Washington, D.C. 20549

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V.

SANTANDER MEXICO FINANCIAL GROUP, S.A.B. de C.V.

01219 México, D.F.

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V.

TABLE OF CONTENTS

| I. | CEO Message / Key Highlights for the Quarter |

| | |

| II. | Summary of 3Q12 Consolidated Results |

| | |

| III. | Analysis of 3Q12 Consolidated Results |

| | |

| IV. | Relevant Events |

| | |

| V. | Credit Ratings |

| | |

| VI. | 3Q Earnings Call Dial-In Information |

| | |

| VII. | Financial Statements |

| | |

| VIII. | Notes to the Financial Statements |

3Q. 12 | EARNINGS REPORT | 0

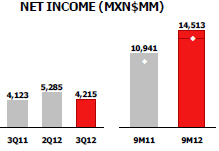

Grupo Financiero Santander México Reports Third Quarter 2012 Net Income of Ps.4,215 Million

Solid Profitability and Growth Driven by Focus on Commercial Banking and Operational Efficiency

México City – October 25, 2012, Grupo Financiero Santander México, S.A.B. de C.V., (NYSE: BSMX; BMV: SANMEX), (“Santander México”), one of the leading financial groups in the Mexican financial system, today announced financial results for the three- and nine-month periods ending September 30, 2012.

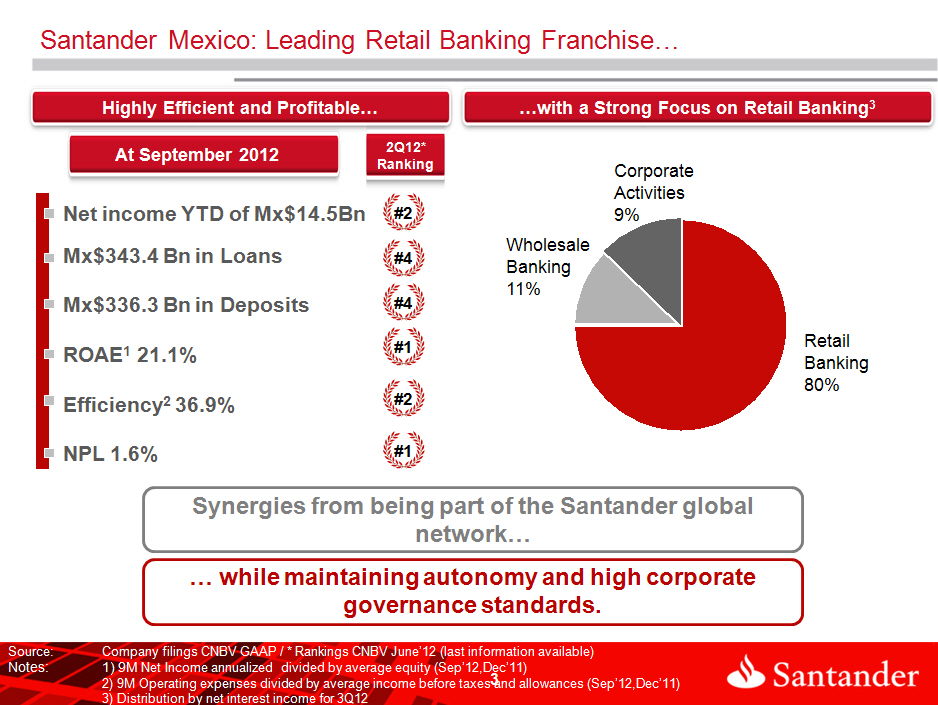

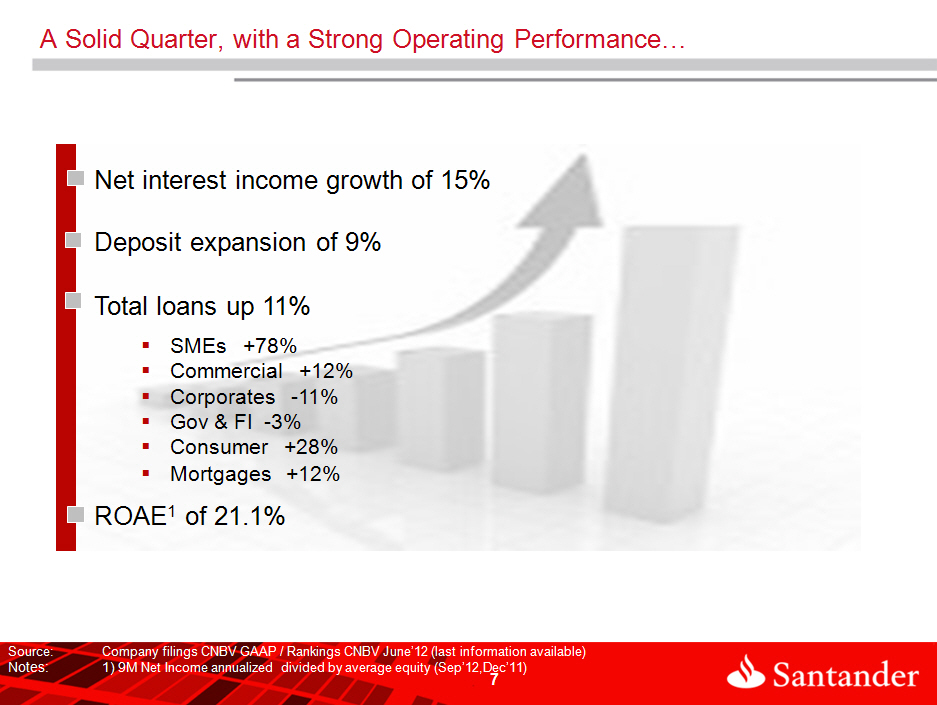

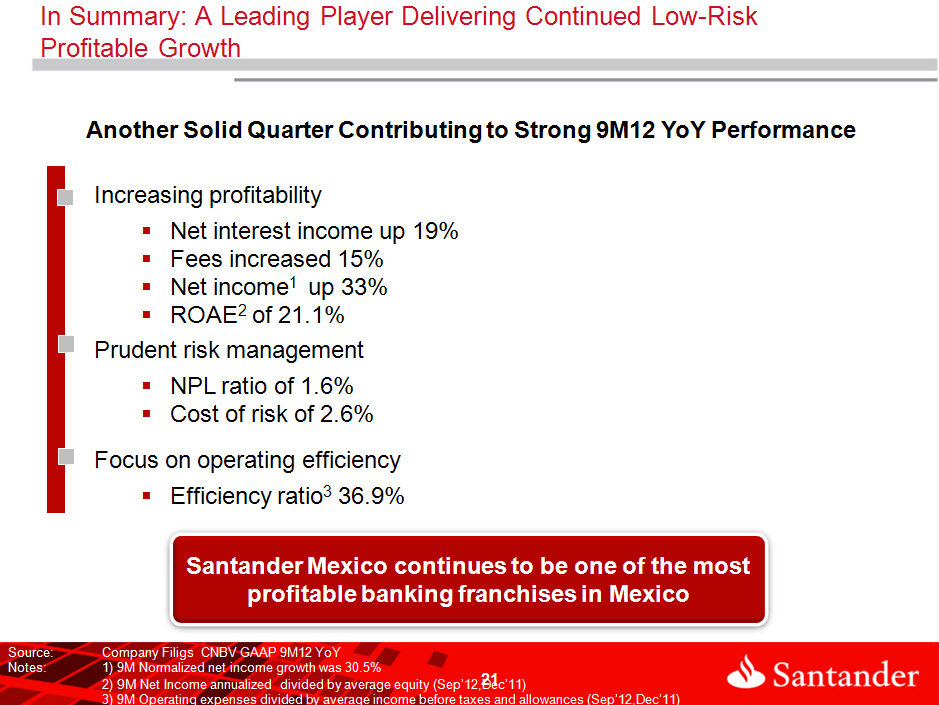

During 3Q12, Santander México reported net income of Ps.4,215 million, representing a 2.2% year-on-year (“YoY”) increase and a 20.2% sequential decrease. These comparisons however are affected by extraordinary gains in 3Q11 for the reversal of provisions to comply with CNBV (Comisión Nacional Bancaria y de Valores) regulations and in 2Q12 for the gain on the sale and leaseback of branches. Excluding these one time events, normalized net income increased 24.8% YoY and 3.5% sequentially. Consolidated net income for 9M12 was Ps.14,513 million, an increase of 32.6%, or Ps.3,572 million higher than the corresponding figure in 9M11. Excluding the aforementioned extraordinary gains in 3Q11 and 2Q12, net income for 9M12 increased 30.5% or Ps.3,107 million.

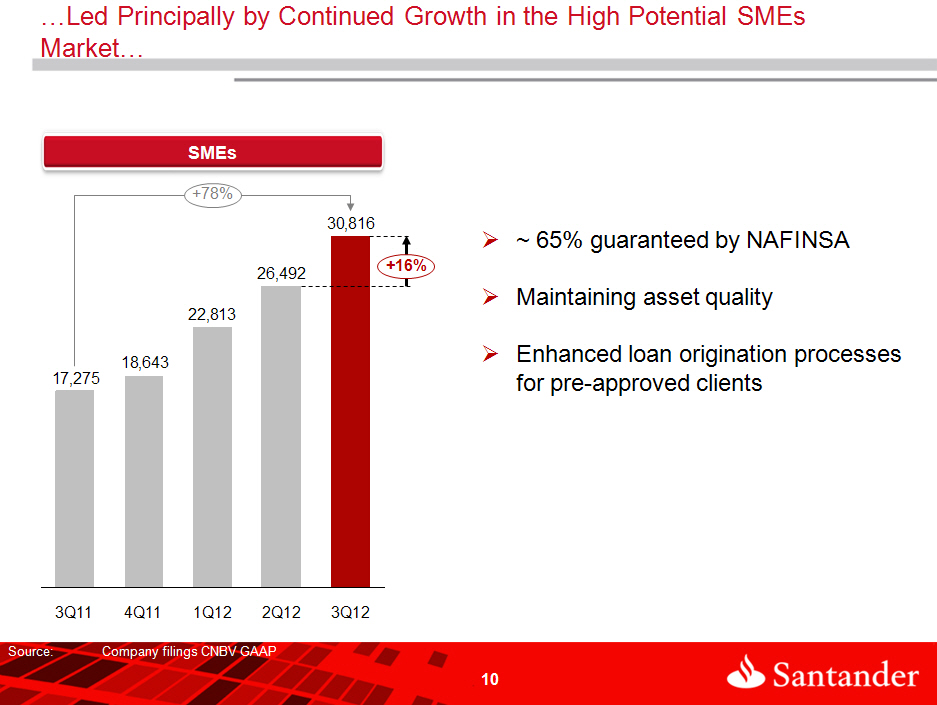

Marcos Martínez, Executive Chairman and CEO, commented, "We are pleased with our strong third quarter results, which reinforce the merits of our strategic focus on commercial banking, low-risk profitable growth and operational efficiency. We delivered year-on-year increases of 14.9% and 14.4% in net interest income and net commissions and fees, respectively. Furthermore, we executed well in our key business segments, as demonstrated by robust year-on-year growth of 28.6%, in both consumer loans and credit cards, as well as 78.4% increase in loans to small and medium enterprises (“SMEs”). Our focused growth strategy together with our strong emphasis on prudent risk management and an efficiency-oriented culture positions Santander México as one of the most profitable franchises in Mexico.”

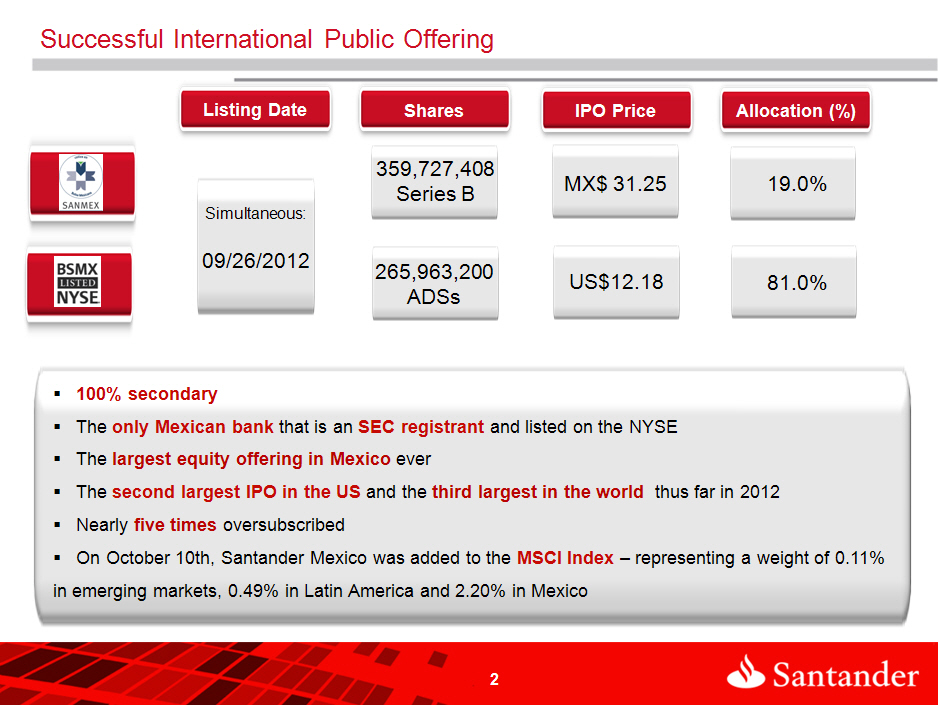

Mr. Martínez continued, “This quarter we achieved a significant milestone in Santander México’s history: our successful international public offering, which values the bank at 16.5 billion dollars. This transaction enhances the Company’s market position and brand recognition, while strengthening organizational transparency and market discipline. We begin a new chapter as a publicly traded company on strong footing and are well positioned to capitalize on the attractive fundamentals of Mexico’s banking industry.”

3Q. 12 | EARNINGS REPORT | 1

SUMMARY OF THIRD QUARTER 2012 CONSOLIDATED RESULTS

Net Income

Santander México reported net income of Ps.4,215 million in 3Q12, a 2.2% YoY increase, and 20.2% below 2Q12. Excluding the net impact from the reversal of provisions in 3Q11 and the gain from the sale of branches in 2Q12, net income would have increased 24.8% YoY and 3.5% sequentially, driven primarily by higher recurring income resulting from higher business volume. As a result, net interest margin and net commission and fee income increased QoQ by 2.2% and 8.1%, respectively.

Capitalization and ROAE

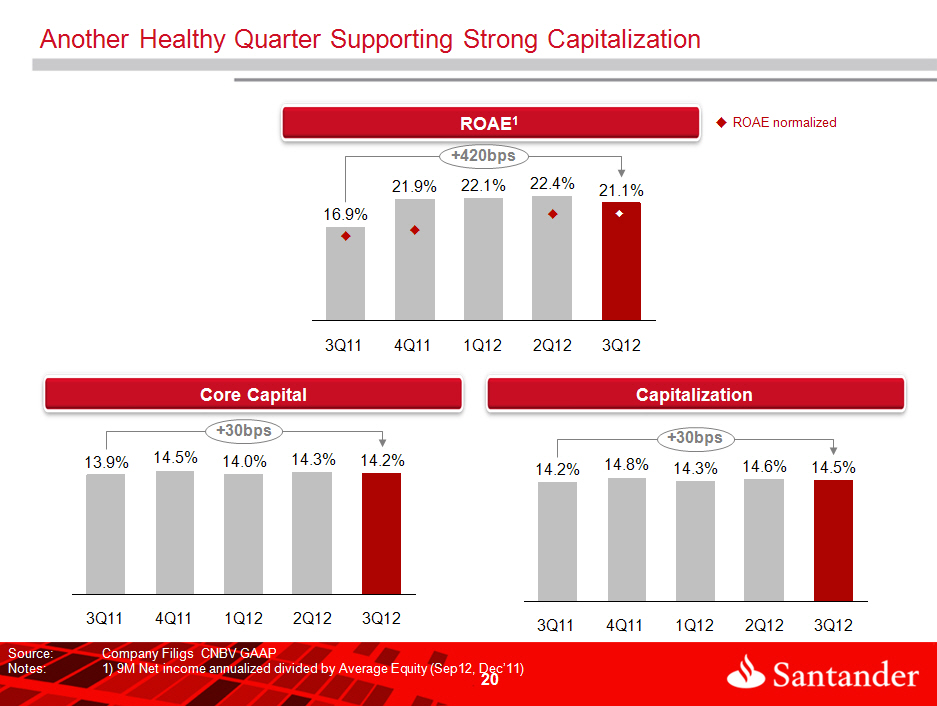

Santander México’s capital ratio was 14.45% in 3Q12, representing a 21 bps increase from 14.24% in 3Q11, and an 18 bps decline from 14.63% in 2Q12.

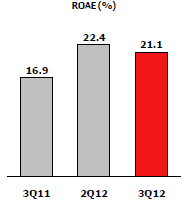

3Q12 ROAE was 21.1%, a 421 bps increase from 3Q11. On a a sequential basis, ROAE declined 127 bps reflecting the extraordinary gain from the sale of branches in 2Q12. Excluding this one-time event, normalized ROAE would have been 19.4% in 3Q12 and 19.8% in 2Q12, representing a slight decrease of 40 bps QoQ.

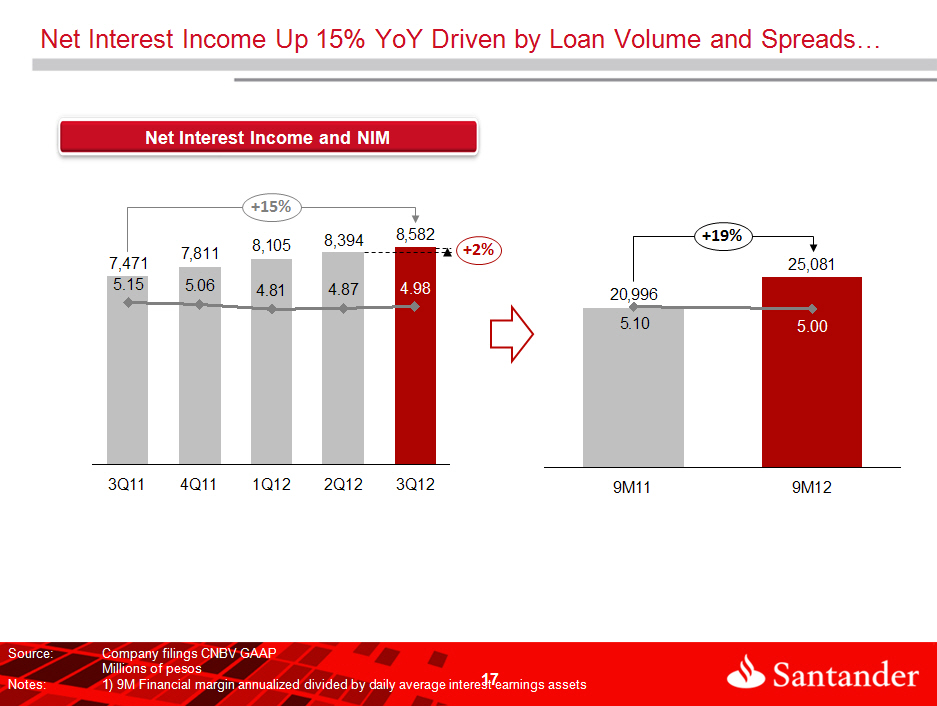

Net Interest Income

Net interest income in 3Q12 increased YoY by 14.9%, or Ps.1,111 million, to Ps.8,582 million. On a sequential basis net interest income rose 2.2%, or Ps.188 million.

Net interest margin for 3Q12 was 4.98%, increasing 11bps from 4.87% in 2Q12 and 17bps below 5.15% in 3Q11.

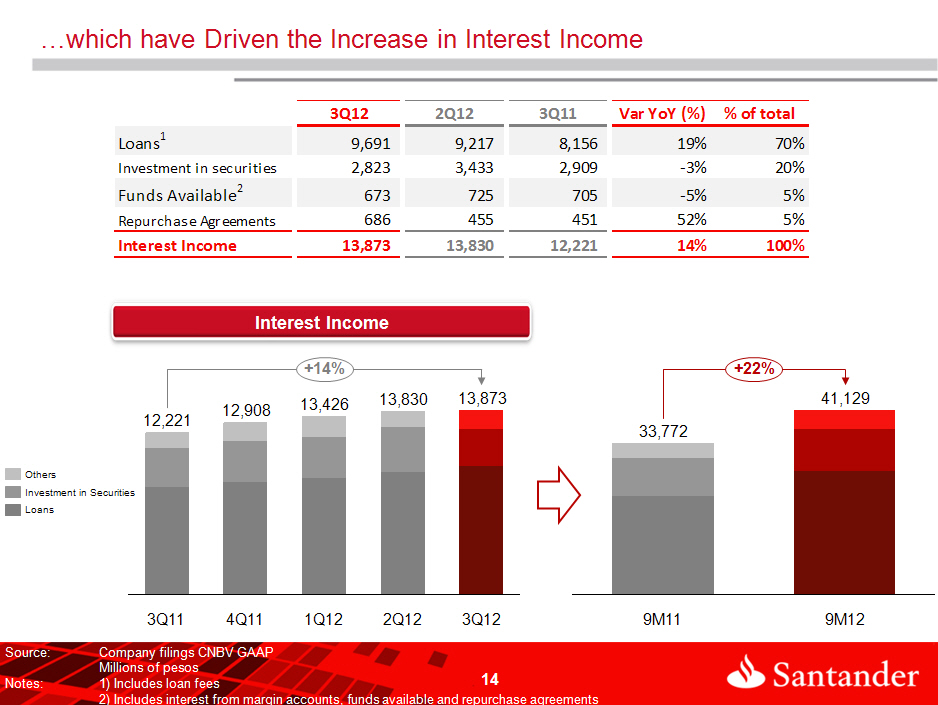

Interest income increased 13.5%, or Ps.1,652 million, reaching Ps.13,873 million in 3Q12 compared with Ps.12,221 million in 3Q11. This growth was mainly driven by higher interest income derived from our loan portfoilio which reached Ps.1,554 million.

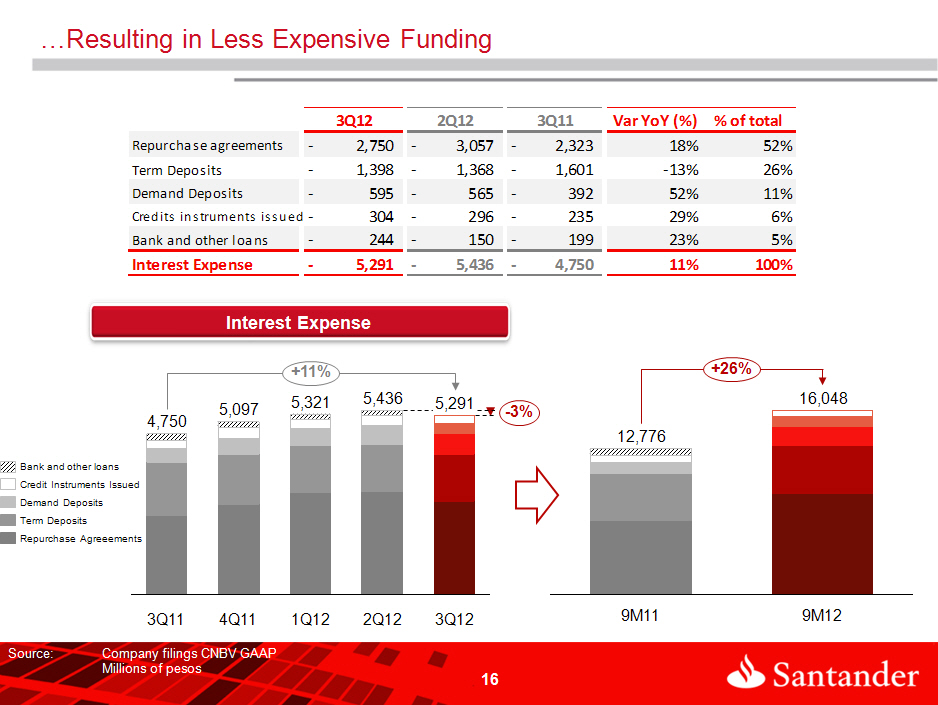

Interest expense increased 11.4%, or Ps.541 million, reaching Ps.5,291 million in 3Q12 compared with Ps.4,750 million in 3Q11. This growth was mainly driven by higher interest paid on our sale and repurchase agreements of Ps.427 million as a consequence of higher volumes.

3Q. 12 | EARNINGS REPORT | 2

Loan Portfolio Growth

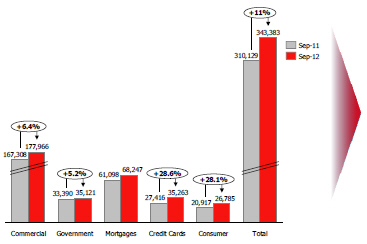

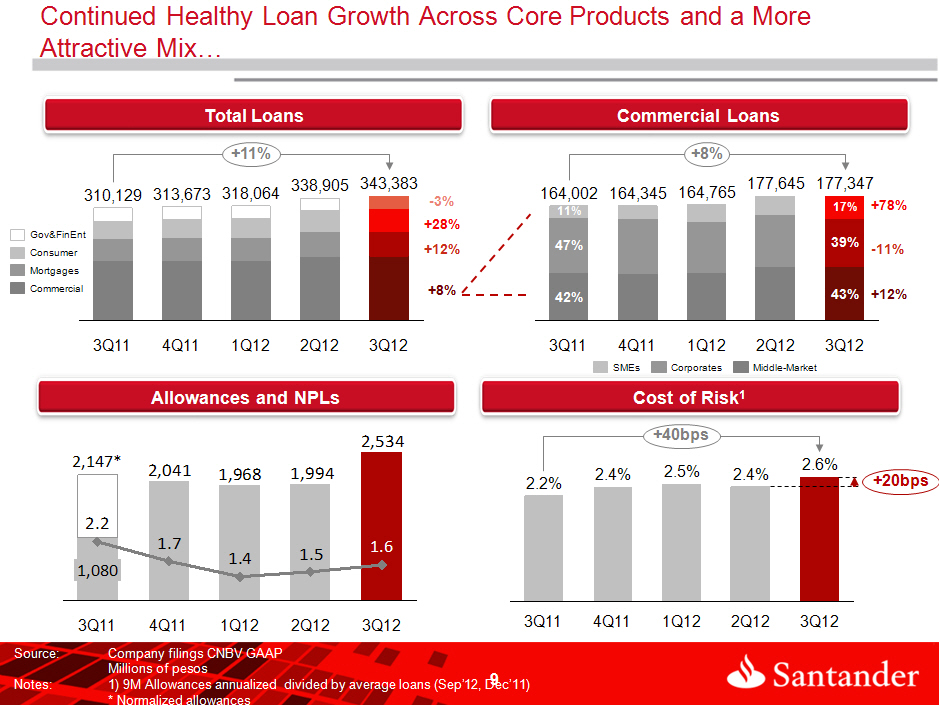

Santander México’s total loan portfolio in 3Q12 increased YoY by 10.7%, or Ps.33,254 million, to Ps.343,383 million, and 1.3%, or Ps.4,478 million, on a sequential basis.

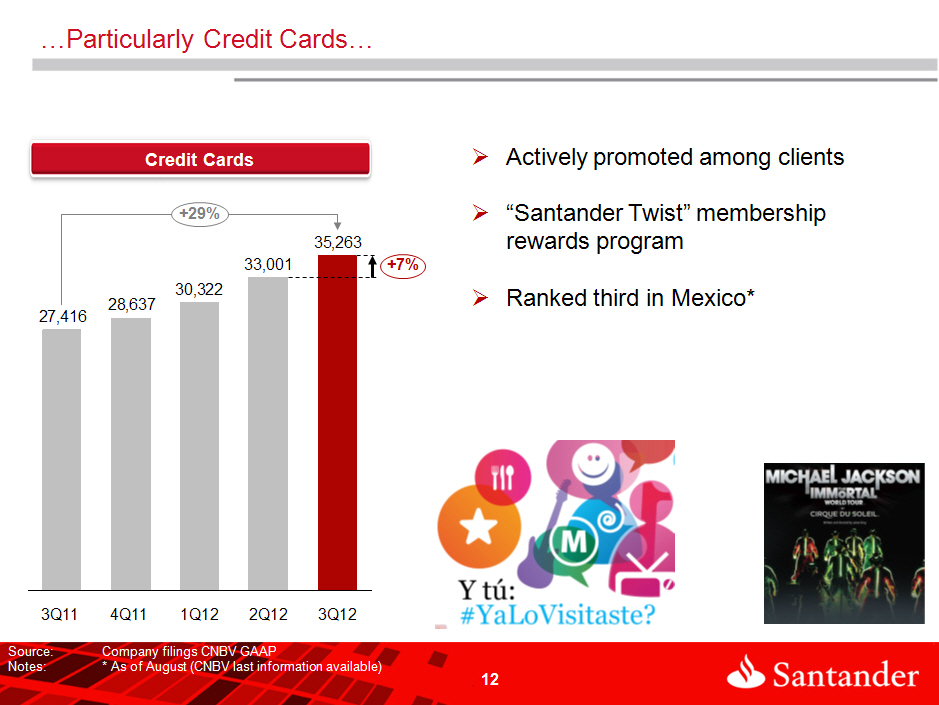

During 3Q12 Santander México continued to expand its loan portfolio across all core products, both in terms of commercial and individual loans. Individual loans were mainly driven by consumer loans, particualrly credit cards and mortgages. Commercial loans benefited from a significant YoY increase in the SME portfolio.

Asset Quality

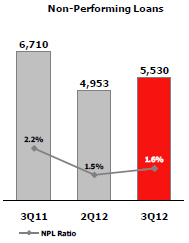

Non-performing loans as of 3Q12 declined to Ps.5,530 million, from Ps.6,710 million reported in 3Q11. On a sequential basis, non-performing loans increased 11.7%, or Ps.577 million.

The NPL ratio for 3Q12 declined to 1.6%, from 2.2% in 3Q11 and remained relatively unchanged from 1.5% in 2Q12, reflecting our stringent credit scoring model and ongoing monitoring of the quality of our portfolio.

The coverage ratio for the quarter increased to 205.4%, from 162.5% in 3Q11, but declined from 224.1% in 2Q12. This sequential decrease was mainly due to the nominal increase in non-performing loans resulting from the growth in the loan portfolio.

Loans to Deposit Ratio

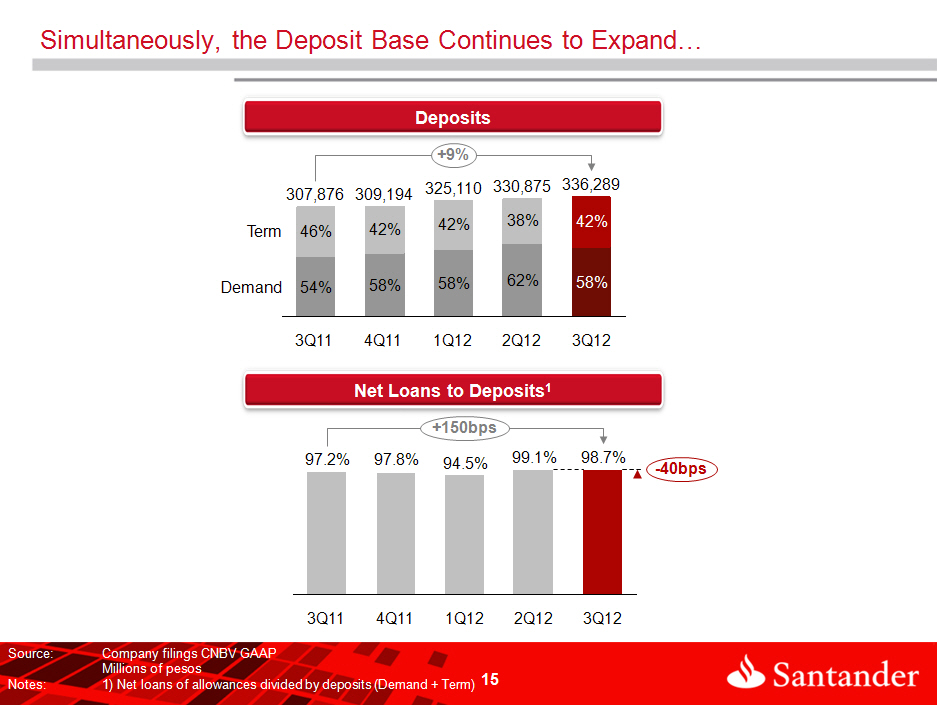

During 3Q12, deposits accounted for more than 50% of the Bank’s total funding sources, and expanded 9.2% YoY and 1.6% sequentially. This desposit base provides a stable, low cost source of funding to support the Bank’s continued growth.

The loan to deposit ratio was 98.7% in 3Q12, increasing from 97.2% in 3Q11, but declining from 99.1% in 2Q12.

Contribution to Net Income

As previously discussed, net income for 3Q12 was Ps.4,215 million, representing a 2.2% YoY increase and a 20.2% decline sequentially. Excluding the net impact of the reversal of provisions in 3Q11 and the gains from the sale of branches branches in 2Q12, net income would have increase 24.8% YoY and 3.5% sequentially.

Casa de Bolsa Santander, the brokerage business, reported net income of Ps.116 million, compared with a Ps.18 million loss reported in 3Q11 and a Ps.12 million gain in 2Q12.

Net income for the Holding and other subisidaries, amounted to Ps.29 million, compared with Ps.206 million in 3Q11 and Ps.32 million in 2Q12.

Grupo Financiero Santander México Earnings Contribution by Subsidiary | | | | | | |

| Million of Mexican Pesos | | | | | | |

| | 3Q12 | 2Q12 | 3Q11 | 9M12 | 9M11 | YoY % |

Banking business1/ | 4,069 | 5,240 | 3,934 | 14,179 | 10,381 | 36.6 |

| Brokerage | 116 | 12 | (18) | 216 | 31 | 596.8 |

Holding and other subsidiaries2/ | 29 | 32 | 206 | 117 | 528 | (77.8) |

| Net income attributable to Grupo Financiero Santander | 4,214 | 5,284 | 4,122 | 14,513 | 10,941 | 32.7 |

1/ Includes Sofomers 2/ Asset management subsidiary and Holding.

3Q. 12 | EARNINGS REPORT | 3

ANALYSIS OF THIRD-QUARTER 2012 CONSOLIDATED RESULTS

Net Income

Grupo Financiero Santander México Income Statement | | | | | | | | |

| Millions of Mexican Pesos | | | | % Change | | | % Change |

| | 3Q12 | 2Q12 | 3Q11 | QoQ | YoY | 9M12 | 9M11 | 12/11 |

| Net interest income | 8,582 | 8,394 | 7,471 | 2.2 | 14.9 | 25,081 | 20,995 | 19.5 |

| Provision for loan losses | (2,534) | (1,994) | (1,080) | (27.1) | (134.6) | (6,496) | (4,515) | (43.9) |

| Net interest income after provisions for loan losses | 6,048 | 6,400 | 6,391 | (5.5) | (5.4) | 18,585 | 16,480 | 12.8 |

| Commission and fee income, net | 3,065 | 2,836 | 2,680 | 8.1 | 14.4 | 8,864 | 7,736 | 14.6 |

| Gains (losses) on financial assets and liabilities | 921 | 106 | 29 | 768.9 | 3,075.9 | 1,781 | 939 | 89.7 |

| Other operating income (expenses) | 88 | 2,005 | 266 | (95.6) | (66.9) | 2,763 | 768 | 259.8 |

| Administrative and promotional expenses | (5,179) | (4,559) | (4,630) | (13.6) | (11.9) | (14,214) | (12,890) | (10.3) |

| Operating income | 4,943 | 6,788 | 4,736 | (27.2) | 4.4 | 17,779 | 13,033 | 36.4 |

| Equity in results of associated companies | 18 | 17 | 13 | 5.9 | 38.5 | 54 | 53 | 1.9 |

| Operating income before taxes | 4,961 | 6,805 | 4,749 | (27.1) | 4.5 | 17,833 | 13,086 | 36.4 |

| Current and deferred income taxes | (746) | (1,519) | (808) | 50.9 | 7.7 | (3,319) | (2,616) | (26.9) |

| Income from continuing operations | 4,215 | 5,286 | 3,941 | (20.3) | 7.0 | 14,514 | 10,470 | 38.6 |

| Profit from discontinued operations, net | 0 | 0 | 184 | 0.0 | (100.0) | 0 | 474 | (100.0) |

| Non-controlling interest | 0 | (1) | (2) | 100.0 | 100.0 | (1) | (3) | 66.7 |

| Net income | 4,215 | 5,285 | 4,123 | (20.2) | 2.2 | 14,513 | 10,941 | 32.6 |

Santander México reported net income of Ps.4,215 million in 3Q12, a 2.2% YoY increase and a 20.2%. sequential decline. Excluding the extraordinary impact from the net effect of the reversal of provisions for loan losses in 3Q11 and the gain from the sale of branches in 2Q12, net income would have increased 24.8% and 3.5%, respectively.

Net interest income for 3Q12 rose to Ps.8,582 million, representing a YoY increase of Ps.1,111 million, or 14.9%, and a sequential gain of Ps.188 million, or 2.2%. This increase resulted from the increase in the Bank’s business volume and a more profitable product mix, despite lower revenues from investments in securities.

Provisions for loan losses for the quarter rose to Ps.2,534 million, representing increases of Ps.1,454 million, or 134.6%, YoY and Ps.540 million, or 27.1%, on a sequential basis. Excluding the Ps.1,067 million reversal of provisions for loan losses in 3Q11, provisions for loan losses would have increased by Ps.387 million, or 18%, during the period.

The NPL ratio as of 3Q12 declined to 1.6%, from 2.2% in 3Q11, and remained relatively unchanged from 1.5% in 2Q12.

The coverage ratio for 3Q12 declined to 205.4%, from 224.1% reported in 2Q12, but increased from 162.5% in 3Q11 as a result of higher non-performing loans but in line with our loan growth.

3Q. 12 | EARNINGS REPORT | 4

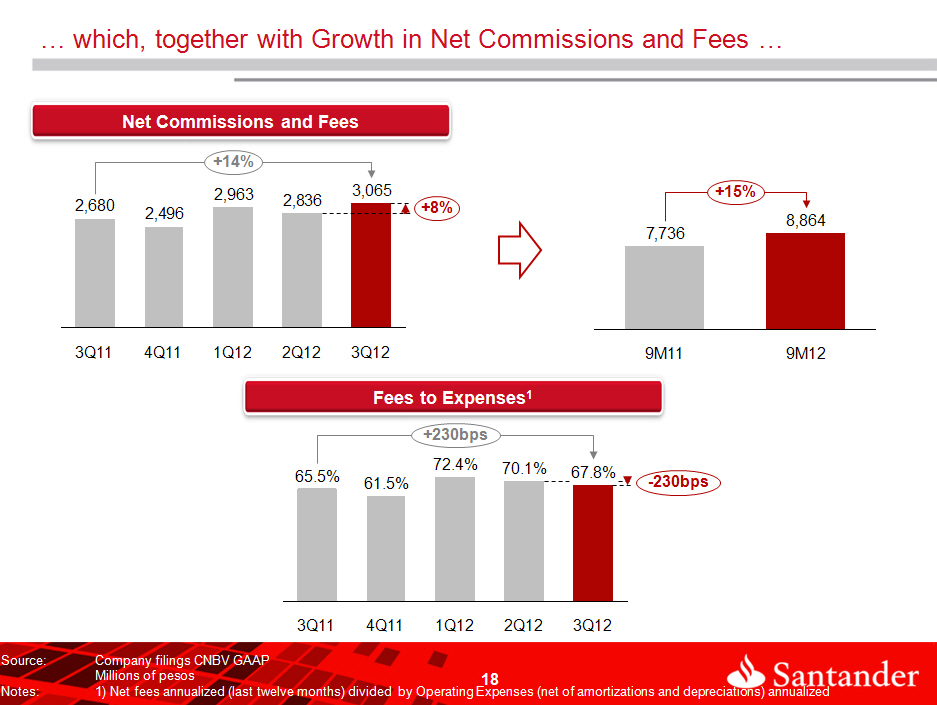

Net commissions and fee income for 3Q12 amounted to Ps.3,065 million, a YoY increase of 14.4%, or Ps.385 million and 8.1%, or Ps.229 million, higher on a sequential basis. The sequential increase is principally due to higher insurance, credit cards, and public offering fees.

Net gains from financial assets and liabilities income in 3Q12 increased to Ps.921 million, compared with Ps.29 million in 3Q11 and Ps.106 million in the 2Q12. Gains from financial assets and liabilities income in 3Q12 is mainly explained by the Ps.408 million valuation gain principally resulting from debt instruments, and a trading gain of Ps.513 million in 3Q12.

For 9M12, gains from financial assets and liabilities income increased to Ps.1,781 million, an 89.7% increase from 9M12 levels.

Other net income in 3Q12 declined to Ps.88 million, from Ps.266 million in 3Q11 and Ps.2,005 million in 2Q12. 2Q12 figures include an extraordinary gain of Ps.1,730 million derived from the sale of branches.

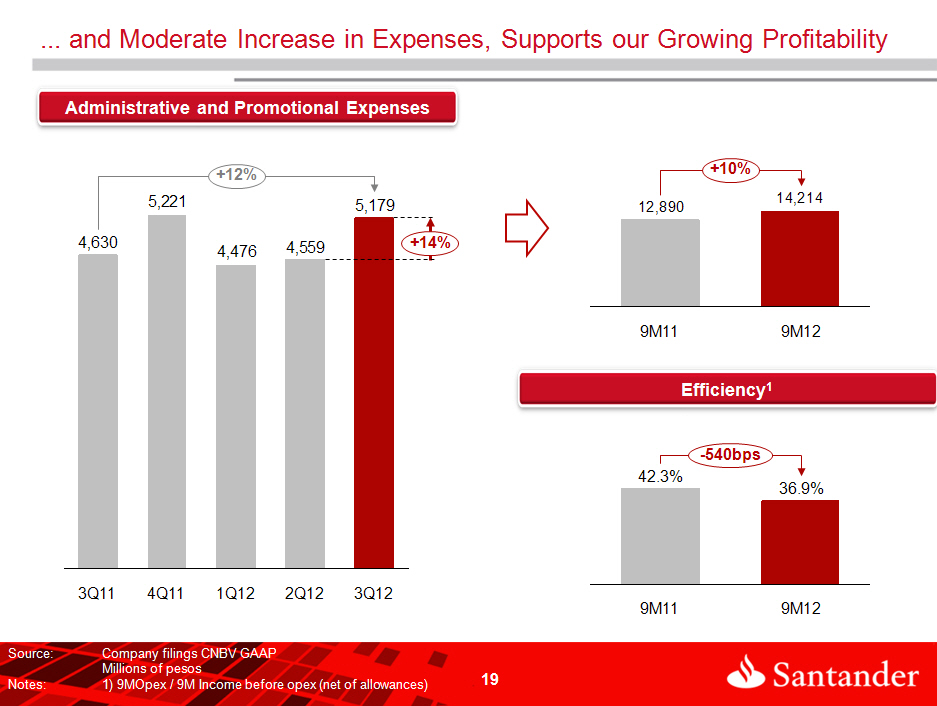

Administrative and promotional expenses as of 3Q12 amounted to Ps.5,179 million, that is Ps.549 million or 11.9% higher than in the 3Q11 and Ps.620 million or 13.6% higher than the amount reported in the 2Q12. The increase is mainly related to personnel and administrative expenses as a consequence of the growth in the business.

Other operating income in 3Q12, totaled Ps.4,943 million, representing a YoY increase of Ps.207 million, or 4.4%. On a sequential basis, other operating income decreased by Ps.1,845 million or 27.2% versus 2Q12. The above includes the effect of the extraordinary income obtained in the 2Q12, from the sale of the branches.

Net income as of 9M12 amounted to Ps.14,513 million, which is a Ps.3,572 million or 32.6% increase versus the Ps.10,941 million obtained in 9M11. Excluding extraordinary incomes, the net income for 9M12 increased Ps.3,107 million, or 30.5%, to Ps.13,301 million. This compares with Ps.10,194 million in 9M11.

These results reflect mainly the combined effect of the following:

| | § | 19.5%, or Ps.4,086 million, in the net interest income of Ps.20,995 million in 9M11 to Ps.25,081 million in the net interest income, basically explained by the increase in the loan portfolio; |

| | § | 14.6%, or Ps.1,128 million in net commissions and fee income, versus the Ps.7,736 million in 9M11 to Ps.8,864 million in 9M12, principally explained by fee income increase in insurance, management of account and technical assistance and public offers; |

| | § | 89.7%, or Ps.842 millions, in net gain from financial assets and liabilities of Ps.939 million in 9M11 to Ps.1,781 million in 9M12; and |

| | § | 259.8%, or Ps.1,995 million in other operating income of Ps.768 million in 9M11 to Ps.2,763 million in 9M12, explained by the Ps.1,730 million sale of the branches made in the 2Q12. |

These positive results were partially offset by:

| | § | Growth in loans provisions for loan losses for Ps.1,981 million, or 43.9%, mainly due to the growth in the loan portfolio as well as the reversal of provisions for loan losses of Ps.1,067 million in 3Q11; and |

| | § | Ps.1,324 million or 10.3% increase in administrative and promotional expenses of Ps.12,890 million in 9M11, to Ps.14,214 million in 9M12, mainly explained by the 12.9% increase in personnel expenses. |

Furthermore, as of 9M12 current and deferred income taxes increased by Ps.703 million or 26.9%, reaching Ps.3,319 million compared with the same period last year.

3Q. 12 | EARNINGS REPORT | 5

Net Interest Income

Grupo Financiero Santander México Net Interest Income | | | | | | | | |

| Millions of Mexican Pesos | | | | % Change | | | % Change |

| | 3Q12 | 2Q12 | 3Q11 | QoQ | YoY | 9M12 | 9M11 | 12/11 |

| Interest income | | | | | | | | |

| Funds Available | 662 | 711 | 662 | (6.9) | 0.0 | 2,107 | 1,920 | 9.7 |

| Margin accounts | 11 | 14 | 43 | (21.4) | (74.4) | 53 | 138 | (61.6) |

| Interest from investment in securities | 2,823 | 3,433 | 2,909 | (17.8) | (3.0) | 9,382 | 8,534 | 9.9 |

| Loan portfolio – excluding credit cards | 7,399 | 7,083 | 6,332 | 4.5 | 16.9 | 21,263 | 16,978 | 25.2 |

| Credit card loan portfolio | 2,141 | 1,975 | 1,654 | 8.4 | 29.4 | 5,943 | 4,803 | 23.7 |

| Loan origination fees | 151 | 159 | 170 | (5.0) | (11.2) | 482 | 440 | 9.5 |

| Sale and repurchase agreements | 686 | 455 | 451 | 50.8 | 52.1 | 1,899 | 959 | 98.0 |

| Interest Income | 13,873 | 13,830 | 12,221 | 0.3 | 13.5 | 41,129 | 33,772 | 21.8 |

| | | | | | | | | |

| Interest expense and similar charges | | | | | | | | |

| Customer deposits – Demand deposits | (595) | (565) | (392) | (5.3) | (51.8) | (1,656) | (1,035) | (60.0) |

| Customer deposits – Time deposits | (1,398) | (1,368) | (1,601) | (2.2) | 12.7 | (4,134) | (4,100) | (0.8) |

| Credit instruments issued | (304) | (296) | (235) | (2.7) | (29.4) | (896) | (592) | (51.4) |

| Interbank loans | (244) | (150) | (199) | (62.7) | (22.6) | (527) | (598) | 11.9 |

| Sale and repurchase agreements | (2,750) | (3,057) | (2,323) | 10.0 | (18.4) | (8,835) | (6,452) | (36.9) |

| Interest Expense | (5,291) | (5,436) | (4,750) | 2.7 | (11.4) | (16,048) | (12,777) | (25.6) |

| | | | | | | | | |

| Net Interest Income | 8,582 | 8,394 | 7,471 | 3.0 | 2.1 | 25,081 | 20,995 | 19.5 |

Net interest income in 3Q12 amounted to Ps.8,582 million, representing QoQ and YoY increases of 2.2%, Ps.188 million, and 14.9%, or Ps.1,111 million, respectively. During 9M12, net interest income rose 19.5%, or Ps.4,086 million, to Ps.25,081 million, from Ps.20,995 million in 9M11. This is principally explained by an increase in interest income on the loan portfolio.

The YoY increase in net interest income is explained by the combined effect of the Ps.1,652 million increase in interest income, from Ps.12,221 million in 3Q11 to Ps$13,873 million in 3Q12, and a Ps.541 million increase in interest expense, from Ps.4,750 million in 3Q11 to Ps. 5,291 million in 3T12. This was the result of a Ps.71,262 million increase in average interest-earnings assets, together with an 11 basis points increase in the average interest rate gained. Average interest-bearing liabilities rose Ps.43,376 million, presenting a 9 basis points increase in the average interest rate paid.

The sequential increase in net interest income is explained by the combined effect of the Ps.43 million increase in interest income, from Ps.13,830 million in 2Q12 to Ps.13,873 million in 3Q12, and a Ps.145 million decline in interest expense, from Ps.5,436 million in 2Q12 to Ps.5,291 million in 3Q12. This is explained by the Ps.16,332 million decline in average-earnings assets, together with a 23 basis points increase in the average interest rate earned, combined with a Ps.16,622 million decline in interest-bearing liabilities, together with a 1 basis point increase in the average interest rate paid.

The increase in net interest income in the nine month period, is explained by the combined effect of the Ps.7,357 million increase in interest income, from Ps.33,772 million in 9M11 to Ps.41,129 million in 9M12, and a Ps.3,271 million increase in interest expense, from Ps. 12,776 million in 9M11 to Ps.16,048 million in 9M12. This is explained by the Ps.127,964 million decline in average-earnings assets, together with a 12 basis points

3Q. 12 | EARNINGS REPORT | 6

decline in the average interest rate earned, combined with a Ps.90,248 million decline in average interest-bearing liabilities, together with an 18 basis point increase in the average interest rate paid.

Interest Income

Interest income was Ps.13,830 million in 2Q12 and Ps.13,873 million in 3Q12. This is explained by the combined increase of Ps.482 million in the loan portfolio and Ps.231 million from the increase in sale and repurchase agreements, negatively impacted by lower interest income on investment in securities for Ps.610 million resulting from the decline of Ps.50,559 million in the average balance of investments in securities.

Interest income increased YoY by 13.5%, or Ps.1,652 million, from Ps.12,221 million in 3Q11 to Ps.13,873 million in 3Q12, principally resulting from the increase in interest income on our loan portfolio of Ps.1,554 million.

The breakdown of interest income for 3Q12 is as follows: loan portfolio 66.9%, investment in securities 20.3%, and 9.8% in other items.

The average interest gain on interest-earning assets increased in 3Q12 to 8.36%, representing an 11 basis points increase from 8.25% in 3Q11 and a 23 basis point growth compared with 8.13% in 2Q12.

3Q12 interest-earning assets decreased by Ps.16,332 million, or 2.4%, mainly driven by: a decline in lower investments in securities of PS.50,559 million, from Ps.254,393 million in 2Q12 to Ps.203,384 million in 3Q12.

9M12 average interest-earning assets increased by 23.5%, or Ps.127,964 million, to Ps.671,752 million, compared with Ps.543,788 million in 9M11.

9M12 interest income increased by Ps.7,357 million, or 21.78%, to Ps.41,129 million, compared with Ps.33,772 in 9M11.

The evolution of the loan portfolio continues to show positive trends, the diversification among all segments, and growth in all core businesses.

Loan Portfolio Composition

3Q. 12 | EARNINGS REPORT | 7

Loan Portfolio

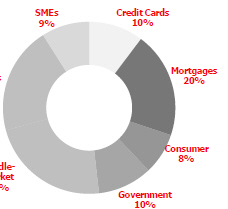

The total loan portfolio rose YoY by 10.7%, or Ps.33,254 million, to Ps.343,383 million as of 3Q12. On a sequential basis, the total loan portfolio increased 1.3%, or Ps.4,478 million. During the quarter, Santander México continued to experience loan growth across all core segments and products.

Grupo Financiero Santander México Loan Portfolio Breakdown | | | | | | | | |

| Millions of Mexican Pesos | | | | | | | | |

| | | | | | | | | |

| | 3Q12 | % | | 2Q12 | % | | 3Q11 | % |

| Commercial | 176,564 | 51.4% | | 176,938 | 52.2% | | 165,468 | 53.4% |

| Government | 35,121 | 10.2% | | 35,554 | 10.5% | | 31,997 | 10.3% |

| Consumer | 59,996 | 17.5% | | 57,043 | 16.8% | | 47,101 | 15.2% |

| Credit cards | 34,208 | 10.0% | | 32,053 | 9.5% | | 26,692 | 8.6% |

| Other | 25,788 | 7.5% | | 24,990 | 7.4% | | 20,409 | 6.6% |

| Mortgages | 66,172 | 19.3% | | 64,417 | 19.0% | | 58,853 | 19.0% |

| Total Performing Loan | 337,853 | 98.4% | | 333,952 | 98.5% | | 303,419 | 97.8% |

| | | | | | | | | |

| Commercial | 1,402 | 0.4% | | 1,313 | 0.4% | | 1,840 | 0.6% |

| Government | 0 | 0.0% | | 0 | 0.0% | | 1,393 | 0.4% |

| Consumer | 2,053 | 0.6% | | 1,709 | 0.5% | | 1,232 | 0.4% |

| Credit cards | 1,055 | 0.3% | | 948 | 0.3% | | 724 | 0.2% |

| Other | 998 | 0.3% | | 761 | 0.2% | | 508 | 0.2% |

| Mortgages | 2,075 | 0.6% | | 1,931 | 0.6% | | 2,245 | 0.7% |

| Total Non-Performing Loan | 5,530 | 1.6% | | 4,953 | 1.6% | | 6,710 | 2.2% |

| | | | | | | | | |

| Total Loan Portfolio | 343,383 | 100.0% | | 338,905 | 100.0% | | 310,129 | 100.0% |

3Q. 12 | EARNINGS REPORT | 8

The Commercial Portfolio, is composed of loans to business and commercial enterprises, as well as loans to government entities and financial institutions, and represents 62.1% of the total performing loans portfolio. Excluding loans to government, the commercial portfolio accounted for 51.8% of the total performing loans portfolio as of 3Q12 and increased 6.4% YoY, principally reflecting the 78.4% and 11.5% increase in SMEs and middle market, respectively. On a sequential basis, and excluding loans to government, the commercial portfolio declined 0.2%, principally supported by the performance of SMEs and middle market during the quarter, which increased 16.9% and 0.4%, respectively. Growth in these segments principally reflects Santander México’s focus on supporting the develpoment of SMEs and therefore the growth of the country.

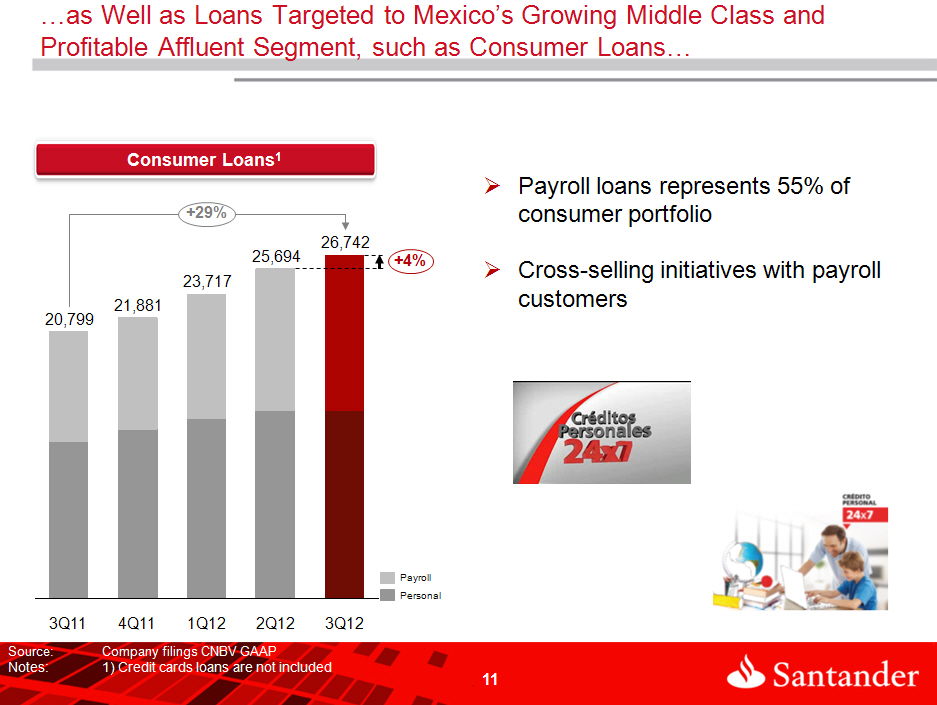

The Individual Loan Portfolio, composed of mortgages, credit card and consumer loans, represents 37.9% of the total loan portfolio. Credit cards, consumer and mortgages loans represent 10.3%, 7.8%, and 19.9% of the total loan portfolio, respectively, and increased YoY by 28.6%, 28.1%, and 11.7%, respectively. This quarter credit card loans increased 6.9% sequentially, reversing a previously reported downward trend in credit card loans. Our mortgage loans strategy remains focused on targeting the middle market segment and residential. Our strategy for consumer loans aims to support families, and loans to this client segment increased 4.1% QoQ. Overall growth in the consumer loan portfolio this quarter was principally driven by the efforts and outstanding results achieved by our commercial teams throughout our branch network, and the progression of our multichannel strategy, which helped drive a 48% YoY increase in consumer loan origination.

Interest Expense

Interest expense increased 11.4%, or Ps.541 million, to Ps.5,291 million in 3Q12, compared with Ps.4,750 million in 3Q11, principally explained by the Ps.427 million increase in interest paid on sale and repurchase agreements due to higher volume. On a sequential basis, interest expense fell Ps.145 million, mainly reflecting a decrease in the average balance of sale and repurchase agreements.

In 9M12 interest expense was Ps.16,048 million, a Ps.3,272 million increase, compared with Ps.12,777 million recorded in 9M11.

The Ps.5,291 million in interest expenses paid in 3Q12, is broken down as follows: sale and repurchase agreements 52%, term deposits 26.4%, demand deposits 11.2%, credit instruments issued 5.7%, and interbank loans 4.7%.

3Q. 12 | EARNINGS REPORT | 9

Total deposits at the end of 3Q12 amounted to Ps.336,289 million, or 9.2% higher than the corresponding figure at quarter-end 3Q11. Santander México continues to implement its strategy of enhancing customer service, in accordance with the needs of each segment. This strategy has allowed us to increase demand deposits from both individuals and corporates. As of 3Q12, demand deposits reached Ps.194,351 million, increasing 16.4% YoY, and declining 5.0% on a sequential basis. Total term deposits remained stable at Ps.141,938 million YoY, and increased 12.4% compared with 2Q12.

Interest expense on demand deposits amounted to Ps.595 million during 3Q12, representing YoY and sequential increases of 51.8% and 5.3%, respectively, driven by a higher average balance in demand deposits and an increase in the interest rate paid.

Interest paid on term deposits declined 12.7% YoY to Ps.1,398 million. On a sequential basis, interest paid on term deposits increased 2.2% reflecting average volume increase together with an average rate increase.

Asset Quality

Non-performing loans at the end of 3Q12 declined by Ps.1,180 million, or 17.6% YoY, to Ps.5,530 million, but increased on a sequential basis by 11.7%, or Ps.577 million. The breakdown of the non-performing loan portfolio is as follows: commercial loans 26.5%, consumer loans 34.5%, and mortgages 39%.

The YoY decrease in non-performing loans, is basically due to a regularization of government non-performing loans, which in 3Q11 accounted for Ps.1,393 million. In addition, a decrease in non-performing commercial and mortgage loans, offset higher non-performing consumer and credit card loans. The sequential increase in non-performing loans is principally due to increases in consumer loans, credit cards loans, and to a lesser extent in mortgage loans.

| Grupo Financiero Santander México | | | | | | |

| Asset Quality | | | | | | | |

| Millions of Pesos | | | | | | | |

| | | 2012 | | 2011 | | Change % |

| | 3Q12 | 2Q12 | | 3Q12 | | QoQ | YoY |

| Total Loans | 343,383 | 338,905 | | 310,129 | | 1.32% | 10.72 |

| Performing Loans | 337,853 | 333,952 | | 303,419 | | 1.17% | 11.35 |

| Non-performing Loans | 5,530 | 4,953 | | 6,710 | | 11.65% | (17.59) |

| | | | | | | | |

| Allowance for loan losses | (11,360) | (11,101) | | (10,906) | | 2.33% | 4.16 |

| | | | | | | | |

| Non-performing loan ratio | 1.61% | 1.46% | | 2.16% | | 15bps | (55)bps |

| Coverage ratio | 205.4 | 224.1 | | 162.5 | | (1,870)bps | 4,292bps |

3Q. 12 | EARNINGS REPORT | 10

The NPL ratio improved to 1.6% in 3Q12, from 2.2% in 3Q11 and remained essentially unchanged compared with the 1.5% reported in 2Q12, reflecting our strict monitoring and portfolio quality assessment processes, which allows the adjustment of loan origination through approval policies in accordance with the performance of the loan portfolio. The coverage ratio for the quarter increased to 205.4%, from 162.5% in 3Q11, but declined from 224.1% in 2Q12. The sequential decrease mainly reflects a nominal increase in non-performing loans resulting from the growth in the loan portfolio.

During 3Q12 allowance for loan losses amounted to Ps.2,534 million, which represented a 27.1% increase compared with 2Q12, principally generated in the mortgage and credit card loan portfolios.

During 9M12, allowances for loan losses increased by 43.9%, or Ps.1,981 million, to Ps.6,496 million compared with the same period last year. This increase is mainly explained by the 10.7% growth in the loan portfolio during the last twelve months, negatively impacted by the reversal of provisions in 3Q11.

3Q. 12 | EARNINGS REPORT | 11

Commission and Fee Income (Net)

Grupo Financiero Santander México Commission and Fee Income | | | | | | | | |

| Millions of Mexican Pesos | | | | | | | | |

| | | | | % Change | | | % Change |

| | 3Q12 | 2Q12 | 3Q11 | QoQ | YoY | 9M12 | 9M11 | 12/11 |

| Credit and debit cards | | | | | | | | |

| Cash management | 1,026 | 926 | 859 | 10.8 | 19.4 | 2,816 | 2,430 | 15.9 |

| Collection and payment services | 176 | 179 | 159 | (1.7) | 10.7 | 530 | 418 | 26.8 |

| Insurance | 347 | 365 | 291 | (4.9) | 19.2 | 1,083 | 949 | 14.1 |

| Investment fund management | 783 | 737 | 593 | 6.2 | 32.0 | 2,193 | 1,656 | 32.4 |

| Financial advisory services | 461 | 465 | 483 | (0.9) | (4.6) | 1,386 | 1,413 | (1.9) |

| Capital markets and securities activities | 430 | 244 | 318 | 76.2 | 35.2 | 1,064 | 963 | 10.5 |

| Checks | 151 | 162 | 147 | (6.8) | 2.7 | 468 | 412 | 13.6 |

| Foreign trade | 86 | 89 | 96 | (3.4) | (10.4) | 265 | 288 | (8.0) |

| Other commissions and fees | 126 | 144 | 96 | (12.5) | 31.3 | 397 | 367 | 8.2 |

| Total | 197 | 195 | 173 | 1.0 | 13.9 | 589 | 507 | 16.2 |

| | 3,783 | 3,506 | 3,215 | 7.9 | 17.7 | 10,791 | 9,403 | 14.8 |

| Fee and Commission Expenses | | | | | | | | |

| Credit and debit cards | | | | | | | | |

| Insurance | (377) | (375) | (282) | (0.5) | (33.7) | (1,039) | (723) | (43.7) |

| Investment fund management | (22) | (23) | (16) | 4.3 | (37.5) | (64) | (48) | (33.3) |

| Capital markets and securities activities | (28) | (27) | (26) | (3.7) | (7.7) | (79) | (74) | (6.8) |

| Checks | (46) | (40) | (30) | (15.0) | (53.3) | (121) | (104) | (16.3) |

| Financial advisory services | (9) | (9) | (10) | 0.0 | 10.0 | (27) | (32) | 15.6 |

| Other commissions and fees | (11) | (1) | (1) | (1,000.0) | (1,000.0) | (22) | (207) | 89.4 |

| Total | (225) | (195) | (170) | (15.4) | (32.4) | (575) | (479) | (20.0) |

| | (718) | (670) | (535) | (7.2) | (34.2) | (1,927) | (1,667) | (15.6) |

| Commission and Fee Income, net | | | | | | | | |

| Credit and debit cards | 3,065 | 2,836 | 2,680 | 8.1 | 14.4 | 8,864 | 7,736 | 14.6 |

In 3Q12 net commission and fee income amounted to Ps.3,065 million, representing a YoY increase of 14.4%, or Ps.385 million. The improvement compared to 3Q11 principally reflects the following YoY increases: 19.2%, or Ps.56 million, in credit and debit card fees; 31.9%, or Ps.184 million, in insurance fees; and 32.2%, or Ps.102 million, in financial advisory services.

Compared to 2Q12, net commission and fee income rose 8.1%, or Ps.229 million, mainly reflecting the

3Q. 12 | EARNINGS REPORT | 12

following sequential increases: 17.8%, or Ps.98 million, in credit card fees; 72.4%, or Ps.176 million, in financial advisory services fees primarily related to public debt and equity offerings; and 6.6%, or Ps.47 million, in insurance fees mainly reflecting growth of “Autocompara”.

During 9M12, net commission and fee income increased 14.6% YoY, or Ps.1,128 million, to Ps.8,864 million.

Net gain (loss) on financial assets and liabilities

Grupo Financiero Santander México Net gain (loss) on financial assets and liabilities Millions of Mexican Pesos | | | |

| | | | | % Change | | | % Change |

| | 3Q12 | 2Q12 | 3Q11 | QoQ | YoY | 9M12 | 9M11 | 12/11 |

| Valuation | | | | | | | | |

| Foreign currencies | (110) | 15 | 89 | (833.3) | (223.6) | (81) | 79 | (202.5) |

| Derivatives | (9) | (542) | 646 | 98.3 | (101.4) | (3) | (3,221) | 99.9 |

| Shares | 1 | 221 | (1,134) | (99.5) | 100.1 | 113 | (2,479) | 104.6 |

| Debt instruments | 526 | 435 | 550 | 20.9 | (4.4) | 1,026 | 439 | 133.7 |

| Subtotal | 408 | 129 | 151 | 216.3 | 170.2 | 1,055 | (5,182) | 120.4 |

| | | | | | | | | |

| Trading | | | | | | | | |

| Foreign currencies | 191 | 659 | 204 | (71.0) | (6.4) | 529 | 932 | (43.2) |

| Derivatives | 338 | (1,017) | 1,013 | 133.2 | (66.6) | (311) | 5,738 | (105.4) |

| Shares | 135 | 274 | (786) | (50.7) | 117.2 | 722 | (304) | 337.5 |

| Debt instruments | (151) | 61 | (553) | (347.5) | 72.7 | (214) | (245) | 12.7 |

| Subtotal | 513 | (23) | (122) | 2,330.4 | 520.5 | 726 | 6,121 | (88.1) |

| | | | | | | | | |

| Total | 921 | 106 | 29 | 768.9 | 3,075.9 | 1,781 | 939 | 89.7 |

In 3Q12, Santander México recorded a net gain on financial assets and liabilities of Ps.921 million, compared with Ps.29 million in 3Q11 and Ps.106 million in the 2Q12. Net gain on financial assets and liabilities in 3Q12 is mainly explained by a valuation gain of Ps.408 million principally related to debt instruments held, and trading gains of Ps.513 million in 3Q12.

Net gain on financial assets and liabilities in 3Q11 is principally the result of a Ps.151 million valuation gain, despite equity valuation losses. This was partially offset by a trading loss of Ps.122 million, as equity and debt instrument trading losses exceeded the gain from derivative instruments.

In 2Q12, a Ps.129 million valuation gain, resulting mainly from equity positions was partially offset by a of Ps.23 million trading loss, explained by a derivative trading loss.

3Q. 12 | EARNINGS REPORT | 13

Other Operating Income (Expense)

Grupo Financiero Santander México Other Operating Income (Expense) | | | | | | | | |

| Millions of Mexican Pesos | | | | % Change | | | % Change |

| | 3Q12 | 2Q12 | 3Q11 | QoQ | YoY | 9M12 | 9M11 | 12/11 |

| | | | | | | | | |

| Recoveries of loans previously charged-off | 467 | 457 | 392 | 2.1 | 19.1 | 1,365 | 1,118 | 22.1 |

| Income from sale of fixed assets | 1 | 1,730 | 0 | (100.0) | 0.0 | 1,732 | 0 | 0.0 |

| Allowance for loan losses released | 0 | 0 | 0 | 0.0 | 0.0 | 378 | 0 | 0.0 |

| Cancellation of liabilities and reserves | 43 | 64 | 33 | (33.3) | 29.3 | 154 | 121 | 27.0 |

| Interest on personnel loans | 31 | 29 | 27 | 8.3 | 16.3 | 89 | 81 | 10.4 |

| Recovered taxes | 0 | 0 | 15 | 0.0 | (100.0) | | 15 | (100.0) |

| Foreclosed assets reserve | (7) | (9) | (18) | 22.2 | 61.1 | (31) | (25) | (23.6) |

| Profit from sale of foreclosed assets | 44 | 34 | 7 | 29.4 | 528.6 | 112 | 12 | 836.0 |

| Acquisition of discounted loan portfolio | 0 | 0 | 0 | 0.0 | 0.0 | 0 | 112 | (100.0) |

| Technical advisory services | 25 | 32 | 17 | (21.3) | 48.2 | 75 | 52 | 44.6 |

| Portfolio recovery legal expenses and costs | (117) | (174) | (91) | 32.7 | (28.7) | (431) | (331) | (30.3) |

| Write-offs and bankruptcies | (343) | (160) | (59) | (114.4) | (481.4) | (614) | (269) | (128.3) |

| Provision for legal and tax contingencies | (97) | (53) | (23) | (83.9) | (323.7) | (199) | (142) | (40.5) |

| IPAB (indemnity) provisions and payments | (2) | (28) | (3) | 91.1 | 17.0 | (33) | (9) | (272.1) |

| Recoveries of loans previously charged-off | 44 | 83 | (31) | (47.0) | 241.9 | 167 | 33 | 406.1 |

| Total | 88 | 2,005 | 266 | (95.6) | (67.0) | 2,763 | 768 | 259.8 |

In 3Q12 other operating income declined to Ps.88 million, from Ps.266 million in 3Q11 and from Ps.2,005 million in 2Q12, which included an extraordinary gain of Ps.1,731 million derived from the sale of 220 branches to Fibra Uno. This gain on sale was partially offset by higher write-offs and losses in 3Q12.

During 9M12, other net operating income increased to Ps.2,763 million, compared with Ps.768 million in 9M11.

Administrative and Promotional Expenses

Administrative and promotional expenses consist of personnel such as payroll and benefits, promotion and advertising expenses, and other general expenses. Personnel expenses consist mainly of salaries, social security contributions, bonuses and our long-term incentive plan for our executives. Other general expenses mainly consist of: expenses related to technology and systems, administrative services, which are mainly services outsourced in the areas of information technology, taxes and duties, professional fees, contributions to IPAB, rental of properties and hardware, advertising and communication, surveillance and cash courier services and expenses related to maintenance, conservation and repair, among others

3Q. 12 | EARNINGS REPORT | 14

Grupo Financiero Santander México Administrative and Promotional Expenses | | | | | | �� | | |

| Millions of Mexican Pesos | | | | % Change | | | % Change |

| | 3Q12 | 2Q12 | 3Q11 | QoQ | YoY | 9M12 | 9M11 | 12/11 |

| Salaries and employee benefits | 2,172 | 2,154 | 1,918 | 0.8 | 13.2 | 6,394 | 5,664 | 12.9 |

| Credit card operation | 100 | 12 | 64 | 733.3 | 56.3 | 177 | 141 | 25.5 |

| Professional fees | 107 | 141 | 209 | (24.1) | (48.8) | 371 | 494 | (24.9) |

| Leasehold | 339 | 326 | 279 | 4.0 | 21.5 | 904 | 734 | 23.2 |

| Promotional and advertising expenses | 151 | 110 | 191 | 37.3 | (20.9) | 368 | 416 | (11.5) |

| Taxes and duties | 307 | 206 | 229 | 49.0 | 34.1 | 673 | 675 | (0.3) |

| Technology services (IT) | 428 | 341 | 360 | 25.5 | 18.9 | 1,169 | 1,015 | 15.2 |

| Depreciation and amortization | 389 | 377 | 376 | 3.2 | 3.5 | 1,147 | 1,076 | 6.6 |

| Contributions to bank savings protection system (IPAB) | 341 | 324 | 325 | 5.2 | 4.9 | 987 | 902 | 9.4 |

| Cash protection | 147 | 172 | 140 | (14.5) | 5.0 | 377 | 370 | 1.9 |

| Other services and expenses | 698 | 396 | 539 | 76.3 | 29.5 | 1,647 | 1,403 | 17.4 |

| | | | | | | | | |

| Total Administrative and Promotional Expenses | 5,179 | 4,559 | 4,630 | 13.6 | 11.9 | 14,214 | 12,890 | 10.3 |

3Q12 administrative and promotional expenses increased 11.9% YoY to Ps.5,179 million, driven by increases in the following areas: Ps.254 million in salaries and employee benefits, Ps.78 million in taxes and duties, Ps.68 million in technology services, Ps.60 million in leaseholds, and Ps.36 million in credit card operations accompanying the growth in the banking business.

On a sequential basis, administrative and promotional expenses rose 13.6%, principally due to the following variances: Ps.18 million in salaries and employee benefits, Ps.88 million in credit card operation, Ps.13 million in leaseholds, and Ps.87 million in technology services.

In 9M12, administrative and promotional expenses increased 10.3% to Ps.14,214 million compared with 9M11.

The efficiency ratio under CNBV standards for 3Q12 was 36.9%, this compares to the corresponding figures of 42.4% and 35% reported in 3Q11 and 2Q12, respectively. For 9M12 the efficiency ratio was 36.9%.

The recurrence ratio in 3Q12 was 67.8%, improving from 65.5% in 3Q11 and slightly decreasing versus 70.1% in 2Q12.

Current and Deferred Taxes

Current and deferred income taxes in 3Q12 amounted to Ps.746 million, 7.7% YoY and 50.9% higher QoQ. During 9M12, current and differed income taxes amounted to Ps.3,319 million, representing a 26.9% increase against 9M12.

3Q. 12 | EARNINGS REPORT | 15

Capitalization and ROAE

| Grupo Financiero Santander México | | | | | |

Capitalization Millions of Mexican Pesos | | | | | |

| | 3Q12 | | 2Q12 | | 3Q11 |

| Tier 1 | 73,570 | | 73,579 | | 68,417 |

| Tier 2 | 1,538 | | 1,529 | | 1,466 |

| Total Capital | 75,108 | | 75,108 | | 69,884 |

| | | | | | |

| Risk-Weighted Assets | | | | | |

| Credit Risk | 313,707 | | 307,413 | | 275,589 |

| Credit, Market, and Operational Risk | 519,647 | | 513,305 | | 490,840 |

| | | | | | |

| Credit Risk Ratios: | | | | | |

| Tier 1 (%) | 23.4 | | 23.9 | | 24.8 |

| Tier 2(%) | 0.5 | | 0.5 | | 0.5 |

| Capitalization Ratio (%) | 23.9 | | 24.4 | | 25.4 |

| | | | | | |

| Total Capital Ratios: | | | | | |

| Tier 1(%) | 14.2 | | 14.3 | | 13.9 |

| Tier 2 (%) | 0.3 | | 0.3 | | 0.3 |

| Capitalization Ratio (%) | 14.5 | | 14.6 | | 14.2 |

Banco Santander México’s capital ratio was 14.45% in 3Q12, above the corresponding figures of 14.23% and below 14.63%, in 3Q11 and 2Q12, respectively. The capital ratio reflelcts the impact of the Ps.7.3 billion cash dividend paid during the quarter. The core capital ratio amounted to 14.2% in 3Q12, compared with 13.9% in 3Q11 and 14.3% in 2Q12.

As of June 2012, Santander México is classified within Category 1 in accordance with Article 134bis of the Mexican Banking Law, and remains in this category as per the preliminary results dated July 2012, which is the most recently available analysis.

ROAE in 3Q12 was 21.1%, an increase of 421 bps from the 16.9% reported in 3Q11, and 130 bps below the 22.4% in 2Q12. This sequential decrease reflects the extraordinary gain from the sale of 220 branches in 2Q12. Normalized ROAE in 3Q12 was 19.4%, a 353 bps increase from 15.8% in 3Q11.

RELEVANT EVENTS

Santander Concludes Public Offering

In September 2012, Santander México successfully closed the secondary public offering of 24.9% of its capital stock. A total of approximately 1.7 billion Series B shares were sold at Ps.31,25 pesos per share, or 12.18 dollars per ADS, valuing Santander México at 16.5 billion dollars and making it the biggest offer of shares in Mexico to date and the second largest offering in the U.S. thus far this year. Of total shares sold, 81% were placed in the United States and in other countries outside of Mexico, and 19% were placed in Mexico.

Dividend Payment

On September 13, 2012 Santander México paid a cash dividend for the total amount of Ps.7.3 billion, of which the Ps.3.0 billion payment was declared at a General Ordinary Stockholders’ meeting held on May 14th, 2012,

3Q. 12 | EARNINGS REPORT | 16

resulting in a dividend per share of Ps.0.44206092314. Additionally, the payment of Ps.4.3 billion was declared at a General Ordinary Stockholders’ meeting held on August 13th, 2012, resulting in a dividend per share of Ps. 0.6336206565.

Agreements approved at the General Extraordinary Stockholders’ Meeting

At the General Extraordinary Stockholders’ meeting that took place on August 13th 2012, shareholders approved the change in the Company’s legal name to adopt the one currently held (Grupo Financiero Santander México, S.A.B. de C.V.).

Incentive Plan

In July 2012, our Board approved, previous recommendation of the Compensation Committee, a stock compensation plan for certain executives who will have the right to receive stock of Grupo financiero Santander Mexico once certain criteria has been met.

This stock option compensation plan is expected to benefit approximately 300 high-level executives of Banco Santander Mexico, Casa de Bolsa Santander, Gestión Santander and the Sofomes fully-owned by Banco Santander México. The establishment of this plan will have a cost os Ps.418.7 million.

CREDIT RATINGS

| Banco Santander (México) | | | | | |

| Ratings | | | | | |

| | Standard & Poor´s | | Moody´s | | Fitch Ratings |

| Global Scale | | | | | |

| Foreign Currency | | | | | |

| Long Term | BBB | | Baa1 | | BBB+ ** |

| Short Term | A-2 | | P-2 | | F2 |

| | | | | | |

| Local Currency | | | | | |

| Long Term | BBB | | A3 | | BBB+ ** |

| Short Term | A-2 | | P-2 | | F2 |

| | | | | | |

| National Scale | | | | | |

| Long Term | mxAAA | | Aaa.mx | | AAA(mex) |

| Short Term | mxA-1+ | | Mx-1 | | F1+(mex) |

| | | | | | |

| Deposit Certificates | | | | | |

| Long Term | BBB | | | | |

| Short Term | A-3 | | | | |

| | | | | | |

| Autonomous Credit Profile (SACP) | bbb+ | | - | | - |

| Rating viability (VR) | - | | - | | bbb+ |

| Support | - | | - | | 2 |

| Financial Strength | - | | C- | | - |

| Outlook | Stable | | Stable | | Stable |

| | | | | | |

| Last publication: | 11-Jul-12 | | 28-Jun-12 | | 13-Jun-12 |

| | | | | | |

| ** Negative Outlook |

3Q. 12 | EARNINGS REPORT | 17

| Brokerage - Casa de Bolsa Santander |

| Ratings | | | | |

| | | Moody´s | | Fitch Ratings |

| Global Scale | | | | |

| National Scale | | | | |

| Long Term | | A3 | | _ |

| Short Term | | Prime-2 | | _ |

| | | | | |

| National Scale | | | | |

| Long Term | | Aaa.mx | | AAA.mx |

| Short Term | | Mx-1 | | F1+mx |

| | | | | |

| Outlook | | Stable | | Stable |

3Q EARNINGS CALL DIAL-IN INFORMATION

Date – Friday, October 26, 2012

Time – 8:00 AM (MCT); 9:00 AM (US ET)

Dial-in Numbers – 1-480-629-9664 México and International; 1-877-941-1427 US and Canada

Access Code – 4570856

Webcast – https://viavid.webcasts.com/starthere.jsp?ei=1009721

Replay – Starting: Friday, October 26, 2012 at 11:00 AM (MCT); 12:00 PM (US ET). Ending: Friday, November 2, 2012 at 11:00 PM (MCT); 12:00 AM (US ET).

About Grupo Financiero Santander México, S.A.B. de C.V. (NYSE: BSMX BMV: SANMEX)

Grupo Financiero Santander México, S.A.B. de C.V., one of Mexico’s leading financial services holding companies, provides a wide range of financial and related services, including retail and commercial banking, securities brokerage, financial advisory, and other related investment activities. Santander México offers a financial services platform focused on mid- to high-income individuals and small- to medium-sized enterprises, while also providing integrated financial services to larger multinational companies in Mexico. As of September 30, 2012, Santander Mexico had total assets of Ps.771.4 million under Mexican Banking GAAP and more than 9.7 million customers. Headquartered in Mexico City, Santander Mexico operates 1,123 branches located throughout Mexico and has a total of 12,766 employees.

We, the undersigned under oath to tell the truth declare that, in the area of our corresponding functions, we prepared the information on Grupo Financiero Santander contained in this quarterly report, which to the best of our knowledge reasonably reflects its situation.

| MARCOS A. MARTINEZ GAVICA | | PEDRO JOSE MORENO CANTALEJO |

| Executive President and Chief Executive Officer | | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

Deputy General Director of Intervention and Control Management | Executive Director – Controller | Executive Director – Audit |

3Q. 12 | EARNINGS REPORT | 18

| | The financial information presented in this report has been obtained from the non-audited financial statements prepared in accordance with the General Nature Provisions applicable to Holding Corporations of Financial Groups which are subject to the supervision of the National Banking and Securities Commission on accounting procedures, published in the Federal Official Gazette on January 31, 2011. The exchange rate used to convert foreign currency transactions to pesos is PPs.13.40840. |

INVESTOR RELATIONS CONTACT

Ana Luisa González

+ 52 (55) 5269 2845

investor@santander.com.mx

LEGAL DISCLAIMER

Grupo Financiero Santander México cautions that this report may contain forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements could be found in various places throughout this reports and include, without limitation, statements regarding our intent, belief, targets or current expectations in connection with: asset growth and sources of funding; growth of our fee-based business; expansion of our distribution network; our focus on strategic businesses; our compound annual growth rate; our risk, efficiency and profitability targets; financing plans; competition; impact of regulation; exposure to market risks including interest rate risk, foreign exchange risk and equity price risk; exposure to credit risks including credit default risk and settlement risk; projected capital expenditures; capitalization requirements and level of reserves; liquidity; trends affecting the economy generally; and trends affecting our financial condition and our results of operations. While these forward-looking statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to: changes in capital markets in general that may affect policies or attitudes towards lending to Mexico or Mexican companies; changes in economic conditions, in Mexico in particular, in the United States or globally; the monetary, foreign exchange and interest rate policies of the Mexican Central Bank (Banco de México); inflation; deflation; unemployment; unanticipated turbulence in interest rates; movements in foreign exchange rates; movements in equity prices or other rates or prices; changes in Mexican and foreign policies, legislation and regulations; changes in requirements to make contributions to, for the receipt of support from programs organized by or requiring deposits to be made or assessments observed or imposed by, the Mexican government; changes in taxes; competition, changes in competition and pricing environments; our inability to hedge certain risks economically; economic conditions that affect consumer spending and the ability of customers to comply with obligations; the adequacy of allowances for loans and other losses; increased default by borrowers; technological changes; changes in consumer spending and saving habits; increased costs; unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms; changes in, or failure to comply with, banking regulations; and certain other factors indicated in the “Risk Factors” section of our Registration Statement on Form F-1 (File No. 333-183409). The risk factors and other key factors that we have indicated in our past and future filings and reports, including those with the U.S. Securities and Exchange Commission, could adversely affect our business and financial performance.

Note: The information contained in this reports is not audited. Nevertheless, the consolidated accounts are prepared on the basis of the accounting principles and regulations prescribed by the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) for credit institutions, as amended (Mexican Banking GAAP). All figures presented are in nominal terms. Historical figures are not adjusted by inflation.

3Q. 12 | EARNINGS REPORT | 19

Grupo Financiero Santander México

| § | Consolidated Balance Sheet |

| § | Consolidated Statement of Income |

| § | Consolidated Statement of Changes in Stockholders’ Equity |

| § | Consolidated Statement of Cash Flows |

The information contained in this report and the financial statements of the Group’s subsidiaries may be consulted on the Internet website: www.santander.com.mx or through the following direct access:

http://www.santander.com.mx/ir/inf_financiera/inf_trimestral.html

There is also information on Santander on the CNBV Website: www.cnbv.gob.mx

3Q. 12 | EARNINGS REPORT | 20

| Grupo Financiero Santander México | | | | | | |

| Consolidated Balance Sheet | | | | | | | |

| Millions of pesos | | | | | | | |

| | | | 2012 | | | | 2011 |

| | Sep | Jun | Mar | Dec | Sep | Jun | Mar |

| Assets | | | | | | | |

| | | | | | | | |

| Cash and due from banks | 91,763 | 96,468 | 75,446 | 84,862 | 90,504 | 104,679 | 93,450 |

| | | | | | | | |

| Margin accounts | 3,053 | 3,825 | 3,604 | 7,910 | 8,544 | 8,261 | 7,719 |

| | | | | | | | |

| Investment in securities | 202,967 | 263,697 | 270,275 | 222,641 | 231,358 | 237,578 | 207,456 |

| Trading securities | 142,939 | 203,958 | 203,413 | 156,319 | 180,087 | 185,997 | 147,642 |

| Securities available for sale | 54,996 | 54,764 | 61,944 | 61,461 | 46,467 | 46,831 | 55,119 |

| Securities held to maturity | 5,032 | 4,975 | 4,918 | 4,861 | 4,804 | 4,750 | 4,695 |

| | | | | | | | |

| Debtors under sale and repurchase agreements | 4,458 | 4,827 | 4,484 | 3,478 | 25,515 | 7,262 | 6,655 |

| | | | | | | | |

| Derivatives | 89,389 | 87,857 | 71,991 | 85,978 | 110,516 | 79,999 | 70,483 |

| Trading purposes | 88,945 | 87,286 | 71,276 | 85,081 | 109,441 | 78,500 | 69,329 |

| Hedging purposes | 444 | 571 | 715 | 897 | 1,075 | 1,499 | 1,154 |

| | | | | | | | |

| Valuation adjustment for hedged financial assets | 240 | 220 | 139 | 122 | 141 | 86 | (12) |

| | | | | | | | |

| Performing loan portfolio | | | | | | | |

| Commercial loans | 211,685 | 212,492 | 198,276 | 197,772 | 197,465 | 183,059 | 175,304 |

| Commercial or business activity | 175,945 | 176,332 | 163,630 | 162,419 | 162,162 | 148,546 | 152,482 |

| Financial entities loans | 619 | 606 | 1,934 | 1,975 | 3,306 | 4,542 | 4,043 |

| Government entities loans | 35,121 | 35,554 | 32,712 | 33,378 | 31,997 | 29,971 | 18,779 |

| Consumer loans | 59,996 | 57,043 | 52,857 | 49,342 | 47,101 | 43,683 | 40,242 |

| Mortage loans | 66,172 | 64,417 | 62,559 | 61,243 | 58,853 | 56,954 | 36,124 |

| Total performing loan portafolio | 337,853 | 333,952 | 313,692 | 308,357 | 303,419 | 283,696 | 251,670 |

| | | | | | | | |

| Nonperforming loan portafolio | | | | | | | |

| Commercial loans | 1,402 | 1,313 | 1,135 | 1,928 | 3,233 | 1,758 | 1,752 |

| Commercial or business activity | 1,402 | 1,313 | 1,135 | 1,926 | 1,840 | 1,758 | 1,752 |

| Government entities loans | 0 | 0 | 0 | 2 | 1,393 | 0 | 0 |

| Consumer loans | 2,053 | 1,709 | 1,255 | 1,270 | 1,232 | 1,321 | 1,131 |

| Mortage loans | 2,075 | 1,931 | 1,982 | 2,118 | 2,245 | 3,690 | 569 |

| Total nonperforming portafolio | 5,530 | 4,953 | 4,372 | 5,316 | 6,710 | 6,769 | 3,452 |

| Total loan portafolio | 343,383 | 338,905 | 318,064 | 313,673 | 310,129 | 290,465 | 255,122 |

| | | | | | | | |

| Allowance for loan losses | (11,360) | (11,101) | (10,875) | (11,191) | (10,906) | (12,892) | (10,449) |

| Loan portafolio (net) | 332,023 | 327,804 | 307,189 | 302,482 | 299,223 | 277,573 | 244,673 |

| Other receivables (net) | 30,231 | 36,483 | 32,310 | 13,649 | 21,958 | 20,771 | 31,710 |

| Foreclosed assets (net) | 172 | 196 | 220 | 253 | 290 | 305 | 155 |

| Property, furniture and fixtures (net) | 3,770 | 3,780 | 5,439 | 5,592 | 5,166 | 5,238 | 5,340 |

| Long-term investment in shares | 218 | 203 | 251 | 234 | 218 | 206 | 226 |

| Deferred taxes (net) | 9,155 | 8,425 | 8,255 | 8,063 | 8,735 | 8,722 | 7,687 |

| Deferred charges, advance payments and intangibles | 3,693 | 3,793 | 4,148 | 3,722 | 3,893 | 3,944 | 2,278 |

| Other assets | 290 | 221 | 197 | 190 | 320 | 305 | 299 |

| Discontinued operations | 0 | 0 | 0 | 0 | 10,511 | 10,702 | 9,817 |

| | | | | | | | |

| Total assets | 771,422 | 837,799 | 783,948 | 739,176 | 816,892 | 765,631 | 687,936 |

3Q. 12 | EARNINGS REPORT | 21

| Grupo Financiero Santander México | | | | | | | | |

| Consolidated Balance Sheet | | | | | | | | |

| Millions of pesos | | | | | | | | |

| | | | 2012 | | | | 2011 | |

| | Sep | Jun | Mar | Dec | Sep | Jun | Mar | |

| Liabilities | | | | | | | | |

| | | | | | | | | |

| Deposits | 358,606 | 352,753 | 346,605 | 330,870 | 328,327 | 316,729 | 286,455 | |

| Demand deposits | 194,351 | 204,606 | 187,787 | 178,065 | 166,923 | 155,932 | 151,450 | |

| Time deposits – General Public | 120,034 | 117,184 | 122,816 | 114,720 | 122,130 | 110,968 | 106,774 | |

| Time deposits – Money market | 21,904 | 9,085 | 14,507 | 16,409 | 18,823 | 32,745 | 11,405 | |

| | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Credit instruments issued | 22,317 | 21,878 | 21,495 | 21,676 | 20,451 | 17,084 | 16,826 | |

| | | | | | | | | |

| Bank and other loans | 34,338 | 24,804 | 21,372 | 19,554 | 36,158 | 23,627 | 17,726 | |

| Demand loans | 5,916 | 6,851 | 5,949 | 2,371 | 20,326 | 10,293 | 7,308 | |

| Short-term loans | 26,092 | 15,704 | 13,278 | 15,156 | 13,772 | 11,187 | 8,310 | |

| Long-term loans | 2,330 | 2,249 | 2,145 | 2,027 | 2,060 | 2,147 | 2,108 | |

| | | | | | | | | |

| Creditors under sale and repurchase agreements | 106,306 | 168,227 | 189,299 | 120,590 | 157,221 | 162,609 | 129,442 | |

| | | | | | | | | |

| Collateral sold or pledged as guarantee | 17,972 | 18,766 | 14,104 | 15,478 | 17,896 | 15,820 | 24,246 | |

| Securities loans | 17,972 | 18,766 | 14,104 | 15,478 | 17,896 | 15,820 | 24,246 | |

| | | | | | | | | |

| Derivatives | 86,613 | 87,960 | 70,292 | 90,649 | 114,399 | 78,362 | 65,948 | |

| Trading purposes | 85,209 | 86,233 | 69,266 | 88,148 | 111,929 | 78,198 | 65,861 | |

| Hedging purposes | 1,404 | 1,727 | 1,026 | 2,501 | 2,470 | 164 | 87 | |

| | | | | | | | | |

| Other payables | 71,702 | 88,648 | 47,647 | 72,493 | 63,114 | 72,706 | 69,844 | |

| Income taxes payable | 767 | 335 | 910 | 507 | 779 | 928 | 7 | |

| Employee profit sharing payable | 117 | 83 | 62 | 153 | 6 | 5 | 40 | |

| Creditors from settlement of transactions | 47,308 | 52,492 | 24,013 | 28,579 | 28,744 | 47,883 | 50,194 | |

| Sundry creditors and other payables | 23,510 | 35,738 | 22,662 | 43,254 | 33,585 | 23,890 | 19,603 | |

| | | | | | | | | |

| Deferred revenues | 1,091 | 1,096 | 1,385 | 1,062 | 1,135 | 1,160 | 1,534 | |

| | | | | | | | | |

| Discontinued operations | 0 | 0 | 0 | 0 | 8,496 | 8,872 | 8,142 | |

| | | | | | | | | |

| Total liabilities | 676,628 | 742,254 | 690,704 | 650,696 | 726,746 | 679,885 | 603,337 | |

| | | | | | | | |

| Paid in capital | 48,195 | 48,195 | 48,195 | 48,195 | 48,195 | 48,195 | 48,195 | |

| Capital stock | 36,357 | 36,357 | 36,357 | 36,357 | 36,357 | 36,357 | 36,357 | |

| Share premium | 11,838 | 11,838 | 11,838 | 11,838 | 11,838 | 11,838 | 11,838 | |

| Other capital | 46,599 | 47,350 | 45,049 | 40,285 | 41,951 | 37,551 | 36,404 | |

| Capital reserves | 349 | 349 | 108 | 108 | 108 | 108 | 108 | |

| Retained earnings | 30,619 | 35,311 | 38,541 | 19,828 | 28,633 | 28,781 | 31,276 | |

| Result from valuation of securities available for sale, net | 727 | 688 | 442 | 465 | 917 | 515 | 314 | |

| Result from valuation of cash flow hedge instruments, net | 382 | 690 | 932 | 1,188 | 1,340 | 1,317 | 1,242 | |

| Net income | 14,513 | 10,298 | 5,013 | 18,683 | 10,941 | 6,818 | 3,452 | |

| Non-controlling interest | 9 | 14 | 13 | 13 | 12 | 12 | 12 | |

| Total stockholders´equity | 94,794 | 95,545 | 93,244 | 88,480 | 90,146 | 85,746 | 84,599 | |

| | | | | | | | | |

| Total liabilities and stockholders´ equity | 771,422 | 837,799 | 783,948 | 739,176 | 816,892 | 765,631 | 687,936 | |

3Q. 12 | EARNINGS REPORT | 22

| Grupo Financiero Santander México | | | | | | | |

| Consolidated Balance Sheet | | | | | | | |

| Millions of pesos | | | | | | | |

| | | | 2012 | | | | 2011 |

| | Sep | Jun | Mar | Dec | Sep | Jun | Mar |

| Memorandum accounts | | | | | | | |

| | | | | | | | |

| FOR THIRD PARTIES | | | | | | | |

| | | | | | | | |

| Current client account | | | | | | | |

| Client Banks | 74 | 261 | 147 | 87 | 107 | 78 | 39 |

| Liquidation of client transactions | 350 | (2,030) | 35 | 20 | (265) | (728) | (798) |

| Dividends on behalf of clients | 0 | 1 | 1 | 0 | 0 | 0 | 1 |

| | | | | | | | |

| Custody services | | | | | | | |

| Assets under custody | 261,131 | 198,793 | 210,076 | 181,374 | 190,125 | 188,854 | 180,571 |

| Client securities abroad | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| | | | | | | | |

| Transactions on behalf of third parties | | | | | | | |

| Sale and repurchase agreements | 44,469 | 55,334 | 65,577 | 51,219 | 53,598 | 47,040 | 36,213 |

| Security loans on behalf of clients | 1,457 | 1,826 | 2,182 | 602 | 495 | 473 | 398 |

| Collaterals received as guarantee on behalf of clients | 19,013 | 15,690 | 19,542 | 21,191 | 21,686 | 4,848 | 5,048 |

| Acquisition of derivatives | 294,269 | 308,411 | 308,379 | 1,751,863 | 1,965,352 | 1,997,790 | 2,027,256 |

| Sale of derivatives | 579,263 | 603,162 | 656,451 | 2,028,099 | 2,222,326 | 2,357,339 | 2,321,732 |

| | | | | | | | |

| Total on behalf of third parties | 1,200,026 | 1,181,447 | 1,262,390 | 4,034,455 | 4,453,424 | 4,595,694 | 4,570,459 |

| | | | | | | | |

| Proprietary record accounts: | | | | | | | |

| | | | | | | | |

| Contingent assets and liabilities | 24,053 | 31,852 | 31,904 | 32,133 | 30,680 | 41,446 | 32,532 |

| | | | | | | | |

| Credit commitments | | | | | | | |

| Trusts | 106,006 | 106,747 | 155,407 | 145,755 | 142,515 | 136,825 | 129,442 |

| Mandates | 2,582 | 1,548 | 1,532 | 1,556 | 1,535 | 1,510 | 1,324 |

| | | | | | | | |

| Assets in custody or under administration | 3,312,634 | 3,062,735 | 3,084,880 | 2,935,454 | 2,908,619 | 2,837,534 | 2,710,653 |

| | | | | | | | |

| Credit Commitments | 160,790 | 203,362 | 157,565 | 162,528 | 273,286 | 256,420 | 234,036 |

| | | | | | | | |

| Collateral received | 90,548 | 52,244 | 49,931 | 39,015 | 63,514 | 53,891 | 35,246 |

| | | | | | | | |

| Collateral received and sold or pledged as guarantee | 66,877 | 26,708 | 29,027 | 18,120 | 20,208 | 30,535 | 3,555 |

| | | | | | | | |

| Uncollected interest earned on past due loan portfolio | 794 | 1,092 | 985 | 701 | 1,553 | 1,441 | 728 |

| | | | | | | | |

| Other accounts | 466,076 | 455,197 | 429,800 | 428,839 | 421,373 | 375,879 | 341,734 |

| | | | | | | | |

| Subtotal | 4,230,360 | 3,941,485 | 3,941,031 | 3,764,101 | 3,863,283 | 3,735,481 | 3,489,250 |

| | | | | | | | |

| Total | 5,430,386 | 5,122,932 | 5,203,421 | 7,798,556 | 8,316,707 | 8,331,175 | 8,059,709 |

3Q. 12 | EARNINGS REPORT | 23

These consolidated financial statements were approved by the Board of directors and signal on its behalf by

| MARCOS A. MARTINEZ GAVICA | | PEDRO JOSE MORENO CANTALEJO |

| | | |

| Executive President and Chief Executive Officer | | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| | | |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

The accompanying notes are part of these consolidated financial statements

www.santander.com.mx

3Q. 12 | EARNINGS REPORT | 24

| Grupo Financiero Santander México | | | | | | | | |

| Consolidated Statement of Income | | | | | | | | |

| Millions of pesos | | | | | | | | |

| | | | | 2012 | | | | 2011 |

| | 9M12 | 3Q | 2Q | 1Q | 9M11 | 3Q | 2Q | 1Q |

| Interest income | 41,129 | 13,873 | 13,830 | 13,426 | 33,772 | 12,221 | 11,389 | 10,162 |

| Interest expense | (16,048) | (5,291) | (5,436) | (5,321) | (12,777) | (4,750) | (4,395) | (3,632) |

| Financial margin | 25,081 | 8,582 | 8,394 | 8,105 | 20,995 | 7,471 | 6,994 | 6,530 |

| | | | | | | | | |

| Allowance for loan losses | (6,496) | (2,534) | (1,994) | (1,968) | (4,515) | (1,080) | (1,963) | (1,472) |

| Financial margin after allowance for loan losses | 18,585 | 6,048 | 6,400 | 6,137 | 16,480 | 6,391 | 5,031 | 5,058 |

| | | | | | | | | |

| Commision and fee income | 10,791 | 3,783 | 3,506 | 3,502 | 9,403 | 3,215 | 3,021 | 3,167 |

| Commision and fee expense | (1,927) | (718) | (670) | (539) | (1,667) | (535) | (531) | (601) |

| Net gain /(loss) on financial assets and liabilities | 1,781 | 921 | 106 | 754 | 939 | 29 | 546 | 364 |

| Othe operating income / (loss) | 2,763 | 88 | 2,005 | 670 | 768 | 266 | 281 | 221 |

| Administrative and promotional expenses | (14,214) | (5,179) | (4,559) | (4,476) | (12,890) | (4,630) | (4,312) | (3,948) |

| Total operating income | 17,779 | 4,943 | 6,788 | 6,048 | 13,033 | 4,736 | 4,036 | 4,261 |

| | | | | | | | | |

| Equity in results of subsidiaries and associated companies | 54 | 18 | 17 | 19 | 53 | 13 | 18 | 22 |

| | | | | | | | | |

| Income from continuing operations before income taxes | 17,833 | 4,961 | 6,805 | 6,067 | 13,086 | 4,749 | 4,054 | 4,283 |

| | | | | | | | | |

| Current income taxes | (4,179) | (1,360) | (1,695) | (1,124) | (5,665) | (603) | (2,004) | (3,058) |

| Deferred income taxes | 860 | 614 | 176 | 70 | 3,049 | (205) | 1,156 | 2,098 |

| | | | | | | | | |

| Income from continuing operations | 14,514 | 4,215 | 5,286 | 5,013 | 10,470 | 3,941 | 3,206 | 3,323 |

| | | | | | | | | |

| Discontinued operations | 0 | 0 | 0 | 0 | 474 | 184 | 161 | 129 |

| | | | | | | | | |

| Consolidated net income | 14,514 | 4,215 | 5,286 | 5,013 | 10,944 | 4,125 | 3,367 | 3,452 |

| | | | | | | | | |

| Non-controlling interest | (1) | 0 | (1) | 0 | (3) | (2) | (1) | 0 |

| | | | | | | | | |

| Net income | 14,513 | 4,215 | 5,285 | 5,013 | 10,941 | 4,123 | 3,366 | 3,452 |

These consolidated financial statements were approved by the Board of directors and signal on its behalf by

| MARCOS A. MARTINEZ GAVICA | | PEDRO JOSE MORENO CANTALEJO |

| | | |

| Executive President and Chief Executive Officer | | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| | | |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

The accompanying notes are part of these consolidated financial statements

www.santander.com.mx

3Q. 12 | EARNINGS REPORT | 25

Grupo Financiero Santander México

Consolidated Statements of Changes in Stockholders’ Equity

From January 1st to September 30, 2012

Millions of pesos

| | | Paid-in Capital | | | Other Capital | |

| CONCEPT | | Capital Stock | | | Additional Paid-In Capital | | | Capital Reserves | | | Retained Earnings | | | Surplus (deficit) from valuation of securities available for sale | | | Surplus (Deficit) from the valuation of cash flow hedge securities | | | Net income (loss) | | | Minority Interest | | | Total stockholders' equity | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| BALANCE AS OF DECEMBER 31, 2011 | | | 36,357 | | | | 11,838 | | | | 108 | | | | 19,828 | | | | 465 | | | | 1,188 | | | | 18,682 | | | | 13 | | | | 88,479 | |

MOVEMENTS INHERENT TO THE SHAREHOLDERS' DECISIONS | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Transfer of Net income (loss) to Retained Earnings | | | | | | | | | | | 241 | | | | 18,441 | | | | | | | | | | | | (18,682 | ) | | | | | | | 0 | |

| Payment of Dividends | | | | | | | | | | | | | | | (7,300 | ) | | | | | | | | | | | | | | | | | | | (7,300 | ) |

| TOTAL | | | 0 | | | | 0 | | | | 241 | | | | 11,141 | | | | 0 | | | | 0 | | | | (18,682 | ) | | | 0 | | | | (7,300 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| MOVEMENTS INHERENT TO THE RECOGNITION OF THE COMPREHENSIVE INCOME | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Surplus (deficit) from valuation of securities available for sale | | | | | | | | | | | | | | | | | | | 262 | | | | | | | | | | | | | | | | 262 | |

| Surplus (deficit) from valuation ofcash flow hedge securities | | | | | | | | | | | | | | | | | | | | | | | (806 | ) | | | | | | | | | | | (806 | ) |

| Repurchase of own shares | | | | | | | (419 | ) | | | | | | | | | | | | | | | | | | | | | | | | | | | (419 | ) |

| Recoveries on loan reserves previously applied to prior year results | | | | | | | | | | | | | | | 45 | | | | | | | | | | | | | | | | | | | | 45 | |

| Equity effect of investment in subsidiaries and associated companies | | | | | | | | | | | | | | | 24 | | | | | | | | | | | | | | | | | | | | 24 | |

| Net Income (Loss) | | | | | | | | | | | | | | | | | | | | | | | | | | | 14,513 | | | | | | | | 14,513 | |

| Minority Interest | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | (4 | ) | | | (4 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| TOTAL | | | 0 | | | | (419 | ) | | | 0 | | | | 69 | | | | 262 | | | | (806 | ) | | | 14,513 | | | | (4 | ) | | | 13,615 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| BALANCE AS OF SEPTEMBER 30, 2012 | | | 36,357 | | | | 11,419 | | | | 349 | | | | 31,038 | | | | 727 | | | | 382 | | | | 14,513 | | | | 9 | | | | 94,794 | |

3Q. 12 | EARNINGS REPORT | 26

These consolidated financial statements were approved by the Board of directors and signal on its behalf by

| MARCOS A. MARTINEZ GAVICA | | PEDRO JOSE MORENO CANTALEJO |

| | | |

| Executive President and Chief Executive Officer | | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| | | |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

The accompanying notes are part of these consolidated financial statements

www.santander.com.mx

3Q. 12 | EARNINGS REPORT | 27

| Grupo Financiero Santander | | | |

| Consolidated Statement of Cash Flows | | | |

| From January 1st to September 30, 2012 | | | |

| Millions of pesos | | | |

| | | | |

| OPERATING ACTIVITIES | | | |

| Net Result | | | 14,513 |

| Adjustments due to items not requiring resources | | | |

| Result from valuation related to investment or financing activities | 679 | | |

| Equity in results of subsidiaries and associated companies | (54) | | |

| Depreciation of properties, furniture and equipment | 473 | | |

| Amortization of intangible assets | 674 | | |

| Provision for impairment in foreclosed assets | 30 | | |

| Income tax, current and deferred | 3,319 | | 5,121 |

| | | | 19,634 |

| | | | |

| CHANGES IN OPERATING ACCOUNTS | | | |

| Change in margin accounts | | | 4,856 |

| Change in Securities | | | 20,047 |

| Changes in Debit balances under repurchase and resale agreements (Reporto) | | (980) |

| Changes in Derivatives (Asset) | | | (4,679) |

| Changes in Loans portfolio | | | (29,541) |

| Changes in Foreclosed assets | | | 51 |

| Changes in Other operating assets | | | (18,038) |

| Changes in Savings | | | 27,737 |

| Changes in Interbank loans and from other entities | | | 14,786 |

| Changes in Credit balances under repurchase and sale agreements (Reporto) | | (14,284) |

| Changes in sold or pledged guarantees | | | 2,494 |

| Changes in Derivatives (Liabilities)) | | | (4,036) |

| Changes in other operating liabilities | | | 11,979 |

| Income tax payments | | | (3,918) |

| Net resources generated by operating activities | | | 26,108 |

| | | | |

| INVESTING ACTIVITIES | | | |

| Sale of Properties, furniture and equipment | | | 2,936 |

| Purchases of properties, furniture and equipment | | | (187) |

| Investments in subsidiaries and associated companies | | | (8) |

| Collection of cash dividends | | | 77 |

| Purchases of intangible assets | | | (612) |

| Net resources generated by investing activities | | | 2,206 |

| | | | |

| FINANCING ACTIVITIES | | | |

| Payments derived from repurchase of own shares | | | (419) |

| Payment of dividends | | | (18,650) |

| Recoveries of reserves applied to results from previous years | | | 45 |

| | | | |

| Net resources generated by financing activities | | | (19,024) |

| | | | |

| Net decrease in funds available | | | 9,290 |

| | | | |

| Adjustments to cash flow due to exchange variations | | | (2,389) |

| | | | |

| Funds available at beginning of year | | | 84,862 |

Funds available at the end of the year | | | 91,763 |

3Q. 12 | EARNINGS REPORT | 1

These consolidated financial statements were approved by the Board of directors and signal on its behalf by

| MARCOS A. MARTINEZ GAVICA | | PEDRO JOSE MORENO CANTALEJO |

| | | |

| Executive President and Chief Executive Officer | | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| | | |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

The accompanying notes are part of these consolidated financial statements

www.santander.com.mx

3Q. 12 | EARNINGS REPORT | 2

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS OF GRUPO FINANCIERO SANTANDER MÉXICO

| § | Significant accounting policies |

| § | Balance Sheet and Income Statement by segment |

| § | Annex 1. Loan portafolio rating |

| § | Annex 2. Financial Ratios |

| § | Notes to Consolidated Financial Statements |

The information contained in this report and the financial statements of the Group’s subsidiaries may be consulted on the Internet website: www.santander.com.mx or through the following direct access:

http://www.santander.com.mx/ir/inf_financiera/inf_trimestral.html

There is also information on Santander on the CNBV Website: www.cnbv.gob.mx

3Q. 12 | EARNINGS REPORT | 3

Significant accounting policies

The significant accounting policies applied by the Financial Group are in conformity with the accounting criteria established by the Commission in the General Provisions Applicable to Financial Groups, Credit Institutions, Brokerage Houses and Regulated Multiple Purpose Financing Entities (the “Provisions”), in its circulars and in general and specific official mandates, which require that management make certain estimates and utilize certain assumptions to determine the valuation of items included in the consolidated financial statements and to make required disclosures. Although the actual results may differ, management believes that the estimates and assumptions utilized were appropriate under the circumstances.

Based on accounting criterion A-1 of the Commission, the accounting of the Financial Group/Bank shall be in conformity with Mexican Financial Reporting Standards (MFRS or NIF) as promulgated by the Mexican Board of Financial Reporting Standards (CINIF), except when the Commission believes that a specific regulation or accounting treatment should be applied on the basis that the institutions subject to its rules carry out specialized transactions.

Changes in the Accounting Criteria of the Commission

Changes that occurred during 2012

During July 2012, the Federal Official Gazette published certain modifications to the accounting criteria for Credit Institutions modifying the accounting criteria relating to trusts and consolidation of special purpose entities (SPE), which define specific rules regarding the recognition, measurement, presentation and disclosure in the financial statements of trusts and special purpose entities of these institutions, thereby allowing to have transparent and comparable financial information with other countries.

The changes are as follows:

| | Ø | The valuation of the trust patrimony recognized in memorandum accounts shall be effected in accordance with the accounting criteria for credit institutions, except in the case of patrimony of trusts who apply and, where appropriate, obtain and retain registration their securities in the National Securities Registry, in which case, such patrimony shall be valued based on the accounting standards established for such purposes by the Commission applicable to securities issuers and other market participants (International Financial Reporting Standards). |

| | Ø | Elimination of accounting treatment of an unconsolidated SPE. |

| | Ø | Clarification that the financial statements of the consolidated SPE should be prepared based on the same accounting criteria and, for transactions of the same nature, the same accounting policies of the consolidated entity should be used. |

| | Ø | When the SPE use criteria or policies other than those applicable to the consolidated entity, the financial statements of the SPE that are used to carry out the consolidation should be modified to be consistent with those of the entity that consolidates the SPE. |

Changes that occurred during 2011

During 2011, the Federal Official Gazette published certain modifications to the accounting criteria for Financial Groups, Credit Institutions, Brokerage Houses and Regulated Multiple Purpose Financing Entities.

The purpose of these changes is to achieve consistency with International Financial Reporting Standards (IFRS), and to provide more complete financial information with improved disclosures. Such changes principally affected investments in securities, derivatives and hedging operations, the credit portfolio, and the presentation of the basic financial statements.

3Q. 12 | EARNINGS REPORT | 4