Management’s Discussion and Analysis of Financial Results

INTRODUCTION

This management’s discussion and analysis (“MD&A”) of Brookfield Property Partners L.P. (“BPY”, the “partnership”, or “we”) covers the financial position as of September 30, 2016 and December 31, 2015 and results of operations for the three and nine months ended September 30, 2016 and 2015. This MD&A should be read in conjunction with the unaudited condensed consolidated financial statements (the “Financial Statements”) and related notes as of September 30, 2016, included elsewhere in this report, and our annual report for the year ended December 31, 2015 on Form 20-F.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND USE OF NON-IFRS MEASURES

This MD&A, particularly “Objectives and Financial Highlights – Overview of the Business” and “Additional Information – Trend Information”, contains “forward-looking information” within the meaning of Canadian provincial securities laws and applicable regulations and “forward-looking statements” within the meaning of “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, include statements regarding our operations, business, financial condition, expected financial results, performance, prospects, opportunities, priorities, targets, goals, ongoing objectives, strategies and outlook, as well as the outlook for North American and international economies for the current fiscal year and subsequent periods, and include words such as “expects”, “anticipates”, “plans”, “believes”, “estimates”, “seeks”, “intends”, “targets”, “projects”, “forecasts”, “likely”, or negative versions thereof and other similar expressions, or future or conditional verbs such as “may”, “will”, “should”, “would” and “could”.

Although we believe that our anticipated future results, performance or achievements expressed or implied by the forward-looking statements and information are based upon reasonable assumptions and expectations, the reader should not place undue reliance on forward-looking statements and information because they involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, which may cause our actual results, performance or achievements to differ materially from anticipated future results, performance or achievement expressed or implied by such forward-looking statements and information.

Factors that could cause actual results to differ materially from those contemplated or implied by forward-looking statements include, but are not limited to: risks incidental to the ownership and operation of real estate properties including local real estate conditions; the impact or unanticipated impact of general economic, political and market factors in the countries in which we do business; the ability to enter into new leases or renew leases on favorable terms; business competition; dependence on tenants’ financial condition; the use of debt to finance our business; the behavior of financial markets, including fluctuations in interest and foreign exchange rates; uncertainties of real estate development or redevelopment; global equity and capital markets and the availability of equity and debt financing and refinancing within these markets; risks relating to our insurance coverage; the possible impact of international conflicts and other developments including terrorist acts; potential environmental liabilities; changes in tax laws and other tax related risks; dependence on management personnel; illiquidity of investments; the ability to complete and effectively integrate acquisitions into existing operations and the ability to attain expected benefits therefrom; operational and reputational risks; catastrophic events, such as earthquakes and hurricanes; and other risks and factors detailed from time to time in our documents filed with the securities regulators in Canada and the United States, as applicable.

We caution that the foregoing list of important factors that may affect future results is not exhaustive. When relying on our forward-looking statements or information, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Except as required by law, we undertake no obligation to publicly update or revise any forward-looking statements or information, whether written or oral, that may be as a result of new information, future events or otherwise.

We disclose a number of financial measures in this MD&A that are calculated and presented using methodologies other than in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). We utilize these measures in managing our business, including performance measurement, capital allocation and valuation purposes and believe that providing these performance measures on a supplemental basis to our IFRS results is helpful to investors in assessing our overall performance. These financial measures should not be considered as a substitute for similar financial measures calculated in accordance with IFRS. We caution readers that these non-IFRS financial measures may differ from the calculations disclosed by other businesses, and as a result, may not be comparable to similar measures presented by others. Reconciliations of these non-IFRS financial measures to the most directly comparable financial measures calculated and presented in accordance with IFRS, where applicable, are included within this MD&A.

OBJECTIVES AND FINANCIAL HIGHLIGHTS

BASIS OF PRESENTATION

Our sole material asset is our 37% interest in Brookfield Property L.P. (the “Operating Partnership”). As we have the ability to direct its activities pursuant to our rights as owners of the general partner units, we consolidate the Operating Partnership. Accordingly, our Financial Statements reflect 100% of its assets, liabilities, revenues, expenses and cash flows, including non-controlling interests therein, which capture the ownership interests of other third parties.

We also discuss the results of operations on a segment basis, consistent with how we manage our business. In the first quarter of 2016, we realigned the organizational and governance structures of our businesses to align them more closely with the nature of the partnership’s investments. Such realignment gave rise to changes in how the partnership presents information for financial reporting and management decision-making purposes and resulted in a change in the partnership’s reporting segments. Consequently, as of January 1, 2016, the partnership’s operating segments are organized into four reportable segments: i) Core Office, ii) Core Retail, iii) Opportunistic and iv) Corporate. All prior period segment disclosures have been recast to reflect the changes in the partnership’s reportable segments. These segments are independently and regularly reviewed and managed by the Chief Executive Officer, who is considered the Chief Operating Decision Maker.

Our partnership’s equity interests include general partnership units (“GP Units”), publicly traded limited partnership units (“LP Units”), redeemable/exchangeable partnership units of the Operating Partnership (“Redeemable/Exchangeable Partnership Units”), special limited partnership units of the Operating Partnership (“Special LP Units”) and limited partnership units of Brookfield Office Properties Exchange LP (“Exchange LP Units”). Holders of the GP Units, LP Units, Redeemable/Exchangeable Partnership Units, Special LP Units, and Exchange LP Units will be collectively referred to throughout this MD&A as “Unitholders”. The LP Units, Redeemable/Exchangeable Partnership Units and Exchange LP Units have the same economic attributes in all respects, except that the Redeemable/Exchangeable Partnership Units have provided Brookfield Asset Management Inc. (“Brookfield Asset Management”) the right to request that its units be redeemed for cash consideration since April 2015. In the event that Brookfield Asset Management exercises this right, our partnership has the right, at its sole discretion, to satisfy the redemption request with its LP Units, rather than cash, on a one-for-one basis. As a result, Brookfield Asset Management, as holder of Redeemable/Exchangeable Partnership Units, participates in earnings and distributions on a per unit basis equivalent to the per unit participation of the LP Units of our partnership. However, given the redemption feature referenced above and the fact that they were issued by our subsidiary, we present the Redeemable/Exchangeable Partnership Units as a component of non-controlling interests. The Exchange LP Units are exchangeable at any time on a one-for-one basis, at the option of the holder, for LP Units. As a result of this redemption feature, we present the Exchange LP Units as a component of non-controlling interests.

This MD&A includes financial data for the three and nine months ended September 30, 2016 and includes material information up to November 9, 2016. Financial data have been prepared using accounting policies in accordance with IFRS as issued by the IASB. Non-IFRS measures used in this MD&A are reconciled to or calculated from such financial information. Unless otherwise specified, all operating and other statistical information is presented as if we own 100% of each property in our portfolio, regardless of whether we own all of the interests in each property, excluding information relating to our interests in China Xintiandi (“CXTD”). We believe this is the most appropriate basis on which to evaluate the performance of properties in the portfolio relative to each other and others in the market. All dollar references, unless otherwise stated, are in millions of U.S. Dollars. Canadian Dollars (“C$”), Australian Dollars (“A$”), British Pounds (“£”), Euros (“€”), Brazilian Reais (“R$”), Indian Rupees (“₨”), and Chinese Yuan (“C¥”) are identified where applicable.

Additional information is available on our website at bpy.brookfield.com, or on www.sedar.com or www.sec.gov.

OVERVIEW OF THE BUSINESS

Our partnership is Brookfield Asset Management’s primary public entity to make investments in the real estate industry. We are a globally-diversified owner and operator of high-quality properties that typically generate stable and sustainable cash flows over the long term. Our goal is to be a leading global owner and operator of real estate, providing investors with a diversified exposure to some of the most iconic properties in the world and to acquire high-quality assets at a discount to replacement cost or intrinsic value. With approximately 14,000 employees involved in Brookfield Asset Management’s real estate businesses around the globe, we have built operating platforms in various real estate sectors, including:

| |

| • | Core Office sector through our 100% common equity interest in Brookfield Office Properties Inc. (“BPO”) and our 50% interest in Canary Wharf Group plc (“Canary Wharf”); |

| |

| • | Core Retail sector through our 29% interest in General Growth Properties, Inc. (“GGP”) (34% on a fully diluted basis, assuming all outstanding warrants are exercised); and |

| |

| • | Opportunistic sector through investments in Brookfield Asset Management-sponsored real estate funds. |

Through these platforms, we have amassed a portfolio of premier properties and development sites around the globe, including:

| |

| • | 149 office properties totaling approximately 101 million square feet primarily located in the world’s leading commercial markets such as New York, London, Los Angeles, Washington, D.C., Sydney, Toronto, and Berlin; |

| |

| • | Office and urban multifamily development sites that enable the construction of 33 million square feet of new properties; |

| |

| • | 126 regional malls and urban retail properties containing over 124 million square feet in the United States; |

| |

| • | 110 opportunistic office properties comprising 24 million square feet of office space in the United States, United Kingdom, Brazil and India; |

| |

| • | Over 27 million square feet of opportunistic retail space across 44 properties across the United States and in select Brazilian markets; |

| |

| • | Over 46 million square feet of industrial space across 185 industrial properties, primarily consisting of modern logistics assets in North America and Europe, with an additional seven million square feet currently under construction; |

| |

| • | Approximately 32,000 multifamily units across 110 properties throughout the United States; |

| |

| • | Nineteen hospitality assets with approximately 14,100 rooms across North America, Europe and Australia; |

| |

| • | Over 300 properties that are leased to automotive dealerships across the United States and Canada on a triple net lease basis; |

| |

| • | Over 160 self-storage facilities comprising approximately 13 million square feet throughout the United States; and |

| |

| • | Fourteen student housing properties with over 5,800 beds in the United Kingdom. |

Our diversified portfolio of high-quality office and retail assets in some of the world’s most dynamic markets has a stable cash flow profile due to its long-term leases. In addition, as a result of the mark-to-market of rents upon lease expiry, escalation provisions in leases and projected increases in occupancy, these assets should generate strong same-property net operating income (“NOI”) growth without significant capital investment. Furthermore, we expect to earn between 8% and 11% unlevered, pre-tax returns on construction costs for our development and redevelopment projects and 20% on our equity invested in Brookfield-sponsored real estate opportunity funds. With this cash flow profile, our goal is to pay an attractive annual distribution to our Unitholders and to grow our distribution by 5% to 8% per annum.

Overall, we seek to earn leveraged after-tax returns of 12% to 15% on our invested capital. These returns will be comprised of current cash flow and capital appreciation. Capital appreciation will be reflected in the fair value gains that flow through our income statement as a result of our revaluation of investment properties in accordance with IFRS to reflect initiatives that increase property level cash flows, change the risk profile of the asset, or to reflect changes in market conditions. From time to time, we will convert some or all of these unrealized gains to cash through asset sales, joint ventures or refinancings.

We believe our global scale and best-in-class operating platforms provide us with a unique competitive advantage as we are able to efficiently allocate capital around the world toward those sectors and geographies where we see the greatest returns. We actively recycle assets on our balance sheet as they mature and reinvest the proceeds into higher yielding investment strategies, further enhancing returns. In addition, due to the scale of our stabilized portfolio and flexibility of our balance sheet, our business model is self-funding and does not require us to access capital markets to fund our continued growth.

PERFORMANCE MEASURES

We expect to generate returns to Unitholders from a combination of cash flow earned from our operations and capital appreciation. Furthermore, if we are successful in increasing cash flow earned from our operations we will be able to increase distributions to Unitholders to provide them with an attractive current yield on their investment.

To measure our performance against these targets, we focus on NOI, same-property NOI, funds from operations (“FFO”), Company FFO, fair value changes, and net income and equity attributable to Unitholders. Some of these performance metrics do not have standardized meanings prescribed by IFRS and therefore may differ from similar metrics used by other companies. We define each of these measures as follows:

| |

| • | NOI: revenues from our commercial and hospitality operations of consolidated properties less direct commercial property and hospitality expenses. |

| |

| • | Same-property NOI: a subset of NOI, which excludes NOI that is earned from assets acquired, disposed of or developed during the periods presented, or not of a recurring nature, and from opportunistic assets. |

| |

| • | FFO: net income, prior to fair value gains, net, depreciation and amortization of real estate assets, and income taxes less non-controlling interests of others in operating subsidiaries and properties share of these items. When determining FFO, we include our proportionate share of the FFO of unconsolidated partnerships and joint ventures and associates, as well as gains (or losses) related to properties developed for sale. |

| |

| • | Company FFO: FFO before the impact of depreciation and amortization of non-real estate assets, transaction costs, gains (losses) associated with non-investment properties and the FFO that would have been attributable to the partnership’s shares of GGP if all outstanding warrants of GGP, which are all currently exercisable, were exercised on a cashless basis. It also includes dilution adjustments to undiluted FFO as a result of the net settled warrants. |

| |

| • | Fair value changes: includes the increase or decrease in the value of investment properties that is reflected in the consolidated statements of income. |

| |

| • | Net income attributable to Unitholders: net income attributable to holders of GP Units, LP Units, Redeemable/Exchangeable Partnership Units, Special LP Units and Exchange LP Units. |

| |

| • | Equity attributable to Unitholders: equity attributable to holders of GP Units, LP Units, Redeemable/Exchangeable Partnership Units, Special LP Units and Exchange LP Units. |

NOI is a key indicator of our ability to increase cash flow from our operations. We seek to grow NOI through pro-active management and leasing of our properties. Same-property NOI allows us to segregate the performance of leasing and operating initiatives on the portfolio from the impact to performance of investing activities and “one-time items”, which for the historical periods presented consist primarily of lease termination income.

We also consider FFO an important measure of our operating performance. FFO is a widely recognized measure that is frequently used by securities analysts, investors and other interested parties in the evaluation of real estate entities, particularly those that own and operate income producing properties. Our definition of FFO includes all of the adjustments that are outlined in the National Association of Real Estate Investment Trusts (“NAREIT”) definition of FFO, including the exclusion of gains (or losses) from the sale of investment properties, the add

back of any depreciation and amortization related to real estate assets and the adjustment for unconsolidated partnerships and joint ventures. We also add back the gains (or losses) related to properties developed for sale. In addition to the adjustments prescribed by NAREIT, we also make adjustments to exclude any unrealized fair value gains (or losses) that arise as a result of reporting under IFRS, and income taxes that arise as certain of our subsidiaries are structured as corporations as opposed to real estate investment trusts (“REITs”). These additional adjustments result in an FFO measure that is similar to that which would result if our partnership was organized as a REIT that determined net income in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”), which is the type of organization on which the NAREIT definition is premised. Our FFO measure will differ from other organizations applying the NAREIT definition to the extent of certain differences between the IFRS and U.S. GAAP reporting frameworks, principally related to the recognition of lease termination income. Because FFO excludes fair value gains (losses), including equity accounted fair value gains (losses), realized gains (losses) on the sale of investment properties, depreciation and amortization of real estate assets and income taxes, it provides a performance measure that, when compared year-over-year, reflects the impact on operations from trends in occupancy rates, rental rates, operating costs and interest costs, providing perspective not immediately apparent from net income. We reconcile FFO to net income rather than cash flow from operating activities as we believe net income is the most comparable measure.

In addition, we consider Company FFO a useful measure for securities analysts, investors and other interested parties in the evaluation of our partnership’s performance. Company FFO, similar to FFO discussed above, provides a performance measure that reflects the impact on operations of trends in occupancy rates, rental rates, operating costs and interest costs. In addition, the adjustments to Company FFO relative to FFO allow the partnership insight into these trends for the real estate operations, by adjusting for non-real estate components.

Net income attributable to unitholders is used by the partnership to evaluate the performance of the partnership as a whole as each of the unitholders participates in the economics of the partnership equally. In calculating net income attributable to unitholders per unit, the partnership excludes the impact of mandatorily convertible preferred units in determining the average number of units outstanding as the holders of mandatorily convertible preferred units do not participate in current earnings.

In addition to monitoring, analyzing and reviewing earnings performance, we also review initiatives and market conditions that contribute to changes in the fair value of our investment properties. These value changes, combined with earnings, represent a total return on the equity attributable to Unitholders and form an important component in measuring how we have performed relative to our targets.

We also consider the following items to be important drivers of our current and anticipated financial performance:

| |

| • | Increases in occupancies by leasing vacant space; |

| |

| • | Increases in rental rates through maintaining or enhancing the quality of our assets and as market conditions permit; and |

| |

| • | Reductions in operating costs through achieving economies of scale and diligently managing contracts. |

We also believe that key external performance drivers include the availability of the following:

| |

| • | Debt capital at a cost and on terms conducive to our goals; |

| |

| • | Equity capital at a reasonable cost; |

| |

| • | New property acquisitions that fit into our strategic plan; and |

| |

| • | Investors for dispositions of peak value or non-core assets. |

FINANCIAL STATEMENTS ANALYSIS

REVIEW OF CONSOLIDATED FINANCIAL RESULTS

In this section, we review our financial position and consolidated performance as of September 30, 2016 and December 31, 2015 and for the three and nine months ended September 30, 2016 and 2015. Further details on our results from operations and our financial positions are contained within the “Segment Performance” section beginning on page 13.

Our investment approach is to acquire high-quality assets at a discount to replacement cost or intrinsic value. We have been actively pursuing this strategy through our flexibility to allocate capital to real estate sectors and geographies with the best risk-adjusted returns and to participate in transactions through our investments in various Brookfield Asset Management-sponsored real estate funds. Some of the more significant transactions are highlighted below:

Significant Developments through the third quarter of 2016

During the first quarter of 2016, we acquired a portfolio of self-storage facilities across the United States for consideration of approximately $320 million in our Opportunistic sector, including the assumption of debt. In our Core Office segment, we sold World Square Retail in Sydney for A$285 million and a realized gain of $112 million and Royal Centre in Vancouver for C$428 million and a realized gain of $171 million.

During the second quarter of 2016, we acquired a portfolio of student housing properties in the United Kingdom for approximately $397 million, the Vintage Estate hotel and specialty retail center in Napa Valley, CA for $197 million and an additional portfolio of self-storage facilities for consideration of $151 million in our Opportunistic sector.

During the third quarter of 2016, through a fund in which the partnership is a limited partner, we acquired the remaining common shares of Rouse Properties, Inc. (“Rouse”) not previously owned by the partnership. In our Core Office segment, we sold One Shelley Street in Sydney for A$525 million for a realized gain of $132 million. In our Opportunistic sector, we sold a portfolio of hotel assets in Germany for net proceeds of approximately €240 million and a realized gain of $107 million.

Significant Developments through the third quarter of 2015

During the first quarter of 2015, we were successful in expanding our core office platform as a result of the acquisition of a further interest in Canary Wharf using proceeds raised at the end of 2014 through the issuance of preferred shares. We, in conjunction with our joint venture partner Qatar Investment Authority (“QIA”), acquired 100% of Canary Wharf (the “Canary Wharf Transaction”), a 9.5 million square feet office portfolio in London with an 11.5 million square feet development pipeline.

During the second quarter of 2015, we formed Brookfield D.C. Office Partners (“D.C. Fund”), to which we contributed three directly held assets and interests in an additional six assets from our Washington, D.C. office portfolio. We retained a 40% economic interest in the D.C. Fund. We also disposed of a 49% interest in 75 State Street in Boston and now account for the remaining interest as an equity accounted investment.

During the third quarter of 2015, we acquired an interest in Center Parcs Group (“Center Parcs UK”), which operates five short-break destinations across the United Kingdom for consideration of approximately $1,958 million. We also acquired an interest in Associated Estates Realty Corp. (“Associated Estates”), a real estate investment trust focused on apartment communities across the United States for consideration of approximately $2,559 million.

Summary Operating Results

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

| Commercial property revenue | $ | 946 |

| $ | 805 |

| $ | 2,632 |

| $ | 2,396 |

|

| Hospitality revenue | 407 |

| 363 |

| 1,215 |

| 897 |

|

| Investment and other revenue | 56 |

| 99 |

| 142 |

| 293 |

|

| Total revenue | 1,409 |

| 1,267 |

| 3,989 |

| 3,586 |

|

| Direct commercial property expense | 367 |

| 333 |

| 1,008 |

| 968 |

|

| Direct hospitality expense | 254 |

| 240 |

| 783 |

| 642 |

|

| Investment and other expense | — |

| 54 |

| 1 |

| 114 |

|

| Interest expense | 430 |

| 397 |

| 1,247 |

| 1,137 |

|

| Depreciation and amortization | 63 |

| 45 |

| 188 |

| 122 |

|

| General and administrative expense | 146 |

| 174 |

| 415 |

| 406 |

|

| Total expenses | 1,260 |

| 1,243 |

| 3,642 |

| 3,389 |

|

| Fair value gains, net | 86 |

| 245 |

| 709 |

| 1,252 |

|

| Share of earnings from equity accounted investments | 420 |

| 238 |

| 836 |

| 1,051 |

|

| Income before taxes | 655 |

| 507 |

| 1,892 |

| 2,500 |

|

| Income tax (benefit) expense | (961 | ) | 72 |

| (733 | ) | (109 | ) |

| Net income | $ | 1,616 |

| $ | 435 |

| $ | 2,625 |

| $ | 2,609 |

|

| Net income attributable to non-controlling interests of others in operating subsidiaries and properties | 361 |

| 242 |

| 770 |

| 557 |

|

Net income attributable to Unitholders(1) | $ | 1,255 |

| $ | 193 |

| $ | 1,855 |

| $ | 2,052 |

|

| | | | | |

NOI(1) | $ | 732 |

| $ | 595 |

| $ | 2,056 |

| $ | 1,683 |

|

FFO(1) | $ | 209 |

| $ | 165 |

| $ | 643 |

| $ | 499 |

|

Company FFO(1) | $ | 232 |

| $ | 218 |

| $ | 699 |

| $ | 597 |

|

| |

(1) | This is a non-IFRS measure our partnership uses to assess the performance of its operations as described in the “Performance Measures” section on page 3. An analysis of the measures and reconciliation to IFRS measures is included in the “Reconciliation of Non-IFRS measures” section starting on page 9. |

Our basic and diluted net income attributable to Unitholders per unit and weighted average units outstanding are calculated as follows:

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions, except per share information) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

Net income attributable to Unitholders - basic(1) | $ | 1,255 |

| $ | 193 |

| $ | 1,855 |

| $ | 2,052 |

|

| Dilutive effect of conversion of capital securities - corporate | 10 |

| — |

| 30 |

| 36 |

|

| Net income attributable to Unitholders - diluted | $ | 1,265 |

| $ | 193 |

| $ | 1,885 |

| $ | 2,088 |

|

| | | | | |

Weighted average number of units outstanding - basic(1) | 780.9 |

| 782.6 |

| 781.1 |

| 782.7 |

|

| Conversion of capital securities - corporate and options | 30.5 |

| 0.4 |

| 35.9 |

| 40.4 |

|

| Weighted average number of units outstanding - diluted | 811.4 |

| 783.0 |

| 817.0 |

| 823.1 |

|

Net income per unit attributable to Unitholders - basic(1) | $ | 1.61 |

| $ | 0.25 |

| $ | 2.37 |

| $ | 2.62 |

|

| Net income per unit attributable to Unitholders - diluted | $ | 1.56 |

| $ | 0.25 |

| $ | 2.31 |

| $ | 2.54 |

|

| |

(1) | Basic net income attributable to Unitholders per unit requires the inclusion of preferred shares of the Operating Partnership that are mandatorily convertible into LP Units without an add back to earnings of the associated carry on the preferred shares. Net income attributable to Unitholders per unit with the add back of the associated carry on the preferred shares would be $1.64 (2015 - $0.28) per unit and $2.49 (2015 - $2.73) per unit for the three and nine months ended September 30, 2016 and 2015, respectively. |

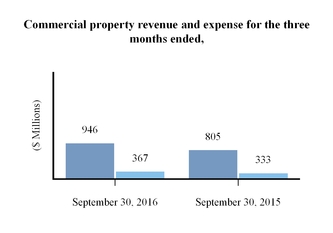

Commercial property revenue and direct commercial property expense

For the three months ended September 30, 2016, commercial property revenue increased by $141 million compared to the same period in the prior year as a result of incremental capital allocated to higher yielding opportunistic investments, same-property growth in our Core Office platform and an increase in our asset base. Acquisitions made in 2015 and 2016, including the privatization of Rouse, Associated Estates, an office portfolio in Brazil, a self-storage portfolio, and a student housing portfolio contributed to a $162 million increase in revenue. These increases were offset by the disposition or partial disposition of mature office assets, some of which resulted in the deconsolidation of certain commercial properties, that provided the capital to pursue the aforementioned acquisitions. Significant dispositions, full or partial, include Royal Centre in Vancouver, Southern Cross East and West in Melbourne, One Shelley Street in Sydney and Manhattan West and One New York Plaza in New York City.

Direct commercial property expense increased by $34 million largely due to additional expenses relating to acquisitions during 2015 and 2016 as mentioned above, partially offset by the disposition of mature assets and the deconsolidation of certain commercial assets. Margins in 2016 were 61.2%, an improvement of 2.6% over 2015.

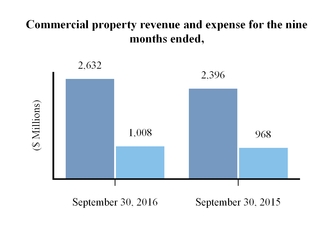

For the nine months ended September 30, 2016, commercial property revenue increased by $236 million compared to the same period in the prior year as a result of acquisition activity, as noted above, and same-property growth in our Core Office platform, particularly in Downtown New York as a result of lease commencements at Brookfield Place New York. Acquisitions made in 2015 and 2016 contributed $323 million of the increase in revenue. These increases were offset by the disposition or partial disposition of mature assets, as noted above.

Direct commercial property expense increased by $40 million largely due to additional expenses relating to acquisitions during 2015 and 2016 as mentioned above, partially offset by the disposition of mature assets and the deconsolidation of certain commercial assets. Margins in 2016 were 61.7%, an improvement of 2.1% over 2015.

Hospitality revenue and direct hospitality expense

Hospitality revenue increased to $407 million for the three months ended September 30, 2016, compared to $363 million in the same period in the prior year. Direct hospitality expense increased to $254 million for the three months ended September 30, 2016, compared to $240 million in the same period in the prior year. Hospitality revenue increased to $1,215 million for the nine months ended September 30, 2016, compared to $897 million in the same period in the prior year. Direct hospitality expense increased to $783 million for the nine months ended September 30, 2016, compared to $642 million in the same period in the prior year. Margins were 37.6% and 35.6% for the three and nine months ended September 30, 2016, respectively. This represents increases of 3.7% and 7.2% over the same periods in the prior year. These increases are primarily related to the acquisition of Center Parcs UK in the third quarter of 2015.

Investment and other revenue and investment and other expense

Investment and other revenue includes management fees, leasing fees, development fees, interest income and other non-rental revenue. Investment and other revenue decreased by $43 million for the three months ended September 30, 2016 as compared to the same period in the prior year. This decrease was primarily due to revenue we recorded in the prior period consisting of development fees earned in our industrial platform of $68 million.

Investment and other revenue decreased by $151 million for the nine months ended September 30, 2016 as compared to the same period in the prior year. This decrease was primarily due to revenue we recorded in the prior period consisting of development fees earned in our industrial platform of $137 million and preferred share dividends received from CXTD of $21 million.

Interest expense

Interest expense increased by $33 million and $110 million for the three and nine months ended September 30, 2016 as compared to the same periods in the prior year, respectively. These increases were due to the assumption of debt obligations as a result of acquisition activity and through incremental debt raised from temporary drawdowns on our credit facilities to source the capital required for acquisitions, partially offset by disposition activity.

General and administrative expense

General and administrative expense decreased by $28 million for the three months ended September 30, 2016 as compared to the same period in the prior year primarily attributable to higher transaction costs in the prior year related to the acquisition of Associated Estates and Center Parcs UK. General and administrative expense increased by $9 million for the nine months ended September 30, 2016 as compared to the same period in the prior year. These increases were primarily attributable to operating costs of newly acquired entities, including Associated Estates, Center Parcs UK, and portfolios of office assets in Brazil, self-storage assets in the United States, and student housing assets in the United Kingdom, offset by higher transaction costs in the prior year.

Fair value gains, net

While we measure and record our commercial properties and developments using valuations prepared by management in accordance with our policy, external appraisals and market comparables, when available, are used to support our valuations.

|

| |

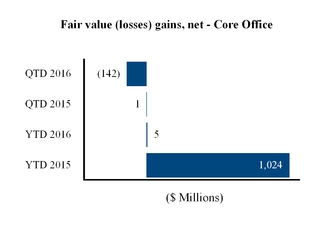

| | Fair value (losses) gains, net for our Core Office sector in the three and nine months ended September 30, 2016 were ($142) million and $5 million, respectively. The valuation loss in the current quarter primarily relates to properties in New York, Calgary and Toronto due to leasing changes.

The prior year included significant fair value gains in New York and Sydney, mainly as a result of cash flow changes, based on leases signed during the period and some discount and capitalization rate compression to reflect improvements in the office markets in the impacted regions. |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

| |

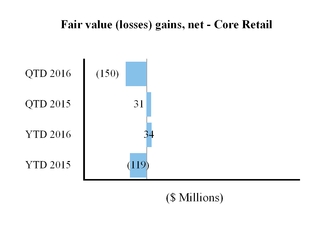

| | Fair value (losses) gains, net for the Core Retail segment relate to the depreciation or appreciation of our warrants in GGP which fluctuate with changes in the market price of the underlying shares. |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

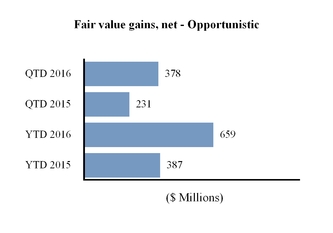

| |

| | Fair value gains, net for the Opportunistic segment in the three and nine months ended September 30, 2016 were $378 million and $659 million, respectively. These were primarily related to fair value gains we recorded from the sale of Hard Rock trademarks of $132 million and the sale of a portfolio of hospitality assets in Germany of $107 million. In addition, the increase is due to fair value gains from our self storage and triple net lease portfolios due to tightening capitalization rates, as supported by comparable market and transaction data. These increases were partially offset by fair value losses in our multifamily portfolio in the Southern United States due to widening capitalization rates. |

| |

| |

| |

| |

| |

| |

| |

| |

| |

In addition, for the three months ended September 30, 2016, we recorded no fair value gains or losses (2015 - fair value losses of $18 million) and for the nine months ended September 30, 2016 we recorded fair value gains of $11 million (2015 - fair value losses of $40 million), primarily related to mark-to-market adjustments of financial instruments and the settlement of derivative contracts during the period.

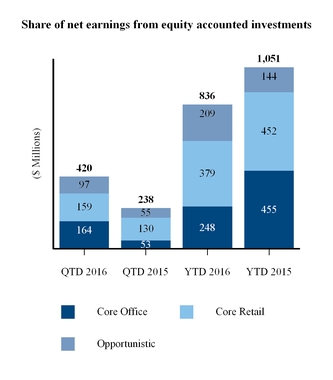

Share of net earnings from equity accounted investments

Our most material equity accounted investments are Canary Wharf in our Core Office sector, GGP in our Core Retail sector and the Diplomat hotel and our interest in the second value-add multifamily fund in our Opportunistic segment.

|

|

Our share of net earnings from equity accounted investments for the three months ended September 30, 2016 of $420 million, represents an increase of $182 million compared to the prior year. The increase was driven by our Core Office sector as a result of fair value gains on properties in the United States compared to fair value losses in the prior period and the mark-to-market adjustment of certain interest rate derivative contracts, of which the loss was greater in the prior period. Also contributing to the increase were higher fair value gains in our Core Retail sector and realized gains on the disposition of a portfolio of industrial properties in our Opportunistic sector.

Our share of net earnings from equity accounted investments for the nine months ended September 30, 2016 of $836 million, represents a decrease of $215 million compared to the prior year. Lower valuation gains were recognized in the current year on a year-to-date basis in our Core Office and Core Retail investments, offset by an increase of fair value gains in our Opportunistic sector, as a result of realized gains from dispositions of industrial and multifamily assets in the current year.

|

Income tax (benefit) expense

During the quarter, we undertook a reorganization to consolidate the ownership of certain subsidiaries holding our core retail and office assets. As a result of the reorganization, there was a change in the tax rate applicable to those subsidiaries, which resulted in a deferred tax recovery during the period, which reduced deferred tax liabilities by approximately $900 million.

Reconciliation of Non-IFRS measures

As described in the “Performance Measures” section on page 3, our partnership uses non-IFRS measures to assess the performance of its operations. An analysis of the measures and reconciliation to IFRS measures is included below.

Commercial property NOI increased by $107 million to $579 million during the three months ended September 30, 2016 compared with $472 million during the same period in the prior year. For the nine months ended September 30, 2016, commercial property NOI increased by $196 million to $1,624 million compared with $1,428 million during the same period in the prior year. The increases are primarily driven by acquisitions across our portfolio and same-property growth, offset by the disposition of mature assets, the deconsolidation of certain assets following partial dispositions thereof and the negative impact of foreign exchange.

Hospitality NOI increased by $30 million to $153 million during the three months ended September 30, 2016 compared with $123 million during the same period in the prior year. For the nine months ended September 30, 2016, hospitality NOI increased by $177 million to $432 million during compared with $255 million during the same period in the prior year. These increases are primarily due to the acquisition of Center Parcs UK.

The following table reconciles NOI to net income for the three and nine months ended September 30, 2016 and 2015:

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

| Commercial property revenue | $ | 946 |

| $ | 805 |

| $ | 2,632 |

| $ | 2,396 |

|

| Direct commercial property expense | (367 | ) | (333 | ) | (1,008 | ) | (968 | ) |

| Commercial property NOI | 579 |

| 472 |

| 1,624 |

| 1,428 |

|

| Hospitality revenue | 407 |

| 363 |

| 1,215 |

| 897 |

|

| Direct hospitality expense | (254 | ) | (240 | ) | (783 | ) | (642 | ) |

| Hospitality NOI | 153 |

| 123 |

| 432 |

| 255 |

|

| Total NOI | 732 |

| 595 |

| 2,056 |

| 1,683 |

|

| Investment and other revenue | 56 |

| 99 |

| 142 |

| 293 |

|

| Share of net earnings from equity accounted investments | 420 |

| 238 |

| 836 |

| 1,051 |

|

| Interest expense | (430 | ) | (397 | ) | (1,247 | ) | (1,137 | ) |

| Depreciation and amortization | (63 | ) | (45 | ) | (188 | ) | (122 | ) |

| General and administrative expense | (146 | ) | (174 | ) | (415 | ) | (406 | ) |

| Investment and other expense | — |

| (54 | ) | (1 | ) | (114 | ) |

| Fair value gains, net | 86 |

| 245 |

| 709 |

| 1,252 |

|

| Income before taxes | 655 |

| 507 |

| 1,892 |

| 2,500 |

|

| Income tax benefit (expense) | 961 |

| (72 | ) | 733 |

| 109 |

|

| Net income | $ | 1,616 |

| $ | 435 |

| $ | 2,625 |

| $ | 2,609 |

|

| Net income attributable to non-controlling interests | 361 |

| 242 |

| 770 |

| 557 |

|

| Net income attributable to Unitholders | $ | 1,255 |

| $ | 193 |

| $ | 1,855 |

| $ | 2,052 |

|

The following table reconciles net income to FFO and Company FFO for the three and nine months ended September 30, 2016 and 2015:

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

| Net income | $ | 1,616 |

| $ | 435 |

| $ | 2,625 |

| $ | 2,609 |

|

| Add (deduct): | | | | |

| Fair value gains, net | (86 | ) | (245 | ) | (709 | ) | (1,252 | ) |

| Share of equity accounted fair value gains, net | (230 | ) | (59 | ) | (208 | ) | (542 | ) |

| Depreciation and amortization of real estate assets | 55 |

| 39 |

| 170 |

| 104 |

|

| Income tax (benefit) expense | (961 | ) | 72 |

| (733 | ) | (109 | ) |

| Non-controlling interests in above items | (185 | ) | (77 | ) | (502 | ) | (311 | ) |

| FFO | $ | 209 |

| $ | 165 |

| $ | 643 |

| $ | 499 |

|

| Add (deduct): | | | | |

Depreciation and amortization of real-estate assets, net(1) | 7 |

| 7 |

| 18 |

| 20 |

|

Transaction costs, net(1) | 15 |

| 33 |

| 34 |

| 58 |

|

Gains/losses associated with non-investment properties, net(1) | (11 | ) | 2 |

| (31 | ) | (12 | ) |

Net contribution from GGP warrants(2) | 12 |

| 11 |

| 35 |

| 32 |

|

| Company FFO | $ | 232 |

| $ | 218 |

| $ | 699 |

| $ | 597 |

|

| |

(1) | Presented net of non-controlling interests. |

| |

(2) | Represents incremental FFO that would have been attributable to the partnership’s share of GGP, if all outstanding warrants of GGP had been exercised on a cashless basis. It also includes the dilution adjustments to FFO as a result of the net settled warrants. |

FFO increased to $209 million during the three months ended September 30, 2016 compared with $165 million during the same period in the prior year. For the nine months ended September 30, 2016, FFO increased to $643 million compared with $499 million during the same period in the prior year. These increases were driven by acquisition activity since the prior period, including Rouse, Associated Estates, an office portfolio in Brazil, a self-storage portfolio in the U.S., and Center Parcs UK, as well as positive same-property growth in our Core Office and Core Retail sectors. These increases were partially offset by the negative impact of foreign exchange rate fluctuations on our earnings from operations outside of the U.S.

Statement of Financial Position Highlights and Key Metrics

|

| | | | | | |

| (US$ Millions) | Sep. 30, 2016 |

| Dec. 31, 2015 |

|

| Investment properties | | |

| Commercial properties | $ | 42,234 |

| $ | 39,111 |

|

| Commercial developments | 2,993 |

| 2,488 |

|

| Equity accounted investments | 16,830 |

| 17,638 |

|

| Hospitality assets | 4,880 |

| 5,016 |

|

| Cash and cash equivalents | 1,562 |

| 1,035 |

|

| Assets held for sale | 3,033 |

| 805 |

|

| Total assets | 77,650 |

| 71,866 |

|

| Debt obligations | 31,790 |

| 30,526 |

|

| Liabilities associated with assets held for sale | 1,726 |

| 242 |

|

| Total equity | 34,476 |

| 30,933 |

|

| Equity attributable to Unitholders | $ | 22,616 |

| $ | 21,958 |

|

Equity per unit(1) | $ | 30.98 |

| $ | 30.09 |

|

(1) Assumes conversion of mandatorily convertible preferred shares. See page 12 for additional information.

As of September 30, 2016, we had $77,650 million in total assets, compared with $71,866 million at December 31, 2015. This $5,784 million increase reflects acquisition activity since the prior year, including the acquisition of our self-storage platform and student housing portfolio. In addition, following the acquisition of incremental interests in Rouse, we are now consolidating this investment, which was previously accounted for under the equity method.

Our investment properties are comprised of commercial, operating, rent-producing properties and commercial developments including active sites and those in planning for future development and land. Commercial properties increased from $39,111 million at the end of 2015 to $42,234 million at September 30, 2016. The increase was largely due to the acquisition of Rouse, our self-storage and student housing portfolios, as well as incremental capital spend to maintain or enhance properties and the impact of foreign exchange. This was offset by the full or partial disposition of certain assets during the year, and the reclassification of certain properties to assets held for sale.

Commercial developments consist of commercial property development sites, density rights and related infrastructure. The total fair value of commercial developments was $2,993 million at September 30, 2016, an increase of $505 million from the balance at December 31, 2015. The increase is primarily attributable to acquisitions of development properties and additional capital spend on our active developments.

The following table presents the changes in investment properties from December 31, 2015 to September 30, 2016:

|

| | | | | | |

| Sep. 30, 2016 |

| (US$ Millions) | Commercial properties |

| Commercial developments |

|

| Commercial properties, beginning of period | $ | 39,111 |

| $ | 2,488 |

|

| Acquisitions | 5,686 |

| 254 |

|

| Capital expenditures | 536 |

| 629 |

|

| Dispositions | (230 | ) | (9 | ) |

| Fair value gains, net | 294 |

| 158 |

|

| Foreign currency translation | 501 |

| (138 | ) |

| Reclassifications to assets held for sale and other changes | (3,664 | ) | (389 | ) |

| Commercial properties, end of period | $ | 42,234 |

| $ | 2,993 |

|

Equity accounted investments, decreased by $808 million since December 31, 2015 primarily due to the reclassification of Rouse to our consolidated results following its privatization in July of the current year and disposition activity, including the sale of our German hotel portfolio and a portfolio of industrial assets in the United States. In addition, the decrease reflects the weakening of the British Pound against the U.S. Dollar, primarily related to our investment in Canary Wharf.

The following table presents a roll-forward of changes in our equity accounted investments:

|

| | | |

| (US$ Millions) | Sep. 30, 2016 |

|

| Equity accounted investments, beginning of period | $ | 17,638 |

|

| Additions | 382 |

|

Disposals and return of capital distributions

| (766 | ) |

| Share of net income | 836 |

|

| Distributions received | (278 | ) |

| Foreign exchange | (410 | ) |

| Reclassification to assets held for sale | (544 | ) |

| Other | (28 | ) |

| Equity accounted investments, end of period | $ | 16,830 |

|

Hospitality assets decreased by $136 million since December 31, 2015, primarily as a result of depreciation expense during the period ended September 30, 2016 and the impact of foreign exchange related to our Center Parcs UK portfolio, offset by capital spend on the properties.

As of September 30, 2016, assets held for sale included three properties in our Core Office segment, as well as five industrial assets in Spain, Italy, and China and a portfolio of multifamily assets in the United States, as we intend to sell controlling interests in these properties to third parties in the next 12 months.

Our debt obligations increased to $31,790 million at September 30, 2016 from $30,526 million at December 31, 2015. Contributing to this increase was the addition of property-specific borrowings related to acquisition activity during the period, as noted above. These increases were partially offset by the disposition of encumbered assets during the period and the repayment of temporary draws on credit facilities used to fund these acquisitions.

The following table presents additional information on our partnership’s outstanding debt obligations:

|

| | | | | | |

| (US$ Millions) | Sep. 30, 2016 |

| Dec. 31, 2015 |

|

| Corporate borrowings | $ | 1,830 |

| $ | 1,632 |

|

| Funds subscription facilities | 529 |

| 1,594 |

|

| Non-recourse borrowings | | |

| Property-specific borrowings | 27,753 |

| 25,938 |

|

| Subsidiary borrowings | 1,678 |

| 1,362 |

|

| Total debt obligations | $ | 31,790 |

| $ | 30,526 |

|

| Current | 4,624 |

| 8,580 |

|

| Non-current | 27,166 |

| 21,946 |

|

| Total debt obligations | $ | 31,790 |

| $ | 30,526 |

|

The following table presents the components used to calculate equity attributable to Unitholders per unit:

|

| | | | | | |

| (US$ Millions, except unit information) | Sep. 30, 2016 |

| Dec. 31, 2015 |

|

| Total equity | $ | 34,476 |

| $ | 30,933 |

|

| Less: | | |

| Interests of others in operating subsidiaries and properties | 11,860 |

| 8,975 |

|

| Equity attributable to Unitholders | 22,616 |

| 21,958 |

|

| Mandatorily convertible preferred shares | 1,570 |

| 1,554 |

|

| Total equity attributable to Unitholders | 24,186 |

| 23,512 |

|

| Partnership units | 710,669,704 |

| 711,412,925 |

|

| Mandatorily convertible preferred shares | 70,038,910 |

| 70,038,910 |

|

| Total partnership units | 780,708,614 |

| 781,451,835 |

|

| Equity attributable to Unitholders per unit | $ | 30.98 |

| $ | 30.09 |

|

Equity attributable to Unitholders was $22,616 million at September 30, 2016, an increase of $658 million from the balance at December 31, 2015. Assuming the conversion of mandatorily convertible preferred shares, equity attributable to unitholders increased to $30.98 per unit at September 30, 2016 from $30.09 per unit at December 31, 2015. The increase was due to current period net income, as noted above, partially offset by the impact of foreign exchange.

Interests of others in operating subsidiaries and properties was $11,860 million at September 30, 2016, an increase of $2,885 million from the balance of $8,975 million at December 31, 2015. The increase was primarily a result of the acquisition of new investments through

Brookfield Asset Management-sponsored funds in which the partnership is a limited partner and additional closes on the second opportunity fund reducing our interests therein.

SUMMARY OF QUARTERLY RESULTS

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| | 2016 | 2015 | 2014 |

| (US$ Millions, except per unit information) | Q3 |

| Q2 |

| Q1 |

| Q4 |

| Q3 |

| Q2 |

| Q1 |

| Q4 |

|

| Revenue | $ | 1,409 |

| $ | 1,333 |

| $ | 1,247 |

| $ | 1,267 |

| $ | 1,267 |

| $ | 1,170 |

| $ | 1,149 |

| $ | 1,070 |

|

| Direct operating costs | 621 |

| 594 |

| 576 |

| 573 |

| 573 |

| 504 |

| 533 |

| 524 |

|

| Net income | 1,616 |

| 569 |

| 440 |

| 1,157 |

| 435 |

| 1,165 |

| 1,009 |

| 1,595 |

|

| Net income attributable to unitholders | 1,255 |

| 349 |

| 251 |

| 863 |

| 193 |

| 1,026 |

| 833 |

| 1,492 |

|

| Net income per share attributable to unitholders - basic | $ | 1.61 |

| $ | 0.45 |

| $ | 0.32 |

| $ | 1.10 |

| $ | 0.25 |

| $ | 1.31 |

| $ | 1.06 |

| $ | 2.09 |

|

| Net income per share attributable to unitholders - diluted | $ | 1.56 |

| $ | 0.44 |

| $ | 0.32 |

| $ | 1.06 |

| $ | 0.25 |

| $ | 1.26 |

| $ | 1.02 |

| $ | 1.97 |

|

Revenue varies from quarter to quarter due to acquisitions and dispositions of commercial and other income producing assets, changes in occupancy levels, as well as the impact of leasing activity at market net rents. In addition, revenue also fluctuates as a result of changes in foreign exchange rates and seasonality. Seasonality primarily affects our retail assets, wherein the fourth quarter exhibits stronger performance in conjunction with the holiday season. In addition, our North American hospitality assets generally have stronger performance in the winter and spring months compared to the summer and fall months, while our European hospitality assets exhibit the strongest performance during the summer months. Fluctuations in our net income is also impacted by the fair value of properties in the period to reflect changes in valuation metrics driven by market conditions or property cash flows.

SEGMENT PERFORMANCE

Our operations are organized into four operating segments which include Core Office, Core Retail, Opportunistic and Corporate.

The following table presents FFO by segment for comparison purposes:

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

| Core Office | $ | 142 |

| $ | 155 |

| $ | 445 |

| $ | 422 |

|

| Core Retail | 95 |

| 96 |

| 297 |

| 280 |

|

| Opportunistic | 97 |

| 38 |

| 262 |

| 162 |

|

| Corporate | (125 | ) | (124 | ) | (361 | ) | (365 | ) |

| FFO | $ | 209 |

| $ | 165 |

| $ | 643 |

| $ | 499 |

|

The following table presents equity attributable to Unitholders by segment as of September 30, 2016 and December 31, 2015:

|

| | | | | | |

| (US$ Millions) | Sep. 30, 2016 |

| Dec. 31, 2015 |

|

| Core Office | $ | 15,196 |

| $ | 15,984 |

|

| Core Retail | 8,852 |

| 8,579 |

|

| Opportunistic | 4,429 |

| 4,251 |

|

| Corporate | (5,861 | ) | (6,856 | ) |

| Total | $ | 22,616 |

| $ | 21,958 |

|

Core Office

Our Core Office segment consists of interests in 149 office properties totaling approximately 101 million square feet, which are located primarily in the world’s leading commercial markets such as New York, London, Los Angeles, Washington, D.C., Sydney, Toronto and Berlin among others and consists primarily of our 100% common share interest in BPO and our 50% joint venture interest in Canary Wharf.

The following table presents FFO and net income attributable to Unitholders in our Core Office segment for the three and nine months ended September 30, 2016 and 2015:

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

| FFO | $ | 142 |

| $ | 155 |

| $ | 445 |

| $ | 422 |

|

| Net income attributable to Unitholders | 141 |

| 112 |

| 495 |

| 1,966 |

|

FFO from our Core Office segment was $142 million for the three months ended September 30, 2016 as compared to $155 million in the same period in the prior year. The decrease is largely attributable to asset dispositions, offset by same-property growth, particularly at Brookfield Place New York. For the nine months ended September 30, 2016, FFO from our Core Office segment was $445 million as compared to $422 million in the same period in the prior year. This increase is largely attributable to rental income being recognized from the lease-up of vacant space at Brookfield Place New York, offset by the impact of asset sales.

Net income attributable to Unitholders increased by $29 million to $141 million during the three months ended September 30, 2016 as compared to $112 million during the same period in 2015. This increase was primarily attributable to higher share of earnings from equity accounted investments as a result of mark-to-market adjustments on certain derivative contracts partially offset by fair value losses in the current year as a result of leasing changes in New York, Calgary and Toronto.

Net income attributable to Unitholders decreased by $1,471 million to $495 million during the nine months ended September 30, 2016 as compared to $1,966 million during the same period in 2015. The decrease was primarily a result of higher fair value gains recorded in the prior period due to the strengthening of market conditions and leasing during the period primarily in New York, London and Sydney, as well as a gain upon contribution of our prior 22% interest in Canary Wharf to our joint venture with QIA in the prior year. This decrease was offset by an income tax benefit as a result of a reorganization of our interests in certain subsidiaries that resulted in a reduction in the tax rate applied to these subsidiaries and higher fair value losses on certain interest rate derivative contracts in the prior year.

The following table presents key operating metrics for our Core Office portfolio as at and for the three months ended September 30, 2016 and 2015:

|

| | | | | | | | | | | | |

| | Consolidated | Unconsolidated |

| (US$ Millions, except where noted) | Sep. 30, 2016 |

| Sep. 30, 2015 |

| Sep. 30, 2016 |

| Sep. 30, 2015 |

|

| Total portfolio: | | | | |

NOI(1) | $ | 284 |

| $ | 292 |

| $ | 110 |

| $ | 110 |

|

| Number of properties | 81 |

| 91 |

| 68 |

| 47 |

|

| Leasable square feet (in thousands) | 54,106 |

| 57,323 |

| 27,120 |

| 21,773 |

|

| Occupancy | 89.9 | % | 91.7 | % | 94.4 | % | 96.1 | % |

In-place net rents (per square foot)(2) | $ | 27.84 |

| $ | 27.95 |

| $ | 40.80 |

| $ | 39.67 |

|

| Same-property: | | | | |

NOI(1,2) | $ | 264 |

| $ | 251 |

| $ | 95 |

| $ | 94 |

|

| Number of properties | 67 |

| 67 |

| 41 |

| 41 |

|

| Leasable square feet (in thousands) | 52,611 |

| 52,765 |

| 19,568 |

| 19,548 |

|

| Occupancy | 90.3 | % | 91.6 | % | 96.3 | % | 96.3 | % |

In-place net rents (per square foot)(2) | $ | 27.90 |

| $ | 26.81 |

| $ | 50.06 |

| $ | 49.08 |

|

(1) NOI for unconsolidated properties is presented on a proportionate basis, representing the Unitholders’ interest in the property.

(2) Prior period presented using the September 30, 2016 exchange rate.

NOI from our consolidated properties decreased to $284 million during the three months ended September 30, 2016 from $292 million during the same period in 2015. This decrease was primarily due to the negative impact of foreign exchange and dispositions in New York, Boston, Seattle, Vancouver, Melbourne, Sydney and Toronto, offset by the incremental NOI contribution from new leases, primarily in Downtown New York.

Same-property NOI for our consolidated properties for the three months ended September 30, 2016 compared with the same period in the prior year increased by $13 million to $264 million. This increase was primarily the result of lease commencements in Downtown New York and higher in-place net rents.

NOI from our unconsolidated properties, which is presented on a proportionate basis, was unchanged at $110 million during the three months ended September 30, 2016, compared to the prior year. This reflects a full quarter of NOI from assets that have been deconsolidated since September 2015, offset by lower occupancy rates which decreased to 94.4% from 96.1% primarily as a result of the acquisition of a portfolio in Berlin, where occupancy is lower than in the remainder of the unconsolidated portfolio.

The following table presents certain key operating metrics related to leasing activity in our Core Office segment for the three months ended September 30, 2016 and 2015:

|

| | | | | | |

| | Total portfolio |

| (US$ Millions, except where noted) | Sep. 30, 2016 |

| Sep. 30, 2015 |

|

| Leasing activity (square feet in thousands) | | |

| New leases | 1,298 |

| 844 |

|

| Renewal leases | 1,115 |

| 949 |

|

| Total leasing activity | 2,413 |

| 1,793 |

|

| Average term (in years) | 8.1 |

| 8.4 |

|

Year one leasing net rents (per square foot)(1) | $ | 30.73 |

| $ | 33.87 |

|

Average leasing net rents (per square foot)(1) | 34.50 |

| 35.79 |

|

Expiring net rents (per square foot)(1) | 29.39 |

| 29.14 |

|

Estimated market net rents for similar space (per square foot)(1) | 38.74 |

| 38.99 |

|

| Tenant improvement and leasing costs (per square foot) | 71.59 |

| 34.47 |

|

(1) Presented using normalized foreign exchange rates, using the September 30, 2016 exchange rate.

For the three months ended September 30, 2016, we leased over 2.4 million square feet at average in-place net rents of $34.50 per square foot. Approximately 54% of our leasing activity represented new leases. Our overall Core Office portfolio’s in-place net rents are currently 17% below market net rents, which gives us confidence that we will be able to increase our NOI in the coming years, as we sign new leases. For the three months ended September 30, 2016, tenant improvements and leasing costs related to leasing activity were $71.59 per square foot, compared to $34.47 per square foot in the prior year.

We calculate net rent as the annualized amount of cash rent receivable from leases on a per square foot basis including tenant expense reimbursements, less operating expenses being incurred for that space, excluding the impact of straight-lining rent escalations or amortization of free rent periods. This measure represents the amount of cash, on a per square foot basis, generated from leases in a given period.

The following table presents fair value gains (losses) from consolidated and unconsolidated investments in our Core Office segment for the three and nine months ended September 30, 2016 and 2015:

|

| | | | | | | | | | | | |

| | Three months ended Sep. 30, | | Nine months ended Sep. 30, | |

| (US$ Millions) | 2016 |

| 2015 |

| 2016 |

| 2015 |

|

| Consolidated properties | $ | (142 | ) | $ | 1 |

| $ | 5 |

| $ | 1,024 |

|

Unconsolidated properties(1) | 96 |

| (14 | ) | 30 |

| 313 |

|

| Total fair value (losses) gains, net | $ | (46 | ) | $ | (13 | ) | $ | 35 |

| $ | 1,337 |

|

(1) Fair value gains for unconsolidated properties are presented on a proportionate basis, representing the Unitholders’ interest in the investment.

We recorded fair value losses, net of $(46) million in the three months ended September 30, 2016 as compared to $(13) million in the same period in the prior year. For the nine months ended September 30, 2016, we recorded fair value gains, net of $35 million as compared to $1,337 million in the same period in the prior year. The losses were driven by fair value losses in our New York, Calgary and Toronto office portfolios, as a result of leasing changes. The prior year included fair value gains in our U.S. and Australian office portfolio, mainly as a result of cash flow changes and discount and terminal capitalization rate compression, as well as a gain upon contributing our prior interest in Canary Wharf to our joint venture with QIA. These gains were partially offset by fair value losses on certain derivative contracts within our investment in Canary Wharf within unconsolidated properties.

The key valuation metrics for commercial properties in our Core Office segment on a weighted-average basis are as follows:

|

| | | | | | | | | | | |

| | Sep. 30, 2016 | Dec. 31, 2015 |

| | Discount rate |

| Terminal capitalization rate |

| Investment horizon | Discount rate |

| Terminal capitalization rate |

| Investment horizon |

|

| Consolidated properties | | | | | | |

| United States | 7.0 | % | 5.6 | % | 12 | 6.9 | % | 5.7 | % | 12 |

|

| Canada | 6.2 | % | 5.6 | % | 10 | 6.1 | % | 5.5 | % | 10 |

|

| Australia | 7.4 | % | 6.2 | % | 10 | 7.6 | % | 6.2 | % | 10 |

|

| Europe | 6.0 | % | 5.0 | % | 12 | 6.0 | % | 5.1 | % | 12 |

|

| Brazil | 9.3 | % | 7.5 | % | 10 | 9.3 | % | 7.5 | % | 10 |

|

| Unconsolidated properties | | | | | | |

| United States | 6.5 | % | 5.4 | % | 11 | 6.3 | % | 5.3 | % | 11 |

|

| Australia | 7.3 | % | 6.4 | % | 10 | 7.4 | % | 6.1 | % | 10 |

|

Europe(1) | 5.1 | % | 5.0 | % | 10 | 5.1 | % | 5.1 | % | 10 |

|

| |

(1) | Certain properties in Europe accounted for under the equity method are valued using both discounted cash flow and yield models. For comparative purposes, the discount and terminal capitalization rates and investment horizon calculated under the discounted cash flow method are presented in the table above. |

The following table provides an overview of the financial position of our Core Office segment as at September 30, 2016 and December 31, 2015:

|

| | | | | | |

| (US$ Millions) | Sep. 30, 2016 |

| Dec. 31, 2015 |

|

| Investment properties | | |

| Commercial properties | $ | 23,351 |

| $ | 25,048 |

|

| Commercial developments | 2,170 |

| 1,627 |

|

| Equity accounted investments | 7,438 |

| 7,697 |

|

| Participating loan interests | 510 |

| 449 |

|

| Accounts receivable and other | 790 |

| 783 |

|

| Cash and cash equivalents | 402 |

| 430 |

|

| Assets held for sale | 1,880 |

| 506 |

|

| Total assets | $ | 36,541 |

| $ | 36,540 |

|

| Debt obligations | 13,540 |

| 13,818 |

|

| Capital securities | 1,075 |

| 1,151 |

|

| Accounts payable and other liabilities | 1,517 |

| 1,583 |

|

| Deferred tax liability | 1,123 |

| 1,193 |

|

| Liabilities associated with assets held for sale | 1,001 |

| 105 |

|

| Non-controlling interests of others in operating subsidiaries and properties | 3,089 |

| 2,706 |

|

| Equity attributable to Unitholders | $ | 15,196 |

| $ | 15,984 |

|

Equity attributable to Unitholders decreased by $788 million to $15,196 million at September 30, 2016 from $15,984 million at December 31, 2015. The decrease was primarily a result of reinvesting the net proceeds from the sale of One New York Plaza, World Square Retail and One Shelley Street in Sydney and Royal Centre in Vancouver, as well as upfinancings within our Core Office portfolio.

Commercial properties totaled $23,351 million at September 30, 2016, compared to $25,048 million at December 31, 2015. The decrease was primarily due to the disposition or reclassification of properties to assets held for sale.

Commercial developments increased by $543 million between December 31, 2015 and September 30, 2016. The increase is as a result of incremental capital expenditures on existing commercial developments as well as acquisition activity during the period.

The following table summarizes the scope and progress of active developments in our Core Office segment as of September 30, 2016:

|

| | | | | | | | | | | | | | | | | | | |

| | Total |

| Proportionate |

| | | Cost | Loan |

| (Millions, except square feet in thousands) | square feet under construction (in 000’s) |

| square feet under construction (in 000’s) |

| Expected date of cash stabilization | Percent pre-leased |

| Total(1) |

| To-date |

| Total |

| Drawn |

|

| Office: | | | | | | | | |

| L’Oréal Brazil Headquarters, Rio de Janeiro | 197 |

| 92 |

| Q4 2017 | 100 | % | R$ | 137 |

| R$ | 77 |

| R$ | — |

| R$ | — |

|

| Brookfield Place East Tower, Calgary | 1,400 |

| 1,400 |

| Q3 2018 | 81 | % | C$ | 799 |

| C$ | 564 |

| C$ | 575 |

| C$ | 291 |

|

| Principal Place - Commercial, London | 621 |

| 621 |

| Q1 2020 | 84 | % | £ | 376 |

| £ | 270 |

| £ | 280 |

| £ | 170 |

|

London Wall Place, London(2) | 505 |

| 253 |

| Q2 2020 | 73 | % | £ | 203 |

| £ | 146 |

| £ | 137 |

| £ | 72 |

|

One Manhattan West, Midtown New York(2) | 2,117 |

| 1,186 |

| Q4 2020 | 30 | % | $ | 1,063 |

| $ | 259 |

| $ | 700 |

| $ | 73 |

|

655 New York Avenue, Washington, D.C.(2) | 766 |

| 383 |

| Q2 2021 | 70 | % | $ | 285 |

| $ | 99 |

| $ | 200 |

| $ | 34 |

|

| 100 Bishopsgate, London | 938 |

| 938 |

| Q4 2021 | 38 | % | £ | 875 |

| £ | 373 |

| £ | 515 |

| £ | 46 |

|

1 Bank Street, London(2) | 715 |

| 358 |

| Q1 2023 | 40 | % | £ | 247 |

| £ | 69 |

| £ | 183 |

| £ | — |

|

| Multifamily: | | | | | | | | |

Three Manhattan West, Midtown New York(2) | 587 |

| 329 |

| Q3 2018 | n/a |

| $ | 414 |

| $ | 296 |

| $ | 268 |

| $ | 130 |

|

| Camarillo, California | 413 |

| 409 |

| Q1 2019 | n/a |

| $ | 127 |

| $ | 49 |

| $ | 83 |

| $ | 3 |

|

| Greenpoint Landing Building G, New York | 250 |

| 238 |

| Q4 2019 | n/a |

| $ | 273 |

| $ | 76 |

| $ | 179 |

| $ | — |

|

Newfoundland, London(2) | 546 |

| 273 |

| Q4 2020 | n/a |

| £ | 242 |

| £ | 84 |

| £ | 174 |

| £ | — |

|

Principal Place - Residential, London(2) | 303 |

| 152 |

| n/a | n/a |

| £ | 190 |

| £ | 61 |

| £ | 122 |

| £ | 6 |

|

Shell Centre - Residential, London(2) | 529 |

| 132 |

| n/a | n/a |

| £ | 164 |

| £ | 62 |

| £ | 96 |

| £ | 15 |

|

| Total | 9,887 |

| 6,764 |

| | | | | | |

| |

(1) | Net of NOI earned during stabilization. |

| |

(2) | Presented on a proportionate basis at our ownership interest in each of these developments. |

The following table presents changes in our partnership’s equity accounted investments in the Core Office segment from December 31, 2015 to September 30, 2016:

|

| | | |

| (US$ Millions) | Sep. 30, 2016 |

|

| Equity accounted investments, beginning of period | $ | 7,697 |

|

| Additions | 229 |

|

| Disposals and return of capital distributions | (81 | ) |

| Share of net income, including fair value gains | 248 |

|

| Distributions received | (68 | ) |

| Foreign exchange | (394 | ) |

| Reclassification to assets held for sale | (205 | ) |

| Other | 12 |

|

| Equity accounted investments, end of period | $ | 7,438 |

|

Equity accounted investments decreased by $259 million since December 31, 2015 to $7,438 million at September 30, 2016. The decrease was primarily driven by the impact of the weakening British Pound, reclassifications to assets held for sale and disposition activity.

At September 30, 2016, we have three properties in New York, Washington, D.C., and London classified as assets held for sale as we intend to sell controlling interests in these properties to third parties in the next 12 months. Assets held for sale at December 31, 2015 consisted of properties in Sydney and Vancouver and have since been disposed of.

Debt obligations decreased from $13,818 million at December 31, 2015 to $13,540 million at September 30, 2016. This decrease is the result of the repayment of debt following the disposition of certain properties and the impact of foreign exchange, offset by refinancing activity of property-level debt related to office properties and drawdowns on existing facilities to fund capital expenditures on development properties.

The following table provides additional information on our outstanding capital securities – Core Office:

|

| | | | | | | | | | |

| (US$ Millions) | Shares outstanding |

| Cumulative dividend rate |

| Sep. 30, 2016 |

| Dec. 31, 2015 |

|

| BPO Class AAA Preferred Shares: | | | | |

Series G(1) | 3,236,308 |

| 5.25 | % | $ | 81 |

| $ | 84 |

|

Series H(2) | — |

| 5.75 | % | — |

| 128 |

|

Series J(1) | 6,592,443 |

| 5.00 | % | 125 |

| 125 |

|

Series K(1) | 4,995,414 |

| 5.20 | % | 95 |

| 90 |

|

| BPO Class B Preferred Shares: | | | | |

Series 1(3) | 3,600,000 |

| 70% of bank prime |

| — |

| — |

|

Series 2(3) | 3,000,000 |

| 70% of bank prime |

| — |

| — |

|

| Capital Securities – Fund Subsidiaries | | | 774 |

| 724 |

|

| Total capital securities | | | $ | 1,075 |

| $ | 1,151 |

|

| |

(1) | BPY and its subsidiaries own 1,003,549, 1,000,000, and 1,004,586 shares of Series G, Series J, and Series K Class AAA preferred shares of BPO as of September 30, 2016, respectively, which has been reflected as a reduction in outstanding shares of the BPO Class AAA Preferred Shares. |

| |