Exhibit (d)

This description of FMS-WM and the Federal Republic is dated June 30, 2017 and appears as Exhibit (d) to the Annual Report on Form 18-K of FMS-WM for the fiscal year ended December 31, 2016.

TABLE OF CONTENTS

i

ii

THIS DOCUMENT (OTHERWISE THAN AS PART OF A PROSPECTUS CONTAINED IN A REGISTRATION STATEMENT FILED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED) DOES NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY SECURITIES OF FMS-WM. THE DELIVERY OF THIS DOCUMENT AT ANY TIME DOES NOT IMPLY THAT THE INFORMATION HEREIN IS CORRECT AS OF ANY TIME SUBSEQUENT TO ITS DATE.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this description, references to “€,” “euro” or “EUR” are to the single European currency of the member states of the European Union participating in the euro and references to “U.S. dollars,” “$” or “USD” are to United States dollars. See “Exchange Rate Information” below for information regarding the rates of conversion of the euro into United States dollars and “The Federal Republic of Germany—General—The European Union and European Integration” for a discussion of the introduction of the euro.

FMS-WM’s accounts are kept, and the economic data on the Federal Republic is expressed, in euro.

Any discrepancies in the tables included in this prospectus between the amounts and the totals thereof are due to rounding.

In this document, references to the “Federal Republic” and “Germany” are to the Federal Republic of Germany and references to the “Federal Government” are to the government of the Federal Republic of Germany. The term “FMS-WM” refers to FMS Wertmanagement.

EXCHANGE RATE INFORMATION

FMS-WM files reports with the Securities and Exchange Commission giving financial and economic data expressed in euro.

The following table shows noon buying rates for euro, expressed as U.S. dollars per EUR 1.00, for the periods and dates indicated, as published on a weekly basis by the Federal Reserve Bank of New York.

| | | | | | | | | | | | | | | | |

Year ended December 31, | | Period End | | | Average(1) | | | High | | | Low | |

2012 | | | 1.3186 | | | | 1.2909 | | | | 1.3463 | | | | 1.2062 | |

2013 | | | 1.3779 | | | | 1.3303 | | | | 1.3816 | | | | 1.2774 | |

2014 | | | 1.2101 | | | | 1.3210 | | | | 1.3927 | | | | 1.2101 | |

2015 | | | 1.0859 | | | | 1.1032 | | | | 1.2015 | | | | 1.0524 | |

2016 | | | 1.0552 | | | | 1.1028 | | | | 1.1516 | | | | 1.0375 | |

| (1) | The average of the noon buying rates on the last business day of each month during the relevant period. |

The following table shows the high and low noon buying rates for euro, expressed as U.S. dollars per EUR 1.00, for each month from December 2017 through June 23, 2017, as reported by the Federal Reserve Bank of New York.

| | | | | | | | |

2016 | | High | | | Low | |

December | | | 1.0758 | | | | 1.0375 | |

2017 | | | | | | |

January | | | 1.0794 | | | | 1.0416 | |

February | | | 1.0802 | | | | 1.0551 | |

March | | | 1.0882 | | | | 1.0514 | |

April | | | 1.0941 | | | | 1.0606 | |

May | | | 1.1236 | | | | 1.0869 | |

June (through June 23) | | | 1.1277 | | | | 1.1124 | |

No representation is made that the euro or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or euro, as the case may be, at any particular rate.

There are, except in limited embargo circumstances, no legal restrictions in the Federal Republic on international capital movements and foreign exchange transactions. However, for statistical purposes only, every individual or corporation residing in the Federal Republic must report to the Deutsche Bundesbank, the German Central Bank, subject to a number of exceptions, any payment received from or made to an individual or a corporation resident outside of the Federal Republic if such payment exceeds EUR 12,500 (or the equivalent in a foreign currency).

1

RECENT DEVELOPMENTS

THE FEDERAL REPUBLIC OF GERMANY

Overview of Key Economic Figures

The following economic information regarding the Federal Republic is derived from the public official documents cited below. Certain of the information is preliminary.

Gross Domestic Product (GDP)

GROSS DOMESTIC PRODUCT

| | | | |

| (adjusted for price, seasonal and calendar effects)(1) |

| | |

Reference period | | Percentage change on previous quarter | | Percentage change on the same quarter in previous year |

1st quarter 2016 | | 0.7 | | 1.9 |

2nd quarter 2016 | | 0.5 | | 1.8 |

3rd quarter 2016 | | 0.2 | | 1.7 |

4th quarter 2016 | | 0.4 | | 1.8 |

1st quarter 2017 | | 0.6 | | 1.7 |

| (1) | Adjustment for seasonal and calendar effects according to the Census X-12-ARIMA method. |

Germany’s gross domestic product (“GDP”) continued to grow, increasing by 0.6% after price, seasonal and calendar adjustments in the first quarter of 2017 compared to the fourth quarter of 2016. When adjusted for price, seasonal and calendar variations, positive contributions in the first quarter of 2017 came both from domestic and foreign demand. Capital formation increased substantially. Due to the mild weather, fixed capital formation especially in construction, but also in machinery and equipment, was markedly up compared to the fourth quarter of 2016. Households and general government increased their final consumption expenditure slightly at the beginning of the year. In addition, the development of foreign trade was more dynamic and contributed to growth as exports increased more than imports.

In a year-on-year comparison, in price and calendar-adjusted terms, the German economy grew by 1.7% compared to the corresponding period in 2016, largely consistent with an increase of 1.8% in the fourth quarter of 2016 and of 1.7% in the third quarter of 2016.

Source: Statistisches Bundesamt, Gross domestic product up 0.6% in the 1st quarter of 2017, press release of May 12, 2017 (https://www.destatis.de/EN/PressServices/Press/pr/2017/05/PE17_155_811.html).

2

Inflation Rate

INFLATION RATE

| | | | |

| (based on overall consumer price index) |

| | |

Reference period | | Percentage change on previous month | | Percentage change on the same month in previous year |

June 2016 | | 0.1 | | 0.3 |

July 2016 | | 0.3 | | 0.4 |

August 2016 | | 0.0 | | 0.4 |

September 2016 | | 0.1 | | 0.7 |

October 2016 | | 0.2 | | 0.8 |

November 2016 | | 0.1 | | 0.8 |

December 2016 | | 0.7 | | 1.7 |

January 2017 | | -0.6 | | 1.9 |

February 2017 | | 0.6 | | 2.2 |

March 2017 | | 0.2 | | 1.6 |

April 2017 | | 0.0 | | 2.0 |

May 2017 | | -0.2 | | 1.5 |

In May 2017, consumer prices in Germany rose by 1.5% compared to May 2016. The inflation rate as measured by the consumer price index thus decreased, following an increase in the previous month (April 2017: +2.0%; March 2017: +1.6%). Compared with April 2017, the consumer price index fell by 0.2% in May 2017.

As opposed to preceding months, the impact of the energy price development on the inflation rate diminished markedly. Energy prices were up 2.0% in May 2017 compared with May 2016 (April and March 2017: +5.1% each), with mineral oil products, in particular, being more expensive than a year earlier (+5.8%, of which heating oil: +11.7%; motor fuels: +4.4%). The year-on-year rates of energy price increases showed diverging trends for the other energy products. Electricity prices, for example, were up by 1.2%, while gas prices were down by 3.4%. Excluding the prices of all types of energy, the inflation rate in May 2017 would have been +1.4% compared to May 2016.

Food prices in May 2017 rose by 2.4% as compared to May 2016. The year-on-year rise in food prices thus accelerated (April 2017: +1.8%). Prices of goods (total) rose by 1.8% in May 2017 compared to May 2016. Prices of services (total) rose more moderately (+1.2%) in May 2017 compared to May 2016. The rise in net rents exclusive of heating expenses (+1.8% on May 2016) had a major impact as households spend a large part of their consumption expenditure on this item. In addition, price increases were observed, for example, for maintenance and repair of vehicles (+3.3%) and catering services (+1.9%).

Compared to April 2017, the consumer price index fell by 0.2% in May 2017. In particular, the prices of energy decreased by 1.4% in May 2017compared to April 2017, mainly due to decreases in the prices of heating oil (–6.5%) and (–2.6%, including supergrade petrol: –2.3%, diesel fuel: –3.0%). Slight month-on-month price decreases were also observed, for example, for clothing (–0.6%) and footwear (–0.4%). Food prices remained unchanged on the previous month.

Source: Statistisches Bundesamt, Consumer prices in May 2017: +1.5% on May 2016, press release of June 14, 2017

(https://www.destatis.de/EN/PressServices/Press/pr/2017/06/PE17_198_611.html).

3

Unemployment Rate

UNEMPLOYMENT RATE

| | | | |

(percent of unemployed persons in the total labor force according to the International Labour Organization (ILO) definition)(1) |

| | |

Reference period | | Original percentages | | Adjusted percentages(2) |

May 2016 | | 4.2 | | 4.2 |

June 2016 | | 4.2 | | 4.2 |

July 2016 | | 4.3 | | 4.2 |

August 2016 | | 4.1 | | 4.1 |

September 2016 | | 3.8 | | 4.1 |

October 2016 | | 3.9 | | 4.0 |

November 2016 | | 3.9 | | 3.9 |

December 2016 | | 3.5 | | 3.9 |

January 2017 | | 4.0 | | 3.9 |

February 2017 | | 4.3 | | 3.9 |

March 2017 | | 4.0 | | 3.9 |

April 2017 | | 4.2 | | 3.9 |

| (1) | The time series on unemployment are based on the German Labour Force Survey. |

| (2) | Adjusted for seasonal and irregular effects (trend cycle component) using the X-12-ARIMA method. |

The number of employed persons increased by approximately 655,000 persons, or 1.5%, from April 2016 to April 2017. Compared to March 2017, the number of employed persons in April 2017 increased by approximately 31,000, or 0.1%, after adjustment for seasonal fluctuations.

In April 2017, the number of unemployed persons increased by approximately 6,000 compared to April 2016. Adjusted for seasonal and irregular effects (trend cycle component), the number of unemployed persons in April 2017 remained almost unchanged at 1.69 million compared to March 2017.

Sources: Statistisches Bundesamt, April 2017: employment up 1.5% on a year earlier, press release of May 31, 2017 (https://www.destatis.de/EN/PressServices/Press/pr/2017/05/PE17_178_132.html); Statistisches Bundesamt, Genesis-Online Datenbank, Result 13231-0001, Unemployed persons, persons in employment, economically active population, unemployment rate: Germany, months, original and adjusted data (https://www-genesis.destatis.de/genesis/online/logon?sequenz=tabelleErgebnis&selectionname=13231-0001&zeitscheiben=2&leerzeilen=false).

Current Account and Foreign Trade

CURRENT ACCOUNT AND FOREIGN TRADE

| | | | |

| | | (balance in EUR billion)(1) |

Item | | January to April 2017 | | January to April 2016 |

Trade in goods, including supplementary trade items | | 87.8 | | 92.1 |

Services | | -4.6 | | -4.3 |

Primary income | | 19.9 | | 19.7 |

Secondary income | | -22.2 | | -15.1 |

| | | | |

Current account | | 80.9 | | 92.4 |

| | | | |

| (1) | Figures may not add up due to rounding. |

Source: Statistisches Bundesamt, German exports in April 2017: –2.9% on April 2016, press release of June 9, 2017

(https://www.destatis.de/EN/PressServices/Press/pr/2017/06/PE17_186_51.html).

4

FMS WERTMANAGEMENT

GENERAL

Overview

FMS-WM is a wind-up institution (Abwicklungsanstalt) organized as a public law entity (Anstalt öffentlichen Rechts) under public law of the Federal Republic with partial legal capacity pursuant to Section 8a para 1 of the German Financial Market Stabilization Fund Act (Finanzmarktstabilisierungsfondsgesetz, “FMStFG”). Partial legal capacity, under German administrative law, means that FMS-WM does not have the right to bring an administrative proceeding against the German Federal Agency for Financial Market Stabilization (Bundesanstalt für Finanzmarktstabilisierung, “FMSA”) under its charter. FMS-WM has, however, full power and legal capacity to contract with third parties and sue and be sued in court. FMS-WM is wholly owned by the German Financial Market Stabilization Fund (Finanzmarktstabilisierungsfonds), a special pool of assets (Sondervermögen) of the Federal Republic, which is abbreviated as “FMS” in German and referred to as “SoFFin” in this document. FMS-WM is charged with liquidating a portfolio of risk positions and non-strategic assets/businesses in an original amount of EUR 175.7 billion (nominal volume) that it assumed from Hypo Real Estate Holding AG and its subsidiaries and special purpose entities (referred to herein collectively as the “HRE Group”) on October 1, 2010. As of 2007, the HRE Group was one of the largest commercial property lenders, issuers of covered bonds and providers of public finance in Germany. It encountered severe financial difficulties in 2008/09 in the course of the global financial markets crisis. Given the systemic importance of the HRE Group and the resulting public interest in stabilizing the HRE Group, the Federal Republic initiated support measures for this financial institution, including the transfer of risk positions and non-strategic assets/businesses to FMS-WM.

FMS-WM pursues its objective of managing and unwinding its portfolio according to a strategic management framework known as the “winding-up plan” (Abwicklungsplan), which is updated and adapted on a regular basis. FMS-WM aims to maximize the value of its portfolio by managing and liquidating it in a value-preserving manner over an extended period of time. For any given part of the portfolio, the plan requires an assessment of whether FMS-WM should sell, hold, or restructure its holdings. As of December 31, 2016, FMS-WM had liquidated approximately EUR 92.7 billion (including the wind-down of the portfolio extension due to the acquisition of Depfa assets in November 2016, the “Portfolio Extension”) of its initial portfolio of EUR 175.7 billion. For additional information on the Portfolio Extension, see “Business and Operations—The Portfolio.”

FMS-WM engages in funding activities, including the issuance of debt securities and/or obtaining financing from financial institutions, in order to refinance funding instruments associated with the portfolio it has assumed as they expire. FMS-WM will have to engage in refinancing activities on the capital markets until its portfolio has been liquidated. As of December 31, 2016, FMS-WM had subscribed capital of EUR 200,000, the total amount of which had been paid in.

FMS-WM’s obligations are backed by the full faith and credit of the Federal Republic. Pursuant to the FMStFG, FMS-WM’s obligations benefit from a statutory guarantee of SoFFin and under FMS-WM’s charter, SoFFin is obligated to cover all losses sustained by FMS-WM and to ensure that FMS-WM is able to pay all its liabilities at any time when due and in full. According to Section 5 of the FMStFG, the Federal Republic, in turn, is directly liable for all of SoFFin’s obligations.

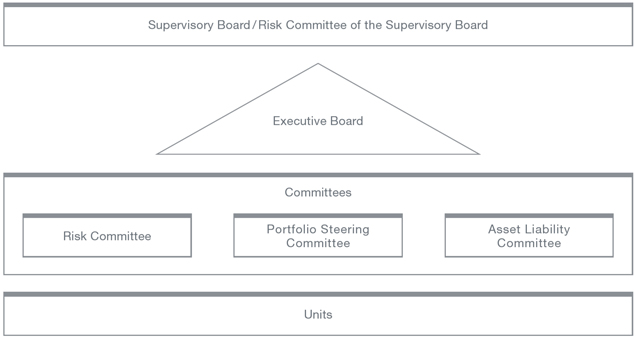

FMS-WM is governed by two corporate bodies: the Supervisory Board (Verwaltungsrat) and the Executive Board (Vorstand). The six-member Supervisory Board is appointed by SoFFin and is responsible for the composition and oversight of the Executive Board as well as for major strategic decisions of FMS-WM. The Executive Board has a minimum of two members (currently three) and is appointed by the Supervisory Board. It is responsible for representing FMS-WM externally and for managing its business.

FMS-WM is registered with the commercial register (Handelsregister) of the local court (Amtsgericht) of Munich under HRA 96076. Its registered office and business address is at Prinzregentenstrasse 56, 80538 Munich, Federal Republic of Germany. Its telephone number is +49 89 9547627-0. FMS-WM maintains a branch in Rome, Italy. The Italian branch was registered with the company register (Registro delle Imprese) of Rome on May 7, 2013 under registration number 12372371000. As of the date hereof, the registered status of the Italian branch is inactive. As of the date hereof, FMS-WM does not intend to open any additional branches.

Creation and Legal Status

FMS-WM’s creation and legal status are a direct result of the German Federal Government’s response to the global financial markets crisis. In October 2008, the German Federal Government enacted a comprehensive package of measures to support key German strategic financial institutions, most notably the HRE Group. This comprehensive package included the FMStFG, which provided for the implementation of SoFFin and established FMSA, a federal agency under public law with legal personality (rechtsfähige Anstalt öffentlichen Rechts) supervised by the German Federal Ministry of Finance (Bundesfinanzministerium).

5

Section 8a of the FMStFG grants FMSA the power to create wind-up institutions. The purpose of these institutions is to assume distressed and non-strategic assets from systemically important financial institutions and to eventually dispose of or liquidate the risk positions transferred to them.

As of 2007, the HRE Group was one of the largest commercial property lenders and providers of public finance in Germany. Most of the commercial property loans were refinanced by the issuance of covered bonds, making the HRE Group the leading German issuer of covered bonds. In the course of the liquidity crisis in September 2008, the HRE Group encountered financial difficulties primarily caused by the heavy debt burden held by one of its subsidiaries, Depfa Bank plc (“Depfa”). Depfa had borrowed short-term money to fund higher interest-bearing long-term positions in public sector finance on a large scale. When the interbank lending market collapsed in September 2008, Depfa faced substantial refinancing problems. Within a short period of time, the entire HRE Group faced solvency issues as well. Due to the HRE Group’s importance for the German financial system, the Federal Republic initiated various support measures, which led to SoFFin becoming the sole owner of the HRE Group in October 2009. The government support measures also included the extension of liquidity guarantees by SoFFin and the creation of FMS-WM as a wind-up institution under Section 8a of the FMStFG on July 8, 2010. Risk positions and non-strategic assets/businesses of the HRE Group were then transferred to FMS-WM on October 1, 2010.

FMS-WM is a public law institution with partial legal capacity (teilrechtsfähige Anstalt des öffentlichen Rechts) created pursuant to German administrative law. It is wholly owned by SoFFin and is subject to the supervision and control of FMSA. FMS-WM may act in its own name, and may be subject to court proceedings. In order to achieve its mandate of unwinding the portfolio of risk positions and non-strategic assets/businesses assumed from the HRE Group, FMS-WM may engage in all kinds of banking and financial services transactions and all other transactions that directly or indirectly serve its purposes. FMS-WM is, however, neither a financial institution nor a financial services institution within the meaning of the German Banking Act (Kreditwesengesetz, “KWG”), nor a financial service provider within the meaning of the German Securities Trading Act (Wertpapierhandelsgesetz, “WpHG”), nor an insurance company within the meaning of the German Insurance Supervision Act (Versicherungsaufsichtsgesetz, “VAG”) nor regulated as such. As a consequence, FMS-WM is prohibited from engaging in transactions that would require a license under the European Union Banking Directive (2006/48/EC) or the European Union Directive on markets for financial instruments (2004/39/EC). Nonetheless, pursuant to its charter and the FMStFG, FMS-WM is subject to certain provisions of the KWG and the WpHG. In particular, FMS-WM is subject to banking supervision by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht) and must comply with the organizational obligations and restrictions on certain activities imposed by the KWG applicable to banks and financial institutions. FMS-WM is, however, exempted from the regulatory capital and liquidity requirements and the licensing requirements under the KWG. FMS-WM is also deemed to be a financial institution for purposes of the German Money Laundering Act (Geldwäschegesetz), and is therefore subject to the provisions thereof.

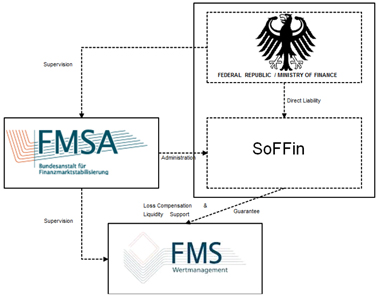

Relationship with the Federal Republic of Germany

The following chart provides an overview of the current relationship between FMS-WM and the Federal Republic:

6

For information on certain changes to the supervision of FMSA and the administration of SoFFin as a result of a pending reorganization of FMSA, see “—Reorganization of FMSA” below.

Relationship with SoFFin

SoFFin

FMS-WM is wholly owned by SoFFin, which is established by law and designated to fulfill specific tasks of the German Federal Government assigned to it under the FMStFG. SoFFin is currently administered by FMSA and, following the pending reorganization of FMSA, is expected to be administered and managed by Federal Republic of Germany – Finance Agency (Bundesrepublik Deutschland – Finanzagentur GmbH) (see “—Reorganization of FMSA”). SoFFin is a special pool of assets (Sondervermögen) of the Federal Republic. The term special pool of assets (Sondervermögen) designates legally dependent assets of the Federal Republic. Accordingly, the FMStFG provides that SoFFin shall have no legal capacity, although in legal relations SoFFin may act, sue and be sued in its own name. There shall be no attachment of, or other measures of compulsory execution against, SoFFin. Any debt incurred by SoFFin is accounted for as direct debt of the Federal Republic. In addition, Section 5 of the FMStFG provides that the Federal Republic is directly liable for the obligations of SoFFin. SoFFin’s obligations are thus effectively obligations of the Federal Republic.

SoFFin’s purpose is to stabilize the German financial sector by extending liquidity guarantees, providing equity capital, assuming risk positions, and setting up wind-up institutions. To this end, SoFFin has been authorized by the German legislature under Section 6 of the FMStFG to extend liquidity guarantees in a total aggregate amount of up to EUR 400 billion. In addition, Section 9 of the FMStFG authorizes the German Federal Ministry of Finance to incur debt in a total aggregate amount of up to EUR 80 billion to cover the cost of measures taken by SoFFin in connection with the provision of equity capital, the assumption of risk positions and the compensation of losses of wind-up institutions. Specifically, the authorization permits the German Federal Ministry of Finance to incur debt up to an amount of EUR 40 billion. Subject to the approval of the parliamentary control panel for financial market stabilization which is comprised of nine members of the budget committee of the German Bundestag, this amount can be increased by up to another EUR 30 billion and, subject to the approval of the budget committee of the German Bundestag, by up to another EUR 10 billion. Any financing required by SoFFin is obtained in the manner used by the Federal Republic to finance itself, i.e., through the issuance of debt instruments by the Federal Republic of Germany – Finance Agency (Bundesrepublik Deutschland – Finanzagentur GmbH). When the Federal Republic incurs debt for SoFFin it results in an increase in the net borrowings and debt of the Federal Republic. Applications for stabilization measures extended by SoFFin could initially be made only until the end of 2010. As a consequence of developments in the euro area, however, the German Federal Government subsequently re-opened the application period, which finally expired at the end of 2015. The timing of the expiration of SoFFin’s mandate to accept new applications for support measures coincided with the assumption by the European Single Resolution Board at the beginning of 2016 of responsibility for resolving and restructuring non-viable systemically important banks.

Guarantee

With effect from January 1, 2014, Section 8a of the FMStFG, which deals with the establishment of wind-up institutions, was amended to provide that SoFFin guarantees all existing and future obligations of FMS-WM with respect to moneys, debt securities and derivative transactions as well as obligations of third parties that are expressly guaranteed by FMS-WM, which FMS-WM has borrowed, issued, entered into or incurred or which have been transferred to FMS-WM during the time period for which SoFFin is the sole obligor of the loss compensation obligation (alleiniger Verlustausgleichspflichtiger). For a description of SoFFin’s loss compensation obligation, see “—Loss Compensation and Liquidity Support Obligations” below. Accordingly, under the guarantee, if FMS-WM fails to make any payment of principal or interest or any other amount required to be paid with respect to securities issued by it when that payment is due and payable, SoFFin will be liable for that payment as and when it becomes due and payable, provided that the security was issued during the time period for which SoFFin was the sole obligor of the loss compensation obligation. SoFFin’s obligation under the guarantee ranks equally, without any preference, with all of its other present and future unsecured and unsubordinated indebtedness. Holders of securities issued by FMS-WM may enforce this obligation directly against SoFFin without first having to take legal action against FMS-WM. If SoFFin fails to make any payment of principal or interest or any other amount required to be paid with respect to securities issued by FMS-WM when that payment is due and payable under the guarantee, the Federal Republic will be liable for that payment as and when it becomes due and payable pursuant to Section 5 of the FMStFG, as described above. The guarantee and the Federal Republic’s direct liability for SoFFin’s obligations pursuant to Section 5 of the FMStFG are strictly a matter of statutory law and are not evidenced by any contract or instrument. Potential claims based on the guarantee and on Section 5 of the FMStFG may be subject to defenses available to FMS-WM and SoFFin with respect to the obligations covered.

7

Loss Compensation and Liquidity Support Obligations

Under FMS-WM’s charter, which was enacted pursuant to Section 8a of the FMStFG, SoFFin is obligated to cover all losses sustained by FMS-WM and to ensure that FMS-WM is able to pay all its liabilities at all times when due and in full. As described above, pursuant to Section 5 of the FMStFG, the Federal Republic is directly liable for SoFFin’s obligations. Accordingly, SoFFin’s loss compensation and liquidity support obligations enable FMS-WM to pursue its operations and effectively mean that FMS-WM’s obligations, including the obligations to holders of debt securities issued by FMS-WM, are backed by the full faith and credit of the Federal Republic.

For the year ended December 31, 2016, SoFFin recorded a profit of EUR 98.6 million (2015: loss of EUR 684.8 million), largely due to other operating income of EUR 1,021.0 recorded as a result the reversal of provisions for the loss compensation obligation for FMS-WM. As of December 31, 2016, the total outstanding stabilization measures provided by SoFFin amounted to EUR 14.6 billion, which related entirely to equity capital (as of December 31, 2015: EUR 15.8 billion).

Relationship with FMSA

FMS-WM operates under the supervision and control of the Federal Republic, which is exercised through FMSA. FMSA was established to manage SoFFin and to implement and monitor the stabilization measures extended by SoFFin. FMSA has the power to create wind-up institutions under Section 8a of FMStFG. FMSA is supervised by the German Federal Ministry of Finance (Bundesfinanzministerium), which ensures that FMSA acts in the public interest. In particular, the German Federal Ministry of Finance supervises FMSA’s activities and nominates the members of FMSA’s management committee (Leitungsausschuss). Certain decision-making powers have been delegated to the management committee by the FMStFG.

FMSA appoints the members of FMS-WM’s Supervisory Board. The Supervisory Board members, in turn, appoint the members of FMS-WM’s Executive Board. Both the Supervisory Board and FMSA may dismiss a member of the Executive Board for good cause.

FMSA is responsible for the legal supervision of FMS-WM. In particular, FMSA has to approve and supervise FMS-WM’s implementation of the winding-up plan as well as any deviations from, or amendments to, the winding-up plan. FMSA may give instructions to FMS-WM’s Executive Board and Supervisory Board in order to ensure that FMS-WM complies with applicable law and the requirements of its charter. Comprehensive reporting obligations by FMS-WM ensure that FMSA has a solid basis for exercising its control and instruction rights.

In keeping with its supervisory role, FMSA action is required for the dissolution of FMS-WM. While there is no set maximum duration for FMS-WM’s existence, FMS-WM’s charter provides that FMS-WM shall exist only until the transferred risk positions and non-strategic assets/businesses have been liquidated in full, at which point it is obligated to notify FMSA. FMSA may initiate the final dissolution process for FMS-WM if it has no remaining liabilities or if SoFFin has assumed any remaining liabilities. Any assets or profits remaining at the time of dissolution will be transferred to SoFFin.

Reorganization of FMSA

In December 2016, the German parliament passed a law for the reorganization of FMSA, under which Germany’s national resolution authority will be integrated into the Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht) and the administration and management of SoFFin will be assumed by the Federal Republic of Germany – Finance Agency (Bundesrepublik Deutschland – Finanzagentur GmbH). FMSA will remain responsible for the German wind-up institutions FMS-WM and Erste Abwicklungsanstalt. Hence, the reorganization does not affect the supervision and control of the mentioned wind-up institutions. The reorganization is expected to be completed by January 1, 2018.

8

BUSINESS AND OPERATIONS

Introduction

FMS-WM is tasked with unwinding the portfolio of risk positions and non-strategic assets/businesses that it assumed on October 1, 2010 from the HRE Group in ways that maximize its value. As described in more detail under “—The Portfolio—Outsourced Portfolio Administration,” FMS-Wertmanagement Service GmbH (“FMS-WM Service”), a wholly owned subsidiary of FMS-WM, performs portfolio management services for FMS-WM. Plans to privatize FMS-WM Service were cancelled in May 2015.

FMS-WM’s activities are characterized by the following strategic goals:

| | • | | Unwinding of the risk assets aimed at maximizing their value: FMS-WM aims to unwind the risk assets in a manner that maximizes their value, subject to defined wind-up and risk strategies that are adjusted on a continuous basis. The winding-up plan—which is the key strategic management tool of FMS-WM—serves as the basis for the implementation of its portfolio liquidation operations. Depending on the market situation and the asset category, the winding-up plan provides for the following strategies in connection with liquidating the portfolio assumed by FMS-WM: |

| | – | | Holding assets, which includes active management of loans and securities with a view to repaying outstanding amounts (e.g., where the risk/return profile is acceptable). |

| | – | | Selling assets to the extent it makes economic sense (e.g., to reduce positions with a higher risk profile and when market opportunities arise). |

| | – | | Restructuring, including workout, wind-up and reorganization measures, relating to both performing and non-performing financial instruments, particularly in the Infrastructure and Commercial Real Estate segments, with a view to maximizing the value of the liquidation measure related to the financial instrument (including by reducing risk). |

| | • | | Cost-effective servicing and management of the risk assets: The unwinding of the risk assets is carried out in part by FMS-WM itself and in part by FMS-WM Service as portfolio servicer. FMS-WM remains solely responsible for the unwinding aimed at maximizing value and the cost-effective servicing and management of the portfolio. |

| | • | | Cost-effective funding and separate market access for FMS-WM: FMS-WM seeks to ensure cost-effective funding for the purpose of carrying out its mandate. Given its backing by the full faith and credit of the Federal Republic, FMS-WM is able to realize funding cost advantages that are not available to the HRE Group. |

In order to achieve its mandate of unwinding the portfolio of risk positions and non-strategic assets/businesses assumed from the HRE Group, FMS-WM may engage in all kinds of banking and financial services transactions and all other transactions that directly or indirectly serve its purposes. FMS-WM is, however, neither a financial institution nor a financial services institution within the meaning of the KWG, nor a financial service provider within the meaning of the WpHG, nor an insurance company within the meaning of the VAG. FMS-WM is also prohibited from engaging in transactions that would require a license under the European Union Banking Directive (2006/48/EC) or the European Union Directive on markets for financial instruments (2004/39/EC).

The Portfolio

FMS-WM assumed a portfolio of risk positions and non-strategic assets/businesses in an original amount of EUR 175.7 billion (nominal volume) from the HRE Group on October 1, 2010. As of December 31, 2016, FMS-WM had liquidated approximately EUR 92.1 billion (excluding the Portfolio Extension) (December 31, 2015: EUR 81.0 billion) of its initial portfolio of EUR 175.7 billion, resulting in a nominal value of the aggregate portfolio of EUR 83.6 billion as of December 31, 2016. Including the Portfolio Extension, the nominal value of the aggregate portfolio amounted to EUR 88.9 billion as of December 31, 2016.

As of December 31, 2016, FMS-WM’s portfolio (including the Portfolio Extension) encompassed 2,097 individual exposures (December 31, 2015: 2,648) with 986 different counterparties (December 31, 2015: 1,329) and a significant amount of derivatives. The individual exposures are located in 54 countries and denominated in 15 currencies. Geographically, the greatest concentrations are in Italy, the United States, the United Kingdom, Spain, Canada and Germany. Less than half (43%) of the exposures in the portfolio are denominated in euro, a third (33%) in U.S. dollars and approximately 17% in British pounds sterling. The portfolio is highly complex and diverse and consists of a particularly high proportion of illiquid exposures with extremely long maturities. To the extent that a legal transfer of risk assets could not be effected as of October 1, 2010 (for example, due to outstanding consent requirements),

9

economic ownership of such risk positions was transferred synthetically to FMS-WM (for example, through subparticipations or guarantees). FMS-WM is currently working on the physical and legal transfer of these risk positions that to date have only been transferred synthetically from the HRE Group to FMS-WM, and exposures relating to synthetically transferred receivables and derivatives still awaiting novation were significantly reduced in fiscal year 2016.

For purposes of risk management and the wind-up reports that FMS-WM submits to FMSA on a monthly basis in accordance with the winding-up plan, FMS-WM has classified the portfolio into four segments: Public Sector, Structured Products, Infrastructure and Commercial Real Estate. The segments in turn were broken down into 30 wind-up clusters as of December 31, 2016. The assets of all four segments include syndicated loans.

On December 19, 2014, FMS-WM acquired all shares in Depfa for a purchase price of EUR 320 million (excluding incidental acquisition expenses). In doing so, FMS-WM implemented the decision of May 13, 2014 by the Federal Government’s inter-ministerial steering committee, which, after considering all options, decided to unwind Depfa and its subsidiaries (“Depfa Group”) via FMS-WM. The Depfa Group is managed as an independent equity investment. FMS-WM appoints two members of the Executive Board and a unit head as non-executive members to Depfa’s board of directors. The Depfa Group’s portfolio consists mostly of positions with investment grade issuer ratings. In fiscal year 2015, FMS-WM was forced to write down the book value of its equity investment in the Depfa Group by EUR 83 million due to persistently low interest rates and higher expenses related to increased regulatory compliance obligations. As of December 31, 2016, Depfa’s consolidated financial statements recognized total assets of EUR 27.6 billion.

On January 19, 2016, FMS-WM announced its intention to buy back certain securities of the Depfa Group denominated in euros, Swiss francs, U.S. dollars and Canadian dollars with a total issue volume of around EUR 3.3 billion. In the context of this public tender offer, FMS-WM purchased EUR 2.6 billion securities, or approximately 79% of the outstanding nominal amount. In addition to this public tender offer, FMS-WM also regularly acquires other bonds and registered securities issued by the Depfa Group on the capital market, when and to the extent market conditions allow. In total, FMS-WM acquired Depfa Group liabilities with a nominal value of EUR 6.0 billion in fiscal year 2016.

On November 4, 2016, FMS-WM sold the repurchased Depfa Group liabilities to Depfa and in return acquired assets from Depfa’s cover pools with a nominal volume of EUR 5.2 billion. The transaction, referred to as the “Portfolio Extension” herein, complied with applicable regulatory and legal requirements and each individual security was transferred at market value. In total, 188 exposures were transferred from Depfa to FMS-WM, comprising primarily exposures to debtors in the United States (amounting to EUR 3.4 billion) and exposures to borrowers in European Union member states (amounting to EUR 1.5 billion). The exposures consist exclusively of receivables and securities attributable to Public Sector and Structured Products segments.

In the first quarter of 2017, FMS-WM purchased further bonds and notes of Depfa Group companies with a nominal value of EUR 0.8 billion. With the aim of ensuring that the Depfa Group is wound up in a way that maximizes its value, these purchased financial instruments are to be on-sold to the Depfa Group companies in fiscal year 2017 in return for Depfa Group exposures.

Outsourced Portfolio Administration

Until September 30, 2013, the HRE Group served as an outside administrator of the portfolio transferred to FMS-WM. The work outsourced to the HRE Group pursuant to a cooperation agreement between FMS-WM and Deutsche Pfandbriefbank AG (“PBB”), the core financial institution of the HRE Group, included many of the administrative activities in connection with the portfolio assumed and, as of December 31, 2012, approximately 500 employees of the HRE Group were working for FMS-WM in connection with portfolio servicing at a cost of approximately EUR 21 million per month.

As the transfer of risk positions and non-strategic assets/businesses from the HRE Group to FMS-WM could be viewed as state aid, the transfer had to be approved by the European Commission. In this context, the Federal Republic committed to ensure that, after September 30, 2013, the HRE Group would provide neither asset management services nor refinancing services for FMS-WM and that, from an organizational point of view, those services can be assumed by third parties. Pursuant to this commitment, the cooperation agreement with PBB has been terminated with effect as of September 30, 2013.

Since October 1, 2013, FMS-WM Service, a service entity established by FMS-WM in April 2012, has been tasked with the full set of portfolio management services and operations services including collateral management, settlement functions and credit operations, while FMS-WM retains final decision-making powers and ultimate responsibility for the risk assets under management. The master agreement governing the outsourcing of business processes and services also grants FMS-WM extensive rights to obtain information and perform inspections, enabling it to monitor and control the servicing of the risk assets by FMS-WM Service. Further, IBM Deutschland GmbH has assumed the provision of comprehensive information technology services as of October 1, 2013, and additional third-party service providers perform regulatory reporting and financial administration functions.

10

FMS-WM’s Segments

As described above, FMS-WM’s portfolio is grouped into four segments: Public Sector, Structured Products, Infrastructure and Commercial Real Estate.

Portfolio data presented in the following include the additions from the Portfolio Extension.

Public Sector

As of December 31, 2016, the Public Sector segment held assets with an aggregate nominal value of EUR 44.3 billion, accounting for 49.8% of FMS-WM’s overall portfolio (December 31, 2015: EUR 47.6 billion). As of the same date, the portfolio in this segment encompassed 927 exposures (December 31, 2015: 907) with 417 counterparties (December 31, 2015: 393). In November 2016, 101 exposures amounting to EUR 1.6 billion were added in connection with the Portfolio Extension.

The borrowers and issuers of the securities held by the Public Sector segment are state and regional governments, municipalities, public law entities and semi-public companies. European Union member states account for the majority of the portfolio, with Italy representing 49% of the portfolio’s aggregate nominal value as of December 31, 2016. As of this date, approximately 79% of the segment was made up of bonds, with loans accounting for the remaining 21%.

FMS-WM is working to improve its position in the medium and long term. To that end, FMS-WM negotiates directly with the issuers of the bonds or the counterparties of hedging transactions with the aim of unwinding, simplifying or untangling complex coupon or derivatives structures.

The ratings breakdown of the Public Sector segment’s portfolio has remained stable relative to the volume unwound in fiscal year 2016, as presented in the following table, which is based on FMS-WM’s internal ratings categories (for information on the corresponding Standard & Poor’s ratings categories, see footnotes to the table).

BREAKDOWNOF PUBLIC SECTOR PORTFOLIOBY RATINGS CATEGORY

| | | | | | | | |

| | | December 31, 2015 | | | December 31, 2016 | |

| | | (unaudited) | |

| | | (€ in billions) | |

IR 1 – 7(1) | | | 17.7 | | | | 17.3 | |

IR 8 – 10(2) | | | 25.2 | | | | 24.4 | |

IR 11 – 13(3) | | | 3.4 | | | | 2.5 | |

IR 14 – 22(4) | | | 0.0 | | | | 0.0 | |

IR 23 – 27(5) | | | — | | | | — | |

IR 28 – 30(6) | | | 1.2 | | | | 0.0 | |

| | | | | | | | |

Total | | | 47.6 | | | | 44.3 | |

| | | | | | | | |

| (1) | Corresponds to S&P’s ratings categories AAA to A-. |

| (2) | Corresponds to S&P’s ratings categories BBB+ to BBB-. |

| (3) | Corresponds to S&P’s ratings categories BB+ to BB-. |

| (4) | Corresponds to S&P’s ratings categories B+ to B-. |

| (5) | Corresponds to S&P’s ratings categories CCC+ to CCC-. |

| (6) | Corresponds to S&P’s ratings category D. |

In October 2016, FMS-WM accepted the offer by the Austrian State of Carinthia in co-operation with the Austrian Government as regards eligible liabilities of HETA ASSET RESOLUTION AG (“HETA”) (bonds issued by Hypo Alpe Adria, which was nationalized in 2009) (the “HETA Bonds”) to exchange the HETA Bonds for securities from the Carinthian Compensation Fund. The HETA Bonds had been subject to a payment moratorium since May 2015. Following its acceptance of the exchange offer, FMS-WM withdrew from the litigation it had initiated in response to the moratorium. As of today, FMS-WM holds no more exposure related to HETA.

11

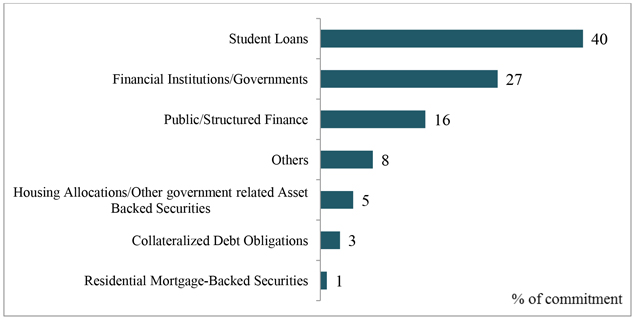

Structured Products

As of December 31, 2016, the Structured Products segment comprised assets with an aggregate nominal value of EUR 30.0 billion, accounting for 33.8% of FMS-WM’s overall portfolio (December 31, 2015: EUR 28.1 billion). As of the same date, the portfolio in this segment encompassed 541 exposures (December 31, 2015: 540) with 280 counterparties (December 31, 2015: 319). In November 2016, 87 exposures amounting to EUR 3.6 billion were transferred to the Structured Products portfolio in connection with the Portfolio Extension. These were mainly structured financial products in the United States.

The Structured Products segment includes practically all types of structured credit instruments from asset-backed securities (“ABS”), commercial and residential mortgage-backed securities (“CMBS” or “RMBS”) or collateralized debt obligations (“CDO”) to exotic interest, inflation and credit derivatives. Many of the underlying assets of these structured products originated in the United States.

The following chart reflects the proportion of the various asset classes in the Structured Products segment.

Forced sales of the exposures may be possible only at substantial discounts, due to, among other reasons, changed market conditions, sharp cuts in external ratings and the poor quality of the assets that serve as collateral for these securities. A hold strategy often is the best option for preventing losses on sales because most structured products are highly illiquid securities, i.e., they are rarely traded in the market. The objective of the portfolio managers is to improve or, where possible, unwind complex structures that are disadvantageous from FMS-WM’s perspective.

Infrastructure

As of December 31, 2016, the Infrastructure segment comprised assets with an aggregate nominal value of EUR 11.5 billion, accounting for 12.9% of FMS-WM’s overall portfolio (December 31, 2015: EUR 13.8 billion). As of the same date, the portfolio in this segment encompassed 338 exposures (December 31, 2015: 361) with 170 counterparties (December 31, 2015: 180).

The exposures in the Infrastructure segment’s portfolio are spread across all five continents, with a focus on the United Kingdom, which makes up 57% of the portfolio’s aggregate nominal value as of December 31, 2016. These exposures encompass corporate loans and securities, project financing, acquisition funding and asset-based loans. The financed properties include regulated utilities (38%), social infrastructure (22%), toll roads (12%), non-road transportation infrastructure (10%), airports and ports (8%), power/energy infrastructure (7%), environmental water/waste infrastructure (3%) and asset finance and others (1%).

Most of the loans in this segment have very long maturities and were closed at margins that are substantially below current market levels because many borrowers were either government or government-sponsored entities or are structures to which the public sector is a party in some other way, for instance as the entity that procures products and services. Furthermore, it is difficult to sell or prematurely repay individual exposures or entire sub-portfolios because the assumptions that were made at the time of entering into the exposures in many of these projects with respect to the degree of utilization or occupancy have in the meantime turned out to be too optimistic.

12

In view of the complexity of the portfolio held by this segment, the segment’s activities focus on restructuring individual transactions to improve the chances of effecting a subsequent redemption, (partial) settlement by a third party or subsequent sale.

Commercial Real Estate

As of December 31, 2016, the Commercial Real Estate segment comprised assets with an aggregate nominal value of EUR 3.1 billion, accounting for 3.5% of FMS-WM’s overall portfolio (December 31, 2015: EUR 5.2 billion). As of the same date, the portfolio in this segment encompassed 291 exposures (December 31, 2015: 840) with 121 counterparties (December 31, 2015: 438).

The exposures in the Commercial Real Estate segment’s portfolio are concentrated primarily in Germany and the United Kingdom, which make up 29% and 27%, respectively, of the portfolio’s aggregate nominal value as of December 31, 2016. Loans secured by mortgages on commercial real estate account for the majority of the global portfolio managed by the Commercial Real Estate segment. The properties financed include office properties (28%), shopping centers (retail) (23%), mixed use (10%), residential properties (4%), hotels (3%), industrial/logistics (2%) and others (30%).

FMS-WM’s Commercial Real Estate segment is managed by FMS-WM’s Commercial Real Estate unit. The standard wind-up strategies of the segment are to “hold,” “restructure” and “sell.” The restructuring strategy approach is pursued when it becomes evident that a borrower cannot repay the loan upon maturity. The objective here is to stabilize the exposure and thus improve the outlook for later repayment or sale of the loan or collateral.

In some cases, FMS-WM carries out foreclosures to enforce claims. In very rare cases, rescue acquisitions are made in which FMS-WM takes over a financed property with the aim of selling it again as quickly as possible after further restructuring. The principle of maximizing value remains of the utmost importance in this case as well.

A major part of the unwinding of the Commercial Real Estate segment’s portfolio is expected to be completed by 2020.

Unwinding the Portfolio

The portfolio assumed by FMS-WM is managed and liquidated in accordance with its winding-up plan, which describes the wind-up measures FMS-WM intends to take and includes a timeline for liquidation measures relating to the risk positions and non-strategic assets/businesses. The winding-up plan is proposed by FMS-WM’s Executive Board and adopted by the Supervisory Board. In accordance with its charter, FMS-WM submits monthly reports to FMSA, which include information on the process of recovery and liquidation under the winding-up plan. In its supervisory capacity, FMSA has the right to request changes to the winding-up plan and approves and supervises FMS-WM’s implementation of the winding-up plan as well as any deviations from, or amendments to, the winding-up plan. FMS-WM monitors prevailing market conditions on an ongoing basis to determine whether the winding-up plan needs to be adapted.

The winding-up plan has been designed with a view to ensuring that FMS-WM at all times has sufficient liquidity to cover its three-month liquidity requirements under stress scenario assumptions over the entire wind-up period, independently of SoFFin’s duty to provide liquidity to FMS-WM and to offset losses incurred by it. It also provides that, in principle, FMS-WM may not engage in new business with the exception of refinancing and hedging transactions and selected new business that reduces portfolio risks in a cost efficient manner (e.g., prolongations as well as selective restructuring measures).

The process of selling individual assets follows detailed, fixed instructions. For instance, a sale has to be based on offers from several bidders and deviations from this process are only permitted under special circumstances. The sales process aims to ensure verification and documentation that bids reflect market prices.

In addition to actively reducing the portfolio volume, an important goal for the successful management of the portfolio is the improvement of the quality of the portfolio’s structure, which FMS-WM strives to achieve by restructuring loan exposures, securities holdings and derivative positions. In this way, FMS-WM substantially improved the medium to long-term prospects for the realization of numerous exposures in fiscal year 2016, for example through intensive negotiations with borrowers, consortium members and issuers. Such successfully implemented restructuring measures have the effect of reducing the portfolio’s complexity and risk.

The unwinding of FMS-WM’s portfolio in fiscal year 2016 reflected the wind-up of the portfolio transferred from the HRE Group to FMS-WM in 2010, the Portfolio Extension, as well as the wind-up of the latter by the balance sheet date. In connection with

13

the Portfolio Extension, FMS-WM acquired risk positions with a nominal volume of EUR 5.2 billion. Despite redemptions of EUR 0.1 billion, the nominal volume of these risk positions increased to EUR 5.3 billion as of December 31, 2016 due to foreign currency effects in an amount of EUR 0.2 billion. As of December 31, 2016, FMS-WM’s aggregate portfolio stood at EUR 88.9 billion (December 31, 2015: EUR 94.7 billion). Not including countervailing currency effects, this corresponds to a wind-up of EUR 92.7 billion, or 52.8%, since October 1, 2010.

Taking into account the Portfolio Extension, in fiscal year 2016 the portfolio was reduced (before currency effects) by EUR 4.6 billion (2015: EUR 15.5 billion) which was positively impacted by currency effects of EUR –1.2 billion (2015: EUR 3.9 billion). Excluding the effects of the Portfolio Extension, portfolio wind-up before foreign currency effects in fiscal year 2016 was EUR 9.7 billion (based on exchange rates as of December 31, 2015) or EUR 11.1 billion taking foreign currency effects into account (2015: EUR 11.6 billion). With respect to the EUR 11.1 billion reduction, active sales accounted for EUR 2.9 billion (2015: EUR 4.3 billion) and contractual redemptions and amortizations accounted for EUR 8.2 billion (2015: EUR 7.3 billion).

The following table shows the portfolio development in fiscal year 2016 (taking into account the Portfolio Extension) and the reconciliation of the nominal value of the portfolio excluding derivatives from the transfer date (October 1, 2010) to total assets as of December 31, 2015 and 2016 (translated at exchange rates as of December 31, 2015 and 2016, respectively):

| | | | | | | | |

| | | As of December 31, | |

| | | 2015 | | | 2016 | |

| | | (unaudited) | |

| | | (€ in billions) | |

Wind-up portfolio commitment as of October 1, 2010 | | | 175.7 | | | | 175.7 | |

– Portfolio wind-up | | | -88.7 | | | | -92.7 | |

+ Currency effects | | | +7.7 | | | | +5.9 | |

relating to the portfolio wind-up | | | +7.7 | | | | +5.7 | |

relating to the Portfolio Extension | | | — | | | | +0.2 | |

| | | | | | | | |

Wind-up portfolio commitment | | | 94.7 | | | | 88.9 | |

– Undrawn credit lines and guarantees | | | -0.7 | | | | -0.7 | |

+ Portfolio of own issues(1) | | | +27.0 | | | | +22.8 | |

+ Other receivables including portions thereof(2) | | | +50.2 | | | | +66.2 | |

| | | | | | | | |

Total assets | | | 171.2 | | | | 177.2 | |

| | | | | | | | |

| (1) | Nominal value before accrued interest. |

| (2) | Mainly contains the cash collateral for derivatives, amortized cost of derivatives taken over, receivables from liquidity facilities used, current credit balances and accrued interest. |

Based on nominal values broken down by segment and taking the Portfolio Extension into account, the portfolio was reduced as follows from October 1, 2010 to December 31, 2016 (translated at exchange rates as of December 31, 2016):

| | | | | | | | | | | | | | | | |

| | | October 1, 2010 | | | Portfolio wind-up | | | Currency effects | | | December 31, 2016 | |

| | | (unaudited) | |

| | | (€ in billions) | |

Public Sector | | | 86.6 | | | | -42.8 | | | | +0.5 | | | | 44.3 | |

Structured Products | | | 43.9 | | | | -19.0 | | | | +5.1 | | | | 30.0 | |

Infrastructure | | | 18.0 | | | | -6.7 | | | | +0.2 | | | | 11.5 | |

Commercial Real Estate | | | 27.2 | | | | -24.2 | | | | +0.1 | | | | 3.1 | |

| | | | | | | | | | | | | | | | |

Total | | | 175.7 | | | | –92.7 | | | | +5.9 | | | | 88.9 | |

| | | | | | | | | | | | | | | | |

The following table shows the remaining maturities of the assets broken down by segments as of December 31, 2016:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Until 2017 | | | 2018–2020 | | | 2021–2030 | | | 2031–2040 | | | After 2040 | | | Total | |

| | | (unaudited) | |

| | | (€ in billions) | |

Public Sector | | | 2.3 | | | �� | 4.8 | | | | 10.6 | | | | 19.4 | | | | 7.2 | | | | 44.3 | |

Structured Products | | | 0.7 | | | | 2.1 | | | | 9.1 | | | | 10.5 | | | | 7.5 | | | | 30.0 | |

Infrastructure | | | 0.1 | | | | 0.6 | | | | 2.0 | | | | 2.8 | | | | 5.9 | | | | 11.5 | |

Commercial Real Estate | | | 1.7 | | | | 1.0 | | | | 0.5 | | | | 0.0 | | | | 0.0 | | | | 3.1 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total(1) | | | 4.8 | | | | 8.5 | | | | 22.2 | | | | 32.7 | | | | 20.7 | | | | 88.9 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Figures may not add up due to rounding. |

14

Exposure to Troubled Sovereigns and Concentration Risks

The portfolio of FMS-WM contains several significant concentration risks, including those in sovereign debt exposures, which are vulnerable to macroeconomic or systemic risks and can cause significant losses in FMS-WM’s portfolio. In particular, there are significant concentrations in the portfolio related to Italy and Spain (together with Portugal, Greece and Ireland, the “peripheral euro area countries”), especially in the Public Sector segment. As of December 31, 2016, Italy comprised an important part of FMS-WM’s exposures at default (“EaD”), accounting for EUR 28.4 billion, representing approximately 27% of FMS-WM’s total EaD (December 31, 2015: EUR 29.3 billion). FMS-WM completely closed its position in Greek securities in the first half of 2016. For more information on the breakdown of FMS-WM’s credit portfolio by countries and regions, see “—Risk Report—Credit Risk—Risk Position—Breakdown of Credit Portfolio by Countries and Regions.”

The following table shows a breakdown of FMS-WM’s EaD by sector for bonds and loans concerning the peripheral euro area countries, including information on related microhedges, as of December 31, 2016.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Exposure at Default – Bonds & Loans per Sector | | | | | | Microhedges(2) | |

Country(1) | | Gross

sovereign | | | Other

public

borrowers | | | Financial

institutions | | | Non-financial

corporations | | | Total EaD per

country | | | Additional (negative)

MtM of Microhedges | |

| | | (unaudited) | |

| | | (€ in billions) | |

Italy | | | 23.8 | | | | 2.3 | | | | 0.2 | | | | 2.1 | | | | 28.4 | | | | 9.4 | |

Spain | | | 1.1 | | | | 2.2 | | | | 0.3 | | | | 1.0 | | | | 4.6 | | | | 0.6 | |

Portugal | | | 0.9 | | | | 0.1 | | | | 0.1 | | | | 0.5 | | | | 1.6 | | | | 0.2 | |

Greece | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Ireland | | | — | | | | 0.2 | | | | — | | | | 0.2 | | | | 0.4 | | | | 0.0 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total(3) | | | 25.8 | | | | 4.8 | | | | 0.6 | | | | 3.8 | | | | 35.0 | | | | 10.3 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | The allocation is based on the country of the economic risk (e.g., location of the collateral), which may be different from the legal domicile of the debtor/issuer in individual cases. |

| (2) | The EaD definition applied by FMS-WM already accounts for negative mark-to-market (“MtM”) values of microhedges as of the date of the asset transfer from the HRE Group in October 2010. In order to avoid redundancies, only the current negative mark-to-market values of microhedge instruments to the extent that they exceed their October 2010 values are included in this table. |

| (3) | Figures may not add up due to rounding. |

Treasury

FMS-WM engages in funding activities, including the issuing of debt securities and/or obtaining financing from financial institutions, in order to refinance funding instruments associated with the assumed portfolio as they expire. FMS-WM will have to engage in refinancing activities until its portfolio has been liquidated. FMS-WM monitors its financing needs and liquidity requirements by means of a liquidity management system similar to the ones used by financial institutions. FMS-WM seeks to ensure that it has sufficient liquidity to cover its three-month liquidity requirements under stress scenario assumptions at all times.

The Group Treasury unit’s core tasks are funding and liquidity management as well as the management of interest rate and foreign exchange risks. In addition, FMS-WM’s Group Treasury unit is responsible for improving FMS-WM’s funding structure on an ongoing basis with the aim of generating positive contributions to FMS-WM’s earnings.

Funding management’s main task is to raise long-term funds in the international capital markets. Maturities typically range from one to ten years, with the majority of bonds having a tenor of three to five years. In fiscal year 2016, FMS-WM successfully raised EUR 15.8 billion via the capital markets (2015: EUR 12.3 billion). In this context, the share of funding with an initial maturity of more than one year, as of December 31, 2016, accounted for approximately 47% of the aggregate funding volume (December 31, 2015: 50%). As a result, FMS-WM was able to maintain a balanced ratio between short- and long-term funding across all currencies in fiscal year 2016. As of December 31, 2016, FMS-WM reported a total outstanding capital market funding of approximately EUR 63 billion with an average remaining maturity of around three years.

FMS-WM’s bonds are being offered in a broad range of formats, including benchmark format, non-benchmark public format and private placements as well as in different currencies, primarily the euro, pound sterling and U.S. dollar, in order to fund the wind-up portfolio at matching currencies. In fiscal year 2016, FMS-WM focused in particular on obtaining U.S. dollar funding on the U.S. capital market through its issuance program in global format established in the United States, and it successfully raised a total of USD 3.5 billion through two U.S. dollar benchmark issues with maturities of three and five years, respectively.

15

As part of its short-term liquidity management, FMS-WM utilizes instruments with maturities of up to one year. In fiscal year 2016, FMS-WM’s issuing activity under its existing money market programs, namely the European Commercial Paper/Certificates of Deposit Program (“ECP/CD Program”) and the U.S. Asset-Backed Commercial Paper Program (“US ABCP Program”), further contributed to a stable and sustainable funding structure for FMS-WM. As of December 31, 2016, the ECP/CD Program had a volume of EUR 31.7 billion (December 31, 2015: EUR 28.8 billion), and the US ABCP Program had a volume of EUR 12.3 billion (December 31, 2015: EUR 10.3 billion).

Interest rate and foreign exchange risks are managed in a centralized fashion on an income-oriented basis guided by a risk aversion policy within the limit system. The aim is to minimize the fluctuations in the fair value and profit/loss due to market risks. To this end, the Group Treasury unit enters into hedging transactions for individual exposures (micro hedges) or at the portfolio level (macro hedges).

16

CAPITALIZATION AND INDEBTEDNESS

The following table sets forth FMS-WM’s actual capitalization and indebtedness as of December 31, 2016.

| | | | |

| | | As of

December 31, 2016 | |

| | | audited | |

| | | (in € millions) | |

Debt | | | | |

Short-term debt | | | 9,728 | |

Bonds and notes | | | 116,243 | |

Loans and advances to bank and loans and advances to customers (not payable on demand) | | | 32,517 | |

Other borrowings and other liabilities | | | 17,669 | |

Equity | | | | |

Total equity | | | 1,041 | |

| | | | |

Total capitalization | | | 177,198 | |

| | | | |

17

ECONOMIC CONDITIONS AND MARKET DEVELOPMENTS

The following sections contain an overview of economic conditions and market developments, which affected the value of FMS-WM’s portfolio and its business in general in 2016.

Macroeconomic Developments

At the beginning of 2016, the global economy was expanding at only a modest pace. While the situation in the emerging markets had stabilized at a low level, growth in the developed economies remained subdued. The U.S. economy grew at only a moderate pace in the first quarter and more slowly than in the previous quarters. In contrast, the euro zone continued its overall economic recovery. In the second half of 2016, the developed economies expanded slightly faster overall, driven mainly by accelerating growth in the United States and Japan. The trend in prices continued to be strongly influenced by crude oil prices, whose sharp decline persisted into January 2016 and was then followed by a recovery.

Developments in the financial markets were influenced mainly by growth of only modest proportions in the global economy and further expansionary monetary policy measures in the major economies. Both the performance of the Chinese economy and the sharp decline in oil prices (which nonetheless subsequently recovered) were troubling issues at the beginning of 2016. The Bank of Japan introduced negative interest rates for some bank deposits in January 2016. In March 2016, the governing council of the European Central Bank (“ECB”) decided on a comprehensive new package of monetary policy measures. Faced with turmoil in the global capital markets and risks to the U.S. economy, the U.S. Federal Reserve took a twelve-month break in its key interest rate normalization process, which it had begun in December 2015, before again raising the federal funds rate by 0.25% at the end of 2016. As a result of these macroeconomic developments, compounded by the increased risk aversion and uncertainty caused by the United Kingdom’s vote on whether to remain in the European Union (the “Brexit Vote”), government bond yields fell to new record lows at the end of the first half-year in 2016. For instance, the yield on 10-year German government bonds stood at just –0.2% at the beginning of July 2016. From summer onwards, however, the global economy proved to be in remarkably robust form and inflation rates rose gradually as a result of the recovery in oil prices. The results of the U.S. presidential election surprised many observers, and strengthened expectations that fiscal policy would be eased and monetary policy tightened. As a result, the trend in yields on government bonds reversed.

Secondary market spreads for the bonds of peripheral euro zone countries – and for Italian bonds in particular – widened in 2016. The ECB’s package of measures was able to achieve only a temporary narrowing before the Brexit Vote in the United Kingdom contributed to the widening of secondary market spreads. Downward pressure was also exerted by the banking crisis in Italy and the December referendum on the reform of the Italian Senate, in which voters rejected the reform proposed by the government.

The euro zone started off the year with strong growth – boosted by mild winter weather – but this trend then proceeded to weaken slightly. Unemployment continued to decline, falling from 10.5% in December 2015 to 9.6% in December 2016. In Germany, the underlying economic trend remained strong overall and GDP rose by 1.9% compared to the previous year. Growth drivers were domestic demand, principally private consumption, followed by government spending and construction investment.

In Italy, growth remained at a moderate level. After Italy’s GDP initially grew by 0.4% in the first quarter of 2016 compared to the previous quarter, growth came to a near standstill, slowing to 0.1% in the second quarter of 2016 due to weak domestic demand. In the third quarter of 2016, GDP grew by 0.3% compared to the previous quarter. While inflation rose from 0.1% to 0.5% compared to 2015, unemployment rose from 11.6% to 12.0%. The robust recovery in the Spanish economy continued, with GDP rising from 0.7% to 0.8% compared to the previous quarter. Inflation in the euro zone fell from 0.2% in December compared to the previous year to –0.2% in February 2016, before then being stabilized by the recovery in energy prices and rising to 1.1% in December 2016 compared to 2015.

To counter the increased risks to price stability, the governing council of the ECB decided to expand its securities purchase program from EUR 60 billion per month to EUR 80 billion, to extend the program until March 2017, to include corporate bonds in the program, to launch new long-term tenders, to set the repo rate at 0.0% and to lower the rate for the deposit facility to –0.4%. The governing council of the ECB also announced that it expected key rates to remain at the current level or lower levels for an extended period. In December 2016, the governing council of the ECB announced an extension of bond purchases to the end of 2017, with the monthly volume reduced to EUR 60 billion starting in April 2017.

After a slight slowdown in growth at the beginning of 2016, the UK economy exhibited a strong recovery in the run-up to the vote on the Brexit Vote. In light of the general uncertainty created by the vote to leave the European Union, and, in particular, the political and economic repercussions, the Bank of England lowered its key interest rates after the vote and resumed its bond purchases. The ensuing easing of monetary conditions and the weakening of pound sterling were the main reasons for the sustained growth trend in the following months. Inflation rose during the year from 0.2% in December 2015 to 1.6% in December 2016, compared to the corresponding month of 2015.

18

In the United States, the oil industry’s reluctance to make capital investments held the economy back at the beginning of 2016, while net exports also weighed on growth. As the negative effects of the weak oil price and strong U.S. dollar ultimately subsided, growth picked up again in the second quarter of 2016, boosted by private consumption. Unemployment fell during the year from 5.0% to 4.7%. Inflation rose from 0.7% in December 2015 to 2.1% in December 2016, with oil prices being the primary driver. In light of the reduced momentum at the beginning of 2016, the U.S. Federal Reserve took a twelve-month break in the cycle of interest rate increases that it had begun at the end of 2015. The benchmark interest rate was ultimately raised by 0.25% at the end of the year, against the background of an improving economy and rising inflation rates.

In the major emerging markets, the deterioration in the economic situation witnessed in 2015 then stabilized at the start of 2016. In China, macroeconomic stimulus measures brought about an end to the slowdown in growth. Recessions eased slightly in Russia and (to a lesser degree) in Brazil. Strong expansion continued apace in India.

Commercial Real Estate

Developments in the real estate markets in which FMS-WM’s real estate collateral is located remained largely positive in 2016. The favorable domestic market environment was used to successfully conclude the sale of the small-scale retail portfolio in Germany. In addition, the strong investor demand for properties in the Dutch real estate market led to the successful sale of FMS-WM’s exposures in this submarket. Geographically speaking, the remaining portfolio is now focused on German, UK and Eastern European financing, as well as properties in the United States.

The aggregate transaction volume in the German commercial real estate financing market was high in 2016. At around EUR 60 billion, investment turnover across all asset classes remained at a high level. The Brexit Vote caused only a brief perturbation in the markets.

The German real estate market continued to be supported mainly by the persistently low level of capital market interest rates; for instance, investors turned to student apartments and nursing homes as investment opportunities with comparatively high returns. Foreign investors were particularly interested in large-scale real estate investments in 2016, resulting in a supply shortage trend matched by rising market prices in this segment.

Infrastructure Markets

At approximately USD 398.9 billion (2015: USD 438.1 billion), global project finance volume (in the securities, loan and equity market) was about 9% lower in 2016 compared to 2015 and at its lowest level since 2012.

The number of finalized projects decreased by about 20% compared to 2015, from 1,365 to 1,096 transactions. The global public-private partnership (PPP) / private finance initiative (PFI) volume was USD 67.1 billion in 2016, down 30% from USD 95.3 billion in 2015.

Capital expenditure in the energy sector picked up year on year. Investment in transportation, oil and gas declined, however, driven by the slump in oil prices, as well as regulatory and political uncertainties. The above developments also generated increased investor interest in the secondary and refinancing market.

Financial Institutions and Covered Bonds

In 2016, the ECB’s low interest rate policy and bond purchase program contributed to the stabilization of the markets. However, despite the measures taken, the spreads of most bonds did not move significantly. The general uncertainty in the markets was further exacerbated by the difficulties besetting Deutsche Bank, which were caused primarily by legal disputes in the United States, and the issue of non-performing loans, which was particularly acute in Italy.

In addition, FMS-WM accepted the exchange offered by the Austrian State of Carinthia in co-operation with the Austrian Government as regards the HETA Bonds subject to a payment moratorium since May 2015, exchanging the HETA Bonds for securities from the Carinthian Compensation Fund. Following its acceptance of the exchange offer, FMS-WM withdrew from the litigation it had initiated in response to the moratorium.

19

Public Sector

In the public sector segment, the most important factors were central bank policies worldwide and the ongoing political risks. While the ECB kept interest rates at historically low levels and continued to provide liquidity to the markets with a bond purchase program, the U.S. Federal Reserve started to reverse the trend of decreasing interest rates and raised the benchmark interest rate in December 2016 for the second time in 12 months. Several political risks materialized in 2016, two of which being the Brexit Vote and the Italian referendum on constitutional reform which was rejected. In Italy, the outcome led to the resignation of the prime minister and generated further uncertainty about domestic political developments.

The ECB responded with measures that initially further stabilized the government bond markets. Accordingly, yields on all major European government bonds declined significantly from the end of 2015 until mid-2016. However, with inflation picking up again in summer 2016, driven, in particular, by the oil price increase, improved global growth prospects and decisions on U.S. fiscal policy, yields then rose towards the end of 2016. In addition, significant changes in spreads on European government bonds were also observed towards the end of 2016, mostly as a result of developing political risks. The yield on 10-year German government bonds, still hovering around 0.5% at the beginning of 2016, temporarily fell below 0.0% in the summer and ended the year at 0.2%. Developments in Spain and Italy were similar: Yields of 1.7% in Spain and 1.5% in Italy at the beginning of 2016 each then decreased by about 1% over the next six months to reach new historical lows by mid-2016. Towards the end of 2016, a significant uptick was recorded, with yields rising to about 1.4% in Spain and about 1.8% in Italy – the latter being caused by the tense political climate.

In Portugal, there was a clear widening of spreads during 2016, with yields on 10-year Portuguese government bonds rising from about 2.5% to 3.8% at the end of the year. Increased interest on the part of institutional investors in Greek government bonds meant that FMS-WM was able to completely close its position in Greek securities in the first half of 2016.

In mid-2016, the Brexit Vote was a source of considerable concern for the markets. After starting the year at about 1.8%, yields on UK 10-year government bonds fell significantly, occasionally dipping below 0.6% in August 2016. Yields then rose to about 1.2% at the end of 2016 on the strength of expectations about the performance of the global economy. FMS-WM expects that the Bank of England will use monetary policy measures to limit the negative effect of the United Kingdom’s exit from the European Union, and will also act to further reduce interest rates.

Structured Products

An outflow of funds from the municipal market was observed until the end of 2016 which resulted in poor performance in the municipal bond segment. Overall, credit quality is still viewed as stable, however, since most of the securities are in the investment-grade segment. The economic situation in Puerto Rico also led to turbulence in the municipal market.

An increasingly low level of coverage for U.S. pension obligations and a lack of restructuring measures were detrimental to individual counterparties, such as the U.S. states of Illinois and New Jersey.

In 2016, the global new issue volume exceeded USD 400 billion, a large percentage of which resulted from the funding of existing issues.

Asset-backed Securities