, Inc. (“ABIS”),** with which he has been associated since prior to 2009. |

| | |

Stephen M. Woetzel, 42 | | Controller | | Vice President of ABIS,** with which he has been associated since prior to 2009. |

| | |

Vincent S. Noto, 49 | | Chief Compliance Officer | | Vice President and Mutual Fund Chief Compliance Officer of the Investment Manager** since 2014. Prior thereto, he was Vice President and Director of Mutual Fund Compliance of the Investment Manager** since 2009. |

* The address for each of the Fund’s Officers is 1345 Avenue of the Americas, New York, NY 10105.

** The Investment Manager, ABI and ABIS are affiliates of the Fund.

*** Became Vice President on April 29, 2014.

The Fund’s prospectus has additional information about the Fund’s Trustees and Officers. An additional copy of the Fund’s prospectus may be obtained (without charge) by visiting our website at www.bernstein.com and clicking on “ Investments”, then “Stocks” or “Bonds”, then “Prospectuses, SAIs and Shareholder Reports” or by calling your Financial Advisor or by calling Bernstein’s mutual fund shareholder helpline at 212.756.4097.

SANFORD C. BERNSTEIN

Distributor

ALLIANCEBERNSTEIN MULTI-MANAGER ALTERNATIVE FUND

1345 AVENUEOFTHE AMERICAS, NEW YORK, NY 10105

800.221.5672

MMAF–0151–0314

ITEM 2. CODE OF ETHICS.

(a) The registrant has adopted a code of ethics that applies to its principal executive officer, principal financial officer and principal accounting officer. A copy of the registrant’s code of ethics is filed herewith as Exhibit 12(a)(1).

(b) During the period covered by this report, no material amendments were made to the provisions of the code of ethics adopted in 2(a) above.

(c) During the period covered by this report, no implicit or explicit waivers to the provisions of the code of ethics adopted in 2(a) above were granted.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

The registrant’s Board of Directors has determined that independent director Lawrence D. Haber qualifies as an audit committee financial expert.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

(a) - (c) The following table sets forth the aggregate fees billed by the independent registered public accounting firm PricewaterhouseCoopers LLP, for the Fund’s current fiscal year for professional services rendered for: (i) the audit of the Fund’s annual financial statements included in the Fund’s annual report to stockholders; (ii) assurance and related services that are reasonably related to the performance of the audit of the Fund’s financial statements and are not reported under (i), which include advice and education related to accounting and auditing issues and quarterly press release review (for those Funds that issue quarterly press releases), and preferred stock maintenance testing (for those Funds that issue preferred stock); and (iii) tax compliance, tax advice and tax return preparation.

| | | | | | | | | | |

| | | Audit Fees | | Audit-Related

Fees | | | Tax Fees | |

2013 | | $57,500 | | $ | — | | | $ | 25,000 | |

2014 | | $52,500 | | $ | — | | | $ | 25,000 | |

(d) Not applicable.

(e) (1) Beginning with audit and non-audit service contracts entered into on or after May 6, 2003, the Fund’s Audit Committee policies and procedures require the pre-approval of all audit and non-audit services provided to the Fund by the Fund’s independent registered public accounting firm. The Fund’s Audit Committee policies and procedures also require pre-approval of all audit and non-audit services provided to the Adviser and Service Affiliates to the extent that these services are directly related to the operations or financial reporting of the Fund.

(e) (2) All of the amounts for Audit Fees, Audit-Related Fees and Tax Fees in the table under Item 4 (a) – (c) are for services pre-approved by the Fund’s Audit Committee.

(f) Not applicable.

(g) The following table sets forth the aggregate non-audit services provided to the Fund, the Fund’s Adviser and entities that control, are controlled by or under common control with the Adviser that provide ongoing services to the Fund:

| | | | | | |

| | | All Fees for Non-Audit Services Provided to the Portfolio, the Adviser and Service Affiliates | | Total Amount of

Foregoing Column Pre-

approved by the Audit

Committee

(Portion Comprised of

Audit Related Fees)

(Portion Comprised of

Tax Fees) | |

2013 | | $243,604 | | $ | 25,000 | |

| | | | $ | — | |

| | | | $ | (25,000 | ) |

2014 | | $5,743,054 | | $ | 25,000 | |

| | | | $ | — | |

| | | | $ | (25,000 | ) |

(h) The Audit Committee of the Fund has considered whether the provision of any non-audit services not pre-approved by the Audit Committee provided by the Fund’s independent registered public accounting firm to the Adviser and Service Affiliates is compatible with maintaining the auditor’s independence.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

The registrant has a separately-designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934. The audit committee members are as follows:

|

Lawrence D. Haber Jeanette Loeb Carter Wolfe |

ITEM 6. SCHEDULE OF INVESTMENTS.

Please see Schedule of Investments contained in the Report to Shareholders included under Item 1 of this Form N-CSR.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

Statement of Policies and Procedures for

Proxy Voting

As a registered investment adviser, AllianceBernstein L.P. (“AllianceBernstein”, “we” or “us”) has a fiduciary duty to act solely in the best interests of our clients. We recognize that this duty requires us to vote client securities in a timely manner and make voting decisions that are intended to maximize long-term shareholder value. Generally, our clients’ objective is to maximize the financial return of their portfolios within appropriate risk parameters. We have long recognized that environmental, social and governance (“ESG”) issues can impact the performance of investment portfolios. Accordingly, we have sought to integrate ESG factors into our investment process to the extent that the integration of such factors is consistent with our fiduciary duty to help our clients achieve their investment objectives and protect their economic interests. For additional information regarding our ESG policies and practices, please refer to our firm’s Statement of Policy Regarding Responsible Investment.

We consider ourselves shareholder advocates and take this responsibility very seriously. Consistent with our commitments, we will disclose our clients’ voting records only to them and as required by mutual fund vote disclosure regulations. In addition, our Proxy Committee may, after careful consideration, choose to respond to surveys so long as doing so does not compromise confidential voting.

This statement is intended to comply with Rule 206(4)-6 of the Investment Advisers Act of 1940. It sets forth our policies and procedures for voting proxies for our discretionary investment advisory clients, including investment companies registered under the Investment Company Act of 1940. This statement applies to AllianceBernstein’s investment groups investing on behalf of clients in both U.S. and non-U.S. securities.