Exhibit 99.2

Table of Contents

Overview | ||||

Company Profile | 2 | |||

Financial Statements | ||||

Summary of Financial Data | 4 | |||

Reconciliations of Return on Invested Capital (ROIC) | 5 | |||

Implied Enterprise Value and Debt adjusted for use of IPO Proceeds | 6 | |||

Operating Portfolio | ||||

Operating Properties | 7 | |||

Change in Operating NRSF | 8 | |||

Redevelopment Costs Summary | 9 | |||

NOI by Facility and Capital Expenditure Summary | 11 | |||

Leasing Statistics - Signed Leases | 12 | |||

Leasing Statistics - Renewed Leases and Rental Churn | 13 | |||

Leasing Statistics - Commenced Leases | 14 | |||

Lease Expirations | 15 | |||

Largest Customers | 16 | |||

Industry Segmentation | 17 | |||

Product Diversification | 18 | |||

Capital Structure | ||||

Debt Summary and Debt Maturities | 19 | |||

Interest Summary | 20 | |||

Appendix | 21 | |||

| QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Forward Looking Statements

Some of the statements contained in this supplemental information constitute forward-looking statements within the meaning of the federal securities laws. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In particular, statements pertaining to the Company’s capital resources, portfolio performance and results of operations contain forward-looking statements. Likewise, all of the statements regarding anticipated growth in funds from operations and anticipated market conditions are forward-looking statements. In some cases, you can identify forward-looking statements by the use of forward-looking terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” or “potential” or the negative of these words and phrases or similar words or phrases which are predictions of or indicate future events or trends and which do not relate solely to historical matters. You can also identify forward-looking statements by discussions of strategy, plans or intentions.

The forward-looking statements contained in this release reflect the Company’s current views about future events and are subject to numerous known and unknown risks, uncertainties, assumptions and changes in circumstances that may cause actual results to differ significantly from those expressed in any forward-looking statement. The Company does not guarantee that the transactions and events described will happen as described (or that they will happen at all). The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements: adverse economic or real estate developments in the Company’s markets or the technology industry; national and local economic conditions; difficulties in identifying properties to acquire and completing acquisitions; the Company’s failure to successfully develop, redevelop and operate acquired properties and operations; significant increases in construction and development costs; the increasingly competitive environment in which the Company operates; defaults on or non-renewal of leases by customers; increased interest rates and operating costs, including increased energy costs; financing risks, including the Company’s failure to obtain necessary outside financing; decreased rental rates or increased vacancy rates; dependence on third parties to provide Internet, telecommunications and network connectivity to the Company’s data centers; the Company’s failure to qualify and maintain its qualification as a real estate investment trust; environmental uncertainties and risks related to natural disasters; financial market fluctuations; and changes in real estate and zoning laws and increases in real property tax rates.

While forward-looking statements reflect the Company’s good faith beliefs, they are not guarantees of future performance. The Company disclaims any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes. For a further discussion of these and other factors that could cause the Company’s future results to differ materially from any forward-looking statements, see the section entitled “Risk Factors” in the Company’s final prospectus related to its IPO filed with the Securities and Exchange Commission on October 10, 2013.

| QTS Q3 Earnings 2013 | Contact: IR@qualitytech.com |

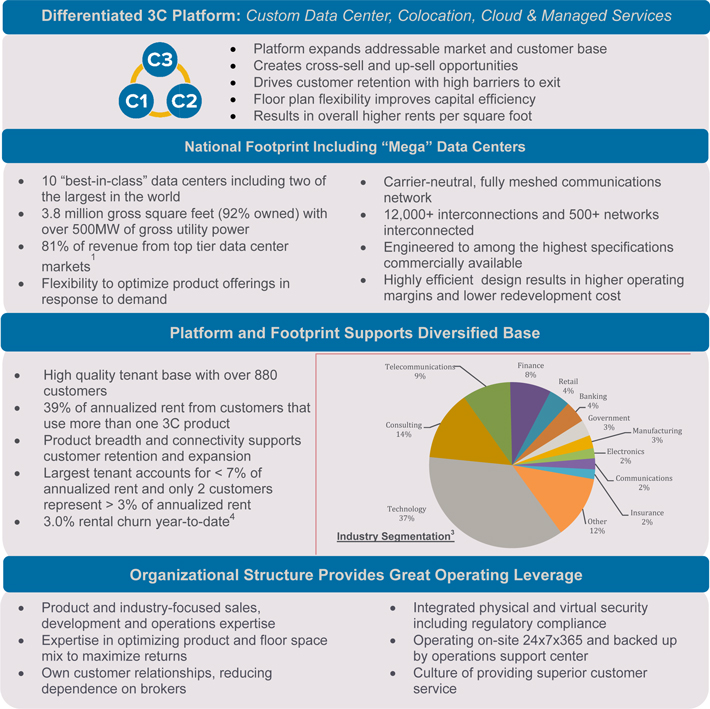

Company Profile

Differentiated 3C Platform: Custom Data Center, Colocation, Cloud & Managed Services

C1 C2 C3

Platform expands addressable market and customer base

Creates cross-sell and up-sell opportunities

Drives customer retention with high barriers to exit

Floor plan flexibility improves capital efficiency

Results in overall higher rents per square foot

National Footprint Including “Mega” Data Centers

10 “best-in-class” data centers including two of the largest in the world

3.8 million gross square feet (92% owned) with over 500MW of gross utility power

81% of revenue from top tier data center markets1

Flexibility to optimize product offerings in response to demand

Carrier-neutral, fully meshed communications network

12,000+ interconnections and 500+ networks interconnected

Engineered to among the highest specifications commercially available

Highly efficient design results in higher operating margins and lower redevelopment cost

Platform and Footprint Supports Diversified Base

High quality tenant base with over 880 customers

39% of annualized rent from customers that use more than one 3C product

Product breadth and connectivity supports customer retention and expansion

Largest tenant accounts for < 7% of annualized rent and only 2 customers represent > 3% of annualized rent

3.0% rental churn year-to-date4

Telecommunications 9%

Finance 8%

Retail 4%

Banking 4%

Government 3%

Manufacturing 3%

Electronics 2%

Communications 2%

Insurance 2%

Other 12%

Technology 37%

Consulting 14%

Industry Segmentation 3

Organizational Structure Provides Great Operating Leverage

Product and industry-focused sales, development and operations expertise

Expertise in optimizing product and floor space mix to maximize returns

Own customer relationships, reducing dependence on brokers

Integrated physical and virtual security including regulatory compliance

Operating on-site 24x7x365 and backed up by operations support center

Culture of providing superior customer service

Note: Data provided as of September 30, 2013.

| 1. | Top 10 North American Multi-Tenant Data Center Markets as defined by 451 Research LLC. |

| 2. | For period ended September 30, 2013. |

| 3. | Percentage contracted MRR as of September 30, 2013. |

| 4. | The monthly recurring rent impact from a customer completely departing our platform in a given period compared to the total monthly recurring rent at the beginning of the period. |

| 2 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

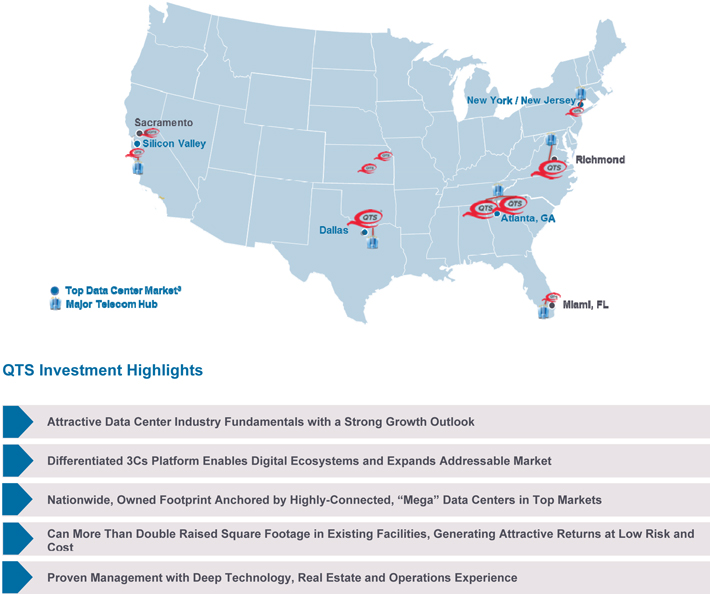

Company Profile

Nationwide Footprint in Top Data Center Markets

1.8 Million Square Feet1(92% owned)2 with over 500 MW of Gross Utility Power

Sacrament

Silicon Valley

QTS

QTS

QTS

Dallas

New York/ New Jersey

QTS

Richmond

QTS

QTS

Atlanta, GA

QTS

Miami, FL

Top Data Center Market 3

Sprint’s Global IP Network4

QTS Investment Highlights

Attractive Data Center Industry Fundamentals with a Strong Growth Outlook

Differentiated 3Cs Platform Enables Digital Ecosystems and Expands Addressable Market

Nationwide, Owned Footprint Anchored by Highly-Connected, “Mega” Data Centers in Top Markets

Can More Than Double Raised Square Footage in Existing Facilities, Generating Attractive Returns at Low Risk and Cost

Proven Management with Deep Technology, Real Estate and Operations Experience

Note: QTS data as of September 30, 2013.

| 1. | Represents our “Basis of Design” Raised Floor NRSF at full buildout. |

| 2. | Based on gross square footage. |

| 3. | Source: 451 Research; North American Multi-Tenant Datacenter Supply: Top 10 Markets. Map only shows markets where QTS has a presence. |

| 3 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Summary of Financial Data

(in thousands, except share, per share and operating portfolio statistics data)

| Three Months Ended | Nine Months Ended September 30, | |||||||||||||||||||||

| Summary of Results | September 30, 2013 | June 30, 2013 | September 30, 2012 | 2013 | 2012 | |||||||||||||||||

|

|

|

|

|

|

|

|

| ||||||||||||||

Total revenue | $ | 46,020 | $ | 42,940 | $ | 36,254 | $ | 130,458 | $ | 107,586 | ||||||||||||

Net income (loss) | 2,709 | (1,232) | (1,757) | (597) | (8,159) | |||||||||||||||||

Other Data | ||||||||||||||||||||||

FFO | $ | 13,440 | $ | 8,878 | $ | 4,947 | $ | 29,751 | $ | 12,835 | ||||||||||||

Operating FFO | 13,440 | 11,057 | 5,351 | 33,028 | 17,657 | |||||||||||||||||

Adjusted Operating FFO | 12,932 | 9,773 | 5,487 | 31,064 | 17,390 | |||||||||||||||||

Recognized MRR in the period | 39,914 | 37,448 | 32,336 | 113,698 | 95,524 | |||||||||||||||||

MRR (at period end) | 13,799 | 12,743 | 10,689 | 13,799 | 10,689 | |||||||||||||||||

EBITDA | 19,184 | 15,091 | 13,783 | 49,560 | 36,122 | |||||||||||||||||

Adjusted EBITDA | 19,694 | 17,690 | 13,391 | 54,142 | 40,644 | |||||||||||||||||

NOI | 29,281 | 26,966 | 21,911 | 82,224 | 66,162 | |||||||||||||||||

NOI as a % of revenue | 63.6% | 62.8% | 60.4% | 63.0% | 61.5% | |||||||||||||||||

Adjusted EBITDA as a % of revenue | 42.8% | 41.2% | 36.9% | 41.5% | 37.8% | |||||||||||||||||

Annualized ROIC | 15.6% | 15.1% | 15.0% | 15.2% | 16.3% | |||||||||||||||||

General and administrative expenses as a % of revenue | 21.9% | 22.6% | 23.9% | 22.5% | 24.0% | |||||||||||||||||

| Balance Sheet Data | Pro forma 2013(1) | September 30, 2013 | December 31, 2012 | |||||||||||||||||||

|

|

|

|

|

|

| ||||||||||||||||

Real estate at cost | $ | 848,386 | $ | 848,386 | $ | 734,829 | ||||||||||||||||

Net investment in real estate | 719,683 | 719,683 | 631,928 | |||||||||||||||||||

Total assets | 779,724 | 781,947 | 685,443 | |||||||||||||||||||

Credit facilities, mortgages payables, and capital leases | 331,371 | 611,371 | 490,282 | |||||||||||||||||||

Debt to last quarter annualized Adjusted EBITDA | 4.2x | |||||||||||||||||||||

Debt to Undepreciated real estate assets | 39.1% | |||||||||||||||||||||

Debt to Implied Enterprise Value (2) | 30.0% | |||||||||||||||||||||

(1) Pro forma September 30, 2013 reflects the application of IPO net proceeds. (2) The detailed calculation is shown on Page 6. |

| |||||||||||||||||||||

Operating Portfolio Statistics | September 30, 2013 | December 31, 2012 | ||||||||||

Built out square footage: | ||||||||||||

Raised floor | 740,533 | 651,236 | ||||||||||

Leasable raised floor (1) | 548,545 | 483,871 | ||||||||||

Leased raised floor | 491,654 | 418,204 | ||||||||||

Total square footage: | ||||||||||||

Total gross square feet | 3,779,519 | 3,081,519 | ||||||||||

Basis-of-design raised floor space (1) | 1,804,777 | 1,519,086 | ||||||||||

Operating data center properties | 10 | 9 | ||||||||||

Basis of design raised floor capacity | 40.9% | 42.9% | ||||||||||

Data center % occupied | 89.6% | 86.4% | ||||||||||

(1) See definition in Appendix.

| 4 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Reconciliations of Return on Invested Capital (ROIC)

(in thousands)

Return on Invested Capital (ROIC) | Three Months Ended | Nine Months Ended | ||||||||||||||||||

| September 30, | June 30, | September 30, | September 30, | |||||||||||||||||

| 2013 | 2013 | 2012 | 2013 | 2012 | ||||||||||||||||

NOI | $ | 29,281 | $ | 26,966 | $ | 21,911 | $ | 82,224 | $ | 66,162 | ||||||||||

Annualized NOI | 117,124 | 107,864 | 87,644 | 109,632 | 88,216 | |||||||||||||||

Average Undepreciated Real Estate Assets and other Net Fixed Assets Placed in Service | 748,490 | 712,930 | 584,958 | 719,967 | 541,511 | |||||||||||||||

Annualized ROIC | 15.6% | 15.1% | 15.0% | 15.2% | 16.3% | |||||||||||||||

Calculation of Average Undepreciated Real Estate Assets and other Net Fixed Assets Placed in Service | As of | As of | ||||||||||||||||||

| September 30, 2013 | June 30, 2013 | September 30, 2012 | September 30, 2013 | September 30, 2012 | ||||||||||||||||

Undepreciated Real Estate Assets and other Net Fixed Assets Placed in Service |

|

|

|

| ||||||||||||||||

Real Estate Assets, net | $ | 719,683 | $ | 701,760 | $ | 547,326 | $ | 719,683 | $ | 547,326 | ||||||||||

Less: Construction in progress | (106,630) | (120,036) | (58,379) | (106,630) | (58,379) | |||||||||||||||

Plus: Accumulated depreciation | 128,703 | 119,576 | 95,013 | 128,703 | 95,013 | |||||||||||||||

Plus: Other fixed assets, net | 10,211 | 7,734 | 5,376 | 10,211 | 5,376 | |||||||||||||||

Plus: Acquired intangibles, net | 6,850 | 7,721 | 177 | 6,850 | 177 | |||||||||||||||

Plus: Leasing Commissions, net | 11,262 | 10,145 | 6,853 | 11,262 | 6,853 | |||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Total as of period end | $ | 770,080 | $ | 726,900 | $ | 596,367 | $ | 770,080 | $ | 596,367 | ||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Average undepreciated real estate assets and other net fixed assets as of reporting period (1) | $ | 748,490 | $ | 712,930 | $ | 584,958 | $ | 719,967 | $ | 541,511 | ||||||||||

(1) Calculated by using quarterly balance of each account.

| 5 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Implied Enterprise Value and Debt adjusted for use of IPO proceeds:

(in thousands, except share data)

Implied Enterprise Value after IPO (1) | ||||

Total Shares Outstanding: | ||||

Class A Common Stock | 28,839,774 | |||

Class B Common Stock | 133,000 | |||

|

| |||

Total Shares Outstanding | 28,972,774 | |||

Units of Limited Partnership (2) | 7,822,389 | |||

|

| |||

Total Shares and Units of Limited Partnership outstanding | 36,795,163 | |||

IPO Share price | $ | 21.00 | ||

|

| |||

Pro forma market equity capitalization (in thousands) | $ | 772,698 | ||

Debt adjusted for use of IPO Proceeds | 331,371 | |||

|

| |||

Implied Enterprise Value (in thousands) | $ | 1,104,069 | ||

|

|

(1) The calculation assumes that the Company’s IPO closed on September 30, 2013 with proceeds applied to outstanding debt.

(2) Includes 25,389 operating partnership units representing the “in the money” value of Class O LTIP units on an “as if” converted basis and 175,000 Class RS LTIP units.

| Debt adjusted for use of IPO Proceeds (in thousands) | September 30, 2013 | |||

Mortgage notes payable | $ | 89,376 | ||

Unsecured credit facility | 520,000 | |||

Capital lease obligations | 1,995 | |||

|

| |||

Total Debt Prior to IPO | 611,371 | |||

Approximate Net IPO Proceeds (1) | (280,000) | |||

|

| |||

Debt adjusted for use of IPO Proceeds | $ | 331,371 | ||

|

| |||

Adjusted Debt to Implied Enterprise Value | 30% | |||

|

| |||

(1) The approximate Net IPO Proceeds do not include certain IPO costs that were incurred and paid prior to September 30, 2013.

| 6 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Operating Properties

(in thousands, except NRSF data)

The following table presents an overview of the initial portfolio of operating properties that the Company owns or leases based on information as of September 30, 2013:

| Total | ||||||||||||||||||||||||||||||||||||||||||

| Gross | Operating Net Rentable Square Feet (Operating NRSF) (3) | Available | Available For | |||||||||||||||||||||||||||||||||||||||

| Year | Square | Supporting | Annualized | Utility | Redevelopment | |||||||||||||||||||||||||||||||||||||

Property | Acquired (1) | Feet (2) | Raised Floor (4) | Office & Other (5) | Infrastructure (6) | Total | % Leased (7) | Rent (8) | Power (MW) (9) | (NRSF) (10) | ||||||||||||||||||||||||||||||||

Richmond, VA | 2010 | 1,318,353 | 84,511 | 27,214 | 113,091 | 224,816 | 75.8 % | $ | 13,904,283 | 110 | 1,060,178 | |||||||||||||||||||||||||||||||

Atlanta, GA (Atlanta - Metro) | 2006 | 968,695 | 358,016 | 24,851 | 308,527 | 691,394 | 96.9 % | $ | 64,705,041 | 72 | 242,628 | |||||||||||||||||||||||||||||||

Dallas, TX* | 2013 | 698,000 | - | - | - | - | N/A % | $ | 0 | 140 | 698,000 | |||||||||||||||||||||||||||||||

Suwanee, GA (Atlanta - Suwanee) | 2005 | 367,322 | 140,422 | 5,981 | 99,760 | 246,163 | 81.6 % | $ | 40,861,475 | 36 | 74,000 | |||||||||||||||||||||||||||||||

Santa Clara, CA** | 2007 | 135,322 | 55,494 | 1,146 | 45,721 | 102,361 | 88.7 % | $ | 19,143,215 | 11 | 25,054 | |||||||||||||||||||||||||||||||

Jersey City, NJ*** | 2006 | 122,448 | 31,503 | 14,220 | 35,387 | 81,110 | 70.7 % | $ | 9,934,596 | 7 | 26,798 | |||||||||||||||||||||||||||||||

Sacramento, CA | 2012 | 92,644 | 45,595 | 3,592 | 27,100 | 76,287 | 88.6 % | $ | 12,220,468 | 8 | 10,665 | |||||||||||||||||||||||||||||||

Overland Park, KS*** | 2003 | 32,706 | 2,493 | 0 | 5,338 | 7,831 | 83.3 % | $ | 636,775 | 1 | - | |||||||||||||||||||||||||||||||

Miami, FL | 2008 | 30,029 | 19,887 | 0 | 6,592 | 26,479 | 55.6 % | $ | 3,965,488 | 4 | - | |||||||||||||||||||||||||||||||

Wichita, KS | 2005 | 14,000 | 2,612 | 2,854 | 8,534 | 14,000 | 100.0 % | $ | 222,120 | 1 | - | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

Total | 3,779,519 | 740,533 | 79,858 | 650,050 | 1,470,441 | 89.6 % | $ | 165,593,461 | 390 | 2,137,323 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

* | This facility was acquired in February 2013 and is under redevelopment | |||

| ** | Owned facility subject to long-term ground sublease | |||

| *** | Represents facilities that we lease. | |||

| (1) | Represents the year a property was acquired or, in the case of a property under lease, the year our initial lease commenced for the property. | |||

| (2) | With respect to the Company’s owned properties, gross square feet represents the entire building area. With respect to leased properties, gross square feet represents that portion of the gross square feet subject to a lease. This includes 171,755 square feet of the Company’s office and support space, which is not included in operating NRSF.

| |||

| (3) | Represents the total square feet of a building that is currently leased or available for lease plus developed supporting infrastructure, based on engineering drawings and estimates, but does not include space held for redevelopment or space used for the Company’s office space.

| |||

| (4) | Represents management’s estimate of the portion of NRSF of the facility with available power and cooling capacity that is currently leased or readily available to be leased to customers as data center space based on engineering drawings.

| |||

| (5) | Represents the operating NRSF of the facility other than data center space (typically office and storage space) that is currently leased or available to be leased. | |||

| (6) | Represents required data center support space, including mechanical, telecommunications and utility rooms, as well as building common areas. | |||

| (7) | Calculated as data center raised floor that is subject to a signed lease for which billing has commenced as of September 30, 2013 divided by leasable raised floor based on the current configuration of the properties (548,545 square feet as of September 30, 2013) expressed as a percentage. | |||

| (8) | Annualized rent is presented for leases commenced as of September 30, 2013. The Company defines annualized rent as MRR multiplied by 12. The Company calculates MRR as monthly contractual revenue under executed contracts as of a particular date, which includes revenue from the Company’s C1, C2 and C3 rental activities and cloud and managed services, but excludes customer recoveries, deferred set up fees and other one-time and variable revenues. MRR does not include the impact from booked not billed contracts as of a particular date, unless otherwise specifically noted. | |||

| (9) | Represents installed utility power and transformation capacity that is available for use by the facility as of September 30, 2013. | |||

| (10) | Reflects space under roof that could be developed into operating NRSF in the future, excluding space currently used by the Company for our own office space, which could also be repurposed in the future. |

| 7 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Change in Operating NRSF

During the quarter, the Company placed in service, 62,020 square feet of operating NRSF and $52 million of capital. This quarter demonstrated our ability to add capacity at less than $7 million per Megawatt. During the nine month period ended September 30, 2013, we placed into service 89,276 square feet of operating NRSF and $89 million of capital. The table below sets forth the changes in each category of operating NRSF during the third quarter of 2013 and nine months ended September 30, 2013.

| Change in Raised Floor NRSF | ||||||||

Property | Three Months Ended September 30, 2013 (1) | Nine Months Ended September 30, 2013 | ||||||

Richmond, VA | 24,581 | 24,581 | ||||||

Atlanta, GA (Atlanta - Metro) | 35,000 | 35,175 | ||||||

Suwanee, GA (Atlanta - Suwanee) | - | 35,000 | ||||||

Jersey City, NJ (2) | 2,439 | (5,480) | ||||||

|

|

|

| |||||

Total | 62,020 | 89,276 | ||||||

|

|

|

| |||||

| (1) | During the third quarter, the Company brought online 62,020 square feet of raised floor space, primarily in Richmond and Atlanta-Metro. The space noted for Atlanta-Metro was included in the operating NRSF of Atlanta-Metro placed in service on June 30, 2013, however, the associated capital was not placed into service until July 1, 2013. Therefore, to match the associated capital placed into service during the quarter, we have included it as placed in service in the third quarter ended for purposes of this table. In addition, the occupancy as of June 30, 2013, would have been 86.8% if the 35,000 square feet in Atlanta-Metro was excluded. |

| (2) | Represents facility that we lease. |

| 8 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Redevelopment Costs Summary

(millions, except NRSF data)

The table below summarizes the Company’s outlook for development projects which are expected to be complete by December 31, 2014. The majority of capital in this plan is discretionary. In addition to the projects completed in the third quarter of 2013, this table reflects modifications to the Company’s capital plan as of June 30, 2013, relating to its plan to operate its facilities at higher efficiency levels and to better match new capacity with lease-up at each facility .

| Under Construction Costs | ||||||||||||||||

|

| |||||||||||||||

Property | Actual (1) | Estimated Cost to Completion (2) | Total | Expected Completion Date | ||||||||||||

Richmond | $ | 10 | $ | 17 | $ | 27 | Q2 2014 | |||||||||

Atlanta Metro | 6 | 58 | 64 | Q2 2014 | ||||||||||||

Dallas | 21 | 35 | 56 | Q3 2014 | ||||||||||||

Atlanta Suwanee | 3 | 5 | 8 | Q2 2014 | ||||||||||||

Jersey City | 3 | 1 | 4 | Q4 2013 | ||||||||||||

Sacramento | 3 | 7 | 10 | Q2 2014 | ||||||||||||

|

|

|

|

|

| |||||||||||

Totals

| $

| 46

|

| $

| 123

|

| $

| 169

|

| |||||||

|

|

|

|

|

| |||||||||||

(1) Actual for NRSF under construction through September 30, 2013. In addition to the $46 million of construction costs incurred through September 30, 2013 for redevelopment projected expected to be completed by December 31, 2014, as of September 30, 2013 we had incurred $61 million of additional costs (including acquisition costs and other capitalized costs) for other redevelopment projects that are expected to be completed after December 31, 2014.

(2) Represents management’s estimate of the additional costs required to complete the current NRSF under development. There may be an increase in costs if customers’ requirements exceed our current basis of design.

| 9 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Redevelopment Summary

(in thousands, except NRSF data)

The following table presents an overview of the Company’s redevelopment pipeline, based on information as of September 30, 2013. This table shows the Company’s ability to increase its raised floor from 740,533 square feet as of September 30, 2013 by more than 2.4 times to over 1,800,000 square feet:

The following table presents an overview of the Company’s redevelopment pipeline, based on information as of September 30, 2013.

| Redevelopment NRSF as of September 30, 2013 | ||||||||||||||||||||||||||||||||||||||||||||

| Under Construction (1) | Future Available (2) | |||||||||||||||||||||||||||||||||||||||||||

Property | Raised Floor | Office & Other | Supporting Infrastructure | Total Under Construction | Raised Floor | Office & Other | Supporting Infrastructure | Office/Other/ Supporting Infrastructure | Total Future Available | Total Available for Redevelopment (NRSF) | ||||||||||||||||||||||||||||||||||

Richmond | 22,084 | 5,000 | 43,655 | 70,739 | 450,000 | 104,000 | 435,439 | 539,439 | 989,439 | 1,060,178 | ||||||||||||||||||||||||||||||||||

Atlanta Metro | 35,000 | 5,270 | - | 40,270 | 134,200 | 13,000 | 55,158 | 68,158 | 202,358 | 242,628 | ||||||||||||||||||||||||||||||||||

Dallas | 26,000 | 22,000 | 30,600 | 78,600 | 266,000 | 66,000 | 287,400 | 353,400 | 619,400 | 698,000 | ||||||||||||||||||||||||||||||||||

Suwanee | 45,000 | - | - | 45,000 | 29,000 | - | - | - | 29,000 | 74,000 | ||||||||||||||||||||||||||||||||||

Santa Clara | - | - | - | - | 25,054 | - | - | - | 25,054 | 25,054 | ||||||||||||||||||||||||||||||||||

Jersey City | - | - | 5,557 | 5,557 | 21,241 | - | - | - | 21,241 | 26,798 | ||||||||||||||||||||||||||||||||||

Sacramento | 9,000 | - | - | 9,000 | 1,665 | - | - | - | 1,665 | 10,665 | ||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

Totals | 137,084 | 32,270 | 79,812 | 249,166 | 927,160 | 183,000 | 777,997 | 960,997 | 1,888,157 | 2,137,323 | ||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||

(1) Reflects NRSF at a facility which the Company expects will be operational by December 31, 2014.

(2) Reflects NRSF at a facility which the Company expects will be operational after December 31, 2014.

| 10 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

NOI by Facility and Capital Expenditure Summary

(in thousands)

The Company calculates net operating income, or NOI, as net income (loss), excluding: interest expense, interest income, depreciation and amortization, write off of unamortized deferred financing costs, gain on extinguishment of debt, transaction costs, gain on legal settlement, gain on sale of real estate, restructuring charge and general and administrative expenses. The Company believes that NOI is another metric that is often utilized to evaluate returns on operating real estate from period to period and also, in part, to assess the value of the operating real estate. The breakdown of NOI by facility is shown below:

| Three Months Ended | Nine Months Ended | |||||||||||||||||||

| September 30, | June 30, | September 30, | September 30, | |||||||||||||||||

| 2013 | 2013 | 2012 | 2013 | 2012 | ||||||||||||||||

Breakdown of NOI by facility: | ||||||||||||||||||||

Atlanta-Metro data center | $ | 13,740 | $ | 12,815 | $ | 10,772 | $ | 38,739 | $ | 30,820 | ||||||||||

Atlanta-Suwanee data center | 7,517 | 6,644 | 6,851 | 20,945 | 23,618 | |||||||||||||||

Santa Clara data center | 2,801 | 2,751 | 2,502 | 8,299 | 8,052 | |||||||||||||||

Richmond data center | 2,859 | 2,413 | 1,798 | 7,538 | 3,914 | |||||||||||||||

Sacramento data center (1) | 1,752 | 1,962 | - | 5,638 | - | |||||||||||||||

Other data centers | 612 | 381 | (12) | 1,065 | (242) | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

NOI | $ | 29,281 | $ | 26,966 | $ | 21,911 | $ | 82,224 | $ | 66,162 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

(1) Facility was acquired in December 2012.

Capital expenditures related to real estate assets are summarized as follows:

| Real Estate Capital Expenditures (1) | ||||||||||||||||||||||||

| Three Months Ended

September 30, | Nine Months Ended

September 30, | |||||||||||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||||||||||

Redevelopment | $ | 22,608 | $ | 30,912 | $ | 79,475 | $ | 75,796 | ||||||||||||||||

Acquisitions | - | 2,624 | 21,173 | 2,624 | ||||||||||||||||||||

Dispositions | - | (601) | (601) | |||||||||||||||||||||

Maintenance capital expenditures | 492 | 370 | 2,240 | 714 | ||||||||||||||||||||

Other capitalized costs | 3,950 | 2,739 | 10,670 | 8,219 | ||||||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||

Total real estate capital expenditures data center | $ | 27,050 | $ | 36,044 | $ | 113,558 | $ | 86,752 | ||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||

(1) Does not include capitalized leasing commissions included in deferred costs, acquired intangibles or other management related fixed assets included in other assets.

| 11 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Leasing Statistics – Signed Leases

(in thousands, except operating statistics data)

The mix of sales has significant impact on quarterly rates, both within major product segments and for overall blended leasing rates. QTS rate performance will vary quarter to quarter based on the mix of deals sold – C1 Custom Data Center, C2 Colocation, and C3 Cloud and Managed Services categories all vary on rate per sq ft basis. The amounts below include renewals where there was a change in square footage rented, but not renewals where square footage remained consistent before and after renewal (See renewal table on page 13 for such renewals).

During the third quarter of 2013, the Company signed 351 new and changed leases aggregating $13.1 million, which includes revenue from new customers and revenues from modified renewals. Removing annualized modified renewal MRR and deducting downgrades results in $8.2 million in incremental annualized rent. The average rent per square foot was approximately $566 per square foot which compares to a trailing four quarter average rate per square foot of approximately $282. Overall third quarter 2013 new and modified lease rates are above the trailing four quarter average due to higher mix of C2 and C3 leases in the quarter.

The prior four quarter average average of $282 per square foot is below overall installed base rates as a function of mega-C1 customer upgrades in 1Q 2013 and in 3Q 2012. As these C1 leases ramp their deployment over 2013 and 2014, we will see marginal pressure on overall blended C1 rates. In contrast, our second mega-C1 client will be returning a significant amount of space in Q4 and 2013 with a smaller reduction in MRR, resulting in higher rates per square foot, which will help overall blended C1 rates throughout the same time period.

Q3 C2 rates are below four quarter average as a function of a large C2 Suite/C3 Managed Services customer lease (3,000 sq ft) with pricing economics reflective of larger space/power commitments versus our average C2 customer. Without the effects of the leases for this customer, C2/C3 rates were more in line with 4Q trailing average.

Annualized Rent of New and Modified Leases represents total MRR associated with all new and modified leases for the respective periods for the purposes of computing annualized rent rates per square foot during the period. Incremental Annualized Rent, net of downgrades reflects net incremental MRR signed during the period for purposes of tracking incremental revenue contribution.

| Period | Number of leases | Total leased sqft | Annualized rent per leased sqft | Annualized Rent of New and Modified leases | Incremental Annualized Rent, net of Downgrades | |||||||||||||||||

|

|

|

|

|

| |||||||||||||||||

New/modified leases signed - Total | Q3 2013 | 351 | 23,138 | $ | 565.6 | $ | 13,086,021 | $ | 8,230,201 | |||||||||||||

| P4QA* | 299 | 55,827 | 282.1 | 15,748,888 | 7,866,739 | |||||||||||||||||

| Q2 2013 | 355 | 17,151 | 747.6 | 12,822,584 | 8,324,853 | |||||||||||||||||

| Q1 2013 | 334 | 110,298 | 208.7 | 23,023,046 | 17,233,394 | |||||||||||||||||

| Q4 2012 | 238 | 10,770 | 744.5 | 8,018,068 | 4,968,522 | |||||||||||||||||

| Q3 2012 | 268 | 85,090 | 224.8 | 19,131,854 | 940,185 | |||||||||||||||||

New/modified leases signed - C1 | Q3 2013 | 11 | 11,446 | $ | 235.5 | $ | 2,695,290 | |||||||||||||||

| P4QA* | 19 | 50,491 | 179.7 | 9,071,629 | ||||||||||||||||||

| Q2 2013 | 11 | 7,920 | 290.6 | 2,301,818 | ||||||||||||||||||

| Q1 2013 | 10 | 106,085 | 161.8 | 17,168,784 | ||||||||||||||||||

| Q4 2012 | 23 | 5,349 | 383.2 | 2,049,979 | ||||||||||||||||||

| Q3 2012 | 31 | 82,609 | 178.7 | 14,765,934 | ||||||||||||||||||

New/modified leases signed - C2/C3 | Q3 2013 | 340 | 11,692 | $ | 888.7 | $ | 10,390,731 | |||||||||||||||

| P4QA* | 280 | 5,337 | 1,251.2 | 6,677,259 | ||||||||||||||||||

| Q2 2013 | 344 | 9,231 | 1,139.7 | 10,520,766 | ||||||||||||||||||

| Q1 2013 | 324 | 4,213 | 1,389.6 | 5,854,262 | ||||||||||||||||||

| Q4 2012 | 215 | 5,421 | 1,100.9 | 5,968,088 | ||||||||||||||||||

| Q3 2012 | 237 | 2,481 | 1,759.7 | 4,365,921 | ||||||||||||||||||

* Average of prior 4 quarters

As of September 30, 2013, our booked-not-billed (“BNB”) MRR balance was approximately $2.0 million, of which approximately $0.4 million was from new customers and approximately $1.6 million was from existing customers. Of this booked-not-billed MRR balance, leases representing approximately $0.5 million of MRR are scheduled to commence in 2013, $0.9 million are scheduled to commence in 2014 and $0.6 million are scheduled to commence in 2015 and thereafter. The annualized rent from our total BNB MRR balance was approximately $23.5 million. Total incremental revenues from the BNB expected to be recognized in fourth quarter 2013 are $1.0 million (representing $6.1 million in annualized revenues), in 2014 $6.7 million (representing $10.4 million in annualized revenues), 2015 and thereafter $7.0 million in annualized revenues.

Note: Figures above do not include cost recoveries. In general, C1 customers reimburse QTS for certain operating costs wheras C2/C3 customers are on a gross lease basis. As a result, pricing and resulting per square foot rates for the C2/C3 customers includes the recovery of such operating costs.

| 12 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Leasing Statistics – Renewed Leases and Rental Churn

(in thousands, except operating statistics data)

The mix of sales has significant impact on quarterly rates, both within major product segments and for overall blended renewal rates. QTS rate performance will vary quarter to quarter based on the mix of deals sold – C1 Custom Data Center, C2 Colocation, and C3 Cloud and Managed Services categories all vary on rate per sq ft basis.

Consistent with our 3Cs strategy and business model, the renewal rates below reflect total MRR per square foot including all subscribed services. For comparability, the Company includes only those customers that have maintained consistent space in the computations below. All customers with space changes are incorporated into new leasing statistics and rates.

The overall blended rate for renewals signed in the third quarter of 2013 was 8.0% higher than the rates for those customers immediately prior to renewal. On a year to date basis, renewal rates were up 0.1%, which reflects the impact of three significant C2/C3 renewals signed in the first two quarters of 2013. These leases were extended at lower total effective rates as a function of services changes associated with the customer deployments. Overall renewal rates increase year to date would have been 3.5% without the impact of these lease renewals.

C1 renewal rates were up 8.3% in 2013. C2/C3 rates were up 7.9% in the quarter, but down slightly year to date as a function of the renewals with service reductions noted above. Without the impact of the three noted leases, C2/C3 renewal rates year to date would have been up 3.0%.

Rental Churn (which the Company defines as MRR lost to complete termination of customer services in a given period compared to total MRR at the beginning of the period) for the third quarter of 2013 was 1.3% and 3% year to date. This compares to a rental churn of 2.2% for the third quarter of 2012, and 6.9% year to date for 2012.

| Period | Number of renewed leases | Total Leased sqft | Annualized rent per leased sqft | Annualized Rent | Rent Change(1) | |||||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||||||

Renewed Leases - Total | Q3 2013 | 47 | 6,812 | 783 | 5,335,293 | 8.0% | ||||||||||||||||||

| YTD 2013 | 168 | 20,073 | $ | 862 | $ | 17,297,138 | 0.1% | (2) | ||||||||||||||||

Renewed Leases - C1 | Q3 2013 | 2 | 3,119 | 476 | 1,484,166 | 8.3% | ||||||||||||||||||

| YTD 2013 | 2 | 3,119 | $ | 476 | $ | 1,484,166 | 8.3% | |||||||||||||||||

Renewed Leases - C2/C3 | Q3 2013 | 45 | 3,693 | 1,043 | 3,851,127 | 7.9% | ||||||||||||||||||

| YTD 2013 | 166 | 16,954 | $ | 933 | $ | 15,812,972 | -0.7% | (3) | ||||||||||||||||

(1) Calculated as the percentage change of the rent per square foot immediately before renewal when compared to the rent per square foot immediately after renewal.

(2) Total rate increase without the impact of the 3 major C2/C3 lease extensions noted above would have been 3.5%.

(3) C2/C3 rate increase without the impact of the 3 major C2/C3 lease extensions noted above would have been 3.0%.

| 13 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Leasing Statistics – Commenced Leases

(in thousands, except operating statistics data)

The mix of sales across C1, C2 and C3 has significant impact on quarterly rates, both within major product segments and for overall blended commencement rates. QTS rate performance will vary quarter to quarter based on the mix of deals sold. C1 Custom Data Center, C2 Colocation (Cabinet, Cage and Suite), and C3 Cloud and Managed Services categories all vary on rate per sq ft basis.

During the third quarter of 2013, we commenced customer leases representing approximately $2.0 million of incremental MRR (representing approximately $23.5 million of annualized rent) at $324 per square foot. This compares to customer leases representing an aggregate trailing four quarter average of approximately $1.3 million of MRR (representing approximately $15.9 million of annualized rent) at $300 per square foot. Both the third quarter of 2013 and the trailing four quarter average rates reflect the impact of significant C1 lease commencements.

Initial commencements from a large C1 lease booked in the first quarter of 2013 impacted third quarter C1 commencement rates. Pricing for this strategic deal reflects the unique power commitment and lease size. The effects of the largest C1 clients can also be seen in the third quarter of 2012, because new business and renewed leases for these two strategic customers also draw down average C1 rates.

C2/C3 average commencement rates were down 19% versus trailing four quarter average and reflect the impact of several large C2 customers on overall rates. Related metrics reflect the presence of these large commencements and their larger footprint pricing economics—new MRR totaled $1.2 million ($14.9 million annualized) versus trailing average of $0.8 million ($9.9 million annualized) and space leased of 15,638 nearly doubled trailing average of 8,500 square feet.

| Period | Number of leases | Total Leased sqft | Annualized rent per leased sqft | Annualized Rent | ||||||||||||||||||

|

|

|

|

|

|

| ||||||||||||||||

Leases commenced - Total | Q3 2013 | 417 | 72,516 | $ | 324.4 | $ | 23,524,566 | |||||||||||||||

| P4QA* | 282 | 53,056 | 300.3 | 15,933,529 | ||||||||||||||||||

| Q2 2013 | 387 | 16,891 | 791.7 | 13,372,729 | ||||||||||||||||||

| Q1 2013 | 283 | 45,373 | 430.4 | 19,526,631 | ||||||||||||||||||

| Q4 2012 | 210 | 13,047 | 620.1 | 8,090,243 | ||||||||||||||||||

| Q3 2012 | 249 | 136,913 | 166.1 | 22,744,515 | ||||||||||||||||||

Leases commenced - C1 | Q3 2013 | 31 | 56,878 | $ | 151.8 | $ | 8,635,316 | |||||||||||||||

| P4QA* | 23 | 44,556 | 133.9 | 5,968,142 | ||||||||||||||||||

| Q2 2013 | 29 | 6,775 | 198.3 | 1,343,731 | ||||||||||||||||||

| Q1 2013 | 25 | �� | 34,801 | 201.9 | 7,025,724 | |||||||||||||||||

| Q4 2012 | 20 | 6,444 | 209.7 | 1,351,431 | ||||||||||||||||||

| Q3 2012 | 17 | 130,203 | 108.7 | 14,151,683 | ||||||||||||||||||

Leases commenced - C2/C3 | Q3 2013 | 386 | 15,638 | $ | 952.1 | $ | 14,889,250 | |||||||||||||||

| P4QA* | 260 | 8,500 | 1,172.4 | 9,965,387 | ||||||||||||||||||

| Q2 2013 | 358 | 10,116 | 1,189.1 | 12,028,998 | ||||||||||||||||||

| Q1 2013 | 258 | 10,572 | 1,182.5 | 12,500,907 | ||||||||||||||||||

| Q4 2012 | 190 | 6,603 | 1,020.6 | 6,738,812 | ||||||||||||||||||

| Q3 2012 | 232 | 6,710 | 1,280.6 | 8,592,832 | ||||||||||||||||||

* Average of prior 4 quarters

| 14 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Lease Expirations

C1 leases are typically 5-7 years with the majority of C1 lease expirations occurring in 2016 and beyond. C2/C3 leases are typically 3 years in duration, thus the majority of C2/C3 lease expirations are in 2014 and 2015. The following table sets forth a summary schedule of the lease expirations as of September 30, 2013 at the properties in the Company’s portfolio. Unless otherwise stated in the footnotes, the information set forth in the table assumes that customers exercise no renewal options and all early termination rights are exercised:

| Year of Lease Expiration (1) | Number of Leases Expiring (2) | Total Raised Floor of Expiring Leases | % of Portfolio Leased Raised Floor | Annualized Rent (3) | % of Portfolio Annualized Rent | C1 as % of Portfolio Annualized Rent | C2 as % of Portfolio Annualized Rent | C3 as % of Portfolio Annualized Rent | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||||

Month-to-Month (4) | 311 | 10,482 | 2 % | 11,817,870 | 7 % | 0 % | 6 % | 1 % | ||||||||||||||||||||||||

Remainder of 2013 | 280 | 49,517 | 10 % | 13,189,622 | 8 % | 2 % | 5 % | 1 % | ||||||||||||||||||||||||

2014 | 898 | 46,916 | 10 % | 36,316,101 | 22 % | 4 % | 16 % | 3 % | ||||||||||||||||||||||||

2015 | 606 | 38,637 | 8 % | 29,150,462 | 18 % | 3 % | 14 % | 1 % | ||||||||||||||||||||||||

2016 | 391 | 50,965 | 10 % | 22,614,899 | 14 % | 4 % | 9 % | 1 % | ||||||||||||||||||||||||

2017 | 65 | 52,695 | 11 % | 14,548,674 | 9 % | 7 % | 1 % | 1 % | ||||||||||||||||||||||||

2018 | 51 | 198,563 | 40 % | 26,993,859 | 16 % | 15 % | 1 % | 1 % | ||||||||||||||||||||||||

After 2018 | 46 | 42,654 | 9 % | 10,961,974 | 7 % | 6 % | 0 % | 1 % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

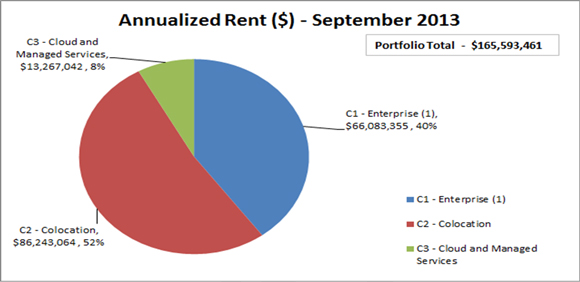

Portfolio Total | 2,648 | 490,429 | 100 % | $ | 165,593,461 | 100 % | 40 % | 52 % | 8 % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||

| (1) | Does not include data for leases expiring in a particular year when leases for the same space have already been signed with replacement customers with future commencement dates. In those cases, the data is included in the year in which the future lease expires. |

| (2) | Represents each agreement with a customer signed as of September 30, 2013 for which billing has commenced; a lease agreement could include multiples spaces and a customer could have multiple leases. |

| (3) | Annualized rent is presented for leases commenced as of September 30, 2013. The Company defines annualized rent as MRR multiplied by 12. The Company calculates MRR as monthly contractual revenue under signed leases as of a particular date, which includes revenue from our C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed leases as of a particular date, unless otherwise specifically noted. This amount reflects the annualized cash rental payments. It does not reflect the accounting associated with any free rent, rent abatements or future scheduled rent increases and also excludes operating expense and power reimbursements. |

| (4) | Consists of customers whose leases expired prior to September 30, 2013 and have continued on a month-to-month basis. |

| 15 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Largest Customers

As of September 30, 2013, the Company’s portfolio was leased to over 880 customers comprised of companies of all sizes representing an array of industries, each with unique and varied business models and needs. The following table sets forth information regarding the ten largest customers in the portfolio based on annualized rent as of September 30, 2013:

Principal Customer Industry | Number of Locations | Annualized Rent (1) | % of Portfolio Annualized Rent | Weighted Average Remaining Lease Term (Months) (2) | ||||||||

Internet | 1 | $ | 11,087,381 | 6.7% | 53 | |||||||

Internet | 1 | 10,547,780 | 6.4% | 60 | ||||||||

Information Technology | 3 | 4,781,403 | 2.9% | 20 | ||||||||

Financial Services | 1 | 4,318,740 | 2.6% | 40 | ||||||||

Financial Services | 2 | 3,224,909 | 1.9% | 51 | ||||||||

Professional Services | 1 | 3,148,080 | 1.6% | 20 | ||||||||

Financial Services | 1 | 3,120,405 | 1.9% | 22 | ||||||||

Internet | 2 | 3,115,417 | 1.9% | 1 | ||||||||

Information Technology | 1 | 3,007,200 | 1.8% | 117 | ||||||||

Information Technology | 2 | 2,648,376 | 1.6% | 7 | ||||||||

|

|

|

|

| ||||||||

Total / Weighted Average | $ | 48,999,691 | 29.2% | 44 | ||||||||

|

|

|

|

| ||||||||

| (1) | Annualized rent is presented for leases commenced as of September 30, 2013. We define annualized rent as MRR multiplied by 12. We calculate MRR as monthly contractual revenue under signed leases as of a particular date, which includes revenue from our C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed leases as of a particular date. This amount reflects the annualized cash rental payments. It does not reflect any free rent, rent abatements or future scheduled rent increases and also excludes operating expense and power reimbursements. |

| (2) | Weighted average based on customer’s percentage of total annualized rent expiring and is as of September 30, 2013. |

| 16 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

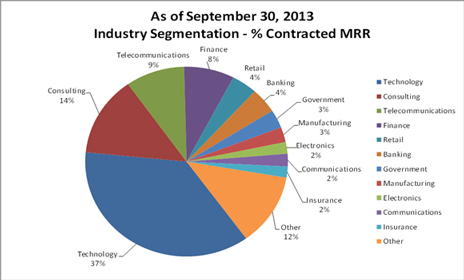

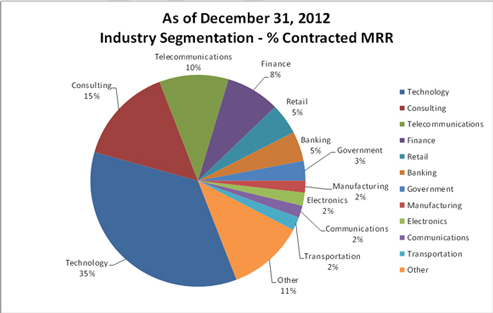

Industry Segmentation

The following table sets forth information relating to the industry segmentation as of September 30, 2013:

The following table sets forth information relating to the industry segmentation as of December 31, 2012:

| 17 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Product Diversification

The following table sets forth information relating to the distribution of leases at our properties, by type of product offering, as of September 30, 2013:

| (1) | As of September 30, 2013, C1 customers renting over 6,600 square represented $32.4 million of our annualized C1 MRR, C1 customers renting between 3,300 and 6,600 square feet represented $19.4 million of our annualized C1 MRR and C1 customers renting below 3,300 square feet represented or $14.3 million of our annualized C1 MRR. |

The following table sets forth information relating to the distribution of leases at our properties, by type of product offering, as of December 31, 2012:

| (1) | As of December 31, 2012, C1 customers renting over 6,600 square represented $24.1 million of our annualized C1 MRR, C1 customers renting between 3,300 and 6,600 square feet represented $16.6 million of our annualized C1 MRR and C1 customers renting below 3,300 square feet represented or $14.3 million of our annualized C1 MRR. |

| 18 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Debt Summary and Maturities

(in thousands)

Pro forma 2013 | September 30, 2013 | December 31, 2012 | ||||||||||

| (unaudited) |

| ||||||||||

Secured Credit Facility | $ | - | $ | - | $ | 316,500 | ||||||

Unsecured Credit Facility | 240,000 | 520,000 | - | |||||||||

Richmond Credit Facility | 70,000 | 70,000 | 70,000 | |||||||||

Atlanta-Metro Equipment Loan | 19,376 | 19,376 | 20,931 | |||||||||

Miami Loan | - | - | 26,048 | |||||||||

Suwanee Land Loan | - | - | 1,600 | |||||||||

Lenexa Loan | - | - | 2,712 | |||||||||

Santa Clara Bridge Loan | - | - | 50,000 | |||||||||

|

|

|

|

|

| |||||||

Total | $ | 329,376 | $ | 609,376 | $ | 487,791 | ||||||

|

|

|

|

|

| |||||||

As of September 30, 2013:

| 2013

| 2014

| 2015

| 2016

| 2017

| Thereafter

| Total

| ||||||||||||||||||||||

Unsecured Credit Facility (1) | $ | - | $ | - | $ | - | $ | - | $ | 295,000 | $ | 225,000 | $ | 520,000 | ||||||||||||||

Richmond Credit Facility (2) | - | - | 70,000 | - | - | - | 70,000 | |||||||||||||||||||||

Atlanta Metro equipment loan | 536 | 2,239 | 2,397 | 2,567 | 2,749 | 8,888 | 19,376 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total | $ | 536 | $ | 2,239 | $ | 72,397 | $ | 2,567 | $ | 297,749 | $ | 233,888 | $ | 609,376 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

As of September 30, 2013 (adjusted for use of IPO proceeds): |

| |||||||||||||||||||||||||||

| Debt instruments | 2013

| 2014

| 2015

| 2016

| 2017

| Thereafter

| Total

| |||||||||||||||||||||

Unsecured Credit Facility (1) | $ | - | $ | - | $ | - | $ | - | $ | 15,000 | $ | 225,000 | $ | 240,000 | ||||||||||||||

Richmond Credit Facility (2) | - | - | 70,000 | - | - | - | 70,000 | |||||||||||||||||||||

Atlanta-Metro Equipment Loan | 536 | 2,239 | 2,397 | 2,567 | 2,749 | 8,888 | 19,376 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total | $ | 536 | $ | 2,239 | $ | 72,397 | $ | 2,567 | $ | 17,749 | $ | 233,888 | $ | 329,376 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

(1) Unsecured Credit Facility revolving portion, has a stated maturity of May 1, 2017 with an option to extend for one additional year.

(2) Richmond Credit Facility has a stated maturity of December 18, 2015 with an option to extend for one additional year.

| 19 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Interest Summary

(in thousands)

| Three Months Ended | Nine Months Ended September 30, | |||||||||||||||||||

| September 30, | June 30, | September 30, | ||||||||||||||||||

| 2013 | 2013 | 2012 | 2013 | 2012 | |||||||||||||||

Interest expense and fees | $ | 4,508 | $ | 5,355 | $ | 6,210 | $ | 16,377 | $ | 17,493 | ||||||||||

Swap interest | 146 | 151 | - | 380 | 493 | |||||||||||||||

Amortization of deferred financing costs | 588 | 693 | 828 | 2,193 | 2,567 | |||||||||||||||

Capitalized interest | (899) | (1,115) | (392) | (2,973) | (1,514) | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total interest expense (1) | $ | 4,343 | $ | 5,084 | $ | 6,646 | $ | 15,977 | $ | 19,039 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

(1) The weighted average interest rate for the three months ended September 30, 2013, June 30, 2013, and September 30, 2012 was 3.58%, 4.36%, and 5.90%, respectively. The weighted average interest rate for the nine months ended September 30, 2013 and 2012 was 4.45% and 5.91%, respectively.

| 20 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Appendix

Non-GAAP Financial Measures

This document includes certain non-GAAP financial measures that management believes are helpful in understanding the Company’s business, as further described below.

The Company considers the following non-GAAP financial measures to be useful to investors as key supplemental measures of the Company’s performance: (1) FFO; (2) Operating FFO; (3) Adjusted Operating FFO; (4) MRR; (5) EBITDA; and (6) Adjusted EBITDA. These non-GAAP financial measures should be considered along with, but not as alternatives to, net income or loss and cash flows from operating activities as a measure of the Company’s operating performance and liquidity. FFO, Operating FFO, Adjusted Operating FFO, MRR, NOI, EBITDA and Adjusted EBITDA, as calculated by us, may not be comparable to FFO, Operating FFO, Adjusted Operating FFO, MRR, NOI, EBITDA and Adjusted EBITDA as reported by other companies that do not use the same definition or implementation guidelines or interpret the standards differently from us.

Definitions

C1 - Custom Data Center. Power costs are passed on to customers (metered power); generally 3,000 square feet or more of raised floor; lease term of 5 to 10 years; customers are large corporations, government agencies, and global Internet businesses.

C2 - Colocation. Power overages charged separately; specified kW included in lease; up to 3,000 square feet of raised floor; lease term of up to 3 years; customers are large corporations, small and medium businesses and government agencies.

C3 - Cloud and Managed Services. Power bundled with service; Small amounts of space; customers rent managed virtual servers; lease term up to 3 years; customers are large corporations, small and medium businesses and government agencies.

Booked-not-billed (“BNB”). The Company defines booked-not-billed as customer leases that have been signed, but for which lease payments have not yet commenced.

Leasable raised floor. The Company defines leasable raised floor as the amount of raised floor square footage that the Company has leased plus the available capacity of raised floor square footage that is in a leasable format as of a particular date and according to a particular product configuration. The amount of leasable raised floor may change even without completion of new redevelopment projects due to changes in the Company’s configuration of C1, C2 and C3 product space.

Basis-of-design raised floor space. The Company defines basis-of-design floor space as the total data center raised floor potential of its existing data center facilities. For Custom Data Center customers the leasable square feet is determined based on a wall to wall square foot calculation and for colocation customers leasable square footage is calculated based on the number of cages (each cage is 64 square feet) and cabinets (each cabinet is 8 square feet).

| 21 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

Operating NRSF. Represents the total square feet of a building that is currently leased or available for lease plus developed supporting infrastructure, based on engineering drawings and estimates, but does not include space held for redevelopment or space used for the Company’s own office space.

FFO, Operating FFO and Adjusted Operating FFO

The Company considers funds from operations, or FFO, to be a supplemental measure of its performance which should be considered along with, but not as an alternative to, net income (loss) and cash provided by operating activities as a measure of operating performance and liquidity. The Company calculates FFO in accordance with the standards established by the National Association of Real Estate Investment Trusts, or NAREIT. FFO represents net income (loss) (computed in accordance with GAAP), adjusted to exclude gains (or losses) from sales of property, real estate related depreciation and amortization and similar adjustments for unconsolidated partnerships and joint ventures. The Company’s management uses FFO as a supplemental performance measure because, in excluding real estate related depreciation and amortization and gains and losses from property dispositions, it provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs.

Due to the volatility and nature of certain significant charges and gains recorded in the Company’s operating results that management believes are not reflective of its core operating performance and liquidity, management computes an adjusted measure of FFO, which the Company refers to as Operating FFO. The Company generally calculates Operating FFO as FFO excluding certain non-recurring and primarily non-cash charges and gains and losses that management believes are not indicative of the results of the Company’s operating real estate portfolio. The Company believes that Operating FFO provides investors with another financial measure that may facilitate comparisons of operating performance and liquidity between periods and, to the extent they calculate Operating FFO on a comparable basis, between REITs.

Adjusted Operating Funds From Operations “Adjusted Operating FFO” is a non-GAAP measure that is used as a supplemental operating measure specifically for comparing year over year ability to fund dividend distribution from operating activities. Adjusted Operating FFO is used by the Company as a basis to address its ability to fund its dividend payments. The Company calculates Adjusted Operating FFO by adding or subtracting from Operating FFO items such as: maintenance capital investment, paid leasing commissions, amortization of deferred financing costs, non-real estate depreciation, straight line rent adjustments, and non-cash compensation.

The Company offers these measures because it recognizes that FFO, Operating FFO and Adjusted Operating FFO will be used by investors as a basis to compare its operating performance and liquidity with that of other REITs. However, because FFO, Operating FFO and Adjusted Operating FFO exclude real estate depreciation and amortization and capture neither the changes in the value of the Company’s properties that result from use or market conditions, nor the level of capital expenditures and capitalized leasing commissions necessary to maintain the operating performance of its properties, all of which have real economic effect and could materially impact its financial condition, cash flows and results of operations, the utility of FFO, Operating FFO and Adjusted Operating FFO as measures of its operating performance and liquidity is limited. The Company’s calculation of FFO may not be comparable to measures calculated by other companies who do not

| 22 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

use the NAREIT definition of FFO or do not calculate FFO in accordance with NAREIT guidance. In addition, the Company’s calculations of FFO, Operating FFO and Adjusted Operating FFO are not necessarily comparable to FFO, Operating FFO and Adjusted Operating FFO as calculated by other REITs that do not use the same definition or implementation guidelines or interpret the standards differently from us. FFO, Operating FFO and Adjusted Operating FFO are non-GAAP measures and should not be considered a measure of the Company’s results of operations or liquidity or as a substitute for, or an alternative to, net income (loss), cash provided by operating activities or any other performance measure determined in accordance with GAAP, nor is it indicative of funds available to fund its cash needs, including our ability to make distributions to our stockholders.

Monthly Recurring Revenue (MRR)

The Company calculates MRR as monthly contractual revenue under signed leases as of a particular date, which includes revenue from its C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed leases as of a particular date, unless otherwise specifically noted.

Separately, the Company calculates recognized MRR as the recurring revenue recognized during a given period, which includes revenue from its C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues.

Management uses MRR and recognized MRR as supplemental performance measures because they provide useful measures of increases in contractual revenue from the Company’s customer leases. MRR and recognized MRR should not be viewed by investors as alternatives to actual monthly revenue, as determined in accordance with GAAP. Other companies may not calculate MRR or recognized MRR in the same manner. Accordingly, the Company’s MRR and recognized MRR may not be comparable to other companies’ MRR and recognized MRR. MRR and recognized MRR should be considered only as supplements to total revenues as a measure of its performance. MRR and recognized MRR should not be used as measures of the Company’s results of operations or liquidity, nor is it indicative of funds available to meet its cash needs, including its ability to make distributions to its stockholders.

Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) and Adjusted EBITDA

The Company calculates EBITDA as net income (loss) adjusted to exclude interest expense and interest income, provision for income taxes (including income taxes applicable to sale of assets) and depreciation and amortization. Management believes that EBITDA is useful to investors in evaluating and facilitating comparisons of the Company’s operating performance between periods and between REITs by removing the impact of its capital structure (primarily interest expense) and asset base charges (primarily depreciation and amortization) from its operating results.

In addition to EBITDA, the Company calculates an adjusted measure of EBITDA, which it refers to as Adjusted EBITDA, as EBITDA excluding unamortized deferred financing costs, gains on

| 23 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |

extinguishment of debt, transaction costs, equity-based compensation expense, restructuring charge, gain (loss) on legal settlement and gain on sale of real estate. The Company believes that Adjusted EBITDA provides investors with another financial measure that can facilitate comparisons of operating performance between periods and between REITs.

Management uses EBITDA and Adjusted EBITDA as supplemental performance measures as they provide useful measures of assessing the Company’s operating results. Other companies may not calculate EBITDA or Adjusted EBITDA in the same manner. Accordingly, the Company’s EBITDA and Adjusted EBITDA may not be comparable to others. EBITDA and Adjusted EBITDA should be considered only as supplements to net income (loss) as measures of the Company’s performance and should not be used as substitutes for net income (loss), as measures of its results of operations or liquidity or as an indications of funds available to meet our cash needs, including our ability to make distributions to our stockholders.

| 24 QTS Q3 2013 Supplemental Information | Contact: IR@qualitytech.com |