Washington, D.C. 20549

Frank L. Newbauer, Esq.

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

APEXcm SMALL/MID CAP GROWTH FUND

(APSGX)

Semi-Annual Report

November 30, 2013

(Unaudited)

APEXcm SMALL/MID CAP GROWTH FUND LETTER TO SHAREHOLDERS | |

Dear Fellow APEXcm Fund Shareholder,

We thank you for your support as the Fund has nearly tripled in net assets during the six months ended November 30, 2013. We were well positioned for a shift to a more growth-oriented environment with your Fund increasing 14.03% (net of expenses) during the six month period. Small/mid cap growth stocks continued to do well as the Russell 2500 Growth Index, the Fund’s benchmark index, rose 16.86%.

APEX PHILOSOPHY

We believe that the best way to provide value added returns is to identify companies, through our research driven process, that exhibit certain favorable fundamental advantages and benefit from secular growth trends allowing us to structure the portfolio in high conviction areas of longer term sustainable growth. Embedded in our portfolio construction is the recognition of companies at different stages of their growth cycle which we designate as “stable” and “emerging” growth stocks. We believe having the spectrum of growth companies that are really innovative and growing rapidly, combined with established growth businesses, can provide relative stability while allowing the opportunity to drive outperformance versus our benchmark and peers over time. Also, we believe the SMID style provides the opportunity to invest in higher growth companies and capture a longer period of growth as these companies mature.

INVESTMENT ENVIRONMENT

During this semi-annual period, investors became more optimistic about the global recovery led by the U.S. In spite of a continued challenging job market, the U.S. economy continues to recover at a moderate pace, led by pent up demand for housing, autos and airplanes. Europe continues to inch forward and Japan has shown strength under the adoption of Abenomics. During this short time period, we have gone from concerns about the Federal Reserve tapering its’ monetary stimulus program, a U.S. government shutdown, Syria violence and slowing growth in the emerging markets to more optimism about a self sustaining global recovery.

KEY PERFORMANCE DRIVERS VERSUS THE BENCHMARK

| | • | Solid stock selection in the Energy, Financials, Health Care, Industrials and Materials sectors added approximately 200 basis points in value. |

| | • | Overall stock selection was negative as Consumer Discretionary and Information Technology sector holdings underperformed by approximately 300 basis points. |

| | • | Overall attribution from sector effect was slightly negative (approximately 30 basis points) due mostly to the underweights in Health Care and Consumer Staples. |

| | • | Additionally, the timing of significant cash inflows into the Fund as the market continued its relentless advance negatively impacted performance. |

KEY POSITIONING AND HOLDINGS DISCUSSION VERSUS THE BENCHMARK

Information Technology: We remain overweight in Information Technology due to attractive valuations with sustainable growth and cash flow characteristics. Several businesses in the payment and processing area performed very well with Alliance Data Systems (+19.21%), FleetCor (+22.25%), Heartland Payment Systems(+22.98%), and Total System Services (+15.50%) all performed admirably. In spite of the success of the holdings in the secular growth payments and processing companies, as mentioned, stock selection overall in Information Technology trailed the benchmark index due mostly to MercadoLibre (-20.77%), Rovi (-46.28%), SolarWinds (-38.26%-sold in November), Akamai (-20.63%-sold in November) and Ixia (-34.96%).

Consumer Discretionary: We remain overweight in Consumer Discretionary as there are several elements of the economy with significant pent up demand. Housing and the corresponding multiplier of durables as well as automotives (we added Dana Holding and Visteon during this semi-annual period) should continue to benefit from resurgence in demand. As mentioned, a few of our holdings had a negative impact on our performance during this time period, most notably International Game Technology (-18.33%), Panera Bread (-24.82%-sold in September), and Dana Holding (-9.31%).

Health Care: Although underweight in Health Care, we continue to add positions to take advantage of key growth areas of biotechnology, specialty pharmas and diagnostic equipment providers. During the semi-annual period, we added Salix Pharmaceuticals with its strong franchise in treating intestinal disorders, along with Jazz Pharmaceuticals providing strong growth with Xyrem, a drug for narcolepsy. During the period, Jazz Pharmaceuticals was up (+48.55%), Incyte (+86.73%) with these gains offset by PAREXEL International being down (-33.25%).

Financials: We remain overweight in Financials, although we did sell Hertz during this six month period. In our view, the steep yield curve, better credit standards and declining delinquencies support this attractively valued sector. Stock selection was excellent with First Republic (+28.83%) and Evercore Partners (+30.02%) leading the way.

Industrials: Although still slightly underweight in Industrials, we continue to selectively add to the Fund’s allocation to Industrials as many companies, especially in aerospace, show good long term secular growth prospects. During the semi-annual period we added B/E Aerospace, a key supplier to new and existing airplanes. Towers Watson, a beneficiary of the roll out of the Affordable Care Act, was up (+22.77%) during this time period.

OUTLOOK

The U.S. economy seems to be gaining momentum boosted by stronger corporate profits and hiring continuing at a steady pace. The U.S. consumer, even in the face of budget turmoil in Washington that temporarily darkened their mood, is showing signs of increasing confidence. We expect the Federal Reserve (the “Fed”) to gradually taper its monthly bond-buying program, allowing interest rates to edge higher. We believe this is the first acknowledgement of a more sustainable recovery, which should benefit quality businesses which grow on the basis of corporate fundamentals instead of the incredible influence of the Fed. An economy that is reaccelerating, accompanied by low inflation, should encourage more capital spending and business investment as well as accelerated hiring as an uptick in demand occurs. We do believe there will be added volatility as the tug of war between the timing of the unwinding of the historic stimulus measures and the healthier cycle of higher consumer and business spending unfolds. We believe this should provide a sense of more normality to the markets and return expectations. Valuations are still reasonable in our opinion and no one can be certain of relative growth trajectories, but we continue to find opportunities and are encouraged by secular growth areas such as the U.S. manufacturing renaissance, U.S. energy independence, personalized medicine, pent up demand in housing and autos and many other substantial long-term sustainable trends.

Thank you for your confidence in the APEXcm Small/Mid Cap Growth Fund.

Sincerely,

Nitin N. Kumbhani

President and Chief Investment Officer

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-888-575-4800.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit our website at www.apexcmfund.com or call 1-888-575-4800 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The APEXcm Small/Mid Cap Growth Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. The opinions of the Fund’s Adviser with respect to those securities may change at any time.

APEXcm SMALL/MID CAP GROWTH FUND

PORTFOLIO INFORMATION

November 30, 2013 (Unaudited)

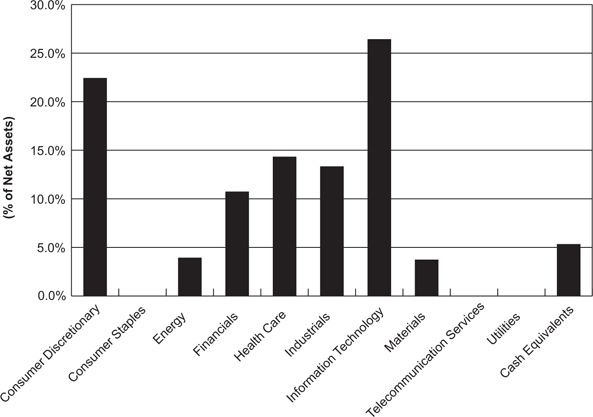

Sector Diversification

| | |

| Illumina, Inc. | | 3.2% |

| Alliance Data Systems Corp. | | 2.4% |

| Signet Jewelers Ltd. | | 2.4% |

| United Rentals, Inc. | | 2.2% |

| Expedia, Inc. | | 2.2% |

| FleetCor Technologies, Inc. | | 2.2% |

| Polaris Industries, Inc. | | 2.1% |

| IAC/InterActiveCorp | | 2.0% |

| MercadoLibre, Inc. | | 2.0% |

| Autoliv, Inc. | | 2.0% |

APEXcm SMALL/MID CAP GROWTH FUND SCHEDULE OF INVESTMENTS November 30, 2013 (Unaudited) | |

| | | | | | |

| Consumer Discretionary — 22.4% | | | | | | |

| Auto Components — 5.6% | | | | | | |

| Autoliv, Inc. | | | 10,531 | | | $ | 977,909 | |

| Dana Holding Corp. | | | 25,761 | | | | 522,433 | |

| Gentex Corp. | | | 16,388 | | | | 488,526 | |

| Visteon Corp. * | | | 9,746 | | | | 766,425 | |

| | | | | | | | 2,755,293 | |

| Hotels, Restaurants & Leisure — 2.7% | | | | | | | | |

| International Game Technology | | | 35,015 | | | | 612,412 | |

| Wyndham Worldwide Corp. | | | 10,320 | | | | 740,047 | |

| | | | | | | | 1,352,459 | |

| Internet & Catalog Retail — 2.2% | | | | | | | | |

| Expedia, Inc. | | | 17,168 | | | | 1,093,430 | |

| | | | | | | | | |

| Leisure Equipment & Products — 2.1% | | | | | | | | |

| Polaris Industries, Inc. | | | 7,624 | | | | 1,017,575 | |

| | | | | | | | | |

| Multi-line Retail — 0.9% | | | | | | | | |

| Dillard's, Inc. | | | 4,673 | | | | 427,579 | |

| | | | | | | | | |

| Specialty Retail — 8.9% | | | | | | | | |

| AutoNation, Inc. * | | | 12,812 | | | | 628,300 | |

| GNC Holdings, Inc. - Class A | | | 10,578 | | | | 636,584 | |

| PetSmart, Inc. | | | 12,561 | | | | 930,896 | |

| Sally Beauty Holdings, Inc. * | | | 9,242 | | | | 260,070 | |

| Signet Jewelers Ltd. | | | 15,492 | | | | 1,190,405 | |

| Williams-Sonoma, Inc. | | | 13,251 | | | | 783,399 | |

| | | | | | | | 4,429,654 | |

| Energy — 3.9% | | | | | | | | |

| Energy Equipment & Services — 1.2% | | | | | | | | |

| Helmerich & Payne, Inc. | | | 8,106 | | | | 624,162 | |

| | | | | | | | | |

| Oil, Gas & Consumable Fuels — 2.7% | | | | | | | | |

| Carrizo Oil & Gas, Inc. * | | | 14,871 | | | | 601,383 | |

| Whiting Petroleum Corp. * | | | 11,937 | | | | 720,995 | |

| | | | | | | | 1,322,378 | |

| Financials — 10.7% | | | | | | | | |

| Capital Markets — 3.6% | | | | | | | | |

| Affiliated Managers Group, Inc. * | | | 3,948 | | | | 790,587 | |

| Evercore Partners, Inc. - Class A | | | 9,712 | | | | 532,703 | |

APEXcm SMALL/MID CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 94.7% (Continued) | | | | | | |

| Financials — 10.7% (Continued) | | | | | | |

| Capital Markets — 3.6% (Continued) | | | | | | |

| Janus Capital Group, Inc. | | | 39,605 | | | $ | 430,902 | |

| | | | | | | | 1,754,192 | |

| Commercial Banks — 2.9% | | | | | | | | |

| Cullen/Frost Bankers, Inc. | | | 8,495 | | | | 610,111 | |

| First Republic Bank/CA | | | 16,432 | | | | 839,675 | |

| | | | | | | | 1,449,786 | |

| Diversified Financial Services — 1.0% | | | | | | | | |

| Interactive Brokers Group, Inc. | | | 10,245 | | | | 248,441 | |

| MarketAxess Holdings, Inc. | | | 3,545 | | | | 249,462 | |

| | | | | | | | 497,903 | |

| Insurance — 1.5% | | | | | | | | |

| XL Group plc | | | 23,443 | | | | 749,942 | |

| | | | | | | | | |

| Real Estate Management & Development — 1.7% | | | | | | | | |

| CBRE Group, Inc. * | | | 34,256 | | | | 830,365 | |

| | | | | | | | | |

| Health Care — 14.3% | | | | | | | | |

| Biotechnology — 2.8% | | | | | | | | |

| Genomic Health, Inc. * | | | 9,038 | | | | 317,957 | |

| Incyte Corp. * | | | 10,800 | | | | 503,280 | |

| United Therapeutics Corp. * | | | 6,173 | | | | 569,830 | |

| | | | | | | | 1,391,067 | |

| Health Care Providers & Services — 2.5% | | | | | | | | |

| Hanger, Inc. * | | | 6,464 | | | | 251,062 | |

| Universal Health Services, Inc. - Class B | | | 11,860 | | | | 977,620 | |

| | | | | | | | 1,228,682 | |

| Life Sciences Tools & Services — 5.8% | | | | | | | | |

| Illumina, Inc. * | | | 16,332 | | | | 1,600,536 | |

| PAREXEL International Corp. * | | | 18,471 | | | | 761,375 | |

| WuXi PharmaTech (Cayman), Inc.* | | | 15,604 | | | | 516,961 | |

| | | | | | | | 2,878,872 | |

| Pharmaceuticals — 3.2% | | | | | | | | |

| Akorn, Inc. * | | | 13,307 | | | | 342,655 | |

| Jazz Phamarceuticals plc * | | | 5,870 | | | | 686,320 | |

| Salix Pharmaceuticals Ltd. * | | | 6,301 | | | | 534,388 | |

| | | | | | | | 1,563,363 | |

| Industrials — 13.3% | | | | | | | | |

| Aerospace & Defense — 1.5% | | | | | | | | |

| B/E Aerospace, Inc. * | | | 8,352 | | | | 726,624 | |

APEXcm SMALL/MID CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 94.7% (Continued) | | | | | | |

| Industrials — 13.3% (Continued) | | | | | | |

| Electrical Equipment — 1.0% | | | | | | |

| EnerSys, Inc. | | | 7,225 | | | $ | 515,504 | |

| | | | | | | | | |

| Machinery — 4.5% | | | | | | | | |

| Nordson Corp. | | | 8,975 | | | | 647,277 | |

| Valmont Industries, Inc. | | | 4,322 | | | | 625,437 | |

| Wabtec Corp. | | | 13,856 | | | | 956,064 | |

| | | | | | | | 2,228,778 | |

| Professional Services — 3.1% | | | | | | | | |

| Robert Half International, Inc. | | | 16,674 | | | | 644,117 | |

| Towers Watson & Co. | | | 7,859 | | | | 884,923 | |

| | | | | | | | 1,529,040 | |

| Road & Rail — 1.0% | | | | | | | | |

| Old Dominion Freight Line, Inc. * | | | 9,371 | | | | 482,888 | |

| | | | | | | | | |

| Trading Companies & Distributors — 2.2% | | | | | | | | |

| United Rentals, Inc. * | | | 16,119 | | | | 1,107,859 | |

| | | | | | | | | |

| Information Technology — 26.4% | | | | | | | | |

| Communications Equipment — 0.7% | | | | | | | | |

| Ixia * | | | 25,640 | | | | 333,064 | |

| | | | | | | | | |

| Electronic Equipment, Instruments & Components — 2.3% | | | | | | | | |

| Dolby Laboratories, Inc. - Class A | | | 13,343 | | | | 479,414 | |

| FEI Co. | | | 7,166 | | | | 652,464 | |

| | | | | | | | 1,131,878 | |

| Internet Software & Services — 6.4% | | | | | | | | |

| AOL, Inc. * | | | 16,340 | | | | 728,437 | |

| IAC/InterActiveCorp | | | 17,616 | | | | 1,007,811 | |

| MercadoLibre, Inc. | | | 9,099 | | | | 1,007,350 | |

| Rackspace Hosting, Inc. * | | | 10,467 | | | | 399,944 | |

| | | | | | | | 3,143,542 | |

| IT Services — 11.1% | | | | | | | | |

| Alliance Data Systems Corp. * | | | 4,978 | | | | 1,205,970 | |

| FleetCor Technologies, Inc. * | | | 8,748 | | | | 1,065,331 | |

| Gartner, Inc. * | | | 13,375 | | | | 864,694 | |

| Heartland Payment Systems, Inc. | | | 14,486 | | | | 650,566 | |

| InterXion Holding N.V.* | | | 12,251 | | | | 275,770 | |

| NeuStar, Inc.* - Class A | | | 9,990 | | | | 487,013 | |

| Total System Services, Inc. | | | 30,995 | | | | 962,395 | |

| | | | | | | | 5,511,739 | |

APEXcm SMALL/MID CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 94.7% (Continued) | | | | | | |

| Information Technology — 26.4% (Continued) | | | | | | |

| Semiconductors & Semiconductor Equipment — 2.4% | | | | | | |

| Entegris, Inc. * | | | 40,659 | | | $ | 446,436 | |

| NXP Semiconductors N.V. * | | | 17,691 | | | | 751,868 | |

| | | | | | | | 1,198,304 | |

| Software — 3.5% | | | | | | | | |

| Informatica Corp. * | | | 11,825 | | | | 458,928 | |

| Manhattan Associates, Inc. * | | | 2,216 | | | | 266,496 | |

| Rovi Corp. * | | | 17,939 | | | | 330,078 | |

| TIBCO Software, Inc. * | | | 28,164 | | | | 680,724 | |

| | | | | | | | 1,736,226 | |

| Materials — 3.7% | | | | | | | | |

| Chemicals — 1.1% | | | | | | | | |

| Albemarle Corp. | | | 7,551 | | | | 518,829 | |

| | | | | | | | | |

| Containers & Packaging — 1.3% | | | | | | | | |

| Silgan Holdings, Inc. | | | 13,701 | | | | 640,522 | |

| | | | | | | | | |

| Paper & Forest Products — 1.3% | | | | | | | | |

| KapStone Paper and Packaging Corp. | | | 12,520 | | | | 667,066 | |

| | | | | | | | | |

Total Common Stocks (Cost $41,045,205) | | | | | | $ | 46,838,565 | |

| | |

MONEY MARKET FUNDS — 5.8% | | | | | | |

Fidelity Institutional Money Market Portfolio - Class I, 0.05% (a) (Cost $2,889,471) | | | 2,889,471 | | | $ | 2,889,471 | |

| | | | | | | | | |

Total Investments at Value — 100.5% (Cost $43,934,676) | | | | | | $ | 49,728,036 | |

| | | | | | | | | |

| Liabilities in Excess of Other Assets — (0.5%) | | | | | | | (269,104 | ) |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 49,458,932 | |

| * | Non-income producing security. |

| (a) | The rate shown is the 7-day effective yield as of November 30, 2013. |

| See accompanying notes to financial statements. |

APEXcm SMALL/MID CAP GROWTH FUND STATEMENT OF ASSETS AND LIABILITIES November 30, 2013 (Unaudited) | |

ASSETS | | | |

| Investments in securities: | | | |

| At acquisition cost | | $ | 43,934,676 | |

| At value (Note 2) | | $ | 49,728,036 | |

| Dividends receivable | | | 38,168 | |

| Receivable for capital shares sold | | | 1,782 | |

| Receivable for investment securities sold | | | 1,007,287 | |

| Other assets | | | 22,248 | |

| Total assets | | | 50,797,521 | |

| | | | | |

| LIABILITIES | | | | |

| Payable for investment securities purchased | | | 1,297,313 | |

| Payable to Adviser (Note 4) | | | 20,881 | |

| Payable to administrator (Note 4) | | | 9,020 | |

| Other accrued expenses | | | 11,375 | |

| Total liabilities | | | 1,338,589 | |

| | | | | |

| NET ASSETS | | $ | 49,458,932 | |

| | | | | |

| NET ASSETS CONSIST OF: | | | | |

| Paid-in capital | | $ | 43,418,068 | |

| Accumulated net investment loss | | | (71,320 | ) |

| Accumulated net realized gains from security transactions | | | 318,824 | |

| Net unrealized appreciation on investments | | | 5,793,360 | |

| NET ASSETS | | $ | 49,458,932 | |

| | | | | |

Shares of beneficial interest outstanding

(unlimited number of shares authorized, no par value) | | | 3,419,125 | |

| | | | | |

Net asset value, offering price and redemption price per share

(Note 2) | | $ | 14.47 | |

| See accompanying notes to financial statements. |

APEXcm SMALL/MID CAP GROWTH FUND STATEMENT OF OPERATIONS For the Six Months Ended November 30, 2013 (Unaudited) | |

INVESTMENT INCOME | | | |

| Dividend income | | $ | 101,159 | |

| | | | | |

| EXPENSES | | | | |

| Investment advisory fees (Note 4) | | | 155,088 | |

| Custody and bank service fees | | | 18,866 | |

| Administration fees (Note 4) | | | 17,411 | |

| Professional fees | | | 16,286 | |

| Fund accounting fees (Note 4) | | | 14,806 | |

| Registration and filing fees | | | 13,998 | |

| Transfer agent fees (Note 4) | | | 9,000 | |

| Compliance fees (Note 4) | | | 6,000 | |

| Trustees' fees and expenses (Note 4) | | | 4,451 | |

| Postage and supplies | | | 2,684 | |

| Insurance expense | | | 2,030 | |

| Other expenses | | | 5,853 | |

| Total expenses | | | 266,473 | |

| Less fee reductions by the Adviser (Note 4) | | | (103,631 | ) |

| Net expenses | | | 162,842 | |

| | | | | |

| NET INVESTMENT LOSS | | | (61,683 | ) |

| | | | | |

| REALIZED AND UNREALIZED GAINS ON INVESTMENTS | | | | |

| Net realized gains from security transactions | | | 352,268 | |

Net change in unrealized appreciation/

depreciation on investments | | | 4,730,390 | |

| NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | | | 5,082,658 | |

| | | | | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 5,020,975 | |

| See accompanying notes to financial statements. |

APEXcm SMALL/MID CAP GROWTH FUND STATEMENTS OF CHANGES IN NET ASSETS | |

| | Six Months Ended November 30, 2013 (Unaudited) | | | Period Ended May 31, 2013(a) | |

| FROM OPERATIONS | | | | | | |

| Net investment income (loss) | | $ | (61,683 | ) | | $ | 9,832 | |

Net realized gains (losses)

from security transactions | | | 352,268 | | | | (33,444 | ) |

Net change in unrealized appreciation/

depreciation on investments | | | 4,730,390 | | | | 1,062,970 | |

| Net increase in net assets resulting from operations | | | 5,020,975 | | | | 1,039,358 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| From net investment income | | | — | | | | (19,469 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Proceeds from shares sold | | | 32,293,006 | | | | 12,444,893 | |

Net asset value of shares issued in reinvestment of

distributions to shareholders | | | — | | | | 19,469 | |

| Payments for shares redeemed | | | (1,008,028 | ) | | | (431,272 | ) |

Net increase in net assets from

capital share transactions | | | 31,284,978 | | | | 12,033,090 | |

| | | | | | | | | |

| TOTAL INCREASE IN NET ASSETS | | | 36,305,953 | | | | 13,052,979 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of period | | | 13,152,979 | | | | 100,000 | |

| End of period | | $ | 49,458,932 | | | $ | 13,152,979 | |

| | | | | | | | | |

| ACCUMULATED NET INVESTMENT LOSS | | $ | (71,320 | ) | | $ | (9,637 | ) |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

| Shares sold | | | 2,456,381 | | | | 1,060,310 | |

| Shares reinvested | | | — | | | | 1,764 | |

| Shares redeemed | | | (73,963 | ) | | | (35,367 | ) |

| Net increase in shares outstanding | | | 2,382,418 | | | | 1,026,707 | |

| Shares outstanding at beginning of period | | | 1,036,707 | | | | 10,000 | |

| Shares outstanding at end of period | | | 3,419,125 | | | | 1,036,707 | |

| (a) | Represents the period from the commencement of operations (June 29, 2012) through May 31, 2013. |

| See accompanying notes to financial statements. |

APEXcm SMALL/MID CAP GROWTH FUND FINANCIAL HIGHLIGHTS | |

Per Share Data for a Share Outstanding Throughout each Period | |

| | Six Months Ended November 30, 2013 (Unaudited) | | | Period Ended May 31, 2013(a) | |

| Net asset value at beginning of period | | $ | 12.69 | | | $ | 10.00 | |

| | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | |

| Net investment income (loss) | | | (0.01 | ) | | | 0.04 | (b) |

| Net realized and unrealized gains on investments | | | 1.79 | | | | 2.72 | |

| Total from investment operations | | | 1.78 | | | | 2.76 | |

| | | | | | | | | |

| Less distributions: | | | | | | | | |

| From net investment income | | | — | | | | (0.07 | ) |

| | | | | | | | | |

| Net asset value at end of period | | $ | 14.47 | | | $ | 12.69 | |

| | | | | | | | | |

Total return (c) | | | 14.03% | (d) | | | 27.65% | (d) |

| | | | | | | | | |

| Net assets at end of period (000's) | | $ | 49,459 | | | $ | 13,153 | |

| | | | | | | | | |

| Ratios/supplementary data: | | | | | | | | |

| Ratio of total expenses to average net assets | | | 1.71% | (e) | | | 4.87% | (e) |

| | | | | | | | | |

Ratio of net expenses to average net assets (f) | | | 1.05% | \(e) | | | 1.05% | (e) |

| | | | | | | | | |

Ratio of net investment income (loss)

to average net assets (f) | | | (0.40% | )(e) | | | 0.26% | (e) |

| | | | | | | | | |

| Portfolio turnover rate | | | 23% | (d) | | | 18% | (d) |

| (a) | Represents the period from the commencement of operations (June 29, 2012) through May 31, 2013. |

| (b) | Calculated using weighted average shares outstanding during the period. |

| (c) | Total return is a measure of the change in value of an investment in the Fund over the period covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses. |

| (d) | Not annualized. |

| (e) | Annualized. |

| (f) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

| See accompanying notes to financial statements. |

APEXcm SMALL/MID CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS

November 30, 2013 (Unaudited)

1. Organization

APEXcm Small/Mid Cap Growth Fund (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report. The Fund commenced operations on June 29, 2012.

The investment objective of the Fund is long-term capital growth.

2. Significant Accounting Policies

The following is a summary of the Fund’s significant accounting policies. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

Securities valuation – The Fund’s portfolio securities are valued at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open. Securities listed on the NYSE or other exchanges are valued on the basis of their last sales prices on the exchanges on which they are primarily traded. If there are no sales on that day, the securities are valued at the closing bid price on the NYSE or other primary exchange for that day. NASDAQ listed securities are valued at the NASDAQ Official Closing Price. If there are no sales on that day, the securities are valued at the last bid price as reported by NASDAQ. Securities traded in the over-the-counter market are valued at the last sale price, if available, otherwise at the most recently quoted bid price. In the event that market quotations are not readily available or are considered unreliable due to market or other events, securities and other assets are valued at fair value as determined in good faith in accordance with procedures adopted by the Board of Trustees of the Trust and will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Factors determining portfolio investments subject to fair value determination include, but are not limited to, the following: the spread between bid and asked prices is substantial; infrequency of sales; thinness of market; the size of reported trades; a temporary lapse in the provision of prices by any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. Securities with remaining maturities of 60 days or less are valued at amortized cost value, absent unusual circumstances.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements.

APEXcm SMALL/MID CAP GROWTH FUND NOTES TO FINANCIAL STATEMENTS (Continued) |

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

| • | Level 1 – quoted prices in active markets for identical securities |

| • | Level 2 – other significant observable inputs |

| • | Level 3 – significant unobservable inputs |

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments as of November 30, 2013:

| | | | | | | | | | | | |

| Common Stocks | | $ | 46,838,565 | | | $ | — | | | $ | — | | | $ | 46,838,565 | |

| Money Market Funds | | | 2,889,471 | | | | — | | | | — | | | | 2,889,471 | |

| Total | | $ | 49,728,036 | | | $ | — | | | $ | — | | | $ | 49,728,036 | |

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by industry type. As of November 30, 2013, the Fund did not have any transfers in and out of any Level. In addition, the Fund did not have derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of November 30, 2013. It is the Fund’s policy to recognize transfers into and out of any Level at the end of the reporting period.

Share valuation – The net asset value per share of the Fund is calculated daily by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of the Fund is equal to the net asset value per share.

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned.

Security transactions – Security transactions are accounted for on the trade date. Gains and losses on securities sold are determined on a specific identification basis.

APEXcm SMALL/MID CAP GROWTH FUND NOTES TO FINANCIAL STATEMENTS (Continued) |

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders – Distributions to shareholders arising from net investment income and net realized capital gains, if any, are distributed at least once each year. The amount of distributions from net investment income and net realized gains are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date. The tax character of distributions paid during the periods ended November 30, 2013 and May 31, 2013 was as follows:

| | | | | | | | | |

| November 30, 2013 | | $ | — | | | $ | — | | | $ | — | |

| May 31, 2013 | | $ | 19,469 | | | $ | — | | | $ | 19,469 | |

On December 31, 2013, the Fund paid short-term and long-term capital gains to shareholders of $0.0572 and $0.0036 per share, respectively. The distributions were paid on December 31, 2013 to shareholders of record on December 30, 2013.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – It is the Fund’s intention to qualify as a regulated investment company under the Internal Revenue Code of 1986 (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized gains are distributed in accordance with the Code. Accordingly, no provision for income tax has been made.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

APEXcm SMALL/MID CAP GROWTH FUND NOTES TO FINANCIAL STATEMENTS (Continued) |

The following information is computed on a tax basis for each item as of November 30, 2013:

| Tax cost of portfolio investments | | $ | 43,937,018 | |

| Gross unrealized appreciation | | $ | 6,371,456 | |

| Gross unrealized depreciation | | | (580,438 | ) |

| Net unrealized appreciation | | | 5,791,018 | |

| Accumulated ordinary loss | | | (71,320 | ) |

| Capital loss carryforward | | | (33,360 | ) |

| Other gains | | | 354,526 | |

| Total accumulated earnings | | $ | 6,040,864 | |

The difference between the federal income tax cost of portfolio investments and the financial statement cost is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to the tax deferral of losses on wash sales.

As of May 31, 2013, the Fund had a short-term capital loss carryforward in the amount of $33,360. This capital loss carryforward, which does not expire, may be utilized in the current and future years to offset net realized capital gains, if any, prior to distributing such gains to shareholders.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for all open tax periods (period ended May 31, 2013) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements.

3. Investment Transactions

During the six months ended November 30, 2013, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $35,864,560 and $6,761,046, respectively.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by the Adviser pursuant to the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, the Fund pays the Adviser an advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.00% of its average daily net assets.

APEXcm SMALL/MID CAP GROWTH FUND NOTES TO FINANCIAL STATEMENTS (Continued) |

The Adviser has contractually agreed, until August 31, 2015, to reduce its advisory fees and to reimburse the Fund’s operating expenses (excluding brokerage costs, taxes, interest, costs to organize the Fund, acquired fund fees and expenses and extraordinary expenses) to the extent necessary so that the Fund’s annual ordinary operating expenses do not exceed an amount equal to 1.05% of its average daily net assets. Accordingly, the Adviser reduced its advisory fees in the amount of $103,631 during the six months ended November 30, 2013.

Advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause the Fund’s ordinary operating expenses, at the time the repayment occurs, to exceed the expense limitation of 1.05% per annum. As of November 30, 2013, the Adviser may in the future recover advisory fee reductions and expense reimbursements totaling $248,507. The Adviser may recover a portion of this amount no later than the dates as stated below:

| May 31, 2016 | | $ | 144,876 | |

| November 30, 2016 | | | 103,631 | |

| | | $ | 248,507 | |

Certain officers of the Fund are also officers of the Adviser.

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides fund administration, fund accounting, compliance and transfer agency services to the Fund. Pursuant to seperate servicing agreements with Ultimus, the Fund pays Ultimus a customary fee for its services. Certain officers of the Trust are also officers of Ultimus.

DISTRIBUTION AGREEMENT

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus.

TRUSTEE COMPENSATION

Each Trustee who is not an interested person of the Trust receives from the Fund a fee of $500 for each Board meeting attended plus reimbursement of travel and other expenses incurred in attending the meetings. Trustees affiliated with the Adviser or Ultimus are not compensated by the Trust for their services.

APEXcm SMALL/MID CAP GROWTH FUND NOTES TO FINANCIAL STATEMENTS (Continued) |

5. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

6. Sector Risk

If the Fund has significant investments in the securities of issuers in industries within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have significant investments in that sector. In addition, this may increase the risk of loss of an investment in the Fund and increase the volatility of the Fund’s net asset value per share. From time to time, a particular set of circumstances may affect this sector or other companies within the sector. For instance, economic or market factors, regulation or deregulation, and technological or other developments may negatively impact all companies in a particular sector and, therefore, the value of the Fund’s portfolio could be adversely affected. As of November 30, 2013, the Fund had 26.4% of the value of its net assets invested in stocks within the Information Technology sector.

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

APEXcm SMALL/MID CAP GROWTH FUND ABOUT YOUR FUND’S EXPENSES (Unaudited) |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (June 1, 2013) and held until the end of the period (November 30, 2013).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the SEC requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

APEXcm SMALL/MID CAP GROWTH FUND ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued) |

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning Account Value June 1, 2013 | Ending Account Value November 30, 2013 | Expenses Paid During Period* |

| Based on Actual Fund Return | $1,000.00 | $1,140.30 | $5.63 |

| Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $1,019.80 | $5.32 |

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.05% for the period, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

OTHER INFORMATION (Unaudited) |

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-888-575-4800, or on the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-888-575-4800, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-888-575-4800. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

This page intentionally left blank.

BARROW ALL-CAP CORE FUND

INVESTOR CLASS (BALAX)

INSTITUTIONAL CLASS (BALIX)

BARROW ALL-CAP LONG/SHORT FUND

INVESTOR CLASS (BFLSX)

INSTITUTIONAL CLASS (BFSLX)

Semi-Annual Report

November 30, 2013

(Unaudited)

BARROW ALL-CAP CORE FUND LETTER TO SHAREHOLDERS | |

Dear Shareholder,

Barrow Street Advisors LLC re-organized the Barrow Street Fund LP, a private investment partnership started on 12/31/2008 (the “Predecessor Partnership”), into the Barrow All-Cap Core Fund (the “Fund”) on the close of business August 30, 2013. For the quarter ended November 30, 2013, the Fund’s Institutional Class posted a total return of +12.49%, which compared favorably against a +11.16% total return for the S&P 500 Index and -1.42% for Bloomberg’s 10-Year U.S. Treasury index. Calendar year-to-date the Fund’s Institutional Class generated a total return of +35.38% compared to +29.12% for the S&P 500. Since 12/31/08, the Fund has generated a total return of +162.10% compared to +122.56% for the S&P 500.

The Fund continued to implement its Systematic Quality Value (“SQV”) strategy, which seeks to employ a disciplined and dispassionate approach to investing in diverse sub-portfolios of high quality companies at prices that are well below our estimate of their intrinsic value. During the quarter, we invested in three new sub-portfolios comprising multiple industry sectors and market capitalizations and composed of numerous businesses with strong balance sheets that are growing, generating ample free cash flow, and re-investing that cash at high internal rates of return.

Drawing on our firm's 17 years of private and public equity investment experience and research, we made these investments with confidence that the market price of a well-constructed portfolio of high-quality stocks purchased at bargain levels will trend toward our estimate of its intrinsic value over time. Our portfolio is highly diversified by market cap segment, sector, industry, and position size.

Our investments are sourced by taking account of the opportunity set of all companies in our broad investment universe each time we commit capital to a new position. We think this approach allows us to uncover investment opportunities that arise from temporary market inefficiencies and to gather up the most compelling investments across a wide array of industries and market caps without the behavioral biases inherent in concentrated-stock and sector-specialized investing.

With regard to hold period, we typically give the market at least one year to re-appraise each of the Fund’s sub-portfolios. The idea here is that it takes time from the date of our investment in any given company for the market to realize that it is trading cheap to its intrinsic value and has high quality business metrics. We are more interested in the performance of each of our diversified sub-portfolios taken as a whole than that of any one position.

The three best-performing positions for the quarter were Endo Health Solutions, Inc., Nu Skin Enterprises, Inc. and Sturm Ruger & Company Inc., which generated total returns of +63.52%, +53.12% and +48.05%, respectively, and contributed to the Fund’s return by 94 bps, 86 bps and 55 bps, respectively. The three worst-performing positions were Questcor Pharmaceuticals, Inc., Terra Nitrogen Company, L.P., and Select Comfort Corp., which generated total returns of (12.61%), (26.17%) and (14.53%), respectively, and reduced the Fund’s return by 18 bps, 18 bps and 10 bps, respectively.

None of our holdings was announced as a take-over target during the quarter. On average, the Fund has experienced three take-outs per quarter, for a total of 54 since 12/31/08, or roughly 4x the market average.1 The control premia we have captured by virtue of holding stocks which end up being merger targets has made repeated and meaningful contributions to the Fund’s total returns, and we expect to continue to benefit from this effect going forward. We remove companies from the Fund’s portfolio soon after they are announced as take-over targets and re-invest that capital.

For the quarter, the portfolio generated a price return of +12.16%, including +14.09% for large caps, +10.19% for mid caps and +11.18% for small caps. This compares to +10.58% for the S&P 500 Index, +10.16% for the S&P 400 Midcap Index, and +13.06% for the Russell 2000 Index. Our sectors with the best absolute performance were health care and industrials, which generated price returns of +16.02% and +15.96%, respectively. Our sectors that did least well were materials and consumer discretionary, which returned +1.32% and +8.75%, respectively.

Going forward, we believe the Fund is well positioned for near-term and long-term success given the quality and value attributes of its stock portfolio. We expect the Fund will continue to outperform its benchmarks over time.

The Fund’s portfolio had a position-weighted EBIT (Earnings Before Interest and Taxes) yield of 9.30% on 11/30/13, which compares favorably with the 6.91% EBIT yield for the S&P 500 and the 2.74% yield-to-maturity of the benchmark 10-year U.S. Treasury note. The Fund’s dividend yield was 2.5%, which was 25% higher than that of the S&P 500. These healthy vital signs are consistent with the use of our private equity framework, which among other things focuses on cash flow over GAAP earnings, in selecting securities for investment.

In addition to the attractive valuation level of our portfolio, we expect to benefit from the absolute and relative level of quality fundamentals in our holdings. As of 11/30/13, our portfolio had the following position-weighted quality characteristics relative to the S&P 500 (SPX): return on equity (29.0% vs. 14.5% SPX); return on assets (13.7% vs. 3.1% SPX), operating margin (19.5% vs. 13.5% SPX) and debt-to-enterprise value (15.1% vs. 33.5% SPX).

Sincerely,

| Nicholas Chermayeff | Robert F. Greenhill, Jr. | David R. Bechtel |

| Co-Portfolio Manager, | Co-Portfolio Manager, | Principal, |

| Investment Committee | Investment Committee | Investment Committee |

| 1 | Barrow calculates the frequency of merger and acquisition (“M&A”) activity in its portfolio on a quarterly basis by dividing the cumulative number of portfolio holdings that have been announced as merger or acquisition targets by the cumulative number of unique holdings it has held in its portfolio. Barrow calculates the frequency of M&A activity in the market on a quarterly basis by dividing the cumulative number of publicly-traded U.S. common stocks that have been announced as acquisition targets per Bloomberg by the total universe of publicly-traded U.S. common stocks as identified by Bloomberg (approximately 10,000). The ratio of portfolio M&A frequency to market-wide M&A frequency is calculated by dividing the portfolio’s average of quarterly M&A frequency since inception 12/31/08 by the market-wide average of quarterly M&A frequency since inception 12/31/08. |

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-877-767-6633.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit our website at www.barrowfunds.com or call 1-877-767-6633 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. The opinions of the Fund’s Adviser with respect to those securities may change at any time. The 30-day SEC yield for the Fund as of November 30, 2013 was 0.86%.

The investment related and performance information discussed above for periods prior to Barrow All-Cap Core Fund’s inception date (close of business August 30, 2013) are based on the activities of the Fund’s predecessor, the Barrow Street Fund LP, an unregistered limited partnership managed by the portfolio managers of Barrow All-Cap Core Fund (the “Predecessor Private Fund”). The Predecessor Private Fund was reorganized into the Institutional Class shares on close of business August 30, 2013, the date that Barrow All- Cap Core Fund commenced operations. Barrow All-Cap Core Fund has been managed in the same style and by the same portfolio managers since the Predecessor Private Fund’s inception on December 31, 2008. The performance information shows the Predecessor Private Fund’s returns calculated using the actual fees and expenses that were charged by the Predecessor Private Fund. This prior performance is net of management fees and other expenses but does not include the effect of the Predecessor Private Fund’s performance fee which was in place until October 7, 2012. From the Predecessor Private Fund’s inception on December 31, 2008 through the date of this prospectus, the Predecessor Private Fund was not subject to certain investment restrictions, diversification requirements and other restrictions of the Investment Company Act of 1940, as amended (the “1940 Act”) or Subchapter M of the Internal Revenue Code of 1986, as amended, which, if they had been applicable, might have adversely affected Barrow All-Cap Core Fund’s performance.

BARROW ALL-CAP LONG/SHORT FUND LETTER TO SHAREHOLDERS | |

Dear Shareholder,

On the close of business August 30, 2013, Barrow Street Advisors LLC launched the Barrow All-Cap Long/Short Fund (the “Fund”). For the quarter ended November 30, 2013, the Fund’s Institutional Class posted a total return of 4.40%, which compares to 11.16% for the S&P 500 Index and -1.42% for Bloomberg’s 10-Year U.S. Treasury index. The Fund maintains a gross exposure of approximately 220% of its net capital with long exposure of 130%, short exposure of 90%, and net exposure of 40%.

The Fund continued to implement its Systematic Quality Value (“SQV”) strategy, which seeks to employ a disciplined and dispassionate approach to investing in diverse sub-portfolios of companies at prices that are well below (longs) or well above (shorts) our appraisal of their intrinsic value. During the quarter, we invested in three new sub-portfolios comprising multiple industry sectors and market capitalizations. We purchased long many high quality businesses with strong balance sheets that are growing, generating ample free cash flow, and re-investing that cash at high internal rates of return. In tandem, we sold short four times as many companies that we consider to be overpriced with poor quality characteristics. Our short positions are tailored to our long positions by market capitalization and sector.

Drawing on our firm's 17 years of private and public equity investment experience and research, we made these investments with confidence that the market price of a well-constructed portfolio of high (or low) quality stocks purchased at bargain (or lofty) levels will trend toward our estimate of its intrinsic value over time. Our long and short portfolios are highly diversified by market cap segment, sector, industry, and position size.

Our investments are sourced by taking account of the opportunity set of all companies in our broad investment universe each time we commit capital to a new position. We think this approach allows us to uncover investment opportunities that arise from temporary market inefficiencies and to gather up the most compelling investments across a wide array of industries and market caps without the behavioral biases inherent in concentrated-stock and sector-specialized investing.

With regard to hold period, we typically give the market at least one year to re-appraise each of the Fund’s positions. The idea here is that it takes time from the date of our investment in any given company for the market to realize that it is trading at a large discount or premium to its intrinsic value, especially when re-considered in light of the high or low quality of their business characteristics. We are more interested in the average performance of each of our diversified sub-portfolios taken as a whole than that of any one position.

The three best-performing positions for the quarter were Endo Health Solutions, Inc. (long), Nu Skin Enterprises, Inc. (long) and Sturm Ruger & Company Inc. (long), which generated total returns of +63.52%, +53.12% and +48.05%, respectively, and increased

the Fund’s return by 121 bps, 112 bps and 71 bps, respectively. The three worst-performing positions were Mako Surgical Corp. (short), Questcor Pharmaceuticals, Inc. (long) and Terra Nitrogen Company, L.P. (long), which generated total returns of +100.13%, -12.61% and -26.17%, respectively, and reduced the Fund’s return by 37 bps, 24 bps and 23 bps, respectively.

None of our long holdings was announced as a take-over target during the quarter. On average, our firm’s investments have experienced three long take-outs per quarter, for a total of 54 since 12/31/08, or roughly four times the market average.1 The control premia we have captured by virtue of holding stocks which end up being merger targets has made repeated and meaningful contributions to our firm’s investments over the years, and we expect to continue to benefit from this effect going forward. We remove companies from the Fund’s portfolio soon after they are announced as take-over targets and re-invest that capital.

During the quarter, the long portfolio generated a price return of +12.16%, including +14.03% for large caps, +10.21% for mid caps and +11.24% for small caps. This compares to +10.58% for the S&P 500 Index, +10.16% for the S&P 400 Midcap Index, and +13.06% for the Russell 2000 Index. Our sectors with the best performance were industrials and health care, which generated price returns of +15.89% and +15.87%, respectively. The two sectors that did least well were consumer discretionary and materials, which returned +8.77% and +1.38%, respectively. Given its gross weight of approximately 130% of the Fund’s net assets, the long portfolio contributed 1570 basis points to the Fund’s return over the quarter.

The short portfolio generated a price return of -12.06%, including -10.25% for large caps, -11.88% for mid caps and -14.52% for small caps. Our sectors with the best performance were health care and energy, which generated price returns of +2.69% and -6.86%, respectively. Our sectors that did least well were industrials and health care, which returned -14.24% and -14.15%, respectively. Given its gross weight of approximately 90% of the Fund’s net assets, the short portfolio reduced by 1085 basis points the Fund’s return over the quarter.

Going forward, we believe the Fund is well positioned for near-term and long-term success given the fundamental quality and value attributes of its positions and its hedged portfolio, designed to reduce price volatility. We expect the Fund’s long and short portfolios to outperform its benchmarks over time.

The Fund’s long portfolio had a position-weighted EBIT (Earnings Before Interest and Taxes) yield of 9.30% on 11/30/13, which compares favorably with the 6.91% EBIT yield for the S&P 500 and the 2.74% yield-to-maturity of the benchmark 10-year U.S. Treasury note. The short portfolio’s position-weighted EBIT yield of 2.15% is substantially lower than the average stock in the market, indicating to us that these securities are significantly overpriced relative to market levels. The Fund’s returns would benefit if the prices of these stocks were to drop. Furthermore, our long portfolio had an attractive dividend yield of 2.5%, which was nearly twice that of the short portfolio (1.3%) and 25% higher than that of the S&P 500 (2.0%). These healthy vital signs are consistent with the use of our private equity framework, which among other things focuses on cash flow over GAAP earnings, in selecting securities for investment.

In addition to the attractive valuation levels of our portfolio, we expect to benefit from the absolute and relative level of quality fundamentals in our holdings. As of 11/30/13, our long and short portfolios had the following position-weighted quality characteristics relative to the S&P 500 (SPX): return on equity (29.0%/8.1% L/S vs. 14.5% SPX); return on assets (13.7%/2.5% L/S vs. 3.1% SPX), operating margin (19.5%/1.8% L/S vs. 13.5% SPX) and debt-to-enterprise value (15.1%/19.0% L/S vs. 33.5% SPX).

Sincerely,

| Nicholas Chermayeff | Robert F. Greenhill, Jr. | David R. Bechtel |

| Co-Portfolio Manager, | Co-Portfolio Manager, | Principal, |

| Investment Committee | Investment Committee | Investment Committee |

| 1 | Barrow calculates the frequency of merger and acquisition (“M&A”) activity in its portfolio on a quarterly basis by dividing the cumulative number of portfolio holdings that have been announced as merger or acquisition targets by the cumulative number of unique holdings it has held in its portfolio. Barrow calculates the frequency of M&A activity in the market on a quarterly basis by dividing the cumulative number of publicly-traded U.S. common stocks that have been announced as acquisition targets per Bloomberg by the total universe of publicly-traded U.S. common stocks as identified by Bloomberg (approximately 10,000). The ratio of portfolio M&A frequency to market-wide M&A frequency is calculated by dividing the portfolio’s average of quarterly M&A frequency since inception 12/31/08 by the market-wide average of quarterly M&A frequency since inception 12/31/08. |

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-877-767-6633.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit our website at www.barrowfunds.com or call 1-877-767-6633 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. The opinions of the Fund’s Adviser with respect to those securities may change at any time. The 30-day SEC yield for the Fund as of November 30, 2013 was -0.94%.

BARROW ALL-CAP CORE FUND

PORTFOLIO INFORMATION

November 30, 2013 (Unaudited)

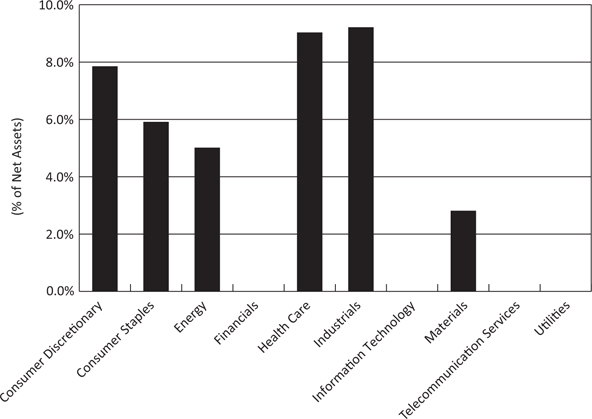

Sector Diversification

Top 10 Equity Holdings

| | |

| Nu Skin Enterprises, Inc. - Class A | | 1.63% |

| Endo Health Solutions, Inc. | | 1.47% |

| Questcor Pharmaceuticals, Inc. | | 1.47% |

| AmSurg Corporation | | 1.37% |

| Northrop Grumman Corporation | | 1.33% |

| Express, Inc. | | 1.29% |

| Raytheon Company | | 1.29% |

| Cardinal Health, Inc. | | 1.28% |

| Deluxe Corporation | | 1.27% |

| USANA Health Sciences, Inc. | | 1.24% |

BARROW ALL-CAP LONG/SHORT FUND

PORTFOLIO INFORMATION

November 30, 2013 (Unaudited)

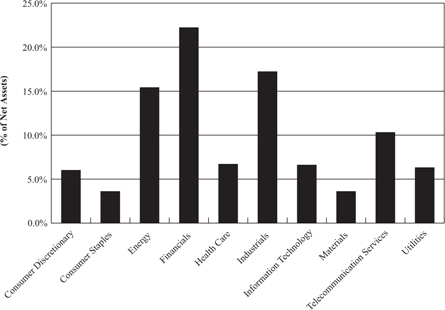

Net Sector Exposure Diversification*

| * | The net percentages are computed by taking the net dollar exposure, including short positions, and dividing by the net assets of the Fund. Consequently, the percentages will not total to 100%. |

| Top 10 Long Common Stocks | | Top 10 Short Common Stocks |

| | | | |

| Nu Skin Enterprises, Inc. - Class A | 2.10% | | West Pharmaceutical Services, Inc. | 0.58% |

| Endo Health Solutions, Inc. | 1.90% | | athenahealth, Inc. | 0.57% |

| Questcor Pharmaceuticals, Inc. | 1.90% | | Team Health Holdings, Inc. | 0.51% |

| AmSurg Corporation | 1.78% | | Align Technology, Inc. | 0.43% |

| Northrop Grumman Corporation | 1.73% | | Actavis plc | 0.42% |

| Express, Inc. | 1.66% | | Andersons, Inc. (The) | 0.42% |

| Raytheon Company | 1.66% | | Haemonetics Corporation | 0.41% |

| Cardinal Health, Inc. | 1.65% | | Constellation Brands, Inc. - Class A | 0.39% |

| Deluxe Corporation | 1.65% | | LifePoint Hospitals, Inc. | 0.39% |

| Dun & Bradstreet Corporation (The) | 1.60% | | Allscripts Healthcare Solutions, Inc. | 0.39% |

BARROW ALL-CAP CORE FUND SCHEDULE OF INVESTMENTS November 30, 2013 (Unaudited) | |

| | | | | | |

| Consumer Discretionary — 22.0% | | | | | | |

| Auto Components — 0.1% | | | | | | |

TRW Automotive Holdings Corporation (a) | | | 248 | | | $ | 19,245 | |

| | | | | | | | | |

| Automobiles — 0.1% | | | | | | | | |

Ford Motor Company (b) | | | 1,057 | | | | 18,054 | |

| | | | | | | | | |

| Diversified Consumer Services — 1.7% | | | | | | | | |

H&R Block, Inc. (b) | | | 5,539 | | | | 154,483 | |

Outerwall, Inc. (a) (b) | | | 1,648 | | | | 112,723 | |

Weight Watchers International, Inc. (b) | | | 2,082 | | | | 67,477 | |

| | | | | | | | 334,683 | |

| Hotels, Restaurants & Leisure — 0.7% | | | | | | | | |

International Game Technology (b) | | | 5,296 | | | | 92,627 | |

Interval Leisure Group, Inc. (b) | | | 1,218 | | | | 32,618 | |

| | | | | | | | 125,245 | |

| Household Durables — 0.6% | | | | | | | | |

iRobot Corporation (a) (b) | | | 769 | | | | 25,539 | |

Tempur Sealy International, Inc. (a) (b) | | | 919 | | | | 46,887 | |

Tupperware Brands Corporation (b) | | | 374 | | | | 34,161 | |

| | | | | | | | 106,587 | |

| Leisure Equipment & Products — 2.7% | | | | | | | | |

LeapFrog Enterprises, Inc. (a) (b) | | | 11,898 | | | | 102,442 | |

Smith & Wesson Holding Corporation (a) (b) | | | 16,825 | | | | 198,872 | |

Sturm, Ruger & Company, Inc. (b) | | | 2,851 | | | | 219,327 | |

| | | | | | | | 520,641 | |

| Media — 5.7% | | | | | | | | |

Crown Media Holdings, Inc. - Class A (a) (b) | | | 6,107 | | | | 20,458 | |

DIRECTV (a) (b) | | | 1,887 | | | | 124,750 | |

Gannett Company, Inc. (b) | | | 1,280 | | | | 34,637 | |

Interpublic Group of Companies, Inc. (b) | | | 9,930 | | | | 172,782 | |

John Wiley & Sons, Inc. - Class A (b) | | | 2,201 | | | | 112,163 | |

Meredith Corporation | | | 268 | | | | 14,295 | |

National CineMedia, Inc. (b) | | | 9,013 | | | | 168,092 | |

Omnicom Group, Inc. (b) | | | 3,051 | | | | 217,994 | |

Valassis Communications, Inc. (b) | | | 6,698 | | | | 196,653 | |

Viacom, Inc. - Class B (b) | | | 515 | | | | 41,288 | |

| | | | | | | | 1,103,112 | |

BARROW ALL-CAP CORE FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 100.0% (Continued) | | | | | | |

| Consumer Discretionary — 22.0% (Continued) | | | | | | |

| Specialty Retail — 7.5% | | | | | | |

American Eagle Outfitters, Inc. (b) | | | 8,188 | | | $ | 133,219 | |

Bed Bath & Beyond, Inc. (a) (b) | | | 1,400 | | | | 109,242 | |

Buckle, Inc. (The) (b) | | | 3,962 | | | | 210,224 | |

Cato Corporation (The) - Class A (b) | | | 1,092 | | | | 37,172 | |

Chico's FAS, Inc. (b) | | | 1,555 | | | | 29,063 | |

Express, Inc. (a) (b) | | | 10,065 | | | | 247,700 | |

Foot Locker, Inc. (b) | | | 4,095 | | | | 159,254 | |

Francesca's Holdings Corporation (a) (b) | | | 2,694 | | | | 52,856 | |

GameStop Corporation - Class A (b) | | | 4,174 | | | | 201,395 | |

Gap, Inc. (The) (b) | | | 2,404 | | | | 98,492 | |

Guess?, Inc. (b) | | | 530 | | | | 18,158 | |

Select Comfort Corporation (a) | | | 6,430 | | | | 135,737 | |

Staples, Inc. (b) | | | 1,226 | | | | 19,040 | |

| | | | | | | | 1,451,552 | |

| Textiles, Apparel & Luxury Goods — 2.9% | | | | | | | | |

Coach, Inc. (b) | | | 3,134 | | | | 181,458 | |

Iconix Brand Group, Inc. (a) (b) | | | 3,140 | | | | 124,595 | |

Steven Madden Ltd. (a) (b) | | | 5,985 | | | | 233,176 | |

Vera Bradley, Inc. (a) | | | 474 | | | | 11,907 | |

| | | | | | | | 551,136 | |

| Consumer Staples — 14.3% | | | | | | | | |

| Beverages — 1.5% | | | | | | | | |

Boston Beer Company, Inc. (The) - Class A (a) | | | 28 | | | | 6,854 | |

Dr Pepper Snapple Group, Inc. (b) | | | 3,972 | | | | 191,689 | |

National Beverage Corporation (b) | | | 3,925 | | | | 82,896 | |

| | | | | | | | 281,439 | |

| Food & Staples Retailing — 0.3% | | | | | | | | |

CVS Caremark Corporation | | | 299 | | | | 20,021 | |

Village Super Market, Inc. - Class A (b) | | | 1,235 | | | | 47,832 | |

| | | | | | | | 67,853 | |

| Food Products — 3.1% | | | | | | | | |

B&G Foods, Inc. (b) | | | 914 | | | | 31,652 | |

Darling International, Inc. (a) (b) | | | 9,906 | | | | 205,351 | |

Dean Foods Company (a) (b) | | | 1,613 | | | | 29,002 | |

Hillshire Brands Company (The) (b) | | | 1,490 | | | | 49,796 | |

Ingredion, Inc. | | | 253 | | | | 17,498 | |

Kraft Foods Group, Inc. | | | 354 | | | | 18,804 | |

Lancaster Colony Corporation (b) | | | 1,834 | | | | 158,934 | |

Mondelēz International, Inc. - Class A (b) | | | 952 | | | | 31,921 | |

BARROW ALL-CAP CORE FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 100.0% (Continued) | | | | | | |

| Consumer Staples — 14.3% (Continued) | | | | | | |

| Food Products — 3.1% (Continued) | | | | | | |

Pilgrim's Pride Corporation (a) (b) | | | 2,226 | | | $ | 36,462 | |

Seaboard Corporation | | | 7 | | | | 19,775 | |

| | | | | | | | 599,195 | |

| Household Products — 0.7% | | | | | | | | |

Energizer Holdings, Inc. (b) | | | 975 | | | | 107,591 | |

Spectrum Brands Holdings, Inc. (b) | | | 288 | | | | 20,327 | |

| | | | | | | | 127,918 | |

| Personal Products — 3.8% | | | | | | | | |

Inter Parfums, Inc. (b) | | | 3,731 | | | | 135,808 | |

Nu Skin Enterprises, Inc. - Class A (b) | | | 2,446 | | | | 312,697 | |

Revlon, Inc. - Class A (a) (b) | | | 2,012 | | | | 53,117 | |

USANA Health Sciences, Inc. (a) (b) | | | 3,257 | | | | 238,119 | |

| | | | | | | | 739,741 | |

| Tobacco — 4.9% | | | | | | | | |

Altria Group, Inc. (b) | | | 5,212 | | | | 192,740 | |

Lorillard, Inc. (b) | | | 4,267 | | | | 219,025 | |

Philip Morris International, Inc. (b) | | | 1,891 | | | | 161,756 | |

Reynolds American, Inc. (b) | | | 3,886 | | | | 196,048 | |

Vector Group Ltd. (b) | | | 10,073 | | | | 164,996 | |

| | | | | | | | 934,565 | |

| Energy — 11.2% | | | | | | | | |

| Energy Equipment & Services — 1.7% | | | | | | | | |

C&J Energy Services, Inc. (a) (b) | | | 7,530 | | | | 178,461 | |

Forum Energy Technologies, Inc. (a) (b) | | | 545 | | | | 14,720 | |

Geospace Technologies Corporation (a) | | | 201 | | | | 17,541 | |

Halliburton Company (b) | | | 801 | | | | 42,197 | |

National Oilwell Varco, Inc. (b) | | | 834 | | | | 67,971 | |

| | | | | | | | 320,890 | |

| Oil, Gas & Consumable Fuels — 9.5% | | | | | | | | |

Alon USA Energy, Inc. (b) | | | 6,824 | | | | 94,171 | |

Alon USA Partners, L.P. (b) | | | 3,891 | | | | 60,544 | |

Chevron Corporation (b) | | | 767 | | | | 93,911 | |

CVR Energy, Inc. (b) | | | 2,601 | | | | 102,688 | |

CVR Refining, L.P. (b) | | | 2,781 | | | | 66,744 | |

Delek US Holdings, Inc. (b) | | | 3,410 | | | | 103,187 | |

HollyFrontier Corporation (b) | | | 3,981 | | | | 191,008 | |

Marathon Oil Corporation (b) | | | 4,476 | | | | 161,315 | |

Marathon Petroleum Corporation (b) | | | 2,529 | | | | 209,249 | |

Northern Tier Energy, L.P. (b) | | | 7,478 | | | | 189,941 | |

Phillips 66 (b) | | | 1,600 | | | | 111,376 | |

BARROW ALL-CAP CORE FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 100.0% (Continued) | | | | | | |

| Energy — 11.2% (Continued) | | | | | | |

| Oil, Gas & Consumable Fuels — 9.5% (Continued) | | | | | | |

Renewable Energy Group, Inc. (a) (b) | | | 2,426 | | | $ | 27,584 | |

Rentech, Inc. (b) | | | 34,518 | | | | 62,478 | |

Stone Energy Corporation (a) | | | 229 | | | | 7,575 | |

Tesoro Corporation (b) | | | 1,566 | | | | 91,815 | |

VAALCO Energy, Inc. (a) (b) | | | 4,905 | | | | 29,675 | |

Western Refining, Inc. (b) | | | 5,823 | | | | 227,505 | |

| | | | | | | | 1,830,766 | |

| Health Care — 21.5% | | | | | | | | |

| Biotechnology — 4.6% | | | | | | | | |

Cubist Pharmaceuticals, Inc. (a) (b) | | | 1,567 | | | | 107,355 | |

Myriad Genetics, Inc. (a) (b) | | | 6,741 | | | | 200,545 | |

PDL BioPharma, Inc. (b) | | | 23,632 | | | | 230,885 | |

Spectrum Pharmaceuticals, Inc. | | | 13,094 | | | | 126,095 | |

United Therapeutics Corporation (a) (b) | | | 2,329 | | | | 214,990 | |

| | | | | | | | 879,870 | |

| Health Care Equipment & Supplies — 2.7% | | | | | | | | |

ArthroCare Corporation (a) (b) | | | 2,602 | | | | 98,147 | |

C.R. Bard, Inc. (b) | | | 704 | | | | 97,772 | |

CareFusion Corporation (a) | | | 460 | | | | 18,331 | |

Globus Medical, Inc. - Class A (a) (b) | | | 7,062 | | | | 136,014 | |

Medtronic, Inc. (b) | | | 1,840 | | | | 105,469 | |

St. Jude Medical, Inc. (b) | | | 1,113 | | | | 65,021 | |

| | | | | | | | 520,754 | |

| Health Care Providers & Services — 9.4% | | | | | | | | |

AmerisourceBergen Corporation (b) | | | 3,147 | | | | 221,958 | |

AMN Healthcare Services, Inc. (a) (b) | | | 1,850 | | | | 25,678 | |

AmSurg Corporation (a) (b) | | | 5,464 | | | | 264,020 | |

Bio-Reference Laboratories, Inc. (a) (b) | | | 3,091 | | | | 90,257 | |

Cardinal Health, Inc. (b) | | | 3,813 | | | | 246,320 | |

Chemed Corporation (b) | | | 2,389 | | | | 186,175 | |

HealthSouth Corporation (b) | | | 3,130 | | | | 112,023 | |

Laboratory Corporation of America Holdings (a) (b) | | | 1,935 | | | | 197,080 | |

MEDNAX, Inc. (a) (b) | | | 1,503 | | | | 166,532 | |

Patterson Companies, Inc. (b) | | | 1,223 | | | | 50,742 | |

PharMerica Corporation (a) | | | 914 | | | | 20,638 | |

Quest Diagnostics, Inc. (b) | | | 3,107 | | | | 189,341 | |

Select Medical Holdings Corporation (b) | | | 1,350 | | | | 11,691 | |

VCA Antech, Inc. (a) (b) | | | 1,232 | | | | 36,898 | |

| | | | | | | | 1,819,353 | |

BARROW ALL-CAP CORE FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 100.0% (Continued) | | | | | | |

| Health Care — 21.5% (Continued) | | | | | | |

| Health Care Technology — 0.3% | | | | | | |

Computer Programs & Systems, Inc. | | | 113 | | | $ | 6,952 | |

Quality Systems, Inc. (b) | | | 1,869 | | | | 43,660 | |

| | | | | | | | 50,612 | |

| Pharmaceuticals — 4.5% | | | | | | | | |

Abbott Laboratories (b) | | | 2,430 | | | | 92,802 | |

Auxilium Pharmaceuticals, Inc. (a) (b) | | | 4,666 | | | | 95,233 | |

Eli Lilly & Company | | | 366 | | | | 18,380 | |

Endo Health Solutions, Inc. (a) (b) | | | 4,212 | | | | 283,004 | |

Impax Laboratories, Inc. (a) (b) | | | 944 | | | | 22,694 | |

Pfizer, Inc. (b) | | | 573 | | | | 18,181 | |

Prestige Brands Holdings, Inc. (a) (b) | | | 1,582 | | | | 55,750 | |

Questcor Pharmaceuticals, Inc. (b) | | | 4,863 | | | | 282,103 | |

| | | | | | | | 868,147 | |