UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22710

BLUEROCK TOTAL INCOME+ REAL ESTATE FUND

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, 32nd Floor, New York, NY 10105

(Address of principal executive offices) (Zip code)

Bluerock Fund Advisor, LLC

1345 Avenue of the Americas, 32nd Floor,

New York, NY 10105

(Name and address of agent for service)

1-844-819-8287

(Registrant’s telephone number, including area code)

Date of fiscal year end: September 30

Date of reporting period: March 31, 2023

| Item | 1. Reports to Stockholders. |

(a)

TABLE OF CONTENTS

| Shareholder Letter | 1 |

| Portfolio Review | 10 |

| Portfolio of Investments | 12 |

| Statement of Assets and Liabilities | 15 |

| Statement of Operations | 16 |

| Statements of Changes in Net Assets | 17 |

| Statement of Cash Flows | 19 |

| Financial Highlights | 20 |

| Notes to Financial Statements | 26 |

| Renewal of Investment Advisory Agreement and Sub-Advisory Agreements | 38 |

| Additional Information | 41 |

| Change in Independent Registered Public Accounting Firm | 42 |

| Privacy Policy | 43 |

SEMI-ANNUAL REPORT: (4Q 2022-1Q 2023) (UNAUDITED)

Letter from the TI+ Portfolio Managers

To Our Valued Shareholders: We are pleased to provide you with an update on the Bluerock Total Income+ Real Estate Fund (“TI+” or the “Fund”) for the six-months ended March 31, 2023. Consistent with other asset classes, the private real estate market has been adjusting to the broader, higher-interest rate economic environment, and did so more significantly in Q4 2022 and Q1 2023. While transactions have slowed considerably, recent data indicate that the private real estate market has largely incorporated the effect of higher interest rates, and the market appears to have acknowledged a sustained, higher rate period with widening transaction cap rates. Accordingly, real estate valuations have followed suit, with cap rates increasing to create a return premium above the riskless rate (the 10-year U.S. Treasury yield). Importantly, real estate fundamentals in the Fund’s high conviction sectors remain positive, with strong rent growth providing support for valuations. We believe the Fund’s strategic overweight to the industrial sector, in particular, has the opportunity for outsized income growth going forward as favorable supply-demand factors persist. The Fund is conservatively positioned with low underlying leverage of 30%. Throughout the 10+ years of the Fund’s history, we have navigated a variety of economic and political environments, and we believe the Fund is well positioned for the next market expansion. |  |

Looking back on the Fund’s prior six months ending March 31, 2023, we note the following highlights:

| FUND HIGHLIGHTS |

| | |

| ASSET MANAGER OF THE YEAR FINALIST: Bluerock Fund Advisor, the Fund’s manager, is proud to report that it was selected as one of three finalists for 2022 Asset Manager of the Year from the Money Management Institute and Barron’s (AUM <$25 billion category). The award recognizes innovation and leadership in the investment advisory solutions industry and honors the asset manager that best exemplifies innovation in delivering better outcomes for investors and financial advisors. |

| | |

| ACTIVELY MANAGED THE PORTFOLIO IN HIGH CONVICTION SECTORS: 92% of the Fund’s underlying portfolio is in industrial, residential, life sciences, and specialty sectors.

|

| | |

| INDEX OUTPERFORMANCE: The Fund (TIPWX) has outperformed the NCREIF ODCE Index by at least 120 basis points over each of the trailing 1, 2, 3, 4, 5 and 7-year time periods, demonstrating the consistent success of the Fund’s strategy over both short- and longer-term periods. |

| | |

| | PAID 41 CONSECUTIVE DISTRIBUTIONS AT A 5.25% ANNUAL RATE* |

| | |

| * | see full distribution disclosure on page 4. |

Past Performance is not a guarantee of future results.

CORPORATE HEADQUARTERS | 1345 AVENUE OF THE AMERICAS | 32ND FLOOR | NEW YORK, NY 10105 | 877.826.BLUE (2583) | BLUEROCK.COM

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

Market Overview:

The Financial Stability Report by the Board of Governors of the Federal Reserve from May 2023 notes that losses on CRE loans will depend on their leverage because owners of buildings with substantial equity cushions are less likely to default. The Report additionally states, LTVs were low for many mortgages because for most property types—office & retail being notable exceptions—values rose materially in the years leading up to the pandemic.

The chart below reflects the lower overall LTV ratios on commercial real estate over the last several years, a reflection of the conservative underwriting standards upheld by various lenders (right hand side), in stark contrast to the years preceding the Great Financial Crisis (left hand side).

Significantly Lower Loan-to-Value (LTV) Ratios in Recent Years vs. Pre-GFC Years

Source: American Council of Life Insurers, Moody’s Analytics

| KEY DRIVERS OF REAL ESTATE PERFORMANCE |

| | |

| LIMITED NEW SUPPLY New real estate supply as a percentage of total inventory is the lowest it has been in the trailing 10-year period compared to previous periods and is forecasted to remain at lower levels.1 |

| | |

| LOW LEVERAGE The use of leverage in the post Great Financial Crisis recovery from 2010-2019 has been the lowest of any real estate/economic recovery in the last 40+ years.2

|

| | |

| |

| HIGH EMPLOYMENT The U.S. unemployment rate was a low 3.5% as of March 2023, near the lowest level since 1969.3 |

| | |

Portfolio Construction

For the past several years, we have positioned the underlying portfolio to minimize expose to the office and retail sectors in favor of industrial, residential, life science, and specialty sectors. Compared to the institutional real estate benchmark (NCREIF ODCE), the portfolio is heavily overweight our high conviction sectors, which we believe positions the Fund well for any challenges, as well as the next market expansion.

Long Term Active Management into High Conviction Sectors and Away from Structurally Challenged Sectors

| 1 | Source: Clarion Partners |

| 2 | Source: Carlyle, Federal Reserve Flow of Funds |

| 3 | Source: Bureau of Labor Statistics, April 2023 |

| 4 | Specialty includes self storage, student housing, senior housing, medical office, land, data center, and life-sciences properties. |

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

Outlook

While inflation remains above long-term rates, its downward trend suggests the Federal Reserve may soon pause its policy tightening. The bond market is already signaling a lower level of expected long-term inflation as evidenced by recent declines in the 10-year U.S. Treasury yield. Periods of high and falling inflation have historically resulted in above average returns for institutional private real estate.

Institutional Private Real Estate Returns During Various Inflationary Environments

NPI ANNUALIZED RETURN

Source: JP Morgan Guide to Alternatives, Q1 2023

However, we are confident that market returns will not be even across sectors. The Fund’s high conviction sectors (highlighted in green) are supported by favorable long-term supply and demand trends and are positioned to deliver outsized Net operating income (NOI) growth, a key driver of valuations.

5-YEAR ANNUALIZED NOI GROWTH RATE PROJECTION BY SECTOR

Source: Green Street, A Great Year Ahead for Commercial Real Estate? March 2023

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

We are excited about these sectors, which reflect our thematic investing approach of capitalizing on long-term, structural demand drivers that transcend economic cycles. Just as we have demonstrated over the Fund’s history, we believe an actively managed portfolio that capitalizes on macro-economic and demographic trends can outperform the institutional real estate index.

We believe the Fund’s rare combination of total return, low volatility, and high risk-adjusted returns (as measured by the Sharpe and Sortino Ratios), combined with 41 consecutive quarterly distributions*, make it a valuable allocation for investment portfolios. We thank you for your continued support of Bluerock Total Income+ Real Estate Fund and look forward to the years ahead.

Sincerely,

|  | | |  |  |

| Adam Lotterman | | | Jordan Ruddy |

| Co-Chief Investment Officer and | | | Co-Chief Investment Officer |

| Senior Portfolio Manager | | | and Portfolio Manager |

| Bluerock Total Income+ Real Estate Fund | | | Bluerock Total Income+ Real Estate Fund |

| | | FUND SUB-ADVISORS |

| | | |

| |  | About Mercer Investment Management | |

| | Mercer Investment Management, Inc. (“Mercer”), acts as sub-advisor to the Fund’s private real estate investments. For more than 75 years, Mercer has been one of the world’s leading advisors to endowments, pension funds, sovereign wealth funds and family offices globally, with over 16,000 clients worldwide, and over $16.2 trillion in assets under advisement (as of 6.30.2022). Mercer works to evaluate over 7,800 investment managers and over 36,000 individual investments/strategies (as of 12.31.2022). | |

| | | |

| | | |

| |  | About DWS | |

| | | | |

| | DWS Group GmbH and Co. KGaA (“DWS”), through its indirect subsidiary RREEF Investment, LLC, acts as sub-advisor to the Fund’s public real estate securities investments and is a registered investment adviser under the Investment Advisers Act of 1940. DWS’ real estate business in the U.S. dates back to 1975. Today, DWS has $877 billion in assets under management and works with 1,757 institutional clients. Of that total, approximately $83.7 billion of AUM is invested in public and private real estate globally, making DWS one of the largest real estate managers in the world (as of 12.31.2022). | |

| | | | | |

| * | The Fund’s distribution policy is to make quarterly distributions to shareholders. The level of quarterly distributions (including any return of capital) is not fixed. However, this distribution policy is subject to change. The Fund’s distribution amounts were calculated based on the ordinary income received from the underlying investments, including short-term capital gains realized from the disposition of such investments. Shareholders should not assume that the source of a distribution from the Fund is net profit. All or a portion of the distributions consist of a return of capital based on the character of the distributions received from the underlying holdings, primarily Real Estate Investment Trusts. The final determination of the source and tax characteristics of all distributions will be made after the end of the year. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares. There is no assurance that the Company will continue to declare distributions or that they will continue at these rates. |

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

Performance

From inception (10.22.2012) through 3.31.2023, TI+ (A Shares) generated a cumulative total return of 124.47%, or 8.05% annualized (load waived). The Fund was able to accomplish this primarily through private real estate investments, generating both income and capital appreciation. Private investments are supplemented with select public real estate securities. The Fund currently offers five share classes outstanding: A, C, I, L and M Shares. A summary of the performance of each share class is presented below.

Fund Performance thru 3.31.2023†

| | One Year | Three Year | Five Year | Since Inception5 |

| TI+ Class A (TIPRX) | -2.33% | 8.64% | 7.95% | 8.05% |

| TI+ Class A with Max Sales Charge6 | -7.95% | 6.52% | 6.68% | 7.44% |

| TI+ Class C (TIPPX) | -3.02% | 7.85% | 7.16% | 7.26% |

| TI+ Class C with Load7 | -3.94% | 7.85% | 7.16% | 7.26% |

| TI+ Class I (TIPWX) | -2.07% | 8.92% | 8.23% | 8.31% |

| TI+ Fund - Class L (TIPLX) | -2.57% | 8.36% | 7.68% | 7.79% |

| TI+ Class L with Max Sales Charge6 | -6.71% | 6.80% | 6.75% | 7.34% |

| TI+ Fund - Class M (TIPMX) | -2.73% | 8.14% | 7.44% | 7.53% |

| 5) | Since Inception returns as of October 22, 2012. Actual Inception date of the A Shares is October 22, 2012. Actual Inception date of the Fund’s C and I Shares is April 1, 2014. Actual Inception date for the L Shares is June 1, 2017. Actual inception date for the M shares is December 27, 2021. |

| 6) | The maximum sales charge for the A Shares is 5.75% and for L Shares is 4.25%. Investors may be eligible for a reduction in sales charges. |

| 7) | Adjusted for early withdrawal charge of 1.00%. |

| † | Returns for Class C, Class I, Class L and Class M Shares prior to their inception dates are based on the performance of Class A Shares. For Class C, Class L , and Class M Shares, prior performance has been adjusted to reflect differences in expenses between the respective classes and Class A. The actual returns of Class I would have been different than those shown because Class I has lower expenses than Class A. |

The total annual fund operating expense ratio, gross of any fee waivers or expense reimbursements, is 2.04% for Class A, 2.74% for Class C, 1.78% for Class I, 2.29% for Class L and 2.58% for Class M per the February 1, 2023 prospectuses.

The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Past performance is not a guarantee of future results. The Fund’s investment advisor has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until January 31, 2024, for Class A, C, I and L shares to ensure that the net annual fund operating expenses will not exceed 1.95% for Class A, 2.70% for Class C, 1.70% for Class I, 2.20% for Class L, and 2.45% for Class M, subject to possible recoupment from the Fund in future years. Please review the Fund’s Prospectuses for more detail on the expense waiver. Results shown reflect the full fee waiver, without which the results could have been lower. A Fund’s performance, especially for very short periods of time, should not be the sole factor in making your investment decisions. For performance information current to the most recent month end, please call toll-free 1-844-819-8287.

Total returns are calculated using SEC Form N-2 instructions and reflect all fees and charges.

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

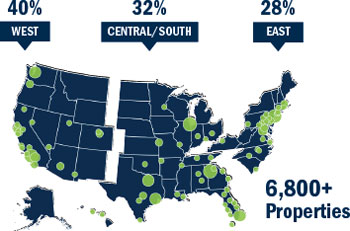

| Geographic Diversification | | Sector Diversification |

| The regions and allocations presented represent the Fund’s institutional fund investments as of 3.31.2023, but is subject to change at any time. | | The sector diversification presented represents examples of how the Fund’s institutional fund investments are allocated as of 3.31.2023 but is subject to change at any time. |

| | | |

| |  |

Highlighted Assets

As of 3.31.2023. The properties shown here are currently owned by the underlying third party institutional private equity real estate funds described herein. Diversification does not ensure profit and Holdings are subject to change.

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

Fund Holdings

As of 3.31.2023, the Gross Asset Value of the underlying real estate in the institutional private real estate funds in which TI+ is invested is over $389 billion, comprising over 6,800 properties across the United States.

| | | PORTFOLIO | GROSS ASSET

VALUE ($MM) | NUMBER OF

PROPERTIES | TYPICAL MINIMUM

INVESTMENT | AVG INVESTMENT

SIZE ($MM) | OCCUPANCY8 | LTV9 | INCEPTION

YEAR |

| | | | | | | | | | |

| | PRIVATE EQUITY REAL ESTATE (Target of 35-45 Select Managers | % of gross investments) |

| 9.80% | IQHQ | $ | 3,806 | 36 | $ | 5,000,000 | $106 | N/A | 60% | 2019 | |

| | 8.21% | Prologis Targeted US Logistics Fund | $ | 26,900 | 742 | $ | 5,000,000 | $36 | 98% | 13% | 2004 | |

| | 5.07% | Cortland Growth & Income Fund | $ | 8,280 | 79 | $ | 5,000,000 | $105 | 91% | 48% | 2018 | |

| | 4.83% | Morgan Stanley Prime Property Fund | $ | 44,065 | 543 | $ | 5,000,000 | $81 | 94% | 20% | 1973 | |

| | 4.77% | Brookfield Premier Real Estate Partners | $ | 10,667 | 178 | $ | 5,000,000 | $60 | 93% | 43% | 2016 | |

| | 4.15% | Realterm Logistics Income Fund | $ | 4,300 | 156 | $ | 5,000,000 | $28 | 98% | 35% | 2017 | |

| | 4.14% | Clarion Lion Industrial Trust | $ | 34,145 | 778 | $ | 2,500,000 | $44 | 98% | 26% | 2002 | |

| | 3.66% | CBRE U.S. Logisitics Partners | $ | 3,133 | 36 | $ | 10,000,000 | $87 | 99% | 29% | 2021 | |

| | 3.42% | CBRE U.S. Core Partners | $ | 11,713 | 213 | $ | 5,000,000 | $55 | 95% | 30% | 2013 | |

| | 3.19% | Invesco U.S. Income Fund | $ | 5,041 | 48 | $ | 10,000,000 | $105 | 92% | 32% | 2013 | |

| | 3.18% | Prudential PRISA II | $ | 17,500 | 160 | $ | 5,000,000 | $109 | 90% | 34% | 1980 | |

| | 3.06% | Clarion Lion Properties Fund | $ | 23,278 | 188 | $ | 5,000,000 | $124 | 93% | 21% | 2000 | |

| | 2.96% | RREEF Core Plus Industrial Fund | $ | 3,317 | 91 | $ | 5,000,000 | $36 | 98% | 8% | 2017 | |

| | 2.84% | Ares Industrial Real Estate Fund | $ | 5,477 | 202 | $ | 5,000,000 | $27 | 97% | 31% | 2019 | |

| | 2.83% | Carlyle Property Investors | $ | 13,630 | 200 | $ | 10,000,000 | $68 | 92% | 49% | 2016 | |

| | 2.55% | Prudential PRISA III | $ | 5,700 | 87 | $ | 5,000,000 | $66 | 85% | 32% | 2003 | |

| | 2.30% | Sentinel Real Estate Fund | $ | 3,200 | 36 | $ | 250,000 | $89 | 94% | 24% | 1976 | |

| | 2.03% | Invesco Core Real Estate Fund | $ | 17,860 | 131 | $ | 5,000,000 | $136 | 95% | 26% | 2004 | |

| | 1.92% | Blackstone Property Partners U.S. | $ | 32,200 | 1,303 | $ | 10,000,000 | $25 | 92% | 47% | 2014 | |

| | 1.85% | Clarion Gables Multifamily Trust | $ | 5,978 | 102 | $ | 5,000,000 | $59 | 95% | 40% | 2015 | |

| | 1.80% | TA Realty Core Property Fund | $ | 8,167 | 89 | $ | 5,000,000 | $92 | 96% | 22% | 2018 | |

| | 1.29% | TA Realty Logistics Fund | $ | 958 | 17 | $ | 5,000,000 | $56 | 87% | 17% | 2021 | |

| | 1.28% | BPP Life Science Fund | $ | 23,600 | 123 | $ | 10,000,000 | $192 | 93% | 43% | 2020 | |

| | 1.25% | Bridge Workforce Housing Fund I | $ | 1,188 | 28 | $ | 1,000,000 | $42 | 93% | 49% | 2017 | |

| | 1.21% | Principal Enhanced Property Fund | $ | 5,308 | 64 | $ | 5,000,000 | $83 | 97% | 35% | 2004 | |

| | 1.16% | Harrison Street Core Property Fund | $ | 14,042 | 397 | $ | 10,000,000 | $35 | 90% | 23% | 2011 | |

| | 1.04% | Stockbridge Smart Markets Fund | $ | 4,937 | 143 | $ | 5,000,000 | $35 | 96% | 22% | 2011 | |

| | 1.03% | RREEF America REIT II | $ | 19,773 | 128 | $ | 5,000,000 | $154 | 92% | 20% | 1998 | |

| | 1.01% | Bain Capital Real Estate Fund I | $ | 3,249 | 83 | $ | 10,000,000 | $39 | 91% | 51% | 2018 | |

| | 0.37% | AEW Core Property Trust | $ | 10,752 | 79 | $ | 5,000,000 | $136 | 97% | 25% | 2007 | |

| | 0.28% | Harrison Street Data Center | $ | 512 | 6 | $ | 5,000,000 | $85 | 96% | 45% | 2021 | |

| | 0.14% | Harrison Street Life Science | $ | 596 | 5 | $ | 5,000,000 | $119 | 81% | 53% | 2021 | |

| | 0.06% | Bain Capital Life Science Fund | $ | 3 | 2 | $ | 5,000,000 | $2 | N/A | 52% | 2020 | |

| | 0.01% | Stockbridge Value Fund II | $ | 122 | 2 | $ | 5,000,000 | $61 | 81% | 33% | 2014 | |

| | 88.70% | iPERE TOTALS / AVERAGES | $373,398 | 6,475 | $193,750,000 | $58 | 93% | 30% | 2011 | |

| | REAL ESTATE DEBT SECURITIES |

| | 4.06% | Freddie Mac Securitized Multifamily Notes10 | $4,958 | 222 | $ | 50,000,000 | $22 | — | — | — | |

| | 1.64% | Ares Real Estate Enhanced Income Fund | $4,800 | 46 | $ | 5,000,000 | $104 | — | — | — | |

| | 1.33% | Bridge Debt Strategies Fund IV | $3,850 | 79 | $ | 1,000,000 | $49 | — | — | — | |

| | 0.90% | H/2 Special Opportunities Fund V | | $539 | 9 | | N/A | $60 | — | — | — | |

| | 0.76% | Bridge Debt Strategies Fund III | $1,860 | 46 | $ | 1,000,000 | $40 | | | | |

| | 8.69% | REAL ESTATE DEBT TOTALS / AVERAGES | $16,007 | 402 | $57,000,000 | $40 | — | — | — | |

| | PUBLIC REAL ESTATE EQUITY SECURITIES AND CASH (Target of 25-50 Real Estate Securities) |

| | 2.36% PUBLIC REAL ESTATE SECURITIES | — | — | — | — | — | — | — | |

| | 0.25% | CASH | — | — | — | — | — | — | — | |

| | | | | | | | | | | |

| | 100% | PORTFOLIO TOTAL | $389,404 | 6,877 | $250,750,000 | $57 | 93% | 30% | 2011 | |

| | | | | | | | | | | | | |

| 8) | Occupancy rates reported from underlying managers, average is the simple average of all private funds. Generally excludes properties under construction, but generally includes properties in lease-up. |

| 9) | Weighted average loan to value: outstanding loan balance divided by the total value of the underlying real estate. For IQHQ, estimated based on expected leverage target. |

| 10) | The Fund expects to invest in the privately offered subordinate classes of K-Notes. Because more-senior classes have payment priority over subordinate classes of K-Notes, the value of subordinate K-Notes is highly sensitive to the default rate and foreclosure recovery rate on the underlying apartment loans. Subordinate K-Notes are also subject to liquidity risk because they are not available to the investing public and have a limited secondary market composed of institutional investors. |

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

Definitions

NFI-ODCE: a capitalization-weighted, gross of fee, time-weighted return index with an inception date of December 31, 1977. Supplemental data is also provided, such as equal-weight and net of fee returns, for informational purposes and additional analysis.

iPERE/NCREIF Property Index (NPI): Institutional private equity real estate (iPERE) can be described as high-quality commercial properties that are usually congregated in large investment portfolios managed professionally on behalf of third-party owners or beneficiaries. The leading benchmark index for iPERE is the National Council of Real Estate Investment Fiduciaries Price Index (NPI) which represents a collection of 10,000+ institutional properties representing all major commercial property types within the U.S. The NPI is a quarterly time series composite total rate of return measure of investment performance of a very large pool of individual commercial real estate properties acquired in the private market for investment purposes only. All properties in the NPI have been acquired, at least in part, on behalf of tax-exempt institutional investors - the great majority being pension funds. As such, all properties are held in a fiduciary environment.

Sharpe Ratio: a measure of the return of an investment based on the level of risk (volatility). A higher number indicating a higher return per unit of risk.

Standard Deviation: measures volatility by calculating the daily dispersion of returns from the mean.

Sortino Ratio: a measure of the return of an investment based on the level of downside volatility. A higher number indicates a higher return per unit of downside.

Sources: Morningstar Direct, Standard & Poors, Yahoo Finance, Federal Reserve Economic Data. Institutional Real Estate: Yield is from the NCREIF Property Index (NPI) as of 9.30.2022, The NPI is a leading benchmark index for Institutional Real Estate which represents a collection of 10,000+ institutional properties representing all major commercial property types within the U.S. The NPI is a quarterly time series composite total rate of return measure of investment performance of a very large pool of individual commercial real estate properties acquired in the private market for investment purposes only. All properties in the NPI have been acquired, at least in part, on behalf of tax-exempt institutional investors - the great majority being pension funds. As such, all properties are held in a fiduciary environment. Bloomberg Barclays U.S. Aggregate Bond Index: A broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Provided the necessary inclusion rules are met, US Aggregate eligible securities also contribute to the multi-currency Global Aggregate Index and the US Universal Index, which includes high yield and emerging markets debt. Risks include rising interest rates or other economic factors that may negatively affect the value of the underlying bonds.

You cannot invest directly in an index and unmanaged indices do not reflect fees, expenses or sales charges. Additionally, a rise in interest rates could cause a decline in the value of fixed income securities. The referenced yields are shown for general market comparisons. Past performance is not a guarantee of future results.

You cannot invest directly in an index. Benchmark performance should not be considered reflective of Fund performance.

Risk Disclosures

Not FDIC Insured | No Bank Guarantee | May Lose Value

Investing in the Fund involves risks, including the risk that you may receive little or no return on your investment or that you may lose part or all of your investment.

The ability of the Fund to achieve its investment objective depends, in part, on the ability of the Advisor to allocate effectively the Fund’s assets across the various asset classes in which it invests and to select investments in each such asset class. There can be no assurance that the actual allocations will be effective in achieving the Fund’s investment objective or delivering positive returns.

Limited liquidity is provided to shareholders only through the Fund’s quarterly repurchase offers for no less than 5% of the Fund’s shares outstanding at net asset value. There is no guarantee that shareholders will be able to sell all of the shares they desire in a quarterly repurchase offer. Since inception, the Fund has made 41 repurchase offers, of which 36 have resulted in the repurchase of all shares tendered, five have resulted in the repurchase of less than all shares tendered. In connection with the February 2023 repurchase offer, the Fund repurchased 55.4% of all shares tendered for repurchase. Quarterly repurchases by the Fund of its shares typically will be funded from available cash or sales of portfolio securities. The sale of securities to fund repurchases could reduce the market price of those securities, which in turn would reduce the Fund’s net asset value.

An investment in shares represents an indirect investment in the securities owned by the Fund. The value of these securities, like other market investments, may move up or down, sometimes rapidly and unpredictably. The Fund is “non-diversified” under the Investment Company Act of 1940 and therefore may invest more than 5% of its total assets in the securities of one or more issuers. As such, changes in the financial condition or market value of a single issuer may cause a greater fluctuation in the Fund’s net asset value than in a “diversified” fund. The Fund is not intended to be a complete investment program.

The Fund is subject to the risk that geopolitical and other similar events will disrupt the economy on a national or global level. For instance, war, terrorism, market manipulation, government defaults, government shutdowns, political changes or diplomatic developments, public health emergencies (such as the spread of infectious diseases, pandemics and epidemics) and natural/environmental disasters can all negatively impact the securities markets.

The current novel coronavirus (COVID-19) global pandemic and the aggressive responses taken by many governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines or similar restrictions, as well as the forced or voluntary closure of, or operational changes to, many retail and other businesses, have had negative impacts, and in many cases severe negative impacts, on markets worldwide. Potential impacts on the real estate market may include lower occupancy rates, decreased lease payments, defaults and foreclosures, among other consequences. It is not known how long such impacts, or any future impacts of other significant events described above, will or would last, but there could be a prolonged period of global economic slowdown.

The Fund will concentrate its investments in real estate industry securities. The value of the Fund’s shares will be affected by factors affecting the value of real estate and the earnings of companies engaged in the real estate industry. These factors include, among others: (i) changes in general economic and market conditions; (ii)changes in the value of real estate properties; (iii) risks related to local economic conditions, overbuilding and increased competition; (iv) increases in property taxes and operating expenses; (v) changes in zoning laws; (vi)casualty and condemnation losses; (vii) variations in rental income, neighborhood values or the appeal of property to tenants; (viii) the availability of financing; (ix) climate change; and (x) changes in interest rates. Many real estate companies utilize leverage, which increases investment risk and could adversely affect a company’s operations and market value in periods of rising interest rates. The value of securities of companies in the real estate industry may go through cycles of relative under-performance and over-performance in comparison to equity securities markets in general.

| SEMI-ANNUAL REPORT (4Q 2022 - 1Q 2023) | BLUEROCK TOTAL INCOME+ REAL ESTATE FUND | (UNAUDITED) |

A significant portion of the Fund’s underlying investments are in private real estate investment funds managed by institutional investment managers (“Institutional Investment Funds”). Investments in Institutional Investment Funds pose specific risks, including: such investments require the Fund to bear a pro rata share of the vehicles’ expenses, including management and performance fees; the Advisor and Sub-Advisor will have no control over investment decisions may by such vehicle; such vehicle may utilize financial leverage; such investments have limited liquidity; the valuation of such investment as of a specific date may vary from the actual sale price that may be obtained if such investment were sold to a third party.

Additional risks related to an investment in the Fund are set forth in the “Risk Factors” section of the prospectus, which include, but are not limited to the following: convertible securities risk; correlation risk; credit risk; fixed income risk; leverage risk; risk of competition between underlying funds; and preferred securities risk.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Bluerock Total Income+ Real Estate Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling toll free 844-819-8287, or online at bluerock.com/ti-fund/documents. The prospectus should be read carefully before investing.

The Bluerock Total Income+ Real Estate Fund is distributed by ALPS Distributors, Inc (ALPS). Bluerock Fund Advisor, LLC is not affiliated with ALPS, Mercer Investment Management, or DWS.

Additional fund performance details available at bluerock.com/ti-fund/performance. Investors may be eligible for a reduction in sales charges. Please see the Fund Prospectus for details. Please note that the indices are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features.

There are limitations when comparing the Bluerock Total Income+ Real Estate Fund to Stock, Bond, and Public Real Estate indices. Many open-end funds which track these indices offer daily liquidity, while closed-end interval funds offer liquidity only on a periodic basis. Deteriorating general market conditions will reduce the value of stock securities. When interest rates rise, the value of bond securities tends to fall. Real estate securities may decline because of adverse developments affecting the real estate industry and real property values. You cannot invest directly in an index and unmanaged indices do not reflect fees, expenses or sales charges. Please see definitions for a description of the risks and comparisons of the investment indexes selected.

This semi-annual report may contain certain forward-looking statements. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” or other similar words. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. These risks, uncertainties and contingencies include, but are not limited to: uncertainties relating to changes in general economic and real estate conditions; uncertainties relating to the implementation of our investment strategy; uncertainties relating to capital proceeds; and other risk factors as outlined in the Fund’s prospectuses, statement of additional information, annual report and semi-annual report filed with the Securities and Exchange Commission.

| | BLU001080 |

| Bluerock Total Income+ Real Estate Fund | Portfolio Review |

March 31, 2023 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment

The Fund’s performance figures for certain periods ended March 31, 2023, compared to select indexes:

| Bluerock Total Income+ Real Estate Fund: | 6 Month | 1 Year | 3 Year | 5 Year | 10 Year | Since Inception Class A* | Since Inception Class C and Class I* | Since Inception Class L* | Since Inception Class M* |

| Class A | | | | | | | | | |

| Without Load | -8.92% | -2.33% | 8.64% | 7.95% | 8.00% | 8.05% | – | – | – |

| With Load(a) | -14.14% | -7.95% | 6.52% | 6.68% | 7.36% | 7.44% | – | – | – |

| Class C | | | | | | | | | |

| Without Load | -9.23% | -3.02% | 7.85% | 7.16% | – | – | 6.77% | – | – |

| With Load(b) | -10.11% | -3.94% | 7.85% | 7.16% | – | – | 6.77% | – | – |

| Class I | -8.78% | -2.07% | 8.92% | 8.23% | – | – | 7.86% | – | – |

| Class L | | | | | | | | | |

| Without Load | -9.02% | -2.57% | 8.36% | 7.68% | – | – | – | 7.54% | – |

| With Load(c) | -12.88% | -6.71% | 6.80% | 6.75% | – | – | – | 6.74% | – |

| Class M | -9.09% | -2.73% | – | – | – | – | – | – | 3.89% |

| S&P 500 Total Return Index | 15.63% | -7.73% | 18.60% | 11.19% | 12.24% | 12.78% | 11.14% | 11.40% | -10.01% |

| Bloomberg U.S. Aggregate Bond Index | 4.89% | -4.78% | -2.77% | 0.91% | 1.36% | 1.33% | 1.54% | 0.73% | -8.35% |

| * | Class A commenced operations October 22, 2012, Class C and Class I commenced operations April 1, 2014, Class L commenced operations June 1, 2017, and Class M commenced operations December 27, 2021. |

| (a) | Adjusted for initial maximum sales charge of 5.75%. |

| (b) | Adjusted for early withdrawal charge of 1.00%. |

| (c) | Adjusted for initial maximum sales charge of 4.25%. |

The S&P 500 Total Return Index is an unmanaged market capitalization-weighted index which is comprised of 500 of the largest U.S. domiciled companies and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged index which represents the U.S. investment-grade fixed-rate bond market (including government and corporate securities, mortgage pass-through securities and asset-backed securities). Investors cannot invest directly in an index or benchmark.

Total returns are calculated using closing Net Asset Value as of March 31, 2023, and may not match returns presented in the Financial Highlights due to adjustments under accounting principles generally accepted in the United States of America.

10

| Bluerock Total Income+ Real Estate Fund | Portfolio Review |

March 31, 2023 (Unaudited)

The performance data quoted is historical. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total returns are calculated using closing Net Asset Value as of March 31, 2023. Total returns are calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the Advisor not waived a portion of its fees. Returns greater than one year are annualized. The Advisor and the Fund have entered into an expense limitation and reimbursement agreement under which the Advisor has contractually agreed to waive its fees and to pay or absorb the ordinary operating expenses of the Fund (excluding any taxes, interest, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses, such as litigation or reorganization costs, but including organizational costs and offering costs), to the extent that such expenses exceed 1.95%, 2.70%, 1.70%, 2.20% and 2.45% of the Fund's average daily net assets attributable to the Class A, Class C, Class I, Class L and Class M shares, respectively. In consideration of the Advisor's agreement to limit the Fund's expenses, the Fund has agreed to repay the Advisor in the amount of any fees the Advisor previously waived or Fund expenses reimbursed, subject to the limitations that: (1) the reimbursement will be made if payable not more than three years from the date incurred; (2) the reimbursement may not be made if it would cause the expense limitation then in effect or in effect at the time of the waiver to be exceeded; and (3) the reimbursement is approved by the Fund's Board of Trustees. The Expense Limitation Agreement will remain in effect at least until January 31, 2024 unless and until the Board approves its modification or termination. After January 31, 2024, the Expense Limitation Agreement may be renewed at the Advisor's and Board's discretion.

The Fund’s total gross annual operating expenses, including the expenses of underlying funds and before any fee waiver, are 2.04%, 2.74%, 1.78%, 2.29% and 2.56% for Class A, Class C, Class I, Class L and Class M, respectively, per the February 1, 2023 prospectus. Class A shares are subject to a maximum sales charge imposed on purchases of 5.75%. Class A shareholders who tender for repurchase Class A shares that were purchased in amounts of $1,000,000 or more that have been held less than one year (365 days) from the purchase date will be subject to an early withdrawal charge of 1.00% of the original purchase price. Class C shares are subject to an early withdrawal charge of 1.00% if redeemed less than 365 days after the purchase. Class L shares are subject to a maximum sales charge imposed on purchases of 4.25%. The above performance figures do not reflect the deduction of taxes that a shareholder would have to pay on Fund distributions or the redemption of the Fund shares. For performance information current to the most recent month-end, please call 1-844-819-8287.

Portfolio Composition as of March 31, 2023

| | Percent of

Net Assets |

| Private Real Estate Securities | 102.15% |

| Real Estate Debt Securities | 4.40% |

| Public Non-Traded Real Estate Investment Trusts | 0.00% |

| Publicly Traded Real Estate Investment Trusts | 2.36% |

| Open-Ended Mutual Fund | 0.20% |

| Short-Term Investment | 0.97% |

| Total Investments | 110.08% |

| Liabilities in Excess of Other Assets | (10.08)% |

| Total Net Assets | 100.00% |

See the Portfolio of Investments in this report for a more detailed account of the Fund’s holdings.

| Semi-Annual Report | March 31, 2023 | 11 |

| Bluerock Total Income+ Real Estate Fund | Portfolio of Investments |

March 31, 2023 (Unaudited)

| Security | | Shares | | | Value | |

| PRIVATE REAL ESTATE SECURITIES (102.15%)(a) | | | | | | | | |

| Apartments (11.02%) | | | | | | | | |

| Bridge Workforce Housing Fund I, LP | | | N/A | | | $ | 88,954,941 | |

| Clarion Gables Multifamily Trust | | | 78,285 | | | | 136,849,053 | |

| Cortland Growth & Income Fund | | | 233,432 | | | | 337,825,348 | |

| Sentinel Real Estate Fund | | | 1,335 | | | | 166,796,624 | |

| | | | | | | | 730,425,966 | |

| Data Centers (0.31%) | | | | | | | | |

| Harrison Street Data Center Fund(b) | | | N/A | | | | 20,376,200 | |

| | | | | | | | | |

| Diversified (48.07%) | | | | | | | | |

| AEW Core Property Trust | | | 21,925 | | | | 25,968,116 | |

| Ares Real Estate Enhanced Income Fund | | | N/A | | | | 117,549,621 | |

| Bain Capital Real Estate Fund I | | | N/A | | | | 71,552,020 | |

| Blackstone Property Partners U.S. | | | 83,352 | | | | 131,839,653 | |

| Bridge Debt Strategies Fund III, LP | | | N/A | | | | 54,563,257 | |

| Bridge Debt Strategies Fund IV, LP | | | N/A | | | | 95,465,380 | |

| Brookfield Premier Real Estate Partners | | | 203,822 | | | | 339,053,361 | |

| Carlyle Property Investors | | | 108,661 | | | | 209,742,143 | |

| CBRE U.S. Core Partners, LP | | | 133,957,632 | | | | 246,242,741 | |

| Clarion Lion Properties Fund | | | 120,367 | | | | 218,541,683 | |

| H/2 Special Opportunities Fund(b)(c) | | | N/A | | | | 65,318,020 | |

| Harrison Street Core Property Fund | | | 52,441 | | | | 84,054,997 | |

| Invesco Core Real Estate Fund | | | 681 | | | | 145,550,570 | |

| Invesco U.S. Income Fund LP | | | 132,226 | | | | 228,061,859 | |

| Morgan Stanley Prime Property Fund LLC | | | 16,398 | | | | 358,645,982 | |

| PGIM PRISA II | | | 148,856 | | | | 228,082,077 | |

| PGIM PRISA III | | | 61,977 | | | | 188,489,737 | |

| Principal Enhanced Property Fund LP | | | 6,175,011 | | | | 91,091,171 | |

| RREEF America REIT II, Inc. | | | 497,740 | | | | 73,390,099 | |

| Stockbridge Smart Markets Fund | | | 39,329 | | | | 76,633,125 | |

| Stockbridge Value Fund II | | | N/A | | | | 117,478 | |

| TA Realty Core Property Fund, LP | | | 91,130 | | | | 135,213,495 | |

| | | | | | | | 3,185,166,585 | |

| Industrial (30.54%) | | | | | | | | |

| Ares Industrial Real Estate Fund | | | 74,933 | | | | 202,839,470 | |

| CBRE U.S. Logistics Partners LP | | | 215,533,862 | | | | 273,015,332 | |

| Clarion Lion Industrial Trust | | | 80,015 | | | | 316,518,867 | |

| Prologis Targeted U.S. Logistics Fund(c) | | | 198,346 | | | | 612,990,967 | |

| Realterm Logistics Income Fund LP | | | 187,289 | | | | 311,116,918 | |

| RREEF Core Plus Industrial Fund LP | | | 935,544 | | | | 210,318,954 | |

| TA Realty Logistics Fund, LP | | | 85,054 | | | | 97,402,113 | |

| | | | | | | | 2,024,202,621 | |

| Life Science (12.21%) | | | | | | | | |

| Bain Capital Real Estate Life Science Fund(b) | | | N/A | | | | 3,716,683 | |

| Blackstone Property Partners Life Science | | | N/A | | | | 90,304,208 | |

| Harrison Street Life Science | | | N/A | | | | 10,344,484 | |

| IQHQ, Inc.(b)(c) | | | 25,663,327 | | | | 704,552,957 | |

| | | | | | | | 808,918,332 | |

| TOTAL PRIVATE REAL ESTATE SECURITIES (Cost $6,008,311,766) | | | | | | | 6,769,089,704 | |

| Security | | Principal | | | Value | |

| REAL ESTATE DEBT SECURITIES (4.40%)(d) | | | | | | | | |

| FREMF 2018-K82 Mortgage Trust, Class X2A, IO, 0.100%, 9/25/2028 | | $ | 1,065,680,614 | | | $ | 4,749,755 | |

| FREMF 2018-K82 Mortgage Trust, Class D, 0.000%, 10/25/2028 | | | 100,392,906 | | | | 63,242,062 | |

The accompanying notes are an integral part of these financial statements.

12

| Bluerock Total Income+ Real Estate Fund | Portfolio of Investments (Continued) |

March 31, 2023 (Unaudited)

| Security | | Principal | | | Value | |

| FREMF 2018-K82 Mortgage Trust, Class X2B, IO, 0.100%, 10/25/2028 | | $ | 262,694,906 | | | $ | 1,213,147 | |

| FREMF 2019-K101 Mortgage Trust, Class X2A, IO, 0.100%, 10/25/2029 | | | 1,179,983,393 | | | | 6,139,402 | |

| FREMF 2019-K101 Mortgage Trust, Class D, 0.000%, 1/25/2030 | | | 109,477,635 | | | | 61,525,079 | |

| FREMF 2019-K101 Mortgage Trust, Class X2B, IO, 0.100%, 1/25/2030 | | | 270,043,635 | | | | 1,463,632 | |

| FREMF 2019-K91 Mortgage Trust, Class X2A, IO, 0.100%, 3/25/2029 | | | 1,115,688,385 | | | | 5,364,621 | |

| FREMF 2019-K91 Mortgage Trust, Class D, 0.000%, 10/25/2029 | | | 103,857,565 | | | | 60,700,098 | |

| FREMF 2019-K91 Mortgage Trust, Class X2B, IO, 0.100%, 10/25/2029 | | | 247,526,565 | | | | 1,265,649 | |

| FREMF 2019-KC03 Mortgage Trust, Class C, 4.365%, 1/25/2026 | | | 58,088,000 | | | | 52,383,694 | |

| FREMF 2021-K132 Mortgage Trust, Class X2A, IO, 0.100%, 8/25/2031 | | | 978,791,587 | | | | 6,395,805 | |

| FREMF 2021-K132 Mortgage Trust, Class X2B, IO, 0.100%, 8/25/2031 | | | 230,992,666 | | | | 1,523,229 | |

| FREMF 2021-K132 Mortgage Trust, Class D, 0.000%, 12/25/2031 | | | 60,501,666 | | | | 25,621,021 | |

| TOTAL REAL ESTATE DEBT SECURITIES (Cost $285,946,357) | | | | | | | 291,587,194 | |

| Security | | Shares | | | Value | |

| PUBLIC EQUITY REAL ESTATE SECURITIES (2.36%) | | | | | | | | |

| Public Non-Traded Real Estate Investment Trusts (0.00%) | | | | | | | | |

| Diversified (0.00%) | | | | | | | | |

| Highlands REIT, Inc.(b)(e) | | | 140,161 | | | | 33,639 | |

| Total Public Non-Traded Real Estate Investment Trusts (Cost $51,627) | | | | | | | 33,639 | |

| | | | | | | | | |

| Publicly Traded Real Estate Investment Trusts (2.36%) | | | | | | | | |

| Apartments (0.26%) | | | | | | | | |

| AvalonBay Communities, Inc. | | | 57,416 | | | | 9,649,333 | |

| Mid-America Apartment Communities, Inc. | | | 49,688 | | | | 7,504,875 | |

| | | | | | | | 17,154,208 | |

| Data Centers (0.24%) | | | | | | | | |

| Equinix, Inc. | | | 22,330 | | | | 16,100,823 | |

| | | | | | | | 16,100,823 | |

| Diversified (0.08%) | | | | | | | | |

| WP Carey, Inc. | | | 71,060 | | | | 5,503,597 | |

| | | | | | | | 5,503,597 | |

| Gaming (0.13%) | | | | | | | | |

| VICI Properties, Inc. | | | 271,516 | | | | 8,856,852 | |

| | | | | | | | 8,856,852 | |

| Healthcare (0.19%) | | | | | | | | |

| Sabra Health Care REIT, Inc. | | | 227,405 | | | | 2,615,158 | |

| Ventas, Inc. | | | 17,892 | | | | 775,618 | |

| Welltower, Inc. | | | 131,744 | | | | 9,444,727 | |

| | | | | | | | 12,835,503 | |

| Hotels (0.07%) | | | | | | | | |

| Ryman Hospitality Properties, Inc.(b) | | | 48,454 | | | | 4,347,777 | |

| | | | | | | | 4,347,777 | |

| Industrial (0.45%) | | | | | | | | |

| EastGroup Properties, Inc. | | | 25,819 | | | | 4,268,397 | |

| Prologis, Inc. | | | 168,968 | | | | 21,082,137 | |

| Rexford Industrial Realty, Inc. | | | 72,013 | | | | 4,295,576 | |

| | | | | | | | 29,646,110 | |

| Manufactured Homes (0.08%) | | | | | | | | |

| Equity LifeStyle Properties, Inc. | | | 81,545 | | | | 5,474,116 | |

| | | | | | | | 5,474,116 | |

| Office (0.06%) | | | | | | | | |

| Alexandria Real Estate Equities, Inc. | | | 30,476 | | | | 3,827,481 | |

| | | | | | | | 3,827,481 | |

The accompanying notes are an integral part of these financial statements.

| Semi-Annual Report | March 31, 2023 | 13 |

| Bluerock Total Income+ Real Estate Fund | Portfolio of Investments (Continued) |

March 31, 2023 (Unaudited)

| Security | | Shares | | | Value | |

| Regional Malls (0.12%) | | | | | | | | |

| Simon Property Group, Inc. | | | 73,411 | | | $ | 8,219,830 | |

| | | | | | | | 8,219,830 | |

| Self-Storage (0.35%) | | | | | | | | |

| Extra Space Storage, Inc. | | | 21,957 | | | | 3,577,454 | |

| Iron Mountain, Inc. | | | 109,346 | | | | 5,785,497 | |

| Life Storage, Inc. | | | 27,959 | | | | 3,665,145 | |

| Public Storage | | | 32,546 | | | | 9,833,449 | |

| | | | | | | | 22,861,545 | |

| Shopping Center (0.11%) | | | | | | | | |

| Kimco Realty Corp. | | | 171,150 | | | | 3,342,559 | |

| Kite Realty Group Trust | | | 181,927 | | | | 3,805,913 | |

| | | | | | | | 7,148,472 | |

| Single Tenant (0.17%) | | | | | | | | |

| Agree Realty Corp. | | | 83,931 | | | | 5,758,506 | |

| Essential Properties Realty Trust, Inc. | | | 140,895 | | | | 3,501,241 | |

| Spirit Realty Capital, Inc. | | | 53,507 | | | | 2,131,719 | |

| | | | | | | | 11,391,466 | |

| Single-Family Rental (0.05%) | | | | | | | | |

| American Homes 4 Rent, Class A | | | 100,503 | | | | 3,160,819 | |

| | | | | | | | 3,160,819 | |

| Total Publicly Traded Real Estate Investment Trusts (Cost $156,858,222) | | | | | | | 156,528,599 | |

| | | | | | | | | |

| TOTAL PUBLIC EQUITY REAL ESTATE SECURITIES (Cost $156,909,849) | | | | | | | 156,562,238 | |

| | | | | | | | | |

| OPEN-ENDED MUTUAL FUND (0.20%) | | | | | | | | |

| Diversified (0.20%) | | | | | | | | |

| Cohen & Steers Institutional Realty Shares, Inc. | | | 298,719 | | | | 12,925,559 | |

| | | | | | | | | |

| TOTAL OPEN-ENDED MUTUAL FUND (Cost $15,000,000) | | | | | | | 12,925,559 | |

| SHORT TERM INVESTMENT (0.97%) | | | | | | | | |

| Fidelity Investments Money Market Fund - Government Portfolio - Class I, 4.700%(f) (Cost $64,441,939) | | | 64,441,939 | | | | 64,441,939 | |

| | | | | | | | | |

| TOTAL INVESTMENTS (110.08%) (Cost $6,530,609,911) | | | | | | $ | 7,294,606,634 | |

| LIABILITIES IN EXCESS OF OTHER ASSETS (-10.08%) | | | | | | | (667,812,483 | ) |

| NET ASSETS (100.00%) | | | | | | $ | 6,626,794,151 | |

Common Abbreviations

IO - Interest Only Security

| (a) | All or a portion of these securities are segregated as collateral for the Lines of Credit as of March 31, 2023. |

| (b) | Non-income producing security. |

| (c) | Holding is comprised of two share classes of the same underlying investment. |

| (d) | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in the ordinary course of business in transactions exempt from registration, normally to qualified institutional buyers. As of March 31, 2023, the aggregate market value of those securities was $291,587,194, representing 4.40% of net assets. |

| (e) | Fair value estimated using fair valuation procedures adopted by the Board of Trustees. Total value of such securities is $33,639, representing 0.00% of net assets. |

| (f) | The rate shown is the 7-day effective yield as of March 31, 2023. |

The accompanying notes are an integral part of these financial statements.

14

| Bluerock Total Income+ Real Estate Fund | Statement of Assets and Liabilities |

March 31, 2023 (Unaudited)

| ASSETS | | | |

| Investments, at value (Cost $6,530,609,911) | | $ | 7,294,606,634 | |

| Receivable for investments sold | | | 14,579 | |

| Receivable for shares sold | | | 6,158,225 | |

| Dividends and Interest receivable | | | 42,391,983 | |

| Deferred borrowing costs (See Note 9) | | | 14,547,900 | |

| Prepaid expenses and other assets | | | 1,619,675 | |

| Total Assets | | | 7,359,338,996 | |

| LIABILITIES | | | | |

| Payable for investments purchased | | | 46,627,143 | |

| Line of credit payable (See Note 9) | | | 675,000,000 | |

| Line of credit interest payable (See Note 9) | | | 785,071 | |

| Investment advisory fees payable | | | 8,326,339 | |

| Shareholder servicing fees payable | | | 342,842 | |

| Administration fees payable | | | 135,072 | |

| Transfer agency fees payable | | | 668,785 | |

| Distribution fees payable | | | 518,137 | |

| Trustees' fees payable | | | 3,932 | |

| Accrued expenses and other liabilities | | | 137,524 | |

| Total Liabilities(a) | | | 732,544,845 | |

| NET ASSETS | | $ | 6,626,794,151 | |

| NET ASSETS CONSIST OF | | | | |

| Paid-in capital | | $ | 5,752,583,835 | |

| Total distributable earnings | | | 874,210,316 | |

| NET ASSETS | | $ | 6,626,794,151 | |

| PRICING OF SHARES | | | | |

| Class A: | | | | |

| Net asset value, per share | | $ | 33.59 | |

| Net assets | | $ | 880,465,272 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 26,212,275 | |

| Maximum offering price per share ((NAV/0.9425), based on maximum sales charge of 5.75% of the offering price) | | $ | 35.64 | |

| Class C: | | | | |

| Net asset value, per share | | $ | 31.44 | |

| Net assets | | $ | 640,518,274 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 20,373,760 | |

| Class I: | | | | |

| Net asset value, per share | | $ | 34.43 | |

| Net assets | | $ | 4,850,428,949 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 140,872,438 | |

| Class L: | | | | |

| Net asset value, per share | | $ | 33.10 | |

| Net assets | | $ | 111,908,776 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 3,381,190 | |

| Maximum offering price per share ((NAV/0.9575), based on maximum sales charge of 4.25% of the offering price) | | $ | 34.57 | |

| Class M: | | | | |

| Net asset value, per share | | $ | 31.56 | |

| Net assets | | $ | 143,472,880 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 4,546,705 | |

| (a) | Separately, see Note 8. Commitments and Contingencies for detail of unfunded commitments |

The accompanying notes are an integral part of these financial statements.

| Semi-Annual Report | March 31, 2023 | 15 |

| Bluerock Total Income+ Real Estate Fund | Statement of Operations |

For the Six Months Ended March 31, 2023 (Unaudited)

| INVESTMENT INCOME | | | |

| Dividend Income | | $ | 92,893,846 | |

| Interest Income | | | 13,316,198 | |

| Total Investment Income | | | 106,210,044 | |

| | | | | |

| EXPENSES | | | | |

| Investment Advisory fees | | | 51,932,255 | |

| Administrative fees | | | 812,657 | |

| Transfer Agency fees | | | 3,282,169 | |

| Shareholder servicing fees: | | | | |

| Class A | | | 1,133,102 | |

| Class C | | | 843,549 | |

| Class L | | | 144,728 | |

| Distribution fees: | | | | |

| Class C | | | 2,530,647 | |

| Class L | | | 144,728 | |

| Class M | | | 525,712 | |

| Legal fees | | | 206,534 | |

| Audit and tax fees | | | 15,457 | |

| Reports to shareholders and printing fees | | | 507,078 | |

| Custody fees | | | 101,790 | |

| Chief compliance officer fees | | | 25,457 | |

| Offering cost (See Note 2) | | | 10,474 | |

| Interest expense (See Note 9) | | | 28,092,542 | |

| Trustees' fees | | | 88,931 | |

| Other expenses | | | 286,892 | |

| Total Expenses | | | 90,684,702 | |

| Recoupment of previously waived fees (See Note 3) | | | 12,248 | |

| Net Expenses | | | 90,696,950 | |

| Net Investment Income | | | 15,513,094 | |

| NET REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS | | | | |

| Net realized gain/(loss) on investments | | | (11,638,027 | ) |

| Net change in unrealized appreciation/(depreciation) on investments | | | (513,717,056 | ) |

| NET REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS | | | (525,355,083 | ) |

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (509,841,989 | ) |

The accompanying notes are an integral part of these financial statements.

16

| Bluerock Total Income+ Real Estate Fund | Statements of Changes in Net Assets |

| | | For the Six Months Ended March 31, 2023 (Unaudited) | | | For the Year Ended September 30, 2022 | |

| OPERATIONS: | | | | | | |

| Net investment income | | $ | 15,513,094 | | | $ | 58,536,284 | |

| Net realized gain on investments | | | (11,638,027 | ) | | | 4,453,394 | |

| Net change in unrealized appreciation/(depreciation) on investments | | | (513,717,056 | ) | | | 774,204,482 | |

| Net Increase/(Decrease) in Net Assets Resulting from Operations | | | (509,841,989 | ) | | | 837,194,160 | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

| Class A | | | | | | | | |

| From distributable earnings | | | – | | | | (7,675,897 | ) |

| From return of capital | | | (23,634,565 | ) | | | (32,759,054 | ) |

| Class C | | | | | | | | |

| From distributable earnings | | | – | | | | (6,868,487 | ) |

| From return of capital | | | (17,386,910 | ) | | | (25,870,814 | ) |

| Class I | | | | | | | | |

| From distributable earnings | | | – | | | | (30,652,553 | ) |

| From return of capital | | | (131,468,681 | ) | | | (176,945,671 | ) |

| Class L | | | | | | | | |

| From distributable earnings | | | – | | | | (1,179,735 | ) |

| From return of capital | | | (3,008,890 | ) | | | (4,655,135 | ) |

| Class M | | | | | | | | |

| From distributable earnings | | | – | | | | – | |

| From return of capital | | | (3,732,233 | ) | | | (3,334,287 | ) |

| Total Distributions to Shareholders | | | (179,231,279 | ) | | | (289,941,633 | ) |

| BENEFICIAL INTEREST TRANSACTIONS: | | | | | | | | |

| Class A | | | | | | | | |

| Shares sold | | | 99,101,440 | | | | 326,482,026 | |

| Distributions reinvested | | | 10,703,660 | | | | 18,457,287 | |

| Shares redeemed | | | (61,654,614 | ) | | | (67,452,549 | ) |

| Shares transferred in/out(a)(b) | | | 2,066,804 | | | | (13,511,953 | ) |

| Class C | | | | | | | | |

| Shares sold | | | 42,631,661 | | | | 189,474,973 | |

| Distributions reinvested | | | 9,729,626 | | | | 19,316,744 | |

| Shares redeemed | | | (25,752,409 | ) | | | (40,073,381 | ) |

| Shares transferred out(a) | | | (22,505,712 | ) | | | (16,110,786 | ) |

| Class I | | | | | | | | |

| Shares sold | | | 607,539,458 | | | | 3,097,711,474 | |

| Distributions reinvested | | | 50,950,551 | | | | 85,274,417 | |

| Shares redeemed | | | (622,588,819 | ) | | | (320,068,884 | ) |

| Shares transferred in(b) | | | 28,406,785 | | | | 30,616,066 | |

| Class L | | | | | | | | |

| Shares sold | | | 10,559,388 | | | | 27,564,881 | |

| Distributions reinvested | | | 1,922,958 | | | | 3,695,999 | |

| Shares redeemed | | | (5,615,130 | ) | | | (5,652,265 | ) |

| Shares transferred out(a) | | | (7,967,877 | ) | | | (995,827 | ) |

| Class M | | | | | | | | |

| Shares sold | | | 21,801,932 | | | | 131,148,089 | |

| Distributions reinvested | | | 2,902,554 | | | | 2,650,602 | |

| Shares redeemed | | | (2,192,861 | ) | | | (2,231 | ) |

| Shares transferred in(b) | | | – | | | | 2,500 | |

| Net Increase in Net Assets Derived from Beneficial Interest Transactions | | | 140,039,395 | | | | 3,468,527,182 | |

| Net increase/(decrease) in net assets | | | (549,033,873 | ) | | | 4,015,779,709 | |

The accompanying notes are an integral part of these financial statements.

| Semi-Annual Report | March 31, 2023 | 17 |

| Bluerock Total Income+ Real Estate Fund | Statements of Changes in Net Assets (Continued) |

| | | For the Six Months Ended March 31, 2023 (Unaudited) | | | For the Year Ended September 30, 2022 | |

| NET ASSETS: | | | | | | | | |

| Beginning of year/period | | | 7,175,828,024 | | | | 3,160,048,315 | |

| End of year/period | | $ | 6,626,794,151 | | | $ | 7,175,828,024 | |

| | | | | | | | | |

| Other Information | | | | | | | | |

| Share Transactions: | | | | | | | | |

| Class A | | | | | | | | |

| Beginning shares | | | 24,823,702 | | | | 17,561,636 | |

| Shares sold | | | 2,755,934 | | | | 9,020,062 | |

| Distributions reinvested | | | 311,027 | | | | 510,773 | |

| Shares redeemed | | | (1,736,464 | ) | | | (1,889,318 | ) |

| Shares transferred in/out(a)(b) | | | 58,076 | | | | (379,451 | ) |

| Net increase in shares outstanding | | | 1,388,573 | | | | 7,262,066 | |

| Ending shares | | | 26,212,275 | | | | 24,823,702 | |

| Class C | | | | | | | | |

| Beginning shares | | | 20,257,084 | | | | 15,754,446 | |

| Shares sold | | | 1,262,517 | | | | 5,588,625 | |

| Distributions reinvested | | | 301,580 | | | | 568,822 | |

| Shares redeemed | | | (773,936 | ) | | | (1,177,505 | ) |

| Shares transferred out(a)(b) | | | (673,485 | ) | | | (477,304 | ) |

| Net increase in shares outstanding | | | 116,676 | | | | 4,502,638 | |

| Ending shares | | | 20,373,760 | | | | 20,257,084 | |

| Class I | | | | | | | | |

| Beginning shares | | | 139,230,213 | | | | 60,339,974 | |

| Shares sold | | | 16,549,336 | | | | 84,290,043 | |

| Distributions reinvested | | | 1,444,481 | | | | 2,297,038 | |

| Shares redeemed | | | (17,126,419 | ) | | | (8,540,362 | ) |

| Shares transferred in(b) | | | 774,827 | | | | 843,520 | |

| Net increase in shares outstanding | | | 1,642,225 | | | | 78,890,239 | |

| Ending shares | | | 140,872,438 | | | | 139,230,213 | |

| Class L | | | | | | | | |

| Beginning shares | | | 3,405,356 | | | | 2,712,664 | |

| Shares sold | | | 299,625 | | | | 776,936 | |

| Distributions reinvested | | | 56,634 | | | | 103,726 | |

| Shares redeemed | | | (162,206 | ) | | | (160,187 | ) |

| Shares transferred out(a) | | | (218,219 | ) | | | (27,783 | ) |

| Net increase/(decrease) in shares outstanding | | | (24,166 | ) | | | 692,692 | |

| Ending shares | | | 3,381,190 | | | | 3,405,356 | |

| Class M | | | | | | | | |

| Beginning shares | | | 3,875,173 | | | | – | |

| Shares sold | | | 648,129 | | | | 3,799,588 | |

| Distributions reinvested | | | 89,772 | | | | 75,570 | |

| Shares redeemed | | | (66,369 | ) | | | (64 | ) |

| Shares transferred in(b) | | | – | | | | 79 | |

| Net increase in shares outstanding | | | 671,532 | | | | 3,875,173 | |

| Ending shares | | | 4,546,705 | | | | 3,875,173 | |

| (a) | Shares transferred out - net reduction in shares of a particular class resulting from transfers to other share classes. |

| (b) | Shares transferred in - net increase in shares of a particular class resulting from transfers from other share classes. |

The accompanying notes are an integral part of these financial statements.

18

| Bluerock Total Income+ Real Estate Fund | Statement of Cash Flows |

| | | For the Six Months Ended March 31, 2023 (Unaudited) | |

| Cash Flows from Operating Activities: | | | | |

| Net decrease in net assets resulting from operations | | $ | (509,841,989 | ) |

| Adjustments to reconcile net increase in net assets resulting from operations to net cash used in operating activities: | | | | |

| Purchase of investment securities | | | (789,590,792 | ) |

| Proceeds from disposition of investment securities | | | 209,183,816 | |

| Net proceeds from short-term investment securities | | | 289,063,816 | |

| Net realized gain on investments | | | 11,638,027 | |

| Net change in unrealized appreciation/(depreciation) on investments | | | 513,717,056 | |

| Discount and premiums amortized | | | (5,912,552 | ) |

| (Increase)/Decrease in Assets: | | | | |

| Dividends and interest receivable | | | (10,787,902 | ) |

| Deferred borrowing costs | | | (14,547,900 | ) |

| Prepaid offering costs | | | 10,475 | |

| Prepaid expenses and other assets | | | (1,469,301 | ) |

| Increase/(Decrease) in Liabilities: | | | | |

| Shareholder servicing fees payable | | | (17,880 | ) |

| Investment advisory fees payable | | | (446,271 | ) |

| Administrative fees payable | | | (155,742 | ) |

| Transfer agency fees payable | | | (1,004,617 | ) |

| Distribution fees payable | | | (27,077 | ) |

| Trustees' fees payable | | | 3,932 | |

| Interest due on line of credit payable | | | 447,361 | |

| Accrued expenses and other liabilities | | | (702,258 | ) |

| Net Cash Used in Operating Activities | | | (310,439,798 | ) |

| | | | | |

| Cash Flows from Financing Activities: | | | | |

| Change in Line of Credit Borrowing | | | 325,000,000 | |

| Proceeds from shares sold | | | 799,582,083 | |

| Payment on shares redeemed | | | (717,803,833 | ) |

| Cash distributions paid | | | (103,021,930 | ) |

| Net Cash Provided by Financing Activities | | | 303,756,320 | |

| | | | | |

| Net Change in Cash | | | (6,683,478 | ) |

| | | | | |

| Cash Beginning of Year | | $ | 6,683,478 | |

| Cash End of Year | | $ | – | |

| | | | | |

| Non-cash financing activities not included herein consist of reinvestment of distributions of: | | $ | 76,209,349 | |

| Cash paid for interest on lines of credit during the Period was: | | | 25,718,081 | |

The accompanying notes are an integral part of these financial statements.

| Semi-Annual Report | March 31, 2023 | 19 |

| Bluerock Total Income+ Real Estate Fund - Class A | Financial Highlights |

The table below sets forth financial data for one share of beneficial interest outstanding throughout each year/period presented.

| | | For the Six Months Ended March 31, 2023 (Unaudited) | | | For the Year Ended September 30, 2022 | | | For the Year Ended September 30, 2021 | | | For the Year Ended September 30, 2020 | | | For the Year Ended September 30, 2019 | | | For the Year Ended September 30, 2018 | |

| Net asset value, beginning of period/year | | $ | 37.10 | | | $ | 32.66 | | | $ | 29.26 | | | $ | 30.43 | | | $ | 30.00 | | | $ | 29.37 | |

| INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.06 | | | | 0.38 | | | | 0.50 | | | | 0.46 | | | | 0.33 | | | | 0.21 | |

| Net realized and unrealized gain/(loss) | | | (2.65 | ) | | | 5.97 | | | | 4.50 | | | | (0.05 | ) | | | 1.69 | | | | 2.00 | |

| Total from investment operations | | | (2.59 | ) | | | 6.35 | | | | 5.00 | | | | 0.41 | | | | 2.02 | | | | 2.21 | |

| DISTRIBUTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | – | | | | – | | | | – | | | | (0.06 | ) | | | – | | | | – | |

| From net realized gain on investments | | | – | | | | (0.42 | ) | | | (0.63 | ) | | | (1.02 | ) | | | (0.32 | ) | | | (0.54 | ) |

| Return of capital | | | (0.92 | ) | | | (1.49 | ) | | | (0.97 | ) | | | (0.50 | ) | | | (1.27 | ) | | | (1.04 | ) |

| Total distributions | | | (0.92 | ) | | | (1.91 | ) | | | (1.60 | ) | | | (1.58 | ) | | | (1.59 | ) | | | (1.58 | ) |

| Net asset value, end of period/year | | $ | 33.59 | | | $ | 37.10 | | | $ | 32.66 | | | $ | 29.26 | | | $ | 30.43 | | | $ | 30.00 | |

| TOTAL RETURN(b)(c) | | | (8.06 | )%(d) | | | 19.76 | % | | | 17.68 | % | | | 1.38 | % | | | 6.94 | % | | | 7.69 | % |

| RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period/year (000s) | | $ | 880,465 | | | $ | 921,035 | | | $ | 573,540 | | | $ | 525,950 | | | $ | 536,913 | | | $ | 373,488 | |

| Ratios to Average Net Assets (including interest expense) | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets excluding fee waivers and reimbursements(e)(f) | | | 2.73 | %(g) | | | 2.01 | % | | | 2.09 | % | | | 2.15 | % | | | 2.20 | % | | | 2.43 | % |

| Ratio of expenses to average net assets including fee waivers and reimbursements(f) | | | 2.73 | %(g) | | | 2.04 | % | | | 2.06 | % | | | 2.17 | % | | | 2.21 | % | | | 2.37 | % |

| Ratio of net investment income to average net assets(f) | | | 0.35 | %(g) | | | 1.06 | % | | | 1.65 | % | | | 1.53 | % | | | 1.10 | % | | | 0.71 | % |

| Ratios to Average Net Assets (excluding interest expense) | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets excluding fee waivers and reimbursements(e)(f) | | | 1.91 | %(g) | | | 1.92 | % | | | 1.98 | % | | | 1.91 | % | | | 1.94 | % | | | 1.99 | % |

| Ratio of expenses to average net assets including fee waivers and reimbursements(f) | | | 1.91 | %(g) | | | 1.95 | % | | | 1.95 | % | | | 1.93 | % | | | 1.95 | % | | | 1.93 | % |

| Portfolio turnover rate | | | 3 | %(d) | | | 4 | % | | | 26 | % | | | 27 | % | | | 8 | % | | | 13 | % |

| (a) | Per share amounts are calculated using the average shares method. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States and, consequently, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (c) | Total returns are historical in nature and assumes changes in net asset value per share, reinvestment of dividends and capital gains distributions, if any, and do not reflect the impact of sales charges. Had the Advisor not absorbed a portion of the Fund expenses, total returns would have been lower. |

| (e) | Represents the ratio of expenses to average net assets absent fee waivers expense reimbursement and/or recoupment by the Advisor. |

| (f) | The ratios of expenses to average net assets and net investment income to average net assets do not directly reflect the expenses of the underlying institutional private real estate investments in which the Fund invests. The Fund invests in each underlying institutional private real estate investment based upon its net asset value, inclusive of management fees, which typically range from 0.50% to 1.30% on an annualized basis. The Fund’s Total Return is reported net of all fees and expenses. |

The accompanying notes are an integral part of these financial statements.

20

| Bluerock Total Income+ Real Estate Fund - Class C | Financial Highlights |

The table below sets forth financial data for one share of beneficial interest outstanding throughout each year/period presented.

| | | For the Six Months

Ended March 31, 2023 (Unaudited) | | | For the Year Ended September 30, 2022 | | | For the Year Ended September 30, 2021 | | | For the Year Ended September 30, 2020 | | | For the Year Ended September 30, 2019 | | | For the Year Ended September 30, 2018 | |

| Net asset value, beginning of period/year | | $ | 34.85 | | | $ | 30.90 | | | $ | 27.89 | | | $ | 29.22 | | | $ | 29.02 | | | $ | 28.63 | |

| INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income/(loss)(a) | | | (0.06 | ) | | | 0.12 | | | | 0.26 | | | | 0.23 | | | | 0.10 | | | | (0.01 | ) |

| Net realized and unrealized gain/(loss) | | | (2.49 | ) | | | 5.63 | | | | 4.27 | | | | (0.04 | ) | | | 1.63 | | | | 1.93 | |

| Total from investment operations | | | (2.55 | ) | | | 5.75 | | | | 4.53 | | | | 0.19 | | | | 1.73 | | | | 1.92 | |

| DISTRIBUTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | – | | | | – | | | | – | | | | (0.06 | ) | | | – | | | | – | |

| From net realized gain on investments | | | – | | | | (0.42 | ) | | | (0.63 | ) | | | (0.98 | ) | | | (0.32 | ) | | | (0.52 | ) |

| Return of capital | | | (0.86 | ) | | | (1.38 | ) | | | (0.89 | ) | | | (0.48 | ) | | | (1.21 | ) | | | (1.01 | ) |

| Total distributions | | | (0.86 | ) | | | (1.80 | ) | | | (1.52 | ) | | | (1.52 | ) | | | (1.53 | ) | | | (1.53 | ) |

| Net asset value, end of period/year | | $ | 31.44 | | | $ | 34.85 | | | $ | 30.90 | | | $ | 27.89 | | | $ | 29.22 | | | $ | 29.02 | |

| TOTAL RETURN(b)(c) | | | (8.37 | )%(d) | | | 18.90 | % | | | 16.81 | % | | | 0.63 | % | | | 6.15 | % | | | 6.86 | % |

| RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period/year (000s) | | $ | 640,518 | | | $ | 706,009 | | | $ | 486,734 | | | $ | 437,183 | | | $ | 401,507 | | | $ | 290,549 | |

| Ratios to Average Net Assets (including interest expense) | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets excluding fee waivers and reimbursements(e)(f) | | | 3.45 | %(g) | | | 2.74 | % | | | 2.81 | % | | | 2.90 | % | | | 2.95 | % | | | 3.18 | % |

| Ratio of expenses to average net assets including fee waivers and reimbursements(f) | | | 3.45 | %(g) | | | 2.74 | % | | | 2.81 | % | | | 2.92 | % | | | 2.96 | % | | | 3.12 | % |

| Ratio of net investment income/(loss) to average net assets(f) | | | (0.38 | )%(g) | | | 0.36 | % | | | 0.91 | % | | | 0.79 | % | | | 0.35 | % | | | (0.04 | )% |

| Ratios to Average Net Assets (excluding interest expense) | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratio of expenses to average net assets excluding fee waivers and reimbursements(e)(f) | | | 2.64 | %(g) | | | 2.65 | % | | | 2.70 | % | | | 2.66 | % | | | 2.69 | % | | | 2.74 | % |

| Ratio of expenses to average net assets including fee waivers and reimbursements(f) | | | 2.64 | %(g) | | | 2.65 | % | | | 2.70 | % | | | 2.68 | % | | | 2.70 | % | | | 2.68 | % |

| Portfolio turnover rate | | | 3 | %(d) | | | 4 | % | | | 26 | % | | | 27 | % | | | 8 | % | | | 13 | % |

| (a) | Per share amounts are calculated using the average shares method. |

| (b) | Includes adjustments in accordance with accounting principles generally accepted in the United States and, consequently, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (c) | Total returns are historical in nature and assumes changes in net asset value per share, and reinvestment of dividends and capital gains distributions, if any. Had the Advisor not absorbed a portion of the Fund expenses, total returns would have been lower. |

| (e) | Represents the ratio of expenses to average net assets absent fee waivers expense reimbursement and/or recoupment by the Advisor. |

| (f) | The ratios of expenses to average net assets and net investment income (loss) to average net assets do not directly reflect the expenses of the underlying institutional private real estate investments in which the Fund invests. The Fund invests in each underlying institutional private real estate investment based upon its net asset value, inclusive of management fees, which typically range from 0.50% to 1.30% on an annualized basis. The Fund’s Total Return is reported net of all fees and expenses. |

The accompanying notes are an integral part of these financial statements.

| Semi-Annual Report | March 31, 2023 | 21 |

| Bluerock Total Income+ Real Estate Fund - Class I | Financial Highlights |

The table below sets forth financial data for one share of beneficial interest outstanding throughout each year/period presented.

| | | For the Six Months Ended March 31, 2023 (Unaudited) | | | For the Year Ended September 30, 2022 | | | For the Year Ended September 30, 2021 | | | For the Year Ended September 30, 2020 | | | For the Year Ended September 30, 2019 | | | For the Year Ended September 30, 2018 | |

| Net asset value, beginning of period/year | | $ | 37.99 | | | $ | 33.35 | | | $ | 29.80 | | | $ | 30.92 | | | $ | 30.40 | | | $ | 29.70 | |

| INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income(a) | | | 0.11 | | | | 0.48 | | | | 0.58 | | | | 0.56 | | | | 0.42 | | | | 0.29 | |

| Net realized and unrealized gain/(loss) | | | (2.73 | ) | | | 6.12 | | | | 4.61 | | | | (0.07 | ) | | | 1.72 | | | | 2.01 | |

| Total from investment operations | | | (2.62 | ) | | | 6.60 | | | | 5.19 | | | | 0.49 | | | | 2.14 | | | | 2.30 | |

| DISTRIBUTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | – | | | | – | | | | – | | | | (0.06 | ) | | | – | | | | – | |

| From net realized gain on investments | | | – | | | | (0.42 | ) | | | (0.63 | ) | | | (1.04 | ) | | | (0.32 | ) | | | (0.54 | ) |

| Return of capital | | | (0.94 | ) | | | (1.54 | ) | | | (1.01 | ) | | | (0.51 | ) | | | (1.30 | ) | | | (1.06 | ) |

| Total distributions | | | (0.94 | ) | | | (1.96 | ) | | | (1.64 | ) | | | (1.61 | ) | | | (1.62 | ) | | | (1.60 | ) |

| Net asset value, end of period/year | | $ | 34.43 | | | $ | 37.99 | | | $ | 33.35 | | | $ | 29.80 | | | $ | 30.92 | | | $ | 30.40 | |