Santander Mexico Financial Group, S.A.B. de C.V. Inactive

Filed: 31 Jul 13, 12:00am

| Form 20-F | X | Form 40-F |

| Yes | No | X |

| Yes | No | X |

| ITEM | |

| 1. | Second quarter 2013 earnings report of Grupo Financiero Santander México, S.A.B. de C.V. |

| 2. | Second quarter 2013 earnings presentation of Grupo Financiero Santander México, S.A.B. de C.V. |

| 3. | Complementary information of Grupo Financiero Santander México, S.A.B. de C.V. for the second quarter of 2013, in compliance with the obligation to report transactions with derivative financial instruments |

GRUPO FINANCIERO SANTANDER MÉXICO, S.A.B. de C.V. | |||||

| By: | /s/ Eduardo Fernández García-Travesí | ||||

| Name: | Eduardo Fernández García-Travesí | ||||

| Title: | General Counsel | ||||

| I. | CEO Message / Key Highlights for the Quarter |

| II. | Summary of 2Q13 Consolidated Results |

| III. | Analysis of 2Q13 Consolidated Results |

| IV. | Relevant Events & Representative Activities and Transactions |

| V. | Credit Ratings |

| VI. | 2Q13 Earnings Call Dial-In Information |

| VII. | Financial Statements |

| VIII. | Notes to the Financial Statements |

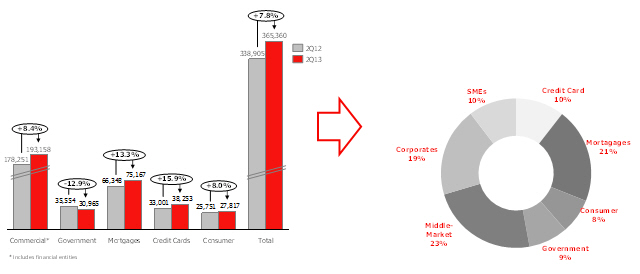

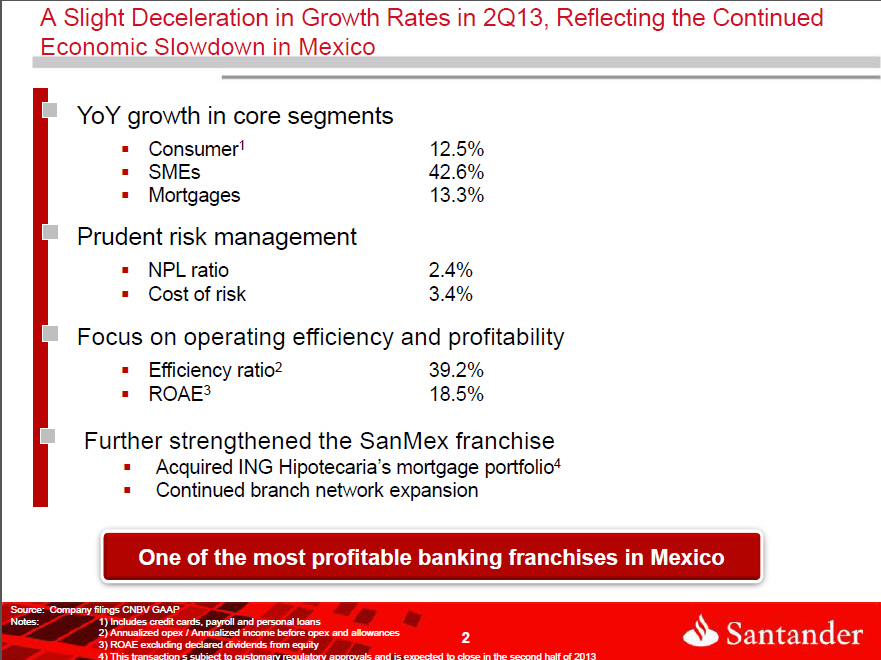

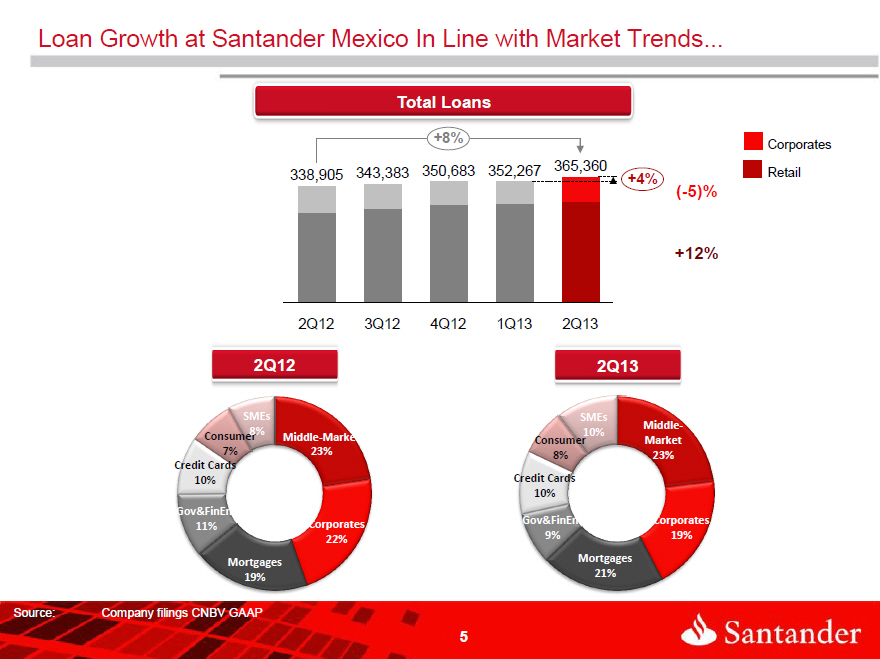

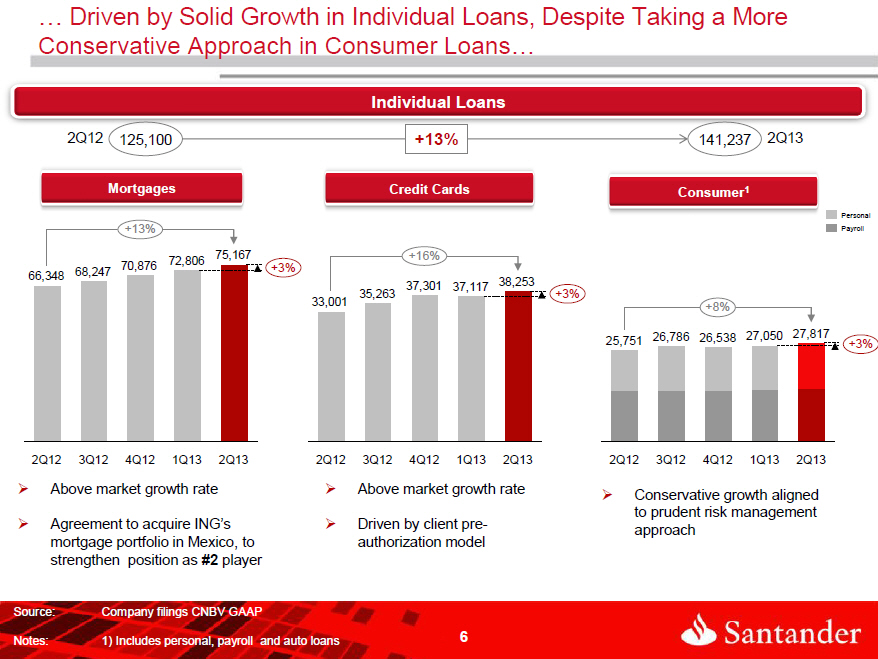

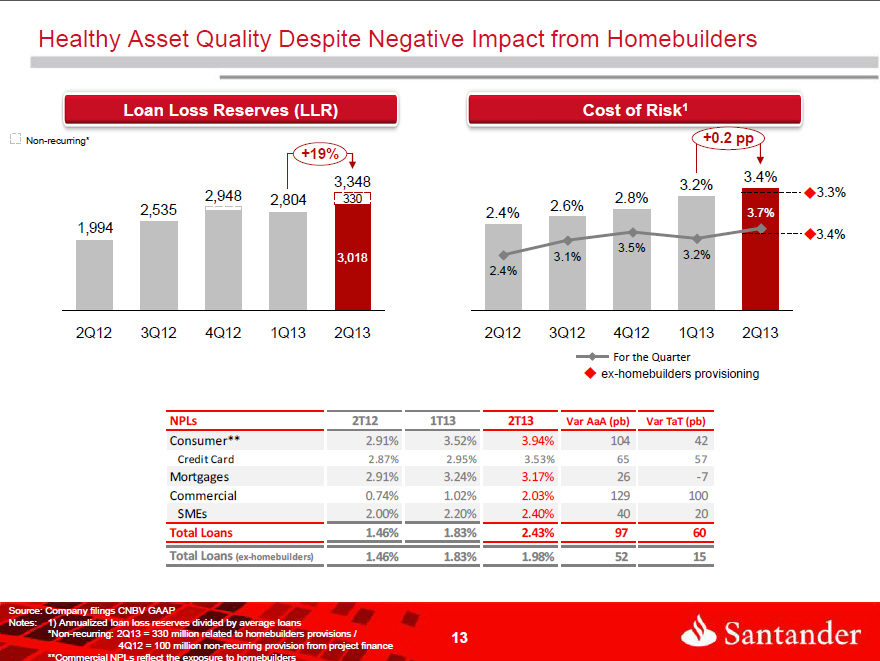

| - | Strong loan growth with YoY increases of 42.6% in SMEs, 15.9% in credit cards, 8.0% in consumer loans, and 13.3% in mortgages |

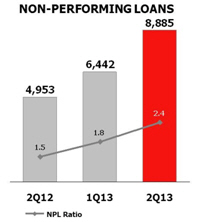

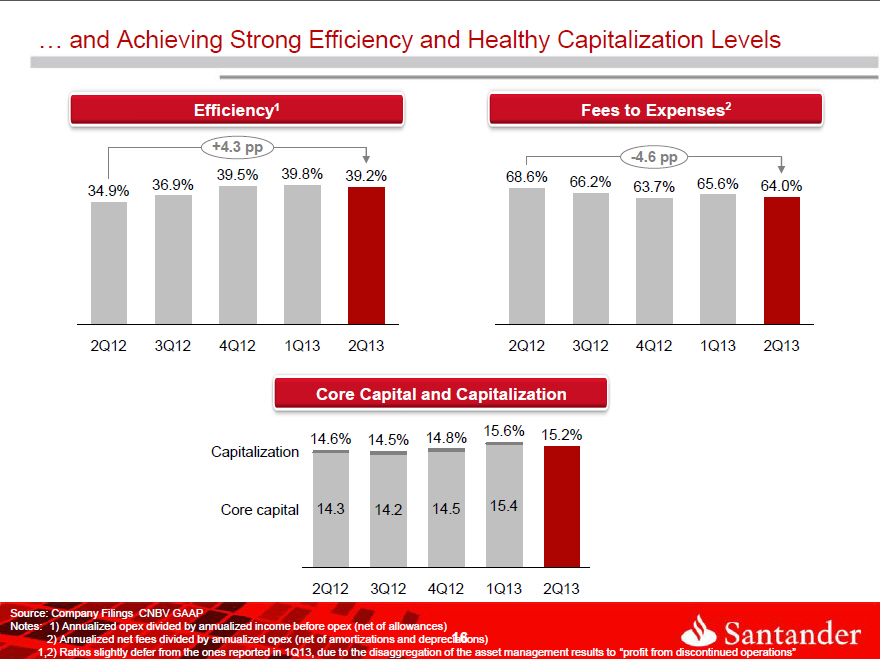

| - | Continued prudent risk management demonstrated by an NPL ratio of 2.4% and cost of risk of 3.4% |

| - | Ongoing emphasis on operational efficiency reflected in a 39.2% ratio |

| Grupo Financiero Santander | |||||||||

| Earnings Contribution by Subsidiary | |||||||||

| Millions of Mexican Pesos | |||||||||

| % Variation | |||||||||

| 2Q13 | 1Q13 | 2Q12 | 2013 | 2012 | YoY % | ||||

| Banking business1/ | 4,239 | 4,574 | 5,242 | 8,813 | 10,112 | (12.8) | |||

| Brokerage | 41 | 101 | 12 | 142 | 100 | 42.0 | |||

| Holding and other subsidiaries2/ | (137) | 42 | 31 | (95) | 86 | (210.5) | |||

| Net income attributable to Grupo Financiero Santander | 4,143 | 4,717 | 5,285 | 8,860 | 10,298 | (14.0) |

| 1/ Includes Sofomers 2/ Asset management subsidiary and Holding. | |||||||||

| Grupo Financiero Santander México | |||||||||

| Income Statement | |||||||||

| Millions of Mexican Pesos | % Change | % Change | |||||||

| 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | 2013 | 2012 | 13/12 | ||

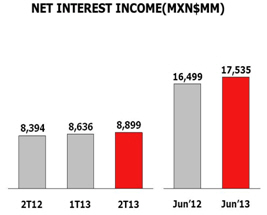

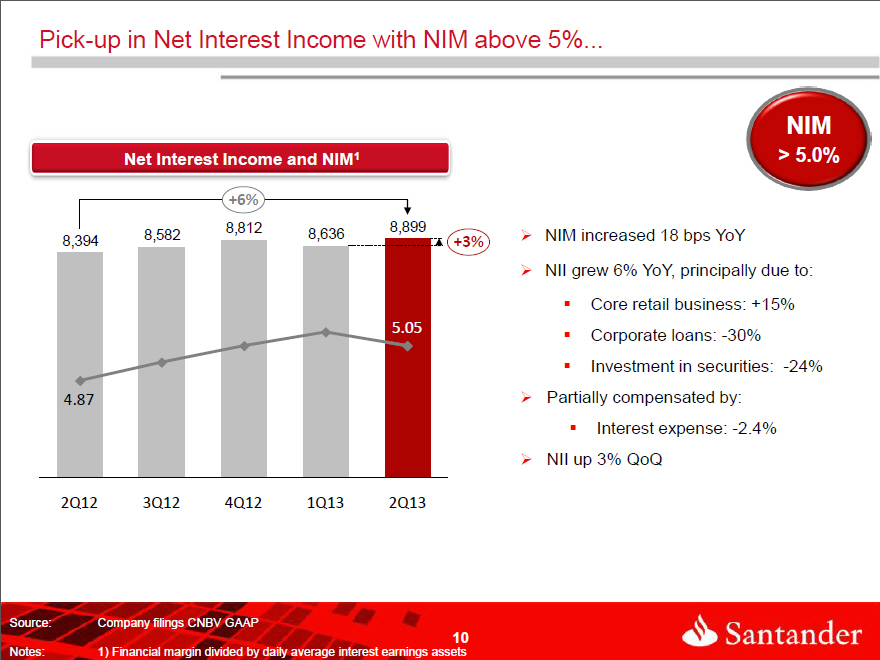

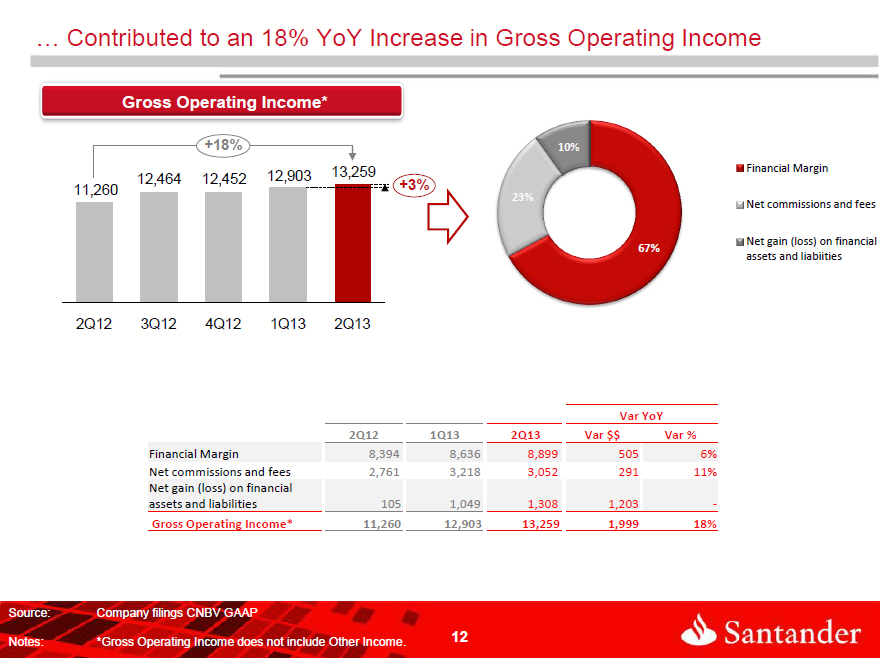

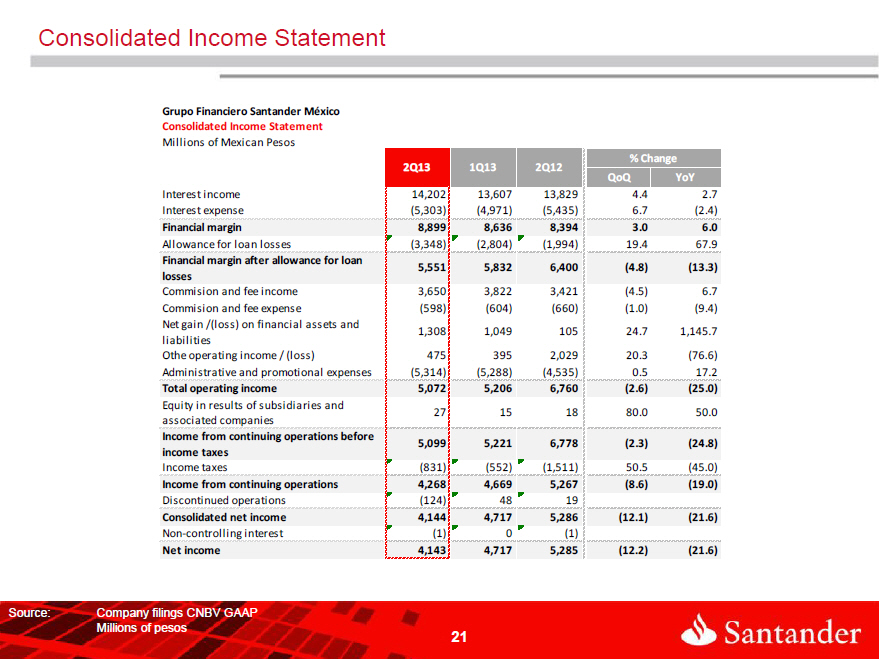

| Net interest income | 8,899 | 8,636 | 8,394 | 3.0 | 6.0 | 17,535 | 16,499 | 6.3 | |

| Provision for loan losses | (3,348) | (2,804) | (1,994) | (19.4) | (67.9) | (6,152) | (3,962) | (55.3) | |

| Net interest income after provisions for loan losses | 5,551 | 5,832 | 6,400 | (4.8) | (13.3) | 11,383 | 12,537 | (9.2) | |

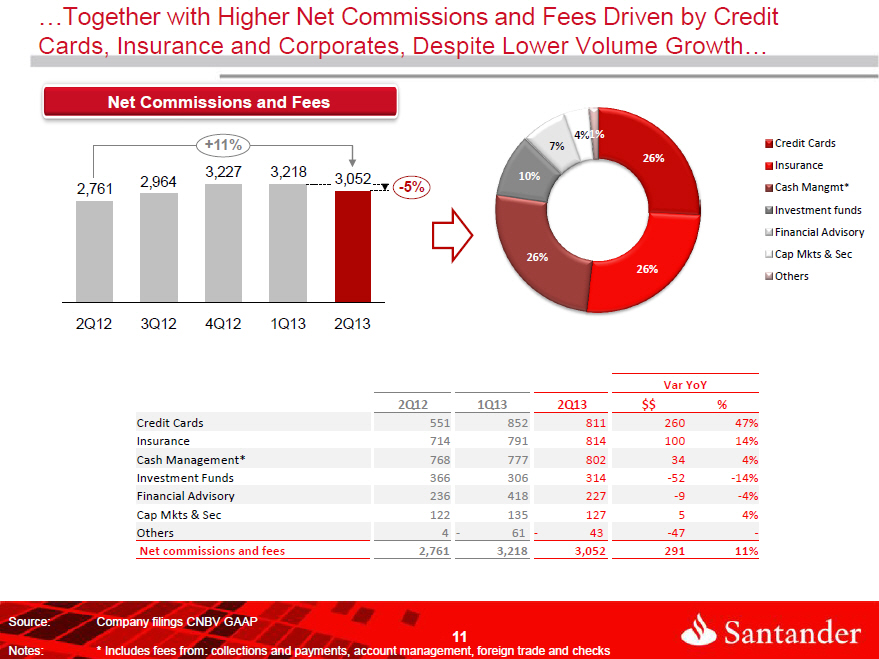

| Commission and fee income, net | 3,052 | 3,218 | 2,761 | (5.2) | 10.5 | 6,270 | 5,652 | 10.9 | |

| Gains (losses) on financial assets and liabilities | 1,308 | 1,049 | 105 | 24.7 | 1,145.7 | 2,357 | 858 | 174.7 | |

| Other operating income (expenses) | 475 | 395 | 2,029 | 20.3 | (76.6) | 870 | 2,722 | (68.0) | |

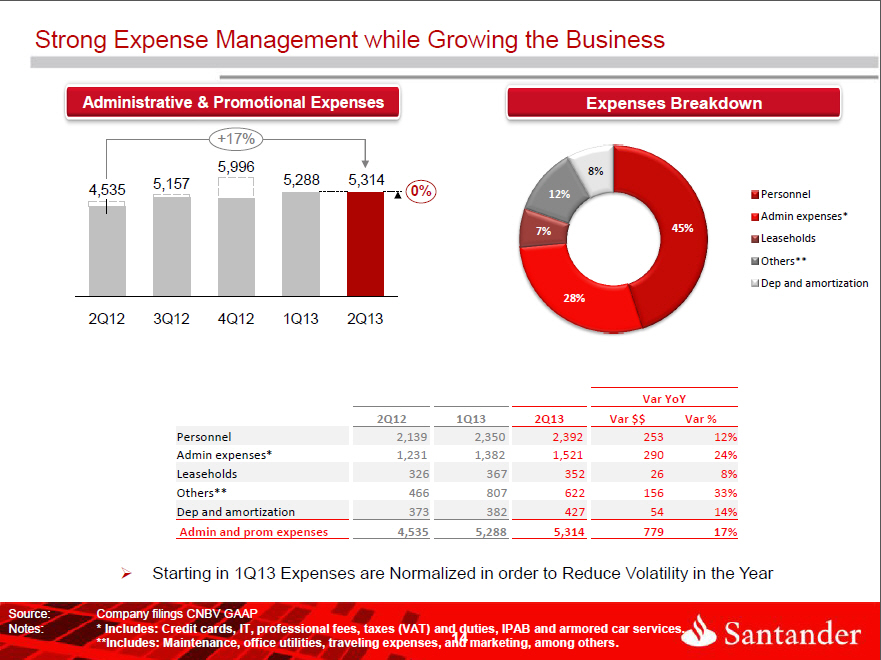

| Administrative and promotional expenses | (5,314) | (5,288) | (4,535) | (0.5) | (17.2) | (10,602) | (8,986) | (18.0) | |

| Operating income | 5,072 | 5,206 | 6,760 | (2.6) | (25.0) | 10,278 | 12,783 | (19.6) | |

| Equity in results of associated companies | 27 | 15 | 18 | 80.0 | 50.0 | 42 | 35 | 20.0 | |

| Operating income before taxes | 5,099 | 5,221 | 6,778 | (2.3) | (24.8) | 10,320 | 12,818 | (19.5) | |

| Current and deferred income taxes | (831) | (552) | (1,511) | (50.5) | 45.0 | (1,383) | (2,557) | 45.9 | |

| Income from continuing operations | 4,268 | 4,669 | 5,267 | (8.6) | (19.0) | 8,937 | 10,261 | (12.9) | |

| Profit from discontinued operations, net | (124) | 48 | 19 | (358.3) | (752.6) | (76) | 38 | (300.0) | |

| Non-controlling interest | (1) | 0 | (1) | 0.0 | 0.0 | (1) | (1) | 0.0 | |

| Net income | 4,143 | 4,717 | 5,285 | (12.2) | (21.6) | 8,860 | 10,298 | (14.0) | |

| · | Ps.330 million of provisions related to the exposure to homebuilders; |

| · | Ps.178 million after tax, related to a price adjustment made to the sale of the insurance business to Zurich, which was registered in the income statement line of profit from discontinued operations; and |

| · | Ps.142 million related to the branch expansion |

| · | Ps.1,731 million non-recurring gain from the sale and leaseback of the 220 branches; and |

| · | Ps.260 million resulting from normalizing expenses to make this line comparable with the methodology adopted in 2013 |

| Grupo Financiero Santander México | ||||||||

| Net Income Adjustments | ||||||||

| Million Pesos | % Change | % Change | ||||||

| 2Q13 | 1Q13 | 2Q12 | YoY | QoQ | ||||

| Net income | 4,143 | 4,717 | 5,285 | (21.6) | (12.2) | |||

| Sale and leaseback of branches | (1,731) | |||||||

| Zurich price adjustment | 178 | |||||||

| Provisions related to homebuilders | 330 | |||||||

| Expenses regularization | (260) | |||||||

| Branch expansion | 142 | 135 | ||||||

| Adjusted net income (before taxes) | 4,793 | 4,852 | 3,294 | |||||

| Taxes on written-off portfolio sale | (250) | |||||||

| Taxes | (142) | (41) | 597 | |||||

| Adjusted net income | 4,651 | 4,562 | 3,891 | 19.5 | 2.0 |

| Grupo Financiero Santander México | |||||||||

| Net Interest Income | |||||||||

| Millions of Mexican Pesos | % Change | % Change | |||||||

| 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | 2013 | 2012 | 13/12 | ||

| Funds Available | 551 | 574 | 618 | (4.0) | (10.8) | 1,125 | 1,274 | (11.7) | |

| Margin accounts | 94 | 96 | 106 | (2.1) | (11.3) | 190 | 213 | (10.8) | |

| Interest from investment in securities | 2,599 | 2,029 | 3,432 | 28.1 | (24.3) | 4,628 | 6,561 | (29.5) | |

| Loan portfolio – excluding credit cards | 7,521 | 7,529 | 7,083 | (0.1) | 6.2 | 15,050 | 13,862 | 8.6 | |

| Credit card loan portfolio | 2,343 | 2,317 | 1,975 | 1.1 | 18.6 | 4,660 | 3,802 | 22.6 | |

| Loan origination fees | 217 | 190 | 160 | 14.2 | 35.6 | 407 | 331 | 23.0 | |

| Sale and repurchase agreements | 877 | 872 | 455 | 0.6 | 92.7 | 1,749 | 1,213 | 44.2 | |

| Interest Income | 14,202 | 13,607 | 13,829 | 4.4 | 2.7 | 27,809 | 27,256 | 2.0 | |

| Average Earning Asset* | 694,266 | 676,938 | |||||||

| Customer deposits – Demand deposits | (685) | (602) | (566) | (13.8) | (21.0) | (1,287) | (1,062) | (21.2) | |

| Customer deposits – Time deposits | (1,439) | (1,451) | (1,361) | 0.8 | (5.7) | (2,890) | (2,726) | (6.0) | |

| Credit instruments issued | (341) | (465) | (296) | 26.7 | (15.2) | (806) | (592) | (36.1) | |

| Interbank loans | (165) | (177) | (156) | 6.8 | (5.8) | (342) | (293) | (16.7) | |

| Sale and repurchase agreements | (2,673) | (2,276) | (3,056) | (17.4) | 12.5 | (4,949) | (6,084) | 18.7 | |

| Interest Expense | (5,303) | (4,971) | (5,435) | (6.7) | 2.4 | (10,274) | (10,757) | 4.5 | |

| Net Interest Income | 8,899 | 8,636 | 8,394 | 3.0 | 6.0 | 17,535 | 16,499 | 6.3 | |

| *Includes Funds Available, Margin Accounts, Investment in securities, Loan portfolio, Repurchase Agreements |

| Grupo Financiero Santander México | ||||||||

| Loan Portfolio Breakdown | ||||||||

| Millions of Mexican Pesos | 2Q13 | % | 1Q13 | % | 2Q12 | % | ||

| Commercial | 189,259 | 51.8% | 175,830 | 49.9% | 176,938 | 52.2% | ||

| Government | 30,965 | 8.5% | 37,641 | 10.7% | 35,554 | 10.5% | ||

| Consumer | 63,464 | 17.4% | 61,906 | 17.6% | 57,043 | 16.8% | ||

| Credit cards | 36,904 | 10.1% | 36,022 | 10.2% | 32,053 | 9.5% | ||

| Other consumer | 26,560 | 7.3% | 5,884 | 7.3% | 24,991 | 7.4% | ||

| Mortgages | 72,787 | 19.9% | 70,448 | 20.0% | 64,417 | 19.0% | ||

| Total Performing Loan | 356,474 | 97.6% | 345,825 | 98.2% | 333,952 | 98.5% | ||

| Commercial | 3,899 | 1.1% | 1,815 | 0.5% | 1,313 | 0.4% | ||

| Government | 0 | 0.0% | 8 | 0.0% | 0 | 0.0% | ||

| Consumer | 2,606 | 0.7% | 2,261 | 0.6% | 1,709 | 0.5% | ||

| Credit cards | 1,349 | 0.4% | 1,096 | 0.3% | 948 | 0.3% | ||

| Other consumer | 1,257 | 0.3% | 1,165 | 0.3% | 761 | 0.2% | ||

| Mortgages | 2,380 | 0.7% | 2,358 | 0.7% | 1,931 | 0.6% | ||

| Total Non-Performing Loan | 8,885 | 2.4% | 6,442 | 1.8% | 4,953 | 1.5% | ||

| Total Loan Portfolio | 365,359 | 100.0% | 352,267 | 100.0% | 338,905 | 100.0% |

| Grupo Financiero Santander México | ||||||

| Asset Quality | ||||||

| Millions of Mexican Pesos | ||||||

| Change % | ||||||

| 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | ||

| Total Loans | 365,360 | 352,267 | 338,905 | 3.72% | 7.81% | |

| Performing Loans | 356,475 | 345,825 | 333,952 | 3.08% | 6.74% | |

| Non-performing Loans | 8,885 | 6,442 | 4,953 | 37.92% | 79.39% | |

| Allowance for loan losses | (15,989) | (11,954) | (11,101) | 33.75% | 44.03% | |

| Non-performing loan ratio | 2.43% | 1.83% | 1.46% | 60bps | 97bps | |

| Coverage ratio | 180.0 | 185.6 | 224.1 | (561)bps | (4,417)bps | |

| Grupo Financiero Santander México | |||||||||

| Net Commission and Fee Income | |||||||||

| Millions of Mexican Pesos | |||||||||

| % Change | % Change | ||||||||

| Commission and fee income | 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | 2013 | 2012 | 13/12 | |

| Credit and debit cards | 1,072 | 1,037 | 926 | 3.4 | 15.8 | 2,109 | 1,790 | 17.8 | |

| Cash management | 179 | 170 | 179 | 5.3 | 0.0 | 349 | 350 | (0.3) | |

| Collection and payment services | 399 | 391 | 365 | 2.0 | 9.3 | 790 | 736 | 7.3 | |

| Investment fund management | 330 | 323 | 381 | 2.2 | (13.4) | 653 | 756 | (13.6) | |

| Insurance | 840 | 818 | 737 | 2.7 | 14.0 | 1,658 | 1,410 | 17.6 | |

| Capital markets and securities activities | 186 | 170 | 162 | 9.4 | 14.8 | 356 | 317 | 12.3 | |

| Checks | 82 | 82 | 89 | 0.0 | (7.9) | 164 | 179 | (8.4) | |

| Foreign trade | 153 | 146 | 144 | 4.8 | 6.3 | 299 | 271 | 10.3 | |

| Financial advisory services | 232 | 500 | 245 | (53.6) | (5.3) | 732 | 641 | 14.2 | |

| Other commissions and fees | 177 | 185 | 193 | (4.3) | (8.3) | 362 | 389 | (6.9) | |

| Total | 3,650 | 3,822 | 3,421 | (4.5) | 6.7 | 7,472 | 6,839 | 9.3 | |

| Commission and fee expense | |||||||||

| Credit and debit cards | (261) | (185) | (375) | (41.1) | 30.4 | (446) | (662) | 32.6 | |

| Investment fund management | (16) | (17) | (15) | 5.9 | (6.7) | (33) | (29) | (13.8) | |

| Insurance | (26) | (27) | (23) | 3.7 | (13.0) | (53) | (45) | (17.8) | |

| Capital markets and securities activities | (59) | (35) | (40) | (68.6) | (47.5) | (94) | (75) | (25.3) | |

| Checks | (8) | (8) | (9) | 0.0 | 11.1 | (16) | (18) | 11.1 | |

| Foreign trade | (3) | (4) | 0 | 25.0 | 0.0 | (7) | 0 | 0.0 | |

| Financial advisory services | (5) | (82) | (9) | 93.9 | 44.4 | (87) | (19) | (357.9) | |

| Other commissions and fees | (220) | (246) | (189) | 10.6 | (16.4) | (466) | (339) | (37.5) | |

| Total | (598) | (604) | (660) | 1.0 | 9.4 | (1,202) | (1,187) | (1.3) | |

| Commission and Fee Income, net | 3,052 | 3,218 | 2,761 | (5.2) | 10.5 | 6,270 | 5,652 | 10.9 | |

| Grupo Financiero Santander México | |||||||||

| Net gain (loss) on financial assets and liabilities | |||||||||

| Millions of Mexican Pesos | % Change | % Change | |||||||

| 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | 2013 | 2012 | 13/12 | ||

| Valuation | |||||||||

| Foreign currencies | 231 | (78) | 15 | 396.2 | 1,440.0 | 153 | 29 | 427.6 | |

| Derivatives | (3,447) | (801) | (541) | (330.3) | (537.2) | (4,248) | 6 | (70,900.0) | |

| Shares | (545) | (106) | 220 | (414.2) | (347.7) | (651) | 111 | (686.5) | |

| Debt instruments | (1,921) | 2,314 | 435 | (183.0) | (541.6) | 393 | 500 | (21.4) | |

| Subtotal | (5,682) | 1,329 | 129 | (527.5) | (4,504.7) | (4,353) | 646 | (773.8) | |

| Trading | |||||||||

| Foreign currencies | 242 | 36 | 659 | 572.2 | (63.3) | 278 | 338 | (17.8) | |

| Derivatives | 6,078 | 1,028 | (1,017) | 491.2 | 697.6 | 7,106 | (649) | 1,194.9 | |

| Shares | (575) | 455 | 273 | (226.4) | (310.6) | (120) | 587 | (120.4) | |

| Debt instruments | 1,245 | (1,799) | 61 | 169.2 | 1,941.0 | (554) | (64) | (765.6) | |

| Subtotal | 6,990 | (280) | (24) | 2,596.4 | 29,225.0 | 6,710 | 212 | 3,065.1 | |

| Total | 1,308 | 1,049 | 105 | 24.7 | 1,146 | 2,357 | 858 | 174.7 | |

| Grupo Financiero Santander México | |||||||||

| Other Operating Income (Expense) | |||||||||

| Millions of Mexican Pesos | % Change | % Change | |||||||

| 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | 2013 | 2012 | 13/12 | ||

| Recoveries of loans previously charged-off | 474 | 527 | 457 | (10.1) | 3.7 | 1,001 | 898 | 11.5 | |

| Income from sale of fixed assets | 0 | 0 | 1,730 | 0.0 | (100.0) | 0 | 1,732 | (100.0) | |

| Allowance for loan losses released | 0 | 0 | 0 | 0.0 | 0.0 | 0 | 378 | (100.0) | |

| Cancellation of liabilities and reserve | 84 | 67 | 64 | 25.4 | 31.3 | 151 | 112 | 34.8 | |

| Interest on personnel loans | 30 | 33 | 30 | (9.1) | 0.0 | 63 | 59 | 6.8 | |

| Foreclosed assets reserve | (8) | (5) | (8) | (60.0) | 0.0 | (13) | (23) | 43.5 | |

| Profit from sale of foreclosed assets | 38 | 30 | 34 | 26.7 | 11.8 | 68 | 68 | 0.0 | |

| Technical advisory services | 14 | 37 | 56 | (62.2) | (75.0) | 51 | 97 | (47.4) | |

| Portfolio recovery legal expenses and costs | (152) | (76) | (174) | (100.0) | 12.6 | (228) | (314) | 27.4 | |

| Write-offs and bankruptcies | (103) | (179) | (173) | 42.5 | 40.5 | (282) | (284) | 0.7 | |

| Provision for legal and tax contingencies | 33 | (61) | (53) | 154.1 | 162.3 | (28) | (102) | 72.5 | |

| IPAB (indemnity) provisions and payments | (3) | (3) | (29) | 0.0 | 89.7 | (6) | (32) | 81.3 | |

| Other | 68 | 25 | 95 | 172.0 | (28.4) | 93 | 133 | (30.1) | |

| Other Operating Income (Expense) | 475 | 395 | 2,029 | 20.3 | (76.6) | 870 | 2,722 | (68.0) | |

| Grupo Financiero Santander México | |||||||||

| Administrative and Promotional Expenses | |||||||||

| Millions of Mexican Pesos | % Change | % Change | |||||||

| 2Q13 | 1Q13 | 2Q12 | QoQ | YoY | 2013 | 2012 | 13/12 | ||

| Salaries and employee benefits | 2,392 | 2,350 | 2,139 | 1.8 | 11.8 | 4,742 | 4,197 | 13.0 | |

| Credit card operation | 69 | 72 | 12 | (4.2) | 475.0 | 141 | 77 | 83.1 | |

| Professional fees | 25 | 136 | 137 | (81.6) | (81.8) | 161 | 256 | (37.1) | |

| Leasehold | 352 | 367 | 326 | (4.1) | 8.0 | 719 | 565 | 27.3 | |

| Promotional and advertising expenses | 76 | 161 | 110 | (52.8) | (30.9) | 237 | 199 | 19.1 | |

| Taxes and duties | 322 | 212 | 207 | 51.9 | 55.6 | 534 | 366 | 45.9 | |

| Technology services (IT) | 540 | 500 | 379 | 8.0 | 42.5 | 1,040 | 834 | 24.7 | |

| Depreciation and amortization | 427 | 382 | 373 | 11.8 | 14.5 | 809 | 749 | 8.0 | |

| Contributions to bank savings protection system (IPAB) | 372 | 360 | 324 | 3.3 | 14.8 | 732 | 646 | 13.3 | |

| Cash protection | 193 | 102 | 172 | 89.2 | 12.2 | 295 | 230 | 28.3 | |

| Other services and expenses | 546 | 646 | 356 | (15.5) | 53.4 | 1,192 | 867 | 37.5 | |

| Total Administrative and Promotional Expenses | 5,314 | 5,288 | 4,535 | 0.5 | 17.2 | 10,602 | 8,986 | 18.0 | |

| Banco Santander México | |||||

| Capitalization | |||||

| Millions of Mexican Pesos | 2Q13 | 1Q13 | 2Q12 | ||

| Tier 1 | 76,074 | 77,252 | 73,578 | ||

| Tier 2 | 0 | 1,283 | 1,529 | ||

| Total Capital | 76,074 | 78,535 | 75,107 | ||

| Risk-Weighted Assets | |||||

| Credit Risk | 322,151 | 329,828 | 307,413 | ||

| Credit, Market, and Operational Risk | 498,996 | 503,213 | 513,305 | ||

| Credit Risk Ratios: | |||||

| Tier 1 (%) | 23.6 | 23.4 | 23.9 | ||

| Tier 2 (%) | 0.0 | 0.4 | 0.5 | ||

| Capitalization Ratio (%) | 23.6 | 23.8 | 24.4 | ||

| Total Capital Ratios: | |||||

| Tier 1(%) | 15.2 | 15.4 | 14.3 | ||

| Tier 2 (%) | 0.0 | 0.3 | 0.3 | ||

| Capitalization Ratio (%) | 15.2 | 15.6 | 14.6 |

| Series “F” Non Independent Directors | |

| D. Carlos Gómez y Gómez | Chairman |

| D. Jesús María Zabalza Lotina | Director |

| D. Marcos Martínez Gavica | Director |

| D. Fernando Solana Morales | Director |

| D. Juan Sebastián Moreno Blanco | Alternate Director |

| D. Rodrigo Brand de Lara | Alternate Director |

| D. Pedro José Moreno Cantalejo | Alternate Director |

| D. Eduardo Fernández García-Travesí | Alternate Director |

| Series “F” Independent Directors | |

| D. Guillermo Güemez García | Director |

| D. Joaquín Vargas Guajardo | Director |

| D. Juan Gallardo Thurlow | Director |

| D. Vittorio Corbo Lioi | Director |

| D. Eduardo Carredano Fernández | Alternate Director |

| D. Alberto Felipe Mulas Alonso | Alternate Director |

| D. Jesús Federico Reyes Heroles González Garza | Alternate Director |

| Series “B” Independent Directors | |

| D. Carlos Fernández González | Director |

| D. Fernando Ruíz Sahagún | Director |

| D. Alberto Torrado Martínez | Director |

| D. Enrique Krauze Kleinbort | Alternate Director |

| D. Luis Orvañanos Lascurain | Alternate Director |

| D. Antonio Purón Mier y Terán | Alternate Director |

| Banco Santander (México) | |||||

| Ratings | |||||

| Standard & Poor´s | Moody´s | Fitch Ratings | |||

| Global Scale | |||||

| Foreign Currency | |||||

| Long Term | BBB | Baa1 | BBB+ | ||

| Short Term | A-2 | P-2 | F2 | ||

| Local Currency | |||||

| Long Term | BBB | A3 | BBB+ | ||

| Short Term | A-2 | P-2 | F2 | ||

| National Scale | |||||

| Long Term | mxAAA | Aaa.mx | AAA(mex) | ||

| Short Term | mxA-1+ | Mx-1 | F1+(mex) | ||

| Deposit Certificates | |||||

| Long Term | BBB | ||||

| Short Term | A-3 | ||||

| Autonomous Credit Profile (SACP) | bbb+ | - | - | ||

| Rating viability (VR) | - | - | bbb+ | ||

| Support | - | - | 2 | ||

| Financial Strength | - | C- | - | ||

| Standalone BCA | - | baa1 | - | ||

| Outlook | Stable | Stable | Stable | ||

| Last publication: | 13-Jun-13 | 14-Jun-13 | 28-May-13 | ||

| Brokerage - Casa de Bolsa Santander | ||||

| Ratings | ||||

| Moody´s | Fitch Ratings | |||

| Global Scale | ||||

| National Scale | ||||

| Long Term | A2 | _ | ||

| Short Term | Prime-1 | _ | ||

| National Scale | ||||

| Long Term | Aaa.mx | AAA.mx | ||

| Short Term | Mx-1 | F1+mx | ||

| Outlook | Stable | Stable |

| Date: | Wednesday, July 31, 2013 |

| Time: | 9:00 AM (MCT); 10:00 AM (US ET) |

| Dial-in Numbers: | 1-888-208-1427 US & Canada; 1-913-312-0665 International & Mexico |

| Access Code: | 5382576 |

| Webcast: | https://viavid.webcasts.com/starthere.jsp?ei=1019473 |

| Replay: | Starting Wednesday, July 31, 2013 at 01:00pm US ET, and ending on Wednesday, August 7, 2013 at 11:59pm US ET |

| Dial-in number: 1-877-870-5176 US & Canada; 1-858-384-5517 International & Mexico | |

Access Code: 5382576 |

| MARCOS A. MARTINEZ GAVICA | PEDRO JOSE MORENO CANTALEJO | |||

| Executive President and Chief Executive Officer | Vice President of Administration and Finance | |||

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA | ||

Deputy General Director of Intervention and Control Management | Executive Director – Controller | Executive Director of Internal Audit | ||

| § | Consolidated Balance Sheet |

| § | Consolidated Statement of Income |

| § | Consolidated Statement of Changes in Stockholders’ Equity |

| § | Consolidated Statement of Cash Flows |

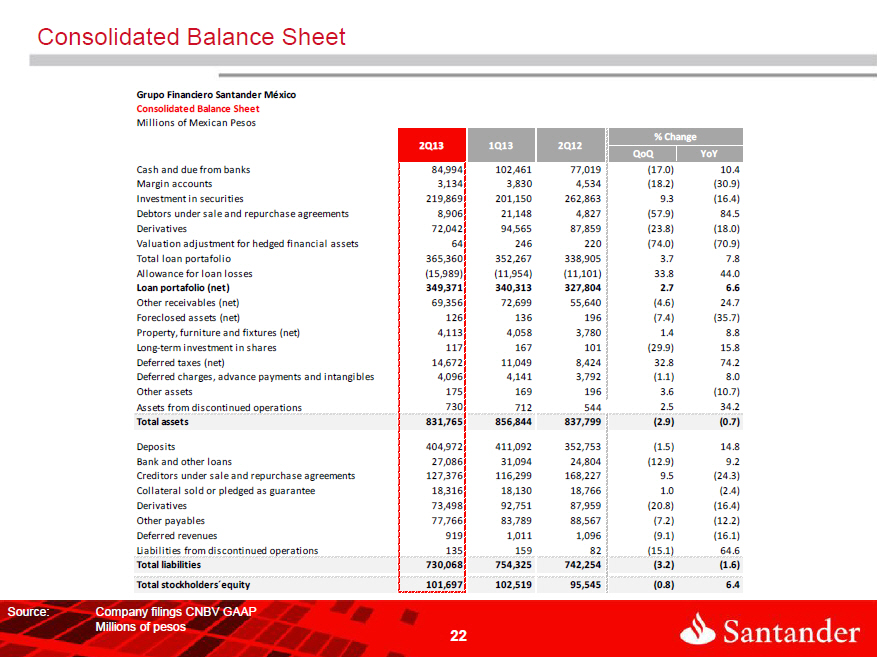

| Grupo Financiero Santander México | |||||||

| Consolidated Balance Sheet | |||||||

| Millions of Mexican Pesos | |||||||

| 2013 | 2012 | ||||||

| Jun | Mar | Dec | Sep | Jun | Mar | ||

| Assets | |||||||

| Cash and due from banks | 84,994 | 102,461 | 81,626 | 74,579 | 77,019 | 60,747 | |

| Margin accounts | 3,134 | 3,830 | 3,995 | 3,817 | 4,534 | 4,187 | |

| Investment in securities | 219,869 | 201,150 | 169,499 | 202,014 | 262,863 | 269,588 | |

| Trading securities | 160,761 | 158,619 | 117,036 | 141,986 | 203,124 | 202,726 | |

| Securities available for sale | 53,908 | 37,384 | 47,373 | 54,996 | 54,764 | 61,944 | |

| Securities held to maturity | 5,200 | 5,147 | 5,090 | 5,032 | 4,975 | 4,918 | |

| Debtors under sale and repurchase agreements | 8,906 | 21,148 | 9,471 | 4,458 | 4,827 | 4,484 | |

| Derivatives | 72,042 | 94,565 | 80,622 | 89,391 | 87,859 | 71,993 | |

| Trading purposes | 71,810 | 94,178 | 80,322 | 88,947 | 87,288 | 71,278 | |

| Hedging purposes | 232 | 387 | 300 | 444 | 571 | 715 | |

| Valuation adjustment for hedged financial assets | 64 | 246 | 210 | 240 | 220 | 139 | |

| Performing loan portfolio | |||||||

| Commercial loans | 220,224 | 213,471 | 214,445 | 211,685 | 212,492 | 198,276 | |

| Commercial or business activity | 188,480 | 175,379 | 175,329 | 175,945 | 176,332 | 163,630 | |

| Financial entities loans | 779 | 451 | 407 | 619 | 606 | 1,934 | |

| Government entities loans | 30,965 | 37,641 | 38,709 | 35,121 | 35,554 | 32,712 | |

| Consumer loans | 63,464 | 61,906 | 61,603 | 59,996 | 57,043 | 52,857 | |

| Mortgage loans | 72,787 | 70,448 | 68,542 | 66,172 | 64,417 | 62,559 | |

| Total performing loan portfolio | 356,475 | 345,825 | 344,590 | 337,853 | 333,952 | 313,692 | |

| Nonperforming loan portfolio | |||||||

| Commercial loans | 3,899 | 1,823 | 1,523 | 1,402 | 1,313 | 1,135 | |

| Commercial or business activity | 3,899 | 1,815 | 1,523 | 1,402 | 1,313 | 1,135 | |

| Government entities loans | 0 | 8 | 0 | 0 | 0 | 0 | |

| Consumer loans | 2,606 | 2,261 | 2,236 | 2,053 | 1,709 | 1,255 | |

| Mortgage loans | 2,380 | 2,358 | 2,334 | 2,075 | 1,931 | 1,982 | |

| Total nonperforming portfolio | 8,885 | 6,442 | 6,093 | 5,530 | 4,953 | 4,372 | |

| Total loan portfolio | 365,360 | 352,267 | 350,683 | 343,383 | 338,905 | 318,064 | |

| Allowance for loan losses | (15,989) | (11,954) | (11,580) | (11,360) | (11,101) | (10,875) | |

| Loan portfolio (net) | 349,371 | 340,313 | 339,103 | 332,023 | 327,804 | 307,189 | |

| Other receivables (net) | 69,356 | 72,699 | 45,884 | 47,167 | 55,640 | 46,677 | |

| Foreclosed assets (net) | 126 | 136 | 150 | 172 | 196 | 220 | |

| Property, furniture and fixtures (net) | 4,113 | 4,058 | 4,095 | 3,770 | 3,780 | 5,439 | |

| Long-term investment in shares | 117 | 167 | 134 | 115 | 101 | 157 | |

| Deferred taxes (net) | 14,672 | 11,049 | 10,512 | 9,087 | 8,424 | 8,183 | |

| Deferred charges, advance payments and intangibles | 4,096 | 4,141 | 4,247 | 3,690 | 3,792 | 4,146 | |

| Other assets | 175 | 169 | 163 | 264 | 196 | 170 | |

| Discontinued operations | 730 | 712 | 626 | 634 | 544 | 628 | |

| Total assets | 831,765 | 856,844 | 750,337 | 771,421 | 837,799 | 783,947 | |

| Grupo Financiero Santander México | |||||||

| Consolidated Balance Sheet | |||||||

| Millions of Mexican Pesos | |||||||

| 2012 | |||||||

| Jun | Mar | Dec | Sep | Jun | Mar | ||

| Liabilities | |||||||

| Deposits | 404,972 | 411,092 | 397,546 | 358,606 | 352,753 | 346,605 | |

| Demand deposits | 218,593 | 226,503 | 210,915 | 194,351 | 204,606 | 187,787 | |

| Time deposits – General Public | 130,599 | 124,871 | 125,584 | 120,034 | 117,184 | 122,816 | |

| Time deposits – Money market | 29,498 | 23,546 | 25,953 | 21,904 | 9,085 | 14,507 | |

| Credit instruments issued | 26,282 | 36,172 | 35,094 | 22,317 | 21,878 | 21,495 | |

| Bank and other loans | 27,086 | 31,094 | 27,463 | 34,339 | 24,804 | 21,372 | |

| Demand loans | 9,659 | 9,075 | 8,240 | 5,916 | 6,851 | 5,949 | |

| Short-term loans | 15,513 | 19,726 | 16,767 | 26,092 | 15,704 | 13,278 | |

| Long-term loans | 1,914 | 2,293 | 2,456 | 2,331 | 2,249 | 2,145 | |

| Creditors under sale and repurchase agreements | 127,376 | 116,299 | 73,290 | 106,306 | 168,227 | 189,299 | |

| Collateral sold or pledged as guarantee | 18,316 | 18,130 | 6,853 | 17,972 | 18,766 | 14,104 | |

| Securities loans | 18,316 | 18,130 | 6,853 | 17,972 | 18,766 | 14,104 | |

| Derivatives | 73,498 | 92,751 | 79,561 | 86,611 | 87,959 | 70,290 | |

| Trading purposes | 72,264 | 91,132 | 77,939 | 85,207 | 86,232 | 69,264 | |

| Hedging purposes | 1,234 | 1,619 | 1,622 | 1,404 | 1,727 | 1,026 | |

| Other payables | 77,766 | 83,789 | 66,610 | 71,567 | 88,567 | 47,468 | |

| Income taxes payable | 180 | 284 | 440 | 720 | 335 | 841 | |

| Employee profit sharing payable | 97 | 83 | 169 | 115 | 81 | 61 | |

| Creditors from settlement of transactions | 52,312 | 62,970 | 38,604 | 47,308 | 52,492 | 24,013 | |

| Sundry creditors and other payables | 25,177 | 20,452 | 27,397 | 23,424 | 35,659 | 22,553 | |

| Deferred revenues | 919 | 1,011 | 1,041 | 1,091 | 1,096 | 1,385 | |

| Discontinued operations | 135 | 159 | 146 | 136 | 82 | 180 | |

| Total liabilities | 730,068 | 754,325 | 652,510 | 676,628 | 742,254 | 690,703 | |

| Paid in capital | 47,881 | 47,776 | 47,811 | 47,776 | 48,195 | 48,195 | |

| Capital stock | 36,357 | 36,357 | 36,357 | 36,357 | 36,357 | 36,357 | |

| Share premium | 11,524 | 11,419 | 11,454 | 11,419 | 11,838 | 11,838 | |

| Other capital | 53,816 | 54,743 | 50,016 | 47,017 | 47,350 | 45,049 | |

| Capital reserves | 1,850 | 349 | 349 | 349 | 349 | 108 | |

| Retained earnings | 43,370 | 48,979 | 31,068 | 31,038 | 35,311 | 38,541 | |

| Result from valuation of securities available for sale, net | (215) | 762 | 678 | 727 | 688 | 442 | |

| Result from valuation of cash flow hedge instruments, net | (59) | (74) | 90 | 382 | 690 | 932 | |

| Net income | 8,860 | 4,717 | 17,822 | 14,512 | 10,298 | 5,013 | |

| Non-controlling interest | 10 | 10 | 9 | 9 | 14 | 13 | |

| Total stockholders´equity | 101,697 | 102,519 | 97,827 | 94,793 | 95,545 | 93,244 | |

| Total liabilities and stockholders´ equity | 831,765 | 856,844 | 750,337 | 771,421 | 837,799 | 783,947 |

| Grupo Financiero Santander México | |||||||

| Consolidated Balance Sheet | |||||||

| Millions of Mexican Pesos | |||||||

| 2013 | 2012 | ||||||

| Jun | Mar | Dec | Sep | Jun | Mar | ||

| Memorandum accounts | |||||||

| FOR THIRD PARTIES | |||||||

| Current client account | |||||||

| Client Banks | 675 | 56 | 74 | 74 | 261 | 147 | |

| Liquidation of client transactions | (1,245) | (47) | 116 | 350 | (2,030) | 35 | |

| Dividends on behalf of clients | 1 | 1 | 1 | 0 | 1 | 1 | |

| Custody services | |||||||

| Assets under custody | 579,068 | 290,289 | 317,118 | 261,131 | 198,793 | 210,076 | |

| Client securities abroad | 0 | 0 | 1 | 0 | 0 | 1 | |

| Transactions on behalf of third parties | |||||||

| Sale and repurchase agreements | 71,235 | 38,874 | 45,914 | 44,469 | 55,334 | 65,577 | |

| Security loans on behalf of clients | 1,121 | 1,201 | 1,256 | 1,457 | 1,826 | 2,182 | |

| Collaterals received as guarantee on behalf of clients | 2,023 | 28,283 | 29,504 | 19,013 | 15,690 | 19,542 | |

| Acquisition of derivatives | 267,400 | 291,038 | 289,248 | 294,269 | 308,411 | 308,379 | |

| Sale of derivatives | 479,013 | 526,154 | 570,945 | 579,263 | 603,162 | 656,451 | |

| Total on behalf of third parties | 1,399,291 | 1,175,849 | 1,254,177 | 1,200,026 | 1,181,448 | 1,262,391 | |

| Proprietary record accounts: | |||||||

| Contingent assets and liabilities | 33,237 | 30,265 | 33,236 | 24,053 | 31,852 | 31,904 | |

| Credit commitments | |||||||

| Trusts | 123,172 | 127,435 | 125,954 | 106,006 | 106,747 | 155,407 | |

| Mandates | 1,612 | 1,596 | 1,580 | 2,582 | 1,548 | 1,532 | |

| Assets in custody or under administration | 4,006,969 | 3,567,360 | 3,561,696 | 3,312,634 | 3,062,735 | 3,084,880 | |

| Credit Commitments | 155,912 | 155,483 | 133,744 | 160,790 | 203,362 | 157,565 | |

| Collateral received | 60,377 | 154,943 | 71,296 | 90,548 | 52,244 | 49,931 | |

| Collateral received and sold or pledged as guarantee | 31,663 | 115,180 | 53,788 | 66,877 | 26,708 | 29,027 | |

| Uncollected interest earned on past due loan portfolio | 1,447 | 1,402 | 1,808 | 794 | 1,092 | 985 | |

| Other accounts | 501,926 | 484,324 | 501,538 | 466,076 | 455,197 | 429,800 | |

| Subtotal | 4,916,315 | 4,637,988 | 4,484,640 | 4,230,360 | 3,941,485 | 3,941,031 | |

| Total | 6,315,606 | 5,813,837 | 5,738,817 | 5,430,386 | 5,122,933 | 5,203,422 | |

| MARCOS A. MARTINEZ GAVICA | PEDRO JOSE MORENO CANTALEJO | |

| Executive President and Chief Executive Officer | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| Deputy General Director of Intervention and Control Management | Executive Director - Controller | Executive Director of Internal Audit |

| Grupo Financiero Santander México | |||||||||

| Consolidated Statement of Income | |||||||||

| Millions of Mexican Pesos | |||||||||

| 2013 | 2012 | ||||||||

| 2013 | 2Q | 1TQ | 2012 | 4Q | 3Q | 2Q | 1Q | ||

| Interest income | 27,809 | 14,201 | 13,608 | 55,388 | 14,259 | 13,873 | 13,830 | 13,426 | |

| Interest expense | (10,274) | (5,302) | (4,972) | (21,495) | (5,447) | (5,291) | (5,436) | (5,321) | |

| Financial margin | 17,535 | 8,899 | 8,636 | 33,893 | 8,812 | 8,582 | 8,394 | 8,105 | |

| Allowance for loan losses | (6,152) | (3,348) | (2,804) | (9,444) | (2,948) | (2,534) | (1,994) | (1,968) | |

| Financial margin after allowance for loan losses | 11,383 | 5,551 | 5,832 | 24,449 | 5,864 | 6,048 | 6,400 | 6,137 | |

| Commission and fee income | 7,472 | 3,650 | 3,822 | 14,368 | 3,858 | 3,671 | 3,421 | 3,418 | |

| Commission and fee expense | (1,202) | (598) | (604) | (2,525) | (631) | (707) | (660) | (527) | |

| Net gain /(loss) on financial assets and liabilities | 2,357 | 1,308 | 1,049 | 2,189 | 413 | 918 | 105 | 753 | |

| Other operating income / (loss) | 870 | 475 | 395 | 3,043 | 209 | 112 | 2,029 | 693 | |

| Administrative and promotional expenses | (10,602) | (5,314) | (5,288) | (20,139) | (5,996) | (5,157) | (4,535) | (4,451) | |

| Total operating income | 10,278 | 5,072 | 5,206 | 21,385 | 3,717 | 4,885 | 6,760 | 6,023 | |

| Equity in results of subsidiaries and associated companies | 42 | 27 | 15 | 70 | 20 | 15 | 18 | 17 | |

| Income from continuing operations before income taxes | 10,320 | 5,099 | 5,221 | 21,455 | 3,737 | 4,900 | 6,778 | 6,040 | |

| Current income taxes | (4,006) | (2,938) | (1,068) | (5,808) | (1,654) | (1,275) | (1,757) | (1,122) | |

| Deferred income taxes | 2,623 | 2,107 | 516 | 2,048 | 1,179 | 547 | 246 | 76 | |

| Income from continuing operations | 8,937 | 4,268 | 4,669 | 17,695 | 3,262 | 4,172 | 5,267 | 4,994 | |

| Discontinued operations | (76) | (124) | 48 | 129 | 49 | 42 | 19 | 19 | |

| Consolidated net income | 8,861 | 4,144 | 4,717 | 17,824 | 3,311 | 4,214 | 5,286 | 5,013 | |

| Non-controlling interest | (1) | (1) | 0 | (2) | (1) | 0 | (1) | 0 | |

| Net income | 8,860 | 4,143 | 4,717 | 17,822 | 3,310 | 4,214 | 5,285 | 5,013 | |

| MARCOS A. MARTINEZ GAVICA | PEDRO JOSE MORENO CANTALEJO | |

| Executive President and Chief Executive Officer | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

| Grupo Financiero Santander México | |||||||||||||

| Consolidated Statements of Changes in Stockholders’ Equity | |||||||||||||

| From January 1 to June 30, 2013 | |||||||||||||

| Millions of Mexican Pesos | Paid-in Capital | Other Capital | |||||||||||

| Capital Stock | Additional Paid-In Capital | Capital Reserves | Retained Earnings | Surplus (deficit) from valuation of securities available for sale | Surplus (Deficit) from the valuation of cash flow hedge securities | Cumulative effect from conversion | Net income (loss) | Minority Interest | Total stockholders' equity | ||||

| BALANCE AS OF DECEMBER 31, 2012 | 36,357 | 11,454 | 349 | 31,068 | 678 | 90 | 0 | 17,822 | 9 | 97,827 | |||

| MOVEMENTS INHERENT TO THE SHAREHOLDERS' DECISIONS | |||||||||||||

| Transfer of Net income (loss) to Retained Earnings | 1 | 17,821 | (17,822) | 0 | |||||||||

| Payment of Dividends | (1,650) | (1,650) | |||||||||||

| TOTAL | 0 | 0 | 1 | 16,171 | 0 | 0 | 0 | (17,822) | 0 | (1,650) | |||

| MOVEMENTS INHERENT TO THE RECOGNITION OF THE COMPREHENSIVE INCOME | |||||||||||||

| Surplus (deficit) from valuation of securities available for sale | (893) | (893) | |||||||||||

| Surplus (deficit) from valuation of cash flow hedge securities | (149) | (149) | |||||||||||

| Reserve for purchase of treasury shares | 1,500 | (1,500) | |||||||||||

| Recognition of Capital payments | 70 | 70 | |||||||||||

| Recoveries on loan reserves previously applied to prior year results | 27 | 27 | |||||||||||

| Initial cumulative effect of change in methodology for measuring allowance for loan with respect to commercial loan portfolio. | (2,412) | (2,412) | |||||||||||

| Equity effect of investment in subsidiaries and associated companies | 16 | 16 | |||||||||||

| Net Income (Loss) | 8,860 | 8,860 | |||||||||||

| Minority Interest | 1 | 1 | |||||||||||

| TOTAL | 0 | 70 | 1,500 | (3,869) | (893) | (149) | 0 | 8,860 | 1 | 5,520 | |||

| BALANCE AS OF JUNE 30, 2013 | 36,357 | 11,524 | 1,850 | 43,370 | (215) | (59) | 0 | 8,860 | 10 | 101,697 | |||

| MARCOS A. MARTINEZ GAVICA | PEDRO JOSE MORENO CANTALEJO | |

| Executive President and Chief Executive Officer | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

| Consolidated Statement of Cash Flows | |||

| From January 1 to June 30, 2013 | |||

| Millions of Mexican Pesos | |||

| OPERATING ACTIVITIES | |||

| Net Result | 8,860 | ||

| Adjustments due to items not requiring resources | |||

| Result from valuation related to investment or financing activities | (99) | ||

| Equity in results of subsidiaries and associated companies | (42) | ||

| Depreciation of properties, furniture and equipment | 307 | ||

| Amortization of intangible assets | 502 | ||

| Recognition of Capital payments | 70 | ||

| Income tax, current and deferred | 1,383 | ||

| Discontinued operations | 76 | 2,197 | |

| 11,057 | |||

| CHANGES IN OPERATING ACCOUNTS | |||

| Change in margin accounts | 861 | ||

| Change in Securities | (51,648) | ||

| Changes in Debit balances under repurchase and resale agreements (Reporto) | 566 | ||

| Changes in Derivatives (Asset) | 8,513 | ||

| Changes in Loans portfolio | (13,711) | ||

| Changes in Foreclosed assets | 24 | ||

| Changes in Other operating assets | (27,026) | ||

| Changes in Savings | 7,426 | ||

| Changes in Interbank loans and from other entities | (377) | ||

| Changes in Credit balances under repurchase and sale agreements (Reporto) | 54,085 | ||

| Changes in sold or pledged guarantees | 11,462 | ||

| Changes in Derivatives (Liabilities)) | (6,064) | ||

| Changes in other operating liabilities | 10,763 | ||

| Income tax payments | (1,851) | ||

| Net resources generated by operating activities | 4,080 | ||

| INVESTING ACTIVITIES | |||

| Sale of Properties, furniture and equipment | 2 | ||

| Purchases of properties, furniture and equipment | (326) | ||

| Collection of cash dividends | 57 | ||

| Purchases of intangible assets | (410) | ||

| Payment for price adjustment in charges for disposal of subsidiaries | (178) | ||

| Net resources generated by investing activities | (855) | ||

| FINANCING ACTIVITIES | |||

| Recoveries of reserves applied to results from previous years | 28 | ||

| Net resources generated by financing activities | 28 | ||

| Net increase in funds available | 3,253 | ||

| Adjustments to cash flow due to exchange variations | 115 | ||

| Funds available at beginning of year | 81,626 | ||

| Funds available at the end of the year | 84,994 |

| MARCOS A. MARTINEZ GAVICA | PEDRO JOSE MORENO CANTALEJO | |

| Executive President and Chief Executive Officer | Vice President of Administration and Finance |

| EMILIO DE EUSEBIO SAIZ | JESÚS GONZÁLEZ DEL REAL | JAVIER PLIEGO ALEGRÍA |

| Deputy General Director of Intervention and Control Management | Executive Vice President of Accounting | Executive Director of Internal Audit |

| Ø | The valuation of the trust's net assets must be recognized in memorandum accounts according to the accounting criteria issued by the Commission, unless trusts request, obtain and maintain the registration of their securities with the National Securities Registry, in which case their net assets must be valued according to the accounting standards issued by the Commission for application to securities issuers and other market participants (International Financial Reporting Standards, or IFRS). |

| Ø | The description of the minimum conditions that must be fulfilled to demonstrate that an entity does not exercise control over an EPE thereby avoiding the consolidation thereof has been eliminated. |

| Ø | The financial statements of the consolidated EPE must be prepared according to the same accounting criterion; likewise, when involving operations of the same nature, the accounting policies applied by the consolidating entity must also be used. |

| Ø | When the EPE uses accounting criteria or policies other than those applicable to the consolidating entity, the financial statements of the EPE utilized for consolidation purposes must be consistent with those of the consolidating entity. |

| Ø | The presentation of the income statement is comprehensively restructured for purposes of compliance with MFRS. The headings of "Other products" and "Other expenses" are eliminated and the items which comprise these headings are now presented within the heading of "Other operating income”. |

| Ø | The accounting standard related to the treatment of collateral granted and received for transactions with derivative financial instruments traded on unrecognized markets. They will be accounted for separately from the margin accounts, and will be recorded in an account receivable or payable, as the case may be. |

| Ø | The valuation of implicit derivatives denominated in foreign currency contained in contracts is not established, when such contracts require payments in a currency that is commonly used to purchase or sale non-financial items in the economic environment in which the transaction is performed (for example, a stable and liquid currency which is commonly used in local transactions or in foreign trade transactions). |

| Ø | In the case of separable hybrid financial instruments, the host contract and the embedded derivative will be presented separately. Previously, it was established that both should be presented together. Now the embedded derivative should be presented under the heading of "Derivatives". |

| Ø | In convergence with NIF, the requirement to present the charge to net income for net additions to allowance for loan losses in a discrete line in the cash flow statement is eliminated. |

| Ø | Bulletin A-2 of the Provisions Applicable to Financial Groups is amended to eliminate the provision which indicated that insurance and bonding companies were not subject to consolidation. |

| Ø | Accounting criterion B-6 “Credit portfolio” of the provisions establishes the following: |

| o | In the case of restructuring and renewals in which multiple loans granted to a given borrower are consolidated into a single loan, which is given a credit rating equal to the lowest rated loan outstanding from the borrower. |

| o | In order to demonstrate sustained payment and no longer classify a restructured or renewed loan as overdue, evidence supporting the borrower's payment capacity must be made available to the Commission. |

| o | The maturity periods used to transfer loans to the overdue portfolio can be monthly, regardless of the number of days of each calendar month, in accordance with the following: |

| 30 days | One month |

| 60 days | Two months |

| 90 days | Three months |

| o | Current loans other than those involving a single principal payment, the payment of interest periodically or at maturity and which are restructured or renewed at least 80% of the original credit period having elapsed are only considered as current if the borrower has a) paid all accrued interest and b) settled the principal of the original credit amount which should have been paid at the renewal or restructuring date. |

| o | In the case of loan payments reflecting timely borrower compliance (sustained credit payment), at least 20% of principal or the total amount of any interest accrued under the restructuring or renewal payment scheme must be covered. |

| o | For loans involving a single principal payment, the periodic payments of interest or a lump sum payment of interest at maturity and which are restructured during the credit period or renewed at any time, are classified as overdue portfolio until evidence of sustained payment is obtained. |

o | Loans that are initially classified as revolving and that are restructured or renewed at any time are only considered as current when the borrower has settled all accrued interest, the loan has no overdue payments and the elements needed to justify the debtor's payment capacity are available, i.e., it is highly likely that the debtor will settle the outstanding payment. |

| o | When a credit line is canceled, the unpaid balance of commissions collected for loans canceled before the end of the 12-month period are directly recognized in the results of the year under the heading of “Commission and fee income”. |

| o | The incorporation of the commissions for loan restructurings as commissions for the initial granting of the loan, which may be deferred during the new term of the restructured loan. |

| o | The commissions collected for granting loans must be presented net of the respective costs and expenses under the “Other assets” or “Deferred revenues and other advances” headings, as appropriate. Likewise, annual credit card commissions must also be presented net of the respective costs and expenses. |

| o | Any deferred charge generated on the acquisition of portfolio should be presented under the heading of "Other assets" and, furthermore, discounts should be presented under the heading of "Deferred revenues and other advances", together with any excess originated on the portfolio acquisitions. |

| Ø | NIF B-8, Consolidated or Combined Financial Statements- Amends the definition of control. The existence of control over an entity is the basis for consolidation of the financial information. With this new definition and in accordance with the criteria of the revised standard, consolidation may be required of certain previously unconsolidated entities that are controlled by the Entity and, vice versa, the Entity may be required to deconsolidate previously consolidated entities over which the Entity has determined it does not exercise control. This NIF establishes that an entity exercises control when it has power to direct relevant activities and if it is exposed to or has rights to variable returns of another entity and has the ability to influence such returns. Additionally, the NIF introduces the concept of protective rights, which are defined as those rights that are designed to protect the non-controlling investor’s participation, while not granting power to such investor. The standard also incorporates the concepts of principal and agent, wherein the principal is the investor entitled to make decisions on its own behalf, while the agent’s role is limited to making decisions on behalf of the principal; consequently, the latter cannot be the party who exercises control. The NIF removes the term “special-purpose entity” and introduces the concept of a structured entity, which is an entity designed in such a way that voting or similar rights are not the determining factor for deciding who has control over it. |

| Ø | NIF C-7, Investments in associated companies, joint businesses and other permanent investments – Establishes that investments in joint businesses should be recognized by applying the equity method and that all the profit and loss effects derived from permanent investments in associated companies, joint businesses and others should be recognized in results under the heading of equity in results of other entities. Requires further disclosures designed to provide greater financial information on the associated companies and joint businesses and eliminates the term specific purpose entity (SPE). |

| Ø | NIF C-21, Agreements with joint control – It defines that a joint agreement is an agreement that regulates an activity over which two or more parties exercise joint control, as follows: 1) joint transaction, when the |

| parties to the agreement have direct rights to the assets and obligations for the liabilities, relative to the agreement and 2) joint business, when the parties have the right to participate only in the residual value of the assets once the liabilities have been deducted. Establishes that the equity held in a joint business should be recognized as a permanent investment and valued by the equity method. |

| Ø | Improvements to NIF 2013 – The principal improvements that generate accounting changes which should be recognized retrospectively in years beginning as of January 1, 2013 are as follows: |

| o | Bulletin C-9, Liabilities, provisions, contingent assets and liabilities and commitment and |

| o | Bulletin C-15, Impairment in the value of long-lived assets and their disposal-If an operation is discontinued, the obligation to restructure any balance sheets of previous periods presented for comparative purposes is eliminated. |

| o | Bulletin D-5, Leases- Stipulates that non-reimbursable lease payments should be deferred over the lease period and recognized in current earnings upon recognition of revenues and related expenses by the lessor and the lease, respectively. |

| Ø | Bulletin B-14, Earnings per Share.- Requires the calculation and disclosure of diluted earnings per share when the entity has incurred a loss from continuing operations, regardless of whether or not there is net income for the period. |

| Ø | Bulletin C-11, Stockholders’ Equity – Eliminates the rule whereby the contributions received by a company must be recorded under stockholders' equity. These amounts must now be recorded as income in the statement of income. |

| Ø | Bulletin C-15, Impairment in the Value of Long-lived Assets and their Disposal – Eliminates a) the limitation that an asset that is not in use may be classified as held for sale, and b) reversal of goodwill impairment losses. The standard also stipulates that impairment losses related to long-lived assets should be classified in the statement of income within the appropriate cost and expenses line items, and not under other income and expenses, or as a special item. |

| Ø | NIF D-4, Income taxes – Modifies the definition of a deductible temporary difference and taxable accruable temporary difference. |

| Grupo Financiero Santander México | ||||||||||||

| Earnings per ordinary share and Earnings per diluted share | ||||||||||||

| (Millions of pesos, except shares and earnings per share) | ||||||||||||

| JUNE 2013 | JUNE 2012 | JUNE 2011 | ||||||||||

| Shares | Earnings | Shares | Earnings | Shares | Earnings | |||||||

| Earnings | -weighted- | per share | Earnings | - weighted - | per share | Earnings | - weighted - | per share | ||||

| Earnings per share | 8,860 | 6,786,394,913 | 1.31 | 10,298 | 6,786,394,913 | 1.52 | 6,818 | 6,786,394,913 | 1.00 | |||

| Treasury stock | (13,401,600) | |||||||||||

| �� | ||||||||||||

| Diluted earnings per share | 8,860 | 6,772,993,313 | 1.31 | 10,298 | 6,786,394,913 | 1.52 | 6,818 | 6,786,394,913 | 1.00 | |||

| Plus (loss) less (profit): | ||||||||||||

| Discontinued operations | 76 | (38) | (333) | |||||||||

| Continued fully diluted earnings per share | 8,936 | 6,772,993,313 | 1.32 | 10,260 | 6,786,394,913 | 1.51 | 6,485 | 6,786,394,913 | 0.96 | |||

| Grupo Financiero Santander México | |||||||

| Consolidated Balance Sheet by Segment | |||||||

| Millions of Mexican Pesos | |||||||

| As of June 30, 2013 | As of June 30, 2012 | ||||||

| Retail Banking 1/ | Wholesale Banking 2/ | Corporate Activities | Retail Banking 1/ | Wholesale Banking 2/ | Corporate Activities | ||

| Assets | |||||||

| Funds Available | 36,442 | 27,499 | 21,053 | 34,725 | 40,018 | 2,276 | |

| Margin Accounts | 0 | 3,134 | 0 | 0 | 4,534 | 0 | |

| Investment in Securities | 0 | 160,112 | 59,758 | 0 | 202,561 | 60,302 | |

| Debit balances under repurchase and resale agreements | 0 | 8,906 | 0 | 0 | 4,827 | 0 | |

| Derivatives | 0 | 71,810 | 232 | 0 | 87,288 | 571 | |

| Valuation adjustments for hedging financial assets | 0 | 0 | 64 | 0 | 0 | 220 | |

| Total loans portfolio | 273,045 | 90,744 | 1,571 | 238,163 | 98,685 | 2,057 | |

| Allowance for loan losses | (11,701) | (4,244) | (44) | (10,712) | (382) | (7) | |

| Loan Portfolio (Net) | 261,345 | 86,500 | 1,526 | 227,451 | 98,303 | 2,050 | |

| Other Account Receivables (Net) | 1,808 | 60,277 | 7,271 | 2,243 | 43,425 | 9,973 | |

| Foreclosed assets (Net) | 11 | 1 | 114 | 18 | 1 | 177 | |

| Properties, furniture and equipment (Net) | 3,475 | 586 | 52 | 3,211 | 535 | 33 | |

| Long-term investments in shares | 0 | 0 | 117 | 0 | 0 | 101 | |

| Deferred taxes and profit sharing | 0 | 0 | 14,672 | 0 | 0 | 8,424 | |

| Other assets | 1,636 | 643 | 1,993 | 1,500 | 620 | 1,868 | |

| Discontinued operations | 0 | 0 | 730 | 0 | 0 | 544 | |

| Total assets | 304,716 | 419,467 | 107,581 | 269,148 | 482,112 | 86,540 | |

| Liabilities | |||||||

| Savings | 295,628 | 72,526 | 10,536 | 275,867 | 46,822 | 8,187 | |

| Bank bonds | 0 | 1,559 | 24,724 | 0 | 1,561 | 20,317 | |

| Bank and other loans | 14,856 | 208 | 12,021 | 13,064 | 252 | 11,487 | |

| Credit balances under repurchase and resale agreements | 36,345 | 79,530 | 11,501 | 12,047 | 101,701 | 54,479 | |

| Guarantees sold or pledged | 0 | 18,316 | 0 | 0 | 18,766 | 0 | |

| Derivatives | 0 | 72,264 | 1,234 | 0 | 86,233 | 1,726 | |

| Other accounts payable | 15,793 | 60,461 | 1,513 | 15,576 | 72,196 | 795 | |

| Deferred credits and advanced collections | 919 | 0 | 0 | 1,096 | 0 | 0 | |

| Discontinued operations | 0 | 0 | 135 | 0 | 0 | 82 | |

| Total Liabilities | 363,541 | 304,864 | 61,663 | 317,651 | 327,531 | 97,072 | |

| Total Stockholders' Equity | 32,936 | 11,464 | 57,296 | 28,768 | 11,943 | 54,834 | |

| Total Liabilities and Stockholders' Equity | 396,478 | 316,327 | 118,959 | 346,419 | 339,474 | 151,906 | |

| Grupo Financiero Santander México | |||||||

| Income Statement by Segment | |||||||

| Millions of Mexican Pesos | |||||||

| As of June 30, 2013 | As of June 30, 2012 | ||||||

| Retail Banking 1/ | Global Wholesale Banking 2/ | Corporate Activities | Retail Banking 1/ | Global Wholesale Banking 2/ | Corporate Activities | ||

| Net interest income before provisions | 7,290 | 833 | 776 | 6,323 | 1,022 | 1,049 | |

| Provisions for loan losses, net | (3,015) | (328) | (5) | (1,968) | (39) | (13) | |

| Net interest income after provisions | 4,275 | 505 | 770 | 4,355 | 983 | 1,062 | |

| Commissions, net | 2,738 | 334 | (20) | 2,475 | 324 | (37) | |

| Intermediation result | 274 | 1,080 | (46) | 168 | 70 | (133) | |

| Other operating income (expenses) | 313 | 6 | 156 | 302 | 1 | 1,725 | |

| Administrative and promotion expenses | (4,772) | (547) | 4 | (4,032) | (494) | (9) | |

| Operating Income | 2,828 | 1,380 | 864 | 3,267 | 885 | 2,608 | |

| Equity in results of non-consolidated subsidiaries and associated companies | (1) | 0 | 28 | (1) | 0 | 19 | |

| Income before income taxes | 2,827 | 1,380 | 893 | 3,266 | 885 | 2,627 | |

| Annex 1 | ||||||

| Loan Portfolio Rating | ||||||

| Grupo Financiero Santander México | ||||||

| As of June 30, 2012 | ||||||

| Millions of Mexican Pesos | ||||||

| Allowance for loan losses | ||||||

| Category | Loan Portfolio | Commercial | Consumer | Mortgages | Total | |

| Risk "A" | 288,919 | 1,206 | 990 | 151 | 2,346 | |

| Risk "A-1" | 203,463 | 580 | 98 | 103 | 781 | |

| Risk "A-2" | 85,456 | 626 | 892 | 48 | 1,565 | |

| Risk "B" | 67,353 | 1,160 | 2,130 | 59 | 3,349 | |

| Risk "B-1" | 27,103 | 282 | 1,132 | 17 | 1,431 | |

| Risk "B-2" | 14,040 | 152 | 382 | 24 | 558 | |

| Risk "B-3" | 26,210 | 725 | 616 | 18 | 1,359 | |

| Risk "C" | 18,687 | 423 | 1,674 | 184 | 2,281 | |

| Risk "C-1" | 11,286 | 298 | 603 | 54 | 954 | |

| Risk "C-2" | 7,401 | 126 | 1,071 | 130 | 1,327 | |

| Risk "D" | 11,813 | 2,019 | 2,686 | 294 | 4,999 | |

| Risk "E" | 4,288 | 1,728 | 826 | 123 | 2,677 | |

| Total rated portfolio | 391,058 | 6,537 | 8,305 | 811 | 15,653 | |

| Provisions created | 15,989 | |||||

| Complementary provisions | 336 | |||||

| Notes: | ||

| 1. | The figures used for grading and the creation of provisions correspond to the ones as of the last day of the month of the balance sheet as of June 31, 2013. | |

| 2. | Loan Portfolio is graded according to the rules for loan portfolio rating issued by the Mexican Treasury Department (Secretaría de Hacienda y Crédito Público (SHCP)) and the methodology established by CNBV. In the case of commercial and mortgages portfolio, such rating may be performed following internal methodologies authorized by CNBV. The institution utilizes a proprietary methodology from June 2009, for a portion of the commercial portfolio, i.e. the companies segment, and the standard methodology of CNBV for the rest of the portfolio. On July 31, 2009, the Bank implemented new rules for grading revolving consumer credit to be applied from August, 2009, as it is explained in Annex 31. From March 2011, the Bank implemented new rules for grading non-revolving consumer credits and mortgages. From September, 2011, the bank implemented new rules for grading loans to States and Municipalities. From June 2013, the bank implemented new rules for grading commercial loans | |

| 3. | Reserves created in excess are explained by the following: The Bank maintains additional reserves to the ones necessary pursuant to the loan portfolio grading process authorized by CNBV, in order to cover potential losses from mortgages portfolio, the valuation of assets determined in the Due Diligence and authorized by the CNBV in Official Letter No. 601DGSIF"C"-38625, for an amount of $27.2 million pesos, as well as to cover the cost of Governmental Programs. | |

| Annex 2 | |||||||

| Financial Ratios | |||||||

| Grupo Financiero Santander México | |||||||

| Percentages | |||||||

| 2Q13 | 1Q13 | 2Q12 | 2013 | 2012 | |||

| Past Due Loans Ratio | 2.4 | 1.8 | 1.5 | 2.4 | 1.5 | ||

| Past Due Loans Coverage | 180.0 | 185.6 | 224.1 | 180.0 | 224.1 | ||

| Operative Efficiency | 2.5 | 2.6 | 2.2 | 2.5 | 2.2 | ||

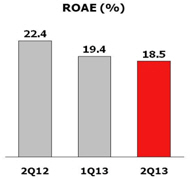

| ROE | 16.2 | 18.8 | 22.4 | 17.4 | 21.8 | ||

| ROA | 2.0 | 2.3 | 2.6 | 2.1 | 2.5 | ||

| Capitalization Ratio: | |||||||

| Credit Risk | 23.6 | 23.8 | 24.4 | 23.6 | 24.4 | ||

| Credit, Market and operations risk | 15.2 | 15.6 | 14.6 | 15.2 | 14.6 | ||

| Liquidity | 122.9 | 116.9 | 147.4 | 122.9 | 147.4 | ||

| NIM (Net Interest Margin) | 3.0 | 3.3 | 3.5 | 3.1 | 3.4 | ||

| Grupo Financiero Santander México | |

| Notes to financial statements as of June 30, 2013 | |

| (Millions of pesos, except for number of shares) | |

| 1. Financial Instruments | |

| Financial instruments are constituted as follows: | |

| Accounting Value | |

| Trading Securities: | |

| Bank Securities | 1,769 |

| Government Securities | 150,632 |

| Private shares | 2,313 |

| Shares | 6,047 |

| 160,761 | |

| Securities available for sale: | |

| Bank Securities | 503 |

| Government Securities | 48,079 |

| Other | 5,326 |

| 53,908 | |

| Securities held until maturity: | |

| Government securities (Cetes especiales) | 5,200 |

| 5,200 | |

| Total Financial Instruments | 219,869 |

| 2. Repurchase and resale agreements | |

| The repurchase and resale agreements portfolio is constituted as follows: | |

| Net balance | |

| Debit Balances | |

| Bank Securities | 4,088 |

| Government Securities | 4,818 |

| Total | 8,906 |

| Credit balances | |

| Bank Securities | 586 |

| Government Securities | 120,175 |

| Private Securities | 6,615 |

| Total | 127,376 |

| (118,470) | |

| 3. Investment in securities different to government securities | |||

| The table below lists the investments in debt securities of a same issuer, with positions equal or greater than 5% of Tier 1 Capital of the Bank. | |||

| Issuer / Series | Maturity date | % Rate | Book Value |

| MX2PPE050004 | 16-Jul-15 | 9.91% | 3,843 |

| US706451BF73 | 15-Dec-15 | 1.88% | 1,449 |

| US71656MAF68 | 28-Sep-15 | 5.79% | 59 |

| US71654QAU67 | 03-May-19 | 3.99% | 461 |

| US71654QAX07 | 21-Jan-21 | 4.42% | 399 |

| Total | 6,211 |

| Tier 1 Capital as of June, 2013 | 76,074 | ||

| 5 % of Tier 1 Capital | 3,804 |

| 4. Derivative Financial Instruments | |||||||

| The nominal value of the different derivative financial instruments agreements for trading and hedging purposes, as of June 30, 2013, are as follows: | |||||||

| Swaps | |||||||

| Interest Rate | 3,133,363 | ||||||

| Foreign Exchange | 610,275 | ||||||

| Futures | Buy | Sell | |||||

| Interest Rate | 55 | 429,405 | |||||

| Foreign Exchange | 1,303 | 7,402 | |||||

| Index | 2,348 | 2,173 | |||||

| Forward Contracts | |||||||

| Interest Rate | 0 | 900 | |||||

| Foreign Exchange | 290,544 | 3,549 | |||||

| Securities | 3,391 | 7,582 | |||||

| Options | Long | Short | |||||

| Interest Rate | 177,448 | 202,841 | |||||

| Foreign Exchange | 9,600 | 9,985 | |||||

| Indexes | 3,747 | 3,200 | |||||

| Securities | 3,994 | 3,045 | |||||

| Total for trading | 4,236,069 | 670,083 | |||||

| Hedge | |||||||

| Cash Flow | |||||||

| Interest Rate Swaps | 9,225 | ||||||

| Foreign Exchange Swaps | 23,502 | ||||||

| Fair Value | |||||||

| Interest Rate Swaps | 8,953 | ||||||

| Foreign Exchange Swaps | 2,608 | ||||||

| Total for hedge | 44,288 | ||||||

| Total Financial Instruments | 4,280,357 | 670,083 | |||||

| 5. Loan Portfolio | ||||

| The loan portfolio, by type of loan and currency, as of June 30, 2013, is constituted as follows: | ||||

| Amount | ||||

| Pesos | USD | UDIS | Total | |

| Current loan portfolio | ||||

| Commercial or business activities | 151,796 | 36,683 | 1 | 188,480 |

| Financial entities | 779 | 0 | 0 | 779 |

| Governmental entities | 18,373 | 12,592 | 0 | 30,965 |

| Commercial loans | 170,948 | 49,275 | 1 | 220,224 |

| Consumer loans | 63,464 | 0 | 0 | 63,464 |

| Mortgages | 70,472 | 883 | 1,432 | 72,787 |

| Total | 304,884 | 50,158 | 1,433 | 356,475 |

| 6. Past Due Loans | |||||

| Amount | |||||

| Pesos | USD | UDIS | Total | ||

| Commercial or business activities | 3,836 | 63 | 0 | 3,899 | |

| Commercial loans | 3,836 | 63 | 0 | 3,899 | |

| Past due consumer loans | 2,606 | 0 | 0 | 2,606 | |

| Past due mortgages | 1,906 | 229 | 245 | 2,380 | |

| Total | 8,348 | 292 | 245 | 8,885 | |

| The analysis of movements in past due loans from January 1 to June 30, 2013, is as follows: | |||||

| Balance as of December 31, 2012 | 6,093 | ||||

| Plus: Transfer from current loan portfolio to past due loans | 10,666 | ||||

| Collections | |||||

| Cash | (1,167) | ||||

| Normalization | (1,428) | ||||

| Awards | 0 | (2,595) | |||

| Restructured loans | (119) | ||||

| Charges off | (5,160) | ||||

| Balance as of June 30, 2013 | 8,885 | ||||

| 7. Allowances for loan losses | |||||||

| The movements in the provision for loan losses, from January 1 to June 30, 2013, are as follows: | |||||||

| Balance as of December 31, 2012 | 11,580 | ||||||

| Allowances created | 6,152 | ||||||

| Recovery credited to income in prior years | (28) | ||||||

| Charge-offs | (5,160) | ||||||

| Against capital allocation change Rating Methodology | 3,445 | ||||||

| Exchange rate effect on foreign currency | 0 | ||||||

| Balance as of June 30, 2013 | 15,989 | ||||||

The table below presents a summary of charge-offs by type of product as of June 30, 2013: | |||||||

| Product | Charge-offs | Debit Relieves | Total | % | |||

| First Quarter | |||||||

| Commercial Loans | 464 | 5 | 469 | 20% | |||

| Mortgage | 213 | 3 | 216 | 9% | |||

| Credit Card | 893 | 36 | 929 | 39% | |||

| Consumer loans | 765 | 21 | 786 | 33% | |||

| Total | 2,335 | 65 | 2,400 | 100% | |||

| Second Quarter | |||||||

| Commercial Loans | 519 | 10 | 529 | 19% | |||

| Mortgage | 102 | 14 | 116 | 4% | |||

| Credit Card | 1254 | 30 | 1284 | 47% | |||

| Consumer loans | 818 | 13 | 831 | 30% | |||

| Total | 2,693 | 67 | 2,760 | 100% | |||

| 2013 | |||||||

| Commercial Loans | 983 | 15 | 998 | 19% | |||

| Mortgage | 315 | 17 | 332 | 6% | |||

| Credit Card | 2147 | 66 | 2213 | 43% | |||

| Consumer loans | 1583 | 34 | 1617 | 31% | |||

| Total | 5,028 | 132 | 5,160 | 100% | |||

| Allowances for Loan Losses from the Commerce Fund | |||||||

| Pursuant to the Commission's authorization in Official Bulletin No. 601-I-DGSIF "C" - 38625 issued on March, 2001; as of June 30, 2013, there are MX$40 million in allowances for loan losses from the commerce fund, which resulted from the restructuring process of Grupo Financiero Santander. As of December 31, 2012, such allowances totaled Mx$ $55. | |||||||

| During the second quarter of 2013, the abovementioned allowances for loan losses had the following breakdown: | |||||||

| Mortgages and commercial loans charge-offs | (15) | (15) | |||||

| Udis reserves actualization and f/x effects | 0 | 0 | |||||

| (15) | (15) | ||||||

| As part of the Commission's authorization for these reserves, in case there are exit loan portfolio recoveries from previously charged off loans, these recoveries will be recorded in the income statement. During the second quarter of 2013, charges due to income statement due to recoveries of previously charge off loans amounted Mx$28. | |||||||

| 9. Programs of benefits to bank debtors with the support of the Federal Government. | |||

| As of June 30, 2013, the accounts receivable from the federal government are $349, regarding the early termination of benefit programs granted to bank debtors. | |||

| Early termination of the support programs for debtors |

On July 15, 2010, an Agreement for the early termination of the support programs for bank debtors (the “Agreement”) was entered into. The credit institutions considered to early terminate the following programs, which were created between years 1995- 1998, derived from restructuring of loans, as follows: 1. Support Program for Mortgages Debtors (Support Program); 2. Support Program for the Construction of Housing, in the stage of individual loans (Support Program), and 3. Agreement on benefits for Mortgages Debtors (Discounts Program) The credit institutions reached an agreement with the Mexican Treasury Department (Secretaría de Hacienda y Crédito Público (SHCP)) and the Commission. The banks were represented by the Mexican Bank’s Association (Asociación de Bancos de México, A.C. (ABM)) and it establishes that, for the correct application of the early termination agreement, the credit institutions are to be subject to the supervision and monitoring of the Commission, and they shall comply with all the comments and corrections made by such Commission and they shall deliver all the information requested by the Commission for the fulfillment of the agreement. Restructured loans or loans in UDIs granted under the Support Programs for debtors, loans in Mexican pesos; loans in Mexican pesos with right to receive the benefits of the Discounts Program and, loans that, as of December 31, 2010, were current, as well as past due loans that as of the aforementioned date, had been restructured, and those loans that, in order to continue in effect, received a write-off or discount, whatever the amount, were subject to the scheme of early termination, provided that evidence of payments was delivered. |

| 10. Average Interest Rates paid on deposits | |||

| The average interest rates paid on deposits during June, 2013, is as follows: | |||

| Pesos | USD | ||

| Average balance | 160,936 | 19,311 | |

| Interest | 1,282 | 3 | |

| Rate | 1.5840% | 0.0340% | |

| 11. Bank and other Loans | ||||||

| As of June 30, 2013, banks and other loans are constituted as follows: | ||||||

| Average | ||||||

| Liabilities | Amount | Rate | Maturity | |||

| Loans in Mexican pesos | ||||||

| Call money | 1,186 | 4.00% | 3 days | |||

| Bank loans | 1,505 | 5.00% | From 3 days to 5 days | |||

| Public fiduciary funds | 5,122 | 3.62% | From 2 days to 17 years | |||

| Government loans | 2,559 | 4.85% | From 1 day to 6 years | |||

| Total | 10,371 | |||||

| Loans in foreign currency | ||||||

| Foreign bank loans | 9,865 | 1.07% | From 88 days to 8 years | |||

| Call money | 6,113 | 0.39% | 3 days | |||

| Public fiduciary funds | 540 | 1.03% | From 1 day to 3 years | |||

| Development bank loans | 137 | 2.56% | From 4 days to 4 years | |||

| Total | 16,655 | |||||

| Total Loans | 27,026 | |||||

| Accrued Interests | 60 | |||||

| Total | 27,086 | |||||

| 12. Current and Deferred Taxes | ||

| Current taxes as of June 30, 2013 | ||

| Income Tax | 2,419 | |

| Deferred taxes | (2,072) | (1) |

| Total Bank | 347 | |

| Current-deferred taxes from other subsidiaries | 1,037 | |

| Total Financial Group | 1,383 | |

| (1) Deferred taxes are broken down as follows: | ||

| Global provision | (468) | |

| Fixed Asset | (91) | |

| Net effect from financial instruments | (1,730) | |

| Accrued Liabilities | 164 | |

| Other | 53 | |

| Total Bank | (2,072) | |

| Provision for loan losses of subsidiaries, net effect | (691) | |

| Others, subsidiaries | 140 | |

| Total deferred tax, Financial Group | (2,623) | |

| As of June 30, 2013, Deferred Assets are registered at 89.81% and Deferred Liabilities are registered at 100% | ||

| Remainder of global provisions and allowances for loan losses | 11,306 | |

| Other concepts | 5,081 | |

| Total Deferred Tax (net) | 16,388 | |

| Deferred taxes registered in balance sheet accounts | 14,672 | |

| Deferred taxes registered in memorandum accounts | 1,716 | |

| 13. Other operating income (expenses) | |

| The main items that constitute the balance of Other Income (Expenses) account, as of June 30, 2013, are the following: | |

| Concept: | |

| Recoveries of previously charged-off loans | 1,001 |

| Write-offs of liabilities and reserves | 151 |

| Profit from sale of foreclosed assets | 68 |

| Interests on employees' loans | 63 |

| Technical Advisory | 51 |

| Expenses on collections | (228) |

| Write-offs | (282) |

| Provisions for legal and fiscal contingencies | (28) |

| Foreclosed assets reserve | (13) |

| Provision and payments to IPAB (Indemnity) | (6) |

| Others | 93 |

| 870 | |

| 14. Capitalization Ratio | |||

| Banco Santander (México), S.A. |

| Table I.1 | ||

| Form for the disclosure of capital of paid-in capital without considering transiency in the application of adjustments in the regulation | ||

| Reference | Capital Description | Capital |

| Level 1 (CET 1) Ordinary capital: Instruments and reserves | ||

| 1 | Ordinary shares that qualify for level 1 Common Capital plus corresponding premium | 34,798 |

| 2 | Results from previous fiscal years | 48,517 |

| 3 | Other elements of comprehensive income (and other reserves) | 18,055 |

| 4 | Capital subject to gradual elimination of level 1 ordinary capital (only applicable for companies that are not lined to shares) | |

| 5 | Ordinary shares issued by subsidiaries held by third parties (amount allowed in level 1 ordinary capital) | |

| 6 | Level 1 ordinary capital before adjustments to regulation | 101,370 |

| Level 1 Ordinary capital: adjustments to regulation | ||

| 7 | Adjustments due to prudential valuation | |

| 8 | Commercial credit (net of its corresponding deferred profit taxes debited) | 1,589 |

| 9 | Other intangibles other than rights to mortgage rights (net of its corresponding deferred profit taxes debited) | 1,962 |

10 (conservative) | Deferred taxes to profit credited relying on future income excluding those that derive from temporary differences (net of deferred profit taxes debited) | 0 |

| 11 | Results of valuation of cash flow hedging instruments | 0 |

| 12 | Reserves to be constituted | 0 |

| 13 | Benefits over remnant of securitization transactions | 0 |

| 14 | Losses and gains caused for the changes in credit rating of liabilities assessed at a reasonable value | |

| 15 | Pension plan for defined benefits | 0 |

16 (conservative) | Investments in proprietary shares | 7 |

17 (conservative) | Reciprocal investments in ordinary capital | 0 |

18 (conservative) | Investments in capital of banks, financial institutions and insurance companies out of the reach of the regulation consolidation, net of short eligible positions, wherein the institution does not hold more than 10% of the issued capital (amount that exceeds the 10% threshold) | 27 |

19 (conservative) | Significant investments in ordinary shares of banks, financial institutions and insurance companies out of the scope of the regulation consolidation, nets of eligible short positions, wherein the institutions holds more than 10% of the issued capital (amount that exceeds the 10% threshold) | 0 |

20 (conservative) | Rights for mortgage services (amount exceeding the 10% threshold) | 0 |

| 21 | Deferred taxes to profit credited resulting from temporary differences (amount exceeding the 10% threshold, net of deferred taxes debited) | 1,056 |

| 22 | Amount exceeding the 15% threshold. | |

| 23 | of which: significant investments wherein the institution holds more than 10% of ordinary shares of financial institutions | |

| 24 | of which: rights for mortgage services | |

| 25 | of which: Taxes to profit Deferred credited deriving from temporary differences | |

| 26 | National regulation adjustments | 20,655 |

| A | of which: Other elements of wholesome profit (and other reserves) | 0 |

| B | of which: investments in subordinated debt | 0 |

| C | of which: profit or increase in the value of assets from the purchase of securitization positions (Originating Institutions) | 0 |

| D | of which: investments in multilateral entities | 0 |

| E | of which: investments in related corporations | 17,727 |

| F | of which: investments in risk capital | 0 |

| G | of which: investments in investment corporations | 0 |

| H | of which: Funding for the purchase of proprietary shares | 0 |

| I | of which: Transactions in breach of provisions | 0 |

| J | of which: Deferred charges and installments | 718 |

| K | of which: Positions in First Losses Schemes | 0 |

| L | of which: Worker's Deferred Profit Sharing | 0 |

| M | of which: Relevant Related Persons | 0 |

| N | of which: Pension plan for defined benefits | 0 |

| O | of witch: Adjustment for capital acknowledgment | 0 |

| P | of which: investments in Clearing Houses | 2,210 |

| 27 | Regulation adjustments that apply to level 1 common stock due to level 1 capital shortage and level 2 capital to cover deductions | 0 |

| 28 | Total regulation adjustments to level 1 Common Capital | 25,295 |

| 29 | Level 1 Common Capital (CET1) | 76,074 |

| Level 1 additional capital: instruments | ||

| 30 | Instruments directly issued that qualify as level 1 additional capital, plus premium | 0 |

| 31 | of which: Qualify as capital under the applicable accounting criteria | 0 |

| 32 | of which: Qualify as liability under the applicable accounting criteria | |

| 33 | Capital instruments directly issued subject to gradual elimination of level 1 additional capital | 0 |

| 34 | Instruments issued of level 1 additional capital and level 1 Common Capital instruments that are not included in line 5 issued by subsidiaries held by third parties (amount allowed at additional level 1) | 0 |

| 35 | of which: instruments issued by subsidiaries subject to gradual elimination | |

| 36 | Level 1 additional capital before regulation adjustments | 0 |

| Level 1 additional capital: regulation adjustments | ||

37 (conservative) | Investments in held instruments of level 1 additional capital | |

38 (conservative) | Investments in reciprocal shares in level 1 additional capital instruments. | |

39 (conservative) | Investments in capital of banks, financial institutions and insurance companies out of the scope of the regulation consolidation, net of short eligible positions, wherein the institution holds more than 10% of the issued capital |

40 (conservative) | Significant investments in ordinary shares of banks, financial institutions and insurance companies out of the scope of the regulation consolidation, nets of eligible short positions, wherein the institutions holds more than 10% of the issued capital | |

| 41 | National regulation adjustments | 0 |

| 42 | Regulation adjustments that apply to level 1 common stock due to level 1 capital shortage and level 2 capital to cover deductions | |

| 43 | Total regulation adjustments to level 1 additional Common Capital | 0 |

| 44 | Level 1 additional capital (AT1) | 0 |

| 45 | Level 1 capital (T1 = CET1 + AT1) | 76,074 |

| Level 2 capital: instruments and reserves | ||

| 46 | Instruments directly issued that qualify as level 2 capital, plus premium | 0 |

| 47 | Capital instruments directly issued subject to gradual elimination of level 2 capital. | 0 |

| 48 | Level 2 capital instruments and level 1 Common Capital instruments and level 1 additional capital that has not been included in lines 5 or 34, which have been issued by subsidiaries held by third parties (amount allowed in level 2 completer capital) | 0 |

| 49 | of which: instruments issued by subsidiaries subject to gradual elimination | 0 |

| 50 | Reserves | 0 |

| 51 | Level 2 capital before regulation adjustments | 0 |

| Level 2 capital : regulation adjustments | ||

52 (conservative) | Investments in own instruments of level 2 capital | |

53 (conservative) | Reciprocal investments in level 2 capital instruments | |

54 (conservative) | Investments in capital of banks, financial institutions and insurance companies out of the scope of the regulation consolidation, net of short eligible positions, wherein the institution does not hold more than 10% of the issued capital (amount exceeding the 10% threshold) | |

55 (conservative) | Significant investments in ordinary shares of banks, financial institutions and insurance companies out of the scope of the regulation consolidation, nets of eligible short positions, wherein the institutions holds more than 10% of the issued capital | |

| 56 | National regulation adjustments | 0 |

| 57 | Total regulation adjustments to level 2 capital | 0 |

| 58 | Level 2 capital (T2) | 0 |

| 59 | Total stock (TC = T1 + T2) | 76,074 |

| 60 | Assets weighted by total risk | 498,996 |

| Capital reasons and supplements | ||

| 61 | Level 1 Common Capital (as percentage of assets weighted by total risks) | 15.25% |

| 62 | Level 1 Stock (as percentage of assets weighted by total risks) | 15.25% |

| 63 | Total capital (as percentage of assets weighted by total risks) | 15.25% |

| 64 | Institutional specific supplement (must at least consist of: the level 1 Common Capital requirement plus the capital maintenance cushion, plus the countercyclical cushion, plus G-SIB cushion; expressed as percentage of the assets weighted by total risks) | 7.00% |

| 65 | of which: Supplement of capital preservation | 2.50% |

| 66 | of which: Supplement of specific bank countercyclical | |