UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22781

Goldman Sachs Trust II

(Exact name of registrant as specified in charter)

71 South Wacker Drive,

Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

Copies to: |

Caroline Kraus | | Geoffrey R.T. Kenyon, Esq. |

Goldman, Sachs & Co. | | Dechert LLP |

200 West Street | | 100 Oliver Street |

New York, New York 10282 | | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: December 31

Date of reporting period: December 31, 2014

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Annual Report to Stockholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Annual Report | | | | December 31, 2014 |

| | |

| | | | Multi-Manager Alternatives Fund |

Goldman Sachs Multi-Manager Alternatives Fund

| | | | |

TABLE OF CONTENTS | | | | |

| |

Principal Investment Strategies and Risks | | | 1 | |

| |

Portfolio Management Discussion and Performance Summaries | | | 4 | |

| |

Schedules of Investments | | | 13 | |

| |

Financial Statements | | | 47 | |

| |

Financial Highlights | | | 50 | |

| |

Notes to Financial Statements | | | 52 | |

| |

Report of Independent Registered Public Accounting Firm | | | 72 | |

| |

Other Information | | | 73 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Fund. For additional information concerning the risks applicable to the Fund, please see the Fund’s Prospectus.

The Goldman Sachs Multi-Manager Alternatives Fund The Goldman Sachs Multi-Manager Alternatives Fund allocates its assets among multiple investment managers (“Underlying Managers”) who are unaffiliated with the Investment Adviser and who employ one or more non-traditional and alternative investment strategies. A strategy implemented by an Underlying Manager and/ or the use of quantitative models to implement that strategy may fail to produce the intended results. Different investment styles (e.g., “alternative”) tend to shift in and out of favor, and at times the Fund may underperform other funds that invest in similar asset classes. These strategies involve risks that may not be present in more traditional (e.g., equity or fixed income) mutual funds.

The Fund’s equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. The securities of mid- and small-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements. The Fund’s investments in fixed income securities and loans are subject to the risks associated with debt securities generally, including credit, interest rate, liquidity, call and extension risk. Foreign and emerging market investments may be more volatile and less liquid than investments in U.S. securities and will be subject to the risks of currency fluctuations and adverse economic or political developments.

Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; risks of default by a counterparty; and liquidity risk. Over-the-counter transactions are subject to less government regulation and supervision.” At times, the Fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all.

The Fund may have a high rate of portfolio turnover, which involves correspondingly greater expenses which must be borne by the Fund, and is also likely to result in short-term capital gains taxable to shareholders. The Fund’s investments in other pooled investment vehicles subject it to additional expenses. The Fund is “non-diversified” and may invest more of its assets in fewer issuers than “diversified” funds. Accordingly, the Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio and to greater losses resulting from these developments.

The Investment Adviser’s Alternative Investments & Manager Selection (“AIMS”) Group is responsible for making recommendations with respect to hiring, terminating, or replacing the Fund’s Underlying Managers, as well as the Fund’s asset allocations. With respect to the Fund, the AIMS Group applies a multifaceted process with respect to manager due diligence, portfolio construction, and risk management. The AIMS Group also manages additional pooled vehicles which have similar investment strategies to those of the Fund that are not offered to retail investors and are not registered under the Investment Company Act of 1940, as amended (the “Act”). Because these vehicles are not registered under the Act, they are subject to fewer regulatory restraints than the Fund (e.g., fewer trading constraints) and (i) may invest with managers other than the Fund’s Underlying Managers, (ii) may employ strategies that are not subject to the same constraints as the Fund, and (iii) may perform differently than the Fund despite their similar strategies.

There may be additional risks that the Fund does not currently foresee or consider material.

1

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

The investment program of the Fund is speculative, entails substantial risks and includes alternative investment techniques not employed by traditional mutual funds. The Fund should not be relied upon as a complete investment program. The Fund’s investment techniques (if they do not perform as designed) may increase the volatility of performance and the risk of investment loss, including the loss of the entire amount that is invested, and there can be no assurance that the investment objective of the Fund will be achieved.

2

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

What Differentiates Goldman Sachs’ Multi-Manager

Alternatives Fund Investment Process?

The Goldman Sachs Multi-Manager Alternatives Fund seeks long-term growth of capital by allocating its assets to underlying managers who employ a range of alternative and non-traditional investment strategies. The Fund benefits from the dedicated expertise of GSAM’s alternative investment team that has a legacy dating back to 19691 and a team of over 300 people located in 8 offices globally.2

| n | | We have over 135 alternative investment professionals2 dedicated to manager selection |

| n | | We employ a rigorous due diligence process to evaluate manager’s skill, strategy, and team and continually monitor managers after an investment is made |

| n | | Our Investment Committee process includes an independent “Devil’s advocate” to promote fluid debate and intense examination of each manager |

| n | | We combine “top down” market and economic environment considerations with “bottom up” manager-specific factors |

| n | | We incorporate judgment and quantitative tools to determine the appropriate investment size in each manager |

| n | | The process is continual with ongoing re-balancing and active management to optimize diversification |

| n | | We have over 50 professionals2 focused on alternative investment risk management and operational diligence |

| n | | We consider risk management an all-encompassing and real time discipline |

| n | | Our dedicated strategists leverage our proprietary risk management systems to continually monitor risk |

| 1 | | In June 1997, The Goldman Sachs Group, Inc. (GSG, Inc.) acquired the assets and business of Commodities Corporation, which GSG, Inc. subsequently renamed Goldman Sachs Hedge Fund Strategies LLC in December 2004. |

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk. Diversification does not protect an investor from market risk and does not ensure a profit.

3

PORTFOLIO RESULTS

Goldman Sachs Multi-Manager Alternatives Fund

Investment Objective

The Fund seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Alternative Investments & Manager Selection (“AIMS”) Group discusses the Goldman Sachs Multi-Manager Alternatives Fund’s (the “Fund”) performance and positioning for the 12-month period ended December 31, 2014 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, Class C, Institutional, Class IR and Class R Shares generated average annual total returns of 2.61%, 1.84%, 3.00%, 2.85% and 2.30%, respectively. These returns compare to the 0.03% average annual total return of the Fund’s primary benchmark, the Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index (the “Index”) during the same time period. The HFRX Global Hedge Fund Index, a broad proxy for hedge fund performance and the Fund’s secondary benchmark, returned -0.58% during the Reporting Period. |

| | To compare, the MSCI World Index, not the Fund’s benchmark but designed to measure the equity market performance of developed markets, had an average annual total return of 4.94% during the Reporting Period. Similarly not benchmarks of the Fund, the Barclays Global Aggregate Bond Index, designed to measure the broad global investment grade fixed income market, and the Barclays U.S. Corporate High Yield Bond Index, designed to measure the U.S. non-investment grade fixed-rate debt market, had average annual total returns of 0.59% and 2.45%, respectively, during the Reporting Period. |

| | References to the Fund’s benchmarks and to other indices mentioned herein are for informational purposes only, and unless otherwise noted, are not an indication of how the Fund is managed. The use of the Index as the Fund’s primary benchmark does not imply the Fund is being managed like cash and does not imply low risk or low volatility. |

| | Notably, during the Reporting Period, the Fund had a realized beta to the MSCI World Index of 0.50. (Beta is a measure of the sensitivity of an asset’s returns to broad market returns.) The Fund’s overall annualized volatility was 4.9% during the Reporting Period, while the overall annualized volatility of the global equity markets, as measured by the MSCI World Index, during the same time period was 8.2%. |

| Q | | What economic and market factors most influenced the financial markets as a whole during the Reporting Period? |

| A | | Global stock markets delivered strong returns in 2014, with U.S., European, Japanese and emerging market equity markets posting positive returns (in local currency terms) during the Reporting Period. U.S. equity markets, as represented by the S&P 500 Index, rose to record levels during the Reporting Period. The U.S. equity market was driven by an improving job market and low interest rates, which bolstered investor confidence despite a dramatic fall in oil prices during the second half of 2014 (which particularly weighed on energy stocks) and fears of a prolonged period of slow economic growth in Europe and China. European and Asian equity markets also managed gains (in local currency terms) for the calendar year 2014 even as geopolitical issues like elections in Brazil and Russia’s annexation of Crimea provided momentary headwinds to equity markets. |

| | The U.S. fixed income market exhibited exceptional resilience during the Reporting Period considering that expectations at the beginning of 2014 were for bond yields to rise as the Federal Reserve (the “Fed”) ended its quantitative easing program and perhaps might raise interest rates. The first half of 2014 in the fixed income market could largely be defined by investors looking for investment income in higher yielding but lower credit quality securities. However, the latter half of the year saw investors exit these higher yielding instruments on the back of lower inflation expectations predicated on lower global economic growth. The yield on the frequently-referenced 10-year U.S. Treasury note stood at 2.17% at the end of the Reporting Period, a significant decline from 3.03% at the start of 2014. Both high yield and leveraged loans, represented by the Barclays U.S. |

4

PORTFOLIO RESULTS

| | Corporate High Yield Bond Index and the S&P/LSTA Leveraged Loan Index, respectively, had positive returns for the year, although both slightly trailed the Barclays Global Aggregate Bond Index. |

| | The U.S. dollar strengthened versus all major currencies during the Reporting Period. The Japanese yen and the euro depreciated versus the U.S. dollar due to fears of sustained slow domestic economic growth. The Australian dollar and the New Zealand dollar weakened versus the U.S. dollar due to lower commodity demand and a slowing Chinese economy. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund’s performance during the Reporting Period can be attributed to the performance of the Fund’s Underlying Managers, who are unaffiliated investment managers that employ one or more non-traditional and alternative investment strategies. During the Reporting Period, the Fund allocated capital to nine Underlying Managers — Ares Management LLC (“Ares”); Brigade Capital Management, L.P.1 (“Brigade”); First Pacific Advisors, LLC (“FPA”); GAM International Management Limited (“GAM”); Graham Capital Management, L.P. (“Graham”); Halcyon Liquid Strategies IC Management LP (“Halcyon”); Lateef Investment Management (“Lateef”); Polaris Capital Management, LLC (“Polaris”) and Sirios Capital Management, L.P. (“Sirios”). These nine Underlying Managers represented five strategies — dynamic equity (Lateef and Polaris); equity long/short (FPA and Sirios); event driven and credit (Ares, Brigade and Halcyon); tactical trading (Graham); and opportunistic fixed income (GAM). |

| | Three Underlying Managers were added during the Reporting Period — Sirios, Polaris and Corsair Capital Management, L.P. (“Corsair”). Sirios utilizes an equity long/short strategy investing in a concentrated long portfolio with select alpha shorts composed of highly liquid, large cap companies and some exchange traded fund shorts as appropriate. The Fund’s Board approved Sirios in April 2014, and we allocated capital to the eighth Underlying Manager during the third quarter of 2014. Polaris utilizes a dynamic equity strategy focused on global and international equity value investing. The Fund’s Board approved Polaris in August 2014 and we allocated capital to the ninth Underlying Manager during the fourth quarter of 2014. Corsair utilizes an equity long/short strategy that employs a catalyst driven, research intensive approach focusing on companies going through strategic and/or structural change. The Fund’s Board approved Corsair in November 2014, and we expect to allocate capital to the Underlying Manager during the first quarter of 2015. |

| | Of the nine Underlying Managers with allocated capital during the Reporting Period, four generated positive returns and five generated negative returns. |

| Q | | Which strategies most significantly affected Fund performance? |

| A | | Of the five strategies employed across the Underlying Managers during the Reporting Period, four generated positive returns and one posted a negative return. |

| | The Fund’s tactical trading strategy generated the strongest positive performance during the Reporting Period, with long-dated interest rate futures, equity and currency exposures contributing to gains. Tactical trading strategies seek to produce total return by long and short investing across global fixed income, currency, equity and commodity markets. Tactical trading managers may employ various investment styles. Tactical trading managers that employ a global macro style may select their investments based upon fundamental analysis, or determining an asset’s value based upon factors that directly affect its value. Tactical trading managers that employ a managed futures investing style may use quantitative modeling techniques, i.e., determining an asset’s value based upon an analysis of price history, price momentum and the asset’s value relative to that of other assets, among other factors. Some tactical trading managers may employ both fundamental analysis and quantitative modeling techniques. Tactical trading managers typically have no bias to be long, short or neutral. |

| | The Fund’s equity long/short strategy generated the second-strongest positive performance during the Reporting Period, attributable primarily to long positions in the consumer discretionary and information technology sectors. Equity long/short strategies generally involve long and short investing, based on fundamental evaluations, research and various analytical measurements, in equity and equity-related investments. Equity long/short managers may, for example, buy stocks they expect to outperform or they believe are undervalued, and may also sell short stocks they believe will underperform or they believe are overvalued. Long positions benefit from an increase in the price of the underlying instrument or asset class, while short positions benefit from a decrease in that price. |

| 1 | | Effective July 1, 2014, Brigade Capital Management, LLC converted from a limited liability company to a limited partnership; its legal name is now Brigade Capital Management, L.P. |

5

PORTFOLIO RESULTS

| | The dynamic equity strategy used in the Fund posted positive performance during the Reporting Period, driven primarily by equity market exposure and stock selection, with positions in the health care and industrial sectors representing the top contributors. Dynamic equity strategies generally involve investing in equity instruments, often with a long-term view. Dynamic equity strategies are less likely to track a benchmark than traditional long-only strategies, and dynamic equity managers are less constrained than traditional long-only managers with respect to factors such as position concentration, sector and country weights, style and market capitalization. |

| | The Fund’s event driven and credit strategies posted modestly positive performance, aided by positions in select corporate high yield bonds and bank loans, although equity holdings in the energy sector detracted. Event driven and credit strategies seek to achieve gains from market movements in security prices caused by specific corporate events or changes in perceived relative value. These strategies may include, among others, merger arbitrage, distressed credit, opportunistic credit and value with a catalyst investing styles. |

| | The Fund’s opportunistic fixed income strategy posted modestly negative returns during the Reporting Period, struggling due to unanticipated volatility in emerging market interest rates and a decline in the price of high yield bonds in their portfolio. More specifically, the strategy’s weak performance was due to its developed market rate positioning as yield curves in the U.K. and U.S. flattened, meaning the yield differential between longer-term and shorter-term maturities narrowed. Opportunistic fixed income strategies seek to deliver positive absolute returns in excess of cash investments regardless of economic cycle (i.e., downturns and upswings) or cyclical credit availability. Opportunistic fixed income managers seek to maintain diversified exposure across various fixed income and floating rate market segments, with a focus on more liquid markets, assessing the relative value across sectors and adjusting portfolio weightings based on opportunity. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | The Underlying Managers of the Fund employ derivatives and similar instruments as part of their underlying strategies to hedge market exposure and/or to gain implicit leverage, subject to the constraints of the Investment Company Act of 1940, as amended. During the Reporting Period, credit default swaps, options on credit default swaps, equity futures, interest rate futures, interest rate swaps, options on interest rate futures, interest rate swaptions, bond futures, options on bond futures, forward foreign exchange contracts and foreign exchange options were used in the Fund. |

| Q | | Were there any notable changes in the Fund’s allocations during the Reporting Period? |

| A | | During the Reporting Period, shifts to the Fund’s asset allocation were made in response to the market environment and as a result of allocation to two new Underlying Managers, (i.e., Sirios and Polaris). More specifically, we increased the Fund’s allocations to equity long/short and event driven and credit strategies and reduced its allocations to dynamic equity, opportunistic fixed income and tactical trading strategies in recognition of historically high equity market valuations and to seek to take advantage of equity strategies that have the ability to participate in investment opportunities with a more asymmetrical risk/return profile. The Fund’s allocation to cash also decreased during the Reporting Period. |

| Q | | What is the Fund’s tactical view and strategy for the months ahead? |

| A | | We intend to continue to closely monitor global economic recovery, monetary policy and market volatility, while using active portfolio management and alternative investment strategies to position the Fund as we aim to deliver positive absolute returns across a variety of market environments. We believe the flexibility to allocate tactically across these alternative strategies may enable us to provide investors with positive absolute returns in a variety of market conditions and with significant diversification benefits. We intend to continue to actively explore adding new Underlying Managers with what we consider to be unique alternative capabilities as market conditions warrant. |

6

PORTFOLIO RESULTS

Index Definitions:

The Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index measures total return on cash, including price and interest income, based on short-term government Treasury Bills of about 90-day maturity, as reported by BofA Merrill Lynch.

The HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. The HFRX Global Hedge Fund Index is a trademark of Hedge Fund Research, Inc. (“HFR”). HFR has not participated in the formation of the Fund. HFR does not endorse or approve the Fund or make any recommendation with respect to investing in the Fund. (Source: Hedgefundresearch.com)

The Barclays Global Aggregate Bond Index is an unmanaged index, provides a broad-based measure of the global investment-grade fixed-rate debt markets and covers the most liquid portion of the global investment grade fixed-rate bond market, including government, credit and collateralized securities.

The Barclays U.S. Corporate High Yield Bond Index covers the universe of U.S. dollar denominated, nonconvertible, fixed rate, non-investment grade debt. Index holdings must have at least one year to final maturity, at least $150 million par amount outstanding, and be publicly issued with a rating of Ba1 or lower.

The MSCI World Index captures large and mid cap representation across the following 23 Developed Markets countries: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the UK and the US.

The S&P/LSTA U.S. Leveraged Loan Index provides an overview of the Senior Secured, Floating Rate Leveraged Loan market as well as an expansive review of the S&P Leveraged Loan Index (LLI) and sub-indexes including daily pricing on the S&P/LSTA LLI 100.

The S&P 500 Index is the Standard & Poor’s 500 Composite Index of 500 stocks, an unmanaged index of common stock prices. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an index.

All index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index.

7

FUND BASICS

Multi-Manager Alternatives Fund

as of December 31, 2014

| | | | | | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | January 1, 2014– December 31, 2014 | | Fund Total Return

(based on NAV)1 | | | Bank of America Merrill Lynch Three-

Month U.S. Treasury Bill Index2 | | | HFRX Global Hedge

Fund Index3 | |

| | Class A | | | 2.61 | % | | | 0.03 | % | | | -0.58 | % |

| | Class C | | | 1.84 | | | | 0.03 | | | | -0.58 | |

| | Institutional | | | 3.00 | | | | 0.03 | | | | -0.58 | |

| | Class IR | | | 2.85 | | | | 0.03 | | | | -0.58 | |

| | | Class R | | | 2.30 | | | | 0.03 | | | | -0.58 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. At the end of the month that issue is sold and rolled into a newly selected issue. The issue selected at each month-end rebalancing is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date. To qualify for selection, an issue must have settled on or before the month-end rebalancing date. While the index will often hold the Treasury Bill issued at the most recent 3-month auction, it is also possible for a seasoned 6-month Bill to be selected. |

| | 3 | | The HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies; including but not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry. |

| | | | HFRI and HFRX and related indices are trademarks and service marks of Hedge Fund Research, Inc. (“HFR”) which has no affiliation with GSAM. Information regarding HFR indices was obtained from HFR’s website and other public sources and is provided for comparison purposes only. HFR does not endorse or approve any of the statements made herein. |

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS4 |

| | | For the period ended 12/31/14 | | One Year | | | Since Inception | | | Inception Date |

| | Class A | | | -3.05 | % | | | 1.21 | % | | 4/30/13 |

| | Class C | | | -0.17 | | | | 3.85 | | | 4/30/13 |

| | Institutional | | | 3.00 | | | | 5.03 | | | 4/30/13 |

| | Class IR | | | 2.85 | | | | 4.94 | | | 4/30/13 |

| | | Class R | | | 2.30 | | | | 4.36 | | | 4/30/13 |

| | 4 | | The Standardized Average Annual Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.50% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Class IR and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

8

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS5 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 2.68 | % | | | 4.12 | % |

| | Class C | | | 3.43 | | | | 4.87 | |

| | Institutional | | | 2.28 | | | | 3.72 | |

| | Class IR | | | 2.43 | | | | 3.87 | |

| | | Class R | | | 2.92 | | | | 4.36 | |

| | 5 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least April 30, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | |

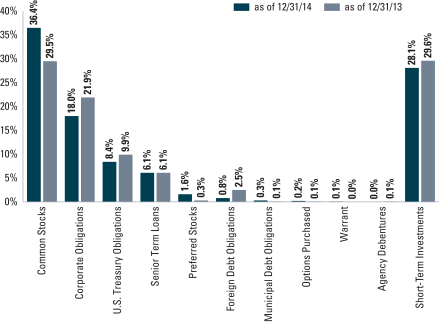

| FUND COMPOSITION (%) |

| As of December 31, 2014 | | |

| | | | The percentage shown for each investment category reflects the value of investments in that category as a percentage of the Fund’s market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. Short-term investments represent investment companies and repurchase agreements. |

9

FUND BASICS

| | | | | | | | |

| | TOP TEN EQUITY HOLDINGS AS OF 12/31/146 |

| | | Holding | | % of Net Assets | | | Line of Business |

| | Northstar Realty Finance Corp. | | | 1.0 | % | | Real Estate Investment Trusts |

| | CVS Health Corp. | | | 0.9 | | | Food & Staples Retailing |

| | Oracle Corp. | | | 0.8 | | | Software |

| | Aon PLC | | | 0.8 | | | Insurance |

| | American International Group, Inc. | | | 0.7 | | | Insurance |

| | NextEra Energy, Inc. | | | 0.7 | | | Electric Utilities |

| | Ally Financial, Inc. | | | 0.7 | | | Consumer Finance |

| | Cedar Fair L.P. | | | 0.7 | | | Hotels, Restaurants & Leisure |

| | Ashland, Inc. | | | 0.6 | | | Chemicals |

| | | Microsoft Corp. | | | 0.6 | | | Software |

| | 6 | | The top 10 holdings may not be representative of the Fund’s future investments. |

| | | | | | |

| | UNDERLYING MANAGER ALLOCATION (%)7 | |

| | | As of December 31, 2014 | | | |

| | Ares Capital Management, LLC | | | 13.8 | |

| | Halcyon Liquid IC Strategies Management, L.P. | | | 16.4 | |

| | Brigade Capital Management, L.P. | | | 12.2 | |

| | Sirios Capital Management, L.P. | | | 8.8 | |

| | First Pacific Advisors, LLC | | | 16.3 | |

| | Lateef Investment Management, L.P. | | | 3.2 | |

| | Polaris Capital Management, LLC | | | 5.5 | |

| | GAM International Management Ltd | | | 8.2 | |

| | | Graham Capital Management, L.P. | | | 15.8 | |

| | 7 | | The charts above only represent capital allocated to the Underlying Managers, as a percentage of net assets, and as such the weightings may not sum to 100%. |

10

FUND BASICS

| | | | |

| | STRATEGY ALLOCATION (%)8 |

| | | As of December 31, 2014 | | |

| |

| | |  |

| | | | Equity Long/Short Strategies generally involve long and short investing, based on fundamental evaluations, research and various analytical measurements, in equity and equity-related investments. Dynamic Equity Strategies generally are long-biased strategies that are less constrained than traditional long-only managers with respect to factors such as position concentration, sector and country weights, style, and market capitalization. Event Driven and Credit Strategies typically seek to take advantage of corporate events and company-specific catalysts such as bankruptcies, mergers or takeovers. Opportunistic Fixed Income Strategies seek to maintain diversified exposure across various fixed income and floating rate market segments, including, among others, global emerging markets, investment grade and high yield debt markets, convertible bonds, and bank loans. Tactical Trading Strategies seek to produce total return by long and short investing across global fixed income, currency, equity, and commodity markets. Tactical Trading managers typically have no bias to be long, short, or neutral. |

| | 8 | | The chart above only represents capital allocated to the Underlying Managers, as a percentage of net assets, and as such the weightings may not sum to 100%. |

11

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

Performance Summary

December 31, 2014

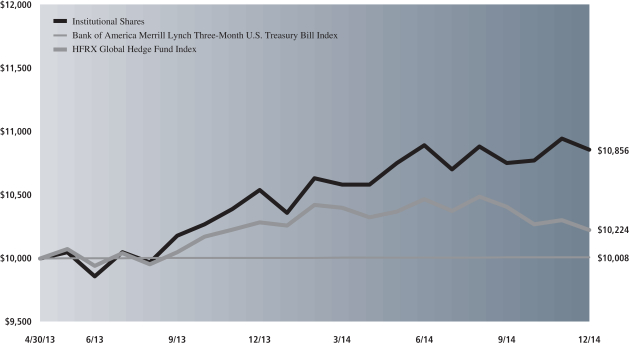

The following graph shows the value, as of December 31, 2014, of a $10,000 investment made on April 30, 2013 (commencement of operations) in Institutional Shares at NAV. For comparative purposes, the performance of the Fund’s current benchmarks, the Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index and the HFRX Global Hedge Fund Index, are shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class C, Class IR and Class R Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

|

| Multi-Manager Alternatives Fund’s Lifetime Performance |

Performance of a $10,000 Investment, with distributions reinvested, from April 30, 2013 through December 31, 2014.

| | | | | | |

| Average Annual Total Return through December 31, 2014 | | | One Year | | | Since Inception |

Class A (Commenced April 30, 2013) | | | | | | |

Excluding sales charges | | | 2.61% | | | 4.67% |

Including sales charges | | | -3.05% | | | 1.21% |

| | | | | | |

Class C (Commenced April 30, 2013) | | | | | | |

Excluding contingent deferred sales charges | | | 1.84% | | | 3.85% |

Including contingent deferred sales charges | | | -0.17% | | | 3.85% |

| | | | | | |

Institutional (Commenced April 30, 2013) | | | 3.00% | | | 5.03% |

| | | | | | |

Class IR (Commenced April 30, 2013) | | | 2.85% | | | 4.94% |

| | | | | | |

Class R (Commenced April 30, 2013) | | | 2.30% | | | 4.36% |

| | | | | | |

12

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

Schedule of Investments

December 31, 2014

| | | | | | | | |

| Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – 38.9% | |

| | Aerospace & Defense – 0.9% | |

| | 62,332 | | | Airbus Group NV | | $ | 3,081,569 | |

| | 202,400 | | | Meggitt PLC | | | 1,628,155 | |

| | 4,432 | | | Precision Castparts Corp.(a) | | | 1,067,580 | |

| | 12,800 | | | United Technologies Corp. | | | 1,472,000 | |

| | | | | | | | |

| | | | | | | 7,249,304 | |

| | |

| | Auto Components – 0.1% | |

| | 9,400 | | | Cie Generale des Etablissements Michelin | | | 848,507 | |

| | |

| | Beverages – 1.2% | | | | |

| | 25,000 | | | Anheuser Busch InBev NV ADR | | | 2,808,000 | |

| | 26,600 | | | Asahi Group Holdings Ltd. | | | 822,932 | |

| | 16,300 | | | Carlsberg A/S Class B | | | 1,251,838 | |

| | 53,572 | | | Constellation Brands, Inc. Class A*(a) | | | 5,259,163 | |

| | | | | | | | |

| | | | | | | 10,141,933 | |

| | |

| | Biotechnology* – 0.6% | |

| | 13,898 | | | Celgene Corp. | | | 1,554,630 | |

| | 13,110 | | | Cubist Pharmaceuticals, Inc. | | | 1,319,522 | |

| | 20,320 | | | Gilead Sciences, Inc.(a) | | | 1,915,363 | |

| | | | | | | | |

| | | | | | | 4,789,515 | |

| | |

| | Capital Markets – 0.4% | |

| | 813 | | | Affiliated Managers Group, Inc.* | | | 172,551 | |

| | 76,612 | | | NorthStar Asset Management Group, Inc.(a) | | | 1,729,133 | |

| | 15,567 | | | T. Rowe Price Group, Inc. | | | 1,336,583 | |

| | | | | | | | |

| | | | | | | 3,238,267 | |

| | |

| | Chemicals – 1.9% | |

| | 44,366 | | | Ashland, Inc.(a) | | | 5,313,272 | |

| | 9,900 | | | BASF SE | | | 830,421 | |

| | 18,000 | | | LANXESS AG | | | 833,621 | |

| | 14,600 | | | Methanex Corp. | | | 670,685 | |

| | 39,984 | | | Rockwood Holdings, Inc.(a) | | | 3,150,739 | |

| | 569,000 | | | Showa Denko KK | | | 700,444 | |

| | 6,400 | | | Solvay SA | | | 866,016 | |

| | 15,500 | | | Symrise AG | | | 933,799 | |

| | 4,031 | | | The Sherwin-Williams Co.(a) | | | 1,060,314 | |

| | 21,700 | | | Yara International ASA | | | 966,353 | |

| | | | | | | | |

| | | | | | | 15,325,664 | |

| | |

| | Commercial Banks – 2.1% | |

| | 265,098 | | | Bank of America Corp.(a) | | | 4,742,603 | |

| | 23,000 | | | CIT Group, Inc. | | | 1,100,090 | |

| | 51,600 | | | Citigroup, Inc. | | | 2,792,076 | |

| | 50,541 | | | Comerica, Inc.(a) | | | 2,367,340 | |

| | 47,400 | | | DNB ASA | | | 699,180 | |

| | 10,573 | | | JPMorgan Chase & Co. | | | 661,658 | |

| | 112,100 | | | Sberbank of Russia ADR | | | 452,895 | |

| | 20,814 | | | Signature Bank*(a) | | | 2,621,731 | |

| | 95,600 | | | SpareBank 1 SR Bank ASA | | | 673,420 | |

| | 50,700 | | | Standard Chartered PLC | | | 758,264 | |

| | 18,300 | | | Svenska Handelsbanken AB | | | 856,218 | |

| | | | | | | | |

| | | | | | | 17,725,475 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Commercial Services & Supplies – 0.3% | |

| | 54,500 | | | Caverion Corp. | | $ | 436,896 | |

| | 31,800 | | | Loomis AB Class B | | | 918,626 | |

| | 23,968 | | | Tyco International PLC | | | 1,051,236 | |

| | | | | | | | |

| | | | | | | 2,406,758 | |

| | |

| | Communications Equipment – 0.8% | |

| | 38,600 | | | ARRIS Group, Inc.* | | | 1,165,334 | |

| | 128,800 | | | Cisco Systems, Inc. | | | 3,582,572 | |

| | 25,200 | | | QUALCOMM, Inc. | | | 1,873,116 | |

| | | | | | | | |

| | | | | | | 6,621,022 | |

| | |

| | Computers & Peripherals – 0.2% | |

| | 749 | | | Samsung Electronics Co. Ltd. | | | 900,481 | |

| | 17,400 | | | Wincor Nixdorf AG | | | 840,283 | |

| | | | | | | | |

| | | | | | | 1,740,764 | |

| | |

| | Construction & Engineering – 0.2% | |

| | 276,220 | | | Trevi Finanziaria Industriale SpA | | | 940,017 | |

| | 65,400 | | | YIT OYJ | | | 338,451 | |

| | | | | | | | |

| | | | | | | 1,278,468 | |

| | |

| | Construction Materials – 0.2% | |

| | 35,600 | | | CRH PLC | | | 856,019 | |

| | 12,200 | | | Imerys SA | | | 897,565 | |

| | | | | | | | |

| | | | | | | 1,753,584 | |

| | |

| | Consumer Finance(a) – 0.7% | |

| | 81,655 | | | Ally Financial, Inc.* | | | 1,928,691 | |

| | 61,715 | | | Discover Financial Services | | | 4,041,715 | |

| | | | | | | | |

| | | | | | | 5,970,406 | |

| | |

| | Containers & Packaging – 0.9% | |

| | 147,547 | | | Berry Plastics Group, Inc.*(a) | | | 4,655,108 | |

| | 73,900 | | | Owens-Illinois, Inc.* | | | 1,994,561 | |

| | 114,400 | | | Rexam PLC | | | 805,375 | |

| | | | | | | | |

| | | | | | | 7,455,044 | |

| | |

| | Diversified Consumer Services(a) – 0.1% | |

| | 33,311 | | | Service Corp. | | | 756,160 | |

| | |

| | Diversified Financial Services – 0.7% | |

| | 177,526 | | | FNFV Group* | | | 2,794,259 | |

| | 28,100 | | | Groupe Bruxelles Lambert SA | | | 2,397,499 | |

| | 25,400 | | | Investor AB | | | 923,488 | |

| | | | | | | | |

| | | | | | | 6,115,246 | |

| | |

| | Diversified Telecommunication Services – 0.3% | |

| | 51,200 | | | Deutsche Telekom AG | | | 819,217 | |

| | 29,422 | | | Verizon Communications, Inc.(a) | | | 1,376,361 | |

| | | | | | | | |

| | | | | | | 2,195,578 | |

| | |

| | Electric Utilities(a) – 0.7% | |

| | 56,035 | | | NextEra Energy, Inc. | | | 5,955,960 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 13 |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

Schedule of Investments (continued)

December 31, 2014

| | | | | | | | |

| Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Electrical Equipment – 0.4% | |

| | 15,292 | | | Acuity Brands, Inc.(a) | | $ | 2,141,950 | |

| | 29,822 | | | AMETEK, Inc. | | | 1,569,532 | |

| | | | | | | | |

| | | | | | | 3,711,482 | |

| | |

| | Electronic Equipment, Instruments & Components – 0.5% | |

| | 44,100 | | | TE Connectivity Ltd. | | | 2,789,325 | |

| | 37,442 | | | Trimble Navigation Ltd.* | | | 993,711 | |

| | | | | | | | |

| | | | | | | 3,783,036 | |

| | |

| | Energy Equipment & Services(a) – 0.2% | |

| | 3,976 | | | Dresser-Rand Group, Inc.* | | | 325,237 | |

| | 24,767 | | | Halliburton Co. | | | 974,086 | |

| | | | | | | | |

| | | | | | | 1,299,323 | |

| | |

| | Food & Staples Retailing – 1.2% | |

| | 77,400 | | | CVS Health Corp. | | | 7,454,394 | |

| | 29,200 | | | Walgreens Boots Alliance, Inc. | | | 2,225,040 | |

| | | | | | | | |

| | | | | | | 9,679,434 | |

| | |

| | Food Products – 0.5% | |

| | 191,600 | | | Greencore Group PLC | | | 851,062 | |

| | 9,800 | | | MEIJI Holdings Co. Ltd. | | | 891,596 | |

| | 152,700 | | | Orkla ASA | | | 1,039,500 | |

| | 33,900 | | | Unilever NV | | | 1,326,090 | |

| | | | | | | | |

| | | | | | | 4,108,248 | |

| | |

| | Health Care Equipment & Supplies(a) – 0.8% | |

| | 16,178 | | | Becton Dickinson & Co. | | | 2,251,330 | |

| | 39,453 | | | Covidien PLC | | | 4,035,253 | |

| | | | | | | | |

| | | | | | | 6,286,583 | |

| | |

| | Health Care Providers & Services – 1.4% | |

| | 126,635 | | | Brookdale Senior Living, Inc.*(a) | | | 4,643,705 | |

| | 29,100 | | | Express Scripts Holding Co.* | | | 2,463,897 | |

| | 6,158 | | | HCA Holdings, Inc.* | | | 451,935 | |

| | 81,641 | | | Synergy Health PLC | | | 2,647,490 | |

| | 9,480 | | | Universal Health Services, Inc. Class B(a) | | | 1,054,745 | |

| | | | | | | | |

| | | | | | | 11,261,772 | |

| | |

| | Hotels, Restaurants & Leisure – 2.1% | |

| | 177,816 | | | Amaya, Inc.* | | | 4,369,639 | |

| | 15,439 | | | Carnival Corp. | | | 699,850 | |

| | 122,970 | | | Cedar Fair LP(a) | | | 5,881,655 | |

| | 462,100 | | | Genting Malaysia Bhd | | | 536,600 | |

| | 46,800 | | | Lottomatica SpA | | | 1,044,989 | |

| | 166,981 | | | Morgans Hotel Group Co.*(a) | | | 1,309,131 | |

| | 8,262 | | | Restaurant Brands International, Inc.*(a) | | | 322,553 | |

| | 2,904,882 | | | REXLot Holdings Ltd. | | | 233,777 | |

| | 9,871 | | | The Habit Restaurants, Inc. Class A* | | | 319,327 | |

| | 165,853 | | | The Intertain Group Ltd. | | | 1,885,796 | |

| | 7,695 | | | Wynn Resorts Ltd. | | | 1,144,708 | |

| | | | | | | | |

| | | | | | | 17,748,025 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Household Durables – 0.7% | |

| | 132,245 | | | Barratt Developments PLC | | $ | 962,495 | |

| | 31,300 | | | Bellway PLC | | | 938,739 | |

| | 54,500 | | | Duni AB | | | 807,177 | |

| | 38,400 | | | Persimmon PLC* | | | 937,877 | |

| | 460,100 | | | Taylor Wimpey PLC | | | 981,584 | |

| | 6,435 | | | Whirlpool Corp.(a) | | | 1,246,717 | |

| | | | | | | | |

| | | | | | | 5,874,589 | |

| | |

| | Household Products – 0.2% | |

| | 13,000 | | | Henkel AG & Co. KGaA | | | 1,259,290 | |

| | |

| | Independent Power Producers & Energy Traders(a) – 0.1% | |

| | 34,767 | | | TerraForm Power, Inc. Class A | | | 1,073,605 | |

| | |

| | Industrial Conglomerates – 0.3% | |

| | 19,431 | | | Danaher Corp. | | | 1,665,431 | |

| | 18,200 | | | Jardine Matheson Holdings Ltd. | | | 720,666 | |

| | 700 | | | Jardine Strategic Holdings Ltd. | | | 23,681 | |

| | | | | | | | |

| | | | | | | 2,409,778 | |

| | |

| | Insurance – 2.1% | |

| | 2,970 | | | Alleghany Corp.* | | | 1,376,595 | |

| | 108,855 | | | American International Group, Inc. | | | 6,096,969 | |

| | 67,908 | | | Aon PLC | | | 6,439,716 | |

| | 10,500 | | | Hannover Rueck SE | | | 947,219 | |

| | 4,400 | | | Muenchener Rueckversicherungs AG | | | 876,204 | |

| | 49,322 | | | The Progressive Corp. | | | 1,331,201 | |

| | | | | | | | |

| | | | | | | 17,067,904 | |

| | |

| | Internet & Catalog Retail*(a) – 0.5% | |

| | 136,653 | | | Liberty Interactive Corp. Class A | | | 4,020,331 | |

| | |

| | Internet Software & Services* – 0.9% | |

| | 3,857 | | | Google, Inc. Class A(a) | | | 2,046,756 | |

| | 2,059 | | | Google, Inc. Class C | | | 1,083,857 | |

| | 89,670 | | | Yahoo!, Inc.(a) | | | 4,529,232 | |

| | | | | | | | |

| | | | | | | 7,659,845 | |

| | |

| | IT Services – 0.2% | |

| | 13,289 | | | Accenture PLC Class A | | | 1,186,841 | |

| | 26,000 | | | Infosys Ltd. ADR | | | 817,960 | |

| | | | | | | | |

| | | | | | | 2,004,801 | |

| | |

| | Life Sciences Tools & Services – 0.4% | |

| | 29,400 | | | Thermo Fisher Scientific, Inc. | | | 3,683,526 | |

| | |

| | Machinery – 1.4% | |

| | 52,627 | | | EnPro Industries, Inc.*(a) | | | 3,302,871 | |

| | 20,500 | | | Joy Global, Inc. | | | 953,660 | |

| | 20,300 | | | Kone Oyj Class B | | | 924,213 | |

| | 29,200 | | | Konecranes Oyj | | | 834,979 | |

| | 24,064 | | | SPX Corp.(a) | | | 2,067,579 | |

| | 13,164 | | | Stanley Black & Decker, Inc. | | | 1,264,797 | |

| | 10,400 | | | Sulzer AG | | | 1,112,500 | |

| | 14,601 | | | Wabtec Corp. | | | 1,268,681 | |

| | | | | | | | |

| | | | | | | 11,729,280 | |

| | |

| | |

| 14 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

| | | | | | | | |

| Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Media – 2.3% | |

| | 39,649 | | | DISH Network Corp. Class A* | | $ | 2,890,015 | |

| | 22,400 | | | IPSOS | | | 642,798 | |

| | 27,467 | | | Liberty Global PLC Series C*(a) | | | 1,326,931 | |

| | 17,140 | | | Naspers Ltd. | | | 2,217,147 | |

| | 13,277 | | | Scripps Networks Interactive Class A | | | 999,360 | |

| | 112,100 | | | The Interpublic Group of Cos., Inc. | | | 2,328,317 | |

| | 36,950 | | | Time Warner, Inc.(a) | | | 3,156,269 | |

| | 36,079 | | | Twenty-First Century Fox, Inc. Class A | | | 1,385,614 | |

| | 21,783 | | | Viacom, Inc. Class B(a) | | | 1,639,171 | |

| | 118,400 | | | WPP PLC | | | 2,461,733 | |

| | | | | | | | |

| | | | | | | 19,047,355 | |

| | |

| | Metals & Mining – 0.6% | |

| | 201,600 | | | Alcoa, Inc. | | | 3,183,264 | |

| | 18,800 | | | BHP Billiton PLC ADR | | | 808,400 | |

| | 23,400 | | | MMC Norilsk Nickel OJSC ADR | | | 332,748 | |

| | 163,650 | | | Norsk Hydro ASA | | | 921,846 | |

| | | | | | | | |

| | | | | | | 5,246,258 | |

| | |

| | Multiline Retail – 0.3% | |

| | 124,951 | | | Hudson’s Bay Co. | | | 2,641,415 | |

| | |

| | Oil, Gas & Consumable Fuels – 1.4% | |

| | 7,700 | | | California Resources Corp.* | | | 42,427 | |

| | 63,300 | | | Canadian Natural Resources Ltd. | | | 1,954,704 | |

| | 65,900 | | | Etablissements Maurel et Prom* | | | 615,892 | |

| | 87,300 | | | Gazprom OAO ADR | | | 395,469 | |

| | 10,200 | | | Lukoil OAO ADR | | | 401,009 | |

| | 30,200 | | | Occidental Petroleum Corp. | | | 2,434,422 | |

| | 36,400 | | | Rosneft OAO GDR | | | 127,764 | |

| | 17,500 | | | Sasol Ltd. | | | 653,150 | |

| | 19,740 | | | SemGroup Corp. Class A(a) | | | 1,350,019 | |

| | 713,600 | | | Thai Oil PCL | | | 908,049 | |

| | 44,146 | | | The Williams Cos., Inc.(a) | | | 1,983,921 | |

| | 126,100 | | | Tullow Oil PLC | | | 812,633 | |

| | | | | | | | |

| | | | | | | 11,679,459 | |

| | |

| | Pharmaceuticals – 1.0% | |

| | 23,649 | | | Hospira, Inc.* | | | 1,448,501 | |

| | 14,102 | | | Merck & Co., Inc.(a) | | | 800,852 | |

| | 9,400 | | | Novartis AG | | | 871,789 | |

| | 15,800 | | | Teva Pharmaceutical Industries Ltd. ADR | | | 908,658 | |

| | 19,555 | | | Valeant Pharmaceuticals International, Inc.* | | | 2,798,516 | |

| | 31,220 | | | Zoetis, Inc. | | | 1,343,397 | |

| | | | | | | | |

| | | | | | | 8,171,713 | |

| | |

| | Professional Services – 0.5% | |

| | 21,909 | | | Nielsen Holdings NV | | | 979,990 | |

| | 21,754 | | | Robert Half International, Inc. | | | 1,269,998 | |

| | 15,198 | | | Towers Watson & Co. Class A | | | 1,719,958 | |

| | | | | | | | |

| | | | | | | 3,969,946 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Real Estate Investment Trusts – 2.9% | |

| | 45,766 | | | Colony Financial, Inc.(a) | | $ | 1,090,146 | |

| | 764,337 | | | Gramercy Property Trust, Inc. | | | 5,273,925 | |

| | 84,659 | | | iStar Financial, Inc. Series D | | | 2,116,475 | |

| | 92,314 | | | iStar Financial, Inc. Series E | | | 2,280,156 | |

| | 93,122 | | | Lamar Advertising Co. Class A(a) | | | 4,995,064 | |

| | 454,547 | | | Northstar Realty Finance Corp.(a) | | | 7,990,936 | |

| | | | | | | | |

| | | | | | | 23,746,702 | |

| | |

| | Real Estate Management & Development – 0.1% | |

| | 6,992 | | | Jones Lang LaSalle, Inc. | | | 1,048,311 | |

| | |

| | Road & Rail – 0.6% | |

| | 15,064 | | | Hertz Global Holdings, Inc.* | | | 375,696 | |

| | 3,446 | | | J.B. Hunt Transport Services, Inc. | | | 290,326 | |

| | 2,842 | | | Kansas City Southern | | | 346,809 | |

| | 21,229 | | | Old Dominion Freight Line, Inc.*(a) | | | 1,648,220 | |

| | 16,101 | | | Saia, Inc.*(a) | | | 891,351 | |

| | 13,175 | | | Union Pacific Corp.(a) | | | 1,569,538 | |

| | | | | | | | |

| | | | | | | 5,121,940 | |

| | |

| | Semiconductors & Semiconductor Equipment – 0.6% | |

| | 44,900 | | | Analog Devices, Inc. | | | 2,492,848 | |

| | 37,300 | | | Intel Corp. | | | 1,353,617 | |

| | 2,843 | | | MModal, Inc. | | | 22,798 | |

| | 50,159 | | | SunEdison, Inc.*(a) | | | 978,602 | |

| | | | | | | | |

| | | | | | | 4,847,865 | |

| | |

| | Software – 1.4% | |

| | 113,800 | | | Microsoft Corp. | | | 5,286,010 | |

| | 143,500 | | | Oracle Corp. | | | 6,453,195 | |

| | | | | | | | |

| | | | | | | 11,739,205 | |

| | |

| | Specialty Retail(a) – 0.1% | |

| | 21,755 | | | Penske Automotive Group, Inc. | | | 1,067,518 | |

| | |

| | Textiles, Apparel & Luxury Goods – 0.1% | |

| | 4,900 | | | Christian Dior SA | | | 838,576 | |

| | 276 | | | Hermes International | | | 98,279 | |

| | | | | | | | |

| | | | | | | 936,855 | |

| | |

| | Transportation Infrastructure – 0.1% | |

| | 103,618 | | | BBA Aviation PLC | | | 579,079 | |

| | |

| | Water Utilities – 0.1% | |

| | 438,000 | | | Guangdong Investment Ltd. | | | 570,471 | |

| | |

| | Wireless Telecommunication Services – 0.6% | |

| | 29,000 | | | Freenet AG | | | 824,536 | |

| | 13,500 | | | KDDI Corp. | | | 848,124 | |

| | 83,354 | | | T-Mobile US, Inc.*(a) | | | 2,245,557 | |

| | 29,200 | | | Vodafone Group PLC ADR | | | 997,764 | |

| | | | | | | | |

| | | | | | | 4,915,981 | |

| | |

| | TOTAL COMMON STOCKS | |

| | (Cost $303,289,644) | | $ | 321,558,580 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 15 |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

Schedule of Investments (continued)

December 31, 2014

| | | | | | | | | | | | | | |

Principal Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – 19.2% | |

| | Aerospace & Defense – 0.3% | |

| Alliant Techsystems, Inc.(b)(c) | |

| $ | 200,000 | | | | 5.250 | % | | | 10/01/21 | | | $ | 197,500 | |

| Bombardier, Inc.(b) | |

| | 500,000 | | | | 4.750 | | | | 04/15/19 | | | | 495,625 | |

| | 500,000 | | | | 6.000 | (c) | | | 10/15/22 | | | | 505,000 | |

| Moog, Inc.(b)(c) | |

| | 273,000 | | | | 5.250 | | | | 12/01/22 | | | | 276,413 | |

| Oshkosh Corp.(c) | |

| | 300,000 | | | | 5.375 | | | | 03/01/22 | | | | 305,250 | |

| Spirit AeroSystems, Inc.(c) | |

| | 510,000 | | | | 5.250 | | | | 03/15/22 | | | | 515,737 | |

| TransDigm, Inc.(c) | |

| | 320,000 | | | | 6.000 | | | | 07/15/22 | | | | 320,000 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 2,615,525 | |

| | |

| | Airlines(b) – 0.0% | |

| Air Canada | |

| | 335,000 | | | | 7.750 | | | | 04/15/21 | | | | 349,656 | |

| | |

| | Automotive – 0.2% | |

| Affinia Group, Inc.(c) | |

| | 85,000 | | | | 7.750 | | | | 05/01/21 | | | | 87,337 | |

| Faurecia | |

| EUR | 297,500 | | | | 3.250 | | | | 01/01/18 | | | | 117,969 | |

| General Motors Co. | |

| $ | 80,000 | | | | 3.500 | | | | 10/02/18 | | | | 81,600 | |

| Gestamp Funding Luxembourg SA(b)(c) | |

| | 250,000 | | | | 5.625 | | | | 05/31/20 | | | | 252,500 | |

| Schaeffler Finance BV(b)(c) | |

| | 221,000 | | | | 4.250 | | | | 05/15/21 | | | | 217,685 | |

| Schaeffler Holding Finance BV(b)(c)(d) | |

| | 625,000 | | | | 6.750 | | | | 11/15/22 | | | | 653,125 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,410,216 | |

| | |

| | Banks – 1.7% | |

| AmBank M Bhd | |

| | 200,000 | | | | 3.125 | | | | 07/03/19 | | | | 200,490 | |

| Bangkok Bank PCL | |

| | 200,000 | | | | 3.300 | | | | 10/03/18 | | | | 204,623 | |

| CaixaBank SA | |

| EUR | 100,000 | | | | 4.500 | | | | 11/22/16 | | | | 109,122 | |

| Citigroup, Inc.(e) | |

| $ | 700,000 | | | | 0.933 | | | | 11/24/17 | | | | 700,174 | |

| Credit Suisse New York | |

| | 500,000 | | | | 3.000 | | | | 10/29/21 | | | | 497,676 | |

| | 1,000,000 | | | | 3.625 | | | | 09/09/24 | | | | 1,018,086 | |

| HSBC USA, Inc.(e) | |

| | 800,000 | | | | 0.843 | | | | 11/13/19 | | | | 799,978 | |

| ING Bank NV(b) | |

| | 200,000 | | | | 1.375 | | | | 03/07/16 | | | | 200,719 | |

| | 800,000 | | | | 0.925 | (e) | | | 10/01/19 | | | | 801,112 | |

| JPMorgan Chase & Co. | |

| | 500,000 | | | | 2.200 | | | | 10/22/19 | | | | 494,893 | |

| JPMorgan Chase Bank NA(c)(e) | |

| EUR | 600,000 | | | | 0.784 | | | | 05/31/17 | | | | 724,434 | |

| JPMorgan Chase Capital XXI(c)(e) | |

| $ | 320,000 | | | | 1.182 | | | | 02/02/37 | | | | 262,400 | |

| | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Banks – (continued) | |

| JPMorgan Chase Capital XXIII(c)(e) | |

| $ | 110,000 | | | | 1.232 | % | | | 05/15/47 | | | $ | 89,100 | |

| Lloyds Bank PLC(c)(e) | |

| | 90,000 | | | | 0.600 | | | | 06/29/49 | | | | 59,580 | |

| | 270,000 | | | | 0.438 | | | | 11/29/49 | | | | 178,740 | |

| Lloyds Banking Group PLC(b)(c)(e) | |

| | 245,000 | | | | 6.657 | | | | 05/21/49 | | | | 261,538 | |

| | 100,000 | | | | 6.413 | | | | 10/01/49 | | | | 106,500 | |

| Lloyds TSB Bank PLC | |

| | 300,000 | | | | 6.375 | | | | 01/21/21 | | | | 359,465 | |

| Macquarie Bank Ltd. | |

| | 461,000 | | | | 5.000 | | | | 02/22/17 | | | | 491,705 | |

| | 300,000 | | | | 1.045 | (b)(e) | | | 03/24/17 | | | | 301,301 | |

| Royal Bank of Canada | |

| | 110,000 | | | | 1.200 | | | | 09/19/17 | | | | 109,322 | |

| Royal Bank of Scotland PLC | |

| | 250,000 | | | | 2.550 | | | | 09/18/15 | | | | 252,503 | |

| | 340,000 | | | | 7.648 | (c)(e) | | | 08/29/49 | | | | 396,100 | |

| Santander International Debt SA | |

| GBP | 200,000 | | | | 3.160 | | | | 12/01/15 | | | | 316,337 | |

| Standard Chartered PLC(b) | |

| $ | 150,000 | | | | 3.850 | | | | 04/27/15 | | | | 151,432 | |

| State Street Capital Trust IV(c)(e) | |

| | 40,000 | | | | 1.241 | | | | 06/01/77 | | | | 33,200 | |

| UBS AG(e) | |

| | 750,000 | | | | 0.873 | | | | 08/14/19 | | | | 752,351 | |

| Wachovia Capital Trust III(c)(e) | |

| | 170,000 | | | | 5.570 | | | | 03/29/49 | | | | 164,135 | |

| Washington Mutual Bank(f) | |

| | 10,000,000 | | | | 0.000 | | | | 11/06/09 | | | | 2,750,000 | |

| | 3,000,000 | | | | 0.000 | | | | 06/16/10 | | | | 825,000 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 13,612,016 | |

| | |

| | Brokerage – 0.2% | |

| Morgan Stanley, Inc. | |

| | 800,000 | | | | 0.975 | (e) | | | 01/05/18 | | | | 800,203 | |

| | 400,000 | | | | 3.875 | | | | 04/29/24 | | | | 410,428 | |

| | 500,000 | | | | 3.700 | | | | 10/23/24 | | | | 506,404 | |

| The Bear Stearns Cos. LLC(e) | |

| | 200,000 | | | | 0.621 | | | | 11/21/16 | | | | 199,511 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,916,546 | |

| | |

| | Building Materials – 0.1% | |

| Cemex SAB de CV(b)(c) | |

| | 200,000 | | | | 7.250 | | | | 01/15/21 | | | | 211,000 | |

| Gibraltar Industries, Inc.(c) | |

| | 600,000 | | | | 6.250 | | | | 02/01/21 | | | | 612,000 | |

| Norbord, Inc.(b) | |

| | 300,000 | | | | 5.375 | | | | 12/01/20 | | | | 292,246 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,115,246 | |

| | |

| | Chemicals – 0.2% | | | | | | | | | | | | | |

| Cornerstone Chemical Co.(b)(c) | |

| | 465,000 | | | | 9.375 | | | | 03/15/18 | | | | 474,300 | |

| Momentive Performance Materials, Inc.(c) | |

| | 750,000 | | | | 3.880 | | | | 10/24/21 | | | | 633,750 | |

| | |

| | |

| 16 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

| | | | | | | | | | | | | | |

Principal Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Chemicals – (continued) | |

| MPM Escrow LLC | |

| $ | 750,000 | | | | 8.875 | % | | | 10/15/20 | | | $ | — | |

| Rain CII Carbon LLC/CII Carbon Corp.(b)(c) | |

| | 770,000 | | | | 8.250 | | | | 01/15/21 | | | | 787,325 | |

| SPCM SA(b)(c) | |

| | 49,000 | | | | 6.000 | | | | 01/15/22 | | | | 50,960 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,946,335 | |

| | |

| | Commercial Services – 0.0% | |

| RAG-Stiftung(g) | |

| EUR | 100,000 | | | | 0.000 | | | | 12/31/18 | | | | 121,187 | |

| Total System Services, Inc.(c) | |

| $ | 100,000 | | | | 3.750 | | | | 06/01/23 | | | | 97,709 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 218,896 | |

| | |

| | Consumer Cyclical Services – 0.8% | |

| APX Group, Inc.(c) | |

| | 65,000 | | | | 6.375 | | | | 12/01/19 | | | | 61,912 | |

| | 30,000 | | | | 8.750 | (b) | | | 12/01/20 | | | | 25,575 | |

| | 1,340,000 | | | | 8.750 | | | | 12/01/20 | | | | 1,142,350 | |

| Aramark Services, Inc.(c) | |

| | 1,000,000 | | | | 5.750 | | | | 03/15/20 | | | | 1,032,500 | |

| Ashtead Capital, Inc.(b)(c) | |

| | 115,000 | | | | 6.500 | | | | 07/15/22 | | | | 123,050 | |

| Ceridian HCM Holding, Inc.(b)(c) | |

| | 250,000 | | | | 11.000 | | | | 03/15/21 | | | | 272,500 | |

| First Data Corp.(b)(c) | |

| | 860,000 | | | | 6.750 | | | | 11/01/20 | | | | 922,350 | |

| Iron Mountain, Inc.(c) | |

| | 989,000 | | | | 5.750 | | | | 08/15/24 | | | | 989,000 | |

| Monitronics International, Inc.(c) | |

| | 870,000 | | | | 9.125 | | | | 04/01/20 | | | | 824,325 | |

| Multi-Color Corp.(b)(c) | |

| | 1,000,000 | | | | 6.125 | | | | 12/01/22 | | | | 997,500 | |

| The ADT Corp. | |

| | 160,000 | | | | 6.250 | | | | 10/15/21 | | | | 164,800 | |

| United Rentals North America, Inc.(c) | |

| | 90,000 | | | | 7.375 | | | | 05/15/20 | | | | 97,200 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 6,653,062 | |

| | |

| | Consumer Noncyclical – 0.1% | |

| BAT International Finance PLC | |

| | 200,000 | | | | 1.125 | | | | 03/29/16 | | | | 200,147 | |

| NeuStar, Inc.(c) | |

| | 291,000 | | | | 4.500 | | | | 01/15/23 | | | | 250,988 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 451,135 | |

| | |

| | Consumer Products – Household & Leisure(c) – 0.2% | |

| Albea Beauty Holdings SA(b) | |

| | 400,000 | | | | 8.375 | | | | 11/01/19 | | | | 416,000 | |

| American Achievement Corp.(b) | |

| | 890,000 | | | | 10.875 | | | | 04/15/16 | | | | 853,287 | |

| Elizabeth Arden, Inc. | |

| | 713,000 | | | | 7.375 | | | | 03/15/21 | | | | 648,830 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,918,117 | |

| | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Consumer Products – Non Durable(c) – 0.0% | |

| Sally Holdings LLC | |

| $ | 100,000 | | | | 6.875 | % | | | 11/15/19 | | | $ | 106,250 | |

| | |

| | Diversified Financial Services – 0.5% | |

| Alphabet Holding Co., Inc.(c)(d) | |

| | 907,000 | | | | 7.750 | | | | 11/01/17 | | | | 768,682 | |

| Bankrate, Inc.(b)(c) | |

| | 1,500,000 | | | | 6.125 | | | | 08/15/18 | | | | 1,402,500 | |

| Henderson UK Finance PLC | |

| GBP | 100,000 | | | | 7.250 | | | | 03/24/16 | | | | 163,048 | |

| LCR Finance PLC | |

| | 200,000 | | | | 4.500 | | | | 12/07/28 | | | | 390,190 | |

| Magyar Nemzeti Vagyonkezelo Zrt | |

| EUR | 100,000 | | | | 3.375 | | | | 04/02/19 | | | | 122,215 | |

| OHL Investments SA | |

| | 100,000 | | | | 4.000 | | | | 04/25/18 | | | | 113,896 | |

| OneMain Financial Holdings, Inc.(b)(c) | |

| $ | 460,000 | | | | 7.250 | | | | 12/15/21 | | | | 471,500 | |

| Volkswagen International Finance NV | |

| EUR | 200,000 | | | | 5.500 | | | | 11/09/15 | | | | 269,043 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 3,701,074 | |

| | |

| | Energy – 0.3% | |

| American Energy-Permian Basin LLC/AEPB Finance Corp.(b)(c) | |

| $ | 750,000 | | | | 7.125 | | | | 11/01/20 | | | | 555,000 | |

| Basic Energy Services, Inc.(c) | |

| | 100,000 | | | | 7.750 | | | | 02/15/19 | | | | 77,000 | |

| Blue Racer Midstream LLC/Blue Racer Finance Corp.(b)(c) | |

| | 295,000 | | | | 6.125 | | | | 11/15/22 | | | | 283,938 | |

| Chesapeake Energy Corp.(c)(e) | |

| | 100,000 | | | | 3.481 | | | | 04/15/19 | | | | 98,000 | |

| CITGO Petroleum Corp.(b)(c) | |

| | 133,000 | | | | 6.250 | | | | 08/15/22 | | | | 134,995 | |

| EXCO Resources, Inc.(c) | |

| | 665,000 | | | | 8.500 | | | | 04/15/22 | | | | 487,112 | |

| FTS International, Inc.(b)(c) | |

| | 170,000 | | | | 6.250 | | | | 05/01/22 | | | | 122,400 | |

| Pacific Drilling SA(b)(c) | |

| | 70,000 | | | | 5.375 | | | | 06/01/20 | | | | 56,000 | |

| Petrobras International Finance Co. | |

| | 144,000 | | | | 5.375 | | | | 01/27/21 | | | | 133,128 | |

| Seventy Seven Energy, Inc.(c) | |

| | 600,000 | | | | 6.500 | | | | 07/15/22 | | | | 354,000 | |

| Southern Star Central Corp.(b)(c) | |

| | 180,000 | | | | 5.125 | | | | 07/15/22 | | | | 181,800 | |

| Technip SA | |

| EUR | 111,600 | | | | 0.500 | | | | 01/01/16 | | | | 111,990 | |

| YPF SA(b) | |

| $ | 230,000 | | | | 8.750 | | | | 04/04/24 | | | | 228,850 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 2,824,213 | |

| | |

| | Energy – Exploration & Production – 0.8% | |

| Aabar Investments PJSC | |

| EUR | 200,000 | | | | 4.000 | | | | 05/27/16 | | | | 286,491 | |

| Alpha Natural Resources, Inc. | |

| | 100,000 | | | | 3.750 | | | | 12/15/17 | | | | 49,938 | |

| | 825,000 | | | | 6.000 | (c) | | | 06/01/19 | | | | 261,937 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 17 |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

Schedule of Investments (continued)

December 31, 2014

| | | | | | | | | | | | | | |

Principal Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Energy – Exploration & Production – (continued) | |

| CONSOL Energy, Inc.(c) | |

| EUR | 100,000 | | | | 8.250 | % | | | 04/01/20 | | | $ | 104,250 | |

| ENI SpA | |

| | 200,000 | | | | 0.250 | | | | 11/30/15 | | | | 241,115 | |

| EnQuest PLC(b)(c) | |

| $ | 370,000 | | | | 7.000 | | | | 04/15/22 | | | | 215,525 | |

| Halcon Resources Corp.(c) | |

| | 350,000 | | | | 9.750 | | | | 07/15/20 | | | | 264,250 | |

| | 803,000 | | | | 8.875 | | | | 05/15/21 | | | | 604,257 | |

| Harvest Operations Corp. | |

| | 400,000 | | | | 2.125 | | | | 05/14/18 | | | | 397,155 | |

| Ithaca Energy, Inc.(b)(c) | |

| | 200,000 | | | | 8.125 | | | | 07/01/19 | | | | 151,000 | |

| Jupiter Resources, Inc.(b)(c) | |

| | 45,000 | | | | 8.500 | | | | 10/01/22 | | | | 33,750 | |

| Linn Energy LLC/Linn Energy Finance Corp.(c) | |

| | 800,000 | | | | 7.250 | | | | 11/01/19 | | | | 676,000 | |

| MEG Energy Corp.(b)(c) | |

| | 55,000 | | | | 7.000 | | | | 03/31/24 | | | | 50,325 | |

| Memorial Production Partners LP/Memorial Production Finance

Corp.(c) |

|

| | 829,000 | | | | 7.625 | | | | 05/01/21 | | | | 663,200 | |

| | 265,000 | | | | 6.875 | (b) | | | 08/01/22 | | | | 199,412 | |

| Midstates Petroleum Co., Inc./Midstates Petroleum Co. LLC(c) | |

| | 1,243,000 | | | | 10.750 | | | | 10/01/20 | | | | 665,005 | |

| | 100,000 | | | | 9.250 | | | | 06/01/21 | | | | 51,000 | |

| Peabody Energy Corp. | |

| | 350,000 | | | | 6.000 | | | | 11/15/18 | | | | 318,500 | |

| | 300,000 | | | | 6.250 | | | | 11/15/21 | | | | 258,000 | |

| Penn Virginia Resource Partners LP/Penn Virginia Resource

Finance Corp.(c) |

|

| | 200,000 | | | | 6.500 | | | | 05/15/21 | | | | 202,000 | |

| Plains Exploration & Production Co.(c) | |

| | 146,000 | | | | 6.875 | | | | 02/15/23 | | | | 162,425 | |

| SandRidge Energy, Inc.(c) | |

| | 1,095,000 | | | | 7.500 | | | | 02/15/23 | | | | 689,850 | |

| SM Energy Co.(b)(c) | |

| | 117,000 | | | | 6.125 | | | | 11/15/22 | | | | 110,273 | |

| Walter Energy, Inc.(c) | |

| | 40,000 | | | | 9.875 | | | | 12/15/20 | | | | 8,500 | |

| | 125,000 | | | | 8.500 | | | | 04/15/21 | | | | 24,688 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 6,688,846 | |

| | |

| | Energy – Services(b)(c) – 0.1% | |

| Hiland Partners LP/Hiland Partners Finance Corp. | |

| | 400,000 | | | | 7.250 | | | | 10/01/20 | | | | 380,000 | |

| | 625,000 | | | | 5.500 | | | | 05/15/22 | | | | 531,250 | |

| Trinidad Drilling Ltd. | |

| | 100,000 | | | | 7.875 | | | | 01/15/19 | | | | 92,000 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,003,250 | |

| | |

| | Entertainment & Leisure(c) – 0.5% | |

| AMC Entertainment, Inc. | |

| | 500,000 | | | | 5.875 | | | | 02/15/22 | | | | 508,750 | |

| | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Entertainment & Leisure(c) – (continued) | |

| Cedar Fair LP/Canada’s Wonderland Co./Magnum Management

Corp. |

|

| $ | 150,000 | | | | 5.250 | % | | | 03/15/21 | | | $ | 152,625 | |

| | 830,000 | | | | 5.375 | (b) | | | 06/01/24 | | | | 825,850 | |

| Cinemark USA, Inc. | |

| | 1,000,000 | | | | 4.875 | | | | 06/01/23 | | | | 950,000 | |

| Guitar Center, Inc.(b) | |

| | 115,000 | | | | 6.500 | | | | 04/15/19 | | | | 99,763 | |

| | 1,285,000 | | | | 9.625 | | | | 04/15/20 | | | | 857,737 | |

| Regal Entertainment Group | |

| | 400,000 | | | | 5.750 | | | | 03/15/22 | | | | 382,000 | |

| Six Flags Entertainment Corp.(b) | |

| | 500,000 | | | | 5.250 | | | | 01/15/21 | | | | 500,000 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 4,276,725 | |

| | |

| | Environmental(c) – 0.1% | |

| Clean Harbors, Inc. | |

| | 510,000 | | | | 5.125 | | | | 06/01/21 | | | | 507,450 | |

| | |

| | Finance – 1.1% | |

| Ally Financial, Inc. | |

| | 200,000 | | | | 3.500 | | | | 01/27/19 | | | | 197,500 | |

| | 263,000 | | | | 7.500 | | | | 09/15/20 | | | | 308,368 | |

| CIT Group, Inc.(b) | |

| | 100,000 | | | | 5.500 | | | | 02/15/19 | | | | 105,500 | |

| Escrow Lehman Brother Holdings | |

| | 25,000,000 | | | | 1.000 | | | | 09/26/14 | | | | 3,687,500 | |

| | 7,000,000 | | | | 1.000 | | | | 12/30/16 | | | | 1,006,250 | |

| | 60,000 | | | | 10.750 | (f) | | | 08/15/20 | | | | — | |

| | 8,000,000 | | | | 1.000 | | | | 12/31/49 | | | | 1,150,000 | |

| Harland Clarke Holdings Corp.(b)(c) | |

| | 960,000 | | | | 9.250 | | | | 03/01/21 | | | | 916,800 | |

| Icahn Enterprises LP/Icahn Enterprises Finance Corp.(c) | |

| | 360,000 | | | | 4.875 | | | | 03/15/19 | | | | 359,100 | |

| | 300,000 | | | | 5.875 | | | | 02/01/22 | | | | 301,313 | |

| Nomura Holdings, Inc. | |

| | 500,000 | | | | 2.000 | | | | 09/13/16 | | | | 502,682 | |

| Opal Acquisition, Inc.(b)(c) | |

| | 320,000 | | | | 8.875 | | | | 12/15/21 | | | | 324,800 | |

| The NASDAQ OMX Group, Inc. | |

| | 140,000 | | | | 5.550 | | | | 01/15/20 | | | | 153,788 | |

| | 100,000 | | | | 4.250 | (c) | | | 06/01/24 | | | | 101,720 | |

| USB Realty Corp.(b)(c)(e) | |

| | 100,000 | | | | 1.378 | | | | 01/15/49 | | | | 90,000 | |

| Walter Investment Management Corp.(c) | |

| | 312,000 | | | | 7.875 | | | | 12/15/21 | | | | 282,360 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 9,487,681 | |

| | |

| | Food & Beverage – 0.2% | |

| B&G Foods, Inc.(c) | |

| | 700,000 | | | | 4.625 | | | | 06/01/21 | | | | 682,500 | |

| Carlsberg Breweries A/S | |

| GBP | 200,000 | | | | 7.250 | | | | 11/28/16 | | | | 344,019 | |

| CP Foods Holdings Ltd. | |

| $ | 200,000 | | | | 0.500 | | | | 01/15/19 | | | | 201,500 | |

| | |

| | |

| 18 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS MULTI-MANAGER ALTERNATIVES FUND

| | | | | | | | | | | | | | |

Principal Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Food & Beverage – (continued) | |

| Heineken NV | |

| GBP | 70,000 | | | | 7.250 | % | | | 03/10/15 | | | $ | 110,294 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,338,313 | |

| | |

| | Gaming – 1.0% | |

| Ameristar Casinos, Inc.(c) | |

| $ | 300,000 | | | | 7.500 | | | | 04/15/21 | | | | 312,750 | |

| Caesars Entertainment Operating Co., Inc.(c) | |

| | 2,015,000 | | | | 9.000 | | | | 02/15/20 | | | | 1,481,025 | |

| Chester Downs & Marina LLC(b)(c) | |

| | 1,150,000 | | | | 9.250 | | | | 02/01/20 | | | | 833,750 | |

| Graton Economic Development Authority(b)(c) | |

| | 1,055,000 | | | | 9.625 | | | | 09/01/19 | | | | 1,149,950 | |

| MGM Resorts International | |

| | 1,013,000 | | | | 6.625 | | | | 12/15/21 | | | | 1,061,117 | |

| Mohegan Tribal Gaming Authority(c) | |

| | 780,000 | | | | 9.750 | | | | 09/01/21 | | | | 797,550 | |

| MTR Gaming Group, Inc.(c)(d) | |

| | 240,000 | | | | 11.500 | | | | 08/01/19 | | | | 258,000 | |

| Scientific Games International, Inc.(b)(c) | |

| | 405,000 | | | | 7.000 | | | | 01/01/22 | | | | 410,063 | |

| | 200,000 | | | | 10.000 | | | | 12/01/22 | | | | 183,500 | |

| Seminole Hard Rock Entertainment, Inc.(b)(c) | |

| | 1,000,000 | | | | 5.875 | | | | 05/15/21 | | | | 990,000 | |

| Shingle Springs Tribal Gaming Authority(b)(c) | |

| | 945,000 | | | | 9.750 | | | | 09/01/21 | | | | 1,060,762 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 8,538,467 | |

| | |

| | Health Care – Medical Products(c) – 0.5% | |

| Biomet, Inc. | |

| | 1,000,000 | | | | 6.500 | | | | 08/01/20 | | | | 1,065,000 | |

| Fresenius Medical Care US Finance II, Inc.(b) | |

| | 750,000 | | | | 4.125 | | | | 10/15/20 | | | | 753,750 | |

| | 600,000 | | | | 4.750 | | | | 10/15/24 | | | | 606,000 | |

| Grifols Worldwide Operations Ltd.(b) | |

| | 500,000 | | | | 5.250 | | | | 04/01/22 | | | | 511,250 | |

| Halyard Health, Inc.(b) | |

| | 1,000,000 | | | | 6.250 | | | | 10/15/22 | | | | 1,020,000 | |

| Immucor, Inc. | |

| | 440,000 | | | | 11.125 | | | | 08/15/19 | | | | 475,200 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 4,431,200 | |

| | |

| | Health Care – Pharmaceuticals – 0.3% | | | | | |

| Forest Laboratories, Inc.(b) | |

| | 160,000 | | | | 4.375 | | | | 02/01/19 | | | | 169,019 | |

| Lantheus Medical Imaging, Inc.(c) | |

| | 430,000 | | | | 9.750 | | | | 05/15/17 | | | | 412,800 | |

| Mallinckrodt International Finance SA/Mallinckrodt CB LLC(b)(c) | |

| | 425,000 | | | | 5.750 | | | | 08/01/22 | | | | 435,625 | |

| Roche Holdings, Inc.(b)(e) | |

| | 500,000 | | | | 0.597 | | | | 09/30/19 | | | | 499,272 | |

| Valeant Pharmaceuticals International, Inc.(b)(c) | |

| | 500,000 | | | | 6.750 | | | | 08/15/18 | | | | 531,250 | |

| | 53,000 | | | | 6.875 | | | | 12/01/18 | | | | 54,855 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 2,102,821 | |

| | |

| | | | | | | | | | | | | | |

| | Corporate Obligations – (continued) | |

| | Health Care – Services – 0.6% | |

| Acadia Healthcare Co., Inc.(c) | |

| $ | 980,000 | | | | 5.125 | % | | | 07/01/22 | | | $ | 965,300 | |

| Amsurg Corp.(b)(c) | |

| | 104,000 | | | | 5.625 | | | | 07/15/22 | | | | 106,600 | |

| CHS/Community Health Systems, Inc.(c) | |

| | 150,000 | | | | 8.000 | | | | 11/15/19 | | | | 160,125 | |

| | 500,000 | | | | 5.125 | | | | 08/01/21 | | | | 521,250 | |

| DaVita HealthCare Partners, Inc.(c) | |

| | 500,000 | | | | 5.125 | | | | 07/15/24 | | | | 511,250 | |

| | HCA, Inc. | | | | | | | | | | | | | |

| | 115,000 | | | | 3.750 | | | | 03/15/19 | | | | 115,288 | |

| | 500,000 | | | | 6.500 | | | | 02/15/20 | | | | 559,375 | |

| Kindred Escrow Corp. II(b) | |

| | 795,000 | | | | 8.000 | | | | 01/15/20 | | | | 844,687 | |