Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22747

ALPS SERIES TRUST

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

303.623.5277

(Registrant’s telephone number, including area code)

JoEllen L. Legg, Esq., Secretary

ALPS Series Trust

1290 Broadway, Suite 1100

Denver, CO 80203

(Name and address of agent for service)

Copy to:

Robert Robertson, Esq.

Dechert LLP

One Bush Street, Suite 1600

San Francisco, CA 94104-4446

Date of fiscal year end: September 30

Date of reporting period: October 1, 2013 – September 30, 2014

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

Table of Contents

|

| 1 | ||||

| 5 | ||||

| 8 | ||||

| 9 | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 19 | ||||

| 21 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 1-855-254-6467 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

|

September 30, 2014 (Unaudited) |

Dear Shareholder,

Thank you for investing in the Cognios Market Neutral Large Cap Fund (the “Fund”). We value this opportunity to offer insight into the Fund’s investment adviser, Cognios Capital, LLC.

At Cognios, we believe that all investors should have access to the investment strategies necessary to diversify their portfolios. However, market neutral equity investment strategies have historically been more common in the hedge fund industry. Launching the Cognios Market Neutral Large Cap Fund allowed us to offer our hedged strategy as an alternative investment to investors that either (a) traditionally have not been able to invest in hedge funds or (b) were hedge fund investors in the past, but who now prefer the daily liquidity1, enhanced transparency2, and absence of incentive fees provided in a mutual fund format.

Consistent with our core values, Cognios’ goal is to make sure that every shareholder has a thorough understanding of our investment strategies. Information is power, and we believe educated investors are better clients. Below we describe in general terms the investment strategy of the Fund. A more complete description is provided in the Fund’s Prospectus.

The Fund employs a Beta-adjusted long/short market neutral equity investment strategy. With this type of strategy, the investment adviser buys (takes long positions in) stocks of companies that it believes are likely to outperform securities that the adviser “sells short”. In a short sale, the adviser borrows shares of a stock and then sells those shares with the obligation to repurchase them at some future date. The long positions generally make money for a fund when those stocks go up in price (and pay dividends) and the short positions generally make money for a fund when their prices go down (as long as they go down more than the dividends paid by those stocks that were sold short). A fund is “Beta market neutral” when there is as much stock sold short as there are positions bought long after adjusting for each of the positions’ sensitivities to moves in the broad stock market, so the overall profits for the fund are “neutralized” to the overall movement of the stock market. Beta is a measure of the sensitivity of a stock’s price changes to broad stock market movements over time.

By attempting to hedge out all of the market Beta, the Fund’s returns over time should be essentially “pure Alpha” (i.e., Alpha is the excess return of a portfolio after considering its Beta exposure.)

When these long and short portfolios are combined to hedge out the market Beta, the market neutral pure Alpha portfolio can make or lose money whether the entire stock market is up or down. In general, as the broad stock market increases, the Fund is likely to make money on its long positions but lose money on its short positions. Conversely, in general, as the broad stock market declines, the Fund is likely to lose money on its long positions but make money on its short positions. So while the general direction of the stock market shouldn’t make much of a difference to the Fund’s returns, what does matter is how the long positions perform relative to the short positions. The Fund generally makes money when the long positions outperform the short positions, even if all of the long and short positions are up or even if all of the long and short positions are down.

Annual Report | September 30, 2014 | 1 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Shareholder Letter |

September 30, 2014 (Unaudited) |

Because these risk factors are not likely to impact the Fund but are likely to impact many of the investments in the rest of an investor’s public equity portfolio (i.e., the Fund’s returns are likely to be uncorrelated with the overall stock market over time), the Fund potentially can serve to diversify an investment portfolio.

One potential risk in particular is worth highlighting in this market environment. Many investors are concerned that rising interest rates might lead to low or even negative returns in the future for their fixed income allocation. Rising interest rates could have negative potential implications for the stock market as well. When interest rates rise, market participants increase their required hurdle rate of return, resulting in a decline in the intrinsic values of stocks. Since we do not expect the Fund’s returns to be dependent upon general movements in interest rates over time, certain investors may want to consider a market neutral equity investment strategy, like the one employed by this Fund, to replace at least a portion of their longer term fixed income or equity investment allocations. Of course, each individual investor’s circumstances vary, but investors might want to discuss these possibilities with their qualified investment adviser.

Cognios selects stocks for the long and short portfolios using our firm’s proprietary investment process called ROTA/ROME® . The ROTA/ROME® investment process is a fundamental quantitative stock selection approach that focuses on a company’s Return on Tangible Assets (“ROTA”) and Return on Market value of Equity (“ROME,” which is essentially a company’s profit yield on its stock price). We believe that our ROTA/ROME process differentiates the Fund from other market neutral funds in that the Fund will exhibit more volatility when compared to other comparable funds; however, we believe that this also will lead to superior returns, resulting in superior risk-adjusted measures such as Sharpe Ratio3 and Sortino Ratio4. Additional details about the ROTA/ROME® investment process are outlined in the Fund’s prospectus. More information about the potential benefits of taking both long and short positions is available on the FAQ page of the Fund’s website, www.cogniosfunds.com.

Regarding performance of the Fund, NAV per share gained 12.41% including distributions for the Institutional Class Shares (COGIX) and gained 12.12% including distributions for the Investor Class Shares (COGMX) during the twelve months ended September 30, 2014. For the six months ended September 30, 2014, COGIX shares gained 6.60%, while the COGMX shares gained 6.42%.

The Fund held sixty-eight separate long positions and one hundred thirty-six separate short positions over the course of the last six months. Forty-seven of the sixty-eight long positions were profitable and thirty-six of the one hundred thirty-six short positions were profitable for the period. The long positions generated 17.6% gains on average equity capital while the short positions generated losses of 8.4% on average equity capital.

The performance data is obviously important; but since the portfolio is hedged, the independence of the performance versus the S&P 500 is also very important. Beta, Alpha, Correlation (a statistical measure of how two securities move in relation to each other) and R Squared are statistics that are commonly used to measure this independence. We track these measures on monthly basis (21 data points) and the data is presented in the tables below:

2 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Shareholder Letter |

September 30, 2014 (Unaudited) |

| Beta to the S&P 500 | Annualized Alpha to the S&P 500 | |||

COGIX | 0.21 | 2.20% | ||

COGMX | 0.21 | 1.81% | ||

| Correlation of Returns to the S&P 500 | R Squared of Returns to the S&P 5005 | |||

COGIX | 27.1% | 7.3% | ||

COGMX | 27.8% | 7.7% | ||

As the tables above indicate, Beta, Correlation and R Squared are all low, meaning that the performance of the Fund is statistically independent of the performance of the S&P 500. Meanwhile, the Alpha of the Fund is positive, which is good, but we hope this statistic moves higher in the future with improved performance.

We at Cognios look forward to future opportunities to connect with our shareholders. We strive to continuously add value to your investment experience by providing access to fund information, portfolio updates and straightforward commentary.

If you have any questions regarding the Cognios Market Neutral Large Cap Fund, please contact your account manager or financial adviser, or call one of our shareholder associates at 855-254-6467. We also invite you to visit Cognios’ website at www.cognios.com to learn more about our firm, our team and our values.

We thank you for investing with Cognios and for the trust you have placed in us.

Sincerely,

|

| |||

Jonathan Angrist

| Brian Machtley | |||

Portfolio Managers | ||||

Cognios Capital, LLC | ||||

| 1 | Purchases and redemptions may be made on any day the New York Stock Exchange is open for trading. You may purchase and sell shares directly with the Fund through the Fund’s website at www.cogniosfunds.com. |

| 2 | The Fund’s holdings will be updated quarterly at www.cogniosfunds.com. |

| 3 | The Sharpe Ratio is a ratio to measure risk-adjusted performance. The Sharpe ratio is calculated by subtracting the risk-free rate - such as that of the 10-year U.S. Treasury bond - from the rate of return for a portfolio and dividing the result by the standard deviation of the portfolio returns. |

Annual Report | September 30, 2014 | 3 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Shareholder Letter |

September 30, 2014 (Unaudited) |

| 4 | The Sortino Ratio is a modification of the Sharpe ratio that differentiates harmful volatility from general volatility by taking into account the standard deviation of negative asset returns, called downside deviation. |

| 5 | R Squared is the coefficient of determination and indicates how well data points fit in a model. In the example in the above table, 7.3% of the monthly movement in share price of COGIX can be explained by the movement of the S&P 500. |

4 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

|

September 30, 2014 (Unaudited) |

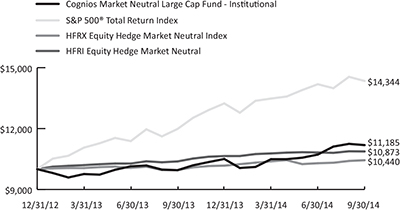

Performance (as of September 30, 2014)

Six Month | 1 Year | Since Inception* | ||||

Cognios Market Neutral Large Cap Fund - Investor | 6.42% | 12.12% | 6.34% | |||

Cognios Market Neutral Large Cap Fund - Institutional | 6.60% | 12.41% | 6.62% | |||

S&P 500® Total Return Index(a) | 6.42% | 19.73% | 22.92% | |||

HFRX Equity Hedge Market Neutral Index(b) | 0.54% | 4.90% | 2.50% | |||

HFRI Equity Hedge Market Neutral(c) | 0.91% | 4.74% | 4.91% |

The performance data quoted above represents past performance. Past performance is not a guarantee of future results. Investment return and value of the Fund shares will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Performance may be lower or higher than performance data quoted. Fund performance current to the most recent month-end is available by calling 855.254.6467 or by visiting www. cogniosfunds.com.

| * | Fund’s inception date is December 31, 2012. |

| (a) | The S&P 500® Total Return Index is an unmanaged index of 500 common stocks chosen for the market size, liquidity and industry group representation. It is a market-value weighted index. |

| (b) | The HFRX Equity Hedge Market Neutral Index – As of September 30, 2014, the secondary benchmark for the Fund was changed from the HFRI Equity Hedge Market Neutral Index to the HFRX Equity Market Neutral Index. The methodology used to construct the HFRX Equity Market Neutral Index requires that funds have a performance record of at least 12 months and assets greater than $50 million to be included as a constituent of the Index. The HFRX Equity Market Neutral Index also required funds to trade on a transparent basis and be open to new investors. As such, the Adviser believes that the methodology used and components of the HFRX Equity Hedge Market Neutral Index represent a more mature and accessible peer group for performance comparison and help to minimize selection, survivorship and reporting bias for the index. Both index returns and index methodology are provided by Hedge Fund Research Inc. |

| (c) | The HFRI Equity Hedge Market Neutral Index is a common benchmark for long/short market neutral hedge funds (funds traditionally only available to high net-worth accredited and institutional investors that are also “qualified clients” as defined by the SEC). More information about this index may be found at www.hedgefundresearch.com. |

Returns of less than one year are cumulative.

Indices are not actively managed and do not reflect deduction for fees, expenses or taxes. An investor cannot invest directly into an index.

The returns shown above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares.

The total annual operating expenses and total annual operating expenses after fee waivers and/or reimbursement you may pay as an investor in the Fund’s Investor Class and Institutional Class shares (as reported in the January 28, 2014 Prospectus) are 7.44% and 4.13%; and 7.19% and 3.88%, respectively.

Annual Report | September 30, 2014 | 5 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio Update |

September 30, 2014 (Unaudited) |

Performance of $10,000 Initial Investment (as of September 30, 2014)

The graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Sector Allocation (as a % of Net Assets)*

Basic Materials - Long | 4.32% | |||

Basic Materials (Short) | -17.80% | |||

Communications - Long | 17.53% | |||

Communications (Short) | -15.99% | |||

Consumer Cyclical - Long | 12.18% | |||

Consumer Cyclical (Short) | -13.91% | |||

Consumer Non-cyclical - Long | 24.06% | |||

Consumer Non-cyclical (Short) | -3.76% | |||

Diversified (Short) | -0.07% | |||

Energy - Long | 17.40% | |||

Energy (Short) | -12.99% | |||

Financials - Long | 3.75% | |||

Financials (Short) | -15.21% | |||

Industrials - Long | 10.60% | |||

Industrials (Short) | -9.66% | |||

Technology - Long | 21.61% | |||

Technology (Short) | -2.72% | |||

Utilities - Long | 6.32% | |||

Cash, Cash Equivalents, & Other Net Assets | 74.34% | |||

| ||||

TOTAL | 100.00% | |||

| ||||

| * | Holdings are subject to change. Table presents indicative values only. |

6 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio Update |

September 30, 2014 (Unaudited) |

Top 10 Long Positions (as a % of Net Assets)*

| Security | Ticker | Weight | ||

Edwards Lifesciences Corp. | EW | 6.32% | ||

ADT Corp. | ADT | 5.93% | ||

L-3 Communications Holdings, Inc. | LLL | 4.34% | ||

CF Industries Holdings, Inc. | CF | 4.32% | ||

Raytheon Co. | RTN | 4.23% | ||

Bed Bath & Beyond, Inc. | BBBY | 4.10% | ||

NetApp, Inc. | NTAP | 4.08% | ||

Expedia, Inc. | EXPE | 4.03% | ||

EMC Corp. | EMC | 4.00% | ||

DIRECTV | DTV | 3.99% |

| * | Holdings are subject to change. Table presents indicative values only. |

Annual Report | September 30, 2014 | 7 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

|

September 30, 2014 (Unaudited) |

Examples. As a shareholder of the Cognios Market Neutral Large Cap Fund (the “Fund”), you will incur two types of costs: (1) transaction costs, (2) ongoing costs, including management fees, distribution and service (12b-1) fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on April 1, 2014 and held until September 30, 2014.

Actual Expenses. The first line under each class in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period April 1, 2014 - September 30, 2014” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line under each class in the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line under each class in the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value April 1, 2014 | Ending Account Value September 30, 2014 | Expense Ratio(a) | Expenses Paid During Period April 1, 2014 - September 30, 2014(b) | |||||||

Investor Class | ||||||||||

Actual | $ 1,000.00 | $ 1,064.20 | 4.23% | $ 21.89 | ||||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,003.86 | 4.23% | $ 21.25 | ||||||

Institutional Class | ||||||||||

Actual | $ 1,000.00 | $ 1,066.00 | 4.00% | $ 20.72 | ||||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,005.01 | 4.00% | $ 20.11 | ||||||

| (a) | Annualized, based on the Fund’s most recent fiscal half-year expenses. Expense ratio excluding interest expense and dividends paid on borrowed securities is 2.25% and 2.00% for Investor Class and Institutional Class, respectively. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183), divided by 365. |

8 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

| September 30, 2014

|

| Shares | Value (Note 2) | |||||||

| ||||||||

COMMON STOCKS (117.77%) |

| |||||||

Basic Materials (4.32%) |

| |||||||

CF Industries Holdings, Inc.(a) | 2,261 | $ | 631,316 | |||||

|

| |||||||

Total Basic Materials | 631,316 | |||||||

|

| |||||||

Communications (17.53%) | ||||||||

Cablevision Systems Corp. - Class A | 31,434 | 550,409 | ||||||

Corning, Inc. | 15,069 | 291,435 | ||||||

DIRECTV(b) | 6,744 | 583,491 | ||||||

Expedia, Inc.(a) | 6,713 | 588,193 | ||||||

Harris Corp. | 8,238 | 547,003 | ||||||

|

| |||||||

Total Communications | 2,560,531 | |||||||

|

| |||||||

Consumer Cyclical (12.18%) | ||||||||

Bed Bath & Beyond, Inc.(a)(b) | 9,093 | 598,592 | ||||||

Delta Air Lines, Inc.(a) | 7,905 | 285,766 | ||||||

GameStop Corp. - Class A | 13,678 | 563,534 | ||||||

Southwest Airlines Co.(a) | 9,795 | 330,777 | ||||||

|

| |||||||

Total Consumer Cyclical | 1,778,669 | |||||||

|

| |||||||

Consumer Non-cyclical (24.06%) | ||||||||

ADT Corp.(a) | 24,410 | 865,579 | ||||||

Aetna, Inc.(a) | 3,825 | 309,825 | ||||||

CR Bard, Inc.(a) | 3,891 | 555,285 | ||||||

Edwards Lifesciences Corp.(b) | 9,036 | 923,027 | ||||||

WellPoint, Inc. | 2,727 | 326,204 | ||||||

Western Union Co. | 33,339 | 534,757 | ||||||

|

| |||||||

Total Consumer Non-cyclical | 3,514,677 | |||||||

|

| |||||||

Energy (17.40%) | ||||||||

Chesapeake Energy Corp.(a) | 5,688 | 130,767 | ||||||

Denbury Resources, Inc. | 18,486 | 277,845 | ||||||

Devon Energy Corp. | 4,184 | 285,265 | ||||||

Ensco PLC - Class A(a) | 6,244 | 257,940 | ||||||

Murphy Oil Corp.(a) | 5,073 | 288,704 | ||||||

Newfield Exploration Co.(a)(b) | 7,073 | 262,196 | ||||||

Noble Corp. PLC | 11,113 | 246,931 | ||||||

Southwestern Energy Co.(b) | 14,218 | 496,919 | ||||||

Tesoro Corp.(a) | 4,836 | 294,899 | ||||||

|

| |||||||

Total Energy | 2,541,466 | |||||||

|

| |||||||

Financials (3.75%) | ||||||||

Affiliated Managers Group, Inc.(a)(b) | 2,737 | 548,385 | ||||||

|

| |||||||

Total Financials | 548,385 | |||||||

|

| |||||||

| See Notes to Financial Statements. | ||

Annual Report | September 30, 2014 | 9 | |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio of Investments

|

September 30, 2014 |

| Shares | Value (Note 2) | |||||||||||

| ||||||||||||

Industrials (10.60%) |

| |||||||||||

L-3 Communications Holdings, Inc.(a) |

| 5,325 | $ | 633,249 | ||||||||

Raytheon Co. |

| 6,073 | 617,138 | |||||||||

Textron, Inc.(a) |

| 8,264 | 297,422 | |||||||||

|

| |||||||||||

Total Industrials |

| 1,547,809 | ||||||||||

|

| |||||||||||

Technology (21.61%) | ||||||||||||

Apple, Inc. |

| 5,681 | 572,361 | |||||||||

CA, Inc. |

| 20,696 | 578,246 | |||||||||

EMC Corp. |

| 19,975 | 584,469 | |||||||||

Hewlett-Packard Co. |

| 8,335 | 295,642 | |||||||||

NetApp, Inc.(a) |

| 13,855 | 595,211 | |||||||||

Seagate Technology PLC |

| 9,260 | 530,320 | |||||||||

|

| |||||||||||

Total Technology |

| 3,156,249 | ||||||||||

|

| |||||||||||

Utilities (6.32%) | ||||||||||||

Consolidated Edison, Inc.(a) |

| 5,424 | 307,324 | |||||||||

Entergy Corp.(a) |

| 4,062 | 314,114 | |||||||||

Pinnacle West Capital Corp.(a) |

| 5,514 | 301,285 | |||||||||

|

| |||||||||||

Total Utilities |

| 922,723 | ||||||||||

|

| |||||||||||

TOTAL COMMON STOCKS (Cost $16,907,824) |

| 17,201,825 | ||||||||||

| ||||||||||||

| 7-Day Yield | Shares | Value (Note 2) | ||||||||||

| ||||||||||||

SHORT TERM INVESTMENTS (0.32%) | ||||||||||||

Money Market Fund (0.32%) | ||||||||||||

Daily Income Fund - U.S. Treasury | 0.01000% | 46,378 | 46,378 | |||||||||

|

| |||||||||||

TOTAL SHORT TERM INVESTMENTS (Cost $46,378) | 46,378 | |||||||||||

| ||||||||||||

TOTAL INVESTMENTS (118.09%) (Cost $16,954,202) | $ | 17,248,203 | ||||||||||

| ||||||||||||

SECURITIES SOLD SHORT (-92.11%) (Proceeds $13,529,415) | (13,453,215) | |||||||||||

| ||||||||||||

Other Assets In Excess Of Liabilities (74.02%) | 10,811,307 (c) | |||||||||||

| ||||||||||||

NET ASSETS (100.00%) | $ | 14,606,295 | ||||||||||

| ||||||||||||

| See Notes to Financial Statements. | ||

10 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio of Investments

|

September 30, 2014 |

| Shares | Value (Note 2) | |||||||

| ||||||||

SCHEDULE OF SECURITIES SOLD SHORT | ||||||||

COMMON STOCKS (-92.11%) | ||||||||

Basic Materials (-17.80%) |

| |||||||

Alcoa, Inc. | (19,424) | $ | (312,532) | |||||

Allegheny Technologies, Inc. | (3,553) | (131,816) | ||||||

EI du Pont de Nemours & Co. | (11,272) | (808,879) | ||||||

FMC Corp. | (2,258) | (129,135) | ||||||

Freeport-McMoRan, Inc. | (9,474) | (309,326) | ||||||

MeadWestvaco Corp. | (3,481) | (142,512) | ||||||

Monsanto Co. | (3,048) | (342,931) | ||||||

The Mosaic Co. | (3,076) | (136,605) | ||||||

Nucor Corp. | (5,273) | (286,218) | ||||||

|

| |||||||

Total Basic Materials | (2,599,954) | |||||||

|

| |||||||

Communications (-15.99%) | ||||||||

CBS Corp. - Class B | (3,658) | (195,703) | ||||||

Discovery Communications, Inc. - Class A | (1,599) | (60,442) | ||||||

Facebook, Inc. | (4,698) | (371,330) | ||||||

Graham Holdings Co. - Class B | (208) | (145,515) | ||||||

Interpublic Group of Cos., Inc. | (4,023) | (73,701) | ||||||

News Corp. - Class A | (4,431) | (72,447) | ||||||

The Priceline Group, Inc. | (282) | (326,719) | ||||||

TripAdvisor, Inc. | (978) | (89,409) | ||||||

Twenty-First Century Fox, Inc. - Class A | (9,822) | (336,796) | ||||||

Yahoo! Inc | (16,273) | (663,125) | ||||||

|

| |||||||

Total Communications | (2,335,187) | |||||||

|

| |||||||

Consumer Cyclical (-13.91%) | ||||||||

BorgWarner, Inc. | (1,690) | (88,911) | ||||||

CarMax, Inc. | (3,601) | (167,266) | ||||||

Carnival Corp. | (5,344) | (214,668) | ||||||

DR Horton, Inc. | (6,922) | (142,039) | ||||||

Ford Motor Co. | (22,478) | (332,450) | ||||||

Goodyear Tire & Rubber Co. | (5,781) | (130,564) | ||||||

Harman International Industries, Inc. | (690) | (67,648) | ||||||

Lennar Corp. - Class A | (3,813) | (148,059) | ||||||

Michael Kors Holdings, Ltd. | (1,522) | (108,656) | ||||||

Mohawk Industries, Inc. | (1,203) | (162,188) | ||||||

PVH Corp. | (1,352) | (163,795) | ||||||

Tiffany & Co. | (2,113) | (203,503) | ||||||

Whirlpool Corp. | (701) | (102,101) | ||||||

|

| |||||||

Total Consumer Cyclical | (2,031,848) | |||||||

|

| |||||||

| See Notes to Financial Statements. | ||

Annual Report | September 30, 2014 | 11 | |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio of Investments

|

September 30, 2014 |

| Shares | Value (Note 2) | |||||||

| ||||||||

Consumer Non-cyclical (-3.76%) | ||||||||

Avery Dennison Corp. | (1,426) | $ | (63,671) | |||||

Biogen Idec, Inc. | (1,022) | (338,088) | ||||||

Tenet Healthcare Corp. | (2,474) | (146,931) | ||||||

|

| |||||||

Total Consumer Non-cyclical | (548,690) | |||||||

|

| |||||||

Diversified (-0.07%) | ||||||||

Leucadia National Corp. | (410) | (9,774) | ||||||

|

| |||||||

Total Diversified | (9,774) | |||||||

|

| |||||||

Energy (-12.99%) | ||||||||

Apache Corp. | (3,482) | (326,855) | ||||||

Baker Hughes, Inc. | (7,214) | (469,343) | ||||||

Cameron International Corp. | (3,335) | (221,377) | ||||||

CONSOL Energy, Inc. | (3,819) | (144,587) | ||||||

Nabors Industries, Ltd. | (2,922) | (66,505) | ||||||

Peabody Energy Corp. | (9,596) | (118,798) | ||||||

QEP Resources, Inc. | (2,220) | (68,332) | ||||||

Rowan Cos. PLC - Class A | (2,563) | (64,870) | ||||||

Transocean, Ltd. | (3,274) | (104,670) | ||||||

The Williams Cos, Inc. | (5,644) | (312,395) | ||||||

|

| |||||||

Total Energy | (1,897,732) | |||||||

|

| |||||||

Financials (-15.21%) | ||||||||

American Express Co. | (1,301) | (113,890) | ||||||

American International Group, Inc. | (1,785) | (96,426) | ||||||

Ameriprise Financial, Inc. | (233) | (28,748) | ||||||

Bank of America Corp. | (13,078) | (222,980) | ||||||

Bank of New York Mellon Corp. | (1,406) | (54,454) | ||||||

BB&T Corp. | (892) | (33,191) | ||||||

BlackRock, Inc. | (207) | (67,962) | ||||||

Capital One Financial Corp. | (702) | (57,297) | ||||||

Charles Schwab Corp. | (1,619) | (47,582) | ||||||

Citigroup, Inc. | (3,782) | (195,983) | ||||||

Comerica, Inc. | (205) | (10,221) | ||||||

Discover Financial Services | (572) | (36,831) | ||||||

E*Trade Financial Corp. | (327) | (7,387) | ||||||

Fifth Third Bancorp | (1,040) | (20,821) | ||||||

General Growth Properties, Inc. - REIT | (1,110) | (26,140) | ||||||

Genworth Financial, Inc. - Class A | (553) | (7,244) | ||||||

Goldman Sachs Group, Inc. | (551) | (101,147) | ||||||

The Hartford Financial Services Group, Inc. | (558) | (20,786) | ||||||

Host Hotels & Resorts, Inc. - REIT | (945) | (20,157) | ||||||

| See Notes to Financial Statements. | ||

12 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio of Investments

|

September 30, 2014 |

| Shares | Value (Note 2) | |||||||

| ||||||||

Financials (continued) | ||||||||

Huntington Bancshares, Inc. | (890) | $ | (8,660) | |||||

JPMorgan Chase & Co. | (4,689) | (282,465) | ||||||

KeyCorp | (989) | (13,183) | ||||||

Kimco Realty Corp. - REIT | (454) | (9,947) | ||||||

Lincoln National Corp. | (324) | (17,360) | ||||||

Macerich Co. - REIT | (155) | (9,894) | ||||||

Morgan Stanley | (2,442) | (84,420) | ||||||

Navient Corp. | (457) | (8,093) | ||||||

PNC Financial Services Group, Inc. | (675) | (57,767) | ||||||

Principal Financial Group, Inc. | (368) | (19,309) | ||||||

Prologis, Inc. - REIT | (625) | (23,563) | ||||||

Prudential Financial, Inc. | (570) | (50,126) | ||||||

Regions Financial Corp. | (1,718) | (17,249) | ||||||

State Street Corp. | (526) | (38,719) | ||||||

SunTrust Banks, Inc. | (660) | (25,100) | ||||||

Unum Group | (287) | (9,867) | ||||||

Vornado Realty Trust - REIT | (235) | (23,491) | ||||||

Wells Fargo & Co. | (6,502) | (337,259) | ||||||

XL Group PLC | (301) | (9,984) | ||||||

Zions Bancorporation | (208) | (6,044) | ||||||

|

| |||||||

Total Financials | (2,221,747) | |||||||

|

| |||||||

Industrials (-9.66%) | ||||||||

Agilent Technologies, Inc. | (2,496) | (142,222) | ||||||

Deere & Co. | (3,226) | (264,500) | ||||||

General Electric Co. | (15,212) | (389,731) | ||||||

Ingersoll-Rand PLC | (2,018) | (113,734) | ||||||

Martin Marietta Materials, Inc. | (540) | (69,628) | ||||||

Ryder System, Inc. | (867) | (78,004) | ||||||

Sealed Air Corp. | (4,116) | (143,566) | ||||||

Vulcan Materials Co. | (2,352) | (141,661) | ||||||

Xylem, Inc. | (1,908) | (67,715) | ||||||

|

| |||||||

Total Industrials | (1,410,761) | |||||||

|

| |||||||

Technology (-2.72%) | ||||||||

Adobe Systems, Inc. | (3,708) | (256,557) | ||||||

| See Notes to Financial Statements. | ||

Annual Report | September 30, 2014 | 13 | |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Portfolio of Investments

|

September 30, 2014 |

| Shares | Value (Note 2) | |||||||

| ||||||||

Technology (continued) | ||||||||

First Solar, Inc. | (2,142) | $ | (140,965) | |||||

|

| |||||||

Total Technology | (397,522) | |||||||

|

| |||||||

TOTAL COMMON STOCKS (Proceeds $13,529,415) | (13,453,215) | |||||||

| ||||||||

TOTAL SECURITIES SOLD SHORT (-92.11%) (Proceeds $13,529,415) | $ | (13,453,215) | ||||||

| ||||||||

| (a) | Security, or a portion of security, is being held as collateral for short sales. As of September 30, 2014, the aggregate market value of those securities was $8,031,363, which represents approximately 54.99% of net assets. |

| (b) | Non-income producing security. |

| (c) | Includes segregated cash that is being held as collateral for securities sold short. |

Common Abbreviations:

Ltd - Limited

PLC - Public Limited Company.

REIT - Real Estate Investment Trust.

For Fund compliance purposes, the Fund’s industry classifications refer to any one of the industry sub-classifications used by one or more widely recognized market indexes and/or as defined by the Fund’s management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of the Fund’s net assets. (unaudited)

| See Notes to Financial Statements. | ||

14 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Statement of Assets and Liabilities

|

September 30, 2014 |

ASSETS: | ||||

Investments, at value (cost $16,954,202) | $ | 17,248,203 | ||

Segregated cash with brokers | 19,554 | |||

Deposit with broker for securities sold short (Note 2) | 10,804,078 | |||

Receivable for shares sold | 40,000 | |||

Due from advisor | 3,783 | |||

Dividends receivable | 7,293 | |||

Prepaid assets | 9,359 | |||

|

| |||

Total Assets | 28,132,270 | |||

|

| |||

LIABILITIES: | ||||

Securities sold short (proceeds $13,529,415) | 13,453,215 | |||

Payable for dividends on short sales | 11,000 | |||

Payable for distribution and service fees | 1,163 | |||

Payable to trustees | 144 | |||

Payable to chief compliance officer | 1,667 | |||

Payable to principal financial officer | 833 | |||

Accrued expenses and other liabilities | 57,953 | |||

|

| |||

Total Liabilities | 13,525,975 | |||

|

| |||

NET ASSETS | $ | 14,606,295 | ||

|

| |||

NET ASSETS CONSIST OF: | ||||

Paid-in capital (Note 5) | $ | 12,930,894 | ||

Accumulated net investment loss | (45) | |||

Accumulated net realized gain on investments and securities sold short | 1,305,245 | |||

Net unrealized appreciation on investments and securities sold short | 370,201 | |||

|

| |||

NET ASSETS | $ | 14,606,295 | ||

|

| |||

PRICING OF SHARES | ||||

Investor Class: | ||||

Net Asset Value, offering and redemption price per share | $ | 10.77 | ||

Net Assets | $ | 5,699,437 | ||

Shares of beneficial interest outstanding | 528,991 | |||

Institutional Class: | ||||

Net Asset Value, offering and redemption price per share | $ | 10.82 | ||

Net Assets | $ | 8,906,858 | ||

Shares of beneficial interest outstanding | 823,373 | |||

| See Notes to Financial Statements. | ||

Annual Report | September 30, 2014 | 15 | |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

|

For the Year Ended September 30, 2014 |

INVESTMENT INCOME: | ||||

Dividends | 398,403 | |||

|

| |||

Total Investment Income | 398,403 | |||

|

| |||

EXPENSES: | ||||

Investment advisory fee (Note 6) | 228,509 | |||

Dividend expense on securities sold short | 196,940 | |||

Interest expense | 110,311 | |||

Administration fee | 120,465 | |||

Distribution and service fees | 13,273 | |||

Custodian fee | 10,012 | |||

Legal fees | 30,140 | |||

Audit fees | 15,850 | |||

Transfer agent fee | 39,641 | |||

Trustees fees and expenses | 17,436 | |||

Registration and filing fees | 27,556 | |||

Printing fees | 7,997 | |||

Chief compliance officer fee | 20,000 | |||

Principal financial officer fee | 10,000 | |||

Insurance expense | 11,828 | |||

Other expenses | 8,233 | |||

|

| |||

Total Expenses | 868,191 | |||

|

| |||

Less fees waived/reimbursed by investment adviser | ||||

Investor Class | (92,011) | |||

Institutional Class | (125,422) | |||

|

| |||

Total fees waived/reimbursed by investment adviser (Note 6) | (217,433) | |||

|

| |||

Less fess waived by Administrator (Note 6) | (25,556) | |||

|

| |||

Net Expenses | 625,202 | |||

|

| |||

NET INVESTMENT LOSS | (226,799) | |||

|

| |||

REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | ||||

Net realized gain/(loss) on: | ||||

Investments | 5,376,751 | |||

Securities sold short | (3,617,570) | |||

|

| |||

Net realized gain | 1,759,181 | |||

|

| |||

Change in appreciation/(depreciation) on | (314,873) | |||

Securities sold short | 920,110 | |||

|

| |||

Net change | 605,237 | |||

|

| |||

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS AND SECURITIES SOLD SHORT | 2,364,418 | |||

|

| |||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 2,137,619 | ||

|

| |||

| See Notes to Financial Statements. | ||

16 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Statements of Changes in Net Assets

|

For the Year Ended September 30, 2014 | For the Period Ended September 30, 2013(a) | |||||||

| ||||||||

OPERATIONS: | ||||||||

Net investment loss | $ | (226,799) | $ | (122,150) | ||||

Net realized gain on investments and securities sold short | 1,759,181 | 276,717 | ||||||

Net change in unrealized appreciation/(depreciation) on investments and securities sold short | 605,237 | (235,036) | ||||||

|

|

|

| |||||

Net increase/(decrease) in net assets resulting from operations | 2,137,619 | (80,469) | ||||||

|

|

|

| |||||

DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

From net realized gains on investments: | ||||||||

Investor Class | (170,799) | – | ||||||

Institutional Class | (215,970) | – | ||||||

|

|

|

| |||||

Total distributions | (386,769) | – | ||||||

|

|

|

| |||||

BENEFICIAL SHARE TRANSACTIONS (Note 5): | ||||||||

Investor Class: | ||||||||

Shares sold | 125,097 | 5,053,401 | ||||||

Dividends reinvested | 170,799 | – | ||||||

Shares redeemed | (105,773) | (41) | ||||||

|

|

|

| |||||

Net increase from beneficial share transactions | 190,123 | 5,053,360 | ||||||

|

|

|

| |||||

Institutional Class: | ||||||||

Shares sold | 35,902,787 | 6,138,562 | ||||||

Dividends reinvested | 215,970 | – | ||||||

Shares redeemed | (34,648,888) | (16,000) | ||||||

|

|

|

| |||||

Net increase from beneficial share transactions | 1,469,869 | 6,122,562 | ||||||

|

|

|

| |||||

Net increase in net assets | 3,410,842 | 11,095,453 | ||||||

|

|

|

| |||||

NET ASSETS: | ||||||||

Beginning of period | 11,195,453 | 100,000 | ||||||

|

|

|

| |||||

End of period (including accumulated net investment loss of $(45) and $(144)) | $ | 14,606,295 | $ | 11,195,453 | ||||

|

|

|

| |||||

| (a) | Commenced operations on January 2, 2013. |

| See Notes to Financial Statements. | ||

Annual Report | September 30, 2014 | 17 | |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

|

For the Year Ended September 30, 2014 |

CASH FLOWS FROM OPERATING ACTIVITIES: | ||||

Net increase in net assets from operations | $ | 2,137,619 | ||

Adjustments to reconcile net increase in net assets from operations to net cash used in operating activities: | ||||

Purchases of investment securities | (83,091,031) | |||

Proceeds from disposition of investment securities | 84,300,876 | |||

Proceeds from securities sold short transactions | 54,285,333 | |||

Purchases to cover securities sold short transactions | (54,320,801) | |||

Net purchases from short-term investment securities | (17,237) | |||

Net realized gain on investments and securities sold short | (1,759,181) | |||

Net change in unrealized appreciation on investments and securities sold short | (605,237) | |||

Changes in assets and liabilities: | ||||

Increase in segregated cash with brokers | (9,939) | |||

Increase in deposit with broker for securities sold short | (2,178,024) | |||

Decrease in receivable due from adviser | 4,374 | |||

Decrease in dividends receivable | 7,949 | |||

Increase in prepaid assets | (2,888) | |||

Decrease in payable for dividends on short sales | (514) | |||

Increase in payable for distribution and service fees | 128 | |||

Decrease in payable to trustees | (662) | |||

Increase in other accrued expenses and other liabilities | 16,012 | |||

| ||||

Net cash used in operating activities | (1,233,223) | |||

| ||||

CASH FLOWS PROVIDED BY FINANCING ACTIVITIES: | ||||

Proceeds from sale of shares | 35,987,884 | |||

Cost of shares redeemed | (34,754,661) | |||

| ||||

Net cash provided by financing activities | 1,233,223 | |||

| ||||

NET INCREASE IN CASH FOR THE PERIOD | – | |||

| ||||

CASH, BEGINNING OF PERIOD | $ | – | ||

CASH, END OF PERIOD | $ | – | ||

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | ||||

Non-cash financing activities not included herein consist of reinvestment of distributions of: | $ | 386,769 | ||

| See Notes to Financial Statements. | ||

18 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund - Investor Class | Financial Highlights | |

For a share outstanding throughout the periods presented. |

For the Year Ended September 30, 2014 | For the Period Ended September 30, 2013(a) | |||||||

| ||||||||

NET ASSET VALUE, BEGINNING OF PERIOD | $ | 9.93 | $ | 10.00 | ||||

INCOME/(LOSS) FROM OPERATIONS: | ||||||||

Net investment loss(b) | (0.17) | (0.12) | ||||||

Net realized and unrealized gain on investments | 1.35 | 0.05 | ||||||

|

| |||||||

Total from Investment Operations | 1.18 | (0.07) | ||||||

|

| |||||||

LESS DISTRIBUTIONS: | ||||||||

From net realized gains on investments | (0.34) | – | ||||||

|

| |||||||

Total Distributions | (0.34) | – | ||||||

|

| |||||||

NET INCREASE/(DECREASE) IN NET ASSET VALUE | 0.84 | (0.07) | ||||||

|

| |||||||

NET ASSET VALUE, END OF PERIOD | $ | 10.77 | $ | 9.93 | ||||

|

| |||||||

TOTAL RETURN(c) | 12.12 | % | (0.70)%(d) | |||||

SUPPLEMENTAL DATA: | ||||||||

Net assets, End of Period (in 000s) | $ | 5,699 | $ | 5,067 | ||||

RATIOS TO AVERAGE NET ASSETS (excluding interest expense and dividend expense on securities sold short) | ||||||||

Operating expenses excluding reimbursement/waiver | 4.15 | % | 4.38%(e) | |||||

Operating expenses including reimbursement/waiver | 2.25 | % | 2.25%(e) | |||||

Net investment income including reimbursement/waiver | 0.30 | % | 0.19%(e) | |||||

RATIOS TO AVERAGE NET ASSETS (including interest expense and dividend expense on securities sold short) | ||||||||

Operating expenses excluding reimbursement/waiver | 6.16 | % | 6.27%(e) | |||||

Operating expenses including reimbursement/waiver | 4.26 | % | 4.13%(e) | |||||

Net investment loss including reimbursement/waiver | (1.71) | % | (1.69)%(e) | |||||

PORTFOLIO TURNOVER RATE | 461 | % | 155%(d) | |||||

| (a) | Commenced operations on January 2, 2013. |

| (b) | Per share amounts are based upon average shares outstanding. |

| (c) | The total return would have been lower had certain expenses not been reimbursed / waived during the period. The return shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (d) | Not annualized. |

| (e) | Annualized. |

| See Notes to Financial Statements. | ||

Annual Report | September 30, 2014 | 19 | |

Table of Contents

| Cognios Market Neutral Large Cap Fund - Institutional Class | Financial Highlights | |

For a share outstanding throughout the periods presented. |

For the Year Ended September 30, 2014 | For the Period Ended September 30, 2013(a) | |||||||

| ||||||||

NET ASSET VALUE, BEGINNING OF PERIOD | $ | 9.95 | $ | 10.00 | ||||

INCOME/(LOSS) FROM OPERATIONS: | ||||||||

Net investment loss(b) | (0.14) | (0.10) | ||||||

Net realized and unrealized gain on investments | 1.35 | 0.05 | ||||||

|

| |||||||

Total from Investment Operations | 1.21 | (0.05) | ||||||

|

| |||||||

LESS DISTRIBUTIONS: | ||||||||

From net realized gains on investments | (0.34) | – | ||||||

|

| |||||||

Total Distributions | (0.34) | – | ||||||

|

| |||||||

NET INCREASE/(DECREASE) IN NET ASSET VALUE | 0.87 | (0.05) | ||||||

|

| |||||||

NET ASSET VALUE, END OF PERIOD | $ | 10.82 | $ | 9.95 | ||||

|

| |||||||

TOTAL RETURN(c) | 12.41 | % | (0.50)%(d) | |||||

SUPPLEMENTAL DATA: | ||||||||

Net assets, End of Period (in 000s) | $ | 8,907 | $ | 6,128 | ||||

RATIOS TO AVERAGE NET ASSETS (excluding interest expense and dividend expense on securities sold short) | ||||||||

Operating expenses excluding reimbursement/waiver | 3.43 | % | 4.13%(e) | |||||

Operating expenses including reimbursement/waiver | 2.00 | % | 2.00%(e) | |||||

Net investment income including reimbursement/waiver | 0.65 | % | 0.46%(e) | |||||

RATIOS TO AVERAGE NET ASSETS (including interest expense and dividend expense on securities sold short) | ||||||||

Operating expenses excluding reimbursement/waiver | 5.45 | % | 6.02%(e) | |||||

Operating expenses including reimbursement/waiver | 4.01 | % | 3.88%(e) | |||||

Net investment loss including reimbursement/waiver | (1.37) | % | (1.42)%(e) | |||||

PORTFOLIO TURNOVER RATE | 461 | % | 155%(d) | |||||

| (a) | Commenced operations on January 2, 2013. |

| (b) | Per share amounts are based upon average shares outstanding. |

| (c) | The total return would have been lower had certain expenses not been reimbursed / waived during the period. The return shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (d) | Not annualized. |

| (e) | Annualized. |

See Notes to Financial Statements.

| ||

20 | www.cogniosfunds.com | |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

|

September 30, 2014 |

1. ORGANIZATION

ALPS Series Trust (the “Trust”), a Delaware statutory trust, is an open-end management investment company registered under the Investment Company Act of 1940 (the “1940 Act”). As of September 30, 2014, the Trust had nine registered funds. This annual report describes the Cognios Market Neutral Large Cap Fund (the “Fund”). The Fund seeks long-term growth of capital independent of stock market direction. The Fund currently offers Investor Class shares and Institutional Class shares. Each share class of the Fund represents an investment in the same portfolio of securities, but each share class has its own expense structure. The Board of Trustees (the “Board”) may establish additional funds and classes of shares at any time in the future without shareholder approval.

2. SIGNIFICANT ACCOUNTING POLICIES

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America for investment companies “U.S. GAAP”. The Fund is considered an investment company for financial reporting purposes. The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates. The following is a summary of significant accounting policies consistently followed by the Fund in preparation of the financial statements.

Investment Valuation: The Fund generally values its securities based on market prices determined at the close of regular trading on the New York Stock Exchange (“NYSE”), normally 4:00 p.m. Eastern Time, on each day the NYSE is open for trading.

For equity securities and mutual funds that are traded on an exchange, the market price is usually the closing sale or official closing price on that exchange. In the case of equity securities not traded on an exchange, or if such closing prices are not otherwise available, the securities are valued at the mean of the most recent bid and ask prices on such day.

Redeemable securities issued by open-end registered investment companies are valued at the investment company’s applicable net asset value, with the exception of exchange-traded open-end investment companies, which are priced as equity securities.

When such prices or quotations are not available, or when the Fair Value Committee appointed by the Board believes that they are unreliable, securities may be priced using fair value procedures approved by the Board.

Short Sales: The Fund may sell securities short. To do this, the Adviser will borrow and then sell (take short positions in) equity securities of U.S. companies that the Adviser believes are likely to underperform the long positions over time. To complete such a transaction, the Fund must borrow the security to deliver to the buyer. The Fund then is obligated to replace the security borrowed by purchasing it in the open market at some later date. The Fund bears the risk of a loss if the market

Annual Report | September 30, 2014 | 21 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

price of the security increases between the date of the short sale and the date on which the Fund replaces the borrowed security. The Fund will realize a gain if the security declines in value between those dates. There can be no assurance that securities necessary to cover a short position will be available for purchase. To mitigate leverage risk, the Fund will segregate liquid assets (which may include its long positions) at least equal to its short position exposure, marked-to-market daily. The Fund maintains collateral consisting of cash, U.S. Government securities or other liquid assets in an amount at least equal to the market value of their respective short positions. The Fund is liable for any dividends or interest payable on securities while those securities are in a short position. The Fund typically intends to hold securities sold short for the short term, therefore, they are excluded from the purchase and sales of investments in Note 4 and the Fund’s Portfolio Turnover Calculation in the Financial Highlights. As of September 30, 2014, the Fund held securities sold short with a market value of $13,453,215.

Fair Value Measurements: The Fund discloses the classification of its fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

Level 1 – | Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; | |

Level 2 – | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and | |

Level 3 – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. | |

22 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

The following is a summary of the inputs used to value the Fund’s investments as of September 30, 2014:

| Investments in Securities at Value | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| ||||||||||||||||

Common Stocks | ||||||||||||||||

Basic Materials | $ | 631,316 | $ | – | $ | – | $ | 631,316 | ||||||||

Communications | 2,560,531 | – | – | 2,560,531 | ||||||||||||

Consumer Cyclical | 1,778,669 | – | – | 1,778,669 | ||||||||||||

Consumer Non-cyclical | 3,514,677 | – | – | 3,514,677 | ||||||||||||

Energy | 2,541,466 | – | – | 2,541,466 | ||||||||||||

Financials | 548,385 | – | – | 548,385 | ||||||||||||

Industrials | 1,547,809 | – | – | 1,547,809 | ||||||||||||

Technology | 3,156,249 | – | – | 3,156,249 | ||||||||||||

Utilities | 922,723 | – | – | 922,723 | ||||||||||||

Short Term Investments | 46,378 | – | – | 46,378 | ||||||||||||

| ||||||||||||||||

Total | $ | 17,248,203 | $ | – | $ | – | $ | 17,248,203 | ||||||||

| ||||||||||||||||

| ||||||||||||||||

Other Financial Instruments | ||||||||||||||||

| ||||||||||||||||

Liabilities | ||||||||||||||||

Securities Sold Short | ||||||||||||||||

Basic Materials | $ | (2,599,954) | $ | – | $ | – | $ | (2,599,954) | ||||||||

Communications | (2,335,187) | – | – | (2,335,187) | ||||||||||||

Consumer Cyclical | (2,031,848) | – | – | (2,031,848) | ||||||||||||

Consumer Non-cyclical | (548,690) | – | – | (548,690) | ||||||||||||

Diversified | (9,774) | – | – | (9,774) | ||||||||||||

Energy | (1,897,732) | – | – | (1,897,732) | ||||||||||||

Financials | (2,221,747) | – | – | (2,221,747) | ||||||||||||

Industrials | (1,410,761) | – | – | (1,410,761) | ||||||||||||

Technology | (397,522) | – | – | (397,522) | ||||||||||||

| ||||||||||||||||

Total | $ | (13,453,215) | $ | – | $ | – | $ | (13,453,215) | ||||||||

| ||||||||||||||||

The Fund recognizes transfers between levels as of the end of the fiscal year. For the fiscal year ended September 30, 2014, the Fund did not have any transfers between Level 1 and Level 2 securities. There were no Level 3 securities held during the period.

Offering Costs: The Fund incurred offering costs during the fiscal year ended September 30, 2014. These offering costs, including fees for printing initial prospectuses, legal and registration fees, are being amortized over the first twelve months from the inception date of the Fund. Amounts amortized through September 30, 2014 are shown on the Fund’s Statement of Operations within other expenses.

Fund Expenses: Some expenses can be directly attributed to the Fund and are apportioned among the classes based on average net assets of each class.

Annual Report | September 30, 2014 | 23 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

Trust Expenses: Some expenses of the Trust can be directly attributed to the Fund. Expenses that cannot be directly attributed to the Fund are apportioned among all funds in the Trust based on average net assets of each fund.

Class Expenses: Expenses that are specific to a class of shares are charged directly to that share class. Fees provided under the distribution (Rule 12b-1) and/or shareholder service plans for a particular class of the Fund are charged to the operations of such class.

Federal Income Taxes: The Fund complies with the requirements under Subchapter M of the Internal Revenue Code of 1986 applicable to regulated investment companies and intends to distribute substantially all of its net taxable income and net capital gains, if any, each year so that it will not be subject to excise tax on undistributed income and gains. The Fund is not subject to income taxes to the extent such distributions are made.

As of and during the fiscal year ended September 30, 2014, the Fund did not have a liability for any unrecognized tax benefits in the accompanying financial statements. The Fund files U.S. federal, state and local income tax returns as required. The Fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return for federal purposes and four years for most state returns. The Fund’s Administrator has analyzed the Fund’s tax positions taken on federal and state income tax returns for all open tax years and has concluded that as of September 30, 2014, no provision for income tax is required in the Fund’s financial statements related to these tax positions.

Investment Transactions and Investment Income: Investment transactions are accounted for on the date the investments are purchased or sold (trade date basis). Net realized gains and losses from investment transactions are reported on an identified cost basis. Interest income, which includes accretion of discounts and amortization of premiums, is accrued and recorded as earned. Dividend income is recognized on the ex-dividend date. All of the realized and unrealized gains and losses and net investment income, are allocated daily to each class in proportion to its average daily net assets.

Distributions to Shareholders: The Fund normally pays dividends and distributes capital gains, if any, on an annual basis. Income dividend distributions are derived from interest and other income the Fund receives from its investments, including short term capital gains. Long term capital gain distributions are derived from gains realized when the Fund sells a security it has owned for more than one year. The Fund may make additional distributions and dividends at other times if its portfolio manager or managers believe doing so may be necessary for the Fund to avoid or reduce taxes. Net investment income/(loss) and net realized gain/(loss) may differ for financial statement and tax purposes.

24 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

3. TAX BASIS INFORMATION

Reclassifications: As of September 30, 2014, permanent differences in book and tax accounting were reclassified. The following reclassifications have been made on the Statement of Assets and Liabilities and have no impact on the net asset value of the Fund:

| Paid-in Capital | Accumulated Net Investment Income | Accumulated Net Realized Loss on Investments | ||||||||||

| ||||||||||||

| $ | 0 | $ | 226,898 | $ | (226,898) | |||||||

Tax Basis of Distributions to Shareholders: The character of distributions made during the period from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or realized gain were recorded by the Fund. The amounts and characteristics of tax basis distributions and composition of distributable earnings/(accumulated losses) are finalized at fiscal year-end.

The tax character of distributions paid by the Fund for the fiscal year ended September 30, 2014 were as follows:

| Distributions Paid From: | 2014 | |||

| ||||

Ordinary Income | $ | 386,769 | ||

| ||||

Total | $ | 386,769 | ||

| ||||

Components of Distributable Earnings on a Tax Basis: As of September 30, 2014, the components of distributable earnings on a tax basis were as follows:

Undistributed ordinary income | $ | 1,351,210 | ||

Accumulated Capital Gains | 504,148 | |||

Net unrealized depreciation on investments and securities sold short | (179,912) | |||

Other cumulative effect of timing differences | (45) | |||

| ||||

Total | $ | 1,675,401 | ||

| ||||

Unrealized Appreciation and Depreciation on Investments: As of September 30, 2014, the aggregate cost of investments, gross unrealized appreciation/(depreciation) and net unrealized appreciation for Federal tax purposes were as follows:

Gross unrealized appreciation (excess of value over tax cost) | $ | 358,830 | ||

Gross unrealized depreciation (excess of tax cost over value) | (614,942) | |||

Net appreciation on short sales | 76,200 | |||

| ||||

Net unrealized depreciation | $ | (179,912) | ||

| ||||

Cost of investments for income tax purposes | $ | 17,504,315 | ||

| ||||

Annual Report | September 30, 2014 | 25 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

Capital Losses: As of September 30, 2014, the Fund had no accumulated capital loss carryforwards.

4. SECURITIES TRANSACTIONS

Purchases and sales of securities, excluding short-term securities and securities sold short, during the fiscal year ended September 30, 2014, were as follows:

| Purchases of Securities | Proceeds from Sales of Securities | |||

| ||||

| $ 83,091,031 | $ 84,300,876 | |||

5. BENEFICIAL SHARE TRANSACTIONS

The capitalization of the Trust consists of an unlimited number of shares of beneficial interest with no par value per share. Holders of the shares of the Fund of the Trust have one vote for each share held and a proportionate fraction of a vote for each fractional share. All shares issued and outstanding are fully paid and are non-assessable, transferable and redeemable at the option of the shareholder. Shares have no pre-emptive rights.

Transactions in common shares were as follows:

| For the Year Ended September 30, 2014 | For the Period Ended September 30, 2013 (a) | |||||||

Investor Class | ||||||||

Shares sold | 12,035 | 505,279 | ||||||

Shares issued in reinvestment of distributions to shareholders | 17,200 | – | ||||||

Shares redeemed | (10,519) | (4) | ||||||

|

|

|

| |||||

Net increase in shares outstanding | 18,716 | 505,275 | ||||||

|

|

|

| |||||

Institutional Class | ||||||||

Shares sold | 3,511,372 | 612,556 | ||||||

Shares issued in reinvestment of distributions to shareholders | 21,706 | – | ||||||

Shares redeemed | (3,325,663) | (1,598) | ||||||

|

|

|

| |||||

Net increase in shares outstanding | 207,415 | 610,958 | ||||||

|

|

|

| |||||

| (a) | Commenced operations on January 2, 2013. |

Control is defined by the 1940 Act as the beneficial ownership, either directly or through one or more controlled companies, of more than 25% of the voting securities of a company. The Fund has one affiliated shareholder representing approximately 77% of total Fund shares. Investment activities of these shareholders could have a material impact on the Fund.

26 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

6. MANAGEMENT AND RELATED PARTY TRANSACTIONS

Investment Advisory: Cognios Capital, LLC (“Cognios Capital” or the “Adviser”), subject to the authority of the Board, is responsible for the overall management and administration of the Fund’s business affairs. The Adviser manages the investments of the Fund in accordance with the Fund’s investment objective, policies and limitations and investment guidelines established by the Adviser and the Board.

Pursuant to the Investment Advisory Agreement (the “Advisory Agreement”), the Fund pays the Adviser an annual management fee of 1.50% based on the Fund’s average daily net assets. The management fees are paid on a monthly basis. The initial term of the Advisory Agreement is two years. The Board may extend the Advisory Agreement for additional one-year terms. The Board, shareholders of the Fund or Adviser may terminate the Advisory Agreement upon 60 days’ notice.

Pursuant to a fee waiver letter agreement (the “Fee Waiver Agreement”), the Adviser has agreed contractually to reduce the fees payable to it under the Advisory Agreement (but not below zero) and/or reimburse other expenses of the Fund attributable to services provided by the Fund’s administrator and its affiliates (including, but not limited to, organizational expenses and offering costs), to the extent necessary to limit the Total Annual Fund Operating Expenses of each of the Investor Class and Institutional Class shares of the Fund (exclusive of brokerage costs, interest, taxes, dividends, litigation expenses, indemnification amounts, borrowing costs, brokerage expenses and dividend expenses on securities sold short, distribution/12b-1 fees and extraordinary expenses) to 2.00% of the Fund’s average annual net assets. The Fee Waiver Agreement is in effect through January 31, 2015, and may not be terminated or modified prior to this date except with the approval of the Fund’s Board of Trustees. The Adviser will be permitted to recover expenses on a class-by-class basis expenses it has borne through the Fee Waiver Agreement to the extent that the Fund’s expenses in later periods fall below the annual rates set forth in the Fee Waiver Agreement. The Fund will not be obligated to pay any such deferred fees and expenses more than three years after the end of the fiscal year in which the fees and expenses were deferred.

For the fiscal year ended September 30, 2014, the fee waivers and/or reimbursements were as follows:

Fees Waived/Reimbursed by Adviser | ||||

| ||||

Investor Class | $ | (92,011) | ||

Institutional Class | (125,422) | |||

| ||||

TOTAL | $ | (217,433) | ||

| ||||

As of September 30, 2014, the balances of recoupable expenses for each class were as follows:

| Expiring in 2016 | Expiring in 2017 | |||||||

| ||||||||

Investor Class | $ | (79,516) | $ | (92,011) | ||||

Institutional Class | (88,889) | (125,422) | ||||||

Annual Report | September 30, 2014 | 27 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

Administrator: ALPS Fund Services, Inc. (“ALPS”) serves as administrator to the Fund. The Fund has agreed to pay expenses incurred in connection with its administrative activities. Pursuant to the Administration, Bookkeeping and Pricing Services Agreement, ALPS will provide operational services to the Fund including, but not limited to, fund accounting and fund administration and generally assist in the Fund’s operations.

The Fund’s administration fee is accrued on a daily basis and paid on a monthly basis following the end of the month, based on the greater of (a) an annual total fee of $135,000; or (b) the following basis point fee schedule:

| Average Total Net Assets | Contractual Fee | |

Between $0-$250M | 0.10% | |

$250M-$500M | 0.07% | |

Above $500M | 0.03% |

Annually thereafter, the parties agree to reevaluate the compensation paid under the agreement by the Trust on behalf of the Fund to ALPS for the services it performs for the Fund.

ALPS is reimbursed by the Fund for certain out-of-pocket expenses. ALPS has agreed to reimburse the Fund for expenses relating to insurance and certain routine legal services for the fiscal period ended September 30, 2014.

Transfer Agent: ALPS serves as transfer agent for the Fund under a Transfer Agency and Services Agreement with the Trust. Under this agreement, ALPS is paid an annual base fee of $25,000 for services performed on behalf of the Fund plus fees for open accounts and is reimbursed for certain out-of-pocket expenses.

Compliance Services: ALPS provides services as the Fund’s Chief Compliance Officer to monitor and test the policies and procedures of the Fund in conjunction with requirements under Rule 38a-1 of the 1940 Act under a Chief Compliance Officer Services Agreement. Under this agreement, ALPS is paid an annual base fee of $20,000 for services performed on behalf of the Fund and is reimbursed for certain out-of-pocket expenses.

Principal Financial Officer: ALPS receives an annual base fee of $10,000 for providing Principal Financial Officer services to the Fund and is reimbursed for certain out-of-pocket expenses.

Distribution: ALPS Distributors, Inc. (the “Distributor”) (as affiliate of ALPS Fund Services, Inc.) acts as the principal underwriter of the Fund’s shares pursuant to a Distribution Agreement with the Trust. Shares of the Fund are offered on a continuous basis through the Distributor, as agent of the Fund. The Distributor is not obligated to sell any particular amount of shares and is not entitled to any compensation for its services as the Fund’s principal underwriter.

The Fund has adopted a Distribution and Services Plan (the “Plan”) pursuant to Rule 12b-1 of the 1940 Act for its Investor Class shares. The Plan allows the Fund to use Investor Class assets to pay fees in connection with the distribution and marketing of Investor Class shares and/or the provision of shareholder services to Investor Class shareholders. The Plan permits payment for services in connection with the administration of plans or programs that use Investor Class shares

28 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

of the Fund, if any, as their funding medium and for related expenses. The Plan permits the Fund to make total payments at an annual rate of up to 0.25% of the Fund’s average daily net assets attributable to its Investor Class shares. Plan fees are shown as distribution and service fees on the Statement of Operations.

7. TRUSTEES

As of September 30, 2014, there were four Trustees, three of whom are not “interested persons” (as defined in the 1940 Act) of the Trust (the “Independent Trustees”). Prior to October 1, 2014, the Independent Trustees received a quarterly retainer of $2,000, plus $1,000 for each regular Board or Committee meeting attended, $1,000 for each special telephonic Board or Committee meeting attended and $1,000 for each special in-person Board meeting attended. Effective October 1, 2014, the Independent Trustees receive a quarterly retainer of $4,000, plus $2,000 for each regular Board or Committee meeting attended, $2,000 for each special telephonic Board or Committee meeting attended and $2,000 for each special in-person Board meeting attended. The Independent Trustees are also reimbursed for all reasonable out-of-pocket expenses relating to attendance at meetings and for meeting-related expenses. Officers of the Trust and Trustees who are interested persons of the Trust receive no salary or fees from the Trust.

8. INDEMNIFICATIONS

Under the Trust’s organizational documents, its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust enters into contracts with service providers that may contain general indemnification clauses which may permit indemnification to the extent permissible under applicable law. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred.

9. CHANGES IN ACCOUNTANTS

On June 30, 2014, KPMG LLP acquired certain assets of ROTHSTEIN-KASS, P.A. (d/b/a Rothstein Kass & Company, P.C.) and certain of its affiliates (“Rothstein Kass”), the independent public accounting firm for the Fund. As a result of this transaction, on June 30, 2014, Rothstein Kass resigned as the independent registered public accounting firm for the Fund.

The Fund commenced operations on January 2, 2013 and the Fund’s fiscal year end is September 30th. The report of Rothstein Kass on the Fund’s financial statements for the fiscal year ended September 30, 2013 contained no adverse opinion or disclaimer of opinion and were not qualified or modified as to uncertainty, audit scope or accounting principles.

During the fiscal year ended September 30, 2013 and through June 30, 2014, there were no disagreements with Rothstein Kass on any matter of accounting principles or practices, financial statement disclosure or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of Rothstein Kass, would have caused Rothstein Kass to make reference thereto in its reports on the financial statements for such year.

Annual Report | September 30, 2014 | 29 |

Table of Contents

| Cognios Market Neutral Large Cap Fund | ||

Notes to Financial Statements |

September 30, 2014 |

During the fiscal year ended September 30, 2013 and through June 30, 2014, there were no reportable events (as defined in Item 304(a)(1)(v)) of Regulation S-K).

The Board of Trustees of the Trust approved the selection of KPMG LLP to serve as the Fund’s independent registered public accounting firm for the Fund’s fiscal year ending September 30, 2014 at an in-person meeting held on August 22, 2014. During the fiscal year ended September 30, 2013 and through June 30, 2014, the Trust on behalf of the Fund had not consulted with Rothstein Kass regarding either (i) the application of accounting principles to a specified transaction, either completed or proposed; or the type of audit opinion that might be rendered on the Fund’s financial statements, and neither a written report was provided to the Trust on behalf of the Fund or oral advice was provided that Rothstein Kass concluded was an important factor considered by the Trust on behalf of the Fund in reaching a decision as to the accounting, auditing or financial reporting issue; or (ii) any matter that was either the subject of a disagreement, as that term is defined in Item 304(a)(1)(iv) of Regulation S-K and the related instructions to Item 304 of Regulation S-K, or a reportable event, as that term is defined in Item 304(a)(1)(v) of Regulation S-K.

30 | www.cogniosfunds.com |

Table of Contents

| Cognios Market Neutral Large Cap Fund |

Report of Independent Registered

Public Accounting Firm

The Board of Trustees and Shareholders

ALPS Series Trust: