UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-22671

AB MULTI-MANAGER ALTERNATIVE FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800)221-5672

Date of fiscal year end: March 31, 2020

Date of reporting period: September 30, 2019

ITEM 1. REPORTS TO STOCKHOLDERS.

SEP 09.30.19

SEMI-ANNUAL REPORT

AB MULTI-MANAGER ALTERNATIVE FUND

Beginning January 1, 2021, as permitted by new regulations adopted by the Securities and Exchange Commission, the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website address to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically at any time by contacting your Bernstein financial advisor or by calling the Fund at (212) 486 5800.

You may elect to receive all future reports in paper form free of charge. You can contact your Bernstein financial advisor to request that you continue to receive paper copies of your shareholder reports or you can call the Fund at (212) 486 5800. Your election to receive reports in paper form will apply to all funds held in your Bernstein account.

| | |

| |

| Investment Products Offered | | • Are Not FDIC Insured• May Lose Value• Are Not Bank Guaranteed |

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent12-month period ended June 30, without charge. Simply visit AB’s website at www.abfunds.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227 4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year as an exhibit to its reports onForm N-PORT. The Fund’sForm N-PORT reports are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-PORT may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC 0330.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

SEMI-ANNUAL REPORT

November 19, 2019

This report provides certain performance data for AB Multi-Manager Alternative Fund (the “Fund”) for the semi-annual reporting period ended September 30, 2019.

The Fund’s investment objective is to seek long-term capital appreciation.

RETURNS AS OF SEPTEMBER 30, 2019(unaudited)

| | | | | | | | |

| | |

| | | 6 Months | | | 12 Months | |

| | |

| AB MULTI-MANAGER ALTERNATIVE FUND | | | 0.80% | | | | 0.53% | |

| | |

| Benchmark: HFRI FOF Composite Index | | | 0.40% | | | | -0.18% | |

| | |

| MSCI World Index (net) | | | 4.56% | | | | 1.83% | |

| | |

| Bloomberg Barclays US Aggregate Bond Index | | | 5.42% | | | | 10.30% | |

INVESTMENT RESULTS

The table above provides performance data for the Fund and its benchmark, the HFRI Fund of Funds (“HFRI FOF”) Composite Index, for thesix- and12-month periods ended September 30, 2019. The table also includes the performance of the Morgan Stanley Capital International (“MSCI”) World Index (net) and the Bloomberg Barclays US Aggregate Bond Index.

During both periods, the Fund outperformed its benchmark, the HFRI FOF Composite Index, but underperformed the MSCI World Index (net) and the Bloomberg Barclays US Aggregate Index.

During thesix-month period, Global Macro, Event Driven, Multi-Strategy and Long/Short Equity Underlying Portfolios contributed to absolute performance, while Credit/Distressed detracted. Global Macro benefited from positive macro trends in interest rates and precious metals, relative value positioning across interest-rate curves and cross-country rates, as well as tactical positioning across developed-market equity indices. Event Driven and Long/Short Equity benefited from a positive equity market environment, and in certain cases outperformed the equity index, while only taking a fraction of the net market exposure. Outperformance was primarily driven by long positions, while short positions were mixed during the period. As to Credit/Distressed, market events weighed on sentiment during the most recent quarter.

For the12-month period, Long/Short Equity, Event Driven, Global Macro, and Multi-Strategy Underlying Portfolios contributed to absolute performance while Credit/Distressed detracted. Long/Short Equity and Event Driven benefited from a broadly supportive backdrop for both equities and

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 1 |

corporate fixed-income securities. Repositioning was also a benefit following the volatile fourth quarter of 2018, as Underlying Portfolios rotated exposure into oversold sectors and securities that generated outsized gains, as the market backdrop improved over the subsequent quarters. Global Macro benefited from positive macro trends, most notably lower interest rates globally and a rally in precious metals. Credit/Distressed was the sole detractor during the12-month period, as gains in structured credits were more than offset by declining sentiment in select stressed and distressed positions.

For both periods, the Fund utilized total return swaps for hedging and investment purposes, which detracted from absolute performance. The Fund also used currency forwards for hedging purposes, which had no material impact on absolute performance.

As a result of changes to the Fund’s investment policies that were effective July 31, 2018, including changes to allow for greater direct investment in securities and other financial instruments (in addition to investment in Underlying Portfolios), the portfolio composition evolved over time, and increasingly the Fund’s performance is a reflection of those changes.

MARKET REVIEW AND INVESTMENT STRATEGY

US and European stocks gained during thesix-month period ended September 30, 2019, while Asian and emerging-market stocks declined. In fixed income, developed-market treasuries rallied and outpaced the positive returns of global high-yield and investment-grade securities. The pursuit of yield combined with the mixed global economic outlook led to global bond markets outperforming their respective equity markets, but only by a small margin. As a result, more than 25% of the global government bond market traded at negative yields. While generally supportive, equity markets had more persistent volatility during this period. Further, equity volatility made its way into the microstructure of the markets with historically significant rotations in market leadership in September. These rotations led to negative alpha contributions from stock selection and mixed results from equity-focused hedge funds. However, this feature served as a tailwind for the Fund’s non-equity strategies (particularly relative value and global macro), which represented more than half of the portfolio allocation.

During the12-month period, the volatility trends were even more pronounced, starting with steep declines from the fourth quarter of 2018 that even the strong rally between January through September was barely able to overcome. Comparatively, fixed income was steadily bid higher, leading to double-digit positive returns during the period. But while challenging for managers to navigate at times, especially for more directional funds, the volatility also led to increased dispersion within the equity market and created opportunities to trade both long and short, which benefited the Fund’s lower net market exposure and market neutral strategies. These

| | |

| |

| 2 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

types of strategies were increased throughout the period and produced gains that more than offset the impact from the directional component.

INVESTMENT POLICIES

There can be no assurance that the Fund will achieve its investment objective, be able to structure its investments as anticipated, or that its returns will be positive over any period of time. The Fund is not intended as a complete investment program for investors.

The Fund seeks to achieve its investment objective primarily by allocating its assets among investments in a diversified portfolio of private investment vehicles commonly referred to as hedge funds (“Underlying Portfolios”). The Fund will invest primarily in Underlying Portfolios pursuing the following strategies: Long/Short Equity, Event Driven, Credit/Distressed, Emerging Markets, Global Macro and Multi-Strategy. For more information on these strategies, please see “Consolidated Portfolio of Investments” on pages 8–21. As a secondary strategy, the Fund will generally also make direct investments in securities and other financial instruments. For more information regarding the Fund’s risks, please see “Disclosures and Risks” on pages 4–6 and “Note E—Risks Involved in Investing in the Fund” of the Notes to Consolidated Financial Statements on pages 40–43.

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 3 |

DISCLOSURES AND RISKS

Benchmark Disclosure

All indices are unmanaged and do not reflect fees and expenses associated with the active management of a mutual fund portfolio.The HFRI FOF Composite Index is an equal-weighted performance index that includes over 650 constituent funds of hedge funds that report their monthlynet-of-fee returns to Hedge Fund Research, have at least $50 million under management and have been actively trading for at least 12 months. The MSCI World Index (net, free float-adjusted, market capitalization weighted) represents the equity market performance of developed markets. The Bloomberg Barclays US Aggregate Index represents the performance of securities within the US investment-grade fixed-rate bond market, with index components for government and corporate securities, mortgage pass-through securities, asset-backed securities and commercial mortgage-backed securities. MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI. Net returns include the reinvestment of dividends after deduction ofnon-US withholding tax. An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word about Risk

An investment in the Fund’s shares involves a high degree of risk and should not constitute a complete investment program. Before making an investment decision, you should carefully consider the following risk factors, together with the other information contained in the prospectus. At any point in time, an investment in the Fund’s shares may be worth less than the original amount invested, even after taking into account the distributions paid, if any, and the ability of shareholders to reinvest distributions. If any of the risks discussed below occurs, the Fund’s results of operations could be materially and adversely affected. If this were to happen, the price of Fund shares could decline significantly and you could lose all or a part of your investment.

Investment in this Fund is highly speculative and involves substantial risk, including loss of principal, and therefore may not be suitable for all investors.

General Risk Factors:Underlying Portfolios and the Fund’s direct investments may exhibit high volatility, and investors may lose all or substantially all of their investment. Investments by Underlying Portfolios and the Fund in illiquid assets and foreign markets and the use of short sales, options, leverage, futures, swaps and other derivative instruments may

| | |

| |

| 4 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

DISCLOSURES AND RISKS(continued)

create special risks and substantially increase the impact and likelihood of adverse price movements. Interests in Underlying Portfolios are subject to limitations on transferability and are illiquid, and no secondary market for interests typically exists or is likely to develop. Underlying Portfolios are typically not registered with securities regulators and are therefore generally subject to little or no regulatory oversight. Performance compensation payable to an Underlying Portfolio investment advisor may create an incentive to make riskier or more speculative investments. Underlying Portfolios typically charge higher fees than many other types of investments, which can offset trading profits, if any. There can be no assurance that any Underlying Portfolio will achieve its investment objectives.

Tax Risks:The Fund intends to be treated as a regulated investment company (“RIC”) under the Internal Revenue Code. However, in order to qualify as a RIC and also to avoid having to pay an “excise tax,” the Fund will be subject to certain limitations on its investments and operations, including a requirement that a specified proportion of its income come from qualifying sources, an asset diversification requirement and minimum distribution requirements. Satisfaction of the various requirements requires significant support and information from the Underlying Portfolios, and such support and information may not be available, sufficient, verifiable, or provided on a timely basis.

Limited Liquidity: The Fund’s shares are not listed on any securities exchange or traded in any other market, and are subject to substantial restrictions on transfer. Although the Fund has offered to repurchase shares on a quarterly basis, such periodic repurchase offers are at the sole discretion of the Fund’s Board of Trustees, and there is no assurance that these repurchase offers will continue. It will normally be four to six months between the time an investor tenders shares for repurchase (i.e., requests that the Fund repurchase shares as part of a repurchase offer) and the investor’s receipt of any cash proceeds associated with the repurchase.

Fund of Funds Considerations: The Fund will have no control rights over and limited transparency into the investment programs of the Underlying Portfolios in which it invests. In valuing the Fund’s holdings, the Investment Manager will generally rely on financial information provided by Underlying Portfolios, which may be unaudited, estimated and/or may not involve third parties. The Fund’s investment opportunities may be limited as a result of withdrawal terms or anticipated liquidity needs (e.g., withdrawal restrictions imposed by underlying hedge funds may delay, preclude or involve expense in connection with portfolio adjustments by the Investment Manager).

These risks are fully discussed in the Fund’s prospectus. As with all investments, you may lose money by investing in the Fund.

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 5 |

DISCLOSURES AND RISKS(continued)

An Important Note About Historical Performance

The performance shown in this report represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes.

| | |

| |

| 6 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

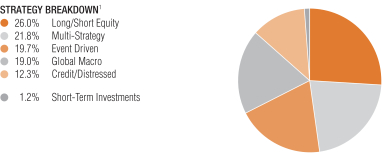

PORTFOLIO SUMMARY

September 30, 2019(unaudited)

Net Assets ($mil): $982.1

| 1 | All data are as of September 30, 2019. The Fund’s portfolio strategy breakdown is based on the Investment Manager’s internal classification and is expressed as a percentage of total investment exposure, including exposure from derivatives (see “Consolidated Portfolio of Investments” section of the report for additional details). |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 7 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS

September 30, 2019 (unaudited)

| | | | | | | | | | | | | | |

Underlying

Portfolios | | Shares | | | Fair Value ($) | | | % Net Assets | | | Liquidity* |

|

Long/Short Equity | | | | | | | | | | | | | | |

Coatue Offshore Fund, Ltd. | | | 144,099 | | | $ | 34,990,943 | | | | 3.6 | % | | Quarterly |

Darsana Overseas Fund Ltd. | | | 16,260 | | | | 26,690,416 | | | | 2.7 | | | Quarterly |

Janchor PartnersPan-Asian Fund | | | 264,641 | | | | 33,268,294 | | | | 3.4 | | | Triennially |

Luminus Energy Partners QP, LP | | | 9,708 | | | | 34,293,920 | | | | 3.5 | | | Quarterly |

Nokota Capital Offshore Fund, Ltd. | | | 2,589 | | | | 3,383,995 | | | | 0.3 | | | Quarterly |

Nokota LC, LLC | | | 1,249 | | | | 1,094,282 | | | | 0.1 | | | At Fund’s Discretion |

PFM Healthcare Offshore Fund, Ltd. | | | 30,698 | | | | 27,452,136 | | | | 2.8 | | | Quarterly |

Schonfeld Fundamental Equity Offshore Fund Ltd. | | | 30,000 | | | | 32,284,981 | | | | 3.3 | | | Quarterly |

The Children’s Investment Fund | | | 161,000 | | | | 24,890,600 | | | | 2.5 | | | Triennially |

Think Investments Offshore Ltd. | | | 22,314 | | | | 37,162,982 | | | | 3.8 | | | Semi-Annual |

Two Creeks Capital Offshore Fund, Ltd. | | | 7,839 | | | | 10,801,081 | | | | 1.1 | | | Quarterly |

Tybourne Equity (Offshore) Fund | | | 9,956 | | | | 14,561,368 | | | | 1.5 | | | Quarterly |

| | | | | | | | | | | | | | |

Total | | | | | | | 280,874,998 | | | | 28.6 | | | |

| | | | | | | | | | | | | | |

| | | | |

Global Macro | | | | | | | | | | | | | | |

Alphadyne International Partners, LP | | | 62,221 | | | | 74,844,924 | | | | 7.6 | | | Quarterly |

Autonomy Global Macro Fund LP | | | 210,557 | | | | 28,987,138 | | | | 2.9 | | | Monthly |

Brevan Howard AS Macro Fund Limited | | | 280,000 | | | | 28,823,200 | | | | 2.9 | | | Monthly |

Rokos Global Macro Fund LP | | | 401,922 | | | | 24,285,836 | | | | 2.5 | | | Monthly |

Tudor BVI Global Fund LP | | | 15,205 | | | | 48,796,925 | | | | 5.0 | | | Quarterly |

| | | | | | | | | | | | | | |

Total | | | | | | | 205,738,023 | | | | 20.9 | | | |

| | | | | | | | | | | | | | |

| | |

| |

| 8 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | | | |

Underlying

Portfolios | | Shares | | | Fair Value ($) | | | % Net Assets | | | Liquidity* |

|

| | | | |

Multi-Strategy | | | | | | | | | | | | | | |

Elliott International Limited | | | 33,772 | | | $ | 49,372,900 | | | | 5.0 | % | | Quarterly |

LMR Fund Limited | | | 400,000 | | | | 40,559,311 | | | | 4.2 | | | Quarterly |

Myriad Opportunities US Fund Limited | | | 27,081 | | | | 29,435,819 | | | | 3.0 | | | Quarterly |

Renaissance Institutional Diversified Global Equities Onshore Fund LP | | | 39,844 | | | | 42,299,480 | | | | 4.3 | | | Monthly |

Schonfeld Strategic Partners Offshore Fund Ltd. | | | 20,000 | | | | 21,583,617 | | | | 2.2 | | | Monthly |

| | | | | | | | | | | | | | |

Total | | | | | | | 183,251,127 | | | | 18.7 | | | |

| | | | | | | | | | | | | | |

| | | | |

Event Driven | | | | | | | | | | | | | | |

Empyrean Capital Overseas Fund, Ltd. | | | 34,984 | | | | 38,955,404 | | | | 4.0 | | | Quarterly |

Governors Lane Offshore Fund Ltd. | | | 13,774 | | | | 15,385,000 | | | | 1.6 | | | Quarterly |

Indaba Capital Partners (Cayman), LP | | | 31,293 | | | | 38,326,797 | | | | 3.9 | | | Quarterly |

Lion Point International, Ltd. | | | 29,565 | | | | 32,492,820 | | | | 3.3 | | | Semi-Annual |

Luxor Capital Partners Liquidating SPV, LLC | | | 2,317 | | | | 2,852,047 | | | | 0.3 | | | At Fund’s Discretion |

Senator Global Opportunity Fund LP | | | 24,746 | | | | 29,706,211 | | | | 3.0 | | | Quarterly |

Starboard Leaders Fund LP | | | 1,199 | | | | 1,115,769 | | | | 0.1 | | | At Fund’s Discretion |

| | | | | | | | | | | | | | |

Total | | | | | | | 158,834,048 | | | | 16.2 | | | |

| | | | | | | | | | | | | | |

| | | | |

Credit/Distressed | | | | | | | | | | | | | | |

Caius Capital International Fund | | | 30,036 | | | | 35,130,125 | | | | 3.6 | | | Quarterly |

King Street Capital, Ltd. | | | 248,296 | | | | 25,148,953 | | | | 2.5 | | | Quarterly |

Silver Point Capital Offshore Fund, Ltd. | | | 2,685 | | | | 40,581,291 | | | | 4.1 | | | Annual |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 9 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | | | |

Underlying

Portfolios | | Shares | | | Fair Value ($) | | | % Net Assets | | | Liquidity* |

|

Waterfall Eden Fund, LP | | | 30,000 | | | $ | 31,044,644 | | | | 3.2 | % | | Quarterly |

Wingspan Overseas Fund, Ltd. | | | 953 | | | | 628,568 | | | | 0.1 | | | Fund in Liquidation |

| | | | | | | | | | | | | | |

Total | | | | | | | 132,533,581 | | | | 13.5 | | | |

| | | | | | | | | | | | | | |

| | | | |

Total Underlying Portfolios

(cost $846,712,821) | | | | | | | 961,231,777 | | | | 97.9 | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Short-Term Investments | | | | | | | | | | | | | | |

Investment Companies | | | | | | | | | | | | | | |

AB Fixed Income Shares, Inc. – Government Money Market Portfolio – Class AB, 1.89%(a)(b)(c)

(cost $12,500,000) | | | 12,500,000 | | | | 12,500,000 | | | | 1.2 | | | |

| | | | | | | | | | | | | | |

| | | | |

Total Investments

(cost $859,212,821) | | | | | | | 973,731,777 | | | | 99.1 | | | |

Other assets less liabilities | | | | | | | 8,348,460 | | | | 0.9 | | | |

| | | | | | | | | | | | | | |

| | | | |

Net Assets | | | | | | $ | 982,080,237 | | | | 100.0 | % | | |

| | | | | | | | | | | | | | |

TOTAL RETURN SWAPS (see Note C)

| | | | | | | | | | | | | | | | | | | | |

Counterparty &

Referenced Obligation | | Rate Paid/

Received | | Payment

Frequency | | Current Notional

(000) | | | Maturity

Date | | | Unrealized

Appreciation/

(Depreciation) | |

Receive Total Return on Reference Obligation | |

Barclays Bank PLC | | | | | | | | | | | | | | | | | | | | |

Barclays Commodity Hedging Insights 2 | | 0.02% | | Quarterly | | | USD | | | | 3,694 | | | | 10/15/19 | | | $ | (22,691 | ) |

Barclays Commodity Strategy 1673 Index | | 0.30% | | Quarterly | | | USD | | | | 2,495 | | | | 10/15/19 | | | | (42,225 | ) |

| | |

| |

| 10 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | | | | | | | | | | | |

Counterparty &

Referenced Obligation | | Rate Paid/

Received | | Payment

Frequency | | | Current Notional

(000) | | | Maturity

Date | | | Unrealized

Appreciation/

(Depreciation) | |

Credit Suisse International | | | | | | | | | | | | | | | | | | | | | | |

Credit Suisse Managed Futures Liquid Index (Net Excess) | | 0.35% | | | Quarterly | | | | USD | | | | 7,537 | | | | 3/16/20 | | | $ | (1,905 | ) |

Goldman Sachs & Co. | | | | | | | | | | | | | | | | | | | | | | |

Advanced Disposal Services | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 2,127 | | | | 1/15/21 | | | | (6,997 | ) |

Inmarsat PLC | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | GBP | | | | 1,778 | | | | 1/05/21 | | | | 192,085 | |

Mellanox Technologies Ltd. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 891 | | | | 1/05/21 | | | | (60,239 | ) |

Spark Therapeutics Inc. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 1,093 | | | | 1/05/21 | | | | (173,921 | ) |

SunTrust Banks Inc. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 2,224 | | | | 1/05/21 | | | | 127,048 | |

Versum Materials Inc. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 2,153 | | | | 1/05/21 | | | | 495,105 | |

Wabco Holdings Inc. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 2,155 | | | | 1/05/21 | | | | 1,979 | |

Wellcare Health Plans Inc. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 2,007 | | | | 1/05/21 | | | | (84,636 | ) |

Goldman Sachs International | | | | | | | | | | | | | | | | | | | | | | |

Cross Asset Trend Basket Series 2 10% Volatility Target ER Strategy(1) | | 0.00% | | | Quarterly | | | | USD | | | | 12,340 | | | | 5/15/20 | | | | (17,588 | ) |

GSISM49E(2) | | 0.00% | | | Quarterly | | | | USD | | | | 18,309 | | | | 5/15/20 | | | | – 0 | – |

RP Equity Carry Series 1 Excess Return Strategy | | 0.00% | | | Quarterly | | | | USD | | | | 1,761 | | | | 10/15/19 | | | | (12,728 | ) |

JPMorgan Chase Bank, NA | | | | | | | | | | | | | | | | | | | | | | |

AVON Products Inc. | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 1,788 | | | | 8/14/20 | | | | 170,502 | |

Carbon Black Inc. CFD | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 42 | | | | 8/14/20 | | | | 128 | |

Carrizo Oil & Gas Inc. | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 1,753 | | | | 8/14/20 | | | | (308,544 | ) |

Cobham PLC CFD | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 717 | | | | 8/14/20 | | | | (12,196 | ) |

Gannett Co. Inc. | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 1,857 | | | | 8/14/20 | | | | 121,960 | |

Grandvision NV | | 1 Month EURIBOR Plus 0.40% | | | Maturity | | | | EUR | | | | 1,124 | | | | 8/14/20 | | | | 6,220 | |

Greene King PLC | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | GBP | | | | 1,522 | | | | 8/14/20 | | | | 10,283 | |

J.P.Morgan RCI – 24 Alpha | | 0.50% | | | Quarterly | | | | USD | | | | 2,266 | | | | 10/15/19 | | | | (9,349 | ) |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 11 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | | | | | | | | | | | |

Counterparty &

Referenced Obligation | | Rate Paid/

Received | | Payment

Frequency | | | Current Notional

(000) | | | Maturity

Date | | | Unrealized

Appreciation/

(Depreciation) | |

JMABRCX4 | | 0.72% | | | Quarterly | | | | USD | | | | 3,073 | | | | 3/16/20 | | | $ | 5,516 | |

JMABRG34(3) | | 0.60% | | | Quarterly | | | | USD | | | | 2,182 | | | | 10/15/19 | | | | (31,158 | ) |

JPABGERP(4) | | 0.43% | | | Maturity | | | | USD | | | | 12,525 | | | | 12/16/19 | | | | (3,132 | ) |

JPABSAA1(5) | | 0.00% | | | Maturity | | | | USD | | | | 22,483 | | | | 8/14/20 | | | | 1,661 | |

JPMorgan Alternative FX Mean Reversion JPM 2RM1 Index | | 0.00% | | | Maturity | | | | USD | | | | 3,967 | | | | 8/14/20 | | | | (2,002 | ) |

Kinder Morgan Canada Ltd. | | 1 Month CDOR Plus 0.40% | | | Maturity | | | | CAD | | | | 1,594 | | | | 8/14/20 | | | | 13,137 | |

Old Line Bancshares | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 1,517 | | | | 8/14/20 | | | | 67,417 | |

Transat A.T. Inc. | | 1 Month CDOR Plus 0.40% | | | Maturity | | | | CAD | | | | 1,234 | | | | 8/14/20 | | | | (127,086 | ) |

United Community Financial CFD | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 128 | | | | 8/14/20 | | | | 5,134 | |

United Financial Bancorp Inc. | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 790 | | | | 8/14/20 | | | | (31,906 | ) |

Viacom Inc. – Class B | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 1,975 | | | | 8/14/20 | | | | (137,991 | ) |

Morgan Stanley Capital Services, LLC | | | | | | | | | | | | | | | | | | | | | | |

Acacia Communications Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 2,157 | | | | 12/11/19 | | | | 3,921 | |

Allergan PLC | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 2,152 | | | | 12/11/19 | | | | 44,115 | |

Altran Technologies SA | | 1 Month EURIBOR Plus 0.50% | | | Maturity | | | | EUR | | | | 299 | | | | 12/11/19 | | | | 9,888 | |

C&J Enery Services Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,184 | | | | 12/11/19 | | | | (271,497 | ) |

Caesars Entertainment Corp. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 2,143 | | | | 12/11/19 | | | | (2,556 | ) |

Celgene Corp. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 2,219 | | | | 12/11/19 | | | | 273,991 | |

Connecticut Water Service Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 354 | | | | 12/11/19 | | | | (2,145 | ) |

Cypress Semiconductor Corp. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 2,220 | | | | 12/11/19 | | | | 102,682 | |

LegacyTexas Financial Group | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,924 | | | | 12/11/19 | | | | 160,197 | |

Medidata Solutions Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 2,133 | | | | 12/11/19 | | | | (8,707 | ) |

Mellanox Technologies Ltd. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,040 | | | | 12/11/19 | | | | (106,802 | ) |

Milacron Holdings Corp. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,733 | | | | 12/11/19 | | | | (46,871 | ) |

Morgan Stanley Volume B3U Index | | 0.50% | | | Quarterly | | | | USD | | | | 4,091 | | | | 10/15/19 | | | | 5,863 | |

MSABFLSU | | 0.65% | | | Maturity | | | | USD | | | | 4,377 | | | | 12/16/19 | | | | (1,815 | ) |

MSCBRMF4(6) | | 0.60% | | | Quarterly | | | | USD | | | | 4,299 | | | | 10/15/19 | | | | 195,283 | |

MSUSABDM(7) | | 0.00% | | | Quarterly | | | | USD | | | | 33,403 | | | | 12/11/19 | | | | (1,732 | ) |

MSUSABEM(8) | | 0.00% | | | Quarterly | | | | USD | | | | 37,061 | | | | 12/11/19 | | | | (9,804 | ) |

| | |

| |

| 12 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | | | | | | | | | | | |

Counterparty &

Referenced Obligation | | Rate Paid/

Received | | Payment

Frequency | | | Current Notional

(000) | | | Maturity

Date | | | Unrealized

Appreciation/

(Depreciation) | |

MSUSABEQ | | 0.00% | | | Quarterly | | | | USD | | | | 10,521 | | | | 12/11/19 | | | $ | (903 | ) |

OMNOVA Solutions Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,327 | | | | 12/11/19 | | | | 5,849 | |

Pacific Biosciences of California Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 901 | | | | 12/11/19 | | | | (395,111 | ) |

Rudolph Technologies Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 943 | | | | 12/11/19 | | | | (56,238 | ) |

Sprint Nextel Corp. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,216 | | | | 12/11/19 | | | | (68,862 | ) |

Valley National Bancorp | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 1,145 | | | | 12/11/19 | | | | 24,059 | |

|

Pay Total Return on Reference Obligation | |

Goldman Sachs & Co. | | | | | | | | | | | | | | | | | | | | | | |

BB&T Corp. | | 1 Month LIBOR Plus 0.35% | | | Maturity | | | | USD | | | | 2,234 | | | | 1/05/21 | | | | (117,139 | ) |

Centene Corp. | | 1 Month LIBOR Minus 0.30% | | | Maturity | | | | USD | | | | 1,132 | | | | 1/05/21 | | | | 248,898 | |

JPMorgan Chase Bank, NA | | | | | | | | | | | | | | | | | | | | | | |

Callon Petroleum Corp. | | 1 Month LIBOR Minus 0.29% | | | Maturity | | | | USD | | | | 1,817 | | | | 8/14/20 | | | | 311,296 | |

CBS Corp. – Class B | | 1 Month LIBOR Plus 0.40% | | | Maturity | | | | USD | | | | 1,978 | | | | 8/14/20 | | | | 144,053 | |

First Defiance FINL Corp. CFD | | 1 Month LIBOR Minus 0.29% | | | Maturity | | | | USD | | | | 128 | | | | 8/14/20 | | | | (3,841 | ) |

Natura Cosmeticos SA | | 1 Month LIBOR Minus 6.50% | | | Maturity | | | | USD | | | | 1,982 | | | | 8/14/20 | | | | (158,118 | ) |

New Media Investment Group | | 1 Month LIBOR Minus 0.30% | | | Maturity | | | | USD | | | | 827 | | | | 8/14/20 | | | | (93,730 | ) |

People’s United Financial Inc. | | 1 Month LIBOR Minus 0.30% | | | Maturity | | | | USD | | | | 790 | | | | 8/14/20 | | | | 37,289 | |

PPL Corporation | | 1 Month CDOR Minus 0.48% | | | Maturity | | | | CAD | | | | 1,610 | | | | 8/14/20 | | | | (8,985 | ) |

Wesbanco Inc. | | 1 Month LIBOR Minus 0.30% | | | Maturity | | | | USD | | | | 1,533 | | | | 8/14/20 | | | | (76,945 | ) |

Morgan Stanley Capital Services, LLC | | | | | | | | | | | | | | | | | | | | | | |

Abbvie Inc. | | 1 Month LIBOR Minus 2.36% | | | Maturity | | | | USD | | | | 838 | | | | 12/11/19 | | | | (93,272 | ) |

Bristol-Myers Squibb Co. | | 1 Month LIBOR Minus 0.30% | | | Maturity | | | | USD | | | | 1,133 | | | | 12/11/19 | | | | (91,517 | ) |

Eldorado Resorts Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 659 | | | | 12/11/19 | | | | 105,701 | |

Hillenbrand Inc. | | 1 Month LIBOR Plus 0.30% | | | Maturity | | | | USD | | | | 518 | | | | 12/11/19 | | | | 74,780 | |

Keane Group Inc. | | 1 Month LIBOR Minus 2.36% | | | Maturity | | | | USD | | | | 1,080 | | | | 12/11/19 | | | | 270,953 | |

Nanometrics Inc. | | 1 Month LIBOR Minus 2.36% | | | Maturity | | | | USD | | | | 939 | | | | 12/11/19 | | | | 63,123 | |

Oritani Financial Corp. | | 1 Month LIBOR Minus 2.36% | | | Maturity | | | | USD | | | | 1,165 | | | | 12/11/19 | | | | (14,182 | ) |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 13 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | | | | | | | | | | | |

Counterparty &

Referenced Obligation | | Rate Paid/

Received | | Payment

Frequency | | | Current Notional

(000) | | | Maturity

Date | | | Unrealized

Appreciation/

(Depreciation) | |

Prosperity Bancshares Inc. | | 1 Month LIBOR Minus 2.36% | | | Maturity | | | | USD | | | | 1,648 | | | | 12/11/19 | | | $ | (166,159 | ) |

T-Mobile US Inc. | | 1 Month LIBOR Minus 0.22% | | | Maturity | | | | USD | | | | 1,592 | | | | 12/11/19 | | | | (182,788 | ) |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | $ | 234,103 | |

| | | | | | | | | | | | | | | | | | | | | | |

| (a) | Affiliated investments. |

| (b) | The rate shown represents the7-day yield as of period end. |

| (c) | To obtain a copy of the fund’s shareholder report, please go to the Securities and Exchange Commission’s website at www.sec.gov, or call AB at (800)227-4618. |

| * | The investment strategies and liquidity of the Underlying Portfolios in which the Fund invests are as follows: |

Long/Short Equity Underlying Portfolios seek to buy securities with the expectation that they will increase in value (called “going long”) and sell securities short in the expectation that they will decrease in value (“going short”). Underlying Portfolios within this strategy are generally subject to 45 – 120 day redemption notice periods. The majority of the Underlying Portfolios are no longer subject to initial lockups. Certain Underlying Portfolios have lock up periods of up to three years.

Event Driven Underlying Portfolios seek to take advantage of information inefficiencies resulting from a particular corporate event, such as a takeover, liquidation, bankruptcy, tender offer, buyback, spin(off, exchange offer, merger or other type of corporate reorganization. Underlying Portfolios within this strategy are generally subject to 60 – 90 day redemption notice periods. The majority of the Underlying Portfolios are no longer subject to initial lockups. Certain Underlying Portfolios have lock up periods of up to one year.

Global Macro Underlying Portfolios aim to identify and exploit imbalances in global economics and asset classes, typically utilizing macroeconomic and technical market factors rather than“bottom-up” individual security analysis. The Underlying Portfolios within this strategy are subject to 30 – 90 day redemption notice periods. Certain Underlying Portfolios have lock up periods of up to one year.

Credit/Distressed Underlying Portfolios invest in a variety of fixed income and other securities, including bonds (corporate and government), bank debt, asset-backed financial instruments, mortgage-backed securities and mezzanine and distressed securities, as well as securities of distressed companies and high yield securities. Underlying Portfolios within this strategy are generally subject to 60 – 90 day redemption notice periods. The majority of the Underlying Portfollios are no longer subject to initial lockups. Certain Underlying Portfolios may have lock up periods of two years.

Multi-Strategy Underlying Portfolios invest across multiple strategies, including long/short equity, event driven, global macro, credit/distressed and emerging markets, in which the investment process is predicated on movements in underlying economic variables and the impact these variables have on equity, fixed income, currency, commodity and other financial instrument markets. Underlying Portfolios within this strategy are generally subject to 45 – 90 day redemption notice periods. Certain Underlying Portfolios may have lock up periods of up to two years.

The Fund may also make direct investments in securities (other than securities of Underlying Portfolios), options, futures, options on futures, swap contracts, or other derivative or financial instruments.

Currency Abbreviations:

AUD – Australian Dollar

BRL – Brazilian Real

CAD – Canadian Dollar

CHF – Swiss Franc

CLP – Chilean Peso

CNH – Chinese Yuan Renminbi (Offshore)

CNY – Chinese Yuan Renminbi

COP – Colombian Peso

| | |

| |

| 14 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

CZK – Czech Koruna

EUR – Euro

GBP – Great British Pound

HUF – Hungarian Forint

IDR – Indonesian Rupiah

ILS – Israeli Shekel

INR – Indian Rupee

JPY – Japanese Yen

KRW – South Korean Won

MXN – Mexican Peso

NOK – Norwegian Krone

NZD – New Zealand Dollar

PEN – Peruvian Sol

PHP – Philippine Peso

PLN – Polish Zloty

RUB – Russian Ruble

SEK – Swedish Krona

SGD – Singapore Dollar

THB – Thailand Baht

TRY – Turkish Lira

TWD – New Taiwan Dollar

USD – United States Dollar

ZAR – South African Rand

Glossary:

BOBL – Bundesobligationen

CBT – Chicago Board of Trade

EAFE – Europe, Australia, and Far East

EURIBOR – Euro Interbank Offered Rate

KC HRW – Kansas City Hard Red Winter

LIBOR – London Interbank Offered Rates

LME – London Metal Exchange

MSCI – Morgan Stanley Capital International

OAT – Obligations Assimables du Trésor

OSE – Osaka Securities Exchange

RBOB – Reformulated Gasoline Blend-Stock for Oxygen Blending (Unleaded Gas)

REIT – Real Estate Investment Trust

SPI – Share Price Index

TSX – Toronto Stock Exchange

ULSD –Ultra-Low Sulfur Diesel

WTI – West Texas Intermediate

| (1) | The following table represents the 50 largest (long/(short)) basket holdings underlying the total return swap with Cross Asset Trend Basket Series 2 10% Volatility Target ER Strategy as of September 30, 2019. |

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

3 Month EURIBOR 12/20 | | $ | 6,017,701 | | | | 48.7 | % |

3 Month EURIBOR 3/21 | | | 6,017,222 | | | | 48.7 | % |

3 Month EURIBOR 6/20 | | | 6,015,967 | | | | 48.7 | % |

3 Month EURIBOR 3/20 | | | 6,014,770 | | | | 48.7 | % |

90 Day Sterling Futures 3/21 | | | 5,949,620 | | | | 48.1 | % |

90 Day Sterling Futures 12/20 | | | 5,948,290 | | | | 48.1 | % |

90 Day Sterling Futures 6/20 | | | 5,947,206 | | | | 48.1 | % |

90 Day Sterling Futures 3/20 | | | 5,945,759 | | | | 48.1 | % |

90 Day Euro Futures 6/20 | | | 5,914,380 | | | | 47.9 | % |

90 Day Euro Futures 3/20 | | | 5,907,887 | | | | 47.8 | % |

90 Day Euro Futures 3/21 | | | 5,710,936 | | | | 46.2 | % |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 15 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

90 Day Euro Futures 12/20 | | $ | 5,705,399 | | | | 46.2 | % |

U.S. 2 Yr Note (CBT) 12/19 | | | 5,064,182 | | | | 41.0 | % |

Euro-SCHATZ Futures 12/19 | | | 3,674,224 | | | | 29.7 | % |

Euro-BOBL Futures 12/19 | | | 3,173,020 | | | | 25.7 | % |

Japan 10 Yr Bond (OSE) 12/19 | | | 2,400,371 | | | | 19.4 | % |

U.S. 5 Yr Note (CBT) 12/19 | | | 2,312,993 | | | | 18.7 | % |

USD/SGD 10/19 | | | (1,731,073 | ) | | | (14.0 | )% |

Euro-Bund Futures 12/19 | | | 1,588,982 | | | | 12.9 | % |

U.S. 10 Yr Note (CBT) 12/19 | | | 1,516,663 | | | | 12.3 | % |

Long Gilt Futures 12/19 | | | 1,288,124 | | | | 10.4 | % |

USD/TWD 10/31/19 | | | (1,279,489 | ) | | | (10.4 | )% |

USD/EUR 10/31/19 | | | (1,017,902 | ) | | | (8.2 | )% |

USD/PHP 10/31/19 | | | 1,016,065 | | | | 8.2 | % |

USD/IDR 10/31/19 | | | 978,433 | | | | 7.9 | % |

USD/ILS 10/31/19 | | | 898,956 | | | | 7.3 | % |

USD/KRW 10/31/19 | | | (865,537 | ) | | | (7.0 | )% |

U.S. Long Bond (CBT) 12/19 | | | 862,943 | | | | 7.0 | % |

USD/CZK 10/31/19 | | | (851,643 | ) | | | (6.9 | )% |

USD/CNH 10/31/19 | | | (827,905 | ) | | | (6.7 | )% |

USD/AUD 10/31/19 | | | (763,427 | ) | | | (6.2 | )% |

USD/NZD 10/31/19 | | | (721,014 | ) | | | (5.8 | )% |

USD/CHF 10/31/19 | | | (721,014 | ) | | | (5.8 | )% |

USD/PLN 10/31/19 | | | (709,702 | ) | | | (5.7 | )% |

USD/CAD 10/31/19 | | | (678,601 | ) | | | (5.5 | )% |

USD/HUF 10/31/19 | | | (662,389 | ) | | | (5.4 | )% |

USD/SEK 10/31/19 | | | (636,189 | ) | | | (5.1 | )% |

USD/GBP 10/31/19 | | | (636,189 | ) | | | (5.1 | )% |

USD/NOK 10/31/19 | | | (636,189 | ) | | | (5.1 | )% |

USD/CLP 10/31/19 | | | (567,762 | ) | | | (4.6 | )% |

LME PRI Aluminum Futures 11/19 | | | (510,387 | ) | | | (4.1 | )% |

Gold 100 Oz. Futures 12/19 | | | 479,948 | | | | 3.9 | % |

S&P/TSX 60 Index Futures 12/19 | | | 464,100 | | | | 3.8 | % |

USD/BRL 10/31/19 | | | (425,821 | ) | | | (3.4 | )% |

USD/MXN 10/31/19 | | | 425,821 | | | | 3.4 | % |

LME Copper Futures 11/19 | | | (410,000 | ) | | | (3.3 | )% |

Swiss Market Index Futures 12/19 | | | 383,517 | | | | 3.1 | % |

SPI 200 Futures 10/19 | | | 382,390 | | | | 3.1 | % |

USD/RUB 10/31/19 | | | 378,508 | | | | 3.1 | % |

USD/TRY 10/31/19 | | | 378,508 | | | | 3.1 | % |

Other Long | | | 5,432,378 | | | | 44.0 | % |

Other (Short) | | | (4,194,665 | ) | | | (33.9 | )% |

| (2) | The following table represents the 50 largest (long/(short)) equity basket holdings underlying the total return swap with GSISM49E as of September 30, 2019. |

| | | | | | | | | | | | |

| Security Description | | Shares | | | Current Notional | | | Percent of

Basket’s Value | |

Apple, Inc. | | | (3,513 | ) | | $ | (786,813 | ) | | | (4.3 | )% |

Microsoft Corp. | | | (4,510 | ) | | | (627,053 | ) | | | (3.4 | )% |

Amazon.com, Inc. | | | (323 | ) | | | (559,938 | ) | | | (3.1 | )% |

Alphabet, Inc. | | | (220 | ) | | | (268,287 | ) | | | (1.5 | )% |

Nestle SA | | | (2,291 | ) | | | (248,743 | ) | | | (1.4 | )% |

Proctor & Gamble Co. (The) | | | (1,907 | ) | | | (237,194 | ) | | | (1.3 | )% |

Visa, Inc. | | | (1,341 | ) | | | (230,653 | ) | | | (1.3 | )% |

| | |

| |

| 16 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Security Description | | Shares | | | Current Notional | | | Percent of

Basket’s Value | |

Berkshire Hathaway, Inc. | | | (991 | ) | | $ | (206,179 | ) | | | (1.1 | )% |

Facebook, Inc. | | | (1,145 | ) | | | (203,931 | ) | | | (1.1 | )% |

JPMorgan Chase & Co. | | | (1,705 | ) | | | (200,624 | ) | | | (1.1 | )% |

Home Depot, Inc. (The) | | | (835 | ) | | | (193,819 | ) | | | (1.1 | )% |

MasterCard, Inc. | | | (691 | ) | | | (187,735 | ) | | | (1.0 | )% |

Walt Disney Co. (The) | | | (1,393 | ) | | | (181,513 | ) | | | (1.0 | )% |

Exxon Mobil Corp. | | | (2,571 | ) | | | (181,513 | ) | | | (1.0 | )% |

Bank of America Corp. | | | (5,838 | ) | | | (170,300 | ) | | | (0.9 | )% |

Intel Corp. | | | (3,279 | ) | | | (168,951 | ) | | | (0.9 | )% |

Coca-Cola Co. (The) | | | (3,086 | ) | | | (168,010 | ) | | | (0.9 | )% |

Cypress Semiconductor Corp. | | | 7,073 | | | | 165,072 | | | | 0.9 | % |

Wells Fargo & Co. | | | (3,204 | ) | | | (161,626 | ) | | | (0.9 | )% |

United Health Group | | | (740 | ) | | | (160,874 | ) | | | (0.9 | )% |

Cisco Systems, Inc. | | | (3,150 | ) | | | (155,660 | ) | | | (0.9 | )% |

HollyFrontier Corp. | | | 2,891 | | | | 155,079 | | | | 0.8 | % |

Boeing Co. (The) | | | (403 | ) | | | (153,351 | ) | | | (0.8 | )% |

United Airlines Holdings, Inc. | | | 1,692 | | | | 149,561 | | | | 0.8 | % |

Jacobs Engineering Group, Inc. | | | 1,630 | | | | 149,161 | | | | 0.8 | % |

Universal Health Services, Inc. | | | 1,000 | | | | 148,679 | | | | 0.8 | % |

Alphabet, Inc. | | | (122 | ) | | | (148,423 | ) | | | (0.8 | )% |

Akami Technologies, Inc. | | | 1,622 | | | | 148,226 | | | | 0.8 | % |

Hormel Foods Corp. | | | 3,383 | | | | 147,949 | | | | 0.8 | % |

Bridgestone Corp. | | | 3,816 | | | | 147,746 | | | | 0.8 | % |

Ameren Corp. | | | 1,830 | | | | 146,514 | | | | 0.8 | % |

Seagate Technology PLC | | | 2,708 | | | | 145,677 | | | | 0.8 | % |

ANSYS, Inc. | | | 656 | | | | 145,263 | | | | 0.8 | % |

Discovery, Inc. | | | 5,890 | | | | 145,009 | | | | 0.8 | % |

AGNC Investment Corp. | | | 8,947 | | | | 143,963 | | | | 0.8 | % |

Delta Air Lines, Inc. | | | 2,496 | | | | 143,765 | | | | 0.8 | % |

Swiss Life Holding AG | | | 300 | | | | 143,319 | | | | 0.8 | % |

Nucor Corp. | | | 2,780 | | | | 141,541 | | | | 0.8 | % |

Cincinnati Financial Corp. | | | 1,212 | | | | 141,378 | | | | 0.8 | % |

Leidos Holdings, Inc. | | | 1,643 | | | | 141,079 | | | | 0.8 | % |

Telstra Corp. Ltd. | | | 59,592 | | | | 141,074 | | | | 0.8 | % |

Chipotle Mexican Grill, Inc. | | | 166 | | | | 139,494 | | | | 0.8 | % |

Ally Financial, Inc. | | | 4,206 | | | | 139,475 | | | | 0.8 | % |

EPAM Systems, Inc. | | | 763 | | | | 139,077 | | | | 0.8 | % |

Booz Allen Hamilton Holding Co. | | | 1,939 | | | | 137,709 | | | | 0.8 | % |

Bio-Rad Laboratories, Inc. | | | 414 | | | | 137,639 | | | | 0.8 | % |

Fifth Third Bancorp | | | 5,026 | | | | 137,602 | | | | 0.8 | % |

Cummins, Inc. | | | 844 | | | | 137,257 | | | | 0.7 | % |

T-Mobile US, Inc. | | | 1,741 | | | | 137,126 | | | | 0.7 | % |

Synchrony Financial | | | 4,013 | | | | 136,803 | | | | 0.7 | % |

Other Long | | | 1,269,835 | | | | 24,274,573 | | | | 132.6 | % |

Other (Short) | | | (531,252 | ) | | | (18,454,817 | ) | | | (100.8 | )% |

| (3) | The following table represents the (long/(short)) basket holdings underlying the total return swap with JMABRG34 as of September 30, 2019. |

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

Gasoline RBOB Futures 11/19 | | $ | (659,249 | ) | | | (30.3 | )% |

NY Harbor ULSD Futures 11/19 | | | (642,487 | ) | | | (29.5 | )% |

Gasoline RBOB Futures 3/20 | | | 641,362 | | | | 29.5 | % |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 17 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

NY Harbor ULSD Futures 3/20 | | $ | 630,083 | | | | 29.0 | % |

Brent Crude Futures 1/20 | | | (629,647 | ) | | | (28.9 | )% |

Brent Crude Futures 5/20 | | | 625,557 | | | | 28.8 | % |

WTI Crude Futures 3/20 | | | 615,993 | | | | 28.3 | % |

WTI Crude Futures 11/19 | | | (615,094 | ) | | | (28.3 | )% |

Natural Gas Futures 3/20 | | | 605,522 | | | | 27.8 | % |

Natural Gas Futures 11/19 | | | (594,473 | ) | | | (27.3 | )% |

LME Zinc Futures 11/19 | | | (572,514 | ) | | | (26.3 | )% |

LME Zinc Futures 3/20 | | | 565,726 | | | | 26.0 | % |

Corn Futures 12/19 | | | (563,407 | ) | | | (25.9 | )% |

Corn Futures 3/20 | | | 559,568 | | | | 25.7 | % |

Coffee ‘C’ Futures 12/19 | | | (554,923 | ) | | | (25.5 | )% |

Coffee ‘C’ Futures 3/20 | | | 554,382 | | | | 25.5 | % |

Soybean Futures 11/19 | | | (546,835 | ) | | | (25.1 | )% |

Soybean Futures 3/20 | | | 544,700 | | | | 25.0 | % |

Copper Futures 3/20 | | | 535,048 | | | | 24.6 | % |

Copper Futures 12/19 | | | (534,672 | ) | | | (24.6 | )% |

LME PRI Aluminum Futures 11/19 | | | (515,591 | ) | | | (23.7 | )% |

LME PRI Aluminum Futures 3/20 | | | 514,923 | | | | 23.7 | % |

LME Nickel Futures 11/19 | | | (498,282 | ) | | | (22.9 | )% |

LME Nickel Futures 3/20 | | | 496,536 | | | | 22.8 | % |

Live Cattle Futures 4/20 | | | 370,382 | | | | 17.0 | % |

Live Cattle Futures 12/19 | | | (367,401 | ) | | | (16.9 | )% |

Lean Hogs Futures 4/20 | | | 275,502 | | | | 12.7 | % |

Lean Hogs Futures 12/19 | | | (274,399 | ) | | | (12.6 | )% |

Wheat Futures (CBT) 12/19 | | | (191,013 | ) | | | (8.8 | )% |

Wheat Futures (CBT) 3/20 | | | 190,981 | | | | 8.8 | % |

KC HRW Wheat Futures 12/19 | | | (189,704 | ) | | | (8.7 | )% |

KC HRW Wheat Futures 3/20 | | | 187,778 | | | | 8.6 | % |

Cotton No.2 Futures 12/19 | | | (183,703 | ) | | | (8.4 | )% |

Cotton No.2 Futures 3/20 | | | 183,655 | | | | 8.4 | % |

Soybean Meal Futures 3/20 | | | 179,121 | | | | 8.2 | % |

Soybean Meal Futures 12/19 | | | (178,833 | ) | | | (8.2 | )% |

Soybean Oil Futures 3/20 | | | 174,852 | | | | 8.0 | % |

Soybean Oil Futures 12/19 | | | (174,674 | ) | | | (8.0 | )% |

Sugar #11 (World) Futures 3/20 | | | 3,671 | | | | 0.2 | % |

| (4) | The following table represents the 50 largest (long/(short)) equity basket holdings underlying the total return swap with JPABGERP as of September 30, 2019. |

| | | | | | | | | | | | |

| Security Description | | Shares | | | Current Notional | | | Percent of

Basket’s Value | |

JPMorgan Cash Index | | | (10,963 | ) | | $ | (3,301,741 | ) | | | (26.4 | )% |

iA Financial Corp., Inc. | | | 3,436 | | | | 156,460 | | | | 1.2 | % |

Western Union Co. (The) | | | 6,509 | | | | 150,822 | | | | 1.2 | % |

Hongkong Land Holdings Ltd. | | | (26,747 | ) | | | (150,317 | ) | | | (1.2 | )% |

Jardine Matheson Holdings Ltd. | | | (2,753 | ) | | | (147,283 | ) | | | (1.2 | )% |

Jardine Strategic Holdings Ltd. | | | (4,869 | ) | | | (145,489 | ) | | | (1.2 | )% |

Dairy Farm International Holdings | | | (22,008 | ) | | | (138,649 | ) | | | (1.1 | )% |

Concho Resources, Inc. | | | (1,851 | ) | | | (125,667 | ) | | | (1.0 | )% |

Teijin Ltd. | | | 6,138 | | | | 117,903 | | | | 0.9 | % |

Atco Ltd./Canada | | | 3,215 | | | | 117,726 | | | | 0.9 | % |

Uber Technologies, Inc. | | | (3,784 | ) | | | (115,284 | ) | | | (0.9 | )% |

| | |

| |

| 18 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Security Description | | Shares | | | Current Notional | | | Percent of

Basket’s Value | |

Direct Line Insurance Group PLC | | | 311 | | | $ | 114,992 | | | | 0.9 | % |

Air Canada | | | 3,518 | | | | 114,807 | | | | 0.9 | % |

EssilorLuxottica SA | | | (791 | ) | | | (114,017 | ) | | | (0.9 | )% |

Juniper Networks, Inc. | | | 4,588 | | | | 113,561 | | | | 0.9 | % |

Fortescue Metals Group Ltd. | | | 19,048 | | | | 113,052 | | | | 0.9 | % |

Lida Group Holdings Co. Ltd. | | | 6,916 | | | | 112,491 | | | | 0.9 | % |

Compass Group PLC | | | 44 | | | | 112,331 | | | | 0.9 | % |

Koninklijke Philips NV | | | 2,416 | | | | 111,950 | | | | 0.9 | % |

Mitsubishi Materials Corp. | | | 4,044 | | | | 109,081 | | | | 0.9 | % |

H&R Block, Inc. | | | 4,612 | | | | 108,934 | | | | 0.9 | % |

Heineken Holding NV | | | 1,078 | | | | 107,313 | | | | 0.9 | % |

Tesla, Inc. | | | (426 | ) | | | (102,635 | ) | | | (0.8 | )% |

Intesa Sanpaolo SpA | | | (42,287 | ) | | | (100,293 | ) | | | (0.8 | )% |

Ryanair Holdings PLC | | | (8,711 | ) | | | (100,233 | ) | | | (0.8 | )% |

Sumitomo Chemical Co. Ltd. | | | 22,239 | | | | 99,801 | | | | 0.8 | % |

International Flavors & Fragrances | | | (794 | ) | | | (97,412 | ) | | | (0.8 | )% |

Kraft Heinz Co. (The) | | | (3,443 | ) | | | (96,184 | ) | | | (0.8 | )% |

Brookfield Property REIT, Inc. | | | 4,688 | | | | 95,581 | | | | 0.8 | % |

Worldline SA/France | | | (1,507 | ) | | | (95,101 | ) | | | (0.8 | )% |

Suzuki Motor Corp. | | | (2,195 | ) | | | (93,163 | ) | | | (0.7 | )% |

Continental Resources, Inc./OK | | | (3,018 | ) | | | (92,939 | ) | | | (0.7 | )% |

Aker BP ASA | | | (3,468 | ) | | | (92,905 | ) | | | (0.7 | )% |

Lundin Petroleum AB | | | (3,092 | ) | | | (92,871 | ) | | | (0.7 | )% |

Cimarex Energy Co. | | | (1,921 | ) | | | (92,071 | ) | | | (0.7 | )% |

Nektar Therapeutics | | | (4,923 | ) | | | (89,673 | ) | | | (0.7 | )% |

Murata Manufacturing Co. Ltd. | | | (1,859 | ) | | | (89,186 | ) | | | (0.7 | )% |

Delivery Hero SE | | | (2,000 | ) | | | (88,872 | ) | | | (0.7 | )% |

Varian Medical Systems, Inc. | | | 731 | | | | 87,003 | | | | 0.7 | % |

Fresnillo PLC | | | (100 | ) | | | (84,171 | ) | | | (0.7 | )% |

Credit Saison Co. Ltd. | | | 6,171 | | | | 82,734 | | | | 0.7 | % |

Keikyu Corp. | | | 4,262 | | | | 82,616 | | | | 0.7 | % |

NIKE, Inc. | | | (875 | ) | | | (82,169 | ) | | | (0.7 | )% |

Eurazeo SE | | | 1,100 | | | | 81,840 | | | | 0.7 | % |

Atmos Energy Corp. | | | (714 | ) | | | (81,296 | ) | | | (0.6 | )% |

Kikkoman Corp. | | | (1,696 | ) | | | (80,988 | ) | | | (0.6 | )% |

HollyFrontier Corp. | | | 1,509 | | | | 80,928 | | | | 0.6 | % |

Trend Micro, Inc./Japan | | | 1,694 | | | | 80,586 | | | | 0.6 | % |

Dollar Tree, Inc. | | | (705 | ) | | | (80,460 | ) | | | (0.6 | )% |

Acom Co. Ltd. | | | (20,503 | ) | | | (80,436 | ) | | | (0.6 | )% |

Other Long | | | 1,872,103 | | | | 22,332,683 | | | | 178.3 | % |

Other (Short) | | | (923,969 | ) | | | (18,408,487 | ) | | | (146.9 | )% |

| (5) | The following table represents the 50 largest (long/(short)) equity basket holdings underlying the total return swap in JPABSAA1 as of September 30, 2019. |

| | | | | | | | | | | | |

| Security Description | | Shares | | | Current Notional | | | Percent of

Basket’s Value | |

S&P 500 Total Return | | | (1,736 | ) | | $ | (10,431,010 | ) | | | (46.4 | )% |

MSCI Daily TR Gross EAFE | | | (803 | ) | | | (6,415,412 | ) | | | (28.5 | )% |

JPMorgan Cash Index | | | (17,966 | ) | | | (5,410,853 | ) | | | (24.1 | )% |

MSCI Daily TR Gross Canada | | | (84 | ) | | | (644,789 | ) | | | (2.9 | )% |

Roche Holding AG | | | 1,977 | | | | 575,965 | | | | 2.6 | % |

Fidelity National Financial, Inc. | | | 11,598 | | | | 515,058 | | | | 2.3 | % |

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 19 |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | | | | | |

| Security Description | | Shares | | | Current Notional | | | Percent of

Basket’s Value | |

Microsoft Corp. | | | 3,685 | | | $ | 512,279 | | | | 2.3 | % |

Nice Ltd. | | | 438,913 | | | | 438,913 | | | | 2.0 | % |

Apple, Inc. | | | 1,916 | | | | 429,217 | | | | 1.9 | % |

Merck & Co., Inc. | | | 5,087 | | | | 428,183 | | | | 1.9 | % |

Walmart, Inc. | | | 3,502 | | | | 415,630 | | | | 1.8 | % |

Dollar General Corp. | | | 2,522 | | | | 400,838 | | | | 1.8 | % |

Royal Dutch Shell PLC | | | 134 | | | | 395,502 | | | | 1.8 | % |

Automatic Data Processing, Inc. | | | 2,367 | | | | 382,046 | | | | 1.7 | % |

Ross Stores, Inc. | | | 3,412 | | | | 374,790 | | | | 1.7 | % |

Bank LeumiLe-Israel BM | | | 372,272 | | | | 372,272 | | | | 1.7 | % |

RELX PLC | | | 15,501 | | | | 368,907 | | | | 1.6 | % |

Oracle Corp. | | | 6,662 | | | | 366,592 | | | | 1.6 | % |

Oracle Corp. Japan | | | 4,196 | | | | 363,810 | | | | 1.6 | % |

Eli Lilly & Co. | | | 3,166 | | | | 354,071 | | | | 1.6 | % |

Paychex, Inc. | | | 4,138 | | | | 342,541 | | | | 1.5 | % |

Check Point Software Technology | | | 3,034 | | | | 332,268 | | | | 1.5 | % |

Nippon Building Fund, Inc. | | | 42 | | | | 322,624 | | | | 1.4 | % |

Comcast Corp. | | | 7,114 | | | | 320,692 | | | | 1.4 | % |

Toronto-Dominion Bank (The) | | | 5,343 | | | | 311,758 | | | | 1.4 | % |

adidas AG | | | 994 | | | | 309,588 | | | | 1.4 | % |

Procter & Gamble Co. (The) | | | 2,358 | | | | 293,326 | | | | 1.3 | % |

Salmar ASA | | | 6,622 | | | | 290,814 | | | | 1.3 | % |

AutoZone, Inc. | | | 260 | | | | 281,706 | | | | 1.3 | % |

Royal Bank of Canada | | | 3,468 | | | | 281,524 | | | | 1.3 | % |

Home Depot, Inc. (The) | | | 1,211 | | | | 281,085 | | | | 1.3 | % |

United Health Group, Inc. | | | 1,293 | | | | 281,037 | | | | 1.3 | % |

Enel SpA | | | 37,175 | | | | 277,656 | | | | 1.2 | % |

Wolters Kluwer NV | | | 3,791 | | | | 276,800 | | | | 1.2 | % |

Booz Allen Hamilton Holding Co. | | | 3,859 | | | | 274,033 | | | | 1.2 | % |

Aristocrat Leisure Ltd. | | | 13,193 | | | | 272,286 | | | | 1.2 | % |

Qantas Airways Ltd. | | | 63,644 | | | | 269,998 | | | | 1.2 | % |

L3Harris Technologies, Inc. | | | 1,263 | | | | 263,486 | | | | 1.2 | % |

Pfizer, Inc. | | | 7,126 | | | | 256,031 | | | | 1.1 | % |

Compass Group PLC | | | 99 | | | | 255,088 | | | | 1.1 | % |

CME Group, Inc. | | | 1,194 | | | | 252,414 | | | | 1.1 | % |

Nippon Telegraph & Telephone Co. | | | 5,276 | | | | 251,693 | | | | 1.1 | % |

Novo Nordisk A/S | | | 4,816 | | | | 247,619 | | | | 1.1 | % |

Bristol-Myers Squibb Co. | | | 4,871 | | | | 246,995 | | | | 1.1 | % |

HKT Trust & HKT Ltd. | | | 154,976 | | | | 245,925 | | | | 1.1 | % |

McDonald’s Corp. | | | 1,132 | | | | 243,061 | | | | 1.1 | % |

Visa, Inc. | | | 1,413 | | | | 243,032 | | | | 1.1 | % |

PNC Financial Services Group, Inc. | | | 1,733 | | | | 242,938 | | | | 1.1 | % |

Unilever PLC | | | 40 | | | | 239,089 | | | | 1.1 | % |

Merlin Properties Socimi SA | | | 17,097 | | | | 238,771 | | | | 1.1 | % |

Other Long | | | 125,228 | | | | 7,875,129 | | | | 35.0 | % |

| (6) | The following table represents the (long/(short)) basket holdings underlying the total return swap with MSCBRMF4 as of September 30, 2019. |

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

Euro-BTP Futures 12/19 | | $ | 5,080,086 | | | | 118.2 | % |

Euro-Schatz Futures 12/19 | | | 4,226,669 | | | | 98.3 | % |

| | |

| |

| 20 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED PORTFOLIO OF INVESTMENTS(continued)

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

U.S. 2 Yr Note (CBT) 12/19 | | $ | (3,678,935 | ) | | | (85.6 | )% |

Long Gilt Futures 12/19 | | | (2,811,761 | ) | | | (65.4 | )% |

U.S. 10 Yr Note (CBT) 12/19 | | | 2,513,817 | | | | 58.5 | % |

Euro-Bund Futures 12/19 | | | (2,304,870 | ) | | | (53.6 | )% |

Canada 10 Yr Bond Futures 12/19 | | | (2,258,867 | ) | | | (52.5 | )% |

Australia 10 Yr Bond Futures 12/19 | | | 1,422,218 | | | | 33.1 | % |

Euro-BOBL Futures 12/19 | | | 1,403,301 | | | | 32.6 | % |

Euro-OAT Futures 12/19 | | | (477,655 | ) | | | (11.1 | )% |

U.S. Long Bond (CBT) Futures 12/19 | | | 427,353 | | | | 9.9 | % |

U.S. 5 Yr Note (CBT) Futures 12/19 | | | 403,277 | | | | 9.4 | % |

Euro BUXL 30 Yr Bond Futures 12/19 | | | (104,474 | ) | | | (2.4 | )% |

| (7) | The following table represents the (long/(short)) basket holdings underlying the total return swap with MSUSABDM as of September 30, 2019. |

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

CAD/USD 10/31/19 | | $ | 3,881,661 | | | | 11.6 | % |

NZD/USD 10/31/19 | | | 3,504,185 | | | | 10.5 | % |

SEK/USD 10/31/19 | | | (2,281,562 | ) | | | (6.8 | )% |

CHF/USD 10/31/19 | | | (1,660,229 | ) | | | (5.0 | )% |

AUD/USD 10/31/19 | | | 1,499,885 | | | | 4.5 | % |

EUR/USD 10/31/19 | | | (744,932 | ) | | | (2.2 | )% |

JPY/USD 10/31/19 | | | 307,326 | | | | 0.9 | % |

NOK/USD 10/31/19 | | | (250,538 | ) | | | (0.8 | )% |

| (8) | The following table represents the (long/(short)) basket holdings underlying the total return swap with MSUSABEM as of September 30, 2019. |

| | | | | | | | |

| Security Description | | Current Notional | | | Percent of

Basket’s Value | |

CLP/USD 10/30/19 | | $ | (3,859,091 | ) | | | (10.4 | )% |

HUF/USD 10/31/19 | | | (3,117,671 | ) | | | (8.4 | )% |

RUB/USD 10/31/19 | | | 2,498,585 | | | | 6.7 | % |

MXN/USD 10/31/19 | | | 2,491,171 | | | | 6.7 | % |

BRL/USD 10/31/19 | | | (1,972,177 | ) | | | (5.3 | )% |

TWD/USD 10/31/19 | | | 1,875,793 | | | | 5.1 | % |

PHP/USD 10/31/19 | | | (1,868,378 | ) | | | (5.0 | )% |

PEN/USD 10/30/19 | | | (1,720,094 | ) | | | (4.6 | )% |

IDR/USD 10/31/19 | | | 1,653,367 | | | | 4.5 | % |

INR/USD 10/31/19 | | | 1,519,911 | | | | 4.1 | % |

CZK/USD 10/31/19 | | | 1,301,192 | | | | 3.5 | % |

KRW/USD 10/31/19 | | | (1,297,485 | ) | | | (3.5 | )% |

TRY/USD 10/31/19 | | | 1,075,059 | | | | 2.9 | % |

ZAR/USD 10/31/19 | | | 1,023,160 | | | | 2.8 | % |

CNY/USD 10/31/19 | | | 915,654 | | | | 2.5 | % |

THB/USD 10/31/19 | | | (344,760 | ) | | | (0.9 | )% |

COP/USD 10/31/19 | | | (211,305 | ) | | | (0.6 | )% |

PLN/USD 10/31/19 | | | 3,707 | | | | 0.0 | % |

See notes to consolidated financial statements.

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 21 |

CONSOLIDATED STATEMENT OF ASSETS & LIABILITIES

September 30, 2019(unaudited)

| | | | |

| Assets | |

Investments in unaffiliated Underlying Portfolios, at value (cost $846,712,821) | | $ | 961,231,777 | |

Investments in affiliated Underlying Portfolios, at value (cost $12,500,000) | | | 12,500,000 | |

Cash | | | 36,313,902 | |

Cash collateral due from broker | | | 14,560,000 | |

Foreign currencies, at value (cost $22,043) | | | 21,735 | |

Unrealized appreciation on total return swaps | | | 3,300,116 | |

Receivable for investments sold | | | 705,236 | |

Receivable for terminated total return swaps | | | 578,837 | |

Affiliated dividends receivable | | | 17,482 | |

| | | | |

Total assets | | | 1,029,229,085 | |

| | | | |

| Liabilities | |

Payable for shares of beneficial interest redeemed | | | 36,919,610 | |

Subscriptions received in advance | | | 4,530,000 | |

Unrealized depreciation on total return swaps | | | 3,066,013 | |

Payable for terminated total return swaps | | | 1,174,500 | |

Management fee payable | | | 852,792 | |

Administrative fee payable | | | 180,650 | |

Transfer Agent fee payable | | | 30,073 | |

Trustees’ fees payable | | | 1,800 | |

Accrued expenses | | | 393,410 | |

| | | | |

Total liabilities | | | 47,148,848 | |

| | | | |

Net Assets | | $ | 982,080,237 | |

| | | | |

| Composition of Net Assets | |

Shares of beneficial interest, at par | | $ | 86,564 | |

Additionalpaid-in capital | | | 940,539,382 | |

Distributable earnings | | | 41,454,291 | |

| | | | |

Net Assets | | $ | 982,080,237 | |

| | | | |

Shares of beneficial interest outstanding—unlimited shares authorized, with par value of $.001 (based on 86,564,054 shares outstanding) | | $ | 11.35 | |

| | | | |

See notes to consolidated financial statements.

| | |

| |

| 22 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED STATEMENT OF OPERATIONS

Six Months Ended September 30, 2019(unaudited)

| | | | | | | | |

| Investment Income | | | | | | | | |

Dividends—Affiliated issuers | | | | | | $ | 341,850 | |

| | | | | | | | |

| Expenses | | | | | | | | |

Management fee (see Note B) | | $ | 5,193,801 | | | | | |

Custodian | | | 237,784 | | | | | |

Administrative | | | 169,137 | | | | | |

Credit facility fees | | | 127,083 | | | | | |

Transfer agency | | | 109,876 | | | | | |

Audit and tax | | | 59,212 | | | | | |

Legal | | | 55,394 | | | | | |

Registration fees | | | 42,070 | | | | | |

Trustees’ fees | | | 17,186 | | | | | |

Printing | | | 16,078 | | | | | |

Amortization of offering expenses | | | 14,033 | | | | | |

Miscellaneous | | | 48,577 | | | | | |

| | | | | | | | |

Total expenses before interest expense | | | 6,090,231 | | | | | |

Interest expense | | | 11,441 | | | | | |

| | | | | | | | |

Total expenses | | | 6,101,672 | | | | | |

Less: expenses waived and reimbursed by the Investment Manager (see Note B) | | | (14,762 | ) | | | | |

| | | | | | | | |

Net expenses | | | | | | | 6,086,910 | |

| | | | | | | | |

Net investment loss | | | | | | | (5,745,060 | ) |

| | | | | | | | |

| Realized and Unrealized Gain (Loss) on Investment and Foreign Currency Transactions | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | |

Investment transactions | | | | | | | 30,646,057 | |

Forward currency exchange contracts | | | | | | | 74,724 | |

Swaps | | | | | | | (675,402 | ) |

Foreign currency transactions | | | | | | | 10,158 | |

Net change in unrealized appreciation/depreciation of: | | | | | | | | |

Investments | | | | | | | (15,694,925 | ) |

Forward currency exchange contracts | | | | | | | 29,748 | |

Swaps | | | | | | | (739,358 | ) |

Foreign currency denominated assets and liabilities | | | | | | | 21,466 | |

| | | | | | | | |

Net gain on investment and foreign currency transactions | | | | | | | 13,672,468 | |

| | | | | | | | |

Contributions from Affiliates (see Note B) | | | | | | | 1,871 | |

| | | | | | | | |

Net Increase in Net Assets from Operations | | | | | | $ | 7,929,279 | |

| | | | | | | | |

See notes to consolidated financial statements.

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 23 |

CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS

| | | | | | | | |

| | | Six Months Ended

September 30, 2019

(unaudited) | | | Year Ended

March 31,

2019 | |

| Increase (Decrease) in Net Assets from Operations | | | | | | | | |

Net investment loss | | $ | (5,745,060 | ) | | $ | (13,006,387 | ) |

Net realized gain on investment transactions | | | 30,055,537 | | | | 59,748,305 | |

Net change in unrealized appreciation/depreciation of investments and foreign currency denominated assets and liabilities | | | (16,383,069 | ) | | | (40,578,976 | ) |

Contributions from Affiliates (see Note B) | | | 1,871 | | | | – 0 | – |

| | | | | | | | |

Net increase in net assets from operations | | | 7,929,279 | | | | 6,162,942 | |

| Transactions in Shares of Beneficial Interest | | | | | | | | |

Net decrease (see Note D) | | | (65,434,918 | ) | | | (121,636,894 | ) |

| | | | | | | | |

Total decrease | | | (57,505,639 | ) | | | (115,473,952 | ) |

| Net Assets | | | | | | | | |

Beginning of period | | | 1,039,585,876 | | | | 1,155,059,828 | |

| | | | | | | | |

End of period | | $ | 982,080,237 | | | $ | 1,039,585,876 | |

| | | | | | | | |

See notes to consolidated financial statements.

| | |

| |

| 24 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

CONSOLIDATED STATEMENT OF CASH FLOWS

For the six months ended September 30, 2019(unaudited)

| | | | | | | | |

| Cash flows from operating activities | | | | | | | | |

Net increase in net assets from operations | | | | | | $ | 7,929,279 | |

| Reconciliation of net increase in net assets from operations to net increase in cash from operating activities | | | | | | | | |

Purchases of Underlying Portfolio shares | | $ | (100,393,238 | ) | | | | |

Purchases of short-term investments | | | (150,398,640 | ) | | | | |

Sales of Underlying Portfolio shares | | | 161,672,846 | | | | | |

Proceeds from disposition of short-term investments | | | 153,465,270 | | | | | |

Net realized gain on investment transactions and foreign currency transactions | | | (30,055,537 | ) | | | | |

Net realized gain on forward currency exchange contracts | | | 74,724 | | | | | |

Net change in unrealized appreciation/depreciation of investments and foreign currency denominated assets and liabilities | | | 16,383,069 | | | | | |

Decrease in deferred offering cost | | | 14,033 | | | | | |

Decrease in receivable for investments sold | | | 5,934,902 | | | | | |

Decrease in affiliated dividends receivable | | | 11,505 | | | | | |

Increase in cash collateral due from broker | | | (1,880,000 | ) | | | | |

Decrease in investments in Underlying Portfolios received in advance | | | (120,000 | ) | | | | |

Decrease in management fee payable | | | (35,400 | ) | | | | |

Decrease in administrative fee payable | | | (4,704 | ) | | | | |

Increase in Transfer Agent fee payable | | | 5,285 | | | | | |

Increase in Trustees’ fee payable | | | 1,800 | | | | | |

Decrease in accrued expenses | | | (71,739 | ) | | | | |

Proceeds on swaps, net | | | 1,231,889 | | | | | |

| | | | | | | | |

Total adjustments | | | | | | | 55,836,065 | |

| | | | | | | | |

Net cash provided by (used in) operating activities | | | | | | | 63,765,344 | |

| Cash flows from financing activities | | | | | | | | |

Subscriptions, including change in subscriptions received in advance | | | 24,203,039 | | | | | |

Redemptions, net of payable for shares of beneficial interest redeemed | | | (91,777,276 | ) | | | | |

| | | | | | | | |

Net cash provided by (used in) financing activities | | | | | | | (67,574,237 | ) |

Effect of exchange rate on cash | | | | | | | 31,624 | |

| | | | | | | | |

Net decrease in cash | | | | | | | (3,777,269 | ) |

Cash at beginning of period | | | | | | | 40,112,906 | |

| | | | | | | | |

Cash at end of period | | | | | | $ | 36,335,637 | |

| | | | | | | | |

| Supplemental disclosure of cash flow information | | | | | | | | |

Interest expense paid during the period | | $ | 11,441 | | | | | |

See notes to consolidated financial statements.

| | |

| |

| abfunds.com | | AB MULTI-MANAGER ALTERNATIVE FUND | 25 |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2019(unaudited)

NOTE A

Significant Accounting Policies

AB Multi-Manager Alternative Fund (the “Fund”) is a statutory trust formed under the laws of the State of Delaware and registered under the Investment Company Act of 1940 as a diversified,closed-end management investment company. The Fund commenced operations on October 1, 2012. The Fund’s investment objective is to seek long-term capital appreciation. There can be no assurance that the Fund will achieve its investment objective, be able to structure its investments as anticipated, or that its returns will be positive over any period of time. The Fund is not intended as a complete investment program for investors. The Fund seeks to achieve its investment objective primarily by allocating its assets among investments in private investment vehicles (“Underlying Portfolios”), commonly referred to as hedge funds, that are managed by unaffiliated asset managers that employ a broad range of investment strategies. As a secondary strategy, the Fund will generally also make direct investments in securities and other financial instruments. As part of the Fund’s investment strategy, the Fund seeks exposure to commodities and commodities-related instruments and derivatives primarily through investments in AB Multi-Manager Alternative Fund (Cayman), Ltd., a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). The Subsidiary commenced operations on September 21, 2018. The Fund is the sole shareholder of the Subsidiary and it is intended that the Fund will remain the sole shareholder and will continue to control the Subsidiary. Under the Articles of Association of the Subsidiary, shares issued by the Subsidiary confer upon a shareholder the right to receive notice of, to attend and to vote at general meetings of the Subsidiary and shall confer upon the shareholder rights in awinding-up or repayment of capital and the right to participate in the profits or assets of the Subsidiary. As of September 30, 2019, net assets of the Fund were $982,080,237, of which $10,869,527, or approximately 1%, represented the Fund’s ownership of all issued shares and voting rights of the Subsidiary. This report presents the consolidated financial statements of the Fund and the Subsidiary. All intercompany transactions and balances have been eliminated in consolidation. The consolidated financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the consolidated financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates. The Fund is an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies. The following is a summary of significant accounting policies followed by the Fund.

| | |

| |

| 26 | AB MULTI-MANAGER ALTERNATIVE FUND | | abfunds.com |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS(continued)

1. Valuation of Investments

The Fund’s Board of Trustees (the “Board”) has approved pricing and valuation policies and procedures pursuant to which the Fund’s investments in Underlying Portfolios are valued at fair value (the “Valuation Procedures”). Among other matters, the Valuation Procedures set forth the Fund’s valuation policies and the mechanisms and processes to be employed on a monthly basis to implement such policies. In accordance with the Valuation Procedures, fair value of an Underlying Portfolio as of each valuation time ordinarily is the value determined as of suchmonth-end for each Underlying Portfolio in accordance with the Underlying Portfolio’s valuation policies and reported at the time of the Fund’s valuation.