UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| | |

| ☐ | Definitive Proxy Statement |

| | |

| ☒ | Definitive Additional Materials |

| | |

| ☐ | Soliciting Material Under Rule 14a-12 |

| | |

ASHFORD HOSPITALITY PRIME, INC.

(Name of Registrant as Specified in Its Charter)

(Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| | | |

| ☒ | No fee required. |

| | |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| | | |

| | (1) | Title of each class of securities to which transaction applies: |

| | (2) | Aggregate number of securities to which transaction applies: |

| | (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| | (4) | Proposed maximum aggregate value of transaction: |

| | (5) | Total fee paid: |

| | |

| ☐ | Fee paid previously with preliminary materials: |

| | |

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. |

| | | |

| | (1) | Amount previously paid: |

| | (2) | Form, Schedule or Registration Statement No.: |

| | (3) | Filing Party: |

| | (4) | Date Filed: |

On May 11, 2016, Ashford Hospitality Prime, Inc. issued the following press release and investor presentation.

| Contact: | Mike Geller | Trevor Gibbons | Marilynn Meek |

| | Edelman | Edelman | Financial Relations Board |

| | (212) 729-2163 | (212) 704-8166 | (212) 827-3773 |

ASHFORD PRIME FILES INVESTOR PRESENTATION

DALLAS, May 11, 2016 -- Ashford Hospitality Prime, Inc., (NYSE: AHP) (“Ashford Prime” or the “Company”) today filed an investor presentation with the Securities and Exchange Commission in connection with the Company’s 2016 Annual Meeting of Stockholders (the “2016 Annual Meeting”). The presentation highlights Ashford Prime’s long-stated strategy of investing in high RevPAR, high quality hotels in gateway and resort markets. In addition, the presentation emphasizes the Company’s strong track record of delivering excellence through operational results, prudent and accretive growth, and the return of capital to stockholders; as well as strong governance and oversight from a highly-qualified Board of Directors.

In addition, the presentation demonstrates that the Company believes there is no compelling reason for stockholders to elect any of the nominees proposed by Sessa Capital (“Sessa”). The presentation is available on the Company’s website at www.ahpreit.com and www.ashfordprimefacts.com. Key takeaways from the investor presentation include:

| · | The Company’s belief that Sessa’s litigious and reckless proxy contest is destroying stockholder value in an attempt to take control of Ashford Prime’s board – and strip the Company of its assets and value in order to manufacture a short-term profit for itself and its own investors – with a slate of nominees that do not have the relevant experience in lodging or hotel market cycles necessary to lead the Company. |

| · | The Company’s belief that there is no compelling reason for stockholders to elect any member of Sessa’s slate to the board. Furthermore, the Company believes that if Sessa’s slate is elected and not first approved by the board, the election would not only remove a highly qualified board with a long history of hospitality experience, but would also trigger a termination fee payable to the Company’s advisor, Ashford Inc., in the hundreds of millions of dollars, which would significantly destroy stockholder value. |

| · | The Company believes that the current board of Ashford Prime, with 45 years of public board experience and significant industry expertise, is the best positioned to add value to the Company. Ashford Prime’s current board and management team have a strong track record of delivering results in operational excellence, prudent and accretive growth, and returning capital to stockholders, and have a plan in place to continue delivering on its primary objective of maximizing value for all stockholders. |

| · | The Company believes that the current board of Ashford Prime, through its strong governance and oversight, has taken multiple steps to increase stockholder value including the implementation of immediate structural changes and longer-term initiatives resulting from the conclusion of a thorough strategic review process; a 140% increase in the common dividend; the evaluation of a new Chief Executive Officer and independent directors; and sale of four hotel assets that do not have the RevPAR level or quality consistent with the Company’s strategy. |

Ashford Prime has retained Cadwalader Wickersham & Taft LLP as legal counsel. Moelis & Company LLC is acting as financial advisor to Ashford Prime in connection with Sessa’s proxy contest.

Ashford Prime is a real estate investment trust (REIT) focused on investing in luxury hotels located in resort and gateway markets.

Forward-Looking Statements

Certain statements and assumptions in this press release contain or are based upon “forward-looking” information and are being made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to risks and uncertainties. When we use the words “will likely result,” “may,” “anticipate,” “estimate,” “should,” “expect,” “believe,” “intend,” or similar expressions, we intend to identify forward-looking statements. Such forward-looking statements include, but are not limited to, our business and investment strategy, our understanding of our competition, current market trends and opportunities, and projected capital expenditures. Such statements are subject to numerous assumptions and uncertainties, many of which are outside of our control.

These forward-looking statements are subject to known and unknown risks and uncertainties, which could cause actual results to differ materially from those anticipated, including, without limitation: general volatility of the capital markets, the general economy or the hospitality industry, whether the result of market events or otherwise; our ability to deploy capital and raise additional capital at reasonable costs to repay debts, invest in our properties and fund future acquisitions; unanticipated increases in financing and other costs, including a rise in interest rates; the degree and nature of our competition; actual and potential conflicts of interest with Ashford Hospitality Trust, Inc., Ashford Hospitality Advisors, LLC (“Ashford LLC”), Ashford Inc., Remington Lodging & Hospitality, LLC, our executive officers and our non-independent directors; our ability to implement and execute on planned initiatives announced in connection with the conclusion of our independent directors’ strategic review process; changes in personnel of Ashford LLC or the lack of availability of qualified personnel; changes in governmental regulations, accounting rules, tax rates and similar matters;

legislative and regulatory changes, including changes to the Internal Revenue Code and related rules, regulations and interpretations governing the taxation of real estate investment trusts (“REITs”); and limitations imposed on our business and our ability to satisfy complex rules in order for us to qualify as a REIT for U.S. federal income tax purposes. These and other risk factors are more fully discussed in the section entitled “Risk Factors” in our Annual Report on Form 10-K, and from time to time, in our other filings with the Securities and Exchange Commission (“SEC”).

The forward-looking statements included in this press release are only made as of the date of this press release. Investors should not place undue reliance on these forward-looking statements. We are not obligated to publicly update or revise any forward-looking statements, whether as a result of new information, future events or circumstances, changes in expectations or otherwise.

ADDITIONAL INFORMATION AND WHERE TO FIND IT

Ashford Hospitality Prime, Inc. (“Ashford Prime”), its directors, executive officers and other employees may be deemed to be participants in the solicitation of proxies from Ashford Prime’s stockholders in connection with its 2016 Annual Meeting of Stockholders (the “2016 Annual Meeting”). Stockholders may obtain information regarding the names, affiliations and interests of such individuals in Ashford Prime’s definitive proxy statement, filed with the SEC on April 25, 2016. Additional information regarding the identity of potential participants, and their direct or indirect interests, by security holdings or otherwise, is set forth in the definitive proxy statement and, to the extent applicable, will be updated in other materials to be filed with the SEC in connection with Ashford Prime’s 2016 Annual Meeting.

Ashford Prime has filed a definitive proxy statement in connection with the 2016 Annual Meeting. ASHFORD PRIME STOCKHOLDERS ARE STRONGLY URGED TO READ THE DEFINITIVE PROXY STATEMENT, THE ACCOMPANYING GOLD PROXY CARD AND OTHER RELEVANT DOCUMENTS FILED BY ASHFORD PRIME WITH THE SEC IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. The definitive proxy statement and an accompanying GOLD proxy card are, along with other relevant documents, available at no charge on the SEC’s website at www.sec.gov. Copies of these documents will also be available free of charge from Ashford Prime by directing a request to Ashford Hospitality Prime, Inc., Attn: Investor Relations, 14185 Dallas Parkway, Suite 1100, Dallas, Texas 75254 or by calling (972) 490-9600.

-END-

Investor Presentation – May 2016

Certain statements and assumptions in this presentation contain or are based upon “forward-looking” information and are being made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to risks and uncertainties. When we use the words “will likely result,” “may,” “anticipate,” “estimate,” “should,” “expect,” “believe,” “intend,” or similar expressions, we intend to identify forward-looking statements. Such forward-looking statements include, but are not limited to, our business and investment strategy, our understanding of our competition, current market trends and opportunities, and projected capital expenditures. Such statements are subject to numerous assumptions and uncertainties, many of which are outside of our control. These forward-looking statements are subject to known and unknown risks and uncertainties, which could cause actual results to differ materially from those anticipated, including, without limitation: general volatility of the capital markets, the general economy or the hospitality industry, whether the result of market events or otherwise; our ability to deploy capital and raise additional capital at reasonable costs to repay debts, invest in our properties and fund future acquisitions; unanticipated increases in financing and other costs, including a rise in interest rates; the degree and nature of our competition; actual and potential conflicts of interest with Ashford Hospitality Trust, Inc., Ashford Hospitality Advisors, LLC (“Ashford LLC”), Ashford Inc., Remington Lodging & Hospitality, LLC, our executive officers and our non-independent directors; our ability to implement and execute on planned initiatives announced in connection with the conclusion of our independent directors’ strategic review process; changes in personnel of Ashford LLC or the lack of availability of qualified personnel; changes in governmental regulations, accounting rules, tax rates and similar matters; legislative and regulatory changes, including changes to the Internal Revenue Code and related rules, regulations and interpretations governing the taxation of real estate investment trusts (“REITs”); and limitations imposed on our business and our ability to satisfy complex rules in order for us to qualify as a REIT for U.S. federal income tax purposes. These and other risk factors are more fully discussed in the section entitled “Risk Factors” in our Annual Report on Form 10-K, and from time to time, in our other filings with the Securities and Exchange Commission (“SEC”). The forward-looking statements included in this presentation are only made as of the date of this presentation. Investors should not place undue reliance on these forward-looking statements. We are not obligated to publicly update or revise any forward-looking statements, whether as a result of new information, future events or circumstances, changes in expectations or otherwise.EBITDA is defined as net income before interest, taxes, depreciation and amortization. EBITDA yield is defined as trailing twelve month EBITDA divided by the purchase price. A capitalization rate is determined by dividing the property's net operating income by the purchase price. Net operating income is the property's funds from operations minus a capital expense reserve of either 4% or 5% of gross revenues. Hotel EBITDA flow-through is the change in Hotel EBITDA divided by the change in total revenues. EBITDA, FFO, AFFO, CAD and other terms are non-GAAP measures, reconciliations of which have been provided in prior earnings releases and filings with the SEC.This overview is for informational purposes only and is not an offer to sell, or a solicitation of an offer to buy or sell, any securities of Ashford Prime or any of its respective affiliates, and may not be relied upon in connection with the purchase or sale of any such security.Additional Information and Where to Find ItAshford Hospitality Prime, Inc. (“Ashford Prime”), its directors, executive officers and other employees may be deemed to be participants in the solicitation of proxies from Ashford Prime’s stockholders in connection with its 2016 Annual Meeting of Stockholders (the “2016 Annual Meeting”). Stockholders may obtain information regarding the names, affiliations and interests of such individuals in Ashford Prime’s definitive proxy statement, filed with the SEC on April 25, 2016. Additional information regarding the identity of potential participants, and their direct or indirect interests, by security holdings or otherwise, is set forth in the definitive proxy statement and, to the extent applicable, will be updated in other materials to be filed with the SEC in connection with Ashford Prime’s 2016 Annual Meeting.Ashford Prime has filed a definitive proxy statement in connection with the 2016 Annual Meeting. ASHFORD PRIME STOCKHOLDERS ARE STRONGLY URGED TO READ THE DEFINITIVE PROXY STATEMENT, THE ACCOMPANYING GOLD PROXY CARD AND OTHER RELEVANT DOCUMENTS FILED BY ASHFORD PRIME WITH THE SEC IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. The definitive proxy statement and an accompanying GOLD proxy card are, along with other relevant documents, available at no charge on the SEC’s website at www.sec.gov. Copies of these documents will also be available free of charge from Ashford Prime by directing a request to Ashford Hospitality Prime, Inc., Attn: Investor Relations, 14185 Dallas Parkway, Suite 1100, Dallas, Texas 75254 or by calling (972) 490-9600. 2 Certain Disclosures

Background on Ashford Prime 3 Ashford Hospitality Prime, Inc. ("Ashford Prime" or the "Company")(NYSE: AHP) was created in November 2013 through a spin-off of 8 high quality hotels from Ashford Hospitality Trust, Inc. ("Ashford Trust")(NYSE: AHT)The spin-off was a way to unlock value for stockholdersOur strategy: invest in high RevPAR, high quality luxury hotels in gateway and resort marketsAHP was designed to have an external manager, Ashford Inc. (NYSE MKT: AINC)Lower cost than if internally advisedAn incentive structure for AINC that is aligned with AHP market performanceManagement team has a long, successful track recordSuperior long-term total shareholder returns vs. peersExtensive experience in managing lodging investments over multiple cyclesAshford Prime is majority controlled by a set of experienced, independent directorsThe Company has among the highest insider equity ownership among its peersRecently, the Board completed a wide ranging and thorough review of strategic alternativesThe Board has taken several steps to maximize value for shareholders and continues to evaluate a number of initiatives – including, potentially, a new CEO and additional independent Board members

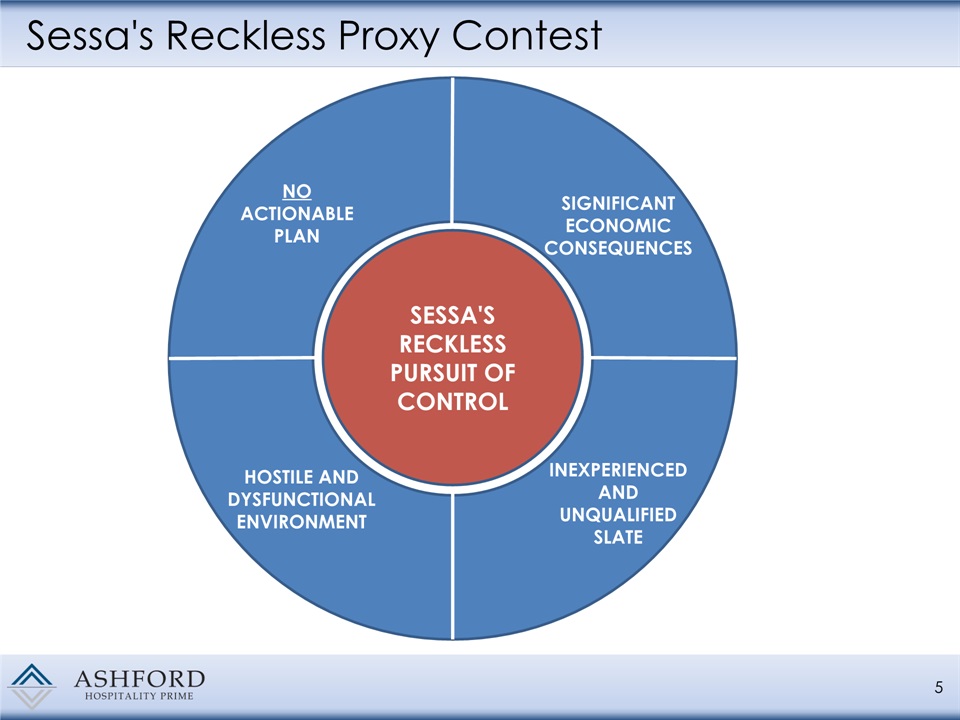

Background on our Dispute with Sessa Capital 4 History Sessa began accumulating stock in March 2015Sessa’s tone became negative when pace of buybacks slowedSessa filed a 13D in September 2015 and demanded a unilateral reduction of the termination fee under the advisory agreements, which is not possible – then criticized our efforts even though we had already announced a full review of alternatives in August (and receptivity to a sale) Sessa sued the Company and the Directors, and to protect the stockholders’ interests, the Company countersuedThe Independent Directors concluded the review in April 2016 and recommended several steps to create value for shareholders We attempted to settle, but Sessa claimed that our proposals were inadequate and would accept nothing short of full board control Summary: Why Sessa Is an Unacceptable Steward for Ashford Prime Shareholders Sessa’s slate has no relevant industry experience, no knowledge of the lodging cycle and no significant board experienceSessa apparently fails to understand that our advisory agreement is a contractual commitment and cannot be unilaterally amendedSessa has articulated absolutely no actionable plan for the Company, other than litigation with our external advisorAHP may lose access to "key money,” which could impede the Company’s ability to consummate accretive growthThe election of Sessa’s slate (a minority or a majority) could create a dysfunctional relationship with AINCThe election of Sessa’s slate will trigger a termination fee in the hundreds of millions of dollars to AINC, the Company’s advisor, if the Sessa slate is not first approved by the incumbent Board Sessa has NO actionable plan to maximize value for AHP shareholders. The election of the Sessa slate will trigger a termination fee in the hundreds of millions of dollars, significantly eroding shareholder value. The result would likely be an unworkable and hostile dynamic between AHP and our external advisor

Sessa's Reckless Proxy Contest 5 NO ACTIONABLE PLAN SIGNIFICANT ECONOMIC CONSEQUENCES INEXPERIENCED AND UNQUALIFIED SLATE HOSTILE AND DYSFUNCTIONAL ENVIRONMENT SESSA'S RECKLESS PURSUIT OF CONTROL

6 AHP BELIEVES SESSA'S CAMPAIGN IS RECKLESS AND VALUE DESTRUCTIVE The election of Sessa's slate will trigger a termination fee that is in the hundreds of millions of dollars, payable to AINC, the Company’s advisor, if Sessa’s slate is not first approved by the incumbent Board, which would significantly destroy shareholder value:Severely impacts cash balanceLikely results in dilutive equity raiseIf a majority, or even a minority, of Sessa’s slate is elected, there are other consequences beyond the termination fee payment:AHP could be in litigation with the Sessa members of its own boardSessa’s board members would be in litigation with AHP’s external advisorThe result: a hostile environment and dysfunctional situation AHP Believes Sessa’s Proxy Campaign Is Reckless 1 2 In addition to Sessa’s failure to articulate any actionable plan for the Company and Sessa’s slate being wholly inexperienced, Sessa’s campaign materially jeopardizes shareholder value. Here’s why: The Company believes the election of a minority or majority of Sessa’s slate materially jeopardizes stockholder value and risks that Ashford Prime would become a dysfunctional Company and a “zombie stock”

Strong Governance & Oversight from the Current Board 7 THIS BOARD HAS CONSISTENT TRACK RECORD OF MAXIMIZING SHAREHOLDER VALUE This Board has taken multiple steps to increase stockholder value:Increased the common dividend from $0.05 per quarter to $0.12, a 140% increase Bought back ~$30 million of stock and recently announced an intent to initiate a new $50 million share repurchase programAttractive acquisitionsRefinanced debt at lower rates to increase cash flowRecently announced a plan to sell four hotels that do not have the RevPAR level or quality consistent with Ashford Prime's strategyEvaluating appointment of a new CEO, primarily dedicated to value creation at Ashford PrimeEvaluating the addition of up to two additional Independent DirectorsInitiated strategic review process to maximize value (before Sessa's initial 13D filing)Aggregate 45 years of public board experience

8 STRONG OPERATIONAL PERFORMANCE 7.3% RevPAR growth in 2015 was the highest amongst our peersPortfolio RevPAR of $199 is second amongst our peers AHP Leadership Has Delivered Results in Operational Excellence

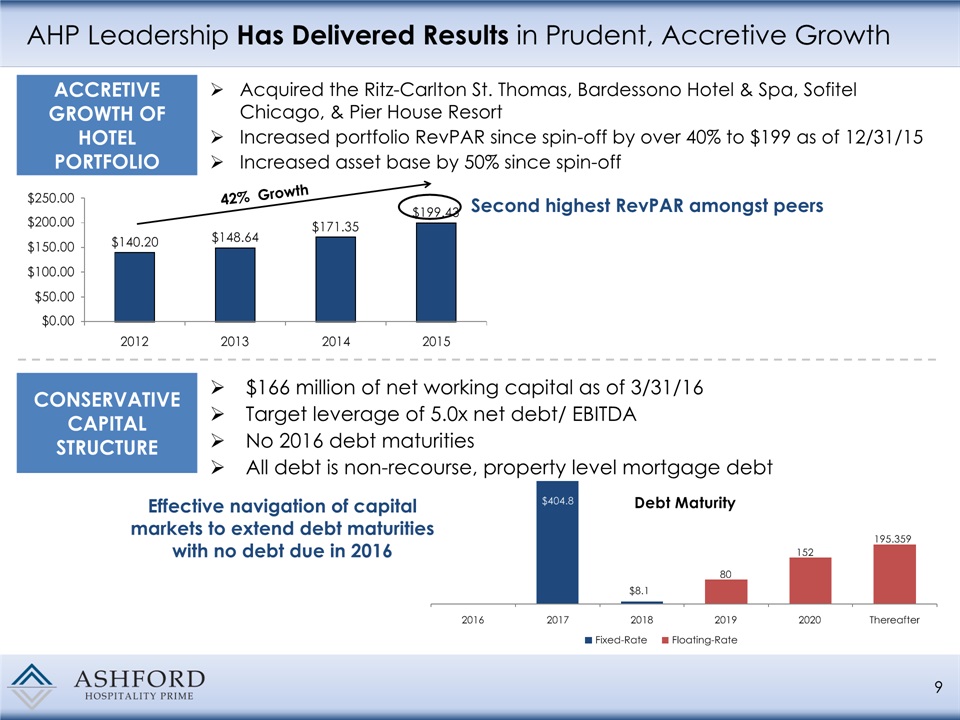

9 AHP Leadership Has Delivered Results in Prudent, Accretive Growth ACCRETIVE GROWTH OF HOTEL PORTFOLIO CONSERVATIVE CAPITAL STRUCTURE Acquired the Ritz-Carlton St. Thomas, Bardessono Hotel & Spa, Sofitel Chicago, & Pier House ResortIncreased portfolio RevPAR since spin-off by over 40% to $199 as of 12/31/15Increased asset base by 50% since spin-off $166 million of net working capital as of 3/31/16Target leverage of 5.0x net debt/ EBITDANo 2016 debt maturitiesAll debt is non-recourse, property level mortgage debt 42% Growth Second highest RevPAR amongst peers Effective navigation of capital markets to extend debt maturities with no debt due in 2016

10 AHP Leadership Has Delivered Results in Returning Capital to Shareholders Increased quarterly common dividend by 140% since spin-off Q1 2016 AFFO per share growth of over 45% Disciplined Capital Strategies Weighted Average Interest Rate Decreased weighted average interest rate by 60 bps since 2013 improving cash flow Bought back ~$30 million of stock at discount to NAVRefinanced debt at lower weighted average interest rates$70 million convertible preferred equity raise at $18.90 conversion price (69% premium to current stock price as of April 29, 2016)

11 HIGHLY ALIGNED MANAGEMENT TEAM Insider ownership of 15%, 6x more than hotel REIT industry averageInsider ownership among the highest of its peersManagement has significant personal wealth invested in the CompanyIncentive fee based on AHP total return outperformance vs. its peersManagement can earn equity compensation from the Company in the form of performance based equity, which we believe reinforces alignment with stockholders Insider Equity Ownership Highly-aligned management team with among highest insider equity ownership of publicly-traded Hotel REITs Over 6x higher than industry peer average Public Lodging REITs include: CHSP, CLDT, DRH, FCH, HST, HT, INN, LHO, PEB, RLJ, SHOSource: Company filings.* Insider equity ownership for Ashford Prime includes direct & indirect interests & interests of related parties AHP’s Management Team Is Aligned Like No Other

12 Maximizing Value is the #1 Objective of This Board THOROUGH AND DISCIPLINED STRATEGIC REVIEW PROCESS TO MAXIMIZE SHAREHOLDER VALUE In August of 2015, we announced a full review of strategic alternatives and engaged independent financial and legal advisorsThe Board reviewed a wide range of alternatives, including:Sale of the CompanySales of individual assetsJoint venturesMergersVarious recombination scenarios with other Ashford entitiesShare repurchasesCapital raising across various structuresIn April 2016, we announced conclusion to strategic review process and other initiatives to enhance stockholder value:$50 million share repurchase programLiquidation of hedge fund investment; utilization of cash to fund share repurchase20% increase in quarterly common dividendUnwinding of the OP Unit enfranchisement preferred equity transactionCommencing sale process for up to four assets that lack the RevPAR level and product quality consistent with the long-term vision of the CompanyMore recently, we announced that we are evaluating the appointment of a new CEO whose primary responsibility would be value creation at AHP along with the addition of up to two Independent Directors

Benefits of the Ashford Structure 13 Structural Attractiveness Publicly traded external advisor increases transparency and provides strong alignment7 member Board with 5 independent directorsBase Fee – based on AHP’s total enterprise value rather than book valueIncentive Fee paid only if total stockholder return exceeds peer group average (outperformance capped at 25%)AHP owns 9.7% of AINC so shareholders participate in economics of the advisor Benefits of Structure Increased scale through affiliation with Ashford Trust (AHP = 12 hotels; AHT = 132 hotels)Strong brand relationships given large scaleCapital markets benefits given scale across the platformsAbility to partner with Ashford Trust on portfolio acquisitionsG&A savings from being externally managedOther cost synergies given scale (property insurance, etc.) Key money investment from advisorDecreased fee as market cap growsReciprocal termination rights

Sessa's Criticisms Are Misleading: Here are the Facts 14 ALLEGED CONFLICTS OF INTEREST Among highest insider ownership of any hotel REITBase fee based on enterprise value (not book value)Incentive fee based on total return outperformance vs. peersFive of Ashford Prime's seven directors are independentCharter provision requiring that related party transactions be approved by disinterested directorsAshford Inc. (NYSE MKT: AINC) has its own Board with a majority of independent directors TERMINATION FEE Sessa’s Criticisms AHT shareholders at the time of the spin-off were on both sides of the transactionContractual obligation between two independent public entitiesAshford Prime does not have the right to unilaterally change the termination feeJune 2015 amendment clarified termination fee calculation methodology in the advisory agreement; there were no changes to the calculationSessa bought stock knowing the terms of the termination fee. Then after the amendment that it protests so much, continued to buy stockCalculation of the change of control termination fee has not changed since the spin-offIf the termination fee was instead calculated as solely contractual damages, the Company believes it could be even higher than the current termination feeNature of termination fee is to compensate advisor ; it is NOT a golden parachute and fee flows to shareholders of advisorThe Company believes that the Ashford Inc. Board is more likely to consider negotiating the termination fee with current Board as opposed to Sessa's purported slate given litigation Sessa has pursued against Ashford Inc. Our Response

Sessa's Criticisms Are Misleading: Here are the Facts (Cont'd) 15 Sessa’s Criticisms Our Response ALLEGED WEAK CORPORATE GOVERNANCE Sessa is not asking for governance changes but rather unilateral contractual changes with Ashford Inc. that the Company believes Ashford Inc. will not agree toHighly-qualified, majority independent Board in place7 member Board with 5 independent directorsLead independent directorThe Board stepped into the advisory agreement with the current termination fee structure as it was put in place at the time of the spin-off Opted out of MUTANon-staggered BoardProactively initiated strategic review process prior to any contact from SessaStockholders may call special meetingStockholders may fill Board vacancies ALLEGED DISAPPOINTING STRATEGIC REVIEW The Board retained independent financial and legal advisors as part of the strategic reviewAll available strategic alternatives were considered The strategic review took 8 months, was deliberate and comprehensive and was affected by changing market conditions and impact on valuations and capital marketsThe conclusion of the strategic review is the best alternative currently available to the Company to maximize value for shareholders

Sessa's Criticisms Are Misleading: Here are the Facts (Cont'd) 16 Sessa’s Criticisms Our Response PURCHASE OF AINC STOCK Investment allows AHP shareholders to participate in the economics of AINC and we believe it will be an attractive investment for AHPWe viewed this as an attractive opportunity to acquire a large stake in our advisor without driving the price up ($95 price equated to 90-Day VWAP at the time)Stock prices of all asset managers have dropped substantially since this past summer POOR STOCK PRICE PERFORMANCE We have taken several steps to improve valueBought back ~5% of our outstanding sharesDoubled common dividend, announced an additional 20% increaseRefinanced debt at lower interest rates to improve cash flowStrong operational performance since spinThe proposed changes from the recently concluded strategic review process are intended to maximize stockholder returnsHighest total stockholder return in 2015 amongst peersStock dropped 18% the week Sessa nominated directors and continues to be negatively impacted by Sessa contrary to typical market reaction from involvement of activist investors

17 The Sessa Slate of Proposed Directors Lacks Relevant Experience JOHN PETRY ZERO hospitality experienceLacks public company board experienceLacks corporate executive experienceLacks governance expertiseInitiated unprovoked litigation with the CompanyInitiated unprovoked litigation with the Company’s advisorInconsistent strategic approaches and no clear plan to maximize value Puts the interests of his stock over long-term stockholders LAWRENCE CUNNINGHAM ZERO hospitality experienceLacks public company board experienceLacks corporate executive experience DANIEL SILVERS ZERO relevant hospitality experience CHRIS WHEELER ZERO hospitality experience PHILIP LIVINGSTON ZERO hospitality experienceLacks governance expertiseResume padding by falsely claiming to be a CPASerious issues raised about trading activity / formation of a "Group“ with purchases of AHP stockInconsistent and unstable executive experience with 9 prior CEO/CFO positionsOversaw significant destruction of shareholder value at Ambassador Group, which eventually went through dissolution

Current Board of Directors is Experienced and Qualified Ashford Prime’s Independent Directors hold 5 out of the 7 Board seats and are wholly focused on value creation for stockholders 18 Aggregate 45 Years of Public Board Experience 13 years of public board experienceFounder, Chairman, & CEO of AHP Montgomery J. BennettChairman 10 years of public board experiencePreviously CEO of CNL Real Estate Advisors and previously CEO of Trustreet Properties Curtis B. McWilliamsLead Director 3 years of public board experiencePresident of AHP Douglas A. KesslerPresident 2 years of public board experiencePartner at the law firm of Stefani Carter & Associates, LLC Stefani D. CarterIndependent Director 13 years of public board experienceHead of Lodging and Leisure Capital Markets of the First Fidelity Mortgage Corporation W. Michael MurphyIndependent Director 2 years of public board experienceCounsel at the law firm of Dykema Cox Smith Matthew D. RinaldiIndependent Director 2 years of public board experiencePartner at the law firm of Pillsbury Winthrop Shaw Pittman, LLP Andrew L. StrongIndependent Director Denotes independent director

Ashford Prime’s Board is Highly Qualified and Experienced 19 Real Estate and/or REIT Experience Lodging & Hospitality Experience Finance, M&A, and/or Legal Experience Public Board Experience Montgomery J. Bennett Curtis B. McWilliams Douglas A. Kessler Matthew D. Rinaldi Stefani D. Carter W. Michael Murphy Andrew L. Strong ASHFORD PRIME'S BOARD IS HIGHLY QUALIFIED AND EXPERIENCED

Ashford Prime’s Management Team is Experienced and Qualified 20 Aggregate 139 Years of Relevant Industry Experience 27 years of hospitality experience13 years with Ashford (14 years with Ashford predecessor)Cornell School of Hotel Administration BSCornell S.C. Johnson MBA Montgomery J. BennettChief Executive Officer & Chairman of the Board 20 years of hospitality experience13 years with Ashford10 years with Goldman SachsStanford BA, MBA Douglas A. KesslerPresident 24 years of hospitality experience13 years with Ashford (11 years with Ashford predecessor)University of North Texas BS, University of Houston JD David A. BrooksChief Operating Officer, General Counsel 16 years of hospitality experience13 years with Ashford3 years with ClubCorpCFA charterholderSouthern Methodist University BBA Deric S. Eubanks, CFAChief Financial Officer 10 years of hospitality experience5 years with Ashford (5 years with Ashford predecessor)5 years with Stephens Investment BankOklahoma State University BS Jeremy J. WelterEVP of Asset Management 31 years of hospitality experience13 years with Ashford (18 years with Ashford predecessor)Pepperdine University BS, University of Houston MS, CPA Mark L. NunneleyChief Accounting Officer 11 years of hospitality experience11 years with Ashford3 years of M&A experience at Dresser Inc. & Merrill LynchPrinceton University AB J. Robison HaysChief Strategy Officer

Management's Long Term Track Record of Creating Value at Ashford Trust 21 Since IPO on August 26, 2003Peer average includes: CHSP, CLDT, DRH, FCH, HST, HT, INN, LHO, RLJ, SHOReturns as of 1/11/16Source: SNL Total Stockholder Return Significant long-term outperformance proves management's ability to create value for shareholders over time (1)

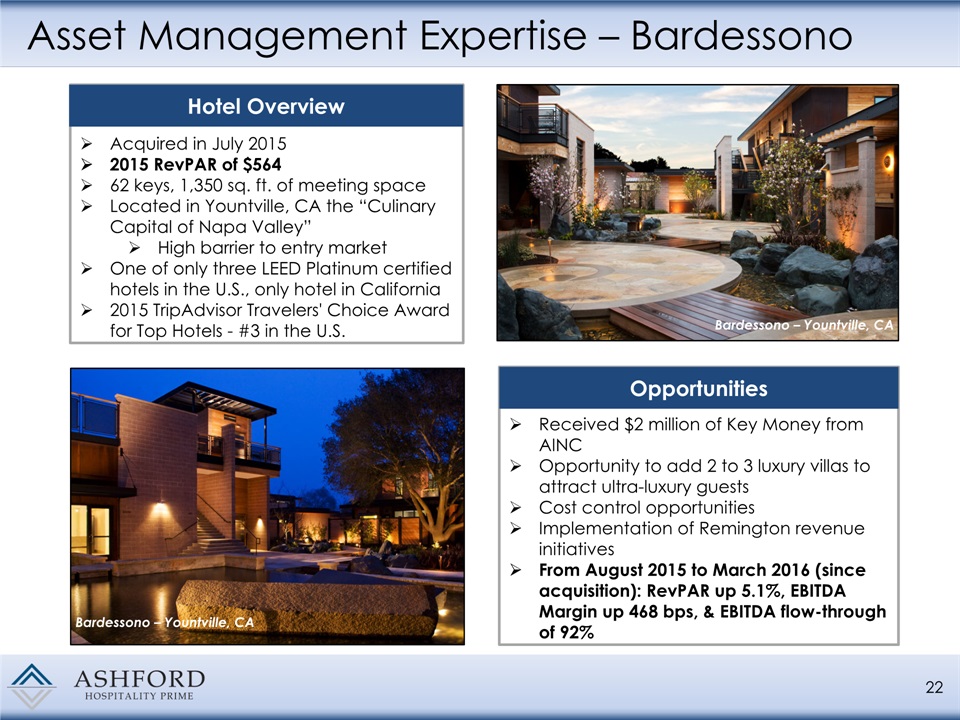

Asset Management Expertise – Bardessono 22 Acquired in July 20152015 RevPAR of $56462 keys, 1,350 sq. ft. of meeting spaceLocated in Yountville, CA the “Culinary Capital of Napa Valley”High barrier to entry marketOne of only three LEED Platinum certified hotels in the U.S., only hotel in California2015 TripAdvisor Travelers' Choice Award for Top Hotels - #3 in the U.S. Hotel Overview Received $2 million of Key Money from AINCOpportunity to add 2 to 3 luxury villas to attract ultra-luxury guestsCost control opportunitiesImplementation of Remington revenue initiativesFrom August 2015 to March 2016 (since acquisition): RevPAR up 5.1%, EBITDA Margin up 468 bps, & EBITDA flow-through of 92% Opportunities Bardessono – Yountville, CA Bardessono – Yountville, CA

Asset Management Expertise – Pier House 23 Asset management performance significantly exceeded underwritingEliminated $1.5mm in expenses through cost cutting initiatives: Right-sized staffing levelImplemented improved housekeeping practicesIdentified additional F&B efficienciesRealized synergies with other Remington-managed Key West assetsSaved $385,000 in insurance expense by adding to Ashford programRealized approximately $350,000 in annualized incremental parking revenue Implemented Strategies Pier House Resort – Key West, FL Jun-May 2013 Pre-Takeover Jun-May 2014Post-Takeover Increase (%, BPs) RevPAR $283.94 $323.66 14.0% Total Revenue* $19,196 $21,284 10.9% RPI $97.7 $101.7 4.09% EBITDA* $6,031 $8,312 37.8% EBITDA Flow 109.2% *$ in Thousands Original going-in cap rate of 6.2% in May 2013 and current cap rate of 10.0%

Asset Management Expertise – Ritz St. Thomas 24 The Ritz-Carlton St. Thomas Acquired in December 2015180 keys, 10,000 sq. ft. of meeting spaceAcquisition completed at favorable metrics of 7.2x TTM EBITDA and 10% TTM NOI cap rateLocated in St. Thomas in the U.S. Virgin Islands with high barriers to entry30 oceanfront acres along Great BayRecognized in the 2015 U.S. News & World Report's Best Hotel Rankings Hotel Overview Significant upside after recently completed extensive $22 million renovation of guest rooms and public spaceSince closing of the acquisition, our asset management team has identified several opportunities to improve performanceEBITDA Margin up 208 bps, & EBITDA flow-through of 129.1% in the 1st quarter 2016 (1st full quarter of ownership) with no change in property manager Opportunities Great Bay ViewThe Ritz-Carlton St. Thomas

Key Takeaways 25 Current Board is committed to maximizing value and recently completed a thorough review of strategic alternatives Electing the current Board will NOT trigger termination fee in the hundreds of millions of dollars which could significantly destroy shareholder value Current Board is highly-qualified with 45 years of public board experience The Company believes that the current board of Ashford Prime is best positioned to maximize value Current Board announced a plan and is implementing initiatives designed to maximize immediate and long-term stockholder value The Company believes there is no compelling reason for stockholders to elect any member of Sessa's slate to the Board

Investor Presentation – May 2016