united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22718

Two Roads Shared Trust

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

Richard Malinowski, Gemini Fund Services, LLC.

4221 North 203rd Street, Suite 100, Elkhorn, NE 68022

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 10/31

Date of reporting period: 10/31/20

ITEM 1. REPORTS TO SHAREHOLDERS.

| |

| Annual Report | |

| October 31, 2020 | |

Conductor Global Equity Value Fund

| Class A | RAALX |

| Class C | RACLX |

| Class I | RAILX |

| Class Y | RAYLX |

Conductor International Equity Value Fund

| Class A | RIALX |

| Class I | RIYLX |

| www.conductorfunds.com | |

| 1-844-GO-RAILX (1-844-467-2459) | |

| This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which contains information about each Fund’s investment objective, risks, fees and expenses. Investors are reminded to read the prospectus carefully before investing in a Fund. | |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website www.conductorfunds.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically or to continue receiving paper copies of shareholder reports, which are available free of charge, by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by following the instructions included with paper Fund documents that have been mailed to you.

December 2020

First, let us begin by welcoming you to the seventh yearly update for the Conductor Global Equity Value Fund, (the “Global Fund”) and for the recently launched Conductor International Equity Value Fund (the “International Fund” and together with Global Fund, each a “Fund” and collectively the “Funds”). We always look forward to keeping you updated regularly on the status of the various positions in the portfolios and the global market and economic trends that affect our positioning.

FY 2020 has been defined almost exclusively by the Covid-19 pandemic, which ushered in extraordinary market volatility and whiplash-inducing economic swings around the globe. Throw in one of the most contentious election cycles in American history, and investors were subject to a market backdrop without parallel. Relative performance in many of our target equity market segments once again lagged as the trends pushing against global and value remained on the same pathway observed over the past several years. The uncertainty and fear surrounding Covid and its broader economic impact continued to weigh on international stocks, which underperformed those in the United States, though emerging market stocks, entering the fiscal year near historic low valuations, showed signs of life towards the end of the fiscal year. Global value stocks, which have underperformed for the better part of the last decade, seemed to be affected most by pandemic-induced fear and uncertainty. Weak relative performance trends for value actually accelerated through most of the year as investors sought the “certainty” of large -cap technology haven names despite the, by many measure, historic valuation gulf between value and growth. Steadfast as ever, we still believe that value remains positioned to outperform growth in coming years and that international stocks are positioned to outperform US stocks. Value stocks remain significantly and historically undervalued relative to growth stocks. International stocks, whether emerging or developed market, remain significantly undervalued compared to their US counterparts on a historical basis.

From 11/1/2019 to 10/31/2020, the MSCI World Index was up 4.95%, while the MSCI All Country World Index was up 5.45%. The Global Fund’s Benchmark, the MSCI All Country World Value Index was down -11.50%, while the MSCI All Country World Growth Index was up 23.41%. The MSCI All Country Small and Mid -Cap Index was up 1.04% versus 6.25% for the MSCI All Country Large-Cap Index. The MSCI EAFE, covering ex-US developed countries, was down -6.36%, while the MSCI Emerging Markets Index was up 8.59%. The S&P 500 was up 9.70%. Over the same period, the Conductor Global Equity Value Fund Class Y was down -14.27%.

The International Fund Class I was launched on 12/3/2019. Between 12/3/19 and 10/31/20 the International Fund was down -15.15% versus -2.34% for the MSCI All Country World ex USA index and -14.98% for the MSCI All Country World ex USA Value index.

1

Disclosures:

The referenced indices are shown for general market comparisons and are not meant to represent the Funds. Investors cannot directly invest in an index; unmanaged index returns do not reflect any fees, expenses or sales charges.

The Funds’ maximum sales charge for Class “A” shares is 5.75%. The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that investor’s shares, when redeemed, may be worth more or less than their original cost. The Funds’ investment adviser has contractually agreed to reduce its fees and/or absorb expenses of each Fund, at least until March 1, 2021, to ensure that each of the Fund’s total annual operating expenses (exclusive of any front -end or contingent deferred loads; brokerage fees and commissions; expenses of other investment companies in which the Fund may invest (“acquired fund fees and expenses”); borrowing costs, such as interest and dividend expense on securities sold short; taxes; and extraordinary expenses, such as litigation expenses) will not exceed 2.15%, 2.90%, 1.90%, and 1.25% of average daily net assets attributable to Global Fund Class A, Class C, Class I, and Class Y shares, respectively; and 1.45% and 1.20% of the average daily net assets attributable to International Fund Class A and Class I shares, respectively. These expense reimbursements are subject to possible recoupment from Funds in future years on a rolling three -year basis (within the three years after the fees have been waived or reimbursed) if such recoupment can be achieved without exceeding the foregoing expense limits as well as any expense limitation that was in effect at the time the reimbursement was made. Please review the funds’ prospectus for more information regarding the funds’ fees and expenses. For performance information current to the most recent month-end, please call toll-free 844-467-2459 or by visiting www.conductorfunds.com.

The views in this report are those of the Funds’ management. This report contains certain forward-looking statements about factors that may affect the performance of the funds in the future. These statements are based on the Funds’ management’s predictions and expectations concerning certain future events, such as the performance of the economy on the whole and of specific industry sectors. Management believes these forward-looking statements are reasonable, although they are inherently uncertain and difficult to predict.

2

Global Year in Review:

In essence, one issue alone dominated global market discussion this year: the devastating Covid-19 pandemic. Once news of the pandemic and its spread around the world took hold in mid to late February 2020, investors were subjected to market whipsaws and news-flow whipsaws unprecedented excepting the worst days of the 2008/2009 global financial crisis, or the days surrounding the market crash of 1987. Immediately, talk pivoted towards lockdowns, healthcare treatments, vaccines, hospital capacity, business survivability within highly affected industries, government stimulus, bailouts, central bank accommodation, and political polarization. At its lowest on March 23rd, the MSCI ACWI Index was down over 30% from 2019 calendar year end levels. The rebound rally for this Index from those lows to the end of the 2020 fiscal year exceeded 45%. Amidst it all, volatility measures, such as the VIX index in the US, reached levels observed only during the very worst moments of the global financial crisis.

Of course, the uncertainty in markets captured in the wild swings of index returns and volatility indicators was merely a reflection of the wild swings occurring in global macroeconomic headline indicators. GDP numbers declined at rates never seen before around the globe during CY Q2, only to rebound during the ensuing months at an unprecedented pace (though as of October 31, 2020 global GDP remains below the levels of Q4:2019). Global trade flows collapsed. Certain industries, such as those focused on home delivery and convenience, benefitted mightily, while others, such as those focused on the global hospitality industry, were driven to the point of insolvency.

Governments and central banks around the globe opened the fiscal and monetary spigots in quick order, perhaps saving the global economy from a far worse outcome, though many economists still ponder whether enough firepower has been directed towards the crisis. The United States government approved more than $ 2 trillion, approximately 11% of GDP, in aid towards individuals and businesses. The Federal Reserve provided extraordinary assistance to maintain liquidity in fixed income and money markets. The United Kingdom approved close to $ 100 billion in spending to shore up health services and businesses. Across the European Union, governments approved well over a trillion euros worth of stimulus. The European Central Bank, like its American counterpart, worked diligently to maintain accommodative monetary conditions. Global equity markets took their cues from the extraordinary response and rebounded accordingly. These strong global equity market gains during the back portion of the fiscal year, however, obscure an economic backdrop that remains just as confusing and uncertain as the situation early in the crisis. And, certain dislocations that were present in global equity markets prior to the crisis, such as significantly over-extended valuation metrics in many corners of the world (especially the US) and wide performance differentials between various sub-components such as value and growth stocks, only became more dislocated as the crisis unfolded. Broader macroeconomic and societal dislocations and problem subjects such as widening income stratification, mega-cap tech companies’ roles in the

3

global economy, the urban/rural skills divide in many countries, and the relationship between economic superpowers China and the US have only become more complicated and contentious as Covid continues to upend the economic and political order.

Coming into the 2020 fiscal year, as pointed out in last year’s letter, global macroeconomic trends were already softening, corporate earnings had already plateaued, and valuations in places like the United States were already reaching unsustainable levels. Even with vaccines potentially ready to mitigate the worst of the crisis, US (especially) and international equity markets face headwinds, valuation and otherwise, that we believe will be difficult to shake off even under the most favorable political and societal conditions. Lo and behold, the US finds itself emerging from one of the most contentious and, perhaps, strangest election and post-election periods in its modern history. Across the Atlantic, as of this writing, Brexit negotiations between the UK and the EU remain as twisted as ever. Of course, the new US administration and Congress could find a path towards compromise and kumbaya, and the EU and UK could come up with a long-lasting face and trade -saving deal in the coming days and weeks, but it’s just as easy, we feel, to foresee a period of significant distrust and acrimony in Washington and significant fracturing between the EU and UK, and within the EU itself. These two economic blocs represent a significant portion of global GDP and market-cap. Against that backdrop, we’re inclined to say that volatility will remain a feature of global equity markets going forward. As we’re required to do, we’ll continue to invest our capital in value -oriented names. We believe that now, more than ever, value is in a unique position to provide substantial and superior risk-adjusted returns over the next several years, whether markets continue the current smooth sailing trend or re-enter treacherous waters.

4

Conductor Global: Portfolio Positioning

Below, we provide the sector and geographic exposure breakdowns for the Global Fund portfolio, both at fiscal year-end 2019 and fiscal year-end 2020. Of note, we break out the sector and geographic exposures embedded in any ETF exposure to show the true risk allocations and exposures. We also include the sector and geographic performance data for the MSCI All Country World Index (the “ACWI”) as a frame of reference rather than MSCI World. Like our portfolio, the ACWI has exposure to Emerging markets while the MSCI World does not.

| Sector 10/31/19 | Fund Portfolio % | ACWI % | Differential |

| Cash | 9.07% | 0.45% | 8.62% |

| Consumer Disc. | 14.76% | 10.86% | 3.90% |

| Consumer Staples | 3.69% | 8.37% | -4.68% |

| Energy | 4.24% | 5.25% | -1.01% |

| Financials/RE | 12.72% | 19.94% | -7.22% |

| Health Care | 2.66% | 11.53% | -8.87% |

| Industrials | 10.56% | 10.13% | 0.43% |

| Info Tech | 18.82% | 16.54% | 2.28% |

| Materials | 4.07% | 4.68% | -0.61% |

| Communication Svcs | 8.51% | 8.79% | -0.28% |

| Utilities | 10.90% | 3.46% | 7.44% |

| Sector 10/31/20 | Fund Portfolio % | ACWI % | Differential |

| Cash | 31.24% | 0.33% | 30.91% |

| Consumer Disc. | 18.20% | 13.05% | 5.15% |

| Consumer Staples | 2.39% | 7.81% | -5.42% |

| Energy | 1.04% | 2.74% | -1.70% |

| Financials/RE | 2.80% | 15.40% | -12.60% |

| Health Care | 1.39% | 12.28% | -10.89% |

| Industrials | 8.91% | 9.55% | -0.64% |

| Info Tech | 9.96% | 21.14% | -11.18% |

| Materials | 18.70% | 4.79% | 13.91% |

| Communication Svcs | 1.79% | 9.72% | -7.93% |

| Utilities | 3.57% | 3.18% | 0.39% |

5

| ACWI Sector Performance 10/31/19 to 10/31/20 | Performance % |

| Consumer Disc. | 24.52% |

| Consumer Staples | 0.26% |

| Energy | -41.72% |

| Financials | -17.79% |

| Real Estate | -15.10% |

| Health Care | 10.79% |

| Industrials | -1.82% |

| Info Tech | 33.35% |

| Materials | 7.45% |

| Communication Svcs | 16.50% |

| Utilities | -1.56% |

| Region 10/31/19 | Fund Portfolio % | ACWI % | Differential |

| Africa/Mid East | 4.21% | 1.20% | 3.01% |

| Asia Pacific | 40.54% | 18.57% | 21.97% |

| Central Asia | 0.71% | 0.99% | -0.28% |

| Eastern Europe | 0.37% | 0.73% | -0.36% |

| North America | 20.77% | 56.92% | -36.15% |

| South/Central Am. | 9.13% | 1.17% | 7.96% |

| Western Europe | 15.49% | 20.11% | -4.62% |

| Not Classified | 8.79% | 0.30% | 8.49% |

| Region 10/31/20 | Fund Portfolio % | ACWI % | Differential |

| Africa/Mid East | 0.00% | 1.13% | -1.13% |

| Asia Pacific | 40.25% | 19.50% | 20.75% |

| Central Asia | 0.00% | 1.03% | -1.03% |

| Eastern Europe | 1.11% | 0.50% | 0.61% |

| North America | 18.15% | 59.45% | -41.30% |

| South/Central Am. | 3.57% | 0.81% | 2.76% |

| Western Europe | 5.69% | 17.40% | -11.71% |

| Not Classified | 31.24% | 0.19% | 31.05% |

6

| ACWI Region Performance 10/31/19 to 10/31/20 (USD) | Performance % |

| United States (S&P 500) | 9.70% |

| Europe | -8.71% |

| Japan | -2.61% |

| Asia AC ex-Japan | 16.16% |

| EM Latin America | -32.94% |

Portfolio Positioning and Relative Performance Observations:

As a reminder, the investment process for adding individual equities to the Global Fund is not thematically oriented but focused on quantitative fundamental metrics. The Global Fund screens global equities using a variety of traditional cash flow, income statement, and balance sheet ratios and adds companies exhibiting valuation ratios at levels below the overall levels for the relevant global indices. The typical portfolio company, we believe, also exhibits lower quantitative probabilities for bankruptcy (i.e. better balance sheet health) at time of entry than the median company in global Indices. In an attempt to avoid “value traps” and manage risk, the Global Fund also employs momentum-based technical rules to assist with stock selection. Likewise, technical rules help govern when positions should be removed from the portfolio. Finally, the Global Fund employs a top down model incorporating macroeconomic data, valuation data, and index-level technical data to assess overall market risk. During times of extremely high risk, the Adviser believes, although there are no guarantees, that the Global Fund has the capability of significantly reducing risk exposures. Overall, the shifts in exposures listed above and briefly described below are simply governed by the models we employ, not any qualitative judgment by the portfolio manager as to which sectors or geographies should out or underperform in the future.

SECTOR

| ● | Over the course of FY 2020, the Fund saw the biggest exposure reductions in the Info Tech and Financials sectors, with the biggest increases in Materials and Consumer Discretionary. The Covid stimulus/reflationary trade significantly improved the relative performance opportunities for the beaten-down materials sector, which resulted in increased allocation. A similar dynamic played out with beaten down consumer discretionary names, particularly in the global retail industry. The Global Fund exited a number of the value-oriented tech names during the more volatile days of the Covid crisis. Because the IT sector in general holds the highest valuations of any sector, exposure remained low as the year progressed. We expect this to remain the case. The financial sector remains inexpensive long-term when compared to historical valuation levels, but poor relative strength/performance has kept the Global Fund from significantly increasing the allocation to this point. Nonetheless, because of the inherent value |

7

characteristics of the Financials sector, we expect exposure to increase in the coming quarters. Energy is another value-oriented sector that could see a material increase in allocation in the future.

| ● | In regard to sector attribution relative to the MSCI All Country World Index, the Consumer Discretionary and Information Technology Sectors cost the portfolio 6% and 5% respectively in relative performance. Much of the poor performance in Consumer Discretionary reflected poor performance of many names through the crisis. Improved performance among Consumer Discretionary names later in the fiscal year mitigated some of the relative performance deficit. In the case of the Info Tech sector’s negative contribution, Global Fund under-allocation to large-cap growth technology names during the year significantly curtailed overall performance relative to the benchmark. Underweight positioning in Financials and Energy added approximately 2% points in relative performance. The standout performer during the fiscal year was the Materials sector; the overweight there, combined with solid stock selection, added approximately 3% points in relative performance. The biggest drag of all, however, was the much larger than benchmark cash position, which cost the portfolio approximately 7% in relative performance. |

GEOGRAPHY

| ● | In terms of geographic allocation, since the beginning of FY 2020, the Global Fund has been significantly underweight US and European equities relative to benchmark, and significantly overweight Asia/Pacific equities. Overall, the Global Fund has been overweight international equities generally. As mentioned above, the Global Fund has maintained a substantial cash position throughout the year, mostly at the expense of US exposure. Going forward, we expect to maintain a significant underweight to US equities owing to the fact that US equity indices remain the most overvalued top-level indices globally. We expect Asia/Pacific to remain a core part of the portfolio and anticipate more Europe exposure. |

| ● | Looking at attribution from a geographic perspective, North American/US stocks were the biggest weight on relative performance against global benchmarks, costing the portfolio over six percentage points in relative performance, mostly due to the very strong performance of US equities and the Global Fund’s significant underweight positioning. The Global Fund’s overweight in South/Central American stocks through the year cost the portfolio approximately 2% in relative performance. As mentioned above, excess cash cost the portfolio approximately 7% points in relative performance. |

8

Conductor International: Portfolio Positioning

Below, we provide the sector and geographic exposure breakdowns for the International Fund, both at inception on December 3, 2019 and at fiscal year-end 2020 (10/31/20). Of note, we break out the sector and geographic exposures embedded in any ETF exposure to show the true risk allocations and exposures. We also include the sector and geographic performance data for the MSCI All Country World ex-US Index (the “ACWI ex-US”) as a frame of reference rather than MSCI World ex-US index. Like our portfolio, the ACWI has exposure to Emerging markets while the MSCI World does not.

| Sector 12/03/19 | Fund Portfolio % | ACWI ex-US % | Differential |

| Cash | 0.72% | 0.47% | 0.25% |

| Consumer Disc. | 25.59% | 11.84% | 13.75% |

| Consumer Staples | 3.55% | 9.56% | -6.01% |

| Energy | 1.71% | 6.37% | -4.66% |

| Financials/RE | 6.72% | 24.54% | -17.82% |

| Health Care | 5.34% | 8.85% | -3.51% |

| Industrials | 12.33% | 11.98% | 0.35% |

| Info Tech | 24.04% | 9.16% | 14.88% |

| Materials | 10.62% | 7.25% | 3.37% |

| Communication Svcs | 3.15% | 6.64% | -3.49% |

| Utilities | 6.24% | 3.34% | 2.90% |

| Sector 10/31/20 | Fund Portfolio % | ACWI ex-US % | Differential |

| Cash | 30.04% | 0.43% | 29.61% |

| Consumer Disc. | 10.70% | 14.36% | -3.66% |

| Consumer Staples | 2.32% | 9.48% | -7.16% |

| Energy | 1.95% | 3.99% | -2.04% |

| Financials/RE | 6.49% | 19.73% | -13.24% |

| Health Care | 3.69% | 9.93% | -6.24% |

| Industrials | 11.11% | 11.52% | -0.41% |

| Info Tech | 8.62% | 11.62% | -3.00% |

| Materials | 16.31% | 7.77% | 8.54% |

| Communication Svcs | 4.47% | 7.83% | -3.36% |

| Utilities | 4.29% | 3.34% | 0.95% |

9

| ACWI ex-US Sector Performance 12/03/19 to 10/31/20 | Performance % |

| Consumer Disc. | 13.17% |

| Consumer Staples | -2.97% |

| Energy | -37.52% |

| Financials | -19.31% |

| Health Care | 6.68% |

| Industrials | -4.21% |

| Info Tech | 21.87% |

| Materials | 4.89% |

| Communication Svcs | 14.28% |

| Utilities | 0.16% |

| Region 12/03/19 | Fund Portfolio % | ACWI ex-US % | Differential |

| Africa/Mid East | 3.14% | 2.72% | 0.42% |

| Asia Pacific | 57.92% | 41.96% | 15.96% |

| Central Asia | 0.89% | 2.43% | -1.54% |

| Eastern Europe | 0.51% | 1.53% | -1.02% |

| North America | 2.00% | 7.50% | -5.50% |

| South/Central Am. | 11.86% | 2.42% | 9.44% |

| Western Europe | 23.04% | 41.10% | -18.06% |

| Not Classified | 0.65% | 0.35% | 0.30% |

| Region 10/31/20 | Fund Portfolio % | ACWI ex-US % | Differential |

| Africa/Mid East | 1.02% | 2.73% | -1.71% |

| Asia Pacific | 44.31% | 46.51% | -2.2% |

| Central Asia | 1.04% | 2.48% | -1.44% |

| Eastern Europe | 0.37% | 1.19% | -0.82% |

| North America | 4.58% | 6.92% | -2.34% |

| South/Central Am. | 3.96% | 1.70% | 2.26% |

| Western Europe | 14.72% | 38.09% | -23.37% |

| Not Classified | 30.00% | 0.37% | 29.63% |

| ACWI Region Performance 12/03/19 to 10/31/20 (USD) | Performance % |

| Europe | -8.63% |

| Japan | -4.83% |

| Asia AC ex-Japan | 16.06% |

| EM Latin America | -30.31% |

| EM Africa/Mid East | -16.66% |

10

Portfolio Positioning and Relative Performance Observations:

As a reminder, the investment process for adding individual equities to the International Fund is not thematically oriented but focused on quantitative fundamental metrics. The International Fund screens global equities using a variety of traditional cash flow, income statement, and balance sheet ratios and adds companies exhibiting valuation ratios at levels below the overall levels for the relevant global indices. The typical portfolio company, we believe, also exhibits lower quantitative probabilities for bankruptcy (i.e. better balance sheet health) at time of entry than the median company in global indices. In an attempt to avoid “value traps” and manage risk, the International Fund also employs momentum-based technical rules to assist with stock selection. Likewise, technical rules help govern when positions should be removed from the portfolio. Finally, the International Fund employs a top down model incorporating macroeconomic data, valuation data, and index-level technical data to assess overall market risk. During times of extremely high risk, the Adviser believes the Fund has the capability of significantly reducing risk exposures. Overall, the shifts in exposures listed above and briefly described below are simply governed by the models we employ, not any qualitative judgment by the portfolio manager as to which sectors or geographies should out or underperform in the future.

SECTOR

| ● | Over the course of the period from its inception through October 31, 2020, the International Fund saw the biggest exposure reductions in the Info Tech and Consumer Discretionary sectors, with the biggest increases in Materials and Communication Services. The Covid stimulus/reflationary trade significantly improved the relative performance opportunities for the beaten-down materials sector, which resulted in increased allocation. The reduction in consumer discretionary stocks was a stark contrast with the Global Fund; the primary reason that the International Fund didn’t maintain the same exposures to Consumer Discretionary mainly comes down to the fact that many of the positive trends in those stocks took place in the US. The International Fund exited a number of the value-oriented tech names during the more volatile days of the Covid crisis. Because the IT sector in general holds the highest valuations of any sector, exposure remained low as the fiscal period progressed. We expect this to remain the case. The financial sector remains inexpensive long-term when compared to historical valuation levels, but poor relative strength/performance has kept the International Fund from significantly increasing the allocation to this point. Nonetheless, because of the inherent value characteristics of the Financials sector, we expect exposure to increase in the coming quarters. Energy is another value- oriented sector that could see a material increase in allocation in the future. |

| ● | In regard to sector attribution relative to the MSCI All Country World ex-US Index, the Consumer Discretionary sector cost the portfolio 7% in relative performance, by far the most negative sector in that regard. Like the Global Fund, high cash levels |

11

cost the International Fund performance as markets rallied into the end of the fiscal period. In the case of the International Fund, cash drag cost the portfolio approximately 3.5% of relative performance. Much of the poor performance in Consumer Discretionary reflected poor performance of many names through the crisis. Improved performance among Consumer Discretionary names later in the fiscal year mitigated some of the relative performance deficit. Underweight positioning in Financials added approximately 2.5% points in relative performance. The standout performer, during the fiscal period was the Materials sector; the overweight there, combined with solid stock selection, added approximately 3% points in relative performance.

GEOGRAPHY

| ● | In terms of geographic allocation, since its inception, the International Fund has been significantly underweight European equities relative to benchmark, and generally overweight Asia/Pacific equities. The International Fund maintained a substantial cash position from its inception through October 31, 2020. Going forward, we expect Asia/Pacific equities to remain a core part of the portfolio and anticipate an increase in Europe exposure. |

| ● | Looking at attribution from a geographic perspective, core European equities were the biggest weight on relative performance for the International Fund against the international benchmark, costing the portfolio approximately 3.5 percentage points in relative performance, The International Fund’s overweight in South/Central American stocks through the period cost the portfolio approximately 1.5% in relative performance. Excess cash cost the portfolio approximately 3.5% points in relative performance. Exposure to Eastern Europe and Central Asia very slightly contributed positively to relative performance, the only regions to do so. |

12

Portfolio Characteristics

The portfolios as currently constructed (12/7/20) continue to reflect our value and quality orientations. The gaps between portfolio and benchmark valuation metrics have actually widened over the past year. Weighted average levels for portfolio and benchmark valuation metrics (since portfolio inception) can be found in the following table:

| Valuation Metric | Global Fund Portfolio | ACWI |

| EV/EBITDA, TTM | 7.37x | 15.89x |

| Price to Book | 1.47x | 2.75x |

| Price to Earnings, TTM | 17.62x | 31.53x |

| Price to Cash Flow, TTM | 5.75x | 13.14x |

| Price to Sales | 0.63x | 2.05x |

| Debt to Equity | 50.42% | 151.24% |

| Dividend Yield | 4.05% | 1.87% |

| Valuation Metric | International Fund Portfolio | ACWI ex-US |

| EV/EBITDA, TTM | 9.53x | 13.06x |

| Price to Book | 1.62x | 1.86x |

| Price to Earnings, TTM | 23.49x | 33.58x |

| Price to Cash Flow, TTM | 9.03x | 10.27x |

| Price to Sales | 0.90x | 1.48x |

| Debt to Equity | 84.75% | 166.40% |

| Dividend Yield | 3.27% | 2.31% |

13

Disclosures:

Investing in each of the Funds carries certain risks. Adverse changes in currency exchange rates may erode or reverse any potential gains from each of the Fund’s investments. The risk of investing in emerging market securities, primarily increased foreign investment risk. Investments in foreign securities could subject the Funds to greater risks including currency fluctuation, economic conditions, and different governmental and accounting standards. There is a risk that issuers and counterparties will not make payments on securities and other investments held by the Funds, resulting in losses to the Funds. Investments in lesser-known, small and medium capitalization companies may be more vulnerable than larger, more established organizations. There can be a higher portfolio turnover due to active and frequent trading that may result in higher transactional and brokerage costs. The Adviser from time to time employs various hedging techniques. The success of each of the Fund’s hedging strategy will be subject to the Adviser’s ability to correctly assess the degree of correlation between the performance of the instruments used in the hedging strategy and the performance of the investments in the portfolio being hedged. The risk on a short sale is the risk of loss if the value of a security sold short increases prior to the delivery date, since the Funds must pay more for the security than it received from the purchaser in the short sale. Therefore, the risk of loss may be unlimited.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds. This and other information about each Fund is contained in the prospectus and should be read carefully before investing. The prospectus for the funds can be obtained by calling toll free 1- 844-GO-RAILX or www.conductorfunds.com. The Funds are distributed by Northern Lights Distributors, LLC., Member FINRA/SIPC IronHorse Capital Management and Northern Lights Distributors, LLC are not affiliated.

14

Definitions:

ETF: The Funds invest in exchange traded funds (ETFs) and performance is subject to underlying investment weightings which will vary. ETFs are subject to expenses, which will be indirectly paid by the Funds. The cost of investing in a Fund that invests in ETFs will generally be higher than the cost of investing in a Fund that invests directly in individual stocks and bonds.

Asset allocation is an investment strategy that aims to balance risk and reward by apportioning a portfolio’s assets according to an individual’s goals, risk tolerance, and investment horizon. The three main asset classes - equities, fixed-income, and cash and equivalents - have different levels of risk and return, so each will behave differently over time.

MSCI World Index: The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 23 developed market country indexes: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States.

The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI consists of 46 country indexes comprising 23 developed and 23 emerging market country indexes. The developed market country indexes included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indexes included are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

S&P 500 Index: The S&P 500 Index is a broad-based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general.

MSCI Emerging Markets Index: The MSCI Emerging Markets Index is a free float- adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

15

MSCI Europe Index: The MSCI Europe Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the developed markets in Europe. The MSCI Europe Index consists of the following 15 developed market country indexes: Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom.

MSCI Index Variants

The MSCI Global Standard Indexes include large and mid-cap segments and provide exhaustive coverage of these size segments. The indexes target a coverage range of around 85% of the free float-adjusted market capitalization in each market. The Large Cap Indexes target a coverage range of around 70% of the free float-adjusted market capitalization in each market and the Mid Cap Indexes target a coverage range of around 15% of the free float-adjusted market capitalization in each market.

The MSCI Global Small Cap Indexes provide an exhaustive representation of the small cap size segment. The indexes target companies that are in the Investable Market Index (IMI) but that are not in the Standard Index in each market.

The MSCI Global Value and Growth Indexes cover the full range of MSCI Developed, Emerging and All Country Indexes across large, mid and small cap size segmentations. They are also cover large and mid-cap size segments for the MSCI Frontier Markets Indexes. The indexes are constructed using an approach that provides a precise definition of style using eight historical and forward-looking fundamental data points for every security. Each security is placed into either the Value or Growth Indexes or may be partially allocated to both (with no double counting). The objective of this index design is to divide constituents of an underlying MSCI Equity Index into respective value and growth indexes, each targeting 50% of the free float adjusted market capitalization of the underlying market index.

TOPIX: An index that measures stock prices on the Tokyo Stock Exchange (TSE). This capitalization-weighted index lists all firms that are considered to be under the ‘first section’ on the TSE, which groups all of the large firms on the exchange into one pool. The second section groups all of the remaining smaller firms.

EV/EBITDA: A ratio used to determine the value of a company. The enterprise multiple looks at a firm as a potential acquirer would, because it takes debt into account - an item which other multiples like the P/E ratio do not include.

Price to Book: A ratio used to compare a stock’s market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value per share.

16

P/E trailing 12 month: The sum of a company’s price-to-earnings, calculated by taking the current stock price and dividing it by the trailing earnings per share for the past 12 months. This measure differs from forward P/E, which uses earnings estimates for the next four quarters.

Altman Z-score: The output of a credit-strength test that gauges a publicly traded manufacturing company’s likelihood of bankruptcy. The Altman Z-score, is based on five financial ratios that can be calculated from data found on a company’s annual 10K report. The Altman Z-score is calculated as follows:

Z-Score = 1.2A + 1.4B + 3.3C + 0.6D + 1.0E

Where:

A = Working Capital/Total Assets

B = Retained Earnings/Total Assets

C = Earnings Before Interest & Tax/Total Assets

D = Market Value of Equity/Total Liabilities

E = Sales/Total Assets

A score below 1.8 means the company is probably headed for bankruptcy, while companies with scores above 3.0 are not likely to go bankrupt. The lower/higher the score, the lower/higher the likelihood of bankruptcy.

The views in this report are those of the Funds’ management. This report contains certain forward-looking statements about factors that may affect the performance of the Funds in the future. These statements are based on the Funds’ management’s predictions and expectations concerning certain future events such as the performance of the economy as a whole and of specific industry sectors. Management believes these forward-looking statements are reasonable, although they are inherently uncertain and difficult to predict.

6275-NLD-12/21/2020

17

| Conductor Global Equity Value Fund |

| Portfolio Review (Unaudited) |

| October 31, 2020 |

The Fund’s performance figures* for the periods ended October 31, 2020, compared to its benchmark:

| Annualized | |||||||

| Since | |||||||

| Commencement | |||||||

| of Operations | Since Inception | Since Inception | Since Inception | ||||

| One Year | Three Years | Five Years | 12/27/2013 (a) | 4/15/2014 | 9/17/2015 | 4/19/16 | |

| Class A with Load (b) | (19.92)% | (7.62)% | 1.23% | N/A | 1.64% | N/A | N/A |

| Class A | (15.05)% | (5.77)% | 2.43% | N/A | 2.56% | N/A | N/A |

| Class C | (15.70)% | (6.49)% | 1.67% | N/A | N/A | 2.14% | N/A |

| Class I | (14.82)% | (5.55)% | 2.68% | 2.29% | N/A | N/A | N/A |

| Class Y | (14.27)% | (4.99)% | N/A | N/A | N/A | N/A | 3.42% |

| MSCI All Country World Value Index (c) | (12.21)% | (2.44)% | 2.92% | 2.14% | 2.04% | 3.54% | 3.11% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Ironhorse Capital, LLC (the “Advisor”) has contractually agreed to reduce the Fund’s fees and/or absorb expenses of the Fund until at least March 1, 2021 to ensure that total annual Fund operating expenses (exclusive of any front-end or contingent deferred loads; brokerage fees and commissions; expenses of other investment companies in which the Fund may invest (“acquired fund fees and expenses”); borrowing costs, such as interest and dividend expense on securities sold short; taxes; and extraordinary expenses, such as litigation expenses) do not exceed 2.15%, 2.90%, 1.90% and 1.25% of average daily net assets attributable to Class A, Class C, Class I and Class Y shares, respectively. This agreement may be terminated by the Fund’s Board of Trustees on 60 days’ written notice to the Advisor. These fee waivers and expense reimbursements are subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years of when the amount was waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits as well as any expense limitation that was in effect at the time the waiver or reimbursement was made. Class A Shares are subject to a maximum sales charge of 5.75% imposed on purchases. Per the fee table in the Fund’s February 28, 2020 prospectus, the Fund’s total annual operating expense ratio before expense waivers, if any, is 2.06%, 2.81%, 1.82%, and 1.77% for Class A, Class C, Class I, and Class Y shares, respectively. For performance information current to the most recent month-end, please call toll-free 1-844-GO-RAILX. |

| (a) | The inception date of Class I is December 26, 2013. Class I commenced operations on December 27, 2013. |

| (b) | Class A with load total return is calculated using the maximum sales charge of 5.75% |

| (c) | The MSCI All Country World Value Index captures large and mid-cap securities exhibiting overall value style characteristics across 23 developed markets countries and 24 emerging markets countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. Investors cannot invest directly in an index or benchmark. Index returns are gross of any fees, brokerage commissions or other expense of investing. |

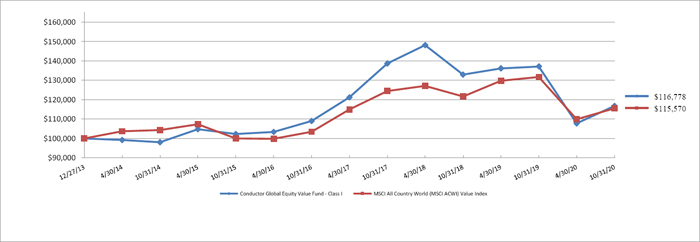

Comparison of the Change in Value of a $100,000 Investment ^

| ^ | Performance shown is for Class I shares. The performance of the Fund’s other classes may be greater or less than the line shown due to differences in loads and fees paid by shareholders in different share classes. |

| Portfolio Composition as of October 31, 2020 | ||||

| Holdings by Industry/Asset Class | % of Net Assets | |||

| Short-Term Investments | 32.6 | % | ||

| Retail - Discretionary | 10.1 | % | ||

| Technology Hardware | 9.4 | % | ||

| Automotive | 6.7 | % | ||

| Chemicals | 6.6 | % | ||

| Steel | 6.1 | % | ||

| Metals & Mining | 4.9 | % | ||

| Technology Services | 3.8 | % | ||

| Gas & Water Utilities | 3.6 | % | ||

| Other** | 17.9 | % | ||

| Other Assets and Liabilities - Net | (1.7 | )% | ||

| 100.0 | % | |||

| ** | Other represents less than 2.0% weightings in the following industries: Asset Management, Commercial Support Services, Containers & Packaging, Electrical Equipment, Entertainment Content, Health Care Facilities & Services, Home Construction, Household Products, Machinery, Oil & Gas Producers, Retail - Consumer Staples, Semiconductors and Specialty Finance. |

Please refer to the Portfolio of Investments in this annual report for a detailed analysis of the Fund’s holdings.

18

| Conductor International Equity Value Fund |

| Portfolio Review (Unaudited) |

| October 31, 2020 |

The Fund’s performance figures* for the period ended October 31, 2020, compared to its benchmark:

| Since | |

| Commencement of | |

| Operations (a) | |

| Class A with Load (b) | (20.03)% |

| Class A | (15.15)% |

| Class I | (15.15)% |

| MSCI All Country World ex-USA IMI Net Index (c) | (2.59)% |

| MSCI All Country World ex-USA Net Index (d) | (2.80)% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. The Advisor has contractually agreed to reduce the Fund’s fees and/or absorb expenses of the Fund until at least March 1, 2021 to ensure that total annual Fund operating expenses after expense waiver and reimbursement (exclusive of any front-end or contingent deferred loads; brokerage fees and commissions; expenses of other investment companies in which the Fund may invest (“acquired fund fees and expenses”); borrowing costs, such as interest and dividend expense on securities sold short; taxes; and extraordinary expenses, such as litigation expenses) do not exceed 1.45% and 1.20% of average daily net assets attributable to Class A and Class I shares, respectively. This agreement may be terminated by the Fund’s Board of Trustees on 60 days’ written notice to the Advisor. These fee waivers and expense reimbursements are subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years of when the amount was waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits as well as any expense limitation that was in effect at the time the waiver or reimbursement was made. Class A Shares are subject to a maximum sales charge of 5.75% imposed on purchases. Per the fee table in the Fund’s February 28, 2020 prospectus, the Fund’s total annual operating expense ratio before expense waivers, if any, is 2.41% and 2.16% for Class A and Class I shares, respectively. For performance information current to the most recent month-end, please call toll-free 1-844-GO-RAILX. |

| (a) | The inception date of Class A and Class I is December 3, 2019. Class A and Class I commenced operations on December 5, 2019. |

| (b) | Class A with load total return is calculated using the maximum sales charge of 5.75% |

| (c) | The MSCI All Country World ex-USA IMI Net Index captures large, mid and small cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 26 Emerging Markets (EM) countries. You cannot invest directly in an index. Index returns are gross of any fees, brokerage commissions or other expense of investing. |

| (d) | The MSCI All Country World ex-USA Net Index is a market-capitalization-weighted index maintained by Morgan Stanley Capital International (MSCI). It is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI ACWI Ex-U.S. includes both developed and emerging markets. You cannot invest directly in an index. Index returns are gross of any fees, brokerage commissions or other expense of investing. |

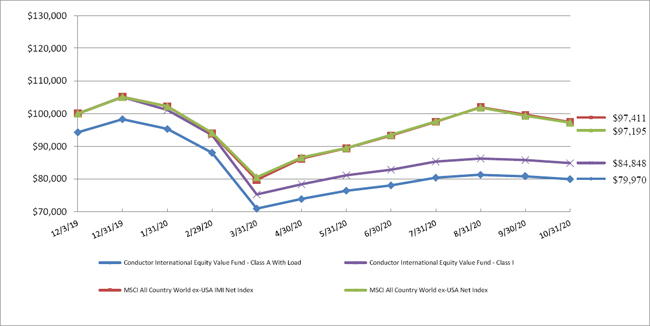

Comparison of the Change in Value of a $100,000 Investment

| Portfolio Composition as of October 31, 2020 | ||||

| Holdings by Industry/Asset Class | % of Net Assets | |||

| Short-Term Investment | 27.2 | % | ||

| Equity Funds | 26.9 | % | ||

| Technology Hardware | 8.7 | % | ||

| Chemicals | 5.8 | % | ||

| Metals & Mining | 3.8 | % | ||

| Technology Services | 3.5 | % | ||

| Gas & Water Utilities | 3.3 | % | ||

| Steel | 3.0 | % | ||

| Automotive | 3.0 | % | ||

| Other ** | 12.6 | % | ||

| Other Assets and Liabilities - Net | 2.2 | % | ||

| 100.0 | % | |||

| ** | Other represents less than 2.2% weightings in the following industries: Containers & Packaging, Entertainment Content, Health Care Facilities & Services, Home Construction, Oil & Gas Producers, Retail - Discretionary, Specialty Finance, Transportation & Logistics and Transportation Equipment. |

Please refer to the Portfolio of Investments in this annual report for a detailed analysis of the Fund’s holdings.

19

| Conductor Global Equity Value Fund |

| PORTFOLIO OF INVESTMENTS |

| October 31, 2020 |

| Shares | Value | |||||||

| COMMON STOCKS - 65.2% | ||||||||

| ASSET MANAGEMENT - 1.0% | ||||||||

| 34,690 | Waddell & Reed Financial, Inc. ^ | $ | 532,492 | |||||

| AUTOMOTIVE - 6.7% | ||||||||

| 14,235 | BorgWarner, Inc. | 497,940 | ||||||

| 4,835 | Continental A.G. | 513,724 | ||||||

| 19,730 | Cooper Tire & Rubber Company | 678,515 | ||||||

| 19,200 | FCC Company Ltd. | 368,437 | ||||||

| 15,650 | Linamar Corporation | 511,565 | ||||||

| 19,500 | Stanley Electric Company Ltd. | 555,356 | ||||||

| 18,700 | TS Tech Company Ltd. | 517,593 | ||||||

| 3,643,130 | ||||||||

| CHEMICALS - 6.6% | ||||||||

| 11,780 | Covestro A.G. | 562,213 | ||||||

| 35,500 | Lintec Corporation | 786,958 | ||||||

| 15,100 | LOTTE Fine Chemical Company Ltd. | 648,580 | ||||||

| 14,100 | Nitto Denko Corporation | 990,607 | ||||||

| 49,000 | Zeon Corporation | 596,155 | ||||||

| 3,584,513 | ||||||||

| COMMERCIAL SUPPORT SERVICES - 2.0% | ||||||||

| 32,020 | Kelly Services, Inc. | 556,508 | ||||||

| 10,930 | Randstad N.V. * | 545,369 | ||||||

| 1,101,877 | ||||||||

| CONTAINERS & PACKAGING - 1.0% | ||||||||

| 47,965 | Transcontinental, Inc. ^ | 568,106 | ||||||

| ELECTRICAL EQUIPMENT- 1.0% | ||||||||

| 15,600 | Tokyo Seimitsu Company Ltd. | 526,367 | ||||||

| ENTERTAINMENT CONTENT - 1.8% | ||||||||

| 25,800 | GungHo Online Entertainment, Inc. | 641,056 | ||||||

| 317,000 | IGG, Inc. | 343,149 | ||||||

| 984,205 | ||||||||

| HEALTH CARE FACILITIES & SERVICES - 1.4% | ||||||||

| 30,000 | H.U. Group Holdings, Inc. | 763,269 | ||||||

| HOME CONSTRUCTION - 1.5% | ||||||||

| 66,300 | Haseko Corporation | 794,880 | ||||||

| HOUSEHOLD PRODUCTS - 1.3% | ||||||||

| 14,340 | Nu Skin Enterprises, Inc. | 707,679 | ||||||

The accompanying notes are an integral part of these financial statements.

20

| Conductor Global Equity Value Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| October 31, 2020 |

| Shares | Value | |||||||

| MACHINERY - 2.0% | ||||||||

| 21,235 | Doosan Bobcat, Inc. | $ | 542,646 | |||||

| 11,200 | OKUMA Corporation | 543,624 | ||||||

| 1,086,270 | ||||||||

| METALS & MINING - 4.9% | ||||||||

| 175,940 | Fortescue Metals Group Ltd. | 2,152,361 | ||||||

| 32,430 | Warrior Met Coal, Inc. | 486,450 | ||||||

| 2,638,811 | ||||||||

| OIL & GAS PRODUCERS - 1.0% | ||||||||

| 60,800 | ITOCHU ENEX Company Ltd. | 571,965 | ||||||

| RETAIL - CONSUMER STAPLES - 1.1% | ||||||||

| 27,000 | Arcs Company Ltd. | 597,713 | ||||||

| RETAIL - DISCRETIONARY - 9.8% | ||||||||

| 45,850 | Bed Bath & Beyond, Inc. ^ | 907,830 | ||||||

| 26,615 | Buckle, Inc. (The) | 637,695 | ||||||

| 12,155 | Dillard’s, Inc. | 543,693 | ||||||

| 55,300 | EDION Corporation | 544,693 | ||||||

| 14,920 | Foot Locker, Inc. | 550,250 | ||||||

| 769,600 | Matahari Department Store Tbk P.T. * | 51,919 | ||||||

| 57,980 | Qurate Retail, Inc. | 392,525 | ||||||

| 6,500 | Shimamura Company Ltd. | 692,970 | ||||||

| 44,240 | Takkt A.G. * | 470,131 | ||||||

| 24,327 | Urban Outfitters, Inc. * | 543,465 | ||||||

| 5,335,171 | ||||||||

| SEMICONDUCTORS - 1.0% | ||||||||

| 15,100 | Ulvac, Inc. | 553,104 | ||||||

| SPECIALTY FINANCE - 1.8% | ||||||||

| 108,720 | Resurs Holding A.B. | 497,019 | ||||||

| 19,882 | Synchrony Financial | 497,448 | ||||||

| 994,467 | ||||||||

| STEEL - 6.1% | ||||||||

| 18,960 | APERAM S.A. | 508,824 | ||||||

| 57,660 | BlueScope Steel Ltd. | 595,552 | ||||||

| 21,000 | Maruichi Steel Tube Ltd. | 481,773 | ||||||

| 259,400 | Novolipetsk Steel PJSC | 607,328 | ||||||

| 11,675 | Nucor Corporation | 557,597 | ||||||

| 42,200 | Russel Metals, Inc. ^ | 561,590 | ||||||

| 3,312,664 | ||||||||

| TECHNOLOGY HARDWARE - 9.4% | ||||||||

| 315,000 | FLEXium Interconnect, Inc. | 1,286,096 | ||||||

| 40,000 | Inaba Denki Sangyo Company Ltd. | 962,938 | ||||||

| 14,400 | Mabuchi Motor Company Ltd. | 593,694 | ||||||

| 466,000 | Pegatron Corporation | 1,004,243 | ||||||

| 24,000 | Taiyo Holdings Company Ltd. | 1,256,465 | ||||||

| 5,103,436 | ||||||||

The accompanying notes are an integral part of these financial statements.

21

| Conductor Global Equity Value Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| October 31, 2020 |

| Shares | Value | |||||||

| TECHNOLOGY SERVICES - 3.8% | ||||||||

| 120,000 | NEC Networks & System Integration Corporation | $ | 2,080,848 | |||||

| TOTAL COMMON STOCKS (Cost - $31,062,414) | 35,480,967 | |||||||

| PREFERRED STOCK - 3.9% | ||||||||

| GAS & WATER UTILITIES - 3.6% | ||||||||

| 63,058 | Cia de Gas de Sao Paulo | 1,956,266 | ||||||

| RETAIL - DISCRETIONARY - 0.3% | ||||||||

| 1,739 | Qurate Retail, Inc. * | 170,109 | ||||||

| 2,126,375 | ||||||||

| TOTAL PREFERRED STOCK - (Cost - $1,116,380) | ||||||||

| SHORT-TERM INVESTMENTS - 32.6% | ||||||||

| INVESTMENT PURCHASED AS SECURITIES LENDING COLLATERAL - 2.5% | ||||||||

| 1,377,465 | Dreyfus Cash Management Fund - Institutional Class, 0.10% + (a) | 1,377,465 | ||||||

| MONEY MARKET FUND - 30.1% | ||||||||

| 16,371,400 | Dreyfus Cash Management Fund - Institutional Class, 0.10% + | 16,389,410 | ||||||

| TOTAL SHORT-TERM INVESTMENTS (Cost - $17,751,693) | 17,766,875 | |||||||

| TOTAL INVESTMENTS - 101.7% (Cost - $49,930,487) | $ | 55,374,217 | ||||||

| OTHER ASSETS AND LIABILITIES - NET - (1.7)% | (941,341 | ) | ||||||

| TOTAL NET ASSETS - 100.0% | $ | 54,432,876 | ||||||

| * | Non-income producing security. |

| ^ | All or a portion of the security is on loan. Total loaned securities had a value of $1,839,359 at October 31, 2020. |

| + | Money market fund; interest rate reflects seven day effective yield on October 31, 2020. |

| (a) | Security was purchased with cash received as collateral for securities on loan as of October 31, 2020. Total collateral had a value of $1,377,465 at October 31, 2020. Additional collateral received from the borrower not disclosed in the Portfolio of Investments had a value of $554,737 as of October 31, 2020. |

| Portfolio Composition as of October 31, 2020 | ||||

| Holdings by Country | % of Market Value | |||

| United States | 47.0 | % | ||

| Japan | 27.8 | % | ||

| Australia | 5.0 | % | ||

| Taiwan | 4.1 | % | ||

| Brazil | 3.3 | % | ||

| Canada | 3.0 | % | ||

| Germany | 2.8 | % | ||

| Korea | 2.2 | % | ||

| Netherlands | 1.0 | % | ||

| Russia | 1.1 | % | ||

| Other** | 2.7 | % | ||

| 100.0 | % | |||

| ** | Other represents less than 1.0% weightings in each of the following countries: Belgium, Hong Kong, Indonesia and Sweden. |

The accompanying notes are an integral part of these financial statements.

22

| Conductor International Equity Value Fund |

| PORTFOLIO OF INVESTMENTS |

| October 31, 2020 |

| Shares | Value | |||||||

| COMMON STOCKS - 40.4% | ||||||||

| AUTOMOTIVE - 3.0% | ||||||||

| 235 | Continental A.G. | $ | 24,973 | |||||

| 618 | Faurecia SE* | 23,442 | ||||||

| 1,400 | FCC Company Ltd. | 26,905 | ||||||

| 75,320 | ||||||||

| CHEMICALS - 5.8% | ||||||||

| 562 | Covestro A.G. | 26,827 | ||||||

| 846 | Johnson Matthey PLC | 23,505 | ||||||

| 700 | LOTTE Fine Chemical Company Ltd. | 30,067 | ||||||

| 600 | Nitto Denko Corporation | 42,216 | ||||||

| 16,800 | Petronas Chemicals Group Bhd | 23,671 | ||||||

| 146,286 | ||||||||

| CONTAINERS & PACKAGING - 1.0% | ||||||||

| 2,235 | Transcontinental, Inc. | 26,451 | ||||||

| ENTERTAINMENT CONTENT - 2.2% | ||||||||

| 5,200 | Gree, Inc. | 27,156 | ||||||

| 1,200 | GungHo Online Entertainment, Inc. | 29,861 | ||||||

| 57,017 | ||||||||

| HEALTH CARE FACILITIES & SERVICES - 1.2% | ||||||||

| 1,200 | H.U. Group Holdings, Inc. | 30,576 | ||||||

| HOME CONSTRUCTION - 1.4% | ||||||||

| 2,900 | Haseko Corporation | 34,820 | ||||||

| METALS & MINING - 3.8% | ||||||||

| 7,887 | Fortescue Metals Group Ltd. | 96,396 | ||||||

| OIL & GAS PRODUCERS - 0.8% | ||||||||

| 18,026 | Viva Energy Group Ltd. | 21,304 | ||||||

| RETAIL - DISCRETIONARY - 2.2% | ||||||||

| 25,700 | Matahari Department Store Tbk P.T. * | 1,734 | ||||||

| 300 | Shimamura Company Ltd. | 32,031 | ||||||

| 2,040 | Takkt A.G. * | 21,682 | ||||||

| 55,447 | ||||||||

| SPECIALTY FINANCE - 0.9% | ||||||||

| 5,130 | Resurs Holding A.B. | 23,445 | ||||||

The accompanying notes are an integral part of these financial statements.

23

| Conductor International Equity Value Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| October 31, 2020 |

| Shares | Value | |||||||

| STEEL - 3.0% | ||||||||

| 2,830 | BlueScope Steel Ltd. | $ | 29,203 | |||||

| 1,000 | Maruichi Steel Tube Ltd. | 22,976 | ||||||

| 1,800 | Russel Metals, Inc. | 23,935 | ||||||

| 76,114 | ||||||||

| TECHNOLOGY HARDWARE - 8.7% | ||||||||

| 14,000 | FLEXium Interconnect, Inc. | 57,160 | ||||||

| 1,700 | Inaba Denki Sangyo Company Ltd. | 40,986 | ||||||

| 700 | Mabuchi Motor Company Ltd. | 28,903 | ||||||

| 20,000 | Pegatron Corporation | 43,100 | ||||||

| 1,000 | Taiyo Holdings Company Ltd. | 52,430 | ||||||

| 222,579 | ||||||||

| TECHNOLOGY SERVICES - 3.5% | ||||||||

| 5,100 | NEC Networks & System Integration Corporation | 88,567 | ||||||

| TRASPORTATION & LOGISTICS - 2.1% | ||||||||

| 227 | Hyundai Glovis Co. Ltd. | 33,736 | ||||||

| 1,910 | Westshore Terminals Investment Corp. | 19,181 | ||||||

| 52,917 | ||||||||

| TRASPORTATION EQUIPMENT - 0.8% | ||||||||

| 6,900 | Zhuzhou CRRC Times Electric Co. Ltd. | 21,242 | ||||||

| TOTAL COMMON STOCKS (Cost - $946,729) | 1,028,481 | |||||||

| PREFERRED STOCK - 3.3% | ||||||||

| GAS & WATER UTILITIES - 3.3% | ||||||||

| 2,700 | Cia de Gas de Sao Paulo | |||||||

| TOTAL PREFERRED STOCK - (Cost - $78,464) | 83,355 | |||||||

| EXCHANGE TRADED FUNDS - 26.9% | ||||||||

| EQUITY FUNDS - 26.9% | ||||||||

| 11,096 | Vanguard FTSE Developed Markets ETF | 437,737 | ||||||

| 5,667 | Vanguard FTSE Emerging Markets ETF | 248,271 | ||||||

| TOTAL EXCHANGE TRADED FUNDS - (Cost - $717,081) | 686,008 | |||||||

| SHORT-TERM INVESTMENT - 27.2% | ||||||||

| MONEY MARKET FUND - 27.2% | ||||||||

| 691,361 | Dreyfus Cash Management Fund - Institutional Class, 0.10% + | 692,122 | ||||||

| TOTAL SHORT-TERM INVESTMENTS (Cost - $691,575) | ||||||||

| TOTAL INVESTMENTS - 97.8% (Cost - $2,433,849) | $ | 2,489,966 | ||||||

| OTHER ASSETS AND LIABILITIES - NET - 2.2% | 56,092 | |||||||

| TOTAL NET ASSETS - 100.0% | $ | 2,546,058 | ||||||

| + | Money market fund; interest rate reflects seven day effective yield on October 31, 2020. |

| * | Non-income producing security. |

The accompanying notes are an integral part of these financial statements.

24

| Conductor International Equity Value Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| October 31, 2020 |

| Portfolio Composition as of October 31, 2020 | ||||

| Holdings by Country | % of Market Value | |||

| United States | 27.8 | % | ||

| International ETF | 27.6 | % | ||

| Japan | 18.4 | % | ||

| Australia | 5.9 | % | ||

| Taiwan | 4.0 | % | ||

| Brazil | 3.5 | % | ||

| Germany | 3.0 | % | ||

| Canada | 2.8 | % | ||

| Korea | 2.6 | % | ||

| Other** | 4.4 | % | ||

| 100.0 | % | |||

| ** | Other represents less than 1.0% weightings in each of the following countries: France, Hong Kong, Indonesia, United Kingdom and |

The accompanying notes are an integral part of these financial statements.

25

| Conductor Funds |

| Statements of Assets and Liabilities |

| October 31, 2020 |

| Conductor Global Equity | Conductor International | |||||||

| Value Fund | Equity Value Fund | |||||||

| ASSETS | ||||||||

| Securities, at cost | $ | 49,930,487 | $ | 2,433,849 | ||||

| Securities, at fair value | $ | 55,374,217 | $ | 2,489,966 | ||||

| Foreign currency (cost: $13,641 and $0) | 13,111 | — | ||||||

| Receivable for securities sold | 2,265,288 | 22,839 | ||||||

| Dividends and interest receivable | 276,387 | 6,487 | ||||||

| Receivable due from advisor | — | 34,547 | ||||||

| Prepaid expenses and other assets | 39,337 | 12,249 | ||||||

| TOTAL ASSETS | 57,968,340 | 2,566,088 | ||||||

| LIABILITIES | ||||||||

| Collateral on securities loaned (see note 8) | 1,377,465 | — | ||||||

| Payable for investments purchased | 2,027,700 | — | ||||||

| Payable for fund shares redeemed | 40,831 | — | ||||||

| Audit and tax fees payable | 17,687 | 16,893 | ||||||

| Investment advisory fees payable | 47,006 | — | ||||||

| Payable to related parties | 14,209 | 2,162 | ||||||

| Distribution (12b-1) fees payable | 730 | — | ||||||

| Accrued expenses and other liabilities | 9,836 | 975 | ||||||

| TOTAL LIABILITIES | 3,535,464 | 20,030 | ||||||

| NET ASSETS | $ | 54,432,876 | $ | 2,546,058 | ||||

| NET ASSETS CONSIST OF: | ||||||||

| Paid in capital | $ | 62,043,594 | $ | 3,044,323 | ||||

| Accumulated deficit | (7,610,718 | ) | (498,265 | ) | ||||

| NET ASSETS | $ | 54,432,876 | $ | 2,546,058 | ||||

The accompanying notes are an integral part of these financial statements.

26

| Conductor Funds |

| Statements of Assets and Liabilities (Continued) |

| October 31, 2020 |

| Conductor Global Equity | Conductor International | |||||||

| Value Fund | Equity Value Fund | |||||||

| NET ASSET VALUE PER SHARE: | ||||||||

| Class A Shares: | ||||||||

| Net Assets | $ | 971,406 | $ | 8 | ||||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 96,721 | 1 | ||||||

| Net asset value (Net Assets ÷ Shares Outstanding) and redemption price per share (a) | $ | 10.04 | $ | 8.33 | (b) | |||

| Maximum offering price per share (maximum sales charge of 5.75%) | $ | 10.65 | $ | 8.84 | (b) | |||

| Class C Shares: | ||||||||

| Net Assets | $ | 589,757 | ||||||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 59,473 | |||||||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (a) | $ | 9.92 | ||||||

| Class I Shares: | ||||||||

| Net Assets | $ | 39,583,780 | $ | 2,546,050 | ||||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 3,921,792 | 305,574 | ||||||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (a) | $ | 10.09 | $ | 8.33 | ||||

| Class Y Shares: | ||||||||

| Net Assets | $ | 13,287,933 | ||||||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 1,280,712 | |||||||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (a) | $ | 10.38 | ||||||

| (a) | Redemptions made within 30 days of purchase may be assessed a redemption fee of 1.00%. |

| (b) | NAV/offering price may not recalculate due to rounding of shares. |

The accompanying notes are an integral part of these financial statements.

27

| Conductor Funds |

| Statements of Operations |

| For the Year or Period Ended October 31, 2020 |

| Conductor Global Equity | Conductor International | |||||||

| Value Fund | Equity Value Fund (a) | |||||||

| INVESTMENT INCOME | ||||||||

| Dividend Income (Foreign Taxes Withheld: $160,695 and $7,740) | $ | 2,001,453 | $ | 78,254 | ||||

| Interest Income | 53,341 | 2,351 | ||||||

| Securities Lending Income (net of fees) | 25,456 | — | ||||||

| TOTAL INVESTMENT INCOME | 2,080,250 | 80,605 | ||||||

| EXPENSES | ||||||||

| Investment advisory fees | 793,947 | 27,550 | ||||||

| Distribution (12b-1) fees: | ||||||||

| Class A | 3,473 | — | ||||||

| Class C | 8,650 | — | ||||||

| Administrative services fees | 40,365 | 30,237 | ||||||

| Registration fees | 77,392 | 1,326 | ||||||

| Third party administrative services fees | 72,245 | 1,262 | ||||||

| Custodian fees | 10,634 | 6,736 | ||||||

| Transfer agent fees | 70,340 | 10,076 | ||||||

| Audit fees | 46,747 | 17,393 | ||||||

| Accounting services fees | 29,113 | 14,752 | ||||||

| Legal fees | 42,971 | 27,492 | ||||||

| Printing and postage expenses | 22,632 | 2,238 | ||||||

| Compliance officer fees | 38,017 | 5,886 | ||||||

| Trustees fees and expenses | 17,012 | 7,643 | ||||||

| Insurance expense | 19,491 | 207 | ||||||

| Tax expense | 13,232 | — | ||||||

| Other expenses | 13,827 | 1,891 | ||||||

| TOTAL EXPENSES | 1,320,088 | 154,689 | ||||||

| Less: Fees waived/reimbursed by the Advisor | (202,291 | ) | (125,955 | ) | ||||

| NET EXPENSES | 1,117,797 | 28,734 | ||||||

| NET INVESTMENT INCOME | 962,453 | 51,871 | ||||||

| REALIZED AND UNREALIZED GAIN/(LOSS) | ||||||||

| Net realized loss from: | ||||||||

| Investments | (6,743,188 | ) | (547,781 | ) | ||||

| Foreign currency translations | (212,603 | ) | (14,173 | ) | ||||

| Realized loss from investments and foreign currency transactions | (6,955,791 | ) | (561,954 | ) | ||||

| Net change in unrealized appreciation/(depreciation) of: | ||||||||

| Investments | (4,919,434 | ) | 56,117 | |||||

| Foreign currency translations | 3,981 | 29 | ||||||

| Unrealized appreciation/(depreciation) on investments and foreign currency translations | (4,915,453 | ) | 56,146 | |||||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (11,871,244 | ) | (505,808 | ) | ||||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (10,908,791 | ) | $ | (453,937 | ) | ||

| (a) | The Conductor International Equity Value Fund commenced investment operations on December 5, 2019. |

The accompanying notes are an integral part of these financial statements.

28

| Conductor Global Equity Value Fund |

| Statements of Changes in Net Assets |

| For the Year Ended | For the Year Ended | |||||||

| October 31, | October 31, | |||||||

| 2020 | 2019 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income | $ | 962,453 | $ | 1,704,955 | ||||

| Net realized loss from investments and foreign currency translations | (6,955,791 | ) | (6,073,661 | ) | ||||

| Net change in unrealized appreciation/(depreciation) of investments and foreign currency translations | (4,915,453 | ) | 6,649,109 | |||||

| Net increase/(decrease) in net assets resulting from operations | (10,908,791 | ) | 2,280,403 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Total Distributions Paid: | ||||||||

| Class A | (16,310 | ) | (297,412 | ) | ||||

| Class C | (2,817 | ) | (152,054 | ) | ||||

| Class I | (640,074 | ) | (5,408,051 | ) | ||||

| Class Y | (222,123 | ) | (3,719,978 | ) | ||||

| From Return of Capital | (117,449 | ) | — | |||||

| Net decrease in net assets resulting from distributions to shareholders | (998,773 | ) | (9,577,495 | ) | ||||

| FROM SHARES OF BENEFICIAL INTEREST | ||||||||

| Proceeds from shares sold: | ||||||||

| Class A | — | 200,620 | ||||||

| Class C | — | 164,334 | ||||||

| Class I | 364,985 | 657,483 | ||||||

| Class Y | 2,250,854 | 9,889,360 | ||||||

| Net asset value of shares issued in reinvestment of distributions: | ||||||||

| Class A | 17,446 | 276,374 | ||||||

| Class C | 4,242 | 150,021 | ||||||

| Class I | 639,841 | 4,755,569 | ||||||

| Class Y | 245,715 | 3,546,864 | ||||||

| Redemption fee proceeds: | ||||||||

| Class C | 103 | — | ||||||

| Class Y | 64 | — | ||||||

| Payments for shares redeemed: | ||||||||

| Class A | (847,207 | ) | (1,177,857 | ) | ||||

| Class C | (588,431 | ) | (441,850 | ) | ||||

| Class I | (5,447,321 | ) | (1,792,702 | ) | ||||

| Class Y | (13,699,477 | ) | (27,103,774 | ) | ||||

| Net decrease in net assets from shares of beneficial interest | (17,059,186 | ) | (10,875,558 | ) | ||||

| TOTAL DECREASE IN NET ASSETS | (28,966,750 | ) | (18,172,650 | ) | ||||

| NET ASSETS | ||||||||

| Beginning of Year | 83,399,626 | 101,572,276 | ||||||

| End of Year | $ | 54,432,876 | $ | 83,399,626 | ||||

The accompanying notes are an integral part of these financial statements.

29

| Conductor Global Equity Value Fund |

| Statements of Changes in Net Assets (Continued) |

| For the Year Ended | For the Year Ended | |||||||

| October 31, | October 31, | |||||||

| 2020 | 2019 | |||||||

| SHARE ACTIVITY | ||||||||

| Class A: | ||||||||

| Shares Sold | — | 17,137 | ||||||

| Shares Reinvested | 1,735 | 24,379 | ||||||

| Shares Redeemed | (78,890 | ) | (103,344 | ) | ||||

| Net decrease in shares of beneficial interest outstanding | (77,155 | ) | (61,828 | ) | ||||

| Class C: | ||||||||

| Shares Sold | — | 13,799 | ||||||

| Shares Reinvested | 435 | 13,408 | ||||||

| Shares Redeemed | (55,921 | ) | (39,127 | ) | ||||

| Net decrease in shares of beneficial interest outstanding | (55,486 | ) | (11,920 | ) | ||||

| Class I: | ||||||||

| Shares Sold | 29,727 | 55,991 | ||||||

| Shares Reinvested | 63,106 | 415,838 | ||||||

| Shares Redeemed | (490,802 | ) | (153,832 | ) | ||||

| Net increase/(decrease) in shares of beneficial interest outstanding | (397,969 | ) | 317,997 | |||||

| Class Y: | ||||||||

| Shares Sold | 213,723 | 851,414 | ||||||

| Shares Reinvested | 23,317 | 305,523 | ||||||

| Shares Redeemed | (1,213,859 | ) | (2,250,127 | ) | ||||

| Net decrease in shares of beneficial interest outstanding | (976,819 | ) | (1,093,190 | ) | ||||

The accompanying notes are an integral part of these financial statements.

30

| Conductor International Equity Value Fund |

| Statement of Changes in Net Assets |

| For the Period* Ended | ||||

| October 31, | ||||

| 2020 | ||||

| FROM OPERATIONS | ||||

| Net investment income | $ | 51,871 | ||

| Net realized loss from investments and foreign currency translations | (561,954 | ) | ||

| Net change in unrealized appreciation of investments and foreign currency translations | 56,146 | |||

| Net decrease in net assets resulting from operations | (453,937 | ) | ||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||

| Total Distributions Paid: | ||||

| Class A | — | (a) | ||

| Class I | (44,328 | ) | ||

| From Return of Capital | (7,847 | ) | ||

| Net decrease in net assets resulting from distributions to shareholders | (52,175 | ) | ||

| FROM SHARES OF BENEFICIAL INTEREST | ||||

| Proceeds from shares sold: | ||||

| Class A | 10 | |||

| Class I | 2,999,985 | |||

| Net asset value of shares issued in reinvestment of distributions: | ||||

| Class A | — | (a) | ||

| Class I | 52,175 | |||

| Net increase in net assets from shares of beneficial interest | 3,052,170 | |||

| TOTAL INCREASE IN NET ASSETS | 2,546,058 | |||

| NET ASSETS | ||||

| Beginning of Year | — | |||

| End of Year | $ | 2,546,058 | ||

| SHARE ACTIVITY | ||||

| Class A: | ||||

| Shares Sold | 1 | |||

| Shares Reinvested | — | (b) | ||

| Net increase in shares of beneficial interest outstanding | 1 | |||

| Class I: | ||||

| Shares Sold | 299,998 | |||

| Shares Reinvested | 5,576 | |||

| Net increase in shares of beneficial interest outstanding | 305,574 | |||

| * | The Conductor International Equity Value Fund commenced investment operations on December 5, 2019. |

| (a) | Represents less than $1. |

| (b) | Represents less than 1 share. |

The accompanying notes are an integral part of these financial statements.

31

| Conductor Global Equity Value Fund |

| Financial Highlights |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout each Year |

| Class A Shares* | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| October 31, | October 31, | October 31, | October 31, | October 31, | ||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | 2016 | ||||||||||||||||

| Net asset value, beginning of year | $ | 12.01 | $ | 13.00 | $ | 13.75 | $ | 10.84 | $ | 10.20 | ||||||||||

| Activity from investment operations: | ||||||||||||||||||||

| Net investment income/(loss) (1) | 0.12 | 0.19 | 0.05 | 0.01 | (0.03 | ) | ||||||||||||||

| Net realized and unrealized gain/(loss) on investments | (1.94 | ) | 0.10 | (0.63 | ) | 2.90 | 0.67 | |||||||||||||

| Total from investment operations | (1.82 | ) | 0.29 | (0.58 | ) | 2.91 | 0.64 | |||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | (0.13 | ) | (0.18 | ) | (0.15 | ) | — | — | ||||||||||||

| Net return of capital | (0.02 | ) | — | — | — | — | ||||||||||||||

| Net realized gains | — | (1.10 | ) | (0.02 | ) | — | — | |||||||||||||

| Total distributions | (0.15 | ) | (1.28 | ) | (0.17 | ) | — | — | ||||||||||||

| Paid-in-Capital From Redemption Fees | — | — | 0.00 | (6) | — | — | ||||||||||||||

| Net asset value, end of year | $ | 10.04 | $ | 12.01 | $ | 13.00 | $ | 13.75 | $ | 10.84 | ||||||||||

| Total return (2) | (15.05 | )% | 2.94 | % | (4.33 | )% | 26.85 | % | 6.27 | % | ||||||||||

| Net assets, end of year (000’s) | $ | 971 | $ | 2,088 | $ | 3,065 | $ | 3,624 | $ | 1,887 | ||||||||||

| Ratio of gross expenses to average net assets (3)(4) | 2.30 | % (8) | 1.94 | % | 1.81 | % | 1.95 | % | 2.37 | % | ||||||||||

| Ratio of net expenses to average net assets (4) | 2.17 | % (8) | 1.94 | % | 2.11 | % (7) | 2.15 | % (7) | 2.14 | % | ||||||||||

| Ratio of net investment income/(loss) to average net assets (4)(5) | 1.08 | % | 1.59 | % | 0.36 | % | 0.06 | % | (0.33 | )% | ||||||||||

| Portfolio Turnover Rate | 91 | % | 108 | % | 141 | % | 90 | % | 123 | % | ||||||||||

| * | The Conductor Global Equity Value Fund Class A commenced investment operations on April 15, 2014. |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Total returns are historical and assume changes in share price and reinvestment of dividends and distributions. Total returns for periods less than one year are not annualized. Total returns shown exclude the effect of the maximum applicable sales charges of 5.75% and, if applicable, wire redemption fees. Had the Advisor not waived its fees, the returns would have been lower. |

| (3) | Represents the ratio of expenses to average net assets absent fee waivers by the Advisor. |

| (4) | The ratios of expenses and net investment income/(loss) to average net assets do not reflect the Fund’s proportionate share of income and expenses of underlying investment companies in which the Fund invests. |