united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

| Investment Company Act file number | 811-22718 |

| Two Roads Shared Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450, Cincinnati, OH | 45246 |

| (Address of principal executive offices) | (Zip code) |

| The Corporation Trust Company |

| 1209 Orange Street, Wilmington, DE 19801 |

| (Name and address of agent for service) |

| Registrant’s telephone number, including area code: | 631-490-4300 |

| Date of fiscal year end: | 7/31 | |

| | | |

| Date of reporting period: | 7/31/2024 | |

Item 1. Reports to Stockholders.

(a)

Anfield Universal Fixed Income ETF

(AFIF) Cboe BZX Exchange, Inc.

Annual Shareholder Report - July 31, 2024

This annual shareholder report contains important information about Anfield Universal Fixed Income ETF for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://regentsparkfunds.com/our-funds/anfield-universal-fixed-income-etf/?cb=2099. You can also request this information by contacting us at 949.891.0600.

What were the Fund’s costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Anfield Universal Fixed Income ETF | $116 | 1.11% |

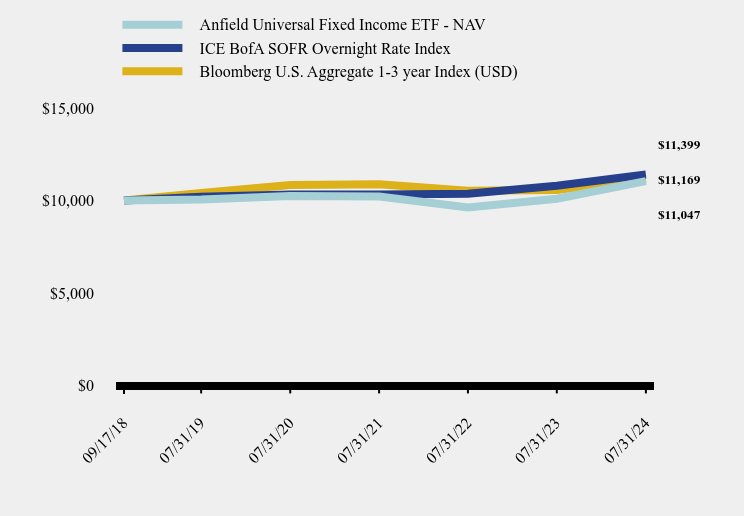

How did the Fund perform during the reporting period?

The Anfield Universal Fixed Income ETF (“AFIF” or “the Fund”) delivered positive returns and outperformed both the Bloomberg US Aggregate 1-3 Year Index and the ICE BofA SOFR Overnight Rate Index for the annual period ended July 31st, 2024, although past performance does not guarantee future results. AFIF posted an annual net total return of +9.49% versus the Bloomberg US Aggregate 1-3 Year Index’s return of +5.71%, and the ICE BofA SOFR Overnight Rate Index’s return of +5.56%. This outperformance was mainly driven by the Fund’s overweight to corporate credit, which was a strong performer throughout the annual period. In particular, the Fund benefited from its allocations to US high yield credit, investment grade and high yield collateralized loan obligations (“CLOs”), and bank loans. These positions have performed well since trade implementation. In general, the Fund benefited from the portfolio management team’s belief that interest rates would remain higher than what was generally expected during the annual period. Thus, the team maintained their conservative duration positioning (roughly 1/3 of the US Aggregate Bond Index). Overall, the team emphasized what it perceived as higher quality, yield-enhancing corporate credit, mortgage-backed, and asset-backed security allocations while favoring the front-end of the yield curve as the team did not believe extending further out was worth the additional risk. Looking forward, the team plans to continue selectively adding positions they believe offer a positive risk reward payoff in the coming interest rate environment, including shorter duration high yield bonds, bank loans, and select CLO tranches.

Average Annual Total Returns

| 1 Year | 5 Years | Since Inception (September 17, 2018) |

|---|

| Anfield Universal Fixed Income ETF - NAV | 9.49% | 1.91% | 1.71% |

| Anfield Universal Fixed Income ETF - Market Price | 10.00% | 1.85% | 1.73% |

| ICE BofA SOFR Overnight Rate Index | 5.56% | 2.24% | 2.26% |

| Bloomberg U.S. Aggregate 1-3 year Index (USD) | 5.71% | 1.44% | 1.90% |

The Fund's past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

How has the Fund performed since inception?

Total Return Based on $10,000 Investment

| Anfield Universal Fixed Income ETF - NAV | ICE BofA SOFR Overnight Rate Index | Bloomberg U.S. Aggregate 1-3 year Index (USD) |

|---|

| 09/17/18 | $10,000 | $10,000 | $10,000 |

| 07/31/19 | $10,052 | $10,205 | $10,397 |

| 07/31/20 | $10,242 | $10,321 | $10,832 |

| 07/31/21 | $10,209 | $10,326 | $10,874 |

| 07/31/22 | $9,625 | $10,362 | $10,522 |

| 07/31/23 | $10,090 | $10,799 | $10,566 |

| 07/31/24 | $11,047 | $11,399 | $11,169 |

| Net Assets | $104,117,484 |

| Number of Portfolio Holdings | 275 |

| Advisory Fee | $794,563 |

| Portfolio Turnover | 49% |

Asset Weighting (% of total investments)

| Value | Value |

|---|

| Asset Backed Securities | 18.1% |

| Collateralized Mortgage Obligations | 9.4% |

| Corporate Bonds | 55.7% |

| Term Loans | 11.9% |

| U.S. Government & Agencies | 4.9% |

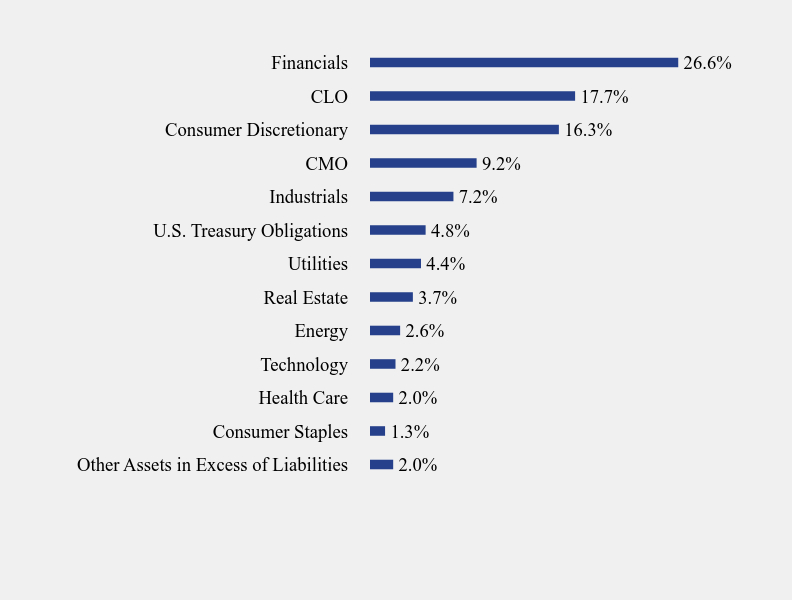

What did the Fund invest in?

Sector Weighting (% of net assets)

| Value | Value |

|---|

| Other Assets in Excess of Liabilities | 2.0% |

| Consumer Staples | 1.3% |

| Health Care | 2.0% |

| Technology | 2.2% |

| Energy | 2.6% |

| Real Estate | 3.7% |

| Utilities | 4.4% |

| U.S. Treasury Obligations | 4.8% |

| Industrials | 7.2% |

| CMO | 9.2% |

| Consumer Discretionary | 16.3% |

| CLO | 17.7% |

| Financials | 26.6% |

Top 10 Holdings (% of net assets)

| Holding Name | % of Net Assets |

| United States Treasury Bill | 4.8% |

| Electricite de France S.A. | 2.1% |

| OZLM XXIV Ltd., C2 | 2.0% |

| Carlyle US CLO Ltd., C | 1.9% |

| United Airlines, Inc. | 1.9% |

| Air Canada | 1.9% |

| Apidos CLO XV, DRR | 1.9% |

| Energy Transfer, L.P. | 1.9% |

| Great Outdoors Group, LLC | 1.9% |

| Deutsche Bank A.G. | 1.9% |

No material changes occurred during the year ended July 31, 2024.

Anfield Universal Fixed Income ETF

Annual Shareholder Report - July 31, 2024

Where can I find additional information about the Fund?

Additional information is available on the Fund's website ( https://regentsparkfunds.com/our-funds/anfield-universal-fixed-income-etf/?cb=2099 ), including its:

Prospectus

Financial information

Holdings

Proxy voting information

(b) Not applicable

Item 2. Code of Ethics.

| (a) | The registrant has, as of the end of the period covered by this report, adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, and principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party. |

| | |

| (b) | Not applicable. |

| | |

| (c) | During the period covered by this report, there were no amendments to any provision of the code of ethics. |

| | |

| (d) | During the period covered by this report, there were no waivers or implicit waivers of a provision of the code of ethics. |

| | |

| (e) | Not applicable. |

| | |

| (f) | See Item 19(a)(1) |

Item 3. Audit Committee Financial Expert.

| | (a)(1) The registrant’s board of trustees has determined that the registrant has at least one audit committee financial expert serving on the audit committee. |

| | |

| | (a)(2) Mark Gersten and Neil M. Kaufman are audit committee financial experts, as defined in Item 3 of Form N-CSR. Mr. Gersten and Mr. Kaufman are independent for purposes of this Item. |

| | |

| |

(a)(3) Not applicable. |

Item 4. Principal Accountant Fees and Services.

| (a) | Audit Fees. The aggregate fees billed for each of the last two fiscal years for professional services rendered by the registrant’s principal accountant for the audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years are as follows: |

| Trust Series | 2024 | 2023 |

| Anfield Universal Fixed Income ETF | $21,000 | $20,000 |

| (b) | Audit-Related Fees. There were no fees billed in each of the last two fiscal years for assurances and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item. |

| | |

| (c) | Tax Fees. The aggregate fees billed in each of the last two fiscal years for professional services rendered by the principal accountant for tax compliance are as follows: |

| Trust Series | 2024 | 2023 |

| Anfield Universal Fixed Income ETF | $4,625 | $4,400 |

Preparation of Federal & State income tax returns, assistance with calculation of required income, capital gain and excise distributions and preparation of Federal excise tax returns.

| (d) | All Other Fees. The aggregate fees billed in each of the last two fiscal years for products and services provided by the registrant’s principal accountant, other than the services reported in paragraphs (a) through (c) of this item were $0 and $0 for the fiscal years ended July 31, 2024 and 2023 respectively. |

| | |

| (e)(1) | The audit committee does not have pre-approval policies and procedures. Instead, the audit committee or audit committee chairman approves on a case-by-case basis each audit or non-audit service before the principal accountant is engaged by the registrant. |

| | |

| (e)(2) | There were no services described in each of paragraphs (b) through (d) of this Item that were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X. |

| | |

| (f) | Not applicable. |

| | |

| (g) | All non-audit fees billed by the registrant’s principal accountant for services rendered to the registrant for the fiscal years ended July 31, 2024 and 2023 respectively are disclosed in (b)-(d) above. There were no audit or non-audit services performed by the registrant’s principal accountant for the registrant’s adviser. |

| | |

| (h) | Not applicable. |

| | |

| (i) | Not applicable. |

| | |

| (j) | Not applicable. |

Item 5. Audit Committee of Listed Registrants.

The registrant is an issuer as defined in Rule 10A-3 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and has a separately-designated standing audit committee established in accordance with Section 3(a)(58)A of the Exchange Act. The registrant’s audit committee members are Mark Garbin, Mark Gersten, Neil M. Kaufman and Anita K. Krug.

Item 6. Investments.

(a) The Registrant's schedule of investments in unaffiliated issuers is included in the Financial Statements under Item 7 of this form.

(b) Not applicable.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

|

| |

| |

| Anfield Universal Fixed Income ETF |

| |

| AFIF |

| |

| |

| |

| |

| |

| |

| |

| July 31, 2024 |

| |

| Annual Financial Statements |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Advised by: |

| Regents Park Funds, LLC |

| 19900 MacArthur Blvd., Suite 655 |

| Irvine, CA 92612 |

| RegentsParkFunds.com |

| 1-866-866-4848 |

| |

| |

| Distributed by Northern Lights Distributors, LLC |

| Member FINRA |

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | ASSET BACKED SECURITIES — 17.7% | | | | | | | | | | |

| | | | | CLO — 17.6% | | | | | | | | | | |

| | 2,000,000 | | | Apidos CLO XV Series 2013-15A DRR(a),(b) | | TSFR3M + 2.962% | | 8.2440 | | 04/20/31 | | $ | 2,001,076 | |

| | 500,000 | | | Ares XXXIIR CLO Ltd. Series 2014-32RA C(a),(b) | | TSFR3M + 3.162% | | 8.4840 | | 05/15/30 | | | 501,633 | |

| | 250,000 | | | Carlyle Global Market Strategies CLO Ltd. Series 2013-4A CRR(a),(b) | | TSFR3M + 2.012% | | 7.3130 | | 01/15/31 | | | 250,045 | |

| | 2,000,000 | | | Carlyle US CLO Ltd. Series 2018-2A C(a),(b) | | TSFR3M + 3.162% | | 8.4630 | | 10/15/31 | | | 2,007,864 | |

| | 1,000,000 | | | Columbia Cent CLO Ltd. Series 2018-28A C(a),(b) | | TSFR3M + 3.682% | | 9.0090 | | 11/07/30 | | | 999,034 | |

| | 1,500,000 | | | Dryden 37 Senior Loan Fund Series 2015-37A ER(a),(b) | | TSFR3M + 5.412% | | 10.7130 | | 01/15/31 | | | 1,346,421 | |

| | 1,600,000 | | | Dryden 55 CLO Ltd. Series 2018-55A D(a),(b) | | TSFR3M + 3.112% | | 8.4130 | | 04/15/31 | | | 1,568,565 | |

| | 2,000,000 | | | Mountain View CLO IX Ltd. Series 2015-9A CR(a),(b) | | TSFR3M + 3.382% | | 8.6830 | | 07/15/31 | | | 1,931,556 | |

| | 1,000,000 | | | Oaktree CLO Ltd. Series 2019-1A D(a),(b) | | TSFR3M + 4.062% | | 9.3440 | | 04/22/30 | | | 1,001,958 | |

| | 2,150,000 | | | OZLM XXIV Ltd. Series 2019-24A C2(a),(b) | | TSFR3M + 4.522% | | 9.8040 | | 07/20/32 | | | 2,119,419 | |

| | 1,750,000 | | | Shackleton CLO Ltd. Series 2014-5RA D(a),(b) | | TSFR3M + 3.412% | | 8.7390 | | 05/07/31 | | | 1,733,085 | |

| | 2,000,000 | | | Venture XV CLO Ltd. Series 2013-15A DR2(a),(b) | | TSFR3M + 4.182% | | 9.4830 | | 07/15/32 | | | 1,925,584 | |

| | 1,000,000 | | | Zais Matrix CDO I Series 2022-18A D1(a),(b) | | TSFR3M + 4.670% | | 9.9550 | | 01/25/35 | | | 989,345 | |

| | | | | | | | | | | | | | 18,375,585 | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 0.1% | | | | | | | | | | |

| | 49,453 | | | Alternative Loan Trust Series 2007-J1 3A2(c) | | | | 4.0640 | | 11/25/36 | | | 44,690 | |

| | 1,962,650 | | | BCAP, LLC Trust Series 2007-AA2 21IO(b),(d) | | | | 0.4230 | | 04/25/37 | | | 22,374 | |

| | | | | | | | | | | | | | 67,064 | |

| | | | | TOTAL ASSET BACKED SECURITIES (Cost $18,687,405) | | | | | | | | | 18,442,649 | |

| | | | | | | | | | | | | |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 9.2% | | | | | | | | | | |

| | 100,863 | | | Fannie Mae Interest Strip Series 291 2(d) | | | | 8.0000 | | 11/25/27 | | | 6,613 | |

| | 72,779 | | | Fannie Mae Interest Strip Series 343 6(d) | | | | 5.0000 | | 10/25/33 | | | 8,119 | |

| | 88,152 | | | Fannie Mae Interest Strip Series 346 2(d) | | | | 5.5000 | | 12/25/33 | | | 14,912 | |

| | 53,392 | | | Fannie Mae Interest Strip Series 355 12(b),(d) | | | | 6.0000 | | 07/25/34 | | | 6,883 | |

| | 290,225 | | | Fannie Mae Interest Strip Series 364 2(d) | | | | 4.5000 | | 09/25/35 | | | 42,436 | |

| | 469,903 | | | Fannie Mae Interest Strip Series 365 4(d) | | | | 5.0000 | | 04/25/36 | | | 72,302 | |

| | 131,046 | | | Fannie Mae Interest Strip Series 384 28(b),(d) | | | | 6.0000 | | 05/25/36 | | | 22,810 | |

| | 73,901 | | | Fannie Mae Interest Strip Series 370 2(d) | | | | 6.0000 | | 06/25/36 | | | 16,052 | |

| | 669,461 | | | Fannie Mae Interest Strip Series 378 4(d) | | | | 5.0000 | | 07/25/36 | | | 120,954 | |

| | 500,825 | | | Fannie Mae Interest Strip Series 371 2(d) | | | | 6.5000 | | 07/25/36 | | | 98,994 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 9.2% (Continued) | | | | | | | | | | |

| | 123,373 | | | Fannie Mae Interest Strip Series 377 2(d) | | | | 5.0000 | | 10/25/36 | | $ | 21,397 | |

| | 1,447,166 | | | Fannie Mae Interest Strip Series 395 7(d) | | | | 5.5000 | | 11/25/36 | | | 275,517 | |

| | 77,408 | | | Fannie Mae Interest Strip Series 383 20(d) | | | | 5.5000 | | 07/25/37 | | | 12,546 | |

| | 387,729 | | | Fannie Mae Interest Strip Series 385 3(d) | | | | 5.0000 | | 01/25/38 | | | 62,869 | |

| | 436,786 | | | Fannie Mae Interest Strip Series 407 40(d) | | | | 6.0000 | | 01/25/38 | | | 88,848 | |

| | 761,037 | | | Fannie Mae Interest Strip Series 398 C9(d) | | | | 6.0000 | | 05/25/39 | | | 218,057 | |

| | 222,366 | | | Fannie Mae Interest Strip Series 396 2(d) | | | | 4.5000 | | 06/25/39 | | | 31,460 | |

| | 326,856 | | | Fannie Mae Interest Strip Series 399 2(d) | | | | 5.5000 | | 11/25/39 | | | 68,479 | |

| | 907,890 | | | Fannie Mae Interest Strip Series 408 C4(d) | | | | 5.5000 | | 11/25/40 | | | 165,862 | |

| | 338,941 | | | Fannie Mae Interest Strip Series 409 C18(d) | | | | 4.0000 | | 04/25/42 | | | 62,929 | |

| | 56,917 | | | Fannie Mae REMICS Series 2001-32 SA(b),(d) | | SOFR30A + 7.836% | | 2.4880 | | 07/25/31 | | | 2,751 | |

| | 384,824 | | | Fannie Mae REMICS Series 2003-7 SN(b),(d) | | SOFR30A + 7.636% | | 2.2880 | | 02/25/33 | | | 45,412 | |

| | 98,176 | | | Fannie Mae REMICS Series 2003-43 IY(d) | | | | 6.0000 | | 05/25/33 | | | 10,777 | |

| | 184,681 | | | Fannie Mae REMICS Series 2004-62 TP(b),(d) | | SOFR30A + 37.870% | | 5.5000 | | 07/25/33 | | | 22,576 | |

| | 234,889 | | | Fannie Mae REMICS Series 2004-70 XJ(b),(d) | | | | 5.0000 | | 10/25/34 | | | 34,810 | |

| | 171,683 | | | Fannie Mae REMICS Series 2004-91 DS(b),(d) | | SOFR30A + 6.536% | | 1.1880 | | 12/25/34 | | | 14,486 | |

| | 58,311 | | | Fannie Mae REMICS Series 2005-87 SE(b),(d) | | SOFR30A + 5.936% | | 0.5880 | | 10/25/35 | | | 4,249 | |

| | 101,174 | | | Fannie Mae REMICS Series 2005-89 S(b),(d) | | SOFR30A + 6.586% | | 1.2380 | | 10/25/35 | | | 7,712 | |

| | 146,317 | | | Fannie Mae REMICS Series 2007-28 LS(b),(d) | | SOFR30A + 6.511% | | 1.1630 | | 01/25/36 | | | 14,201 | |

| | 19,130 | | | Fannie Mae REMICS Series 2006-8 WN(b),(d) | | SOFR30A + 6.586% | | 1.2380 | | 03/25/36 | | | 1,824 | |

| | 41,556 | | | Fannie Mae REMICS Series 2006-8 HL(b),(d) | | SOFR30A + 6.586% | | 1.2380 | | 03/25/36 | | | 3,892 | |

| | 1,217,631 | | | Fannie Mae REMICS Series 2007-18 BF(b),(d) | | SOFR30A + 0.494% | | 5.8420 | | 04/25/36 | | | 144,759 | |

| | 1,257,707 | | | Fannie Mae REMICS Series 2007-28 CF(b),(d) | | SOFR30A + 0.504% | | 5.8520 | | 07/25/36 | | | 171,553 | |

| | 110,503 | | | Fannie Mae REMICS Series 2006-101 SA(b),(d) | | SOFR30A + 6.466% | | 1.1180 | | 10/25/36 | | | 11,265 | |

| | 103,691 | | | Fannie Mae REMICS Series 2006-116 S(b),(d) | | SOFR30A + 6.486% | | 1.1380 | | 12/25/36 | | | 9,076 | |

| | 46,404 | | | Fannie Mae REMICS Series 2006-125 SM(b),(d) | | SOFR30A + 7.086% | | 1.7380 | | 01/25/37 | | | 4,606 | |

| | 186,850 | | | Fannie Mae REMICS Series 2007-36 SN(b),(d) | | SOFR30A + 6.656% | | 1.3080 | | 04/25/37 | | | 20,297 | |

| | 664,075 | | | Fannie Mae REMICS Series 2007-55 S(b),(d) | | SOFR30A + 6.646% | | 1.2980 | | 06/25/37 | | | 29,851 | |

| | 79,021 | | | Fannie Mae REMICS Series 2007-72 EK(b),(d) | | SOFR30A + 6.286% | | 0.9380 | | 07/25/37 | | | 7,700 | |

| | 88,471 | | | Fannie Mae REMICS Series 2007-66 AS(b),(d) | | SOFR30A + 6.486% | | 1.1380 | | 07/25/37 | | | 7,017 | |

| | 589,264 | | | Fannie Mae REMICS Series 2007-88 MI(b),(d) | | SOFR30A + 6.406% | | 1.0580 | | 09/25/37 | | | 49,333 | |

| | 92,977 | | | Fannie Mae REMICS Series 2007-106 SN(b),(d) | | SOFR30A + 6.296% | | 0.9480 | | 11/25/37 | | | 8,630 | |

| | 169,844 | | | Fannie Mae REMICS Series 2007-109 DI(b),(d) | | SOFR30A + 6.286% | | 0.9380 | | 12/25/37 | | | 18,688 | |

| | 258,632 | | | Fannie Mae REMICS Series 2007-117 SM(b),(d) | | SOFR30A + 6.186% | | 0.8380 | | 01/25/38 | | | 21,796 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 9.2% (Continued) | | | | | | | | | | |

| | 4,699,291 | | | Fannie Mae REMICS Series 2010-89 AI(b),(d) | | SOFR30A + 6.336% | | 0.1500 | | 02/25/38 | | $ | 15,711 | |

| | 17,136 | | | Fannie Mae REMICS Series 2008-24 SP(b) | | SOFR30A + 22.864% | | 3.2570 | | 02/25/38 | | | 17,095 | |

| | 1,591,586 | | | Fannie Mae REMICS Series 2008-58 SE(b),(d) | | SOFR30A + 5.886% | | 0.5380 | | 07/25/38 | | | 139,650 | |

| | 277,623 | | | Fannie Mae REMICS Series 2009-66 SH(b),(d) | | SOFR30A + 5.936% | | 0.5880 | | 09/25/39 | | | 15,048 | |

| | 86,404 | | | Fannie Mae REMICS Series 2009-112 ST(b),(d) | | SOFR30A + 6.136% | | 0.7880 | | 01/25/40 | | | 7,895 | |

| | 79,350 | | | Fannie Mae REMICS Series 2010-126 UI(d) | | | | 5.5000 | | 10/25/40 | | | 8,860 | |

| | 268,266 | | | Fannie Mae REMICS Series 2010-130 HI(d) | | | | 6.0000 | | 11/25/40 | | | 50,647 | |

| | 331,884 | | | Fannie Mae REMICS Series 2010-139 SA(b),(d) | | SOFR30A + 5.916% | | 0.5680 | | 12/25/40 | | | 32,615 | |

| | 64,994 | | | Fannie Mae REMICS Series 2011-11 PI(d) | | | | 4.0000 | | 03/25/41 | | | 7,595 | |

| | 226,750 | | | Fannie Mae REMICS Series 2017-87 KI(d) | | | | 5.0000 | | 06/25/41 | | | 31,477 | |

| | 351,215 | | | Fannie Mae REMICS Series 2011-96 SA(b),(d) | | SOFR30A + 6.436% | | 1.0880 | | 10/25/41 | | | 25,132 | |

| | 2,074,784 | | | Fannie Mae REMICS Series 2012-30 CI(d) | | | | 5.0000 | | 10/25/41 | | | 227,112 | |

| | 1,414,056 | | | Fannie Mae REMICS Series 2011-122 DS(b),(d) | | SOFR30A + 6.406% | | 1.0580 | | 12/25/41 | | | 182,473 | |

| | 555,887 | | | Fannie Mae REMICS Series 2012-68 NS(b),(d) | | SOFR30A + 6.586% | | 1.2380 | | 03/25/42 | | | 34,994 | |

| | 756,405 | | | Fannie Mae REMICS Series 2012-89 SA(b),(d) | | SOFR30A + 5.436% | | 0.0880 | | 08/25/42 | | | 52,812 | |

| | 1,252,855 | | | Fannie Mae REMICS Series 2012-103 TI(d) | | | | 5.0000 | | 09/25/42 | | | 212,494 | |

| | 82,990 | | | Fannie Mae REMICS Series 2014-68 IB(d) | | | | 4.5000 | | 02/25/43 | | | 7,548 | |

| | 258,040 | | | Fannie Mae REMICS Series 2013-103 JS(b),(d) | | SOFR30A + 5.886% | | 0.5380 | | 10/25/43 | | | 23,355 | |

| | 314,635 | | | Fannie Mae REMICS Series 2014-38 QI(d) | | | | 5.5000 | | 12/25/43 | | | 51,045 | |

| | 1,015,308 | | | Fannie Mae REMICS Series 2014-87 MS(b),(d) | | SOFR30A + 6.136% | | 0.7880 | | 01/25/45 | | | 96,978 | |

| | 209,260 | | | Fannie Mae REMICS Series 2015-33 OI(d) | | | | 5.0000 | | 06/25/45 | | | 25,042 | |

| | 398,712 | | | Fannie Mae REMICS Series 2016-39 LS(b),(d) | | SOFR30A + 5.886% | | 0.5380 | | 07/25/46 | | | 42,523 | |

| | 1,372,314 | | | Fannie Mae REMICS Series 2017-97 SW(b),(d) | | SOFR30A + 6.086% | | 0.7380 | | 12/25/47 | | | 182,582 | |

| | 919,928 | | | Fannie Mae REMICS Series 2017-108 SA(b),(d) | | SOFR30A + 6.036% | | 0.6880 | | 01/25/48 | | | 129,878 | |

| | 2,751,972 | | | Fannie Mae REMICS Series 2018-54 SA(b),(d) | | SOFR30A + 6.136% | | 0.7880 | | 08/25/48 | | | 268,148 | |

| | 443,400 | | | Fannie Mae REMICS Series 2018-58 IO(d) | | | | 5.5000 | | 08/25/48 | | | 69,823 | |

| | 110,658 | | | Fannie Mae REMICS Series 2018-74 MI(d) | | | | 4.5000 | | 10/25/48 | | | 21,368 | |

| | 388,816 | | | Fannie Mae REMICS Series 2019-41 SB(b),(d) | | SOFR30A + 5.936% | | 0.5880 | | 08/25/49 | | | 47,369 | |

| | 1,044,120 | | | Fannie Mae REMICS Series 2020-10 S(b),(d) | | SOFR30A + 5.936% | | 0.5880 | | 05/25/59 | | | 131,254 | |

| | 77,487 | | | Freddie Mac REMICS Series 2367 SG(b),(d) | | SOFR30A + 7.766% | | 2.4280 | | 06/15/31 | | | 7,268 | |

| | 847,203 | | | Freddie Mac REMICS Series 5112 IB(d) | | | | 6.5000 | | 05/15/32 | | | 104,003 | |

| | 67,125 | | | Freddie Mac REMICS Series 2444 TI(b),(d) | | | | 6.5000 | | 05/15/32 | | | 8,336 | |

| | 188,827 | | | Freddie Mac REMICS Series 2463 SB(b),(d) | | SOFR30A + 7.886% | | 2.5480 | | 06/15/32 | | | 15,774 | |

| | 25,447 | | | Freddie Mac REMICS Series 2524 SX(b),(d) | | SOFR30A + 7.786% | | 2.4480 | | 11/15/32 | | | 2,699 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 9.2% (Continued) | | | | | | | | | | |

| | 41,564 | | | Freddie Mac REMICS Series 2616 SC(b),(d) | | SOFR30A + 7.886% | | 2.5480 | | 12/15/32 | | $ | 3,211 | |

| | 503,312 | | | Freddie Mac REMICS Series 2802 SI(b),(d) | | SOFR30A + 5.886% | | 0.5480 | | 05/15/34 | | | 32,737 | |

| | 250,839 | | | Freddie Mac REMICS Series 2980 SL(b),(d) | | SOFR30A + 6.586% | | 1.2480 | | 11/15/34 | | | 21,593 | |

| | 259,274 | | | Freddie Mac REMICS Series 2950 SN(b),(d) | | SOFR30A + 5.936% | | 0.5980 | | 03/15/35 | | | 15,204 | |

| | 698,294 | | | Freddie Mac REMICS Series 3055 MS(b),(d) | | SOFR30A + 6.486% | | 1.1480 | | 10/15/35 | | | 68,686 | |

| | 47,436 | | | Freddie Mac REMICS Series 3117 JS(b),(d) | | SOFR30A + 6.586% | | 1.2480 | | 02/15/36 | | | 4,453 | |

| | 195,291 | | | Freddie Mac REMICS Series 3149 SM(b),(d) | | SOFR30A + 6.536% | | 1.1980 | | 05/15/36 | | | 15,454 | |

| | 88,889 | | | Freddie Mac REMICS Series 3239 SI(b),(d) | | SOFR30A + 6.536% | | 1.1980 | | 11/15/36 | | | 8,943 | |

| | 194,438 | | | Freddie Mac REMICS Series 3303 SG(b),(d) | | SOFR30A + 5.986% | | 0.6480 | | 04/15/37 | | | 16,390 | |

| | 185,852 | | | Freddie Mac REMICS Series 3355 BI(b),(d) | | SOFR30A + 5.936% | | 0.5980 | | 08/15/37 | | | 15,383 | |

| | 184,092 | | | Freddie Mac REMICS Series 3368 AI(b),(d) | | SOFR30A + 5.916% | | 0.5780 | | 09/15/37 | | | 16,624 | |

| | 124,962 | | | Freddie Mac REMICS Series 4340 TI(d) | | | | 5.5000 | | 07/15/39 | | | 6,326 | |

| | 136,015 | | | Freddie Mac REMICS Series 3572 VS(b),(d) | | SOFR30A + 6.616% | | 1.2780 | | 09/15/39 | | | 15,104 | |

| | 160,919 | | | Freddie Mac REMICS Series 4451 DI(d) | | | | 3.5000 | | 10/15/39 | | | 6,412 | |

| | 1,993,971 | | | Freddie Mac REMICS Series 3652 CS(b),(d) | | SOFR30A + 6.436% | | 1.0980 | | 03/15/40 | | | 230,290 | |

| | 143,552 | | | Freddie Mac REMICS Series 3758 S(b),(d) | | SOFR30A + 5.916% | | 0.5780 | | 11/15/40 | | | 11,821 | |

| | 482,302 | | | Freddie Mac REMICS Series 3935 SH(b),(d) | | SOFR30A + 6.486% | | 1.1480 | | 12/15/40 | | | 12,520 | |

| | 102,250 | | | Freddie Mac REMICS Series 4139 PO(e) | | | | 2.3100 | | 08/15/42 | | | 67,452 | |

| | 131,643 | | | Freddie Mac REMICS Series 4091 TS(b),(d) | | SOFR30A + 6.436% | | 1.0980 | | 08/15/42 | | | 16,707 | |

| | 373,640 | | | Freddie Mac REMICS Series 4471 JI(d) | | | | 4.5000 | | 09/15/43 | | | 64,374 | |

| | 1,096,615 | | | Freddie Mac REMICS Series 4995 KI(d) | | | | 5.5000 | | 12/25/43 | | | 180,179 | |

| | 164,963 | | | Freddie Mac REMICS Series 4456 IA(d) | | | | 4.0000 | | 03/15/45 | | | 27,771 | |

| | 7,617,579 | | | Freddie Mac REMICS Series 4583 TI(b),(d) | | SOFR30A + 5.986% | | 0.1000 | | 05/15/46 | | | 21,647 | |

| | 218,018 | | | Freddie Mac REMICS Series 4583 ST(b),(d) | | SOFR30A + 5.886% | | 0.5480 | | 05/15/46 | | | 23,213 | |

| | 370,222 | | | Freddie Mac REMICS Series 4618 SA(b),(d) | | SOFR30A + 5.886% | | 0.5480 | | 09/15/46 | | | 50,513 | |

| | 712,528 | | | Freddie Mac REMICS Series 5007 SK(b),(d) | | SOFR30A + 5.986% | | 0.6380 | | 08/25/50 | | | 86,340 | |

| | 524,035 | | | Freddie Mac REMICS Series 5136 IJ(d) | | | | 2.5000 | | 02/25/51 | | | 62,918 | |

| | 896,802 | | | Freddie Mac REMICS Series 5086 HI(d) | | | | 4.5000 | | 03/25/51 | | | 197,884 | |

| | 971,471 | | | Freddie Mac REMICS Series 5174 NI(d) | | | | 3.5000 | | 12/25/51 | | | 172,835 | |

| | 213,272 | | | Freddie Mac REMICS Series 4291 MS(b),(d) | | SOFR30A + 5.786% | | 0.4480 | | 01/15/54 | | | 18,184 | |

| | 90,412 | | | Freddie Mac Strips Series 221 IO(d) | | | | 7.0000 | | 03/15/32 | | | 15,098 | |

| | 3,223,075 | | | Freddie Mac Strips Series 324 C17(d) | | | | 3.5000 | | 12/15/33 | | | 306,646 | |

| | 234,729 | | | Freddie Mac Strips Series 238 8(d) | | | | 5.0000 | | 04/15/36 | | | 40,033 | |

| | 263,693 | | | Freddie Mac Strips Series 240 IO(d) | | | | 5.5000 | | 07/15/36 | | | 49,374 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 9.2% (Continued) | | | | | | | | | | |

| | 46,372 | | | Freddie Mac Strips Series 239 IO(d) | | | | 6.0000 | | 08/15/36 | | $ | 7,556 | |

| | 389,455 | | | Freddie Mac Strips Series 247 24(d) | | | | 5.0000 | | 09/15/36 | | | 60,558 | |

| | 661,953 | | | Freddie Mac Strips Series 244 IO(d) | | | | 5.5000 | | 12/15/36 | | | 99,998 | |

| | 311,266 | | | Freddie Mac Strips Series 303 105(b),(d) | | | | 4.0000 | | 01/15/43 | | | 43,335 | |

| | 1,108,770 | | | Freddie Mac Strips Series 324 C24(d) | | | | 5.0000 | | 12/15/43 | | | 230,140 | |

| | 648,374 | | | Freddie Mac Strips Series 365 121(b),(d) | | | | 4.0000 | | 10/15/47 | | | 93,572 | |

| | 589,674 | | | Freddie Mac Strips Series 365 C10(d) | | | | 3.5000 | | 06/15/49 | | | 111,396 | |

| | 950,222 | | | Freddie Mac Strips Series 367 116(b),(d) | | | | 3.5000 | | 06/15/50 | | | 141,984 | |

| | 529,369 | | | Government National Mortgage Association Series 2021-78 QI(d) | | | | 5.0000 | | 05/20/34 | | | 50,872 | |

| | 346,240 | | | Government National Mortgage Association Series 2004-46 S(b),(d) | | TSFR1M + 6.986% | | 1.6400 | | 06/20/34 | | | 19,365 | |

| | 24,655 | | | Government National Mortgage Association Series 2004-106 HW(b) | | TSFR1M + 26.928% | | 0.2890 | | 12/16/34 | | | 24,855 | |

| | 117,282 | | | Government National Mortgage Association Series 2007-40 SW(b),(d) | | TSFR1M + 4.066% | | — | | 07/20/37 | | | 544 | |

| | 131,773 | | | Government National Mortgage Association Series 2008-2 SM(b),(d) | | TSFR1M + 6.386% | | 1.0580 | | 01/16/38 | | | 9,587 | |

| | 76,111 | | | Government National Mortgage Association Series 2008-6 SD(b),(d) | | TSFR1M + 6.346% | | 1.0000 | | 02/20/38 | | | 42 | |

| | 962,788 | | | Government National Mortgage Association Series 2008-15 CI(b),(d) | | TSFR1M + 6.376% | | 1.0300 | | 02/20/38 | | | 30,230 | |

| | 116,053 | | | Government National Mortgage Association Series 2008-27 SI(b),(d) | | TSFR1M + 6.356% | | 1.0100 | | 03/20/38 | | | 3,349 | |

| | 95,984 | | | Government National Mortgage Association Series 2008-36 SB(b),(d) | | TSFR1M + 6.156% | | 0.8100 | | 04/20/38 | | | 43 | |

| | 145,418 | | | Government National Mortgage Association Series 2008-51 SE(b),(d) | | TSFR1M + 6.136% | | 0.8080 | | 06/16/38 | | | 9,788 | |

| | 120,170 | | | Government National Mortgage Association Series 2008-51 SC(b),(d) | | TSFR1M + 6.136% | | 0.7900 | | 06/20/38 | | | 7,098 | |

| | 58,321 | | | Government National Mortgage Association Series 2008-95 DS(b),(d) | | TSFR1M + 7.186% | | 1.8400 | | 12/20/38 | | | 1,560 | |

| | 101,608 | | | Government National Mortgage Association Series 2009-43 SA(b),(d) | | TSFR1M + 5.836% | | 0.4900 | | 06/20/39 | | | 3,623 | |

| | 41,935 | | | Government National Mortgage Association Series 2010-19 SD(b),(d) | | TSFR1M + 6.436% | | 1.1080 | | 07/16/39 | | | 224 | |

| | 356,319 | | | Government National Mortgage Association Series 2013-170 ID(b),(d) | | | | 3.2490 | | 02/20/40 | | | 30,222 | |

| | 68,155 | | | Government National Mortgage Association Series 2010-113 BS(b),(d) | | TSFR1M + 5.886% | | 0.5400 | | 09/20/40 | | | 7,213 | |

| | 1,059,653 | | | Government National Mortgage Association Series 2010-133 SB(b),(d) | | TSFR1M + 5.906% | | 0.5780 | | 10/16/40 | | | 115,906 | |

| | 119,181 | | | Government National Mortgage Association Series 2010-152 SA(b),(d) | | TSFR1M + 5.936% | | 0.6080 | | 11/16/40 | | | 12,801 | |

| | 310,893 | | | Government National Mortgage Association Series 2012-77 DI(d) | | | | 4.0000 | | 01/20/41 | | | 17,750 | |

| | 132,303 | | | Government National Mortgage Association Series 2012-69 QI(d) | | | | 4.0000 | | 03/16/41 | | | 14,943 | |

| | 312,444 | | | Government National Mortgage Association Series 2011-148 SN(b),(d) | | TSFR1M + 6.576% | | 1.2480 | | 11/16/41 | | | 38,825 | |

| | 1,012,885 | | | Government National Mortgage Association Series 2013-4 ID(d) | | | | 5.5000 | | 05/16/42 | | | 189,048 | |

| | 842,398 | | | Government National Mortgage Association Series 2012-126 IO(d) | | | | 3.5000 | | 10/20/42 | | | 133,831 | |

| | 115,033 | | | Government National Mortgage Association Series 2013-5 BI(d) | | | | 3.5000 | | 01/20/43 | | | 18,861 | |

| | 206,076 | | | Government National Mortgage Association Series 2013-53 OI(d) | | | | 3.5000 | | 04/20/43 | | | 21,146 | |

| | 955,889 | | | Government National Mortgage Association Series 2015-179 BI(d) | | | | 4.0000 | | 08/20/43 | | | 68,087 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 9.2% (Continued) | | | | | | | | | | |

| | 84,078 | | | Government National Mortgage Association Series 2013-181 SA(b),(d) | | TSFR1M + 5.986% | | 0.6400 | | 11/20/43 | | $ | 6,330 | |

| | 181,677 | | | Government National Mortgage Association Series 2014-58 SA(b),(d) | | TSFR1M + 5.986% | | 0.6400 | | 04/20/44 | | | 18,870 | |

| | 326,702 | | | Government National Mortgage Association Series 2014-91 SB(b),(d) | | TSFR1M + 5.486% | | 0.1580 | | 06/16/44 | | | 31,254 | |

| | 68,226 | | | Government National Mortgage Association Series 2016-81 IM(d) | | | | 4.0000 | | 10/20/44 | | | 4,371 | |

| | 1,350,943 | | | Government National Mortgage Association Series 2014-146 EI(d) | | | | 5.0000 | | 10/20/44 | | | 276,063 | |

| | 1,138,175 | | | Government National Mortgage Association Series 2017-56 IE(d) | | | | 4.0000 | | 11/20/44 | | | 98,458 | |

| | 515,246 | | | Government National Mortgage Association Series 2019-22 SA(b),(d) | | TSFR1M + 5.486% | | 0.1400 | | 02/20/45 | | | 44,413 | |

| | 288,432 | | | Government National Mortgage Association Series 2015-36 MI(d) | | | | 5.5000 | | 03/20/45 | | | 41,511 | |

| | 444,728 | | | Government National Mortgage Association Series 2015-64 SG(b),(d) | | TSFR1M + 5.486% | | 0.1400 | | 05/20/45 | | | 42,939 | |

| | 74,505 | | | Government National Mortgage Association Series 2016-27 IA(d) | | | | 4.0000 | | 06/20/45 | | | 9,750 | |

| | 241,042 | | | Government National Mortgage Association Series 2017-99 DI(d) | | | | 4.0000 | | 07/20/45 | | | 13,631 | |

| | 515,089 | | | Government National Mortgage Association Series 2015-144 SA(b),(d) | | TSFR1M + 6.086% | | 0.7400 | | 10/20/45 | | | 71,502 | |

| | 302,354 | | | Government National Mortgage Association Series 2016-84 IG(d) | | | | 4.5000 | | 11/16/45 | | | 55,746 | |

| | 442,460 | | | Government National Mortgage Association Series 2016-4 SM(b),(d) | | TSFR1M + 5.536% | | 0.1900 | | 01/20/46 | | | 39,212 | |

| | 179,024 | | | Government National Mortgage Association Series 2016-9 SA(b),(d) | | TSFR1M + 5.986% | | 0.6400 | | 01/20/46 | | | 18,473 | |

| | 902,405 | | | Government National Mortgage Association Series 2016-121 JS(b),(d) | | TSFR1M + 5.986% | | 0.6400 | | 09/20/46 | | | 108,455 | |

| | 185,785 | | | Government National Mortgage Association Series 2016-145 UI(d) | | | | 3.5000 | | 10/20/46 | | | 31,687 | |

| | 174,311 | | | Government National Mortgage Association Series 2017-68 CI(d) | | | | 5.5000 | | 05/16/47 | | | 33,806 | |

| | 296,486 | | | Government National Mortgage Association Series 2018-8 IO(d) | | | | 4.0000 | | 01/20/48 | | | 58,541 | |

| | 18,642,816 | | | Government National Mortgage Association Series 2020-86 TK(b),(d) | | TSFR1M + 6.086% | | 0.1500 | | 08/20/48 | | | 94,596 | |

| | 178,905 | | | Government National Mortgage Association Series 2018-120 JI(d) | | | | 5.5000 | | 09/20/48 | | | 25,759 | |

| | 269,295 | | | Government National Mortgage Association Series 2018-154 IT(d) | | | | 5.5000 | | 10/20/48 | | | 48,945 | |

| | 453,981 | | | Government National Mortgage Association Series 2019-6 SA(b),(d) | | TSFR1M + 5.936% | | 0.5900 | | 01/20/49 | | | 47,262 | |

| | 1,368,812 | | | Government National Mortgage Association Series 2020-47 MI(d) | | | | 3.5000 | | 04/20/50 | | | 247,761 | |

| | 654,828 | | | Government National Mortgage Association Series 2020-167 NS(b),(d) | | TSFR1M + 6.186% | | 0.8400 | | 11/20/50 | | | 84,555 | |

| | 2,398,079 | | | Government National Mortgage Association Series 2019-H16 CI(b),(d) | | | | 0.5880 | | 10/20/69 | | | 106,477 | |

| | | | | TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS (Cost $13,679,955) | | | | | | | | | 9,562,942 | |

| | | | | | | | | | | | | | | |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 54.6% | | | | | | | | | | |

| | | | | ASSET MANAGEMENT — 5.6% | | | | | | | | | | |

| | 750,000 | | | Ares Capital Corporation | | | | 3.2500 | | 07/15/25 | | | 733,366 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 54.6% (Continued) | | | | | | | | | | |

| | | | | ASSET MANAGEMENT — 5.6% (Continued) | | | | | | | | | | |

| | 1,250,000 | | | Bain Capital Specialty Finance, Inc. | | | | 2.9500 | | 03/10/26 | | $ | 1,188,955 | |

| | 600,000 | | | Blackstone Secured Lending Fund | | | | 3.6250 | | 01/15/26 | | | 581,021 | |

| | 1,480,000 | | | FS KKR Capital Corporation | | | | 4.1250 | | 02/01/25 | | | 1,466,462 | |

| | 650,000 | | | Nuveen Finance, LLC(a) | | | | 4.1250 | | 11/01/24 | | | 647,435 | |

| | 500,000 | | | UBS Group A.G.(a),(b) | | SOFRRATE + 1.560% | | 2.5930 | | 09/11/25 | | | 498,269 | |

| | 500,000 | | | UBS Group A.G.(a),(b) | | H15T1Y + 1.550% | | 4.4880 | | 05/12/26 | | | 496,158 | |

| | 250,000 | | | UBS Group A.G.(a),(b) | | SOFRRATE + 2.044% | | 2.1930 | | 06/05/26 | | | 243,265 | |

| | | | | | | | | | | | | | 5,854,931 | |

| | | | | AUTOMOTIVE — 8.4% | | | | | | | | | | |

| | 764,000 | | | Ford Motor Credit Company, LLC | | | | 3.6640 | | 09/08/24 | | | 762,014 | |

| | 985,000 | | | Ford Motor Credit Company, LLC | | | | 4.6870 | | 06/09/25 | | | 976,715 | |

| | 1,000,000 | | | Ford Motor Credit Company, LLC | | | | 5.1250 | | 06/16/25 | | | 994,976 | |

| | 600,000 | | | Ford Motor Credit Company, LLC | | | | 4.1340 | | 08/04/25 | | | 591,575 | |

| | 1,083,000 | | | Ford Motor Credit Company, LLC | | | | 3.3750 | | 11/13/25 | | | 1,054,424 | |

| | 500,000 | | | Ford Motor Credit Company, LLC | | | | 4.5420 | | 08/01/26 | | | 491,406 | |

| | 500,000 | | | Ford Motor Credit Company, LLC | | | | 4.8500 | | 11/20/29 | | | 476,860 | |

| | 1,250,000 | | | General Motors Financial Company, Inc. | | | | 1.2000 | | 10/15/24 | | | 1,238,571 | |

| | 310,000 | | | Harley-Davidson Financial Services, Inc.(a) | | | | 3.3500 | | 06/08/25 | | | 303,769 | |

| | 980,000 | | | Nissan Motor Acceptance Company, LLC(a) | | | | 1.1250 | | 09/16/24 | | | 973,616 | |

| | 723,000 | | | Nissan Motor Acceptance Company, LLC | | | | 2.0000 | | 03/09/26 | | | 681,775 | |

| | 200,000 | | | Nissan Motor Company Ltd.(a) | | | | 3.5220 | | 09/17/25 | | | 195,184 | |

| | | | | | | | | | | | | | 8,740,885 | |

| | | | | BANKING — 15.9% | | | | | | | | | | |

| | 550,000 | | | ABN AMRO Bank N.V.(a) | | | | 4.7500 | | 07/28/25 | | | 544,921 | |

| | 287,000 | | | Bank of America Corporation | | | | 4.2000 | | 08/26/24 | | | 286,654 | |

| | 100,000 | | | Bank of America Corporation Series N(b) | | SOFRRATE + 0.910% | | 0.9810 | | 09/25/25 | | | 99,280 | |

| | 500,000 | | | Bank of Montreal | | | | 5.1000 | | 01/31/25 | | | 496,681 | |

| | 1,000,000 | | | BNP Paribas S.A. | | | | 4.2500 | | 10/15/24 | | | 996,233 | |

| | 1,002,000 | | | BNP Paribas S.A.(a) | | | | 4.3750 | | 09/28/25 | | | 989,878 | |

| | 1,000,000 | | | BPCE S.A.(a) | | | | 4.5000 | | 03/15/25 | | | 990,708 | |

| | 1,617,000 | | | Credit Agricole S.A.(a) | | | | 4.3750 | | 03/17/25 | | | 1,603,728 | |

| | 750,000 | | | Credit Suisse A.G. | | | | 4.7500 | | 08/09/24 | | | 749,853 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 54.6% (Continued) | | | | | | | | | | |

| | | | | BANKING — 15.9% (Continued) | | | | | | | | | | |

| | 1,950,000 | | | Deutsche Bank A.G. | | | | 4.5000 | | 04/01/25 | | $ | 1,934,057 | |

| | 255,000 | | | Deutsche Bank A.G.(b) | | SOFRRATE + 2.581% | | 3.9610 | | 11/26/25 | | | 253,502 | |

| | 1,000,000 | | | Deutsche Bank A.G.(b) | | H15T5Y + 4.524% | | 6.0000 | | 02/14/2170 | | | 960,738 | |

| | 645,000 | | | Discover Bank | | | | 2.4500 | | 09/12/24 | | | 642,516 | |

| | 1,000,000 | | | First Citizens BancShares, Inc.(a),(b) | | TSFR3M + 4.234% | | 9.5730 | | 06/15/2170 | | | 1,021,616 | |

| | 500,000 | | | JPMorgan Chase & Company | | | | 3.8750 | | 09/10/24 | | | 499,125 | |

| | 1,015,000 | | | KeyCorporation(b) | | SOFRINDX + 1.250% | | 3.8780 | | 05/23/25 | | | 1,016,068 | |

| | 625,000 | | | Lloyds Banking Group plc | | | | 4.5000 | | 11/04/24 | | | 623,114 | |

| | 200,000 | | | Lloyds Banking Group plc | | | | 4.5820 | | 12/10/25 | | | 197,850 | |

| | 750,000 | | | Manufacturers & Traders Trust Company | | | | 2.9000 | | 02/06/25 | | | 739,354 | |

| | 500,000 | | | Manufacturers & Traders Trust Company | | | | 4.6500 | | 01/27/26 | | | 495,001 | |

| | 500,000 | | | NatWest Markets plc(a) | | | | 0.8000 | | 08/12/24 | | | 499,272 | |

| | 800,000 | | | Societe Generale S.A.(a) | | | | 4.2500 | | 04/14/25 | | | 789,432 | |

| | 175,000 | | | Societe Generale S.A.(a) | | | | 4.7500 | | 11/24/25 | | | 172,520 | |

| | | | | | | | | | | | | | 16,602,101 | |

| | | | | BEVERAGES — 0.6% | | | | | | | | | | |

| | 665,000 | | | JDE Peet’s N.V.(a) | | | | 0.8000 | | 09/24/24 | | | 659,309 | |

| | | | | | | | | | | | | | | |

| | | | | BIOTECH & PHARMA — 1.3% | | | | | | | | | | |

| | 375,000 | | | Teva Pharmaceutical Finance Netherlands III BV | | | | 7.1250 | | 01/31/25 | | | 376,590 | |

| | 766,000 | | | Teva Pharmaceutical Finance Netherlands III BV | | | | 3.1500 | | 10/01/26 | | | 725,491 | |

| | 250,000 | | | Teva Pharmaceutical Finance Netherlands III BV | | | | 4.7500 | | 05/09/27 | | | 242,587 | |

| | | | | | | | | | | | | | 1,344,668 | |

| | | | | ELECTRIC UTILITIES — 4.4% | | | | | | | | | | |

| | 2,000,000 | | | Electricite de France S.A.(a),(b) | | H15T5Y + 5.411% | | 9.1250 | | 06/15/2173 | | | 2,220,969 | |

| | 715,000 | | | FirstEnergy Corporation | | | | 2.0500 | | 03/01/25 | | | 700,164 | |

| | 1,300,000 | | | FirstEnergy Transmission, LLC(a) | | | | 4.3500 | | 01/15/25 | | | 1,290,053 | |

| | 421,000 | | | Pennsylvania Electric Company(a) | | | | 4.1500 | | 04/15/25 | | | 416,000 | |

| | | | | | | | | | | | | | 4,627,186 | |

| | | | | HEALTH CARE FACILITIES & SERVICES — 0.7% | | | | | | | | | | |

| | 750,000 | | | Laboratory Corp of America Holdings | | | | 3.2500 | | 09/01/24 | | | 748,216 | |

| | | | | | | | | | | | | | | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 54.6% (Continued) | | | | | | | | | | |

| | | | | INSTITUTIONAL FINANCIAL SERVICES — 1.1% | | | | | | | | | | |

| | 1,000,000 | | | Bank of New York Mellon Corporation (The) Series H(b) | | H15T5Y + 3.352% | | 3.7000 | | 03/20/2170 | | $ | 959,673 | |

| | 200,000 | | | Morgan Stanley(b) | | SOFRRATE + 0.509% | | 5.8520 | | 01/22/25 | | | 200,091 | |

| | | | | | | | | | | | | | 1,159,764 | |

| | | | | INSURANCE — 0.6% | | | | | | | | | | |

| | 100,000 | | | Athene Global Funding(a) | | | | 2.5000 | | 01/14/25 | | | 98,551 | |

| | 506,000 | | | Kemper Corporation | | | | 4.3500 | | 02/15/25 | | | 502,647 | |

| | | | | | | | | | | | | | 601,198 | |

| | | | | LEISURE FACILITIES & SERVICES — 2.3% | | | | | | | | | | |

| | 425,000 | | | International Game Technology plc(a) | | | | 6.2500 | | 01/15/27 | | | 429,138 | |

| | 800,000 | | | Las Vegas Sands Corporation | | | | 2.9000 | | 06/25/25 | | | 780,384 | |

| | 784,000 | | | Penn National Gaming, Inc.(a) | | | | 5.6250 | | 01/15/27 | | | 765,706 | |

| | 375,000 | | | Scientific Games International, Inc.(a) | | | | 7.0000 | | 05/15/28 | | | 378,027 | |

| | | | | | | | | | | | | | 2,353,255 | |

| | | | | OIL & GAS PRODUCERS — 2.6% | | | | | | | | | | |

| | 1,976,000 | | | Energy Transfer, L.P.(b) | | H15T5Y + 5.694% | | 6.5000 | | 11/15/2169 | | | 1,967,533 | |

| | 750,000 | | | Plains All American Pipeline, L.P. / PAA Finance | | | | 3.6000 | | 11/01/24 | | | 745,941 | |

| | | | | | | | | | | | | | 2,713,474 | |

| | | | | REAL ESTATE INVESTMENT TRUSTS — 3.7% | | | | | | | | | | |

| | 677,000 | | | Crown Castle, Inc. | | | | 3.2000 | | 09/01/24 | | | 675,253 | |

| | 700,000 | | | GLP Capital, L.P. / GLP Financing II, Inc. | | | | 3.3500 | | 09/01/24 | | | 699,648 | |

| | 800,000 | | | VICI Properties, L.P. / VICI Note Company, Inc.(a) | | | | 3.5000 | | 02/15/25 | | | 789,304 | |

| | 1,705,000 | | | VICI Properties, L.P. / VICI Note Company, Inc.(a) | | | | 4.6250 | | 06/15/25 | | | 1,689,721 | |

| | | | | | | | | | | | | | 3,853,926 | |

| | | | | RETAIL - CONSUMER STAPLES — 0.8% | | | | | | | | | | |

| | 750,000 | | | Walgreens Boots Alliance, Inc. | | | | 3.8000 | | 11/18/24 | | | 746,694 | |

| | | | | | | | | | | | | | | |

| | | | | RETAIL - DISCRETIONARY — 1.5% | | | | | | | | | | |

| | 1,605,000 | | | Penske Automotive Group, Inc. | | | | 3.5000 | | 09/01/25 | | | 1,567,029 | |

| | | | | | | | | | | | | | | |

| | | | | SPECIALTY FINANCE — 3.3% | | | | | | | | | | |

| | 375,000 | | | AerCap Global Aviation Trust(a),(b) | | TSFR3M + 4.300% | | 6.5000 | | 06/15/45 | | | 374,822 | |

| | 500,000 | | | Ally Financial, Inc. | | | | 5.7500 | | 11/20/25 | | | 501,306 | |

| | 250,000 | | | Ally Financial, Inc. | | | | 6.0000 | | 07/15/29 | | | 248,425 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 54.6% (Continued) | | | | | | | | | | |

| | | | | SPECIALTY FINANCE — 3.3% (Continued) | | | | | | | | | | |

| | 550,000 | | | Aviation Capital Group, LLC(a) | | | | 5.5000 | | 12/15/24 | | $ | 549,234 | |

| | 650,000 | | | Aviation Capital Group, LLC(a) | | | | 4.8750 | | 10/01/25 | | | 644,981 | |

| | 500,000 | | | ILFC E-Capital Trust I(a),(b) | | TSFR3M + 1.812% | | 7.1590 | | 12/21/65 | | | 416,282 | |

| | 750,000 | | | Synchrony Financial | | | | 4.5000 | | 07/23/25 | | | 741,087 | |

| | | | | | | | | | | | | | 3,476,137 | |

| | | | | TRANSPORTATION & LOGISTICS — 1.8% | | | | | | | | | | |

| | 698,000 | | | Air Canada(a) | | | | 3.8750 | | 08/15/26 | | | 671,965 | |

| | 1,175,000 | | | Delta Air Lines, Inc. | | | | 2.9000 | | 10/28/24 | | | 1,166,877 | |

| | | | | | | | | | | | | | 1,838,842 | |

| | | | | TOTAL CORPORATE BONDS (Cost $56,982,632) | | | | | | | | | 56,887,615 | |

| | | | | | | | | | | | | | | |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | TERM LOANS — 11.7% | | | | | | | | | | |

| | | | | COMMERCIAL SUPPORT SERVICES — 0.8% | | | | | | | | | | |

| | 876,858 | | | Aramark Services, Inc.(b) | | TSFR1M + 2.000% | | 7.3440 | | 04/06/28 | | | 880,255 | |

| | | | | | | | | | | | | | | |

| | | | | LEISURE FACILITIES & SERVICES — 2.1% | | | | | | | | | | |

| | 997,500 | | | Caesars Entertainment, Inc.(b) | | TSFR3M + 2.750% | | 7.0940 | | 02/16/31 | | | 1,000,971 | |

| | 245,634 | | | Light & Wonder International, Inc.(b) | | TSFR1M + 2.350% | | 8.0790 | | 04/14/29 | | | 247,630 | |

| | 997,500 | | | Restaurant Brands(b) | | TSFR1M + 1.750% | | 7.0940 | | 09/20/30 | | | 994,657 | |

| | | | | | | | | | | | | | 2,252,258 | |

| | | | | RETAIL - DISCRETIONARY — 1.9% | | | | | | | | | | |

| | 1,962,322 | | | Great Outdoors Group, LLC(b) | | TSFR1M + 3.865% | | 9.2080 | | 03/05/28 | | | 1,962,322 | |

| | | | | | | | | | | | | | | |

| | | | | SEMICONDUCTORS — 1.1% | | | | | | | | | | |

| | 1,167,020 | | | MKS Instruments, Inc.(b) | | TSFR1M + 2.250% | | 7.5970 | | 08/17/29 | | | 1,173,222 | |

| | | | | | | | | | | | | | | |

| | | | | SOFTWARE — 1.1% | | | | | | | | | | |

| | 1,221,875 | | | Sunshine Software Merger Sub, Inc.(b) | | TSFR3M + 3.865% | | 9.2530 | | 10/15/28 | | | 1,149,076 | |

| | | | | | | | | | | | | | | |

| | | | | TRANSPORTATION & LOGISTICS — 4.7% | | | | | | | | | | |

| | 750,000 | | | AAdvantage Loyalty IP Ltd.(b) | | TSFR3M + 5.012% | | 8.0330 | | 04/20/28 | | | 776,858 | |

| | 1,995,000 | | | Air Canada(b) | | TSFR3M + 2.500% | | 7.8470 | | 03/21/31 | | | 2,004,047 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| SCHEDULE OF INVESTMENTS (Continued) |

| July 31, 2024 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | TERM LOANS — 11.7% (Continued) | | | | | | | | | | |

| | | | | TRANSPORTATION & LOGISTICS — 4.7% (Continued) | | | | | |

| | 1,995,000 | | | United Airlines, Inc.(b) | | TSFR1M + 2.750% | | 8.0330 | | 02/22/31 | | $ | 2,005,335 | |

| | | | | | | | | | | | | | 4,786,240 | |

| | | | | TOTAL TERM LOANS (Cost $12,222,505) | | | | 12,194,373 | |

| | | | | | | | | | | | | | | |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | | | (%) | | Maturity | | Fair Value | |

| | | | | U.S. GOVERNMENT & AGENCIES — 4.8% | | | | | | | | | | |

| | | | | U.S. TREASURY BILLS — 4.8% | | | | | | | | | | |

| | 5,000,000 | | | United States Treasury Bill(e) | | | | 5.2700 | | 09/26/24 | | | 4,959,182 | |

| | | | | | | | | | | | | | | |

| | | | | TOTAL U.S. GOVERNMENT & AGENCIES (Cost $4,959,783) | | | | 4,959,182 | |

| | | | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 98.0% (Cost $106,532,280) | | | $ | 102,046,761 | |

| | | | | OTHER ASSETS IN EXCESS OF LIABILITIES - 2.0% | | | | 2,070,723 | |

| | | | | NET ASSETS - 100.0% | | | $ | 104,117,484 | |

| | |

| CLO | - Collateralized Loan Obligations |

| | |

| LLC | - Limited Liability Company |

| | |

| L.P. | - Limited Partnership |

| | |

| Ltd. | - Limited Company |

| | |

| N.V. | - Naamioze Vennootschap |

| | |

| plc | - Public Limited Company |

| | |

| REMIC | - Real Estate Mortgage Investment Conduit |

| | |

| S.A. | - Société Anonyme |

| | |

| H15T1Y | US Treasury Yield Curve Rate T Note Constant Maturity 1 Year |

| | |

| H15T5Y | US Treasury Yield Curve Rate T Note Constant Maturity 5 Year |

| | |

| SOFR30A | United States 30 Day Average SOFR Secured Overnight Financing Rate |

| | |

| SOFRINDX | United States SOFR Secured Overnight Financing Index |

| | |

| SOFRRATE | United States SOFR Secured Overnight Financing Rate |

| | |

| TSFR1M | Term SOFR Secured Overnight Financing Rate 1 Month |

| | |

| TSFR3M | Term SOFR Secured Overnight Financing Rate 3 Month |

| (a) | Security exempt from registration under Rule 144A or Section 4(2) of the Securities Act of 1933. The security may be resold in transactions exempt from registration, normally to qualified institutional buyers. As of July 31, 2024 the total market value of 144A securities is $39,739,418 or 38.2% of net assets. |

| (b) | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| (c) | Step bond. Coupon rate is fixed rate that changes on a specified date. The rate shown is the current rate at July 31, 2024. |

| (d) | Interest only securities. |

| (e) | Zero coupon bond. Rate disclosed is the current yield as of July 31, 2024. |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| STATEMENT OF ASSETS AND LIABILITIES |

| July 31, 2024 |

| ASSETS | | | | |

| Investment securities: | | | | |

| At cost | | $ | 106,532,280 | |

| At fair value | | $ | 102,046,761 | |

| Cash | | | 1,323,025 | |

| Dividends and interest receivable | | | 920,256 | |

| Deposits for futures contracts | | | 320,660 | |

| TOTAL ASSETS | | | 104,610,702 | |

| | | | | |

| LIABILITIES | | | | |

| Payable for securities purchased | | | 340,076 | |

| Investment advisory fees payable | | | 71,299 | |

| Payable to related parties | | | 47,910 | |

| Accrued expenses and other liabilities | | | 33,933 | |

| TOTAL LIABILITIES | | | 493,218 | |

| NET ASSETS | | $ | 104,117,484 | |

| | | | | |

| Composition of Net Assets: | | | | |

| Paid in capital | | $ | 114,046,751 | |

| Accumulated losses | | | (9,929,267 | ) |

| NET ASSETS | | $ | 104,117,484 | |

| | | | | |

| Net Asset Value Per Share: | | | | |

| Net Assets | | $ | 104,117,484 | |

| Shares of beneficial interest outstanding (a) | | | 11,375,000 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | | $ | 9.15 | |

| (a) | Unlimited number of shares of beneficial interest authorized, no par value. |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| STATEMENT OF OPERATIONS |

| For the Year Ended July 31, 2024 |

| INVESTMENT INCOME | | | | |

| Interest | | $ | 7,594,550 | |

| Dividends | | | 32,396 | |

| TOTAL INVESTMENT INCOME | | | 7,626,946 | |

| | | | | |

| EXPENSES | | | | |

| Investment advisory fees | | | 794,563 | |

| Administration fees | | | 220,861 | |

| Audit fees | | | 33,580 | |

| Legal fees | | | 28,641 | |

| Trustees fees and expenses | | | 21,235 | |

| Printing and postage expenses | | | 18,828 | |

| Compliance officer fees | | | 17,791 | |

| Custodian fees | | | 16,719 | |

| Transfer agent fees | | | 12,034 | |

| Insurance expense | | | 8,040 | |

| Other expenses | | | 5,167 | |

| TOTAL EXPENSES | | | 1,177,459 | |

| | | | | |

| NET INVESTMENT INCOME | | | 6,449,487 | |

| | | | | |

| NET REALIZED AND UNREALIZED GAIN (LOSS) FROM INVESTMENTS | | | | |

| Net realized loss from investments | | | (1,003,176 | ) |

| Net change in unrealized appreciation on investments | | | 4,227,367 | |

| NET REALIZED AND UNREALIZED GAIN FROM INVESTMENTS | | | 3,224,191 | |

| | | | | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 9,673,678 | |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | For the | | | For the | |

| | | Year Ended | | | Year Ended | |

| | | July 31, 2024 | | | July 31, 2023 | |

| FROM OPERATIONS | | | | | | | | |

| Net investment income | | $ | 6,449,487 | | | $ | 5,793,854 | |

| Net realized loss from investments | | | (1,003,176 | ) | | | (1,042,763 | ) |

| Net realized gain from redemptions in-kind | | | — | | | | 63,438 | |

| Distributions of realized gains by underlying investment companies | | | — | | | | 271 | |

| Net change in unrealized appreciation on investments | | | 4,227,367 | | | | 459,564 | |

| Net increase in net assets resulting from operations | | | 9,673,678 | | | | 5,274,364 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Total distributions paid | | | (6,656,392 | ) | | | (5,707,888 | ) |

| Net decrease in net assets from distribution to shareholders | | | (6,656,392 | ) | | | (5,707,888 | ) |

| | | | | | | | | |

| FROM SHARES OF BENEFICIAL INTEREST | | | | | | | | |

| Proceeds from shares sold | | | 11,104,592 | | | | 14,342,119 | |

| Payments for shares redeemed | | | (26,782,626 | ) | | | (18,264,082 | ) |

| Net decrease in net assets from shares of beneficial interest | | | (15,678,034 | ) | | | (3,921,963 | ) |

| | | | | | | | | |

| TOTAL DECREASE IN NET ASSETS | | | (12,660,748 | ) | | | (4,355,487 | ) |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of the year | | | 116,778,232 | | | | 121,133,719 | |

| End of the year | | $ | 104,117,484 | | | $ | 116,778,232 | |

| | | | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Shares sold | | | 1,225,000 | | | | 1,625,000 | |

| Shares redeemed | | | (2,975,000 | ) | | | (2,075,000 | ) |

| Net decrease in shares of beneficial interest outstanding | | | (1,750,000 | ) | | | (450,000 | ) |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout the Years

| | | For the | | | For the | | | For the | | | For the | | | For the | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | July 31, 2024 | | | July 31, 2023 | | | July 31, 2022 | | | July 31, 2021 | | | July 31, 2020 | |

| Net asset value, beginning of year | | $ | 8.90 | | | $ | 8.92 | | | $ | 9.69 | | | $ | 9.86 | | | $ | 9.84 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (a) | | | 0.55 | | | | 0.44 | | | | 0.22 | | | | 0.13 | | | | 0.12 | |

| Net realized and unrealized gain (loss) on investments | | | 0.27 | | | | (0.03 | ) | | | (0.80 | ) | | | (0.16 | ) | | | 0.01 | |

| Total from investment operations | | | 0.82 | | | | 0.41 | | | | (0.58 | ) | | | (0.03 | ) | | | 0.13 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.57 | ) | | | (0.43 | ) | | | (0.19 | ) | | | (0.14 | ) | | | (0.11 | ) |

| Total distributions | | | (0.57 | ) | | | (0.43 | ) | | | (0.19 | ) | | | (0.14 | ) | | | (0.11 | ) |

| Net asset value, end of year | | $ | 9.15 | | | $ | 8.90 | | | $ | 8.92 | | | $ | 9.69 | | | $ | 9.86 | |

| Market price, end of year | | $ | 9.16 | | | $ | 8.87 | | | $ | 8.90 | | | $ | 9.70 | | | $ | 9.86 | |

| Total return (b)(c) | | | 9.49 | % | | | 4.83 | % | | | (5.73 | )% | | | (0.32 | )% | | | 1.88 | % |

| Market price total return | | | 10.00 | % | | | 4.72 | % | | | (6.03 | )% | | | (0.22 | )% | | | 1.47 | % |

| Net assets, at end of year (000)s | | $ | 104,117 | | | $ | 116,778 | | | $ | 121,134 | | | $ | 129,179 | | | $ | 121,756 | |

| Ratio of gross expenses to average net assets (d)(e) | | | 1.11 | % | | | 1.06 | % | | | 0.98 | % | | | 1.00 | % | | | 1.23 | % |

| Ratio of net expenses to average net assets (e)(f) | | | 1.11 | % | | | 1.06 | % | | | 0.98 | % | | | 1.00 | % | | | 1.21 | % |

| Ratio of net investment income to average net assets (g) | | | 6.09 | % | | | 4.98 | % | | | 2.37 | % | | | 1.35 | % | | | 1.21 | % |

| Portfolio Turnover Rate (h) | | | 49 | % | | | 31 | % | | | 53 | % | | | 135 | % | | | 227 | % |

| | | | | | | | | | | | | | | | | | | | | |

| (a) | Per share amounts calculated using the average shares method, which more appropriately represents the per share data for the period. |

| (b) | Total return is calculated assuming a purchase of shares at net asset value on the first day and a sale at net asset value on the last day of the period. Distributions are assumed, for the purpose of this calculation, to be reinvested at the ex-dividend date net asset value per share on their respective payment dates. Total return would have been lower absent fee waiver/expense reimbursement. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States and, consequently, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (d) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Adviser. |

| (e) | Does not include the expenses of other investment companies in which the Fund invests. |

| (f) | Represents the ratio of expenses to average net assets inclusive of fee waivers and/or expense reimbursements by the Adviser. |

| (g) | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

| (h) | Portfolio turnover rate excludes securities received or delivered from in-kind transactions. |

See accompanying notes to financial statements.

| Anfield Universal Fixed Income ETF |

| NOTES TO FINANCIAL STATEMENTS |

| July 31, 2024 |

The Anfield Universal Fixed Income ETF (the “Fund”) is a series of shares of beneficial interest of the Two Roads Shared Trust (the “Trust”), a statutory trust organized under the laws of the State of Delaware on June 8, 2012, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a diversified, open-end management investment company. The Fund commenced operations on September 17, 2018. The Fund’s investment objective is to seek current income. The Fund is an actively managed ETF that normally invests at least 80% of its net assets, including any borrowings for investment purposes, in a diversified portfolio of fixed income instruments.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board’s (“FASB”) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies”.

Security Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price (“NOCP”). In the absence of a sale such securities shall be valued at the mean between the last bid and ask prices on the day of valuation. Debt securities (other than short-term obligations) are valued each day by an independent pricing service approved by the Board of Trustees (the “Board”) using methods which include current market quotations from a major market maker in the securities and based on methods which include the consideration of yields or prices of securities of comparable quality, coupon, maturity and type. Futures and future options are valued at the final settled price or, in the absence of a settled price, at the last sale price on the day of valuation. The independent pricing service does not distinguish between smaller-sized bond positions known as “odd lots” and larger institutional-sized bond positions known as “round lots”. The Fund may fair value a particular bond if the adviser does not believe that the round lot value provided by the independent pricing service reflects fair value of the Fund’s holding. Short-term debt obligations having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost.

The Fund may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities are valued using the “fair value” procedures approved by the Trustees of the Trust (the “Board”). The Board has appointed the Adviser as its valuation designee (the “Valuation Designee”) for all fair value determinations and responsibilities, other than overseeing pricing service providers used by the Trust. This designation is subject to Board oversight and certain reporting and other requirements designed to facilitate the Board’s ability to effectively oversee the designee’s fair value determinations. The Board may also enlist third party consultants such as a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist the Valuation Designee in determining a security-specific fair value. The Board is responsible for reviewing and approving fair value methodologies utilized by the Valuation Designee, approval of which shall be based upon whether the Valuation Designee followed the valuation procedures approved by the Board.

Exchange Traded Funds (“ETFs”) – The Fund may invest in ETFs. ETFs are a type of index fund bought and sold on a securities exchange. An ETF trades like common stock and represents a fixed portfolio of securities designed to track the performance and dividend yield of a particular domestic or foreign market index. The Fund may purchase an ETF to temporarily gain exposure to a portion of the U.S. or a foreign market. The risks of owning an ETF generally reflect the risks of owning the underlying securities they are designed to track, although the lack of liquidity on an ETF could result in it being more volatile. Additionally, ETFs have fees and expenses that reduce their value.

| Anfield Universal Fixed Income ETF |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| July 31, 2024 |

Futures Contracts – The Fund may purchase or sell futures contracts to gain exposure to, or hedge against, changes in the value of equities, interest rates, foreign currencies, or commodities. Initial margin deposits required upon entering into futures contracts are satisfied by the segregation of specific securities or cash as collateral for the account of the broker (the Fund’s agent in acquiring the futures position). During the period the futures contracts are open, changes in the value of the contracts are recognized as unrealized gains or losses by “marking to market” on a daily basis to reflect the market value of the contracts at the end of each day’s trading. Variation margin payments are received or made depending upon whether unrealized gains or losses are incurred. When the contracts are closed, the Fund recognizes a realized gain or loss equal to the difference between the proceeds from, or cost of, the closing transaction and the Fund’s basis in the contract. If the Fund was unable to liquidate a futures contract and/or enter into an offsetting closing transaction, the Fund would continue to be subject to market risk with respect to the value of the contracts and continue to be required to maintain the margin deposits on the futures contracts. Risks may exceed amounts recognized in the consolidated statement of assets and liabilities. With futures, there is minimal counterparty credit risk to the Fund since futures are exchange traded and the exchange’s clearinghouse, as counterparty to all exchange traded futures, guarantees the futures against default. The fund did not hold any futures contracts during the fiscal year.

Option Transactions – The Fund is subject to equity price risk in the normal course of pursuing its investment objective and may purchase or sell options to help hedge against risk. When the Fund writes a call option, an amount equal to the premium received is included in the statement of assets and liabilities as a liability. The amount of the liability is subsequently marked-to-market to reflect the current market value of the option. If an option expires on its stipulated expiration date or if the Fund enters into a closing purchase transaction, a gain or loss is realized. If a written call option is exercised, a gain or loss is realized for the sale of the underlying security and the proceeds from the sale are increased by the premium originally received. As writer of an option, the Fund has no control over whether the option will be exercised and, as a result, retains the market risk of an unfavorable change in the price of the security underlying the written option.

The Fund may purchase put and call options. Put options are purchased to hedge against a decline in the value of securities held in the Fund’s portfolio. If such a decline occurs, the put options will permit the Fund to sell the securities underlying such options at the exercise price, or to close out the options at a profit. The premium paid for a put or call option plus any transaction costs will reduce the benefit, if any, realized by the Fund upon exercise of the option, and, unless the price of the underlying security rises or declines sufficiently, the option may expire worthless to the Fund. In addition, in the event that the price of the security in connection with which an option was purchased moves in a direction favorable to the Fund, the benefits realized by the Fund as a result of such favorable movement will be reduced by the amount of the premium paid for the option and related transaction costs. Written and purchased options are non-income producing securities. With purchased options, there is minimal counterparty risk to the Fund since these options are exchange traded and the exchange’s clearinghouse, as counterparty to all exchange traded options, guarantees against a possible default.

Valuation of Underlying Funds – The Fund may invest in portfolios of open-end or closed-end investment companies (the “Underlying Funds”). The Underlying Funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value according to the methods approved by the board of directors of the Underlying Funds.

Open-ended funds are valued at their respective net asset values as reported by such investment companies. The shares of many closed-end investment companies, after their initial public offering, frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurances that the market discount or market premium on shares of any closed-end investment company purchased by the Fund will not change.

| Anfield Universal Fixed Income ETF |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| July 31, 2024 |

Fair Valuation Process – The applicable investments are valued by the Valuation Designee pursuant to valuation procedures established by the Board. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source); (ii) securities for which, in the judgment of the Valuation Designee, the prices or values available do not represent the fair value of the instrument; factors which may cause the Valuation Designee to make such a judgment include, but are not limited to, the following: only a bid price or an asked price is available; the spread between bid and asked prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; and (iv) securities with respect to which an event that affects the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to the Fund’s calculation of its net asset value. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If a current bid from such independent dealers or other independent parties is unavailable, the Valuation Designee shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Fund’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Fund utilizes various methods to measure the fair value of all of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

| Anfield Universal Fixed Income ETF |