KTS Comments: 1/5/2014

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22819

ETFis Series Trust I

(Exact name of registrant as specified in charter)

6 East 39th Street, 10th Floor, New York, New York 10016

(Address of principal executive offices) (Zip code)

William J. Smalley, President, 6 East 39th Street, 10th Floor, New York, New York 10016

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 593-4383

Date of fiscal year end: 10/31/2014

Date of reporting period: 10/31/2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Annual Report

October 31, 2014

InfraCap MLP ETF

|

| TABLE OF CONTENTS |

| October 31, 2014 |

| Shareholder Letter |

| October 31, 2014 |

Dear Fellow Shareholders:

We are pleased to present the annual report for the InfraCap MLP ETF (the “Fund”). We introduced the Fund on October 1, 2014. The net asset value (NAV) decreased from $25.00 to $24.21 from inception to October 31, 2014.

While the stock market has performed well, energy prices have waned over the past few months and as a result, the Fund, like MLPs and other energy focused indices and benchmarks, struggled to keep up with the U.S. stock market.

Over the next 12 months, we believe that energy prices will stabilize if the economy continues to grow. With monetary stimulus likely to slow, we expect periods of volatility and income will continue to be difficult for investors to find.

While investing in MLPs will always carry risks, we believe that the unique structure of these securities can help provide diversification and higher income streams in many market conditions.

On the following pages, you will find a brief review of the Fund as well as its performance for the period ended October 31, 2014. You will also find the financial statements and portfolio information.

Thank you for investing in the InfraCap MLP ETF.

Sincerely,

William Smalley

President

ETFis Series Trust I

This material must be accompanied or preceded by the prospectus.

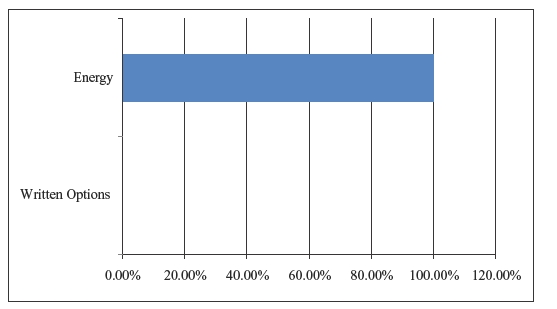

| Portfolio Summary |

| October 31, 2014 |

| Written Options | 0.1 | % | |

| Energy | 99.9 | % | |

Management’s Discussion of Operations

This discussion of operations relates to a short fiscal period. InfraCap MLP ETF (the Fund) began operations on October 1, 2014 (commencement of operations), and the fiscal year ended on October 31, 2014. During this period, the net asset value of the Fund fell from $25.00 to $24.21.

The Fund was launched during a period of weakness in oil prices. Additionally, stock prices of energy companies broadly declined during the month of October. Prices of publicly-traded Master Limited Partnerships (MLPs) were impacted by these market pressures. For the period ended October 31, 2014 the fund returned (3.17)% while its index, the Alerian MLP Infrastructure Index, returned (3.22)%.

Key elements of the portfolio strategy for the Fund were initiated during the month:

| • | Portfolio weightings of individual stocks were determined based on the manager’s proprietary valuation models and the dynamics of pending or anticipated corporate events; |

| • | General partner interests were evaluated relative to the total return potential of related master limited partnership interests, and positions in the general partners were established when determined to offer superior total return potential; |

| • | Modest leverage was added to take advantage of share price weaknesses identified in specific securities; |

| • | Initial options trades were executed with the objective of generating incremental investment returns. As of October 31, 2014, the options transactions have not had a material impact on the performance of the Fund. |

These key elements will tend to make the returns of the Fund different than Alerian MLP Infrastructure Index, and this period covered by the report was no exception.

At October 31, 2014, the Fund utilized leverage of 9.3% of its net asset value.

It should be noted that the Fund is fully taxed as a corporation. This tax treatment is the same as for other open-end and closed-end funds that focus on the MLP asset class. One consequence is that the Fund’s net asset value may be impacted by a tax reserve. The gross expenses that are reported in the Fund’s financial highlights include the tax reserve. The net expenses reported in the financial highlights exclude the tax reserve.

Another consequence of our tax status is that owners of the Fund will receive a Form 1099 for tax reporting purposes. So shareholders of the Fund do not face the complications of Schedule K-1 reporting, state filing requirements and UBTI (unrelated business tax income) that direct owners of MLP shares must address.

| Portfolio Summary (continued) |

| October 31, 2014 |

Performance as of 10/31/2014

| | Average Annual Total Return |

| | Fund

Net Asset Value | | Fund

Market Price | | Alerian MLP

Infrastructure Index(1) |

| Since Inception(2) | (3.17 | )% | | (3.36 | )% | | (3.22 | )% |

| 1 | The index shown is reflective of the Alerian MLP Index as of October 31, 2014. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.infracapmlp.com or call toll free (888) 383-4184. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

S&P 500® Total Return Index is the Standard & Poor's composite index of 500 stocks, a widely recognized, unmanaged index of common stock prices. The Alerian MLP Infrastructure Index is comprised of 25 midstream energy Master Limited Partnerships. An investor cannot invest directly in an unmanaged index.

Premium/Discount Information

| | | | | Market Price

Above or Equal to NAV | | Market Price

Below NAV |

| | | Basis Point

Differential | | Number

of Days | | % of

Total Days | | Number

of Days | | % of

Total Days |

| InfraCap MLP Fund | | | | | | | | | | | | | | | | |

| October 2, 2014 – October 31, 2014 | | 0-24.99 | | | | 8 | | | | 36 | % | | | 2 | | | 9% |

| | | 25-49.99 | | | | 1 | | | | 5 | % | | | 2 | | | 9% |

| | | 50-74.99 | | | | 1 | | | | 5 | % | | | 1 | | | 5% |

| | | 75-99.99 | | | | 0 | | | | 0 | % | | | 1 | | | 5% |

| | | >100 | | | | 4 | | | | 17 | % | | | 2 | | | 9% |

| Total | | | | | | | 14 | | | | 63 | % | | | 8 | | | 37% |

| Shareholder Expense Example |

As a shareholder of the Fund, you incur ongoing costs including advisory fees and other fund expenses, if any. The following example is intended to help you understand your ongoing costs (in dollars and cents) of investing in a Fund and to compare these costs with the ongoing costs of investing in other funds. The example is based on an investment of $1,000 invested at October 1, 2014 (commencement of operations) and held throughout the entire period ended October 31, 2014.

Actual expenses

The first line under each Fund in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for your Fund under the heading entitled “Expenses Paid During Period 10/1/2014 Through 10/31/2014” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second line under each Fund in the table provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of Fund shares. Therefore, the second line under each Fund in the table is useful in comparing ongoing Fund costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value

10/1/14 | | Ending

Account

Value

10/31/14 | | Annualized

Expense Ratios

for the Period | | Expenses Paid

During Period

10/1/2014

Through

10/31/2014(1) |

| InfraCap MLP ETF | | | | | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 968.29 | | | | 0.95% | | | | $0.79 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.42 | | | | 0.95% | | | | $4.84 | |

| 1 | Actual expenses are calculated using each Fund’s annualized expense ratio, which includes waived fees or reimbursed expenses, if any, by the average account value for the period, multiplied by 30/365 (to reflect commencement of operations). Hypothetical expenses are calculated for the six month period. |

| Schedule of Investments — InfraCap MLP ETF |

| October 31, 2014 |

| Security Description | | Shares | | Value ($) |

| Common Stocks — 109.3%(1) | | | | | | | | |

| Energy — 109.3% | | | | | | | | |

| Access Midstream Partners LP | | | 9,140 | | | $ | 569,330 | |

| Atlas Energy LP | | | 2,860 | | | | 107,336 | |

| Atlas Pipeline Partners LP | | | 1,215 | | | | 44,591 | |

| Buckeye Partners LP | | | 4,565 | | | | 344,201 | |

| Crestwood Midstream Partners LP | | | 7,445 | | | | 148,081 | |

| DCP Midstream Partners LP | | | 1,525 | | | | 80,749 | |

| El Paso Pipeline Partners LP | | | 4,285 | | | | 174,185 | |

| Enbridge Energy Partners LP | | | 4,890 | | | | 176,382 | |

| Energy Transfer Equity LP | | | 2,055 | | | | 119,930 | |

| Energy Transfer Partners LP | | | 5,690 | | | | 366,607 | |

| EnLink Midstream LLC | | | 1,250 | | | | 47,375 | |

| EnLink Midstream Partners LP | | | 1,875 | | | | 56,250 | |

| Enterprise Products Partners LP(2) | | | 11,420 | | | | 421,398 | |

| EQT Midstream Partners LP | | | 1,220 | | | | 108,068 | |

| Genesis Energy LP | | | 2,275 | | | | 109,155 | |

| Kinder Morgan Energy Partners LP | | | 7,200 | | | | 675,359 | |

| Magellan Midstream Partners LP | | | 5,405 | | | | 442,507 | |

| MarkWest Energy Partners LP | | | 7,255 | | | | 508,212 | |

| NuStar Energy LP | | | 115 | | | | 6,992 | |

| ONEOK Partners LP | | | 2,570 | | | | 131,327 | |

| ONEOK, Inc. | | | 1,860 | | | | 109,628 | |

| Plains All American Pipeline LP | | | 7,325 | | | | 412,764 | |

| Plains GP Holdings LP, Class A | | | 4,025 | | | | 115,437 | |

| Regency Energy Partners LP | | | 5,320 | | | | 159,600 | |

| Spectra Energy Partners LP | | | 360 | | | | 19,440 | |

| Sunoco Logistics Partners LP | | | 6,505 | | | | 310,484 | |

| Targa Resources Corp. | | | 500 | | | | 64,315 | |

| Targa Resources Partners LP | | | 3,155 | | | | 192,707 | |

| Tesoro Logistics LP | | | 2,065 | | | | 116,260 | |

| Western Gas Equity Partners LP | | | 2,055 | | | | 126,835 | |

| Western Gas Partners LP | | | 2,165 | | | | 151,334 | |

| Williams Cos., Inc. (The) | | | 2,245 | | | | 124,620 | |

| Williams Partners LP | | | 1,455 | | | | 75,005 | |

| TOTAL INVESTMENTS — 109.3% | | | | | | | | |

| (Cost $6,598,845) | | | | | | | 6,616,464 | |

| Liabilities in Excess of Other Assets — (9.3)% | | (564,600 | ) |

| Net Assets — 100.0% | | | | | | $ | 6,051,864 | |

| Security Description | | Number of

Contracts | | Value ($) |

| Written Options — (0.0)%(2) | | | | | | | | |

| Puts | | | | | | | | |

| Enterprise Products | | | | | | | | |

| Partners LP, Expires 01/17/15, | | | | | | | | |

| Strike Price $35.00 | | | (20 | ) | | $ | (2,100 | ) |

| Calls | | | | | | | | |

| Enterprise Products | | | | | | | | |

| Partners LP, Expires 01/17/15, | | | | | | | | |

| Strike Price $40.00 | | | (10 | ) | | | (550 | ) |

| | | | | | | | | |

| TOTAL WRITTEN OPTIONS — (0.0)%(3) | | | | |

| (Premiums Received $2,313) | | | | | | $ | (2,650 | ) |

| (1) | Substantially all the securities, or a portion thereof, have been pledged as collateral for open written option contracts. The aggregate market value of the collateral at October 31, 2014 was $3,484,982. |

| (2) | Subject to written put and call options. |

| (3) | Amount rounds to less than 0.05%. |

The accompanying notes are an integral part of these financial statements.

| Statement of Assets and Liabilities |

| October 31, 2014 |

| | | InfraCap MLP

ETF |

| Assets: | | |

| Investments, at cost | | $ | 6,598,845 | |

| Investments, at value | | | 6,616,464 | |

| Receivables: | | | | |

| Investment securities sold | | | 29,932 | |

| Return of capital from master limited partnerships | | | 35,377 | |

| Dividends and interest receivable | | | 1,314 | |

| Total Assets | | | 6,683,087 | |

| | | | | |

| Liabilities: | | | | |

| Due to custodian and broker | | | 267,922 | |

| Payables: | | | | |

| Subadvisory and Advisory fees | | | 3,023 | |

| Investment securities purchased | | | 352,051 | |

| Deferred tax liability | | | 5,577 | |

| Written Options, at value (premiums received $2,313) | | | 2,650 | |

| Total Liabilities | | | 631,223 | |

| Net Assets | | $ | 6,051,864 | |

| | | | | |

| Net Assets Consist of: | | | | |

| Paid-in capital | | $ | 6,041,863 | |

| Accumulated net investment loss, net of income taxes | | | (1,099 | ) |

| Undistributed net realized gain on investments, written options, net of income taxes | | | 5 | |

| Net unrealized appreciation on investments, written options, net of income taxes | | | 11,095 | |

| Net Assets | | $ | 6,051,864 | |

| Shares outstanding (unlimited number of shares of beneficial interest authorized, no par value) | | | 250,004 | |

| Net asset value per share | | $ | 24.21 | |

The accompanying notes are an integral part of these financial statements.

| | | InfraCap MLP

ETF |

| | | For the Period

Ended

October 31, 2014* |

| Investment Income: | | | | |

| Distributions from master limited partnerships | | $ | 35,377 | |

| Less: Return of capital distributions | | | (35,377 | ) |

| Dividend income | | | 1,311 | |

| Total Investment Income | | | 1,311 | |

| | | | | |

| Expenses: | | | | |

| Advisory fees | | | 239 | |

| Subadvisory fees | | | 2,784 | |

| Deferred income tax benefit | | | (613 | ) |

| Total Expenses | | | 2,410 | |

| Net Investment Loss | | | (1,099 | ) |

| | | | | |

| Net Realized Gain on: | | | | |

| Investments | | | 8 | |

| Deferred income tax expense | | | (3 | ) |

| Total Realized Gain | | | 5 | |

| | | | | |

| Change in Net Unrealized Appreciation (Depreciation) on: | | | | |

| Investments | | | 17,619 | |

| Written Options | | | (337 | ) |

| Deferred income tax expense | | | (6,187 | ) |

| Change in Net Unrealized Appreciation | | | 11,095 | |

| Net Realized and Change in Unrealized Gain | | | 11,100 | |

| | | | | |

| Net Increase in Net Assets Resulting from Operations | | $ | 10,001 | |

| | | | |

| * From October 1, 2014 (commencement of operations) through October 31, 2014. | | | | |

The accompanying notes are an integral part of these financial statements.

| Statement of Changes in Net Assets |

| | | InfraCap MLP

ETF |

| | | For the Period

Ended

October 31, 2014* |

| Increase (Decrease) in Net Assets Resulting from Operations: | | | | |

| Net investment loss, net of income taxes | | $ | (1,099 | ) |

| Net realized gain on investments, net of income taxes | | | 5 | |

| Net change in net unrealized appreciation, net of income taxes | | | 11,095 | |

| Net increase in net assets resulting from operations | | | 10,001 | |

| | | | | |

| Shareholder Transactions: | | | | |

| Proceeds from shares sold | | | 6,041,863 | |

| Cost of shares redeemed | | | — | |

| Net increase in net assets resulting from shareholder transactions | | | 6,041,863 | |

| Net increase in net assets | | | 6,051,864 | |

| | | | | |

| Net Assets: | | | | |

| Beginning of period | | | — | |

| End of period | | $ | 6,051,864 | |

| Accumulated net investment loss | | | (1,099 | ) |

| | | | | |

| Shares Created and Redeemed: | | | | |

| Shares outstanding, beginning of period | | | — | |

| Shares sold | | | 250,004 | |

| Shares redeemed | | | — | |

| Shares outstanding, end of period | | | 250,004 | |

| | | | |

| * From October 1, 2014 (commencement of operations) through October 31, 2014. | | | | |

The accompanying notes are an integral part of these financial statements.

| | InfraCap MLP

ETF |

| | Period Ended

October 31, 20141 |

| Per Share Data for a Share Outstanding Throughout the Period: | | | |

| Net asset value, beginning of period | $ | 25.00 | |

| Investment operations: | | | |

| Net investment loss2 | | (0.01 | ) |

| Net realized and unrealized loss on investments8 | | (0.78 | ) |

| Total from investment operations | | (0.79 | ) |

| Net Asset Value, End of Period | $ | 24.21 | |

| Net Asset Value Total Return3 | | (3.17 | )% |

| Net assets, end of period (000’s omitted) | $ | 6,052 | |

| | | | |

| RATIOS/SUPPLEMENTAL DATA: | | | |

| Ratios to Average Net Assets: | | | |

| Gross expenses, including deferred income tax expense/benefit9 | | 2.70 | %4 |

| Net expenses, excluding deferred income tax expense/benefit9 | | 0.95 | %4 |

| Net investment loss10 | | (0.35 | )%4 |

| Portfolio turnover rate5 | | — | %6,7 |

| |

| 1 | From October 1, 2014 (commencement of operations) to October 31, 2014. |

| 2 | Based on average shares outstanding. |

| 3 | Net asset value total return is calculated assuming an initial investment made at the net asset value on the first day of the period, reinvestment of dividends and distributions at net asset value during the period, and redemption at net asset value on the last day of the period. Total return calculated for a period of less than one year is not annualized. |

| 4 | Annualized. |

| 5 | Portfolio turnover excludes the value of portfolio securities received or delivered as a result of in-kind creations or redemptions of the Fund’s capital shares. |

| 6 | Amount rounds to less than 1%. |

| 7 | Not annualized. |

| 8 | The per share amount of realized and unrealized loss on investments does not accord with the amounts reported in the Statement of Operations due to the timing of creation of fund shares in relation to fluctuating market values. |

| 9 | Deferred tax expense/benefit estimate for the ratios of expenses to average net assets is derived from net investment loss and net realized and unrealized gains on investments. |

| 10 | The ratio of net investment loss to average net assets is net of a deferred tax benefit estimate derived from net investment loss only. |

The accompanying notes are an integral part of these financial statements.

| Notes to Financial Statements |

| October 31, 2014 |

1. ORGANIZATION

The ETFis Series Trust I (the “Trust”) was organized as a Delaware statutory trust on September 20, 2012 and is registered with the Securities and Exchange Commission (the “SEC”) as an open-end management investment company under the Investment Company Act of 1940 (the “1940 Act”). The Trust currently consists of three investment portfolios, InfraCap MLP ETF (the “Fund”), Manna Core Equity Enhanced Dividend Income Fund and Tuttle Tactical Management U.S. Core ETF; however, only the Fund has commenced operations. The shares of the Fund are referred to herein as “Fund Shares” or “Shares”. The offering of Shares is registered under the Securities Act of 1933, as amended (the “Securities Act”). At October 31, 2014, InfraCap MLP ETF was the only fund in operations. The Fund commenced operations on October 1, 2014.

The Fund’s investment objective is to seek total return primarily through investments in equity securities of publicly traded master limited partnerships and limited liability companies taxed as partnerships (“MLPs”).

2. SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates

These financial statements are prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”), which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and reported amounts of increases and decreases in the net assets from operations during the reporting period. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Fund:

Indemnification

In the normal course of business, the Fund may enter into contracts that contain a variety of representations which provide general indemnifications for certain liabilities. The Fund’s maximum exposure under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

MLP Distributions

The Fund expects that a portion of the distributions it receives from MLPs may be treated as a tax-deferred return of capital, thus reducing the Fund’s current tax liability. However, the amount of taxes currently paid by the Fund will vary depending on the amount of income and gains derived from investments and/or sales of MLP interests, and such taxes will reduce your return from an investment in the Fund.

Investment Valuation

The Net Asset Value (“NAV”) is determined as of the close of trading (generally, 4:00 PM Eastern Time) on each day the New York Stock Exchange (“NYSE”) is open for trading. NAV per share is calculated by dividing the Fund’s net assets by the number of fund shares outstanding.

Securities Valuation

Security holdings traded on a national securities exchange are valued based on their last sale price. Price information on listed securities is taken from the exchange where the security is primarily traded. Securities regularly traded in an over the counter market are valued at the latest quoted sale price in such market or in the case of the NYSE or NASDAQ, at the NYSE or NASDAQ Official Closing Price. If market quotations are not readily available, or if it is determined that a quotation of a security does not represent fair value, then the security is valued at fair value as determined in good faith using procedures adopted by the Trust’s Board of Trustees (the “Board”). Short-term securities with 60 days or less remaining to maturity are valued using the amortized cost method, which approximates current market value.

Purchased and written options contracts listed on exchanges are valued at their reported mean of bid and ask quotations; over-the-counter derivative contracts are fair valued using price evaluations provided by a pricing service approved by the Board of Trustees of the Trust.

| Notes to Financial Statements (continued) |

| October 31, 2014 |

Fair Value Measurement

Accounting Standards Codification, Fair Value Measurements and Disclosures (“ASC 820”) defines fair value, establishes a framework for measuring fair value in accordance with GAAP, and requires disclosure about fair value measurements. It also provides guidance on determining when there has been a significant decrease in the volume and level of activity for an asset or liability, when a transaction is not orderly, and how that information must be incorporated into fair value measurement. Under ASC 820, various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the following hierarchy:

| • | Level 1 — Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| • | Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar securities, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| • | Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following summarizes inputs used as of October 31, 2014 in valuing the Fund’s assets and liabilities carried at fair value:

| | | Level 1 | | Level 2 | | Level 3 |

| Common Stocks | | $ | 6,616,464 | | | $ | — | | | $ | — | |

| Other Financial Instruments* | | | (2,650 | ) | | | — | | | | — | |

| Total | | $ | 6,613,814 | | | $ | — | | | $ | — | |

* Other financial instruments include written option contracts, which are valued at fair value.

For significant movements between levels within the fair value hierarchy, the Fund has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement. There were no significant transfers between levels during the period ended October 31, 2014.

A reconciliation of assets in which Level 3 inputs are used in determining fair value is presented when there are significant Level 3 investments at the end of the period. There were no Level 3 securities as of October 31, 2014.

Security Transactions

Security transactions are accounted for on the trade date. Realized gains and losses on sales of investment securities are calculated using specific identification.

Master Netting Arrangements

Accounting Standards Update No. 2011-11 “Disclosures about Offsetting Assets and Liabilities” (“ASU 2011-11”) is generally intended to (i) help investors and other financial statement users to better assess the effect or potential effect of offsetting arrangements on a company’s financial position (ii) improve transparency in the reporting of how companies mitigate credit risk and (iii) facilitate comparisons between those entities that prepare their financial statements on the basis of US GAAP and those entities that prepare their financial statements on the basis of international financial reporting standards. ASU 2011-11 requires entities to disclose (i) gross and net information about both instruments and transactions eligible for offset in the financial statements and (ii) instruments and transactions subject to an agreement similar to a master netting agreement. ASU 2011-11 is limited in scope to the following financial instruments, to the extent they are offset in the financial statements or subject to an enforceable master netting arrangement or similar agreement: (i) recognized derivative instruments accounted for under ASC 815 (Derivatives and Hedging); (ii) repurchase agreements and reverse repurchase agreements; and (iii) securities borrowing and securities lending transactions.

In order to better define its contractual rights and to secure rights that will help the Fund mitigate its counterparty risk, the Fund may enter into an International Swaps and Derivatives Association, Inc. Master Agreement (“ISDA Master Agreement”) or similar agreement with its counterparties. An ISDA Master Agreement is a bilateral agreement between the Fund and a counterparty that governs over-the-counter derivatives (“OTC”), including forward contracts, and typically contains, among other things, collateral posting terms, netting and rights of set-off provisions in the event of a default and/or termination event. Under an ISDA Master Agreement, the Fund may, under certain circumstances, offset with the counterparty certain derivative financial instruments’ payables and receivables to create a single net payment. The provisions of the ISDA Master Agreement typically permit a single net payment in the event of a default (close-out netting) or similar event, including the bankruptcy or insolvency of the counterparty.

| Notes to Financial Statements (continued) |

| October 31, 2014 |

Collateral requirements generally differ by type of derivative. Collateral terms are contract-specific for OTC derivatives (e.g. foreign exchange contracts, options and certain swaps). Generally, for transactions traded under an ISDA Master Agreement, the collateral requirements are typically calculated by netting the marked to market amount for each transaction under such agreement and comparing that amount to the value of any collateral currently pledged by the Fund and the counterparty. Generally, the amount of collateral due from or to a counterparty must exceed a minimum transfer amount threshold before a transfer is required to be made. To the extent amounts due to the Fund from its derivatives counterparties are not fully collateralized, contractually or otherwise, the Fund bears the risk of loss from counterparty non-performance.

As of October 31, 2014, the Fund had written options with a fair value of $(2,650).

Investment Income and Expenses

Dividend income is recognized on the ex-dividend date. The Fund distributes all or substantially all of its net investment income to shareholders in the form of dividends. Expenses are recognized on the accrual basis.

3. INVESTMENT MANAGEMENT AND OTHER AGREEMENTS

Investment Advisory Agreement

The Trust has entered into an Investment Advisory Agreement (the “Advisory Agreement”) with ETFis Capital LLC, (the “Adviser”), on behalf of the Fund. Pursuant to the Advisory Agreement, the Adviser has overall supervisory responsibility for the general management and investment of the Fund’s securities portfolio. For its services, the Adviser is entitled to an annual rate of 0.075% of the Fund’s average daily net assets.

Sub-Advisory Agreement

Infrastructure Capital Advisors, LLC serves as investment sub-advisor (the “Sub-Adviser”) to the Fund. The Sub-Adviser provides investment advice and management services to the Fund. Pursuant to an investment sub-advisory agreement (“Investment Sub-Advisory Agreement”) among the Trust, the Sub-Adviser and the Advisor, the Sub-adviser receives an annual fee equal of 0.875% based on the average daily net assets. The Sub-Adviser has agreed to pay all expenses of the Fund, except the Sub-Adviser’s fee, the Adviser’s fee brokerage expenses, taxes, interest, litigation expenses, payments under any 12b-1 plan adopted by the Fund, and other non-routine or extraordinary expenses of the Fund.

Distribution Agreement (12b-1 Fees)

ETF Distributors LLC (the “Distributor”) serves as the Fund’s Distributor. The Distributor will not distribute shares in less than Creation Units, and does not maintain a secondary market in shares. The shares are expected to be traded in the secondary market.

The Board of Trustees has adopted a distribution and service plan, where the Fund is authorized to pay distribution fees in connection with the sale and distribution of its shares and pay service fees in connection with the provision of ongoing services to shareholders. No distribution fees are currently paid by the Fund and there are no current plans to impose the fees.

Operational Administrator

ETF Issuer Solutions Inc. (the “Administrator”), located at 6 E. 39th Street, Suite 1003, New York, New York 10016, serves as the Fund’s operational administrator. The Administrator supervises the overall administration of the Trust and the Fund including, among other responsibilities, the coordination and day-to-day oversight of the Fund’s operations, the service providers' communications with the Fund and each other and assistance with Trust, Board and contractual matters related to the Fund and other series of the Trust. The Administrator also provides persons satisfactory to the Board to serve as officers of the Trust.

Accounting Services Administrator, Custodian and Transfer Agent

The Bank of New York Mellon (“BNY Mellon”), located at One Wall Street, New York, New York 10286, directly and through its subsidiary companies, provides necessary administrative, accounting, tax and financial reporting for the maintenance and operations of the Trust as the Fund’s accounting services administrator. BNY Mellon also serves as the custodian for the Fund’s assets, and serves as transfer agent and dividend paying agent for the Fund.

4. CREATION AND REDEMPTION TRANSACTIONS

The Fund issues and redeems shares on a continuous basis at NAV in groups of 50,000 shares called “Creation Units.” Creation Units of the Fund are issued and redeemed generally in exchange for specified securities held by the Fund generally included in the Index and a specified cash payment. Redemptions of Creation Units are effected principally for cash. In each instance of such cash creations or redemptions, the Trust may impose transaction fees based on transaction expenses related to the particular exchange that will be higher than the transaction fees associated with in-kind purchases or redemptions.

| Notes to Financial Statements (continued) |

| October 31, 2014 |

Only “Authorized Participants” who have entered into contractual arrangements with the Distributor may purchase or redeem shares directly from the Fund. An Authorized Participant is either (i) a broker-dealer or other participant in the clearing process through the Continuous Net Settlement System of the National Securities Clearing Corporation or (ii) a DTC participant and, in each case, must have executed a Participant Agreement with the Distributor. Most retail investors will not qualify as Authorized Participants or have the resources to buy and sell whole Creation Units. Therefore, they will be unable to purchase or redeem the shares directly from the Fund. Rather, most retail investors will purchase shares in the secondary market with the assistance of a broker and will be subject to customary brokerage commissions or fees.

5. FEDERAL INCOME TAX

The Fund is taxed as a regular C-corporation for federal income tax purposes. Currently, the maximum marginal regular federal income tax rate of a corporation is 35 percent, but the Fund expects to pay tax at a rate of 34 percent. The Fund may be subject to a 20 percent federal alternative minimum tax on its federal alternative taxable income to the extent that its alternative minimum tax exceeds its regular federal income tax. This differs from most investment companies, which elect to be treated as “regulated investment companies” under the Code in order to avoid paying entity level income taxes. Under current law, the Fund is not eligible to elect treatment as a regulated investment company due to its investments primarily in MLPs invested in energy assets. As a result, the Fund will be obligated to pay applicable federal and state corporate income taxes on its taxable income as opposed to most other investment companies which are not so obligated. The Fund expects that a portion of the distributions it receives from MLPs may be treated as a tax-deferred return of capital, thus reducing the Fund’s current tax liability. However, the amount of taxes paid by the Fund will vary depending on the amount of income and gains derived from investments and/or sales of MLP interests and such taxes will reduce your return from an investment in the Fund.

Cash distributions from MLPs to the Fund that exceed such Fund’s allocable share of such MLP’s net taxable income are considered a tax-deferred return of capital that will reduce the Fund’s adjusted tax basis in the equity securities of the MLP. These reductions in such Fund’s adjusted tax basis in the MLP equity securities will increase the amount of gain (or decrease the amount of loss) recognized by the Fund on a subsequent sale of the securities. The Fund will accrue deferred income taxes for any future tax liability associated with (i) that portion of MLP distributions considered to be a tax-deferred return of capital as well as (ii) capital appreciation of its investments. Upon the sale of an MLP security, the Fund may be liable for previously deferred taxes. The Fund will rely to some extent on information provided by the MLPs, which is not necessarily timely, to estimate deferred tax liability for purposes of financial statement reporting and determining the NAV. From time to time, Infrastructure Capital Management, LLC will modify the estimates or assumptions related to the Fund’s deferred tax liability as new information becomes available. The Fund will generally compute deferred income taxes based on the marginal regular federal income tax rate applicable to corporations and an assumed rate attributable to state taxes.

Since the Fund will be subject to taxation on its taxable income, the NAV of Fund shares will also be reduced by the accrual of any deferred tax liabilities. The Index however is calculated without any adjustments for taxes. As a result, the Fund’s after tax performance could differ significantly from the Index even if the pretax performance of the Fund and the performance of the Index are closely correlated.

The Fund’s income tax expense/(benefit) consists of the following:

| October 31, 2014 | | Current | | Deferred | | Total |

| Federal | | | — | | | $ | 5,297 | | | $ | 5,297 | |

| State | | | — | | | | 280 | | | | 280 | |

| Total tax expense | | | — | | | $ | 5,577 | | | $ | 5,577 | |

Deferred income taxes reflect the net tax effect of temporary differences between the carrying amount of assets and liabilities for financial reporting and tax purposes.

Components of the Fund’s deferred tax assets and liabilities are as follows:

| | | As of October 31, 2014 |

| Deferred tax assets: | | | | |

| Net Operating Loss Carryforward | | $ | 610 | |

| Less Deferred tax liabilities: | | | | |

| Net unrealized gain on investment securities | | | (6,187 | ) |

| Net Deferred tax liability | | $ | (5,577 | ) |

| Notes to Financial Statements (continued) |

| October 31, 2014 |

The net operating loss carryforward is available to offset future taxable income. The net operating loss can be carried forward for 20 years and, accordingly, would begin to expire as of October 31, 2034. The Fund has net operating loss carryforwards for federal income tax purposes as follows:

| | | Year-Ended | | Amount | | Expiration |

| Federal | | 10/31/2014 | | 1,704 | | 11/30/2034 |

Although the Fund currently has a net deferred tax liability, it reviews the recoverability of its deferred tax assets based upon the weight of available evidence. When assessing the recoverability of its deferred tax assets, significant weight was given to the effects of potential future realized and unrealized gains on investments and the period over which these deferred tax assets can be realized Currently, any capital losses that may be generated by the Fund in the future are eligible to be carried back up to three years and can be carried forward for five years to offset capital gains recognized by the Fund in those years. Net operating losses that may be generated by the Fund in the future are eligible to be carried back up to two years and can be carried forward for 20 years to offset income generated by the Fund in those years.

Based upon the Fund’s assessment, it has determined that it is more likely than not that its deferred tax assets will be realized through future taxable income of the appropriate character. Accordingly, no valuation allowance has been established for the Fund’s deferred tax assets. The Fund will continue to assess the need for a valuation allowance in the future. Significant declines in the fair value of its portfolio of investments may change the Fund’s assessment of the recoverability of these assets and may result in the recording of a valuation allowance against all or a portion of the Fund’s gross deferred tax assets.

Total income tax benefit (current and deferred) differs from the amount computed by applying the federal statutory income tax rate of 34% to net investment and realized and unrealized gain/(losses) on investment before taxes as follows:

| | | Period Ended

October 31,2014 |

| Income tax expense at statutory rate | | $ | 5,297 | |

| State income taxes (net of federal benefit) | | | 280 | |

| Net income tax expense | | $ | 5,577 | |

The following is a tabular reconciliation of the total amounts of unrecognized tax benefits:

| | | Inception to

October 31, 2014 | |

| Unrecognized tax benefit — Beginning | | $ | — | |

| Gross increases — tax positions in prior period | | | — | |

| Gross decreases — tax positions in prior period | | | — | |

| Gross increases — tax positions in current period | | | — | |

| Settlement | | | — | |

| Lapse of statute of limitations | | | — | |

| Unrecognized tax benefit — Ending | | $ | — | |

The Fund recognizes interest accrued related to unrecognized tax benefits and penalties as income tax expense. For the period from Inception to October 31, 2014, the Fund had no accrued penalties or interest.

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on U.S. tax returns and state tax returns filed since inception of the Fund. No U.S. federal or state income tax returns are currently under examination. The Fund’s initial tax year will be for the period ended October 31, 2014 and this period remains subject to examination by tax authorities in the United States. Due to the nature of the Fund’s investments, the Fund may be required to file income tax returns in several states. The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months.

| Notes to Financial Statements (continued) |

| October 31, 2014 |

The adjusted cost basis of investment and gross unrealized appreciation and depreciation of investments, excluding written options, for federal income tax purposes were as follows:

| | | As of October 31, 2014 |

| Gross unrealized appreciation — investment securities | | $ | 136,979 | |

| Gross unrealized depreciation — investment securities | | | (119,360 | ) |

| Net Unrealized appreciation — investment securities | | | 17,619 | |

| Cost basis of investments | | $ | 6,598,845 | |

6. INVESTMENT TRANSACTIONS

Purchases and sales of investments (excluding in-kind transactions) for the period ended October 31, 2014 were as follows:

| Purchases | | Sales |

| $573,069 | | $29,931 |

Purchases and sales of in-kind transactions for the period ended October 31, 2014 were as follows:

In-Kind

Purchases | | In-Kind

Sales |

| $6,091,074 | | $ — |

7. DERIVATIVE FINANCIAL INSTRUMENTS

Options

Transactions in options written during the period ended October 31, 2014, which serve as an indicator of the volume of activity, were as follows:

| | | Notional

Amount | | Premiums

Received |

| Options outstanding, at beginning of period | | $ | — | | | $ | — | |

| Options written | | | 30 | | | | 2,313 | |

| Options closed | | | — | | | | — | |

| Options expired | | | — | | | | — | |

| Options outstanding, at end of period | | $ | 30 | | | $ | 2,313 | |

The Fund may write covered call and put options on portfolios securities and other financial instruments. Premiums received are recorded as liabilities. The liabilities are subsequently adjusted to reflect the current value of the options written. Premiums received from writing options which expire are treated as realized gains. Premiums received from writing options which are exercised or are closed are added to or offset against the proceeds or amount paid on the transactions to determine the net realized gain or loss. By writing a covered call option, the Fund, in exchange for the premium, foregoes the opportunity for capital appreciation above the exercise price should the market of the price of the underlying security increase. By writing a put option, the Fund, in exchange for the premium, accepts the risk of having to purchase a security at an exercise price that is above the current price. Changes in value of written options are reported as change in unrealized gain (loss) on written options in the Statement of Operations. When the written option expires, is terminated or is sold, the Fund will record a gain or loss, which is reported as realized gain (loss) on written options in the Statement of Operations.

The Fund may purchase call and put options on the portfolio securities or other financial instruments. The Fund may purchase call options to protect against an increase in the price of the security or financial instrument it anticipates purchasing. The Fund may purchase put options on securities which it holds or other financial instruments to protect against a decline in the value of the security or financial instrument or to close out covered written positions. Changes in value of purchased options are reported as part of change in unrealized gain (loss) on investments in the Statement of Operations. When the purchased option expires, is terminated or is sold, the Fund will record a gain or loss, which is reported as part of realized gain (loss) on investments in the Statement of Operations.

| Notes to Financial Statements (continued) |

| October 31, 2014 |

Risks may arise from an imperfect correlation between the change in market value of the securities held by the Fund and the prices of options relating to the securities purchased or sold by the Fund and from possible lack of liquid secondary market for an option. The maximum exposure to loss for any purchased option is limited to the premium initially paid for the option. Written uncovered call options subject the Fund to unlimited risk of loss. Written covered call options limit the upside potential of a security above the strike price. Put options written subject the Fund to risk of loss if the value of the security declines below the exercise price minus the put premium.

Transactions in derivative instruments reflected on the Statement of Assets and Liabilities at October 31, 2014, is:

| | | Equity Risk |

| Liabilities | | |

| Written Options, at value | | $ | 2,650 | |

| Total Liabilities | | $ | 2,650 | |

Transactions in derivative instruments reflected on the Statement of Operations during the period were as follows:

| | | Equity Risk |

| Net Change in Unrealized Depreciation | | |

| Written Options | | $ | (337 | ) |

| Net unrealized loss | | $ | (337 | ) |

For the period ended October 31, 2014, the monthly average notional value of the written options contracts held by the Fund was $(2,650).

8. INVESTMENT RISKS

As with any investment, an investment in the Fund could result in a loss or the performance of the Fund could be inferior to that of other investments. An investor should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing. The Fund’s prospectus and statement of additional information contain this and other important information.

Equity Risk

The Fund invests in equity securities. Equity risk is the risk that the value of the securities that the Fund holds will fall due to general market and economic conditions, perceptions regarding the industries in which the issuers of securities the Fund holds participate or factors relating to specific companies in which the Fund invest.

Energy Industry Risks

The Fund invests primarily in energy infrastructure companies. Energy infrastructure companies are subject to risks specific to the industry they serve including, but not limited to: reduced volumes of natural gas or other energy commodities available for transporting, processing or storing; new construction risks and acquisition risk which can limit growth potential; a sustained reduced demand for crude oil, natural gas and refined petroleum products resulting from a recession or an increase in market price or higher taxes; changes in the regulatory environment; extreme weather; rising interest rates which could result in a higher cost of capital and drive investors into other investment opportunities; and threats of attack by terrorists.

MLP Risk

Investments in securities of MLPs involve risks that differ from investments in common stock including risks related to limited control and limited rights to vote on matters affecting the MLP, risks related to potential conflicts of interest between the MLP and the MLP’s general partner and cash flow risks. MLP common units and other equity securities can be affected by macro-economic and other factors affecting the stock market in general, expectations of interest rates, investor sentiment towards MLPs or the energy sector, changes in a particular issuer’s financial condition or unfavorable or unanticipated poor performance of a particular issuer (in the case of MLPs, generally measured in terms of distributable cash flow). Prices of common units of individual MLPs and other equity securities also can be affected by fundamentals unique to the partnership or company, including earnings power and coverage ratios.

| Notes to Financial Statements (continued) |

| October 31, 2014 |

Returns of Capital Distributions from the Fund Reduce the Tax Basis of Shares

A portion of the Fund’s distributions are expected to be treated as a return of capital for tax purposes. Returns of capital distribution are not taxable income to you but reduce your tax basis in your Shares. Such a reduction in tax basis will result in larger taxable gains and/or lower tax losses on a subsequent sale of Shares. Shareholders who periodically receive the payment of dividends or other distributions consisting of a return of capital may be under the impression that they are receiving net profits from the Fund when, in fact, they are not. Shareholders should not assume that the source of the distributions is from the net profits of the Fund.

Counterparty Risk

The Fund is exposed to counterparty risk, or the risk that an institution or other entity with which the Fund has unsettled or open transactions will default. The potential loss to the Fund could exceed the value of the financial assets recorded in the Fund’s financial statements. Financial assets, which potentially expose the Fund to counterparty risk, consist principally of cash due from counterparties and investments. The Adviser seeks to minimize the Fund’s counterparty risk by performing reviews of each counterparty and by minimizing concentration of counterparty risk by undertaking transactions with multiple customers and counterparties on recognized and reputable exchanges. Delivery of securities sold is only made once the Fund has received payment. Payment is made on a purchase once the securities have been delivered by the counterparty. The trade will fail if either party fails to meet its obligation.

Non-Diversified Risk

The Fund is non-diversified and can invest a greater portion of its assets in securities of individual issuers than diversified funds. As a result, changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a diversified fund. This may increase the Fund’s volatility and cause the performance of a relatively small number of issuers to have a greater impact on the Fund’s performance.

New Fund Risk

The Fund is a new fund. As a new fund, there can be no assurance that the Fund will grow to or maintain an economically viable size, in which case the Fund may experience greater tracking error to its Underlying Index than it otherwise would be at higher asset levels or it could ultimately liquidate.

9. SUBSEQUENT EVENTS

The Fund has evaluated subsequent events through the date of issuance of this report and has determined that there are no other material events that would require disclosure.

| Report of Independent Registered Public Accounting Firm |

| October 31, 2014 |

To the Board of Trustees of ETFis Series Trust I

and the Shareholders of InfraCap MLP ETF

We have audited the accompanying statement of assets and liabilities of InfraCap MLP ETF, (the “Fund”), a series of shares of beneficial interest in ETFis Series Trust I, including the schedule of investments, as of October 31, 2014, and the related statements of operations, changes in net assets and the financial highlights for the period October 1, 2014 (commencement of operations) through October 31, 2014. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2014 by correspondence with the custodian and brokers. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of InfraCap MLP ETF, as of October 31, 2014, and the results of its operations, the changes in its net assets and its financial highlights for the period October 1, 2014 through October 31, 2014, in conformity with accounting principles generally accepted in the United States of America.

BBD, LLP

Philadelphia, Pennsylvania

December 23, 2014

| Approval of Advisory Agreements & Board Considerations (unaudited) |

On August 26, 2014, at an in-person meeting at which a majority of the Independent Trustees were present, the Board of Trustees, including the Independent Trustees voting separately, reviewed and unanimously approved an investment advisory agreement between Etfis Capital LLC (the “Adviser”) and the Trust (the “Advisory Agreement”) and an investment sub-advisory agreement among Infrastructure Capital Advisors, LLC (the “Sub-Adviser”), the Adviser and the Trust (the “Sub-Advisory Agreement”), each with respect to the InfraCap MLP ETF (“Fund”).

Throughout this process, the Independent Trustees were advised and supported by independent counsel to the Independent Trustees. The Board received and reviewed a substantial amount of information provided by the Adviser and Sub-Adviser in response to requests of the Board and counsel.

In deciding on whether to ratify and approve the Advisory Agreement, the Trustees considered numerous factors, including:

The nature, extent, and quality of the services to be provided by the Adviser. In this regard, the Board considered the responsibilities the Adviser would have under the Advisory Agreement. Accordingly, the Board considered the services that would be provided by the Adviser to the Fund including, without limitation, the administrative services that the Adviser and its employees would provide to the Fund, the services already provided by the Adviser related to organizing the Fund, the Adviser’s coordination of services for the Fund by the Fund’s service providers, its compliance procedures and practices, and its efforts to promote the Fund and assist in its distribution. The Board noted that many of the Trust’s executive officers are employees of the Adviser, and serve the Trust without additional compensation from the Fund (an exception is the CCO, who is compensated by the Trust). After reviewing the foregoing information and further information in the Adviser Memorandum (including descriptions of the Adviser’s business and the Adviser’s Form ADV), and discussing the Adviser’s proposed services to the Fund with the Adviser, the Board concluded that the quality, extent, and nature of the services provided by the Adviser are satisfactory and adequate for the Fund.

The investment management capabilities and experience of the Adviser. In this regard, the Board evaluated the management experience of the Adviser, in the light of the services they will be providing. In particular, the Board received information from the Adviser regarding, among other things, the Adviser’s experience in organizing exchange traded funds and coordinating their operation and administration. After consideration of these factors, the Board determined that the Adviser would be an appropriate manager for the Fund.

The costs of the services to be provided and profits to be realized by the Adviser from its relationship with the Fund. In this regard, the Board examined and evaluated the arrangements between the Adviser and the Fund under the proposed Investment Advisory Agreement. The Board also compared the Fund’s proposed management fee with fees paid to other investment advisers to exchange traded funds, particularly where the funds have sub-advisers. The Board also considered the management fees and expense ratios of funds to the Fund’s proposed unified fee structure, noting that the Fund’s management fee and expense ratio would be higher than some funds and lower than others that would be comparable to the Fund based on the type of fund, the style of investment management, the size of the fund, the nature of the fund or the markets invested in or other factors. The Board also considered that the proposed fee was not as low as that of some other funds that have large amounts of assets.

The Board also considered potential benefits for the Adviser in managing the Fund, including promotion of the Adviser’s name, the ability for the Adviser to place small accounts into the Fund, the potential for the Adviser to generate soft dollars from Fund trades that may benefit the Adviser’s clients other than the Fund, and the interests of the Adviser and its affiliates in providing administrative services to the Fund. Following these comparisons and upon further consideration and discussion of the foregoing, the Board concluded that the fees to be paid to the Adviser by the Fund are appropriate and within the range of what would have been negotiated at arm’s length.

The extent to which economies of scale would be realized as the Fund grows and whether management fee levels reflect these economies of scale for the benefit of the Fund’s investors. In this regard, the Board considered that the Fund’s fee arrangements with the Adviser involve a unified fee arrangement. The Board considered that the Fund would likely experience benefits from the unified fee and would continue to do so until the Fund’s assets grow substantially. Following further discussion of the Fund’s projected asset levels, expectations for growth and level of fees, the Board determined that the Fund’s fee arrangements with the Adviser would likely provide benefits through the proposed unified fee.

After full consideration of the above factors as well as other factors, the Board unanimously approved the Advisory Agreement.

In deciding on whether to ratify and approve the Sub-Advisory Agreement, the Trustees considered numerous factors, including:

The nature, extent, and quality of the services to be provided by the Sub-Adviser. In this regard, the Board considered the responsibilities the Sub-Adviser would have under the Sub-Advisory Agreement. Accordingly, the Board considered the services that would be provided by the Sub-Adviser to the Fund including, without limitation, its investment advisory services, its compliance procedures and practices, and its efforts to promote the Fund and assist in its distribution. After reviewing the foregoing information and further information in

| Approval of Advisory Agreements & Board Considerations (unaudited) (continued) |

the information provided by the Sub-Adviser (including descriptions of the Sub-Adviser’s business and the Sub-Adviser’s Form ADV), the Board concluded that the quality, extent, and nature of the services provided by the Sub-Adviser are satisfactory and adequate for the Fund.

The investment management capabilities and experience of the Sub-Adviser. In this regard, the Board evaluated the investment management experience of the Sub-Adviser. In particular, the Board received information from the Sub-Adviser regarding the experience of the Fund’s portfolio managers in investing in securities, including MLPs. The Board discussed with the Sub-Adviser the investment objectives and strategies for the Fund and the Sub-Adviser’s plans for implementing such strategies for the Fund. The Board also considered the consistency of the Sub-Adviser’s investment management approach. After consideration of these factors, the Board determined that the Sub-Adviser would be an appropriate manager for the Fund.

The costs of the services to be provided and profits to be realized by the Sub-Adviser from its relationship with the Fund. In this regard, the Board examined and evaluated the arrangements between the Sub-Adviser and the Fund under the proposed Investment Sub-Advisory Agreement, including the fact that the Fund would utilize a “unified fee structure” whereby a single fee would be paid to the Sub-Adviser for the provision of investment management and all other services to the Fund. The Board noted that, under such an arrangement, the Sub-Adviser would likely supplement the cost of operating the Fund for some period of time, until assets are sufficient to generate enough for the Sub-Adviser to pay for all of the Fund’s service providers and expenses. The Board considered the Sub-Adviser’s staffing, personnel, and methods of operating; the Sub-Adviser’s compliance policies and procedures; the financial condition of the Sub-Adviser and the level of commitment to the Fund and the Sub-Adviser by the principals of the Sub-Adviser; the projected asset levels of the Fund; the Sub-Adviser’s payment of startup costs for the Fund and the overall expenses of the Fund. The Board reviewed the Fund’s proposed unified fee arrangement with the Sub-Adviser and noted the benefit that would result to the Fund from the unified fee for a period of time based on the projected asset levels of the Fund.

The Board also considered potential benefits to the Sub-Adviser in managing the Fund, including promotion of the Sub-Adviser’s name, the ability for the Sub-Adviser to place small accounts into the Fund and the potential for the Sub-Adviser to generate soft dollars from Fund trades. The Board compared the fees and expenses of the Fund (including the management fee) to comparative funds, including funds that have an investment strategy similar to the Fund. The Board also compared the fees to be paid by the Fund as compared to the fees paid by other clients of the Sub-Adviser, and considered the similarities and differences of services received by such other clients as compared to the services that will be received by the Fund. Following these comparisons and upon further consideration and discussion of the foregoing, the Board concluded that the fees to be paid to the Sub-Adviser by the Fund are appropriate and within the range of what would have been negotiated at arm’s length.

The extent to which economies of scale would be realized as the Fund grows and whether management fee levels reflect these economies of scale for the benefit of the Fund’s investors. In this regard, the Board considered that the Fund’s fee arrangements with the Sub-Adviser involve a unified fee arrangement. The Board considered that the Fund would likely experience benefits from the unified fee and would continue to do so until the Fund’s assets grow to a level where the Sub-Adviser begins to receive the full fee. Thereafter, the Board noted that the Fund has the potential to benefit from economies of scale under its agreements with its service providers. Following further discussion of the Fund’s projected asset levels, expectations for growth and level of fees, the Board determined that the Fund’s fee arrangements with the Sub-Adviser would provide benefits through the proposed unified fee.

After full consideration of the above factors as well as other factors, the Board unanimously approved the Sub-Advisory Agreement.

| Supplemental Information (unaudited) |

| October 31, 2014 |

TRUSTEES AND OFFICERS OF THE TRUST

The Trustees of the Trust, their addresses, positions with the Trust, ages, term of office and length of time served, principal occupations during the past five years, the number of portfolios in the Fund Complex overseen by each Trustee and other directorships, if any, held by the Trustees, are set forth below. The SAI includes additional information about the Fund’s Trustees and is available, without charge, upon request, by calling the Adviser (collect) at (212) 593-4383.

| Name and Age | Position(s)

held with

Trust | Length of

Time Served | Principal Occupation(s)

During Past Five Years | Number of

Portfolios in

Fund Complex*

Overseen by

Trustee | Other

Directorships

Held by

Trustee During

Past Five Years |

| INDEPENDENT TRUSTEES |

| James Simpson (43) | Trustee | Since Inception | President, ETP Resources, LLC (2009-Present) (a financial services consulting company); Vice President, Northern Trust Securities, Inc. and Vice President, Northern Trust Global Investments (2008-2009) | Three | None. |

| Robert S. Tull (61) | Trustee | Since Inception | Independent Consultant (2013-present); Chief Operating Officer, Factor Advisors, LLC (2010-2013); Chief Operating Officer, GlobalShares (2009-2010) | Three | None. |

| Stephen O’Grady (66) | Trustee | Since September 2014 | Lead Market Maker, GFI Group (2011-2012); Partner, Kellogg Capital Markets (2004-2011) | Three | None. |

| INTERESTED TRUSTEE** |

| William J. Smalley (31) | Trustee, President, Chief Executive Officer and Secretary | Since Inception | President, ETF Issuer Solutions Inc. (2012-Present); Managing Principal, ETF Distributors LLC (2012- Present); Vice President, Factor Advisors, LLC (2010- 2012); Vice President, MacroMarkets, LLC (2006-2010) | Three | None. |

| OTHER EXECUTIVE OFFICERS |

| Brinton W. Frith (43) | Treasurer and Chief Financial Officer | Since Inception | Managing Director, ETF Issuer Solutions Inc. (2013- Present); President, Javelin Investment Management, LLC (2008-2013) | N/A | N/A |

| Matthew B. Brown (36) | Chief Compliance Officer | Since Inception | CEO, ETF Issuer Solutions Inc. (2012-Present); Managing Principal, ETF Distributors LLC (2012- Present); Director, Factor Advisors, LLC (2010-2012); Director of U.S. Operations, SPA ETFs (2009-2010) | N/A | N/A |

| * | The Fund Complex consists of three portfolios: Tuttle Tactical Management U.S. Core ETF, InfraCap MLP ETF and Manna Core Equity Enhanced Dividend Income Fund; however, as of October 31, 2014, Tuttle Tactical Management U.S. Core ETF and Manna Core Equity Enhanced Dividend Income Fund had not commenced operations. |

| ** | Mr. Smalley is an Interested Trustee because he is an employee of the Adviser. |

| 1 | The address for each Trustee and officer is 6 East 39th Street, Suite 1003, New York, NY 10016. |

| 2 | Each Trustee serves until resignation, death, retirement or removal. Officers are elected yearly by the Trustees. |

| 3 | For the fiscal year ended October 31, 2014, the Fund paid the Board of Trustees an aggregate $509.58. |

| Supplemental Information (unaudited) (continued) |

| October 31, 2014 |

INFORMATION ABOUT PORTFOLIO HOLDINGS

The Fund files its complete schedule of portfolio holdings for its first and third fiscal quarters with the Securities and Exchange Commission (“SEC”) on Form N-Q. The Fund’s Form N-Q is available without charge, upon request, by calling toll-free at (877) 756-7873. Furthermore, you may obtain the Form N-Q on the SEC’s website at www.sec.gov. The Fund’s portfolio holdings are posted on the Fund’s website at www.infracapmlp.com daily.

The Fund’s premium/discount information that is current as of the most recent month-end is available by visiting www.infracapmlp.com or by calling (888) 383-4184.

INFORMATION ABOUT PROXY VOTING

A description of the policies and procedures the Fund uses to determine how to vote proxies relating to portfolio securities is provided in the Statement of Additional Information (“SAI”). The SAI is available without charge upon request by calling toll-free at (877) 756-7873, by accessing the SEC’s website at www.sec.gov, or by accessing the Fund’s website at www.infracapmlp.com.

Information regarding how the Fund voted proxies relating to portfolio securities during the period ending October 31 is available by calling toll-free at (888) 756-7873 or by accessing the SEC’s website at www.sec.gov.

Etfis Capital LLC

6 East 39th Street, Suite 1003

New York, NY 10016

(212) 593-4383

InfraCap MLP ETF

Item 2. Code of Ethics.

As of the end of the period covered by this report, the registrant has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party. Pursuant to Item 12(a)(1), a copy of registrant’s code of ethics has been filed with the Commission. During the period covered by this report, the code of ethics has not been amended, and the registrant has not granted any waivers, including implicit waivers, from the provisions of the code of ethics.

Item 3. Audit Committee Financial Expert.

The registrant’s board of trustees has determined that James A. Simpson, one of the trustees on the registrant’s audit committee, meets the qualifications of an audit committee financial expert. Mr. Simpson is “independent” for purposes of this Item.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees. The aggregate fees billed for professional services rendered by the principal accountant for the audit of the registrant’s annual financial statements or for services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements were $10,000.00 for the registrant’s fiscal year ended October 31, 2014.

(b) Audit-Related Fees. No fees were billed in the registrant’s fiscal year ended October 31, 2014 for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item.

(c) Tax Fees. The aggregate fees billed for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning were $0.00 for the registrant’s fiscal year ended October 31, 2014.

(d) All Other Fees. None.

(e)(1) The audit committee has not adopted pre-approval policies and procedures described in paragraph (c)(7) of Rule 2-01 of Regulation S-X.

(e)(2) None of the services described in paragraph (b) through (d) of this Item were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50% of hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) During the fiscal year ended October 31, 2014, aggregate non-audit fees of $0.00 were billed by the registrant’s accountant for services rendered to the registrant. No non-audit fees were billed in the registrant’s first fiscal year by the registrant’s accountant for services rendered to the registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant.

(h) Not applicable.

Item 5. Audit Committee of Listed Registrants.

The registrant has established a separately-designated standing audit committee comprised of all of the independent trustees of the board of trustees of the registrant. The members of the audit committee are Stephen G. O’Grady, James Simpson and Robert S. Tull.

Item 6. Schedule of Investments

(a) Included as part of the report to shareholders filed under Item 1 of this Form.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

The registrant does not have procedures in place to consider nominees recommended by shareholders. The registrant’s nominating committee generally will not consider nominees recommended by shareholders.

Item 11. Controls and Procedures.

| (a) | The registrant’s principal executive and principal financial officers, or persons performing similar functions, have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)). |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) that occurred during the registrant’s second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting. |

Item 12. Exhibits.

(a)(1) Code of ethics, or any amendment thereto, that is the subject of disclosure required by Item 2 is attached hereto.