UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

| REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934 |

For the month of February, 2013

Commission File Number: 001-35658

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V.

(Exact Name of Registrant as Specified in Its Charter)

SANTANDER MEXICO FINANCIAL GROUP, S.A.B. de C.V.

(Translation of Registrant’s Name into English)

Avenida Prolongación Paseo de la Reforma 500

Colonia Lomas de Santa Fe

Delegación Álvaro Obregón

01219 México, D.F.

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V.

TABLE OF CONTENTS

| ITEM | |

| 1. | Fourth quarter 2012 earnings report of Grupo Financiero Santander México, S.A.B. de C.V. |

| 2. | Fourth quarter and full-year 2012 earnings presentation of Grupo Financiero Santander México, S.A.B. de C.V. |

| 3. | Complementary information of Grupo Financiero Santander México, S.A.B. de C.V. for the fourth quarter of 2012, in compliance with the obligation to report transactions with derivative financial instruments |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| | GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V. | |

| | | By: | /s/ Eduardo Fernández García-Travesí | |

| | | | Name: | Eduardo Fernández García-Travesí | |

| | | | Title: | General Counsel | |

Date: February 19, 2013

Item 1

| | 4Q.12 | Earnings Report | 0 |

| |

|

| | |  |

TABLE OF CONTENTS

| I. | CEO Message / Key Highlights for the Quarter |

| II. | Summary of 4Q12 Consolidated Results |

| III. | Analysis of 4Q12 Consolidated Results |

| VI. | 4Q Earnings Call Dial-In Information |

| VIII. | Notes to the Financial Statements |

| | 4Q.12 | Earnings Report | 1 |

| |

|

| | | |

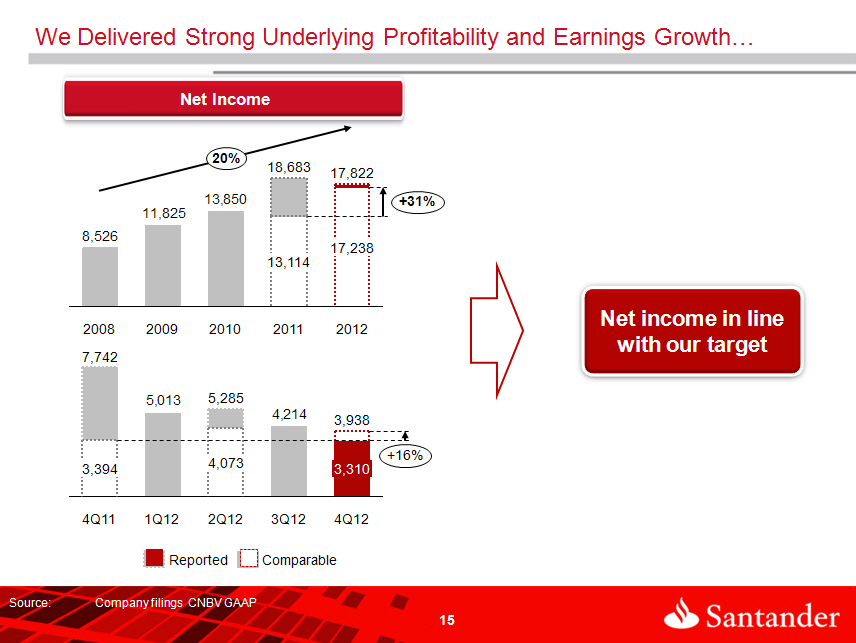

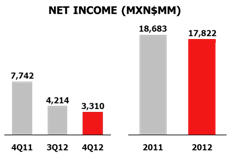

Grupo Financiero Santander México Reports Fourth Quarter 2012 Net Income of Ps.3,310 Million

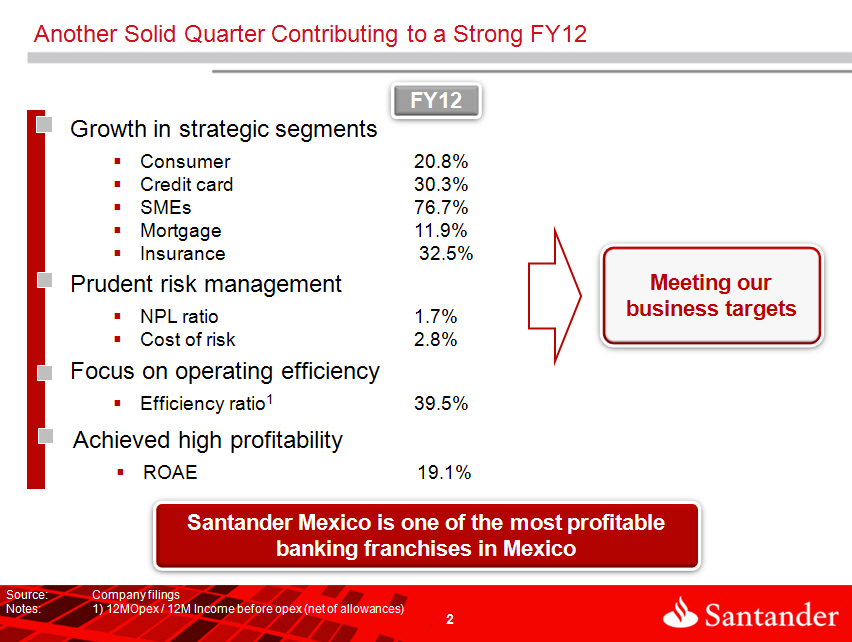

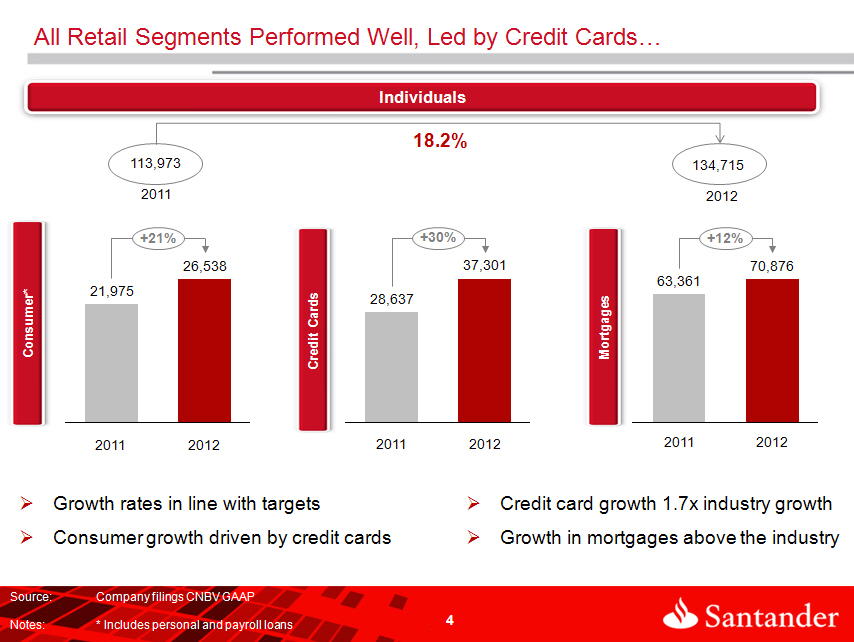

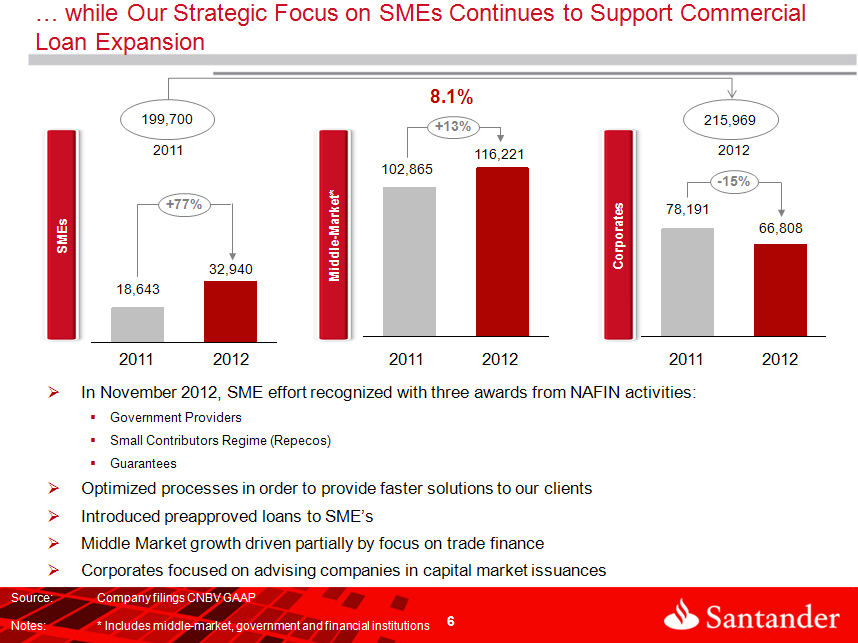

| · | Strong loan growth in commercial banking with YoY increases of 20.8% in consumer loans, 30.3% in credit cards, 76.7% in SMEs and 11.9% in mortgages |

| · | Prudent risk management demonstrated by an NPL ratio of 1.7% and cost of risk of 2.8% |

| · | Continued focus on operating efficiency, achieving a 39.5% ratio |

México City – February 18, 2013, Grupo Financiero Santander México, S.A.B. de C.V., (NYSE: BSMX; BMV: SANMEX), (“Santander México”), one of the leading financial groups in the Mexican financial system, today announced financial results for the three- and twelve-month periods ending December 31, 2012.

Comparable net income for 4Q12 was Ps.3,938 million, representing a 16.0% YoY increase. Including a non-recurring gain of Ps.4,348 million in 4Q11 from the sale of the insurance business to Zurich Financial Services Group (“Zurich”), as well as, incremental administrative and promotional expenses, an accounts receivable write-off and higher provisions in 4Q12, reported net income for the quarter was Ps.3,310 million, representing a decrease of 57.2% YoY and 21.5% on a sequential basis.

Comparable net income for FY12 increased by 31.4%, or Ps.4,124 million, to Ps.17,238 million. Including an extraordinary gain of Ps.4,822 million from the sale of the insurance business and income from this business in FY11, a Ps.1,067 million extraordinary gain in 3Q11 from the reversal of provisions to comply with CNBV (Comisión Nacional Bancaria y de Valores) regulations, and a Ps.1,731 million gain from the sale and leaseback of 220 branches in 2Q12, as well as, higher costs and provisions in 4Q12 as discussed above, reported net income for FY12 was Ps.17,822 million, a 4.6% decrease, from FY11.

Marcos Martínez, Executive Chairman and CEO, commented, "We reported a solid operating performance this quarter, balancing robust growth with strong asset quality and operational efficiency. Net interest income expanded 13% year-on year and net commissions and fees grew 34%. Continued growth in retail loans underscores the merits of our strategic focus. Performance in key business segments was strong in 2012, with year-on-year increases of 21% in consumer loans, 30% in credit cards, and 77% in loans to small and medium enterprises (“SMEs”). We achieved growth while maintaining a strong focus on prudent risk management - reflected in controlled NPL ratios and a stable cost of risk. This, together with our efficiency-oriented culture, positions Santander México as one of the most profitable franchises in the country.”

Mr. Martínez continued, “We expect Santander México’s momentum to continue in 2013 and beyond, supported by our sharp strategic focus, our favorable view of Mexico’s political and economic landscape, and our expectations for attractive yet sensible Mexican financial system growth.”

| Grupo Financiero Santander México | | | | |

| Highlights | | | | |

| | 4Q12 | 3Q12 | 4Q11 | YoY |

| Income Statement Data | | | | |

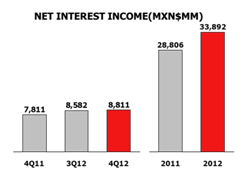

| Net interest income | 8,811 | 8,582 | 7,811 | 12.8% |

| Fee and commission, net | 3,339 | 3,065 | 2,496 | 33.8% |

| Core revenues | 12,150 | 11,647 | 10,307 | 17.9% |

| Provisions for loan losses | 2,948 | 2,535 | 2,041 | 44.4% |

| Administrative and promotional expenses | 6,022 | 5,179 | 5,221 | 15.3% |

| Net income | 3,310 | 4,214 | 7,741 | -57.2% |

| Net income per share * | 2.6 | 2.1 | 2.0 | 28.6% |

| Balance Sheet Data | | | | |

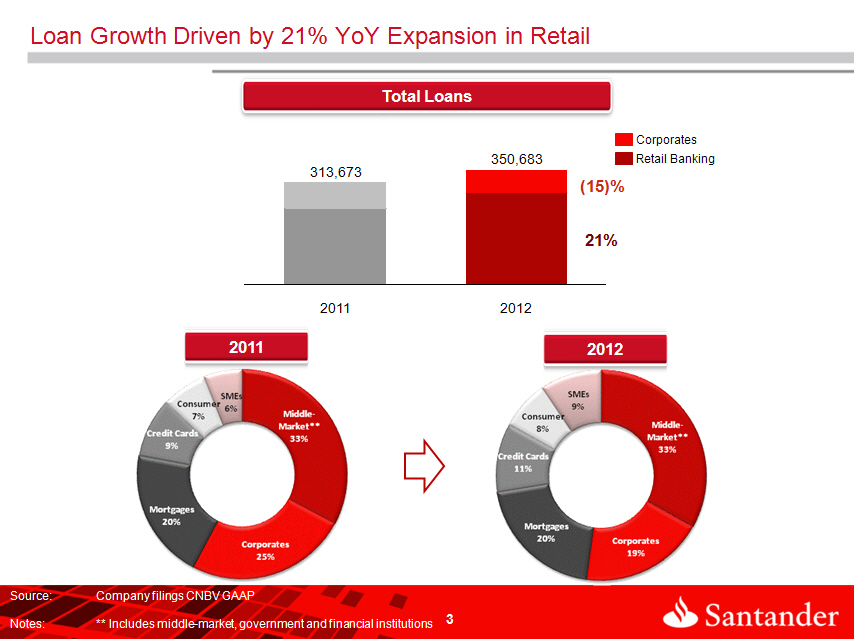

| Total loans | 350,683 | 343,383 | 313,673 | 11.8% |

| Deposits | 362,452 | 336,289 | 309,194 | 17.2% |

| Shareholders´s equity | 97,827 | 94,793 | 88,479 | 10.6% |

| Key Ratios | | | | pbs |

| Net interest margin | 5.0% | 5.0% | 5.1% | (2.6) |

| Net loans to deposits ratio | 93.6% | 98.7% | 97.8% | (427.1) |

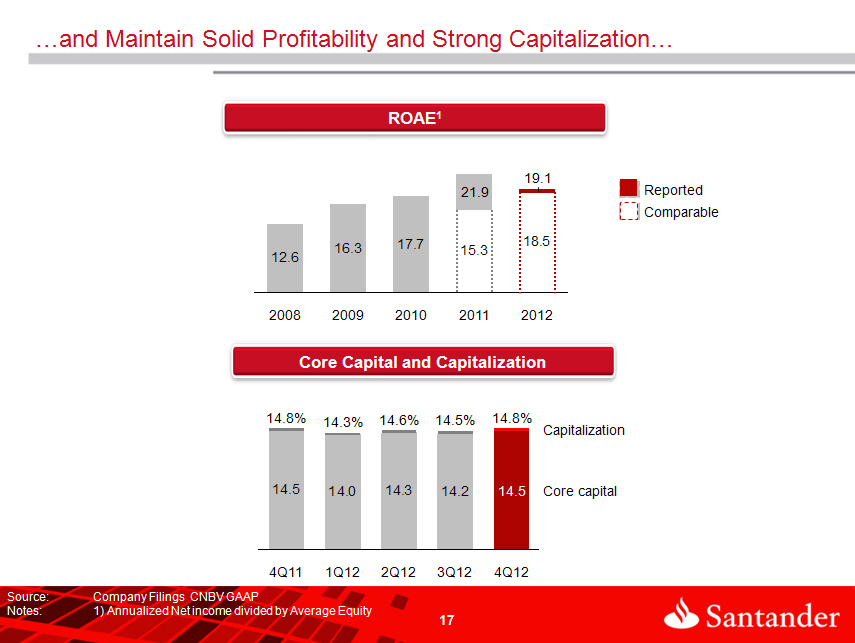

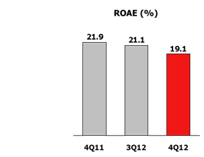

| ROAE | 19.1% | 21.1% | 21.9% | (273.2) |

| ROAA | 2.3% | 2.6% | 2.6% | (31.7) |

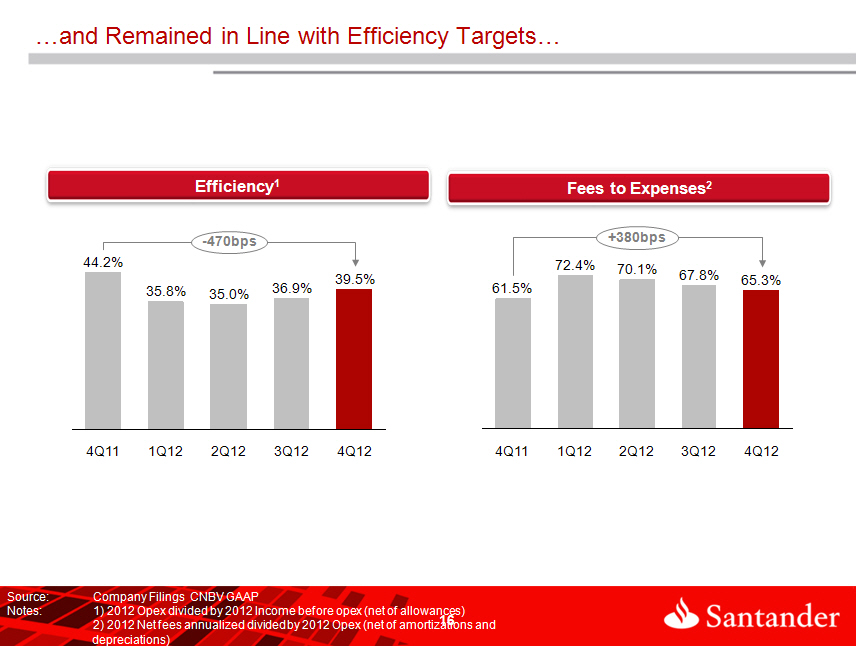

| Efficiency ratio | 39.5% | 36.9% | 44.2% | (469.3) |

| Capital ratio | 14.8% | 14.5% | 14.8% | (5.0) |

| NPLs ratio | 1.74% | 1.61% | 1.69% | 4.3 |

| Coverage ratio | 190.1% | 205.4% | 210.5% | (2,046.1) |

| Operating Data | | | | % |

| Branches** | 1,170 | 1,123 | 1,125 | 4.0% |

| ATMs | 4,946 | 4,840 | 4,689 | 5.5% |

| Customers | 10,013,228 | 9,764,741 | 9,310,681 | 7.5% |

| Employees | 13,385 | 12,766 | 12,395 | 8.0% |

| * | Treasury Shares and discontinued operations are not included |

| ** | Includes Brokerage House Branches |

| | 4Q.12 | Earnings Report | 2 |

| |

|

| | | |

SUMMARY OF FOURTH QUARTER 2012 CONSOLIDATED RESULTS

Net Income Santander México reported net income of Ps.3,310 million in 4Q12, a 57.2% YoY decrease, and 21.5% below 3Q12. Excluding the extraordinary gain in 4Q11 from the sale of the insurance business to Zurich and the aforementioned items in 4Q12, net income would have increased 16.0% YoY. Recurring income resulting from higher business volume is reflected in the net interest margin and net commission and fee income, which increased QoQ by 2.7% and 8.9%, respectively. | |  |

Capitalization and ROAE Santander México’s capital ratio was 14.8% in 4Q12, in line with the figure reported in 4Q11, and higher than the 14.5% reported in 3Q12. 4Q12 ROAE was 19.1%, below reported ROAE of 21.9% and 21.1% in 4Q11 and 3Q12, respectively. Excluding the aforementioned gains in 3Q11, 4Q11 and 2Q12 as well as the aforementioned costs in 4Q12, normalized ROAE would have been 18.5% in 4Q12 and 15.3% in 4Q11, representing an increase of 320 bps. | |  |

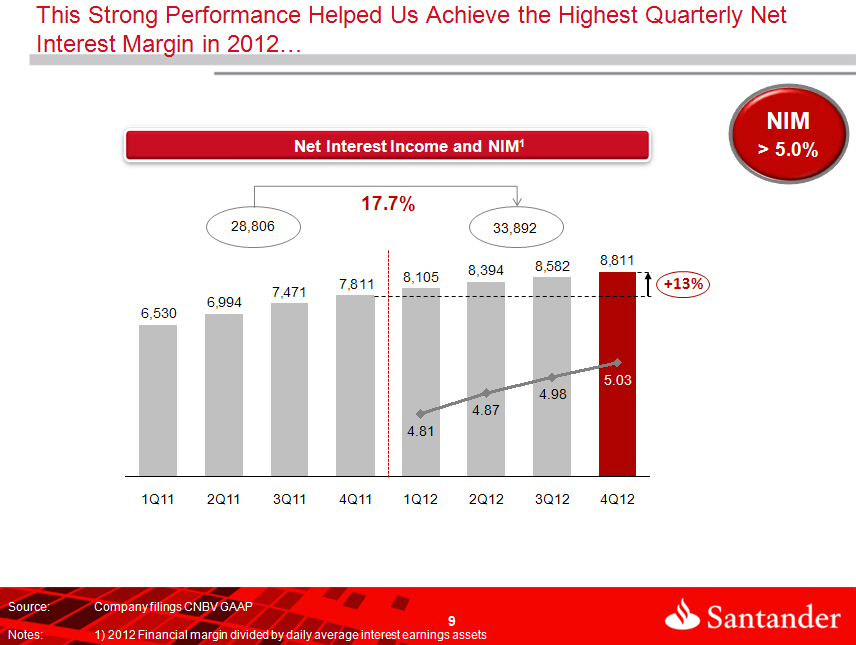

Net Interest Income Net interest income in 4Q12 increased YoY by 12.8%, or Ps.1,000 million, to Ps.8,811 million. On a sequential basis net interest income rose 2.7%, or Ps.229 million, from Ps.8,582 million reported in 3Q12. Net interest margin for 4Q12 was 5.03%, increasing 5 bps from 4.98% in 3Q12 and 3 bps below 5.06% in 4Q11. Interest income increased 10.5%, or Ps.1,351 million, reaching Ps.14,259 million in 4Q12 compared with Ps.12,908 million in 4Q11. This growth was mainly driven by higher interest income derived from our loan portfolio, which increased YoY by Ps.1,591 million. | |  |

Interest expense rose 6.9%, or Ps.351 million, reaching Ps.5,448 million in 4Q12 compared with Ps.5,097 million in 4Q11. This growth was mainly driven by the Ps.201 million increase in interest paid on our sale and repurchase agreements and in our credit instruments issued, as well as a Ps.91 million increase in interest paid on demand and term deposits as a consequence of higher volumes.

| | 4Q.12 | Earnings Report | 3 |

| |

|

| | | |

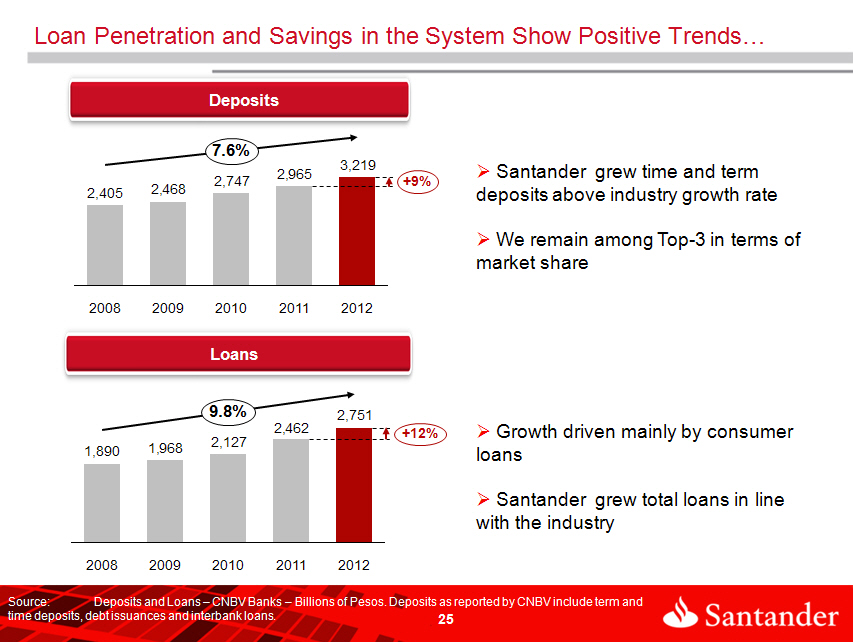

Loan Portfolio Growth

Santander México’s total loan portfolio in 4Q12 increased YoY by 11.8%, or Ps.37,010 million, to Ps.350,683 million, and 2.1%, or Ps.7,300 million, on a sequential basis.

In 4Q12, Santander México’s loan portfolio expanded YoY across all core products, both in terms of commercial and individual loans. Individual loans were mainly driven by consumer loans, mortgages and credit cards. Commercial loans continue to benefit from a significant YoY increase in the SME portfolio.

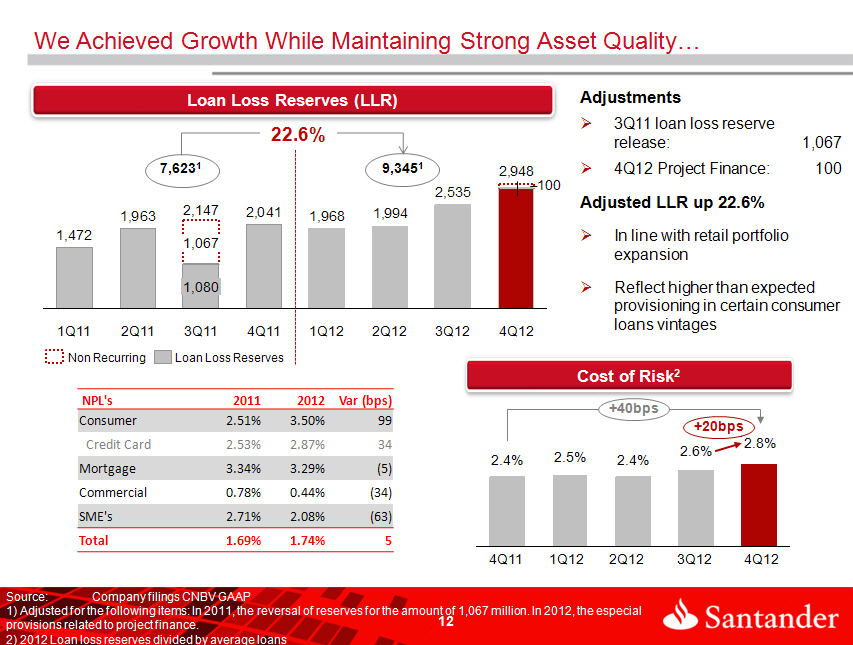

Asset Quality

The NPL ratio for 4Q12 stood at 1.74%, a 5 bps increase from the level reported in 4Q11 and 13 bps above 1.61% in 3Q12, reflecting Santander Mexico’s stringent credit scoring model and ongoing monitoring of the quality and growth of its loan portfolio.

NPLs as of 4Q12 increased 14.6% to Ps.6,093 million, from Ps.5,316 million reported in 4Q11. On a sequential basis, NPLs increased 10.2%.

The coverage ratio for the quarter decreased to 190.1%, from the 210.5% and 205.4% reported in 4Q11 and 3Q12, respectively. The decline in coverage ratio primarily reflects a nominal increase in non-performing loans resulting from the growth in the loan portfolio. Non-performing loans, however, increased more than the provisions for loan losses because the majority of the increase in the non-performing portfolio was driven by mortgages which are guaranteed by properties and thus require lower provisions than the consumer portfolio.

Loans to Deposit Ratio

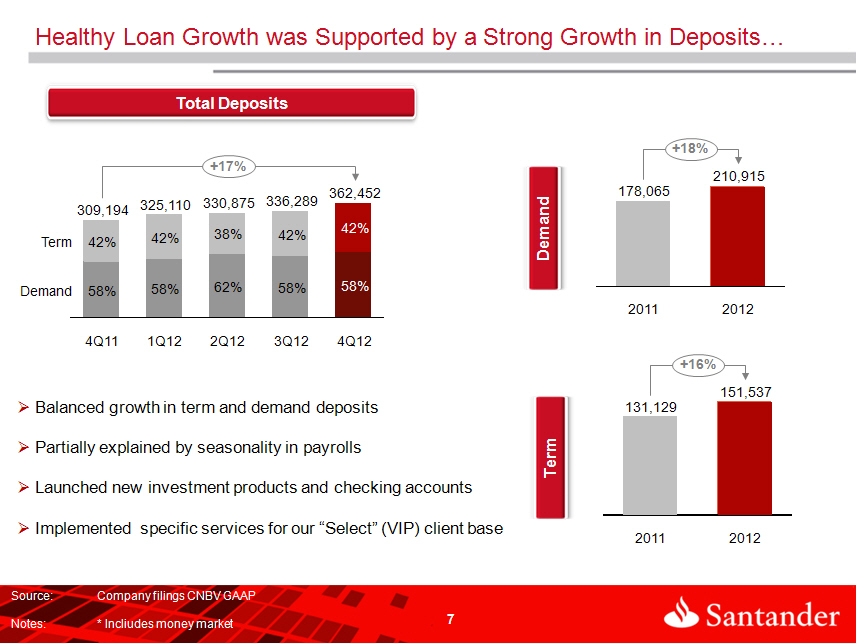

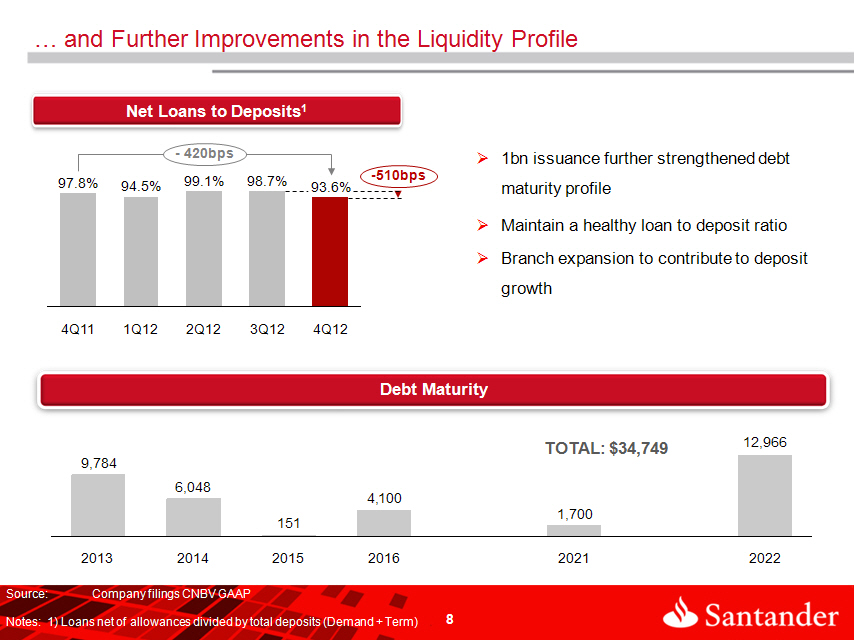

During 4Q12, deposits accounted for 55% of the Santander Mexico’s total funding sources, and expanded 17.2% YoY and 7.8% sequentially. This deposit base provides a stable, low cost source of funding to support Santander Mexico’s continued growth.

The net loan to deposit ratio was 93.6% in 4Q12, decreasing from 97.8% in 4Q11 and from 98.7% in 3Q12.

Contribution to Net Income

As previously discussed, net income for 4Q12 was Ps.3,310 million, representing declines of 57.2% YoY and 21.5% sequentially. Excluding the net impact of the extraordinary gain in 4Q11 from the sale of the insurance business to Zurich and the aforementioned items in 4Q12, net income would have increased 16.0% YoY.

Casa de Bolsa Santander, the brokerage business, reported net income of Ps.53 million, compared with gains of Ps.35 million in 4Q11 and Ps.116 million in 3Q12.

Net income for the Holding and other subsidiaries amounted to Ps.39 million in 4Q12, a decrease from Ps.4,387 million reported in 4Q11, which includes the gain from the sale of the insurance business to Zurich. Sequentially, 4Q12 was higher than the Ps.29 million reported in 3Q12.

| | 4Q.12 | Earnings Report | 4 |

| |

|

| | | |

| | Grupo Financiero Santander | | | | | | | | | | |

| | Earnings Contribution by Subsidiary | | | | | | | | | | |

| | Millions of Mexican Pesos | | | | | | | | | | |

| | | | 4Q12 | 3Q12 | | 4Q11 | | 2012 | 2011 | | YoY % |

| | Banking business1/ | | 3,218 | 4,069 | | 3,319 | | 17,398 | 13,700 | | 27.0 |

| | Brokerage | | 53 | 116 | | 35 | | 269 | 66 | | 307.6 |

| | Holding and other subsidiaries2/ | | 39 | 29 | | 4,387 | | 155 | 4,916 | | (96.8) |

| | Net income attributable to Grupo Financiero Santander | | 3,310 | 4,214 | | 7,741 | | 17,822 | 18,682 | | (4.6) |

1/ Includes Sofomes 2/ Asset management subsidiary and Holding.

| | 4Q.12 | Earnings Report | 5 |

| |

|

| | | |

ANALYSIS OF FOURTH-QUARTER 2012 CONSOLIDATED RESULTS

Net Income

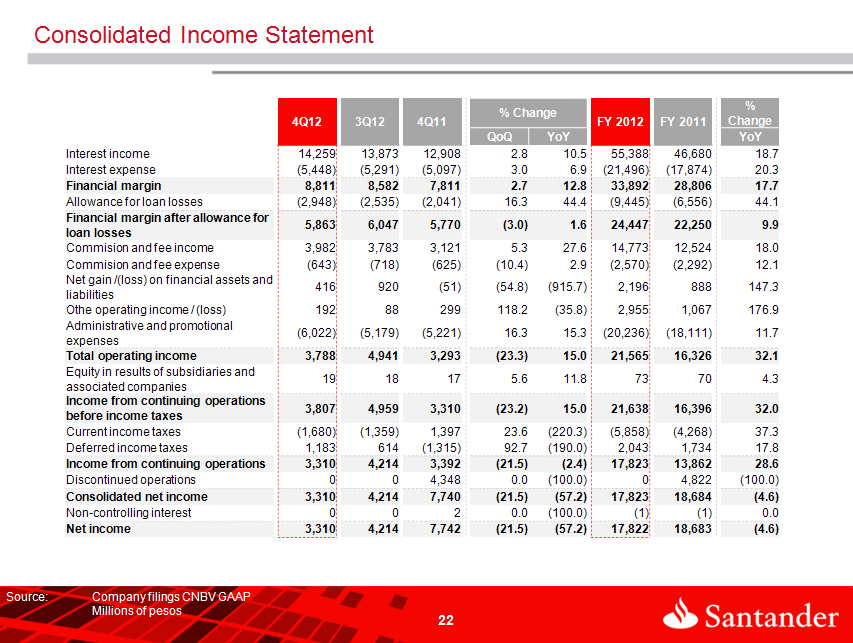

| | Grupo Financiero Santander México | | | | | | | | | | |

| | Income Statement | | | | | | | | | | |

| | Millions of Mexican Pesos | | | | | | % Change | | | % Change |

| | | | 4Q12 | 3Q12 | 4Q11 | | QoQ | YoY | 2012 | 2011 | 12/11 |

| | | | | | | | | | | | |

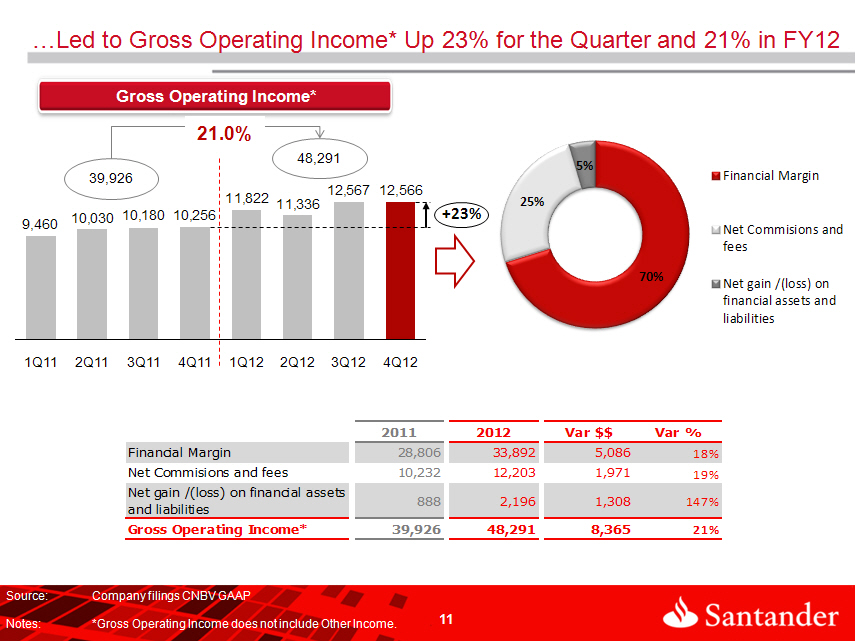

| | Net interest income | | 8,811 | 8,582 | 7,811 | | 2.7 | 12.8 | 33,892 | 28,806 | 17.7 |

| | Provision for loan losses | | (2,948) | (2,535) | (2,041) | | (16.3) | (44.4) | (9,445) | (6,556) | (44.1) |

| | Net interest income after provisions for loan losses | | 5,863 | 6,047 | 5,770 | | (3.0) | 1.6 | 24,447 | 22,250 | 9.9 |

| | Commission and fee income, net | | 3,339 | 3,065 | 2,496 | | 8.9 | 33.8 | 12,203 | 10,232 | 19.3 |

| | Gains (losses) on financial assets and liabilities | | 416 | 920 | (51) | | (54.8) | 915.7 | 2,196 | 888 | 147.3 |

| | Other operating income (expenses) | | 192 | 88 | 299 | | 118.2 | (35.8) | 2,955 | 1,067 | 176.9 |

| | Administrative and promotional expenses | | (6,022) | (5,179) | (5,221) | | (16.3) | (15.3) | (20,236) | (18,111) | (11.7) |

| | Operating income | | 3,788 | 4,941 | 3,293 | | (23.3) | 15.0 | 21,565 | 16,326 | 32.1 |

| | Equity in results of associated companies | | 19 | 18 | 17 | | 5.6 | 11.8 | 73 | 70 | 4.3 |

| | Operating income before taxes | | 3,807 | 4,959 | 3,310 | | (23.2) | 15.0 | 21,638 | 16,396 | 32.0 |

| | Current and deferred income taxes | | (497) | (745) | 81 | | 33.3 | (713.6) | (3,815) | (2,535) | (50.5) |

| | Income from continuing operations | | 3,310 | 4,214 | 3,391 | | (21.5) | (2.4) | 17,823 | 13,861 | 28.6 |

| | Profit from discontinued operations, net | | 0 | 0 | 4,348 | | 0.0 | (100.0) | 0 | 4,822 | (100.0) |

| | Non-controlling interest | | 0 | 0 | 2 | | 0.0 | (100.0) | (1) | (1) | 0.0 |

| | Net income | | 3,310 | 4,214 | 7,741 | | (21.5) | (57.2) | 17,822 | 18,682 | (4.6) |

During 4Q12, Santander México reported net income of Ps.3,310 million, representing a 57.2% YoY decrease and a 21.5% sequential decrease. These comparisons, however, are affected by a non-recurring gain of Ps.4,348 million in 4Q11 on the sale of the insurance business to Zurich.

Net income for 4Q12 was negatively impacted by higher provisions and write-offs as follows:

| · | Ps.100 million provision derived from a project finance client; |

| · | Ps.245 million write-off of account receivables in connection with certain guarantees subject to conditions that were not met and that had originated in mortgage loans with FOVI. |

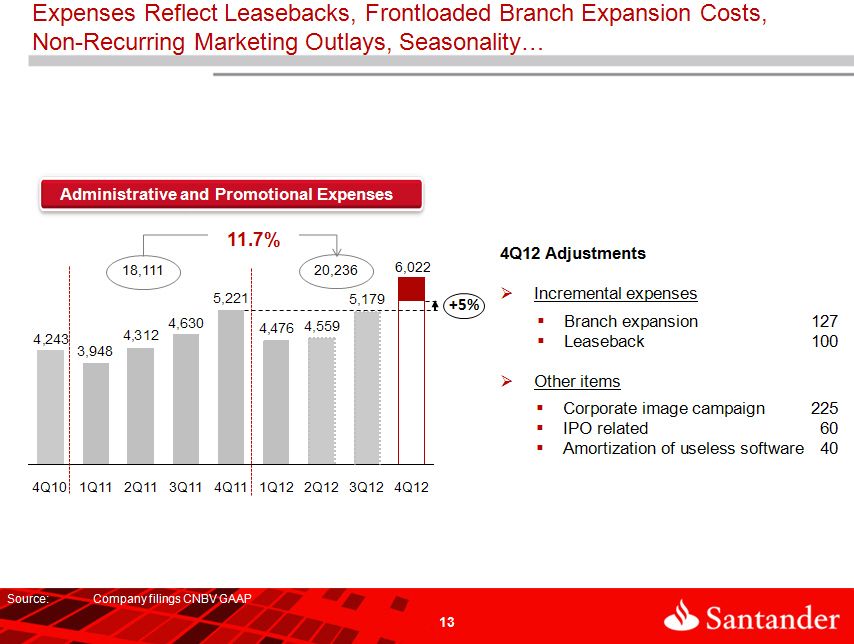

Results for the quarter were also negatively affected by the following incremental administrative and promotional expenses:

| · | Ps.225 million in marketing expenses from a corporate image campaign; |

| · | Ps.127 million related to the opening of 15 branches during the quarter and frontloading of expenses for branch openings in 2013; |

| · | Ps.100 million incremental rent from the 220 branches sold and leased back; |

| · | Ps.60 million expenses related to the Company’s IPO; and |

| · | Ps.40 million from the amortization of obsolete software |

Excluding these items, 4Q12 net income would have increased 16.0% YoY.

| | 4Q.12 | Earnings Report | 6 |

| |

|

| | | |

| | Grupo Financiero Santander México | | | | | | | | | | | | | | | | |

| | Net Income Adjustments | | | | | | | | | | | | | | | | |

| | Million Pesos | | | | | | | | | | | % Variación | | | | | % Variación |

| | | 4T12 | 3T12 | 2T12 | 1T12 | | 4T11 | 3T11 | 2T11 | 1T11 | | Interanual | | 2012 | 2011 | | 12/11 |

| | Net income | 3,310 | 4,214 | 5,285 | 5,013 | | 7,742 | 4,123 | 3,366 | 3,452 | | -57.2% | | 17,822 | 18,683 | | -4.6% |

| | Gain from the sale of the insurance business | | | | | 4,348 | 184 | 161 | 129 | | | | | 4,822 | | |

| | Sale and leaseback of branches | | | 1,731 | | | | | | | | | | 1,731 | | | |

| | Reversal of provisions | | | | | | | 1,067 | | | | | | | 1,067 | | |

| | FOVI write-off | (245) | | | | | | | | | | | | (245) | | | |

| | Corporate image campaign | (225) | | | | | | | | | | | | (225) | | | |

| | Project finance provisions | (100) | | | | | | | | | | | | (100) | | | |

| | IPO related expenses | (60) | | | | | | | | | | | | (60) | | | |

| | Amortization of obsolete software | (40) | | | | | | | | | | | | (40) | | | |

| | Branch expansion | (127) | | | | | | | | | | | | (127) | | | |

| | Rent from sale and leaseback | (100) | | | | | | | | | | | | (100) | | | |

| | Adjusted net income (before taxes) | 4,207 | 4,214 | 3,554 | 5,013 | 3,394 | 2,872 | 3,205 | 3,323 | | | | 16,988 | 6,266 | | |

| | Taxes | (269) | | 519 | | | | 320 | | | | | | 250 | 320 | | |

| | Adjusted net income | 3,938 | 4,214 | 4,073 | 5,013 | | 3,394 | 3,192 | 3,205 | 3,323 | | 16.0% | | 17,238 | 13,114 | | 31.4% |

Net interest income for 4Q12 rose to Ps.8,811 million, representing a YoY increase of Ps.1,000 million, or 12.8%. On a sequential basis, net interest income increased Ps.229 million, or 2.7%. An increase in the Bank’s business volume and a more profitable product mix resulted in a Ps.1,591 million increase in interest income, which more than offset the Ps.201 million rise in interest paid on our sale and repurchase agreements and on our issued credit instruments.

Provisions for loan losses for the quarter rose to Ps.2,948 million, representing increases of Ps.907 million, or 44.4%, YoY and Ps.413 million, or 16.3%, on a sequential basis. Results were impacted by provision derived from a project finance client discussed above, as well as provisions resulting from a trial campaign aimed at a specific target segment.

The NPL ratio for 4Q12 stood at 1.74%, a 5 bps increase from the level reported in 4Q11 and 13 bps from 1.61% in 3Q12.

The coverage ratio for the quarter decreased to 190.1% from 210.5% and 205.4% reported in 4Q11 and 3Q12, respectively. The decline in coverage ratio primarily reflects a nominal increase in non-performing loans resulting from the growth in the loan portfolio. Non-performing loans, however, increased more than the provisions for loan losses because the majority of the increase in the non-performing portfolio was driven by mortgages which are guaranteed by properties and thus require lower provisions than the consumer portfolio.

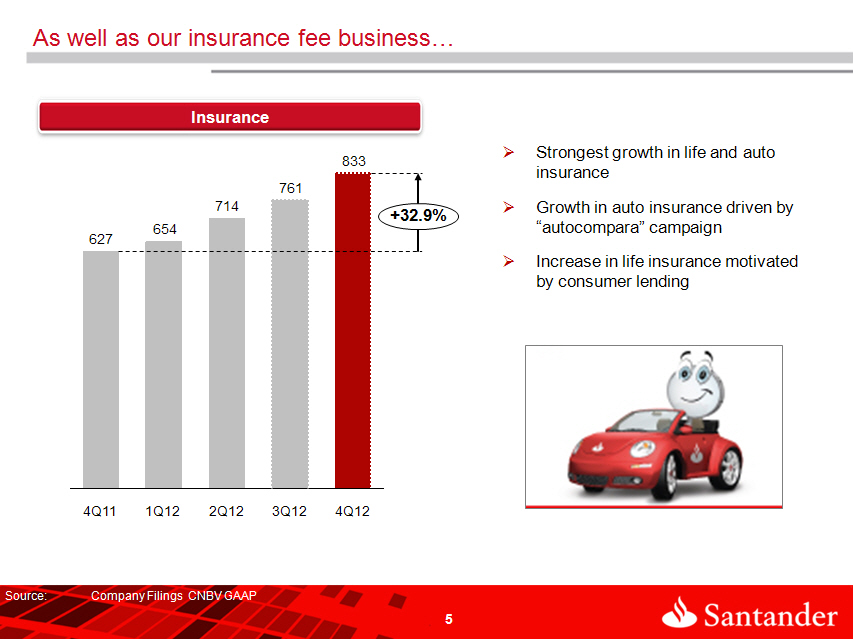

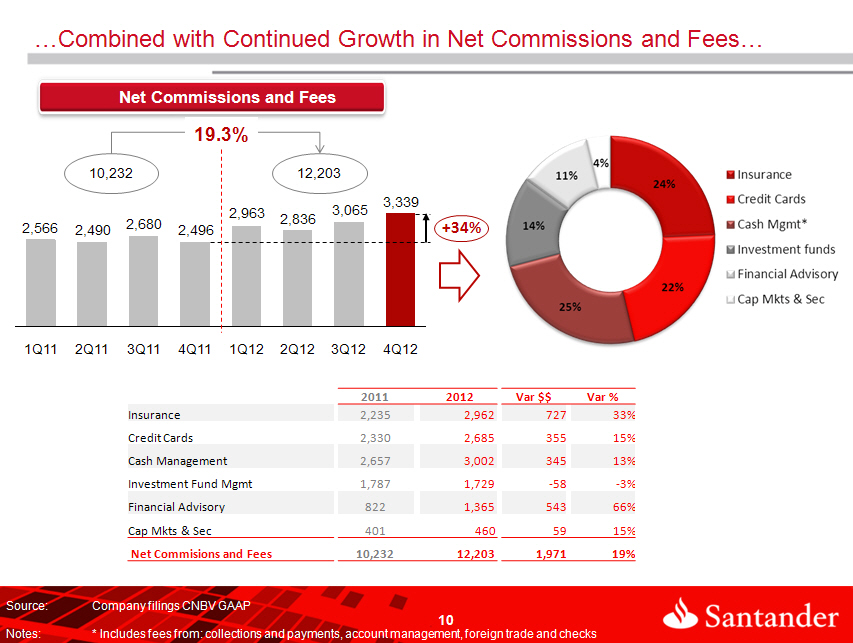

Net commissions and fee income for 4Q12 amounted to Ps.3,339 million, a 33.8% YoY increase, or Ps.843 million, and 8.9%, or Ps.274 million, higher on a sequential basis. The sequential increase is principally due to higher commissions from credit cards and insurance, which grew 39.9% and 9.5%, respectively.

During 4Q12, Santander México reported a Ps.416 million net gain from financial assets and liabilities, compared with a Ps.51 million net loss in 4Q11 and a Ps.920 million gain in 3Q12. Net gain on financial assets and liabilities in 4Q12 is mainly explained by trading gains of Ps.1,958 million, partially offset by valuation losses of Ps.1,542 million, principally related to derivatives and debt instruments. For FY12, gains from financial assets and liabilities income increased 147.3%, or Ps.1,308 million, to Ps.2,196 million.

Other income in 4Q12 declined to Ps.192 million, from Ps.299 million in 4Q11, and increased Ps.104 million from the Ps.88 million reported in 3Q12.

Administrative and promotional expenses for 4Q12 amounted to Ps.6,022 million, Ps.801 million, or 15.3%, higher than in 4Q11 and Ps.843 million, or 16.3%, higher than in 3Q12. The increase is mainly related to higher expenses to support business growth, as well as the items discussed above: leaseholds from the 220 branches sold and leased back, branch openings, a corporate image campaign, certain expenses in connection with the recent IPO and the amortization of obsolete software.

Operating income in 4Q12, totaled Ps.3,788 million, representing a YoY increase of Ps.495 million, or 15.0%. On a sequential basis, operating income decreased by Ps.1,153 million, or 23.3%.

| | 4Q.12 | Earnings Report | 7 |

| |

|

| | | |

Net income for FY12 amounted to Ps.17,822 million, a decrease of 4.6%, or Ps.861, from the Ps.18,683 million obtained for FY11. Excluding extraordinary gains and the aforementioned incremental costs, net income for FY12 would have been of Ps.17,238 million, an increase of 31.4%, or Ps.4,124 million from the Ps.13,114 million registered for FY11.

These results reflect mainly the combined impact of the following increases:

| § | 17.7%, or Ps.5,086 million, in net interest income from Ps.28,806 million for FY11 to Ps.33,892 million for FY12, reflecting a higher-margin product mix and the increase in the loan portfolio; |

| § | 19.3%, or Ps.1,971 million, in net commissions and fee income, from Ps.10,232 million for FY11 to Ps.12,203 million for FY12, principally due to increases in insurance, account management and financial advisory; |

| § | 147.3%, or Ps.1,308 million, in net gains from financial assets and liabilities from Ps.888 million for FY11 to Ps.2,196 million for FY12; and |

| § | 176.9%, or Ps.1,888 million, in other operating income from Ps.1,067 million for FY11 to Ps.2,955 million for FY12, explained by the Ps.1,731 million sale and leaseback of branches in 2Q12. |

These positive results were partially offset by:

| § | Increase in provisions for loan losses of Ps.2,889 million, or 44.1%, mainly due to the growth in the loan portfolio as well as the reversal of provisions for loan losses of Ps.1,067 million in 3Q11. The increase in provisions for loan losses is mainly related to: 1) variation in the loan portfolio mix, with more weight in consumer and credit card products which require a higher level of provisions; 2) provisions derived from a project finance client; and 3) the impact from a trial campaign aimed at a specific target segment. |

| § | Ps.2,125 million or 11.7% increase in administrative and promotional expenses from Ps.18,111 million in FY11 to Ps.20,236 million for FY12, mainly explained by the following increases: 13.6%, or Ps.1,044 million in personnel expenses; 24.7%, or Ps.446 million in other expenses; 28.7%, or Ps.281 million in leaseholds; and 10.4%, or Ps.170 million in technology expenses. As explained above, administrative and promotional expenses for the year also reflect higher costs incurred in 4Q12. |

| | 4Q.12 | Earnings Report | 8 |

| |

|

| | | |

Net Interest Income

| | Grupo Financiero Santander México | | | | | | | |

| | Net Interest Income | | | | | | | |

| | Millions of Mexican Pesos | | | | | | % Change | | | % Change |

| | | | 4Q12 | 3Q12 | 4Q11 | | QoQ | YoY | 2012 | 2011 | 12/11 |

| | Funds Available | | 577 | 574 | 702 | | 0.5 | (17.8) | 2,425 | 2,622 | (7.5) |

| | Margin accounts | | 96 | 99 | 38 | | (3.0) | 152.6 | 408 | 176 | 131.8 |

| | Interest from investment in securities | | 2,661 | 2,823 | 3,055 | | (5.7) | (12.9) | 12,043 | 11,589 | 3.9 |

| | Loan portfolio – excluding credit cards | | 7,637 | 7,399 | 6,571 | | 3.2 | 16.2 | 28,900 | 23,549 | 22.7 |

| | Credit card loan portfolio | | 2,321 | 2,141 | 1,787 | | 8.4 | 29.9 | 8,264 | 6,590 | 25.4 |

| | Loan origination fees | | 143 | 151 | 152 | | (5.3) | (5.9) | 625 | 592 | 5.6 |

| | Sale and repurchase agreements | | 824 | 686 | 603 | | 20.1 | 36.7 | 2,723 | 1,562 | 74.3 |

| | Interest Income | | 14,259 | 13,873 | 12,908 | | 0.3 | 10.5 | 55,388 | 46,680 | 18.7 |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | Customer deposits – Demand deposits | | (508) | (595) | (468) | | 14.6 | (8.5) | (2,165) | (1,503) | (44.0) |

| | Customer deposits – Time deposits | | (1,518) | (1,386) | (1,467) | | (9.5) | (3.5) | (5,630) | (5,567) | (1.1) |

| | Credit instruments issued | | (402) | (304) | (301) | | (32.2) | (33.6) | (1,298) | (893) | (45.4) |

| | Interbank loans | | (242) | (256) | (183) | | 5.5 | (32.2) | (791) | (781) | (1.3) |

| | Sale and repurchase agreements | | (2,778) | (2,750) | (2,678) | | (1.0) | (3.7) | (11,612) | (9,130) | (27.2) |

| | Interest Expense | | (5,448) | (5,291) | (5,097) | | (3.0) | (6.9) | (21,496) | (17,874) | (20.3) |

| | | | | | | | | | | | |

| | Net Interest Income | | 8,811 | 8,582 | 7,811 | | 2.7 | 12.8 | 33,892 | 28,806 | 17.7 |

Net interest income in 4Q12 amounted to Ps.8,811 million, representing QoQ and YoY increases of 2.7%, or Ps.229 million, and 12.8%, or Ps.1,000 million, respectively. For FY12, net interest income rose 17.7%, or Ps.5,086 million, to Ps.33,892 million, from Ps.28,806 million for FY11.

The YoY increase in net interest income for the quarter is explained by the combined effect of the Ps.1,351 million increase in interest income, from Ps.12,908 million in 4Q11 to Ps.14,259 million in 4Q12, and a Ps.351 million increase in interest expense, from Ps.5,097 million in 4Q11 to Ps.5,448 million in 4Q12. This was the result increases of Ps.39,314 million in average interest-earnings assets and 33 bpss in the average interest rate gained. Average interest-bearing liabilities rose Ps.44,431 million, representing a 4 bps increase in the average interest rate paid.

The sequential increase in net interest income resulted from the combined effect of the Ps.386 million increase in interest income, from Ps.13,873 million in 3Q12 to Ps.14,259 million in 4Q12, and a Ps.157 million increase in interest expense, from Ps.5,291 million in 3Q12 to Ps.5,448 million in 4Q12. This is explained by increases of Ps.13,638 million in average-earnings assets and 6 bpss in the average interest rate earned, combined with increases of Ps.15,329 million in interest-bearing liabilities and 1 bpss in the average interest rate paid.

The increase in net interest income in the twelve month period, resulted from the combined effect of the Ps.8,708 million increase in interest income, from Ps.46,680 million for FY11 to Ps.55,388 million for FY12, and a Ps.3,622 million increase in interest expense, from Ps.17,874 million for FY11 to Ps.21,496 million for FY12. This is explained by the Ps.110,886 million increase in average-earnings assets, together with a 7 bps decline in

| | 4Q.12 | Earnings Report | 9 |

| |

|

| | | |

the average interest rate earned, combined with a Ps.92,968 million increase in average interest-bearing liabilities and a 5 bps increase in the average interest rate paid.

Interest Income

Interest income rose to Ps.14,259 million in 4Q12 from Ps.13,873 million in 3Q12. This is explained by the combined increases of Ps.410 million in the loan portfolio and Ps.138 million in repurchase agreements, partially offset by lower interest income on investment in securities for Ps.162 million resulting from the decline of Ps.10,297 million in the average balance of investments in securities.

4Q12 interest-earning assets increased QoQ by Ps.13,638 million, or 2.1%, mainly driven by: a Ps.10,297 million decline in investments in securities, from Ps.203,834 million in 3Q12 to Ps.195,537 million in 4Q12, which was more than offset by a 17.9% increase in repurchase agreements.

The average interest gain on interest-earning assets rose in 4Q12 to 8.42%, representing a 33 bps increase from 8.09% in 4Q11 and a 6 bps growth compared with 8.36% in 3Q12.

Interest income rose YoY by 10.5%, or Ps.1,351 million, from Ps.12,908 million in 4Q11 to Ps.14,259 million in 4Q12, principally due to the increases of Ps.1,591 million in interest income on our loan portfolio and Ps.221 million in repurchase agreements.

The breakdown of interest income for 4Q12 is as follows: loan portfolio, which is considered as the main source of recurring income, accounts for 70.8%; investment in securities 18.7%; and 10.5% in other items.

FY12 average interest-earning assets increased by 19.7%, or Ps.110,886 million, to Ps.673,177 million, compared with Ps.562,291 million for FY11. FY12 interest income increased by Ps.8,709 million, or 18.7%, to Ps.55,388 million, compared with Ps.46,680 million for FY11.

The evolution of the loan portfolio continues to show positive trends, with diversification across all segments and growth in all core businesses.

| | 4Q.12 | Earnings Report | 10 |

| |

|

| | | |

Loan Portfolio

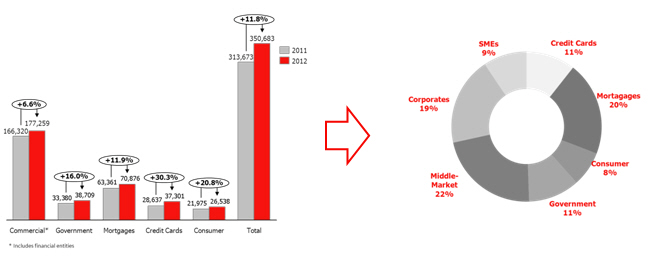

The total loan portfolio rose YoY by 11.8%, or Ps.37,010 million, to Ps.350,683 million in 4Q12. On a sequential basis, the total loan portfolio increased 2.1%, or Ps.7,300 million. During the quarter, Santander México continued to experience loan growth across all core segments and strategic products.

| Grupo Financiero Santander México | | | | | | | | |

| Loan Portfolio Breakdown | | | | | | | | |

| Millions of Mexican Pesos | 4Q12 | % | | 3Q12 | % | | 4Q11 | % |

| | | | | | | | | |

| Commercial | 175,736 | 50.11% | | 176,564 | 51.42% | | 164,394 | 52.41% |

| Government | 38,709 | 11.04% | | 35,121 | 10.23% | | 33,378 | 10.64% |

| Consumer | 61,603 | 17.57% | | 59,996 | 17.47% | | 49,342 | 15.73% |

| Credit cards | 36,230 | 10.33% | | 34,208 | 9.96% | | 27,912 | 8.90% |

| Other consumer | 25,373 | 7.24% | | 25,788 | 7.51% | | 21,430 | 6.83% |

| Mortgages | 68,542 | 19.55% | | 66,172 | 19.27% | | 61,243 | 19.52% |

| Total Performing Loan | 344,590 | 98.26% | | 337,853 | 98.39% | | 308,357 | 98.31% |

| | | | | | | | | |

| | | | | | | | | |

| Commercial | 1,523 | 0.43% | | 1,402 | 0.41% | | 1,926 | 0.61% |

| Government | 0 | 0.00% | | 0 | 0.00% | | 2 | 0.00% |

| Consumer | 2,236 | 0.64% | | 2,053 | 0.60% | | 1,270 | 0.40% |

| Credit cards | 1,071 | 0.31% | | 1,055 | 0.31% | | 724 | 0.23% |

| Other consumer | 1,165 | 0.33% | | 998 | 0.29% | | 546 | 0.17% |

| Mortgages | 2,334 | 0.67% | | 2,075 | 0.60% | | 2,118 | 0.68% |

| Total Non-Performing Loan | 6,093 | 1.74% | | 5,530 | 1.61% | | 5,316 | 1.69% |

| | | | | | | | | |

| Total Loan Portfolio | 350,683 | 100.00% | | 343,383 | 100.00% | | 313,673 | 100.00% |

| | 4Q.12 | Earnings Report | 11 |

| |

|

| | | |

The Commercial Portfolio is composed of loans to business and commercial enterprises, as well as loans to government entities and financial institutions, and represents 61.6% of the total loan portfolio. Excluding loans to government, the commercial portfolio accounted for 50.5% of the total loan portfolio. As of 4Q12 commercial loans increased 8.1% YoY, principally reflecting the 76.7% and 14.2% increase in SMEs and middle market, respectively. On a sequential basis, excluding loans to government, the commercial portfolio remained stable, principally supported by the performance of SMEs during the quarter, which increased 6.9%.

The Individual Loan Portfolio, composed of mortgages, credit card and consumer loans, represents 38.4% of the total loan portfolio. Credit cards, consumer and mortgages loans represent 10.6%, 7.6%, and 20.2% of the total loan portfolio, respectively, and increased YoY by 30.3%, 20.8%, and 11.9%, respectively. Our mortgage loans strategy remains focused on targeting the middle market segment and residential. The Individual Loan Portfolio increased 3.9% QoQ. Our strategy for consumer loans aims to support families, and loans to these clients expanded 2.9% QoQ. Credit card loans increased 5.8%, principally driven by marketing campaigns implemented during the last part of the year to encourage the use of credit cards with zero interest financing, as well as the results achieved by our commercial teams throughout our branch network and our multichannel strategy.

Interest Expense

Interest expense increased 6.9%, or Ps.351 million, to Ps.5,448 million in 4Q12, compared with Ps.5,097 million in 4Q11, principally explained by a Ps.260 million increase in interest paid on repurchase agreements, interbank loans and credit instruments issued, due to higher volume. On a sequential basis, interest expense increased Ps.157 million, mainly reflecting a higher average balance of credit instruments issued and term deposits.

For FY12 interest expense was Ps.21,496 million, a Ps.3,622 million, or 20.3% increase, compared with Ps.17,874 million recorded for FY11.

The Ps.5,448 million in interest expenses paid in 4Q12 is broken down as follows: sale and repurchase agreements 51.0%, term deposits 27.9%, demand deposits 9.3%, credit instruments issued 7.4%, and interbank loans 4.4%.

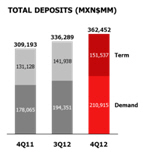

Total deposits at the end of 4Q12 amounted to Ps.362,452 million, representing a 17.2% YoY increase. Santander México continues to implement its strategy of enhancing customer service in accordance with the needs of each segment. This strategy has resulted in an increase in demand deposits from both individuals and corporates. As of 4Q12, demand deposits reached Ps.210,915 million, increasing 18.4% YoY and 8.5% on a sequential basis. Total term deposits reached Ps.151,537 million, a 15.6% YoY increase, and 6.8% compared with 3Q12.

Interest expense on demand deposits amounted to Ps.508 million during 4Q12, representing a YoY increase of 8.5% and a sequential decline of 14.6%. The increase in 4Q12 YoY, was mainly driven by a higher average balance in demand deposits, which rose 9.1%, or Ps.12,104 million.

| | 4Q.12 | Earnings Report | 12 |

| |

|

| | | |

Interest paid on term deposits increased 2.0% YoY to Ps.1,543 million. On a sequential basis, interest paid on term deposits increased 11.2%. The 2.0% increase compared to 4Q11 reflects average volume together with an average rate increase.

Asset Quality

Non-performing loans at the end of 4Q12 increased by Ps.777 million, or 14.6% YoY, to Ps.6,093 million, and also increased on a sequential basis by 10.2%, or Ps.563 million. The breakdown of the non-performing loan portfolio is as follows: commercial loans 25.0%, consumer loans 36.7%, and mortgages 38.3%.

The YoY increase in non-performing loans, primarily reflects growth of the loan portfolio, particularly the higher participation of consumer loans, credit cards loans, mortgage loans and SMEs products in the overall mix. On a sequential basis, mortgages presented the highest increase in non-performing loans.

| | Grupo Financiero Santander México | | | | | | |

| | Asset Quality | | | | | | | | |

| | Millions of Mexican Pesos | | 2012 | 2012 | | 2011 | | Change % |

| | | | 4Q | 3Q | | 4Q | | QoQ | YoY |

| | Total Loans | | 350,683 | 343,383 | | 313,673 | | 2.13% | 11.80% |

| | Performing Loans | | 344,590 | 337,853 | | 308,357 | | 1.99% | 11.75% |

| | Non-performing Loans | | 6,093 | 5,530 | | 5,316 | | 10.18% | 14.62% |

| | | | | | | | | | |

| | Allowance for loan losses | | (11,580) | (11,360) | | (11,191) | | 1.94% | 3.48% |

| | | | | | | | | | |

| | Non-performing loan ratio | | 1.74% | 1.61% | | 1.69% | | 13bps | 4bps |

| | Coverage ratio | | 190.1 | 205.4 | | 210.5 | | (1,537)bps | (2,046)bps |

The NPL ratio for 4Q12 stood at 1.74%, a 5 bps increase from the level reported in 4Q11 and 13 bps from 1.61% in 3Q12, reflecting Santander México’s strict monitoring and portfolio quality assessment processes, which allows the adjustment of loan origination through approval policies in accordance with the performance of the loan portfolio. The coverage ratio for the quarter decreased to 190.1%, from 210.5% in 4Q11, and from 205.4% in 3Q12. The sequential decline in the coverage ratio primarily reflects a nominal increase in non-performing loans resulting from the growth of the loan portfolio. Non-performing loans, however, increased more than the provisions for loan losses because the majority of the increase in the non-performing portfolio was driven by mortgages which are guaranteed by properties and thus require lower provisions than the consumer portfolio.

| | 4Q.12 | Earnings Report | 13 |

| |

|

| | | |

During 4Q12 allowance for loan losses amounted to Ps.2,948 million, which represented a 16.3% increase compared with 3Q12, principally generated in consumer, mortgages and credit card loan portfolios. 4Q12 allowance for loan losses were impacted by provisions derived from a project finance client and the impact from a trial campaign aimed at a specific target segment.

For FY12, allowances for loan losses increased by 44.1%, or Ps.2,889 million, to Ps.9,445 million compared with the same period last year. This increase is mainly explained by the 11.8% growth in the loan portfolio during the last twelve months, the low comparison base resulting from the reversal of provisions in 3Q11 to comply with CNBV (Comisión Nacional Bancaria y de Valores) regulations, and the higher provisions in 4Q12 discussed above.

| | 4Q.12 | Earnings Report | 14 |

| |

|

| | | |

Commission and Fee Income (Net)

| | Grupo Financiero Santander México | | | | | | | | |

| | Net Commission and Fee Income | | | | | | | | |

| | Millions of Mexican Pesos | | | | | | | | |

| | | | | | | | % Change | | | % Change |

| | Commission and fee income | | 4Q12 | 3Q12 | 4Q11 | | QoQ | YoY | 2012 | 2011 | 12/11 |

| | Credit and debit cards | | 1,194 | 1,026 | 903 | | 16.4 | 32.2 | 4,010 | 3,333 | 20.3 |

| | Cash management | | 181 | 176 | 172 | | 2.8 | 5.2 | 711 | 590 | 20.5 |

| | Collection and payment services | | 351 | 347 | 308 | | 1.2 | 14.0 | 1,434 | 1,257 | 14.1 |

| | Investment fund management | | 452 | 461 | 464 | | (2.0) | (2.6) | 1,838 | 1,877 | (2.1) |

| | Insurance | | 856 | 783 | 655 | | 9.3 | 30.7 | 3,049 | 2,311 | 31.9 |

| | Capital markets and securities activities | | 153 | 151 | 137 | | 1.3 | 11.7 | 621 | 548 | 13.3 |

| | Checks | | 91 | 86 | 94 | | 5.8 | (3.2) | 356 | 382 | (6.8) |

| | Foreign trade | | 130 | 126 | 123 | | 3.2 | 5.7 | 527 | 489 | 7.8 |

| | Financial advisory services | | 330 | 430 | 85 | | (23.3) | 288.2 | 1,394 | 1,048 | 33.0 |

| | Other commissions and fees | | 244 | 197 | 180 | | 23.9 | 35.6 | 833 | 689 | 20.9 |

| | Total | | 3,982 | 3,783 | 3,121 | | 5.3 | 27.6 | 14,773 | 12,524 | 18.0 |

| | | | | | | | | | | | |

| | Commission and fee expense | | | | | | | | | | |

| | Credit and debit cards | | (286) | (377) | (280) | | 24.1 | (2.1) | (1,325) | (1,003) | (32.1) |

| | Investment fund management | | (30) | (28) | (16) | | (7.1) | (87.5) | (109) | (90) | (21.1) |

| | Insurance | | (23) | (22) | (28) | | (4.5) | 17.9 | (87) | (76) | (14.5) |

| | Capital markets and securities activities | | (40) | (46) | (43) | | 13.0 | 7.0 | (161) | (147) | (9.5) |

| | Checks | | (11) | (9) | (11) | | (22.2) | 0.0 | (38) | (43) | 11.6 |

| | Financial advisory services | | (7) | (11) | (19) | | 36.4 | 63.2 | (29) | (226) | 87.2 |

| | Other commissions and fees | | (246) | (225) | (228) | | (9.3) | (7.9) | (821) | (707) | (16.1) |

| | Total | | (643) | (718) | (625) | | 10.4 | (2.9) | (2,570) | (2,292) | (12.1) |

| | | | | | | | | | | | |

| | Commission and Fee Income, net | | 3,339 | 3,065 | 2,496 | | 8.9 | 33.8 | 12,203 | 10,232 | 19.3 |

In 4Q12 net commission and fee income amounted to Ps.3,339 million, representing a YoY increase of 33.8%, or Ps.843 million. This improvement principally reflects the following YoY increases: 45.7%, or Ps.285 million, in credit and debit card fees; 32.9%, or Ps.206 million, in insurance fees; and 389.4%, or Ps.257 million, in financial advisory services.

Compared to 3Q12, net commission and fee income rose 8.9%, or Ps.274 million, mainly reflecting the following sequential increases: 39.9%, or Ps.259 million, in credit card fees; and 9.5%, or Ps.72 million, in insurance fees mainly reflecting growth of “Autocompara”.

For FY12, net commission and fee income increased 19.3% YoY, or Ps.1,971 million, to Ps.12,203 million.

| | 4Q.12 | Earnings Report | 15 |

| |

|

| | | |

Net gain (loss) on financial assets and liabilities

| | Grupo Financiero Santander México | | | | | | |

| | Net gain (loss) on financial assets and liabilities | | | | |

| | Millions of Mexican Pesos | | | | | | % Change | | | % Change |

| | | | 4Q12 | 3Q12 | 4Q11 | | QoQ | YoY | 2012 | 2011 | 12/11 |

| | Valuation | | | | | | | | | | |

| | Foreign currencies | | 6 | (110) | (115) | | 105.5 | 105.2 | (75) | (36) | (108.3) |

| | Derivatives | | (993) | (9) | 92 | | (10,933.3) | (1,179.3) | (996) | (3,129) | 68.2 |

| | Shares | | 345 | 0 | 1,127 | | 100.0 | (69.4) | 457 | (1,352) | 133.8 |

| | Debt instruments | | (900) | 526 | (386) | | (271.1) | (133.2) | 126 | 53 | 137.7 |

| | Subtotal | | (1,542) | 407 | 718 | | (478.9) | (314.8) | (488) | (4,464) | 89.1 |

| | | | | | | | | | | | |

| | Trading | | | | | | | | | | |

| | Foreign currencies | | (435) | 191 | 202 | | (327.7) | (315.3) | 94 | 1,134 | (91.7) |

| | Derivatives | | 1,294 | 338 | (1,135) | | 282.8 | 214.0 | 983 | 4,603 | (78.6) |

| | Shares | | 306 | 135 | (224) | | 126.7 | 236.6 | 1,028 | (528) | 294.7 |

| | Debt instruments | | 793 | (151) | 388 | | 625.2 | 104.4 | 579 | 143 | 304.9 |

| | Subtotal | | 1,958 | 513 | (769) | | 281.7 | 354.6 | 2,684 | 5,352 | (49.9) |

| | | | | | | | | | | | |

| | Total | | 416 | 920 | (51) | | (55) | 916 | 2,196 | 888 | 147.3 |

In 4Q12, Santander México recorded a net gain on financial assets and liabilities of Ps.416 million, compared with a net loss of -Ps.51 million in 4Q11 and a net gain of Ps.920 million in 3Q12. The net gain on financial assets and liabilities in 4Q12 is mainly explained by trading gains of Ps.1,958 million, which were partially offset by a Ps.1,542 million valuation loss principally related to derivatives and debt instruments. This compares to gains of Ps.407 million and Ps.513 million in 3Q12 from valuation and trading, respectively. During 4Q11, Santander México reported a Ps.718 million valuation gain, despite currency and debt instrument losses which was more than offset by a Ps.769 million trading loss.

| | 4Q.12 | Earnings Report | 16 |

| |

|

| | | |

Other Operating Income (Expense)

| | Grupo Financiero Santander México | | | | | | | | |

| | Other Operating Income (Expense) | | | | | | | | |

| | | | | | | | % Change | | | % Change |

| | | | 4Q12 | 3Q12 | 4Q11 | | QoQ | YoY | 2012 | 2011 | 12/11 |

| | | | | | | | | | | | |

| | Recoveries of loans previously charged-off | | 439 | 467 | 407 | | (6.0) | 7.9 | 1,804 | 1,525 | 18.3 |

| | Income from sale of fixed assets | | 9 | 1 | 13 | | 800.0 | (30.8) | 1,741 | 13 | 13,292.3 |

| | Allowance for loan losses released | | 0 | 0 | 0 | | (100.0) | 0.0 | 378 | 0 | 0.0 |

| | Recovered taxes | | 0 | 0 | 81 | | 0.0 | (100.0) | 0 | 96 | (100.0) |

| | Cancellation of liabilities and reserve | | 47 | 43 | 55 | | 9.3 | (14.5) | 201 | 176 | 14.2 |

| | Interest on personnel loans | | 33 | 31 | 29 | | 6.5 | 13.8 | 122 | 110 | 10.9 |

| | Foreclosed assets reserve | | (14) | (6) | (23) | | (133.3) | 39.1 | (44) | (48) | 8.3 |

| | Profit from sale of foreclosed assets | | 35 | 43 | 42 | | (18.6) | (16.7) | 146 | 54 | 170.4 |

| | Acquisition of discounted loan portfolio | | | 0 | 0 | | 0.0 | 0.0 | 0 | 112 | (100.0) |

| | Technical advisory services | | 28 | 25 | 20 | | 12.0 | 40.0 | 103 | 72 | 43.1 |

| | Portfolio recovery legal expenses and costs | | (179) | (118) | (121) | | (51.7) | (47.9) | (611) | (452) | (35.2) |

| | Write-offs and bankruptcies | | (178) | (331) | (114) | | 46.2 | (56.1) | (791) | (383) | (106.5) |

| | Provision for legal and tax contingencies | | (73) | (97) | (100) | | 24.7 | 27.0 | (272) | (242) | (12.4) |

| | IPAB (indemnity) provisions and payments | | (2) | (2) | (25) | | 0.0 | 92.0 | (35) | (34) | (2.9) |

| | Recoveries of loans previously charged-off | | 0 | 0 | 32 | | 0.0 | (100.0) | 0 | 32 | (100.0) |

| | Other | | 47 | 32 | 3 | | 46.9 | 1,466.7 | 213 | 36 | 491.7 |

| | | | | | | | | | | | |

| | Other Operating Income (Expense) | | 192 | 88 | 299 | | 118.1 | (35.8) | 2,955 | 1,067 | 176.9 |

In 4Q12 other operating income declined to Ps.192 million, from Ps.299 million in 4Q11 and from Ps.88 million in 3Q12.

For FY12, other net operating income increased to Ps.2,955 million, compared with Ps.1,067 million for FY11. This growth is mainly explained by the extraordinary gain derived from the sale of 220 branches to Fibra Uno in 2Q12.

| | 4Q.12 | Earnings Report | 17 |

| |

|

| | | |

Administrative and Promotional Expenses

Administrative and promotional expenses consist of personnel such as payroll and benefits, promotion and advertising expenses, and other general expenses. Personnel expenses consist mainly of salaries, social security contributions, bonuses and our long-term incentive plan for our executives. Other general expenses mainly consist of: expenses related to technology and systems, administrative services, which are mainly services outsourced in the areas of information technology, taxes and duties, professional fees, contributions to IPAB, rental of properties and hardware, advertising and communication, surveillance and cash courier services and expenses related to maintenance, conservation and repair, among others.

| | Grupo Financiero Santander México | | | | | | | | | | |

| | Administrative and Promotional Expenses | | | | | | | | |

| | Millions of Mexican Pesos | | | | | | % Change | | | % Change |

| | | | 4Q12 | 3Q12 | 4Q11 | | QoQ | YoY | 2012 | 2011 | 12/11 |

| | Salaries and employee benefits | | 2,342 | 2,170 | 2,026 | | 7.9 | 15.6 | 8,734 | 7,690 | 13.6 |

| | Credit card operation | | 79 | 100 | 102 | | (21.0) | (22.5) | 256 | 243 | 5.3 |

| | Professional fees | | 244 | 108 | 202 | | 125.9 | 20.8 | 616 | 696 | (11.5) |

| | Leasehold | | 357 | 339 | 246 | | 5.3 | 45.1 | 1,261 | 980 | 28.7 |

| | Promotional and advertising expenses | | 401 | 151 | 411 | | 165.6 | (2.4) | 769 | 827 | (7.0) |

| | Taxes and duties | | 408 | 307 | 317 | | 32.9 | 28.7 | 1,081 | 992 | 9.0 |

| | Technology services (IT) | | 462 | 504 | 478 | | (8.3) | (3.3) | 1,803 | 1,633 | 10.4 |

| | Depreciation and amortization | | 410 | 389 | 388 | | 5.4 | 5.7 | 1,557 | 1,464 | 6.4 |

| | Contributions to bank savings protection system (IPAB) | | 355 | 341 | 326 | | 4.1 | 8.9 | 1,342 | 1,228 | 9.3 |

| | Cash protection | | 189 | 147 | 183 | | 28.6 | 3.3 | 566 | 553 | 2.4 |

| | Other services and expenses | | 775 | 623 | 542 | | 24.4 | 43.0 | 2,251 | 1,805 | 24.7 |

| | | | | | | | | | | | |

| | Total Administrative and Promotional Expenses | | 6,022 | 5,179 | 5,221 | | 16.3 | 15.3 | 20,236 | 18,111 | 11.7 |

4Q12 administrative and promotional expenses rose 15.3% YoY to Ps.6,022 million, driven by increases in the following areas: Ps.316 million in salaries and employee benefits, Ps.111 million in leaseholds, Ps.91 million in taxes and duties and Ps.233 million in other expenses.

On a sequential basis, administrative and promotional expenses rose 16.3%, principally due to the following increases: Ps.250 million in promotional expenses, Ps.172 million in salaries and employee benefits, Ps.152 million in other expenses, Ps.101 million in tax and duties, Ps.21 million in credit cards operation and Ps.18 million in leaseholds.

Results for the quarter were negatively affected by the following incremental administrative and promotional expenses:

| § | Ps.225 million in marketing expenses from a corporate image campaign; |

| § | Ps.127 million related to the opening of 15 branches during the quarter and frontloading of expenses for branch openings in 2013; |

| § | Ps.100 million incremental rent from the 220 branches sold and leased back; |

| § | Ps.60 million expenses related to the Company’s IPO; and |

| § | Ps.40 million from the amortization of obsolete software |

During 4Q12, administrative and promotional expenses grew in line with the recurring business. Additionally, administrative and promotional expenses are seasonally higher in the fourth quarter, mainly explained by expenses in marketing campaigns which become stronger in the second half of the year.

| | 4Q.12 | Earnings Report | 18 |

| |

|

| | | |

For FY12, administrative and promotional expenses increased 11.7% to Ps.20,236 million compared with FY11. This increase is mainly explained by higher: personnel expenses, leaseholds, tax and duties, technology and other administrative expenses.

The efficiency ratio for 4Q12 was 39.5%, which compares to 44.2% and 36.9% reported in 4Q11 and 3Q12, respectively.

The recurrence ratio in 4Q12 was 65.3%, improving from 61.5% in 4Q11 and slightly decreasing versus 67.8% in 3Q12.

Current and Deferred Taxes

Current and deferred income taxes in 4Q12 amounted to Ps.497 million compared with the Ps.82 million tax credit recorded in 4Q11 and below the Ps.745 in 3Q12.

For FY12, current and deferred income taxes amounted to Ps.3,815 million, representing a 50.6%, or Ps.1,281 million increase against FY12.

Capitalization and ROAE

| | Grupo Financiero Santander México | | | | |

| | Capitalization | | | | | | |

| | Millions of Mexican Pesos | | 4Q12 | | 3Q12 | | 4Q11 |

| | Tier 1 | | 74,618 | | 73,570 | | 71,674 |

| | Tier 2 | | 1,579 | | 1,538 | | 1,469 |

| | Total Capital | | 76,197 | | 75,108 | | 73,143 |

| | | | | | | | |

| | Risk-Weighted Assets | | | | | | |

| | Credit Risk | | 320,268 | | 313,707 | | 267,270 |

| | Credit, Market, and Operational Risk | | 515,583 | | 519,647 | | 493,249 |

| | | | | | | | |

| | Credit Risk Ratios: | | | | | | |

| | Tier 1 (%) | | 23.3 | | 23.5 | | 26.8 |

| | Tier 2(%) | | 0.5 | | 0.5 | | 0.5 |

| | Capitalization Ratio (%) | | 23.8 | | 23.9 | | 27.4 |

| | | | | | | | |

| | Total Capital Ratios: | | | | | | |

| | Tier 1(%) | | 14.5 | | 14.2 | | 14.5 |

| | Tier 2 (%) | | 0.3 | | 0.3 | | 0.3 |

| | Capitalization Ratio (%) | | 14.8 | | 14.5 | | 14.8 |

Banco Santander México’s capital ratio was 14.8% in 4Q12, unchanged YoY and above the 14.5% reported in 3Q12. The capital ratio reflects the impact of the Ps.7.3 billion cash dividend paid during 3Q12. The core capital ratio amounted to 14.5% in 4Q12, unchanged from the 14.5% reported in 4Q11 and above 14.2% in 3Q12.

| | 4Q.12 | Earnings Report | 19 |

| |

|

| | | |

As of June 2012, Santander México is classified within Category 1 in accordance with Article 134bis of the Mexican Banking Law, and remains in this category as per the preliminary results dated July 2012, which is the most recently available analysis.

ROAE in 4Q12 was 19.1%, a decrease of 280 bps from the 21.9% reported in 4Q11, and below the 21.1% in 3Q12. Excluding the aforementioned events in 3Q11, 4Q11, 2Q12 and 4Q12, adjusted ROAE would have been 18.5% in 4Q12 and 15.3% in 4Q11, representing a 320 bps YoY increase.

RELEVANT EVENTS

Santander Issues Bond in the International Markets

In November 2012, Banco Santander Mexico issued a 10-year bond in the international markets with a principal amount of US$1 billion at an interest rate of 260 bps over US Treasuries.

Financing of CFE’s Energy Generation Plant

During 4Q12, Banco Santander Mexico concluded a 10.5-year structured financing to fund the second stage of CFE’s “Manzanillo” energy generation plant. Santander Mexico participated in US$247 million of the total US$424 million financing, together with the Korean Development Bank (“KDB”). The transaction was 100% guaranteed under an Export Finance program by Korean Trade Insurance Corporation (“K-sure”), an export credit agency (“ECA”).

Financing of a PEMEX Exploration and Drilling Platform

During 4Q12, Banco Santander Mexico participated in the structuring and syndication of a US$547 million, 5.7-year financing of a Deep Sea Oil and Gas Exploration and Drilling Platform (Group R), the most modern of its kind at PEMEX Exploration. Santander Mexico’s participation in the financing amounted to US$29 million.

AWARDS & RECOGNITION

Santander Mexico is Recognized as “Bank of the Year” by The Banker

In November 2012, Santander Mexico was awarded Bank of the Year 2012 by the prestigious magazine, The Banker. Banco Santander Mexico was recognized this year for the efficiency of its operations, capacity to innovate and its aggressive commercial offering, which combined with a healthy loan portfolio allowed for an increase of almost 35% in net income during fiscal year 2011.

Santander Receives Three Awards from Nafin for its Contribution to SMEs’ Financing

In November 2012, Banco Santander Mexico received three awards from Nacional Financiera (Nafin) for its contribution in providing financing to Small and Medium Enterprises, becoming the first institution to win in three categories during the same year. In the context of the Nafin awards to Financial Intermediaries, Banco Santander was recognized for its leadership and innovation in the “Government Suppliers”, “Small Contributors Regime (REPECOS)” and “Guarantees” categories.

| | 4Q.12 | Earnings Report | 20 |

| |

|

| | | |

CREDIT RATINGS

| | Banco Santander (México) | | | | | | |

| | Ratings | | | | | | |

| | | | Standard & Poor´s | | Moody´s | | Fitch Ratings |

| | Global Scale | | | | | | |

| | Foreign Currency | | | | | | |

| | Long Term | | BBB | | Baa1 | | BBB+ ** |

| | Short Term | | A-2 | | P-2 | | F2 |

| | | | | | | | |

| | Local Currency | | | | | | |

| | Long Term | | BBB | | A3 | | BBB+ ** |

| | Short Term | | A-2 | | P-2 | | F2 |

| | | | | | | | |

| | National Scale | | | | | | |

| | Long Term | | mxAAA | | Aaa.mx | | AAA(mex) |

| | Short Term | | mxA-1+ | | Mx-1 | | F1+(mex) |

| | | | | | | | |

| | Deposit Certificates | | | | | | |

| | Long Term | | BBB | | | | |

| | Short Term | | A-3 | | | | |

| | | | | | | | |

| | Autonomous Credit Profile (SACP) | | bbb+ | | - | | - |

| | Rating viability (VR) | | - | | - | | bbb+ |

| | Support | | - | | - | | 2 |

| | Financial Strength | | - | | C- | | - |

| | Standalone BCA | | - | | baa1 | | - |

| | Outlook | | Stable | | Stable | | Stable |

| | | | | | | | |

| | Last publication: | | 22-Oct-12 | | 28-Jun-12 | | 13-Jun-12 |

| | ** Negative Outlook | | | | | | |

| | 4Q.12 | Earnings Report | 21 |

| |

|

| | | |

| | Brokerage - Casa de Bolsa Santander |

| | Ratings | | | | |

| | | | Moody´s | | Fitch Ratings |

| | Global Scale | | | | |

| | National Scale | | | | |

| | Long Term | | A3 | | _ |

| | Short Term | | Prime-2 | | _ |

| | | | | | |

| | National Scale | | | | |

| | Long Term | | Aaa.mx | | AAA.mx |

| | Short Term | | Mx-1 | | F1+mx |

| | | | | | |

| | Outlook | | Stable | | Stable |

October 22, 2012 Standard and Poor's affirmed Banco Santander (Mexico)'s ratings with stable outlook. Long Tem Global rating remains in "BBB" and "A-2" in short term. Currently the systemic importance was changed to "high" from "moderate"

4Q12 EARNINGS CALL DIAL-IN INFORMATION

| Date: | | Tuesday, February 19, 2013 |

| | | |

| Time: | | 8:00 AM (MCT); 9:00 AM (US ET) |

| | | |

| Dial-in Numbers: | | 1-877-941-4774 US & Canada; 1-480-629-9760 International & Mexico |

| | | |

| Access Code: | | 4595377 |

| | | |

| Webcast: | | https://viavid.webcasts.com/starthere.jsp?ei=1013104 |

| | | |

| Replay: | | Starting Tuesday, February, 19, 2013 at 12:00 PM (MCT); 01:00 PM (US ET), and ending on Tuesday, February 26, 2013 at 10:59 PM (MCT); 11:59 PM (US ET). |

| | | |

| | | Dial-in number: 1.877-870-5176 US & Canada; 1-858-384-5517 International & Mexico |

| | | |

| | | Access Code: 4595377 |

ANALYST COVERAGE

Bank of America Merrill Lynch, Barclays, BBVA Bancomer, Citi, Credit Suisse, Deutsche Bank, EVA Dimensions, GBM, Goldman Sachs, HSBC, Independent Research, JP Morgan, Morgan Stanley, Morningstar, Nau Securities, RBC, UBS and Vector.

Santander México is covered by the aforementioned analysts. Please note that any opinions, estimates or forecasts regarding the performance of Santander México issued by these analysts reflect their own views, and therefore do not represent the opinions, estimates or forecasts of Santander México or its management. Although Santander México may refer to or distribute such statements, this does not imply that Santander México agrees with or endorses any information, conclusions or recommendations included therein.

| | 4Q.12 | Earnings Report | 22 |

| |

|

| | | |

DEFINITION OF RATIOS

ROAE: Annualized net income divided by average equity

EFFICIENCY: Annualized administrative and promotional expenses divided by annualized gross operating income (before administrative and promotional expenses and net of allowances)

RECURRENCIA: Annualized net fees divided by annualized administrative and promotional expenses (net of amortizations and depreciations)

NIM: Financial margin divided by daily average interest earnings assets

ABOUT GRUPO FINANCIERO SANTANDER MEXICO, S.A.B. DE C.V. (NYSE: BSMX; BMV: SANMEX)

Grupo Financiero Santander Mexico, S.A.B. de C.V. (Santander Mexico), one of Mexico’s leading financial services holding companies, provides a wide range of financial and related services, including retail and commercial banking, securities brokerage, financial advisory and other related investment activities. Santander Mexico offers a multichannel financial services platform focused on mid- to high-income individuals and small- to medium-sized enterprises, while also providing integrated financial services to larger multinational companies in Mexico. As of December 31, 2012, Santander Mexico had total assets of Ps.750.3 billion under Mexican GAAP and more than 10.0 million customers. Headquartered in Mexico City, the Company operates 1,170 branches nationwide and has a total of 13,385 employees.

We, the undersigned under oath to tell the truth declare that, in the area of our corresponding functions, we prepared the information on Grupo Financiero Santander contained in this quarterly report, which to the best of our knowledge reasonably reflects its situation.

| MARCOS A. MARTINEZ GAVICA | | PEDRO JOSE MORENO CANTALEJO |

| | | |

| Executive President and Chief Executive Officer | | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | | JESÚS GONZÁLEZ DEL REAL | | JAVIER PLIEGO ALEGRÍA |

| | | | | |

Deputy General Director of Intervention and Control Management | | Executive Director – Controller | | Executive Director – Audit |

| | | |

| | The financial information presented in this report has been obtained from the non-audited financial statements prepared in accordance with the General Nature Provisions applicable to Holding Corporations of Financial Groups which are subject to the supervision of the National Banking and Securities Commission on accounting procedures, published in the Federal Official Gazette on January 31, 2011. The exchange rate used to convert foreign currency transactions to pesos is PPs.13.40840. | |

INVESTOR RELATIONS CONTACT

Gerardo Freire Alvarado

+ 52 (55) 5269-1827

investor@santander.com.mx

| | 4Q.12 | Earnings Report | 23 |

| |

|

| | | |

LEGAL DISCLAIMER

Grupo Financiero Santander México cautions that this report may contain forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements could be found in various places throughout this reports and include, without limitation, statements regarding our intent, belief, targets or current expectations in connection with: asset growth and sources of funding; growth of our fee-based business; expansion of our distribution network; our focus on strategic businesses; our compound annual growth rate; our risk, efficiency and profitability targets; financing plans; competition; impact of regulation; exposure to market risks including interest rate risk, foreign exchange risk and equity price risk; exposure to credit risks including credit default risk and settlement risk; projected capital expenditures; capitalization requirements and level of reserves; liquidity; trends affecting the economy generally; and trends affecting our financial condition and our results of operations. While these forward-looking statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to: changes in capital markets in general that may affect policies or attitudes towards lending to Mexico or Mexican companies; changes in economic conditions, in Mexico in particular, in the United States or globally; the monetary, foreign exchange and interest rate policies of the Mexican Central Bank (Banco de México); inflation; deflation; unemployment; unanticipated turbulence in interest rates; movements in foreign exchange rates; movements in equity prices or other rates or prices; changes in Mexican and foreign policies, legislation and regulations; changes in requirements to make contributions to, for the receipt of support from programs organized by or requiring deposits to be made or assessments observed or imposed by, the Mexican government; changes in taxes; competition, changes in competition and pricing environments; our inability to hedge certain risks economically; economic conditions that affect consumer spending and the ability of customers to comply with obligations; the adequacy of allowances for loans and other losses; increased default by borrowers; technological changes; changes in consumer spending and saving habits; increased costs; unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms; changes in, or failure to comply with, banking regulations; and certain other factors indicated in the “Risk Factors” section of our Registration Statement on Form F-1 (File No. 333-183409). The risk factors and other key factors that we have indicated in our past and future filings and reports, including those with the U.S. Securities and Exchange Commission, could adversely affect our business and financial performance.

Note: The information contained in this report is not audited. Nevertheless, the consolidated accounts are prepared on the basis of the accounting principles and regulations prescribed by the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores) for credit institutions, as amended (Mexican Banking GAAP). All figures presented are in nominal terms. Historical figures are not adjusted by inflation.

| | 4Q.12 | Earnings Report | 24 |

| |

|

| | | |

Grupo Financiero Santander México

| § | Consolidated Balance Sheet |

| § | Consolidated Statement of Income |

| § | Consolidated Statement of Changes in Stockholders’ Equity |

| § | Consolidated Statement of Cash Flows |

The information contained in this report and the financial statements of the Group’s subsidiaries may be consulted on the Internet website: www.santander.com.mx or through the following direct access:

http://www.santander.com.mx/ir/inf_financiera/inf_trimestral.html

There is also information on Santander on the CNBV Website: www.cnbv.gob.mx

| | 4Q.12 | Earnings Report | 25 |

| |

|

| | | |

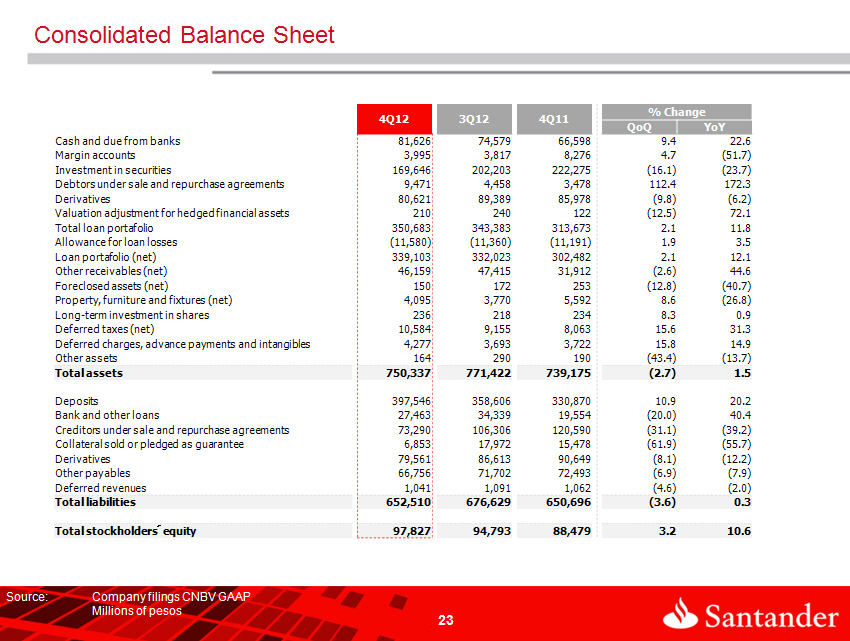

| Grupo Financiero Santander México | | | | | | | | | | | | | | | | | | | |

| Consolidated Balance Sheet | | | | | | | | | | | | | | | | | | | |

| Millions of Mexican Pesos | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | 2012 | | | | | | | | | | | | 2011 | |

| | | Dec | | | Sep | | | Jun | | | Mar | | | Dec | | | Sep | | | Jun | | | Mar | |

| Assets | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Cash and due from banks | | | 81,626 | | | | 74,579 | | | | 77,019 | | | | 60,747 | | | | 66,598 | | | | 73,705 | | | | 93,387 | | | | 84,009 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Margin accounts | | | 3,995 | | | | 3,817 | | | | 4,534 | | | | 4,187 | | | | 8,276 | | | | 8,544 | | | | 8,261 | | | | 7,719 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Investment in securities | | | 169,646 | | | | 202,203 | | | | 262,988 | | | | 269,692 | | | | 222,275 | | | | 231,358 | | | | 237,578 | | | | 207,456 | |

| Trading securities | | | 117,183 | | | | 142,175 | | | | 203,249 | | | | 202,830 | | | | 155,953 | | | | 180,087 | | | | 185,997 | | | | 147,642 | |

| Securities available for sale | | | 47,373 | | | | 54,996 | | | | 54,764 | | | | 61,944 | | | | 61,461 | | | | 46,467 | | | | 46,831 | | | | 55,119 | |

| Securities held to maturity | | | 5,090 | | | | 5,032 | | | | 4,975 | | | | 4,918 | | | | 4,861 | | | | 4,804 | | | | 4,750 | | | | 4,695 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Debtors under sale and repurchase agreements | | | 9,471 | | | | 4,458 | | | | 4,827 | | | | 4,484 | | | | 3,478 | | | | 25,515 | | | | 7,262 | | | | 6,655 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Derivatives | | | 80,621 | | | | 89,389 | | | | 87,857 | | | | 71,991 | | | | 85,978 | | | | 110,516 | | | | 79,999 | | | | 70,483 | |

| Trading purposes | | | 80,321 | | | | 88,945 | | | | 87,286 | | | | 71,276 | | | | 85,081 | | | | 109,441 | | | | 78,500 | | | | 69,329 | |

| Hedging purposes | | | 300 | | | | 444 | | | | 571 | | | | 715 | | | | 897 | | | | 1,075 | | | | 1,499 | | | | 1,154 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Valuation adjustment for hedged financial assets | | | 210 | | | | 240 | | | | 220 | | | | 139 | | | | 122 | | | | 141 | | | | 86 | | | | (12 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Performing loan portfolio | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Commercial loans | | | 214,445 | | | | 211,685 | | | | 212,492 | | | | 198,276 | | | | 197,772 | | | | 197,465 | | | | 183,059 | | | | 175,304 | |

| Commercial or business activity | | | 175,329 | | | | 175,945 | | | | 176,332 | | | | 163,630 | | | | 162,419 | | | | 162,162 | | | | 148,546 | | | | 152,482 | |

| Financial entities loans | | | 407 | | | | 619 | | | | 606 | | | | 1,934 | | | | 1,975 | | | | 3,306 | | | | 4,542 | | | | 4,043 | |

| Government entities loans | | | 38,709 | | | | 35,121 | | | | 35,554 | | | | 32,712 | | | | 33,378 | | | | 31,997 | | | | 29,971 | | | | 18,779 | |

| Consumer loans | | | 61,603 | | | | 59,996 | | | | 57,043 | | | | 52,857 | | | | 49,342 | | | | 47,101 | | | | 43,683 | | | | 40,242 | |

| Mortage loans | | | 68,542 | | | | 66,172 | | | | 64,417 | | | | 62,559 | | | | 61,243 | | | | 58,853 | | | | 56,954 | | | | 36,124 | |

| Total performing loan portafolio | | | 344,590 | | | | 337,853 | | | | 333,952 | | | | 313,692 | | | | 308,357 | | | | 303,419 | | | | 283,696 | | | | 251,670 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Nonperforming loan portafolio | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Commercial loans | | | 1,523 | | | | 1,402 | | | | 1,313 | | | | 1,135 | | | | 1,928 | | | | 3,233 | | | | 1,758 | | | | 1,752 | |

| Commercial or business activity | | | 1,523 | | | | 1,402 | | | | 1,313 | | | | 1,135 | | | | 1,926 | | | | 1,840 | | | | 1,758 | | | | 1,752 | |

| Government entities loans | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 2 | | | | 1,393 | | | | 0 | | | | 0 | |

| Consumer loans | | | 2,236 | | | | 2,053 | | | | 1,709 | | | | 1,255 | | | | 1,270 | | | | 1,232 | | | | 1,321 | | | | 1,131 | |

| Mortage loans | | | 2,334 | | | | 2,075 | | | | 1,931 | | | | 1,982 | | | | 2,118 | | | | 2,245 | | | | 3,690 | | | | 569 | |

| Total nonperforming portafolio | | | 6,093 | | | | 5,530 | | | | 4,953 | | | | 4,372 | | | | 5,316 | | | | 6,710 | | | | 6,769 | | | | 3,452 | |

| Total loan portafolio | | | 350,683 | | | | 343,383 | | | | 338,905 | | | | 318,064 | | | | 313,673 | | | | 310,129 | | | | 290,465 | | | | 255,122 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Allowance for loan losses | | | (11,580 | ) | | | (11,360 | ) | | | (11,101 | ) | | | (10,875 | ) | | | (11,191 | ) | | | (10,906 | ) | | | (12,892 | ) | | | (10,449 | ) |

| Loan portafolio (net) | | | 339,103 | | | | 332,023 | | | | 327,804 | | | | 307,189 | | | | 302,482 | | | | 299,223 | | | | 277,573 | | | | 244,673 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other receivables (net) | | | 46,159 | | | | 47,415 | | | | 55,932 | | | | 47,009 | | | | 31,912 | | | | 38,757 | | | | 32,063 | | | | 41,151 | |

| Foreclosed assets (net) | | | 150 | | | | 172 | | | | 196 | | | | 220 | | | | 253 | | | | 290 | | | | 305 | | | | 155 | |

| Property, furniture and fixtures (net) | | | 4,095 | | | | 3,770 | | | | 3,780 | | | | 5,439 | | | | 5,592 | | | | 5,166 | | | | 5,238 | | | | 5,340 | |

| Long-term investment in shares | | | 236 | | | | 218 | | | | 203 | | | | 251 | | | | 234 | | | | 218 | | | | 206 | | | | 226 | |

| Deferred taxes (net) | | | 10,584 | | | | 9,155 | | | | 8,425 | | | | 8,255 | | | | 8,063 | | | | 8,735 | | | | 8,722 | | | | 7,687 | |

| Deferred charges, advance payments and intangibles | | | 4,277 | | | | 3,693 | | | | 3,793 | | | | 4,148 | | | | 3,722 | | | | 3,893 | | | | 3,944 | | | | 2,278 | |

| Other assets | | | 164 | | | | 290 | | | | 221 | | | | 197 | | | | 190 | | | | 320 | | | | 305 | | | | 299 | |

| Discontinued operations | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 10,511 | | | | 10,702 | | | | 9,817 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total assets | | | 750,337 | | | | 771,422 | | | | 837,799 | | | | 783,948 | | | | 739,175 | | | | 816,892 | | | | 765,631 | | | | 687,936 | |

| | 4Q.12 | Earnings Report | 26 |

| |

|

| | | |

| Grupo Financiero Santander México | | | | | | | | | | | | | | | | | | | |

| Consolidated Balance Sheet | | | | | | | | | | | | | | | | | | | |

| Millions of Mexican Pesos | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | 2012 | | | | | | | | | | | | 2011 | |

| | | Dec | | | Sep | | | Jun | | | Mar | | | Dec | | | Sep | | | Jun | | | Mar | |

| Liabilities | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Deposits | | | 397,546 | | | | 358,606 | | | | 352,753 | | | | 346,605 | | | | 330,870 | | | | 328,327 | | | | 316,729 | | | | 286,455 | |

| Demand deposits | | | 210,915 | | | | 194,351 | | | | 204,606 | | | | 187,787 | | | | 178,065 | | | | 166,923 | | | | 155,932 | | | | 151,450 | |

| Time deposits – General Public | | | 125,584 | | | | 120,034 | | | | 117,184 | | | | 122,816 | | | | 114,720 | | | | 122,130 | | | | 110,968 | | | | 106,774 | |

| Time deposits – Money market | | | 25,953 | | | | 21,904 | | | | 9,085 | | | | 14,507 | | | | 16,409 | | | | 18,823 | | | | 32,745 | | | | 11,405 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Credit instruments issued | | | 35,094 | | | | 22,317 | | | | 21,878 | | | | 21,495 | | | | 21,676 | | | | 20,451 | | | | 17,084 | | | | 16,826 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Bank and other loans | | | 27,463 | | | | 34,339 | | | | 24,804 | | | | 21,372 | | | | 19,554 | | | | 36,158 | | | | 23,627 | | | | 17,726 | |

| Demand loans | | | 8,240 | | | | 5,916 | | | | 6,851 | | | | 5,949 | | | | 2,371 | | | | 20,326 | | | | 10,293 | | | | 7,308 | |

| Short-term loans | | | 16,767 | | | | 26,092 | | | | 15,704 | | | | 13,278 | | | | 15,156 | | | | 13,772 | | | | 11,187 | | | | 8,310 | |

| Long-term loans | | | 2,456 | | | | 2,331 | | | | 2,249 | | | | 2,145 | | | | 2,027 | | | | 2,060 | | | | 2,147 | | | | 2,108 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Creditors under sale and repurchase agreements | | | 73,290 | | | | 106,306 | | | | 168,227 | | | | 189,299 | | | | 120,590 | | | | 157,221 | | | | 162,609 | | | | 129,442 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Collateral sold or pledged as guarantee | | | 6,853 | | | | 17,972 | | | | 18,766 | | | | 14,104 | | | | 15,478 | | | | 17,896 | | | | 15,820 | | | | 24,246 | |

| Securities loans | | | 6,853 | | | | 17,972 | | | | 18,766 | | | | 14,104 | | | | 15,478 | | | | 17,896 | | | | 15,820 | | | | 24,246 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Derivatives | | | 79,561 | | | | 86,613 | | | | 87,960 | | | | 70,292 | | | | 90,649 | | | | 114,399 | | | | 78,362 | | | | 65,948 | |

| Trading purposes | | | 77,939 | | | | 85,209 | | | | 86,233 | | | | 69,266 | | | | 88,148 | | | | 111,929 | | | | 78,198 | | | | 65,861 | |

| Hedging purposes | | | 1,622 | | | | 1,404 | | | | 1,727 | | | | 1,026 | | | | 2,501 | | | | 2,470 | | | | 164 | | | | 87 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other payables | | | 66,756 | | | | 71,702 | | | | 88,648 | | | | 47,647 | | | | 72,493 | | | | 63,114 | | | | 72,706 | | | | 69,844 | |

| Income taxes payable | | | 503 | | | | 767 | | | | 335 | | | | 910 | | | | 507 | | | | 779 | | | | 928 | | | | 7 | |

| Employee profit sharing payable | | | 172 | | | | 117 | | | | 83 | | | | 62 | | | | 153 | | | | 6 | | | | 5 | | | | 40 | |

| Creditors from settlement of transactions | | | 38,604 | | | | 47,308 | | | | 52,492 | | | | 24,013 | | | | 28,579 | | | | 28,744 | | | | 47,883 | | | | 50,194 | |

| Sundry creditors and other payables | | | 27,477 | | | | 23,510 | | | | 35,738 | | | | 22,662 | | | | 43,254 | | | | 33,585 | | | | 23,890 | | | | 19,603 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Deferred revenues | | | 1,041 | | | | 1,091 | | | | 1,096 | | | | 1,385 | | | | 1,062 | | | | 1,135 | | | | 1,160 | | | | 1,534 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Discontinued operations | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 8,496 | | | | 8,872 | | | | 8,142 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total liabilities | | | 652,510 | | | | 676,629 | | | | 742,254 | | | | 690,704 | | | | 650,696 | | | | 726,746 | | | | 679,885 | | | | 603,337 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Paid in capital | | | 47,776 | | | | 47,776 | | | | 48,195 | | | | 48,195 | | | | 48,195 | | | | 48,195 | | | | 48,195 | | | | 48,195 | |

| Capital stock | | | 36,357 | | | | 36,357 | | | | 36,357 | | | | 36,357 | | | | 36,357 | | | | 36,357 | | | | 36,357 | | | | 36,357 | |

| Share premium | | | 11,419 | | | | 11,419 | | | | 11,838 | | | | 11,838 | | | | 11,838 | | | | 11,838 | | | | 11,838 | | | | 11,838 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other capital | | | 50,051 | | | | 47,017 | | | | 47,350 | | | | 45,049 | | | | 40,284 | | | | 41,951 | | | | 37,551 | | | | 36,404 | |

| Capital reserves | | | 349 | | | | 349 | | | | 349 | | | | 108 | | | | 108 | | | | 108 | | | | 108 | | | | 108 | |

| Retained earnings | | | 31,103 | | | | 31,038 | | | | 35,311 | | | | 38,541 | | | | 19,828 | | | | 28,633 | | | | 28,781 | | | | 31,276 | |

| Result from valuation of securities available for sale, net | | | 678 | | | | 727 | | | | 688 | | | | 442 | | | | 465 | | | | 917 | | | | 515 | | | | 314 | |

| Result from valuation of cash flow hedge instruments, net | | | 90 | | | | 382 | | | | 690 | | | | 932 | | | | 1,188 | | | | 1,340 | | | | 1,317 | | | | 1,242 | |

| Net income | | | 17,822 | | | | 14,512 | | | | 10,298 | | | | 5,013 | | | | 18,682 | | | | 10,941 | | | | 6,818 | | | | 3,452 | |

| Non-controlling interest | | | 9 | | | | 9 | | | | 14 | | | | 13 | | | | 13 | | | | 12 | | | | 12 | | | | 12 | |

| Total stockholders´equity | | | 97,827 | | | | 94,793 | | | | 95,545 | | | | 93,244 | | | | 88,479 | | | | 90,146 | | | | 85,746 | | | | 84,599 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Total liabilities and stockholders´ equity | | | 750,337 | | | | 771,422 | | | | 837,799 | | | | 783,948 | | | | 739,175 | | | | 816,892 | | | | 765,631 | | | | 687,936 | |

| | 4Q.12 | Earnings Report | 27 |

| |

|

| | | |

| Grupo Financiero Santander México | | | | | | | | | | | | | | | | | | | |

| Consolidated Balance Sheet | | | | | | | | | | | | | | | | | | | |

| Millions of Mexican Pesos | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | 2012 | | | | | | | | | | | | 2011 | |

| | | Dec | | | Sep | | | Jun | | | Mar | | | Dec | | | Sep | | | Jun | | | Mar | |