UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22842

FORUM FUNDS II

Three Canal Plaza, Suite 600

Portland, Maine 04101

Zachary Tackett, Principal Executive Officer

Three Canal Plaza, Suite 600

Portland, Maine 04101

207-347-2000

Date of fiscal year end: September 30

Date of reporting period: October 1, 2023 – September 30, 2024

ITEM 1. REPORT TO SHAREHOLDERS.

(a) A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act, as amended (“Act”), is attached hereto.

Baywood SociallyResponsible Fund

Annual Shareholder Report - September 30, 2024

This annual shareholder report contains important information about the Baywood SociallyResponsible Fund for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at https://www.skba.com/baywood-funds. You can also request this information by contacting us at (855) 409-2297.

What were the Fund's costs for the last year?

(based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Institutional Class | $101 | 0.89% |

How did the Fund perform in the last year?

While one can never be certain how the market will behave in the short run, we believe we have been building a portfolio to help protect our shareholders’ capital by purchasing companies with attractive growth potential at low relative prices while satisfying their socially responsible desires. It is our belief that the majority of risks in the market today are with the narrow set of companies that have been driving the indices to new highs.

For holdings in the period, consider the largest sector in the SociallyResponsible fund: the financial sector. Stocks in this sector often trade at low valuations, yet many of the companies in the SociallyResponsible fund have fundamentals as good if not better than many highly valued stocks in the broad market index. For comparison sake, take AIG, Corebridge, and American Express and compare them to some of the current top IT holdings in the broad market: Apple, Microsoft, and NVIDIA. Both sets of companies currently have similar earnings growth expectations at an average of 18% EPS growth (3-year) for fund holdings in the financial sector, and an average of 20% for the holdings in the broad market IT sector. Yet we are paying an average of 12 times earnings for our holdings versus an average multiple of 32 times earnings for the IT stocks.

For the fiscal year, the fund underperformed the very concentrated set of returns of the technology laden broad market. Value stocks clearly remain “out-of-favor”, yet the it’s difficult to imagine absolute returns of approximately 27% would be considered disappointing. The market’s preference towards highly valued stocks is represented in the fund’s new regulatory benchmark the Morningstar US Market, which owns Apple, Microsoft, NVIDIA, Amazon, Meta and Alphabet as top stocks. Without owning this narrow set of stocks, one is challenged to keep up with an index loaded up on these companies, yet that is not the goal of the SociallyResponsible fund.

The SociallyResponsible fund’s returns nearly matched the Value index’ 27%. That the fund generally kept up in such a strong market is not disappointing, especially when one considers how it has performed in weaker market periods or downdrafts. Stocks in the energy, health care and industrial sectors contributed most to returns, while holdings in the consumer staples and communication sectors detracted most from returns. It is not surprising that stocks within staples and communications lagged as these tend to be out-of-favor during major market advances. In consumer staples, however not owning Walmart detracted most from returns as the nearly 50% increase in the period buoyed benchmark sector returns. While Walmart is a well-run company, we do not believe the risk-reward equation is in our favor as investors are now paying nearly 30 times next year’s earnings. In health care, fund holdings in Royal Philips, which returned more than double the benchmark’s returns and almost five times the benchmark’s health care sector returns, contributed most to returns as the company continues to move past its quality control issues at the product level and medical equipment sales finally recover from the pandemic era sales slump.

For SKBA’s in depth investment perspectives, please visit our website at www.skba.com.

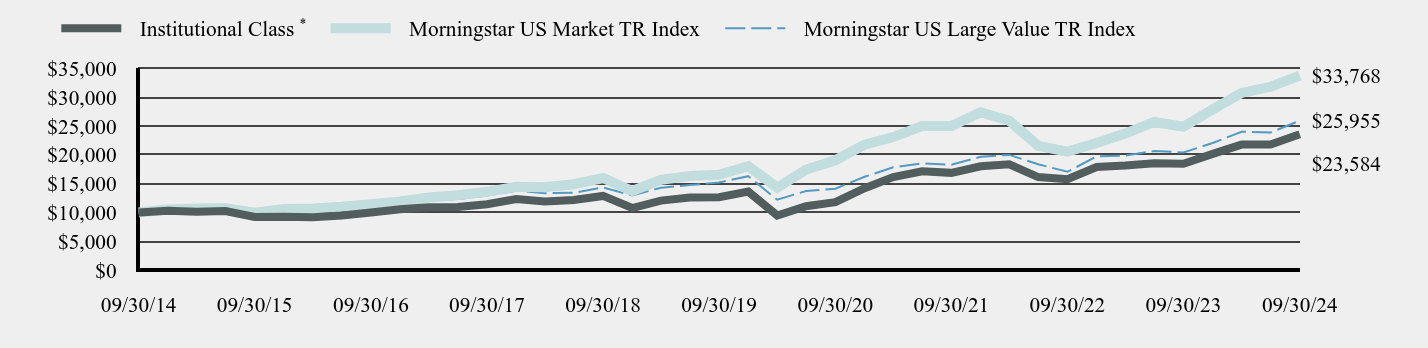

Total Return Based on a $10,000 Investment

| Date | Institutional ClassFootnote Reference* | Morningstar US Market TR Index | Morningstar US Large Value TR Index |

|---|

| 09/30/14 | $10,000 | $10,000 | $10,000 |

| 12/31/14 | $10,278 | $10,514 | $10,215 |

| 03/31/15 | $10,142 | $10,700 | $10,069 |

| 06/30/15 | $10,258 | $10,709 | $10,163 |

| 09/30/15 | $9,230 | $9,957 | $9,423 |

| 12/31/15 | $9,260 | $10,587 | $10,068 |

| 03/31/16 | $9,165 | $10,701 | $10,415 |

| 06/30/16 | $9,452 | $10,979 | $10,869 |

| 09/30/16 | $10,005 | $11,447 | $11,113 |

| 12/31/16 | $10,567 | $11,904 | $11,973 |

| 03/31/17 | $10,889 | $12,607 | $12,273 |

| 06/30/17 | $10,931 | $12,994 | $12,329 |

| 09/30/17 | $11,424 | $13,582 | $12,932 |

| 12/31/17 | $12,334 | $14,460 | $13,779 |

| 03/31/18 | $11,918 | $14,371 | $13,347 |

| 06/30/18 | $12,180 | $14,905 | $13,410 |

| 09/30/18 | $12,871 | $15,980 | $14,341 |

| 12/31/18 | $10,770 | $13,729 | $12,966 |

| 03/31/19 | $12,063 | $15,664 | $14,304 |

| 06/30/19 | $12,584 | $16,321 | $14,748 |

| 09/30/19 | $12,651 | $16,531 | $15,219 |

| 12/31/19 | $13,631 | $18,016 | $16,298 |

| 03/31/20 | $9,478 | $14,311 | $12,208 |

| 06/30/20 | $11,084 | $17,457 | $13,727 |

| 09/30/20 | $11,796 | $19,069 | $14,132 |

| 12/31/20 | $14,207 | $21,782 | $16,198 |

| 03/31/21 | $16,149 | $23,091 | $17,838 |

| 06/30/21 | $17,161 | $25,023 | $18,519 |

| 09/30/21 | $16,880 | $25,031 | $18,286 |

| 12/31/21 | $18,027 | $27,398 | $19,678 |

| 03/31/22 | $18,361 | $25,939 | $20,000 |

| 06/30/22 | $16,145 | $21,569 | $18,369 |

| 09/30/22 | $15,770 | $20,580 | $17,066 |

| 12/31/22 | $17,897 | $22,075 | $19,730 |

| 03/31/23 | $18,150 | $23,707 | $19,872 |

| 06/30/23 | $18,560 | $25,721 | $20,678 |

| 09/30/23 | $18,466 | $24,902 | $20,426 |

| 12/31/23 | $20,172 | $27,911 | $22,063 |

| 03/31/24 | $21,789 | $30,768 | $24,025 |

| 06/30/24 | $21,808 | $31,837 | $23,883 |

| 09/30/24 | $23,584 | $33,768 | $25,955 |

| Footnote | Description |

Footnote* | Performance for Institutional Shares for periods prior to January 8, 2016, reflects the performance and expenses of City National Rochdale Socially Responsible Equity Fund, a series of City National Rochdale Funds (the “Predecessor Fund”). |

The above chart represents historical performance of a hypothetical $10,000 investment over the past 10 years. Due to regulatory changes, effective September 1, 2024, the Fund changed its primary benchmark index from the Morningstar US Large Value TR Index to the Morningstar US Market TR Index. The Fund retained the Morningstar US Large Value TR Index as a secondary benchmark because the Morningstar US Large Value TR Index more closely aligns with the Fund’s investment strategies and investments restrictions.

Average Annual Total Returns

| | One Year | Five Year | Ten Year |

|---|

Institutional ClassFootnote Reference* | 27.72% | 13.27% | 8.96% |

| Morningstar US Market TR Index | 35.60% | 15.36% | 12.94% |

| Morningstar US Large Value TR Index | 27.07% | 11.27% | 10.01% |

| Footnote | Description |

Footnote* | Performance for Institutional Shares for periods prior to January 8, 2016, reflects the performance and expenses of City National Rochdale Socially Responsible Equity Fund, a series of City National Rochdale Funds (the “Predecessor Fund”). |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

| Total Net Assets | $9,048,331 |

| # of Portfolio Holdings | 53 |

| Portfolio Turnover Rate | 23% |

| Investment Advisory Fees (Net of fees waived and expenses reimbursed) | $(96,214) |

Top Ten Holdings

(% of investments)

| Texas Pacific Land Corp. | 4.51% |

| American Express Co. | 4.30% |

| Kontoor Brands, Inc. | 4.17% |

| Koninklijke Philips NV, ADR | 3.97% |

| nVent Electric PLC | 3.50% |

| International Business Machines Corp. | 3.25% |

| NXP Semiconductors NV | 2.99% |

| Kinder Morgan, Inc. | 2.75% |

| CME Group, Inc. | 2.75% |

| Berkshire Hathaway, Inc., Class B | 2.61% |

* excluding cash equivalents

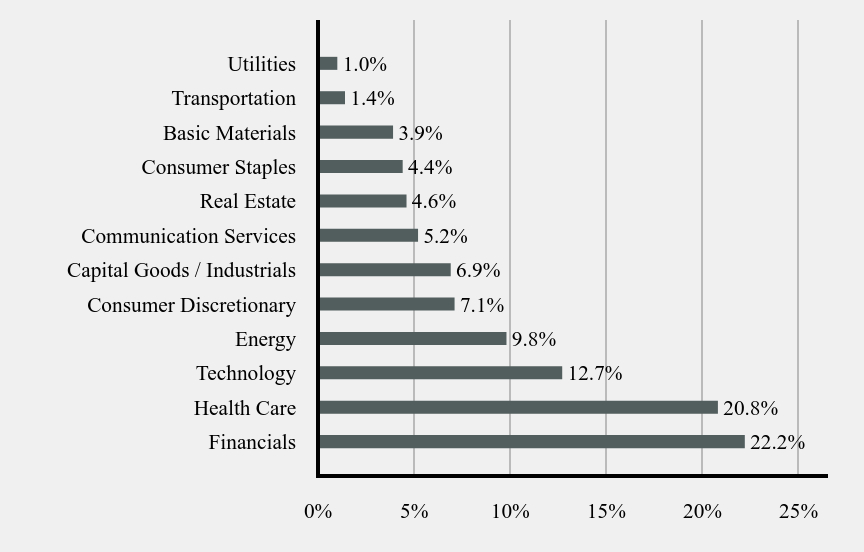

Sector Weightings

(% total investments)

| Value | Value |

|---|

| Financials | 22.2% |

| Health Care | 20.8% |

| Technology | 12.7% |

| Energy | 9.8% |

| Consumer Discretionary | 7.1% |

| Capital Goods / Industrials | 6.9% |

| Communication Services | 5.2% |

| Real Estate | 4.6% |

| Consumer Staples | 4.4% |

| Basic Materials | 3.9% |

| Transportation | 1.4% |

| Utilities | 1.0% |

* excluding cash equivalents

Where can I find additional information about the fund?

Additional information is available by scanning the QR code or at https://www.skba.com/baywood-funds, including its:

prospectus

financial information

holdings

proxy information

Baywood SociallyResponsible Fund

Annual Shareholder Report - September 30, 2024

Annual Shareholder Report - September 30, 2024

This annual shareholder report contains important information about the Baywood ValuePlus Fund for the period of October 1, 2023, to September 30, 2024. You can find additional information about the Fund at https://www.skba.com/baywood-funds. You can also request this information by contacting us at (855) 409-2297.

What were the Fund's costs for the last year?

(based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Institutional Class | $80 | 0.70% |

How did the Fund perform in the last year?

A short prologue regarding the inaugural Tailored Shareholder Report which mandates that funds be compared to broad indexes going forward. For context, the Baywood Funds have historically been compared to domestic value benchmarks, a suitable category given the strategies’ characteristics. Those categories have now been consigned of secondary importance. The quite sudden change in benchmark denotes that the Funds, decidedly value-oriented strategies, will from now on be compared to an index with an unequivocal tech bias. To wit, eight of the ten largest holdings in the Morningstar US Market TR Index can be broadly defined as Tech darlings and weigh in at a hefty 28% of the overall index. The culprits will be familiar: Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet (both classes) and Broadcom. Such a concentration of the largest companies within a narrow subset of industries leaves very little real estate for the remaining 1200 companies vying for room in this index.

Comparison to this benchmark is slightly incongruous at this point in time since Baywood ValuePlus couldn’t be more dissimilar. One thing is clear. Over the foreseeable future, the two will undoubtedly perform very differently. Since your portfolio managers are significant shareholders in the Funds, our bet is on Baywood. Time will tell.

Fund performance for the twelve months ending September 30, 2024, was driven firstly by increasing equity markets. Geopolitical and election year tensions increased noticeably yet markets responded overwhelmingly to the dictum “Don’t Fight the Fed.” By that, we refer to stocks tending to rise during times of easing monetary policy. First, European Union countries began to lower rates, soon followed by the U.S. Federal Reserve lowering its Fed Funds rate by 50 bp’s. Recent stock returns indeed remind us that cheap money tends to rekindle animal spirits.

Declining rates impact the entire capital markets structure, however, as central banks across many parts of the world declared an end to their restrictive monetary policies in the period. Companies with current high levels of debt at generationally low levels – we’ll call these companies corporate sinners – are able to refinance their obligations at less onerous interest rates than what was feared a few months ago. It is not simply the corporate sinners that are benefitting but any entity with financial leverage. With lower costs due to declining interest burdens, companies have the ability to increase spending elsewhere. One can see how the domino effect from central bank policies quickly impacts economic growth. There are of course many additional variables but at its core, monetary profligacy serves as a powerful tonic. We nevertheless believe those effects have mostly played themselves out and that conservatism is called for as reflected in the transactions engaged in the fund over the period.

Baywood ValuePlus participated in this broad rally as a number of our holdings increased over 30%. Royal Philips took the cake with its six-month return nearing 70%. One might presume shares to now be expensive yet despite the significant rally, shares in Philips trade below the market’s multiple and at approximately half the valuation levels of Apple, the largest holding in our new index. Our other medal-winners included Kontoor Brands, Hasbro, 3M and Healthcare Realty. The Fund’s worst performers in the period included Lear, Phillips 66, Conoco, Merck and Molson Coors.

The ValuePlus Fund seeks to achieve its returns over complete cycles by purchasing currently out-of-favor companies that demonstrate solid financials able to pay their shareholders in the form of dividends. The yield on the Fund is over twice that of our new primary benchmark while most of the Fund’s valuation benchmarks are at mere fractions. We believe we are well-positioned for the current market environment, especially considering the strategy has historically offered defensive characteristics.

For SKBA’s in depth investment perspectives, please visit our website at www.skba.com.

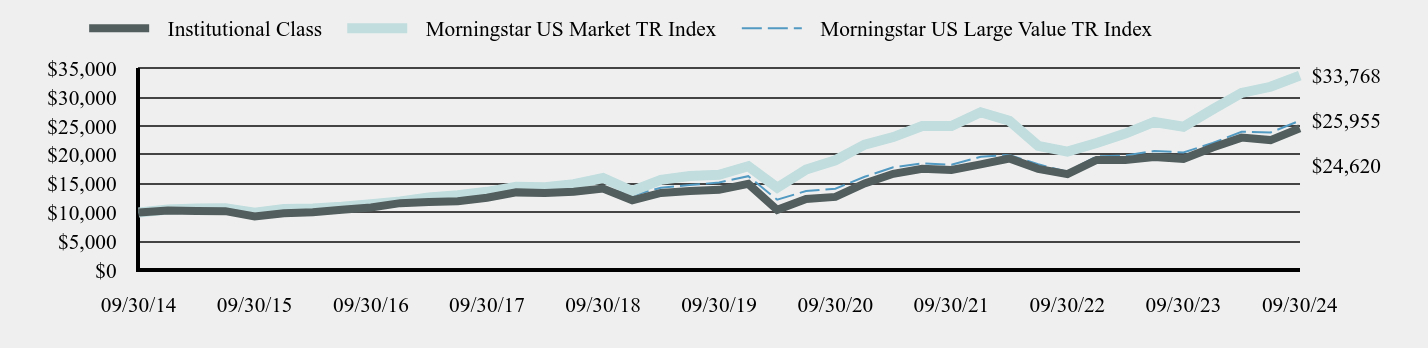

Total Return Based on a $10,000 Investment

| Date | Institutional Class | Morningstar US Market TR Index | Morningstar US Large Value TR Index |

|---|

| 09/30/14 | $10,000 | $10,000 | $10,000 |

| 12/31/14 | $10,344 | $10,514 | $10,215 |

| 03/31/15 | $10,267 | $10,700 | $10,069 |

| 06/30/15 | $10,226 | $10,709 | $10,163 |

| 09/30/15 | $9,320 | $9,957 | $9,423 |

| 12/31/15 | $9,875 | $10,587 | $10,068 |

| 03/31/16 | $10,044 | $10,701 | $10,415 |

| 06/30/16 | $10,455 | $10,979 | $10,869 |

| 09/30/16 | $10,868 | $11,447 | $11,113 |

| 12/31/16 | $11,613 | $11,904 | $11,973 |

| 03/31/17 | $11,831 | $12,607 | $12,273 |

| 06/30/17 | $11,953 | $12,994 | $12,329 |

| 09/30/17 | $12,563 | $13,582 | $12,932 |

| 12/31/17 | $13,487 | $14,460 | $13,779 |

| 03/31/18 | $13,374 | $14,371 | $13,347 |

| 06/30/18 | $13,591 | $14,905 | $13,410 |

| 09/30/18 | $14,142 | $15,980 | $14,341 |

| 12/31/18 | $12,109 | $13,729 | $12,966 |

| 03/31/19 | $13,395 | $15,664 | $14,304 |

| 06/30/19 | $13,732 | $16,321 | $14,748 |

| 09/30/19 | $13,923 | $16,531 | $15,219 |

| 12/31/19 | $14,958 | $18,016 | $16,298 |

| 03/31/20 | $10,450 | $14,311 | $12,208 |

| 06/30/20 | $12,348 | $17,457 | $13,727 |

| 09/30/20 | $12,701 | $19,069 | $14,132 |

| 12/31/20 | $15,037 | $21,782 | $16,198 |

| 03/31/21 | $16,710 | $23,091 | $17,838 |

| 06/30/21 | $17,602 | $25,023 | $18,519 |

| 09/30/21 | $17,374 | $25,031 | $18,286 |

| 12/31/21 | $18,346 | $27,398 | $19,678 |

| 03/31/22 | $19,375 | $25,939 | $20,000 |

| 06/30/22 | $17,570 | $21,569 | $18,369 |

| 09/30/22 | $16,651 | $20,580 | $17,066 |

| 12/31/22 | $19,121 | $22,075 | $19,730 |

| 03/31/23 | $19,108 | $23,707 | $19,872 |

| 06/30/23 | $19,616 | $25,721 | $20,678 |

| 09/30/23 | $19,315 | $24,902 | $20,426 |

| 12/31/23 | $21,281 | $27,911 | $22,063 |

| 03/31/24 | $23,000 | $30,768 | $24,025 |

| 06/30/24 | $22,569 | $31,837 | $23,883 |

| 09/30/24 | $24,620 | $33,768 | $25,955 |

The above chart represents historical performance of a hypothetical $10,000 investment over the past 10 years. Due to regulatory changes, effective September 1, 2024, the Fund changed its primary benchmark index from the Morningstar US Large Value TR Index to the Morningstar US Market TR Index. The Fund retained the Morningstar US Large Value TR Index as a secondary benchmark because the Morningstar US Large Value TR Index more closely aligns with the Fund’s investment strategies and investments restrictions.

Average Annual Total Returns

| | One Year | Five Year | Ten Year |

|---|

| Institutional Class | 27.46% | 12.08% | 9.43% |

| Morningstar US Market TR Index | 35.60% | 15.36% | 12.94% |

| Morningstar US Large Value TR Index | 27.07% | 11.27% | 10.01% |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

| Total Net Assets | $5,033,821 |

| # of Portfolio Holdings | 57 |

| Portfolio Turnover Rate | 22% |

| Investment Advisory Fees (Net of fees waived and expenses reimbursed) | $(129,562) |

Top Ten Holdings

(% of investments)

| RTX Corp. | 4.50% |

| Kontoor Brands, Inc. | 3.88% |

| AT&T, Inc. | 3.45% |

| International Business Machines Corp. | 3.42% |

| Merck & Co., Inc. | 3.04% |

| Koninklijke Philips NV, ADR | 2.92% |

| Medtronic PLC | 2.88% |

| Corebridge Financial, Inc. | 2.83% |

| Kinder Morgan, Inc. | 2.82% |

| ConocoPhillips | 2.39% |

* excluding cash equivalents

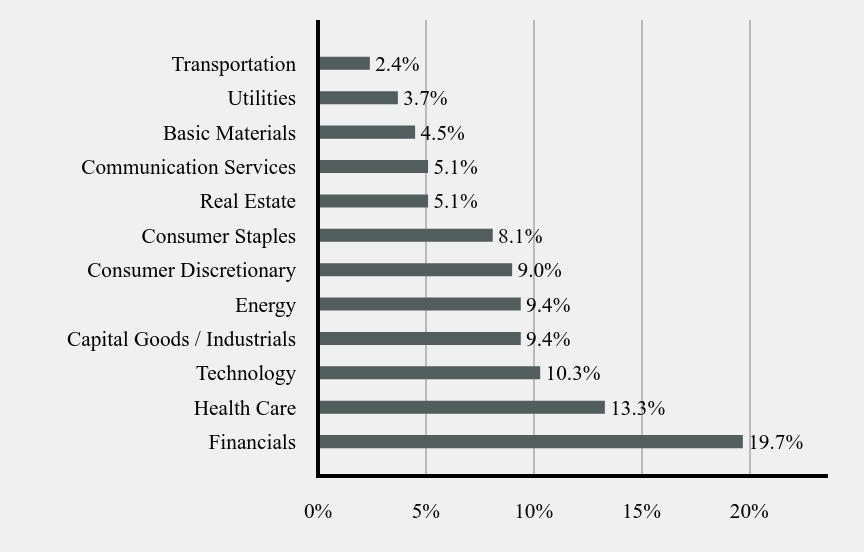

Sector Weightings

(% total investments)

| Value | Value |

|---|

| Financials | 19.7% |

| Health Care | 13.3% |

| Technology | 10.3% |

| Capital Goods / Industrials | 9.4% |

| Energy | 9.4% |

| Consumer Discretionary | 9.0% |

| Consumer Staples | 8.1% |

| Real Estate | 5.1% |

| Communication Services | 5.1% |

| Basic Materials | 4.5% |

| Utilities | 3.7% |

| Transportation | 2.4% |

* excluding cash equivalents

Where can I find additional information about the fund?

Additional information is available by scanning the QR code or at https://www.skba.com/baywood-funds, including its:

prospectus

financial information

holdings

proxy information

Annual Shareholder Report - September 30, 2024

(b) Not applicable.

ITEM 2. CODE OF ETHICS.

(a) As of the end of the period covered by this report, Forum Funds II (the “Registrant”) has adopted a code of ethics, which applies to its Principal Executive Officer and Principal Financial Officer (the “Code of Ethics”).

(c) There have been no amendments to the Registrant’s Code of Ethics during the period covered by this report.

(d) There have been no waivers to the Registrant’s Code of Ethics during the period covered by this report.

(e) Not applicable.

(f)(1) A copy of the Code of Ethics is being filed under Item 19(a)(1) hereto.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

(a)(1) The Board of Trustees has determined that the Registrant has an audit committee financial expert, as defined in Item 3 of Form N-CSR, serving on its audit committee.

(a)(2) The audit committee financial expert, Mr. Mark Moyer, is a non-“interested” Trustee (as defined in Item 3(a)(2) of Form N-CSR.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

(a) Audit Fees - The aggregate fees billed for each of the last two fiscal years (the “Reporting Periods”) for professional services rendered by the Registrant’s principal accountant for the audit of the Registrant’s annual financial statements, or services that are normally provided by the principal accountant in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $27,600 in 2023 and $29,600 in 2024.

(b) Audit-Related Fees – The aggregate fees billed in the Reporting Periods for assurance and related services rendered by the principal accountant that were reasonably related to the performance of the audit of the Registrant’s financial statements and are not reported under paragraph (a) of this Item 4 were $0 in 2023 and $0 in 2024.

(c) Tax Fees - The aggregate fees billed in the Reporting Periods for professional services rendered by the principal accountant to the Registrant for tax compliance, tax advice and tax planning were $6,200 in 2023 and $6,400 in 2024. These services consisted of review or preparation of U.S. federal, state, local and excise tax returns.

(d) All Other Fees - The aggregate fees billed in the Reporting Periods for products and services provided by the principal accountant to the Registrant, other than the services reported in paragraphs (a) through (c) of this Item, were $0 in 2023 and $0 in 2024.

(e)(1) The Audit Committee reviews and approves in advance all audit and “permissible non-audit services” (as that term is defined by the rules and regulations of the U.S. Securities and Exchange Commission) to be rendered to a series of the Registrant (each, a “Series”). In addition, the Audit Committee reviews and approves in advance all “permissible non-audit services” to be provided to an investment adviser (not including any sub-adviser) of a Series, or an affiliate of such investment adviser, that is controlling, controlled by or under common control with the investment adviser and provides on-going services to the Registrant (“Affiliate”), by the Series’ principal accountant if the engagement relates directly to the operations and financial reporting of the Series. The Audit Committee considers whether fees paid by a Series’ investment adviser or an Affiliate to the Series’ principal accountant for audit and permissible non-audit services are consistent with the principal accountant’s independence.

(e)(2) No services included in (b) - (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Not applicable

(g) The aggregate non-audit fees billed by the principal accountant for services rendered to the Registrant for the Reporting Periods were $0 in 2023 and $0 in 2024. There were no fees billed in either of the Reporting Periods for non-audit services rendered by the principal accountant to the Registrant’s investment adviser or any Affiliate.

(h) During the Reporting Period, the Registrant's principal accountant provided no non-audit services to the investment advisers or any entity controlling, controlled by or under common control with the investment advisers to the series of the Registrant to which this report relates.

(i) Not applicable. The Registrant has not retained, for the preparation of the audit report on the financial statements included in the Form N-CSR, a registered public accounting firm that has a branch or office that is located in a foreign jurisdiction and that the Public Company Accounting Oversight Board (the “PCAOB”) has determined that the PCAOB is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction.

(j) Not applicable. The Registrant is not a “foreign issuer,” as defined in 17 CFR 240.3b-4.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

Not applicable.

ITEM 6. INVESTMENTS.

(a) Included as part of financial statements filed under Item 7(a).

(b) Not applicable.

ITEM 7. FINANCIAL STATEMENTS AND FINANCIAL HIGHLIGHTS FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES.

(a)

Annual

Financials

and

Other

Information

September

30,

2024

Advised

by:

SKBA

Capital

Management,

LLC

www.baywoodfunds.com

BAYWOOD

VALUE

PLUS

FUND

SCHEDULE

OF

INVESTMENTS

September

30,

2024

See

Notes

to

Financial

Statements.

The

following

is

a

summary

of

the

inputs

used

to

value

the

Fund's instruments

as

of

September

30,

2024.

The

inputs

or

methodology

used

for

valuing

securities

are

not

necessarily

an

indication

of

the

risks

associated

with

investing

in

those

securities.

For

more

information

on

valuation

inputs,

and

their

aggregation

into

the

levels

used

in

the

table

below,

please

refer

to

the

Security

Valuation

section

in

Note

2

of

the

accompanying

Notes

to

Financial

Statements.

The

Level

1

value

displayed

in

this

table

is

Common

Stock

and

a

Money

Market

Fund.

Refer

to

this

Schedule

of

Investments

for

a

further

breakout

of

each

security

by

industry.

Shares

Security

Description

Value

Common

Stock

-

96.4%

Basic

Materials

-

4.3%

300

Air

Products

and

Chemicals,

Inc.

$

89,322

400

Packaging

Corp.

of

America

86,160

600

Rio

Tinto

PLC,

ADR

42,702

218,184

Capital

Goods

/

Industrials

-

9.0%

700

3M

Co.

95,690

300

L3Harris

Technologies,

Inc.

71,361

110

Parker-Hannifin

Corp.

69,500

1,800

RTX

Corp.

218,088

454,639

Communication

Services

-

4.9%

7,600

AT&T,

Inc.

167,200

1,900

Comcast

Corp.,

Class A

79,363

246,563

Consumer

Discretionary

-

8.7%

500

Darden

Restaurants,

Inc.

82,065

400

Genuine

Parts

Co.

55,872

800

Hasbro,

Inc.

57,856

2,300

Kontoor

Brands,

Inc.

188,094

200

Lowe's

Cos.,

Inc.

54,170

438,057

Consumer

Staples

-

7.9%

800

Ingredion,

Inc.

109,944

2,600

Kenvue,

Inc.

60,138

1,110

Molson

Coors

Beverage

Co.,

Class B

63,847

300

PepsiCo.,

Inc.

51,015

400

Target

Corp.

62,344

250

The

Hershey

Co.

47,945

395,233

Energy

-

9.0%

500

Chevron

Corp.

73,635

1,100

ConocoPhillips

115,808

1,400

Equinor

ASA,

ADR

35,462

6,200

Kinder

Morgan,

Inc.

136,958

700

Phillips

66

92,015

453,878

Financials

-

19.0%

1,500

Air

Lease

Corp.

67,935

1,100

American

International

Group,

Inc.

80,553

1,100

Brookfield

Asset

Management,

Ltd.

52,019

1,200

Citigroup,

Inc.

75,120

500

CME

Group,

Inc.

110,325

4,700

Corebridge

Financial,

Inc.

137,052

1,200

MetLife,

Inc.

98,976

3,000

Radian

Group,

Inc.

104,070

900

The

Charles

Schwab

Corp.

58,329

1,100

Truist

Financial

Corp.

47,047

1,000

U.S.

Bancorp

45,730

1,400

Wells

Fargo

&

Co.

79,086

956,242

Health

Care

-

12.8%

140

Amgen,

Inc.

45,109

700

Cardinal

Health,

Inc.

77,364

4,336

Koninklijke

Philips

NV,

ADR

(a)

141,874

1,550

Medtronic

PLC

139,547

1,300

Merck

&

Co.,

Inc.

147,628

3,200

Pfizer,

Inc.

92,608

644,130

Real

Estate

-

5.0%

4,200

Healthcare

Realty

Trust,

Inc.

REIT

76,230

1,104

Realty

Income

Corp.

REIT

70,016

2,600

VICI

Properties,

Inc.

REIT

86,606

Shares

Security

Description

Value

Real

Estate

-

5.0%

(continued)

500

Weyerhaeuser

Co.

REIT

$

16,930

249,782

Technology

-

9.9%

1,200

Cisco

Systems,

Inc.

63,864

750

International

Business

Machines

Corp.

165,810

900

NetApp,

Inc.

111,159

400

NXP

Semiconductors

NV

96,004

300

Texas

Instruments,

Inc.

61,971

498,808

Transportation

-

2.3%

250

FedEx

Corp.

68,420

200

Union

Pacific

Corp.

49,296

117,716

Utilities

-

3.6%

700

American

Electric

Power

Co.,

Inc.

71,820

1,200

Pinnacle

West

Capital

Corp.

106,308

178,128

Total

Common

Stock

(Cost

$3,390,286)

4,851,360

Shares

Security

Description

Value

Money

Market

Fund

-

3.3%

168,206

First

American

Government

Obligations

Fund,

Class X,

4.82%

(b)

(Cost

$168,206)

168,206

Investments,

at

value

-

99.7%

(Cost

$3,558,492)

$

5,019,566

Other

Assets

&

Liabilities,

Net

-

0.3%

14,255

Net

Assets

-

100.0%

$

5,033,821

ADR

American

Depositary

Receipt

PLC

Public

Limited

Company

REIT

Real

Estate

Investment

Trust

(a)

Non-income

producing

security.

(b)

Dividend

yield

changes

daily

to

reflect

current

market

conditions.

Rate

was

the

quoted

yield

as

of

September

30,

2024.

Valuation

Inputs

Investments

in

Securities

Level

1

-

Quoted

Prices

$

5,019,566

Level

2

-

Other

Significant

Observable

Inputs

–

Level

3

-

Significant

Unobservable

Inputs

–

Total

$

5,019,566

BAYWOOD

VALUE

PLUS

FUND

SCHEDULE

OF

INVESTMENTS

September

30,

2024

See

Notes

to

Financial

Statements.

PORTFOLIO

HOLDINGS

(Unaudited)

%

of

Total

Investments

Basic

Materials

4.3%

Capital

Goods

/

Industrials

9.1%

Communication

Services

4.9%

Consumer

Discretionary

8.7%

Consumer

Staples

7.9%

Energy

9.0%

Financials

19.1%

Health

Care

12.8%

Real

Estate

5.0%

Technology

9.9%

Transportation

2.3%

Utilities

3.6%

Money

Market

Fund

3.4%

100.0%

BAYWOOD

VALUE

PLUS

FUND

STATEMENT

OF

ASSETS

AND

LIABILITIES

September

30,

2024

See

Notes

to

Financial

Statements.

ASSETS

Investments,

at

value

(Cost

$3,558,492)

$

5,019,566

Receivables:

Fund

shares

sold

2,109

Dividends

6,374

From

investment

advisor

11,586

Prepaid

expenses

9,446

Total

Assets

5,049,081

LIABILITIES

Accrued

Liabilities:

Fund

services

fees

4,752

Other

expenses

10,508

Total

Liabilities

15,260

NET

ASSETS

$

5,033,821

COMPONENTS

OF

NET

ASSETS

Paid-in

capital

$

3,422,273

Distributable

Earnings

1,611,548

NET

ASSETS

$

5,033,821

SHARES

OF

BENEFICIAL

INTEREST

AT

NO

PAR

VALUE

(UNLIMITED

SHARES

AUTHORIZED)

218,400

NET

ASSET

VALUE,

OFFERING

AND

REDEMPTION

PRICE

PER

SHARE

$

23.05

BAYWOOD

VALUE

PLUS

FUND

STATEMENT

OF

OPERATIONS

FOR

THE

YEAR

ENDED

SEPTEMBER

30,

2024

See

Notes

to

Financial

Statements.

INVESTMENT

INCOME

Dividend

income

(Net

of

foreign

withholding

taxes

of

$2,474)

$

158,399

Total

Investment

Income

158,399

EXPENSES

Investment

advisor

fees

22,305

Fund

services

fees

58,616

Transfer

agent

fees

19,380

Custodian

fees

5,185

Registration

fees

20,826

Professional

fees

33,579

Trustees'

fees

and

expenses

7,246

Shareholder

reports

17,470

Other

expenses

19,485

Total

Expenses

204,092

`Fees

waived

and

expenses

reimbursed

(172,867)

Net

Expenses

31,225

NET

INVESTMENT

INCOME

127,174

NET

REALIZED

AND

UNREALIZED

GAIN

(LOSS)

Net

realized

gain

on

investments

129,979

Net

change

in

unrealized

appreciation

(depreciation)

on

investments

821,954

NET

REALIZED

AND

UNREALIZED

GAIN

951,933

INCREASE

IN

NET

ASSETS

RESULTING

FROM

OPERATIONS

$

1,079,107

BAYWOOD

VALUE

PLUS

FUND

STATEMENTS

OF

CHANGES

IN

NET

ASSETS

See

Notes

to

Financial

Statements.

For

the

Years

Ended

September

30,

2024

2023

OPERATIONS

Net

investment

income

$

127,174

$

120,020

Net

realized

gain

129,979

120,610

Net

change

in

unrealized

appreciation

(depreciation)

821,954

275,694

Increase

in

Net

Assets

Resulting

from

Operations

1,079,107

516,324

DISTRIBUTIONS

TO

SHAREHOLDERS

Total

Distributions

Paid

(240,472)

(191,543)

CAPITAL

SHARE

TRANSACTIONS

Sale

of

shares

111,881

334,388

Reinvestment

of

distributions

239,380

191,229

Redemption

of

shares

(75,626)

(164,807)

Increase

in

Net

Assets

from

Capital

Share

Transactions

275,635

360,810

Increase

in

Net

Assets

1,114,270

685,591

NET

ASSETS

Beginning

of

Year

3,919,551

3,233,960

End

of

Year

$

5,033,821

$

3,919,551

SHARE

TRANSACTIONS

Sale

of

shares

5,376

16,809

Reinvestment

of

distributions

11,622

9,826

Redemption

of

shares

(3,694)

(8,369)

Increase

in

Shares

13,304

18,266

BAYWOOD

VALUE

PLUS

FUND

FINANCIAL

HIGHLIGHTS

See

Notes

to

Financial

Statements.

These

financial

highlights

reflect

selected

data

for

a

share

outstanding

throughout

each

year.

For

the

Years

Ended

September

30,

2024

2023

2022

2021

2020

INSTITUTIONAL

SHARES

NET

ASSET

VALUE,

Beginning

of

Year

$

19.11

$

17.31

$

20.03

$

14.96

$

17.03

INVESTMENT

OPERATIONS

Net

investment

income

(a)

0.60

0.60

0.55

0.45

0.39

Net

realized

and

unrealized

gain

(loss)

4.49

2.17

(1.26)

5.04

(1.86)

Total

from

Investment

Operations

5.09

2.77

(0.71)

5.49

(1.47)

DISTRIBUTIONS

TO

SHAREHOLDERS

FROM

Net

investment

income

(0.56)

(0.59)

(0.49)

(0.42)

(0.38)

Net

realized

gain

(0.59)

(0.38)

(1.52)

–

(0.22)

Total

Distributions

to

Shareholders

(1.15)

(0.97)

(2.01)

(0.42)

(0.60)

NET

ASSET

VALUE,

End

of

Year

$

23.05

$

19.11

$

17.31

$

20.03

$

14.96

TOTAL

RETURN

27.46%

16.00%

(4.16)%

36.80%

(8.77)%

RATIOS/SUPPLEMENTARY

DATA

Net

Assets

at

End

of

Year

(000s

omitted)

$

5,034

$

3,920

$

3,234

$

3,389

$

2,588

Ratios

to

Average

Net

Assets:

Net

investment

income

2.84%

3.08%

2.77%

2.39%

2.51%

Net

expenses

0.70%

0.70%

0.70%

0.70%

0.70%

Gross

expenses

(b)

4.57%

4.75%

5.19%

5.66%

6.68%

PORTFOLIO

TURNOVER

RATE

22%

28%

48%

35%

40%

(a)

Calculated

based

on

average

shares

outstanding

during

each

year.

(b)

Reflects

the

expense

ratio

excluding

any

waivers

and/or

reimbursements.

BAYWOOD

SOCIALLY

RESPONSIBLE

FUND

SCHEDULE

OF

INVESTMENTS

September

30,

2024

See

Notes

to

Financial

Statements.

The

following

is

a

summary

of

the

inputs

used

to

value

the

Fund's instruments

as

of

September

30,

2024.

The

inputs

or

methodology

used

for

valuing

securities

are

not

necessarily

an

indication

of

the

risks

associated

with

investing

in

those

securities.

For

more

information

on

valuation

inputs,

and

their

aggregation

into

the

levels

used

in

the

table

below,

please

refer

to

the

Security

Valuation

section

in

Note

2

of

the

accompanying

Notes

to

Financial

Statements.

The

Level

1

value

displayed

in

this

table

is

Common

Stock.and

a

Money

Market

Fund.

Refer

to

this

Schedule

of

Investments

for

a

further

breakout

of

each

security

by

industry.

Shares

Security

Description

Value

Common

Stock

-

97.6%

Basic

Materials

-

3.8%

200

Air

Products

and

Chemicals,

Inc.

$

59,548

5,900

Graphic

Packaging

Holding

Co.

174,581

500

Packaging

Corp.

of

America

107,700

341,829

Capital

Goods

/

Industrials

-

6.7%

800

3M

Co.

109,360

13,000

Clarivate

PLC

(a)

92,300

300

Cummins,

Inc.

97,137

4,400

nVent

Electric

PLC

309,144

607,941

Communication

Services

-

5.1%

600

Alphabet,

Inc.,

Class A

99,510

9,200

AT&T,

Inc.

202,400

3,800

Comcast

Corp.,

Class A

158,726

460,636

Consumer

Discretionary

-

7.0%

1,900

Aptiv

PLC

(a)

136,819

900

Genuine

Parts

Co.

125,712

4,500

Kontoor

Brands,

Inc.

368,010

630,541

Consumer

Staples

-

4.3%

7,900

Kenvue,

Inc.

182,727

1,600

Mondelez

International,

Inc.,

Class A

117,872

500

PepsiCo.,

Inc.

85,025

385,624

Energy

-

9.6%

2,600

Devon

Energy

Corp.

101,712

11,000

Kinder

Morgan,

Inc.

242,990

3,000

Schlumberger

NV

125,850

450

Texas

Pacific

Land

Corp.

398,133

868,685

Financials

-

21.6%

2,600

Air

Lease

Corp.

117,754

1,400

American

Express

Co.

379,680

3,100

American

International

Group,

Inc.

227,013

500

Berkshire

Hathaway,

Inc.,

Class B

(a)

230,130

2,775

Brookfield

Corp.

147,491

400

Cboe

Global

Markets,

Inc.

81,948

1,100

CME

Group,

Inc.

242,715

7,000

Corebridge

Financial,

Inc.

204,120

700

Interactive

Brokers

Group,

Inc.

97,552

4,050

W

R

Berkley

Corp.

229,757

1,958,160

Health

Care

-

20.3%

1,500

AstraZeneca

PLC,

ADR

116,865

4,000

Avantor,

Inc.

(a)

103,480

800

Becton

Dickinson

&

Co.

192,880

1,400

Cardinal

Health,

Inc.

154,728

7,500

Fortrea

Holdings,

Inc.

(a)

150,000

10,708

Koninklijke

Philips

NV,

ADR

(a)

350,366

650

Labcorp

Holdings,

Inc.

145,262

2,300

Medtronic

PLC

207,069

1,800

Merck

&

Co.,

Inc.

204,408

200

Regeneron

Pharmaceuticals,

Inc.

(a)

210,248

1,835,306

Real

Estate

-

4.5%

10,000

Healthcare

Realty

Trust,

Inc.

REIT

181,500

2,071

Realty

Income

Corp.

REIT

131,343

2,800

Weyerhaeuser

Co.

REIT

94,808

407,651

Shares

Security

Description

Value

Technology

-

12.4%

2,300

Cisco

Systems,

Inc.

$

122,406

1,100

Coherent

Corp.

(a)

97,801

3,200

Corning,

Inc.

144,480

3,600

Intel

Corp.

84,456

1,300

International

Business

Machines

Corp.

287,404

1,000

NetApp,

Inc.

123,510

1,100

NXP

Semiconductors

NV

264,011

1,124,068

Transportation

-

1.4%

500

Union

Pacific

Corp.

123,240

Utilities

-

0.9%

900

WEC

Energy

Group,

Inc.

86,562

Total

Common

Stock

(Cost

$5,367,986)

8,830,243

Shares

Security

Description

Value

Money

Market

Fund

-

4.3%

388,822

First

American

Government

Obligations

Fund,

Class X,

4.82%

(b)

(Cost

$388,822)

388,822

Investments,

at

value

-

101.9%

(Cost

$5,756,808)

$

9,219,065

Other

Assets

&

Liabilities,

Net

-

(1.9)%

(170,734)

Net

Assets

-

100.0%

$

9,048,331

ADR

American

Depositary

Receipt

PLC

Public

Limited

Company

REIT

Real

Estate

Investment

Trust

(a)

Non-income

producing

security.

(b)

Dividend

yield

changes

daily

to

reflect

current

market

conditions.

Rate

was

the

quoted

yield

as

of

September

30,

2024.

Valuation

Inputs

Investments

in

Securities

Level

1

-

Quoted

Prices

$

9,219,065

Level

2

-

Other

Significant

Observable

Inputs

–

Level

3

-

Significant

Unobservable

Inputs

–

Total

$

9,219,065

BAYWOOD

SOCIALLY

RESPONSIBLE

FUND

SCHEDULE

OF

INVESTMENTS

September

30,

2024

See

Notes

to

Financial

Statements.

PORTFOLIO

HOLDINGS

(Unaudited)

%

of

Total

Investments

Basic

Materials

3.7%

Capital

Goods

/

Industrials

6.6%

Communication

Services

5.0%

Consumer

Discretionary

6.9%

Consumer

Staples

4.2%

Energy

9.4%

Financials

21.3%

Health

Care

19.9%

Real

Estate

4.4%

Technology

12.2%

Transportation

1.3%

Utilities

0.9%

Money

Market

Fund

4.2%

100.0%

BAYWOOD

SOCIALLY

RESPONSIBLE

FUND

STATEMENT

OF

ASSETS

AND

LIABILITIES

September

30,

2024

See

Notes

to

Financial

Statements.

ASSETS

Investments,

at

value

(Cost

$5,756,808)

$

9,219,065

Receivables:

Fund

shares

sold

1,927

Dividends

10,579

From

investment

advisor

9,168

Prepaid

expenses

9,633

Total

Assets

9,250,372

LIABILITIES

Payables:

Investment

securities

purchased

185,563

Fund

shares

redeemed

12

Accrued

Liabilities:

Fund

services

fees

5,229

Other

expenses

11,237

Total

Liabilities

202,041

NET

ASSETS

$

9,048,331

COMPONENTS

OF

NET

ASSETS

Paid-in

capital

$

5,363,015

Distributable

Earnings

3,685,316

NET

ASSETS

$

9,048,331

SHARES

OF

BENEFICIAL

INTEREST

AT

NO

PAR

VALUE

(UNLIMITED

SHARES

AUTHORIZED)

511,901

NET

ASSET

VALUE,

OFFERING

AND

REDEMPTION

PRICE

PER

SHARE

$

17.68

BAYWOOD

SOCIALLY

RESPONSIBLE

FUND

STATEMENT

OF

OPERATIONS

FOR

THE

YEAR

ENDED

SEPTEMBER

30,

2024

See

Notes

to

Financial

Statements.

INVESTMENT

INCOME

Dividend

income

(Net

of

foreign

withholding

taxes

of

$2,355)

$

218,203

Total

Investment

Income

218,203

EXPENSES

Investment

advisor

fees

56,540

Fund

services

fees

64,384

Transfer

agent

fees

19,380

Custodian

fees

5,336

Registration

fees

18,687

Professional

fees

33,833

Trustees'

fees

and

expenses

7,551

Shareholder

reports

19,164

Other

expenses

20,765

Total

Expenses

245,640

Fees

waived

and

expenses

reimbursed

(173,754)

Net

Expenses

71,886

NET

INVESTMENT

INCOME

146,317

NET

REALIZED

AND

UNREALIZED

GAIN

(LOSS)

Net

realized

gain

on

investments

224,950

Net

change

in

unrealized

appreciation

(depreciation)

on

investments

1,604,921

NET

REALIZED

AND

UNREALIZED

GAIN

1,829,871

INCREASE

IN

NET

ASSETS

RESULTING

FROM

OPERATIONS

$

1,976,188

BAYWOOD

SOCIALLY

RESPONSIBLE

FUND

STATEMENTS

OF

CHANGES

IN

NET

ASSETS

See

Notes

to

Financial

Statements.

For

the

Years

Ended

September

30,

2024

2023

OPERATIONS

Net

investment

income

$

146,317

$

135,177

Net

realized

gain

224,950

157,089

Net

change

in

unrealized

appreciation

(depreciation)

1,604,921

809,424

Increase

in

Net

Assets

Resulting

from

Operations

1,976,188

1,101,690

DISTRIBUTIONS

TO

SHAREHOLDERS

Total

Distributions

Paid

(304,037)

(296,577)

CAPITAL

SHARE

TRANSACTIONS

Sale

of

shares

1,659,816

260,194

Reinvestment

of

distributions

297,165

290,272

Redemption

of

shares

(1,561,909)

(910,587)

Increase

(Decrease)

in

Net

Assets

from

Capital

Share

Transactions

395,072

(360,121)

Increase

in

Net

Assets

2,067,223

444,992

NET

ASSETS

Beginning

of

Year

6,981,108

6,536,116

End

of

Year

$

9,048,331

$

6,981,108

SHARE

TRANSACTIONS

Sale

of

shares

104,055

18,016

Reinvestment

of

distributions

19,247

20,068

Redemption

of

shares

(96,661)

(63,325)

Increase

(Decrease)

in

Shares

26,641

(25,241)

BAYWOOD

SOCIALLY

RESPONSIBLE

FUND

FINANCIAL

HIGHLIGHTS

See

Notes

to

Financial

Statements.

These

financial

highlights

reflect

selected

data

for

a

share

outstanding

throughout

each

year.

For

the

Years

Ended

September

30,

2024

2023

2022

2021

2020

INSTITUTIONAL

SHARES

NET

ASSET

VALUE,

Beginning

of

Year

$

14.39

$

12.80

$

14.32

$

10.18

$

11.21

INVESTMENT

OPERATIONS

Net

investment

income

(a)

0.29

0.27

0.25

0.18

0.15

Net

realized

and

unrealized

gain

(loss)

3.60

1.91

(1.14)

4.19

(0.90)

Total

from

Investment

Operations

3.89

2.18

(0.89)

4.37

(0.75)

DISTRIBUTIONS

TO

SHAREHOLDERS

FROM

Net

investment

income

(0.26)

(0.27)

(0.21)

(0.14)

(0.15)

Net

realized

gain

(0.34)

(0.32)

(0.42)

(0.09)

(0.13)

Total

Distributions

to

Shareholders

(0.60)

(0.59)

(0.63)

(0.23)

(0.28)

NET

ASSET

VALUE,

End

of

Year

$

17.68

$

14.39

$

12.80

$

14.32

$

10.18

TOTAL

RETURN

27.72%

17.10%

(6.58)%

43.10%

(6.67)%

RATIOS/SUPPLEMENTARY

DATA

Net

Assets

at

End

of

Year

(000s

omitted)

$

9,048

$

6,981

$

6,536

$

6,766

$

3,626

Ratios

to

Average

Net

Assets:

Net

investment

income

1.81%

1.88%

1.73%

1.31%

1.45%

Net

expenses

0.89%

0.89%

0.89%

0.89%

0.89%

Gross

expenses

(b)

3.03%

3.12%

3.17%

3.76%

5.10%

PORTFOLIO

TURNOVER

RATE

23%

25%

22%

15%

30%

(a)

Calculated

based

on

average

shares

outstanding

during

each

year.

(b)

Reflects

the

expense

ratio

excluding

any

waivers

and/or

reimbursements.

BAYWOOD

FUNDS

NOTES

TO

FINANCIAL

STATEMENTS

September

30,

2024

Note

1.

Organization

Baywood

Value

Plus

Fund

and

Baywood

Socially

Responsible

Fund

(individually,

a

“Fund”

and

collectively,

the

“Funds”)

are

diversified

portfolios

of

Forum

Funds

II

(the

“Trust”).

The

Trust

is

a

Delaware

statutory

trust

that

is

registered

as

an

open-end,

management

investment

company

under

the

Investment

Company

Act

of

1940,

as

amended

(the

“Act”).

Under

its

Trust

Instrument,

the

Trust

is

authorized

to

issue

an

unlimited

number

of

each

Fund’s

shares

of

beneficial

interest

without

par

value.

The

Baywood

Value

Plus

Fund

commenced

operations

on

December

2,

2013,

through

a

reorganization

of

a

collective

investment

trust

into

the

Baywood

Value

Plus

Fund.

The

collective

investment

trust

was

previously

managed

by

the

Baywood

Value

Plus

Fund’s

Advisor

and

portfolio

management

team.

This

collective

investment

trust

was

organized

and

commenced

operations

on

June

27,

2008.

The

Baywood

Value

Plus

Fund

currently

offers

Institutional

Shares.

The

Baywood

Value

Plus

Fund

seeks

to

achieve

long-term

capital

appreciation

by

investing

in

undervalued

equity

securities.

The

Baywood

Socially

Responsible

Fund

commenced

operations

on

January

3,

2005.

The

Baywood

Socially

Responsible

Fund

currently

offers

Institutional

Shares.

The

Baywood

Socially

Responsible

Fund

seeks

to

provide

long-term

capital

growth.

Note

2.

Summary

of

Significant

Accounting

Policies

The

Funds

are

investment

companies

and

follow

accounting

and

reporting

guidance

under

Financial

Accounting

Standards

Board

Accounting

Standards

Codification

Topic

946,

“Financial

Services

–

Investment

Companies.”

These

financial

statements

are

prepared

in

accordance

with

accounting

principles

generally

accepted

in

the

United

States

of

America

(“GAAP”),

which

require

management

to

make

estimates

and

assumptions

that

affect

the

reported

amounts

of

assets

and

liabilities,

the

disclosure

of

contingent

liabilities

at

the

date

of

the

financial

statements,

and

the

reported

amounts

of

increases

and

decreases

in

net

assets

from

operations

during

the

fiscal

year.

Actual

amounts

could

differ

from

those

estimates.

The

following

summarizes

the

significant

accounting

policies

of

each

Fund:

Security

Valuation

–

Securities

are

recorded

at

fair

value

using

last

quoted

trade

or

official

closing

price

from

the

principal

exchange

where

the

security

is

traded,

as

provided

by

independent

pricing

services

on

each

Fund

business

day.

In

the

absence

of

a

last

trade,

securities

are

valued

at

the

mean

of

the

last

bid

and

ask

price

provided

by

the

pricing

service.

Shares

of

non-exchange

traded

open-end

mutual

funds

are

valued

at

net

asset

value

per

share

(“NAV”).

Short-term

investments

that

mature

in

sixty

days

or

less

may

be

recorded

at

amortized

cost,

which

approximates

fair

value.

Pursuant

to

Rule

2a-5

under

the

Investment

Company

Act,

the

Trust’s

Board

of

Trustees

(the

“Board”)

has

designated

the

Advisor,

as

defined

in

Note

3,

as

each

Fund’s

valuation

designee

to

perform

any

fair

value

determinations

for

securities

and

other

assets

held

by

each

Fund.

The

Advisor

is

subject

to

the

oversight

of

the

Board

and

certain

reporting

and

other

requirements

intended

to

provide

the

Board

the

information

needed

to

oversee

the

Advisor’s

fair

value

determinations.

The

Advisor

is

responsible

for

determining

the

fair

value

of

investments

for

which

market

quotations

are

not

readily

available

in

accordance

with

policies

and

procedures

that

have

been

approved

by

the

Board.

Under

these

procedures,

the

Advisor

convenes

on

a

regular

and

ad

hoc

basis

to

review

such

investments

and

considers

a

number

of

factors,

including

valuation

methodologies

and

significant

unobservable

inputs,

when

arriving

at

fair

value.

The

Board

has

approved

the

Advisor’s

fair

valuation

procedures

as

a

part

of

each

Fund’s

compliance

program

and

will

review

any

changes

made

to

the

procedures.

The

Advisor

provides

fair

valuation

inputs.

In

determining

fair

valuations,

inputs

may

include

market-based

analytics

that

may

consider

related

or

comparable

assets

or

liabilities,

recent

transactions,

market

multiples,

book

values

and

other

relevant

investment

information.

Advisor

inputs

may

include

an

income-based

approach

in

which

the

anticipated

future

cash

flows

of

the

investment

are

discounted

in

determining

fair

value.

Discounts

may

also

be

applied

based

on

the

nature

or

duration

of

any

restrictions

on

the

disposition

of

the

investments.

The

Advisor

performs

regular

reviews

of

valuation

methodologies,

key

inputs

and

assumptions,

disposition

analysis

and

market

activity.

Fair

valuation

is

based

on

subjective

factors

and,

as

a

result,

the

fair

value

of

an

investment

may

differ

from

the

security’s

market

price

and

may

not

be

the

price

at

which

the

asset

may

be

sold.

Fair

valuation

could

result

in

a

different

NAV

than

a

NAV

determined

by

using

market

quotes.

GAAP

has

a

three-tier

fair

value

hierarchy.

The

basis

of

the

tiers

is

dependent

upon

the

level

of

various

“inputs”

used

to

determine

the

value

of

each

Fund’s

investments.

These

inputs

are

summarized

in

the

three

broad

levels

listed

below:

Level

1

-

Quoted

prices

in

active

markets

for

identical

assets

and

liabilities.

BAYWOOD

FUNDS

NOTES

TO

FINANCIAL

STATEMENTS

September

30,

2024

Level

2

-

Prices

determined

using

significant

other

observable

inputs

(including

quoted

prices

for

similar

securities,

interest

rates,

prepayment

speeds,

credit

risk,

etc.).

Short-term

securities

are

valued

at

amortized

cost,

which

approximates

market

value,

are

categorized

as

Level

2

in

the

hierarchy.

Municipal

securities,

long-term

U.S.

government

obligations

and

corporate

debt

securities

are

valued

in

accordance

with

the

evaluated

price

supplied

by

a

pricing

service

and

generally

categorized

as

Level

2

in

the

hierarchy.

Other

securities

that

are

categorized

as

Level

2

in

the

hierarchy

include,

but

are

not

limited

to,

warrants

that

do

not

trade

on

an

exchange,

securities

valued

at

the

mean

between

the

last

reported

bid

and

ask

quotation

and

international

equity

securities

valued

by

an

independent

third

party

with

adjustments

for

changes

in

value

between

the

time

that

the

securities’

respective

local

market

closes

and

the

close

of

the

U.S.

market.

Level

3

-

Significant

unobservable

inputs

(including

each

Fund’s

own

assumptions

in

determining

the

fair

value

of

investments).

The

aggregate

value

by

input

level,

as

of

September

30,

2024,

for

each

Fund’s

investments

is

included

at

the

end

of

each

Fund’s

Schedule

of

Investments.

REITs

–

Each

Fund

has

made

certain

investments

in

real

estate

investment

trusts

(“REITs”)

which

pay

dividends

to

their

shareholders

based

upon

funds

available

from

operations.

It

is

quite

common

for

these

dividends

to

exceed

the

REIT’s

taxable

earnings

and

profits

resulting

in

the

excess

portion

of

such

dividends

being

designated

as

a

return

of

capital.

Each

Fund

may

include

the

gross

dividends

from

such

REITs

in

income

or

may

utilize

estimates

of

any

potential

REIT

dividend

reclassifications

in

each

Fund’s

annual

distributions

to

shareholders

and,

accordingly,

a

portion

of

each

Fund’s

distributions

may

be

designated

as

a

return

of

capital,

require

reclassification,

or

be

under

distributed

on

an

excise

basis

and

subject

to

excise

tax.

Security

Transactions,

Investment

Income

and

Realized

Gain

and

Loss

–

Investment

transactions

are

accounted

for

on

the

trade

date.

Dividend

income

is

recorded

on

the

ex-dividend

date.

Foreign

dividend

income

is

recorded

on

the

ex-dividend

date

or

as

soon

as

possible

after

determining

the

existence

of

a

dividend

declaration

after

exercising

reasonable

due

diligence.

Interest

income

is

recorded

on

an

accrual

basis.

Premium

is

amortized

to

the

next

call

date

above

par,

and

discount

is

accreted

to

maturity

using

the

effective

interest

method

and

included

in

interest

income.

Identified

cost

of

investments

sold

is

used

to

determine

the

gain

and

loss

for

both

financial

statement

and

federal

income

tax

purposes.

Distributions

to

Shareholders

–

Distributions

to

shareholders

of

net

investment

income,

if

any,

are

declared

and

paid

at

least

annually.

Distributions

to

shareholders

of

net

capital

gains,

if

any,

are

declared

and

paid

at

least

at

least

annually.

Distributions

to

shareholders

are

recorded

on

the

ex-dividend

date.

Distributions

are

based

on

amounts

calculated

in

accordance

with

applicable

federal

income

tax

regulations,

which

may

differ

from

GAAP.

These

differences

are

due

primarily

to

differing

treatments

of

income

and

gain

on

various

investment

securities

held

by

each

Fund,

timing

differences

and

differing

characterizations

of

distributions

made

by

each

Fund.

Federal

Taxes

–

Each

Fund

intends

to

continue

to

qualify

each

year

as

a

regulated

investment

company

under

Subchapter

M

of

Chapter

1,

Subtitle

A,

of

the

Internal

Revenue

Code

of

1986,

as

amended

(“Code”),

and

to

distribute

all

of

its

taxable

income

to

shareholders.

In

addition,

by

distributing

in

each

calendar

year

substantially

all

of

its

net

investment

income

and

capital

gains,

if

any,

the

Funds

will

not

be

subject

to

a

federal

excise

tax.

Therefore,

no

federal

income

or

excise

tax

provision

is

required.

Each

Fund

recognizes

interest

and

penalties,

if

any,

related

to

unrecognized

tax

benefits

as

income

tax

expense

in

the

Statements

of

Operations.

During

the

year,

each

Fund

did

not

incur

any

interest

or

penalties.

Each

Fund

files

a

U.S.

federal

income

and

excise

tax

return

as

required.

Each

Fund’s

federal

income

tax

returns

are

subject

to

examination

by

the

Internal

Revenue

Service

for

a

period

of

three

fiscal

years

after

they

are

filed.

As

of

September

30,

2024,

there

are

no

uncertain

tax

positions

that

would

require

financial

statement

recognition,

de-recognition

or

disclosure.

Income

and

Expense

Allocation

–

The

Trust

accounts

separately

for

the

assets,

liabilities

and

operations

of

each

of

its

investment

portfolios.

Expenses

that

are

directly

attributable

to

more

than

one

investment

portfolio

are

allocated

among

the

respective

investment

portfolios

in

an

equitable

manner.

Commitments

and

Contingencies

–

In

the

normal

course

of

business,

each

Fund

enters

into

contracts

that

provide

general

indemnifications

by

each

Fund

to

the

counterparty

to

the

contract.

Each

Fund’s

maximum

exposure

under

these

arrangements

is

dependent

on

future

claims

that

may

be

made

against

each

Fund

and,

therefore,

cannot

be

estimated;

however,

based

on

experience,

the

risk

of

loss

from

such

claims

is

considered

remote.

Each

Fund

has

determined

that

none

of

these

arrangements

requires

disclosure

on

each

Fund’s

statement

of

assets

and

liabilities.

BAYWOOD

FUNDS

NOTES

TO

FINANCIAL

STATEMENTS

September

30,

2024

Note

3.

Fees

and

Expenses

Investment

Advisor

–

SKBA

Capital

Management,

LLC

(the

“Advisor”)

is

the

investment

adviser

to

the

Funds.

Pursuant

to

an