Table of Contents

As filed with the Securities and Exchange Commission on March 28, 2018.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number001-38055

NETSHOES (CAYMAN) LIMITED

(Exact Name of Registrant as Specified in its charter)

N/A

(Translation of Registrant’s name into English)

The Cayman Islands

(Jurisdiction of Incorporation or Organization)

Rua Vergueiro 961, Liberdade

01504-001 São Paulo – SP, Brazil

(Address of principal executive offices)

Marcio Kumruian

Chief Executive Officer

Tel.: +55 11 3028-8298, Email: ir@netshoes.com

Rua Vergueiro 961, Liberdade

01504-001 São Paulo – SP, Brazil

(Name, Telephone,E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class: | Name of each exchange on which registered: | |

| Common Shares, nominal value of US$0.0033 | The New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Table of Contents

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

| At December 31, 2017 | 31,056,244 shares of common stock |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Note- Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 ofRegulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, anon-accelerated filer or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” inRule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ | |

Non-accelerated filer ☒ | Emerging growth company ☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☐ U.S. GAAP | ☒ International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined inRule 12b-2 of the Exchange Act).

Yes ☐ No ☒

Table of Contents

| Page | ||||||||

| 1 | ||||||||

ITEM 1. | 4 | |||||||

ITEM 2. | 4 | |||||||

ITEM 3. | 5 | |||||||

A. | 5 | |||||||

B. | 9 | |||||||

C. | 9 | |||||||

D. | 9 | |||||||

ITEM 4. | 36 | |||||||

A. | 36 | |||||||

B. | 37 | |||||||

C. | 55 | |||||||

D. | 55 | |||||||

ITEM 4A. | 57 | |||||||

ITEM 5. | 57 | |||||||

A. | 57 | |||||||

B. | 70 | |||||||

C. | 76 | |||||||

D. | 76 | |||||||

E. | 76 | |||||||

F. | 77 | |||||||

G. | 77 | |||||||

ITEM 6. | 77 | |||||||

A. | 77 | |||||||

B. | 79 | |||||||

C. | 82 | |||||||

D. | 84 | |||||||

E. | 85 | |||||||

ITEM 7. | 85 | |||||||

A. | 85 | |||||||

B. | 89 | |||||||

C. | 91 | |||||||

ITEM 8. | 91 | |||||||

A. | 91 | |||||||

B. | 93 | |||||||

ITEM 9. | 93 | |||||||

A. | 93 | |||||||

B. | 94 | |||||||

C. | 94 | |||||||

D. | 94 | |||||||

E. | 94 | |||||||

F. | 94 | |||||||

i

Table of Contents

| Page | ||||||||

ITEM 10. | 94 | |||||||

A. | 94 | |||||||

B. | 94 | |||||||

C. | 107 | |||||||

D. | 108 | |||||||

E. | 108 | |||||||

F. | 112 | |||||||

G. | 112 | |||||||

H. | 112 | |||||||

I. | 112 | |||||||

ITEM 11. | 112 | |||||||

ITEM 12. | 114 | |||||||

A. | 114 | |||||||

B. | 114 | |||||||

C. | 114 | |||||||

D. | 114 | |||||||

| PART II | 114 | |||||||

ITEM 13. | 114 | |||||||

ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 114 | ||||||

ITEM 15. | 114 | |||||||

A. | 114 | |||||||

B. | Management’s Annual Report on Internal Control Over Financial Reporting | 115 | ||||||

C. | 115 | |||||||

D. | 115 | |||||||

ITEM 16. | 115 | |||||||

ITEM 16A. | 115 | |||||||

ITEM 16B. | 115 | |||||||

ITEM 16C. | 115 | |||||||

ITEM 16D. | 115 | |||||||

ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 115 | ||||||

ITEM 16F. | 116 | |||||||

ITEM 16G. | 116 | |||||||

ITEM 16H. | 116 | |||||||

| 116 | ||||||||

ITEM 17. | 116 | |||||||

ITEM 18. | 116 | |||||||

ITEM 19. | 116 | |||||||

| F-1 | ||||||||

ii

Table of Contents

INTRODUCTION

Certain Definitions

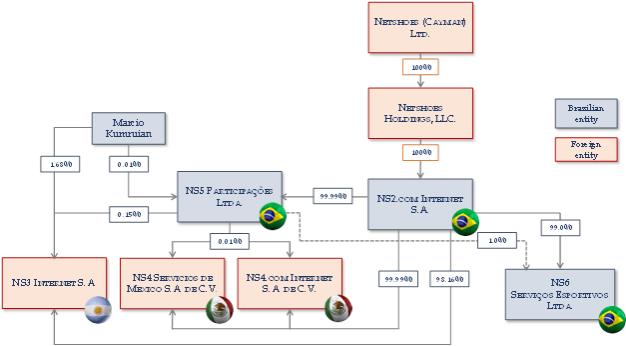

Unless otherwise indicated, all references herein to “Netshoes,” “we,” “us” and “our company” refer to Netshoes (Cayman) Limited, an exempted company with limited liability incorporated under the laws of the Cayman Islands, and its consolidated subsidiaries. References to “NS2” are to our subsidiary NS2.com Internet S.A., a corporation (sociedade anônima) incorporated under the laws of Brazil. References to “common shares” refer to the common shares of Netshoes (Cayman) Limited, except where the context requires otherwise. The term “Brazil” refers to the Federative Republic of Brazil, and the phrase “Brazilian government” refers to the federal government of Brazil. All references to “real,” “reais,” “Brazilianreal,” “Brazilianreais,” or “R$” are to the Brazilianreal, the official currency of Brazil; all references to “U.S. dollar,” “U.S. dollars,” or “US$” are to U.S. dollars, the official currency of the United States, all references to “Argentine peso,” or “ARS” are to the Argentinepeso, the official currency of Argentina, and all references to “Mexican peso,” or “MXN” are to the Mexicanpeso, the official currency of Mexico.

Financial Information

The financial information contained in this annual report derives from our audited consolidated financial statements as of December 31, 2016 and 2017 and for the fiscal years ended December 31, 2015, 2016 and 2017. These financial statements and related notes included elsewhere in this annual report are collectively referred to as our audited consolidated financial statements herein and throughout this annual report. Our audited consolidated financial statements are prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. Our fiscal year ends on December 31 of each year, so all references to a particular fiscal year are to the applicable year ended December 31.

Convenience Translation

The reporting currency for our audited consolidated financial statements is the Brazilian real and, solely for the convenience of the reader, we have provided convenience translations into U.S. dollars using the selling exchange rates published by the Brazilian Central Bank (Banco Central do Brasil) on its website. Unless otherwise indicated, convenience translations from reais into U.S. dollars in this annual report use the Brazilian Central Bank offer exchange rate published on December 31, 2017, which was R$3.3080 per US$1.00. No representation is made that the Brazilian reais amounts referred to could have been, or could be, converted into U.S. dollars at any particular rate. See “Item 3. Key Information––A. Selected Financial Data––Exchange Rates” for information regarding historical exchange rates of reais to U.S. dollars.

Market Data

This annual report includes statistical and other industry and market data that we obtained from industry publications and research, government andnon-government organization reports, surveys and studies conducted by third parties, including data and information we obtained from,e-Bit, Euromonitor International, IBOPE DTM, among others, and data derived from management’s knowledge and our experience in the industries in which we operate. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. Information derived from management’s knowledge and our experience is presented on a reasonable, good faith basis. Estimates of market and industry data are based on statistical models, key assumptions and limited data sampling, and actual market and industry data may differ significantly from estimated industry data.

1

Table of Contents

Rounding

Certain figures included in this annual report have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be exact arithmetic aggregations or percentages of the figures that precede them.

Emerging Growth Company Status

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the date of our first sale of our common equity securities pursuant to an effective registration statement under the Securities Act, (b) in which we have total annual revenues of at least US$1.07 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common shares that is held bynon-affiliates exceeds US$700.0 million as of the prior June 30, and (2) the date on which we have issued more than US$1.0 billion innon-convertible debt during the prior three-year period. As an emerging growth company, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies including, but not limited to, exemptions from the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, and any Public Company Accounting Oversight Board, or PCAOB, rules, including any future audit rule promulgated by the PCAOB (unless the SEC determines otherwise). Accordingly, the information about us available to you will not be the same as, and may be more limited than, the information available to shareholders of anon-emerging growth company.

Forward-Looking Statements

This annual report on Form20-F contains information that constitute forward-looking statements within the meaning of Section 27A of the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or Exchange Act, that are not based on historical facts and are not assurances of future results. The forward-looking statements contained in this annual report, which address our expected business and financial performance, among other matters, contain words such as “believe,” “expect,” “estimate,” “anticipate,” “intend,” “plan,” “aim,” “will,” “may,” “should,” “could,” “would,” “likely,” “potential” and similar expressions. We have made forward-looking statements that address, among other things our current expectations, plans, forecasts, projections and strategies about future events and financial trends that affect, or may affect, our business, industry, market share, reputation, financial condition, results of operations, margins, cash flow and/or the market price of our common shares, all of which are subject to known and unknown risks and uncertainties. Our actual results could differ materially from those expressed or forecast in any forward-looking statements as a result of a variety of assumptions and factors. These factors include, but are not limited to, the following:

| • | our ability to continuously record profits and positive operating cash flows; |

| • | the growth of eCommerce; |

| • | the inherent risks related to eCommerce, such as the interruption or failure of our computer or information technology systems; |

| • | reliance on one third-party data hosting service providers; |

| • | the efficient operation of our distribution centers; |

| • | our dependence on key suppliers and third-party couriers; |

| • | logistics and transportation challenges; |

| • | our ability to appropriately manage our working capital needs; |

2

Table of Contents

| • | the inherent risks of the lines of business into which we are expanding; |

| • | our ability to innovate and respond to technological advances and changing customer demands and shopping patterns; |

| • | current competition and the emergence of new market participants in our industry; |

| • | the maintenance of tax incentives; |

| • | our ability to attract and retain qualified personnel; |

| • | failure to enhance our brand recognition or maintain a positive public image; |

| • | failure to protect our intellectual property rights; |

| • | the occurrence of natural disasters that could have a material adverse effect on our business; |

| • | impacts of future legislation changes on our business; |

| • | the macroeconomic, political and business environment in the countries where we operate and their impact on our business, notably with respect to inflation, exchange rates, interest rates; |

| • | our ability to maintain our classification as an emerging growth company under the JOBS Act; and |

| • | the other factors discussed under section “Risk factors” in this annual report on Form20-F. |

Prospective investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and that actual results may differ materially from those in the forward-looking statements. The accompanying information contained in this annual report on Form20-F, including without limitation the information set forth under the heading “Item 5. Operating and Financial Review and Prospects,” identifies important factors that could cause such differences. In light of the risks, uncertainties and assumptions associated with forward-looking statements, you should not place undue reliance on any forward-looking statements. Additional risks that we may currently deem immaterial or that are not presently known to us could also cause the forward-looking events discussed in this annual report on Form20-F not to occur.

Our forward-looking statements speak only as of the date of this annual report on Form20-F or as of the date they are made, and except as otherwise required by applicable securities laws, we undertake no obligation to publicly update any forward-looking statement, whether because of new information, future events or otherwise.

Glossary of Certain Terms Used in this Annual Report

Unless the context otherwise requires, references in this annual report on Form20-F to:

| • | “active customers” mean customers who made purchases online with us during the preceding twelve months as of the relevant dates; |

| • | “average basket size” mean the sum of total order value from online purchases with us and in ourbrick-and-mortar store divided by the number of total orders for the relevant period; |

| • | “business-to-business operation” or “B2B operation” mean our offline sales of nutrition supplements and vitamins, among others, to other retailers such as drugstores, supermarkets and body shops in Brazil; |

| • | “eCommerce” mean product purchases using desktops, tablets or mobile devices; |

3

Table of Contents

| • | “GMV” mean the sum of net sales, returns, GMV from marketplace and net sales taxes, less marketplace and NCard activation commission fees; |

| • | “offline purchases with us” in the context of our product orders or sales, mean our product sales through our B2B operations; |

| • | “ourbrick-and-mortar store” mean our omni-channel store for fashion and beauty products located in the city of São Paulo, Brazil; |

| • | “our sites” mean www.netshoes.com.br, www.netshoes.com.mx, www.netshoes.com.ar, www.zattini.com.br, and www.shoestock.com.br; |

| • | “mCommerce” mean product purchases using only mobile sites and applications; |

| • | “purchases online with us,” “online purchases with us” and“business-to-consumer online operation, or B2C operation” in the context of our active customers, average basket size and GMV, mean product sales through our sites (including those sales effected through our marketplace) and the third-party sites that we manage; |

| • | “third-party sites that we manage” mean all partner-branded online stores that we manage. See “Item 4. Information on the Company—B. Business Overview—Our Additional Sources of Revenues—Partner-Branded Stores”; |

| • | “total orders” mean the total number of orders invoiced to active customers during the relevant period; and |

| • | “total order value” mean the total amount invoiced to a customer in connection with a product sale (including shipping fees and taxes). |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

4

Table of Contents

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

The following selected financial data, as of December 31, 2016 and 2017 and for the years ended December 31, 2015, 2016 and 2017 have been derived from our audited consolidated financial statements included elsewhere in this annual report on Form20-F. December 31, 2014 figures have been provided in the disclosure documents for our initial public offering. The following selected financial and other data is qualified by reference to and should be read in conjunction with our audited consolidated financial statements and the notes thereto contained in this annual report on Form20-F, as well as the information set forth under the heading “Item 5. Operating and Financial Review and Prospects.”

Consolidated Statements of Profits or Loss

| Years Ended December 31, | ||||||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | 2017 | ||||||||||||||||

| R$ | R$ | R$ | R$ | US$ | ||||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

Net sales | 1,125,795 | 1,505,686 | 1,739,540 | 1,889,006 | 571,042 | |||||||||||||||

Cost of sales | (753,440 | ) | (1,010,501 | ) | (1,188,744 | ) | (1,291,427 | ) | (390,395 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Gross profit | 372,355 | 495,185 | 550,796 | 597,579 | 180,647 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating expenses: | ||||||||||||||||||||

Selling and marketing expenses | (322,643 | ) | (398,514 | ) | (443,692 | ) | (509,208 | ) | (153,932 | ) | ||||||||||

General and administrative expenses | (147,375 | ) | (157,228 | ) | (174,564 | ) | (153,136 | ) | (46,293 | ) | ||||||||||

Other operating expense, net | (4,724 | ) | (3,503 | ) | (5,252 | ) | (3,933 | ) | (1,189 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total operating expenses | (474,742 | ) | (559,245 | ) | (623,508 | ) | (666,277 | ) | (201,414 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating loss | (102,387 | ) | (64,060 | ) | (72,712 | ) | (68,698 | ) | (20,767 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Financial income | 32,598 | 61,294 | 28,366 | 30,131 | 9,109 | |||||||||||||||

Financial expense | (74,447 | ) | (96,667 | ) | (107,550 | ) | (131,776 | ) | (39,836 | ) | ||||||||||

Loss before income tax | (144,236 | ) | (99,433 | ) | (151,896 | ) | (170,343 | ) | (51,494 | ) | ||||||||||

Income tax expense | (139 | ) | (80 | ) | — | (2 | ) | (1 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net loss | (144,375 | ) | (99,513 | ) | (151,896 | ) | (170,345 | ) | (51,495 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net loss attributable to: | ||||||||||||||||||||

Owners of Netshoes (Cayman) Limited | (143,966 | ) | (98,676 | ) | (151,074 | ) | (169,746 | ) | (51,314 | ) | ||||||||||

Non-controlling interests | (409 | ) | (837 | ) | (822 | ) | (599 | ) | (181 | ) | ||||||||||

Loss per common share attributable to owners of Netshoes (Cayman) Limited (Basic and Diluted)(1) | (7.54 | ) | (4.66 | ) | (7.05 | ) | (5.95 | ) | (1.80 | ) | ||||||||||

| (1) | Basic loss per common share is calculated based on the weighted average number of common shares for the relevant period. Diluted loss per common share reflects, for each period, the potential dilution of share options that could be exercised or converted into common shares, and is computed by dividing net loss attributable to the owners of Netshoes (Cayman) Limited by the weighted average number of common shares outstanding plus the potentially dilutive effect of all of our share options. Earnings per common share data for all periods have been calculated after giving effect to the share split that occurred on April 18, 2017 in connection with the completion of our initial public offering. When we report net loss attributable to the owners of Netshoes (Cayman) Limited, the diluted loss per common share is equal to the basic loss per common share due to the anti-dilutive effect of the outstanding share options. |

5

Table of Contents

Consolidated Statements of Financial Position

| As of December 31, | ||||||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | 2017 | ||||||||||||||||

| R$ | R$ | R$ | R$ | US$ | ||||||||||||||||

| (In thousands) | ||||||||||||||||||||

Selected Statements of Financial Position Data | ||||||||||||||||||||

Cash and cash equivalents | 242,372 | 249,064 | 111,304 | 395,962 | 119,698 | |||||||||||||||

Total current assets(1) | 743,408 | 938,358 | 824,711 | 1,113,558 | 336,625 | |||||||||||||||

Total assets | 861,956 | 1,113,568 | 1,113,722 | 1,497,125 | 452,577 | |||||||||||||||

Total current liabilities | 378,416 | 523,271 | 616,695 | 796,330 | 240,728 | |||||||||||||||

Total long-term debt(2) | 335,410 | 333,993 | 387,382 | 285,971 | 86,448 | |||||||||||||||

Share-based payment liability | 30,113 | 35,978 | 30,139 | — | — | |||||||||||||||

Total liabilities | 616,949 | 824,566 | 989,697 | 1,013,776 | 306,461 | |||||||||||||||

Total shareholders’equity | 245,007 | 289,002 | 124,025 | 483,349 | 146,116 | |||||||||||||||

| (1) | Inclusive of cash and cash equivalents. |

| (2) | Includes current portion of long-term debt. See note 17 to our audited consolidated financial statements included elsewhere in this annual report. |

Selected Operating Data

| Years Ended December 31, | ||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | |||||||||||||

Active customers (in thousands)(1) | 3,753 | 4,676 | 5,562 | 6,669 | ||||||||||||

Total orders (in thousands)(2) | 6,846 | 8,497 | 10,268 | 12,325 | ||||||||||||

% of total orders placed from mobile devices(3) | 11.6 | % | 20.2 | % | 32.2 | % | 46.1 | % | ||||||||

Average basket size(4) | R$ | 210.8 | R$ | 219.1 | R$ | 206.6 | R$ | 203.1 | ||||||||

| (1) | Customers who made purchases online with us during the preceding twelve months as of the relevant dates. |

| (2) | Total number of orders invoiced to active customers during the relevant period. |

| (3) | The sum of total orders placed by active customers through our mobile site and applications as a percentage of total orders placed by active customers for the relevant period. This operational metric is especially relevant as sales made on mobile devices have become an important part of our business. |

| (4) | The sum of total order value from online purchases with us divided by the number of total orders for the relevant period. |

Non-IFRS Financial Measures

We usenon-IFRS financial measures for financial and operational decision-making purposes. To provide investors and others with additional information regarding our financial results and operating performance, we have disclosed in the tables below and within this annual report our EBITDA, EBITDA Margin, EBITDA Brazil, EBITDA International and GMV which arenon-IFRS financial measures.

EBITDA and EBITDA Margin

We define: (1) “EBITDA” as net income (loss) plus interest income/expense, net (which includes interest income, imputed interest on installment sales, interest expenses related to debt, imputed interest on credit purchases and debt issuance costs), income tax, and depreciation and amortization expenses; and (2) “EBITDA Margin” as EBITDA divided by net sales for the relevant period, expressed as a percentage. EBITDA and EBITDA Margin are not measures of financial performance in accordance with IFRS and should not be considered as a substitute for other measures of financial performance reported in accordance with IFRS. These measurements assist our management and may be useful to investors in comparing our operating performance consistently over time as they eliminate the impact of our capital structure (primarily interest charges), asset base (primarily depreciation and amortization) and items outside the control of our management (primarily taxes). These measurements have limitations as analytical tools, including:

| • | EBITDA does not reflect changes in, or cash requirements for, our working capital needs or contractual commitments; |

| • | EBITDA does not reflect our tax expense or the cash requirements to pay our taxes; |

| • | Although depreciation and amortization arenon-cash charges, the assets being depreciated or amortized will often need to be replaced in the future, and EBITDA does not reflect any cash requirements for these replacements; and |

| • | Other companies may calculate EBITDA differently than we do, and therefore this presentation of EBITDA may not be comparable to other similarly titled measures used by other companies. |

6

Table of Contents

Because of these limitations, you should consider EBITDA and EBITDA Margin alongside other financial performance measures, like net income (loss) and our other IFRS results. The following table reflects the reconciliation of our net loss to EBITDA and EBITDA Margin for each of the periods indicated:

| Years Ended December 31, | ||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | |||||||||||||

| (In thousands) | ||||||||||||||||

Net loss | R$ | (144,375 | ) | R$ | (99,513 | ) | R$ | (151,896 | ) | R$ | (170,345 | ) | ||||

Add (subtract): | ||||||||||||||||

Interest income/expense, net (1) | 27,755 | 32,484 | 76,823 | 95,234 | ||||||||||||

Income tax expense | 139 | 80 | — | 2 | ||||||||||||

Depreciation and amortization | 16,523 | 20,415 | 31,202 | 31,820 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

EBITDA | R$ | (99,958 | ) | R$ | (46,534 | ) | R$ | (43,871 | ) | R$ | (43,289 | ) | ||||

|

|

|

|

|

|

|

| |||||||||

Net Sales | R$ | 1,125,795 | R$ | 1,505,686 | R$ | 1,739,540 | R$ | 1,889,006 | ||||||||

|

|

|

|

|

|

|

| |||||||||

EBITDA Margin | (8.9 | )% | (3.1 | )% | (2.5 | )% | (2.3 | )% | ||||||||

| (1) | Includes interest income, imputed interest on installment sales, interest expenses related to debt, imputed interest on credit purchases and debt issuance costs. |

EBITDA Brazil and EBITDA International

We define: (1) “EBITDA Brazil” as net income (loss) of our Brazil business segment plus interest income / expense, net (which includes interest income, imputed interest on installment sales, interest expenses related to debt, imputed interest on credit purchases and debt issuance costs), income tax, and depreciation and amortization expenses, in each case, related to this business segment and (2) “EBITDA International” as net income (loss) of our International business segment plus interest income / expense, net (which includes interest income, imputed interest on installment sales, interest expenses related to debt, imputed interest on credit purchases and debt issuance costs), income tax, and depreciation and amortization expenses, in each case, related to this business segment. EBITDA Brazil and EBITDA International are not measures of financial performance in accordance with IFRS and should not be considered as a substitute for other measures of financial performance reported in accordance with IFRS. These measurements may be useful to investors in comparing the operating performance of our business segments consistently over time as they eliminate the impact of our capital structure (primarily interest charges), asset base (primarily depreciation and amortization) and items outside the control of our management (primarily taxes). These measurements have similar limitations as analytical tools as those applicable for EBITDA.

Because of these limitations, you should consider EBITDA Brazil and EBITDA International alongside other financial performance measures of our business segments, like net loss and our other IFRS results. For further information on our reportable segment results, see note 3 to our audited consolidated financial statements included elsewhere in this annual report. The following tables reflect the reconciliation of the net loss of each of our business segments to their respective EBITDA for each of the periods indicated:

EBITDA Brazil

| Years Ended December 31, | ||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | |||||||||||||

| (In thousands) | ||||||||||||||||

Net loss (Brazil) | R$ | (95,521 | ) | R$ | (30,493 | ) | R$ | (88,237 | ) | R$ | (102,420 | ) | ||||

Add (subtract): | ||||||||||||||||

Interest income / expense, net(1) | 25,086 | 22,592 | 65,855 | 83,976 | ||||||||||||

Income tax expense | — | — | — | — | ||||||||||||

Depreciation and amortization | 15,405 | 18,470 | 27,777 | 27,503 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

EBITDA Brazil(2) | R$ | (55,030 | ) | R$ | 10,569 | R$ | 5,395 | R$ | 9,060 | |||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | Includes interest income, imputed interest on installment sales, interest expenses related to debt, imputed interest on credit purchases and debt issuance costs related to our Brazil business segment. |

| (2) | Items not allocated directly to our reportable business segments (operating expenses, financial income and financial expenses recorded in Netshoes (Cayman) Limited and Netshoes Holding, LLC) are recorded and disclosed separately as corporate and others. As a result, the sum of EBITDA Brazil and EBITDA International does not sum up to EBITDA. |

7

Table of Contents

EBITDA International

| Years Ended December 31, | ||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | |||||||||||||

| (In thousands) | ||||||||||||||||

Net loss (International) | R$ | (40,062 | ) | R$ | (56,781 | ) | R$ | (53,329 | ) | R$ | (51,833 | ) | ||||

Add (subtract): | ||||||||||||||||

Interest income / expense, net (1) | 2,669 | 9,892 | 11,049 | 9,265 | ||||||||||||

Income tax expense | 139 | 80 | — | 2 | ||||||||||||

Depreciation and amortization | 1,118 | 1,520 | 1,262 | 967 | ||||||||||||

EBITDA International(2) | R$ | (36,1.36 | ) | R$ | (45,289 | ) | R$ | (41,018 | ) | R$ | (41,597 | ) | ||||

|

|

|

|

|

|

|

| |||||||||

| (1) | Includes interest income, imputed interest on installment sales, interest expenses related to debt, imputed interest on credit purchases and debt issuance costs related to our International business segment. |

| (2) | Items not allocated directly to our reportable business segments (operating expenses, financial income and financial expenses recorded in Netshoes (Cayman) Limited and Netshoes Holding, LLC) are recorded and disclosed separately as corporate and others. As a result, the sum of EBITDA Brazil and EBITDA International does not sum up to EBITDA. |

GMV

We define “GMV” as the sum of net sales, returns, GMV from marketplace and net sales taxes, less marketplace and NCard activation commission fees. GMV is a metric useful to investors as it provides an indication of the total volume of product sales (in terms of gross merchandise value) transacted in online and offline purchases with us as well as the growth trend of our marketplace, which has become an increasingly important part of our business. GMV is not a measure of financial performance in accordance with IFRS and should not be considered as a substitute for other measures of financial performance reported in accordance with IFRS. Because of these limitations, you should consider GMV alongside other financial performance measures, like net sales and our other IFRS results. The following table reflects the reconciliation of our net sales to GMV for each of the periods indicated:

| Years Ended December 31, | ||||||||||||||||

| 2014 | 2015 | 2016 | 2017 | |||||||||||||

| (In thousands) | ||||||||||||||||

Net sales(1) | R$ | 1,125,795 | R$ | 1,505,686 | R$ | 1,739,540 | R$ | 1,889,006 | ||||||||

Add (subtract): | ||||||||||||||||

Net sales taxes(2) | 243,875 | 262,227 | 291,646 | 336,357 | ||||||||||||

Returns(3) | 73,536 | 99,102 | 142,464 | 199,379 | ||||||||||||

Marketplace commission fees(4) | — | — | (9,086 | ) | (38,873 | ) | ||||||||||

NCard activation commission fees(5) | — | — | (354 | ) | (1,974 | ) | ||||||||||

Sub-Total: | R$ | 1,443,207 | R$ | 1,867,015 | R$ | 2,164,210 | R$ | 2,383,895 | ||||||||

|

|

|

|

|

|

|

| |||||||||

GMV from marketplace(6) | — | — | 38,288 | 199,626 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

GMV | R$ | 1,443,207 | R$ | 1,867,015 | R$ | 2,202,498 | R$ | 2,583,521 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | Net sales includes revenue from product sales and other revenues, net of promotional discounts, returns and net sales taxes. See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Components of our Results of Operations.” |

| (2) | Value added taxes added in our product sales, net of value added taxes incentives granted to us and recorded in our net sales. For further discussion regarding the tax incentives applicable to us, see notes 5 and 7 to our audited consolidated financial statements included elsewhere in this annual report. |

| (3) | Represents revenue from product sales that are returned by our customers. |

| (4) | Represents the commission revenue arising from product sales of qualified third-partybusiness-to-consumer, or B2C, vendors through our marketplace, launched in February 2016, that we record as net sales on a net basis. For further information, see “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Components of our Results of Operations.” |

| (5) | Represents the commission revenue generated by customers’ activation of NCards, an initiative launched in April 2016. For further information, see “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Components of our Results of Operations.” |

| (6) | Means the gross merchandise value of product sales through our online marketplace, launched in February 2016. |

Exchange Rates

The Brazilian foreign exchange system allows the purchase and sale of foreign currency and the international transfer of reaisby any person or legal entity, regardless of the amount, subject to certain regulatory procedures.

8

Table of Contents

In the past, the Central Bank has intervened occasionally to control unstable movements in foreign exchange rates. We cannot predict whether the Central Bank or the Brazilian government will continue to permit the realto float freely or will intervene in the exchange rate market through the return of a currency band system or otherwise. The realmay depreciate or appreciate against the U.S. dollar and other currencies substantially. Furthermore, Brazilian law provides that, whenever there is a serious imbalance in Brazil’s balance of payments or there are serious reasons to foresee a serious imbalance, temporary restrictions may be imposed on remittances of foreign capital abroad. We cannot assure you that such measures will not be taken by the Brazilian government in the future. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in Brazil and the Rest of Latin America— Exchange rate instability may adversely increase our costs and affect our financial condition and results of operations.”

The following table shows the selling rate for U.S. dollars for the periods and dates indicated. The information in the “Average” column represents the average of the daily exchange rates during the periods presented. The numbers in the “Period End” column are the quotes for the exchange rate as of the last business day of the period in question.

| Reais per U.S. Dollar | ||||||||||||||||

Year | High | Low | Average | Period End | ||||||||||||

2013 | 2.4457 | 1.9528 | 2.1605 | 2.3426 | ||||||||||||

2014 | 2.7403 | 2.1974 | 2.3547 | 2.6562 | ||||||||||||

2015 | 4.1949 | 2.5754 | 3.3387 | 3.9048 | ||||||||||||

2016 | 4.1558 | 3.1193 | 3.4833 | 3.2591 | ||||||||||||

2017 | 3.3807 | 3.0510 | 3.1925 | 3.3080 | ||||||||||||

| Reais per U.S. Dollar | ||||||||

Month | High | Low | ||||||

September 2017 | 3.1932 | 3.0852 | ||||||

October 2017 | 3.2801 | 3.1315 | ||||||

November 2017 | 3.2920 | 3.2136 | ||||||

December 2017 | 3.3332 | 3.2322 | ||||||

January 2018 | 3.2697 | 3.1391 | ||||||

February 2018 | 3.2821 | 3.1730 | ||||||

March 2018 (through March 27, 2018) | 3.3256 | 3.2246 | ||||||

Source: Central Bank.

The exchange rate on December 31, 2017 was R$3.3080 per US$1.00 and on March 27, 2018 was 3.3256 per US$1.00.

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Risks Related to Our Business and Industry

The eCommerce market in Brazil and in other countries where we operate is developing, and the expansion of our business depends on the continued growth of eCommerce, as well as increased availability, quality and usage of the Internet in Brazil and in other countries where we operate.

Our future sales depend substantially on consumers’ widespread acceptance and use of the Internet as a way to conduct commerce. Rapid growth in the use of the Internet (particularly as a way to provide and purchase products and services) is a relatively recent phenomenon in Brazil, Argentina and Mexico and we cannot assure you that this acceptance and use will continue or increase. In order to grow our customer base successfully, consumers who have historically used physical channels of commerce to purchase lifestyle, sporting, fashion and beauty goods must accept and use new ways of conducting business and exchanging information. Furthermore, if the penetration of Internet access in Brazil, Argentina and Mexico does not increase quickly, that may limit our potential growth, particularly in regions with low levels of Internet quality and access and/or low levels of income.

9

Table of Contents

The Internet penetration in Brazil, Argentina and Mexico may never reach a percentage similar to more developed countries for reasons that are beyond our control, including the lack of necessary network infrastructure or delayed development of enabling technologies, performance improvements and security measures. The infrastructure for the Internet in Brazil, Argentina and Mexico may not be able to support continued growth in the number of users, their frequency of use or their bandwidth requirements. In addition, Internet reliability may not improve in the region due to delays in telecommunications, infrastructure development or other technology shortfalls, or due to increased government regulation. If telecommunications services are not sufficiently available to support the growth of the Internet in the region, response times could be slower, which would adversely affect the use of the Internet and our services in particular.

Furthermore, the price of Internet access and Internet-connected devices, such as personal computers, tablets, mobile phones and other portable devices, may limit our potential growth in parts of Brazil, Argentina and Mexico with low levels of income. Given the comparatively low level of income in the region, the penetration rate for Internet-connected devices is significantly lower in Brazil and in other countries in the region than it is in the United States and many other more developed countries, and the cost of Internet access is still relatively high as compared with other more developed countries. In addition, there may be increases in Internet access fees or telecommunication fees in the region. If that happens, our potential number of customers may decrease, which in turn may adversely affect our sales.

If the Internet or the markets for our Internet-based services in the region fail to grow as anticipated, such lack of growth may have a material adverse impact on our business prospects, results of operations and financial condition.

We operate in a rapidly evolving market. Accordingly, we may be unable to accurately forecast net sales or earnings and appropriately plan our future expenditures.

Considering the emerging nature of the markets in which we compete, the rapidly evolving nature of our business, the relative newness of eCommerce in Latin America, our business diversification and continuous innovation and the general economic and business conditions in Latin America, it is particularly difficult for us to forecast our net sales or earnings accurately. Our current and future expenditure levels are based largely on our investment plans and are, to a large extent, fixed. We may not be able to adjust spending in a timely manner to compensate for any unexpected net sales shortfalls arising from the rapidly evolving nature of our business or other conditions that affect our business. Accordingly, any significant shortfall in net sales relative to our planned expenditures would have an immediate adverse effect on our business, results of operations and financial condition.

Since our inception, we have never recorded profits in a fiscal year.

Since our inception, we have not recorded profits on a consolidated basis. Although we have been improving our results of operations year over year, we may not be able to record profits on a consolidated basis in the near future or at all. If our operating activities are not profitable and provide us with sufficient cash flows to meet our operational and investment needs, we may be required to seek additional sources of capital, which could include equity, equity-linked and debt financing. Equity financing would have a dilutive effect on our common shares, and new investors in any subsequent transactions could gain rights, preferences and privileges senior to those of our common shareholders. Debt financing, if available, may involve restrictive covenants and could reduce our operational flexibility and profitability. We cannot assure you that any additional financing will be available to us on acceptable terms, if at all. If adequate funds are not available or are not available on acceptable terms, we may not be able to fund our expansion, take advantage of acquisition opportunities, develop or enhance services or products or respond to competitive pressures. These inabilities may have a material adverse effect on our business, results of operations and financial condition.

We depend on search engines,e-mail, and other messaging services to attract a substantial portion of the customers who visit our sites, and changes in search engine logic, or any restrictions on the sending of emails or messages or an inability to timely deliver such communications could adversely affect our business and results of operations.

Our site traffic is generated by different advertising channels. A portion is generated by customers clicking on search results displayed by search engines, such as Google, Yahoo or Bing. These search engines typically provide two types of results: algorithmic and purchased listings. Algorithmic listings cannot be purchased and instead are determined and displayed solely by a set of formulas designed by the search engine provider. Purchased listings can be purchased by companies and other entities in order to attract users to their sites. We rely on both algorithmic and purchased listings to attract a substantial portion of the customers that we serve. The cost of purchased search listing advertising may increase as demand for such advertising channels grows, and further increases may have a negative impact on our ability to maintain or increase profitability. Further, search engines revise their algorithms from time to time in an attempt to optimize their search result listings and to maximize the advertising revenue generated by those listings. Search engines may also place websites on a “blacklist” or remove them from their indexes. We cannot guarantee that a removal by Google, Yahoo, Bing or another search engine will not happen to us in the future or that we will be able to adapt to changes in their algorithms in a timely manner.

10

Table of Contents

If the search engines on which we rely for site traffic remove us from their indices or otherwise modify their algorithms such that we have less favorable placement or do not appear among search results, our business will be adversely affected. Such circumstances may result in fewer customers clicking through to our sites, requiring us to resort to other more costly resources to attempt to replace that traffic, and this may reduce our net sales and harm our business. We may also be unable to purchase listings on alternative search engines and if we are able to purchase listings from such alternative search engines, those companies may charge higher prices for advertising or have fewer users.

Also, our business partially relies on email and other messaging services for promoting our sites and product offerings. We provide promotional emails to consumers in our database and we rely on a third-party service for the delivery of all our emails. Delays or errors in the delivery of such emails or other messaging we send may occur and are beyond our control. From time to time, Internet service providers or other third parties may block bulk email transmissions or otherwise experience technical difficulties that result in our inability to successfully deliver emails or other messages to our customers. Changes in the laws or regulations that limit our ability to send such communications or impose additional requirements upon us in connection with sending such communications could also materially and adversely impact our business. In addition, changes in how webmail applications organize and prioritize email may reduce the number of our emails being opened, including if our email messages are delivered to “spam” or similar folders. Actions by third parties to block, impose restrictions on or charge for the delivery of emails or other messages or delays in the distribution of such messages could materially and adversely impact our business. We also use social media services and other retargeting channels to send communications and product offerings to our customers. Changes in the terms of use of social media services and other retargeting channels that would limit our ability to send promotional communications or our customers’ ability to receive communications, disruptions or downtime experienced by these services or a decline in the use of or engagement with social media by customers and potential customers could harm our business.

Our success depends in part on our ability to increase our net sales per active customer. If our efforts to increase customer loyalty and repeat purchasing and to maintain high levels of customer engagement and the average basket size of our customers are not successful, our growth prospects and net sales will be materially adversely affected.

Our ability to grow our business depends on our ability to retain our existing customer base, generate increased sales and repeat purchases from this customer base, and maintain high levels of customer engagement. To do this, we must continue to provide our customers and potential customers with an intuitive, convenient, efficient and differentiated shopping experience and to continue to offer products that our customers find compelling. If we fail to increase net sales per active customer, generate repeat purchases or maintain high levels of customer engagement and average basket size, our growth prospects, operating results and financial condition could be materially adversely affected.

Failure to maintain sufficient working capital could limit our growth and harm our business, financial condition and results of operations.

We have significant working capital requirements primarily driven by payment terms agreed with our suppliers and extended payment terms that we offer our customers. For the year ended December 31, 2017, 71.3% of our product sales were paid in installments by our customers. Differences between the date when we pay our suppliers and the date when we receive payments from customers may negatively affect our liquidity and our cash flows. In addition, we expect our working capital needs to increase as our total number of products sold increases. In order to finance our working capital needs, we enter into financing arrangements to decrease the amount of time it takes for us to collect our trade accounts receivable, or factoring, and to increase the amount of time we have to pay our trade accounts payable, or reverse factoring. We believe factoring allows us to gain access to capital faster than we would otherwise without those financing arrangements. For the year ended December 31, 2017, our volume of factoring of trade accounts receivable with financial institutions reached R$1,113.8 million (compared to R$789.2 million for the year ended December 31, 2016). There can be no assurance that these types of financing arrangements will continue to be available to us on acceptable terms, or at all. If we do not have sufficient working capital, we may not be able to pursue our growth strategy, respond to competitive pressures or fund key strategic initiatives, such as the development of our sites, which may adversely affect our business, financial condition and results of operations.

11

Table of Contents

If we are unable to predict or effectively react to changes in consumer demand or shopping patterns, we may face significant inventory risk or lose customers and our sales may decline.

Our success depends in part on our ability to anticipate and respond in a timely manner to changing consumer demands and preferences and shopping patterns and seasonality regarding sporting, lifestyle, fashion and beauty goods. The products we sell must appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to change. Sudden changes in consumer spending patterns, consumer demands and preferences are especially likely in fashion and beauty, markets in which we recently began operating and have limited experience. Also, consumer preferences could shift rapidly and our future success depends in part on our ability to select and offer products in a way that anticipates and responds to those changes. If we misjudge the market for our merchandise and do not forecast consumer demand accurately, our sales may decline significantly.

We may experience excess inventory levels (for example, if we overstock unpopular products) and be forced to take significant inventory markdowns, which could have a negative impact on our profitability. Conversely, shortages of products that prove popular could negatively impact our net sales. In addition, a major shift in consumer demand away from sporting, fashion or beauty goods could have a material adverse effect on our business, results of operations and financial condition. We often agree to purchase products from our suppliers several months in advance of the proposed delivery; however, product demand can change significantly between the time we commit to buy a product and its expected date of sale. Also, we carry a broad selection of products—some at significant inventory levels—and we may be unable to sell products in sufficient quantities or during the selling seasons. Any one of these inventory risks may adversely affect our operating results.

For instance, in the second half 2017, after remodeling our B2B operation, as of December 31, 2017, we had R$117.7 million of nutritional supplement products stored in our inventories. Although these products have great demand in our B2C operation, there can be no assurance that we will be able to sell them in sufficient quantities prior to their expiration date. For further information regarding the remodeling of our B2B operation, (see Item 4. Information on the Company—B. Business Overview— Our Additional Sources of Revenues”).

A number of factors, many of which are outside our control, may affect consumer demand, shopping patterns or the predictability of our inventory levels, including: general economic conditions; lockouts or strikes involving professional sports teams; the retirement of sports or other celebrities used in marketing for the various products we sell; sports scandals or scandals involving celebrities we use in campaigns to advertise our sites; litigation; and pricing and other actions taken by our competitors.

Failure to anticipate and respond to changing consumer preferences and shopping patterns in a timely manner could lead to, among other things, lower sales and excess inventory levels.

Our business is subject to substantial fluctuation as a result of the seasonal buying patterns of our customers.

We experience seasonal fluctuations in our net sales and operating results, both of which may vary fromquarter-to-quarter in the future. We have historically generated significantly higher net sales in the fourth quarter, which includes the Black November period and the holiday selling season. Accordingly, a reduction in consumer confidence during the holiday season would have a significant impact on our business. Further, in the fourth quarter we generally have increased expenses for personnel and advertising, due to anticipated higher purchase volumes. Seasonality also influences our buying patterns since we purchase merchandise for seasonal activities in advance of a season, which directly impacts our inventory and accounts payable levels and cash flows. If we miscalculate the demand for the amount of products we will sell or for the product mix during the fourth quarter, our net sales can decline, which can harm our financial performance. If fourth quarter net sales are not high enough to allow us to fully recoup our personnel and advertising expenses or are lower than the targets used to determine our inventory levels, this shortfall can negatively impact our results of operations. See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Seasonality and Quarterly Results of Operations.”

Our quarterly results of operations may also fluctuate significantly as a result of a variety of other factors, including, among other things, the timing of the introduction of and advertising for new products and changes in our product mix. As a result of these seasonal and quarterly fluctuations, we believe that comparisons of our operating results between different quarters within a single year are not necessarily meaningful and that these comparisons cannot be relied upon as indicators of our future performance. Any seasonal or quarterly fluctuations that we report in the future may not match the expectations of market analysts and investors. This could cause the price of our common shares to fluctuate significantly.

12

Table of Contents

We derive our net sales from product categories that represent discretionary spending, and changes in global macroeconomic conditions may decrease the demand for the products we sell and adversely affect our growth strategies and business prospects.

Our operating results are affected by the relative condition of the economy. Our business and financial performance may be adversely affected by current and future economic conditions that cause a decline in business and consumer spending, including a reduction in the availability of credit, increased unemployment levels, higher energy and fuel costs, rising interest rates, financial market volatility and recession. Additionally, we may experience difficulties in operating and growing our operations as a result of economic pressures.

As a business that depends on consumer discretionary spending, we may be adversely affected if our customers reduce their purchases due to continued job losses, foreclosures, bankruptcies, higher consumer debt and interest rates, reduced access to credit, lower consumer confidence, uncertainty or changes in tax policies and tax rates. Decreases in customer traffic or average value per transaction negatively affect our financial performance, and a prolonged period of depressed consumer spending could have a material adverse effect on our business. Promotional activities and decreased demand for consumer products, particularlyhigher-end products, could affect profitability and margins. The timing and duration of the different economic cycles in Brazil are difficult to forecast and mitigate. As a consequence, our sales, operating and financial results for a particular period are difficult to predict, and, therefore, it is difficult to forecast future results. Any of the foregoing could have a material adverse effect on our business, results of operations and financial condition and could adversely affect our share price.

A continued or future slowdown in Brazil, Argentina, Mexico or the global economy or a negative economic outlook could materially adversely affect consumer spending habits and potentially our future operating results.

If we are unable to appropriately address new market risks or the inherent risks in the lines of business into which we are expanding, our growth potential, reputation and results of operations could be materially and adversely affected.

We are engaged in an effort to expand our operations into other products and services in order to monetize our user traffic and distribution capabilities. Our ability to monetize our user traffic is critical to our envisioned plans for growth. As we expand into new business segments, such as fashion and beauty, we will face new risks associated with lines of business in which we have limited or no experience and in which we may be less well-known. We may be unable to attract a sufficient number of customers, fail to anticipate competitive conditions or face difficulties in operating effectively in these new segments. In addition, profitability, if any, in our newer activities may be lower than in our more mature lines of business, and we may not be successful enough to recover our investments in them.

Most of our new lines of business are subject to risks similar to those that our sporting goods business is subject, such as changes in consumer demands or shopping patterns, risks related to our suppliers and private label brands, seasonality and distribution risks. However, some of them are subject to their own set of inherent risks. For instance, we launched an online marketplace in February 2016, and maintaining a trusted status for its operations will be critical to its success. Any damage to our reputation related to, or loss of trust in, our online marketplace operations could have a negative impact on our business and result in consumers, merchants and other participants choosing not to carry out transactions or reducing their activity level on our online marketplace, which could limit our potential for growth. The success of our online marketplace will depend on, among other things, our ability to (1) attract both consumers and merchants to our online marketplace, (2) offer a secure and reliable transactional environment (including payment services) for both consumers and merchants, (3) create an effective set of rules governing our online marketplace, that is perceived as fair, (4) restrict access to our online marketplace for merchants who are not reliable or do not offer high-quality products and (5) ensure that third-party couriers used by merchants will be able to provide reliable logistics services in order to deliver products to customers within the agreed-upon timeframe.

The online retail industry is intensely competitive, and we may not compete successfully against new and existing competitors, which may materially and adversely affect our results of operations.

The retail market for the products we sell is intensely competitive. Consumers have many choices online and offline, including global, regional and local retailers. Our current and potential competitors includebrick-and-mortar retailers specializing in sporting goods, fashion and beauty, generalbrick-and-mortar retailers and pure-play eCommerce players, such as other B2C eCommerce retailers. In the future, we may also face competition from new entrants, the consolidation of existing competitors or companies spun off from our larger competitors.

13

Table of Contents

We face a variety of competitive challenges, including: sourcing products efficiently, pricing the products we sell competitively, maintaining optimal inventory levels, selling products effectively, maintaining the quality of the products we sell, building our customer base, conducting effective marketing activities, anticipating and responding quickly to changing consumer demands and preferences (which is especially true for the fashion and beauty segments), attracting visitors to our sites and maintaining favorable brand recognition. In addition, as we further develop our business, we will face increasing challenges to compete for and retain high quality suppliers. If we cannot properly address these challenges, our business and prospects would be materially and adversely affected. Other online retailers may be acquired by, receive investments from or enter into strategic relationships with well-established and well-funded companies or investors, which would help enhance their competitive positions. Certain of our competitors may be able to secure more favorable terms with suppliers, devote greater resources to marketing campaigns, adopt more aggressive pricing or inventory policies and devote substantially more resources to infrastructure and logistics development. Increased competition may reduce our sales performance, product margins, market share and brand recognition.

We cannot assure you that we will be able to compete successfully against current and future competitors, and competitive pressures may materially and adversely affect our business, financial condition and results of operations.

Interruption or failure of our information technology and communications systems could impair our operations, which could damage our reputation and harm our results of operations. Specifically, we rely on certain third-party providers to provide us with Internet data centers to host our sites and back-office end systems and keep them fully operational. Disruptions with this provider or in the services it provides to us could materially affect our reputation, operations or financial results.

Our success and ability to sell products online and provide high quality customer service depend on the efficient and uninterrupted operation of our computer and information technology systems. Any failure of our computer systems and information technology to operate effectively or to integrate with other systems, performance inadequacy or breach in security may cause interruptions in the availability of our sites, delays in product fulfillment and reduced efficiency of our operations. We experience service disruptions from time to time and on occasion, our site has not properly displayed promotions as marketed. Any failures, problems or security breaches may adversely affect the number of customers willing to purchase the products we offer in the future. Factors that could occur and significantly disrupt our operations include: system failures and outages caused by fire, floods, earthquakes, power loss, telecommunications failures, sabotage, vandalism, terrorist attacks and similar events; software errors; computer viruses, worms, physical or electronicbreak-ins and similar disruptions from unauthorized tampering with our computer systems and data centers; and security breaches related to the storage and transmission of proprietary information or customer information, such as credit card numbers or other personal information. Also, if too many customers access our sites within a short period of time due to increased holiday demand or any other reason, like one we had in the past we may in the future experience system interruptions that make our sites unavailable or prevent us from efficiently fulfilling orders, which may reduce the volume of goods we sell and the attractiveness of our products and services. We cannot assure you that such events will not occur and while we have backup systems and contingency plans for certain aspects of our operations and business processes, our planning does not account for all possible scenarios.

Specifically, we rely on certain technologies that we license from third parties, such as Processor, to host our eCommerce sites in cloud and keep them operational, and on Uol Diveo, to provide us with two data centers to host our back-office end systems. Failure by Processor or Uol Diveo to adequately keep our sites fully operational, including any prolonged or unscheduled service disruption that affects our customers’ ability to utilize our sites and effect purchases therein, could result in the loss of sales and customers and/or increased costs, which could materially affect our reputation, operations or financial results. In addition, we rely in part on Uol Diveo and Processor to advise us of any security breaches, and if they do not provide notice on a timely basis, our reputation and results of operations may be adversely affected. We may have limited access to alternative services and may not be able to timely replace Processor or Uol Diveo, or find a replacement on a cost-efficient basis, in the event of termination of these agreements, disruptions, failures to provide services or other issues with them that may adversely affect our business. See “Item 10. Additional Information—C. Material Contracts.”

Any disruptions or service interruptions that affect our sites could damage our reputation, require us to spend significant capital and other resources and expose us to a risk of loss or litigation and possible liability. We do not carry any business interruption insurance to compensate for losses that may occur as a result of any of these events and our agreements with third-party service providers do not require those providers to indemnify us for any losses resulting from any disruption in service. Accordingly, our results of operations may be adversely affected if any of the above disruptions should occur.

14

Table of Contents

Our business may be harmed if we are unable to secure licenses for third-party technologies on which we rely.

We rely on licenses to utilize certain technology provided by third parties, such as our key database technology, our eCommerce platform, operating systems for our servers and other computers and components for our servers. These third-party technology licenses may cease to be available to us on commercially reasonable terms, or at all. If we are unable to obtain licenses for, or otherwise make use of this technology, we would need to obtain substitute technology, which may not be available. If substitute technology is available, it may be of lower quality or have lower performance standards or may only be available at a greater cost, any of which could materially adversely affect our business, results of operations and financial condition.

Also, because we often depend upon the successful operation of third-party products in conjunction with our software, any errors in these third-party products, which may be outside our control, may prevent the implementation or impair the functionality of our software and Internet-based services, delay the introduction of new services and harm our reputation.

If we are not able to continue to innovate and adapt to changes in technology or in our industry, our business, financial condition and results of operations would be materially and adversely affected.

The Internet is characterized by rapidly changing technology, evolving industry standards, new mobile apps, protocols and technologies, new service and product introductions, triggering further changes in customer demands and shopping patterns. Our failure to innovate and adapt to these changes would have a material adverse effect on our business, financial condition and results of operations. For example, total orders placed from mobile devices are growing at a fast pace. In the year ended December 31, 2017, orders placed by our customers from mobile devices represented approximately 46.1% of our total orders (compared to 32.2% in the year ended December 31, 2016 and 20.2% in the year ended December 31, 2015). The variety of technical and other configurations across different mobile devices and platforms increases the challenges associated with this environment. If we are unable to continue to (1) attract new mobile consumers and increase or maintain levels of mobile engagement or (2) to rapidly adapt to future changes in technology, our ability to maintain or grow our business would be materially and adversely affected.

We rely on a small number of third-party couriers to deliver the products we sell to our customers, and their failure to provide high quality delivery services or our failure to effectively manage our relationships with them may materially and adversely affect our business, financial condition and results of operations.

We currently rely on a small number of third-party courier companies to deliver products to our consumers, and any failure by our key third-party service couriers to perform or any adverse change to their financial conditions could have a material adverse effect on our reputation and results of operations. In particular, we rely significantly on the Brazilian official post office (Correios), Total Express and Transfolha, which together delivered 62.9% of the purchase orders shipped to our customers for the year ended December 31, 2017. Our third-party couriers may offer us less favorable terms in the future, which may increase our shipping costs and materially and adversely affect our financial condition and results of operation. For instance,Correios has recently announced a general increase in the prices it charges for the shipment of products, and this increase in cost may be particularly damaging to the qualified third-party B2C vendors selling products through our marketplace (and consequently to the successful development of our marketplace) if they are not capable of either absorbing this increased cost or passing on this additional cost to customers without affecting overall sales volumes. Further, most of our agreements with third-party couriers can be terminated upon delivery of thirty days’ prior written notice by any of the parties. If any of these agreements are terminated, there can be no assurance that we will be able to successfully substitute another service provider to provide delivery services on the same terms, in a timely manner or at all.

Additionally, interruptions to or failures in these third parties’ shipping services could prevent the timely or successful delivery of our products and adversely affect our operations. These interruptions may be due to unforeseen events such as inclement weather, natural disasters, pressure from unions, labor unrest or a strike, which are all beyond our control or the control of these third-party couriers. For example, our distribution network is sensitive to fluctuation in oil prices, which may result in increased shipping costs for third-party courier companies (as well as our suppliers’ transportation costs), which may, in turn, increase the prices of the products we sell and make us less competitive. Also, products may not be delivered to certain limited regions impacted by urban violence, which may prevent us from delivering our products to our customers’ homes.

If we do not deliver products in a timely manner or if we deliver damaged products, our customers may refuse to accept them and lose confidence in us. Many of the products we sell may be especially sensitive to delivery delays given that they are often purchased in anticipation of a specific date. Other products have a limited shelf-life and become quickly outdated. Any inability to promptly and successfully deliver the products we sell to customers, may result in the loss of their business and a material and adverse effect on our financial condition and reputation.

15

Table of Contents

We are partially dependent upon a select number of prime brands manufactured by certain retail companies. We do not have long-term agreements with our suppliers, and they can cease or limit our access to their products at any time, which could adversely impact our results depending on the importance of the supplier.

Our business partially depends on a select number of prime brands. For instance, for the years ended December 31, 2015, 2016 and 2017, Nike, Adidas, Mizuno and Asics made up approximately 41.2%, 34.4% and 39.2%, respectively, of our net sales. We currently do not have long-term agreements with our suppliers. If any of these suppliers choose not to sell their products to us or limit our access to their products (for example, by entering into exclusive distribution arrangements with other retailers), our capacity to grow, our market share and our financial results could be adversely impacted. Also, to the extent that the increase in the sales of our private label products on our sites negatively affects the sales of our suppliers’ products, our relationship with certain of them could be adversely impacted.

In addition, our suppliers participate in an extremely competitive market with few global brands having the majority of the market share. In order to gain scale or market share, these brands could merge or acquire competitors. The further concentration of our suppliers could negatively impact our ability to negotiate with them and limit the number of companies that could act as our main suppliers.

If we are unable to successfully manage the logistical challenge of expanding our operations, including the requisite technological capabilities, our results of operations and business could be materially and adversely affected.