UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22819

ETFis Series Trust I

(Exact name of registrant as specified in charter)

1540 Broadway, 16th Floor, New York, New York 10036

(Address of principal executive offices) (Zip code)

William J. Smalley, President, 1540 Broadway, 16th Floor, New York, New York 10036

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 593-4383

Date of fiscal year end: 10/31/2015

Date of reporting period: 10/31/2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

ETFis Series Trust I

BIOSHARES BIOTECHNOLOGY CLINICAL TRIALS FUND

BIOSHARES BIOTECHNOLOGY PRODUCTS FUND

TUTTLE TACTICAL MANAGEMENT MULTI-STRATEGY INCOME ETF

TUTTLE TACTICAL MANAGEMENT U.S. CORE ETF

VIRTUS NEWFLEET MULTI-SECTOR UNCONSTRAINED BOND ETF

INFRACAP MLP ETF

| Virtus ETFs | ANNUAL REPORT |

| | October 31, 2015 |

|

| Table of Contents |

| October 31, 2015 |

|

| Shareholder Letter |

| October 31, 2015 |

Dear Fellow ETFis Funds Shareholder:

I am pleased to present the second annual report for the ETFis Series Trust I, which reviews the performance of the Funds within the Trust for the twelve months ended October 31, 2015.

Over the reporting period, the Trust expanded from one fund to seven funds representing the distinct investment strategies of five sub-advisers. New additions include two funds which provide exposure to the niche areas of clinical trials and product within the biotechnology space; two tactical asset allocation funds: one focused primarily on the U.S. equity market, the other on fixed income and non-traditional income strategies; an unconstrained global bond fund with the flexibility to invest across fixed income sectors; and a fund that offers exposure to equity securities of companies in the utility sector.

| Fund | | Sub-adviser | | Inception Date |

| BioShares Biotechnology Clinical Trials Fund (BBC) | | LifeSci Index Partners, LLC | | December 16, 2014 |

| BioShares Biotechnology Products Fund (BBP) | | LifeSci Index Partners, LLC | | December 16, 2014 |

| Tuttle Tactical Management Multi-Strategy Income ETF (TUTI) | | Tuttle Tactical Management | | June 9, 2015 |

| Tuttle Tactical Management U.S. Core ETF (TUTT) | | Tuttle Tactical Management | | February 24, 2015 |

| Virtus Newfleet Multi-Sector Unconstrained Bond ETF (NFLT) | | Newfleet Asset Management | | August 10, 2015 |

| InfraCap MLP ETF (AMZA) | | Infrastructure Capital Advisers, LLC | | October 1, 2014 |

| Reaves Utilities ETF (UTES)* | | Reaves Asset Management | | September 23, 2015 |

| * | Fund not included within this report as its fiscal year-end is July 31. |

The report provides financial statements and portfolio information for all of the above Funds, with the exception of Reaves Utilities ETF. For the Funds with a performance history of more than six months, the report also provides commentary from the portfolio manager on how the Fund performed relative to the markets in which it invests.

On behalf of the sub-advisers, thank you for your investment. If you have questions, please contact your financial adviser, or call 1-888-383-0553. We also invite you to visit our website, www.virtusetfs.com, to learn more about the funds.

Sincerely,

William Smalley

President

ETFis Series Trust I

This material must be accompanied or preceded by the prospectus.

|

| Portfolio Summaries |

| October 31, 2015 |

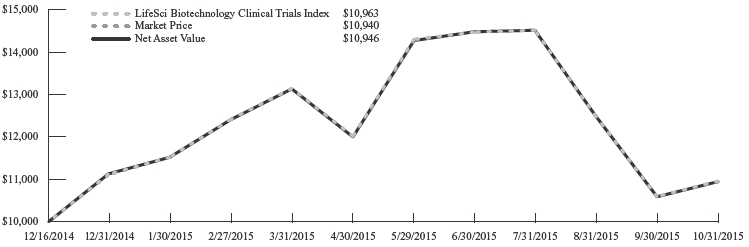

BioShares Biotechnology Clinical Trials Fund

For the partial fiscal year from inception date (12/16/2014) through fiscal year end (10/31/2015), the S&P 500 index was up 5.4% compared to 9.6% for the LifeSci Biotechnology Clinical Trials Index. Although volatility has been high, biotechnology stocks in general have outperformed the broader stock market.

The BioShares Biotechnology Clinical Trials Fund (“BBC” or “the Fund”) performed in-line with its respective index up 9.46%.

BBC benefited from (1) continued advancement of various clinical trials particularly in various cancers, Duchenne’s muscular dystrophy and Alzheimer’s, (2) technological advancements in areas including gene therapy, immuno-oncology, microbial research and gene editing, and (3) continued M&A trends resulting in 4 stocks in the portfolio entering into definitive acquisition agreements. BBC suffered from (1) questions on valuation levels of individual stocks, particularly as stocks in the portfolio are unprofitable, (2) increasing concerns on the high prices of prescription pharmaceutical products, and (3) various clinical trial failures or disappointments in areas such as sickle-cell disease, macular degeneration and various cancers.

Biotechnology Sector Risk: The fund’s assets will be concentrated in investments in the securities of issuers engaged primarily in the biotechnology industry. Companies within the biotechnology sector spend heavily on research and development, which may not necessarily lead to commercially successful products in the near or long term. In order to fund operations, these companies may require financing from the capital markets, which may not always be available on satisfactory terms or at all. The biotechnology sector is also subject to significant governmental regulation, and the need for governmental approvals, including, without limitation, FDA approval. The securities of biotechnology companies, especially those of smaller or newer companies, tend to be more volatile than those of companies with larger capitalizations or markets generally.

| Asset Allocation as of 10/31/2015 (based on net assets) (unaudited) |

| Healthcare | | | 99.8 | % |

| Other Assets | | | 0.2 | % |

| Total | | | 100 | % |

Performance as of 10/31/2015 (unaudited)

| | | Total Return |

| | | Fund

Net Asset Value | | Fund

Market Price | | LifeSci Biotechnology

Clinical Trials Index1 |

| Since Inception2 | | 9.46% | | 9.40% | | 9.63% |

| 1 | The LifeSci Biotechnology Clinical Trials Index is designed to track the performance of U.S. listed biotechnology stocks with a lead drug in the clinical trial stage of development, typically a Phase 1, Phase 2 or Phase 3 trial, but prior to receiving marketing approval. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.bioshares.com or call toll free (888) 383-0553. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

Exchange Traded Funds: The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss.

Correlation to Index: The performance of the fund and its index may vary somewhat due to factors such as fund flows, transaction costs, and timing differences associated with additions to and deletions from its index.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

BioShares Biotechnology Clinical Trials Fund (continued)

Non-Diversified: The fund is non-diversified and may be more susceptible to factors negatively impacting its holdings to the extent that each security represents a larger portion of the fund’s assets.

No Guarantee: There is no guarantee that the portfolio will meet its objective.

Prospectus: For additional information on risks, please see the fund’s prospectus. The Fund may not be suitable for all investors.

Value of a $10,000 Investment Since Inception at Net Asset Value (unaudited)

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund, assuming reinvestment of distributions. Past performance does not guarantee future results.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

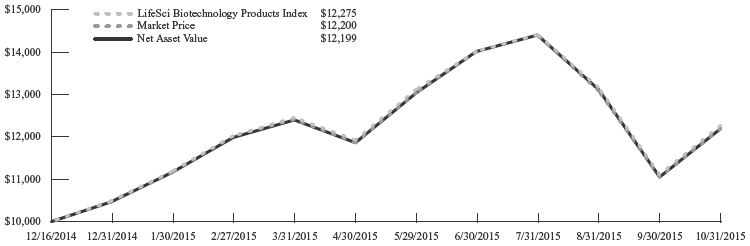

BioShares Biotechnology Products Fund

For the partial fiscal year from inception date (12/16/2014) through fiscal year end (10/31/2015), the S&P 500 index was up 5.4% compared The LifeSci Biotechnology Products Index, 22.8%. Although volatility has been high, biotechnology stocks in general have outperformed the broader stock market.

BioShares Biotechnology Products Fund (“BBP” or “the Fund”) NAV was up 21.99%.

The Fund benefited from (1) continued M&A trends resulting in 5 stocks in the portfolio entering into definitive acquisition agreements and (2) continued strong revenue growth. The Fund suffered from (1) increasing concerns on the high prices of prescription pharmaceutical products and (2) questions on valuation levels of individual stocks.

Biotechnology Sector Risk: The fund’s assets will be concentrated in investments in the securities of issuers engaged primarily in the biotechnology industry. Companies within the biotechnology sector spend heavily on research and development, which may not necessarily lead to commercially successful products in the near or long term. In order to fund operations, these companies may require financing from the capital markets, which may not always be available on satisfactory terms or at all. The biotechnology sector is also subject to significant governmental regulation, and the need for governmental approvals, including, without limitation, FDA approval. The securities of biotechnology companies, especially those of smaller or newer companies, tend to be more volatile than those of companies with larger capitalizations or markets generally.

| Asset Allocation as of 10/31/2015 (based on net assets) (unaudited) |

| Healthcare | | | 100 | % |

| Other Liabilities | | | (0.0 | )%* |

| Total | | | 100 | % |

* Amount rounds to less than 0.05%.

Performance as of 10/31/2015 (unaudited)

| | | Total Return |

| | | Fund

Net Asset Value | | Fund

Market Price | | LifeSci Biotechnology

Products Index1 |

| Since Inception2 | | 21.99% | | 22.00% | | 22.75% |

| 1 | The LifeSci Biotechnology Products Index is designed to track the performance of U.S. listed biotechnology stocks with at least one drug therapy approved by the U.S. Food and Drug Administration for marketing. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.bioshares.com or call toll free (888) 383-0553. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

Exchange Traded Funds: The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss.

Correlation to Index: The performance of the fund and its index may vary somewhat due to factors such as fund flows, transaction costs, and timing differences associated with additions to and deletions from its index.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

BioShares Biotechnology Products Fund (continued)

Non-Diversified: The fund is non-diversified and may be more susceptible to factors negatively impacting its holdings to the extent that each security represents a larger portion of the fund’s assets.

No Guarantee: There is no guarantee that the portfolio will meet its objective.

Prospectus: For additional information on risks, please see the fund’s prospectus. The Fund may not be suitable for all investors.

Value of a $10,000 Investment Since Inception at Net Asset Value (unaudited)

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund, assuming reinvestment of distributions. Past performance does not guarantee future results.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

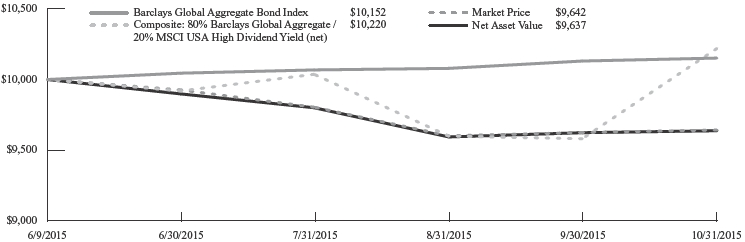

Tuttle Tactical Management Multi-Strategy Income ETF

This discussion of operations relates to a short fiscal period. Tuttle Tactical Management Multi Strategy Income ETF (“TUTI” or “the Fund”) began operations on June 9, 2015 (commencement of operations), and the fiscal year ended on October 31, 2015. During this period, the net asset value of TUTI fell from $24.61 to $23.72. During the same period, the Barclay’s Aggregate Bond Index rose 1.52%.

TUTI was launched during a period of market turmoil. June and July saw crisis’ in Greece and China and August saw a global market selloff followed by a swift rally in October. While the Fund’s defensive positions helped insulate it from much of the market volatility during the period, the Fund’s performance was, nevertheless, negatively impacted by its exposure to equity markets during the selloff.

Key elements of the portfolio strategy for the Fund were initiated during the period:

| • | The models were enhanced to be more sensitive to increasing stock market volatility |

| • | The models were enhanced to be less sensitive to rebalance date risk. |

These key elements will better allow the Fund to adapt to choppy market environments.

| Asset Allocation as of 10/31/2015 (based on net assets) (unaudited) |

| Debt Funds | | | 63.8 | % |

| Equity Funds | | | 32.3 | % |

| Other Assets | | | 3.9 | % |

| Total | | | 100 | % |

Performance as of 10/31/2015 (unaudited)

| | | Total Return |

| | | Fund

Net Asset Value | | Fund

Market Price | | Barclays Global

Aggregate Bond Index1 | | Composite: 80%

Barclays Global Aggregate

Bond / 20% MSCI USA High

Dividend Yield (net)2 |

| Since Inception3 | | (3.63)% | | (3.58)% | | 1.52% | | 2.20% |

| 1 | The Barclays Global Aggregate Bond Index measures the global investment grade fixed rate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

| 2 | The composite index consists of 80% Barclays Global Aggregate Bond Index (an index measuring the global investment grade bond market, calculated on a total return basis) and 20% MSCI USA High Dividend Yield Index (an index that measures performance of equities in the large and mid cap segments (excluding REITs) of the US market, that have higher dividend income and quality characteristics than average dividend yields that are both sustainable and persistent, calculated on a total return basis with net dividends reinvested). The composite index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.tuttlefunds.com or call toll free (888) 383-0553. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

Exchange Traded Funds: The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss.

Portfolio Turnover: The fund’s principal investments strategies will result in a consistently high portfolio turnover rate. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

Tuttle Tactical Management Multi-Strategy Income ETF (continued)

Allocation: The fund’s exposure to different asset classes may not be optimal for market conditions at a given time. Asset allocation does not guarantee a profit or protect against a loss in declining markets.

No Guarantee: There is no guarantee that the portfolio will meet its objective.

Prospectus: For additional information on risks, please see the fund’s prospectus. The Fund may not be suitable for all investors.

Value of a $10,000 Investment Since Inception at Net Asset Value (unaudited)

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund, assuming reinvestment of distributions. Past performance does not guarantee future results.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

Tuttle Tactical Management U.S. Core ETF

This discussion of operations relates to a short fiscal period. Tuttle Tactical Management U.S. Core ETF (“TUTT” or “the Fund”) began operations on February 24, 2015 (commencement of operations), and the fiscal year ended on October 31, 2015. During this period, the net asset value of TUTT fell from $24.62 to $23.01. During the same period, the S&P 500 rose 0.36%.

February was an extremely strong month for the market but the Fund launched at an intermediate term market top from a near fully invested market position. Through mid-year, the Fund’s performance generally followed the equity markets, which experienced mild volatility, but remained relatively steady. However, stock prices broadly declined during August and September and quickly reversed in October.

Tactical strategies like the Fund’s can underperform in these types of choppy market environments because market downturns that rapidly reverse may result in the portfolio experiencing some of the market decline while shifting to defensive allocations that then miss out on the unexpected rally. The Fund experienced this scenario during the August-October period, when the Fund’s performance was adversely impacted by the timing of the Fund’s shift into more defensive positions.

Key elements of the portfolio strategy for the Fund were initiated during the period:

| • | The models were enhanced to be more sensitive to increasing stock market volatility |

| • | The models were enhanced to be less sensitive to rebalance date risk. |

These key elements will better allow the Fund to adapt to choppy market environments.

| Asset Allocation as of 10/31/2015 (based on net assets) (unaudited) |

| Debt Funds | | | 57.9 | % |

| Equity Funds | | | 40.2 | % |

| Other Assets | | | 1.9 | % |

| Total | | | 100 | % |

Performance as of 10/31/2015 (unaudited)

| | | Total Return |

| | | Fund

Net Asset Value | | Fund

Market Price | | S&P 500® Index1 |

| Since Inception2 | | (6.53)% | | (6.48)% | | 0.36% |

| 1 | The S&P 500® Index is a free-float market capitalization-weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.tuttlefunds.com or call toll free (888) 383-0553. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

Exchange Traded Funds: The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss.

Portfolio Turnover: The fund’s principal investments strategies will result in a consistently high portfolio turnover rate. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account.

Allocation: The fund’s exposure to different asset classes may not be optimal for market conditions at a given time. Asset allocation does not guarantee a profit or protect against a loss in declining markets.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

Tuttle Tactical Management U.S. Core ETF (continued)

No Guarantee: There is no guarantee that the portfolio will meet its objective.

Prospectus: For additional information on risks, please see the fund’s prospectus. The Fund may not be suitable for all investors.

Value of a $10,000 Investment Since Inception at Net Asset Value (unaudited)

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund, assuming reinvestment of distributions. Past performance does not guarantee future results.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

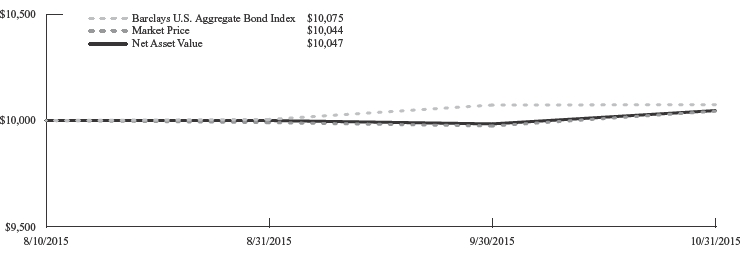

Virtus Newfleet Multi-Sector Unconstrained Bond ETF

The Virtus Newfleet Multi-Sector Unconstrained Bond ETF (NYSE: NFLT) launched on August 10, 2015. This actively managed ETF seeks to provide a high level of current income and, secondarily, capital appreciation.

Newfleet Asset Management’s cornerstone philosophy emphasizes choosing the right pockets of the global bond market at the right times. Newfleet believes the most effective way to achieve long-term excess returns is through the combination of active sector rotation and disciplined risk management. NFLT is a logical extension of Newfleet’s proven multi-sector approach. While NFLT embraces the virtues of diversification, the lack of formal sector, industry, or country limitations means that the portfolio management team can express its highest conviction ideas within the portfolio.

At its inception, NFLT was seeded with $122.5 million of investor capital. The portfolio management team made the conscious decision to methodically invest the proceeds as the period of mid-to-late August is generally quiet with many on Wall Street taking mandatory vacation pre-Labor Day. Rather than invest rapidly at potentially unattractive levels, the team was patient in entering the most attractive fixed income sectors over the period.

The Fund continued to receive inflows during September and October. Throughout this period, the team continued to methodically invest the proceeds in the sectors believed to offer the best relative value. By the end of September, a little over seven weeks after launch, NFLT was 49% invested, with $130 million of assets under management. As of October 31, 2015, NFLT was 68% invested, with $153 million of net assets under management.

| Asset Allocation as of 10/31/2015 (based on net assets) (unaudited) |

| Corporate Bonds | | | 32.7 | % |

| Term Loans | | | 14.1 | % |

| Mortgage Backed Securities | | | 11.1 | % |

| Foreign Bonds | | | 6.2 | % |

| Asset Backed Securities | | | 3.8 | % |

| Money Market Funds | | | 42.7 | % |

| Other Liabilities | | | (10.6 | )% |

| Total | | | 100 | % |

Performance as of 10/31/2015 (unaudited)

| | | Total Return |

| | | Fund

Net Asset Value | | Fund

Market Price | | Barclays U.S.

Aggregate Bond Index1 |

| Since Inception2 | | 0.47% | | 0.44% | | 0.75% |

| 1 | The Barclays U.S. Aggregate Bond Index measures the U.S. investment grade fixed rate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.virtus.com or call toll free (888) 383-0553. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities.

High Yield-High Risk Fixed Income Securities: There is a greater level of credit risk and price volatility involved with high yield securities than investment grade securities.

Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

Virtus Newfleet Multi-Sector Unconstrained Bond ETF (continued)

Bank Loans: Loans may be unsecured or not fully collateralized, may be subject to restrictions on resale and/or trade infrequently on the secondary market. Loans can carry significant credit and call risk, can be difficult to value and have longer settlement times than other investments, which can make loans relatively illiquid at times.

ABS/MBS: Changes in interest rates can cause both extension and prepayment risks for asset- and mortgage-backed securities. These securities are also subject to risks associated with the repayment of underlying collateral.

Derivatives: Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

Market Price/NAV: At the time of purchase and/or sale, an investor’s shares may have a market price that is above or below the fund’s NAV, which may increase the investor’s risk of loss.

Prospectus: For additional information on risks, please see the fund’s prospectus.

Value of a $10,000 Investment Since Inception at Net Asset Value (unaudited)

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund, assuming reinvestment of distributions. Past performance does not guarantee future results.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

InfraCap MLP ETF

Management’s Discussion of Operations

Overview

InfraCap MLP ETF (“the Fund”) seeks to provide a high level of current income, a growing income stream, and long-term capital appreciation. The Fund is an actively-managed portfolio of high quality, midstream energy master limited partnerships (MLPs) and related general partners. The Fund also utilizes options strategies and modest leverage to enhance income and total return.

The Fund focuses on the midstream MLP sector because most of these companies have a long-term history of relatively stable and growing cash distributions. These companies are typically involved in the production, gathering, transportation, storage, and processing of oil, natural gas, natural gas liquids and refined products.

Update

During the fiscal year ended on October 31, 2015, the net asset value of the Fund fell from $24.21 to $14.28. This decline occurred during a period of unrelenting weakness in crude oil prices and continued weakness in natural gas prices. Stocks in the midstream energy sector underperformed the broader market and other energy-related indices by a substantial margin.

The Fund’s performance was specifically enhanced by its underweight position in Shell Midstream Partners LP (SHLX) as well as overweight positions in Spectra Energy Corporation (SE) and Oneok Inc. (OKE).

Conversely, the Fund’s performance was hindered by its overweight positions in Targa Resources Corporation (TRGP), Williams Partners LP (WPZ) and Energy Transfer Equity L.P. (ETE).

The use of leverage was a significant drag on performance during the period. The ratio of leverage to total assets increased during this period primarily due to the reduction in asset values.

Dividends paid to investors during the year increased sequentially from quarter to quarter. The cumulative dividend payout to investors during the fiscal year was $2.03 per share.

Shares outstanding increased during the fiscal year from 250,004 to 1,400,004.

Dividend Payments

The dividend rate is determined on a quarterly basis, and the rate may be adjusted during the year. An important consideration in determining the level of dividend payments is the estimated amount of distributable cash flow (“DCF”).

DCF is investment income less expenses. Investment income includes cash distributions from master limited partnerships, dividends received from stocks, and net realized gains (losses) from written and purchased options contracts. Expenses include advisory fees, other miscellaneous fees and leverage costs.

The Supplemental Financial Data table includes the calculation of distributable cash flow and should be reviewed as part of this discussion. It should be noted that this calculation differs from the Statement of Operations because of the following factors: 1) GAAP does not include MLP distributions in investment income because these distributions are typically treated as return of capital; and 2) GAAP does not include net realized gains (losses) on written and purchased options contracts as investment income but reports them separately as realized and unrealized gains (losses).

Use of Leverage

The Fund’s use of leverage is consistent with the limits set forth in the Investment Company Act of 1940 which states that the ratio of debt to total assets should not exceed 33%. The leverage ratio is impacted by increases and decreases in the market value of the Fund’s investments, the use of debt to finance the purchase of new securities, and/or the sale of investments where proceeds are used to pay down debt.

The Fund’s policy is to maintain the leverage ratio in a range of 10-33% over the long term. Additional leverage may be used when attractive investment opportunities arise but such leverage would be reduced over time. This leverage policy is consistent with the Fund’s investment objective to provide investors with a high level of current income. Total leverage represented 25.3% of total assets at year-end which was at the high-end of the long-term target range.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

InfraCap MLP ETF (continued)

Taxes

It should be noted that AMZA is fully taxed as a corporation. This tax treatment is the same as for other open-end and closed-end funds that focus on the Master Limited Partnership asset class. One consequence is that the Fund’s net asset value may be impacted by a tax reserve. The gross expenses that are reported in the Fund’s financial highlights include the tax reserve. The net expenses reported in the financial highlights exclude the tax reserve.

Another consequence of our tax status is that owners of the Fund will receive a Form 1099 for tax reporting purposes. So shareholders of the Fund do not face the complications of Schedule K-1 reporting, state filing requirements and UBTI (unrelated business tax income) that direct owners of MLP shares must address.

| Asset Allocation as of 10/31/2015 (based on net assets) (unaudited) |

| Energy | | | 133.8 | % |

| Purchased Options | | | 0.0 | %* |

| Written Options | | | (0.7 | )% |

| Other Liabilities | | | (33.1 | )% |

| Total | | | 100 | % |

* Amount rounds to less than 0.05%.

Performance as of 10/31/2015 (unaudited)

| | | Average Annual Total Return |

| | | Fund

Net Asset Value | | Fund

Market Price | | Alerian MLP

Infrastructure Index1 |

| 1 Year | | (34.34)% | | (33.95)% | | (29.05)% |

| Since Inception2 | | (34.27)% | | (34.01)% | | (29.10)% |

| 1 | The Alerian MLP Infrastructure Index is a composite of energy infrastructure Master Limited Partnerships (MLPs), whose constituents earn the majority of their cash flow from the transportation, storage, and processing of energy commodities. The index is calculated using a float-adjusted, capitalization-weighted methodology on a total-return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. |

Performance data quoted represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. For the most current month-end performance data please visit www.infracapmlp.com or call toll free (888) 383-0553. Market price returns are based on the mid-point of the highest bid and lowest offer for Fund shares as of the scheduled close of regular trading on the New York Stock Exchange (“NYSE”) Arca, ordinarily 4:00 p.m. Eastern time, on each day during which the NYSE is open for trading, and do not represent the returns an investor would receive if shares were traded at other times.

Interest Rate Risk: As yield-based investments, MLPs carry interest rate risk and may underperform in rising interest rate environments. Additionally, when investors have heightened fears about the economy, the risk spread between MLPs and competing investment options can widen, which may have an adverse effect on the stock price of MLPs. Rising interest rates may increase the potential cost of MLPs financing projects or cost of operations, and may affect the demand for MLP investments, either of which may result in lower performance by or distributions from the Fund’s MLP investments.

Exchange Traded Funds: The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Short Sales: The fund may engage in short sales, and may experience a loss if the price of a borrowed security increases before the date on which the fund replaces the security.

Leverage: When a fund leverages its portfolio, the value of its shares may be more volatile and all other risks may be compounded.

|

| Portfolio Summaries (continued) |

| October 31, 2015 |

InfraCap MLP ETF (continued)

Derivatives: Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

MLPs: Investments in Master Limited Partnerships may be adversely impacted by tax law changes, regulation, or factors affecting underlying assets.

Prospectus: For additional information on risks, please see the fund’s prospectus.

Value of a $10,000 Investment Since Inception at Net Asset Value (unaudited)

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund, assuming reinvestment of distributions. Past performance does not guarantee future results.

|

| Shareholder Expense Examples (unaudited) |

As a shareholder of a Fund, you incur ongoing costs, including advisory fees and other fund expenses, if any. The following example is intended to help you understand your ongoing costs (in dollars and cents) of investing in a Fund and to compare these costs with the ongoing costs of investing in other funds. The examples are based on an investment of $1,000 invested at the beginning of the period and held throughout the entire period (May 1, 2015 to October 31, 2015), unless otherwise noted for Funds with operations less than six months.

Actual expenses

The first line under each Fund in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for your Fund under the heading entitled “Expenses Paid Through 10/31/15” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second line under each Fund in the table provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of Fund shares. Therefore, the second line under each Fund in the table is useful in comparing ongoing Fund costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value

10/31/15 | | Annualized

Expense Ratios(2) | | Expenses Paid

During the

Period |

| BioShares Biotechnology Clinical Trials Fund | | | | | | | | |

| Actual | | $1,000.00 | | $ 912.14 | | 0.85% | | $4.10(3) |

| Hypothetical(1) | | $1,000.00 | | $1,020.92 | | 0.85% | | $4.33(3) |

| |

| BioShares Biotechnology Products Fund | | | | | | | | |

| Actual | | $1,000.00 | | $1,028.21 | | 0.87% | | $4.45(3) |

| Hypothetical(1) | | $1,000.00 | | $1,020.82 | | 0.87% | | $4.43(3) |

| |

| Tuttle Tactical Management Multi-Strategy Income ETF | | | | | | | | |

| Actual | | $1,000.00 | | $ 963.80 | | 0.93% | | $3.63(4) |

| Hypothetical(1) | | $1,000.00 | | $1,020.52 | | 0.93% | | $4.74(5) |

| |

| Tuttle Tactical Management U.S. Core ETF | | | | | | | | |

| Actual | | $1,000.00 | | $ 955.06 | | 0.90% | | $4.44(3) |

| Hypothetical(1) | | $1,000.00 | | $1,020.67 | | 0.90% | | $4.58(3) |

| |

| Virtus Newfleet Multi-Sector Unconstrained Bond ETF | | | | | | | | |

| Actual | | $1,000.00 | | $1,004.70 | | 0.80% | | $1.78(6) |

| Hypothetical(1) | | $1,000.00 | | $1,021.70 | | 0.80% | | $4.08(5) |

| |

| InfraCap MLP ETF | | | | | | | | |

| Actual | | $1,000.00 | | $ 676.93 | | 1.15% | | $4.86(3) |

| Hypothetical(1) | | $1,000.00 | | $1,019.41 | | 1.15% | | $5.85(3) |

| 1 | Assuming 5% return before expenses. |

| 2 | Annualized expense ratios reflect expenses net of waived fees or reimbursed expenses, if applicable. |

| 3 | Expenses are calculated using each Fund’s annualized expense ratio, multiplied by the average account value for the period, multiplied by 184/365 (to reflect the six-month period). |

| 4 | Actual expenses are calculated using the Fund’s annualized expense ratio, multiplied by the average account value for the period, multiplied by 144/365 (to reflect the period June 9, 2015 to October 31, 2015). |

| 5 | Hypothetical expenses are calculated using the Fund’s annualized expense ratio, multiplied by the average account value for the period, multiplied by 184/365 (to reflect the six-month period). |

| 6 | Actual expenses are calculated using the Fund’s annualized expense ratio, multiplied by the average account value for the period, multiplied by 82/365 (to reflect the period August 10, 2015 to October 31, 2015). |

|

| Schedule of Investments — BioShares Biotechnology Clinical Trials Fund |

| October 31, 2015 |

| | | | | |

| Security Description | | Shares | | Value |

| Common Stocks — 99.8% | | | | | | | | |

| Health Care — 99.8% | | | | | | | | |

| ACADIA Pharmaceuticals, Inc.* | | | 8,801 | | | $ | 306,451 | |

| Acceleron Pharma, Inc.* | | | 11,075 | | | | 345,651 | |

| Achillion Pharmaceuticals, Inc.* | | | 39,379 | | | | 307,944 | |

| Advaxis, Inc.* | | | 14,020 | | | | 155,482 | |

| Affimed N.V.* | | | 27,836 | | | | 176,480 | |

| Agenus, Inc.* | | | 35,550 | | | | 162,108 | |

| Agios Pharmaceuticals, Inc.* | | | 3,297 | | | | 240,219 | |

| Alder Biopharmaceuticals, Inc.* | | | 7,099 | | | | 227,026 | |

| Alnylam Pharmaceuticals, Inc.* | | | 2,651 | | | | 227,853 | |

| Amicus Therapeutics, Inc.* | | | 24,555 | | | | 184,162 | |

| Arbutus Biopharma Corp.* | | | 23,026 | | | | 126,643 | |

| Array BioPharma, Inc.* | | | 47,879 | | | | 245,140 | |

| Arrowhead Research Corp.* | | | 51,005 | | | | 262,676 | |

| Atara Biotherapeutics, Inc.* | | | 6,116 | | | | 157,609 | |

| Avalanche Biotechnologies, Inc.* | | | 8,840 | | | | 74,521 | |

| Bellicum Pharmaceuticals, Inc.* | | | 13,757 | | | | 172,100 | |

| BioCryst Pharmaceuticals, Inc.* | | | 27,790 | | | | 249,832 | |

| Bluebird Bio, Inc.* | | | 1,916 | | | | 147,781 | |

| Celldex Therapeutics, Inc.* | | | 13,912 | | | | 167,779 | |

| Cempra, Inc.* | | | 10,319 | | | | 229,082 | |

| Chimerix, Inc.* | | | 8,401 | | | | 329,151 | |

| Clovis Oncology, Inc.* | | | 4,047 | | | | 404,336 | |

| Concert Pharmaceuticals, Inc.* | | | 19,882 | | | | 451,520 | |

| CTI BioPharma Corp.* | | | 161,393 | | | | 214,653 | |

| Curis, Inc.* | | | 104,809 | | | | 213,810 | |

| Dicerna Pharmaceuticals, Inc.* | | | 21,234 | | | | 212,765 | |

| Dynavax Technologies Corp.* | | | 16,679 | | | | 378,780 | |

| Endocyte, Inc.* | | | 58,665 | | | | 301,538 | |

| Epizyme, Inc.* | | | 17,363 | | | | 227,282 | |

| Esperion Therapeutics, Inc.* | | | 4,392 | | | | 105,408 | |

| FibroGen, Inc.* | | | 18,296 | | | | 426,480 | |

| Five Prime Therapeutics, Inc.* | | | 15,158 | | | | 487,330 | |

| Galena Biopharma, Inc.* | | | 172,749 | | | | 290,218 | |

| Geron Corp.* | | | 87,922 | | | | 305,089 | |

| Idera Pharmaceuticals, Inc.* | | | 92,409 | | | | 255,049 | |

| Ignyta, Inc.* | | | 20,823 | | | | 213,228 | |

| Immune Design Corp.* | | | 13,331 | | | | 173,303 | |

| ImmunoGen, Inc.* | | | 24,660 | | | | 288,522 | |

| Immunomedics, Inc.* | | | 84,051 | | | | 251,312 | |

| Infinity Pharmaceuticals, Inc.* | | | 31,082 | | | | 321,699 | |

| Inovio Pharmaceuticals, Inc.* | | | 40,446 | | | | 256,023 | |

| Insmed, Inc.* | | | 14,934 | | | | 296,291 | |

| Intercept Pharmaceuticals, Inc.* | | | 1,407 | | | | 221,180 | |

| Juno Therapeutics, Inc.* | | | 5,721 | | | | 296,119 | |

| Karyopharm Therapeutics, Inc.* | | | 12,837 | | | | 171,374 | |

| Kite Pharma, Inc.* | | | 5,877 | | | | 399,930 | |

| La Jolla Pharmaceutical Co.* | | | 15,477 | | | | 386,770 | |

| Lexicon Pharmaceuticals, Inc.* | | | 43,515 | | | | 413,828 | |

| Lion Biotechnologies, Inc.* | | | 29,483 | | | | 190,755 | |

| MacroGenics, Inc.* | | | 9,722 | | | | 302,063 | |

| Merrimack Pharmaceuticals, Inc.* | | | 31,480 | | | | 294,023 | |

| Mirati Therapeutics, Inc.* | | | 11,075 | | | | 391,834 | |

| Neurocrine Biosciences, Inc.* | | | 8,077 | | | | 396,500 | |

| NewLink Genetics Corp.* | | | 7,610 | | | | 291,235 | |

| Northwest Biotherapeutics, Inc.* | | | 33,937 | | | | 165,613 | |

| Novavax, Inc.* | | | 38,758 | | | | 261,617 | |

| OncoMed Pharmaceuticals, Inc.* | | | 13,624 | | | | 272,616 | |

| Oncothyreon, Inc.* | | | 88,374 | | | | 261,587 | |

| Ophthotech Corp.* | | | 7,041 | | | | 351,557 | |

| Paratek Pharmaceuticals, Inc.* | | | 12,478 | | | | 216,618 | |

| | | | | |

| Security Description | | Shares | | Value |

| Common Stocks (continued) | | | | | | | | |

| Portola Pharmaceuticals, Inc.* | | | 7,738 | | | $ | 368,406 | |

| Prothena Corp. PLC* | | | 7,260 | | | | 373,963 | |

| PTC Therapeutics, Inc.* | | | 6,840 | | | | 170,111 | |

| Puma Biotechnology, Inc.* | | | 2,647 | | | | 218,166 | |

| Radius Health, Inc.* | | | 7,032 | | | | 451,665 | |

| Regulus Therapeutics, Inc.* | | | 32,339 | | | | 215,054 | |

| Relypsa, Inc.* | | | 10,034 | | | | 160,444 | |

| Rigel Pharmaceuticals, Inc.* | | | 97,110 | | | | 246,659 | |

| Sage Therapeutics, Inc.* | | | 4,405 | | | | 221,263 | |

| Sangamo BioSciences, Inc.* | | | 31,596 | | | | 222,752 | |

| Sarepta Therapeutics, Inc.* | | | 12,044 | | | | 289,779 | |

| Sorrento Therapeutics, Inc.* | | | 22,949 | | | | 198,279 | |

| Spark Therapeutics, Inc.* | | | 4,739 | | | | 255,432 | |

| Synergy Pharmaceuticals, Inc.* | | | 70,157 | | | | 449,706 | |

| Synta Pharmaceuticals Corp.* | | | 145,664 | | | | 97,595 | |

| Tetraphase Pharmaceuticals, Inc.* | | | 8,014 | | | | 72,366 | |

| TG Therapeutics, Inc.* | | | 23,086 | | | | 285,574 | |

| Threshold Pharmaceuticals, Inc.* | | | 82,836 | | | | 315,605 | |

| Tokai Pharmaceuticals, Inc.* | | | 24,225 | | | | 267,686 | |

| Trevena, Inc.* | | | 49,605 | | | | 477,200 | |

| Ultragenyx Pharmaceutical, Inc.* | | | 3,877 | | | | 385,180 | |

| uniQure N.V.* | | | 10,633 | | | | 188,523 | |

| Verastem, Inc.* | | | 42,334 | | | | 77,895 | |

| Versartis, Inc.* | | | 18,888 | | | | 195,113 | |

| Xencor, Inc.* | | | 16,868 | | | | 182,680 | |

| XOMA Corp.* | | | 93,418 | | | | 113,970 | |

| Zafgen, Inc.* | | | 9,657 | | | | 92,997 | |

| ZIOPHARM Oncology, Inc.* | | | 32,067 | | | | 365,243 | |

| ZS Pharma, Inc.* | | | 6,314 | | | | 410,473 | |

| TOTAL INVESTMENTS — 99.8% | | | | | | | | |

| (Cost $30,855,074) | | | | | | | 23,225,324 | |

| Other Assets in Excess of Liabilities — 0.2% | | | | | | | 35,420 | |

| Net Assets — 100.0% | | | | | | $ | 23,260,744 | |

| * | Non-income producing security. |

The accompanying notes are an integral part of these financial statements.

|

| Schedule of Investments — BioShares Biotechnology Products Fund |

| October 31, 2015 |

| | | | | |

| Security Description | | Shares | | Value |

| Common Stocks — 100.0% | | | | | | | | |

| Health Care — 100.0% | | | | | | | | |

| Acorda Therapeutics, Inc.* | | | 20,833 | | | $ | 750,821 | |

| Aegerion Pharmaceuticals, Inc.* | | | 36,387 | | | | 534,161 | |

| Alexion Pharmaceuticals, Inc.* | | | 3,871 | | | | 681,296 | |

| Amgen, Inc. | | | 4,316 | | | | 682,705 | |

| Anacor Pharmaceuticals, Inc.* | | | 9,654 | | | | 1,085,206 | |

| Arena Pharmaceuticals, Inc.* | | | 158,535 | | | | 299,631 | |

| ARIAD Pharmaceuticals, Inc.* | | | 78,433 | | | | 536,482 | |

| Biogen, Inc.* | | | 1,727 | | | | 501,711 | |

| BioMarin Pharmaceutical, Inc.* | | | 5,500 | | | | 643,720 | |

| Celgene Corp.* | | | 6,041 | | | | 741,291 | |

| Dyax Corp.* | | | 26,569 | | | | 731,445 | |

| Enanta Pharmaceuticals, Inc.* | | | 15,520 | | | | 435,957 | |

| Exelixis, Inc.* | | | 194,378 | | | | 1,170,156 | |

| Gilead Sciences, Inc. | | | 5,676 | | | | 613,746 | |

| Halozyme Therapeutics, Inc.* | | | 32,824 | | | | 513,696 | |

| Incyte Corp.* | | | 6,469 | | | | 760,302 | |

| Ironwood Pharmaceuticals, Inc.* | | | 55,605 | | | | 631,673 | |

| Isis Pharmaceuticals, Inc.* | | | 10,739 | | | | 517,083 | |

| Keryx Biopharmaceuticals, Inc.* | | | 69,278 | | | | 310,365 | |

| Ligand Pharmaceuticals, Inc.* | | | 7,428 | | | | 671,120 | |

| MannKind Corp.* | | | 109,936 | | | | 363,888 | |

| Medicines Co. (The)* | | | 23,415 | | | | 801,730 | |

| Medivation, Inc.* | | | 11,924 | | | | 501,523 | |

| Momenta Pharmaceuticals, Inc.* | | | 29,529 | | | | 484,571 | |

| Nektar Therapeutics* | | | 59,929 | | | | 711,357 | |

| Omeros Corp.* | | | 34,267 | | | | 429,366 | |

| Orexigen Therapeutics, Inc.* | | | 151,722 | | | | 461,235 | |

| PDL BioPharma, Inc. | | | 103,575 | | | | 474,373 | |

| Progenics Pharmaceuticals, Inc.* | | | 98,765 | | | | 724,935 | |

| Raptor Pharmaceutical Corp.* | | | 46,027 | | | | 250,847 | |

| Regeneron Pharmaceuticals, Inc.* | | | 1,343 | | | | 748,575 | |

| Retrophin, Inc.* | | | 21,703 | | | | 415,178 | |

| Seattle Genetics, Inc.* | | | 14,339 | | | | 594,925 | |

| Theravance Biopharma, Inc.* | | | 46,995 | | | | 702,575 | |

| United Therapeutics Corp.* | | | 3,608 | | | | 529,041 | |

| Vanda Pharmaceuticals, Inc.* | | | 51,625 | | | | 554,452 | |

| Vertex Pharmaceuticals, Inc.* | | | 5,431 | | | | 677,463 | |

| XenoPort, Inc.* | | | 104,782 | | | | 640,218 | |

| TOTAL INVESTMENTS — 100.0% | | | | | | | | |

| (Cost $26,417,862) | | | | | | | 22,878,819 | |

| Liabilities in Excess of Other Assets — (0.0)%(1) | | | | | | | (4,672 | ) |

| Net Assets — 100.0% | | | | | | $ | 22,874,147 | |

| * | Non-income producing security. |

The accompanying notes are an integral part of these financial statements.

|

| Schedule of Investments — Tuttle Tactical Management Multi-Strategy Income ETF |

| October 31, 2015 |

| | | | | |

| Security Description | | Shares | | Value |

| Exchange Traded Funds — 96.1% | | | | | | | | |

| Debt Funds — 63.8% | | | | | | | | |

| iShares 1-3 Year Treasury Bond ETF | | | 262,131 | | | $ | 22,236,573 | |

| iShares Core U.S. Aggregate Bond ETF | | | 4,422 | | | | 483,988 | |

| iShares iBoxx $ High Yield Corporate Bond ETF | | | 45,238 | | | | 3,871,015 | |

| ProShares Short 20+ Year Treasury* | | | 179,625 | | | | 4,416,979 | |

| SPDR Barclays International Treasury Bond ETF | | | 1 | | | | 52 | |

| Total Debt Funds | | | | | | | 31,008,607 | |

| |

| Equity Funds — 32.3% | | | | | | | | |

| iShares Select Dividend ETF | | | 44,452 | | | | 3,417,025 | |

| ProShares S&P 500 Dividend Aristocrats ETF | | | 62,814 | | | | 3,135,047 | |

| Schwab US Dividend Equity ETF | | | 152,265 | | | | 5,953,561 | |

| Vanguard Dividend Appreciation ETF | | | 40,943 | | | | 3,222,624 | |

| Total Equity Funds | | | | | | | 15,728,257 | |

| |

| TOTAL INVESTMENTS — 96.1% | | | | | | | | |

| (Cost $46,612,906) | | | | | | | 46,736,864 | |

| Other Assets in Excess of Liabilities — 3.9% | | | | | | | 1,883,681 | |

| Net Assets — 100.0% | | | | | | $ | 48,620,545 | |

| * | Non-income producing security. |

The accompanying notes are an integral part of these financial statements.

|

| Schedule of Investments — Tuttle Tactical Management U.S. Core ETF |

| October 31, 2015 |

| | | | | |

| Security Description | | Shares | | Value |

| Exchange Traded Funds — 98.1% | | | | | | | | |

| Debt Funds — 57.9% | | | | | | | | |

| Direxion Daily 20 Year Plus Treasury | | | | | | | | |

| Bull 3x Shares* | | | 17,054 | | | $ | 1,333,282 | |

| iShares 1-3 Year Treasury Bond ETF | | | 305,083 | | | | 25,880,191 | |

| iShares 20+ Year Treasury Bond ETF | | | 136,617 | | | | 16,773,835 | |

| Total Debt Funds | | | | | | | 43,987,308 | |

| |

| Equity Funds — 40.2% | | | | | | | | |

| Consumer Discretionary Select Sector | | | | | | | | |

| SPDR Fund | | | 20,085 | | | | 1,626,282 | |

| Consumer Staples Select Sector SPDR Fund | | | 31,520 | | | | 1,572,218 | |

| Direxion Daily S&P 500 Bull 3x Shares* | | | 20,221 | | | | 1,771,764 | |

| iShares Core S&P Small-Cap ETF | | | 118,883 | | | | 13,439,723 | |

| SPDR S&P 500 ETF Trust | | | 50,741 | | | | 10,550,576 | |

| Technology Select Sector SPDR Fund | | | 36,490 | | | | 1,592,789 | |

| Total Equity Funds | | | | | | | 30,553,352 | |

| |

| TOTAL INVESTMENTS — 98.1% | | | | | | | | |

| (Cost $74,079,925) | | | | | | | 74,540,660 | |

| Other Assets in Excess of Liabilities — 1.9% | | | | | | | 1,406,494 | |

| Net Assets — 100.0% | | | | | | $ | 75,947,154 | |

| * | Non-income producing security. |

The accompanying notes are an integral part of these financial statements.

|

| Schedule of Investments — Virtus Newfleet Multi-Sector Unconstrained Bond ETF |

| October 31, 2015 |

| | | | | |

| Investments | | Principal | | Value |

| CORPORATE BONDS — 32.7% | | | | | | | | |

| Communications — 1.1% | | | | | | | | |

| Level 3 Financing, Inc., 5.38%, 01/15/24(1) | | $ | 160,000 | | | $ | 162,400 | |

| Neptune Finco Corp., 10.13%, 01/15/23(1) | | | 400,000 | | | | 424,000 | |

| Neptune Finco Corp., 6.63%, 10/15/25(1) | | | 200,000 | | | | 211,000 | |

| Sprint Communications, Inc., 6.00%, 11/15/22 | | | 465,000 | | | | 398,500 | |

| T-Mobile USA, Inc., 6.13%, 01/15/22 | | | 500,000 | | | | 510,000 | |

| Total Communications | | | | | | | 1,705,900 | |

| |

| Consumer Discretionary — 7.7% | | | | | | | | |

| Argos Merger Sub, Inc., 7.13%, 03/15/23(1) | | | 600,000 | | | | 633,000 | |

| Boyd Gaming Corp., 6.88%, 05/15/23 | | | 600,000 | | | | 639,000 | |

| Caesars Entertainment Resort Properties LLC / | | | | | | | | |

| Caesars Entertainment Resort Properties, | | | | | | | | |

| 8.00%, 10/01/20 | | | 250,000 | | | | 249,375 | |

| Caesars Growth Properties Holdings LLC / | | | | | | | | |

| Caesars Growth Properties Finance, Inc., | | | | | | | | |

| 9.38%, 05/01/22 | | | 300,000 | | | | 249,750 | |

| CalAtlantic Group, Inc., 5.88%, 11/15/24 | | | 440,000 | | | | 464,200 | |

| CCO Holdings LLC / CCO Holdings | | | | | | | | |

| Capital Corp., 5.13%, 05/01/23(1) | | | 325,000 | | | | 326,625 | |

| CCO Safari II LLC, 4.91%, 07/23/25(1) | | | 500,000 | | | | 509,007 | |

| Clear Channel Worldwide | | | | | | | | |

| Holdings, Inc., 7.63%, 03/15/20 | | | 750,000 | | | | 780,937 | |

| DISH DBS Corp., 5.00%, 03/15/23 | | | 580,000 | | | | 537,950 | |

| iHeartCommunications, Inc., 9.00%, 12/15/19 | | | 520,000 | | | | 442,000 | |

| Jarden Corp., 5.00%, 11/15/23(1) | | | 180,000 | | | | 185,850 | |

| Landry’s, Inc., 9.38%, 05/01/20(1) | | | 600,000 | | | | 646,500 | |

| Lennar Corp., 4.50%, 06/15/19 | | | 450,000 | | | | 469,125 | |

| Lennar Corp., 4.88%, 12/15/23 | | | 145,000 | | | | 145,181 | |

| MDC Holdings, Inc., 5.50%, 01/15/24 | | | 640,000 | | | | 656,000 | |

| MGM Resorts International, 6.75%, 10/01/20 | | | 850,000 | | | | 909,500 | |

| Penn National Gaming, Inc., 5.88%, 11/01/21 | | | 450,000 | | | | 461,250 | |

| QVC, Inc., 5.13%, 07/02/22 | | | 600,000 | | | | 609,670 | |

| RCN Telecom Services LLC / RCN Capital | | | | | | | | |

| Corp., 8.50%, 08/15/20(1) | | | 500,000 | | | | 527,500 | |

| Scientific Games International, Inc., | | | | | | | | |

| 7.00%, 01/01/22(1) | | | 455,000 | | | | 459,550 | |

| Signet UK Finance PLC, 4.70%, 06/15/24 | | | 500,000 | | | | 502,384 | |

| Toll Brothers Finance Corp., 5.88%, 02/15/22 | | | 600,000 | | | | 648,750 | |

| TRI Pointe Holdings, Inc., 4.38%, 06/15/19 | | | 150,000 | | | | 149,813 | |

| TRI Pointe Holdings, Inc., 5.88%, 06/15/24 | | | 600,000 | | | | 603,000 | |

| Total Consumer Discretionary | | | | | | | 11,805,917 | |

| |

| Consumer Staples — 1.2% | | | | | | | | |

| Dole Food Co., Inc., 7.25%, 05/01/19(1) | | | 500,000 | | | | 503,000 | |

| Rite Aid Corp., 6.13%, 04/01/23(1) | | | 600,000 | | | | 648,750 | |

| Safeway, Inc., 7.25%, 02/01/31 | | | 185,000 | | | | 180,375 | |

| Tops Holding LLC / Tops Markets II Corp., | | | | | | | | |

| 8.00%, 06/15/22(1) | | | 500,000 | | | | 520,000 | |

| Total Consumer Staples | | | | | | | 1,852,125 | |

| |

| Energy — 2.0% | | | | | | | | |

| Enbridge Energy Partners LP, 4.38%, 10/15/20 | | | 80,000 | | | | 81,121 | |

| Kinder Morgan, Inc., 5.63%, 11/15/23(1) | | | 600,000 | | | | 584,032 | |

| Regency Energy Partners LP / Regency Energy | | | | | | | | |

| Finance Corp., 5.00%, 10/01/22 | | | 530,000 | | | | 515,819 | |

| Sunoco LP / Sunoco Finance Corp., | | | | | | | | |

| 6.38%, 04/01/23(1) | | | 1,075,000 | | | | 1,088,438 | |

| Transocean, Inc., 5.05%, 12/15/16 | | | 755,000 | | | | 753,822 | |

| Total Energy | | | | | | | 3,023,232 | |

| | | | | |

| Investments | | Principal | | Value |

| CORPORATE BONDS — (continued) | | | | | | | | |

| Financials — 8.4% | | | | | | | | |

| Air Lease Corp., 2.63%, 09/04/18 | | $ | 400,000 | | | $ | 398,658 | |

| American Campus Communities Operating | | | | | | | | |

| Partnership LP, 3.35%, 10/01/20 | | | 80,000 | | | | 80,731 | |

| Ares Finance Co. II LLC, 5.25%, 09/01/25(1) | | | 625,000 | | | | 631,315 | |

| Aviation Capital Group Corp., 2.88%, 09/17/18 | | | 455,000 | | | | 455,218 | |

| Aviation Capital Group Corp., 2.88%, 09/17/18(1) | | | 190,000 | | | | 190,091 | |

| Bank of New York Mellon Corp. (The), | | | | | | | | |

| 4.95%, 12/29/49(2) | | | 760,000 | | | | 760,950 | |

| Block Financial LLC, 4.13%, 10/01/20 | | | 380,000 | | | | 386,311 | |

| Capital One Financial Corp., 4.20%, 10/29/25 | | | 460,000 | | | | 460,928 | |

| Compass Bank, 3.88%, 04/10/25 | | | 500,000 | | | | 466,517 | |

| Corrections Corp. of America, 5.00%, 10/15/22 | | | 700,000 | | | | 712,250 | |

| Digital Delta Holdings LLC, 3.40%, 10/01/20(1) | | | 645,000 | | | | 648,972 | |

| DuPont Fabros Technology LP, 5.88%, 09/15/21 | | | 600,000 | | | | 633,000 | |

| First Cash Financial Services, Inc., | | | | | | | | |

| 6.75%, 04/01/21 | | | 300,000 | | | | 300,750 | |

| First Horizon National Corp., 3.50%, 12/15/20 | | | 610,000 | | | | 608,631 | |

| General Motors Financial Co., Inc., | | | | | | | | |

| 3.45%, 04/10/22 | | | 650,000 | | | | 635,646 | |

| JPMorgan Chase & Co., 5.00%, 12/29/49(2) | | | 615,000 | | | | 607,159 | |

| Kilroy Realty LP, 4.38%, 10/01/25 | | | 640,000 | | | | 650,235 | |

| Kimco Realty Corp., 3.40%, 11/01/22 | | | 395,000 | | | | 395,834 | |

| McGraw Hill Financial, Inc., 3.30%, 08/14/20(1) | | | 259,000 | | | | 263,851 | |

| McGraw Hill Financial, Inc., 4.00%, 06/15/25(1) | | | 400,000 | | | | 398,136 | |

| National Retail Properties, Inc., 4.00%, 11/15/25 | | | 185,000 | | | | 184,479 | |

| Prudential Financial, Inc., 5.63%, 06/15/43(2) | | | 450,000 | | | | 472,050 | |

| Sabra Health Care LP / Sabra Capital | | | | | | | | |

| Corp., 5.50%, 02/01/21 | | | 355,000 | | | | 371,756 | |

| Select Income REIT, 4.15%, 02/01/22 | | | 540,000 | | | | 532,692 | |

| Teachers Insurance & Annuity Association of | | | | | | | | |

| America, 4.38%, 09/15/54(1)(2) | | | 550,000 | | | | 553,498 | |

| Ventas Realty LP, 4.13%, 01/15/26 | | | 450,000 | | | | 451,167 | |

| Wells Fargo & Co., 7.98%, 03/29/49(2) | | | 500,000 | | | | 533,125 | |

| Total Financials | | | | | | | 12,783,950 | |

| |

| Health Care — 4.3% | | | | | | | | |

| AbbVie, Inc., 3.60%, 05/14/25 | | | 500,000 | | | | 492,496 | |

| Acadia Healthcare Co., Inc., 5.63%, 02/15/23(1) | | | 90,000 | | | | 90,563 | |

| Acadia Healthcare Co., Inc., 5.63%, 02/15/23 | | | 385,000 | | | | 387,406 | |

| Capsugel SA, 7.00%, 05/15/19(1)(3) | | | 455,000 | | | | 459,266 | |

| Endo Ltd. / Endo Finance LLC / Endo | | | | | | | | |

| Finco, Inc., 6.00%, 07/15/23(1) | | | 450,000 | | | | 452,250 | |

| HCA, Inc., 6.50%, 02/15/20 | | | 700,000 | | | | 784,875 | |

| HealthSouth Corp., 5.75%, 09/15/25(1) | | | 495,000 | | �� | | 495,309 | |

| inVentiv Health, Inc., 9.00%, 01/15/18(1) | | | 150,000 | | | | 155,250 | |

| Mallinckrodt International Finance SA / | | | | | | | | |

| Mallinckrodt CB LLC, 5.63%, 10/15/23(1) | | | 775,000 | | | | 735,281 | |

| Owens & Minor, Inc., 3.88%, 09/15/21 | | | 625,000 | | | | 633,747 | |

| Quintiles Transnational Corp., | | | | | | | | |

| 4.88%, 05/15/23(1) | | | 200,000 | | | | 206,624 | |

| Tenet Healthcare Corp., 4.50%, 04/01/21 | | | 750,000 | | | | 753,750 | |

| Tenet Healthcare Corp., 8.13%, 04/01/22 | | | 370,000 | | | | 393,125 | |

| Valeant Pharmaceuticals International, Inc., | | | | | | | | |

| 5.38%, 03/15/20(1) | | | 625,000 | | | | 546,875 | |

| Total Health Care | | | | | | | 6,586,817 | |

| |

| Industrials — 4.5% | | | | | | | | |

| ADS Waste Holdings, Inc., 8.25%, 10/01/20 | | | 375,000 | | | | 395,156 | |

| ADT Corp. (The), 6.25%, 10/15/21 | | | 600,000 | | | | 651,000 | |

| Builders FirstSource, Inc., 10.75%, 08/15/23(1) | | | 200,000 | | | | 207,500 | |

The accompanying notes are an integral part of these financial statements.

|

| Schedule of Investments — Virtus Newfleet Multi-Sector Unconstrained Bond ETF (continued) |

| October 31, 2015 |

| | | | | |

| Investments | | Principal | | Value |

| CORPORATE BONDS — (continued) | | | | | | | | |

| Industrials — (continued) | | | | | | | | |

| CEB, Inc., 5.63%, 06/15/23(1) | | $ | 300,000 | | | $ | 305,625 | |

| Hawaiian Airlines Pass-Through Certificates, | | | | | | | | |

| Class B, Series 2013-1, 4.95%, 01/15/22 | | | 1,105,410 | | | | 1,073,630 | |

| HD Supply, Inc., 5.25%, 12/15/21(1) | | | 700,000 | | | | 737,625 | |

| Masco Corp., 5.95%, 03/15/22 | | | 600,000 | | | | 666,000 | |

| NCI Building Systems, Inc., 8.25%, 01/15/23(1) | | | 350,000 | | | | 372,750 | |

| Penske Truck Leasing Co. LP / PTL Finance | | | | | | | | |

| Corp., 3.38%, 02/01/22(1) | | | 500,000 | | | | 498,100 | |

| SBA Tower Trust, 3.16%, 10/15/20(1) | | | 375,000 | | | | 374,850 | |

| Toll Brothers Finance Corp., 4.88%, 11/15/25 | | | 400,000 | | | | 400,500 | |

| TransDigm, Inc., 6.00%, 07/15/22 | | | 600,000 | | | | 609,000 | |

| United Rentals North America, Inc., | | | | | | | | |

| 5.50%, 07/15/25 | | | 535,000 | | | | 535,669 | |

| Total Industrials | | | | | | | 6,827,405 | |

| |

| Information Technology — 1.9% | | | | | | | | |

| Fidelity National Information Services, Inc., | | | | | | | | |

| 2.85%, 10/15/18 | | | 65,000 | | | | 65,734 | |

| Fidelity National Information Services, Inc., | | | | | | | | |

| 3.63%, 10/15/20 | | | 210,000 | | | | 213,970 | |

| Fidelity National Information Services, Inc., | | | | | | | | |

| 4.50%, 10/15/22 | | | 340,000 | | | | 347,605 | |

| First Data Corp., 11.75%, 08/15/21 | | | 1,025,000 | | | | 1,171,063 | |

| First Data Corp., 7.00%, 12/01/23(1) | | | 120,000 | | | | 122,400 | |

| Hewlett Packard Enterprise Co., 2.45%, | | | | | | | | |

| 10/05/17(1) | | | 135,000 | | | | 135,458 | |

| Hewlett Packard Enterprise Co., 2.85%, | | | | | | | | |

| 10/05/18(1) | | | 130,000 | | | | 130,364 | |

| Hewlett Packard Enterprise Co., | | | | | | | | |

| 3.60%, 10/15/20(1) | | | 25,000 | | | | 25,207 | |

| Hewlett Packard Enterprise Co., | | | | | | | | |

| 4.40%, 10/15/22(1) | | | 135,000 | | | | 136,319 | |

| Hewlett Packard Enterprise Co., | | | | | | | | |

| 4.90%, 10/15/25(1) | | | 135,000 | | | | 133,659 | |

| KLA-Tencor Corp., 4.65%, 11/01/24 | | | 450,000 | | | | 453,937 | |

| Total Information Technology | | | | | | | 2,935,716 | |

| |

| Materials — 0.3% | | | | | | | | |

| Berry Plastics Corp., 6.00%, 10/15/22(1) | | | 500,000 | | | | 525,000 | |

| |

| Telecommunication Services — 0.8% | | | | | | | | |

| AT&T, Inc., 3.00%, 06/30/22 | | | 600,000 | | | | 589,407 | |

| CenturyLink, Inc., 5.63%, 04/01/20 | | | 385,000 | | | | 386,882 | |

| Frontier Communications Corp., | | | | | | | | |

| 8.88%, 09/15/20(1) | | | 90,000 | | | | 93,656 | |

| Frontier Communications Corp., | | | | | | | | |

| 10.50%, 09/15/22(1) | | | 100,000 | | | | 104,000 | |

| Total Telecommunication Services | | | | | | | 1,173,945 | |

| |

| Utilities — 0.5% | | | | | | | | |

| Calpine Corp., 5.38%, 01/15/23 | | | 470,000 | | | | 451,787 | |

| Exelon Corp., 2.85%, 06/15/20 | | | 30,000 | | | | 30,056 | |

| NRG Yield Operating LLC, 5.38%, 08/15/24 | | | 345,000 | | | | 317,400 | |

| Total Utilities | | | | | | | 799,243 | |

| Total Corporate Bonds | | | | | | | | |

| (Cost $49,559,450) | | | | | | | 50,019,250 | |

| | | | | |

| Investments | | Principal | | Value |

| TERM LOANS — 14.1% | | | | | | | | |

| Consumer Discretionary — 4.1% | | | | | | | | |

| Aristocrat International Pty, Ltd., 4.75%, | | | | | | | | |

| 10/20/21(2) | | $ | 640,000 | | | $ | 642,602 | |

| Brickman Group Ltd LLC (The), 7.50%, | | | | | | | | |

| 12/18/21(2) | | | 325,000 | | | | 308,425 | |

| Caesars Entertainment Resort Properties | | | | | | | | |

| LLC, 7.00%, 10/11/20(2) | | | 249,365 | | | | 237,053 | |

| CDS US Intermediate Holdings, Inc., | | | | | | | | |

| 5.00%, 07/08/22(2) | | | 450,000 | | | | 452,624 | |

| CS Intermediate Holdco 2 LLC, 4.00%, | | | | | | | | |

| 04/04/21(2) | | | 498,737 | | | | 496,166 | |

| Delta 2 Lux Sarl, 4.75%, 07/30/21(2) | | | 460,000 | | | | 452,364 | |

| iHeartCommunications, Inc., 6.94%, | | | | | | | | |

| 01/30/19(2) | | | 175,000 | | | | 147,014 | |

| Infiltrator Systems Integrated LLC, 5.25%, | | | | | | | | |

| 05/21/22(2) | | | 400,000 | | | | 400,400 | |

| Mohegan Tribal Gaming Authority, 5.50%, | | | | | | | | |

| 06/15/18(2) | | | 640,000 | | | | 634,240 | |

| Party City Holdings, Inc., 4.25%, | | | | | | | | |

| 08/19/22(2) | | | 380,000 | | | | 380,473 | |

| Scientific Games International, Inc., 6.00%, | | | | | | | | |

| 10/01/21(2) | | | 299,246 | | | | 292,950 | |

| Staples, Inc., 3.50%, 04/24/21(2) | | | 400,000 | | | | 398,614 | |

| TI Group Automotive Systems LLC, | | | | | | | | |

| 4.50%, 06/30/22(2) | | | 515,000 | | | | 510,707 | |

| TWCC Holding Corp., 5.75%, 02/13/20(2) | | | 448,872 | | | | 449,815 | |

| Virgin Media Investment Holdings, Ltd., | | | | | | | | |

| 3.50%, 06/30/23(2) | | | 400,000 | | | | 398,358 | |

| Total Consumer Discretionary | | | | | | | 6,201,805 | |

| |

| Consumer Staples — 0.9% | | | | | | | | |

| Albertsons LLC, 5.50%, 08/25/21(2) | | | 600,000 | | | | 600,783 | |

| Coty, Inc., 3.75%, 10/27/22(2) | | | 107,000 | | | | 107,569 | |

| Galleria Co., 3.75%, 10/22/22(2) | | | 214,000 | | | | 214,569 | |

| Hostess Brands LLC, 8.50%, 08/03/23(2) | | | 500,000 | | | | 499,845 | |

| Total Consumer Staples | | | | | | | 1,422,766 | |

| |

| Energy — 0.2% | | | | | | | | |

| Chelsea Petroleum Products I LLC, 5.25%, | | | | | | | | |

| 07/22/22(2) | | | 330,000 | | | | 328,763 | |

| |

| Health Care — 2.7% | | | | | | | | |

| Concordia Healthcare Corp., 5.25%, 10/21/21(2) | | | 262,000 | | | | 252,613 | |

| Greatbatch, Ltd., 5.25%, 10/27/22(2) | | | 212,000 | | | | 212,895 | |

| inVentiv Health, Inc., 7.75%, 05/15/18(2) | | | 500,000 | | | | 499,065 | |

| MedImpact OpCo Holdings, Inc., 5.75%, | | | | | | | | |

| 10/23/22(2) | | | 275,000 | | | | 274,656 | |

| NVA Holdings, Inc., 8.00%, 08/14/22(2) | | | 380,000 | | | | 377,308 | |

| Onex Schumacher Finance LP, 5.00%, | | | | | | | | |

| 07/31/22(2) | | | 282,000 | | | | 280,942 | |

| Ortho-Clinical Diagnostics, Inc., 4.75%, | | | | | | | | |

| 06/30/21(2) | | | 750,000 | | | | 740,625 | |

| RegionalCare Hospital Partners, Inc., | | | | | | | | |

| 5.25%, 04/23/19(2) | | | 500,000 | | | | 494,585 | |

| Sedgwick Claims Management Services, | | | | | | | | |

| Inc., 6.75%, 02/28/22(2) | | | 650,000 | | | | 611,409 | |

| Surgery Center Holdings, Inc., 5.25%, | | | | | | | | |

| 11/03/20(2) | | | 380,000 | | | | 378,735 | |

| Total Health Care | | | | | | | 4,122,833 | |

The accompanying notes are an integral part of these financial statements.

|

| Schedule of Investments — Virtus Newfleet Multi-Sector Unconstrained Bond ETF (continued) |

| October 31, 2015 |

| | | | | |

| Investments | | Principal | | Value |

| TERM LOANS — (continued) | | | | | | | | |

| Industrials — 0.5% | | | | | | | | |

| TransDigm, Inc., 3.75%, 06/04/21(2) | | $ | 324,179 | | | $ | 320,173 | |

| Waste Industries USA, Inc., 4.25%, 02/27/20(2) | | | 448,872 | | | | 451,047 | |

| Total Industrials | | | | | | | 771,220 | |

| |

| Information Technology — 3.9% | | | | | | | | |

| First Data Corp., 3.70%, 03/24/18(2) | | | 6,050,000 | | | | 6,012,732 | |

| |

| Materials — 0.8% | | | | | | | | |

| Anchor Glass Container Corp., 4.50%, | | | | | | | | |

| 06/24/22(2) | | | 325,000 | | | | 325,405 | |

| Summit Materials LLC, 4.25%, 07/17/22(2) | | | 450,000 | | | | 449,156 | |

| Univar USA, Inc., 4.25%, 07/01/22(2) | | | 450,000 | | | | 444,737 | |

| Total Materials | | | | | | | 1,219,298 | |

| |

| Technology — 0.3% | | | | | | | | |

| Applied Systems, Inc., 7.50%, 01/23/22(2) | | | 414,000 | | | | 401,321 | |

| |

| Telecommunication Services — 0.3% | | | | | | | | |

| Crown Castle Operating Co., 3.00%, 01/31/21(2) | | | 523,668 | | | | 524,348 | |

| |

| Utilities — 0.4% | | | | | | | | |

| NRG Energy, Inc., 2.75%, 07/01/18(2) | | | 538,619 | | | | 525,040 | |

| |

| Total Term Loans | | | | | | | | |

| (Cost $21,583,177) | | | | | | | 21,530,126 | |

| |

| MORTGAGE BACKED SECURITIES — 11.1% |

| Commercial Mortgage Backed Securities — 4.3% |

| Colony Multifamily Mortgage Trust, Class A, | | | | | | | | |

| Series 2014-1, 2.54%, 04/20/50(1) | | | 955,508 | | | | 954,234 | |

| Credit Suisse Commercial Mortgage Trust, | | | | | | | | |

| Class A1AM, Series 2007-C5, | | | | | | | | |

| 5.87%, 09/15/40(2) | | | 1,000,000 | | | | 1,017,551 | |

| Csail Commercial Mortgage Trust, Class AS, | | | | | | | | |

| Series 2015-C2, 3.85%, 06/15/57 | | | 340,000 | | | | 348,034 | |

| DBUBS Mortgage Trust, Class D, | | | | | | | | |

| Series 2011-LC3A, 5.58%, 08/10/44(1)(2) | | | 905,000 | | | | 953,842 | |

| FREMF Mortgage Trust, Class B, | | | | | | | | |

| Series 2015-K720, 3.39%, 07/25/22(1)(2)(4)(5) | | | 330,000 | | | | 294,355 | |

| Hilton USA Trust, Class EFX, | | | | | | | | |

| Series 2013-HLT, 4.60%, 11/05/30(1)(2) | | | 1,000,000 | | | | 1,009,885 | |

| JPMorgan Chase Commercial Mortgage | | | | | | | | |

| Securities Trust, Class D, Series 2010-CNTR, | | | | | | | | |

| 6.39%, 08/05/32(1)(2) | | | 400,000 | | | | 451,333 | |

| Morgan Stanley Bank of America Merrill | | | | | | | | |

| Lynch Trust, Class AS, Series 2015-C22, | | | | | | | | |

| 3.56%, 04/15/48 | | | 1,000,000 | | | | 1,004,488 | |

| Morgan Stanley Bank of America Merrill | | | | | | | | |

| Lynch Trust, Class C, Series 2015-C26, | | | | | | | | |

| 4.41%, 11/15/48(4)(5) | | | 385,000 | | | | 383,542 | |

| Total Commercial Mortgage Backed Securities | | | | | | | 6,417,264 | |

| |

| Mortgage Securities — 1.9% | | | | | | | | |

| Fannie Mae, 3.50%, 08/01/45 | | | 2,483,064 | | | | 2,587,185 | |

| Freddie Mac Gold, 3.00%, 04/01/45 | | | 252,859 | | | | 255,142 | |